Exhibit 99.1

|

Old Second Bancorp, Inc. |

|

For Immediate Release |

|

(NASDAQ: OSBC) |

|

October 23, 2013 |

|

Contact: |

J. Douglas Cheatham |

|

|

Chief Financial Officer |

|

|

(630) 906-5484 |

Old Second Bancorp, Inc. Announces Third Quarter Net Income of $72.9 Million

Reversal of valuation allowance against deferred tax assets resulted in a $70 million benefit

Net income before taxes of $2.9 million for the quarter

Regulatory Consent Order (OCC) terminated

Loan loss reserve release reflects stabilized and improved credit quality

AURORA, IL, October 23, 2013 — Old Second Bancorp, Inc. (the “Company” or “Old Second”) (NASDAQ: OSBC), parent company of Old Second National Bank (the “Bank”), today announced financial results for the third quarter of 2013. The Company reported net income of $72.9 million after a $70.0 million benefit from the reversal of the valuation allowance against deferred tax assets. Income before taxes for the quarter, reflecting the benefit of a $1.8 million reversal in loan loss reserve, totaled $2.9 million. These results compare to net income of $3.5 million in the second quarter of this year and $120,000 in the third quarter of 2012. The Company’s net income available to common shareholders of $71.6 million, or $5.08 per diluted share ($0.11 per share excluding the reversal of the valuation allowance against deferred tax assets), for the quarter compared to net loss available to common shareholders of $1.1 million or $(0.08) per diluted share, in the third quarter of 2012.

The Company reported net income of $81.9 million for the first nine months of 2013 ($11.9 million income before taxes excluding the reversal of the valuation allowance against the deferred tax assets), compared to a net loss of $1.6 million in the same period of 2012. The Company’s net income available to common shareholders of $78.0 million, or $5.52 per diluted share ($0.56 per share excluding the reversal of the valuation allowance against the deferred tax assets), for the first nine months of 2013 compared to a net loss available to common shareholders of $5.3 million, or $(0.37) per diluted share, in the first nine months of 2012.

Chairman Bill Skoglund said “Results for the third quarter and for the first nine months of 2013 reflect ongoing progress in our return to enduring profitability. Improvements in overall real estate markets in our market areas were offset by intense competition from other financial institutions and low loan demand from our small business customers resulting in restrained loan growth. Further, the move to a higher market interest rate environment pressured our residential mortgage business in the same manner as seen nationwide.”

Mr. Skoglund continued “Our momentum is building as our bankers solidify existing relationships and add to pipelines with current and prospective customers. Our organization becomes stronger as problems from past decisions are resolved — evidenced by the action taken in the third quarter to reverse the reserve against our deferred tax assets and by this month’s decision of the Office of the Comptroller of Currency to terminate the Consent Order under which we’ve been operating. Nonaccrual loans are down to $43.6 million from $77.5 million at December 31, 2012 and $58.2 million at June 30, 2013. Similarly, other real estate owned declined to $49.1 million from $72.4 million at year end 2012 and $59.5 million at June 30, 2013. Our mission remains robust improvement in earnings per share from greater revenues in all our products coupled with disciplined expense management.”

2013 Financial Highlights/Overview

Operating Environment

· Loan growth prospects reasonably improving. Overall loan growth goal not yet attained.

· Loyal deposit customers and value added customer service maintains deposit base.

· Troubled real estate owned and real estate markets stabilizing.

· Marketable securities portfolio managed to utilize liquid funds in low interest rate environment.

Earnings

· Third quarter income before taxes of $2.9 million compared to income before taxes of $120,000 in the third quarter of 2012. The increase was primarily due to the release of $1.8 million in loan loss reserves and reduced other real owned estate expenses.

· Net income available to common shareholders of $71.6 million for the third quarter reflected the benefit of the reversal of the valuation allowance against the deferred tax assets.

· In 2013, income before taxes declined from $3.5 million in the second quarter to $2.9 million in the third quarter. This decline primarily resulted from a $1.6 million, or 56.3%, reduction in residential mortgage revenue, and reduced gains on securities sales from $745,000 in the second quarter to a $7,000 loss in the third quarter.

· The tax-equivalent net interest margin was 3.25% during the third quarter of 2013 compared to 3.44% in the same quarter of 2012. The third quarter of 2013 margin was an increase of 18 basis points compared to the second quarter of 2013.

· Noninterest income of $29.5 million was $1.7 million lower in the first nine months of 2013 compared to the same period of 2012, reflecting reduced residential mortgage revenue, service charges on deposits, and lease revenue from other real estate owned (“OREO”).

· Noninterest expenses of $65.2 million were 9.4% lower in the first nine months of 2013 than in the same period of 2012, reflecting overall expense control and reduced expenses in most categories. Notable reductions are found in OREO expenses (down $6.9 million year over year essentially on still elevated but improved valuation adjustment expense, general bank insurance and the partial accounting recovery of some legal fees paid on OREO.

Capital

|

|

|

September 30, |

|

June 30, |

|

Percent |

|

|

|

|

2013 |

|

2013 |

|

Change |

|

|

The Bank’s leverage capital ratio |

|

11.08 |

% |

10.40 |

% |

0.68 |

% |

|

The Bank’s total risk-based capital ratio |

|

17.08 |

% |

16.30 |

% |

0.78 |

% |

|

The Company’s leverage capital ratio |

|

7.11 |

% |

5.46 |

% |

1.65 |

% |

|

The Company’s total risk-based capital ratio |

|

15.15 |

% |

14.70 |

% |

0.45 |

% |

|

The Company’s tangible common equity to tangible assets |

|

3.33 |

% |

(0.18 |

)% |

3.51 |

% |

Asset Quality & Earning Assets

· Nonperforming loans declined $34.8 million (42.2%) during the nine months ending September 30, 2013 to $47.8 million, from $82.6 million as of December 31, 2012. Nonperforming loans declined primarily because of successful negotiations by our staff with guarantors and movement to OREO, as well as loans being upgraded to accruing status when the financial condition of borrowers improved.

· OREO declined from $72.4 million at December 31, 2012, to $49.1 million at September 30, 2013. OREO dispositions totaling $30.9 million in the nine month period ending September 30, 2013 were somewhat offset by new OREO and improvements to existing OREO of $14.3

million. Valuation write-downs of properties held for sale reduced the reported total by $6.7 million with related expense recognized.

· Securities available-for-sale decreased $206.4 million during 2013 to $373.5 million from $579.9 million at December 31, 2012 with the third quarter reclassification of $258.1 million to the held-to-maturity category. In all prior periods, all securities were held as available for sale. At $269.0 million (72.0% of the September 30, 2013 available-for-sale portfolio), of asset-backed securities were the largest component of the available-for-sale portfolio and total securities holdings as of September 30, 2013. The Company’s asset-backed securities were heavily oriented to those backed by student loan debt guaranteed by the U.S. Department of Education.

Net Interest Income

ANALYSIS OF AVERAGE BALANCES,

TAX EQUIVALENT INTEREST AND RATES

Three Months ended September 30, 2013, and 2012

(Dollar amounts in thousands - unaudited)

|

|

|

2013 |

|

2012 |

| ||||||||||||

|

|

|

Average |

|

|

|

|

|

Average |

|

|

|

|

| ||||

|

|

|

Balance |

|

Interest |

|

Rate |

|

Balance |

|

Interest |

|

Rate |

| ||||

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Interest bearing deposits |

|

$ |

36,456 |

|

$ |

22 |

|

0.24 |

% |

$ |

46,138 |

|

$ |

29 |

|

0.25 |

% |

|

Securities: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Taxable |

|

605,546 |

|

3,113 |

|

2.06 |

|

404,855 |

|

1,868 |

|

1.85 |

| ||||

|

Non-taxable (tax equivalent) |

|

13,937 |

|

228 |

|

6.54 |

|

9,518 |

|

151 |

|

6.35 |

| ||||

|

Total securities |

|

619,483 |

|

3,341 |

|

2.16 |

|

414,373 |

|

2,019 |

|

1.95 |

| ||||

|

Dividends from FRB and FHLB stock |

|

10,292 |

|

76 |

|

2.95 |

|

11,984 |

|

77 |

|

2.57 |

| ||||

|

Loans and loans held-for-sale (1) |

|

1,088,936 |

|

14,382 |

|

5.17 |

|

1,230,180 |

|

16,279 |

|

5.18 |

| ||||

|

Total interest earning assets |

|

1,755,167 |

|

17,821 |

|

3.99 |

|

1,702,675 |

|

18,404 |

|

4.24 |

| ||||

|

Cash and due from banks |

|

19,584 |

|

— |

|

— |

|

31,850 |

|

— |

|

— |

| ||||

|

Allowance for loan losses |

|

(34,197 |

) |

— |

|

— |

|

(40,823 |

) |

— |

|

— |

| ||||

|

Other noninterest bearing assets |

|

190,836 |

|

— |

|

— |

|

228,859 |

|

— |

|

— |

| ||||

|

Total assets |

|

$ |

1,931,390 |

|

|

|

|

|

$ |

1,922,561 |

|

|

|

|

| ||

|

Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

NOW accounts |

|

$ |

283,192 |

|

$ |

63 |

|

0.09 |

% |

$ |

270,908 |

|

$ |

65 |

|

0.10 |

% |

|

Money market accounts |

|

311,213 |

|

104 |

|

0.13 |

|

321,762 |

|

137 |

|

0.17 |

| ||||

|

Savings accounts |

|

225,825 |

|

39 |

|

0.07 |

|

213,927 |

|

51 |

|

0.09 |

| ||||

|

Time deposits |

|

493,722 |

|

1,674 |

|

1.35 |

|

526,314 |

|

1,973 |

|

1.49 |

| ||||

|

Interest bearing deposits |

|

1,313,952 |

|

1,880 |

|

0.57 |

|

1,332,911 |

|

2,226 |

|

0.66 |

| ||||

|

Securities sold under repurchase agreements |

|

21,646 |

|

1 |

|

0.02 |

|

7,164 |

|

1 |

|

0.06 |

| ||||

|

Other short-term borrowings |

|

15,707 |

|

5 |

|

0.12 |

|

652 |

|

— |

|

— |

| ||||

|

Junior subordinated debentures |

|

58,378 |

|

1,336 |

|

9.15 |

|

58,378 |

|

1,243 |

|

8.52 |

| ||||

|

Subordinated debt |

|

45,000 |

|

209 |

|

1.82 |

|

45,000 |

|

223 |

|

1.94 |

| ||||

|

Notes payable and other borrowings |

|

500 |

|

4 |

|

3.13 |

|

500 |

|

5 |

|

3.91 |

| ||||

|

Total interest bearing liabilities |

|

1,455,183 |

|

3,435 |

|

0.94 |

|

1,444,605 |

|

3,698 |

|

1.02 |

| ||||

|

Noninterest bearing deposits |

|

366,889 |

|

— |

|

— |

|

380,226 |

|

— |

|

— |

| ||||

|

Other liabilities |

|

37,466 |

|

— |

|

— |

|

28,130 |

|

— |

|

— |

| ||||

|

Stockholders’ equity |

|

71,852 |

|

— |

|

— |

|

69,600 |

|

— |

|

— |

| ||||

|

Total liabilities and stockholders’ equity |

|

$ |

1,931,390 |

|

|

|

|

|

$ |

1,922,561 |

|

|

|

|

| ||

|

Net interest income (tax equivalent) |

|

|

|

$ |

14,386 |

|

|

|

|

|

$ |

14,706 |

|

|

| ||

|

Net interest income (tax equivalent) to total earning assets |

|

|

|

|

|

3.25 |

% |

|

|

|

|

3.44 |

% | ||||

|

Interest bearing liabilities to earning assets |

|

82.91 |

% |

|

|

|

|

84.84 |

% |

|

|

|

| ||||

(1) Interest income from loans is shown on a tax equivalent basis as discussed in the table on page 19 and includes fees of $793,000 and $498,000 for the third quarter of 2013 and 2012, respectively. Nonaccrual loans are included in the above stated average balances.

Note: Tax equivalent basis is calculated using a marginal tax rate of 35%.

ANALYSIS OF AVERAGE BALANCES,

TAX EQUIVALENT INTEREST AND RATES

Nine Months ended September 30, 2013, and 2012

(Dollar amounts in thousands - unaudited)

|

|

|

2013 |

|

2012 |

| ||||||||||||

|

|

|

Average |

|

|

|

|

|

Average |

|

|

|

|

| ||||

|

|

|

Balance |

|

Interest |

|

Rate |

|

Balance |

|

Interest |

|

Rate |

| ||||

|

Assets |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Interest bearing deposits |

|

$ |

49,676 |

|

$ |

91 |

|

0.24 |

% |

$ |

48,871 |

|

$ |

89 |

|

0.24 |

% |

|

Securities: |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Taxable |

|

574,761 |

|

8,109 |

|

1.88 |

|

365,549 |

|

5,222 |

|

1.90 |

| ||||

|

Non-taxable (tax equivalent) |

|

14,912 |

|

679 |

|

6.07 |

|

10,417 |

|

467 |

|

5.98 |

| ||||

|

Total securities |

|

589,673 |

|

8,788 |

|

1.99 |

|

375,966 |

|

5,689 |

|

2.02 |

| ||||

|

Dividends from FRB and FHLB stock |

|

10,742 |

|

228 |

|

2.83 |

|

12,562 |

|

228 |

|

2.42 |

| ||||

|

Loans and loans held-for-sale (1) |

|

1,116,964 |

|

43,327 |

|

5.12 |

|

1,293,533 |

|

51,741 |

|

5.26 |

| ||||

|

Total interest earning assets |

|

1,767,055 |

|

52,434 |

|

3.92 |

|

1,730,932 |

|

57,747 |

|

4.39 |

| ||||

|

Cash and due from banks |

|

24,110 |

|

— |

|

— |

|

27,528 |

|

— |

|

— |

| ||||

|

Allowance for loan losses |

|

(37,122 |

) |

— |

|

— |

|

(46,824 |

) |

— |

|

— |

| ||||

|

Other noninterest bearing assets |

|

196,298 |

|

— |

|

— |

|

236,281 |

|

— |

|

— |

| ||||

|

Total assets |

|

$ |

1,950,341 |

|

|

|

|

|

$ |

1,947,917 |

|

|

|

|

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

|

|

|

|

|

|

| ||||

|

NOW accounts |

|

$ |

290,691 |

|

$ |

192 |

|

0.09 |

% |

$ |

275,712 |

|

$ |

204 |

|

0.10 |

% |

|

Money market accounts |

|

319,876 |

|

342 |

|

0.14 |

|

311,046 |

|

438 |

|

0.19 |

| ||||

|

Savings accounts |

|

226,193 |

|

121 |

|

0.07 |

|

211,331 |

|

165 |

|

0.10 |

| ||||

|

Time deposits |

|

498,846 |

|

5,327 |

|

1.43 |

|

565,183 |

|

6,920 |

|

1.64 |

| ||||

|

Interest bearing deposits |

|

1,335,606 |

|

5,982 |

|

0.60 |

|

1,363,272 |

|

7,727 |

|

0.76 |

| ||||

|

Securities sold under repurchase agreements |

|

22,206 |

|

2 |

|

0.01 |

|

4,502 |

|

2 |

|

0.06 |

| ||||

|

Other short-term borrowings |

|

20,000 |

|

24 |

|

0.16 |

|

4,635 |

|

4 |

|

0.11 |

| ||||

|

Junior subordinated debentures |

|

58,378 |

|

3,937 |

|

8.99 |

|

58,378 |

|

3,660 |

|

8.36 |

| ||||

|

Subordinated debt |

|

45,000 |

|

610 |

|

1.79 |

|

45,000 |

|

684 |

|

2.00 |

| ||||

|

Notes payable and other borrowings |

|

500 |

|

12 |

|

3.16 |

|

500 |

|

13 |

|

3.42 |

| ||||

|

Total interest bearing liabilities |

|

1,481,690 |

|

10,567 |

|

0.95 |

|

1,476,287 |

|

12,090 |

|

1.09 |

| ||||

|

Noninterest bearing deposits |

|

359,438 |

|

— |

|

— |

|

373,975 |

|

— |

|

— |

| ||||

|

Other liabilities |

|

35,432 |

|

— |

|

— |

|

25,629 |

|

— |

|

— |

| ||||

|

Stockholders’ equity |

|

73,781 |

|

— |

|

— |

|

72,026 |

|

— |

|

— |

| ||||

|

Total liabilities and stockholders’ equity |

|

$ |

1,950,341 |

|

|

|

|

|

$ |

1,947,917 |

|

|

|

|

| ||

|

Net interest income (tax equivalent) |

|

|

|

$ |

41,867 |

|

|

|

|

|

$ |

45,657 |

|

|

| ||

|

Net interest income (tax equivalent) to total earning assets |

|

|

|

|

|

3.17 |

% |

|

|

|

|

3.52 |

% | ||||

|

Interest bearing liabilities to earning assets |

|

83.85 |

% |

|

|

|

|

85.29 |

% |

|

|

|

| ||||

(1) Interest income from loans is shown on a tax equivalent basis as discussed in the table on page 19 and includes fees of $2.0 million and $1.4 million for the first nine months of 2013 and 2012, respectively. Nonaccrual loans are included in the above stated average balances.

Note: Tax equivalent basis is calculated using a marginal tax rate of 35%.

Net interest and dividend income decreased $3.9 million, from $45.4 million in the first nine months of 2012, to $41.6 million in the first nine months of 2013. Average earning assets increased $36.1 million, or 2.1%, from $1.73 billion in the first nine months of 2012, to $1.77 billion in the first nine months of 2013 as a result of growth in investment securities. Management continued to emphasize asset quality in marketable securities purchases and new loan originations continued to be limited. Average loans, including loans held-for-sale, decreased $176.6 million from the first nine months of 2012 to the first nine months of 2013. The net interest margin was 3.25% for the third quarter of 2013 compared to 3.44% on this metric for the third quarter of 2012.

Asset Quality

|

|

|

Three Months Ended |

|

Year to Date |

| ||||||||

|

Loan Charge-offs, net of (recoveries) |

|

September 30, |

|

September 30, |

| ||||||||

|

(in thousands) |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| ||||

|

Real estate-construction |

|

|

|

|

|

|

|

|

| ||||

|

Homebuilder |

|

$ |

(5 |

) |

$ |

(151 |

) |

$ |

(307 |

) |

$ |

768 |

|

|

Land |

|

44 |

|

(57 |

) |

42 |

|

(723 |

) | ||||

|

Commercial speculative |

|

— |

|

(1,130 |

) |

(49 |

) |

668 |

| ||||

|

All other |

|

(1 |

) |

45 |

|

— |

|

165 |

| ||||

|

Total real estate-construction |

|

38 |

|

(1,293 |

) |

(314 |

) |

878 |

| ||||

|

Real estate-residential |

|

|

|

|

|

|

|

|

| ||||

|

Investor |

|

2,218 |

|

187 |

|

2,133 |

|

3,234 |

| ||||

|

Owner occupied |

|

350 |

|

343 |

|

401 |

|

1,440 |

| ||||

|

Revolving and junior liens |

|

817 |

|

481 |

|

1,867 |

|

1,290 |

| ||||

|

Total real estate-residential |

|

3,385 |

|

1,011 |

|

4,401 |

|

5,964 |

| ||||

|

Real estate-commercial, nonfarm |

|

|

|

|

|

|

|

|

| ||||

|

Owner general purpose |

|

(5 |

) |

(39 |

) |

(43 |

) |

1,100 |

| ||||

|

Owner special purpose |

|

(5 |

) |

62 |

|

(148 |

) |

1,288 |

| ||||

|

Non-owner general purpose |

|

— |

|

119 |

|

(156 |

) |

4,492 |

| ||||

|

Non-owner special purpose |

|

73 |

|

— |

|

(751 |

) |

78 |

| ||||

|

Retail properties |

|

265 |

|

137 |

|

(277 |

) |

4,038 |

| ||||

|

Total real estate-commercial, nonfarm |

|

328 |

|

279 |

|

(1,375 |

) |

10,996 |

| ||||

|

Real estate-commercial, farm |

|

— |

|

— |

|

— |

|

— |

| ||||

|

Commercial |

|

(31 |

) |

(20 |

) |

204 |

|

78 |

| ||||

|

Other |

|

25 |

|

52 |

|

84 |

|

108 |

| ||||

|

|

|

$ |

3,745 |

|

$ |

29 |

|

$ |

3,000 |

|

$ |

18,024 |

|

Charge-offs for third quarter 2013 were primarily from previously established specific reserves on nonaccrual loans deemed uncollectible. Charge-off activity continued to improve for the year to date period in 2013 compared to the same year to date period in 2012, reflecting an improved economy in our target markets and past work done on loan quality improvement.

|

|

|

Nonperforming Loans as of |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Real estate-construction |

|

$ |

5,928 |

|

$ |

6,303 |

|

$ |

16,035 |

|

$ |

(375 |

) |

$ |

(10,107 |

) |

|

Real estate-residential: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Investor |

|

8,307 |

|

13,662 |

|

13,007 |

|

(5,355 |

) |

(4,700 |

) | |||||

|

Owner occupied |

|

6,212 |

|

7,927 |

|

14,875 |

|

(1,715 |

) |

(8,663 |

) | |||||

|

Revolving and junior liens |

|

2,543 |

|

3,431 |

|

3,306 |

|

(888 |

) |

(763 |

) | |||||

|

Real estate-commercial, nonfarm |

|

24,754 |

|

31,190 |

|

55,642 |

|

(6,436 |

) |

(30,888 |

) | |||||

|

Real estate-commercial, farm |

|

— |

|

53 |

|

1,790 |

|

(53 |

) |

(1,790 |

) | |||||

|

Commercial |

|

29 |

|

104 |

|

1,157 |

|

(75 |

) |

(1,128 |

) | |||||

|

|

|

$ |

47,773 |

|

$ |

62,670 |

|

$ |

105,812 |

|

$ |

(14,897 |

) |

$ |

(58,039 |

) |

Nonperforming loans consist of nonaccrual loans, nonperforming restructured accruing loans and loans 90 days or greater past due still accruing. The largest decrease in the nonperforming loans since September 30, 2012 was in the real estate-commercial, nonfarm segment as this segment’s upgrades and migration to OREO were greater than the migration of loans to nonperforming status.

|

|

|

Classified loans as of |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Real estate-construction |

|

$ |

6,236 |

|

$ |

7,005 |

|

$ |

22,387 |

|

$ |

(769 |

) |

$ |

(16,151 |

) |

|

Real estate-residential: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Investor |

|

10,642 |

|

13,968 |

|

16,406 |

|

(3,326 |

) |

(5,764 |

) | |||||

|

Owner occupied |

|

7,292 |

|

11,008 |

|

17,684 |

|

(3,716 |

) |

(10,392 |

) | |||||

|

Revolving and junior liens |

|

3,675 |

|

5,086 |

|

5,053 |

|

(1,411 |

) |

(1,378 |

) | |||||

|

Real estate-commercial, nonfarm |

|

40,832 |

|

43,827 |

|

73,720 |

|

(2,995 |

) |

(32,888 |

) | |||||

|

Real estate-commercial, farm |

|

— |

|

53 |

|

1,790 |

|

(53 |

) |

(1,790 |

) | |||||

|

Commercial |

|

264 |

|

705 |

|

1,748 |

|

(441 |

) |

(1,484 |

) | |||||

|

Other |

|

1 |

|

1 |

|

5 |

|

— |

|

(4 |

) | |||||

|

|

|

$ |

68,942 |

|

$ |

81,653 |

|

$ |

138,793 |

|

$ |

(12,711 |

) |

$ |

(69,851 |

) |

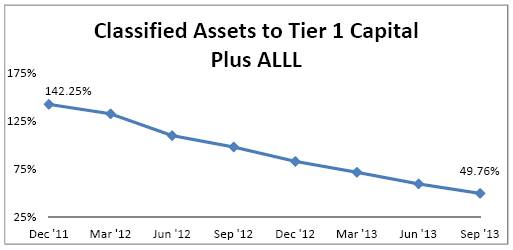

Classified loans include nonaccrual, performing troubled debt restructurings and all other loans considered substandard. All three components are down since September 30, 2012. Classified assets include both classified loans and OREO. Management monitors a ratio of classified assets to the sum of Bank Tier 1 capital and the allowance for loan and lease loss reserve. This ratio reflects another measure of overall improvement in loan related asset quality. The decline in both classified loans and OREO as well as improved Tier 1 capital in the third quarter improved this ratio for the eleventh straight quarter.

Allowance for Loan and Lease Losses

Below is a reconciliation for the activity for the periods indicated (in thousands):

|

|

|

Three Months Ending |

| |||||||

|

|

|

9/30/2013 |

|

6/30/2013 |

|

9/30/2012 |

| |||

|

|

|

|

|

|

|

|

| |||

|

Allowance at beginning of quarter |

|

$ |

35,042 |

|

$ |

38,634 |

|

$ |

40,286 |

|

|

Charge-offs: |

|

|

|

|

|

|

| |||

|

Commercial |

|

29 |

|

25 |

|

2 |

| |||

|

Real estate - commercial |

|

851 |

|

1,018 |

|

355 |

| |||

|

Real estate - construction |

|

53 |

|

894 |

|

909 |

| |||

|

Real estate - residential |

|

3,594 |

|

1,014 |

|

1,230 |

| |||

|

Consumer and other loans |

|

168 |

|

134 |

|

186 |

| |||

|

Total charge-offs |

|

4,695 |

|

3,085 |

|

2,682 |

| |||

|

Recoveries: |

|

|

|

|

|

|

| |||

|

Commercial |

|

60 |

|

25 |

|

22 |

| |||

|

Real estate - commercial |

|

523 |

|

505 |

|

76 |

| |||

|

Real estate - construction |

|

15 |

|

480 |

|

2,202 |

| |||

|

Real estate - residential |

|

209 |

|

179 |

|

219 |

| |||

|

Consumer and other loans |

|

143 |

|

104 |

|

134 |

| |||

|

Total recoveries |

|

950 |

|

1,293 |

|

2,653 |

| |||

|

Net charge-offs (recoveries) |

|

3,745 |

|

1,792 |

|

29 |

| |||

|

(Release) provision for loan losses |

|

(1,750 |

) |

(1,800 |

) |

— |

| |||

|

Allowance at end of quarter |

|

$ |

29,547 |

|

$ |

35,042 |

|

$ |

40,257 |

|

|

|

|

|

|

|

|

|

| |||

|

Average total loans (exclusive of loans held-for-sale) |

|

$ |

1,085,487 |

|

$ |

1,113,315 |

|

$ |

1,222,829 |

|

|

Net charge-offs to average loans |

|

0.35 |

% |

0.16 |

% |

0.00 |

% | |||

|

Allowance at quarter end to average loans |

|

2.72 |

% |

3.15 |

% |

3.29 |

% | |||

|

|

|

|

|

|

|

|

| |||

|

Ending balance: Individually evaluated for impairment |

|

$ |

2,150 |

|

$ |

5,036 |

|

$ |

7,585 |

|

|

Ending balance: Collectively evaluated for impairment |

|

$ |

27,397 |

|

$ |

30,006 |

|

$ |

32,672 |

|

The coverage ratio of the allowance for loan losses to nonperforming loans was 61.9% as of September 30, 2013, which reflects an increase from 55.9% as of June 30, 2013. A decrease of $14.9 million in nonperforming loans in the three months drove the overall coverage ratio change. Management updated the estimated specific allocations in the third quarter after receiving more recent appraisals for detailed collateral valuations or information on cash flow trends related to the impaired credits. Management determined the estimated amount to provide in the allowance for loan losses based upon a number of considerations, including loan growth or contraction, the quality and composition of the loan portfolio and loan loss experience. The latter item was also weighted more heavily based upon recent loss experience. The construction and development (“C & D”) portfolio, which has accounted for significant losses in previous periods, has had diminished adverse migration and the remaining credits are exhibiting more stable credit characteristics. Management believes that adequate reserves have been established for the inherent risk of loss in the C & D portfolio.

Management regularly reviews the performance of the higher risk pool within commercial real estate loans and adjusts the population and the related loss factors taking into account adverse market trends, including collateral valuation, as well as assessments of the credits in that pool. Those assessments capture management’s estimate of the potential for adverse migration to an impaired status as well as its estimation of what the potential valuation impact from that migration would be if it were to occur. The amount of assets subject to this pool factor decreased by 36.5% at September 30, 2013, as compared to December 31, 2012. Management has also observed that many stresses in those credits were generally attributable to cyclical economic events that were showing some signs of stabilization. Those signs included a reduction in loan migration to watch status, as well as a decrease in 30 to 89 day past due loans and some stabilization in values of certain properties.

The above changes in estimates were made by management to be consistent with observable trends within loan portfolio segments and in conjunction with market conditions and credit review administration activities. Several environmental factors are also evaluated on an ongoing basis and are

included in the assessment of the adequacy of the allowance for loan losses. Management determined that an overall improvement in loan asset quality justified a $1.8 million loan loss reserve release in the third quarter. When measured as a percentage of loans outstanding, the total allowance for loan losses decreased from 3.33% of total loans as of September 30, 2012, to 2.74% of total loans at September 30, 2013. In management’s judgment, an adequate allowance for estimated losses has been established for inherent losses at September 30, 2013; however, there can be no assurance that actual losses will not exceed the estimated amounts in the future.

Other Real Estate Owned

OREO decreased $10.4 million, from $59.5 million at June 30, 2013, to $49.1 million at September 30, 2013. Disposition activity and valuation writedowns in the third quarter more than offset numerous but smaller dollar additions to OREO, leading to this overall decrease. In the third quarter of 2013, management successfully managed OREO transactions as shown below. As a result, OREO holdings in all categories (vacant land suitable for farming, single family residences, lots suitable for development, multi-family and commercial property) were down in the quarter. Overall, a net gain on sale of $608,000 was realized in the third quarter.

|

|

|

Three Months Ended |

|

Year to Date |

| ||||||||

|

|

|

September 30, |

|

September 30, |

| ||||||||

|

(in thousands) |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| ||||

|

Beginning balance |

|

$ |

59,465 |

|

$ |

89,671 |

|

$ |

72,423 |

|

$ |

93,290 |

|

|

Property additions |

|

3,015 |

|

7,594 |

|

14,196 |

|

26,944 |

| ||||

|

Development improvements |

|

10 |

|

131 |

|

60 |

|

646 |

| ||||

|

Less: |

|

|

|

|

|

|

|

|

| ||||

|

Property disposals |

|

11,463 |

|

4,829 |

|

30,928 |

|

20,517 |

| ||||

|

Period valuation adjustments |

|

1,961 |

|

4,474 |

|

6,685 |

|

12,270 |

| ||||

|

Other real estate owned |

|

$ |

49,066 |

|

$ |

88,093 |

|

$ |

49,066 |

|

$ |

88,093 |

|

The OREO valuation reserve decreased to $24.6 million, which was 33.4% of gross OREO at September 30, 2013. The valuation reserve represented 24.9% and 30.3% of gross OREO at September 30, 2012 and December 31, 2012, respectively. In management’s judgment, an adequate property valuation allowance has been established to present OREO at current estimates of fair value less costs to sell; however, there can be no assurance that additional losses will not be incurred on disposition or updates to valuation in the future.

OREO Properties by Type

|

|

|

September 30, 2013 |

|

June 30, 2013 |

|

September 30, 2012 |

| |||||||||

|

(in thousands) |

|

Amount |

|

% of Total |

|

Amount |

|

% of Total |

|

Amount |

|

% of Total |

| |||

|

Single family residence |

|

$ |

6,585 |

|

13% |

|

$ |

8,161 |

|

14% |

|

$ |

10,642 |

|

12% |

|

|

Lots (single family and commercial) |

|

18,993 |

|

39% |

|

23,781 |

|

40% |

|

29,638 |

|

34% |

| |||

|

Vacant land |

|

3,135 |

|

6% |

|

3,266 |

|

5% |

|

7,325 |

|

8% |

| |||

|

Multi-family |

|

2,194 |

|

5% |

|

2,210 |

|

4% |

|

9,447 |

|

11% |

| |||

|

Commercial property |

|

18,159 |

|

37% |

|

22,047 |

|

37% |

|

31,041 |

|

35% |

| |||

|

Total OREO properties |

|

$ |

49,066 |

|

100% |

|

$ |

59,465 |

|

100% |

|

$ |

88,093 |

|

100% |

|

Net OREO Aging

|

|

|

September 30, 2013 |

|

June 30, 2013 |

|

September 30, 2012 |

| |||||||||

|

(in thousands) |

|

Amount |

|

% of Total |

|

Amount |

|

% of Total |

|

Amount |

|

% of Total |

| |||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||

|

0-90 Days |

|

$ |

3,012 |

|

6% |

|

$ |

4,025 |

|

7% |

|

$ |

7,249 |

|

8% |

|

|

91-180 Days |

|

3,033 |

|

6% |

|

3,086 |

|

5% |

|

2,654 |

|

3% |

| |||

|

181 Days - 1 Year |

|

4,968 |

|

10% |

|

6,380 |

|

11% |

|

18,036 |

|

21% |

| |||

|

1 Year to 2 Years |

|

10,569 |

|

22% |

|

20,356 |

|

34% |

|

44,836 |

|

51% |

| |||

|

2 Years to 3 Years |

|

20,738 |

|

42% |

|

17,404 |

|

29% |

|

10,507 |

|

12% |

| |||

|

3 Years to 4 Years |

|

5,189 |

|

11% |

|

4,529 |

|

8% |

|

4,663 |

|

5% |

| |||

|

4 Years + |

|

1,557 |

|

3% |

|

3,685 |

|

6% |

|

148 |

|

0% |

| |||

|

Total |

|

$ |

49,066 |

|

100% |

|

$ |

59,465 |

|

100% |

|

$ |

88,093 |

|

100% |

|

As part of our OREO management process, we age or track the time that OREO is held for sale. The table above shows that, in total, where 32% of our OREO at September 30, 2012, had been held for less than one year, that percentage dropped to 22% at September 30, 2013. When properties are tracked as being held for one to three years, the percentage of total OREO in those categories rose to 64% at September 30, 2013, essentially unchanged from 63% at September 30, 2012. While the dollar totals held for more than three years were smaller than other aging categories, a similar trend was found in properties held in OREO for more than three years (14% as of September 30, 2013, an increase of 9% from September 30, 2012) with approximately $1.6 million held for over four years at September 30, 2013.

While newer properties additions to our OREO have slowed, some items held in OREO have been slow to sell leading to the above aging trend. Properties held for longer periods can be a source of incremental cost as they age on the market.

Noninterest Income

|

|

|

Three Months Ended |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Noninterest income |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Trust income |

|

$ |

1,494 |

|

$ |

1,681 |

|

$ |

1,489 |

|

$ |

(187 |

) |

$ |

5 |

|

|

Service charges on deposits |

|

1,904 |

|

1,799 |

|

1,982 |

|

105 |

|

(78 |

) | |||||

|

Residential mortgage revenue |

|

1,232 |

|

2,821 |

|

2,699 |

|

(1,589 |

) |

(1,467 |

) | |||||

|

Securities gains, net |

|

(7 |

) |

745 |

|

513 |

|

(752 |

) |

(520 |

) | |||||

|

Increase in cash surrender value of bank-owned life insurance |

|

419 |

|

372 |

|

425 |

|

47 |

|

(6 |

) | |||||

|

Death benefit realized on bank-owned life insurance |

|

6 |

|

375 |

|

— |

|

(369 |

) |

6 |

| |||||

|

Debit card interchange income |

|

873 |

|

900 |

|

788 |

|

(27 |

) |

85 |

| |||||

|

Lease revenue from other real estate owned |

|

309 |

|

257 |

|

840 |

|

52 |

|

(531 |

) | |||||

|

Net gain on sales of other real estate owned |

|

608 |

|

386 |

|

20 |

|

222 |

|

588 |

| |||||

|

Other income |

|

1,549 |

|

1,147 |

|

1,592 |

|

402 |

|

(43 |

) | |||||

|

Total noninterest income |

|

$ |

8,387 |

|

$ |

10,483 |

|

$ |

10,348 |

|

$ |

(2,096 |

) |

$ |

(1,961 |

) |

Noninterest income is down in the third quarter from the second quarter as a result of sharply lower residential mortgage revenue and gains on securities sales. Other income increased in the third quarter from the second quarter on recognition in income of a forfeited purchase deposit from a loan sale where the purchaser did not complete the sale as contractually required. Similar results are found in the year over year comparison except that other income was essentially flat.

Noninterest Expense

|

|

|

Three Months Ended |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Noninterest expense |

|

|

|

|

|

|

|

|

|

|

| |||||

|

Salaries and employee benefits |

|

$ |

9,299 |

|

$ |

9,177 |

|

$ |

8,963 |

|

$ |

122 |

|

$ |

336 |

|

|

Occupancy expense, net |

|

1,266 |

|

1,242 |

|

1,242 |

|

24 |

|

24 |

| |||||

|

Furniture and equipment expense |

|

1,026 |

|

1,104 |

|

1,078 |

|

(78 |

) |

(52 |

) | |||||

|

FDIC insurance |

|

987 |

|

1,024 |

|

1,029 |

|

(37 |

) |

(42 |

) | |||||

|

General bank insurance |

|

489 |

|

491 |

|

851 |

|

(2 |

) |

(362 |

) | |||||

|

Amortization of core deposit intangible assets |

|

524 |

|

525 |

|

420 |

|

(1 |

) |

104 |

| |||||

|

Advertising expense |

|

347 |

|

328 |

|

400 |

|

19 |

|

(53 |

) | |||||

|

Debit card interchange expense |

|

366 |

|

362 |

|

388 |

|

4 |

|

(22 |

) | |||||

|

Legal fees |

|

615 |

|

486 |

|

760 |

|

129 |

|

(145 |

) | |||||

|

OREO valuation expense |

|

1,961 |

|

2,589 |

|

4,474 |

|

(628 |

) |

(2,513 |

) | |||||

|

Other OREO expense |

|

1,500 |

|

1,356 |

|

2,071 |

|

144 |

|

(571 |

) | |||||

|

Other expense |

|

3,119 |

|

3,510 |

|

3,187 |

|

(391 |

) |

(68 |

) | |||||

|

Total noninterest expense |

|

$ |

21,499 |

|

$ |

22,194 |

|

$ |

24,863 |

|

$ |

(695 |

) |

$ |

(3,364 |

) |

Salaries and benefits were up from the second quarter 2013 and year over year on accrual of management bonus amounts under Board approved incentive plans. Legal fees increased on complex loan workouts in the third quarter. Legal fees were down year over year on continued management control of legal expense. OREO valuation expense decreased from the second quarter 2013 and third quarter 2012 as property valuation declines, while still sizable, were more moderate than in the past.

Additional Loan Detail

|

|

|

Major Classification of Loans as of |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Commercial |

|

$ |

86,822 |

|

$ |

86,173 |

|

$ |

81,438 |

|

$ |

649 |

|

$ |

5,384 |

|

|

Real estate - commercial |

|

554,874 |

|

563,061 |

|

621,715 |

|

(8,187 |

) |

(66,841 |

) | |||||

|

Real estate - construction |

|

30,996 |

|

34,964 |

|

48,606 |

|

(3,968 |

) |

(17,610 |

) | |||||

|

Real estate - residential |

|

376,859 |

|

386,504 |

|

436,837 |

|

(9,645 |

) |

(59,978 |

) | |||||

|

Consumer |

|

2,570 |

|

2,793 |

|

3,167 |

|

(223 |

) |

(597 |

) | |||||

|

Overdraft |

|

544 |

|

505 |

|

613 |

|

39 |

|

(69 |

) | |||||

|

Lease financing receivables |

|

11,204 |

|

11,863 |

|

3,229 |

|

(659 |

) |

7,975 |

| |||||

|

Other |

|

13,236 |

|

16,371 |

|

12,677 |

|

(3,135 |

) |

559 |

| |||||

|

|

|

1,077,105 |

|

1,102,234 |

|

1,208,282 |

|

(25,129 |

) |

(131,177 |

) | |||||

|

Net deferred loan costs and (fees) |

|

535 |

|

469 |

|

7 |

|

66 |

|

528 |

| |||||

|

|

|

$ |

1,077,640 |

|

$ |

1,102,703 |

|

$ |

1,208,289 |

|

$ |

(25,063 |

) |

$ |

(130,649 |

) |

Trends seen in the past continued in the third quarter. As in the past, while loan pipelines are increasing, the lack of expansion by local businesses is still leading to weaker loan demand while competition remains intense. Low line utilization and loan maturities in the face of difficult pricing competition continue. Ongoing pay downs along with the reduced volume of transactional business, although at a slower than historical pace, have contributed to the overall loan decline.

Additional Securities Detail

|

|

|

As of |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Securities available-for-sale, at fair value |

|

|

|

|

|

|

|

|

|

|

| |||||

|

U.S. Treasury |

|

$ |

1,548 |

|

$ |

1,547 |

|

$ |

1,511 |

|

$ |

1 |

|

$ |

37 |

|

|

U.S. government agencies |

|

1,693 |

|

6,726 |

|

49,455 |

|

(5,033 |

) |

(47,762 |

) | |||||

|

U.S. government agency mortgage-backed |

|

— |

|

52,414 |

|

73,291 |

|

(52,414 |

) |

(73,291 |

) | |||||

|

States and political subdivisions |

|

19,841 |

|

20,119 |

|

12,805 |

|

(278 |

) |

7,036 |

| |||||

|

Corporate Bonds |

|

22,200 |

|

34,429 |

|

34,217 |

|

(12,229 |

) |

(12,017 |

) | |||||

|

Collateralized mortgage obligations |

|

48,125 |

|

168,505 |

|

96,438 |

|

(120,380 |

) |

(48,313 |

) | |||||

|

Asset-backed securities |

|

268,984 |

|

290,853 |

|

135,086 |

|

(21,869 |

) |

133,898 |

| |||||

|

Collateralized debt obligations |

|

11,087 |

|

10,344 |

|

9,543 |

|

743 |

|

1,544 |

| |||||

|

Total securities available-for-sale |

|

$ |

373,478 |

|

$ |

584,937 |

|

$ |

412,346 |

|

$ |

(211,459 |

) |

$ |

(38,868 |

) |

|

Securities held-to-maturity, at amortized cost |

|

|

|

|

|

|

|

|

|

|

| |||||

|

U.S. government agency mortgage-backed |

|

$ |

35,241 |

|

$ |

— |

|

$ |

— |

|

$ |

35,241 |

|

$ |

35,241 |

|

|

Collateralized mortgage obligations |

|

222,860 |

|

— |

|

— |

|

222,860 |

|

222,860 |

| |||||

|

Total securities held-to-maturity |

|

$ |

258,101 |

|

$ |

— |

|

$ |

— |

|

$ |

258,101 |

|

$ |

258,101 |

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||

|

Total secutities |

|

$ |

631,579 |

|

$ |

584,937 |

|

$ |

412,346 |

|

$ |

46,642 |

|

$ |

219,233 |

|

Total holdings show a net increase of $46.6 million since June 30, 2013 with all categories declining except total collateralized mortgage obligations, which were up $102.5 million in the period. Securities held with the intent to hold to maturity were established in the third quarter in response to increases in overall market interest rates. Management decisions on securities to be classified as held to maturity were made based on the characteristics of individual securities.

Deposits Detail

|

|

|

As Of |

|

September 30, 2013 |

| |||||||||||

|

|

|

September 30, |

|

June 30, |

|

September 30, |

|

June 30, |

|

September 30, |

| |||||

|

(in thousands) |

|

2013 |

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| |||||

|

Noninterest bearing |

|

$ |

373,499 |

|

$ |

366,406 |

|

$ |

381,111 |

|

$ |

7,093 |

|

$ |

(7,612 |

) |

|

Savings |

|

227,823 |

|

227,687 |

|

211,452 |

|

136 |

|

16,371 |

| |||||

|

NOW accounts |

|

272,632 |

|

287,492 |

|

265,215 |

|

(14,860 |

) |

7,417 |

| |||||

|

Money market accounts |

|

309,066 |

|

312,773 |

|

321,614 |

|

(3,707 |

) |

(12,548 |

) | |||||

|

Certificates of deposits: |

|

|

|

|

|

|

|

|

|

|

| |||||

|

of less than $100,000 |

|

299,632 |

|

306,302 |

|

323,464 |

|

(6,670 |

) |

(23,832 |

) | |||||

|

of $100,000 or more |

|

190,471 |

|

189,963 |

|

194,078 |

|

508 |

|

(3,607 |

) | |||||

|

|

|

$ |

1,673,123 |

|

$ |

1,690,623 |

|

$ |

1,696,934 |

|

$ |

(17,500 |

) |

$ |

(23,811 |

) |

The Company saw some decline in total deposits in the third quarter and year over year, but overall total deposits were essentially flat during the quarter and year over year reflecting sluggish loan activity and other liquidity sources. Deposit growth goal for 2013 through the end of the third quarter was not attained.

Borrowings

One of the Company’s most significant borrowing relationships continued to be the $45.5 million credit facility with Bank of America. That credit facility began in January 2008 and was originally composed of a $30.5 million senior debt facility including $500,000 in term debt, as well as $45.0 million of subordinated debt. The subordinated debt and the term debt portion of the senior debt facility mature on March 31, 2018. The interest rate on the senior debt facility resets quarterly and is based on, at the Company’s option, either the lender’s prime rate or three-month LIBOR plus 90 basis points. The interest rate on the subordinated debt resets quarterly and is equal to three-month LIBOR plus 150 basis

points. The Company had no principal outstanding balance on the senior line of credit when it matured but did have $500,000 in principal outstanding in term debt and $45.0 million in principal outstanding in subordinated debt at the end of both December 31, 2012, and September 30, 2013. The term debt is secured by all of the outstanding capital stock of the Bank. The Company has made all required interest payments on the outstanding principal amounts on a timely basis. Pursuant to the Written Agreement described below with the Federal Reserve Bank of Chicago (the “Federal Reserve”), the Company must receive the Federal Reserve’s approval prior to making any interest payments on the subordinated debt.

The credit facility agreement contains usual and customary provisions regarding acceleration of the senior debt upon the occurrence of an event of default by the Company under the senior debt agreement. The senior debt agreement also contains certain customary representations and warranties and financial and negative covenants. At September 30, 2013, the Company was out of compliance with one of the financial covenants contained within the credit agreement. Previously, the Company had been out of compliance with two of the financial covenants. The agreement provides that upon an event of default as the result of the Company’s failure to comply with a financial covenant, relating to the senior debt, the lender may (i) terminate all commitments to extend further credit, (ii) increase the interest rate on the revolving line of the term debt by 200 basis points, (iii) declare the senior debt immediately due and payable, and (iv) exercise all of its rights and remedies at law, in equity and/or pursuant to any or all collateral documents, including foreclosing on the collateral. The total outstanding principal amount of the senior debt is the $500,000 in term debt. Because the subordinated debt is treated as Tier 2 capital for regulatory capital purposes, the senior debt agreement does not provide the lender with any rights of acceleration or other remedies with regard to the subordinated debt upon an event of default caused by the Company’s failure to comply with a financial covenant.

The Company increased its securities sold under repurchase agreements $2.8 million, or 15.9%, from December 31, 2012. The Company’s other short-term borrowings decreased $45.0 million from December 31, 2012, as a Federal Home Loan Bank of Chicago (“FHLB”) advance matured and was replaced with short term FHLB advances that will mature in October 2013.

Capital

The Company completed the sale of $27.5 million of cumulative trust preferred securities by its unconsolidated subsidiary, Old Second Capital Trust I in June 2003. An additional $4.1 million of cumulative trust preferred securities was sold in July 2003. The costs associated with the issuance of the cumulative trust preferred securities are being amortized over 30 years. The trust preferred securities may remain outstanding for a 30-year term but, subject to regulatory approval, can be called in whole or in part by the Company. The stated call period commenced on June 30, 2008 and a call can be exercised by the Company from time to time thereafter. When not in deferral, cash distributions on the securities are payable quarterly at an annual rate of 7.80%. The Company issued a new $32.6 million subordinated debenture to the trust in return for the aggregate net proceeds of this trust preferred offering. The interest rate and payment frequency on the debenture are equivalent to the cash distribution basis on the trust preferred securities.

The Company issued an additional $25.0 million of cumulative trust preferred securities through a private placement completed by an additional unconsolidated subsidiary, Old Second Capital Trust II, in April 2007. Although nominal in amount, the costs associated with that issuance are being amortized over 30 years. These trust preferred securities also mature in 30 years, but subject to the aforementioned regulatory approval, can be called in whole or in part on a quarterly basis commencing June 15, 2017. The quarterly cash distributions on the securities are fixed at 6.77% through June 15, 2017 and float at 150 basis points over three-month LIBOR thereafter. The Company issued a new $25.8 million subordinated debenture to the Old Second Capital Trust II in return for the aggregate net proceeds of this trust preferred offering. The interest rate and payment frequency on the debenture are equivalent to the cash distribution basis on the trust preferred securities.

Under the terms of the subordinated debentures issued to each of Old Second Capital Trust I and II, the Company is allowed to defer payments of interest for 20 quarterly periods without default or

penalty, but such amounts will continue to accrue. Also during the deferral period, the Company generally may not pay cash dividends on or repurchase its common stock or preferred stock, including the Series B Stock described below . In August of 2010, the Company elected to defer regularly scheduled interest payments on the $58.4 million of junior subordinated debentures. Because of the deferral on the subordinated debentures, the trusts will defer regularly scheduled dividends on the trust preferred securities. Both of the debentures issued by the Company are recorded on the Consolidated Balance Sheets as junior subordinated debentures and the related interest expense for each issuance is included in the Consolidated Statements of Operations. The total accumulated unpaid interest on the junior subordinated debentures including compounded interest from July 1, 2010 on the deferred payments totals $15.7 million at September 30, 2013.

As of September 30, 2013, total stockholders’ equity was $142.0 million, which was an increase of $69.5 million, or 95.8%, from $72.6 million as of December 31, 2012. This increase was driven by the reversal of the valuation allowance on a significant portion of net deferred tax assets, made possible by recent profits. Unrealized loss on securities available-for-sale net of deferred taxes was $1.3 million at December 31, 2012 and $12.4 million at September 30, 2013, causing a reduction in stockholders’ equity of $11.1 million. Additionally, as discussed further below total stockholders’ equity benefited by the Company not declaring and accruing a dividend for the third quarter of 2013 on its Series B Perpetual Preferred Stock (the “Series B Stock”).

As of September 30, 2013, the Company’s regulatory capital ratios of total capital to risk weighted assets, Tier 1 capital to risk weighted assets and Tier 1 capital to average assets increased to 15.15%, 10.07% and 7.11%, respectively, compared to 13.62%, 6.81% and 4.85%, respectively, at December 31, 2012. The Company, on a consolidated basis, exceeded the minimum capital ratios to be deemed “well capitalized” at September 30, 2013. The same capital ratios at the Bank were 17.08%, 15.82% and 11.08%, respectively, at September 30, 2013, compared to 14.86%, 13.59%, and 9.67%, at December 31, 2012. The Bank’s ratios exceeded the heightened capital ratios agreed to in the May 2011 consent order the Bank entered with the Office of the Comptroller of the Currency (“OCC”) (the “Consent Order”). As indicated above, the Consent Order was terminated as of October 17, 2013.

Although the Consent Order has been terminated, the Bank continues to be subject to the risk-based capital guidelines developed by the OCC and other bank regulatory agencies. In connection with the current economic environment, the Bank’s level of nonperforming assets and the risk-based capital guidelines, the Bank’s board of directors has determined that the Bank should maintain a Tier 1 leverage capital ratio at or above eight percent (8%) and a total risk-based capital ratio at or above twelve percent (12%). The Bank currently exceeds those thresholds.

During July 2013, the Board of Governors of the Federal Reserve System and the OCC issued their final rules for regulatory capital and the implementation of Basel III that will become effective for organizations such as the Company on January 1, 2015. The final rules also introduce certain new capital and other requirements for banking organizations. Management is reviewing the new rules to assess the manner in which the new rules will impact the Company.

While the Bank’s Consent Order has been terminated by the OCC, the Company continues to be subject to a written agreement (the “Written Agreement”) with the Federal Reserve. Key provisions of the Written Agreement include restrictions on the Company’s payment of dividends on its capital stock, restrictions on the Company’s receipt of dividends or other payments from the Bank that reduce the Bank’s capital, restrictions on payments on subordinated debt and trust preferred securities, restrictions on incurring additional debt or repurchasing stock, capital planning provisions, requirements to submit cash flow projections to the Federal Reserve, requirements to comply with certain notice provisions pertaining to changes in directors or senior management, requirements to comply with regulatory restrictions on indemnification and severance payments, and requirements to submit certain reports to the Federal Reserve. The Written Agreement also calls for the Company to serve as a source of strength for the Bank.

In addition to the above regulatory ratios, the Company’s non-GAAP tangible common equity to tangible assets increased to 3.33% at September 30, 2013, largely attributable to increased capital resulting from the reversal of the valuation allowance on a significant portion of net deferred tax assets, made possible by recent profits. The Tier 1 common equity to risk weighted assets increased 0.61% at September 30, 2013. September 30, 2013 results compared to (0.17)% at September 30, 2012.

As previously announced in the third quarter of 2010, the Company elected to defer regularly scheduled interest payments on $58.4 million of junior subordinated debentures related to the trust preferred securities issued by its two statutory trust subsidiaries, Old Second Capital Trust I and Old Second Capital Trust II (the “Trust Preferred Securities”). Because of the deferral on the subordinated debentures, the trusts will defer regularly scheduled distributions on their Trust Preferred Securities. The total accumulated deferred distributions on the Trust Preferred Securities including compounded interest from July 1, 2010 totaled $15.7 million at September 30, 2013.

All of the Old Second Bancorp Series B Stock held by Treasury from the Troubled Asset Relief Program Capital Purchase Program was sold to third parties, including certain of our directors, at auctions conducted earlier this year. At December 31, 2012, Old Second Bancorp carried $71.9 million of Series B Stock in total stockholders’ equity. At September 30, 2013, the Company carried $72.7 million of Series B Stock.

Following the completed auctions, the Company’s Board elected to stop declaring and accruing the dividend on the Series B Stock. Previously, the Company had declared and accrued the dividend on the Series B Stock quarterly throughout the deferral period. Given the discount reflected in the results of the auction, the Board believes that the Company will likely be able to repurchase the Series B Stock in the future at a price less than the face amount of the Series B Stock plus accrued and unpaid dividends. Therefore, under GAAP, the Company did not fully accrue the dividend on the Series B Stock in the first quarter and did not accrue for it in subsequent quarters. The Company will continue to evaluate whether declaring dividends on the Series B Stock is appropriate in future periods. Pursuant to the terms of the Series B Stock, the dividends paid on the Series B Stock will increase from 5% to 9% in 2014.

Non-GAAP Presentations: Management has traditionally disclosed certain non-GAAP ratios to evaluate and measure the Company’s performance, including a net interest margin calculation. The net interest margin is calculated by dividing net interest income on a tax equivalent basis by average earning assets for the period. Management believes this measure provides investors with information regarding balance sheet profitability. Management also presents an efficiency ratio that is non-GAAP. The efficiency ratio is calculated by dividing adjusted noninterest expense by the sum of net interest income on a tax equivalent basis and adjusted noninterest income. Management believes this measure provides investors with information regarding the Company’s operating efficiency and how management evaluates performance internally. Consistent with industry practice, management also disclosed the tangible common equity to tangible assets and the Tier 1 common equity to risk weighted assets in the discussion immediately above and in the following tables. The tables provide a reconciliation of each non-GAAP measure to the most comparable GAAP equivalent.

Forward Looking Statements: This report may contain forward-looking statements. Forward looking statements are identifiable by the inclusion of such qualifications as expects, intends, believes, may, likely or other indications that the particular statements are not based upon facts but are rather based upon the Company’s beliefs as of the date of this release. Actual events and results may differ significantly from those described in such forward-looking statements, due to changes in the economy, interest rates or other factors. Additionally, all statements in this document, including forward-looking statements, speak only as of the date they are made, and the Company undertakes no obligation to update any statement in light of new information or future events. For additional information concerning the Company and its business, including other factors that could materially affect the Company’s financial results or cause actual results to differ substantially from those discussed or implied in forward looking statements contained in this release, please review our filings with the Securities and Exchange Commission.

Financial Highlights (unaudited)

In thousands, except share data

|

|

|

As of and for the |

|

As of and for the |

| ||||||||

|

|

|

Three Months Ended |

|

Nine Months Ended |

| ||||||||

|

|

|

September 30, |

|

September 30, |

| ||||||||

|

|

|

2013 |

|

2012 |

|

2013 |

|

2012 |

| ||||

|

Summary Statements of Operations: |

|

|

|

|

|

|

|

|

| ||||

|

Net interest and dividend income |

|

$ |

14,289 |

|

$ |

14,635 |

|

$ |

41,579 |

|

$ |

45,429 |

|

|

(Release) provision for loan losses |

|

(1,750 |

) |

— |

|

(6,050 |

) |

6,284 |

| ||||

|

Noninterest income |

|

8,387 |

|

10,348 |

|

29,466 |

|

31,208 |

| ||||

|

Noninterest expense |

|

21,499 |

|

24,863 |

|

65,220 |

|

71,949 |

| ||||

|

Benefit for income taxes |

|

(69,997 |

) |

— |

|

(69,997 |

) |

— |

| ||||

|

Net income (loss) |

|

72,924 |

|

120 |

|

81,872 |

|

(1,596 |

) | ||||

|

Net income (loss) available to common stockholders |

|

71,601 |

|

(1,135 |

) |

77,955 |

|

(5,312 |

) | ||||

|

|

|

|

|

|

|

|

|

|

| ||||

|

Key Ratios (annualized): |

|

|

|

|

|

|

|

|

| ||||

|

Return on average assets |

|

14.98 |

% |

0.02 |

% |

5.61 |

% |

(0.11 |

)% | ||||

|