EX-99.1

Exhibit 99.1

|

|

|

|

|

|

|

|

|

News Release

|

| CONTACTS: |

|

Jim Eglseder (Investors) |

|

FOR IMMEDIATE RELEASE |

|

|

(513) 534-8424 |

|

July 21, 2011 |

|

|

Rich Rosen, CFA (Investors) |

|

|

|

|

(513) 534-3307 |

|

|

|

|

Debra DeCourcy, APR (Media) |

|

|

|

|

(513) 534-4153 |

|

|

FIFTH THIRD BANCORP ANNOUNCES SECOND QUARTER 2011 NET INCOME TO COMMON SHAREHOLDERS OF $328 MILLION OR

$0.35 PER SHARE

| |

• |

|

2Q11 net income available to common shareholders of $328 million or $0.35 per diluted common share |

| |

• |

|

1Q11 net income to common of $88 million or $0.10 per share ($241 million or $0.27 excluding the effect of accelerated TARP discount accretion)

|

| |

• |

|

2Q10 net income to common of $130 million or $0.16 per share |

| |

• |

|

2Q11 net income of $337 million compared with 1Q11 net income of $265 million and 2Q10 net income of $192 million |

| |

• |

|

2Q11 return on assets of 1.2 percent |

| |

• |

|

2Q11 return on average common equity of 11.0 percent; return on average tangible common equity of 14.0 percent |

| |

• |

|

Pre-provision net revenue (PPNR)* of $619 million |

| |

• |

|

Net interest income of $869 million, down 2 percent sequentially; 3.62 percent net interest margin; period end loans up 1 percent driven by 3 percent

growth in C&I loans |

| |

• |

|

Noninterest income of $656 million, up 12 percent sequentially driven primarily by stronger mortgage-related revenue, card and processing revenue and

corporate banking revenue |

| |

• |

|

Noninterest expense of $901 million, down 2 percent sequentially driven primarily by seasonal decrease in FICA and unemployment costs

|

| |

• |

|

Credit trends remain favorable |

| |

• |

|

2Q11 net charge-offs of $304 million (1.56 percent of loans and leases), the lowest level since the first quarter of 2008, vs. 1Q11 NCOs of $367

million and 2Q10 NCOs of $434 million |

| |

• |

|

Total nonperforming assets of $2.3 billion including held-for-sale declined $78 million or 3 percent sequentially (lowest levels since 2Q08);

nonperforming assets excluding held-for-sale of $2.1 billion declined $38 million or 2 percent |

| |

• |

|

NPA ratio of 2.66 percent down 7 bps from 1Q11, NPL ratio of 2.09 percent down 2 bps from 1Q11; NPL inflows of $449 million down 55 percent from peak

in 3Q09 |

| |

• |

|

Total delinquencies (includes loans and leases 30-89 days past due and over 90 days past due) declined 9 percent sequentially to lowest level since

2006 |

| |

• |

|

Allowance to loan ratio of 3.35 percent, 125 percent of nonperforming assets, 160 percent of nonperforming loans and leases, and 2.1 times annualized

2Q11 net charge-offs |

| |

• |

|

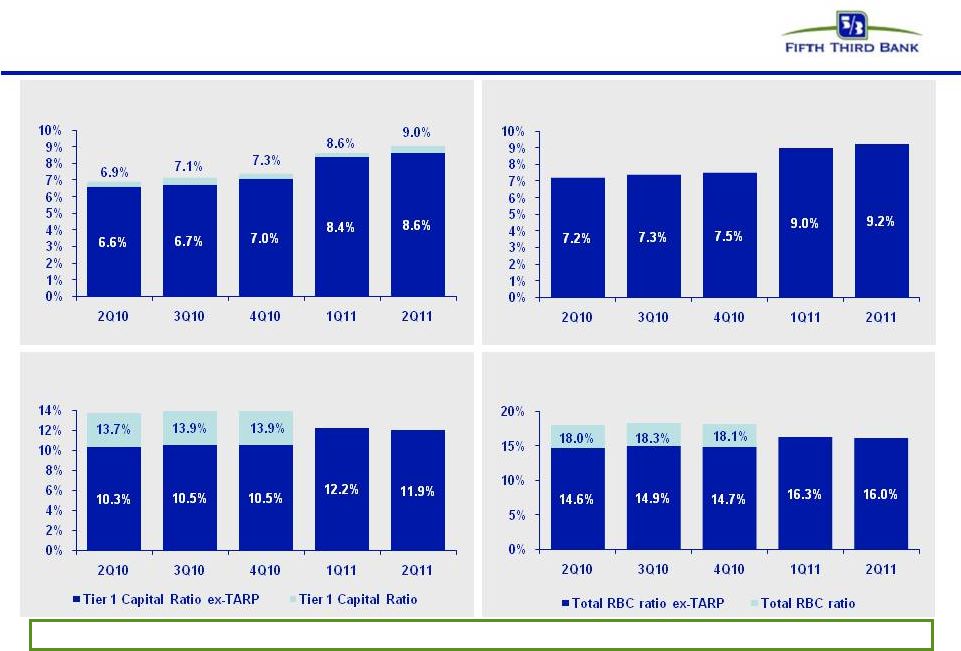

Strong capital ratios; exceed fully phased-in Basel III proposed standards |

| |

• |

|

Tier 1 common ratio 9.20 percent, up 21 bps sequentially (pro forma** ~9.6 percent on a full-phased in Basel III adjusted basis)

|

| |

• |

|

Tier 1 ratio 11.93 percent, Total capital ratio 16.03 percent, Leverage ratio 11.03 percent |

| |

• |

|

Tangible common equity ratio of 8.64 percent excluding unrealized gains/losses, up 25 bps; 8.96 percent including unrealized gains/losses, up 36 bps

|

| |

• |

|

Book value per share of $13.23, tangible book value per share of $10.55 |

| |

• |

|

Tangible book value per share growth 11 percent from 2Q10, 4 percent from 1Q11 |

| * |

Pre-provision net revenue (PPNR): net interest income plus noninterest income minus noninterest expense and taxable equivalent adjustment

|

| ** |

Estimate, subject to final rule-making and clarification by U.S. banking regulators; currently assumes unrealized securities gains are included in common equity for

purposes of this calculation |

Fifth Third Bancorp (Nasdaq: FITB) today reported second quarter 2011 net income of $337 million, compared

with net income of $265 million in the first quarter of 2011 and net income of $192 million in the second quarter of 2010. After preferred dividends, second quarter 2011 net income available to common shareholders was $328 million or $0.35 per

diluted share, compared with first quarter net income of $88 million or $0.10 per diluted share, and net income of $130 million or $0.16 per diluted share in the second quarter of 2010.

First quarter 2011 net income available to common shareholders was reduced by $153 million, or $0.17 per diluted share, of discount accretion recorded in preferred dividends accelerated by the February

repurchase of $3.408 billion of TARP CPP Preferred Stock.

Earnings Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Earnings ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income attributable to Bancorp |

|

$ |

337 |

|

|

$ |

265 |

|

|

$ |

333 |

|

|

$ |

238 |

|

|

$ |

192 |

|

|

|

27 |

% |

|

|

75 |

% |

| Net income available to common shareholders |

|

$ |

328 |

|

|

$ |

88 |

|

|

$ |

270 |

|

|

$ |

175 |

|

|

$ |

130 |

|

|

|

272 |

% |

|

|

153 |

% |

|

|

|

|

|

|

|

|

| Common Share Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings per share, basic |

|

|

0.36 |

|

|

|

0.10 |

|

|

|

0.34 |

|

|

|

0.22 |

|

|

|

0.16 |

|

|

|

260 |

% |

|

|

125 |

% |

| Earnings per share, diluted |

|

|

0.35 |

|

|

|

0.10 |

|

|

|

0.33 |

|

|

|

0.22 |

|

|

|

0.16 |

|

|

|

250 |

% |

|

|

119 |

% |

| Cash dividends per common share |

|

|

0.06 |

|

|

|

0.06 |

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

0.01 |

|

|

|

— |

|

|

|

500 |

% |

|

|

|

|

|

|

|

|

| Financial Ratios |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Return on average assets |

|

|

1.22 |

% |

|

|

0.97 |

% |

|

|

1.18 |

% |

|

|

0.84 |

% |

|

|

0.68 |

% |

|

|

26 |

% |

|

|

79 |

% |

| Return on average common equity |

|

|

11.0 |

|

|

|

3.1 |

|

|

|

10.4 |

|

|

|

6.8 |

|

|

|

5.2 |

|

|

|

255 |

% |

|

|

112 |

% |

| Return on average tangible common equity |

|

|

14.0 |

|

|

|

4.2 |

|

|

|

13.9 |

|

|

|

9.4 |

|

|

|

7.4 |

|

|

|

234 |

% |

|

|

89 |

% |

| Tier I capital |

|

|

11.93 |

|

|

|

12.20 |

|

|

|

13.89 |

|

|

|

13.85 |

|

|

|

13.65 |

|

|

|

(2 |

%) |

|

|

(13 |

%) |

| Tier I common equity |

|

|

9.20 |

|

|

|

8.99 |

|

|

|

7.48 |

|

|

|

7.34 |

|

|

|

7.17 |

|

|

|

2 |

% |

|

|

28 |

% |

| Net interest margin (a) |

|

|

3.62 |

|

|

|

3.71 |

|

|

|

3.75 |

|

|

|

3.70 |

|

|

|

3.57 |

|

|

|

(2 |

%) |

|

|

1 |

% |

| Efficiency (a) |

|

|

59.1 |

|

|

|

62.5 |

|

|

|

62.6 |

|

|

|

56.2 |

|

|

|

62.1 |

|

|

|

(5 |

%) |

|

|

(5 |

%) |

|

|

|

|

|

|

|

|

| Common shares outstanding (in thousands) |

|

|

919,818 |

|

|

|

918,728 |

|

|

|

796,273 |

|

|

|

796,283 |

|

|

|

796,320 |

|

|

|

— |

|

|

|

16 |

% |

| Average common shares outstanding (in thousands): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Basic |

|

|

914,601 |

|

|

|

880,830 |

|

|

|

791,072 |

|

|

|

791,017 |

|

|

|

790,839 |

|

|

|

4 |

% |

|

|

16 |

% |

| Diluted |

|

|

955,478 |

|

|

|

894,841 |

|

|

|

836,225 |

|

|

|

797,492 |

|

|

|

802,255 |

|

|

|

7 |

% |

|

|

19 |

% |

| (a) |

Presented on a fully taxable equivalent basis |

“Fifth Third’s second quarter results were strong and reflected continued improvement in credit trends,” said Kevin T. Kabat, president

and CEO of Fifth Third Bancorp. “Bottom-line results were the best Fifth Third has generated since 2007 and drove strong returns – a 1.2 percent return on assets, a 14 percent return on average tangible common equity, and 4 percent

unannualized sequential growth in tangible book value per share.

Noninterest income increased 12 percent from the first quarter and expenses

were well-controlled, down 2 percent. Mortgage banking revenue improved significantly from the first quarter, and card and processing revenue and corporate banking revenue were both up 10 percent or more. Period-end loan balances were up 1 percent

driven by 3 percent growth in both C&I and residential mortgage loans; average transaction deposits increased 2 percent and core deposits increased 1 percent reflecting continued CD run-off.

2

Net interest income and the net interest margin were both down modestly in the quarter reflecting a flatter

yield curve and heightened loan pricing competition. We expect both measures to improve in the third and fourth quarters.

Credit results

continued to trend favorably. Net charge-offs were $304 million, down 17 percent from last quarter and were the lowest level we’ve experienced since the beginning of 2008. Nonperforming asset levels and delinquencies also declined. We expect

further improvement in credit results in the second half of the year.

Overall, we expect second half 2011 results to produce similarly strong

or stronger returns and build upon the 11 percent growth in tangible book value per share we’ve generated over the past year.”

Income Statement Highlights

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Condensed Statements of Income ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income (taxable equivalent) |

|

$ |

869 |

|

|

$ |

884 |

|

|

$ |

919 |

|

|

$ |

916 |

|

|

$ |

887 |

|

|

|

(2 |

%) |

|

|

(2 |

%) |

| Provision for loan and lease losses |

|

|

113 |

|

|

|

168 |

|

|

|

166 |

|

|

|

457 |

|

|

|

325 |

|

|

|

(33 |

%) |

|

|

(65 |

%) |

| Total noninterest income |

|

|

656 |

|

|

|

584 |

|

|

|

656 |

|

|

|

827 |

|

|

|

620 |

|

|

|

12 |

% |

|

|

6 |

% |

| Total noninterest expense |

|

|

901 |

|

|

|

918 |

|

|

|

987 |

|

|

|

979 |

|

|

|

935 |

|

|

|

(2 |

%) |

|

|

(4 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Income before income taxes (taxable equivalent) |

|

|

511 |

|

|

|

382 |

|

|

|

422 |

|

|

|

307 |

|

|

|

247 |

|

|

|

33 |

% |

|

|

107 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Taxable equivalent adjustment |

|

|

5 |

|

|

|

5 |

|

|

|

5 |

|

|

|

4 |

|

|

|

5 |

|

|

|

— |

|

|

|

— |

|

| Applicable income taxes |

|

|

169 |

|

|

|

112 |

|

|

|

83 |

|

|

|

65 |

|

|

|

50 |

|

|

|

51 |

% |

|

|

238 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income |

|

|

337 |

|

|

|

265 |

|

|

|

334 |

|

|

|

238 |

|

|

|

192 |

|

|

|

27 |

% |

|

|

75 |

% |

| Less: Net income attributable to noncontrolling interest |

|

|

— |

|

|

|

— |

|

|

|

1 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income attributable to Bancorp |

|

|

337 |

|

|

|

265 |

|

|

|

333 |

|

|

|

238 |

|

|

|

192 |

|

|

|

27 |

% |

|

|

75 |

% |

| Dividends on preferred stock |

|

|

9 |

|

|

|

177 |

|

|

|

63 |

|

|

|

63 |

|

|

|

62 |

|

|

|

(95 |

%) |

|

|

(85 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net income available to common shareholders |

|

|

328 |

|

|

|

88 |

|

|

|

270 |

|

|

|

175 |

|

|

|

130 |

|

|

|

272 |

% |

|

|

153 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Earnings per share, diluted |

|

$ |

0.35 |

|

|

$ |

0.10 |

|

|

$ |

0.33 |

|

|

$ |

0.22 |

|

|

$ |

0.16 |

|

|

|

250 |

% |

|

|

119 |

% |

Net Interest Income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Interest Income ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total interest income (taxable equivalent) |

|

$ |

1,050 |

|

|

$ |

1,065 |

|

|

$ |

1,109 |

|

|

$ |

1,130 |

|

|

$ |

1,121 |

|

|

|

(1 |

%) |

|

|

(6 |

%) |

| Total interest expense |

|

|

181 |

|

|

|

181 |

|

|

|

190 |

|

|

|

214 |

|

|

|

234 |

|

|

|

— |

|

|

|

(23 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest income (taxable equivalent) |

|

$ |

869 |

|

|

$ |

884 |

|

|

$ |

919 |

|

|

$ |

916 |

|

|

$ |

887 |

|

|

|

(2 |

%) |

|

|

(2 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Average Yield |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Yield on interest-earning assets |

|

|

4.37 |

% |

|

|

4.47 |

% |

|

|

4.52 |

% |

|

|

4.57 |

% |

|

|

4.51 |

% |

|

|

(2 |

%) |

|

|

(3 |

%) |

| Yield on interest-bearing liabilities |

|

|

1.00 |

% |

|

|

1.02 |

% |

|

|

1.04 |

% |

|

|

1.13 |

% |

|

|

1.23 |

% |

|

|

(2 |

%) |

|

|

(19 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest rate spread (taxable equivalent) |

|

|

3.37 |

% |

|

|

3.45 |

% |

|

|

3.48 |

% |

|

|

3.44 |

% |

|

|

3.28 |

% |

|

|

(2 |

%) |

|

|

3 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net interest margin (taxable equivalent) |

|

|

3.62 |

% |

|

|

3.71 |

% |

|

|

3.75 |

% |

|

|

3.70 |

% |

|

|

3.57 |

% |

|

|

(2 |

%) |

|

|

1 |

% |

|

|

|

|

|

|

|

|

| Average Balances ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Loans and leases, including held for sale |

|

$ |

79,153 |

|

|

$ |

79,379 |

|

|

$ |

79,148 |

|

|

$ |

78,854 |

|

|

$ |

78,807 |

|

|

|

— |

|

|

|

— |

|

| Total securities and other short-term investments |

|

|

17,192 |

|

|

|

17,290 |

|

|

|

18,066 |

|

|

|

19,309 |

|

|

|

20,891 |

|

|

|

(1 |

%) |

|

|

(18 |

%) |

| Total interest-earning assets |

|

|

96,345 |

|

|

|

96,669 |

|

|

|

97,214 |

|

|

|

98,163 |

|

|

|

99,698 |

|

|

|

— |

|

|

|

(3 |

%) |

| Total interest-bearing liabilities |

|

|

72,503 |

|

|

|

72,372 |

|

|

|

72,657 |

|

|

|

75,076 |

|

|

|

76,415 |

|

|

|

— |

|

|

|

(5 |

%) |

| Bancorp shareholders’ equity |

|

|

12,365 |

|

|

|

13,052 |

|

|

|

14,007 |

|

|

|

13,852 |

|

|

|

13,563 |

|

|

|

(5 |

%) |

|

|

(9 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3

Net interest income of $869 million on a taxable equivalent basis decreased $15 million from the first

quarter of 2011. The decline in net interest income was attributable to lower yields on commercial and consumer loans, a flatter yield curve and lower LIBOR rates, partially offset by higher loan balances, lower deposit costs and CDs maturing or

migrating into lower cost deposit categories. A higher day-count increased net interest income by $6 million, offset by higher interest expense resulting from hedge ineffectiveness and the full quarter effect of the issuance of $1 billion in

fixed-rate debt in the first quarter of 2011. The net interest margin was 3.62 percent, a decrease of 9 bps from 3.71 percent in the previous quarter, and was impacted by the previously mentioned items. Of the decrease, 2 bps was attributable to

hedge ineffectiveness, 2 bps to the higher day-count, and 1 bp to the increase in long-term debt.

Compared with the second quarter of 2010,

net interest income decreased $18 million while the net interest margin increased 5 bps. The decrease in net interest income was largely the result of lower loan yields, partially offset by higher average loan balances and run-off in higher-priced

CDs. The net interest margin improvement largely reflected deposit growth and shift in mix from higher cost term deposits to lower cost deposit products.

Securities

Average securities and other short-term investments were $17.2 billion in the

second quarter of 2011, consistent with $17.3 billion in the previous quarter and down from $20.9 billion in the second quarter of 2010. Lower cash balances held at the Fed contributed to the sequential and year-over-year declines.

Loans

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June |

|

|

March |

|

|

December |

|

|

September |

|

|

June |

|

|

|

|

|

|

|

| |

|

2011 |

|

|

2011 |

|

|

2010 |

|

|

2010 |

|

|

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

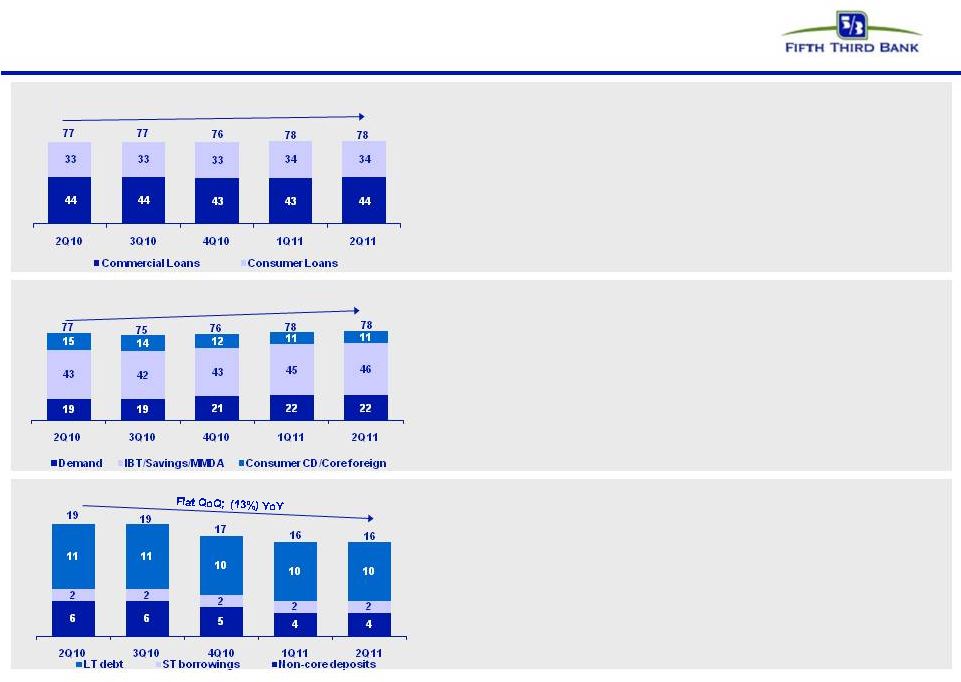

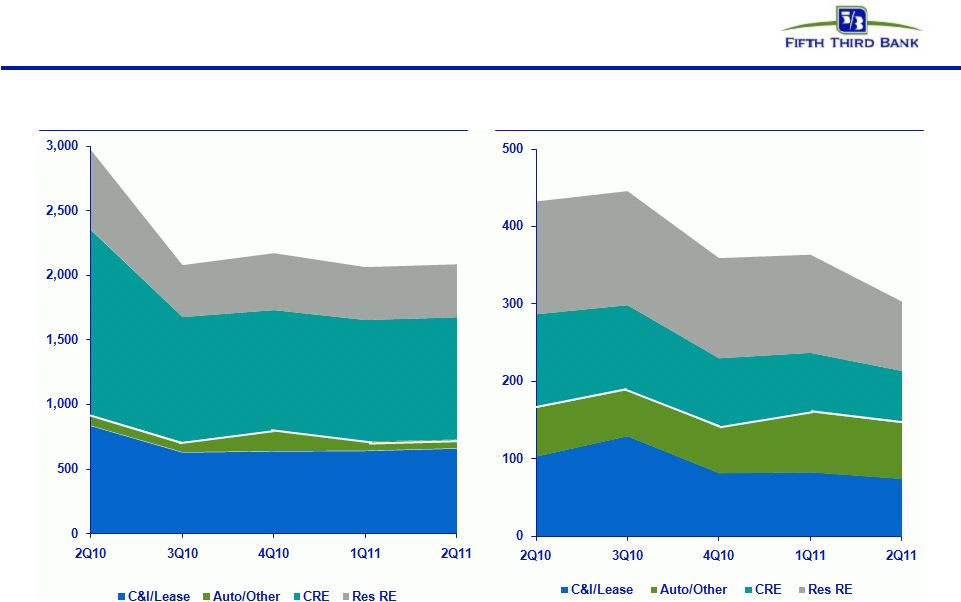

| Average Portfolio Loans and Leases ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Commercial: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Commercial and industrial loans |

|

$ |

27,909 |

|

|

$ |

27,331 |

|

|

$ |

26,338 |

|

|

$ |

26,344 |

|

|

$ |

26,176 |

|

|

|

2 |

% |

|

|

7 |

% |

| Commercial mortgage |

|

$ |

10,394 |

|

|

$ |

10,685 |

|

|

|

10,985 |

|

|

|

11,375 |

|

|

|

11,659 |

|

|

|

(3 |

%) |

|

|

(11 |

%) |

| Commercial construction |

|

$ |

1,918 |

|

|

$ |

2,030 |

|

|

|

2,171 |

|

|

|

2,885 |

|

|

|

3,160 |

|

|

|

(6 |

%) |

|

|

(39 |

%) |

| Commercial leases |

|

$ |

3,349 |

|

|

$ |

3,364 |

|

|

|

3,314 |

|

|

|

3,257 |

|

|

|

3,336 |

|

|

|

— |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subtotal - commercial loans and leases |

|

|

43,570 |

|

|

|

43,410 |

|

|

|

42,808 |

|

|

|

43,861 |

|

|

|

44,331 |

|

|

|

— |

|

|

|

(2 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Consumer: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Residential mortgage loans |

|

|

9,654 |

|

|

|

9,282 |

|

|

|

8,382 |

|

|

|

7,837 |

|

|

|

7,805 |

|

|

|

4 |

% |

|

|

24 |

% |

| Home equity |

|

|

11,144 |

|

|

|

11,376 |

|

|

|

11,655 |

|

|

|

11,897 |

|

|

|

12,102 |

|

|

|

(2 |

%) |

|

|

(8 |

%) |

| Automobile loans |

|

|

11,188 |

|

|

|

11,070 |

|

|

|

10,825 |

|

|

|

10,517 |

|

|

|

10,170 |

|

|

|

1 |

% |

|

|

10 |

% |

| Credit card |

|

|

1,834 |

|

|

|

1,852 |

|

|

|

1,844 |

|

|

|

1,838 |

|

|

|

1,859 |

|

|

|

(1 |

%) |

|

|

(1 |

%) |

| Other consumer loans and leases |

|

|

547 |

|

|

|

646 |

|

|

|

722 |

|

|

|

667 |

|

|

|

706 |

|

|

|

(15 |

%) |

|

|

(23 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subtotal - consumer loans and leases |

|

|

34,367 |

|

|

|

34,226 |

|

|

|

33,428 |

|

|

|

32,756 |

|

|

|

32,642 |

|

|

|

— |

|

|

|

5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total average loans and leases (excluding held for sale) |

|

$ |

77,937 |

|

|

$ |

77,636 |

|

|

$ |

76,236 |

|

|

$ |

76,617 |

|

|

$ |

76,973 |

|

|

|

— |

|

|

|

1 |

% |

|

|

|

|

|

|

|

|

| Average loans held for sale |

|

|

1,216 |

|

|

|

1,743 |

|

|

|

2,912 |

|

|

|

2,237 |

|

|

|

1,834 |

|

|

|

(30 |

%) |

|

|

(34 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

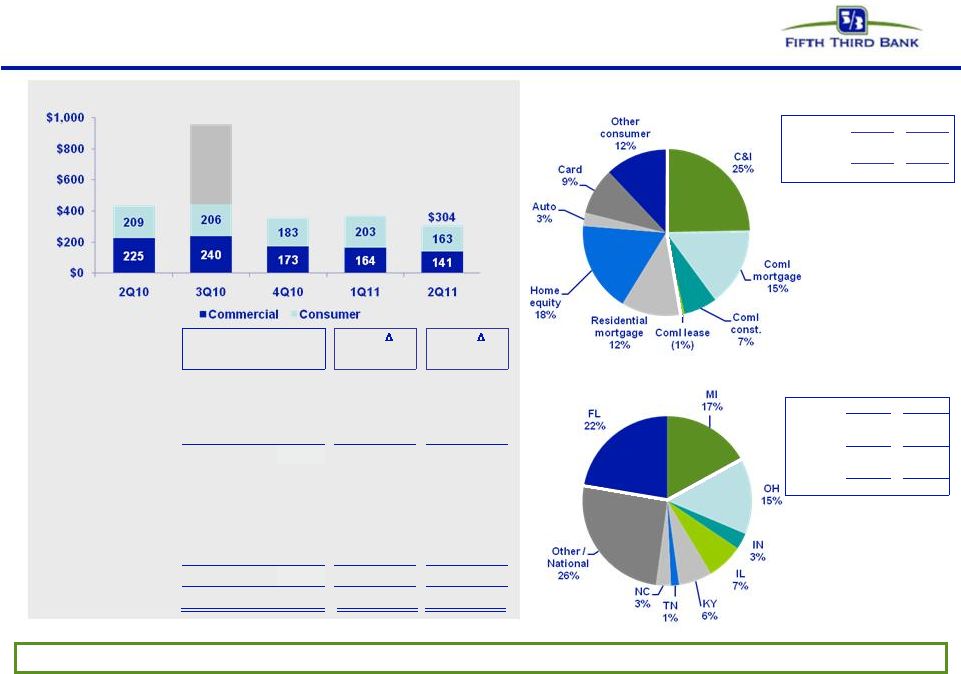

Average loan and lease balances (excluding loans held-for-sale) were up $301 million sequentially and increased $964

million, or 1 percent from the second quarter of 2010. Period end loan and lease balances grew $502 million, or 1 percent from the first quarter and $1.7 billion or 2 percent from a year ago.

4

Average commercial portfolio loan and lease balances were up $160 million sequentially and declined $761

million or 2 percent from the second quarter of 2010. Commercial and industrial (C&I) average loans increased 2 percent sequentially and 7 percent compared with the second quarter of 2010. Average commercial mortgage and commercial construction

loan balances declined by a combined 3 percent sequentially and 17 percent from the same period the previous year, reflecting continued low customer demand and tighter underwriting standards. The year-over-year comparison was also affected by the

transfer of $961 million of loans to loans held-for-sale at the end of the third quarter 2010. Commercial line usage, on an end of period basis for the second quarter, was consistent at 32.9 percent of committed lines versus 33.3 percent in the

first quarter of 2011 and 32.1 percent in the second quarter of 2010.

Average consumer portfolio loan and lease balances were up $141 million

sequentially and increased $1.7 billion, or 5 percent from the second quarter of 2010. Average residential mortgage loans increased 4 percent sequentially and 24 percent compared with the second quarter of 2010. Sequential and year-over-year growth

reflected the continued retention of certain shorter-term fixed-rate residential mortgages, branch originated, which totaled $283 million in the second quarter. Average auto loans increased 1 percent sequentially and 10 percent year-over-year as

continued strong loan origination volumes more than offset pay-downs. This growth was partially offset by lower home equity loan balances, which declined 2 percent sequentially and 8 percent year-over-year due to lower demand and production.

Average loans held-for-sale of $1.2 billion declined $527 million from first quarter levels and $618 million compared with the second quarter

of 2010 driven primarily by lower balances of mortgage loans in the held-for-sale warehouse due to deliveries in excess of origination volumes.

Deposits

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June |

|

|

March |

|

|

December |

|

|

September |

|

|

June |

|

|

|

|

|

|

|

| |

|

2011 |

|

|

2011 |

|

|

2010 |

|

|

2010 |

|

|

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Average Deposits ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Demand deposits |

|

$ |

22,174 |

|

|

$ |

21,582 |

|

|

$ |

21,066 |

|

|

$ |

19,362 |

|

|

$ |

19,406 |

|

|

|

3 |

% |

|

|

14 |

% |

| Interest checking |

|

|

18,701 |

|

|

|

18,539 |

|

|

|

17,578 |

|

|

|

17,142 |

|

|

|

18,652 |

|

|

|

1 |

% |

|

|

— |

|

| Savings |

|

|

21,817 |

|

|

|

21,324 |

|

|

|

20,602 |

|

|

|

19,905 |

|

|

|

19,446 |

|

|

|

2 |

% |

|

|

12 |

% |

| Money market |

|

|

5,009 |

|

|

|

5,136 |

|

|

|

4,985 |

|

|

|

4,940 |

|

|

|

4,679 |

|

|

|

(2 |

%) |

|

|

7 |

% |

| Foreign office (a) |

|

|

3,805 |

|

|

|

3,580 |

|

|

|

3,733 |

|

|

|

3,592 |

|

|

|

3,325 |

|

|

|

6 |

% |

|

|

14 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subtotal - Transaction deposits |

|

|

71,506 |

|

|

|

70,161 |

|

|

|

67,964 |

|

|

|

64,941 |

|

|

|

65,508 |

|

|

|

2 |

% |

|

|

9 |

% |

| Other time |

|

|

6,738 |

|

|

|

7,363 |

|

|

|

8,490 |

|

|

|

10,261 |

|

|

|

11,336 |

|

|

|

(8 |

%) |

|

|

(41 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Subtotal - Core deposits |

|

|

78,244 |

|

|

|

77,524 |

|

|

|

76,454 |

|

|

|

75,202 |

|

|

|

76,844 |

|

|

|

1 |

% |

|

|

2 |

% |

| Certificates - $100,000 and over |

|

|

3,955 |

|

|

|

4,226 |

|

|

|

4,858 |

|

|

|

6,096 |

|

|

|

6,354 |

|

|

|

(6 |

%) |

|

|

(38 |

%) |

| Other |

|

|

2 |

|

|

|

1 |

|

|

|

9 |

|

|

|

4 |

|

|

|

5 |

|

|

|

77 |

% |

|

|

(54 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total deposits |

|

$ |

82,201 |

|

|

$ |

81,751 |

|

|

$ |

81,321 |

|

|

$ |

81,302 |

|

|

$ |

83,203 |

|

|

|

1 |

% |

|

|

(1 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| (a) |

Includes commercial customer Eurodollar sweep balances for which the Bancorp pays rates comparable to other commercial deposit accounts. |

Average core deposits increased 1 percent sequentially and 2 percent from the second quarter of 2010, as transaction deposit growth was partially offset

by continued runoff of consumer time deposits (CDs). Average transaction deposits, excluding consumer time deposits, increased 2 percent from the first quarter of 2011 and 9 percent year-over-year. Sequential and year-over-year growth was primarily

driven by higher demand deposit account (DDA) and savings balances.

5

Retail average transaction deposits increased 4 percent sequentially and 13 percent from the second quarter

of 2010 and reflected growth across all transaction deposit account categories for each comparison period, particularly DDA and savings. Consumer CDs included in core deposits declined 9 percent sequentially and 41 percent year-over-year, driven by

maturities of higher-rate CDs and customer reluctance to purchase longer CD maturities given the current low rate environment.

Commercial

average transaction deposits decreased 2 percent sequentially and increased 1 percent from the previous year. The sequential decline reflects seasonally higher balances in the first quarter. Growth in DDAs was offset by lower interest checking,

money market and foreign office accounts. On a year-over-year basis, strong DDA growth more than offset lower public funds balances. Average public funds balances were $5.7 billion, flat sequentially and down $663 million from the second quarter of

2010 due to ongoing pricing adjustments which continue to reflect our excess liquidity position.

Noninterest Income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Noninterest Income ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Service charges on deposits |

|

$ |

126 |

|

|

$ |

124 |

|

|

$ |

140 |

|

|

$ |

143 |

|

|

$ |

149 |

|

|

|

1 |

% |

|

|

(16 |

%) |

| Corporate banking revenue |

|

|

95 |

|

|

|

86 |

|

|

|

103 |

|

|

|

86 |

|

|

|

93 |

|

|

|

11 |

% |

|

|

2 |

% |

| Mortgage banking net revenue |

|

|

162 |

|

|

|

102 |

|

|

|

149 |

|

|

|

232 |

|

|

|

114 |

|

|

|

58 |

% |

|

|

42 |

% |

| Investment advisory revenue |

|

|

95 |

|

|

|

98 |

|

|

|

93 |

|

|

|

90 |

|

|

|

87 |

|

|

|

(3 |

%) |

|

|

10 |

% |

| Card and processing revenue |

|

|

89 |

|

|

|

80 |

|

|

|

81 |

|

|

|

77 |

|

|

|

84 |

|

|

|

10 |

% |

|

|

5 |

% |

| Other noninterest income |

|

|

83 |

|

|

|

81 |

|

|

|

55 |

|

|

|

195 |

|

|

|

85 |

|

|

|

3 |

% |

|

|

(2 |

%) |

| Securities gains, net |

|

|

6 |

|

|

|

8 |

|

|

|

21 |

|

|

|

4 |

|

|

|

8 |

|

|

|

(25 |

%) |

|

|

(25 |

%) |

| Securities gains, net - non-qualifying hedges |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| on mortgage servicing rights |

|

|

— |

|

|

|

5 |

|

|

|

14 |

|

|

|

— |

|

|

|

— |

|

|

|

NM |

|

|

|

NM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total noninterest income |

|

$ |

656 |

|

|

$ |

584 |

|

|

$ |

656 |

|

|

$ |

827 |

|

|

$ |

620 |

|

|

|

12 |

% |

|

|

6 |

% |

|

|

|

|

|

|

|

|

| NM: Not Meaningful |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest income of $656 million increased $72 million or 12 percent sequentially and $36 million or 6 percent compared

with results a year ago. The sequential growth was driven by higher mortgage-related revenue, corporate banking revenue and card and processing revenue. The year-over-year growth reflected higher mortgage-related revenue partially offset by lower

deposit service charges due to the effect of the August 2010 implementation of Regulation E.

Second quarter 2011 results included a $29

million positive valuation adjustment on warrants and puts related to the 2009 sale of an interest in our processing business, compared with $2 million in negative valuation adjustments on these instruments in the first quarter of 2011 and a $10

million positive valuation adjustment in the second quarter of 2010. Second quarter 2011 results included a $4 million reduction in income due to the increase in fair value of the liability related to the total return swap entered into as part of

the 2009 sale of Visa, Inc. Class B shares. This item reduced noninterest income in the first quarter of 2011 by $9 million. Excluding these items, as well as investment securities gains in all periods, noninterest income increased $38 million, or 6

percent, from the previous quarter driven by higher mortgage-related revenue, corporate banking

6

revenue and card and processing revenue. On a year-over-year basis, noninterest income excluding the items mentioned above increased $23 million, or 4 percent, due to higher mortgage-related

revenue partially offset by lower deposit service charges.

Service charges on deposits of $126 million increased 1 percent sequentially from

a seasonally light first quarter and decreased 16 percent compared with the same quarter last year, due to lower retail service charges. Retail service charges were flat compared with the previous quarter and declined 34 percent compared with the

second quarter of 2010, largely due to the implementation of new overdraft regulations and overdraft policies. Commercial service charges increased 2 percent sequentially and 3 percent compared with the same quarter last year.

Corporate banking revenue of $95 million increased 11 percent from the first quarter of 2011 and increased 2 percent from the same period last year.

Sequential results were driven by higher lease remarketing fees, syndication fee revenue and institutional sales revenue. On a year-over-year basis, higher revenue from business lending fees primarily drove the increase.

Mortgage banking net revenue was $162 million in the second quarter of 2011, a 58 percent increase from the first quarter of 2011 and a 42 percent

increase from the second quarter of 2010. Second quarter 2011 originations were $3.1 billion, a decrease from $3.9 billion in the previous quarter and $3.8 billion in the second quarter of 2010. Second quarter 2011 originations resulted in gains of

$64 million on mortgages sold compared with gains of $62 million during the previous quarter and $89 million during the second quarter of 2010. Gain on sale margins increased sequentially from weak first quarter levels as interest rates were

generally lower this quarter. Mortgage servicing fees this quarter were $58 million, compared with $58 million in the first quarter of 2011 and $54 million in the second quarter of 2010. Mortgage banking revenue is also affected by net servicing

asset value adjustments, which include mortgage servicing rights (MSR) amortization and MSR valuation adjustments (including mark-to-market adjustments on free-standing derivatives used to economically hedge the MSR portfolio). These net servicing

asset valuation adjustments were positive $40 million in the second quarter of 2011 (reflecting MSR amortization of $25 million and MSR valuation adjustments of positive $65 million); negative $18 million in the first quarter of 2011 (MSR

amortization of $28 million and MSR valuation adjustments of positive $10 million); and negative $29 million in the second quarter of 2010 (MSR amortization of $25 million and negative $4 million in MSR valuation adjustments). The mortgage-servicing

asset, net of the valuation reserve, was $847 million at quarter end on a servicing portfolio of $56 billion.

Investment advisory revenue of

$95 million decreased 3 percent sequentially and increased 10 percent from the second quarter of 2010. The sequential decline was primarily driven by seasonally high tax-related private client services fees in the first quarter and a less active

securities trading environment in the second quarter. Year-over-year improvement reflected an overall increase in equity and bond market values.

7

Card and processing revenue was $89 million in the second quarter of 2011, an increase of 10 percent

sequentially and 5 percent from the second quarter of 2010. The sequential increase reflected higher transaction volumes compared with the seasonally weak first quarter, while the year-over-year comparison reflected higher transaction volumes as

general improvement in the economy drove increased spending.

Other noninterest income totaled $83 million in the second quarter of 2011

compared with $81 million in the previous quarter and $85 million in the second quarter of 2010. Other noninterest income included revenue associated with the transition service agreement (TSA) entered into as part of our processing business sale,

revenue from our equity interest in the processing business, effects of the valuation of warrants and puts related to the processing business sale, and changes in income related to the valuation of the total return swap entered into as part of the

2009 sale of Visa, Inc. Class B shares. For periods ending June 30, 2011, March 31, 2011, and June 30, 2010, TSA revenue was $5 million, $11 million, and $13 million, respectively; revenue from our processing business equity

interest was $6 million, $9 million, and $6 million, respectively; warrant/put valuation adjustments were positive $29 million, negative $2 million, and positive $10 million, respectively; and reductions in income related to the Visa, Inc. total

return swap were $4 million this quarter and $9 million in the first quarter. Excluding these items, other noninterest income decreased $25 million from the previous quarter and $9 million from the first quarter of 2010, primarily due to the effects

of higher net credit-related costs recognized in other noninterest income.

Net credit-related costs recognized in other noninterest income

were $28 million in the second quarter of 2011 versus $3 million last quarter and $15 million in the second quarter of 2010. Second quarter 2011 results included $8 million of net gains on sales of commercial loans held-for-sale and $9 million of

fair value charges on commercial loans held-for-sale, as well as $26 million of losses on other real estate owned (OREO). First quarter 2011 results included $17 million of net gains on sales of commercial loans held-for-sale and $16 million of fair

value charges on commercial loans held-for-sale, as well as $2 million of losses on OREO. Second quarter 2010 results included net gains of $6 million on the sale of loans held-for-sale, $7 million of fair value charges on commercial loans

held-for-sale, and $13 million of losses on OREO.

Net gains on investment securities were $6 million in the second quarter of 2011, compared

with investment securities gains of $8 million in the previous quarter and $8 million in the second quarter of 2010.

There were no gains on

securities held as non-qualifying hedges for the MSR, compared with $5 million in the first quarter of 2011 and none in the second quarter of 2010.

8

Noninterest Expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

|

% Change |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

|

Seq |

|

|

Yr/Yr |

|

| Noninterest Expense ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Salaries, wages and incentives |

|

$ |

365 |

|

|

$ |

351 |

|

|

$ |

385 |

|

|

$ |

360 |

|

|

$ |

356 |

|

|

|

4 |

% |

|

|

2 |

% |

| Employee benefits |

|

|

79 |

|

|

|

97 |

|

|

|

73 |

|

|

|

82 |

|

|

|

73 |

|

|

|

(19 |

%) |

|

|

9 |

% |

| Net occupancy expense |

|

|

75 |

|

|

|

77 |

|

|

|

76 |

|

|

|

72 |

|

|

|

73 |

|

|

|

(3 |

%) |

|

|

2 |

% |

| Technology and communications |

|

|

48 |

|

|

|

45 |

|

|

|

52 |

|

|

|

48 |

|

|

|

45 |

|

|

|

6 |

% |

|

|

6 |

% |

| Equipment expense |

|

|

28 |

|

|

|

29 |

|

|

|

32 |

|

|

|

30 |

|

|

|

31 |

|

|

|

(4 |

%) |

|

|

(9 |

%) |

| Card and processing expense |

|

|

29 |

|

|

|

29 |

|

|

|

26 |

|

|

|

26 |

|

|

|

31 |

|

|

|

1 |

% |

|

|

(8 |

%) |

| Other noninterest expense |

|

|

277 |

|

|

|

290 |

|

|

|

343 |

|

|

|

361 |

|

|

|

326 |

|

|

|

(4 |

%) |

|

|

(15 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total noninterest expense |

|

$ |

901 |

|

|

$ |

918 |

|

|

$ |

987 |

|

|

$ |

979 |

|

|

$ |

935 |

|

|

|

(2 |

%) |

|

|

(4 |

%) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

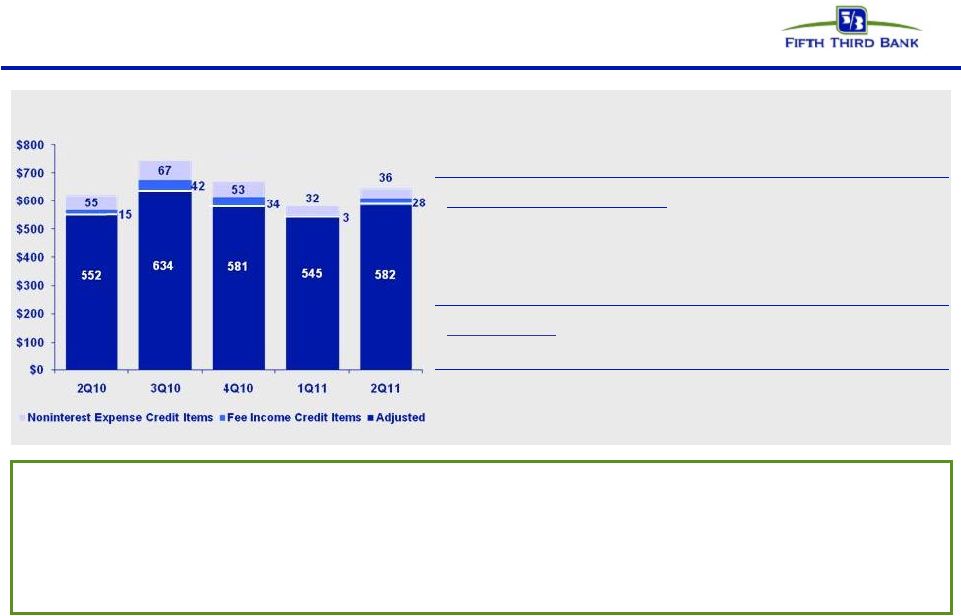

Noninterest expense of $901 million decreased 2 percent from the first quarter of 2011 and decreased 4 percent from the

second quarter of 2010. Excluding $6 million of debt extinguishment gains in the second quarter and $3 million in the first quarter recorded as a reduction to other noninterest expense, noninterest expense declined $14 million sequentially and $28

million compared with the second quarter of 2010. The remaining sequential decline was primarily driven by lower employee benefits expense due to a decrease in FICA and unemployment costs from seasonally high first quarter levels as well as

improvements in other noninterest expense, partially offset by higher salaries, wages, and incentives. The remaining year-over-year decline was due to significantly lower credit-related expenses. Each period included operating expenses related to

the processing business that were largely offset by revenue under the TSA reported in other noninterest income.

Credit costs related to

problem assets recorded as noninterest expense totaled $36 million in the second quarter of 2011, compared with $32 million in the first quarter of 2011 and $55 million in the second quarter of 2010. Second quarter credit-related expenses included

provision expense for mortgage repurchases of $14 million, compared with $8 million in the first quarter and $18 million a year ago. (Realized mortgage repurchase losses were $22 million in the second quarter of 2011, compared with $24 million last

quarter and $19 million in the second quarter of 2010.) Provision for unfunded commitments was a benefit of $14 million in the current quarter, compared with a benefit of $16 million last quarter and a benefit of $6 million a year ago. Derivative

valuation adjustments related to customer credit risk were $1 million in expense this quarter versus a net of zero last quarter and $9 million in expense a year ago. OREO expense was $6 million this quarter, compared with $13 million last quarter

and $7 million a year ago. Other problem asset-related expenses were $30 million in the second quarter, compared with $28 million the previous quarter and $26 million in the same period last year.

9

Credit Quality

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

| Total net losses charged off ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Commercial and industrial loans |

|

($ |

76 |

) |

|

($ |

83 |

) |

|

($ |

85 |

) |

|

($ |

237 |

) |

|

($ |

104 |

) |

| Commercial mortgage loans |

|

|

(47 |

) |

|

|

(54 |

) |

|

|

(80 |

) |

|

|

(268 |

) |

|

|

(78 |

) |

| Commercial construction loans |

|

|

(20 |

) |

|

|

(26 |

) |

|

|

(11 |

) |

|

|

(121 |

) |

|

|

(43 |

) |

| Commercial leases |

|

|

2 |

|

|

|

(1 |

) |

|

|

3 |

|

|

|

(1 |

) |

|

|

— |

|

| Residential mortgage loans |

|

|

(36 |

) |

|

|

(65 |

) |

|

|

(62 |

) |

|

|

(204 |

) |

|

|

(85 |

) |

| Home equity |

|

|

(54 |

) |

|

|

(63 |

) |

|

|

(65 |

) |

|

|

(66 |

) |

|

|

(61 |

) |

| Automobile loans |

|

|

(8 |

) |

|

|

(20 |

) |

|

|

(19 |

) |

|

|

(17 |

) |

|

|

(20 |

) |

| Credit card |

|

|

(28 |

) |

|

|

(31 |

) |

|

|

(33 |

) |

|

|

(36 |

) |

|

|

(42 |

) |

| Other consumer loans and leases |

|

|

(37 |

) |

|

|

(24 |

) |

|

|

(4 |

) |

|

|

(6 |

) |

|

|

(1 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total net losses charged off |

|

|

(304 |

) |

|

|

(367 |

) |

|

|

(356 |

) |

|

|

(956 |

) |

|

|

(434 |

) |

|

|

|

|

|

|

| Total losses |

|

|

(343 |

) |

|

|

(397 |

) |

|

|

(399 |

) |

|

|

(992 |

) |

|

|

(472 |

) |

| Total recoveries |

|

|

39 |

|

|

|

30 |

|

|

|

43 |

|

|

|

36 |

|

|

|

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total net losses charged off |

|

($ |

304 |

) |

|

($ |

367 |

) |

|

($ |

356 |

) |

|

($ |

956 |

) |

|

($ |

434 |

) |

| Ratios (annualized) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net losses charged off as a percent of average loans and leases (excluding held for sale) |

|

|

1.56 |

% |

|

|

1.92 |

% |

|

|

1.86 |

% |

|

|

4.95 |

% |

|

|

2.26 |

% |

| Commercial |

|

|

1.30 |

% |

|

|

1.52 |

% |

|

|

1.59 |

% |

|

|

5.66 |

% |

|

|

2.03 |

% |

| Consumer |

|

|

1.89 |

% |

|

|

2.43 |

% |

|

|

2.20 |

% |

|

|

4.00 |

% |

|

|

2.57 |

% |

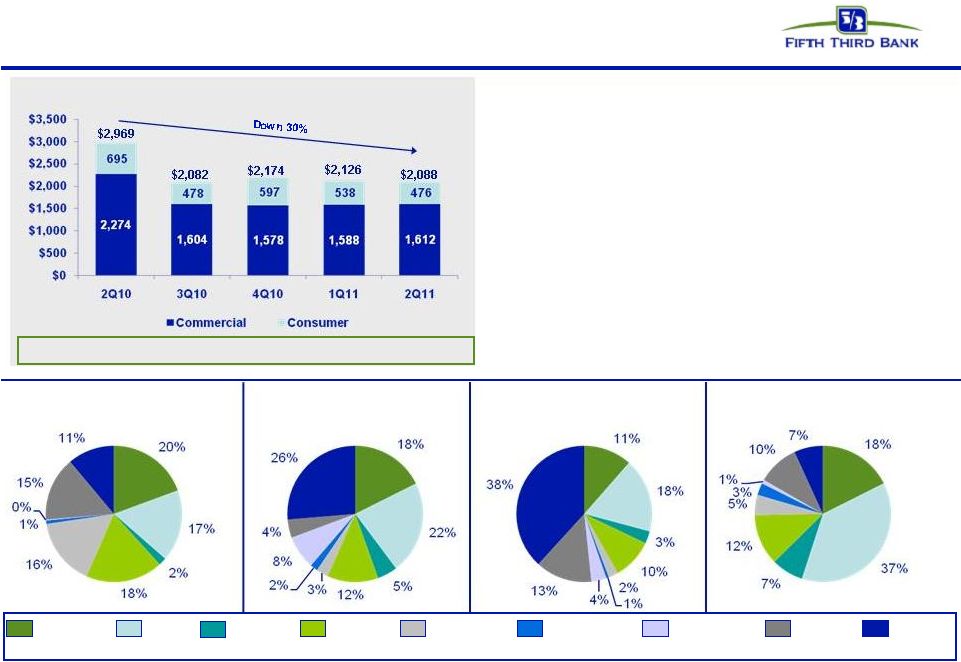

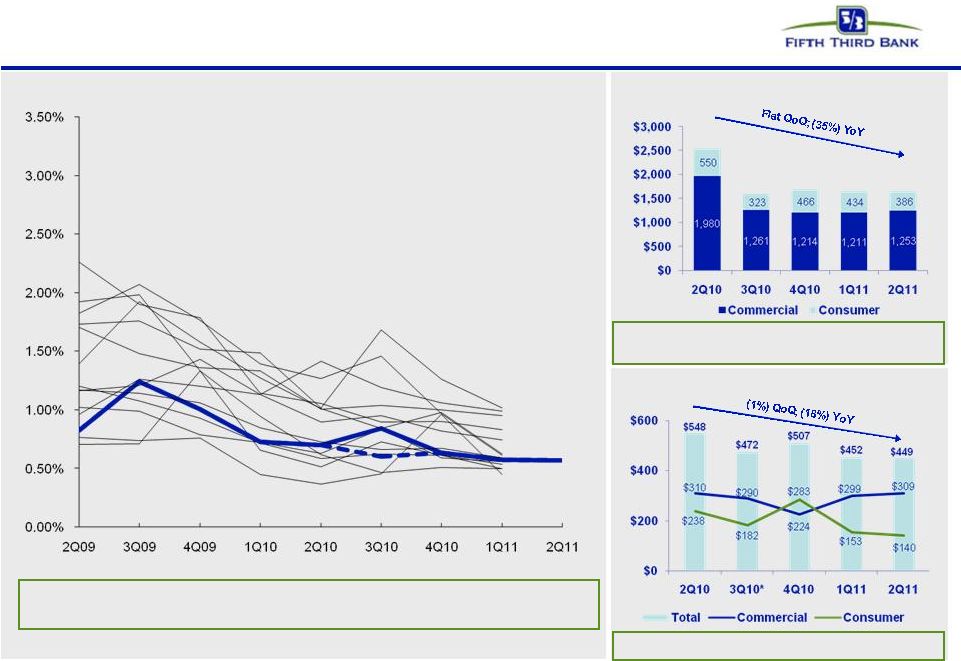

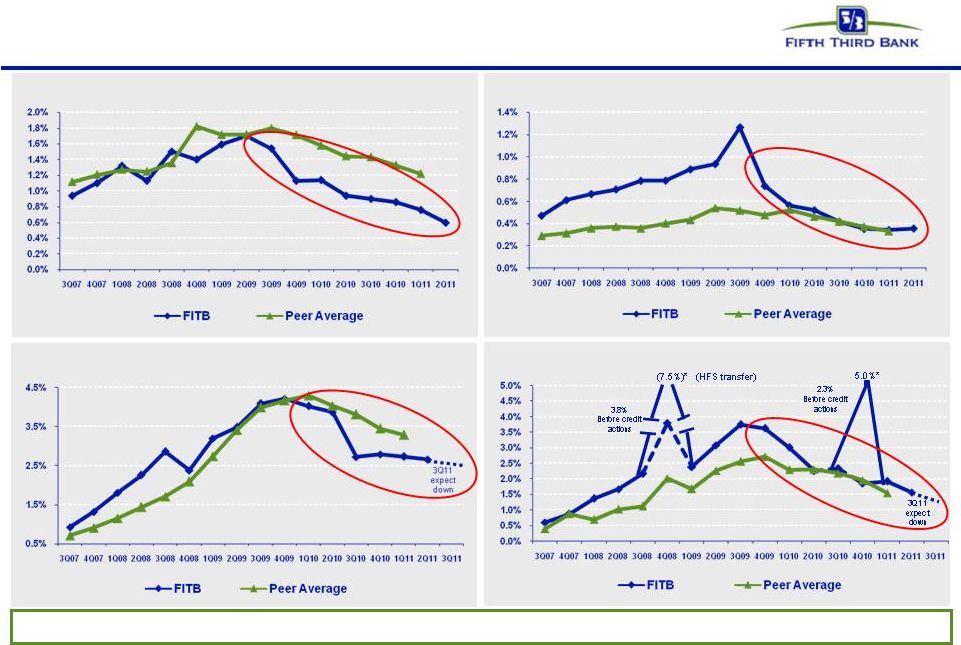

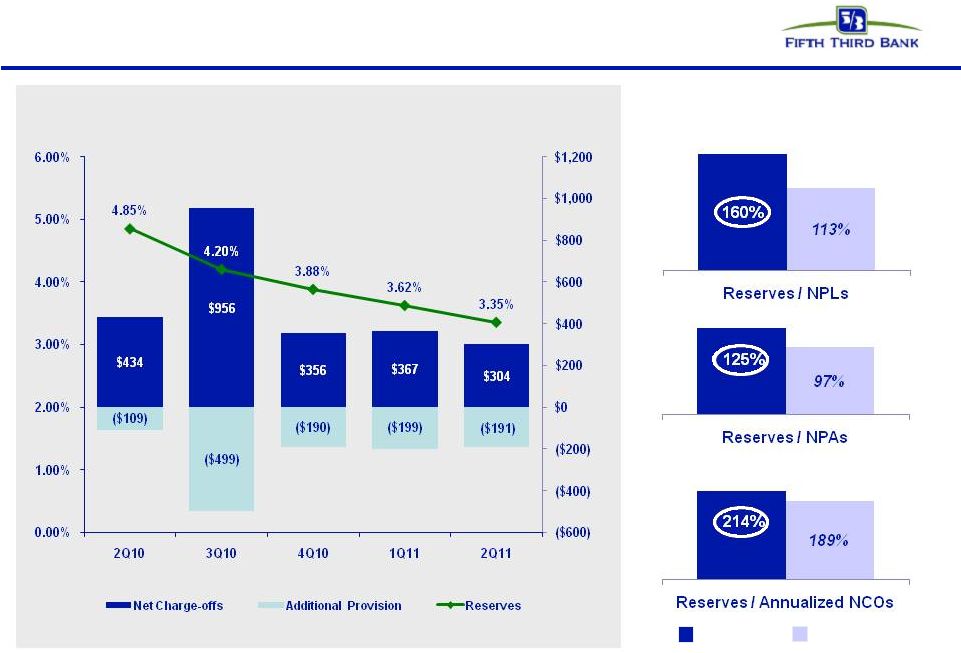

Net charge-offs were $304 million in the second quarter of 2011, or 156 bps of average loans on an annualized basis.

First quarter 2011 net charge-offs were $367 million, or 192 bps of average loans on an annualized basis. Second quarter 2010 net charge-offs were $434 million, or 226 bps of average loans on an annualized basis.

Commercial net charge-offs were $141 million, or 130 bps, down $23 million versus $164 million, or 152 bps, in the first quarter. Improvement in

charge-offs was broad-based. C&I net losses were $76 million, compared with net losses of $83 million in the previous quarter. Commercial mortgage net losses totaled $47 million compared with net losses of $54 million in the first quarter.

Commercial construction net losses were $20 million, compared with net losses of $26 million in the prior quarter. Net losses on residential builder and developer portfolio loans across the C&I and commercial real estate categories totaled $14

million. Originations of homebuilder / developer loans were suspended in 2007 and the remaining portfolio balance is $597 million, down from a peak of $3.3 billion in the second quarter of 2008.

Consumer net charge-offs were $163 million, or 189 bps, down $40 million versus $203 million, or 243 bps, in the first quarter. Improvements were driven

by trends in the residential mortgage and automobile portfolios, partially offset by the effect of charge-offs on loans from a credit relationship in the other consumer loans and leases portfolio described below. Net charge-offs on residential

mortgage loans in the portfolio were $36 million, down from $65 million in the previous quarter, with lower losses in Florida driving $16 million of improvement. Home equity net charge-offs were $54 million, compared with portfolio losses of $63

million in the first quarter. Net losses on brokered home equity loans represented 36 percent of second quarter home equity losses; such loans are 14 percent of the total home equity portfolio. The home equity portfolio included $1.6 billion of

brokered loans, down from a peak of $2.6 billion in 2007; originations of these loans were discontinued in 2007. Net charge-offs in the auto portfolio of $8 million declined $12 million from the prior

10

quarter. Net losses on consumer credit card loans were $28 million, down $3 million from the previous quarter. Net charge-offs in other consumer loans were $37 million, up $13 million from the

previous quarter, primarily the result of a commercial loan that was foreclosed upon in the fourth quarter 2010 which was collateralized by individual consumer loans. These loans were subsequently moved to other consumer loans. We recorded $34

million and $23 million of charge-offs related to these loans in the second and first quarters of 2011, respectively, and have no remaining loss exposure following the second quarter 2011 charge-offs.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

For the Three Months Ended |

|

| |

|

June

2011 |

|

|

March

2011 |

|

|

December

2010 |

|

|

September

2010 |

|

|

June

2010 |

|

| Allowance for Credit Losses ($ in millions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Allowance for loan and lease losses, beginning |

|

$ |

2,805 |

|

|

$ |

3,004 |

|

|

$ |

3,194 |

|

|

$ |

3,693 |

|

|

$ |

3,802 |

|

| Total net losses charged off |

|

|

(304 |

) |

|

|

(367 |

) |

|

|

(356 |

) |

|

|

(956 |

) |

|

|

(434 |

) |

| Provision for loan and lease losses |

|

|

113 |

|

|

|

168 |

|

|

|

166 |

|

|

|

457 |

|

|

|

325 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Allowance for loan and lease losses, ending |

|

|

2,614 |

|

|

|

2,805 |

|

|

|

3,004 |

|

|

|

3,194 |

|

|

|

3,693 |

|

|

|

|

|

|

|

| Reserve for unfunded commitments, beginning |

|

|

211 |

|

|

|

227 |

|

|

|

231 |

|

|

|

254 |

|

|

|

260 |

|

| Provision for unfunded commitments |

|

|

(14 |

) |

|

|

(16 |

) |

|

|

(4 |

) |

|

|

(23 |

) |

|

|

(6 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Reserve for unfunded commitments, ending |

|

|

197 |

|

|

|

211 |

|

|

|

227 |

|

|

|

231 |

|

|

|

254 |

|

|

|

|

|

|

|

| Components of allowance for credit losses: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Allowance for loan and lease losses |

|

|

2,614 |

|

|

|

2,805 |

|

|

|

3,004 |

|

|

|

3,194 |

|

|

|

3,693 |

|

| Reserve for unfunded commitments |

|

|

197 |

|

|

|

211 |

|

|

|

227 |

|

|

|

231 |

|

|

|

254 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total allowance for credit losses |

|

$ |

2,811 |

|

|

$ |

3,016 |

|

|

$ |

3,231 |

|

|

$ |

3,425 |

|

|

$ |

3,947 |

|

| Allowance for loan and lease losses ratio |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| As a percent of loans and leases |

|

|

3.35 |

% |

|

|

3.62 |

% |

|

|

3.88 |

% |

|

|

4.20 |

% |

|

|

4.85 |

% |

| As a percent of nonperforming loans and leases (a) |

|

|

160 |

% |

|

|

170 |

% |

|

|

179 |

% |

|

|

202 |

% |

|

|

146 |

% |

| As a percent of nonperforming assets (a) |

|

|

125 |

% |

|

|

132 |

% |

|

|

138 |

% |

|

|

153 |

% |

|

|

124 |

% |

| (a) |

Excludes non accrual loans and leases in loans held for sale |

Provision for loan and lease losses totaled $113 million in the second quarter of 2011, down $55 million from the first quarter of 2011 and $212 million from the second quarter of 2010. The allowance for

loan and lease losses represented 3.35 percent of total loans and leases outstanding as of quarter end, compared with 3.62 percent last quarter, and represented 160 percent of nonperforming loans and leases, 125 percent of nonperforming assets, and

214 percent of second quarter annualized net charge-offs.

11

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|