| Exhibit 99.1

|

CVB Financial Corp.

November 2016

|

|

Safe Harbor

Certain matters set forth herein constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including forward-looking statements relating to the Company’s current business plans and expectations regarding the Company’s future financial position and operating results. These forward-looking statements are subject to risks and uncertainties that could cause actual results, performance and/or achievements to differ materially from those projected. These risks and uncertainties include, but are not limited to, CVBF’s ability to realize cost savings within expected time frames or at all; whether governmental approvals for the proposed transaction will be obtained within expected time frames or ever; whether the conditions to the closing of the proposed transaction, including approval by VCBP shareholders, are satisfied; local, regional, national and international economic and market conditions and events and the impact they may have on CVBF, CVBF’s customers, assets, and liabilities; our ability to attract deposits and other sources of funding or liquidity; supply and demand for real property inventory and periodic deterioration in values of California real estate, both residential and commercial; a prolonged slowdown or decline in construction or sales activity; changes in the financial performance and/or condition of our borrowers or certain key vendors or counterparties; changes in the level of nonperforming assets and any accompanying reserves and/or charge-offs; the cost or effect of acquisitions we may make; the effect of changes in laws, regulations and relevant judicial decisions (including laws, regulations and judicial decisions concerning financial reforms, taxes, bank capital levels, securities and securities trading and hedging, employment, executive compensation, insurance, vendor management and information security) with which we and our subsidiaries must or believe we should comply; changes in estimates of future reserve requirements and minimum capital requirements based upon the periodic review thereof under relevant regulatory and accounting requirements, including changes in the Basel Committee framework establishing capital standards for credit, operations and market risk; inflation, interest rate, securities market and monetary fluctuations; changes in government interest rates or monetary policies; changes in the amount and availability of deposit insurance; cyber-security threats, including loss of system functionality or theft or loss of Company or customer data or money; political instability; acts of war or terrorism, or natural disasters, such as earthquakes, or the effects of pandemic diseases; the timely development and acceptance of new banking products and services and the perceived overall value of these products and services by customers and potential customers; the Company’s relationships with and reliance upon vendors with respect to the operation of certain of the Company key internal and external systems and applications; changes in consumer spending, borrowing and savings preferences or habits; technological changes and the expanding use of technology in banking (including the adoption of mobile banking applications); the ability to retain and increase market share, retain and grow customers and control expenses; changes in the competitive environment among financial and bank holding companies, banks and other financial service providers; continued volatility in the credit and equity markets and its effect on the general economy or local or regional business conditions; fluctuations in the price of the Company’s stock; the effect of changes in accounting policies and practices, as may be adopted from time-to-time by the regulatory agencies, as well as by the Public Company Accounting Oversight Board, the Financial Accounting Standards Board and other accounting standard-setters; changes in our organization, management, compensation and benefit plans, and our ability to retain or expand our management team and/or our board of directors; the costs and effects of legal, compliance and regulatory changes and developments, including pending or threatened litigation, the resolution of legal proceedings or regulatory or other governmental inquiries or investigations, and the results of regulatory examinations or reviews; our success at managing the risks involved in the foregoing items and all other factors set forth in the Company’s public reports including its Annual Report on Form 10-K for the year ended December 31, 2015, and particularly the discussion of risk factors within that document. The Company does not undertake, and specifically disclaims any obligation, to update any forward-looking statements to reflect occurrences or unanticipated events.

cbbank.com 2

|

|

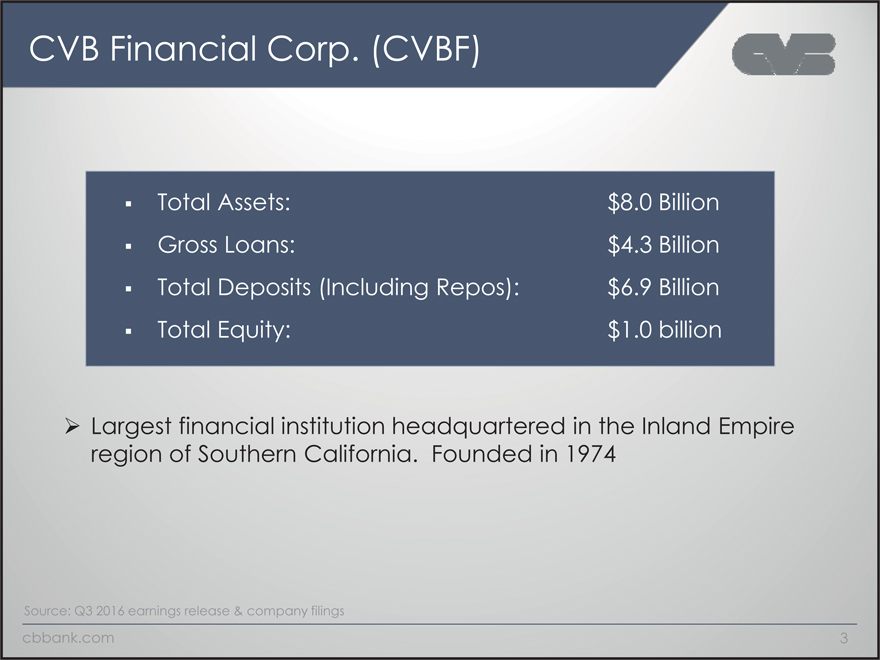

CVB Financial Corp. (CVBF)

Total Assets: $8.0 Billion Gross Loans: $4.3 Billion Total Deposits (Including Repos): $6.9 Billion Total Equity: $1.0 billion

Largest financial institution headquartered in the Inland Empire region of Southern California. Founded in 1974

Source: Q3 2016 earnings release & company filings cbbank.com 3

|

|

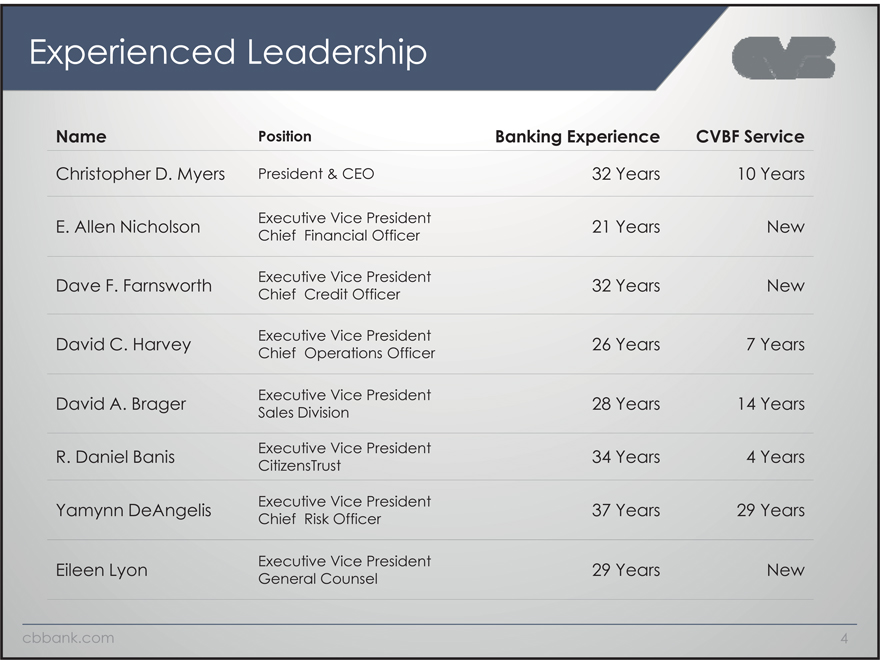

Experienced Leadership

Name Position Banking ExperienceCVBF Service

Christopher D. Myers President & CEO 32 Years10 Years

E. Allen Nicholson Executive Vice President 21 YearsNew

Chief Financial Officer

Dave F. Farnsworth Executive Vice President 32 YearsNew

Chief Credit Officer

David C. Harvey Executive Vice President 26 Years7 Years

Chief Operations Officer

David A. Brager Executive Vice President 28 Years14 Years

Sales Division

R. Daniel Banis Executive Vice President 34 Years4 Years

CitizensTrust

Yamynn DeAngelis Executive Vice President 37 Years29 Years

Chief Risk Officer

Eileen Lyon Executive Vice President 29 YearsNew

General Counsel

cbbank.com 4

|

|

Board of Directors

Name CVBF Experience Age

Ray O’Brien—Chairman 4 Years 59

George Borba Jr.—Vice Chairman 3 Years 49

Steve Del Guercio 4 Years 55

Robert Jacoby 11 Years 75

Kristina Leslie 1 Year 51

Hal Oswalt 2 Years 68

Anna Kan New 43

Chris Myers—CEO 10 Years 54

cbbank.com 5

|

|

CVB Financial Corp.

Who is CVB Financial Corp.?

cbbank.com

|

|

Largest Bank Holding Companies

Headquartered in California

Rank Name Asset Size (9/30/16)

1 Wells Fargo & Company $1,942,124

2 First Republic Bank* $67,994

3 SVB Financial Group $43,274

4 East West Bancorp $33,255

5 Pacwest Bancorp $21,315

6 Cathay General Bancorp $14,099

7 Hope Bancorp, Inc. $13,508

8 Banc of California, Inc. $11,216

9 CVB Financial Corp. $8,044

10 Opus Bank* $7,709

* Bank only, no holding company

Source: SNL Financial In millions

cbbank.com 7

|

|

8

RANKED # 1

CVB Financial Corp. Ranked #1, Holding company for Citizens business Bank

|

|

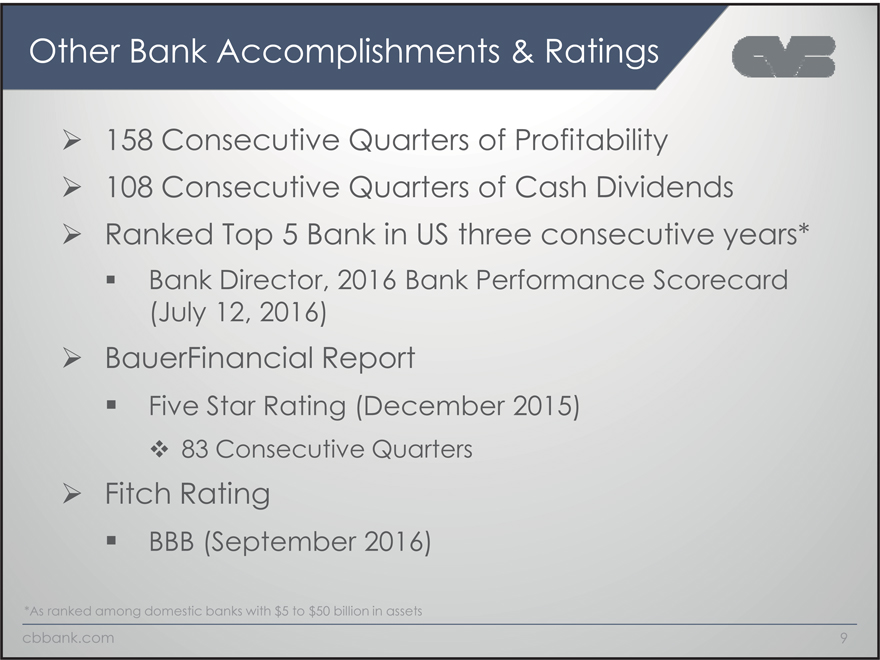

Other Bank Accomplishments & Ratings

158 Consecutive Quarters of Profitability 108 Consecutive Quarters of Cash Dividends Ranked Top 5 Bank in US three consecutive years*

Bank Director, 2016 Bank Performance Scorecard (July 12, 2016)

BauerFinancial Report

Five Star Rating (December 2015)

83 Consecutive Quarters

Fitch Rating

BBB (September 2016)

*As ranked among domestic banks with $5 to $50 billion in assets cbbank.com 9

|

|

Our Markets

cbbank.com

|

|

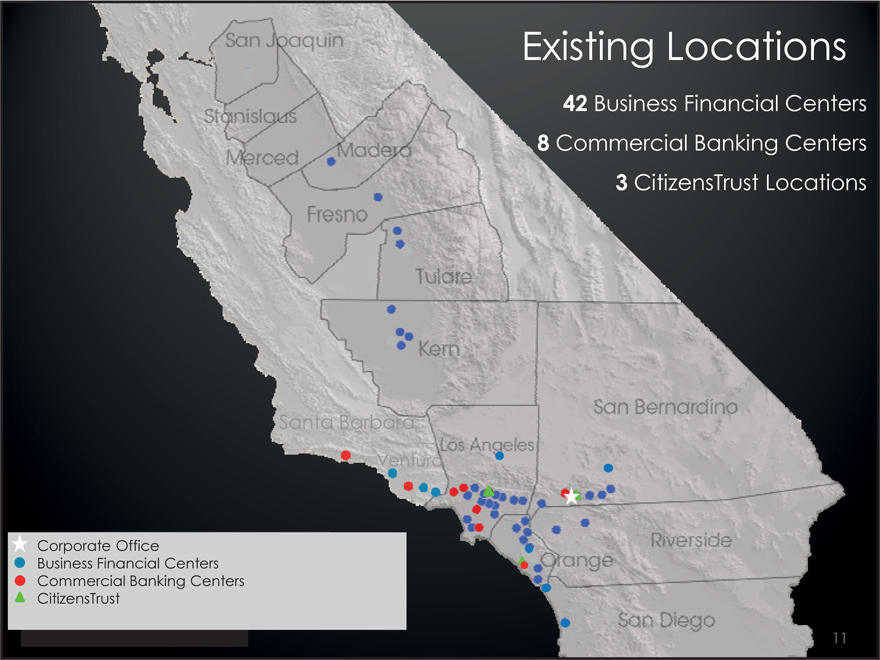

Existing Locations

42 Business Financial Centers

8 Commercial Banking Centers

3 CitizensTrust Locations

Santa Barbara

Ventura

Corporate Office

Business Financial Centers Commercial Banking Centers CitizensTrust

cbbank 11

|

|

New Acquisition

Valley Commerce Bancorp ‘VCBP’

cbbank.com

|

|

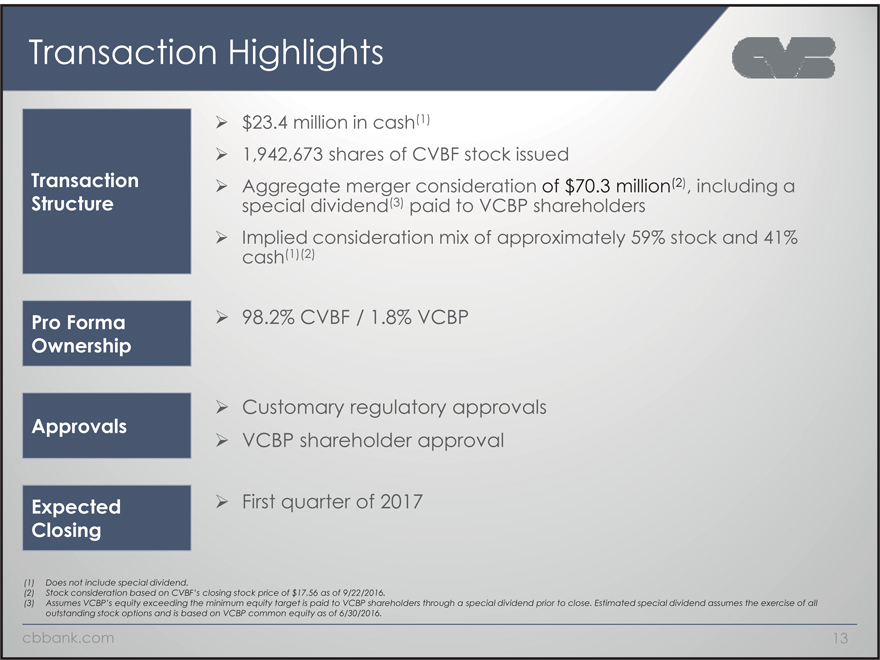

Transaction Highlights

$23.4 million in cash(1)

1,942,673 shares of CVBF stock issued

Transaction Aggregate merger consideration of $70.3 million(2), including a Structure special dividend(3) paid to VCBP shareholders Implied consideration mix of approximately 59% stock and 41%

cash(1)(2)

Pro Forma 98.2% CVBF / 1.8% VCBP

Ownership

Approvals Customary regulatory approvals VCBP shareholder approval

Expected First quarter of 2017

Closing

(1) Does not include special dividend.

(2) Stock consideration based on CVBF’s closing stock price of $17.56 as of 9/22/2016.

(3) Assumes VCBP’s equity exceeding the minimum equity target is paid to VCBP shareholders through a special dividend prior to close. Estimated special dividend assumes the exercise of all outstanding stock options and is based on VCBP common equity as of 6/30/2016.

cbbank.com 13

|

|

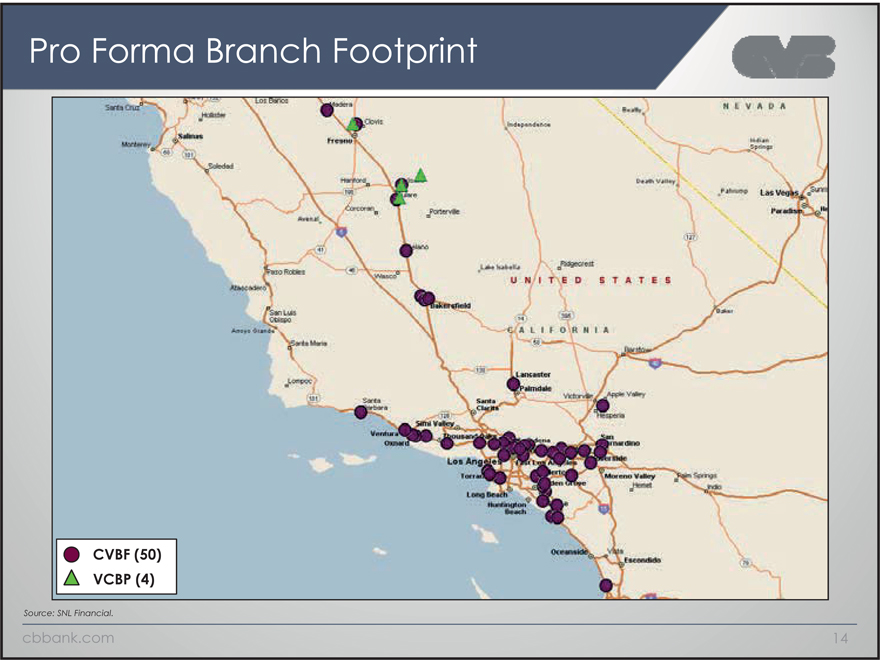

Pro Forma Branch Footprint

• CVBF (50)

• VCBP (4)

Source: SNL Financial.

cbbank.com 14

|

|

Financial Impact

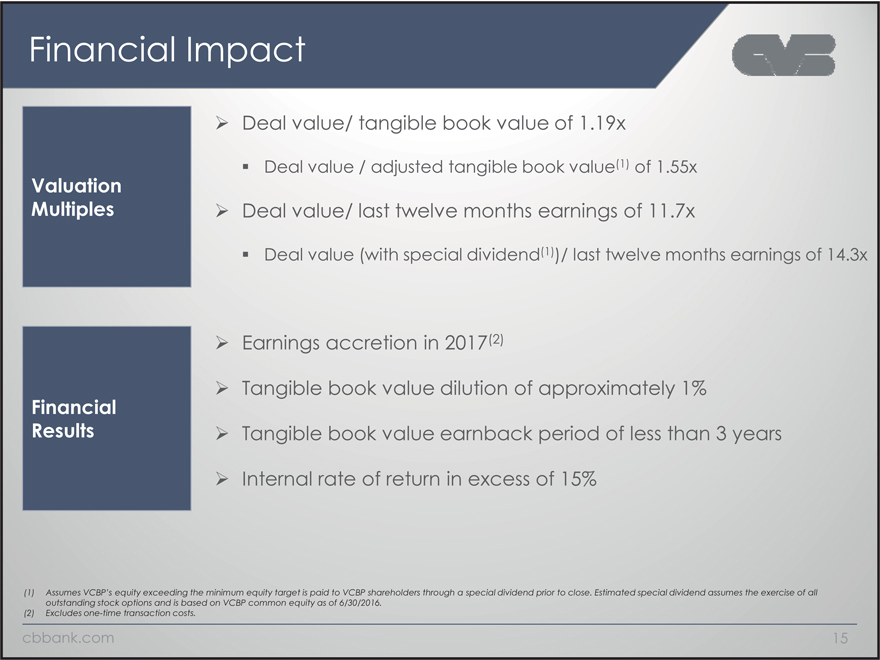

Deal value/ tangible book value of 1.19x

Deal value / adjusted tangible book value(1) of 1.55x

Valuation

Multiples Deal value/ last twelve months earnings of 11.7x

Deal value (with special dividend(1))/ last twelve months earnings of 14.3x

Earnings accretion in 2017(2)

Financial Tangible book value dilution of approximately 1% Results Tangible book value earnback period of less than 3 years Internal rate of return in excess of 15%

(1) Assumes VCBP’s equity exceeding the minimum equity target is paid to VCBP shareholders through a special dividend prior to close. Estimated special dividend assumes the exercise of all outstanding stock options and is based on VCBP common equity as of 6/30/2016.

(2) Excludes one-time transaction costs.

cbbank.com 15

|

|

De Novo Expansion

cbbank.com

|

|

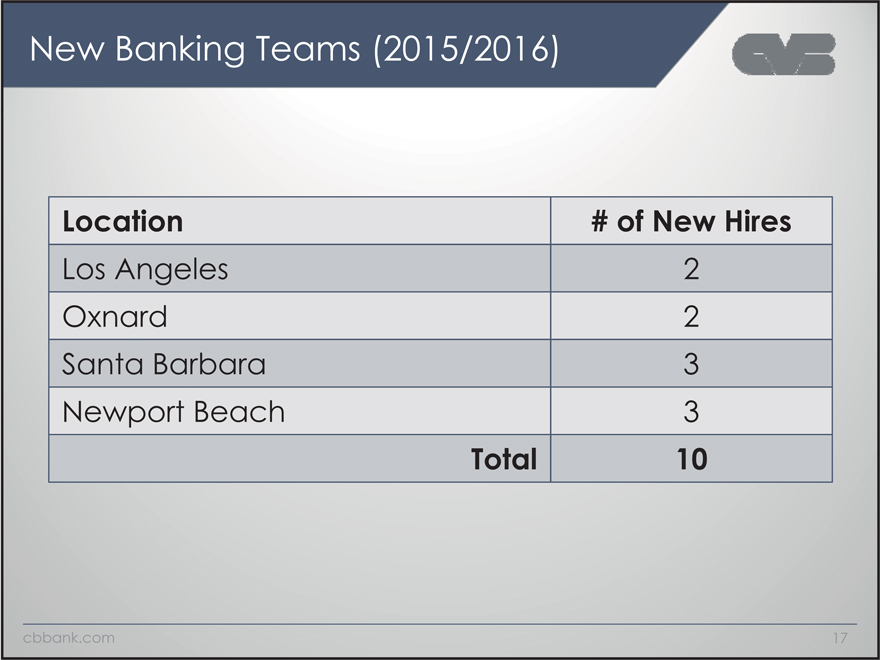

New Banking Teams (2015/2016)

Location # of New Hires

Los Angeles 2 Oxnard 2 Santa Barbara 3 Newport Beach 3

Total 10

cbbank.com 17

|

|

Financial Performance

cbbank.com

|

|

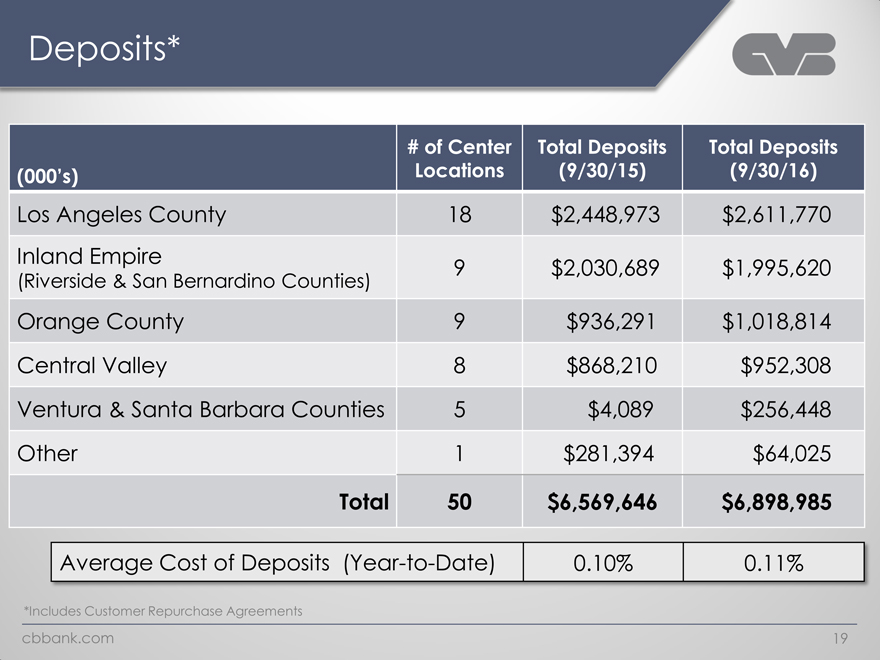

Deposits*

# of Center Total Deposits Total Deposits (000’s) Locations (9/30/15) (9/30/16)

Los Angeles County 18 $2,448,973 $2,611,770 Inland Empire

9 $2,030,689 $1,995,620

(Riverside & San Bernardino Counties)

Orange County 9 $936,291 $1,018,814 Central Valley 8 $868,210 $952,308 Ventura & Santa Barbara Counties 5 $4,089 $256,448 Other 1 $281,394 $64,025

Total 50 $6,569,646 $6,898,985

Average Cost of Deposits (Year-to-Date) 0.10% 0.11%

*Includes Customer Repurchase Agreements cbbank.com 19

|

|

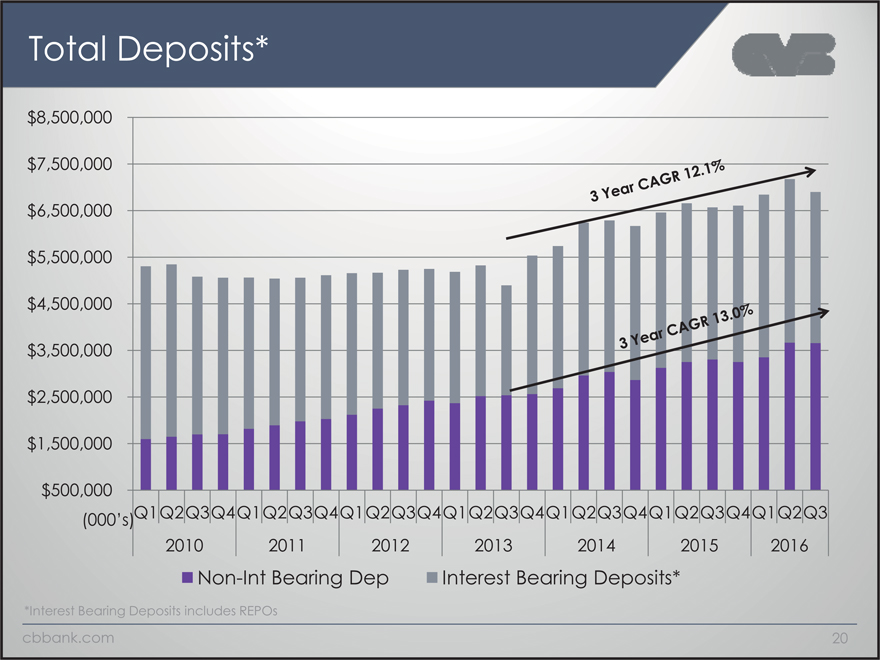

Total Deposits*

$8,500,000

$7,500,000

$6,500,000

$5,500,000

$4,500,000

$3,500,000

$2,500,000

$1,500,000

$500,000

(000’s) Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3

2010 2011 20122013201420152016

Non-Int Bearing Dep Interest Bearing Deposits*

*Interest Bearing Deposits includes REPOs

cbbank.com 20

|

|

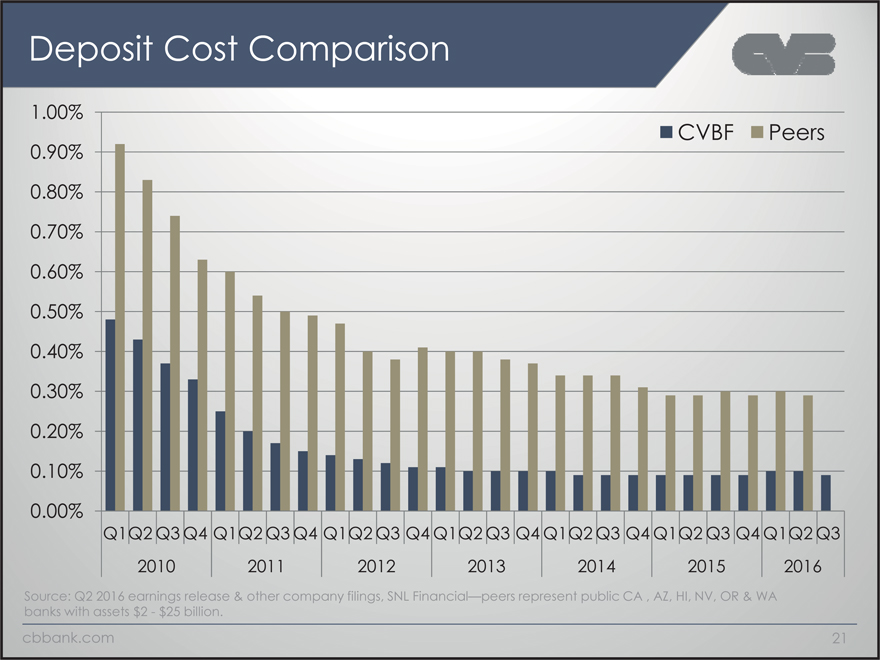

Deposit Cost Comparison

1.00%

CVBFPeers

0.90%

0.80%

0.70%

0.60%

0.50%

0.40%

0.30%

0.20%

0.10%

0.00%

Q1Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1Q2 Q3 Q4 Q1Q2 Q3

2010 2011 20122013201420152016

Source: Q2 2016 earnings release & other company filings, SNL Financial—peers represent public CA , AZ, HI, NV, OR & WA

banks with assets $2—$25 billion.

cbbank.com 21

|

|

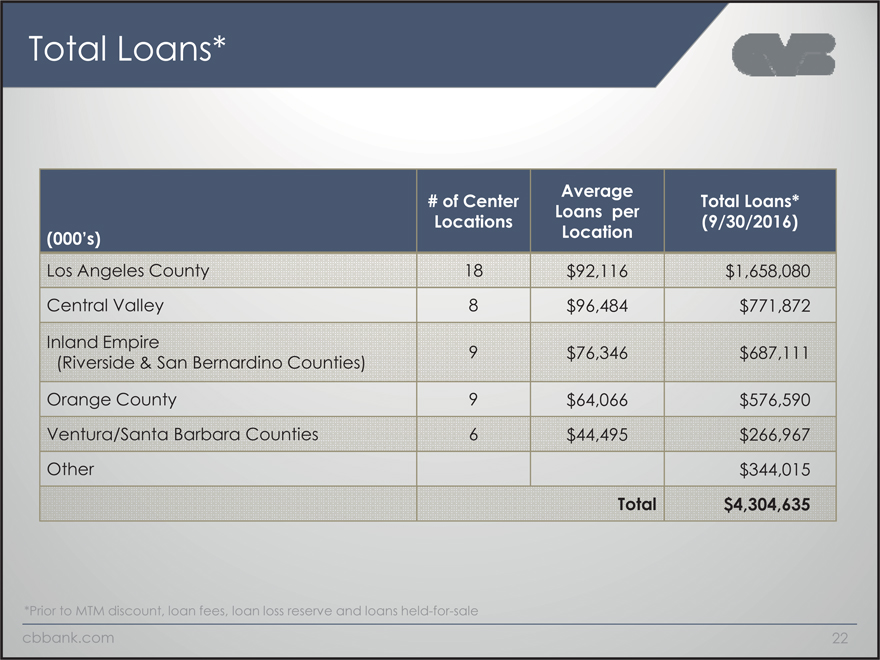

Total Loans*

Average

# of Center Total Loans* Loans per (000’s) Location

Los Angeles County 18 $92,116 $1,658,080 Central Valley 8 $96,484 $771,872 Inland Empire

9 $76,346 $687,111 (Riverside & San Bernardino Counties) Orange County 9 $64,066 $576,590 Ventura/Santa Barbara Counties 6 $44,495 $266,967 Other $344,015

Total $4,304,635

*Prior to MTM discount, loan fees, loan loss reserve and loans held-for-sale cbbank.com 22

|

|

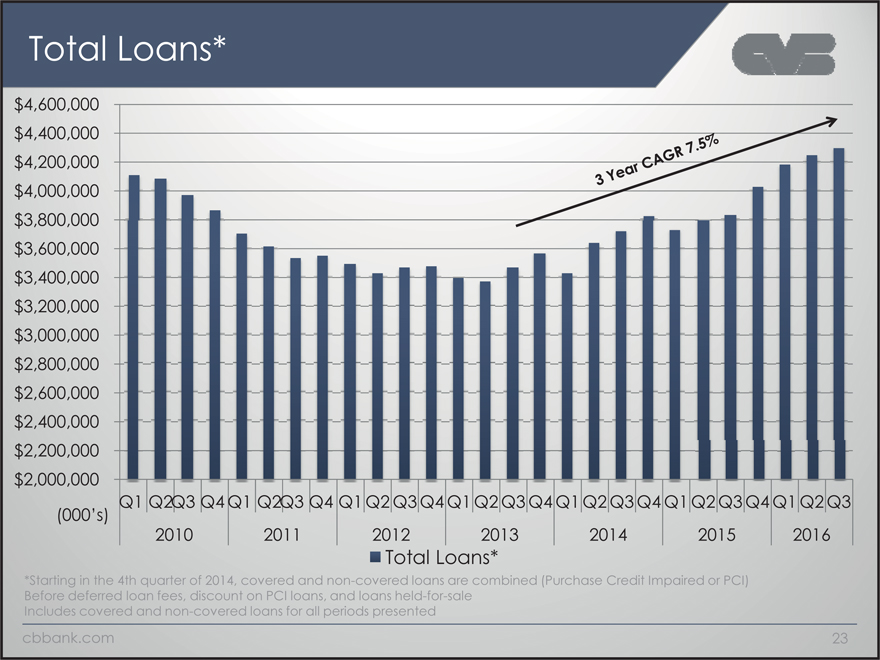

Total Loans*

$ 4,600,000

$ 4,400,000

$ 4,200,000

$ 4,000,000

$ 3,800,000

$ 3,600,000

$ 3,400,000

$ 3,200,000

$ 3,000,000

$ 2,800,000

$ 2,600,000

$ 2,400,000

$ 2,200,000

$ 2,000,000

Q1 Q2Q3 Q4 Q1 Q2Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

(000’s)

2010 201120122013201420152016

Total Loans*

*Starting in the 4th quarter of 2014, covered and non-covered loans are combined (Purchase Credit Impaired or PCI)

Before deferred loan fees, discount on PCI loans, and loans held-for-sale

Includes covered and non-covered loans for all periods presented

cbbank.com 23

|

|

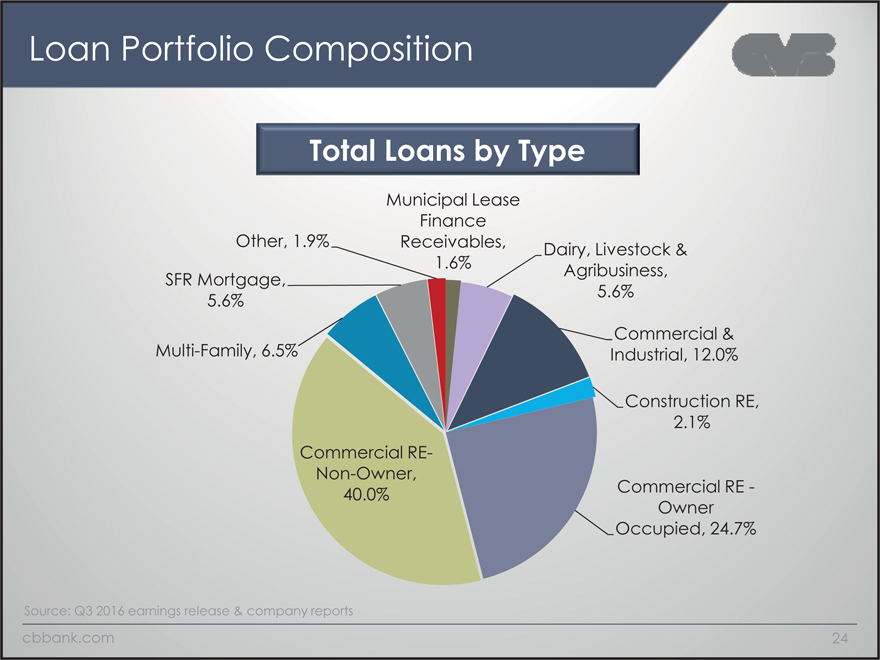

Loan Portfolio Composition

Total Loans by Type

Municipal Lease

Finance

Other, 1.9% Receivables, Dairy, Livestock &

1.6% Agribusiness,

SFR Mortgage,

5.6% 5.6%

Commercial &

Multi-Family, 6.5% Industrial, 12.0%

Construction RE,

2.1%

Commercial RE-

Non-Owner,

40.0% Commercial RE -

Owner

Occupied, 24.7%

Source: Q3 2016 earnings release & company reports

cbbank.com 24

|

|

Credit Quality

cbbank.com

|

|

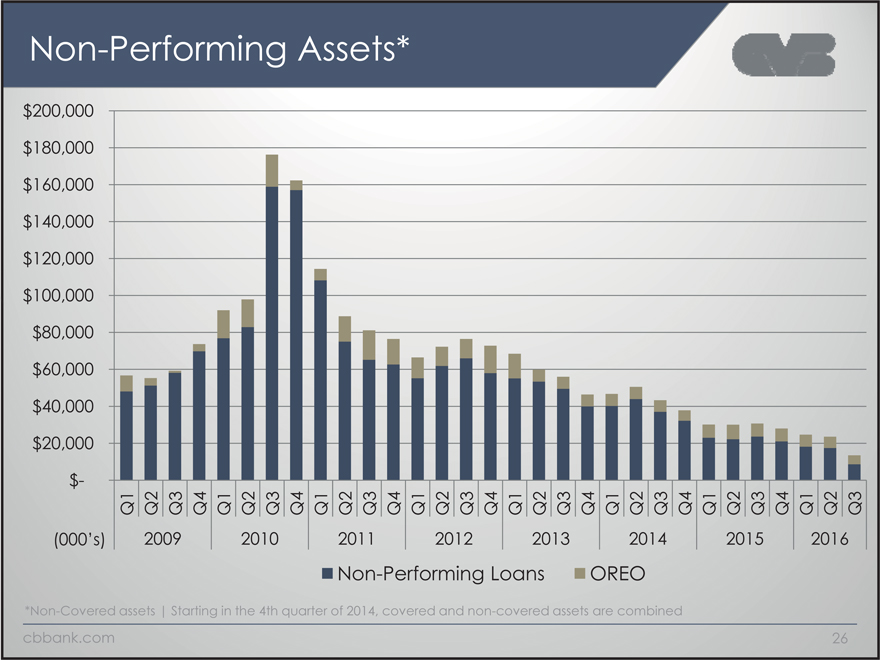

Non-Performing Assets*

$200,000

$180,000

$160,000

,

$120,000

$100,000

$80,000

$60,000

$40,000

$20,000

$-

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

(000’s) 2009 2010 20112012201320142015 2016

Non-Performing LoansOREO

*Non-Covered assets | Starting in the 4th quarter of 2014, covered and non-covered assets are combined

cbbank.com 26

|

|

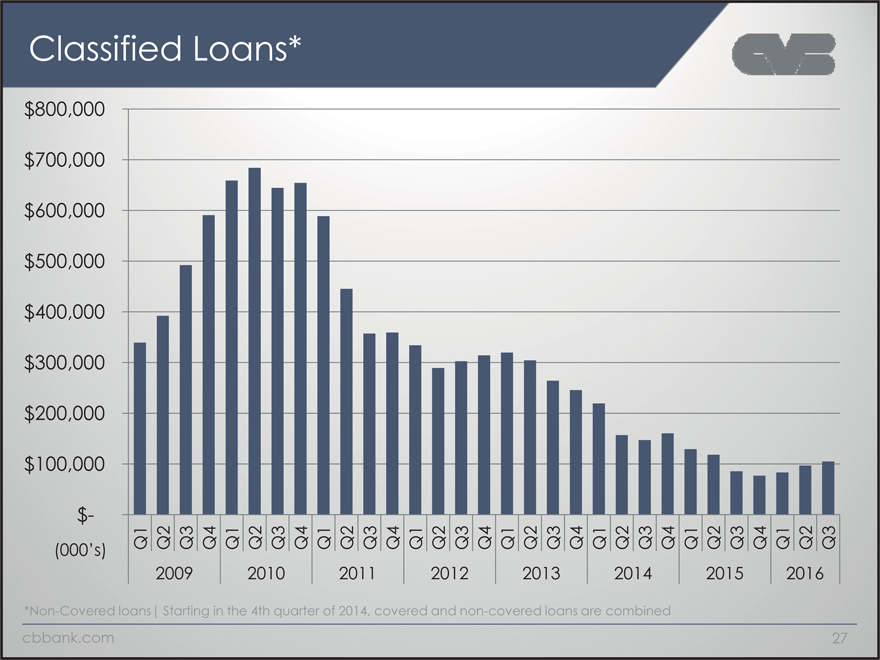

Classified Loans*

$800,000

$700,000

$600,000

$500,000

$400,000

$300,000

$200,000

$100,000

$-

(000’s) Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2009 2010 201120122013201420152016

*Non-Covered loans| Starting in the 4th quarter of 2014, covered and non-covered loans are combined

cbbank.com 27

|

|

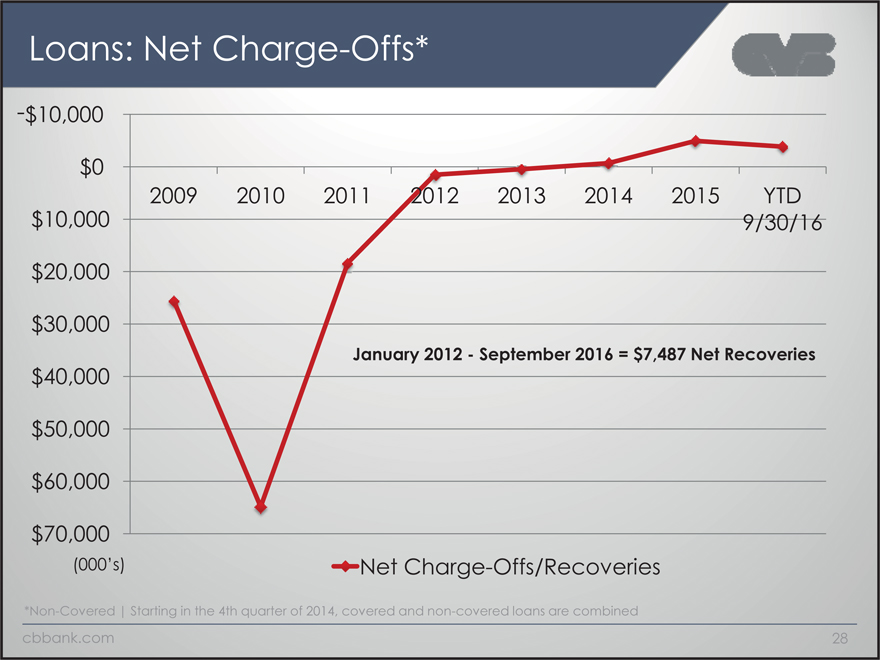

Loans: Net Charge-Offs*

-$10,000

$0

2009 2010 2011 2012 2013 2014 2015 YTD

$10,000 9/30/16

$20,000

$30,000

January 2012—September 2016 = $7,487 Net Recoveries

$40,000

$50,000

$60,000

$70,000

(000’s) Net Charge-Offs/Recoveries

*Non-Covered | Starting in the 4th quarter of 2014, covered and non-covered loans are combined

cbbank.com 28

|

|

Profits

cbbank.com

|

|

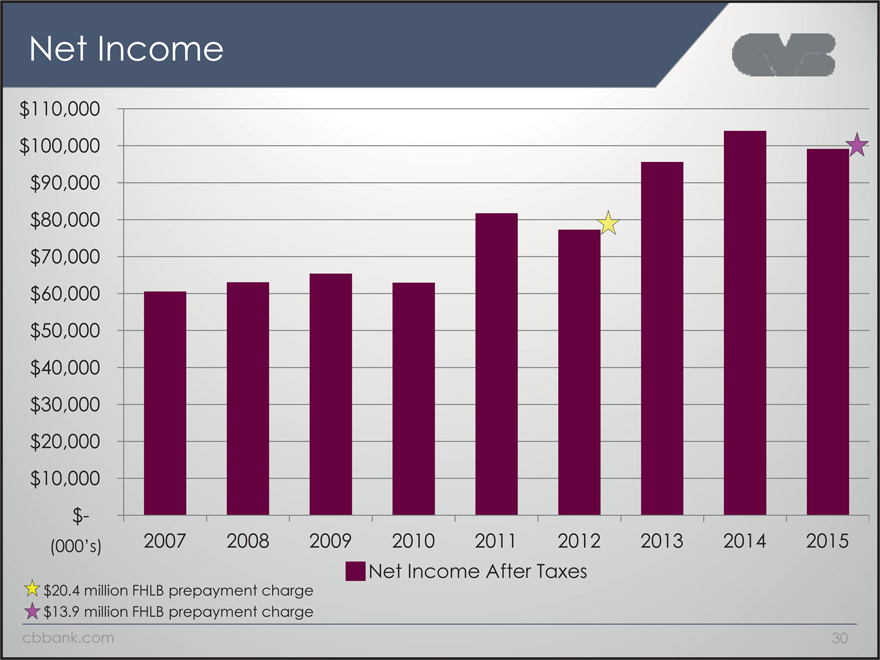

Net Income

$110,000

$100,000

$90,000

$80,000

$70,000

$60,000

$50,000

$40,000

$30,000

$20,000

$10,000

$-

(000’s) 2007 2008 20092010 2011 2012201320142015

Net Income After Taxes

$20.4 million FHLB prepayment charge

$13.9 million FHLB prepayment charge

cbbank.com 30

|

|

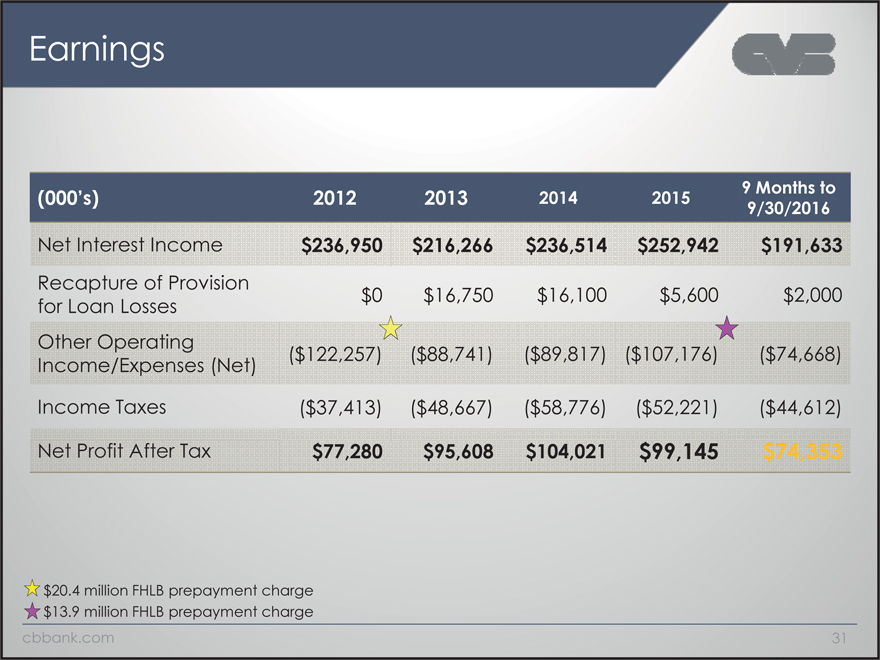

Earnings

(000’s) 2012 2013201420159 Months to

9/30/2016

Net Interest Income $236,950 $216,266$236,514$252,942$191,633

Recapture of Provision

for Loan Losses $0 $16,750$16,100$5,600$2,000

Other Operating

Income/Expenses (Net) ($122,257) ($88,741)($89,817)($107,176)($74,668)

Income Taxes ($37,413) ($48,667)($58,776)($52,221)($44,612)

Net Profit After Tax $77,280 $95,608$104,021$99,145$74,353

$ 20.4 million FHLB prepayment charge

$ 13.9 million FHLB prepayment charge

cbbank.com 31

|

|

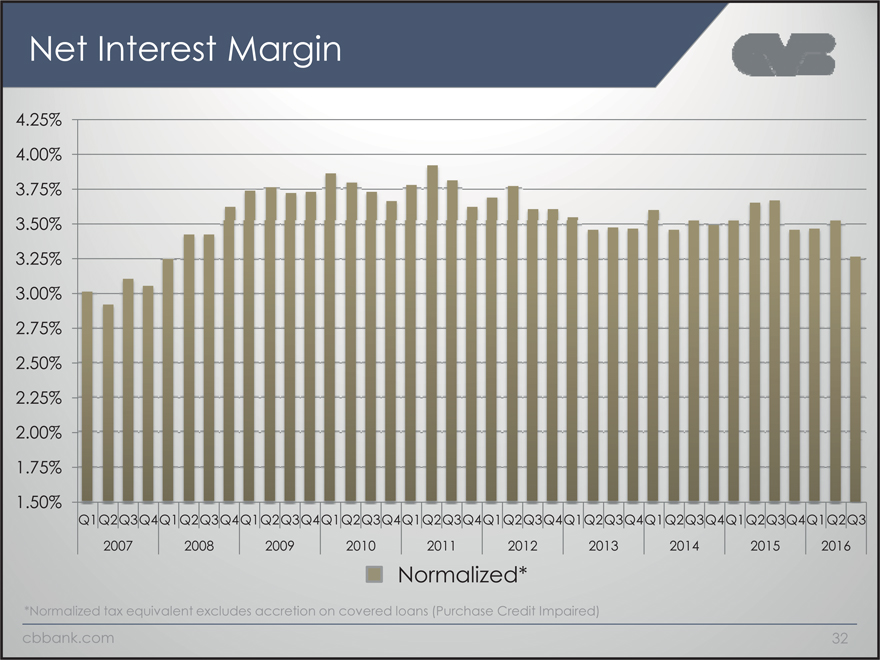

Net Interest Margin

4.25%

4.00%

3.75%

3.50%

3.25%

3.00%

2.75%

2.50%

2.25%

2.00%

1.75%

1.50%

Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3

2007 2008 20092010201120122013201420152016

Normalized*

*Normalized tax equivalent excludes accretion on covered loans (Purchase Credit Impaired)

cbbank.com 32

|

|

Efficiency & Expenses

cbbank.com

|

|

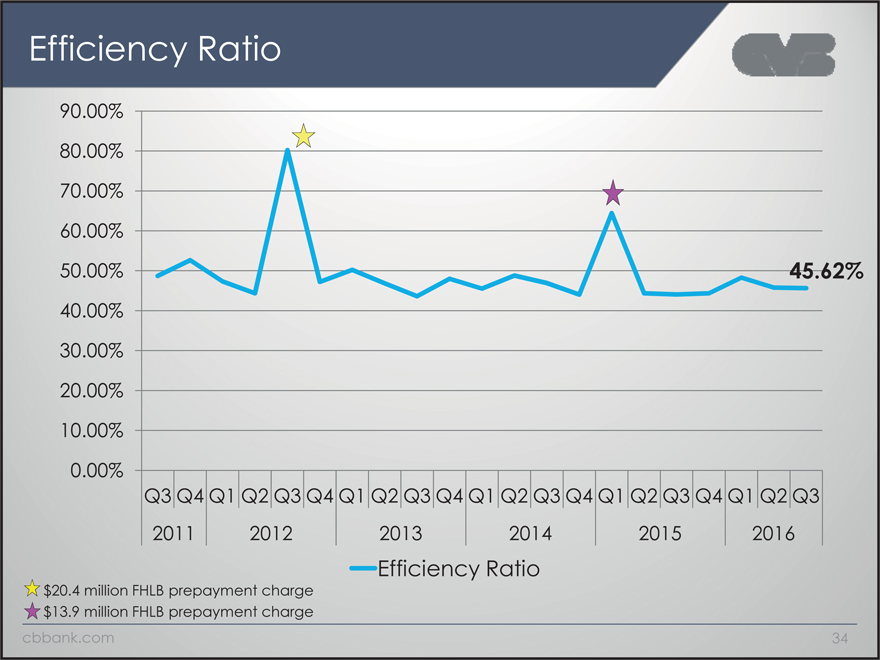

Efficiency Ratio

90.00%

80.00%

70.00%

60.00%

50.00% 45.62%

40.00%

30.00%

20.00%

10.00%

0.00%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 20122013201420152016

Efficiency Ratio

$ 20.4 million FHLB prepayment charge

$ 13.9 million FHLB prepayment charge

cbbank.com 34

|

|

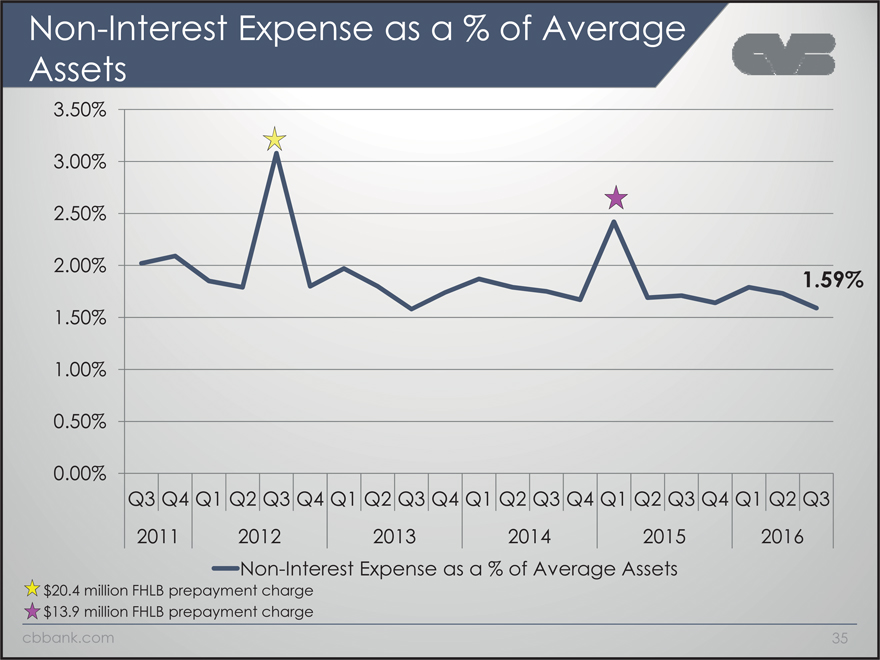

Non-Interest Expense as a % of Average

Assets

3.50%

3.00%

2.50%

2.00% 1.59%

1.50%

1.00%

0.50%

0.00%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 20122013201420152016

Non-Interest Expense as a % of Average Assets

$ 20.4 million FHLB prepayment charge

$ 13.9 million FHLB prepayment charge

cbbank.com 35

|

|

Capital

cbbank.com

|

|

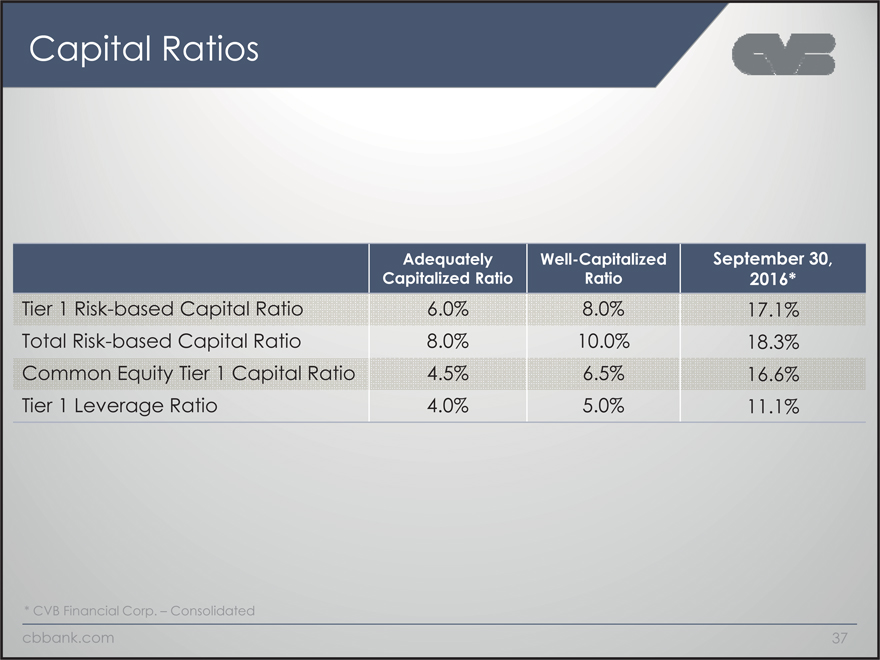

Capital Ratios

Adequately Well-CapitalizedSeptember 30,

Capitalized Ratio Ratio2016*

Tier 1 Risk-based Capital Ratio 6.0% 8.0%17.1%

Total Risk-based Capital Ratio 8.0% 10.0%18.3%

Common Equity Tier 1 Capital Ratio 4.5% 6.5%16.6%

Tier 1 Leverage Ratio 4.0% 5.0%11.1%

* CVB Financial Corp. – Consolidated

cbbank.com 37

|

|

Securities & Investments

cbbank.com

|

|

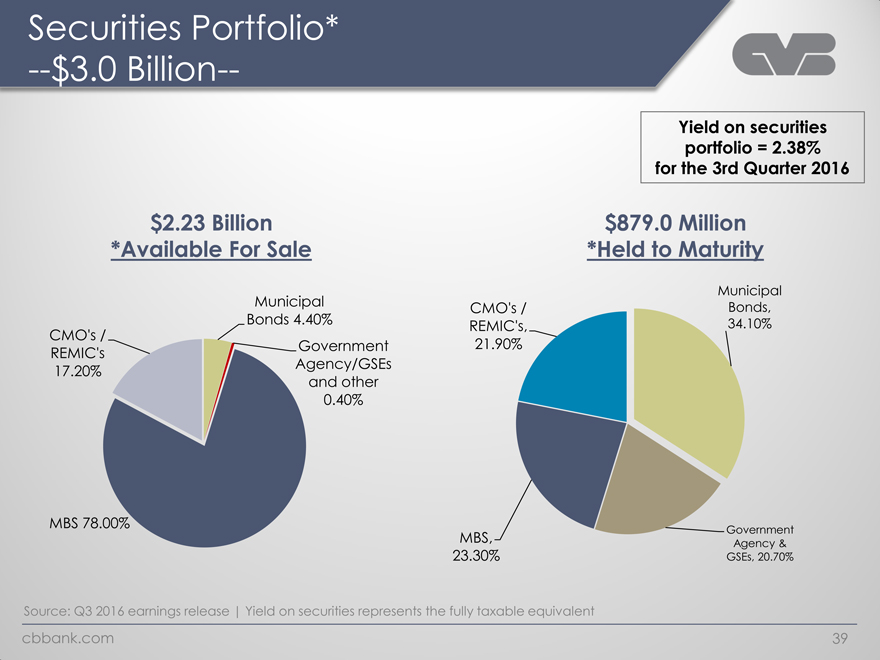

Securities Portfolio*

--$3.0 Billion--

Yield on securities portfolio = 2.38% for the 3rd Quarter 2016

$2.23 Billion $879.0 Million

*Available For Sale *Held to Maturity

Municipal

Municipal CMO’s / Bonds, CMO’s / Bonds 4.40% REMIC’s, 34.10% Government 21.90% REMIC’s 17.20% Agency/GSEs and other

0.40%

MBS 78.00% MBS, Government

Agency & 23.30% GSEs, 20.70%

Source: Q3 2016 earnings release | Yield on securities represents the fully taxable equivalent cbbank.com 39

|

|

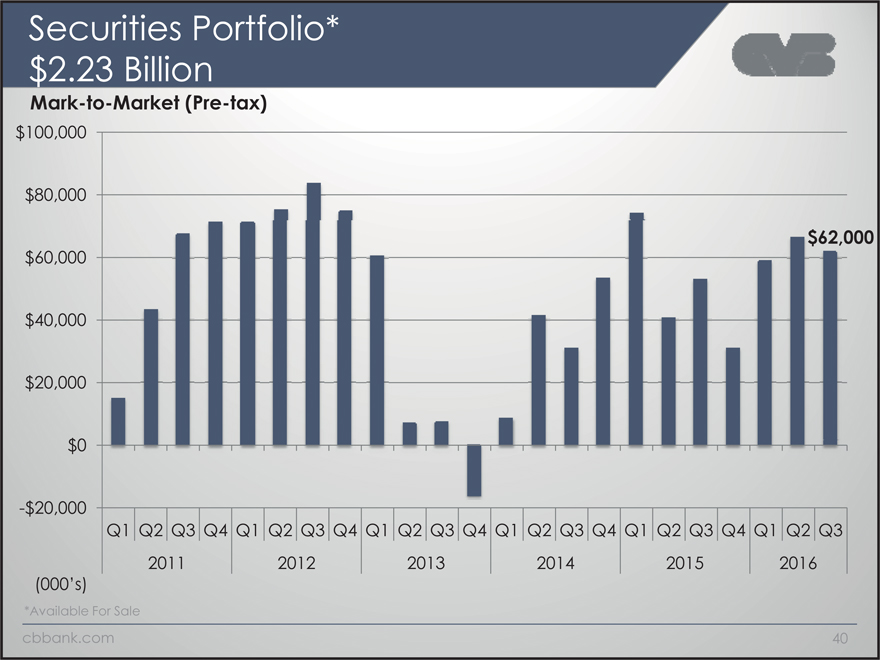

Securities Portfolio*

$2.23 Billion

Mark-to-Market (Pre-tax)

$100,000

$80,000

$62,000

$60,000

$40,000

$20,000

$0

-$20,000

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2011 2012 2013201420152016

(000’s)

*Available For Sale

cbbank.com 40

|

|

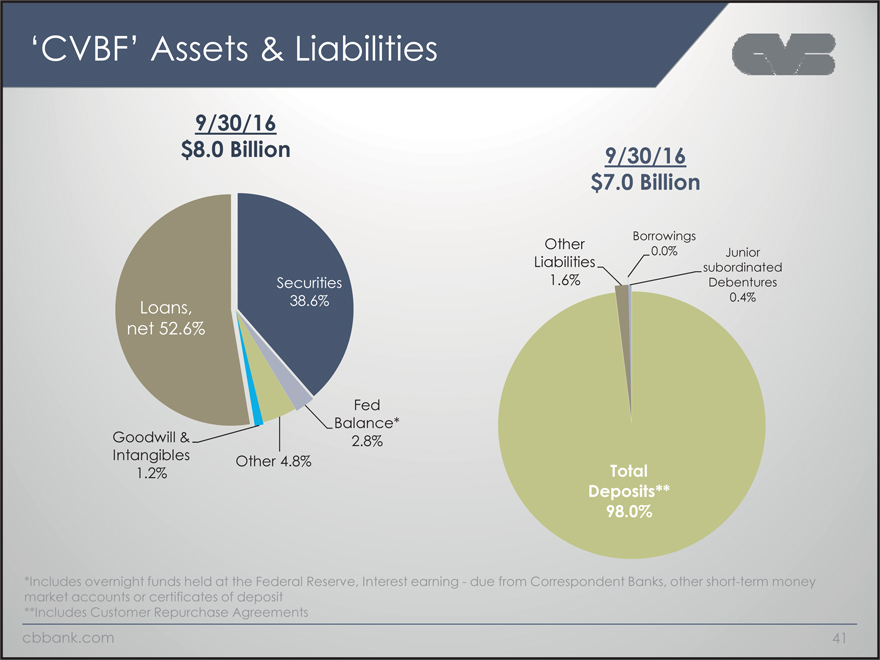

‘CVBF’ Assets & Liabilities

9/30/16

$8.0 Billion 9/30/16

$7.0 Billion

Borrowings

Other0.0%Junior

Liabilitiessubordinated

Securities 1.6%Debentures

Loans, 38.6% 0.4%

net 52.6%

Fed

Balance*

Goodwill & .

Intangibles Other 4.8%

1.2% Total

DepositsDeposits****

98.0%

*Includes overnight funds held at the Federal Reserve, Interest earning—due from Correspondent Banks, other short-term money

market accounts or certificates of deposit

**Includes Customer Repurchase Agreements

cbbank.com 41

|

|

Yield on Securities vs. Yield on Loans

6.00%

5.46%

5.00%

5.17% 4.41%

4.00%

3.00%

2.38%

2.00%

1.00%

0.00%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2009 2010 20112012201320142015 2016

Yield on Loans* Yield on Securities**

*Excluding Discount Accretion on PCI loans

**Includes Available for Sale and Held to Maturity, TE

cbbank.com 42

|

|

Our Growth Strategy

cbbank.com

|

|

Our Vision

Citizens Business Bank will strive to become the premier financial services company operating throughout the state of California, servicing the comprehensive financial needs of successful small to medium sized businesses and their owners.

cbbank.com 44

|

|

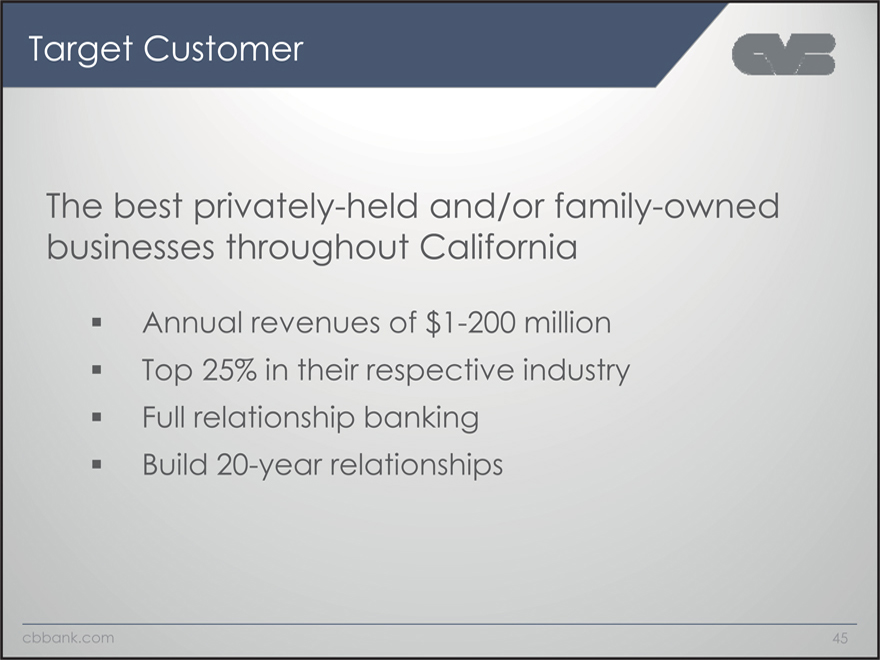

Target Customer

The best privately-held and/or family-owned businesses throughout California

Annual revenues of $1-200 million? Top 25% in their respective industry? Full relationship banking? Build 20-year relationships

cbbank.com 45

|

|

Three Areas of Growth

Same Store DeNovo

Sales San Diego Oxnard (2014) (2015) Santa Barbara (2015)

American Acquisitions County Security Bank Commerce Bank (2014) (2016) Valley Business Bank (deal announced Sept.

2016)

cbbank.com 46

|

|

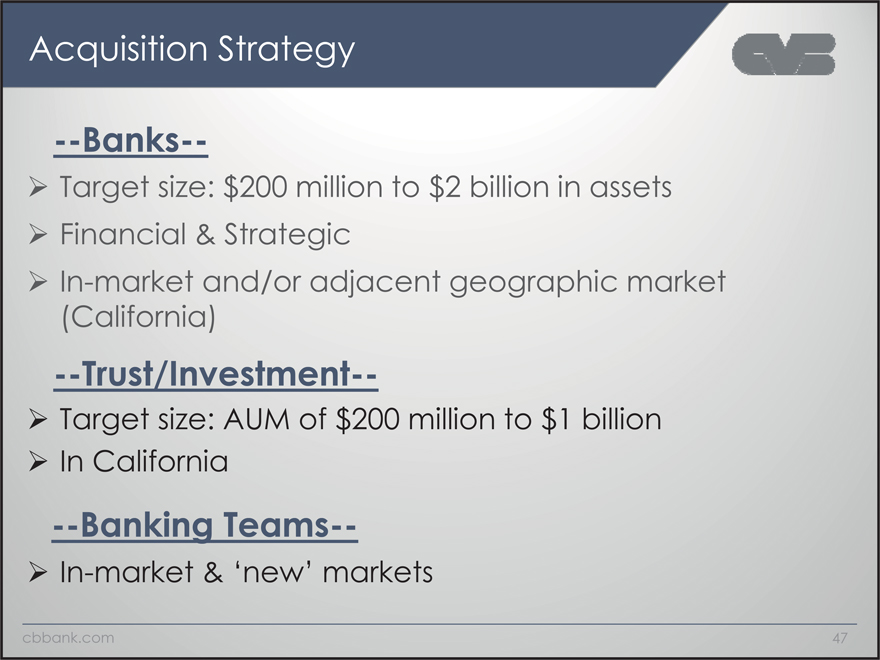

Acquisition Strategy

—Banks—

Target size: $200 million to $2 billion in assets Financial & Strategic In-market and/or adjacent geographic market (California)

—Trust/Investment—

Target size: AUM of $200 million to $1 billion In California

—Banking Teams—

In-market & ‘new’ markets

cbbank.com 47

|

|

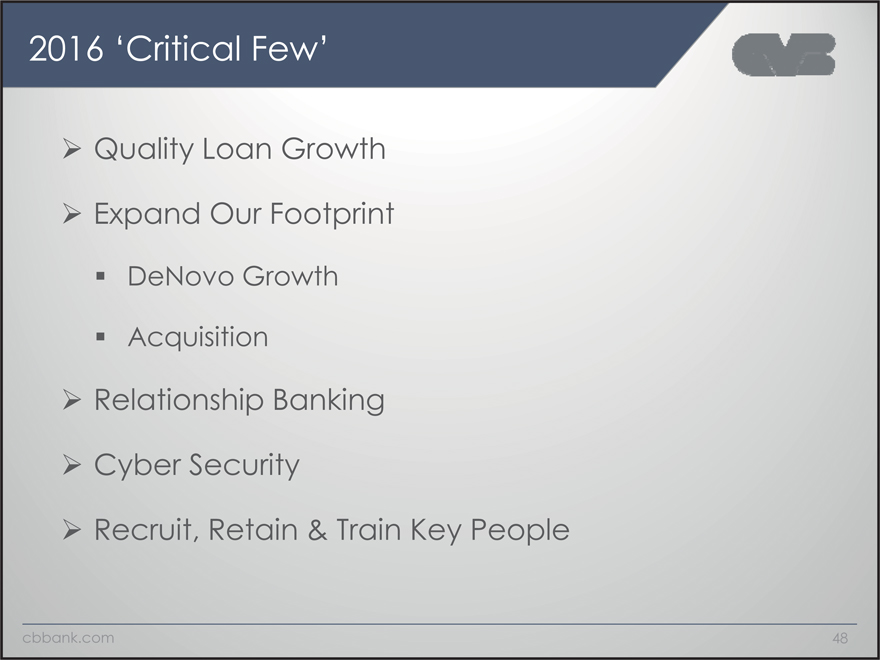

2016 ‘Critical Few’

Quality Loan Growth Expand Our Footprint

DeNovo Growth

Acquisition

Relationship Banking Cyber Security

Recruit, Retain & Train Key People

cbbank.com 48

|

|

Copy of presentation at www.cbbank.com

cbbank.com