Table of Contents

As filed with the Securities and Exchange Commission on July 19, 2024

File No. [ ]

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

( ) Pre-Effective Amendment No.

( ) Post-Effective Amendment No.

EMPOWER FUNDS, INC.

(Exact Name of Registrant as Specified in Charter)

8515 E. Orchard Road

Greenwood Village, Colorado 80111

(Address of Principal Executive Offices)

Registrant’s Telephone Number, including Area Code (866) 831-7129

Jonathan D. Kreider

President & Chief Executive Officer

Empower Funds, Inc.

8515 E. Orchard Road

Greenwood Village, Colorado 80111

(Name and Address of Agent for Service)

Copy to:

Ryan L. Logsdon

Chief Legal Officer & Secretary

Empower Funds, Inc.

8515 E. Orchard Road

Greenwood Village, Colorado 80111

Approximate date of proposed public offering: As soon as practicable after the effective date of this Registration Statement.

TITLE OF SECURITIES BEING REGISTERED: Shares of Common Stock (par value $0.10 per share) of the Registrant.

No filing fee is required because of reliance on Section 24(f) and an indefinite number of shares have previously been registered pursuant to Rule 24f-2 under the Investment Company Act of 1940.

It is proposed this filing will become effective on August 26, 2024, pursuant to Rule 488.

Table of Contents

Dear Shareholder,

We wish to provide you with important information concerning your investment in the Empower Ariel Mid Cap Value Fund (the “Target Fund”), a series of Empower Funds, Inc. (“Empower Funds”). The Board of Directors of Empower Funds (the “Board”) has approved the reorganization of the Target Fund into the Empower Mid Cap Value Fund (the “Acquiring Fund”), also a series of Empower Funds (the “Reorganization”). The Target Fund and the Acquiring Fund are collectively referred to herein as the “Funds” or individually as a “Fund.”

After careful consideration, the Board, including a majority of the directors who are not “interested persons” of the Funds, as that term is defined in the Investment Company Act of 1940, as amended, approved the Reorganization. Upon the recommendation of Empower Capital Management, LLC, the investment adviser of both Funds, the Board unanimously concluded that: (i) the Reorganization is in the best interests of each Fund; and (ii) the interests of the shareholders of each Fund will not be diluted as a result of the Reorganization. The Reorganization is expected to occur on or about October 25, 2024, and upon completion shareholders of the Target Fund will become shareholders of the Acquiring Fund.

The Reorganization is intended to be a tax-free reorganization for federal income tax purposes, and the closing of the Reorganization will be conditioned upon, among other things, receiving an opinion of counsel to the effect that the Reorganization will qualify as a tax-free reorganization for federal income tax purposes. As a result, it is anticipated that shareholders will not recognize any gain or loss as a direct result of this Reorganization.

Detailed information about the Agreement and Plan of Reorganization (the “Agreement”) and the reasons for the Board’s approval of the Agreement are contained in the enclosed materials.

NO ACTION ON YOUR PART IS REQUIRED TO EFFECT THE REORGANIZATION. You will automatically receive shares of the Acquiring Fund in exchange for your shares of the Target Fund on or about October 25, 2024. If you have any questions, please contact us at (866) 831-7129.

If you have any questions after considering the enclosed materials, please call.

| Sincerely, |

|

|

Jonathan D. Kreider |

| President & Chief Executive Officer |

| Empower Funds, Inc. |

Table of Contents

Important Information for Empower Ariel Mid Cap Value Fund Shareholders

The enclosed Information Statement/Prospectus describes the contemplated reorganization of the Empower Ariel Mid Cap Value Fund (the “Target Fund”), a series of Empower Funds, Inc. (“Empower Funds”), into the Empower Mid Cap Value Fund (the “Acquiring Fund”), also a series of Empower Funds (the “Reorganization”). The Target Fund and the Acquiring Fund are collectively referred to herein as the “Funds” or individually as a “Fund.”

Although we recommend that you read the complete Information Statement/Prospectus, for your convenience, we have provided the following brief overview of the Reorganization. Please refer to the more complete information about the Reorganization contained in the Information Statement/Prospectus.

SHAREHOLDER APPROVAL IS NOT REQUIRED TO EFFECT THE REORGANIZATION. YOU ARE NOT ASKED TO RETURN A PROXY OR TO TAKE ANY OTHER ACTION AT THIS TIME.

| Q. | Why am I receiving this Information Statement/Prospectus? |

| A. | You are receiving this Information Statement/Prospectus because you are invested in the Target Fund through an insurance company separate account for certain variable annuity contracts and variable life insurance policies, an individual retirement account, or a qualified retirement plan (collectively, “Permitted Accounts”). |

| Q. | What will happen on the effective date of the Reorganization? |

| A. | As of the close of business on the effective date of the Reorganization, investments in the Institutional Class and Investor Class shares of the Target Fund will automatically become investments in the corresponding Institutional Class or Investor Class shares of the Acquiring Fund. The total net asset value of the shares of the Acquiring Fund that you receive on the effective date of the Reorganization will be equal to the total net asset value of your investment in the Target Fund. You will not incur any fees or charges or any federal income tax liability as a direct result of the Reorganization. It is currently anticipated that the Reorganization will take effect on or about October 25, 2024. |

| Q. | Why has this Reorganization been proposed for the Target Fund? |

| A. | At a meeting held on June 12-13, 2024, the Board of Directors of Empower Funds (the “Board”) considered the Reorganization upon the recommendation of Empower Capital Management, LLC (“ECM”), both Funds’ investment adviser. ECM proposed the Reorganization in order to address the underperformance of the Target Fund and, secondarily, as part of a continuing effort to reduce redundancy in its fund offerings by consolidating two mid cap value offerings into a single offering, the Acquiring Fund. ECM believes that shareholders of the Target Fund will benefit from the historically better and more consistent performance of the Acquiring Fund. ECM also believes one mid cap value fund is more commercially viable and beneficial to shareholders of both Funds than maintaining two separate mid cap value funds. The Reorganization is also intended to create a larger combined Fund with a broader shareholder base and a larger asset base against which fixed dollar costs may be allocated and potentially create economies of scale to benefit shareholders. The Board concluded the Reorganization is in the best interests of the Target Fund and its shareholders, and the Target Fund’s existing shareholders will not be diluted as a result of the Reorganization. In reaching this conclusion, the Board considered a number of factors, which are discussed in greater detail in the enclosed materials. |

Table of Contents

| Q. | How do the fees and expenses compare? |

| A. | Currently, the management fee and expense limit of the Acquiring Fund is higher than the management fee and expense limit of the Target Fund. However, in connection with its approval of the Reorganization, the Board approved lowering the management fee and expense limit of the Acquiring Fund to match those of the Target Fund. The total annual operating expenses of the Acquiring Fund immediately following the Reorganization are expected to be the same as the total annual operating expenses of the Target Fund. As a result, total annual operating expenses will remain unchanged for shareholders of the Target Fund and shareholders of the Acquiring Fund will receive a reduction in total annual operating expenses when the Reorganization takes effect. For details on fees and expenses, please see the section entitled “Fees and Expenses” of the Information Statement/Prospectus. |

| Q. | Will you receive new shares in exchange for your current shares? |

| A. | Yes. As part of the Reorganization, you will receive shares of the corresponding class of the Acquiring Fund in an amount equal to the total net asset value of the Target Fund shares that you surrender in the Reorganization, determined in each case as of the close of trading on the effective date of the Reorganization. Although the number of shares of the Acquiring Fund you receive may differ from the number of shares you held in the Target Fund, the total net asset value will be the same. |

| Q. | Will I have to pay federal income taxes as a result of the Reorganization? |

| A. | No. The Reorganization is intended to qualify as a tax-free reorganization for federal income tax purposes. It is expected that shareholders of the Target Fund will recognize no gains or losses for federal income tax purposes as a direct result of the Reorganization. The section entitled “The Reorganization - Material Federal Income Tax Consequences” of the Information Statement/Prospectus provides additional information regarding the federal income tax consequences of the Reorganization. |

| Q. | Who will pay for the Reorganization? |

| A. | ECM will bear all expenses of the Reorganization even if the Reorganization is not completed, including legal costs, audit fees, and printing and mailing expenses. ECM estimates the costs of the Reorganization to be $95,000. |

| Q. | What is the timetable for the Reorganization? |

| A. | The Reorganization is expected to take effect at the close of business on October 25, 2024, or such other date as the officers of Empower Funds reasonably determine. |

| Q. | Whom do I call if I have questions? |

| A. | If you need any assistance, or have any questions regarding the Reorganization, please call (866) 831-7129. |

Table of Contents

Information Statement/Prospectus

Dated August 26, 2024

EMPOWER FUNDS, INC.

Relating to the Acquisition of the Assets and Liabilities of

EMPOWER ARIEL MID CAP VALUE FUND

by EMPOWER MID CAP VALUE FUND

This Information Statement/Prospectus is being furnished to shareholders of the Empower Ariel Mid Cap Value Fund (the “Target Fund”), a series of Empower Funds, Inc. (“Empower Funds”), a Maryland corporation registered as an open-end investment company under the Investment Company Act of 1940, as amended (the “1940 Act). This Information Statement/Prospectus is provided in connection with the reorganization of the Target Fund into the Empower Mid Cap Value Fund (the “Acquiring Fund”), also a series of Empower Funds (the “Reorganization”). The Target Fund and the Acquiring Fund are referred to herein collectively as the “Funds” and individually as a “Fund.”

Upon completion of the Reorganization, holders of Institutional Class and Investor Class shares of the Target Fund will receive Institutional Class and Investor Class shares, respectively of the Acquiring Fund. Shares of the Acquiring Fund received in the Reorganization will have the same total net asset value as the total net asset value of the Target Fund shares surrendered by such shareholders, determined in each case as of the close of trading on the closing date of the Reorganization. The Board of Directors of Empower Funds (the “Board”) determined the Reorganization is in the best interests of the Target Fund, the Acquiring Fund, and their respective shareholders. The address, principal executive office and telephone number of Empower Funds is 8515 East Orchard Road, Greenwood Village, Colorado 80111 and (866) 831-7129.

The Securities and Exchange Commission has not approved or disapproved these securities or determined whether the information in this Information Statement/Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This Information Statement/Prospectus concisely sets forth the information shareholders of the Target Fund should know about the Reorganization (in effect, investing in Institutional Class and Investor Class shares of the Acquiring Fund) and constitutes an offering of Institutional Class and Investor Class shares of common stock, par value $0.10 per share, of the Acquiring Fund. Please read it carefully and retain it for future reference.

SHAREHOLDER APPROVAL IS NOT REQUIRED TO EFFECT THE REORGANIZATION. YOU ARE NOT ASKED TO RETURN A PROXY OR TO TAKE ANY OTHER ACTION AT THIS TIME.

The following documents contain additional information about the Funds, have been filed with the Securities and Exchange Commission (“SEC”), and are incorporated into this Information Statement/Prospectus by reference:

| i. |

| ii. |

| iii. | supplement to the Empower Ariel Mid Cap Value Fund dated June 14, 2024 (File No. 811-03364). |

| iv. | the statement of additional information relating to the Reorganization, dated August 26, 2024 (the “Reorganization SAI”). |

Table of Contents

| v. |

| vi. |

No other parts of the documents referenced above are incorporated by reference herein.

Copies of the foregoing may be obtained without charge by calling (866) 831-7129 or writing to Empower Funds, Inc., Attn: Secretary, 8515 East Orchard Road, Greenwood Village, Colorado 80111. If you wish to request the Reorganization SAI, please ask for the “Reorganization SAI.”

Empower Funds is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the 1940 Act, and in accordance therewith, files reports and other information with the SEC. Reports, proxy statements, registration statements and other information filed by Empower Funds (including the registration statement relating to the Acquiring Fund on Form N-14 of which this Information Statement/Prospectus is a part) may be obtained, with payment of a duplication fee, by electronic request at the following e-mail address: publicinfo@sec.gov, or by writing the SEC’s Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, D.C. 20549. You may also access reports and other information about the Funds on the EDGAR database on the SEC’s website at http://www.sec.gov.

Table of Contents

| 1 | ||||

| 1 | ||||

| 2 | ||||

| DISTRIBUTION, PURCHASE, REDEMPTION, EXCHANGE OF SHARES AND DIVIDENDS |

2 | |||

| MATERIAL FEDERAL INCOME TAX CONSEQUENCES OF THE REORGANIZATION |

2 | |||

| 2 | ||||

| 2 | ||||

| 2 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 8 | ||||

| 8 | ||||

| 10 | ||||

| 11 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 13 | ||||

| 13 | ||||

| PAYMENTS TO INSURERS, BROKER-DEALERS AND OTHER FINANCIAL INTERMEDIARIES |

14 | |||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| CONTINUATION OF SHAREHOLDER ACCOUNTS AND PLANS; SHARE CERTIFICATES |

16 | |||

| 16 | ||||

| 16 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

| 19 | ||||

| 19 | ||||

| 22 | ||||

| 24 | ||||

| A-1 |

Table of Contents

SUMMARY

The following is a summary of the more complete information contained in this Information Statement/Prospectus and the information attached hereto or incorporated herein by reference, including the Agreement and Plan of Reorganization (the “Agreement”). Once the Reorganization is complete, shareholders of the Target Fund will become shareholders of the Acquiring Fund and will cease to be shareholders of the Target Fund. You are receiving this Information Statement/Prospectus because you are invested in the Target Fund through an insurance company separate account for a variable annuity contract or variable life insurance policy, an individual retirement account (“IRA”), or a qualified retirement plan (“Permitted Account(s)”).

Shareholders should read the entire Information Statement/Prospectus carefully together with the Acquiring Fund’s Prospectus which is incorporated herein by reference. This Information Statement/Prospectus constitutes an offering of Institutional Class and Investor Class shares of the Acquiring Fund.

The Target Fund was launched January 1, 1994, and the Acquiring Fund was launched May 15, 2008. Empower Capital Management, LLC (“ECM”) is the adviser to both the Target Fund and Acquiring Fund. Ariel Investments, LLC (“Ariel”) is the sub-adviser of the Target Fund, and Goldman Sachs Asset Management, L.P. (“GSAM”) is the sub-adviser of the Acquiring Fund.

ECM proposed the Reorganization in order to address the underperformance of the Target Fund and, secondarily, as part of a continuing effort to reduce redundancy in its fund offerings by consolidating two mid cap value offerings into a single offering, the Acquiring Fund. ECM believes that shareholders of the Target Fund will benefit from the historically better and more consistent performance of the Acquiring Fund. ECM also believes one mid cap value fund is more commercially viable and beneficial to shareholders of both Funds than maintaining two separate mid cap value funds. The Reorganization is also intended to create a larger combined Fund with a broader shareholder base and a larger asset base against which fixed dollar costs may be allocated and potentially create economies of scale to benefit shareholders. It is intended that GSAM will continue to be the sub-adviser of the Acquiring Fund at the close of business on or about October 25, 2024 (the “Closing Date”).

Currently, the management fee and expense limit of the Acquiring Fund is higher than the management fee and expense limit of the Target Fund. However, in connection with its approval of the Reorganization, the Board approved lowering the management fee and expense limit of the Acquiring Fund to match those of the Target Fund. The total annual operating expenses of the Acquiring Fund immediately following the Reorganization are expected to be the same as the total annual operating expenses of the Target Fund. As a result, total annual operating expenses will remain unchanged for shareholders of the Target Fund and shareholders of the Acquiring Fund will receive a reduction in total annual operating expenses when the Reorganization takes effect. For more details on fees and expenses, please see “Fees and Expenses” below.

This Information Statement/Prospectus is being furnished to shareholders of the Target Fund in connection with the reorganization of the Target Fund with and into the Acquiring Fund pursuant to the terms and conditions of the Agreement entered into by Empower Funds, on behalf of the Funds and ECM. The Agreement provides for (i) the transfer of all assets of the Target Fund to the Acquiring Fund in exchange for Institutional Class and Investor Class shares of common stock, par value $0.10 per share, of the Acquiring Fund, and the assumption by the Acquiring Fund of all the liabilities of the Target Fund; and (ii) the distribution by the Target Fund of Institutional Class and Investor Class shares of the Acquiring Fund to holders of the Target Fund’s Institutional Class and Investor Class shares, respectively, resulting in the complete liquidation and termination of the Target Fund. The Board unanimously approved the Reorganization and the Agreement at a meeting held on June 12-13, 2024. Once the Reorganization is completed, Target Fund shareholders will become shareholders of the Acquiring Fund.

It is anticipated that the closing of the Reorganization (the “Closing”) will occur at the close of business on the Closing Date, but it may be at a different time as described herein. For a more detailed discussion about the Reorganization, please see “The Reorganization” below.

1

Table of Contents

Reasons for the Reorganization

The Board believes the Reorganization is in the best interests of the Target Fund and the Acquiring Fund, as well as their respective shareholders. For a more detailed discussion of the Board’s considerations regarding the approval of the Reorganization, see “The Board’s Approval of the Reorganization” below.

Distribution, Purchase, Redemption, Exchange of Shares and Dividends

The Funds have identical procedures for purchasing, exchanging, and redeeming shares for each share class. The Funds offer two classes of shares: Institutional Class and Investor Class. The corresponding classes of each Fund have the same investment eligibility criteria. Each Fund earns dividends, interest and other income from its investments, and ordinarily distributes this income (less expenses), if any, to shareholders as dividends annually. Each Fund also realizes capital gains from its investments, and distributes these gains (less any losses), if any, to shareholders as capital gains distributions at least once annually. See “Comparison of the Funds - Purchase and Sale of Fund Shares” below for a more detailed discussion.

Material Federal Income Tax Consequences of the Reorganization

It is expected that neither shareholders of the Target Fund nor investors who hold shares of the Target Fund through Permitted Accounts will recognize gain or loss for federal income tax purposes as a direct result of the Reorganization. In addition, neither Fund will generally recognize gain nor loss for federal income tax purposes as a direct result of the Reorganization. To the extent that portfolio investments received by the Acquiring Fund in the Reorganization are sold after the Reorganization, the Acquiring Fund may recognize income and capital gain (after the application of any available capital loss carryovers), which will be distributed to shareholders who hold shares of the combined fund (including former Target Fund shareholders who hold shares of the Acquiring Fund following the Reorganization). Such distribution is not expected to be taxable for federal income tax purposes to investors who hold shares of the Acquiring Fund through Permitted Accounts. None of the Target Fund’s investments are expected to be sold after the Reorganization as a result of any portfolio repositioning.

It is estimated that approximately 97% of the Target Fund’s portfolio will be sold prior to the Reorganization in connection with this portfolio repositioning. It is estimated that such portfolio repositioning would have resulted in realized losses of approximately $2,684,072 (approximately $0.03 per share) and brokerage commissions or other transaction costs of approximately $7,939 (approximately $0.003 per share), based on average commission rates normally paid by the Acquiring Fund, if such sales occurred on December 31, 2023. For a more detailed discussion of the federal income tax consequences of this Reorganization, please see “The Reorganization - Material Federal Income Tax Consequences” below.

The Funds have substantially similar investment objectives.

| Target Fund – Investment Objective | Acquiring Fund – Investment Objective | |

| The Fund seeks long-term capital appreciation. |

The Fund seeks long-term growth of capital. |

The table below provides information about the fees and expenses attributable to Institutional Class and Investor Class shares of the Funds, and the pro forma fees and expenses of the combined fund. The pro forma fees and expenses are based on the amounts shown in the table for each Fund, assuming the Reorganization occurred as of the fiscal year ended December 31, 2023. The tables below do not reflect the fees and expenses of any Permitted Account. If the fees and expenses imposed by a Permitted Account were reflected, the fees and expenses shown below would be higher because the Permitted Accounts contain fees and expenses that are separate and distinct from the fees and expenses associated with investing in a Fund.

2

Table of Contents

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)

| Target Fund as of 12/31/2023 |

Acquiring Fund as of 12/31/2023 |

Combined Fund Pro Forma as of 12/31/2023

| ||||

| Institutional Class | ||||||

| Management Fees |

0.67% | 0.78% | 0.67% | |||

| Distribution and Service (12b-1) Fees |

0.00% | 0.00% | 0.00% | |||

| Total Other Expenses |

0.11% | 0.03% | 0.11% | |||

| Shareholder Services Expenses |

0.00% | 0.00% | 0.00% | |||

| Other Expenses |

0.11% | 0.03% | 0.11% | |||

| Total Annual Fund Operating Expenses |

0.78% | 0.81% | 0.78% | |||

| Fee Waiver and Expense Reimbursements |

(0.08)%1 | (0.01)%2 | (0.08)%3 | |||

| Total Annual Fund Operating Expenses After Reimbursements |

0.70% | 0.80% | 0.70% | |||

1 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.70% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs for the Target Fund (the “Target Fund Expense Limit”). The agreement’s current term ends on April 30, 2025, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Target Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Target Fund Expense Limit in place at the time of recoupment.

2 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.80% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Acquiring Fund Expense Limit”). The agreement’s current term ends on April 30, 2026, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Acquiring Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Acquiring Fund Expense Limit in place at the time of recoupment.

3 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.70% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Combined Fund Expense Limit”). The agreement’s current term ends on April 30, 2026, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Combined Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Combined Fund Expense Limit in place at the time of recoupment.

3

Table of Contents

| Target Fund as of 12/31/2023 |

Acquiring Fund as of 12/31/2023 |

Combined Fund Pro Forma as of 12/31/2023

| ||||

| Investor Class | ||||||

| Management Fees |

0.67% | 0.78% | 0.67% | |||

| Distribution and Service (12b-1) Fees |

0.00% | 0.00% | 0.00% | |||

| Total Other Expenses |

0.47% | 0.46% | 0.47% | |||

| Shareholder Services Expenses |

0.35% | 0.35% | 0.35% | |||

| Other Expenses |

0.12% | 0.11% | 0.12% | |||

| Total Annual Fund Operating Expenses |

1.14% | 1.24% | 1.14% | |||

| Fee Waiver and Expense Reimbursements |

(0.09)%1 | (0.09)%2 | (0.09)%3 | |||

| Total Annual Fund Operating Expenses After Reimbursements |

1.05% | 1.15% | 1.05% | |||

1 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.70% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs for the Target Fund (the “Target Fund Expense Limit”). The agreement’s current term ends on April 30, 2025, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Target Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Target Fund Expense Limit in place at the time of recoupment.

2 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.80% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Acquiring Fund Expense Limit”). The agreement’s current term ends on April 30, 2026, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Acquiring Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Acquiring Fund Expense Limit in place at the time of recoupment.

3 The investment adviser has contractually agreed to waive management fees or reimburse expenses if Total Annual Fund Operating Expenses of any Class exceed 0.70% of the Class’s average daily net assets, excluding Distribution and Service (12b-1) Fees, Shareholder Services Fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Combined Fund Expense Limit”). The agreement’s current term ends on April 30, 2026, and automatically renews for one-year terms unless it is terminated upon termination of the investment advisory agreement or by Empower Funds or the investment adviser upon written notice within 90 days of the end of the current term. Under the agreement, the investment adviser may recoup, subject to the approval of the Board of Directors of Empower Funds, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided Total Annual Fund Operating Expenses of the Class plus such recoupment do not exceed the lesser of the Combined Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Combined Fund Expense Limit in place at the time of recoupment.

The Example below is intended to help you compare the cost of investing in each Fund and the pro forma cost of investing in the combined fund. The Example does not reflect the fees and expenses of any insurance company separate accounts for Permitted Accounts. If the fees and expenses of any Permitted Account were reflected, the fees and expenses in the Example would be higher because the Permitted Accounts contain fees and expenses that are separate and distinct from the fees and expenses associated with investing in a Fund.

The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of each period. The Example also assumes the Expense Limit is in place for the first year, that your investment has a 5% return each year, that all dividends and capital gains are reinvested, and that the Fund’s operating

4

Table of Contents

expenses are the amount shown in the fee table and remain the same for the years shown. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| Institutional Class | Target Fund |

Acquiring Fund |

Combined Fund Pro Forma | |||||

| 1 Year |

$72 | $82 | $72 | |||||

| 3 Years |

$241 | $258 | $241 | |||||

| 5 Years |

$425 | $449 | $425 | |||||

| 10 Years |

$959 | $1,001 | $959 | |||||

| Investor Class | ||||||||

| 1 Year |

$107 | $117 | $107 | |||||

| 3 Years |

$353 | $385 | $353 | |||||

| 5 Years |

$619 | $672 | $619 | |||||

| 10 Years |

$1,378 | $1,492 | $1,378 |

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate generally indicates higher transaction costs. These costs, which are not reflected in annual fund operating expenses or in the Example above, affect the Funds’ performance. During the most recent fiscal year, the Target Fund’s turnover rate was 20% of the average value of its portfolio. During the most recent fiscal year, the Acquiring Fund’s turnover rate was 217% of the average value of its portfolio.

Principal Investment Strategies

The Target Fund and the Acquiring Fund have substantially similar principal investment strategies with the primary differences being related to the following:

| ● | The Target Fund holds a more limited number of securities in its portfolio; |

| ● | The Target Fund selects issuers that take steps toward preserving the environment and does not invest in corporations whose primary source of revenue is derived from the production or sale of tobacco products, the manufacture of firearms or the operation of for-profit prisons; |

| ● | The Acquiring Fund includes mid cap foreign issuers that are traded in the U.S.; |

| ● | The Acquiring Fund may invest in real estate investment trusts and derivatives; |

| ● | The Acquiring Fund may engage in frequent trading; and |

| ● | The Acquiring Fund uses a quantitative model to select investments. |

The principal investment strategies for each Fund are as follows:

| Target Fund - Principal Investment Strategies | Acquiring Fund - Principal Investment Strategies | |

| The Fund will, under normal circumstances, invest at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in equity securities of mid-capitalization (“mid cap”) companies. For purposes of the 80% policy, the Fund considers mid cap companies to be those whose market capitalization falls within the range of the Russell Midcap® Index at the time of initial purchase. As of December 31, 2023, the market capitalizations of the companies in the Russell Midcap® Index ranged from $270 million to $73.3 billion. If the market capitalization of a company held by the Fund moves outside this range, the Fund may, but is not required to, sell the securities. |

The Fund will, under normal circumstances, invest at least 80% of its net assets (plus the amount of any borrowings for investment purposes) in equity securities of U.S. mid-capitalization (“mid cap”) companies, including foreign issuers that are traded in the U.S. For purposes of the 80% policy, the Fund considers mid cap companies to be those whose market capitalization falls within the range of the Russell Midcap® Value Index at the time of initial purchase. As of December 31, 2023, the market capitalization range of the Russell Midcap® Value Index was between $750 million and $59 billion. If the market capitalization of a company held by the Fund moves outside this range, the Fund may, but is not required to, sell the securities.

|

5

Table of Contents

|

The Fund emphasizes a “value style” of investing, seeking companies that are undervalued in comparison to their peers due to economic, market, company-specific or other factors, but have the prospect of achieving improved valuations in the future. |

The Fund emphasizes a “value style” of investing, seeking companies that are undervalued in comparison to their peers due to economic, market, company-specific or other factors, but have the prospect of achieving improved valuations in the future. | |

| The Fund generally holds between 25-45 securities in its portfolio, focusing on a limited number of companies and industries in which the portfolio managers have expertise, and will often invest a significant portion of its assets in certain sectors, such as the financial sector. |

The Fund may invest in real estate investment trusts (“REITs”) and derivatives, including but not limited to futures contracts. The Fund may engage in active and frequent trading of its portfolio securities. The Fund may also focus its investments in certain sectors, such as the financial sector. | |

| The Fund also currently observes the following operating policies: actively seeking investment in companies that achieve excellence in both financial return and environmental soundness and selecting issuers that take positive steps toward preserving the environment; and not investing in corporations whose primary source of revenue is derived from the production or sale of tobacco products, the manufacture of firearms or the operation of for-profit prisons. |

||

|

Empower Capital Management, LLC (“ECM”) is the Fund’s investment adviser and, subject to the approval of the Board of Directors of Empower Funds (the “Board”), selects the Fund’s sub-adviser and monitors its performance on an ongoing basis. The Fund’s investment portfolio is managed by Ariel Investments, LLC (the “Sub-Adviser” or “Ariel”). Ariel invests primarily in undervalued mid cap companies that show a strong potential for growth. Ariel seeks to invest in quality companies whose financial strength, valuable products or services and savvy management teams create durable competitive advantages. Ariel also integrates environmental, social, and governance (“ESG”) considerations across its investment process as part of the broader review of material risks and opportunities for a given investment. ESG considerations are only one component in the evaluation of eligible investments and may not be a determinative factor in the final investment decision. |

Empower Capital Management, LLC (“ECM”) is the Fund’s investment adviser and, subject to the approval of the Board of Directors of Empower Funds (the “Board”), selects the Fund’s sub-adviser and monitors its performance on an ongoing basis. The Fund’s investment portfolio is managed by Goldman Sachs Asset Management, L.P. (the “Sub-Adviser” or “GSAM”). GSAM manages the Fund using a quantitative investment process, in combination with a qualitative overlay. GSAM’s investment style emphasizes fundamentally based stock selection, careful portfolio construction and efficient implementation. | |

In evaluating the Reorganization, you should consider the risks of investing in the Acquiring Fund. The principal investment risks of investing in the Acquiring Fund are described below in the section entitled “Principal Investment Risks.”

The principal risks of each Fund are substantially similar, but some principal risks differ between the Funds and are described below. There can be no assurance the Target Fund and the Acquiring Fund will achieve their investment objectives. An investment in the Target Fund or the Acquiring Fund is not a deposit with a bank, is not insured,

6

Table of Contents

endorsed or guaranteed by the FDIC or any government agency, and is subject to the possible loss of your original investment.

The following principal risks are identical for both Funds:

Equity Securities Risk - The value of equity securities held by the Fund may decline as a result of factors directly related to a company, a particular industry or industries, or general market conditions that are not specifically related to a company or an industry.

Market Risk - The value of the Fund’s investments may decrease, sometimes rapidly or unexpectedly, due to factors affecting specific issuers held by the Fund, particular industries represented in the Fund’s portfolio, or the overall securities markets. A variety of factors can increase the volatility of the Fund’s holdings and markets generally, including political or regulatory developments, recessions, inflation, rapid interest rate changes, war or acts of terrorism, sanctions, natural disasters, outbreaks of infectious illnesses or other widespread public health issues, or adverse investor sentiment generally. Certain events may cause instability across global markets, including reduced liquidity and disruptions in trading markets, while some events may affect certain geographic regions, countries, sectors, and industries more significantly than others. These adverse developments may cause broad declines in an issuer’s value due to short-term market movements or for significantly longer periods during more prolonged market downturns.

Small and Medium Size Company Risk - The stocks of small and medium size companies often trade in lower volumes, may be less liquid, and are subject to greater or more unpredictable price changes than stocks of larger companies. Such companies may also have limited markets, financial resources or product lines, may lack management depth, and may be more vulnerable to adverse business or market developments. Accordingly, stocks of small and medium size companies tend to be more sensitive to changing economic, market, and industry conditions and tend to be more volatile and less liquid than stocks of larger companies, especially over the short term, and are more likely not to survive or accomplish their goals with the result that the value of their stock could decline significantly. In addition, there may be less publicly available information concerning small and medium size companies upon which to base an investment decision.

Value Stock Risk - A “value” style of investing is subject to the risk that returns on “value” stocks are less than returns on other styles of investing or the overall stock market. Value stocks tend to trade at lower price-to-book and price-to-earnings ratios, which suggests the market as a whole views their potential future earnings as limited.

Sector Risk - The Fund may, from time to time, invest a significant portion of its assets in companies within a particular sector and its performance may suffer if that sector underperforms the overall market.

Management Risk - A strategy, investment decision, technique, analysis, or model used by the portfolio managers may fail to produce the intended results or imperfections, errors or limitations in the tools and data used by the portfolio managers may cause unintended results. Therefore, the Fund could underperform in comparison to other funds with similar objectives and investment strategies and may generate losses even in a favorable market.

The following principal risks are unique to the Target Fund:

Environmental, Social and Governance Considerations Risk - The Target Fund’s portfolio selection strategy is not solely based on ESG considerations, and therefore the issuers in which the Target Fund invests may not be considered ESG-focused companies. Consideration of ESG factors may affect the Target Fund’s exposure to certain issuers or industries and may not work as intended. While ESG considerations may have the potential to contribute to the Target Fund’s long-term performance, there is no guarantee that such results will be achieved.

The following principal risks are unique to the Acquiring Fund:

Real Estate Investment Trust/Real Estate Risk - Investments in real estate-related instruments may be affected by similar risks as direct investment in real estate and the real estate market generally, including, among others: economic, legal, cultural, governmental, environmental or technological factors that affect property values, rents or occupancies of real estate. Historically, the real estate industry has been cyclical and particularly sensitive to economic downturns

7

Table of Contents

and other events that limit demand for real estate, which would adversely impact the value of real estate investments. Real estate companies, including REITs or similar structures, tend to be small and mid cap companies, which means their shares may be more volatile and less liquid. REITs and real estate-related companies may not be diversified due to ownership of a limited number of properties or concentration in a particular geographic region or property type. REITs are also subject to risks associated with changes in interest rates.

Quantitative Model Risk - Securities selected by GSAM using a quantitative investment model can perform differently than the market as a whole based on the factors used in the model, the weight placed on each factor, and changes in the factors’ historical trends. Due to the significant role technology plays in a quantitative investment model, its use carries the risk of potential issues with the design, coding, implementation or maintenance of the computer programs, data and/or technology used in the model. There can be no assurance that the use of a quantitative investment model will enable the Acquiring Fund to achieve its objective.

Foreign Securities Risk - Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, geopolitical (including war or armed conflict), regulatory, market, currency valuation, or economic or other developments and can perform differently than the U.S. market. Current sanctions or the threat of potential sanctions or other similar measures may also impair the value or liquidity of affected securities and negatively impact the Acquiring Fund.

Currency Risk - Adverse fluctuations in exchange rates between the U.S. dollar and other currencies may cause the Acquiring Fund to lose money on investments denominated in foreign currencies.

Derivatives Risk - The use of derivatives, including but not limited to futures contracts, may expose the Acquiring Fund to additional risks that it would not be subject to if it invested directly in the securities underlying those derivatives. These risks include imperfect correlations with underlying investments or the Acquiring Fund’s other portfolio holdings, the risk that a derivative could expose the Acquiring Fund to the risk of magnified losses resulting from leverage, the risk that a counterparty may be unwilling or unable to meet its obligations, high price volatility, liquidity risk, segregation risk, valuation risk and legal restrictions.

Portfolio Turnover Risk - High portfolio turnover rates generally result in higher transaction costs (which are borne directly by the Acquiring Fund and indirectly by shareholders).

Fundamental Investment Restrictions

The Funds have identical fundamental investment restrictions that cannot be changed without shareholder approval. In addition, each Fund is diversified. A diversified fund, with respect to 75% of its assets, may not invest more than 5% of its total assets in the securities of any one issuer (other than securities issued by other investment companies or by the U.S. government, its agencies, instrumentalities or authorities) and may not purchase more than 10% of the outstanding voting securities of any one issuer.

The bar charts and tables below provide an indication of the risk of investment in the Funds by showing the performance of the Funds’ Investor Class shares in each full calendar year since inception and by comparing the Funds’ Institutional and Investor Class average annual total returns to the performance of a broad-based securities market index and an additional index with investment characteristics similar to those of each Fund. The returns shown below for the Funds are historical and are not an indication of future performance. Total return figures assume reinvestment of dividends and capital gains distributions and include the effect of the Funds’ recurring expenses, but do not include fees and expenses of any Permitted Account. If the fees and expenses of any Permitted Account were reflected, the Funds’ performance would have been lower than what is shown below. Upon the completion of the Reorganization, the performance information for the Target Fund will be that of the Acquiring Fund due to an accounting and performance survivor analysis conducted in connection with the Reorganization.

Updated performance information may be obtained at https://www.empower.com/investments/empower-funds/fund-documents (the web site does not form a part of this Prospectus).

8

Table of Contents

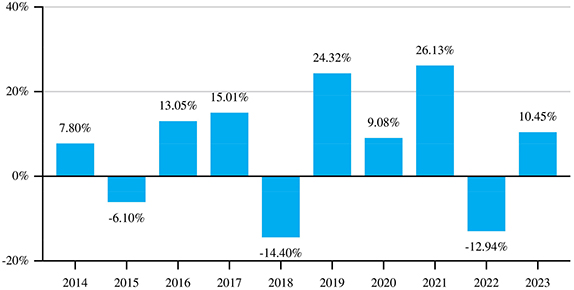

Target Fund Calendar Year Total Returns

| Quarter Ended | Total Return | |||

|

Best Quarter |

December 31, 2020 | 23.72% | ||

|

Worst Quarter |

March 31, 2020 | -29.70% |

Target Fund Average Annual Total Returns for the Periods Ended December 31, 2023

|

One Year |

Five Years |

Ten Years |

Since Inception |

Inception Date | ||||||

| Institutional Class |

10.92% | 10.80% | N/A | 6.29% | 5/1/2015 | |||||

| Investor Class |

10.45% | 10.46% | 6.36% | N/A | ||||||

| Russell 3000® Index¹ (reflects no deduction for fees, expenses or taxes) |

25.96% | 15.16% | 11.48% | 11.53% | ||||||

| Russell Midcap® Value Index (reflects no deduction for fees, expenses or taxes) |

12.71% | 11.16% | 8.26% | 7.71% |

1 The Fund changed its broad-based securities market benchmark from the Russell Midcap® Value Index to the Russell 3000® Index to reflect that the Russell 3000® Index may be considered more broadly representative of the overall applicable securities market. The Fund will retain the Russell Midcap® Value Index as its additional benchmark for performance comparison purposes.

9

Table of Contents

Acquiring Fund Calendar Year Total Returns

| Quarter Ended | Total Return | |||

|

Best Quarter |

December 31, 2020 | 19.60% | ||

|

Worst Quarter |

March 31, 2020 | -33.86% |

Acquiring Fund Average Annual Total Returns for the Periods Ended December 31, 2023

|

One Year |

Five Years |

Ten Years |

Since Inception |

Inception Date | ||||||

| Institutional Class |

15.53% | 10.05% | N/A | 7.77% | 5/1/2015 | |||||

| Investor Class |

15.15% | 9.70% | 8.12% | N/A | ||||||

| Russell 3000® Index¹ (reflects no deduction for fees, expenses or taxes) |

25.96% | 15.16% | 11.48% | 11.53% | ||||||

| Russell Midcap® Value Index (reflects no deduction for fees, expenses or taxes) |

12.71% | 11.16% | 8.26% | 7.71% | ||||||

|

1 The Fund changed its broad-based securities market benchmark from the Russell Midcap® Value Index to the Russell 3000® Index to reflect that the Russell 3000® Index may be considered more broadly representative of the overall applicable securities market. The Fund will retain the Russell Midcap® Value Index as its additional benchmark for performance comparison purposes. | ||||||||||

ECM, a subsidiary of Empower Annuity Insurance Company of America (“Empower of America”), serves as investment adviser to each Fund. ECM provides investment advisory, fund operations, and accounting services to Empower Funds. ECM, a Colorado limited liability company with its principal business address at 8515 East Orchard Road, Greenwood Village, Colorado 80111, is registered as an investment adviser pursuant to the Investment Advisers Act of 1940, as amended (the “Advisers Act”). As of December 31, 2023, ECM provided investment management services for mutual funds and other investment portfolios representing assets of $64.1 billion. ECM and its affiliates have been providing investment management services since 1969.

10

Table of Contents

Each Fund pays a fee to ECM for investment advisory services. For the fiscal year ended December 31, 2023, ECM received an investment advisory fee from the Target Fund at an annual rate of 0.67% of the Target Fund’s average daily net assets which was calculated daily and paid monthly. ECM is entitled to an investment advisory fee from the Acquiring Fund at an annual rate of 0.78% of the Fund’s average daily net assets up to $1 billion dollars, 0.73% of the average daily net assets over $1 billion and 0.68% of the average daily net assets over $2 billion which is calculated daily and paid monthly. For the fiscal year ended December 31, 2023, ECM received an investment advisory fee from the Acquiring Fund at an annual rate of 0.78% of the Fund’s average daily net assets which was calculated daily and paid monthly. Effective October 25, 2024, ECM will receive an investment advisory fee from the Acquiring Fund at an annual rate of 0.67% of the Acquiring Fund’s average daily net assets which is calculated daily and paid monthly.

Pursuant to the terms of the investment advisory agreement between Empower Funds and ECM, ECM is responsible for all fees and expenses incurred in performing the services set forth in the agreement with respect to each Fund. Each Fund pays all other fees and expenses incurred in its operation, all of its general administrative expenses, all shareholder services fees with respect to Investor Class shares, and any extraordinary expenses, including litigation costs. The investment advisory agreement automatically renews for one-year terms unless it is terminated by Empower Funds or ECM upon written notice within 90 days of the end of the current term or upon termination of the investment advisory agreement.

For the Target Fund, ECM has contractually agreed to waive advisory fees or reimburse expenses if total annual Target Fund operating expenses of any Class exceed 0.70% of that Class’s average daily net assets, excluding shareholder services fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Target Fund Expense Limit”). The expense limitation agreement’s current term ends on April 30, 2025, and automatically renews for one-year terms unless it is terminated by Empower Funds or ECM upon written notice within 90 days of the end of the current term or upon termination of the investment advisory agreement. Under the agreement, ECM may recoup, subject to Board approval, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided total annual Fund operating expenses of the Class plus such recoupment do not exceed the lesser of the Target Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Target Fund Expense Limit in place at the time of recoupment.

For the Acquiring Fund, subsequent to the Reorganization, ECM has contractually agreed to waive advisory fees or reimburse expenses if total annual Acquiring Fund operating expenses of any Class exceed 0.70% of that Class’s average daily net assets, excluding shareholder services fees, brokerage expenses, taxes, dividend interest on short sales, interest expenses, and any extraordinary expenses, including litigation costs (the “Acquiring Fund Expense Limit”). The expense limitation agreement’s current term ends on April 30, 2026, and automatically renews for one-year terms unless it is terminated by Empower Funds or ECM upon written notice within 90 days of the end of the current term or upon termination of the investment advisory agreement. Under the agreement, ECM may recoup, subject to Board approval, these waivers and reimbursements in future periods, not exceeding three years following the particular waiver/reimbursement, provided total annual Fund operating expenses of the Class plus such recoupment do not exceed the lesser of the Acquiring Fund Expense Limit that was in place at the time of the waiver/reimbursement or the Acquiring Fund Expense Limit in place at the time of recoupment.

Empower Funds and ECM operate under a manager-of-managers structure under an order issued by the SEC. The current order permits ECM to enter into, terminate, or materially amend sub-advisory agreements without shareholder approval, unless the sub-adviser is an affiliated person. This means ECM is responsible for monitoring the sub-advisers’ performance through quantitative and qualitative analysis and will periodically report to the Board of Directors as to whether each sub-adviser’s agreement should be renewed, terminated or modified. ECM will not enter into a sub-advisory agreement with any sub-adviser that is an affiliated person, as defined in Section 2(a)(3) of the 1940 Act, of Empower Funds or ECM other than by reason of serving as a sub-adviser to one or more funds without such agreement, including the compensation to be paid thereunder, being approved by the shareholders of the applicable Fund (including the Acquiring Fund). Under the terms of such order, however, Empower Funds must furnish to shareholders of the Funds all information about a new sub-adviser or sub-advisory agreement that would be

11

Table of Contents

included in a proxy statement within 90 days after the addition of the new sub-adviser or the implementation of any material change in the sub-advisory agreement.

The Funds enter into contractual arrangements with various parties, including, among others, the Funds’ investment adviser, who provides services to the Funds. Shareholders are not parties to or intended (or “third-party”) beneficiaries of those contractual arrangements.

Subsequent to the Reorganization, GSAM will continue to be responsible for the investment and reinvestment of the assets of the Acquiring Fund and for making decisions to buy, sell, or hold any particular security for the Acquiring Fund. GSAM will bear all expenses in connection with the performance of its services, such as compensating and furnishing office space for its officers and employees connected with investment and economic research, trading and investment management of the Acquiring Fund. ECM, in turn, pays sub-advisory fees to GSAM for its services out of ECM’s advisory fee described above.

The following is additional information regarding the current sub-adviser to the Target Fund and the Acquiring Fund.

Sub-Adviser of the Target Fund

Ariel, a Delaware limited liability company with its principal business address at 200 East Randolph Street, Suite 2900, Chicago, Illinois 60601, is registered as an investment adviser pursuant to the Advisers Act and is a privately held minority-owned money manager.

| ● | John W. Rogers, Jr., Chairman & Co-Chief Executive Officer, has served as portfolio manager of the Target Fund since 2002 and founded Ariel in 1983. |

| ● | Timothy Fidler, CFA, Executive Vice President, has served as portfolio manager of the Target Fund since 2011 and joined Ariel in 1999. |

Sub-Adviser of the Acquiring Fund

GSAM, a Delaware limited partnership with its principal business address at 200 West Street, New York, New York 10282, is registered as an investment adviser pursuant to the Advisers Act. GSAM is an indirect wholly-owned subsidiary of The Goldman Sachs Group, Inc., and an affiliate of Goldman Sachs & Co. LLC.

| ● | Len Ioffe, CFA, Managing Director, has served as portfolio manager of the Acquiring Fund since 2011 and joined GSAM in 1994. |

| ● | Osman Ali, CFA, Managing Director, has served as portfolio manager of the Acquiring Fund since 2013 and joined GSAM in 2003. |

| ● | Dennis Walsh, Managing Director, has served as portfolio manager of the Acquiring Fund since 2013 and joined GSAM in 2005. |

| ● | Takashi Suwabe, Managing Director, has served as portfolio manager of the Acquiring Fund since 2021 and joined GSAM in 2004. |

| ● | Sharanya Srinivasan, Managing Director, has served as portfolio manager of the Acquiring Fund since 2024 and joined GSAM in 2019. |

As of the date of this Information Statement/Prospectus, there are six members of the Board, one of whom is an “interested person” (as that term is defined in the 1940 Act) and five of whom are not “interested persons” of Empower Funds or ECM, as that term is defined in Section 2(a)(19) of the 1940 Act (the “Independent Directors”). The names and business addresses of the directors and officers of the Funds and their principal occupations and other affiliations

12

Table of Contents

during the past five years are set forth under “Management of Empower Funds” in the Funds’ SAI, as supplemented, which is incorporated herein by reference.

Purchase and Sale of Fund Shares

Neither Fund is sold directly to the general public, but instead may be offered as an underlying investment for Permitted Accounts. Permitted Accounts may place orders on any business day to purchase and redeem shares of a Fund based on instructions received from owners of variable contracts or IRAs, or from participants of retirement plans. Please contact your registered representative, IRA custodian or trustee, retirement plan sponsor or administrator for information concerning the procedures for purchasing and redeeming shares of the Funds.

The Funds do not have any initial or subsequent investment minimums. However, Permitted Accounts may impose investment minimums.

For a complete description of purchase, redemption and exchange options, see the section of each Fund’s Prospectus entitled “Shareholder Information.”

Each Fund earns dividends, interest and other income from its investments, and ordinarily distributes this income (less expenses) to shareholders as dividends annually. Each Fund also realizes capital gains from its investments and distributes these gains (less any losses) to shareholders as capital gains distributions at least once annually. Both dividends and capital gains distributions of each Fund are reinvested in additional shares of such Fund at net asset value.

The Target Fund intends to distribute all its net investment income and net capital gains, if any, for the period ending on the Closing Date to its shareholders prior to Closing. See “The Reorganization - Material Federal Income Tax Consequences” below.

Federal Income Tax Information

Each Fund qualifies and intends to continue to qualify as a “regulated investment company” under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). If the Funds qualify as regulated investment companies and distribute their income as required by the Code, the Funds will not be subject to federal income tax to the extent their net investment income and realized net capital gains are distributed to shareholders. Currently, Permitted Accounts generally are not subject to federal income tax on any Fund distributions. Owners of variable contracts, retirement plan participants, owners of qualified college savings programs, and IRA owners are also generally not subject to federal income tax on Fund distributions until such amounts are withdrawn from the variable contract, retirement plan or IRA or are withdrawn from a qualified college savings program for other than qualified expenses. More information regarding federal income taxation of Permitted Account owners and participants may be found in the applicable prospectus and/or disclosure documents for that Permitted Account.

Shareholder Services Agreement

Empower Funds entered into a Shareholder Services Agreement with Empower Retirement, LLC (“Empower”), an affiliate of ECM and a subsidiary of Empower of America. Pursuant to the Shareholder Services Agreement, Empower provides various recordkeeping, administrative and shareholder services (“Shareholder Services”) to shareholders that invest in the Funds through Permitted Accounts. The Shareholder Services provided by Empower include but are not limited to (1) executing purchase and redemption instructions received from shareholders; (2) recording the ownership interest of each shareholder and maintaining a record of the number of shares issued to each shareholder; (3) maintaining a call center and investigating all inquiries from shareholders; (4) distributing annual prospectus updates, supplements to the prospectuses and SAI, and annual and semi-annual shareholder reports to shareholders; (5) preparing and delivering quarterly statements to shareholders; and (6) preparing and delivering confirmations for each purchase, redemption or exchange transaction of a shareholder. The Shareholder Services provided by Empower are not in the capacity of a sub-transfer agent for the Funds. Pursuant to the Shareholder Services Agreement, Empower receives a fee equal to 0.35% of the average daily net asset value of the Investor Class shares of the Funds (“Shareholder Services Fee”). To the extent the Funds are offered on other platforms and other entities provide the

13

Table of Contents

Shareholder Services, Empower or its affiliates enter into a separate agreement with such entity and pay the Shareholder Services Fee to that entity.

Payments to Insurers, Broker-Dealers and Other Financial Intermediaries

Empower of America and/or its affiliates (collectively, the “Empower of America Funds Group” or “EAFG”) may make payments to broker-dealers and other financial intermediaries, including insurance companies, for providing marketing support services, networking, shareholder services, and/or administrative or recordkeeping support services with respect to the Funds. The existence or level of such payments may be based on factors that include, without limitation, differing levels or types of services provided by the broker-dealer or other financial intermediary, the expected level of assets or sales of shares, the placing of a Fund on a recommended or preferred list, and/or access to an intermediary’s personnel and other factors. Such payments are paid from EAFG’s legitimate profits and other financial resources (not from a Fund). To the extent permitted by SEC and Financial Industry Regulatory Authority rules and other applicable laws and regulations, EAFG may pay or allow other promotional incentives or payments to dealers and other financial intermediaries.

The sale of Fund shares, and/or shares of other mutual funds affiliated with Empower Funds, is not considered a factor in the selection of broker-dealers to execute a Fund’s portfolio transactions. Accordingly, the allocation of portfolio transactions for execution by broker-dealers that sell Empower Funds is not considered marketing support payments to such broker-dealers.

EAFG’s payments to financial intermediaries could be significant to the intermediary and may provide the intermediary with an incentive to favor a Fund or affiliated funds. Your financial intermediary may charge you additional fees or commissions other than those disclosed in this Prospectus. Contact your financial intermediary for information about any payments it receives from EAFG and any services it provides, as well as about fees and/or commissions it charges.

Empower may receive payments from registered investment advisers and/or their affiliates (“Partner(s)”), including current and potential sub-advisers to Empower Funds, as applicable, for providing services to Partners and Partner products offered through Empower’s retirement platforms. Program services include but are not limited to: (1) consideration for inclusion in Empower products developed for some segments of the retirement and IRA market, (2) inclusion on the Empower Select investment platform, which is available in the small plan recordkeeping market, (3) a waiver of the connectivity fee, (4) enhanced marketing opportunities, (5) additional reporting capabilities, (6) collaboration in thought leadership opportunities, (7) access to meetings with Empower leadership, Empower staff, and the third-party advisory and brokerage firms through which Empower distributes its services, and (8) access to conferences put on by Empower. The level of payments made by Partners may be based on differing levels or types of services provided by Empower, among other considerations.

Additional information concerning the Funds is contained in this Information Statement/Prospectus and additional information regarding the Acquiring Fund is contained in the Acquiring Fund’s prospectus which is incorporated by reference. The cover page of this Information Statement/Prospectus describes how you may obtain further information.

The Reorganization will be governed by the Agreement, which is attached as Appendix A. The Agreement provides that the Target Fund will transfer all of its assets to the Acquiring Fund solely in exchange for the issuance of full and fractional shares of the Acquiring Fund and the assumption by the Acquiring Fund of all the liabilities of the Target Fund. The Closing of the Reorganization will take place at the close of business on the Closing Date.

The Target Fund will transfer all of its assets to the Acquiring Fund, and in exchange, the Acquiring Fund will assume all the liabilities of the Target Fund and deliver to the Target Fund a number of full and fractional Institutional Class and Investor Class shares of the Acquiring Fund having a net asset value equal to the value of the assets of the Target

14

Table of Contents

Fund less the liabilities of the Target Fund assumed by the Acquiring Fund as of the close of regular trading on the New York Stock Exchange on the Closing Date. At the designated time on the Closing Date, as set forth in the Agreement, the Target Fund will distribute in complete liquidation and termination of the Target Fund, pro rata, by class, to its shareholders of record all Acquiring Fund shares received by the Target Fund. This distribution will be accomplished by the transfer of the Acquiring Fund shares credited to the account of the Target Fund on the books of the Acquiring Fund to open accounts on the share records of the Acquiring Fund in the name of the Target Fund shareholders and representing the respective pro rata number of Acquiring Fund shares of the appropriate class due such shareholders. All issued and outstanding shares of the Target Fund will be canceled on the books of the Target Fund. As a result of the Reorganization, each Target Fund Institutional Class and Investor Class shareholder will receive a number of Acquiring Fund Institutional Class and Investor Class shares respectively, equal in net asset value, as of the close of regular trading on the New York Stock Exchange on the Closing Date, to the net asset value as of such time of the Target Fund Institutional Class and Investor Class shares, surrendered by such shareholder.

The consummation of the Reorganization is subject to the terms and conditions set forth in the Agreement and the representations and warranties set forth in the Agreement being true. The Agreement may be terminated by mutual agreement of the Funds. In addition, either Fund may at its option terminate the Agreement at or before the Closing if (i) the Closing has not occurred on or before ten months from the date of the Agreement, unless such date is extended by mutual agreement of the parties, or (ii) the other party materially breaches its obligations under the Agreement or makes a material and intentional misrepresentation in the Agreement or in connection with the Agreement.

The Target Fund will, within a reasonable period of time before the Closing, furnish the Acquiring Fund with a list of the Target Fund’s portfolio securities and other investments. The Acquiring Fund will, within a reasonable period of time before the Closing, furnish the Target Fund with a list of the securities, if any, on the Target Fund’s list referred to above that the Acquiring Fund does not wish to acquire, and the Target Fund will dispose of the securities on the Acquiring Fund’s list before the Closing. Notwithstanding the foregoing, nothing in the Agreement will require the Target Fund to dispose of any investments or securities if, in the reasonable judgment of the Target Fund, such disposition would adversely affect the tax-free nature of the Reorganization for federal income tax purposes or would otherwise not be in the best interests of the Target Fund. It is estimated that approximately 97% of the Target Fund’s portfolio will be sold prior to the Reorganization in connection with this portfolio repositioning. It is estimated that such portfolio repositioning would have resulted in realized losses of approximately $2,684,072 (approximately $0.03 per share) and brokerage commissions or other transaction costs of approximately $7,939 (approximately $0.003 per share), based on average commission rates normally paid by the Acquiring Fund, if such sales occurred on December 31, 2023.

It is expected that neither shareholders of the Target Fund nor investors who hold shares of the Target Fund through Permitted Accounts will recognize gain or loss for federal income tax purposes as a direct result of the Reorganization. In addition, neither Fund will generally recognize gain nor loss for federal income tax purposes as a direct result of the Reorganization. To the extent that portfolio investments received by the Acquiring Fund in the Reorganization are sold after the Reorganization, the Acquiring Fund may recognize income and capital gain (after the application of any available capital loss carryovers), which will be distributed to shareholders who hold shares of the combined fund (including former Target Fund shareholders who hold shares of the Acquiring Fund following the Reorganization). Such distribution is not expected to be taxable for federal income tax purposes to investors who hold shares of the Acquiring Fund through Permitted Accounts. None of the Target Fund’s investments are expected to be sold after the Reorganization as a result of any portfolio repositioning. For a more detailed discussion of the federal income tax consequences of the Reorganization, please see “The Reorganization - Material Federal Income Tax Consequences” below.

Description of Securities to be Issued

Shares of Common Stock. The Acquiring Fund offers two classes of shares – Institutional Class and Investor Class. Each share of the Acquiring Fund represents an equal proportionate interest in that Fund with each other share and is entitled to such dividends and distributions out of the income belonging to the Acquiring Fund as are declared by the Board. Each share class represents interests in the same portfolio of investments, but differing class-level expenses will result in differing net asset values and dividends and distributions for each class. Upon any liquidation of the Acquiring Fund, Institutional Class and Investor Class shareholders are entitled to share pro rata in the net assets belonging to the Acquiring Fund allocable to the Institutional Class and Investor Class, respectively, available for

15

Table of Contents

distribution after satisfaction of outstanding liabilities of the Acquiring Fund allocable to the Institutional Class and Investor Class. All issued and outstanding shares of the Acquiring Fund are, and on the Closing Date will be, duly and validly issued and outstanding, fully paid and non-assessable, and not subject to preemptive or dissenter’s rights. Additional classes of shares may be authorized by the Board in the future.

Voting Rights of Shareholders. Shares attributable to a Fund held in variable contracts will be voted by insurance company separate accounts based on instructions received from owners of variable contracts. The number of votes that an owner of a variable contract has the right to cast will be determined by applying his/her percentage interest in a Fund (held through a variable contract) to the total number of votes attributable to the Fund. In determining the number of votes, fractional shares will be recognized. Shares held in the variable contracts for which a Fund does not receive instructions, and shares owned by ECM, which provided initial capital to the Fund, will be voted in the same proportion as shares for which the Fund has received instructions. As a result of such proportionate voting a small number of variable contracts owners may determine the outcome of the shareholder vote(s).