UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

|

[X] |

ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the fiscal year ended December 31, 2015

|

[ ] |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. |

For the transition period from _______ to ______

Commission file number: 001-36335

|

|

ENSERVCO CORPORATION

(Exact name of registrant as specified in its charter)

|

Delaware |

84-0811316 | |

|

(State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

|

501 South Cherry St., Ste. 1000 Denver, CO |

80246 | |

|

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number: (303) 333-3678

Securities registered pursuant to Section 12(b) of the Securities Exchange Act:

|

Title of each class |

Name of each exchange on which registered |

|

Common stock, $0.005 par value |

NYSE MKT |

Securities registered pursuant to Section 12(g) of the Securities Exchange Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act: ☐ Yes ☑ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act: ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).☑ Yes ☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☑

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Securities Exchange Act of 1934.

|

Large accelerated filer ☐ |

|

|

|

Accelerated filer ☐ |

|

Non-accelerated filer ☐ |

|

|

|

Smaller reporting company ☑ |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ☐ No ☑

The aggregate market value of the common stock held by non-affiliates of the Registrant was approximately $28,447,592 based upon the closing sale price of the Registrant’s Common Stock of $1.50 as of June 30, 2015, the last trading day of the registrant’s most recently completed second fiscal quarter. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 22, 2016, there were 38,130,160 shares of the Enservco Corporation’s common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the registrant’s definitive information statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A not later than 120 days after the registrant's fiscal year ended December 31, 2015, in connection with the registrant’s 2016 Annual Meeting of Shareholders, are incorporated herein by reference into Part III of this Annual Report on Form 10-K.

PART I

ITEM 1. BUSINESS

Enservco Corporation (“Enservco”) and its wholly-owned subsidiaries (collectively referred to as the “Company”, “we” or “us”) provides well enhancement and fluid management services to the domestic onshore oil and natural gas industry. These services include frac water heating, hot oiling and acidizing (well enhancement services), and water transfer, water treatment, water hauling, fluid disposal, frac tank rental (fluid management services) and other general oilfield services. The Company owns and operates a fleet of more than 340 specialized trucks, trailers, frac tanks and other well-site related equipment and serves customers in several major domestic oil and gas fields including the DJ Basin/Niobrara field in Colorado, the Bakken field in North Dakota, the Marcellus and Utica Shale fields in Pennsylvania and Ohio, the Jonah Field, Green River and Powder River Basins in Wyoming, the Eagle Ford Shale in Texas and the Mississippi Lime and Hugoton Fields in Kansas and Oklahoma.

Enservco was originally incorporated as Aspen Exploration Corporation under the laws of the State of Delaware on February 28, 1980 for the primary purpose of acquiring, exploring and developing oil and natural gas and other mineral properties. During the first half of 2009, Aspen disposed of its oil and natural gas producing assets and as a result was no longer engaged in active business operations. On June 24, 2010, Aspen entered into an Agreement and Plan of Merger and Reorganization with Dillco Fluid Service, Inc. (“Dillco”) which set forth the terms by which Dillco became a wholly owned subsidiary of Aspen on July 27, 2010 (the “Merger Transaction”). On December 30, 2010, Aspen changed its name to “Enservco Corporation.” As such, throughout this report the terms the “Company” and/or “Enservco” are intended to refer to the Company on a post-Merger Transaction basis and as a whole, with respect to both historical and forward looking contexts.

The Company’s executive (or corporate) offices are located at 501 South Cherry St., Ste. 1000, Denver, CO 80246. Our telephone number is (303) 333-3678, and our facsimile number is (720) 974-3417. Our website is www.enservco.com.

Cautionary Note Regarding Forward-Looking Statements

The information discussed in this annual report on Form 10-K as well as some statements in press releases and some oral statements of the Company’s officers during presentations about the Company include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”). All statements, other than statements of historical facts, included herein and therein concerning, among other things, planned capital expenditures, future cash flows and borrowings, pursuit of potential acquisition opportunities, our financial position, business strategy and other plans and objectives for future operations, are forward-looking statements. These forward-looking statements are identified by their use of terms and phrases such as “may,” “expect,” “estimate,” “project,” “plan,” “believe,” “intend,” “achievable,” “anticipate,” “will,” “continue,” “potential,” “should,” “could,” and similar terms and phrases. Although we believe that the expectations reflected in these forward-looking statements are reasonable, they do involve certain assumptions, risks and uncertainties and are not (and should not considered to be) guarantees of future performance. Our results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including, among others:

|

● |

Our capital requirements and the uncertainty of being able to obtain additional funding on terms acceptable to us; |

|

● |

The volatility of domestic and international oil and natural gas prices and the resulting impact on production and drilling activity, and the effect that lower prices may have on our customers’ demand for our services, the result of which may adversely impact our revenues and financial performance; |

|

● |

The broad geographical diversity of our operations which, while expected to diversify the risks related to a slow-down in one area of operations, also adds to our costs of doing business; |

|

● |

The financial constraints imposed as a result of our indebtedness, including restrictions imposed on us under the terms of our credit facility agreement and our need to generate sufficient cash flows to repay our debt obligations; |

|

● |

Our history of losses and working capital deficits which, at times, were significant; |

|

● |

Adverse weather and environmental conditions; |

|

● |

Our reliance on a limited number of customers; |

|

● |

Our ability to retain key members of our senior management and key technical employees; |

|

● |

The potential impact of environmental, health and safety, and other governmental regulations, and of current or pending legislation with which we and our customers must comply; |

|

● |

Developments in the global economy; |

|

● |

Changes in tax laws; |

|

● |

The effects of competition; |

|

● |

The effect of seasonal factors; and |

|

● |

The effect of further sales or issuances of our common stock and the price and volume volatility of our common stock. |

Finally, our future results will depend upon various other risks and uncertainties, including, but not limited to, those detailed in the section entitled “Risk Factors” included elsewhere in this annual report. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this section and elsewhere in this annual report. Other than as required under securities laws, we do not assume a duty to update these forward-looking statements, whether as a result of new information, subsequent events or circumstances, changes in expectations or otherwise.

Corporate Structure

The Company’s business operations are conducted primarily through Heat Waves and Dillco. The below table provides an overview of the Company’s current subsidiaries and their activities.

|

Name |

State of Formation |

Ownership |

Business |

|

Heat Waves Hot Oil Service LLC (“Heat Waves”) |

Colorado |

100% by Enservco |

Oil and natural gas well services, including logistics and stimulation. |

|

Dillco Fluid Service, Inc. (“Dillco”) |

Kansas |

100% by Enservco |

Oil and natural gas field fluid logistic services primarily in the Hugoton Basin in western Kansas and northwestern Oklahoma. |

|

Heat Waves Water Management LLC (“HWWM”) |

Colorado |

100% by Enservco |

Water Transfer and Water Treatment Services |

|

HE Services, LLC (“HES”) |

Nevada |

100% by Heat Waves |

No active business operations. Owns construction equipment used by Heat Waves. |

|

Real GC, LLC (“Real GC”) |

Colorado |

100% by Heat Waves |

No active business operations. Owns real property in Garden City, Kansas that is used by Heat Waves. |

On November 24, 2015, Heat Waves Water Management LLC (“HWWM”) was organized under the laws of the state of Colorado as a wholly owned subsidiary of Enservco for the purposes of launching a new water management division. Effective January 1, 2016, HWWM acquired the water transfer assets from WET Oil Services, LLC- including vehicles, high and low volume pumps, manifolds, pipe, and other support equipment for water transfer operations. In addition, effective January 1, 2016, HWWM acquired a new water treatment technology utilized in devices sold under the name of HydroFLOW and various other water transfer assets including high and low volume pumps, lay flat hose, trailers, generators, pipe and other equipment from HII Technologies, Inc. and its affiliates (“HIIT”). The total purchase price for both acquisitions was approximately $4.0 million dollars. HydroFLOW products offer water treatment services based on patented hydropath technology that can remove bacteria and scale from water using electrical induction to reduce or eliminate down-hole scaling and corrosion. HWWM will provide water transfer services and water treatment services to the onshore oil and natural gas sector.

Overview of Business Operations

As described above, the Company primarily conducts its business operations through its principal operating subsidiaries, Heat Waves, HWWM, and Dillco, which provide oil field services to the domestic onshore oil and natural gas industry. These services include frac water heating, hot oiling, pressure testing, acidizing, water transfer, bacteria and scale treatment, freshwater and saltwater hauling, fluid disposal, frac tank rental, well site construction and other general oil field services. As described in the table above, certain assets utilized by Heat Waves and Dillco in their business operations are owned by other subsidiary entities. The Company currently operates in the following geographic regions:

|

● |

Eastern USA Region, including the southern region of the Marcellus Shale formation (southwestern Pennsylvania and northern West Virginia) and the Utica Shale formation in eastern Ohio. The Eastern USA Region operations are deployed from Heat Waves’ operations center in Carmichaels, Pennsylvania which opened in the first quarter of 2011. |

|

● |

Rocky Mountain Region, including western Colorado and southern Wyoming (D-J Basin and Niobrara formations), central Wyoming (Powder River and Green River Basins) and western North Dakota and eastern Montana (Bakken formation). The Rocky Mountain Region operations are deployed from Heat Waves’ operations centers in Killdeer, North Dakota, Tioga, North Dakota, Rock Springs, Wyoming and Platteville, Colorado. |

|

● |

Central USA Region, including the Mississippi Lime and Hugoton Field in southwestern Kansas, Texas panhandle, and northwestern Oklahoma, and the Eagle Ford Shale in south Texas. The Central USA Region operations are deployed from operations centers in Garden City, Kansas, Hugoton, Kansas, Okarche, Oklahoma, and Jourdanton, Texas. |

Management believes that the Company is strategically positioned with its ability to provide its services to a large customer base in key oil and natural gas basins in the United States notwithstanding the current depressed state of the oil and natural gas industry. Management is optimistic that as a result of the significant expenditures the Company has made in new equipment in combination with expanding into new basins and geographical locations, the Company will be able to further grow and develop its business operations when the industry rebounds, although our ability to do so is clearly subject to domestic and international conditions in the oil and gas industry which have been adversely impacted by the substantial decline in crude oil prices since July 2014.

Historically, the Company focused its growth strategy on strategic acquisitions of operating companies and then expanding operations through additional capital investment consisting of the acquisition and fabrication of property and equipment. That strategy also included expanding the Company’s geographical footprint as well as expanding the services it provides. These strategies are exemplified by the acquisitions of operating entities (described in the Operating Entities section below) and:

|

(1) |

In 2014 and 2015, the Company spent approximately $24 million, and $4.5 million, respectively, for the acquisition and fabrication of additional frac water heating, hot oiling, and acidizing equipment; and |

|

(2) |

To expand its footprint, in early 2010 Heat Waves began providing services in the Marcellus Shale natural gas field in southwestern Pennsylvania and West Virginia, and in September 2011 Heat Waves extended its services into the D-J Basin / Niobrara formation and the Bakken formation through opening new operation centers in southern Wyoming and western North Dakota, respectively. In late 2012 the Company expanded its operations, through its Pennsylvania operation center, into the Utica Shale formation in eastern Ohio. Also, in mid-2015 the Company expanded its operations into the Eagle Ford formation through opening a new operations center in southern Texas. |

|

(3) |

To expand its services, in January 2016, Enservco acquired assets for approximately $4.0 million in order to provide water transfer services and bacteria and scaling treatment solutions to its customers in all of its operating areas. |

Going forward, and subject to the availability of adequate financing, the Company expects to continue to pursue its growth strategies of exploring additional acquisitions, potentially expanding the geographic areas in which it operates, and diversifying the products and services it provides to customers, as well as making further investments in its assets and equipment.

Operating Entities

As noted above, the Company conducts its business operations and holds assets primarily through its subsidiary entities. The following describes the operations and assets of the Company’s subsidiaries through which the Company conducts its business operations.

Dillco. From its inception in 1974, Dillco has focused primarily on providing water hauling/disposal/storage services, well site construction services and frac tank rental to energy companies working in the Hugoton gas field in western Kansas and northwestern Oklahoma. Water hauling and disposal services have been the primary sources of Dillco’s revenue. Dillco currently owns and operates a fleet of water hauling trucks and related assets, including specialized tank trucks, frac tanks, water disposal wells, construction and other related equipment. These assets transport, store and dispose of both fresh and salt water, as well as provide well site construction and maintenance services.

Heat Waves. Heat Waves provides a range of well stimulation/maintenance services to a diverse group of independent and major oil and natural gas companies. The primary services provided are intended to:

|

(1) |

Assist in the fracturing of formations for newly drilled oil and natural gas wells; and |

|

(2) |

Help maintain and enhance the production of existing wells throughout their productive life. |

These services consist of frac water heating, hot oiling and acidizing. Heat Waves also provides some water hauling and well site construction services. Heat Waves’ operations are currently in southwestern Kansas, Texas panhandle, northwestern Oklahoma, southern and central Wyoming (Niobrara formation), Colorado (D-J Basin), southwest Pennsylvania/ northwestern West Virginia (Marcellus Shale) region, eastern Ohio (Utica Shale), western North Dakota and eastern Montana (Bakken formation), and southern Texas (Eagle Ford Shale).

HWWM. HWWM was organized in November 2015 as a new wholly owned subsidiary of Enservco for the purpose of launching a new water management division. In connection therewith, HWWM acquired approximately $4 million of water management assets from HIIT and WET in January 2016.

HWWM will provide water transfer services, bacteria and scaling treatment solutions, and equipment rental to customers in the oil and natural gas industry. Water transfer entails using high and low volume pumps, lay flat hose, aluminum pipe and manifolds to move fresh and/or recycled water from a water source such as a pond, lake, river, stream, or water storage facility to frac tanks at drilling locations to be used in connection with well completion activities. In addition to providing traditional water transfer services, HWWM will also utilize a patented hydropath technology (distributed under the name of HydroFLOW) to provide bacteria and scaling treatment services to the oil and gas industry. HydroFLOW utilizes electrical induction to reduce or eliminate down-hole scaling and corrosion and to reduce or eliminate bacteria in water. The hydropath technology is owned by HydroPath Holdings Limited. Pursuant to a Sales Agreement with the North American master distributor, HydroFLOW U.S.A., HWWM has the exclusive right to sell or rent HydroFLOW devices in connection with bacteria deactivation and scale treatment services for treating injection and disposal wells, fracking water and recycled water in the oil and gas industry to customers in the United States (except in Texas where the right regarding injection and disposal wells is exclusive to only 20 companies but non-exclusive for the remaining companies in Texas). We believe this lower-cost and environmentally friendly alternative to conventional chemical treatment of frac and recycled water will significantly reduce the use, and therefore cost, of chemicals now used by oil and gas companies.

HES. HES owns construction and related equipment that Heat Waves used in its well site construction and maintenance services. However, HES does not currently engage in any business activities itself. HES also owns a disposal well near Garden City, Kansas that Dillco uses for salt water disposal.

Products and Services

The Company, through its operating subsidiaries, provides a range of services to owners and operators of oil and natural gas wells. Such services can generally be grouped into the three following categories:

|

(1) |

Well enhancement services, i.e., hot oiling, acidizing, frac water heating, and pressure testing, |

|

(2) |

Fluid management services, i.e., water transfer, water treatment, water/fluid hauling, frac tank rental, and disposal services; and |

|

(3) |

Well site construction and roustabout services. |

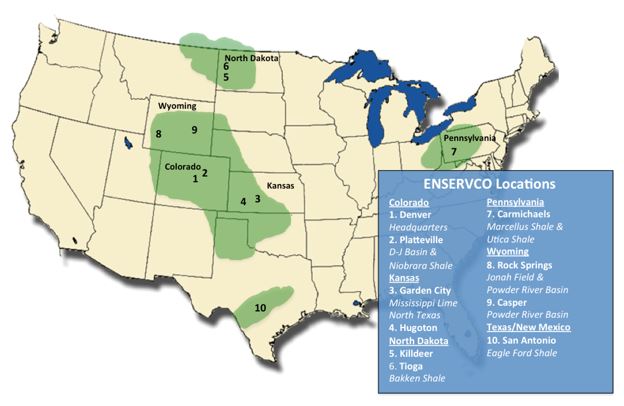

The following map shows the primary areas in which Heat Waves and Dillco currently have active business operations.

|

|

The following is a more complete description of the services provided by The Company through its subsidiaries.

Well Enhancement Services.

Well enhancement services consist of frac water heating, acidizing, hot oiling services, and pressure testing. These services are provided primarily by Heat Waves which currently utilizes a fleet of approximately 198 custom designed trucks and other related equipment. Heat Waves’ operations are currently in southwestern Kansas, northwestern Oklahoma, Texas panhandle, southern Wyoming (Niobrara), Colorado (D-J Basin), southwestern Pennsylvania/northwestern West Virginia (Marcellus Shale), eastern Ohio (Utica Shale), western North Dakota and eastern Montana (Bakken formation), and southern Texas (Eagle Ford Shale). Well enhancement services accounted for approximately 82% of the Company’s total revenues for its 2015 fiscal year on a consolidated basis as compared to 84% for the 2014 fiscal year.

Frac Water Heating - Frac Water Heating is the process of heating water used in connection with the fracturing process of completing a well. Fracturing services are intended to enhance the production from crude oil and natural gas wells where the natural flow has been restricted by underground formations through the creation of conductive flowpaths to enable the hydrocarbons to reach the wellbore. The fracturing process consists of pumping a fluid slurry, which largely consists of fresh water and a “proppant” (explained below), into a cased well at sufficient pressure to fracture (i.e. create conductive flowpaths) the producing formation. Sand, bauxite or synthetic proppants are suspended in the fracturing fluid slurry and are pumped into the well under great pressure to fracture the formation. To ensure these solutions are properly mixed (gel frac) or that plain water (used in slick water fracs) can flow freely, the water frequently needs to be heated to a sufficient temperature as determined by the well owner/operator. Heat Waves currently owns and operates a fleet 53 frac heaters (or the equivalent of 81 burner boxes) designed to heat large amounts of water stored in reservoirs or frac tanks.

Acidizing - Acidizing entails pumping large volumes of specially formulated acids and/or chemicals into a well to dissolve materials blocking the flow of the crude oil or natural gas. The acid is pumped into the well under pressure and allowed time to react. Acidizing is most often used to increase permeability throughout the formation, clean up formation damage near the wellbore caused by drilling, and to remove buildup of materials restricting the flow of crude oil and gas in the formation or through perforations in the well casing. For most customers, Heat Waves supplies the acid solution and also pumps that solution into a given well. In March of 2015, the Company completed its 2014 CAPEX program by adding one mobile acid transport and pump truck which increased its total fleet to seven units as of December 31, 2015.

Hot Oil Services – Hot oil services involve the circulation of a heated fluid, typically oil, to dissolve, melt, or dislodge paraffin or other hydrocarbon deposits from the tubing of a producing oil or natural gas well. These paraffin deposits build up over a period of time from normal production operations, although the rate at which these products build up depends on the chemical character of the crude oil and natural gas being produced. This is performed by circulating the hot oil down the casing and back up the tubing to remove the deposits from the well bore and formation.

Hot oil servicing also includes the heating of oil storage tanks. The heating of storage tanks is done:

|

(1) |

To eliminate water and other soluble waste in the tank for which the operator’s revenue is reduced at the refinery; and |

|

(2) |

Because heated oil flows more efficiently from the tanks to transports taking oil to the refineries in colder weather. |

As of December 31, 2015, Heat Waves owns and operates a fleet of 57 hot oil trucks. During 2015, the Company added eight hot oil trucks from our 2014 CAPEX program. Heat Waves moves these vehicles among the service regions as necessary to maximize their productive time based on customer needs and seasonal conditions.

Pressure Testing – Pressure testing consists of pumping fluids into new or existing wells or other components of the well system such as flow lines to detect leaks. Hot oil trucks and pressure trucks are used to perform this service.

Fluid Management and Other Services.

Water Hauling – The Company currently owns or leases, and operates approximately 65 water hauling trucks and trailers equipped with pumps to move water from or into wells, tanks and other storage facilities in order to assist customers in managing their water-cost needs. Each water hauling transport has a hauling capacity of up to 130 barrels (each barrel being equal to 42 U.S. gallons). The trucks are used to:

|

(1) |

Transport water to fill frac tanks on well locations, |

|

(2) |

Transport contaminated water produced as a by-product of producing wells to disposal wells, including disposal wells that we own and operate, and |

|

(3) |

Transport drilling and completion fluids to and from well locations; following completion of fracturing operations, the trucks are used to transport the flow-back produced as a result of the fracturing process from the well site to disposal wells. |

Most wells produce residual salt or fresh water in conjunction with the extraction of the oil or natural gas. The Company’s trucks pick up water at the well site and transport it to a disposal well for injection or to other environmentally sound surface recycling facilities. This is regular maintenance work that is done on a periodic basis depending on the volume of water a well produces. Water-cost management is an ongoing need for oil and natural gas well operators throughout the life of a well.

The Company’s ability to outperform competitors in this segment is primarily dependent on logistical factors such as the proximity between areas where water is produced or used and the strategic placement and/or access to both disposal wells and recycling facilities. The Company owns four water disposal wells – two in Kansas and two in Oklahoma. It is management’s intent to maintain the Company’s disposal well holdings and access to recycling facilities, but also to use disposal wells and facilities owned by third parties where appropriate.

Typically the Company and a customer enter into a contract for water hauling services after that customer has completed a competitive bidding process. However, in certain instances, customers with requirements for minor or incidental water hauling services usually purchase the services on a “call out” basis and charged according to a published schedule of rates. The Company competes for services both on a call out and contractual basis.

Workover, completion, and remedial activities also provide the opportunity for higher operating margins from tank rentals and water hauling services. Drilling and workover jobs typically require water for multiple purposes. Completion and workover procedures often also require large volumes of water for fracturing operations, a process of stimulating a well hydraulically to increase production. All fluids are required to be transported from the well site to an approved disposal facility.

Competitors in the water hauling business, where the Company provides this service, are mostly small, regionally focused companies. The level of water hauling activity is comprised of a relatively stable demand for services related to the maintenance of producing wells and a highly variable demand for services used in the drilling and completion of new wells. As a result, the level of domestic onshore drilling activity significantly affects the level of the Company’s activity in this service area, and may vary from region to region and from season to season.

Disposal Well Services – The Company owns four disposal wells in Kansas and Oklahoma that allow for the injection of salt water and incidental non-hazardous oil and natural gas wastes.

Our trucks frequently transport fluids to be disposed of into these disposal wells. The Company’s disposal wells are located in southwestern Kansas and northwestern Oklahoma in areas in proximity to our customers’ producing wells in those areas. Most oil and natural gas wells produce varying amounts of water throughout their productive lives. In the states in which we operate, oil and natural gas wastes and water produced from oil and natural gas wells are required by law to be disposed of in authorized facilities, including permitted water disposal wells. All of the Company’s disposal wells are licensed by state authorities pursuant to guidelines and regulations imposed by the Environmental Protection Agency and the Safe Drinking Water Act and are completed in an environmentally sound manner in permeable formations below the fresh water table.

Frac Tank Rental – The Company also generates a small amount of revenues from the rental of frac tanks in the Hugoton Basin. The Company currently owns approximately 20 frac tanks, which can store up to 500 barrels of water and are used by oilfield operators to store fluids at the well site, including fresh water, salt water, and acid for frac jobs, flowback, temporary production and mud storage. Frac tanks are used during all phases of the life of a producing well. The Company generally rents frac tanks at daily rates and charges hourly rates for the transportation of the tanks to and from the well site.

Water Transfer Services – Water transfer entails using high and low volume pumps, lay flat hose, aluminum pipe and manifolds to move fresh and/or recycled water from a water source such as a pond, lake, river, stream, or water storage facility to frac tanks at drilling locations to be used in connection with fracking activities. Water transfer differs from water hauling in that water transfer is typically used in connection with well completion activities and involves moving water via pumps, hoses and pipes whereas water hauling involves moving water via bobtail trucks or water transports for either service or completion work.

Water Treatment Services – The Company uses patented hydropath technology under a sales agreement with HydroFLOW USA to remove bacteria and scale from water. The process uses electrical induction to reduce or eliminate down-hold scaling and corrosion in an environmentally friendly manner.

Construction and Roustabout Services – The Company provides well-site construction and roustabout services to as a supplementary services to existing customer primarily in the Hugoton Basin. Traditionally these services account for less than 1% of consolidated revenues.

Ownership of Company Assets

As described above, the Company (through Heat Waves, HWWM, and Dillco) owns and uses a fleet of trucks, trailers, frac tanks, disposal wells and other assets to provide its services and products. Substantially all of the equipment and personal property assets owned by these entities are subject to a security interest to secure loans made to the Company and its wholly-owned subsidiaries.

Historically, during portions of our fiscal year as supply and demand requires, the Company has leased additional trucks and equipment. These leases are treated as operating leases for accounting purposes, and the rent expense associated with these leases is reported ratably over the term of the lease.

Competitive Business Conditions

The markets in which the Company currently operates are highly competitive. Competition is influenced by such factors as price, capacity, the quality, safety record and availability of equipment, availability of work crews, and reputation and experience of the service provider. The Company believes that an important competitive factor in establishing and maintaining long-term customer relationships is having an experienced, skilled, and well-trained work force that is responsive to our customers’ needs. Although we believe customers consider all of these factors, price is often a primary factor in determining which service provider is awarded the work.

The demand for our services fluctuates primarily in relation to the worldwide commodity price (or anticipated price) of oil and natural gas which, in turn, is largely driven by the worldwide supply of, and demand for, oil and natural gas, political events, as well as speculation within the financial markets. Demand and prices are often volatile and difficult to predict and depends on events that are not within our control. Generally, as supply of those commodities decreases and demand increases, service and maintenance requirements increase as oil and natural gas producers drill new wells and attempt to maximize the productivity of their existing wells to take advantage of the higher priced environment. Conversely, as the supply of commodities increase and demand and crude oil and natural gas prices fall, oil and gas producers drill fewer wells and scale back or suspend service and maintenance work.

The Company’s competition primarily consists of small regional or local contractors. The Company attempts to differentiate itself from its competition in large part through its superior equipment and the range and quality of services it has the capability to provide. The Company invests a significant amount of capital into purchasing, developing, and maintaining a fleet of trucks and other equipment that are critical to the services it provides. Further, the Company concentrates on providing services to a diverse group of large and small independent oil and natural gas companies in a number of geographical areas. We believe we have been successful using this business model and believe it will enable us to continue to grow our business.

Dependence on One or a Few Major Customers

The Company serves numerous major and independent oil and natural gas companies that are active in its core areas of operations.

During the fiscal year ended December 31, 2015, two of the Company’s customers accounted for approximately 21% of consolidated revenues. No other customer exceeded 10% of consolidated revenues. The Company’s top five customers in 2015 accounted for approximately 38% of its total revenues. The loss of any one of these customers or a sustained decrease in demand by any of such customers could result in a substantial loss of revenues and could have a material adverse effect on the Company’s results of operations.

During the fiscal year ended December 31, 2014, one of the Company’s customers accounted for approximately 18% of consolidated revenues. No other customer exceeded 10% of consolidated revenues. The Company’s top five customers in 2014 accounted for approximately 46% of its total revenues.

While the Company believes its equipment could be redeployed in the current market environment if it lost any material customers, such loss could have an adverse effect on the Company’s business until the equipment is redeployed. We believe that the market for the Company’s services is sufficiently diversified that it is not dependent on any single customer or a few major customers.

Seasonality

Portions of the Company’s operations are impacted by seasonal factors, particularly with regards to its frac water heating and hot oiling services. In regards to frac water heating, because customers rely on Heat Waves to heat large amounts of water for use in fracturing formations, demand for this service is much greater in the colder months. Similarly, hot oiling services are in higher demand during the colder months when they are needed for maintenance of existing wells and to heat oil storage tanks.

Acidizing and pressure testing are done all year long with higher revenues during non-winter months.

The hauling of water from producing wells is not as seasonal as our other services since wells produce water whenever they are pumping regardless of weather conditions. Hauling of water for the drilling or fracturing of wells is also not seasonal but dependent on when customers decide to drill or complete wells.

Although they are new businesses to us, we believe water transfer services and bacteria and scaling solutions are not seasonal. However, our water transfer services and to a certain extent our bacteria and scaling solutions, do depend upon the level of drilling, well completion, and production activities.

Raw Materials

The Company purchases a wide variety of raw materials, parts, and components that are made by other manufacturers and suppliers for our use. The Company is not dependent on any single source of supply for those parts, supplies or materials. However, there are a limited number of vendors for propane and certain acids and chemicals. The Company utilizes a limited number of suppliers and service providers available to fabricate and/or construct the trucks and equipment used in its hot oiling, frac water heating, and acid related services.

Patents, Trademarks, Licenses, Franchises, Concessions, Royalty Agreements or Labor Contracts

The Company enters into agreements with local property owners where its disposal wells are located by which the Company generally agrees to pay those property owners a fixed amount per month plus a percentage of revenues derived from utilizing those wells. The terms of these agreements are separately negotiated with the given property owner, and during its 2015 and 2014 fiscal years the total amount paid under these various agreements by the Company was immaterial to the Company and its business operations.

As is the situation with all companies in the frac water heating service business, we rely on certain procedures and practices in performing our services. We have a patent application pending regarding certain of these used in our process of heating frac water. We are aware that one unrelated company (the “Patent Owner”) has been awarded two patents related, in part, to the process they use for heating of frac water and has certain other patent applications pending. For a further discussion of this, see Item 3 – Litigation, below.

Pursuant to a Sales Agreement with HydroFLOW USA, HWWM has the exclusive right to sell or rent patented hydropath devices in connection with bacteria deactivation and scale treatment services for treating injection and disposal wells, fracking water and recycled water in the oil and gas industry to customers in the United States. The hydropath technology is owned by HydroPath Holdings Limited. Pursuant to the Sales Agreement, the Company is required to pay royalties on certain rental transactions and must meet certain annual purchase commitments in order to maintain the exclusivity provision under the Sales Agreement.

Government Regulation

The Company and its subsidiaries are subject to a variety of government regulations ranging from environmental to OSHA to the Department of Transportation. Our operations are also subject to stringent federal, state and local laws regulating the discharge of materials into the environment or otherwise relating to health and safety or the protection of the environment. These federal, state, and local laws and regulations relating to protection of the environment, wildlife protection, historic preservation, and health and safety are extensive and changing. The recent trend in environmental legislation and regulation is generally toward stricter standards, and we expect that this trend will continue as the governmental agencies issue and amend existing regulations. Failure to comply with these laws and regulations as they currently exist or may be amended in the future may result in the assessment of substantial administrative, civil and criminal penalties, as well as the issuance of injunctions limiting or prohibiting activities. Strict adherence with these regulatory requirements increases our cost of doing business and consequently affects our profitability. The Company does not believe that it is in material violation of any regulations that would have a significant negative impact on the Company’s operations.

Through the routine course of providing services, the Company handles and stores bulk quantities of hazardous materials. If leaks or spills of hazardous materials handled, transported or stored by us occur, the Company may be responsible under applicable environmental laws for costs of remediating any damage to the surface or sub-surface (including aquifers).

The Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), also known as “Superfund,” and comparable state statutes impose strict, joint and several liability on owners and operators of sites and on persons who disposed of or arranged for the disposal of “hazardous substances” found at such sites. It is not uncommon for the government to file claims requiring cleanup actions, demands for reimbursement for government-incurred cleanup costs, or natural resource damages, or for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by hazardous substances released into the environment. The Federal Resource Conservation and Recovery Act, or RCRA, and comparable state statutes govern the disposal of “solid waste” and “hazardous waste” and authorize the imposition of substantial fines and penalties for noncompliance, as well as requirements for corrective actions. Although CERCLA currently excludes petroleum from its definition of “hazardous substance,” state laws affecting our operations may impose clean-up liability relating to petroleum and petroleum-related products. In addition, although RCRA classifies certain oil field wastes as “non-hazardous,” such exploration and production wastes could be reclassified as hazardous wastes thereby making such wastes subject to more stringent handling and disposal requirements. CERCLA, RCRA and comparable state statutes can impose liability for clean-up of sites and disposal of substances found on drilling and production sites long after operations on such sites have been completed. Other statutes relating to the storage and handling of pollutants include the Oil Pollution Act of 1990, or OPA, which requires certain owners and operators of facilities that store or otherwise handle oil to prepare and implement spill response plans relating to the potential discharge of oil into surface waters. The OPA contains numerous requirements relating to prevention of, reporting of, and response to oil spills into waters of the United States. State laws mandate oil cleanup programs with respect to contaminated soil. A failure to comply with OPA’s requirements or inadequate cooperation during a spill response action may subject a responsible party to civil or criminal enforcement actions.

In the course of the Company’s operations, it does not typically generate materials that are considered “hazardous substances.” One exception, however, would be spills that occur prior to well treatment materials being circulated down hole. For example, if the Company spills acid on a roadway as a result of a vehicle accident in the course of providing well enhancement/stimulation services, or if a tank with acid leaks prior to down hole circulation, the spilled material may be considered a “hazardous substance.” In this respect, the Company may occasionally be considered to “generate” materials that are regulated as hazardous substances and, as a result, may incur CERCLA liability for cleanup costs. Also, claims may be filed for personal injury and property damage allegedly caused by the release of hazardous substances or other pollutants.

The Clean Water Act (the “CWA”), and comparable state statutes, impose restrictions and controls on the discharge of pollutants, including spills and leaks of oil and other substances, into waters of the United States. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the Environmental Protection Agency (the “EPA”) or an analogous state agency. The CWA regulates storm water run-off from oil and natural gas facilities and requires a storm water discharge permit for certain activities. Such a permit requires the regulated facility to monitor and sample storm water run-off from its operations. The CWA and regulations implemented thereunder also prohibit discharges of dredged and fill material in wetlands and other waters of the United States unless authorized by an appropriately issued permit. The CWA and comparable state statutes provide for civil, criminal and administrative penalties for unauthorized discharges of oil and other pollutants and impose liability on parties responsible for those discharges for the costs of cleaning up any environmental damage caused by the release and for natural resource damages resulting from the release.

The Safe Drinking Water Act (the “SDWA”), and the Underground Injection Control (“UIC”) program promulgated thereunder, regulate the drilling and operation of subsurface injection wells, such as the disposal wells owned and operated by the Company. EPA directly administers the UIC program in some states and in others the responsibility for the program has been delegated to the state. The program requires that a permit be obtained before drilling a disposal well. Violation of these regulations and/or contamination of groundwater by oil and natural gas drilling, production, and related operations may result in fines, penalties, and remediation costs, among other sanctions and liabilities under the SWDA and state laws. In addition, third party claims may be filed by landowners and other parties claiming damages for alternative water supplies, property damages, and bodily injury.

Regulations in the states in which the Company owns and operates wells (Kansas and Oklahoma) require us to obtain a permit to operate each of our disposal wells. The applicable regulatory agency may suspend or modify one of our permits if the Company’s well operations are likely to result in pollution of freshwater, substantial violation of permit conditions or applicable rules, or if the well leaks into the environment.

The federal Energy Policy Act of 2005 amended the SDWA to exclude hydraulic fracturing from the definition of “underground injection” under certain circumstances. However, the repeal of this exclusion has been advocated by certain advocacy organizations and others in the public. The EPA at the request of Congress is currently conducting a national study examining the potential impacts of hydraulic fracturing on drinking water resources and issued a draft assessment report in June 2015. The EPA has asked the EPA Science Advisory Board (“SAB”) to peer review the draft assessment report.

We incur, and expect to continue to incur, capital and operating costs to comply with the environmental laws and regulations described herein. The technical requirements of these laws and regulations are becoming increasingly complex, stringent and expensive to implement.

If new federal or state laws or regulations that significantly restrict hydraulic fracturing are adopted, such legal requirements could result in delays, eliminate certain drilling and injection activities, make it more difficult or costly for our customers to perform fracturing and increase their and our costs of compliance and doing business. It is also possible that drilling and injection operations utilizing our services could adversely affect the environment, which could result in a requirement to perform investigations or clean-ups or in the incurrence of other unexpected material costs or liabilities.

Significant studies and research have been devoted to climate change and global warming, and climate change has developed into a major political issue in the United States and globally. Certain research suggests that greenhouse gas emissions contribute to climate change and pose a threat to the environment. Recent scientific research and political debate has focused in part on carbon dioxide and methane incidental to oil and natural gas exploration and production. Many state governments have enacted legislation directed at controlling greenhouse gas emissions, and future state and federal legislation and regulation could impose additional restrictions or requirements in connection with our operations and favor use of alternative energy sources, which could increase operating costs and decrease demand for oil products. As such, our business could be materially adversely affected by domestic and international legislation targeted at controlling climate change.

We are also subject to a number of federal and state laws and regulations, including the federal Occupational Safety and Health Act, or OSHA, and comparable state laws, whose purpose is to protect the health and safety of workers. In addition, the OSHA hazard communication standard, the EPA community right-to-know regulations under Title III of the federal Superfund Amendment and Reauthorization Act and comparable state statutes require that information be maintained concerning hazardous materials used or produced in our operations and that this information be provided to employees, state and local government authorities and citizens.

Because our trucks travel over public highways to get to customer’s wells, the Company is subject to the regulations of the Department of Transportation. These regulations are very comprehensive and cover a wide variety of subjects from the maintenance and operation of vehicles to driver qualifications to safety. Violations of these regulations can result in penalties ranging from monetary fines to a restriction on the use of the vehicles. Under regulations effective July 1, 2010, the continued violation of regulations could result in a shutdown of all of the vehicles of either Dillco or Heat Waves. The Company does not believe it is in violation of Department of Transportation regulations at this time that would result in a shutdown of vehicles.

Some states and certain municipalities have regulated, or are considering regulating hydraulic fracturing (“fracking”) which, if accomplished, could impact certain of our operations. While the Company does not believe that existing regulations and contemplated actions to limit or prohibit fracking have impacted its activities to date, there can be no assurance that these actions, if taken on a wider scale, may not adversely impact the Company’s business operations and revenues.

Employees

As of March 22, 2016, the Company employed 179 full time employees. Of these employees, 109 are employed by Heat Waves, 41 by Dillco, 20 by HWWM, and 9 are employed by Enservco.

Available Information

We maintain a website at http://www.enservco.com. The information contained on, or accessible through, our website is not part of this Annual Report on Form 10-K. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to reports filed or furnished pursuant to Sections 13(a) and 15(d) of the Exchange Act, are available on our website, free of charge, as soon as reasonably practicable after we electronically file such reports with, or furnish those reports to, the SEC.

In addition, we maintain our corporate governance documents on our website, including:

|

● |

a Code of Business Conduct and Ethics for Directors, Officers and Employees which contains information regarding our whistleblower procedures, |

|

● |

our Insider Trading Policy, |

|

● |

our Audit Committee Charter, |

|

● |

our Trading Blackout Policy, and |

|

● |

our Related Party Transaction Policy. |

ITEM 1A. RISK FACTORS

The Company’s securities are highly speculative and involve a high degree of risk, including among other items the risk factors described below. The below risk factors are intended to generally describe certain risks that could materially affect the Company and its current business operations and activities.

You should carefully consider the risks described below and elsewhere herein in connection with any decision whether to acquire, hold or sell the Company’s securities. If any of the contingencies discussed in the following paragraphs or other materially adverse events actually occur, the business, financial condition and results of operations could be materially and adversely affected. In such case, the trading price of our common stock could decline, and you could lose all or a significant part of your investment.

Operations Related Risks

Our business depends on domestic spending by the crude oil and natural gas industry which has suffered significant negative price volatility since July 2014, volatility which may continue; our business has been, and may in the future be, adversely affected by industry and financial market conditions that are beyond our control.

We depend on our customers’ ability and willingness to make operating and capital expenditures to explore, develop and produce crude oil and natural gas in the United States. Customers’ expectations for future crude oil and natural gas prices, as well as the availability of capital for operating and capital expenditures, may cause them to curtail spending, thereby reducing demand for our services and equipment. Major declines in oil and natural gas prices since July 2014 (when prices were at approximately $100 per barrel) have resulted in substantial declines in capital spending and drilling programs across the industry. As a result of the declines in oil and natural gas prices, most exploration and production companies have shut down or substantially reduced drilling programs and asked service providers to make pricing concessions. Over the last year, the Company has offered pricing concessions to a number of customers. Typically, these concessions have been made with the intent to maintain existing service volumes and/or develop additional business.

Industry conditions and specifically the market price for crude oil and natural gas are influenced by numerous domestic and global factors over which the Company has no control, such as the supply of and demand for oil and natural gas, domestic and worldwide economic conditions, weather conditions, political instability in oil and natural gas producing countries, and merger and divestiture activity among oil and natural gas producers. The volatility of the oil and natural gas industry and the consequent impact on commodity prices as well as exploration and production activity could adversely impact the level of drilling and activity by some of our customers. Where declining prices lead to reduced exploration and development activities in the Company’s market areas, the reduction in exploration and development activities also may have a negative long-term impact on the Company’s business. Continued decline in oil and natural gas prices may result in increased pressure from our customers to make additional pricing concessions in the future and may impact our borrowing arrangements with our principal bank. There can be no assurance that the prices we charge to our customers will return to former levels.

There has also been significant political pressures for the United States economy to reduce its dependence on crude oil and natural gas due to the perceived impacts on climate change. Furthermore there have been significant political efforts to reduce or eliminate hydraulic fracturing operations in certain of the Company’s service areas, particularly in Colorado. These activities may make oil and gas investment and production less attractive.

Higher oil and gas prices do not necessarily result in increased drilling activity because our customers’ expectation of future prices also drives demand for drilling services. Oil and gas prices, as well as demand for the Company’s services, also depend upon other factors that are beyond the Company’s control, including the following:

|

|

● |

demand for crude oil and natural gas; |

|

|

● |

political pressures against crude oil and natural gas exploration and production; |

|

|

● |

cost of exploring for, producing, and delivering oil and natural gas; |

|

|

● |

expectations regarding future energy prices; |

|

|

● |

advancements in exploration and development technology; |

|

|

● |

adoption or repeal of laws regulating oil and gas production in the U.S.; |

|

|

● |

imposition or lifting of economic sanctions against foreign companies; |

|

|

● |

weather conditions; |

|

|

● |

rate of discovery of new oil and natural gas reserves; |

|

|

● |

tax policy regarding the oil and gas industry; and |

|

|

● |

development and use of alternative energy sources. |

Ongoing volatility and uncertainty in the domestic and global economic and political environments have caused the oilfield services industry to experience volatility in terms of demand. While the Company is generally optimistic for the continuing development of the onshore North American oil and gas industry, there are a number of political and economic pressures negatively impacting the economics of continuing production from some existing wells, future drilling operations, and the willingness of banks and investors to provide capital to participants in the oil and gas industry. These cuts in spending will continue to curtail drilling programs as well as discretionary spending on well services, and will continue to result in a reduction in the demand for the Company’s services, the rates we can charge, and equipment utilization. In addition, certain of the Company’s customers could become unable to pay their suppliers, including the Company. Any of these conditions or events could adversely affect our operating results.

Our success depends on key members of our management, the loss of any executive or key personnel could disrupt our business operations.

We depend to a large extent on the services of certain of our executive officers. The loss of the services of Rick Kasch, Austin Peitz, Robert Devers or other key personnel, could disrupt our operations. Although we have entered into employment agreements with Messrs. Kasch, Peitz and Devers, that contain, among other things non-compete and confidentiality provisions, we may not be able to enforce the non-compete and/or confidentiality provisions in the employment agreements.

We depend on several significant customers, and a loss of one or more significant customers could adversely affect our results of operations.

The Company’s customers consist primarily of major and independent oil and natural gas companies. During fiscal year 2015, two of the Company’s customers accounted 21% of consolidated revenues and during fiscal year 2014, one of the Company’s customers accounted for 18% of consolidated revenues. No other customer exceeded 10% of revenues.

The Company’s top five customers accounted for approximately 38% and 46% of its total annual revenues for 2015 and 2014, respectively. The loss of any one of these customers or a sustained decrease in demand by any of such customers could result in a substantial loss of revenues and could have a material adverse effect on the Company’s results of operations.

While the Company believes our equipment could be redeployed in the current market environment if we lost any material customers, such loss could have an adverse effect on the Company’s business until the equipment is redeployed. We believe that the market for the Company’s services is sufficiently diversified that it is not dependent on any single customer or a few major customers.

Demand for the majority of our services is substantially dependent on the levels of expenditures by the domestic oil and natural gas industry. The Company has no influence over its customers’ capital expenditures. On-going economic volatility could have a material adverse effect on our financial condition, results of operations and cash flows.

Demand for the majority of our services depends substantially on the level of expenditures by participants in the domestic (United States) oil and natural gas industry for the exploration, development and production of oil and natural gas reserves. These expenditures are sensitive to the industry’s view of future economic growth in the United States and elsewhere, and the resulting impact on demand for oil and natural gas. Beginning in the second half of 2014, oil prices have declined substantially from historical highs This caused many of our customers to reduce or delay their oil and natural gas exploration and production spending in 2015, which consequently has reduced their demand for our services, and exerted downward pressure on the prices that we charged for our services and products. Given various domestic and global factors, oil and natural gas prices may remain depressed for the foreseeable future.

Furthermore, under an environment of increasing oil and natural gas prices it can lead to increasing costs of exploring for and producing oil and natural gas. Though the addition of frac stimulation into the domestic oil and gas industry has somewhat reduced the overall costs of producing oil and natural gas, the price of drill rigs, pipe, other equipment, fluids, and oil field services and the cost to companies like the Company of providing those services, has generally increased with significant increases in oil and natural gas prices. The resulting reduction in cash flows being experienced by our customers during the past months due to the decline in oil prices and the increase of the costs of exploring for and producing oil and natural gas as noted above could have significant adverse effects on the financial condition of some of our customers. This could result in project modifications, delays or cancellations, general business disruptions, and delay in, or nonpayment of, amounts that are owed to the Company, which could have a material adverse effect on our financial condition, results of operations and cash flows.

Environmental compliance costs and liabilities could reduce our earnings and cash available for operations.

We are subject to increasingly stringent laws and regulations relating to environmental protection and the importation and use of hazardous materials, including laws and regulations governing air emissions, water discharges and waste management. We incur, and expect to continue to incur, capital and operating costs to comply with environmental laws and regulations. The technical requirements of these laws and regulations are becoming increasingly complex, stringent and expensive to implement. These laws may provide for “strict liability” for damages to natural resources or threats to public health and safety. Strict liability can render a party liable for damages without regard to negligence or fault on the part of the party. Some environmental laws provide for joint and several strict liability for remediation of spills and releases of hazardous substances.

The Company uses hazardous substances and transports hazardous wastes in its operations. Accordingly, we could become subject to potentially material liabilities relating to the investigation and cleanup of contaminated properties, and to claims alleging personal injury or property damage as the result of exposures to, or releases of, hazardous substances. In addition, stricter enforcement of existing laws and regulations, new laws and regulations, the discovery of previously unknown contamination or the imposition of new or increased requirements could require the Company to incur costs or become the basis of new or increased liabilities that could reduce its earnings and cash available for operations. The Company believes it is currently in substantial compliance with environmental laws and regulations.

Competition within the well services industry may adversely affect our ability to market our services.

Although the well services industry is highly fragmented, it is very competitive. The well services industry includes numerous small companies capable of competing effectively in our markets on a local basis, as well as several large companies that possess substantially greater financial and other resources than the Company. The Company’s larger competitors have greater resources that could allow those competitors to compete more effectively than the Company. The Company’s small competitors may be able to react to market conditions more quickly. The amount of equipment available may exceed demand at some point in time, which could result in active price competition.

The Company could be impacted by unfavorable results of legal proceedings, such as being found to have infringed on intellectual property rights.

As is the situation with all companies in the frac water heating service business, we rely on certain procedures and practices in performing our services. We have a patent application pending regarding certain procedures used in our process of heating frac water. We are aware that one unrelated company (the “Patent Owner”) has been awarded two patents related, in part, to a process for heating of frac water and is currently seeking additional patents. The Patent Owner is currently in litigation with two different groups of energy companies that are seeking to invalidate the first patent. A North Dakota court has issued a summary judgement that the primary patent owned by the Patent Owner is invalid. The same Court also found that this primary patent is unenforceable due to inequitable conduct by the Patent Owner and/or the inventor. Further, in a pending reexamination involving the same patent, the U.S. Patent and Trademark Office (“USPTO”) has initially rejected all 99 claims of the patent. As of March 18, 2016, the Patent Owner is appealing the judgement and other adverse decisions by the North Dakota court and has filed an appeal with the U.S. Court of Appeals for the Federal Circuit. The Patent Owner has also filed a response to the USPTO’s rejections in the pending reexamination and is awaiting a response from the USPTO.

In October 2014, the Company was served with a complaint that alleges that Enservco and Heat Waves, in offering and selling frac water heating services, infringed and induced others to infringe on two patents owned by the Patent Owner including the patent ruled invalid by the North Dakota Court. The complaint seeks various remedies including injunctive relief and unspecified damages and relates to only a portion of Heat Waves’ frac water heating services. Heat Waves has answered the complaint, denied the Patent Owner’s allegations of infringement and asserted counterclaims asking the Court to find, among other things, that it does not infringe either patent and that both patents are invalid. The Patent Owner has replied to and denied those counterclaims. In July 2015, a Colorado Court granted a joint request by Heat Waves and the Patent Owner to stay the case. The lawsuit is now stayed pending the outcome of the reexamination and the appeal by the Patent Owner of the summary judgment invalidating the Patent Owner’s patent as set forth above. (See Item 3 – Litigation, for more information about this matter.)

However, if Enservco and/or Heat Waves are found to be infringing, they could be liable for the payment of substantial damages or royalties or be subject to a temporary or permanent injunction prohibiting Heat Waves from heating frac water in a manner it may have been using.

Our operations are subject to inherent risks, some of which are beyond our control. These risks may be self-insured, or may not be fully covered under our insurance policies, but to the extent not covered, are self-insured by the Company.

Our operations are subject to hazards inherent in the oil and natural gas industry, such as, but not limited to, accidents, blowouts, explosions, fires and oil spills. These conditions can cause:

|

|

■ |

Personal injury or loss of life, |

|

|

■ |

Damage to or destruction of property, equipment and the environment, and |

|

|

■ |

Suspension of operations by our customers. |

The occurrence of a significant event or adverse claim in excess of the insurance coverage that we maintain or that is not covered by insurance could have a material adverse effect on our financial condition and results of operations. In addition, claims for loss of oil and natural gas production and damage to formations can occur in the well services industry. Litigation arising from a catastrophic occurrence at a location where our equipment and services are being used may result in us being named as a defendant in lawsuits asserting large claims.

The Company maintains insurance coverage that we believe to be customary in the industry against these hazards. In addition, in June 2015, the Company became self-insured under its Employee Group Medical Plan for the first $75,000 per individual participant. However, we do not have insurance against all foreseeable risks, either because insurance is not available or because of the high premium costs. The occurrence of an event not fully insured against, or the failure of an insurer to meet its insurance obligations, could result in substantial losses. In addition, we may not be able to maintain adequate insurance in the future at reasonable rates. Insurance may not be available to cover any or all of the risks to which we are subject, or, even if available, it may be inadequate, or insurance premiums or other costs could rise significantly in the future so as to make such insurance prohibitively expensive. It is likely that, in our insurance renewals, our premiums and deductibles will be higher, and certain insurance coverage either will be unavailable or considerably more expensive than it has been in the recent past. In addition, our insurance is subject to coverage limits, and some policies exclude coverage for damages resulting from environmental contamination.

While our growth strategy includes appropriate acquisitions, we may not be successful in identifying, making and integrating business or asset acquisitions, if any, in the future.

We anticipate that a component of our growth strategy may be to make geographically focused acquisitions of businesses or assets aimed to strengthen our presence and expand services offered in selected regional markets. Pursuit of this strategy may be restricted by the on-going volatility and uncertainty within the credit markets which may significantly limit the availability of funds for such acquisitions. Our ability to use shares of our common stock in an acquisition transaction may be adversely affected by the volatility in the price of our stock.

In addition to restricted funding availability, the success of this strategy will depend on our ability to identify suitable acquisition candidates and to negotiate acceptable financial and other terms. There is no assurance that we will be able to do so. The success of an acquisition also depends on our ability to perform adequate due diligence before the acquisition and on our ability to integrate the acquisition after it is completed. While the Company intends to commit significant resources to ensure that it conducts comprehensive due diligence, there can be no assurance that all potential risks and liabilities will be identified in connection with an acquisition. Similarly, while we expect to commit substantial resources, including management time and effort, to integrating acquired businesses into ours, there is no assurance that we will be successful in integrating these businesses. In particular, it is important that the Company be able to retain both key personnel of the acquired business and its customer base. A loss of either key personnel or customers could negatively impact the future operating results of any acquired business.

In January 2016, HWWM, a wholly owned subsidiary of the Company, acquired various assets including the water transfer assets of HIIT and WET for approximately $4.0 million dollars. The Company’s ability to successfully integrate these acquisitions and expand the water transfer and bacteria and scaling solutions services is a going to be challenging given the current industry environment. There can be no assurance that we will successfully integrate these acquisitions and expand these services.

Compliance with climate change legislation or initiatives could negatively impact our business.

The U.S. Congress has considered legislation to mandate reductions of greenhouse gas emissions and certain states have already implemented, or may be in the process of implementing, similar legislation. Additionally, the U.S. Supreme Court has held in its decisions that carbon dioxide can be regulated as an “air pollutant” under the Clean Air Act, which could result in future regulations even if the U.S. Congress does not adopt new legislation regarding emissions. At this time, it is not possible to predict how legislation or new federal or state government mandates regarding the emission of greenhouse gases could impact our business; however, any such future laws or regulations could require us or our customers to devote potentially material amounts of capital or other resources in order to comply with such regulations. These expenditures could have a material adverse impact on our financial condition, results of operations, or cash flows.

Anti-fracking initiatives could adversely impact our business.

Some states and certain municipalities have regulated, or are considering regulating hydraulic fracturing (“fracking”) which, if accomplished, could impact certain of our operations. While the Company does not believe that these regulations and contemplated actions to limit or prohibit fracking have impacted its activities to date, there can be no assurance that these actions, if taken on a wider scale, may not adversely impact the Company’s business operations and revenues.

Debt Related Risks

Our indebtedness, which is currently collateralized by substantially all of our assets, could restrict our operations and make us more vulnerable to adverse economic conditions.

As of December 31, 2015, the Company owed approximately $21.6 million to banks and financial institutions under various collateralized debt facilities (approximately $23.9 million as of February 29, 2016).

Our current and future indebtedness could have important consequences. For example, it could:

|

|

■ |

Impair our ability to make investments and obtain additional financing for working capital, capital expenditures, acquisitions or other general corporate purposes, |

|

|

■ |

Limit our ability to use operating cash flow in other areas of our business because we must dedicate a substantial portion of these funds to make principal and interest payments on our indebtedness, |

|

|

■ |

Make us more vulnerable to a downturn in our business, our industry or the economy in general as a substantial portion of our operating cash flow will be required to make principal and interest payments on our indebtedness, making it more difficult to react to changes in our business and in industry and market conditions, |

|

|

■ |

Put us at a competitive disadvantage to competitors that have less debt, or |

|

|

■ |

Increase our vulnerability to interest rate increases to the extent that we incur additional variable rate indebtedness, a variable rate that has increased as a result of the Sixth Amendment to our lending agreement with PNC Bank. |