As filed with the Securities and Exchange Commission on August 23, 2021

Registration No. 333-257786

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-14

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| Pre-Effective Amendment No. | ☐ | |||

| Post-Effective Amendment No. 1 | ☒ |

Fidelity Select Portfolios

(Exact Name of Registrant as Specified in Charter)

Registrant’s Telephone Number (617) 563-7000

245 Summer St., Boston, MA 02210

(Address Of Principal Executive Offices)

Cynthia Lo Bessette, Secretary

245 Summer Street

Boston, MA 02210

(Name and Address of Agent for Service)

It is proposed that this filing will become effective immediately upon filing pursuant to paragraph (b).

AIR TRANSPORTATION PORTFOLIO

COMMUNICATIONS EQUIPMENT PORTFOLIO

ENERGY SERVICE PORTFOLIO

NATURAL GAS PORTFOLIO

SERIES OF

FIDELITY® SELECT PORTFOLIOS®

245 SUMMER STREET, BOSTON, MASSACHUSETTS 02210

1-800-544-8544

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To the Shareholders of the above funds:

NOTICE IS HEREBY GIVEN that a Special Meeting of Shareholders (the Meeting) of Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio and Natural Gas Portfolio will be held on October 20, 2021 at 8:00 a.m. Eastern Time (ET).

Shareholders of Computers Portfolio and Consumer Finance Portfolio will also participate in the Meeting to vote on certain other proposals that are included in a notice and proxy statement mailed separately to them.

The purpose of the Meeting is to consider and act upon the following proposals, and to transact such other business as may properly come before the Meeting or any adjournments thereof. In light of public health concerns regarding COVID-19, the Meeting will be held in a virtual format only. The Meeting will be accessible solely by means of remote audio communication. You will not be able to attend the meeting in person.

| (1) | To approve an Agreement and Plan of Reorganization providing for the transfer of all of the assets of Air Transportation Portfolio to Transportation Portfolio in exchange solely for shares of beneficial interest of Transportation Portfolio and the assumption by Transportation Portfolio of Air Transportation Portfolio’s liabilities, in complete liquidation of Air Transportation Portfolio. |

| (2) | To approve an Agreement and Plan of Reorganization providing for the transfer of all of the assets of Communications Equipment Portfolio to Computers Portfolio in exchange solely for shares of beneficial interest of Computers Portfolio and the assumption by Computers Portfolio of Communications Equipment Portfolio’s liabilities, in complete liquidation of Communications Equipment Portfolio. |

| (3) | To approve an Agreement and Plan of Reorganization providing for the transfer of all of the assets of Energy Service Portfolio to Energy Portfolio in exchange solely for shares of beneficial interest of Energy Portfolio and the assumption by Energy Portfolio of Energy Service Portfolio’s liabilities, in complete liquidation of Energy Service Portfolio. |

| (4) | To approve an Agreement and Plan of Reorganization providing for the transfer of all of the assets of Natural Gas Portfolio to Energy Portfolio in exchange solely for shares of beneficial interest of Energy Portfolio and the assumption by Energy Portfolio of Natural Gas Portfolio’s liabilities, in complete liquidation of Natural Gas Portfolio. |

The Board of Trustees has fixed the close of business on August 23, 2021, as the record date for the determination of the shareholders of Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio and Natural Gas Portfolio entitled to notice of, and to vote at, such Meeting and any adjournments thereof.

By order of the Board of Trustees,

Cynthia Lo Bessette, Secretary

August 23, 2021

Your vote is important – please vote your shares promptly.

In light of public health concerns regarding COVID-19 the Meeting will be held in a virtual format only. Shareholders are invited to attend the Meeting by means of remote audio communication at Meetings.computershare.com/MLWPAWG. You will not be able to attend the Meeting in person. You will be required to enter the control number found on your proxy card voting instruction form or notice you previously received. If you have lost or misplaced your control number, please email Computershare Fund Services, the proxy tabulator for the Meeting (“Computershare”), at Fidelity.Investments@proxydirectmail.com or shareholdermeetings@computershare.com (include your full name, street address, city, state & zip code) to verify your identity and obtain your control number.

If your shares are held through a brokerage account or by a bank or other holder of record you will need to request a legal proxy in order to receive access to the virtual Meeting. To do so, you must submit proof of your proxy power (legal proxy) reflecting your holdings, along with your name and email address, to Computershare. Requests for registration must be labeled as “Legal Proxy” and be received no later than 5:00 p.m. ET on October 15, 2021. You will receive a confirmation of your registration by email that includes the control number necessary to access and vote at the Meeting. Requests for registration should be directed to Computershare at Fidelity.Investments@proxydirectmail.com or shareholdermeetings@computershare.com.

Any shareholder who does not expect to virtually attend the Meeting is urged to vote using the touch-tone telephone or internet voting instructions below or by indicating voting instructions on the enclosed proxy card, dating and signing it, and returning it in the envelope provided, which needs no postage if mailed in the United States. In order to avoid unnecessary expense, we ask your cooperation in responding promptly, no matter how large or small your holdings may be. If you wish to wait until the Meeting to vote your shares, you will need to follow the instructions available on the Meeting website during the Meeting.

INSTRUCTIONS FOR EXECUTING PROXY CARD

The following general rules for executing a proxy card may be of assistance to you and help avoid the time and expense involved in validating your vote if you fail to execute your proxy card properly.

| 1. | Individual Accounts: Your name should be signed exactly as it appears in the registration on the proxy card. |

| 2. | Joint Accounts: Either party may sign, but the name of the party signing should conform exactly to a name shown in the registration. |

| 3. | All other accounts should show the capacity of the individual signing. This can be shown either in the form of the account registration itself or by the individual executing the proxy card. For example: |

| REGISTRATION |

VALID SIGNATURE | |||||||

| A. | 1) | ABC Corp. | John Smith, Treasurer | |||||

| 2) | ABC Corp. | John Smith, Treasurer | ||||||

| c/o John Smith, Treasurer | ||||||||

| B. | 1) | ABC Corp. Profit Sharing Plan | Ann B. Collins, Trustee | |||||

| 2) | ABC Trust | Ann B. Collins, Trustee | ||||||

| 3) | Ann B. Collins, Trustee | Ann B. Collins, Trustee | ||||||

| u/t/d 12/28/78 | ||||||||

| C. | 1) | Anthony B. Craft, Cust. | Anthony B. Craft | |||||

| f/b/o Anthony B. Craft, Jr. | ||||||||

| UGMA | ||||||||

INSTRUCTIONS FOR VOTING BY TOUCH-TONE TELEPHONE OR THROUGH THE INTERNET

| 1. | Read the proxy statement, and have your proxy card handy. |

| 2. | Call the toll-free number or visit the web site indicated on your proxy card. |

| 3. | Enter the number found in the box on the front of your proxy card. |

| 4. | Follow the recorded or on-line instructions to cast your vote up until 11:59 p.m. ET on October 19, 2021. |

AIR TRANSPORTATION PORTFOLIO

COMMUNICATIONS EQUIPMENT PORTFOLIO

ENERGY SERVICE PORTFOLIO

NATURAL GAS PORTFOLIO

TRANSPORTATION PORTFOLIO

COMPUTERS PORTFOLIO

ENERGY PORTFOLIO

SERIES OF

FIDELITY SELECT PORTFOLIOS

245 SUMMER STREET, BOSTON, MASSACHUSETTS 02210

1-800-544-8544

PROXY STATEMENT AND PROSPECTUS

AUGUST 23, 2021

This combined Proxy Statement and Prospectus (Proxy Statement) is furnished to shareholders of Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio, and Natural Gas Portfolio.

Each portfolio is a series of Fidelity Select Portfolios (the trust), an open-end management investment company registered with the Securities and Exchange Commission (SEC).

This solicitation of proxies is made by, and on behalf of, the trust’s Board of Trustees to be used at the Special Meeting of Shareholders of Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio, and Natural Gas Portfolio and at any adjournments thereof (the Meeting), to be held on October 20, 2021 at 8:00a.m. Eastern Time (ET).

In light of public health concerns regarding COVID-19, the Board of Trustees and Fidelity Management & Research Company LLC (FMR), the funds’ investment adviser have determined that the Meeting will be held in a virtual format only. The Meeting will be accessible solely by means of remote audio communication. You will not be able to attend the meeting in person. This Proxy Statement and the accompanying proxy card are first being mailed on or about August 23, 2021.

As more fully described in the Proxy Statement, shareholders of each acquired fund listed in the following table are being asked to consider and vote on an Agreement and Plan of Reorganization relating to the proposed acquisition of the acquired fund by the corresponding acquiring fund listed in the following table.

| Proposal |

Acquired Fund |

Acquiring Fund | ||

| 1 | Air Transportation Portfolio | Transportation Portfolio | ||

| 2 | Communications Equipment Portfolio | Computers Portfolio | ||

| 3 | Energy Service Portfolio | Energy Portfolio | ||

| 4 | Natural Gas Portfolio | Energy Portfolio |

The merger transactions contemplated by each Agreement are each referred to as a Reorganization and, together, the Reorganizations. Approval of each Reorganization is determined solely by approval of the shareholders of the proposed acquired fund. It is not necessary for all Reorganizations to be approved for any one of them to occur.

If the Agreement relating to your fund is approved by the fund’s shareholders and the related Reorganization occurs, you will become a shareholder of the applicable Acquiring Fund. Your fund will transfer all of its assets to the applicable Acquiring Fund in exchange solely for shares of beneficial interest of the applicable Acquiring Fund and the assumption by the applicable Acquiring Fund of your fund’s liabilities in complete liquidation of your fund. The total value of your fund holdings will not change as a result of a Reorganization. The Reorganizations are currently scheduled to take place as of the close of business of the New York Stock Exchange (the NYSE) on November 12, 2021 for Air Transportation Portfolio and Communications Equipment Portfolio and on November 19, 2021 for Energy Service Portfolio and Natural Gas Portfolio, or such other time and date as the parties to each respective Agreement may agree (the Closing Date).

THESE SECURITIES HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SEC, NOR HAS THE SEC PASSED UPON THE ACCURACY OR ADEQUACY OF THIS PROXY STATEMENT AND PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The Proxy Statement sets forth concisely the information about each Reorganization and each Acquiring Fund that shareholders should know before voting on the proposed Reorganizations. Please read it carefully and keep it for future reference.

The following documents have been filed with the SEC and are incorporated into this Proxy Statement by reference, which means they are part of this Proxy statement for legal purposes:

(i) the Statement of Additional Information dated August 23, 2021, relating to this Proxy Statement;

(ii) the Prospectus for Transportation Portfolio and Air Transportation Portfolio dated April 29, 2021, as supplemented, a copy of which accompanies this Proxy Statement;

(iii) the Prospectus for Computers Portfolio and Communications Equipment Portfolio dated April 29, 2021, as supplemented, a copy of which accompanies this Proxy Statement;

(iv) the Prospectus for Energy Portfolio, Energy Service Portfolio, and Natural Gas Portfolio dated April 29, 2021, as supplemented, a copy of which accompanies this Proxy Statement; and

(v) the Statement of Additional Information for each Fund dated April 29, 2021, as supplemented.

You can obtain copies of the funds’ current Prospectuses, Statements of Additional Information, or annual or semiannual reports without charge by contacting the trust at Fidelity Distributors Company LLC (FDC), 900 Salem Street, Smithfield, Rhode Island 02917, by calling 1-800-544-8544, or by logging on to www.fidelity.com.

The trust is subject to the informational requirements of the Securities and Exchange Act of 1934, as amended. Accordingly, it must file proxy material, reports, and other information with the SEC. You can review and copy such information at the public reference facilities maintained by the SEC at 100 F Street, N.E., Washington D.C. 20549, the SEC’s Northeast Regional Office, 200 Vesey Street, Suite 400, New York, NY 10281-1022, and the SEC’s Midwest Regional Office, 175 W. Jackson Blvd., Suite 1450, Chicago, IL 60604. Such information is also available from the EDGAR database on the SEC’s web site at http://www.sec.gov. You can also obtain copies of such information, after paying a duplicating fee, by sending a request by e-mail to publicinfo@sec.gov or by writing the SEC’s Public Reference Room, Office of Consumer Affairs and Information Services, Washington, DC 20549. You may obtain information on the operation of the SEC’s Public Reference Room by calling the SEC at 1-202-551-8090.

An investment in the funds is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You could lose money by investing in the funds.

2

3

The following is a summary of certain information contained elsewhere in this Proxy Statement, in each Agreement, and/or in the Prospectuses and Statement of Additional Information of each Acquired Fund or each Acquiring Fund, as applicable, each of which are incorporated herein by reference. Shareholders should read the entire Proxy Statement and the Prospectuses of each Acquiring Fund carefully for more complete information.

What proposal am I being asked to vote on?

Shareholders of Air Transportation Portfolio are being asked to vote on Proposal 1 to approve the Agreement relating to the proposed acquisition of Air Transportation Portfolio by Transportation Portfolio.

Shareholders of Communications Equipment Portfolio are being asked to vote on Proposal 2 to approve the Agreement relating to the proposed acquisition of Communications Equipment Portfolio by Computers Portfolio.

Shareholders of Energy Service Portfolio are being asked to vote on Proposal 3 to approve the Agreement relating to the proposed acquisition of Energy Service Portfolio by Energy Portfolio.

Shareholders of Natural Gas Portfolio are being asked to vote on Proposal 4 to approve the Agreement relating to the acquisition of Natural Gas Portfolio by Energy Portfolio.

Approval of each Reorganization will be determined solely by approval of the shareholders of the individual fund affected. It is not necessary for all four Reorganizations to be approved for any one of them to occur.

Shareholders of record as of the close of business on August 23, 2021 will be entitled to vote at their respective Meetings.

If the Agreement relating to your fund is approved by fund shareholders and the related Reorganization occurs, you will become a shareholder of the applicable Acquiring Fund. Your Acquired Fund will transfer all of its assets to the applicable Acquiring Fund in exchange solely for shares of beneficial interest of the applicable Acquired Fund and the assumption by the applicable Acquiring Fund of your Acquired Fund’s liabilities in complete liquidation of the fund. Each Acquiring Fund will be the accounting survivor. The Reorganizations, described in the following table, are currently scheduled to take place as of the close of business of the NYSE on the Closing Date.

| Acquired Fund: | Acquiring Fund: | |

| Air Transportation Portfolio | Transportation Portfolio | |

| Communications Equipment Portfolio | Computers Portfolio | |

| Energy Service Portfolio | Energy Portfolio | |

| Natural Gas Portfolio | Energy Portfolio |

For more information, shareholders of Air Transportation Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 1 – Agreement and Plan of Reorganization.”

For more information, shareholders of Communications Equipment Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 2 – Agreement and Plan of Reorganization.”

For more information, shareholders of Energy Service Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 3 – Agreement and Plan of Reorganization.”

For more information, shareholders of Natural Gas Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 4 – Agreement and Plan of Reorganization.”

Has the Board of Trustees approved the proposal?

Yes. Each fund’s Board of Trustees has carefully reviewed the proposal and approved the Agreement and the Reorganization. The Board of Trustees unanimously recommends that you vote in favor of your fund’s Reorganization by approving your fund’s Agreement.

What are the reasons for the proposals?

The Board of Trustees considered the following factors, among others, in determining to recommend that you vote in favor of your fund’s Reorganization by approving your fund’s Agreement:

| • | Shareholders will be able to pursue a similar investment strategy in a higher-rated fund with lower expenses. |

| • | Shareholders will gain exposure to broader, modernized, more enduring and more diversified investment mandates. |

| • | Each Acquiring Fund has outperformed the applicable Acquired Fund over the long-term. |

4

| • | Shareholders of each Acquired Fund are expected to benefit from an expense reduction ranging from approximately 5 basis points to 12 basis points, depending on the fund. |

| • | Each Reorganization will qualify as a tax-free exchange for federal income tax purposes. |

For more information, shareholders of Air Transportation Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 1 – Reasons for the Reorganization.”

For more information, shareholders of Communications Equipment Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 2 – Reasons for the Reorganization.”

For more information, shareholders of Energy Service Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 3 – Reasons for the Reorganization.”

For more information, shareholders of Natural Gas Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 4 – Reasons for the Reorganization.”

How will you determine the number of shares of the Acquiring Fund that I will receive?

Although the number of shares you own will most likely change, the total value of your holdings will not change as a result of your Reorganization.

As provided in the Agreement relating to each Proposal, each Acquired Fund will distribute shares of the applicable Acquiring Fund to its shareholders so that each shareholder will receive the number of full and fractional shares of the applicable Acquiring Fund equal in value to the net asset value of shares of the applicable Acquired Fund held by such shareholder on the Closing Date.

For more information, shareholders of Air Transportation Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 1 – Agreement and Plan of Reorganization.”

For more information, shareholders of Communications Equipment Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 2 – Agreement and Plan of Reorganization.”

For more information, shareholders of Energy Service Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 3 – Agreement and Plan of Reorganization.”

For more information, shareholders of Natural Gas Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 4 – Agreement and Plan of Reorganization.”

Is a Reorganization considered a taxable event for federal income tax purposes?

No. Each fund will receive an opinion of counsel that the Reorganization will not result in any gain or loss for federal income tax purposes either to the Acquired Fund or the Acquiring Fund or to the shareholders of the Acquired Fund.

For more information, shareholders of Air Transportation Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 1 – Federal Income Tax Considerations.”

For more information, shareholders of Communications Equipment Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 2 – Federal Income Tax Considerations.”

For more information, shareholders of Energy Service Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 3 – Federal Income Tax Considerations.”

For more information, shareholders of Natural Gas Portfolio please refer to the section entitled “The Proposed Transactions – Proposal 4 – Federal Income Tax Considerations.”

How do the funds’ investment objectives, strategies, policies, and limitations compare?

Air Transportation Portfolio and Transportation Portfolio

Air Transportation Portfolio and Transportation Portfolio have the same investment objective. Each fund seeks capital appreciation. Each fund’s investment objective is fundamental, that is, subject to change only by shareholder approval.

5

Although Air Transportation Portfolio and Transportation Portfolio have similar investment strategies, there are some differences you should be aware of. The following compares the principal investment strategies of Air Transportation Portfolio and Transportation Portfolio:

| Air Transportation Portfolio | Transportation Portfolio | |

| The fund invests primarily in companies engaged in the regional, national, and international movement of passengers, mail, and freight via aircraft. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities. |

The fund invests primarily in companies engaged in providing transportation services or companies engaged in the design, manufacture, distribution, or sale of transportation equipment. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities. | |

| These companies may include, for example, major airlines, commuter airlines, air cargo and express delivery operators, airfreight forwarders, and companies that provide equipment or services to these companies, such as aviation service firms and manufacturers of aerospace equipment. |

These companies may include, for example, companies providing air freight or passenger air, maritime, rail, or land transportation and services; and airport, road, rail tracks and marine port owners and providers of related services. | |

| This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. |

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. | |

| The Adviser does not place any emphasis on income when selecting securities, except when it believes that income may have a favorable effect on a security’s market value. | Same principal strategy. | |

| The Adviser normally invests each fund’s assets primarily in common stocks. | Same principal strategy. | |

| The fund may invest in domestic and foreign securities. Foreign stocks may make up a majority of some funds’ assets at times. | Same principal strategy. | |

| In addition to concentrating on particular industries, the fund may invest a significant percentage of its assets in relatively few companies and may invest up to 25% in a single company. The fund is classified as non-diversified. | Same principal strategy. | |

| In buying and selling securities for a fund, the Adviser relies on fundamental analysis, which involves a bottom-up assessment of a company’s potential for success in light of factors including its financial condition, earnings outlook, strategy, management, industry position, and economic and market conditions. | Same principal strategy. |

Air Transportation Portfolio and Transportation Portfolio have the same non-fundamental investment policies and limitations. Although Air Transportation Portfolio and Transportation Portfolio have similar fundamental investment policies and limitations, there are some differences you should be aware of. The following summarizes the investment policy and limitation differences between Air Transportation Portfolio and Transportation Portfolio:

| Air Transportation Portfolio | Transportation Portfolio | |

| Fundamental policies and limitations (subject to change only by shareholder vote) | Fundamental policies and limitations (subject to change only by shareholder vote) | |

| Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the air transportation industries. | Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the transportation industries. |

Communications Equipment Portfolio and Computers Portfolio

Communications Equipment Portfolio and Computers Portfolio have the same investment objective. Each fund seeks capital appreciation. Each fund’s investment objective is fundamental, that is, subject to change only by shareholder approval.

Although Communications Equipment Portfolio and Computers Portfolio have similar investment strategies, there are some differences and upcoming changes you should be aware of.

Effective November 13, 2021, Computers Portfolio will be repositioned as Tech Hardware Portfolio and certain changes will be made to the fund’s principal investment strategy, as shown in the table below. The repositioning of the fund does not require shareholder approval.

6

The following compares the principal investment strategies of Communications Equipment Portfolio and Computers Portfolio, and repositioned Tech Hardware Portfolio, where indicated:

| Communications Equipment Portfolio |

Computers Portfolio | |

| The fund invests primarily in companies engaged in the development, manufacture, or sale of communications equipment. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

These companies may include, for example, manufacturers of communications equipment and products, including LANs, WANs, routers, telephones, switchboards and exchanges.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. |

The fund invests primarily in companies engaged in research, design, development, manufacture or distribution of products, processes, or services that relate to currently available or experimental hardware technology within the computer industry. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

These companies may include, for example, manufacturers of personal computers, servers, mainframes and workstations, including ATMs; and manufacturers of electronic computer components and peripherals, including data storage components, motherboards, audio and video cards, monitors, keyboards, printers, and other peripherals, and providers of related services.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund.

Tech Hardware Portfolio (effective November 13, 2021) The fund invests primarily in companies engaged in development, manufacture, or distribution of tech hardware. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

These companies may include, for example, manufacturers of computers, communications equipment, and computer hardware, including personal computers, smartphones, tablets, and gaming consoles, servers, mainframes, workstations and ATMs; electronic computer components and peripherals including data storage components, motherboards, audio and video cards, monitors, keyboards and printers; and LANs, WANs, routers, telephones, switchboards and exchanges, and providers of related services. | |

| The Adviser does not place any emphasis on income when selecting securities, except when it believes that income may have a favorable effect on a security’s market value. | Same principal strategy. | |

| The Adviser normally invests each fund’s assets primarily in common stocks. | Same principal strategy. | |

| The fund may invest in domestic and foreign securities. Foreign stocks may make up a majority of some funds’ assets at times. | Same principal strategy. | |

| In addition to concentrating on particular industries, the fund may invest a significant percentage of its assets in relatively few companies and may invest up to 25% in a single company. The fund is classified as non-diversified. | Same principal strategy. | |

| In buying and selling securities for a fund, the Adviser relies on fundamental analysis, which involves a bottom-up assessment of a company’s potential for success in light of factors including its financial condition, earnings outlook, strategy, management, industry position, and economic and market conditions. | Same principal strategy. |

Communications Equipment Portfolio and Computers Portfolio have the same non-fundamental investment policies and limitations. Although Communications Equipment Portfolio and Computers Portfolio have similar fundamental investment policies and limitations, there are some differences you should be aware of.

7

The Adviser anticipates that Computers Portfolio, after it is repositioned as Tech Hardware Portfolio, will modify its fundamental industry concentration policy subject to shareholder approval, to align it with the repositioning of the fund to the Tech Hardware Portfolio.

The proposal to modify the fundamental concentration policy is pending approval by Computers Portfolio shareholders, and was provided to Computers Portfolio shareholders in a separately mailed notice and proxy statement.

The following summarizes the investment policy and limitation differences between Communications Equipment Portfolio and Computers Portfolio, and repositioned Tech Hardware Portfolio:

| Communications Equipment Portfolio |

Computers Portfolio | |

| Fundamental policies and limitations (subject to change only by shareholder vote) | Fundamental policies and limitations (subject to change only by shareholder vote) | |

| Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the communications equipment industries. | Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the computers industries.

Tech Hardware Portfolio (subject to approval by Computers Portfolio shareholders in a separately mailed notice and proxy statement)

Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the tech hardware industry. |

Energy Service Portfolio and Energy Portfolio

Energy Service Portfolio and Energy Portfolio have the same investment objective. Each fund seeks capital appreciation. Each fund’s investment objective is fundamental, that is, subject to change only by shareholder approval.

Although Energy Service Portfolio and Energy Portfolio have similar investment strategies, there are some differences you should be aware of. The following compares the principal investment strategies of Energy Service Portfolio and Energy Portfolio:

| Energy Service Portfolio | Energy Portfolio | |

| The fund invests primarily in companies in the energy service field, including those that provide services and equipment to the conventional areas of oil, gas, electricity, and coal, and newer sources of energy such as nuclear, geothermal, oil shale, and solar power. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. |

The fund invests primarily in companies in the energy field, including the conventional areas of oil, gas, electricity, and coal, and newer sources of energy such as nuclear, geothermal, oil shale, and solar power. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. | |

| The Adviser does not place any emphasis on income when selecting securities, except when it believes that income may have a favorable effect on a security’s market value. | Same principal strategy. | |

| The Adviser normally invests the fund’s assets primarily in common stocks. | Same principal strategy. | |

| The fund may invest in domestic and foreign securities. Foreign stocks may make up a majority of the fund’s assets at times. | Same principal strategy. | |

| In addition to concentrating on particular industries, the fund may invest a significant percentage of its assets in relatively few companies and may invest up to 25% in a single company. The fund is classified as non-diversified. | Same principal strategy. |

8

| Energy Service Portfolio | Energy Portfolio | |

| In buying and selling securities for the fund, the Adviser relies on fundamental analysis, which involves a bottom-up assessment of a company’s potential for success in light of factors including its financial condition, earnings outlook, strategy, management, industry position, and economic and market conditions. | Same principal strategy. |

Energy Service Portfolio and Energy Portfolio have the same non-fundamental investment policies and limitations. Although Energy Service Portfolio and Energy Portfolio have similar fundamental investment policies and limitations, there are some differences you should be aware of. The following summarizes the investment policy and limitation differences between Energy Service Portfolio and Energy Portfolio:

| Energy Service Portfolio | Energy Portfolio | |

| Fundamental policies and limitations (subject to change only by shareholder vote) | Fundamental policies and limitations (subject to change only by shareholder vote) | |

| Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the energy service industries. | Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the energy industries. |

Natural Gas Portfolio and Energy Portfolio

Natural Gas Portfolio and Energy Portfolio have the same investment objective. Each fund seeks capital appreciation. Each fund’s investment objective is fundamental, that is, subject to change only by shareholder approval.

Although Natural Gas Portfolio and Energy Portfolio have similar investment strategies, there are some differences you should be aware of. The following compares the principal investment strategies of Natural Gas Portfolio and Energy Portfolio:

| Natural Gas Portfolio | Energy Portfolio | |

| The Adviser normally invests the fund’s assets primarily in common stocks. | Same principal strategy. | |

| The fund invests primarily in companies engaged in the production, transmission, and distribution of natural gas, and involved in the exploration of potential natural gas sources, as well as those companies that provide services and equipment to natural gas producers, refineries, cogeneration facilities, converters, and distributors. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. |

The fund invests primarily in companies in the energy field, including the conventional areas of oil, gas, electricity and coal, and newer sources of energy such as nuclear, geothermal, oil shale and solar power. The fund normally invests at least 80% of its assets in securities of companies principally engaged in these activities.

This policy can be changed without a vote only upon 60 days’ prior notice to shareholders of the fund. | |

| The fund may invest in domestic and foreign securities. Foreign stocks may make up a majority of the fund’s assets at times. | Same principal strategy. | |

| In addition to concentrating on particular industries, the fund may invest a significant percentage of its assets in relatively few companies and may invest up to 25% in a single company. The fund is classified as non-diversified. | Same principal strategy. | |

| In buying and selling securities for the fund, the Adviser relies on fundamental analysis, which involves a bottom-up assessment of a company’s potential for success in light of factors including its financial condition, earnings outlook, strategy, management, industry position, and economic and market conditions. | Same principal strategy. |

9

Natural Gas Portfolio and Energy Portfolio have the same non-fundamental investment policies and limitations. Although Natural Gas Portfolio and Energy Portfolio have similar fundamental investment policies and limitations, there are some differences you should be aware of. The following summarizes the investment policy and limitation differences between Natural Gas Portfolio and Energy Portfolio:

| Natural Gas Portfolio | Energy Portfolio | |

| Fundamental policies and limitations (subject to change only by shareholder vote) | Fundamental policies and limitations (subject to change only by shareholder vote) | |

| Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the natural gas industries. | Concentration. The fund may not purchase the securities of any issuer if, as a result, less than 25% of the fund’s total assets would be invested in the securities of issuers principally engaged in the energy industries. |

Except as noted above, the funds have the same fundamental and non-fundamental investment policies and limitations.

For a comparison of the principal risks associated with the funds’ principal investment strategies, please refer to the section entitled “Comparison of Principal Risk Factors.”

For more information about each fund’s investment objectives, strategies, policies, and limitations, please refer to the “Investment Details” section of the funds’ Prospectuses, and to the “Investment Policies and Limitations“ section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

Following the Reorganization, each combined fund will be managed in accordance with the investment objective, strategies, policies, and limitations of the applicable Acquiring Fund.

How do the funds’ management and distribution arrangements compare?

The following summarizes the management and distribution arrangements of each Acquired Fund and Acquiring Fund:

Management of the Funds

As the manager, FMR has overall responsibility for directing the funds’ investments and handling their business affairs. As of December 31, 2020, FMR had approximately $3.0 trillion in discretionary assets under management, and approximately $3.8 trillion when combined with all of its affiliates’ assets under management.

FMR Investment Management (UK) Limited (FMR UK), located at 1 St. Martin’s Le Grand, London, EC1A 4AS, United Kingdom; Fidelity Management & Research (Hong Kong) Limited (FMR H.K.), located at Floor 19, 41 Connaught Road Central, Hong Kong; Fidelity Management & Research (Japan) Limited (FMR Japan), located at Kamiyacho Prime Place, 1-17, Toranomon-4-Chome, Minato-ku, Tokyo, Japan are also sub-advisers to the funds.

FMR and each of the sub-advisers are expected to continue serving as manager or sub-adviser of each respective combined fund after the Reorganizations.

Matthew Moulis is currently the portfolio manager of Air Transportation Portfolio and Transportation Portfolio, which he has managed since January 2012. He also manages other funds. Since joining Fidelity Investments in 2007, Mr. Moulis has worked as a research analyst and portfolio manager. Mr. Moulis is expected to continue to be responsible for portfolio management of the combined fund after the Reorganization.

Caroline Tall is currently the portfolio manager of Communications Equipment Portfolio and Computers Portfolio, which she has managed since August 2018 and December 2017, respectively. She also manages other funds. Since joining Fidelity Investments in 2008, Ms. Tall has worked as a research associate, research analyst, and portfolio manager. Ms. Tall is expected to continue to be responsible for portfolio management of the combined fund after the Reorganization.

Maurice FitzMaurice is currently the portfolio manager of Energy Service Portfolio and Energy Portfolio, which he has managed since September 2018 and January 2020, respectively. He also manages other funds. Since joining Fidelity Investments in 1998, Mr. FitzMaurice has worked as a research analyst and portfolio manager. Mr. FitzMaurice is expected to continue to be responsible for portfolio management of the combined fund after the Reorganization.

Peter Belisle is currently the portfolio manager of Natural Gas Portfolio, which he has managed since January 2020. Since joining Fidelity Investments in 2016, Mr. Belisle has worked as a research analyst and portfolio manager. Mr. FitzMaurice, who is currently the portfolio manager of Energy Portfolio, is expected to be responsible for portfolio management of the combined fund after the Reorganization.

10

For information about the compensation of, any other accounts managed by, and any fund shares held by a fund’s portfolio manager, please refer to the “Management Contracts” section of the funds’ Statement of Additional Information, which is incorporated herein by reference.

Each fund has entered into a management contract with FMR, pursuant to which FMR furnishes investment advisory and other services.

Under each fund’s management contract, FMR is not responsible for paying the fund’s operating expenses. Each fund pays its management fee and other operating expenses separately. Each fund pays FMR a management fee calculated by adding a group fee rate to an individual fund fee rate, dividing by twelve, and multiplying the result by the fund’s average net assets. The group fee rate is based on the average net assets of all the mutual funds advised by FMR. This rate cannot rise above 0.52%, and it drops as total assets under management increase. The individual fund fee rate for each fund is 0.30% of its average net assets.

The basis for the Board of Trustees approving the management contract and sub-advisory agreements for each fund is available in each fund’s annual report for the fiscal period ended February 28, 2021.

If any or all of the Reorganizations are approved, each combined fund will retain the respective Acquiring Fund’s management fee structure.

For more information about fund management, please refer to the “Fund Management” section of the funds’ Prospectuses, and to the “Control of Investment Advisers” and “Management Contracts” sections of the funds’ Statement of Additional Information, each of which is incorporated herein by reference.

Distribution of Fund Shares

The principal business address of Fidelity Distributors Company LLC (FDC), each fund’s principal underwriter and distribution agent, is 900 Salem Street, Smithfield, Rhode Island, 02917.

Each Acquiring Fund has adopted a Distribution and Service Plan pursuant to Rule 12b-1 under the Investment Company Act of 1940 (1940 Act) that recognizes that FMR may use its management fee revenues, as well as its past profits or its resources from any other source, to pay FDC for expenses incurred in connection with providing services intended to result in the sale of fund shares and/or shareholder support services. A fund’s Distribution and Service Plan does not authorize payments by the fund other than those that are to be made to FMR under the fund’s management contract.

If any of the Reorganizations are approved, the Distribution and Service Plan for the combined fund will remain unchanged.

For more information about fund distribution, please refer to the “Fund Distribution” section of the funds’ Prospectuses, and to the “Distribution Services” section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

How do the funds’ fees and operating expenses compare, and what are each combined fund’s fees and operating expenses estimated to be following the Reorganizations?

The following tables allow you to compare the fees and expenses of each Acquired Fund and each corresponding Acquiring Fund for the 12 months ended February 28, 2021 and to analyze the pro forma estimated fees and expenses of each Combined fund.

Annual Fund Operating Expenses

The following tables show the fees and expenses of each Acquired Fund and Acquiring Fund for the 12 months ended February 28, 2021, and the pro forma estimated fees and expenses of the combined funds based on the same time period after giving effect to the Reorganizations. Annual fund operating expenses are paid by each fund.

The combined pro forma expenses shown below with respect to the Energy Service Portfolio, Natural Gas Portfolio and Energy Portfolio assume that both of the Reorganizations occur. Appendix 1 provides pro forma expense information for the combined funds assuming only Proposal 3 is approved or only Proposal 4 is approved.

As shown below, each Reorganization is expected to result in lower total operating expenses for shareholders of each Acquired Fund.

Shareholder Fees (paid directly from your investment)

| Air Transportation Portfolio |

Transportation Portfolio |

Transportation Portfolio Pro forma Fund) |

||||||||||

| Maximum sales charge (load) on purchases (as a % of offering price) | None | None | None | |||||||||

| Maximum contingent deferred sales charge (as a % of the lesser of original purchase price or redemption proceeds) | None | None | None | |||||||||

11

Annual Fund Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

| Air Transportation Portfolio |

Transportation Portfolio |

Transportation Portfolio Pro forma (Combined Fund1) |

||||||||||

| Management fee | 0.53% | 0.53% | 0.53% | |||||||||

| Distribution and/or Service (12b-1) fees | None | None | None | |||||||||

| Other expenses | 0.32% | 0.27% | 0.27% | |||||||||

|

|

|

|

|

|

|

|||||||

| Total annual fund operating expenses | 0.85% | 0.80% | 0.80% | |||||||||

1 Based on estimated expenses for the 12 months ended February 28, 2021.

Shareholder Fees (paid directly from your investment)

| Communications Equipment Portfolio |

Computers Portfolio |

Computers Portfolio Pro forma (Combined Fund) |

||||||||||

| Maximum sales charge (load) on purchases (as a % of offering price) | None | None | None | |||||||||

| Maximum contingent deferred sales charge (as a % of the lesser of original purchase price or redemption proceeds) | None | None | None | |||||||||

Annual Fund Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

| Communications Equipment Portfolio |

Computers Portfolio |

Computers Portfolio Pro forma (Combined Fund1) |

||||||||||

| Management fee | 0.53% | 0.53% | 0.53% | |||||||||

| Distribution and/or Service (12b-1) fees | None | None | None | |||||||||

| Other expenses | 0.34% | 0.21% | 0.22% | |||||||||

|

|

|

|

|

|

|

|||||||

| Total annual fund operating expenses | 0.87% | 0.74% | 0.75% | |||||||||

1 Based on estimated expenses for the 12 months ended February 28, 2021.

Shareholder Fees (paid directly from your investment)

| Energy Service Portfolio |

Natural Gas Portfolio |

Energy Portfolio |

Energy Portfolio Pro forma (Combined Fund) |

|||||||||||||

| Maximum sales charge (load) on purchases (as a % of offering price) | None | None | None | None | ||||||||||||

| Maximum contingent deferred sales charge (as a % of the lesser of original purchase price or redemption proceeds) | None | None | None | None | ||||||||||||

Annual Fund Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

| Energy Service Portfolio |

Natural Gas Portfolio |

Energy Portfolio |

Energy Portfolio Pro forma (Combined Fund1) |

|||||||||||||

| Management fee | 0.53% | 0.53% | 0.53% | 0.53% | ||||||||||||

| Distribution and/or Service (12b-1) fees | None | None | None | None | ||||||||||||

| Other expenses | 0.38% | 0.39% | 0.32% | 0.32% | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total annual fund operating expenses | 0.91% | 0.92% | 0.85% | 0.85% | ||||||||||||

1 Based on estimated expenses for the 12 months ended February 28, 2021.

12

Examples of Effect of Fund Expenses

The following tables illustrate the expenses on a hypothetical $10,000 investment in each fund under the current and pro forma (combined fund) expenses calculated at the rates stated above, assuming a 5% annual return after the Reorganizations. The tables illustrate how much a shareholder would pay in total expenses if the shareholder sells all of their shares at the end of each time period indicated and if the shareholder holds their shares.

| Air Transportation |

Transportation Portfolio |

Transportation Portfolio Pro forma (Combined Fund) |

||||||||||

| 1 year | $ | 87 | $ | 82 | $ | 82 | ||||||

| 3 years | $ | 271 | $ | 255 | $ | 255 | ||||||

| 5 years | $ | 471 | $ | 444 | $ | 444 | ||||||

| 10 years | $ | 1,049 | $ | 990 | $ | 990 | ||||||

| Communications Equipment Portfolio |

Computers Portfolio |

Computers Portfolio Pro forma (Combined Fund) |

||||||||||

| 1 year | $ | 89 | $ | 76 | $ | 77 | ||||||

| 3 years | $ | 278 | $ | 237 | $ | 240 | ||||||

| 5 years | $ | 482 | $ | 411 | $ | 417 | ||||||

| 10 years | $ | 1,073 | $ | 918 | $ | 930 | ||||||

| Energy Service Portfolio |

Natural Gas Portfolio |

Energy Portfolio | Energy Portfolio Pro forma (Combined Fund) |

|||||||||||||

| 1 year | $ | 93 | $ | 94 | $ | 87 | $ | 87 | ||||||||

| 3 years | $ | 290 | $ | 293 | $ | 271 | $ | 271 | ||||||||

| 5 years | $ | 504 | $ | 509 | $ | 471 | $ | 471 | ||||||||

| 10 years | $ | 1,120 | $ | 1,131 | $ | 1,049 | $ | 1,049 | ||||||||

These examples assume that all dividends and other distributions are reinvested and that the percentage amounts listed under Annual Operating Expenses remain the same in the years shown. These examples illustrate the effect of expenses but are not meant to suggest actual or expected expenses, which may vary. The assumed return of 5% is not a prediction of, and does not represent, actual or expected performance of any fund.

The combined fund pro forma expenses shown above for Energy Portfolio assume that both Proposal 3 and Proposal 4 are approved. Appendix 2 provides pro forma expenses for the combined fund if only Proposal 3 is approved or if only Proposal 4 is approved.

Do the procedures for purchasing and redeeming shares of the funds differ?

No. The procedures for purchasing and redeeming shares of the funds are the same. If one or all of the Reorganizations are approved, the procedures for purchasing and redeeming shares of the combined funds will remain unchanged.

On June 7, 2021, each Acquired Fund closed to new accounts pending the Reorganizations. Shareholders of each Acquired Fund as of that date can continue to purchase shares of their respective fund. Shareholders of each Acquired Fund may redeem shares of their respective fund through the Closing Date of their fund’s Reorganization.

For information about the procedures for purchasing and redeeming the funds’ shares, including a description of the policies and procedures designed to discourage excessive or short-term trading of fund shares, please refer to the “Additional Information about the Purchase and Sale of Shares” section of the funds’ Prospectuses, and to the “Buying, Selling and Exchanging Information” section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

Do the funds’ exchange privileges differ?

No. The exchange privileges currently offered by the funds are the same. If one or all of the Reorganizations are approved, the exchange privilege offered by the combined funds will remain unchanged.

13

For information about the funds’ exchange privileges, please refer to the “Exchanging Shares” section of the funds’ Prospectuses, and to the “Buying, Selling and Exchanging Information” section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

Do the funds’ dividend and distribution policies differ?

No. The funds’ dividend and distribution policies are the same. If one or all of the Reorganizations are approved, the dividend and distribution policies of the combined funds will remain unchanged.

On or before the Closing Date, each Acquired Fund may declare additional dividends or other distributions in order to distribute substantially all of its investment company taxable income and net realized capital gain.

Whether or not the Reorganizations are approved, each of Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio and Natural Gas Portfolio may be required to recognize gain or loss on any assets subject to “mark-to-market” tax accounting held on February 28 (the last day of each fund’s tax year) or on October 31 (due to excise tax considerations). If the Reorganizations are approved, gains or losses on any such assets held on the Closing Date by Air Transportation Portfolio, Communications Equipment Portfolio, Energy Service Portfolio or Natural Gas Portfolio may be required to be recognized on the Closing Date.

For information about the funds’ dividend and distribution policies, please refer to the “Dividends and Capital Gain Distributions” section of the funds’ Prospectuses, and to the “Distributions and Taxes” section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

Who bears the expenses associated with the Reorganizations?

Each Acquired Fund will bear the cost of each respective Reorganization.

For more information, please refer to the section entitled “Voting Information – Solicitation of Proxies; Expenses.”

COMPARISON OF PRINCIPAL RISK FACTORS

Many factors affect each fund’s performance. A fund’s share price changes daily based on changes in market conditions and interest rates and in response to other economic, political, or financial developments. A fund’s reaction to these developments will be affected by the types of securities in which the fund invests, the financial condition, industry and economic sector, and geographic location of an issuer, and the fund’s level of investment in the securities of that issuer. When you sell your shares they may be worth more or less than what you paid for them, which means that you could lose money by investing in a fund.

The following is a summary of the principal risks associated with an investment in the funds. Because the funds have identical investment objectives and substantially similar strategies as described above, the funds are subject to substantially similar investment risks. Because the funds have some different principal investment strategies as described above, the funds are also subject to some different investment risks, of which you should be aware.

What risks are associated with an investment in all of the funds?

Air Transportation Portfolio and Transportation Portfolio

| Air Transportation Portfolio | Transportation Portfolio | |

| Stock Market Volatility. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Different parts of the market, including different market sectors, and different types of securities can react differently to these developments. | Same risk. | |

| Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market. | Same risk. | |

| Air Transportation Industry Concentration. The air transportation industry can be significantly affected by competition within the industry, domestic and foreign economies, government regulation, labor relations, the price of fuel, and geopolitical developments. | Transportation Industry Concentration. The transportation industry can be significantly affected by changes in the economy, fuel prices, labor relations, insurance costs, and government regulations. |

14

| Air Transportation Portfolio | Transportation Portfolio | |

| Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. The value of securities of smaller issuers can be more volatile than that of larger issuers. | Same risk. |

Communications Equipment Portfolio and Computers Portfolio

| Communications Equipment Portfolio |

Computers Portfolio | |

| Stock Market Volatility. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Different parts of the market, including different market sectors, and different types of securities can react differently to these developments. | Same risk. | |

| Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market. | Foreign Exposure. Foreign markets, particularly emerging markets, can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market. Emerging markets can be subject to greater social, economic, regulatory, and political uncertainties and can be extremely volatile. | |

| Communications Equipment Industry Concentration. The communications equipment industry can be significantly affected by failure to obtain, or delays in obtaining, financing or regulatory approval, intense competition, product compatibility, consumer preferences, corporate capital expenditures, and rapid obsolescence. | Computer Industry Concentration. The computer industry can be significantly affected by competitive pressures, changing domestic and international demand, research and development costs, availability and price of components, and product obsolescence. | |

| Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. The value of securities of smaller issuers can be more volatile than that of larger issuers. | Same risk. | |

| High Portfolio Turnover. High portfolio turnover (more than 100%) may result in increased transaction costs and potentially higher capital gains or losses. The effects of higher than normal portfolio turnover may adversely affect the fund’s performance. | Same risk. | |

| No corresponding risk. | Geographic Concentration in Japan. Because the fund concentrates its investments in Japan, the fund’s performance is expected to be closely tied to social, political, and economic conditions within Japan and to be more volatile than the performance of more geographically diversified funds. |

Energy Service Portfolio and Energy Portfolio

| Energy Service Portfolio | Energy Portfolio | |

| Stock Market Volatility. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Different parts of the market, including different market sectors, and different types of securities can react differently to these developments. | Same risk. |

15

| Energy Service Portfolio | Energy Portfolio | |

| Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market. | Same risk. | |

| Energy Service Industry Concentration. The energy service industry can be significantly affected by the supply of and demand for specific equipment or services, the supply of and demand for oil and gas, the price of oil and gas, exploration and production spending, government regulation, world events, and economic conditions. | Energy Industry Concentration. The energy industries can be significantly affected by fluctuations in energy prices and supply and demand of energy fuels, energy conservation, the success of exploration projects, and tax and other government regulations. | |

| Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. The value of securities of smaller issuers can be more volatile than that of larger issuers. | Same risk. |

Natural Gas Portfolio and Energy Portfolio

| Natural Gas Portfolio | Energy Portfolio | |

| Stock Market Volatility. Stock markets are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Different parts of the market, including different market sectors, and different types of securities can react differently to these developments. | Same risk. | |

| Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market. | Same risk. | |

| Geographic Concentration in Canada. Because the fund concentrates its investments in Canada, the fund’s performance is expected to be closely tied to social, political, and economic conditions within Canada and to be more volatile than the performance of more geographically diversified funds. | No corresponding risk. | |

| Natural Gas Industry Concentration. The natural gas industry is subject to changes in price and supply of energy sources and can be significantly affected by events relating to international politics, energy conservation, the success of energy source exploration projects, and tax and other government regulations. | Energy Industry Concentration. The energy industries can be significantly affected by fluctuations in energy prices and supply and demand of energy fuels caused by geopolitical events, energy conservation, the success of exploration projects, weather or meteorological events, and tax and other government regulations. | |

| Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. The value of securities of smaller issuers can be more volatile than that of larger issuers. | Same risk. | |

| High Portfolio Turnover. High portfolio turnover (more than 100%) may result in increased transaction costs and potentially higher capital gains or losses. The effects of higher than normal portfolio turnover may adversely affect the fund’s performance. | No corresponding risk. |

For more information about the principal risks associated with an investment in the funds, please refer to the “Investment Details” section of the funds’ Prospectuses, and to the “Investment Policies and Limitations“ section of the funds’ Statement of Additional Information, each of which are incorporated herein by reference.

16

How do the funds compare in terms of their performance?

The following information is intended to help you understand the risks of investing in the funds. The information illustrates the changes in the performance in each Acquired Fund’s performance from year to year and compares each Acquired Fund’s performance to the performance of a securities market index over various periods of time. The index description appears in the “Additional Index Information” section of the funds’ prospectuses. Past performance (before and after taxes) is not an indication of future performance.

Year-by-Year Returns

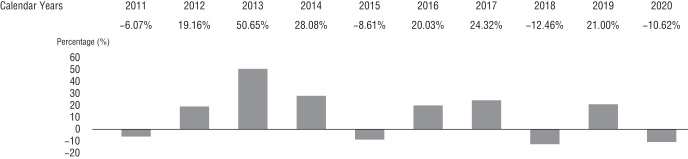

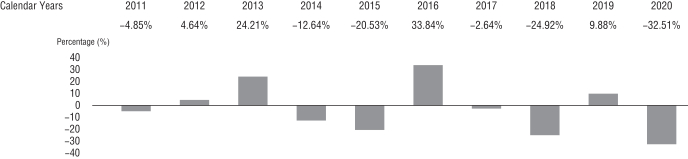

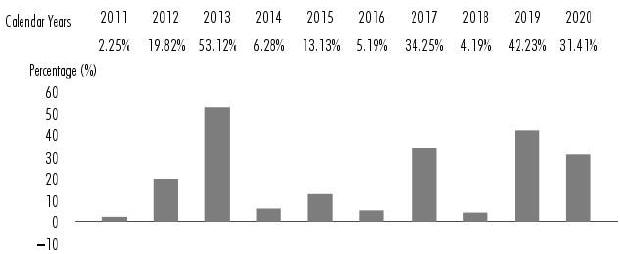

Air Transportation Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

24.63 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–42.40 | % | March 31, 2020 | |||

| Year-to-Date Return |

10.95 | % | March 31, 2021 | |||

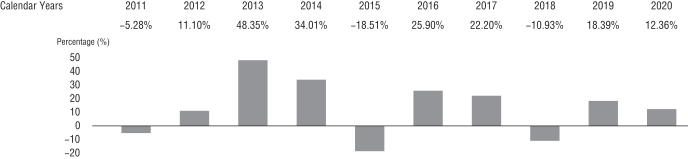

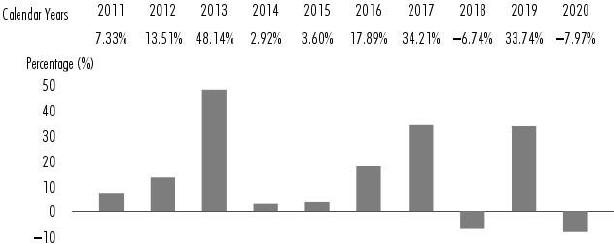

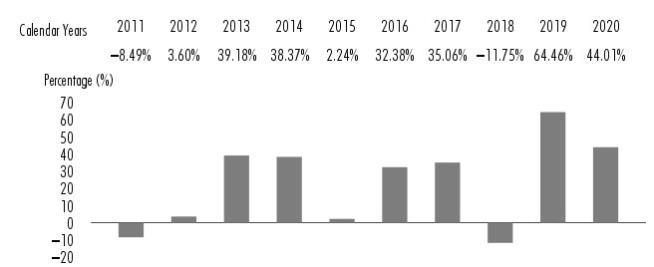

Transportation Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

19.82 | % | September 30, 2020 | |||

| Lowest Quarter Return |

–29.06 | % | March 31, 2020 | |||

| Year-to-Date Return |

11.32 | % | March 31, 2021 | |||

17

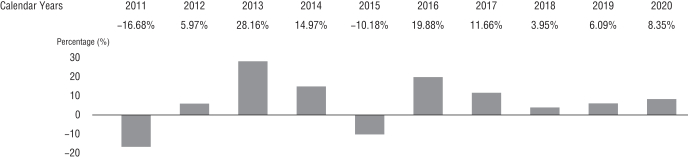

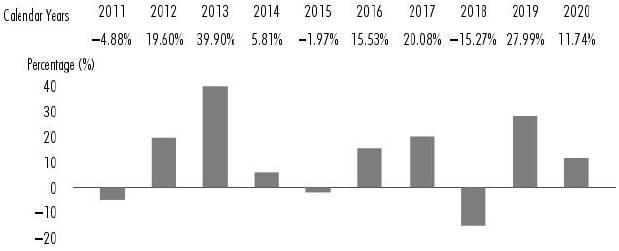

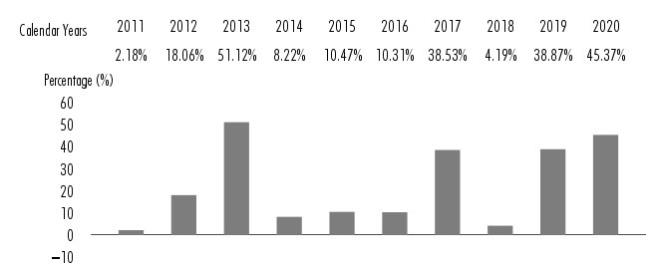

Communications Equipment Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

18.92 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–25.14 | % | September 30, 2011 | |||

| Year-to-Date Return |

12.45 | % | March 31, 2021 | |||

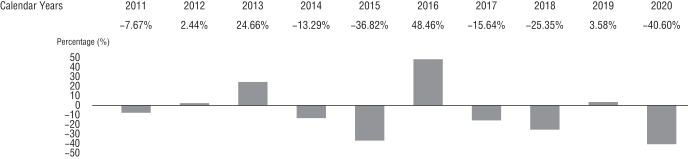

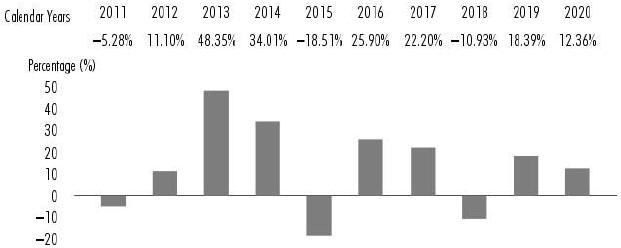

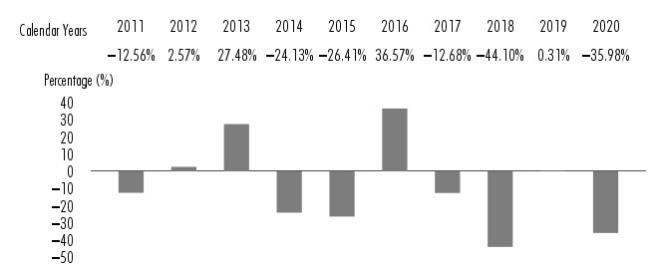

Computers Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

27.30 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–19.07 | % | December 31, 2018 | |||

| Year-to-Date Return |

6.53 | % | March 31, 2021 | |||

Energy Service Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

57.36 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–66.31 | % | March 31, 2020 | |||

| Year-to-Date Return |

22.52 | % | March 31, 2021 | |||

18

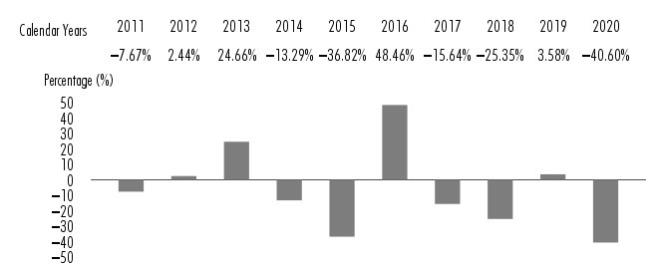

Natural Gas Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

24.46 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–55.51 | % | March 31, 2020 | |||

| Year-to-Date Return |

21.55 | % | March 31, 2021 | |||

Energy Portfolio:

| During the periods shown in the chart: | Returns | Quarter ended | ||||

| Highest Quarter Return |

30.36 | % | December 31, 2020 | |||

| Lowest Quarter Return |

–52.25 | % | March 31, 2020 | |||

| Year-to-Date Return |

27.32 | % | March 31, 2021 | |||

Average Annual Returns

After-tax returns are calculated using the historical highest individual federal marginal income tax rates, but do not reflect the impact of state or local taxes. Actual after-tax returns may differ depending on your individual circumstances. The after-tax returns shown are not relevant if you hold your shares in a retirement account or in another tax-deferred arrangement, such as an employee benefit plan (profit sharing, 401(k), or 403(b) plan). Return After Taxes on Distributions and Sale of Fund Shares may be higher than other returns for the same period due to a tax benefit of realizing a capital loss upon the sale of fund shares.

Air Transportation Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Air Transportation Portfolio | ||||||||||||||||||

| Return Before Taxes | –10.62% | 7.15% | 10.80% | |||||||||||||||

| Return After Taxes on Distributions | –11.27% | 5.44% | 9.30% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | –6.11% | 5.52% | 8.71% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| Nasdaq North America Air Transportation Linked Index (reflects no deduction for fees, expenses, or taxes) |

–9.63% | 8.81% | 11.43% | |||||||||||||||

19

Transportation Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Transportation Portfolio | ||||||||||||||||||

| Return Before Taxes | 12.36% | 12.76% | 12.00% | |||||||||||||||

| Return After Taxes on Distributions | 9.54% | 11.05% | 10.58% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares |

8.16% | 9.79% | 9.58% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| MSCI U.S. IMI Transportation 25/50 Index (reflects no deduction for fees, expenses, or taxes) |

18.04% | 14.03% | 13.02% | |||||||||||||||

Communications Equipment Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Communications Equipment Portfolio | ||||||||||||||||||

| Return Before Taxes | 8.35% | 9.85% | 6.45% | |||||||||||||||

| Return After Taxes on Distributions | 8.25% | 9.00% | 5.70% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | 5.02% | 7.71% | 5.02% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| MSCI North America IMI + ADR Custom Communications Equipment 25/50 Linked Index (reflects no deduction for fees, expenses, or taxes) |

9.47% | 9.04% | 5.89% | |||||||||||||||

Computers Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Computers Portfolio | ||||||||||||||||||

| Return Before Taxes | 45.90% | 24.39% | 15.47% | |||||||||||||||

| Return After Taxes on Distributions | 41.72% | 20.79% | 13.37% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | 28.25% | 18.68% | 12.20% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| FactSet Computers & Peripherals Linked Index (reflects no deduction for fees, expenses, or taxes) |

40.84% | 20.83% | 12.00% | |||||||||||||||

Energy Service Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Energy Service Portfolio | ||||||||||||||||||

| Return Before Taxes | –35.98% | –15.61% | –12.17% | |||||||||||||||

| Return After Taxes on Distributions | –36.30% | –16.21% | –12.78% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | –21.15% | –10.58% | –7.31% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| MSCI U.S. IMI Energy Equipment & Services 25/50 Index (reflects no deduction for fees, expenses, or taxes) |

–41.29% | –18.59% | –13.20% | |||||||||||||||

20

Natural Gas Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Natural Gas Portfolio | ||||||||||||||||||

| Return Before Taxes | –40.60% | –10.47% | –9.43% | |||||||||||||||

| Return After Taxes on Distributions | –40.92% | –10.86% | –9.76% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | –23.81% | –7.37% | –6.11% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| FactSet Natural Gas Linked Index (reflects no deduction for fees, expenses, or taxes) |

–29.73% | –4.38% | –4.60% | |||||||||||||||

Energy Portfolio:

| For the periods ended December 31, 2020 |

Past 1 year |

Past 5 years |

Past 10 years |

|||||||||||||||

| Energy Portfolio | ||||||||||||||||||

| Return Before Taxes | –32.51% | –6.22% | –4.62% | |||||||||||||||

| Return After Taxes on Distributions | –33.06% | –6.62% | –5.38% | |||||||||||||||

| Return After Taxes on Distributions and Sale of Fund Shares | –18.87% | –4.49% | –2.99% | |||||||||||||||

| S&P 500® Index (reflects no deduction for fees, expenses, or taxes) |

18.40% | 15.22% | 13.88% | |||||||||||||||

| MSCI U.S. IMI Energy 25/50 Index (reflects no deduction for fees, expenses, or taxes) |

–33.03% | –5.75% | –3.62% | |||||||||||||||

21

PROPOSAL 1

TO APPROVE AN AGREEMENT AND PLAN OF REORGANIZATION BETWEEN AIR TRANSPORTATION PORTFOLIO AND TRANSPORTATION PORTFOLIO.

Agreement and Plan of Reorganization

The terms and conditions under which the proposed transaction may be consummated are set forth in the Agreement. Significant provisions of the Agreement are summarized below in this Proposal 1; however, this summary is qualified in its entirety by reference to the Agreement, a copy of which is attached as Exhibit A to this Proxy Statement.

The Agreement contemplates (a) Transportation Portfolio acquiring as of the Closing Date all of the assets of Air Transportation Portfolio in exchange solely for shares of Transportation Portfolio and the assumption by Transportation Portfolio of Air Transportation Portfolio’s liabilities; and (b) the distribution of shares of Transportation Portfolio to the shareholders of Air Transportation Portfolio as provided for in the Agreement.

The value of Air Transportation Portfolio’s assets to be acquired by Transportation Portfolio and the amount of its liabilities to be assumed by Transportation Portfolio will be determined as of the close of business of the NYSE on the Closing Date, using the valuation procedures set forth in Transportation Portfolio’s then-current Prospectus and Statement of Additional Information. The net asset value of a share of Transportation Portfolio will be determined as of the same time using the valuation procedures set forth in its then-current Prospectus and Statement of Additional Information.

As of the Closing Date, Transportation Portfolio will deliver to Air Transportation Portfolio, and Air Transportation Portfolio will distribute to its shareholders of record, shares of Transportation Portfolio so that each Air Transportation Portfolio shareholder will receive the number of full and fractional shares of Transportation Portfolio equal in value to the aggregate net asset value of shares of Air Transportation Portfolio held by such shareholder on the Closing Date; Air Transportation Portfolio will be liquidated as soon as practicable thereafter. Each Air Transportation Portfolio shareholder’s account shall be credited with the respective pro rata number of full and fractional shares of Transportation Portfolio due that shareholder. The net asset value per share of Transportation Portfolio will be unchanged by the transaction. Thus, the Reorganization will not result in a dilution of any shareholder’s interest.

Any transfer taxes payable upon issuance of shares of Transportation Portfolio in a name other than that of the registered holder of the shares on the books of Air Transportation Portfolio as of that time shall be paid by the person to whom such shares are to be issued as a condition of such transfer. Any reporting responsibility of Air Transportation Portfolio is and will continue to be its responsibility up to and including the Closing Date and such later date on which Air Transportation Portfolio is liquidated. Transportation Portfolio will be the accounting survivor.