UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-215

Fidelity Hastings Street Trust

(Exact name of registrant as specified in charter)

82 Devonshire St., Boston, Massachusetts 02109

(Address of principal executive offices) (Zip code)

Scott C. Goebel, Secretary

82 Devonshire St.

Boston, Massachusetts 02109

(Name and address of agent for service)

Registrant's telephone number, including area code: 617-563-7000

|

Date of fiscal year end: |

December 31 |

|

|

|

|

Date of reporting period: |

December 31, 2011 |

Item 1. Reports to Stockholders

Fidelity®

Series Emerging Markets Debt

Fund

Fidelity Series Emerging Markets Debt Fund

Class F

Annual Report

December 31, 2011

Contents

|

Performance |

How the fund has done over time. |

|

|

Management's Discussion of Fund Performance |

The Portfolio Manager's review of fund performance, strategy and outlook. |

|

|

Shareholder Expense Example |

An example of shareholder expenses. |

|

|

Investment Changes |

A summary of the fund's investments. |

|

|

Investments |

A complete list of the fund's investments with their market values. |

|

|

Financial Statements |

Statements of assets and liabilities, operations, and changes in net

assets, |

|

|

Notes |

Notes to the financial statements. |

|

|

Report of Independent Registered Public Accounting Firm |

|

|

|

Trustees and Officers |

|

|

|

Distributions |

|

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov. You may also call 1-800-544-8544 for Fidelity Series Emerging Markets Debt Fund or 1-800-835-5092 for Class F to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the fund. This report is not authorized for distribution to prospective investors in the fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. Forms N-Q are available on the SEC's web site at http://www.sec.gov. A fund's Forms N-Q may be reviewed and copied at the SEC's Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330. For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.advisor.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED • MAY LOSE VALUE • NO BANK GUARANTEE

Neither the fund nor Fidelity Distributors Corporation is a bank.

Annual Report

Performance: The Bottom Line

Average annual total return reflects the change in the value of an investment, assuming reinvestment of the fund's distributions from dividend income and capital gains (the profits earned upon the sale of securities that have grown in value, if any) and assuming a constant rate of performance each year. The $10,000 table and the fund's returns do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. During periods of reimbursement by Fidelity, a fund's total return will be greater than it would be had the reimbursement not occurred. How a fund did yesterday is no guarantee of how it will do tomorrow.

Average annual total returns take Fidelity® Series Emerging Markets Debt Fund, a class of the fund, and Class F's cumulative total return and show you what would have happened if Fidelity® Series Emerging Markets Debt Fund and Class F shares had performed at a constant rate each year. These numbers will be reported once the fund is a year old.

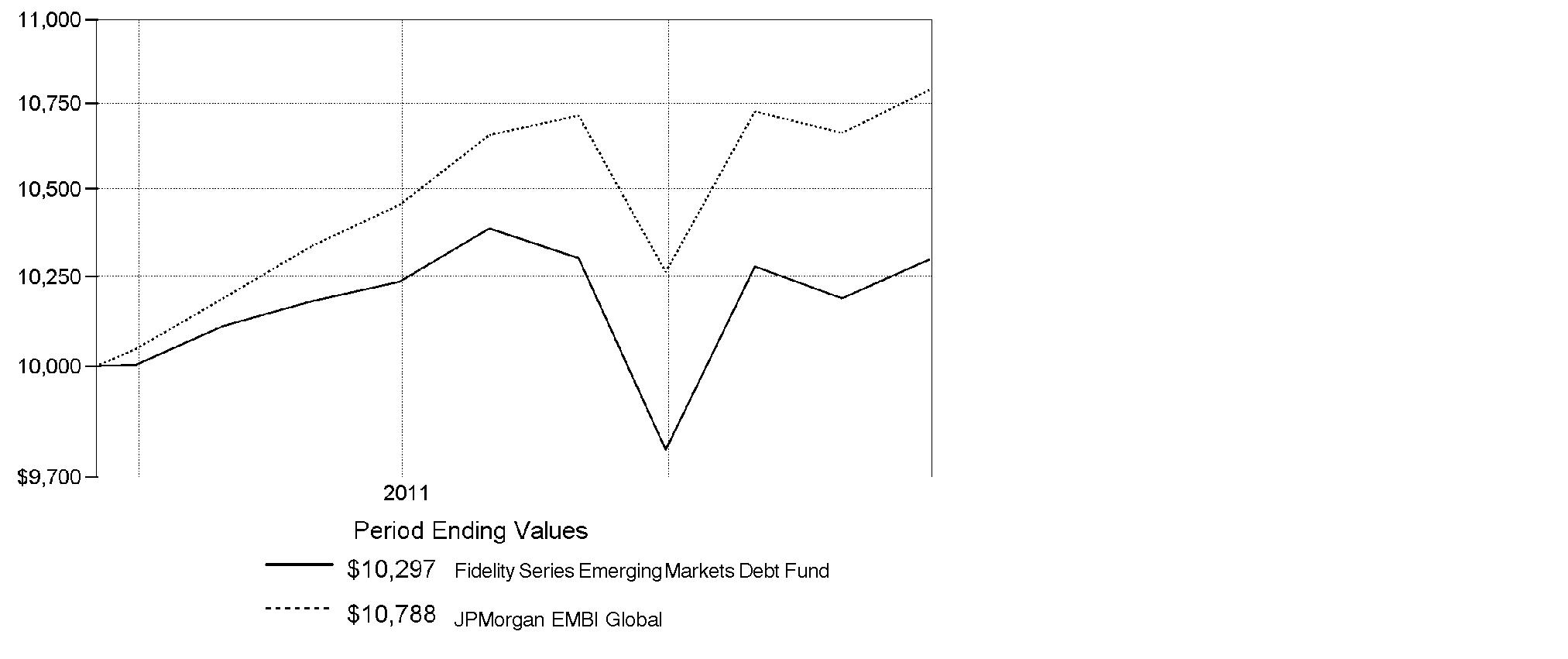

$10,000 Over Life of Fund

Let's say hypothetically that $10,000 was invested in Fidelity Series Emerging Markets Debt Fund on March 17, 2011, when the fund started. The chart shows how the value of your investment would have changed, and also shows how the JPMorgan Emerging Markets Bond Index Global (EMBI Global) performed over the same period.

Annual Report

Management's Discussion of Fund Performance

Market Recap: Emerging-markets debt made steady advances throughout the nine-month period ending December 31, 2011, beating many asset classes worldwide. The JPMorgan Emerging Markets Bond Index Global (EMBI Global) was up 7.37%, overcoming concern about the sovereign debt crisis in Europe to top most equity classes and other higher-risk fixed-income categories, such as U.S. high yield. A sharp decline in September threatened to dampen performance, but the trend was reversed the following month amid improved economic data and steady demand from yield-hungry investors. Looking at the more than 40 individual country components of the EMBI Global, Latin America produced many of the strongest performers. Venezuela led the way, advancing roughly 17%, despite political uncertainty stemming from the health of the nation's president. Mexico, the largest index constituent, gained roughly 12%, while Peru (+15%), Brazil (+13%) and Columbia (+12%) also fared well. Elsewhere, the Philippines and Indonesia advanced 11% and about 10%, respectively. The second-largest index component, Russia, saw a more muted gain, finishing up 3%, while Turkey, another sizable part of the index, posted a similar mark for the period. Only a few notable index components ended up in negative territory, with Argentina and the Ukraine each falling 8% and Hungary down 6%.

Comments from Jonathan Kelly, Portfolio Manager of Fidelity® Series Emerging Markets Debt Fund: From its inception on March 17, 2011, through December 31, 2011, the fund's Series Emerging Markets Debt and Class F shares trailed the EMBI Global. Cash consistently flowed into the fund, resulting in an elevated cash position, which, in a rising bond market, was the largest detractor. In terms of countries, the biggest detractor was an overweighting in Argentina, which lagged the index, although the negative impact was partially offset by strong security selection here. Positioning in Brazil, the Ukraine and Mexico also hurt. I increased the fund's stake in strong-performing Mexico during the period, but lower average exposure than the index detracted. I modestly increased my allocation to the Ukraine, moving to a bigger overweighting, but this hurt due to that market's poor performance. Security selection in China, Venezuela, Turkey and Russia had a negative impact on results. Conversely, contributors included a small out-of-index stake in U.S. Treasuries - used as a more liquid substitute for long-dated investment-grade sovereign debt - which I sold by period end, and underweightings in lagging Turkey, China, Egypt, Hungary and Poland. I increased our allocation to Venezuela during the period, and an average overweighting in this strong-performing country was beneficial.

The views expressed above reflect those of the portfolio manager(s) only through the end of the period as stated on the cover of this report and do not necessarily represent the views of Fidelity or any other person in the Fidelity organization. Any such views are subject to change at any time based upon market or other conditions and Fidelity disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a Fidelity fund are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any Fidelity fund.

Annual Report

Shareholder Expense Example

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, and (2) ongoing costs, including management fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (July 1, 2011 to December 31, 2011).

Actual Expenses

The first line of the accompanying table for each class of the Fund provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class of the Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table for each class of the Fund provides information about hypothetical account values and hypothetical expenses based on a Class' actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Class' actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. In addition, the Fund, as a shareholder in the underlying Fidelity Central Funds, will indirectly bear its pro-rata share of the fees and expenses incurred by the underlying Fidelity Central Funds. These fees and expenses are not included in the Fund's annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

Annual Report

Shareholder Expense Example - continued

|

|

Annualized |

Beginning |

Ending |

Expenses Paid |

|

Series Emerging Markets Debt |

.88% |

|

|

|

|

Actual |

|

$ 1,000.00 |

$ 1,006.10 |

$ 4.45 |

|

HypotheticalA |

|

$ 1,000.00 |

$ 1,020.77 |

$ 4.48 |

|

Class F |

.75% |

|

|

|

|

Actual |

|

$ 1,000.00 |

$ 1,006.70 |

$ 3.79 |

|

HypotheticalA |

|

$ 1,000.00 |

$ 1,021.42 |

$ 3.82 |

A 5% return per year before expenses

* Expenses are equal to each Class' annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period).

Annual Report

Investment Changes (Unaudited)

|

Top Five Countries as of December 31, 2011 |

||

|

(excluding cash equivalents) |

% of fund's |

% of fund's net assets |

|

Venezuela |

12.5 |

9.8 |

|

Argentina |

7.3 |

8.5 |

|

Turkey |

7.1 |

7.3 |

|

Mexico |

6.9 |

6.2 |

|

Russia |

6.8 |

7.0 |

|

Percentages are adjusted for the effect of open futures contracts, if applicable. |

|

Top Five Holdings as of December 31, 2011 |

||

|

(by issuer, excluding cash equivalents) |

% of fund's |

% of fund's net assets |

|

Venezuelan Republic |

6.7 |

5.2 |

|

Turkish Republic |

6.3 |

6.2 |

|

Russian Federation |

6.2 |

6.8 |

|

Petroleos de Venezuela SA |

5.8 |

4.6 |

|

Argentine Republic |

4.9 |

6.8 |

|

|

29.9 |

|

|

Asset Allocation (% of fund's net assets) |

|||||||

|

As of December 31, 2011 |

As of June 30, 2011 |

||||||

|

Corporate Bonds 29.9% |

|

|

Corporate Bonds 29.0% |

|

||

|

Government |

|

|

Government |

|

||

|

Supranational Obligations 0.0% |

|

|

Supranational Obligations 0.1% |

|

||

|

Preferred Securities 1.1% |

|

|

Preferred Securities 0.0% |

|

||

|

Other Investments 0.3% |

|

|

Other Investments 0.8% |

|

||

|

Short-Term |

|

|

Short-Term |

|

||

Annual Report

Investments December 31, 2011

Showing Percentage of Net Assets

|

Nonconvertible Bonds - 29.0% |

||||

|

|

Principal |

Value |

||

|

Argentina - 1.0% |

||||

|

Aeropuertos Argentina 2000 SA 10.75% 12/1/20 (d) |

|

$ 1,200,000 |

$ 1,248,000 |

|

|

Empresa Distribuidora y Comercializadora Norte SA 9.75% 10/25/22 (d) |

|

1,050,000 |

861,000 |

|

|

Pan American Energy LLC 7.875% 5/7/21 (d) |

|

2,130,000 |

2,183,250 |

|

|

Transportadora de Gas del Sur SA 7.875% 5/14/17 (d) |

|

4,425,000 |

4,048,875 |

|

|

YPF SA 10% 11/2/28 |

|

215,000 |

235,425 |

|

|

TOTAL ARGENTINA |

8,576,550 |

|||

|

Brazil - 1.8% |

||||

|

Banco Nacional de Desenvolvimento Economico e Social: |

|

|

|

|

|

5.5% 7/12/20 (d) |

|

1,300,000 |

1,410,500 |

|

|

6.5% 6/10/19 (d) |

|

1,360,000 |

1,550,400 |

|

|

BFF International Ltd. 7.25% 1/28/20 (d) |

|

1,825,000 |

2,012,063 |

|

|

Braskem Finance Ltd. 7% 5/7/20 (d) |

|

2,710,000 |

2,906,475 |

|

|

Companhia de Saneamento Basico do Estado de Sao Paulo (SABESP) 6.25% 12/16/20 (d) |

|

900,000 |

924,750 |

|

|

OGX Petroleo e Gas Participacoes SA 8.5% 6/1/18 (d) |

|

2,110,000 |

2,067,800 |

|

|

Rearden G Holdings Eins GmbH 7.875% 3/30/20 (d) |

|

2,040,000 |

2,024,700 |

|

|

Telemar Norte Leste SA 5.5% 10/23/20 (d) |

|

875,000 |

866,250 |

|

|

Votorantim Cimentos SA 7.25% 4/5/41 (d) |

|

1,000,000 |

970,000 |

|

|

TOTAL BRAZIL |

14,732,938 |

|||

|

British Virgin Islands - 0.3% |

||||

|

Arcos Dorados Holdings, Inc. 10.25% 7/13/16 (d) |

BRL |

4,437,000 |

2,440,922 |

|

|

Canada - 0.6% |

||||

|

Pacific Rubiales Energy Corp. 7.25% 12/12/21 (d) |

|

4,273,000 |

4,283,683 |

|

|

Sino-Forest Corp. 6.25% 10/21/17 (d) |

|

3,220,000 |

805,000 |

|

|

TOTAL CANADA |

5,088,683 |

|||

|

Cayman Islands - 1.3% |

||||

|

Fibria Overseas Finance Ltd. 7.5% 5/4/20 (d) |

|

1,250,000 |

1,215,625 |

|

|

Odebrecht Finance Ltd. 7.5% (d)(e) |

|

5,435,000 |

5,312,713 |

|

|

Petrobras International Finance Co. Ltd.: |

|

|

|

|

|

6.875% 1/20/40 |

|

1,485,000 |

1,692,900 |

|

|

8.375% 12/10/18 |

|

2,015,000 |

2,448,225 |

|

|

TOTAL CAYMAN ISLANDS |

10,669,463 |

|||

|

Chile - 0.1% |

||||

|

Automotores Gildemeister SA 8.25% 5/24/21 (d) |

|

1,070,000 |

1,091,400 |

|

|

Nonconvertible Bonds - continued |

||||

|

|

Principal |

Value |

||

|

Colombia - 0.2% |

||||

|

Emgesa SA ESP 8.75% 1/25/21 (d) |

COP |

$ 900,000,000 |

$ 501,419 |

|

|

Empresas Publicas de Medellin 8.375% 2/1/21 (d) |

COP |

1,296,000,000 |

705,998 |

|

|

TOTAL COLOMBIA |

1,207,417 |

|||

|

Dominican Republic - 0.0% |

||||

|

Cerveceria Nacional Dominicana C por A 16% 3/27/12 (d) |

|

220,000 |

178,926 |

|

|

Egypt - 0.1% |

||||

|

African Export-Import Bank 8.75% 11/13/14 |

|

1,125,000 |

1,206,563 |

|

|

El Salvador - 0.4% |

||||

|

Telemovil Finance Co. Ltd. 8% 10/1/17 (d) |

|

3,550,000 |

3,621,000 |

|

|

Georgia - 0.2% |

||||

|

Georgian Railway Ltd. 9.875% 7/22/15 |

|

1,300,000 |

1,293,500 |

|

|

Indonesia - 0.5% |

||||

|

Indo Energy Finance BV 7% 5/7/18 (d) |

|

1,100,000 |

1,100,000 |

|

|

PT Adaro Indonesia 7.625% 10/22/19 (d) |

|

800,000 |

876,000 |

|

|

PT Pertamina Persero: |

|

|

|

|

|

5.25% 5/23/21 (d) |

|

1,600,000 |

1,632,000 |

|

|

6.5% 5/27/41 (d) |

|

830,000 |

852,825 |

|

|

TOTAL INDONESIA |

4,460,825 |

|||

|

Ireland - 0.4% |

||||

|

SCF Capital Ltd. 5.375% 10/27/17 (d) |

|

1,000,000 |

860,000 |

|

|

VIP Finance Ireland Ltd. 7.748% 2/2/21 (d) |

|

1,375,000 |

1,172,188 |

|

|

Vnesheconombank Via VEB Finance PLC 6.8% 11/22/25 (d) |

|

1,069,000 |

1,034,258 |

|

|

TOTAL IRELAND |

3,066,446 |

|||

|

Kazakhstan - 0.7% |

||||

|

Development Bank of Kazakhstan JSC 5.5% 12/20/15 (d) |

|

1,650,000 |

1,625,250 |

|

|

Zhaikmunai Finance BV 10.5% 10/19/15 (d) |

|

4,075,000 |

3,952,750 |

|

|

TOTAL KAZAKHSTAN |

5,578,000 |

|||

|

Luxembourg - 2.8% |

||||

|

Alrosa Finance SA: |

|

|

|

|

|

(Reg. S) 8.875% 11/17/14 |

|

2,550,000 |

2,760,375 |

|

|

7.75% 11/3/20 (d) |

|

1,050,000 |

1,044,750 |

|

|

Aquarius Investments Luxemburg 8.25% 2/18/16 |

|

1,400,000 |

1,393,000 |

|

|

EVRAZ Group SA 8.25% 11/10/15 (d) |

|

2,875,000 |

2,889,375 |

|

|

Nonconvertible Bonds - continued |

||||

|

|

Principal |

Value |

||

|

Luxembourg - continued |

||||

|

MHP SA 10.25% 4/29/15 (d) |

|

$ 2,260,000 |

$ 2,011,400 |

|

|

RSHB Capital SA 6% 6/3/21 (d) |

|

1,005,000 |

879,375 |

|

|

Steel Capital SA Ln Partner Net Program 6.25% 7/26/16 (d) |

|

2,185,000 |

2,037,513 |

|

|

T2 Capital Finance Co. SA 6.95% 2/6/17 (Reg. S) (c) |

|

2,396,000 |

2,384,020 |

|

|

TMK Capital SA 7.75% 1/27/18 |

|

1,445,000 |

1,231,863 |

|

|

Vimpel Communications 8.25% 5/23/16 (Reg. S) (Issued by UBS Luxembourg SA for Vimpel Communications) |

|

6,175,000 |

6,144,125 |

|

|

TOTAL LUXEMBOURG |

22,775,796 |

|||

|

Mexico - 3.1% |

||||

|

Alestra SA de RL de CV 11.75% 8/11/14 |

|

3,445,000 |

3,806,725 |

|

|

Gruma SAB de CV 7.75% (Reg. S) (e) |

|

2,745,000 |

2,745,000 |

|

|

Kansas City Southern de Mexico SA de CV 12.5% 4/1/16 |

|

626,000 |

726,160 |

|

|

Petroleos Mexicanos: |

|

|

|

|

|

5.5% 1/21/21 |

|

2,950,000 |

3,208,125 |

|

|

6% 3/5/20 |

|

1,450,000 |

1,634,875 |

|

|

6.5% 6/2/41 |

|

1,250,000 |

1,406,250 |

|

|

6.5% 6/2/41 (d) |

|

1,165,000 |

1,304,800 |

|

|

6.625% (d)(e) |

|

7,605,000 |

7,643,025 |

|

|

8% 5/3/19 |

|

1,350,000 |

1,684,125 |

|

|

TV Azteca SA de CV 7.5% 5/25/18 (Reg. S) |

|

1,335,000 |

1,338,338 |

|

|

TOTAL MEXICO |

25,497,423 |

|||

|

Mongolia - 0.1% |

||||

|

Trade & Development Bank of Mongolia LLC 8.5% 10/25/13 |

|

1,000,000 |

950,000 |

|

|

Multi-National - 0.5% |

||||

|

Eastern and Southern African Trade and Development Bank 6.875% 1/9/16 (Reg. S) |

|

1,000,000 |

910,000 |

|

|

International Bank for Reconstruction & Development: |

|

|

|

|

|

8% 6/20/13 |

NGN |

114,000,000 |

647,615 |

|

|

8.2% 12/12/12 |

NGN |

480,000,000 |

2,794,824 |

|

|

TOTAL MULTI-NATIONAL |

4,352,439 |

|||

|

Netherlands - 3.4% |

||||

|

DTEK Finance BV 9.5% 4/28/15 (d) |

|

1,700,000 |

1,548,700 |

|

|

Nonconvertible Bonds - continued |

||||

|

|

Principal |

Value |

||

|

Netherlands - continued |

||||

|

HSBK (Europe) BV: |

|

|

|

|

|

7.25% 5/3/17 (d) |

|

$ 2,300,000 |

$ 2,225,250 |

|

|

9.25% 10/16/13 (d) |

|

3,120,000 |

3,260,400 |

|

|

Intergas Finance BV 6.375% 5/14/17 (Reg. S) |

|

900,000 |

909,000 |

|

|

KazMunaiGaz Finance Sub BV: |

|

|

|

|

|

6.375% 4/9/21 (d) |

|

1,500,000 |

1,500,000 |

|

|

7% 5/5/20 (d) |

|

1,985,000 |

2,084,250 |

|

|

8.375% 7/2/13 (d) |

|

1,750,000 |

1,839,250 |

|

|

9.125% 7/2/18 (d) |

|

2,275,000 |

2,621,938 |

|

|

11.75% 1/23/15 (d) |

|

2,175,000 |

2,544,750 |

|

|

Majapahit Holding BV: |

|

|

|

|

|

7.25% 6/28/17 (Reg. S) |

|

800,000 |

888,000 |

|

|

7.75% 1/20/20 (d) |

|

1,650,000 |

1,914,000 |

|

|

8% 8/7/19 (d) |

|

1,175,000 |

1,374,750 |

|

|

Metinvest BV 10.25% 5/20/15 (d) |

|

2,200,000 |

2,074,600 |

|

|

VimpelCom Holdings BV 7.5043% 3/1/22 (d) |

|

3,395,000 |

2,851,800 |

|

|

TOTAL NETHERLANDS |

27,636,688 |

|||

|

Pakistan - 0.5% |

||||

|

Pakistan Mobile Communications Ltd. 8.625% 11/13/13 (d) |

|

4,364,000 |

4,058,520 |

|

|

Paraguay - 0.3% |

||||

|

BBVA Paraguay SA 9.75% 2/11/16 (d) |

|

2,400,000 |

2,520,000 |

|

|

Philippines - 0.6% |

||||

|

Development Bank of Philippines 8.375% (e)(f) |

|

1,065,000 |

1,139,550 |

|

|

National Power Corp. 6.875% 11/2/16 (d) |

|

650,000 |

739,375 |

|

|

Power Sector Assets and Liabilities Management Corp.: |

|

|

|

|

|

7.25% 5/27/19 (d) |

|

1,100,000 |

1,325,500 |

|

|

7.39% 12/2/24 (d) |

|

1,300,000 |

1,579,500 |

|

|

TOTAL PHILIPPINES |

4,783,925 |

|||

|

Russia - 0.6% |

||||

|

MTS International Funding Ltd. 8.625% 6/22/20 (d) |

|

4,475,000 |

4,805,255 |

|

|

Trinidad & Tobago - 0.2% |

||||

|

Petroleum Co. of Trinidad & Tobago Ltd. (Reg. S) 6% 5/8/22 |

|

1,290,625 |

1,264,813 |

|

|

Turkey - 0.7% |

||||

|

Akbank T.A.S. 5.125% 7/22/15 (d) |

|

2,850,000 |

2,743,125 |

|

|

Nonconvertible Bonds - continued |

||||

|

|

Principal |

Value |

||

|

Turkey - continued |

||||

|

Turkiye Garanti Bankasi A/S 2.9092% 4/20/16 (d)(f) |

|

$ 1,395,000 |

$ 1,250,269 |

|

|

Turkiye Is Bankasi A/S 5.1% 2/1/16 (d) |

|

1,700,000 |

1,649,000 |

|

|

TOTAL TURKEY |

5,642,394 |

|||

|

United Kingdom - 1.1% |

||||

|

Afren PLC 11.5% 2/1/16 (d) |

|

1,050,000 |

1,029,000 |

|

|

Biz Finance PLC 8.375% 4/27/15 (Reg. S) |

|

3,175,000 |

2,746,375 |

|

|

The State Export-Import Bank of Ukraine JSC 5.7928% 2/9/16 (Issued by Credit Suisse First Boston International for The State Export-Import Bank of Ukraine JSC) (c) |

|

2,500,000 |

1,675,000 |

|

|

Vedanta Resources PLC: |

|

|

|

|

|

6.75% 6/7/16 (d) |

|

3,350,000 |

2,814,000 |

|

|

8.25% 6/7/21 (d) |

|

1,165,000 |

908,700 |

|

|

TOTAL UNITED KINGDOM |

9,173,075 |

|||

|

United States of America - 1.7% |

||||

|

Braskem America Finance Co. 7.125% 7/22/41 (d) |

|

1,060,000 |

1,028,200 |

|

|

NII Capital Corp.: |

|

|

|

|

|

7.625% 4/1/21 |

|

1,260,000 |

1,247,400 |

|

|

10% 8/15/16 |

|

1,050,000 |

1,191,750 |

|

|

Pemex Project Funding Master Trust: |

|

|

|

|

|

5.75% 3/1/18 |

|

2,855,000 |

3,119,088 |

|

|

6.625% 6/15/35 |

|

4,640,000 |

5,220,000 |

|

|

Southern Copper Corp. 6.75% 4/16/40 |

|

1,935,000 |

1,940,999 |

|

|

TOTAL UNITED STATES OF AMERICA |

13,747,437 |

|||

|

Venezuela - 5.8% |

||||

|

Petroleos de Venezuela SA: |

|

|

|

|

|

4.9% 10/28/14 |

|

12,075,000 |

9,448,688 |

|

|

5% 10/28/15 |

|

1,405,000 |

997,550 |

|

|

5.375% 4/12/27 |

|

10,085,000 |

4,916,438 |

|

|

5.5% 4/12/37 |

|

6,300,000 |

3,008,250 |

|

|

8% 11/17/13 |

|

2,685,000 |

2,544,038 |

|

|

8.5% 11/2/17 (d) |

|

24,595,000 |

18,569,225 |

|

|

12.75% 2/17/22 (d) |

|

9,715,000 |

8,136,313 |

|

|

TOTAL VENEZUELA |

47,620,502 |

|||

|

TOTAL NONCONVERTIBLE BONDS (Cost $242,793,556) |

|

|||

|

Government Obligations - 62.2% |

||||

|

|

Principal Amount (b) |

Value |

||

|

Argentina - 6.3% |

||||

|

Argentine Republic: |

|

|

|

|

|

discount (with partial capitalization through 12/31/13) 8.28% 12/31/33 |

|

$ 6,735,740 |

$ 4,900,251 |

|

|

2.5% 12/31/38 (c) |

|

4,000,000 |

1,410,000 |

|

|

7% 9/12/13 |

|

16,225,000 |

15,868,501 |

|

|

7% 10/3/15 |

|

20,205,000 |

18,479,718 |

|

|

City of Buenos Aires 12.5% 4/6/15 (d) |

|

6,880,000 |

7,241,200 |

|

|

Provincia de Cordoba 12.375% 8/17/17 (d) |

|

2,900,000 |

2,436,000 |

|

|

Provincia de Neuquen Argentina 7.875% 4/26/21 (d) |

|

1,295,000 |

1,307,950 |

|

|

TOTAL ARGENTINA |

51,643,620 |

|||

|

Bahamas (Nassau) - 0.3% |

||||

|

Bahamian Republic 6.95% 11/20/29 (d) |

|

1,945,000 |

2,178,400 |

|

|

Bahrain - 0.2% |

||||

|

Bahrain Kingdom 5.5% 3/31/20 |

|

1,350,000 |

1,275,750 |

|

|

Belarus - 1.1% |

||||

|

Belarus Republic: |

|

|

|

|

|

8.75% 8/3/15 (Reg. S) |

|

8,630,000 |

7,476,169 |

|

|

8.95% 1/26/18 |

|

2,025,000 |

1,741,500 |

|

|

TOTAL BELARUS |

9,217,669 |

|||

|

Bermuda - 0.1% |

||||

|

Bermuda Government 5.603% 7/20/20 (d) |

|

920,000 |

1,023,500 |

|

|

Brazil - 2.5% |

||||

|

Banco Nacional de Desenvolvimento Economico e Social 6.369% 6/16/18 (d) |

|

1,715,000 |

1,926,803 |

|

|

Brazilian Federative Republic: |

|

|

|

|

|

7.125% 1/20/37 |

|

2,295,000 |

3,172,838 |

|

|

8.25% 1/20/34 |

|

1,620,000 |

2,446,200 |

|

|

8.75% 2/4/25 |

|

1,075,000 |

1,604,438 |

|

|

8.875% 10/14/19 |

|

800,000 |

1,112,000 |

|

|

10.125% 5/15/27 |

|

3,695,000 |

6,152,175 |

|

|

12.25% 3/6/30 |

|

2,345,000 |

4,467,225 |

|

|

TOTAL BRAZIL |

20,881,679 |

|||

|

Colombia - 2.3% |

||||

|

Colombian Republic: |

|

|

|

|

|

4.375% 7/12/21 |

|

1,955,000 |

2,091,850 |

|

|

7.375% 1/27/17 |

|

1,495,000 |

1,823,900 |

|

|

7.375% 3/18/19 |

|

1,440,000 |

1,818,000 |

|

|

7.375% 9/18/37 |

|

3,250,000 |

4,550,000 |

|

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Colombia - continued |

||||

|

Colombian Republic: - continued |

|

|

|

|

|

10.375% 1/28/33 |

|

$ 3,570,000 |

$ 6,051,150 |

|

|

11.75% 2/25/20 |

|

1,450,000 |

2,283,750 |

|

|

TOTAL COLOMBIA |

18,618,650 |

|||

|

Congo - 0.4% |

||||

|

Congo Republic 3% 6/30/29 (c) |

|

4,409,900 |

3,131,029 |

|

|

Croatia - 1.1% |

||||

|

Croatia Republic: |

|

|

|

|

|

6.375% 3/24/21 (d) |

|

2,375,000 |

2,173,125 |

|

|

6.625% 7/14/20 (d) |

|

3,295,000 |

3,072,588 |

|

|

6.75% 11/5/19 (d) |

|

4,075,000 |

3,881,438 |

|

|

TOTAL CROATIA |

9,127,151 |

|||

|

Dominican Republic - 0.8% |

||||

|

Dominican Republic: |

|

|

|

|

|

1.5522% 8/30/24 (f) |

|

1,750,000 |

1,526,875 |

|

|

7.5% 5/6/21 (d) |

|

3,160,000 |

3,136,300 |

|

|

9.04% 1/23/18 (d) |

|

1,475,519 |

1,608,315 |

|

|

TOTAL DOMINICAN REPUBLIC |

6,271,490 |

|||

|

El Salvador - 0.6% |

||||

|

El Salvador Republic: |

|

|

|

|

|

7.375% 12/1/19 (d) |

|

1,100,000 |

1,188,000 |

|

|

7.625% 2/1/41 (d) |

|

1,200,000 |

1,200,000 |

|

|

7.65% 6/15/35 (Reg. S) |

|

1,275,000 |

1,300,500 |

|

|

7.75% 1/24/23 (Reg. S) |

|

700,000 |

759,500 |

|

|

8.25% 4/10/32 (Reg. S) |

|

800,000 |

868,000 |

|

|

TOTAL EL SALVADOR |

5,316,000 |

|||

|

Gabon - 0.2% |

||||

|

Gabonese Republic 8.2% 12/12/17 (d) |

|

1,650,000 |

1,889,250 |

|

|

Georgia - 0.5% |

||||

|

Georgia Republic 6.875% 4/12/21 (d) |

|

3,635,000 |

3,744,050 |

|

|

Ghana - 0.7% |

||||

|

Ghana Republic: |

|

|

|

|

|

8.5% 10/4/17 (d) |

|

1,450,000 |

1,573,250 |

|

|

14.25% 7/29/13 |

GHS |

1,600,000 |

971,605 |

|

|

14.99% 3/11/13 |

GHS |

2,775,000 |

1,703,930 |

|

|

15.65% 6/3/13 |

GHS |

2,000,000 |

1,238,421 |

|

|

TOTAL GHANA |

5,487,206 |

|||

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Hungary - 0.9% |

||||

|

Hungarian Republic: |

|

|

|

|

|

4.75% 2/3/15 |

|

$ 1,115,000 |

$ 1,014,650 |

|

|

6.25% 1/29/20 |

|

1,650,000 |

1,476,750 |

|

|

6.375% 3/29/21 |

|

2,896,000 |

2,577,440 |

|

|

7.625% 3/29/41 |

|

3,106,000 |

2,717,750 |

|

|

TOTAL HUNGARY |

7,786,590 |

|||

|

Indonesia - 3.6% |

||||

|

Indonesian Republic: |

|

|

|

|

|

4.875% 5/5/21 (d) |

|

2,955,000 |

3,161,850 |

|

|

5.875% 3/13/20 (d) |

|

3,425,000 |

3,878,813 |

|

|

6.625% 2/17/37 (d) |

|

2,550,000 |

3,091,875 |

|

|

6.875% 1/17/18 (d) |

|

2,300,000 |

2,708,250 |

|

|

7.75% 1/17/38 (d) |

|

3,925,000 |

5,308,563 |

|

|

8.5% 10/12/35 (Reg. S) |

|

3,675,000 |

5,301,188 |

|

|

11.625% 3/4/19 (d) |

|

4,025,000 |

5,946,938 |

|

|

TOTAL INDONESIA |

29,397,477 |

|||

|

Iraq - 0.8% |

||||

|

Republic of Iraq 5.8% 1/15/28 (Reg. S) |

|

7,675,000 |

6,293,500 |

|

|

Jordan - 0.1% |

||||

|

Jordanian Kingdom 3.875% 11/12/15 |

|

1,350,000 |

1,272,375 |

|

|

Lebanon - 0.8% |

||||

|

Lebanese Republic: |

|

|

|

|

|

4% 12/31/17 |

|

5,619,000 |

5,548,763 |

|

|

5.15% 11/12/18 |

|

1,050,000 |

1,039,500 |

|

|

TOTAL LEBANON |

6,588,263 |

|||

|

Lithuania - 0.9% |

||||

|

Lithuanian Republic: |

|

|

|

|

|

5.125% 9/14/17 (d) |

|

850,000 |

833,000 |

|

|

6.125% 3/9/21 (d) |

|

2,260,000 |

2,262,938 |

|

|

6.75% 1/15/15 (d) |

|

1,150,000 |

1,201,750 |

|

|

7.375% 2/11/20 (d) |

|

2,550,000 |

2,766,750 |

|

|

TOTAL LITHUANIA |

7,064,438 |

|||

|

Mexico - 3.8% |

||||

|

United Mexican States: |

|

|

|

|

|

5.125% 1/15/20 |

|

3,398,000 |

3,890,710 |

|

|

5.625% 1/15/17 |

|

2,182,000 |

2,503,845 |

|

|

5.75% 10/12/2110 |

|

2,704,000 |

2,879,760 |

|

|

5.95% 3/19/19 |

|

2,090,000 |

2,483,965 |

|

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Mexico - continued |

||||

|

United Mexican States: - continued |

|

|

|

|

|

6.05% 1/11/40 |

|

$ 6,056,000 |

$ 7,403,460 |

|

|

6.5% 6/10/21 |

MXN |

36,115,000 |

2,613,638 |

|

|

6.75% 9/27/34 |

|

4,350,000 |

5,687,625 |

|

|

7.5% 4/8/33 |

|

1,500,000 |

2,107,500 |

|

|

8.3% 8/15/31 |

|

1,160,000 |

1,737,100 |

|

|

TOTAL MEXICO |

31,307,603 |

|||

|

Namibia - 0.3% |

||||

|

Namibia Republic of 5.5% 11/3/21 (d) |

|

2,070,000 |

2,106,225 |

|

|

Nigeria - 0.3% |

||||

|

Republic of Nigeria 6.75% 1/28/21 (d) |

|

2,325,000 |

2,418,000 |

|

|

Pakistan - 0.5% |

||||

|

Islamic Republic of Pakistan 7.125% 3/31/16 (d) |

|

5,550,000 |

4,204,125 |

|

|

Peru - 1.6% |

||||

|

Peruvian Republic: |

|

|

|

|

|

3% 3/7/27 (c) |

|

2,950,000 |

2,537,000 |

|

|

5.625% 11/18/50 |

|

1,725,000 |

1,871,625 |

|

|

7.35% 7/21/25 |

|

1,500,000 |

1,991,250 |

|

|

8.75% 11/21/33 |

|

4,180,000 |

6,384,950 |

|

|

TOTAL PERU |

12,784,825 |

|||

|

Philippines - 2.5% |

||||

|

Philippine Republic: |

|

|

|

|

|

6.375% 1/15/32 |

|

1,000,000 |

1,183,800 |

|

|

6.5% 1/20/20 |

|

1,450,000 |

1,732,750 |

|

|

7.5% 9/25/24 |

|

890,000 |

1,130,300 |

|

|

7.75% 1/14/31 |

|

3,000,000 |

4,020,000 |

|

|

9.5% 2/2/30 |

|

3,945,000 |

6,060,704 |

|

|

9.875% 1/15/19 |

|

1,325,000 |

1,838,438 |

|

|

10.625% 3/16/25 |

|

3,085,000 |

4,858,875 |

|

|

TOTAL PHILIPPINES |

20,824,867 |

|||

|

Poland - 0.8% |

||||

|

Polish Government: |

|

|

|

|

|

3.875% 7/16/15 |

|

850,000 |

858,500 |

|

|

5.125% 4/21/21 |

|

1,170,000 |

1,188,954 |

|

|

6.375% 7/15/19 |

|

4,125,000 |

4,578,750 |

|

|

TOTAL POLAND |

6,626,204 |

|||

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Qatar - 0.5% |

||||

|

State of Qatar: |

|

|

|

|

|

3.125% 1/20/17 (d) |

|

$ 1,980,000 |

$ 1,999,800 |

|

|

5.75% 1/20/42 (d) |

|

1,640,000 |

1,771,200 |

|

|

TOTAL QATAR |

3,771,000 |

|||

|

Russia - 6.2% |

||||

|

Russian Federation: |

|

|

|

|

|

3.625% 4/29/15 (d) |

|

1,600,000 |

1,612,800 |

|

|

7.5% 3/31/30 (Reg. S) |

|

31,542,125 |

36,629,854 |

|

|

11% 7/24/18 (Reg. S) |

|

2,080,000 |

2,839,200 |

|

|

12.75% 6/24/28 (Reg. S) |

|

5,575,000 |

9,505,375 |

|

|

TOTAL RUSSIA |

50,587,229 |

|||

|

Senegal - 0.1% |

||||

|

Republic of Senegal 8.75% 5/13/21 (d) |

|

825,000 |

816,750 |

|

|

Serbia - 1.7% |

||||

|

Republic of Serbia 6.75% 11/1/24 (d) |

|

14,846,002 |

13,955,242 |

|

|

Sri Lanka - 1.1% |

||||

|

Democratic Socialist Republic of Sri Lanka: |

|

|

|

|

|

6.25% 10/4/20 (d) |

|

3,980,000 |

3,970,050 |

|

|

6.25% 7/27/21 (d) |

|

1,970,000 |

1,955,225 |

|

|

7.4% 1/22/15 (d) |

|

2,900,000 |

3,001,500 |

|

|

TOTAL SRI LANKA |

8,926,775 |

|||

|

Turkey - 6.4% |

||||

|

Export Credit Bank of Turkey 5.375% 11/4/16 (d) |

|

1,175,000 |

1,157,375 |

|

|

Turkish Republic: |

|

|

|

|

|

0% 2/20/13 |

TRY |

5,480,000 |

2,573,129 |

|

|

5.125% 3/25/22 |

|

1,565,000 |

1,494,575 |

|

|

5.625% 3/30/21 |

|

2,600,000 |

2,619,500 |

|

|

6% 1/14/41 |

|

1,250,000 |

1,179,750 |

|

|

6.75% 4/3/18 |

|

3,500,000 |

3,815,000 |

|

|

6.75% 5/30/40 |

|

3,200,000 |

3,296,000 |

|

|

6.875% 3/17/36 |

|

6,650,000 |

6,916,000 |

|

|

7% 9/26/16 |

|

2,800,000 |

3,074,400 |

|

|

7.25% 3/15/15 |

|

2,100,000 |

2,285,850 |

|

|

7.25% 3/5/38 |

|

3,825,000 |

4,169,250 |

|

|

7.375% 2/5/25 |

|

6,500,000 |

7,337,200 |

|

|

7.5% 7/14/17 |

|

3,900,000 |

4,392,570 |

|

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Turkey - continued |

||||

|

Turkish Republic: - continued |

|

|

|

|

|

7.5% 11/7/19 |

|

$ 2,900,000 |

$ 3,295,270 |

|

|

11.875% 1/15/30 |

|

2,950,000 |

4,808,500 |

|

|

TOTAL TURKEY |

52,414,369 |

|||

|

Ukraine - 3.7% |

||||

|

Ukraine Financing of Infrastructure Projects State Enterprise 8.375% 11/3/17 (d) |

|

3,650,000 |

3,029,500 |

|

|

Ukraine Government: |

|

|

|

|

|

6.25% 6/17/16 (d) |

|

3,865,000 |

3,381,875 |

|

|

6.385% 6/26/12 (d) |

|

10,890,000 |

10,781,100 |

|

|

6.75% 11/14/17 (d) |

|

2,675,000 |

2,300,500 |

|

|

6.875% 9/23/15 (d) |

|

3,150,000 |

2,827,125 |

|

|

7.65% 6/11/13 (d) |

|

5,630,000 |

5,412,119 |

|

|

7.75% 9/23/20 (d) |

|

1,550,000 |

1,340,750 |

|

|

7.95% 2/23/21 (d) |

|

1,700,000 |

1,491,750 |

|

|

TOTAL UKRAINE |

30,564,719 |

|||

|

United Arab Emirates - 0.1% |

||||

|

United Arab Emirates 7.75% 10/5/20 (Reg. S) |

|

1,190,000 |

1,255,450 |

|

|

Uruguay - 0.8% |

||||

|

Uruguay Republic: |

|

|

|

|

|

7.875% 1/15/33 pay-in-kind |

|

2,150,000 |

3,004,625 |

|

|

8% 11/18/22 |

|

2,756,250 |

3,769,172 |

|

|

TOTAL URUGUAY |

6,773,797 |

|||

|

Venezuela - 6.7% |

||||

|

Venezuelan Republic: |

|

|

|

|

|

oil recovery rights 4/15/20 (g) |

|

48,200 |

1,313,450 |

|

|

6% 12/9/20 |

|

2,330,000 |

1,421,300 |

|

|

7% 3/31/38 |

|

2,000,000 |

1,155,000 |

|

|

7.75% 10/13/19 (Reg. S) |

|

4,375,000 |

3,128,125 |

|

|

8.5% 10/8/14 |

|

2,700,000 |

2,511,000 |

|

|

9% 5/7/23 (Reg. S) |

|

10,025,000 |

7,067,625 |

|

|

9.25% 9/15/27 |

|

7,100,000 |

5,112,000 |

|

|

9.25% 5/7/28 (Reg. S) |

|

4,215,000 |

2,918,888 |

|

|

9.375% 1/13/34 |

|

3,630,000 |

2,495,625 |

|

|

10.75% 9/19/13 |

|

4,250,000 |

4,292,500 |

|

|

11.75% 10/21/26 (Reg. S) |

|

4,435,000 |

3,669,963 |

|

|

11.95% 8/5/31 (Reg. S) |

|

8,740,000 |

7,166,800 |

|

|

Government Obligations - continued |

||||

|

|

Principal Amount (b) |

Value |

||

|

Venezuela - continued |

||||

|

Venezuelan Republic: - continued |

|

|

|

|

|

12.75% 8/23/22 |

|

$ 11,950,000 |

$ 10,784,875 |

|

|

13.625% 8/15/18 |

|

2,415,000 |

2,366,700 |

|

|

TOTAL VENEZUELA |

55,403,851 |

|||

|

Vietnam - 0.9% |

||||

|

Vietnamese Socialist Republic: |

|

|

|

|

|

1.3258% 3/12/16 (f) |

|

423,391 |

359,883 |

|

|

4% 3/12/28 (c) |

|

2,050,000 |

1,681,000 |

|

|

6.75% 1/29/20 (d) |

|

950,000 |

954,750 |

|

|

6.875% 1/15/16 (d) |

|

4,305,000 |

4,434,150 |

|

|

TOTAL VIETNAM |

7,429,783 |

|||

|

TOTAL GOVERNMENT OBLIGATIONS (Cost $512,874,027) |

|

|||

|

Sovereign Loan Participations - 0.3% |

||||

|

|

||||

|

Indonesia - 0.3% |

||||

|

Indonesian Republic loan participation Goldman Sachs 1.25% 12/14/19 (f) |

|

2,791,111 |

|

|

|

Preferred Securities - 1.1% |

|||

|

|

|

|

|

|

Brazil - 0.6% |

|||

|

Globo Comunicacoes e Participacoes SA 6.25% (c)(d)(e) |

4,850,000 |

5,157,870 |

|

|

Cayman Islands - 0.5% |

|||

|

CSN Islands XII Corp. 7% (Reg. S) (e) |

4,150,000 |

3,990,385 |

|

|

TOTAL PREFERRED SECURITIES (Cost $9,178,090) |

|

||

|

Money Market Funds - 5.9% |

|||

|

Shares |

Value |

||

|

Fidelity Cash Central Fund, 0.11% (a) |

48,994,734 |

$ 48,994,734 |

|

|

TOTAL INVESTMENT PORTFOLIO - 98.5% (Cost $816,498,560) |

809,186,434 |

||

|

NET OTHER ASSETS (LIABILITIES) - 1.5% |

12,029,083 |

||

|

NET ASSETS - 100% |

$ 821,215,517 |

||

|

Currency Abbreviations |

||

|

BRL |

- |

Brazilian real |

|

COP |

- |

Colombian peso |

|

GHS |

- |

Ghana Cedi |

|

MXN |

- |

Mexican peso |

|

NGN |

- |

Nigerian naira |

|

TRY |

- |

New Turkish Lira |

|

Legend |

|

(a) Affiliated fund that is available only to investment companies and other accounts managed by Fidelity Investments. The rate quoted is the annualized seven-day yield of the fund at period end. A complete unaudited listing of the fund's holdings as of its most recent quarter end is available upon request. In addition, each Fidelity Central Fund's financial statements, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC's website or upon request. |

|

(b) Principal amount is stated in United States dollars unless otherwise noted. |

|

(c) Security initially issued at one coupon which converts to a higher coupon at a specified date. The rate shown is the rate at period end. |

|

(d) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $303,962,605 or 37.0% of net assets. |

|

(e) Security is perpetual in nature with no stated maturity date. |

|

(f) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end. |

|

(g) Quantity represents share amount. |

|

Affiliated Central Funds |

|

Information regarding fiscal year to date income earned by the Fund from investments in Fidelity Central Funds is as follows: |

|

Fund |

Income earned |

|

Fidelity Cash Central Fund |

$ 49,597 |

|

Other Information |

|

The following is a summary of the inputs used, as of December 31, 2011, involving the Fund's assets and liabilities carried at fair value. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the tables below, please refer to the Security Valuation section in the accompanying Notes to Financial Statements. |

|

Valuation Inputs at Reporting Date: |

||||

|

Description |

Total |

Level 1 |

Level 2 |

Level 3 |

|

Investments in Securities: |

||||

|

Corporate Bonds |

$ 238,040,900 |

$ - |

$ 235,246,076 |

$ 2,794,824 |

|

Government Obligations |

510,378,901 |

- |

506,168,568 |

4,210,333 |

|

Sovereign Loan Participations |

2,623,644 |

- |

- |

2,623,644 |

|

Preferred Securities |

9,148,255 |

- |

9,148,255 |

- |

|

Money Market Funds |

48,994,734 |

48,994,734 |

- |

- |

|

Total Investments in Securities: |

$ 809,186,434 |

$ 48,994,734 |

$ 750,562,899 |

$ 9,628,801 |

|

The following is a reconciliation of Investments in Securities for which Level 3 inputs were used in determining value: |

|

Investments in Securities: |

|

|

Corporate Bonds |

|

|

Beginning Balance |

$ - |

|

Total Realized Gain (Loss) |

- |

|

Total Unrealized Gain (Loss) |

(286,880) |

|

Cost of Purchases |

3,078,589 |

|

Proceeds of Sales |

- |

|

Amortization/Accretion |

3,115 |

|

Transfers in to Level 3 |

- |

|

Transfers out of Level 3 |

- |

|

Ending Balance |

$ 2,794,824 |

|

The change in unrealized gain (loss) for the period attributable to Level 3 securities held at December 31, 2011 |

$ (286,880) |

|

Government Obligations |

|

|

Beginning Balance |

$ - |

|

Total Realized Gain (Loss) |

1,491 |

|

Total Unrealized Gain (Loss) |

(26,987) |

|

Cost of Purchases |

4,258,592 |

|

Proceeds of Sales |

(32,609) |

|

Amortization/Accretion |

9,846 |

|

Transfers in to Level 3 |

- |

|

Transfers out of Level 3 |

- |

|

Ending Balance |

$ 4,210,333 |

|

The change in unrealized gain (loss) for the period attributable to Level 3 securities held at December 31, 2011 |

$ (26,987) |

|

Investments in Securities: - continued |

|

|

Sovereign Loan Participations |

|

|

Beginning Balance |

$ - |

|

Total Realized Gain (Loss) |

12,479 |

|

Total Unrealized Gain (Loss) |

(34,984) |

|

Cost of Purchases |

2,896,299 |

|

Proceeds of Sales |

(259,074) |

|

Amortization/Accretion |

8,924 |

|

Transfers in to Level 3 |

- |

|

Transfers out of Level 3 |

- |

|

Ending Balance |

$ 2,623,644 |

|

The change in unrealized gain (loss) for the period attributable to Level 3 securities held at December 31, 2011 |

$ (34,984) |

|

The information used in the above reconciliation represents fiscal year to date activity for any Investments in Securities identified as using Level 3 inputs at either the beginning or the end of the current fiscal period. Transfers in or out of Level 3 represent the beginning value of any Security or Instrument where a change in the pricing level occurred from the beginning to the end of the period. The cost of purchases and the proceeds of sales may include securities received or delivered through corporate actions or exchanges. Realized and unrealized gains (losses) disclosed in the reconciliations are included in Net Gain (Loss) on the Fund's Statement of Operations. |

|

The composition of credit quality ratings as a percentage of net assets is as follows (Unaudited): |

|

AAA,AA,A |

2.6% |

|

BBB |

27.4% |

|

BB |

25.8% |

|

B |

26.2% |

|

Not Rated |

10.6% |

|

Short-Term Investments and Net Other Assets |

7.4% |

|

|

100.0% |

|

We have used ratings from Moody's Investors Service, Inc. Where Moody's® ratings are not available, we have used S&P® ratings. All ratings are as of the date indicated and do not reflect subsequent changes. |

See accompanying notes which are an integral part of the financial statements.

Annual Report

Financial Statements

Statement of Assets and Liabilities

|

|

December 31, 2011 |

|

|

|

|

|

|

Assets |

|

|

|

Investment in securities, at value - See accompanying schedule: Unaffiliated issuers (cost $767,503,826) |

$ 760,191,700 |

|

|

Fidelity Central Funds (cost $48,994,734) |

48,994,734 |

|

|

Total Investments (cost $816,498,560) |

|

$ 809,186,434 |

|

Cash |

|

1,050,153 |

|

Receivable for investments sold |

|

468,250 |

|

Receivable for fund shares sold |

|

96,468 |

|

Interest receivable |

|

15,012,489 |

|

Distributions receivable from Fidelity Central Funds |

|

4,659 |

|

Prepaid expenses |

|

1,670 |

|

Total assets |

|

825,820,123 |

|

|

|

|

|

Liabilities |

|

|

|

Payable for investments purchased |

$ 1,120,017 |

|

|

Payable for fund shares redeemed |

2,788,477 |

|

|

Accrued management fee |

454,497 |

|

|

Other affiliated payables |

93,068 |

|

|

Other payables and accrued expenses |

148,547 |

|

|

Total liabilities |

|

4,604,606 |

|

|

|

|

|

Net Assets |

|

$ 821,215,517 |

|

Net Assets consist of: |

|

|

|

Paid in capital |

|

$ 827,034,315 |

|

Undistributed net investment income |

|

1,476,968 |

|

Accumulated undistributed net realized gain (loss) on investments and foreign currency transactions |

|

23,895 |

|

Net unrealized appreciation (depreciation) on investments and assets and liabilities in foreign currencies |

|

(7,319,661) |

|

Net Assets |

|

$ 821,215,517 |

|

|

|

|

|

Series Emerging Markets Debt: |

|

$ 9.92 |

|

|

|

|

|

Class F: |

|

$ 9.92 |

See accompanying notes which are an integral part of the financial statements.

Annual Report

Statement of Operations

|

|

For the period March 17, 2011 |

|

|

|

|

|

|

Investment Income |

|

|

|

Dividends |

|

$ 324,491 |

|

Interest |

|

24,337,525 |

|

Income from Fidelity Central Funds |

|

49,597 |

|

Total income |

|

24,711,613 |

|

|

|

|

|

Expenses |

|

|

|

Management fee |

$ 2,610,398 |

|

|

Transfer agent fees |

383,915 |

|

|

Accounting fees and expenses |

193,240 |

|

|

Custodian fees and expenses |

39,249 |

|

|

Independent trustees' compensation |

2,022 |

|

|

Registration fees |

94,635 |

|

|

Audit |

52,409 |

|

|

Legal |

737 |

|

|

Miscellaneous |

1,525 |

|

|

Total expenses before reductions |

3,378,130 |

|

|

Expense reductions |

(142) |

3,377,988 |

|

Net investment income (loss) |

|

21,333,625 |

|

Realized and Unrealized Gain (Loss) Net realized gain (loss) on: |

|

|

|

Investment securities: |

|

|

|

Unaffiliated issuers |

457,314 |

|

|

Foreign currency transactions |

(9,045) |

|

|

Total net realized gain (loss) |

|

448,269 |

|

Change in net unrealized appreciation (depreciation) on: Investment securities |

(7,312,126) |

|

|

Assets and liabilities in foreign currencies |

(7,535) |

|

|

Total change in net unrealized appreciation (depreciation) |

|

(7,319,661) |

|

Net gain (loss) |

|

(6,871,392) |

|

Net increase (decrease) in net assets resulting from operations |

|

$ 14,462,233 |

See accompanying notes which are an integral part of the financial statements.

Annual Report

Financial Statements - continued

Statement of Changes in Net Assets

|

|

For the period |

|

Increase (Decrease) in Net Assets |

|

|

Operations |

|

|

Net investment income (loss) |

$ 21,333,625 |

|

Net realized gain (loss) |

448,269 |

|

Change in net unrealized appreciation (depreciation) |

(7,319,661) |

|

Net increase (decrease) in net assets resulting from operations |

14,462,233 |

|

Distributions to shareholders from net investment income |

(19,621,485) |

|

Distributions to shareholders from net realized gain |

(659,545) |

|

Total distributions |

(20,281,030) |

|

Share transactions - net increase (decrease) |

827,034,314 |

|

Total increase (decrease) in net assets |

821,215,517 |

|

|

|

|

Net Assets |

|

|

Beginning of period |

- |

|

End of period (including undistributed net investment income of $1,476,968) |

$ 821,215,517 |

See accompanying notes which are an integral part of the financial statements.

Annual Report

Financial Highlights - Series Emerging Markets Debt

|

Years ended December 31, |

2011G |

|

Selected Per-Share Data |

|

|

Net asset value, beginning of period |

$ 10.00 |

|

Income from Investment Operations |

|

|

Net investment income (loss)D |

.420 |

|

Net realized and unrealized gain (loss) |

(.127) |

|

Total from investment operations |

.293 |

|

Distributions from net investment income |

(.365) |

|

Distributions from net realized gain |

(.008) |

|

Total distributions |

(.373) |

|

Net asset value, end of period |

$ 9.92 |

|

Total ReturnB,C |

2.97% |

|

Ratios to Average Net AssetsE,H |

|

|

Expenses before reductions |

.90%A |

|

Expenses net of fee waivers, if any |

.90%A |

|

Expenses net of all reductions |

.90%A |

|

Net investment income (loss) |

5.37%A |

|

Supplemental Data |

|

|

Net assets, end of period (000 omitted) |

$ 567,740 |

|

Portfolio turnover rateF |

45%A |

A Annualized

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Calculated based on average shares outstanding during the period.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

F Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

G For the period March 17, 2011 (commencement of operations) to December 31, 2011.

H Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expense ratios before reductions for start-up periods may not be representative of longer-term operating periods. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

See accompanying notes which are an integral part of the financial statements.

Annual Report

Financial Highlights - Class F

|

Years ended December 31, |

2011G |

|

Selected Per-Share Data |

|

|

Net asset value, beginning of period |

$ 10.00 |

|

Income from Investment Operations |

|

|

Net investment income (loss)D |

.430 |

|

Net realized and unrealized gain (loss) |

(.126) |

|

Total from investment operations |

.304 |

|

Distributions from net investment income |

(.376) |

|

Distributions from net realized gain |

(.008) |

|

Total distributions |

(.384) |

|

Net asset value, end of period |

$ 9.92 |

|

Total ReturnB,C |

3.08% |

|

Ratios to Average Net AssetsE,H |

|

|

Expenses before reductions |

.76%A |

|

Expenses net of fee waivers, if any |

.76%A |

|

Expenses net of all reductions |

.76%A |

|

Net investment income (loss) |

5.51%A |

|

Supplemental Data |

|

|

Net assets, end of period (000 omitted) |

$ 253,475 |

|

Portfolio turnover rateF |

45%A |

A Annualized

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Calculated based on average shares outstanding during the period.

E Fees and expenses of any underlying Fidelity Central Funds are not included in the Fund's expense ratio. The Fund indirectly bears its proportionate share of the expenses of any underlying Fidelity Central Funds.

F Amount does not include the portfolio activity of any underlying Fidelity Central Funds.

G For the period March 17, 2011 (commencement of operations) to December 31, 2011.

H Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed by the investment adviser or reductions from expense offset arrangements and do not represent the amount paid by the class during periods when reimbursements or reductions occur. Expense ratios before reductions for start-up periods may not be representative of longer-term operating periods. Expenses net of fee waivers reflect expenses after reimbursement by the investment adviser but prior to reductions from expense offset arrangements. Expenses net of all reductions represent the net expenses paid by the class.

See accompanying notes which are an integral part of the financial statements.

Annual Report

Notes to Financial Statements

For the period ended December 31, 2011

1. Organization.

Fidelity Series Emerging Markets Debt Fund (the Fund) is a non-diversified fund of Fidelity Hastings Street Trust (the Trust) and is authorized to issue an unlimited number of shares. Shares of the Fund are only available for purchase by mutual funds for which Fidelity Management & Research Company (FMR) or an affiliate serves as an investment manager. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Massachusetts business trust. The Fund offers Series Emerging Markets Debt and Class F shares, each of which has equal rights as to assets and voting privileges. Each class has exclusive voting rights with respect to matters that affect that class. Investment income, realized and unrealized capital gains and losses, the common expenses of the Fund, and certain fund-level expense reductions, if any, are allocated on a pro-rata basis to each class based on the relative net assets of each class to the total net assets of the Fund. Each class differs with respect to transfer agent fees incurred. Certain expense reductions may also differ by class.

2. Investments in Fidelity Central Funds.

The Fund invests in Fidelity Central Funds, which are open-end investment companies available only to other investment companies and accounts managed by FMR and its affiliates. The Fund's Schedule of Investments lists each of the Fidelity Central Funds held as of period end, if any, as an investment of the Fund, but do not include the underlying holdings of each Fidelity Central Fund. As an Investing Fund, the Fund indirectly bears its proportionate share of the expenses of the underlying Fidelity Central Funds.

The Money Market Central Funds seek preservation of capital and current income and are managed by Fidelity Investments Money Management, Inc. (FIMM), an affiliate of FMR.

A complete unaudited list of holdings for each Fidelity Central Fund is available upon request or at the Securities and Exchange Commission (the SEC) web site at www.sec.gov. In addition, the financial statements of the Fidelity Central Funds, which are not covered by the Fund's Report of Independent Registered Public Accounting Firm, are available on the SEC web site or upon request.

3. Significant Accounting Policies.

The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of

Annual Report

3. Significant Accounting Policies - continued

the financial statements. The following summarizes the significant accounting policies of the Fund:

Security Valuation. Investments are valued as of 4:00 p.m. Eastern time on the last calendar day of the period. The Fund uses independent pricing services approved by the Board of Trustees to value its investments. When current market prices or quotations are not readily available or reliable, valuations may be determined in good faith in accordance with procedures adopted by the Board of Trustees. Factors used in determining value may include market or security specific events, changes in interest rates and credit quality. The frequency with which these procedures are used cannot be predicted and they may be utilized to a significant extent. The value used for net asset value (NAV) calculation under these procedures may differ from published prices for the same securities.

The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

Level 1 - quoted prices in active markets for identical investments

Level 2 - other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

Level 3 - unobservable inputs (including the Fund's own assumptions based on the best information available)

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. The aggregate value of investments by input level, as of December 31, 2011 for the Fund's investments, as well as a roll forward of Level 3 securities, is included at the end of the Fund's Schedule of Investments. Valuation techniques used to value the Fund's investments by major category are as follows:

Debt securities, including restricted securities, are valued based on evaluated prices received from independent pricing services or from dealers who make markets in such securities. For corporate bonds, foreign government and government agency obligations, preferred securities and sovereign loan participations, pricing services utilize matrix pricing which considers yield or price of bonds of comparable quality, coupon, maturity and type as well as dealer supplied prices and are generally categorized as Level 2 in the hierarchy. When independent prices are unavailable or unreliable, debt securities may be valued utilizing pricing matrices which consider similar factors that would be used by independent pricing services. These are generally categorized as Level 2 in the hierarchy but may be Level 3 depending on the circumstances. The Fund invests a significant portion of its assets in below investment grade securities. The value of these securities

Annual Report

Notes to Financial Statements - continued

3. Significant Accounting Policies - continued

Security Valuation - continued

can be more volatile due to changes in the credit quality of the issuer and is sensitive to changes in economic, market and regulatory conditions.

Investments in open-end mutual funds, including the Fidelity Central Funds, are valued at their closing net asset value each business day and are categorized as Level 1 in the hierarchy.

New Accounting Pronouncements. In May 2011, the Financial Accounting Standards Board issued Accounting Standard Update No. 2011-04, Fair Value Measurement (Topic 820) - Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs. The update is effective during interim and annual periods beginning after December 15, 2011 and will result in additional disclosure for transfers between levels as well as expanded disclosure for securities categorized as Level 3 under the fair value hierarchy.

In December 2011, the Financial Accounting Standards Board issued Accounting Standard Update No. 2011-11, Disclosures about Offsetting Assets and Liabilities. The update creates new disclosure requirements requiring entities to disclose both gross and net information for derivatives and other financial instruments that are either offset in the Statement of Assets and Liabilities or subject to an enforceable master netting arrangement or similar agreement. The disclosure requirements are effective for annual reporting periods beginning on or after January 1, 2013. Management is currently evaluating the impact of the update's adoption on the Fund's financial statement disclosures.

Foreign Currency. The Fund may use foreign currency contracts to facilitate transactions in foreign-denominated securities. Gains and losses from these transactions may arise from changes in the value of the foreign currency or if the counterparties do not perform under the contracts' terms.

Foreign-denominated assets, including investment securities, and liabilities are translated into U.S. dollars at the exchange rate at period end. Purchases and sales of investment securities, income and dividends received and expenses denominated in foreign currencies are translated into U.S. dollars at the exchange rate in effect on the transaction date.

The effects of exchange rate fluctuations on investments are included with the net realized and unrealized gain (loss) on investment securities. Other foreign currency transactions resulting in realized and unrealized gain (loss) are disclosed separately.

Annual Report

3. Significant Accounting Policies - continued

Investment Transactions and Income. For financial reporting purposes, the Fund's investment holdings and NAV include trades executed through the end of the last business day of the period. The NAV per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time and includes trades executed through the end of the prior business day. Gains and losses on securities sold are determined on the basis of identified cost. Dividend income is recorded on the ex-dividend date, except for certain dividends from foreign securities where the ex-dividend date may have passed, which are recorded as soon as the Fund is informed of the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of the securities received. Interest income and distributions from the Fidelity Central Funds are accrued as earned. Interest income includes coupon interest and amortization of premium and accretion of discount on debt securities. Investment income is recorded net of foreign taxes withheld where recovery of such taxes is uncertain.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.