Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-181014-01

This preliminary prospectus supplement relates to an effective registration statement under the Securities Act of 1933, as amended, but it is not complete and may be changed. This preliminary prospectus supplement is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 28, 2014

PROSPECTUS SUPPLEMENT TO PROSPECTUS, DATED APRIL 27, 2012

$1,061,489,000

2014-2 PASS THROUGH TRUSTS

PASS THROUGH CERTIFICATES, SERIES 2014-2

Two classes of the United Airlines Pass Through Certificates, Series 2014-2, are being offered under this prospectus supplement: Class A and B. A separate trust will be established for each class of certificates. The proceeds from the sale of certificates will initially be held in escrow, and interest on the escrowed funds will be payable semiannually on March 3 and September 3, commencing March 3, 2015. The trusts will use the escrowed funds to acquire equipment notes. The equipment notes will be issued by United Airlines, Inc. and will be secured by 15 new Boeing aircraft and 12 new Embraer aircraft scheduled for delivery from November 2014 to July 2015. Payments on the equipment notes held in each trust will be passed through to the holders of certificates of such trust.

Interest on the equipment notes will be payable semiannually on each March 3 and September 3 after issuance (but not before March 3, 2015). Principal payments on the equipment notes are scheduled on March 3 and September 3 of each year, beginning on March 3, 2016.

The Class A certificates will rank senior to the Class B certificates.

BNP Paribas, acting through its New York Branch, will provide the initial liquidity facility for the Class A and B certificates, in each case, in an amount sufficient to make three semiannual interest payments.

The certificates will not be listed on any national securities exchange.

Investing in the certificates involves risks. See “Risk Factors” beginning on page S-17.

| Pass Through Certificates |

Face Amount | Interest Rate |

Final Expected Distribution Date |

Price to Public(1) | ||||

| Class A |

$823,071,000 | % | September 3, 2026 | 100% | ||||

| Class B |

$238,418,000 | % | September 3, 2022 | 100% |

| (1) | Plus accrued interest, if any, from the date of issuance. |

The underwriters will purchase all of the certificates if any are purchased. The aggregate proceeds from the sale of the certificates will be $1,061,489,000. United will pay the underwriters a commission of $ . Delivery of the certificates in book-entry form only will be made on or about August , 2014.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Lead Bookrunners

| Credit Suisse | MORGAN STANLEY | |

Bookrunners

| Deutsche Bank Securities | Goldman, Sachs & Co. |

| Citigroup | Barclays | BNP PARIBAS | Credit Agricole Securities | |||

The date of this prospectus supplement is July , 2014.

Table of Contents

PRESENTATION OF INFORMATION

These offering materials consist of two documents: (a) this Prospectus Supplement, which describes the terms of the certificates that we are currently offering, and (b) the accompanying Prospectus, which provides general information about our pass through certificates, some of which may not apply to the certificates that we are currently offering. The information in this Prospectus Supplement replaces any inconsistent information included in the accompanying Prospectus.

We have given certain capitalized terms specific meanings for purposes of this Prospectus Supplement. The “Index of Terms” attached as Appendix I to this Prospectus Supplement lists the page in this Prospectus Supplement on which we have defined each such term.

At various places in this Prospectus Supplement and the Prospectus, we refer you to other sections of such documents for additional information by indicating the caption heading of such other sections. The page on which each principal caption included in this Prospectus Supplement and the Prospectus can be found is listed in the Table of Contents below. All such cross references in this Prospectus Supplement are to captions contained in this Prospectus Supplement and not in the Prospectus, unless otherwise stated.

On March 31, 2013, United Continental Holdings, Inc. (“UAL”) merged United Air Lines, Inc., a wholly-owned subsidiary, with and into Continental Airlines, Inc. (“Continental”), a wholly-owned subsidiary, to form one legal entity (the “Airlines Merger”), with Continental continuing as the surviving corporation of the Airlines Merger and as a wholly-owned subsidiary of UAL. Upon closing of the Airlines Merger on March 31, 2013, Continental’s name was changed to United Airlines, Inc. (“United”). As a result, the accompanying Prospectus shall be deemed modified to give effect to the Airlines Merger and the name change.

S-1

Table of Contents

Prospectus Supplement

S-2

Table of Contents

Prospectus

| Page | ||||

| 1 | ||||

| 2 | ||||

| 2 | ||||

| 3 | ||||

| 3 | ||||

| 4 | ||||

| 5 | ||||

| 5 | ||||

| 6 | ||||

| 6 | ||||

You should rely only on the information contained in this document or to which this document refers you. We have not authorized anyone to provide you with information that is different. This document may be used only where it is legal to sell these securities. The information in this document may be accurate only on the date of this document.

S-3

Table of Contents

This summary highlights selected information from this Prospectus Supplement and the accompanying Prospectus and may not contain all of the information that is important to you. For more complete information about the Certificates and United, you should read this entire Prospectus Supplement and the accompanying Prospectus, as well as the materials filed with the Securities and Exchange Commission that are considered to be part of this Prospectus Supplement and the Prospectus. See “Incorporation of Certain Documents by Reference” in this Prospectus Supplement and the Prospectus.

Summary of Terms of Certificates

| Class A Certificates |

Class B Certificates | |||

| Aggregate Face Amount |

$823,071,000 | $238,418,000 | ||

| Interest Rate |

% | % | ||

| Initial Loan to Aircraft Value (cumulative)(1) |

55.1% | 71.0% | ||

| Highest Loan to Aircraft Value (cumulative)(2) |

55.1% | 71.0% | ||

| Expected Principal Distribution Window (in years) |

1.6-12.1 | 1.6-8.1 | ||

| Initial Average Life (in years from Issuance Date) |

8.8 | 5.9 | ||

| Regular Distribution Dates |

March 3 and September 3 | March 3 and September 3 | ||

| Final Expected Distribution Date |

September 3, 2026 | September 3, 2022 | ||

| Final Maturity Date |

March 3, 2028 | March 3, 2024 | ||

| Minimum Denomination |

$1,000 | $1,000 | ||

| Section 1110 Protection |

Yes | Yes | ||

| Liquidity Facility Coverage |

3 semiannual interest payments |

3 semiannual interest payments |

| (1) | These percentages are calculated assuming that United selects from the aircraft of each model eligible to be financed pursuant to this Offering the aircraft of such model with the earliest scheduled delivery dates from the manufacturer, in the quantities indicated below: |

| Aircraft Model |

Financed Aircraft | Eligible Aircraft | ||||||||

| Boeing 737-924ER |

11 | 17 | ||||||||

| Boeing 787-9 |

4 | 5 | ||||||||

| Embraer ERJ 175 LR |

12 | 18 | ||||||||

These percentages are determined as of September 3, 2015, the first Regular Distribution Date after all Aircraft are expected to have been financed pursuant to this Offering. In calculating these percentages, we have assumed that the financings of all Aircraft hereunder are completed prior to September 3, 2015 and that the aggregate appraised value of such Aircraft is $1,494,483,067 as of such date. The appraised value is only an estimate and reflects certain assumptions. See “Description of the Aircraft and the Appraisals—The Appraisals”.

| (2) | See “—Loan to Aircraft Value Ratios”. |

S-4

Table of Contents

Equipment Notes and the Aircraft

The 27 Aircraft to be financed pursuant to this Offering will consist of 11 new Boeing 737-924ER aircraft, four new Boeing 787-9 aircraft and 12 new Embraer ERJ 175 LR aircraft scheduled for delivery between November 2014 and July 2015. These aircraft will be selected by United from among 17 new Boeing 737-924ER aircraft, five new Boeing 787-9 aircraft and 18 new Embraer ERJ 175 LR aircraft. See “Description of the Aircraft and the Appraisals—The Appraisals” for a description of the 40 aircraft from which United will select the 27 aircraft that may be financed with the proceeds of this Offering. Set forth below is certain information about the Equipment Notes expected to be held in the Trusts and the aircraft expected to secure such Equipment Notes (assuming for the purposes of the chart below that United selects from the aircraft of each model eligible to be financed pursuant to this Offering the aircraft of such model with the earliest scheduled delivery dates from the manufacturer):

| Aircraft Model |

Registration Number(1) |

Manufacturer’s Serial Number(1) |

Delivery Month(1) | Principal Amount of Equipment Notes |

Appraised Value(2) |

Latest Equipment Note Maturity Date | ||||||||||

| Boeing 737-924ER |

N66841 | 42181 | January 2015 | $ | 36,993,000 | $ | 52,923,333 | September 3, 2026 | ||||||||

| Boeing 737-924ER |

N68842 | 42182 | January 2015 | 36,993,000 | 52,923,333 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N68843 | 42183 | January 2015 | 36,993,000 | 52,923,333 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N69840 | 60317 | February 2015 | 37,024,000 | 52,966,667 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N64844 | 42184 | February 2015 | 37,024,000 | 52,966,667 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N67845 | 42185 | February 2015 | 37,024,000 | 52,966,667 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N67846 | 42186 | February 2015 | 37,024,000 | 52,966,667 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N69847 | 42187 | March 2015 | 37,056,000 | 53,013,333 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N66848 | 42188 | March 2015 | 37,056,000 | 53,013,333 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N62849 | 42199 | April 2015 | 37,133,000 | 53,123,333 | September 3, 2026 | ||||||||||

| Boeing 737-924ER |

N68850 | 42204 | April 2015 | 37,133,000 | 53,123,333 | September 3, 2026 | ||||||||||

| Boeing 787-9 |

N26952 | 36403 | January 2015 | 101,399,000 | 145,063,333 | September 3, 2026 | ||||||||||

| Boeing 787-9 |

N35953 | 36404 | March 2015 | 101,567,000 | 145,303,333 | September 3, 2026 | ||||||||||

| Boeing 787-9 |

N13954 | 36405 | March 2015 | 101,567,000 | 145,303,333 | September 3, 2026 | ||||||||||

| Boeing 787-9 |

N38955 | 37814 | May 2015 | 101,912,000 | 145,796,667 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N89313 | 17000432 | November 2014 | 20,578,000 | 29,440,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N82314 | 17000433 | November 2014 | 20,578,000 | 29,440,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N89315 | 17000436 | November 2014 | 20,578,000 | 29,440,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N86316 | 17000437 | December 2014 | 20,614,000 | 29,490,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N89317 | 17000438 | December 2014 | 20,614,000 | 29,490,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N87318 | 17000442 | December 2014 | 20,614,000 | 29,490,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N87319 | 17000443 | December 2014 | 20,614,000 | 29,490,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N85320 | 17000448 | February 2015 | 20,655,000 | 29,550,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N89321 | TBD | March 2015 | 20,676,000 | 29,580,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N86322 | TBD | April 2015 | 20,690,000 | 29,600,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N85323 | TBD | April 2015 | 20,690,000 | 29,600,000 | September 3, 2026 | ||||||||||

| Embraer ERJ 175 LR |

N86324 | TBD | April 2015 | 20,690,000 | 29,600,000 | September 3, 2026 | ||||||||||

| (1) | The indicated registration number, manufacturer’s serial number and delivery month for each aircraft reflect our current expectations, although these may differ for the actual aircraft financed hereunder. United does not currently have the manufacturer’s serial numbers for certain Embraer ERJ 175 LR aircraft. The deadline for purposes of financing an Aircraft pursuant to this Offering is October 31, 2015 (or later under certain circumstances). The financing pursuant to this Offering of each Aircraft is expected to be effected at or around the time of delivery of such Aircraft by the manufacturer to United. The actual delivery date for any aircraft may be subject to delay or acceleration. See “Description of the Aircraft and the Appraisals—Timing of Financing the Aircraft”. United has certain rights to substitute other aircraft if the scheduled delivery date of any Aircraft is delayed for more than 30 days after the month scheduled for delivery. See “Description of the Aircraft and the Appraisals—Substitute Aircraft”. |

| (2) | The appraised value of each Aircraft set forth above is the lesser of the average and median values of such Aircraft as appraised by three independent appraisal and consulting firms. Such appraisals indicate appraised base value, projected as of the scheduled delivery month of the applicable Aircraft. These appraisals are based upon varying assumptions and methodologies. An appraisal is only an estimate of value and should not be relied upon as a measure of realizable value. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only estimates of Aircraft value”. |

S-5

Table of Contents

The following table sets forth loan to Aircraft value ratios (“LTVs”) for each Class of Certificates as of September 3, 2015, the first Regular Distribution Date after all Aircraft are expected to have been financed pursuant to this Offering, and each Regular Distribution Date thereafter. The LTVs for any Class of Certificates for the period prior to September 3, 2015, are not meaningful, since during such period all of the Equipment Notes expected to be acquired by the Trusts and the related Aircraft will not be included in the calculation. The table should not be considered a forecast or prediction of expected or likely LTVs but simply a mathematical calculation based on one set of assumptions. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only estimates of Aircraft value”.

| Regular Distribution Date |

Assumed Aggregate Aircraft Value(1) |

Outstanding Balance(2) | LTV(3) | |||||||||||||||||

| Class A Certificates |

Class B Certificates |

Class A Certificates |

Class B Certificates |

|||||||||||||||||

| September 3, 2015 |

$ | 1,494,483,067 | $ | 823,071,000 | $ | 238,418,000 | 55.1 | % | 71.0 | % | ||||||||||

| March 3, 2016 |

1,471,704,267 | 799,122,301 | 226,722,767 | 54.3 | % | 69.7 | % | |||||||||||||

| September 3, 2016 |

1,448,925,467 | 775,598,505 | 215,583,994 | 53.5 | % | 68.4 | % | |||||||||||||

| March 3, 2017 |

1,426,146,667 | 752,111,409 | 204,473,600 | 52.7 | % | 67.1 | % | |||||||||||||

| September 3, 2017 |

1,403,367,867 | 728,662,798 | 193,392,969 | 51.9 | % | 65.7 | % | |||||||||||||

| March 3, 2018 |

1,380,589,067 | 705,613,341 | 182,343,573 | 51.1 | % | 64.3 | % | |||||||||||||

| September 3, 2018 |

1,357,810,267 | 682,606,307 | 171,326,985 | 50.3 | % | 62.9 | % | |||||||||||||

| March 3, 2019 |

1,335,031,467 | 659,643,870 | 160,344,883 | 49.4 | % | 61.4 | % | |||||||||||||

| September 3, 2019 |

1,312,252,667 | 636,728,351 | 149,399,064 | 48.5 | % | 59.9 | % | |||||||||||||

| March 3, 2020 |

1,289,473,867 | 613,862,237 | 138,491,450 | 47.6 | % | 58.3 | % | |||||||||||||

| September 3, 2020 |

1,266,695,067 | 591,048,193 | 127,624,103 | 46.7 | % | 56.7 | % | |||||||||||||

| March 3, 2021 |

1,243,916,267 | 568,289,080 | 116,799,235 | 45.7 | % | 55.1 | % | |||||||||||||

| September 3, 2021 |

1,221,137,467 | 545,587,971 | 106,019,222 | 44.7 | % | 53.4 | % | |||||||||||||

| March 3, 2022 |

1,198,358,667 | 522,948,175 | 95,286,623 | 43.6 | % | 51.6 | % | |||||||||||||

| September 3, 2022 |

1,175,579,867 | 500,373,255 | — | 42.6 | % | 0.0 | % | |||||||||||||

| March 3, 2023 |

1,152,801,067 | 477,867,058 | — | 41.5 | % | 0.0 | % | |||||||||||||

| September 3, 2023 |

1,130,022,267 | 455,433,739 | — | 40.3 | % | 0.0 | % | |||||||||||||

| March 3, 2024 |

1,107,243,467 | 433,077,795 | — | 39.1 | % | 0.0 | % | |||||||||||||

| September 3, 2024 |

1,084,464,667 | 410,804,104 | — | 37.9 | % | 0.0 | % | |||||||||||||

| March 3, 2025 |

1,061,685,867 | 388,617,959 | — | 36.6 | % | 0.0 | % | |||||||||||||

| September 3, 2025 |

1,038,907,067 | 366,525,118 | — | 35.3 | % | 0.0 | % | |||||||||||||

| March 3, 2026 |

1,016,128,267 | 344,531,856 | — | 33.9 | % | 0.0 | % | |||||||||||||

| September 3, 2026 |

993,349,467 | — | — | 0.0 | % | 0.0 | % | |||||||||||||

| (1) | We have assumed that all Aircraft will be financed under this Offering prior to September 3, 2015, and that the appraised value of each Aircraft, determined as described under “—Equipment Notes and the Aircraft”, declines from that of the initial appraised value of such Aircraft by approximately 3% per year after the year of delivery of such Aircraft, in each case prior to the final expected Regular Distribution Date. Other rates or methods of depreciation may result in materially different LTVs. We cannot assure you that the depreciation rate and method used for purposes of the table will occur or predict the actual future value of any Aircraft. See “Risk Factors—Risk Factors Relating to the Certificates and the Offering—The Appraisals are only estimates of Aircraft value”. |

| (2) | In calculating the outstanding balances of each Class of Certificates, we have assumed that the Trusts will acquire the Equipment Notes for all Aircraft. Outstanding balances as of each Regular Distribution Date are shown after giving effect to distributions expected to be made on such distribution date. |

| (3) | The LTVs for each Class of Certificates were obtained for each Regular Distribution Date by dividing (i) the expected outstanding balance of such Class (together, in the case of the Class B Certificates, with the expected outstanding balance of the Class A Certificates) after giving effect to the distributions expected to be made on such distribution date, by (ii) the assumed value of all of the Aircraft on such date based on the assumptions described above. For purposes of these calculations, it has been assumed that United selects from the aircraft of each model eligible to be financed pursuant to this Offering the aircraft of such model with the earliest scheduled delivery dates from the manufacturer. The outstanding balances and LTVs of each Class of Certificates will change if the Trusts do not acquire Equipment Notes with respect to all the Aircraft. The LTVs will change if the Trusts acquire Equipment Notes with respect to the other aircraft from which United may choose. |

S-6

Table of Contents

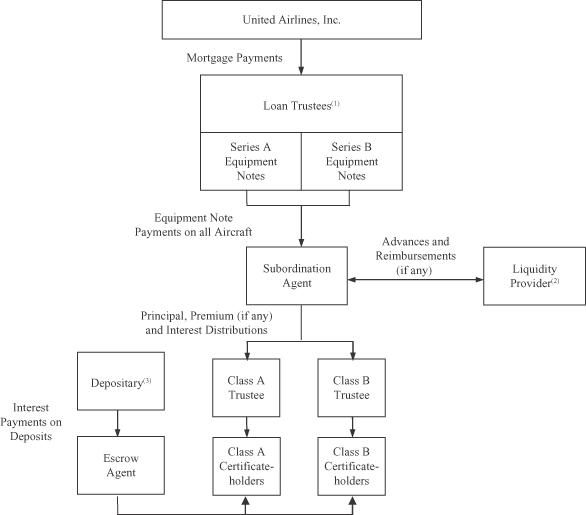

Set forth below is a diagram illustrating the structure for the offering of the Certificates and certain cash flows.

| (1) | The Equipment Notes with respect to each Aircraft will be issued under a separate Indenture. |

| (2) | The Liquidity Facility for each of the Class A Certificates and the Class B Certificates is expected to be sufficient to cover up to three consecutive semiannual interest payments with respect to such Class, except that the Liquidity Facilities will not cover interest on the Deposits. |

| (3) | The proceeds of the offering of each Class of Certificates will initially be held in escrow and deposited with the Depositary, pending financing of each Aircraft. The Depositary will hold such funds as interest bearing Deposits. Each Trust will withdraw funds from the Deposits relating to such Trust to purchase Equipment Notes from time to time as each Aircraft is financed. The scheduled payments of interest on the Equipment Notes and on the Deposits relating to a Trust, taken together, will be sufficient to pay accrued interest on the outstanding Certificates of such Trust. If any funds remain as Deposits with respect to a Trust at the Delivery Period Termination Date, such funds will be withdrawn by the Escrow Agent and distributed to the holders of the Certificates issued by such Trust, together with accrued and unpaid interest thereon. No interest will accrue with respect to the Deposits after they have been fully withdrawn. |

S-7

Table of Contents

| Certificates Offered |

• | Class A Pass Through Certificates, Series 2014-2. |

| • | Class B Pass Through Certificates, Series 2014-2. |

| Each Class of Certificates will represent a fractional undivided interest in a related Trust. |

| Use of Proceeds |

The proceeds from the sale of the Certificates of each Trust will initially be held in escrow and deposited with the Depositary, pending financing of each Aircraft under this Offering. Each Trust will withdraw funds from the Deposits relating to such Trust to acquire Equipment Notes as these Aircraft are financed. The Equipment Notes will be issued to finance the purchase by United of 27 new aircraft. |

| Subordination Agent, Trustee, Paying Agent and Loan Trustee |

Wilmington Trust, National Association. |

| Escrow Agent |

U.S. Bank National Association. |

| Depositary |

BNP Paribas, acting through its New York Branch. |

| Liquidity Provider |

BNP Paribas, acting through its New York Branch. |

| Trust Property |

The property of each Trust will include: |

| • | Equipment Notes acquired by such Trust. |

| • | All monies receivable under the Liquidity Facility for such Trust. |

| • | Funds from time to time deposited with the applicable Trustee in accounts relating to such Trust, including payments made by United on the Equipment Notes held in such Trust. |

| Regular Distribution Dates |

March 3 and September 3, commencing on March 3, 2015. |

| Record Dates |

The fifteenth day preceding the related Distribution Date. |

| Distributions |

The Trustee will distribute all payments of principal, premium (if any) and interest received on the Equipment Notes held in each Trust to the holders of the Certificates of such Trust, subject to the subordination provisions applicable to the Certificates. |

| Scheduled payments of principal and interest made on the Equipment Notes will be distributed on the applicable Regular Distribution Dates. |

| Payments of principal, premium (if any) and interest made on the Equipment Notes resulting from any early redemption of such Equipment Notes will be distributed on a special distribution date after not less than 15 days’ notice from the Trustee to the applicable Certificateholders. |

S-8

Table of Contents

| Subordination |

Distributions on the Certificates will be made in the following order: |

| • | First, to the holders of the Class A Certificates to pay interest on the Class A Certificates. |

| • | Second, to the holders of Class B Certificates to pay interest on the Preferred B Pool Balance. |

| • | Third, to the holders of the Class A Certificates to make distributions in respect of the Pool Balance of the Class A Certificates. |

| • | Fourth, to the holders of the Class B Certificates to pay interest on the Pool Balance of the Class B Certificates not previously distributed under clause “Second” above. |

| • | Fifth, to the holders of the Class B Certificates to make distributions in respect of the Pool Balance of the Class B Certificates. |

| Control of Loan Trustee |

The holders of at least a majority of the outstanding principal amount of Equipment Notes issued under each Indenture will be entitled to direct the Loan Trustee under such Indenture in taking action as long as no Indenture Default is continuing thereunder. If an Indenture Default is continuing, subject to certain conditions, the “Controlling Party” will direct the Loan Trustee under such Indenture (including in exercising remedies, such as accelerating such Equipment Notes or foreclosing the lien on the Aircraft securing such Equipment Notes). |

| The Controlling Party will be: |

| • | The Class A Trustee. |

| • | Upon payment of final distributions to the holders of Class A Certificates, the Class B Trustee. |

| • | Under certain circumstances, and notwithstanding the foregoing, the Liquidity Provider with the largest amount owed to it. |

| In exercising remedies during the nine months after the earlier of (a) the acceleration of the Equipment Notes issued pursuant to any Indenture or (b) the bankruptcy of United, the Equipment Notes and the Aircraft subject to the lien of such Indenture may not be sold for less than certain specified minimums. |

| Right to Purchase Other Classes of Certificates |

If United is in bankruptcy and certain specified circumstances then exist: |

| • | The Class B Certificateholders will have the right to purchase all but not less than all of the Class A Certificates. |

| • | If Additional Junior Certificates have been issued, the holders of such Additional Junior Certificates will have the right to purchase all but not less than all of the Class A and Class B Certificates. |

S-9

Table of Contents

| The purchase price in each case described above will be the outstanding balance of the applicable Class of Certificates plus accrued and unpaid interest. |

| Liquidity Facilities |

Under the Liquidity Facility for each of the Class A and Class B Trusts, the Liquidity Provider will, if necessary, make advances in an aggregate amount sufficient to pay interest on the applicable Certificates on up to three successive semiannual Regular Distribution Dates at the interest rate for such Certificates. Drawings under the Liquidity Facilities cannot be used to pay any amount in respect of the applicable Certificates other than interest and will not cover interest payable on amounts held in escrow as Deposits with the Depositary. |

| Notwithstanding the subordination provisions applicable to the Certificates, the holders of the Certificates to be issued by the Class A Trust or the Class B Trust will be entitled to receive and retain the proceeds of drawings under the Liquidity Facility for such Trust. |

| Upon each drawing under any Liquidity Facility to pay interest on the applicable Certificates, the Subordination Agent will reimburse the applicable Liquidity Provider for the amount of such drawing. Such reimbursement obligation and all interest, fees and other amounts owing to the Liquidity Provider under each Liquidity Facility and certain other agreements will rank equally with comparable obligations relating to the other Liquidity Facility and will rank senior to the Certificates in right of payment. |

| Escrowed Funds |

Funds in escrow for the Certificateholders of each Trust will be held by the Depositary as Deposits relating to such Trust. The Trustees may withdraw these funds from time to time to purchase Equipment Notes on or prior to the deadline established for purposes of this Offering. On each Regular Distribution Date, the Depositary will pay interest accrued on the Deposits relating to such Trust at a rate per annum equal to the interest rate applicable to the Certificates issued by such Trust. The Deposits relating to each Trust and interest paid thereon will not be subject to the subordination provisions applicable to the Certificates. The Deposits cannot be used to pay any other amount in respect of the Certificates. |

| Unused Escrowed Funds |

All of the Deposits held in escrow may not be used to purchase Equipment Notes by the deadline established for purposes of this Offering. This may occur because of delays in the financing of Aircraft or other reasons. See “Description of the Certificates—Obligation to Purchase Equipment Notes”. If any funds remain as Deposits with respect to any Trust after such deadline, such funds will be withdrawn by the Escrow Agent for such Trust and distributed, with accrued and unpaid interest, to the Certificateholders of such Trust after at least 15 days’ prior written notice. See “Description of the Deposit Agreements—Unused Deposits”. |

S-10

Table of Contents

| Obligation to Purchase Equipment Notes |

The Trustees will be obligated to purchase the Equipment Notes issued with respect to each Aircraft pursuant to the Note Purchase Agreement. United will enter into a secured debt financing with respect to each Aircraft pursuant to financing agreements substantially in the forms attached to the Note Purchase Agreement. The terms of such financing agreements must not vary the Required Terms set forth in the Note Purchase Agreement. In addition, United must certify to the Trustees that any substantive modifications do not materially and adversely affect the Certificateholders. United must also obtain written confirmation from each Rating Agency that the use of financing agreements modified in any material respect from the forms attached to the Note Purchase Agreement will not result in a withdrawal, suspension or downgrading of the rating of any Class of Certificates. The Trustees will not be obligated to purchase Equipment Notes if, at the time of issuance, United is in bankruptcy or certain other specified events have occurred. See “Description of the Certificates—Obligation to Purchase Equipment Notes”. |

| Issuances of Additional Classes of Certificates |

Additional pass through certificates of one or more separate pass through trusts, which will evidence fractional undivided ownership interests in equipment notes secured by Aircraft, may be issued. Any such transaction may relate to (a) the issuance of up to two new series of subordinated equipment notes with respect to some or all of the Aircraft at any time after the Issuance Date or (b) the refinancing of Series B Equipment Notes or either of such other series of subordinated equipment notes issued with respect to all (but not less than all) of the Aircraft secured by such refinanced notes at any time after the Delivery Period Termination Date. The holders of Additional Junior Certificates relating to other series of subordinated equipment notes, if issued, will have the right to purchase all of the Class A and B Certificates under certain circumstances after a bankruptcy of United at the outstanding principal balance of the Certificates to be purchased plus accrued and unpaid interest and other amounts due to Certificateholders, but without a premium. Consummation of any such issuance of additional pass through certificates will be subject to satisfaction of certain conditions, including, if issued after the Issuance Date, receipt of confirmation from the Rating Agencies that it will not result in a withdrawal, suspension or downgrading of the rating of any Class of Certificates that remains outstanding. See “Possible Issuance of Additional Junior Certificates and Refinancing of Certificates”. |

Equipment Notes

| (a) Issuer |

United. United’s executive offices are located at 233 S. Wacker Drive, Chicago, Illinois 60606. United’s telephone number is (872) 825-4000. |

| (b) Interest |

The Equipment Notes held in each Trust will accrue interest at the rate per annum for the Certificates issued by such Trust set forth on |

S-11

Table of Contents

| the cover page of this Prospectus Supplement. Interest will be payable on March 3 and September 3 of each year, commencing on the first such date after issuance of such Equipment Notes (but not before March 3, 2015). Interest is calculated on the basis of a 360-day year consisting of twelve 30-day months. |

| (c) Principal |

Principal payments on the Equipment Notes are scheduled on March 3 and September 3 of each year, commencing on March 3, 2016. |

| (d) Redemption |

Aircraft Event of Loss. If an Event of Loss occurs with respect to an Aircraft, all of the Equipment Notes issued with respect to such Aircraft will be redeemed, unless United replaces such Aircraft under the related financing agreements. The redemption price in such case will be the unpaid principal amount of such Equipment Notes, together with accrued interest, but without any premium. |

| Optional Redemption. United may elect to redeem all of the Equipment Notes issued with respect to an Aircraft prior to maturity only if all outstanding Equipment Notes with respect to all other Aircraft are simultaneously redeemed. In addition, United may elect to redeem all of the Series B Equipment Notes in connection with a refinancing of such Series. The redemption price for any optional redemption will be the unpaid principal amount of the relevant Equipment Notes, together with accrued interest and Make-Whole Premium. |

| (e) Security |

The Equipment Notes issued with respect to each Aircraft will be secured by a security interest in such Aircraft. |

| (f) Cross-collateralization |

The Equipment Notes held in the Trusts will be cross-collateralized. This means that any proceeds from the exercise of remedies with respect to an Aircraft will be available to cover shortfalls then due under Equipment Notes issued with respect to the other Aircraft. In the absence of any such shortfall, excess proceeds will be held by the relevant Loan Trustee as additional collateral for such other Equipment Notes. |

| (g) Cross-default |

There will be cross-default provisions in the Indentures. This means that if the Equipment Notes issued with respect to one Aircraft are in default and remedies are exercisable with respect to such Aircraft, the Equipment Notes issued with respect to the remaining Aircraft will also be in default, and remedies will be exercisable with respect to all Aircraft. |

| (h) Section 1110 Protection |

United’s outside counsel will provide its opinion to the Trustees that the benefits of Section 1110 of the U.S. Bankruptcy Code will be available with respect to the Equipment Notes. |

| Certain U.S. Federal Tax Consequences |

Each person acquiring an interest in Certificates generally should report on its federal income tax return its pro rata share of income from the relevant Deposits and income from the Equipment Notes and other property held by the relevant Trust. See “Certain U.S. Federal Tax Consequences”. |

S-12

Table of Contents

| Certain ERISA Considerations |

Each person who acquires a Certificate will be deemed to have represented that either: (a) no employee benefit plan assets have been used to purchase or hold such Certificate or (b) the purchase and holding of such Certificate are exempt from the prohibited transaction restrictions of ERISA and the Code pursuant to one or more prohibited transaction statutory or administrative exemptions. See “Certain ERISA Considerations”. |

| Fitch | Standard & Poor’s | |||||

| Threshold Rating for the Depositary | Long Term | A- | A- |

| Depositary Rating |

The Depositary meets the Depositary Threshold Rating requirement. |

| Fitch | Standard & Poor’s | |||||

| Threshold Rating for the Liquidity Provider for the Class A Trust | Long Term | BBB | BBB+ | |||

| Threshold Rating for the Liquidity Provider for the Class B Trust | Long Term | BBB | BBB+ | |||

| Liquidity Provider Rating |

The Liquidity Provider meets the Liquidity Threshold Rating requirements. |

S-13

Table of Contents

SUMMARY FINANCIAL AND OPERATING DATA

The following tables summarize certain consolidated financial and operating data with respect to United. This information was derived as follows:

Statement of operations data for the six months ended June 30, 2014 and 2013 was derived from the unaudited consolidated financial statements of United, including the notes thereto, included in United’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014. Statement of operations data for years ended December 31, 2013, 2012 and 2011 was derived from the audited consolidated financial statements of United, including the notes thereto, included in United’s Annual Report on Form 10-K filed with the Commission on February 20, 2014 (the “Form 10-K”).

The ratio of earnings to fixed charges for the six months ended June 30, 2014 was derived from Exhibit 12.2 of United’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014. The ratio of earnings to fixed charges for the years ended December 31, 2013, 2012, 2011, 2010 and 2009 was derived from Exhibit 12.2 to the Form 10-K.

Special charges (income) data for the six months ended June 30, 2014 and 2013 was derived from the unaudited consolidated financial statements of United, including the notes thereto, included in United’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014. Special revenue item and special charges (income) data for the years ended December 31, 2013, 2012 and 2011 was derived from the audited consolidated financial statements of United, including the notes thereto, included in the Form 10-K.

Balance sheet data as of June 30, 2014 was derived from the unaudited consolidated financial statements of United, including the notes thereto, included in United’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014. Balance sheet data as of December 31, 2013 and 2012 was derived from the audited consolidated financial statements of United, including the notes thereto, included in the Form 10-K.

| Six Months Ended June 30, |

Year Ended December 31, |

|||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

| (In millions) | (In millions) | |||||||||||||||||||

| Statement of Operations Data(1): |

||||||||||||||||||||

| Operating revenue |

$ | 19,025 | $ | 18,726 | $ | 38,287 | $ | 37,160 | $ | 37,119 | ||||||||||

| Operating expenses |

18,460 | 18,215 | 37,028 | 37,109 | 35,282 | |||||||||||||||

| Operating income |

565 | 511 | 1,259 | 51 | 1,837 | |||||||||||||||

| Net income (loss) |

189 | 122 | 654 | (661 | ) | 850 | ||||||||||||||

| Six Months Ended June 30, 2014 |

Year Ended December 31, |

|||||||||||||||||||||||

| 2013 | 2012 | 2011 | 2010(2) | 2009(2) | ||||||||||||||||||||

| Ratio of Earnings to Fixed Charges(3) |

1.21 | 1.37 | — | 1.41 | 1.21 | — | ||||||||||||||||||

| As of June 30, | As of December 31, | |||||||||||

| 2014 | 2013 | 2012 | ||||||||||

| (In millions) | (In millions) | |||||||||||

| Balance Sheet Data: |

||||||||||||

| Unrestricted cash, cash equivalents and short-term investments |

$ | 5,790 | $ | 5,115 | $ | 6,538 | ||||||

| Total assets |

38,931 | 37,286 | 38,095 | |||||||||

| Debt and capital leases(4) |

12,221 | 12,258 | 12,764 | |||||||||

| Stockholder’s equity |

3,577 | 3,223 | 1,161 | |||||||||

(Footnotes on the next page)

S-14

Table of Contents

| (1) | Includes the following special revenue item and expense (income) items: |

| Six Months Ended June 30, |

Year Ended December 31, |

|||||||||||||||||||

| Special revenue and special charges (income) |

2014 | 2013 | 2013 | 2012 | 2011 | |||||||||||||||

| (In millions) | (In millions) | |||||||||||||||||||

| Special revenue item |

$ | — | $ | — | $ | — | $ | — | $ | 107 | ||||||||||

| Special charges (income): |

||||||||||||||||||||

| Costs associated with permanently grounding Embraer ERJ 135 aircraft |

66 | — | — | — | — | |||||||||||||||

| Severance and benefits |

52 | 14 | 105 | 125 | — | |||||||||||||||

| Integration-related costs |

51 | 115 | 205 | 739 | 517 | |||||||||||||||

| Asset impairments |

33 | — | 33 | 30 | 4 | |||||||||||||||

| (Gains) losses on sale of assets and other special charges, net |

19 | (3 | ) | 32 | (46 | ) | 13 | |||||||||||||

| Additional costs associated with the temporarily grounded Boeing 787 aircraft |

— | 18 | 18 | — | — | |||||||||||||||

| Labor agreement costs |

— | — | 127 | 475 | — | |||||||||||||||

| Termination of a maintenance service contract |

— | — | — | — | 58 | |||||||||||||||

| (2) | As a result of the application of the acquisition method of accounting, the United financial statements prior to October 1, 2010 are not comparable with the financial statements for periods on or after October 1, 2010. |

| (3) | For purposes of calculating this ratio, earnings consist of income before income taxes and cumulative effect of changes in accounting principles adjusted for fixed charges, amortization of capitalized interest, distributed earnings of affiliates, interest capitalized and equity earnings in affiliates. Fixed charges consist of interest expense, the portion of rental expense representative of interest expense, the amount amortized for debt discount, premium and issuance expense and interest previously capitalized. For the years ended December 31, 2012 and 2009, earnings were inadequate to cover fixed charges by $689 million and $653 million, respectively. |

| (4) | Includes the current and noncurrent portions of debt and capital leases. |

S-15

Table of Contents

United transports people and cargo through its mainline operations, which utilize jet aircraft with at least 118 seats, and its regional operations, which utilize smaller aircraft that are operated under contract by United Express carriers. These regional operations are an extension of United’s mainline network.

| Six Months Ended June 30, |

Year Ended December 31, |

|||||||||||||||||||

| 2014 | 2013 | 2013 | 2012 | 2011 | ||||||||||||||||

| Mainline Operations: |

||||||||||||||||||||

| Passengers (thousands)(1) |

45,081 | 45,071 | 91,329 | 93,595 | 96,360 | |||||||||||||||

| Revenue passenger miles (millions)(2) |

87,438 | 87,267 | 178,578 | 179,416 | 181,763 | |||||||||||||||

| Available seat miles (millions)(3) |

104,989 | 104,829 | 213,007 | 216,330 | 219,437 | |||||||||||||||

| Cargo ton miles (millions) |

1,189 | 1,119 | 2,213 | 2,460 | 2,646 | |||||||||||||||

| Passenger load factor(4) |

83.3 | % | 83.2 | % | 83.8 | % | 82.9 | % | 82.8 | % | ||||||||||

| Passenger revenue per available seat mile (cents) |

12.38 | 12.18 | 12.20 | 11.93 | 11.84 | |||||||||||||||

| Average yield per revenue passenger mile (cents)(5) |

14.86 | 14.63 | 14.56 | 14.38 | 14.29 | |||||||||||||||

| Cost per available seat mile (cents) |

14.47 | 14.34 | 14.31 | 14.12 | 13.15 | |||||||||||||||

| Average price per gallon of fuel, including fuel taxes |

$ | 3.12 | $ | 3.15 | $ | 3.12 | $ | 3.27 | $ | 3.01 | ||||||||||

| Fuel gallons consumed (millions) |

1,568 | 1,575 | 3,204 | 3,275 | 3,303 | |||||||||||||||

| Average stage length (miles)(6) |

1,946 | 1,918 | 1,934 | 1,895 | 1,844 | |||||||||||||||

| Average daily utilization of each aircraft (hours)(7) |

10:21 | 10:25 | 10:28 | 10:38 | 10:42 | |||||||||||||||

| Regional Operations: |

||||||||||||||||||||

| Passengers (thousands)(1) |

22,656 | 23,236 | 47,880 | 46,846 | 45,439 | |||||||||||||||

| Revenue passenger miles (millions)(2) |

12,845 | 12,858 | 26,589 | 26,069 | 25,768 | |||||||||||||||

| Available seat miles (millions)(3) |

15,441 | 15,794 | 32,347 | 32,530 | 33,091 | |||||||||||||||

| Passenger load factor(4) |

83.2 | % | 81.4 | % | 82.2 | % | 80.1 | % | 77.9 | % | ||||||||||

| Consolidated Operations: |

||||||||||||||||||||

| Passengers (thousands)(1) |

67,737 | 68,307 | 139,209 | 140,441 | 141,799 | |||||||||||||||

| Revenue passenger miles (millions)(2) |

100,283 | 100,125 | 205,167 | 205,485 | 207,531 | |||||||||||||||

| Available seat miles (millions)(3) |

120,430 | 120,623 | 245,354 | 248,860 | 252,528 | |||||||||||||||

| Passenger load factor(4) |

83.3 | % | 83.0 | % | 83.6 | % | 82.6 | % | 82.2 | % | ||||||||||

| Passenger revenue per available seat mile (cents) |

13.59 | 13.45 | 13.50 | 13.09 | 12.87 | |||||||||||||||

| Average yield per revenue passenger mile (cents)(5) |

16.32 | 16.21 | 16.14 | 15.86 | 15.67 | |||||||||||||||

| (1) | The number of revenue passengers measured by each flight segment flown. |

| (2) | The number of scheduled miles flown by revenue passengers. |

| (3) | The number of seats available for passengers multiplied by the number of scheduled miles those seats are flown. |

| (4) | Revenue passenger miles divided by available seat miles. |

| (5) | The average passenger revenue received for each revenue passenger mile flown. |

| (6) | Average stage length equals the average distance a flight travels weighted for size of aircraft. |

| (7) | The average number of hours per day that an aircraft flown in revenue service is operated (from gate departure to gate arrival). |

S-16

Table of Contents

Unless the context otherwise requires, references in this “Risk Factors” section to “United” include its consolidated subsidiaries, and references to “UAL”, “the Company”, “we”, “us” and “our” mean UAL and its consolidated subsidiaries, including United.

Risk Factors Relating to the Company

Continued periods of historically high fuel prices or significant disruptions in the supply of aircraft fuel could have a material adverse impact on the Company’s operating results, financial position and liquidity.

Aircraft fuel has been the Company’s single largest operating expense for the last several years. The availability and price of aircraft fuel significantly affect the Company’s operations, results of operations, financial position and liquidity. While the Company has been able to obtain adequate supplies of fuel under various supply contracts and has some ability to store fuel close to major hub locations to ensure supply continuity in the short term, the Company cannot predict the continued future availability or price of aircraft fuel.

Continued volatility in fuel prices may negatively impact the Company’s liquidity or financial position in the future. Aircraft fuel prices can fluctuate based on a multitude of factors including market expectations of supply and demand balance, inventory levels, geopolitical events, economic growth expectations, fiscal/monetary policies and financial investment flows. The Company may not be able to increase its fares or other fees if fuel prices rise in the future and any such fare or fee increases may not be sustainable in the highly competitive airline industry. In addition, any increases in fares or other fees may not sufficiently offset the full impact of such increases in fuel prices and may also reduce the general demand for air travel.

To protect against increases in the prices of aircraft fuel, the Company routinely hedges a portion of its future fuel requirements. However, the Company’s hedging program may not be successful in controlling fuel costs, and price protection provided may be limited due to market conditions and other factors. To the extent that the Company uses hedge contracts that have the potential to create an obligation to pay upon settlement if prices decline significantly, including swaps or sold put options as part of a collar, such hedge contracts may limit the Company’s ability to benefit from lower fuel costs in the future. If fuel prices decline significantly from the levels existing at the time we enter into a hedge contract, we may be required to post collateral (margin) with our hedge counterparties beyond certain thresholds. Also, lower fuel prices may result in increased industry capacity and lower fares in general. There can be no assurance that the Company’s hedging arrangements will provide any particular level of protection against rises in fuel prices or that its counterparties will be able to perform under the Company’s hedging arrangements. Additionally, deterioration in the Company’s financial condition could negatively affect its ability to enter into new hedge contracts in the future and may potentially require the Company to post increased amounts of collateral under its fuel hedging agreements.

In addition, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and regulations promulgated by the Commodity Futures Trading Commission (the “CFTC”) require centralized clearing for over-the-counter derivatives and record-keeping and reporting requirements that are applicable to the Company’s fuel hedge contracts. The UAL Board of Directors has approved the Company’s election of the CFTC’s end-user exception, which permits the Company as a non-financial end user of derivatives to hedge commercial risk and be exempt from the CFTC mandatory clearing requirements. However, several of the Company’s hedge counterparties are also subject to these requirements, which may raise the counterparties’ costs. Those increased costs may in turn be passed on to the Company, resulting in increased transaction costs to execute hedge contracts and lower credit thresholds to post collateral (margin).

See Note 10 to the financial statements included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 and Note 7 to the financial statements included in the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014 for additional information on the Company’s hedging programs.

S-17

Table of Contents

Economic and industry conditions constantly change and unfavorable global economic conditions may have a material adverse effect on the Company’s business and results of operations.

The Company’s business and results of operations are significantly impacted by general economic and industry conditions. The airline industry is highly cyclical, and the level of demand for air travel is correlated to the strength of the U.S. and global economies. Robust demand for our air transportation services depends largely on favorable economic conditions, including the strength of the domestic and foreign economies, low unemployment levels, strong consumer confidence levels and the availability of consumer and business credit.

Air transportation is often a discretionary purchase that leisure travelers may limit or eliminate during difficult economic times. In addition, during periods of unfavorable economic conditions, business travelers usually reduce the volume of their travel, either due to cost-saving initiatives or as a result of decreased business activity requiring travel. During such periods, the Company’s business and results of operations may be adversely affected due to significant declines in industry passenger demand, particularly with respect to the Company’s business and premium cabin travelers, and a reduction in fare levels.

Stagnant or weakening global economic conditions either in the United States or in other geographic regions, and any future volatility in U.S. and global financial and credit markets may have a material adverse effect on the Company’s revenues, results of operations and liquidity. If such economic conditions were to disrupt capital markets in the future, the Company may be unable to obtain financing on acceptable terms (or at all) to refinance certain maturing debt and to satisfy future capital commitments.

The Company is subject to economic and political instability and other risks of doing business globally.

The Company is a global business with operations outside of the United States from which it derives approximately 40% of its operating revenues, as measured and reported in the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014. The Company’s operations in Asia, Europe, Latin America, Africa and the Middle East are a vital part of its worldwide airline network. Volatile economic, political and market conditions in these international regions may have a negative impact on the Company’s operating results and its ability to achieve its business objectives. In addition, significant or volatile changes in exchange rates between the U.S. dollar and other currencies, and the imposition of exchange controls or other currency restrictions, may have a material adverse impact upon the Company’s liquidity, revenues, costs and operating results.

During the three months ended March 31, 2014, the Company recorded $21 million of losses as part of Nonoperating income (expense): Miscellaneous, net due to ongoing negotiations applicable to funds held in local Venezuelan currency. Approximately $100 million of the Company’s unrestricted cash balance was held as Venezuelan bolivars as of June 30, 2014. The Company has not been able to repatriate its funds from Venezuela since January 2013, and there can be no assurance that the Company will be able to repatriate any or all of the funds held in Venezuelan bolivars in the future. Additionally, the amount and exchange rate at which the balance of funds will be repatriated are not certain at this time. If economic instability and devaluation of the local currency continue for a period of time in Venezuela, such conditions may have an adverse impact on the Company’s business.

Inadequate liquidity or a negative impact on the Company’s liquidity from factors beyond the Company’s control may have a material adverse effect on the Company’s financial position and business.

The Company has a significant amount of financial leverage from fixed obligations, including aircraft lease and debt financings, leases of airport property and other facilities, and other material cash obligations. In addition, the Company has substantial non-cancelable commitments for capital expenditures, including the acquisition of new aircraft and related spare engines.

S-18

Table of Contents

Although the Company’s cash flows from operations and its available capital, including the proceeds from financing transactions, have been sufficient to meet these obligations and commitments to date, the Company’s future liquidity could be negatively impacted by the risk factors discussed in this Prospectus Supplement under the heading “Risk Factors,” or in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 including, but not limited to, substantial volatility in the price of fuel, adverse economic conditions, disruptions in the global capital markets and catastrophic external events.

If the Company’s liquidity is constrained due to the various risk factors discussed in this Prospectus Supplement under the heading “Risk Factors” or in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 or otherwise, the Company might not be able to timely pay its debts or comply with certain operating and financial covenants under its financing and credit card processing agreements or with other material provisions of its contractual obligations. These covenants require the Company or United, as applicable, to maintain minimum liquidity and/or minimum collateral coverage ratios, depending on the particular agreement. The Company’s ability to comply with these covenants may be affected by events beyond its control, including the overall industry revenue environment, the level of fuel costs and the appraised value of certain collateral. If the Company does not timely pay its debts or comply with such covenants, a variety of adverse consequences could result. These potential adverse consequences include an increase of required reserves under credit card processing agreements, withholding of credit card sale proceeds by its credit card service providers, loss of undrawn lines of credit, occurrence of an event of default under the relevant agreement(s), acceleration of the maturity of debt and/or exercise of other remedies by its creditors and equipment lessors that could result in a material adverse effect on the Company’s financial position and results of operations. The Company cannot provide assurance that it would have sufficient liquidity to repay or refinance such debt if it were accelerated. In addition, an event of default or declaration of acceleration under certain of its financing agreements could result in an event of default under certain of the Company’s other financing agreements due to cross default and cross acceleration provisions. Furthermore, constrained liquidity may limit the Company’s ability to withstand competitive pressures and limit its flexibility in responding to changing business and economic conditions, including increased competition and demand for new services, placing the Company at a disadvantage when compared to its competitors that have less debt, and making the Company more vulnerable than its competitors who have less debt to a downturn in the business, industry or the economy in general.

The Company’s substantial level of indebtedness and non-investment grade credit rating, as well as market conditions and the availability of assets as collateral for loans or other indebtedness, may make it difficult for the Company to raise additional capital to meet its liquidity needs on acceptable terms, or at all.

See Management’s Discussion and Analysis of Financial Condition and Results of Operations, included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 and in the Company’s Quarterly Report on Form 10-Q for the quarter ended June 30, 2014 for further information regarding the Company’s liquidity.

Extensive government regulation could increase the Company’s operating costs and restrict its ability to conduct its business.

Airlines are subject to extensive regulatory and legal oversight. Compliance with U.S. and international regulations imposes significant costs and may have adverse effects on the Company. Laws, regulations, taxes and airport rates and charges, both domestically and internationally, have been proposed from time to time that could significantly increase the cost of airline operations or reduce airline revenue. The Company cannot provide any assurance that current laws and regulations, or laws or regulations enacted in the future, will not adversely affect its financial condition or results of operations.

United provides air transportation under certificates of public convenience and necessity issued by the U.S. Department of Transportation (the “DOT”). If the DOT altered, amended, modified, suspended or revoked these certificates, it could have a material adverse effect on the Company’s business. The DOT is also responsible for

S-19

Table of Contents

promulgating consumer protection and other regulations such as the rule against lengthy tarmac delays, that will impose significant compliance costs on the Company. The Federal Aviation Administration (“FAA”) regulates the safety of United’s operations. United operates pursuant to an air carrier operating certificate issued by the FAA. On January 4, 2014, the FAA’s new and more stringent pilot flight and duty time requirements under Part 117 of the Federal Aviation Regulations took effect, which will disrupt operations and increase costs. In August 2013, the FAA significantly increased the minimum qualifications for air carrier first officers. These new regulations impact the Company and its regional partner flying, as they have caused mainline airlines to hire regional pilots, while simultaneously significantly reducing the pool of new pilots from which regional carriers themselves can hire. Although this is an industry issue, it directly affects the Company and requires it to reduce regional partner flying, as several regional partners are beginning to have difficulty flying their schedules due to reduced new pilot availability. From time to time, the FAA also issues orders, airworthiness directives and other regulations relating to the maintenance and operation of aircraft that require material expenditures or operational restrictions by the Company. These FAA orders and directives could include the temporary grounding of an entire aircraft type if the FAA identifies design, manufacturing, maintenance or other issues requiring immediate corrective action. FAA requirements cover, among other things, retirement of older aircraft, security measures, collision avoidance systems, airborne windshear avoidance systems, noise abatement and other environmental concerns, aircraft operation and safety and increased inspections and maintenance procedures to be conducted on older aircraft. These FAA directives or requirements could have a material adverse effect on the Company. Also, beginning in March 2014, the Occupational Safety and Health Administration’s regulatory programs for hazard communication, hearing conservation and blood borne pathogens in the areas of cabin crewmember safety and health is expected to expose the Company to increased regulatory requirements in the aircraft cabin, with associated increased costs and the possibility for operational impacts.

In addition, the Company’s operations may be adversely impacted due to the existing antiquated air traffic control (“ATC”) system utilized by the U.S. government. During peak travel periods in certain markets, the current ATC system’s inability to handle existing travel demand has led to short-term capacity constraints imposed by government agencies and resulted in delays and disruptions of air traffic. In addition, the current system will not be able to effectively handle projected future air traffic growth. Imposition of these ATC constraints on a long-term basis may have a material adverse effect on our results of operations. Failure to update the ATC system in a timely manner, and the substantial funding requirements of a modernized ATC system that may be imposed on air carriers may have an adverse impact on the Company’s financial condition or results of operations.

The airline industry is subject to extensive federal, state and local taxes and fees that increase the cost of the Company’s operations. In addition to taxes and fees that the Company is currently subject to, proposed taxes and fees are currently pending and if imposed, would increase the Company’s operating expenses. The Bipartisan Budget Act of 2013, signed into law on December 26, 2013, increases the September 11th security fee, effective July 1, 2014. The increase is expected to result in over $3 billion in additional taxation on the industry over the next decade and may result in higher fares and lower demand for air travel.

Access to landing and take-off rights, or “slots,” at several major U.S. airports and many foreign airports served by the Company are, or recently have been, subject to government regulation. Certain of the Company’s major hubs are among increasingly congested airports in the United States and have been or could be the subject of regulatory action that might limit the number of flights and/or increase costs of operations at certain times or throughout the day. The FAA may limit the Company’s airport access by limiting the number of departure and arrival slots at high density traffic airports, which could affect the Company’s ownership and transfer rights, and local airport authorities may have the ability to control access to certain facilities or the cost of access to its facilities, which could have an adverse effect on the Company’s business. The FAA historically has taken actions with respect to airlines’ slot holdings that airlines have challenged; if the FAA were to take actions that adversely affect the Company’s slot holdings, the Company could incur substantial costs to preserve its slots. Further, the Company’s operating costs at airports at which it operates, including the Company’s major hubs, may increase significantly because of capital improvements at such airports that the Company may be required to fund,

S-20

Table of Contents

directly or indirectly. In some circumstances, such costs could be imposed by the relevant airport authority without the Company’s approval and may have a material adverse effect on the Company’s financial condition.

The ability of carriers to operate flights on international routes between airports in the United States and other countries may be subject to change. Applicable arrangements between the United States and foreign governments may be amended from time to time, government policies with respect to airport operations may be revised, and the availability of appropriate slots or facilities may change. The Company currently operates a number of flights on international routes under government arrangements, regulations or policies that designate the number of carriers permitted to operate on such routes, the capacity of the carriers providing services on such routes, the airports at which carriers may operate international flights, or the number of carriers allowed access to particular airports. Any further limitations, additions or modifications to such arrangements, regulations or policies could have a material adverse effect on the Company’s financial position and results of operations. Additionally, a change in law, regulation or policy for any of the Company’s international routes, such as open skies could have a material adverse impact on the Company’s financial position and results of operations and could result in the impairment of material amounts of related tangible and intangible assets. In addition, competition from revenue-sharing joint ventures and other alliance arrangements by and among other airlines could impair the value of the Company’s business and assets on the open skies routes. The Company’s plans to enter into or expand U.S. antitrust immunized alliances and joint ventures on various international routes are subject to receipt of approvals from applicable U.S. federal authorities and obtaining other applicable foreign government clearances or satisfying the necessary applicable regulatory requirements. There can be no assurance that such approvals and clearances will be granted or will continue in effect upon further regulatory review or that changes in regulatory requirements or standards can be satisfied.

Many aspects of the Company’s operations are also subject to increasingly stringent federal, state, local and international laws protecting the environment. Future environmental regulatory developments, such as climate change regulations in the United States and abroad could adversely affect operations and increase operating costs in the airline industry. There are certain climate change laws and regulations that have already gone into effect and that apply to the Company, including the European Union Emissions Trading Scheme (which is subject to international dispute), the State of California’s cap and trade regulations, environmental taxes for certain international flights, limited greenhouse gas reporting requirements and land-use planning laws which could apply to airports and could affect airlines in certain circumstances. In addition, there is the potential for additional regulatory actions in regard to the emission of greenhouse gases by the aviation industry. The precise nature of future requirements and their applicability to the Company are difficult to predict, but the financial impact to the Company and the aviation industry would likely be adverse and could be significant.

The Company’s business and operations may also be impacted by a lack of funding and, in turn, sequestration procedures at the federal government level. In April 2013, for example, the FAA implemented furloughs of air traffic controllers through its capacity reduction plan, resulting in flight delays throughout the United States, including to the Company’s flights, until the U.S. Congress passed a bill suspending such furloughs. Although the U.S. Congress allocated resources under the Bipartisan Budget Act of 2013 that is expected to be in effect for the 2014 and 2015 fiscal years, the risk of future lack of funding and related sequestration obligations by the FAA, the Transportation Security Administration, the U.S. Customs and Border Protection or other federal agencies remains, potentially resulting in a material adverse impact on the Company.

See Item 1, Business—Industry Regulation, of the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 for further information on government regulation impacting the Company.

The Company relies heavily on technology and automated systems to operate its business and any significant failure or disruption of the technology or these systems could materially harm its business.

The Company depends on automated systems and technology to operate its business, including computerized airline reservation systems, flight operations systems, revenue management systems, accounting systems, telecommunication systems and commercial websites, including www.united.com. United’s website and

S-21

Table of Contents

other automated systems must be able to accommodate a high volume of traffic, maintain secure information and deliver important flight and schedule information, as well as process critical financial transactions. These systems could suffer substantial or repeated disruptions due to various events, some of which are beyond the Company’s control, including natural disasters, power failures, terrorist attacks, equipment or software failures, computer viruses or cyber security attacks. Substantial or repeated systems failures or disruptions, including failures or disruptions related to the Company’s complex integration of systems, could reduce the attractiveness of the Company’s services versus those of its competitors, materially impair its ability to market its services and operate its flights, result in the unauthorized release of confidential or otherwise protected information, result in increased costs, lost revenue and the loss or compromise of important data, and may adversely affect the Company’s business, results of operations and financial condition.

The Company is subject to increasing legislative and regulatory and customer focus on privacy issues and data security.

The Company is subject to increasing legislative and regulatory and customer focus on privacy issues and data security. A number of our commercial partners, including credit card companies, have imposed data security standards that the Company must meet and these standards continue to evolve. The Company will continue its efforts to meet new and increasing privacy and security standards; however, it is possible that certain new standards may be difficult to meet and could increase the Company’s costs. Additionally, any compromise of the Company’s technology systems could result in the loss, disclosure, misappropriation of or access to customers’, employees’ or business partners’ information. Any such loss, disclosure, misappropriation or access could result in legal claims or proceedings, liability or regulatory penalties under laws protecting the privacy of personal information. Any significant data breach or the Company’s failure to comply with applicable U.S. and foreign privacy or data security regulations or security standards imposed by our commercial partners may adversely affect the Company’s reputation, business, results of operations and financial condition.

The Company’s business relies extensively on third-party service providers. Failure of these parties to perform as expected, or interruptions in the Company’s relationships with these providers or their provision of services to the Company, could have an adverse effect on the Company’s financial position and results of operations.

The Company has engaged an increasing number of third-party service providers to perform a large number of functions that are integral to its business, including regional operations, operation of customer service call centers, distribution and sale of airline seat inventory, provision of information technology infrastructure and services, provision of aircraft maintenance and repairs, provision of various utilities and performance of aircraft fueling operations, among other vital functions and services. The Company does not directly control these third-party service providers, although it does enter into agreements with many of them that define expected service performance. Any of these third-party service providers, however, may materially fail to meet their service performance commitments to the Company, may suffer disruptions to their systems that could impact their services, or the agreements with such providers may be terminated. For example, flight reservations booked by customers and/or travel agencies via third-party global distribution systems (“GDS”) may be adversely affected by disruptions in the business relationships between the Company and GDS operators. Such disruptions, including a failure to agree upon acceptable contract terms when contracts expire or otherwise become subject to renegotiation, may cause the carriers’ flight information to be limited or unavailable for display, significantly increase fees for both the Company and GDS users, and impair the Company’s relationships with its customers and travel agencies. The failure of any of the Company’s third-party service providers to adequately perform their service obligations, or other interruptions of services, may reduce the Company’s revenues and increase its expenses or prevent the Company from operating its flights and providing other services to its customers. In addition, the Company’s business and financial performance could be materially harmed if its customers believe that its services are unreliable or unsatisfactory.

S-22

Table of Contents

UAL’s obligations for funding United’s defined benefit pension plans are affected by factors beyond UAL’s control.

The Company maintains two primary defined benefit pension plans, one covering certain pilot employees and another covering certain U.S. non-pilot employees. The timing and amount of UAL’s funding requirements under these plans depend upon a number of factors, including labor negotiations with the applicable employee groups and changes to pension plan benefits as well as factors outside of UAL’s control, such as the number of applicable retiring employees, asset returns, interest rates and changes in pension laws. Changes to these and other factors that can significantly increase UAL’s funding requirements, such as its liquidity requirements, could have a material adverse effect on UAL’s financial condition.

Union disputes, employee strikes or slowdowns, and other labor-related disruptions, as well as the integration of United’s workforces in connection with the October 1, 2010 merger could adversely affect the Company’s operations, and could result in increased costs that impair its financial performance.

United is a highly unionized company. As of December 31, 2013, the Company and its subsidiaries had approximately 87,000 active employees, of whom approximately 80% were represented by various U.S. labor organizations.

The successful integration of United’s workforces in connection with the October 1, 2010 merger pursuant to which Continental became a wholly-owned subsidiary of UAL Corporation, now known as United Continental Holdings, Inc. (the “Merger”), and achievement of the anticipated benefits of the combined company depend in part on integrating employee groups and maintaining productive employee relations. In order to fully integrate the pre-Merger represented employee groups, the Company must negotiate a joint collective bargaining agreement covering each combined group. The process for integrating the labor groups is governed by a combination of the Railway Labor Act (the “RLA”), the McCaskill-Bond Amendment, and where applicable, the existing provisions of collective bargaining agreements and union policies. A delay in or failure to integrate employee groups presents the potential for increased operating costs and labor disputes that could adversely affect our operations.

The Company can provide no assurance that a successful or timely resolution of labor negotiations for all amendable collective bargaining agreements will be achieved. There is a risk that unions or individual employees might pursue judicial or arbitral claims arising out of changes implemented as a result of the Merger. There is also a possibility that employees or unions could engage in job actions such as slow-downs, work-to-rule campaigns, sick-outs or other actions designed to disrupt the Company’s normal operations, in an attempt to pressure the Company in collective bargaining negotiations. Although the RLA makes such actions unlawful until the parties have been lawfully released to self-help, and the Company can seek injunctive relief against premature self-help, such actions can cause significant harm even if ultimately enjoined. In addition, achieving joint collective bargaining agreements with our represented employee groups is likely to increase our labor costs, which increase could be material.