SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN ISSUER

Pursuant to Rule 13a-16 or 15d-16 of the

Securities Exchange Act of 1934

January 31, 2012

KONINKLIJKE PHILIPS ELECTRONICS N.V.

(Exact name of registrant as specified in its charter)

Royal Philips Electronics

(Translation of registrant’s name into English)

The Netherlands

(Jurisdiction of incorporation or organization)

Breitner Center, Amstelplein 2, 1096 BC Amsterdam, The Netherlands

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F x Form 40-F ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule101(b)(1): ¨

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule101(b)(7): ¨

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ¨ No x

Name and address of person authorized to receive notices

and communications from the Securities and Exchange Commission:

E.P. Coutinho

Koninklijke Philips Electronics N.V.

Amstelplein 2

1096 BC Amsterdam – The Netherlands

This report comprises a copy of the Quarterly Report of the Philips Group for the three months ended December 31, 2011 and the following press release:

- “Fourth Quarter and Annual Results 2011”, dated January 30, 2012.

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf, by the undersigned, thereunto duly authorized at Amsterdam, on the 31st day of January 2012.

KONINKLIJKE PHILIPS ELECTRONICS N.V.

/s/ E.P. Coutinho

(General Secretary)

Q4 2011 Quarterly report

Philips reports fourth-quarter sales of EUR 6.7 billion;

EBITA of EUR 503 million

| • | Comparable sales up 3%, led by 7% growth at Lighting |

| • | Growth geographies sales up 12% on a comparable basis |

| • | EBITA of 7.5% of sales |

| • | Net income from continuing operations at EUR 112 million |

| • | Free cash flow of EUR 961 million |

| • | Proposed dividend stable at EUR 0.75 per share |

Q4 financials: Year-on-year revenue increased across all operating sectors. EBITA margin declined from 14.1% in Q4 2010 to 7.5% in Q4 2011.

Healthcare comparable sales were 3% higher year-on-year. Comparable equipment order intake grew 3% year-on-year. Equipment orders in growth geographies grew by 17%. Results were impacted by weakness in the European markets, postponed deliveries of existing orders, as well as increased investments in new product innovation and sales channels.

Consumer Lifestyle sales increased 1% on a comparable basis. At an aggregate level, the three growth businesses – Personal Care, Health & Wellness, and Domestic Appliances – achieved a high single-digit comparable sales increase compared to the fourth quarter of 2010. The sector growth rate was impacted by a comparable sales decline at Lifestyle Entertainment. Reported EBITA margin for the quarter was 10%.

Lighting comparable sales increased 7% year-on-year, driven by double-digit sales growth at Lamps and Automotive. LED-based sales grew 37% compared to Q4 2010, now representing 18% of total Lighting sales. Sales in growth geographies increased by 21% in the quarter. Results were impacted by pricing, inventory reduction measures, and operational issues. As part of the turnaround plan, most brands for Consumer Luminaires products will be re-branded as Philips, which resulted in a value adjustment of commercial and brand-related assets leading to a charge of EUR 128 million.

Working capital reductions in the sectors amounted to more than EUR 500 million in the quarter, contributing to a free cash inflow of EUR 961 million in the fourth quarter.

The company completed 35% of its EUR 2 billion share buy-back program since the start of the program in July 2011. Taking into consideration the volatility of the financial markets, Philips has decided to extend the timing of the program until the end of Q2 2013.

Moving forward on Accelerate!, Philips’ change and performance improvement program

Philips is seeing the initial signs of the Accelerate! program positively impacting sales growth in difficult market circumstances. Importantly, the company has attracted key talent for critical positions across the company.

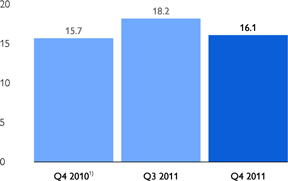

In addition, as part of the company’s efforts to improve its end-to-end processes, inventory as a percentage of sales decreased to 16.1% from 18.2% in Q3 2011, representing a comparable decrease of EUR 585 million, which is an improvement compared to the decrease in inventory seen in the same period last year.

The actions to deliver on the overhead cost reduction program are on track, and the first planned cost savings were realized in the quarter.

The annual incentive system for the executives has been changed to reflect line-of-sight accountability and is now fully aligned with the key performance indicators of the 2013 mid-term financial targets.

CEO quote:

“Our fourth quarter results were impacted by weak European sales, postponement in deliveries of existing orders in our Healthcare sector, and inventory correction actions and other operational issues in our Lighting business. These issues were partially offset by solid results in our Consumer Lifestyle growth businesses, which benefited from the early adoption of the Accelerate! change and performance improvement program. In addition, we delivered strong free cash flow as a result of our work to reduce working capital.

We are cautious about 2012 given the uncertainty in the global economy, and Europe in particular. In addition, we expect our 2012 results to be affected by the previously communicated restructuring charges and one-time investments aimed at improving our business performance trajectory, as part of the multi-year Accelerate! program. Excluding these additional charges, we expect the underlying operating margins and capital efficiency in the sectors to improve in the latter part of 2012.

While we are concerned about the economic environment, all of us at Philips are fully committed to improve our operational performance to achieve our mid-term (2013) financial targets.

Frans van Houten, CEO of Royal Philips Electronics

Please refer to page 17 of this press release for more information about forward-looking statements, third-party market share data, use of non-GAAP information and use of fair-value measurements.

Philips Group

Q4 2011 Quarterly report 3

4 Q4 2011 Quarterly report

Q4 2011 Quarterly report 5

6 Q4 2011 Quarterly report

Q4 2011 Quarterly report 7

Healthcare

8 Q4 2011 Quarterly report

| • | Comparable sales were 3% higher year-on-year, with mid-single-digit growth at Customer Services, Home Healthcare Solutions and Patient Care & Clinical Informatics tempered by flat sales growth at Imaging Systems. From a regional perspective, comparable sales in North America grew 6%. Sales in growth geographies grew 5%, while sales growth in mature geographies was 2%. |

| • | EBITA for Q4 2011 was EUR 409 million, or 15.0% of sales, compared to EUR 522 million, or 19.8% of sales, in Q4 2010. Market weakness in Europe led to postponement of deliveries and affected margin improvement plans for Imaging Systems. In addition, investments in innovation and sales channels to drive growth, as well as one-time charges, resulted in lower earnings at Imaging Systems, Patient Care & Clinical Informatics and Home Healthcare Solutions. Excluding restructuring and acquisition-related charges, EBITA was EUR 430 million, or 15.8% of sales, compared to EUR 518 million, or 19.6% of sales, in Q4 2010. |

| • | Net operating capital decreased by EUR 490 million to EUR 8.4 billion, partly due to currency impact, partly due to impairment taken in Q2 2011. |

| • | Compared to Q4 2010 the number of employees increased by 1,702, largely driven by an increase in commercial and industrial employees. |

Miscellaneous

| • | Restructuring and acquisition-related charges in Q1 2012 are expected to total approximately EUR 15 million. |

Q4 2011 Quarterly report 9

Consumer Lifestyle*

| * | Excluding Television |

10 Q4 2011 Quarterly report

Q4 2011 Quarterly report 11

Lighting

12 Q4 2011 Quarterly report

Q4 2011 Quarterly report 13

Group Management & Services

14 Q4 2011 Quarterly report

Q4 2011 Quarterly report 15

Additional information on the Television business

16 Q4 2011 Quarterly report

Forward-looking statements

Q4 2011 Quarterly report 17

Full-year highlights

18 Q4 2011 Quarterly report

Proposed distribution

Q4 2011 Quarterly report 19

Consolidated statements of income

all amounts in millions of euros unless otherwise stated

| 4th quarter | January-December | |||||||||||||||

| 2010 | 2011 | 2010 | 2011 | |||||||||||||

| Sales |

6,495 | 6,712 | 22,287 | 22,579 | ||||||||||||

| Cost of sales |

(3,832 | ) | (4,301 | ) | (13,191 | ) | (13,932 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Gross margin |

2,663 | 2,411 | 9,096 | 8,647 | ||||||||||||

| Selling expenses |

(1,368 | ) | (1,510 | ) | (4,876 | ) | (5,160 | ) | ||||||||

| General and administrative expenses |

(140 | ) | (207 | ) | (713 | ) | (841 | ) | ||||||||

| Research and development expenses |

(387 | ) | (449 | ) | (1,493 | ) | (1,610 | ) | ||||||||

| Impairment of goodwill |

— | — | — | (1,355 | ) | |||||||||||

| Other business income |

44 | 29 | 93 | 125 | ||||||||||||

| Other business expenses |

(16 | ) | (12 | ) | (27 | ) | (75 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) from operations |

796 | 262 | 2,080 | (269 | ) | |||||||||||

| Financial income |

13 | (6 | ) | 214 | 112 | |||||||||||

| Financial expenses |

(75 | ) | (65 | ) | (335 | ) | (352 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) before taxes |

734 | 191 | 1,959 | (509 | ) | |||||||||||

| Income tax expense |

(227 | ) | (79 | ) | (499 | ) | (283 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income (loss) after taxes |

507 | 112 | 1,460 | (792 | ) | |||||||||||

| Results relating to investments in associates |

(4 | ) | — | 18 | 16 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) from continuing operations |

503 | 112 | 1,478 | (776 | ) | |||||||||||

| Discontinued operations - net of income tax |

(38 | ) | (272 | ) | (26 | ) | (515 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income (loss) |

465 | (160 | ) | 1,452 | (1,291 | ) | ||||||||||

| Attribution of net income for the period |

||||||||||||||||

| Net income (loss) attributable to shareholders |

463 | (162 | ) | 1,446 | (1,295 | ) | ||||||||||

| Net income attributable to non-controlling interests |

2 | 2 | 6 | 4 | ||||||||||||

| Weighted average number of common shares outstanding (after deduction of treasury shares) during the period (in thousands): |

||||||||||||||||

| - basic |

946,951 | 1) | 936,476 | 940,528 | 1) | 951,647 | ||||||||||

| - diluted |

953,604 | 1) | 939,194 | 948,392 | 1) | 956,130 | ||||||||||

| Net income (loss) attributable to shareholders per common share in euros: |

||||||||||||||||

| - basic |

0.49 | (0.17 | ) | 1.54 | (1.36 | ) | ||||||||||

| - diluted2) |

0.49 | (0.17 | ) | 1.52 | (1.36 | ) | ||||||||||

| Ratios |

||||||||||||||||

| Gross margin as a % of sales |

41.0 | 35.9 | 40.8 | 38.3 | ||||||||||||

| Selling expenses as a % of sales |

(21.1 | ) | (22.5 | ) | (21.9 | ) | (22.9 | ) | ||||||||

| G&A expenses as a % of sales |

(2.2 | ) | (3.1 | ) | (3.2 | ) | (3.7 | ) | ||||||||

| R&D expenses as a % of sales |

(6.0 | ) | (6.7 | ) | (6.7 | ) | (7.1 | ) | ||||||||

| EBIT |

796 | 262 | 2,080 | (269 | ) | |||||||||||

| as a % of sales |

12.3 | 3.9 | 9.3 | (1.2 | ) | |||||||||||

| EBITA |

913 | 503 | 2,562 | 1,680 | ||||||||||||

| as a % of sales |

14.1 | 7.5 | 11.5 | 7.4 | ||||||||||||

The year 2010 is restated to present the Television business as discontinued operations

| 1) | Adjusted to make 2010 comparable for the bonus shares (667 thousand) issued in April 2011 |

| 2) | The incremental shares from assumed conversion are not taken into account in the periods for which there is a loss attributable to shareholders, as the effect would be antidilutive |

20 Q4 2011 Quarterly report

Consolidated balance sheets

in millions of euros unless otherwise stated

| December 31, | December 31, | |||||||

| 2010 | 2011 | |||||||

| Non-current assets: |

||||||||

| Property, plant and equipment |

3,145 | 3,014 | ||||||

| Goodwill |

8,035 | 7,016 | ||||||

| Intangible assets excluding goodwill |

4,198 | 3,996 | ||||||

| Non-current receivables |

88 | 127 | ||||||

| Investments in associates |

181 | 203 | ||||||

| Other non-current financial assets |

479 | 346 | ||||||

| Deferred tax assets |

1,351 | 1,713 | ||||||

| Other non-current assets |

75 | 71 | ||||||

|

|

|

|

|

|||||

| Total non-current assets |

17,552 | 16,486 | ||||||

| Current assets: |

||||||||

| Inventories - net |

3,865 | 3,625 | ||||||

| Other current financial assets |

5 | — | ||||||

| Other current assets |

348 | 351 | ||||||

| Derivative financial assets |

112 | 229 | ||||||

| Income tax receivable |

79 | 162 | ||||||

| Receivables |

4,355 | 4,415 | ||||||

| Assets classified as held for sale |

120 | 551 | ||||||

| Cash and cash equivalents |

5,833 | 3,147 | ||||||

|

|

|

|

|

|||||

| Total current assets |

14,717 | 12,480 | ||||||

|

|

|

|

|

|||||

| Total assets |

32,269 | 28,966 | ||||||

| Shareholders’ equity |

15,046 | 12,355 | ||||||

| Non-controlling interests |

46 | 34 | ||||||

|

|

|

|

|

|||||

| Group equity |

15,092 | 12,389 | ||||||

| Non-current liabilities: |

||||||||

| Long-term debt |

2,818 | 3,278 | ||||||

| Long-term provisions |

1,716 | 1,880 | ||||||

| Deferred tax liabilities |

171 | 77 | ||||||

| Other non-current liabilities |

1,714 | 1,999 | ||||||

|

|

|

|

|

|||||

| Total non-current liabilities |

6,419 | 7,234 | ||||||

| Current liabilities: |

||||||||

| Short-term debt |

1,840 | 582 | ||||||

| Derivative financial liabilities |

564 | 744 | ||||||

| Income tax payable |

291 | 191 | ||||||

| Accounts and notes payable |

3,691 | 3,346 | ||||||

| Accrued liabilities |

2,995 | 3,026 | ||||||

| Short-term provisions |

623 | 759 | ||||||

| Liabilities directly associated with assets held for sale |

— | 61 | ||||||

| Other current liabilities |

754 | 634 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

10,758 | 9,343 | ||||||

|

|

|

|

|

|||||

| Total liabilities and group equity |

32,269 | 28,966 | ||||||

Q4 2011 Quarterly report 21

| December 31, | December 31, | |||||||

| 2010 | 2011 | |||||||

| Number of common shares outstanding (after deduction of treasury shares) at the end of period (in thousands) |

946,506 | 926,095 | ||||||

| Ratios |

||||||||

| Shareholders’ equity per common share in euros |

15.90 | 13.34 | ||||||

| Inventories as a % of sales1) |

15.7 | 16.1 | ||||||

| Net debt : group equity |

(8):108 | 5:95 | ||||||

| Net operating capital |

11,951 | 10,427 | ||||||

| Employees at end of period |

119,775 | 2) | 125,241 | |||||

| of which discontinued operations |

3,610 | 3,353 | ||||||

| 1) | Excludes discontinued operations for both inventories and sales figures. Inventories excluding discontinued operations are disclosed in quarterly statistics. |

| 2) | Adjusted to reflect a change of employees reported in the Healthcare sector |

22 Q4 2011 Quarterly report

Consolidated statements of cash flows

all amounts in millions of euros

| 4th quarter | January-December | |||||||||||||||

| 2010 | 2011 | 2010 | 2011 | |||||||||||||

| Cash flows from operating activities: |

||||||||||||||||

| Net income (loss) |

465 | (160 | ) | 1,452 | (1,291 | ) | ||||||||||

| Loss from discontinued operations |

38 | 272 | 26 | 515 | ||||||||||||

| Adjustments to reconcile net income to net cash provided by (used for) operating activities: |

||||||||||||||||

| Depreciation and amortization |

361 | 475 | 1,356 | 1,456 | ||||||||||||

| Impairment of goodwill and other non-current financial assets |

(1 | ) | 5 | 5 | 1,387 | |||||||||||

| Net gain on sale of assets |

(23 | ) | (4 | ) | (204 | ) | (88 | ) | ||||||||

| (Income) loss from investments in associates |

3 | 2 | (18 | ) | (14 | ) | ||||||||||

| Dividends received from investments in associates |

5 | 21 | 19 | 44 | ||||||||||||

| Dividends paid to non-controlling interests |

(3 | ) | (3 | ) | (4 | ) | (4 | ) | ||||||||

| (Increase) decrease in working capital: |

485 | 676 | 16 | (679 | ) | |||||||||||

| Increase in receivables and other current assets |

(132 | ) | (184 | ) | (241 | ) | (339 | ) | ||||||||

| Decrease (increase) in inventories |

256 | 569 | (498 | ) | (81 | ) | ||||||||||

| Increase (decrease) in accounts payable, accrued and other liabilities |

361 | 291 | 755 | (259 | ) | |||||||||||

| Decrease (increase) in non-current receivables, other assets and other liabilities |

24 | (186 | ) | (297 | ) | (596 | ) | |||||||||

| (Decrease) increase in provisions |

(65 | ) | 86 | (211 | ) | 6 | ||||||||||

| Other items |

77 | 23 | (19 | ) | 100 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash provided by operating activities |

1,366 | 1,207 | 2,121 | 836 | ||||||||||||

| Cash flows from investing activities: |

||||||||||||||||

| Purchase of intangible assets |

(36 | ) | (28 | ) | (80 | ) | (116 | ) | ||||||||

| Expenditures on development assets |

(56 | ) | (63 | ) | (193 | ) | (231 | ) | ||||||||

| Capital expenditures on property, plant and equipment |

(174 | ) | (203 | ) | (621 | ) | (725 | ) | ||||||||

| Proceeds from disposals of property, plant and equipment |

52 | 48 | 129 | 128 | ||||||||||||

| Cash from (to) derivatives and securities |

8 | (9 | ) | (25 | ) | 26 | ||||||||||

| Purchase of other non-current financial assets |

— | (13 | ) | (16 | ) | (43 | ) | |||||||||

| Proceeds from other non-current financial assets |

86 | — | 268 | 87 | ||||||||||||

| Purchase of businesses, net of cash acquired |

(170 | ) | (255 | ) | (225 | ) | (509 | ) | ||||||||

| Proceeds from sale of interests in businesses net of cash disposed of |

15 | 12 | 117 | 19 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash used for investing activities |

(275 | ) | (511 | ) | (646 | ) | (1,364 | ) | ||||||||

| Cash flows from financing activities: |

||||||||||||||||

| Proceeds from issuance of (payments on) short-term debt |

119 | (35 | ) | 143 | (217 | ) | ||||||||||

| Principal payments on long-term debt |

(20 | ) | (21 | ) | (78 | ) | (1,097 | ) | ||||||||

| Proceeds from issuance of long-term debt |

26 | 234 | 71 | 457 | ||||||||||||

| Treasury shares transactions |

9 | (208 | ) | 65 | (671 | ) | ||||||||||

| Dividends paid |

— | — | (296 | ) | (259 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash provided by (used for) financing activities |

134 | (30 | ) | (95 | ) | (1,787 | ) | |||||||||

| Net cash provided by (used for) continuing operations |

1,225 | 666 | 1,380 | (2,315 | ) | |||||||||||

| Cash flow from discontinued operations: |

||||||||||||||||

| Net cash provided by (used for) operating activities |

191 | 168 | 34 | (270 | ) | |||||||||||

| Net cash used for investing activities |

(7 | ) | (29 | ) | (56 | ) | (94 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net cash provided by (used for) discontinued operations |

184 | 139 | (22 | ) | (364 | ) | ||||||||||

| Net cash provided by (used for) continuing and discontinued operations |

1,409 | 805 | 1,358 | (2,679 | ) | |||||||||||

Q4 2011 Quarterly report 23

| 4th quarter | January-December | |||||||||||||||

| 2010 | 2011 | 2010 | 2011 | |||||||||||||

| Effect of change in exchange rates on cash and cash equivalents |

39 | 3 | 89 | (7 | ) | |||||||||||

| Cash and cash equivalents at the beginning of the period |

4,385 | 2,339 | 4,386 | 5,833 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash and cash equivalents at the end of the period |

5,833 | 3,147 | 5,833 | 3,147 | ||||||||||||

| Ratio |

||||||||||||||||

| Cash flows before financing activities |

1,091 | 696 | 1,475 | (528 | ) | |||||||||||

| Net cash paid during the period for |

||||||||||||||||

| Pensions |

(132 | ) | (140 | ) | (474 | ) | (639 | ) | ||||||||

| Interest |

(10 | ) | (31 | ) | (226 | ) | (231 | ) | ||||||||

| Income taxes |

(13 | ) | (125 | ) | (206 | ) | (582 | ) | ||||||||

The year 2010 is restated to present the Television business as discontinued operations. For a number of reasons, principally the effects of translation differences, certain items in the statements of cash flows do not correspond to the differences between the balance sheet amounts for the respective items.

24 Q4 2011 Quarterly report

Consolidated statement of changes in equity

in millions of euros

| other reserves | ||||||||||||||||||||||||||||||||||||||||||||||||

| common shares |

capital in excess of par value |

retained earnings |

revaluation reserve |

currency translation differences |

unrealized gain (loss) on available- for- sale financial assets |

changes cash |

total | treasury shares at cost |

total equity |

non-controlling interests |

total equity |

|||||||||||||||||||||||||||||||||||||

| January-December 2011 |

||||||||||||||||||||||||||||||||||||||||||||||||

| Balance as of December 31, 2010 |

197 | 354 | 15,416 | 86 | (65 | ) | 139 | (5 | ) | 69 | (1,076 | ) | 15,046 | 46 | 15,092 | |||||||||||||||||||||||||||||||||

| Net income |

(1,295 | ) | (1,295 | ) | 4 | (1,291 | ) | |||||||||||||||||||||||||||||||||||||||||

| Net current period change |

(431 | ) | (16 | ) | 69 | (68 | ) | (31 | ) | (30 | ) | (477 | ) | (477 | ) | |||||||||||||||||||||||||||||||||

| Reclassifications into income |

— | 3 | (26 | ) | 27 | 4 | 4 | 4 | ||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Total comprehensive income |

(1,726 | ) | (16 | ) | 72 | (94 | ) | (4 | ) | (26 | ) | (1,768 | ) | 4 | (1,764 | ) | ||||||||||||||||||||||||||||||||

| Dividend distributed |

5 | 443 | (711 | ) | (263 | ) | (263 | ) | ||||||||||||||||||||||||||||||||||||||||

| Movement non-controlling interest |

(5 | ) | (5 | ) | (16 | ) | (21 | ) | ||||||||||||||||||||||||||||||||||||||||

| Purchase of treasury shares |

(51 | )1) | (700 | ) | (751 | ) | (751 | ) | ||||||||||||||||||||||||||||||||||||||||

| Re-issuance of treasury shares |

(34 | ) | (6 | ) | 86 | 46 | 46 | |||||||||||||||||||||||||||||||||||||||||

| Share-based compensation plans |

56 | 56 | 56 | |||||||||||||||||||||||||||||||||||||||||||||

| Income tax share-based compensation plans |

(6 | ) | (6 | ) | (6 | ) | ||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| 5 | 459 | (773 | ) | (614 | ) | (923 | ) | (16 | ) | (939 | ) | |||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Balance as of December 31, 2011 |

202 | 813 | 12,917 | 70 | 7 | 45 | (9 | ) | 43 | (1,690 | ) | 12,355 | 34 | 12,389 | ||||||||||||||||||||||||||||||||||

| 1) | Tax payment related to purchase of treasury shares |

Q4 2011 Quarterly report 25

Sectors

all amounts in millions of euros unless otherwise stated

Sales and income (loss) from operations

| 4th quarter | ||||||||||||||||||||||||

| 2010 | 2011 | |||||||||||||||||||||||

| income from operations | income from operations | |||||||||||||||||||||||

| sales | amount | as a % of sales | sales | amount | as a % of sales | |||||||||||||||||||

| Healthcare |

2,642 | 459 | 17.4 | 2,724 | 359 | 13.2 | ||||||||||||||||||

| Consumer Lifestyle |

1,791 | 198 | 11.1 | 1,849 | 167 | 9.0 | ||||||||||||||||||

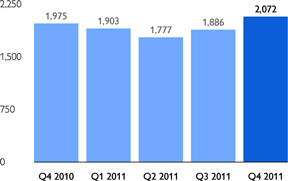

| Lighting |

1,975 | 156 | 7.9 | 2,072 | (130 | ) | (6.3 | ) | ||||||||||||||||

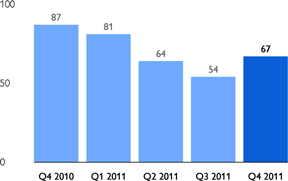

| Group Management & Services |

87 | (17 | ) | — | 67 | (134 | ) | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 6,495 | 796 | 12.3 | 6,712 | 262 | 3.9 | |||||||||||||||||||

| Sales and income (loss) from operations |

| January-December | ||||||||||||||||||||||||

| 2010 | 2011 | |||||||||||||||||||||||

| income from operations | income from operations | |||||||||||||||||||||||

| sales | amount | as a % of sales | sales | amount | as a % of sales | |||||||||||||||||||

| Healthcare |

8,601 | 922 | 10.7 | 8,852 | 93 | 1.1 | ||||||||||||||||||

| Consumer Lifestyle |

5,775 | 679 | 11.8 | 5,823 | 392 | 6.7 | ||||||||||||||||||

| Lighting |

7,552 | 695 | 9.2 | 7,638 | (362 | ) | (4.7 | ) | ||||||||||||||||

| Group Management & Services |

359 | (216 | ) | — | 266 | (392 | ) | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| 22,287 | 2,080 | 9.3 | 22,579 | (269 | ) | (1.2 | ) | |||||||||||||||||

26 Q4 2011 Quarterly report

Sectors and main countries

in millions of euros

| Sales and total assets |

| sales | total assets | |||||||||||||||

| January-December | December 31, | December 31, | ||||||||||||||

| 2010 | 2011 | 2010 | 2011 | |||||||||||||

| Healthcare |

8,601 | 8,852 | 11,962 | 11,591 | ||||||||||||

| Consumer Lifestyle |

5,775 | 5,823 | 3,858 | 3,616 | ||||||||||||

| Lighting |

7,552 | 7,638 | 7,379 | 6,771 | ||||||||||||

| Group Management & Services |

359 | 266 | 8,950 | 6,437 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 22,287 | 22,579 | 32,149 | 28,415 | |||||||||||||

| Assets classified as held for sale |

120 | 1) | 551 | |||||||||||||

|

|

|

|

|

|||||||||||||

| 32,269 | 28,966 | |||||||||||||||

| 1) | Revised to reflect a property, plant and equipment reclassification to assets classified as held for sale |

| Sales and tangible and intangible assets |

| sales | tangible and intangible assets1) | |||||||||||||||

| January-December | December 31, | December 31, | ||||||||||||||

| 20102) | 2011 | 20102,3) | 2011 | |||||||||||||

| Netherlands |

661 | 691 | 1,109 | 908 | ||||||||||||

| United States |

6,430 | 6,373 | 9,693 | 8,473 | ||||||||||||

| China |

1,864 | 2,102 | 785 | 1,126 | ||||||||||||

| Germany |

1,436 | 1,431 | 282 | 252 | ||||||||||||

| France |

1,134 | 1,046 | 100 | 97 | ||||||||||||

| Japan |

856 | 911 | 568 | 618 | ||||||||||||

| Brazil |

654 | 694 | 148 | 119 | ||||||||||||

| Other countries |

9,252 | 9,331 | 2,693 | 2,433 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| 22,287 | 22,579 | 15,378 | 14,026 | |||||||||||||

| 1) | Includes property, plant and equipment, intangible assets excluding goodwill, and goodwill |

| 2) | Revised to reflect an adjusted country allocation |

| 3) | Revised to reflect a property, plant and equipment reclassification to assets classified as held for sale |

Q4 2011 Quarterly report 27

Pension costs

in millions of euros

| Specification of pension costs |

| 4th quarter | ||||||||||||||||||||||||

| 2010 | 2011 | |||||||||||||||||||||||

| Netherlands | other | total | Netherlands | other | total | |||||||||||||||||||

| Costs of defined-benefit plans (pensions) |

||||||||||||||||||||||||

| Service cost |

23 | 18 | 41 | 32 | 18 | 50 | ||||||||||||||||||

| Interest cost on the defined-benefit obligation |

130 | 105 | 235 | 139 | 101 | 240 | ||||||||||||||||||

| Expected return on plan assets |

(186 | ) | (86 | ) | (272 | ) | (178 | ) | (98 | ) | (276 | ) | ||||||||||||

| Curtailments |

— | (1 | ) | (1 | ) | — | (3 | ) | (3 | ) | ||||||||||||||

| Settlements |

— | (6 | ) | (6 | ) | — | (1 | ) | (1 | ) | ||||||||||||||

| Prior service cost |

— | (83 | ) | (83 | ) | — | (22 | ) | (22 | ) | ||||||||||||||

| Other |

1 | 1 | 2 | (1 | ) | 1 | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net periodic cost (income) |

(32 | ) | (52 | ) | (84 | ) | (8 | ) | (4 | ) | (12 | ) | ||||||||||||

| of which discontinued operations |

— | — | — | — | (1 | ) | (1 | ) | ||||||||||||||||

| Costs of defined-contribution plans |

1 | 26 | 27 | 1 | 29 | 30 | ||||||||||||||||||

| of which discontinued operations |

— | 1 | 1 | — | 1 | 1 | ||||||||||||||||||

| Costs of defined-benefit plans (retiree medical) |

||||||||||||||||||||||||

| Service cost |

— | 1 | 1 | — | — | — | ||||||||||||||||||

| Interest cost on the defined-benefit obligation |

— | 5 | 5 | — | 4 | 4 | ||||||||||||||||||

| Curtailment |

— | (9 | ) | (9 | ) | — | — | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net periodic cost |

— | (3 | ) | (3 | ) | — | 4 | 4 | ||||||||||||||||

| Specification of pension costs |

| January-December | ||||||||||||||||||||||||

| 2010 | 2011 | |||||||||||||||||||||||

| Netherlands | other | total | Netherlands | other | total | |||||||||||||||||||

| Costs of defined-benefit plans (pensions) |

||||||||||||||||||||||||

| Service cost |

92 | 77 | 169 | 127 | 73 | 200 | ||||||||||||||||||

| Interest cost on the defined-benefit obligation |

521 | 418 | 939 | 557 | 404 | 961 | ||||||||||||||||||

| Expected return on plan assets |

(743 | ) | (344 | ) | (1,087 | ) | (713 | ) | (389 | ) | (1,102 | ) | ||||||||||||

| Curtailment |

— | (1 | ) | (1 | ) | — | (18 | ) | (18 | ) | ||||||||||||||

| Settlement |

— | (6 | ) | (6 | ) | — | (1 | ) | (1 | ) | ||||||||||||||

| Prior service cost |

— | (119 | ) | (119 | ) | — | (20 | ) | (20 | ) | ||||||||||||||

| Other |

1 | 1 | 2 | (1 | ) | 1 | — | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net periodic cost (income) |

(129 | ) | 26 | (103 | ) | (30 | ) | 50 | 20 | |||||||||||||||

| of which discontinued operations |

2 | — | 2 | 2 | — | 2 | ||||||||||||||||||

| Costs of defined-contribution plans |

7 | 111 | 118 | 7 | 116 | 123 | ||||||||||||||||||

| of which discontinued operations |

— | 4 | 4 | — | 3 | 3 | ||||||||||||||||||

| Costs of defined-benefit plans (retiree medical) |

||||||||||||||||||||||||

| Service cost |

— | 2 | 2 | — | 1 | 1 | ||||||||||||||||||

| Interest cost on the defined-benefit obligation |

— | 20 | 20 | — | 17 | 17 | ||||||||||||||||||

| Prior service cost |

— | (2 | ) | (2 | ) | — | (2 | ) | (2 | ) | ||||||||||||||

| Curtailment |

— | (9 | ) | (9 | ) | — | — | — | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net periodic cost |

— | 11 | 11 | — | 16 | 16 | ||||||||||||||||||

28 Q4 2011 Quarterly report

Reconciliation of non-GAAP performance measures

all amounts in millions of euros unless otherwise stated.

Certain non-GAAP financial measures are presented when discussing the Philips Group’s performance. In the following tables, a reconciliation to the most directly comparable IFRS performance measure is made.

Sales growth composition (in %)

| 4th quarter | January-December | |||||||||||||||||||||||||||||||

| comparable growth |

currency effects |

consolidation changes |

nominal growth |

comparable growth |

currency effects |

consolidation changes |

nominal growth |

|||||||||||||||||||||||||

| 2011 versus 2010 |

||||||||||||||||||||||||||||||||

| Healthcare |

2.5 | 0.4 | 0.2 | 3.1 | 5.3 | (2.5 | ) | 0.1 | 2.9 | |||||||||||||||||||||||

| Consumer Lifestyle |

0.6 | (0.5 | ) | 3.1 | 3.2 | (0.1 | ) | (1.7 | ) | 2.6 | 0.8 | |||||||||||||||||||||

| Lighting |

7.2 | (0.5 | ) | (1.8 | ) | 4.9 | 6.1 | (2.3 | ) | (2.7 | ) | 1.1 | ||||||||||||||||||||

| GM&S |

7.0 | 1.1 | (31.1 | ) | (23.0 | ) | 2.4 | — | (28.3 | ) | (25.9 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

| Philips Group |

3.4 | (0.1 | ) | — | 3.3 | 4.1 | (2.2 | ) | (0.6 | ) | 1.3 | |||||||||||||||||||||

EBITA (or Adjusted income from operations) to Income from operations (or EBIT)

| Philips Group | Healthcare | Consumer Lifestyle |

Lighting | GM&S | ||||||||||||||||

| January to December 2011 |

||||||||||||||||||||

| EBITA (or Adjusted income from operations) |

1,680 | 1,145 | 472 | 445 | (382 | ) | ||||||||||||||

| Amortization of intangibles1) |

(594 | ) | (228 | ) | (80 | ) | (276 | ) | (10 | ) | ||||||||||

| Impairment of goodwill |

(1,355 | ) | (824 | ) | — | (531 | ) | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations (or EBIT) |

(269 | ) | 93 | 392 | (362 | ) | (392 | ) | ||||||||||||

| January to December 2010 |

||||||||||||||||||||

| EBITA (or Adjusted income from operations) |

2,562 | 1,186 | 718 | 869 | (211 | ) | ||||||||||||||

| Amortization of intangibles1) |

(482 | ) | (264 | ) | (39 | ) | (174 | ) | (5 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from operations (or EBIT) |

2,080 | 922 | 679 | 695 | (216 | ) | ||||||||||||||

| 1) | Excluding amortization of software and product development |

Composition of net debt to group equity

| December 31, 2010 |

December 31, 2011 |

|||||||

| Long-term debt |

2,818 | 3,278 | ||||||

| Short-term debt |

1,840 | 582 | ||||||

|

|

|

|

|

|||||

| Total debt |

4,658 | 3,860 | ||||||

| Cash and cash equivalents |

5,833 | 3,147 | ||||||

|

|

|

|

|

|||||

| Net debt (cash) (total debt less cash and cash equivalents) |

(1,175 | ) | 713 | |||||

| Shareholders’ equity |

15,046 | 12,355 | ||||||

| Non-controlling interests |

46 | 34 | ||||||

|

|

|

|

|

|||||

| Group equity |

15,092 | 12,389 | ||||||

| Net debt and group equity |

13,917 | 13,102 | ||||||

| Net debt divided by net debt and group equity (in %) |

(8 | ) | 5 | |||||

| Group equity divided by net debt and group equity (in %) |

108 | 95 | ||||||

Q4 2011 Quarterly report 29

Reconciliation of non-GAAP performance measures (continued)

all amounts in millions of euros

Net operating capital to total assets

| Philips Group | Healthcare | Consumer Lifestyle |

Lighting | GM&S | ||||||||||||||||

| December 31, 2011 |

||||||||||||||||||||

| Net operating capital (NOC) |

10,427 | 8,418 | 887 | 5,020 | (3,898 | ) | ||||||||||||||

| Exclude liabilities comprised in NOC: |

||||||||||||||||||||

| - payables/liabilities |

9,940 | 2,697 | 2,081 | 1,450 | 3,712 | |||||||||||||||

| - intercompany accounts |

— | 103 | 87 | 51 | (241 | ) | ||||||||||||||

| - provisions |

2,639 | 287 | 558 | 227 | 1,567 | |||||||||||||||

| Include assets not comprised in NOC: |

||||||||||||||||||||

| - investments in associates |

203 | 86 | 3 | 23 | 91 | |||||||||||||||

| - other current financial assets |

— | — | — | — | — | |||||||||||||||

| - other non-current financial assets |

346 | — | — | — | 346 | |||||||||||||||

| - deferred tax assets |

1,713 | — | — | — | 1,713 | |||||||||||||||

| - cash and cash equivalents |

3,147 | — | — | — | 3,147 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| 28,415 | 11,591 | 3,616 | 6,771 | 6,437 | ||||||||||||||||

| Assets classified as held for sale |

551 | |||||||||||||||||||

|

|

|

|||||||||||||||||||

| Total assets |

28,966 | |||||||||||||||||||

| December 31, 2010 |

||||||||||||||||||||

| Net operating capital (NOC) |

11,951 | 8,908 | 911 | 5,561 | (3,429 | )1) | ||||||||||||||

| Exclude liabilities comprised in NOC: |

||||||||||||||||||||

| - payables/liabilities |

10,009 | 2,603 | 2,509 | 1,485 | 3,412 | |||||||||||||||

| - intercompany accounts |

— | 54 | 95 | 68 | (217 | ) | ||||||||||||||

| - provisions |

2,339 | 321 | 342 | 247 | 1,429 | |||||||||||||||

| Include assets not comprised in NOC: |

||||||||||||||||||||

| - investments in associates |

181 | 76 | 1 | 18 | 86 | |||||||||||||||

| - other current financial assets |

6 | — | — | — | 6 | |||||||||||||||

| - other non - current financial assets |

479 | — | — | — | 479 | |||||||||||||||

| - deferred tax assets |

1,351 | — | — | — | 1,351 | |||||||||||||||

| - cash and cash equivalents |

5,833 | — | — | — | 5,833 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| 32,149 | 11,962 | 3,858 | 7,379 | 8,950 | ||||||||||||||||

| Assets classified as held for sale1) |

120 | |||||||||||||||||||

|

|

|

|||||||||||||||||||

| Total assets |

32,269 | |||||||||||||||||||

| 1) | Revised to reflect a property, plant and equipment reclassification to assets classified as held for sale |

30 Q4 2011 Quarterly report

Reconciliation of non-GAAP performance measures (continued)

all amounts in millions of euros

Composition of cash flows

| 4th quarter | January-December | |||||||||||||||

| 2010 | 2011 | 2010 | 2011 | |||||||||||||

| Cash flows provided by operating activities |

1,366 | 1,207 | 2,121 | 836 | ||||||||||||

| Cash flows used for investing activities |

(275 | ) | (511 | ) | (646 | ) | (1,364 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Cash flows before financing activities |

1,091 | 696 | 1,475 | (528 | ) | |||||||||||

| Cash flows provided by operating activities |

1,366 | 1,207 | 2,121 | 836 | ||||||||||||

| Purchase of intangible assets |

(36 | ) | (28 | ) | (80 | ) | (116 | ) | ||||||||

| Expenditures on development assets |

(56 | ) | (63 | ) | (193 | ) | (231 | ) | ||||||||

| Capital expenditures on property, plant and equipment |

(174 | ) | (203 | ) | (621 | ) | (725 | ) | ||||||||

| Proceeds from disposals of property, plant and equipment |

52 | 48 | 129 | 128 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net capital expenditures |

(214 | ) | (246 | ) | (765 | ) | (944 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Free cash flows |

1,152 | 961 | 1,356 | (108 | ) | |||||||||||

Q4 2011 Quarterly report 31

Restatement impact of 2012 accounting changes on 2011 figures

As of 2012, we will implement the following three accounting policy changes.

Warranty costs, currently reported in Selling expenses on the income statement, will be reclassified to Cost of sales. The change follows the rationale that warranty costs are an integral part of the sale of goods and services. Amortization of brand name and customer relationship intangible assets currently reported in Cost of sales on the income statement will be reclassified to Selling expenses. This change follows the rationale that the use of brand name and customer relationship intangible assets supports the sales process. The third change relates to intellectual property (IP) policy. Currently, IP royalties on products sold by a sector are allocated to that sector, with the exception of Consumer Lifestyle; At Consumer Lifestyle IP royalties on products no longer sold by the sector are still allocated to it. As of 2012, all IP royalties on products no longer sold by a sector will be allocated to GM&S.

The table below reflects the impact of the accounting changes for the quarters and full year of 2011.

In millions of euros

| 2011 | ||||||||||||||||||||

| 1st quarter | 2nd quarter | 3rd quarter | 4th quarter | Full year | ||||||||||||||||

| IP royalty income (from CL to GM&S) |

||||||||||||||||||||

| Sales |

54 | 48 | 44 | 62 | 208 | |||||||||||||||

| EBIT |

43 | 39 | 39 | 54 | 175 | |||||||||||||||

| EBITA |

43 | 39 | 39 | 54 | 175 | |||||||||||||||

| Amortization of brand name and customer relationship intangible assets1) |

||||||||||||||||||||

| Cost of sales |

67 | 69 | 81 | 198 | 415 | |||||||||||||||

| Selling expenses |

(67 | ) | (69 | ) | (81 | ) | (198 | ) | (415 | ) | ||||||||||

| Warranty costs1) |

||||||||||||||||||||

| Cost of sales |

(80 | ) | (68 | ) | (66 | ) | (114 | ) | (328 | ) | ||||||||||

| Selling expenses |

80 | 68 | 66 | 114 | 328 | |||||||||||||||

| 1) | A positive amount is less costs and a negative amount is additional costs |

32 Q4 2011 Quarterly report

Philips quarterly statistics

all amounts in millions of euros unless otherwise stated

| 2010 | 2011 | |||||||||||||||||||||||||||||||

| 1st | 2nd | 3rd | 4th | 1st | 2nd | 3rd | 4th | |||||||||||||||||||||||||

| quarter | quarter | quarter | quarter | quarter | quarter | quarter | quarter | |||||||||||||||||||||||||

| Sales |

4,982 | 5,350 | 5,460 | 6,495 | 5,257 | 5,216 | 5,394 | 6,712 | ||||||||||||||||||||||||

| % increase |

13 | 15 | 12 | 5 | 6 | (3 | ) | (1 | ) | 3 | ||||||||||||||||||||||

| EBITA |

495 | 507 | 647 | 913 | 438 | 371 | 368 | 503 | ||||||||||||||||||||||||

| as a % of sales |

9.9 | 9.5 | 11.8 | 14.1 | 8.3 | 7.1 | 6.8 | 7.5 | ||||||||||||||||||||||||

| EBIT |

381 | 385 | 518 | 796 | 319 | (1,123 | ) | 273 | 262 | |||||||||||||||||||||||

| as a % of sales |

7.6 | 7.2 | 9.5 | 12.3 | 6.1 | (21.5 | ) | 5.1 | 3.9 | |||||||||||||||||||||||

| Net income (loss) |

201 | 262 | 524 | 465 | 138 | (1,345 | ) | 76 | (160 | ) | ||||||||||||||||||||||

| Net income (loss) - shareholders per common share in euros basic |

0.22 | 0.28 | 0.55 | 0.49 | 0.14 | (1.39 | ) | 0.08 | (0.17 | ) | ||||||||||||||||||||||

| January- | January- | January- | January- | January- | January- | January- | January- | |||||||||||||||||||||||||

| March | June | September | December | March | June | September | December | |||||||||||||||||||||||||

| Sales |

4,982 | 10,332 | 15,792 | 22,287 | 5,257 | 10,473 | 15,867 | 22,579 | ||||||||||||||||||||||||

| % increase |

13 | 14 | 14 | 11 | 6 | 1 | 0 | 1 | ||||||||||||||||||||||||

| EBITA |

495 | 1,002 | 1,649 | 2,562 | 438 | 809 | 1,177 | 1,680 | ||||||||||||||||||||||||

| as a % of sales |

9.9 | 9.7 | 10.4 | 11.5 | 8.3 | 7.7 | 7.4 | 7.4 | ||||||||||||||||||||||||

| EBIT |

381 | 766 | 1,284 | 2,080 | 319 | (804 | ) | (531 | ) | (269 | ) | |||||||||||||||||||||

| as a % of sales |

7.6 | 7.4 | 8.1 | 9.3 | 6.1 | (7.7 | ) | (3.3 | ) | (1.2 | ) | |||||||||||||||||||||

| Net income (loss) |

201 | 463 | 987 | 1,452 | 138 | (1,207 | ) | (1,131 | ) | (1,291 | ) | |||||||||||||||||||||

| Net income (loss) - shareholders per common share in euros basic |

0.22 | 0.49 | 1.05 | 1.54 | 0.14 | (1.26 | ) | (1.18 | ) | (1.36 | ) | |||||||||||||||||||||

| Net income (loss) from continuing operations as a % of shareholders’ equity |

5.7 | 6.3 | 9.2 | 9.8 | 6.6 | (14.8 | ) | (8.8 | ) | (5.8 | ) | |||||||||||||||||||||

| period ended 2010 | period ended 2011 | |||||||||||||||||||||||||||||||

| Inventories as a % of sales1) |

15.1 | 16.9 | 16.8 | 15.7 | 15.7 | 16.8 | 18.2 | 16.1 | ||||||||||||||||||||||||

| Inventories excluding discontinued operations |

3,128 | 3,602 | 3,682 | 3,496 | 3,545 | 3,776 | 4,074 | 3,625 | ||||||||||||||||||||||||

| Net debt : group equity ratio |

1:99 | 2:98 | 1:99 | (8):108 | (3):103 | 1:99 | 8:92 | 5:95 | ||||||||||||||||||||||||

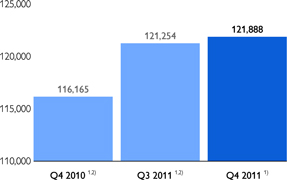

| Total employees (in thousands)2) |

117 | 117 | 118 | 120 | 122 | 125 | 125 | 125 | ||||||||||||||||||||||||

| of which discontinued operations |

5 | 5 | 4 | 4 | 4 | 4 | 4 | 3 | ||||||||||||||||||||||||

| 1) | Excludes discontinued operations for both inventories and sales figures |

| 2) | Adjusted to reflect a change of employees reported in the Healthcare sector for the past periods |

Information also available on Internet, address: www.philips.com/investorrelations

Q4 2011 Quarterly report 33

| © 2011 Koninklijke Philips Electronics N.V. | http://www.philips.com/investorrelations | |

| All rights reserved. |

Fourth Quarter and Annual Results 2011

January 30, 2012

Philips reports fourth-quarter sales of EUR 6.7 billion; EBITA of EUR 503 million

| • | Comparable sales up 3%, led by 7% growth at Lighting |

| • | Growth geographies sales up 12% on a comparable basis |

| • | EBITA of 7.5% of sales |

| • | Net income from continuing operations at EUR 112 million |

| • | Free cash flow of EUR 961 million |

| • | Proposed dividend stable at EUR 0.75 per share |

Q4 financials: Year-on-year revenue increased across all operating sectors. EBITA margin declined from 14.1% in Q4 2010 to 7.5% in Q4 2011.

Healthcare comparable sales were 3% higher year-on-year. Comparable equipment order intake grew 3% year-on-year. Equipment orders in growth geographies grew by 17%. Results were impacted by weakness in the European markets, postponed deliveries of existing orders, as well as increased investments in new product innovation and sales channels.

Consumer Lifestyle sales increased 1% on a comparable basis. At an aggregate level, the three growth businesses – Personal Care, Health & Wellness, and Domestic Appliances – achieved a high single-digit comparable sales increase compared to the fourth quarter of 2010. The sector growth rate was impacted by a comparable sales decline at Lifestyle Entertainment. Reported EBITA margin for the quarter was 10%.

Lighting comparable sales increased 7% year-on-year, driven by double-digit sales growth at Lamps and Automotive. LED-based sales grew 37% compared to Q4 2010, now representing 18% of total Lighting sales. Sales in growth geographies increased by 21% in the quarter. Results were impacted by pricing, inventory reduction measures, and operational issues. As part of the turnaround plan, most brands for Consumer Luminaires products will be re-branded as Philips, which resulted in a value adjustment of commercial and brand-related assets leading to a charge of EUR 128 million.

Working capital reductions in the sectors amounted to more than EUR 500 million in the quarter, contributing to a free cash inflow of EUR 961 million in the fourth quarter.

The company completed 35% of its EUR 2 billion share buy-back program since the start of the program in July 2011. Taking into consideration the volatility of the financial markets, Philips has decided to extend the timing of the program until the end of Q2 2013.

Moving forward on Accelerate!, Philips’ change and performance improvement program

Philips is seeing the initial signs of the Accelerate! program positively impacting sales growth in difficult market circumstances. Importantly, the company has attracted key talent for critical positions across the company.

In addition, as part of the company’s efforts to improve its end-to-end processes, inventory as a percentage of sales decreased to 16.1% from 18.2% in Q3 2011, representing a comparable decrease of EUR 585 million, which is an improvement compared to the decrease in inventory seen in the same period last year.

The actions to deliver on the overhead cost reduction program are on track, and the first planned cost savings were realized in the quarter.

The annual incentive system for the executives has been changed to reflect line-of-sight accountability and is now fully aligned with the key performance indicators of the 2013 mid-term financial targets.

CEO quote:

“Our fourth quarter results were impacted by weak European sales, postponement in deliveries of existing orders in our Healthcare sector, and inventory correction actions and other operational issues in our Lighting business. These issues were partially offset by solid results in our Consumer Lifestyle growth businesses, which benefited from the early adoption of the Accelerate! change and performance improvement program. In addition, we delivered strong free cash flow as a result of our work to reduce working capital.

We are cautious about 2012 given the uncertainty in the global economy, and Europe in particular. In addition, we expect our 2012 results to be affected by the previously communicated restructuring charges and one-time investments aimed at improving our business performance trajectory, as part of the multi-year Accelerate! program. Excluding these additional charges, we expect the underlying operating margins and capital efficiency in the sectors to improve in the latter part of 2012.

While we are concerned about the economic environment, all of us at Philips are fully committed to improve our operational performance to achieve our mid-term (2013) financial targets.”

Frans van Houten, CEO of Royal Philips Electronics

Click here to view the social media release, complete with downloadable multimedia

For further information, please contact:

Steve Klink

Corporate Communications

Tel: +31 20 5977 415

Email: steve.klink@philips.com

Joost Akkermans

Corporate Communications

Tel: +31 20 5977 406

E-mail: joost.akkermans@philips.com

About Royal Philips Electronics

Royal Philips Electronics of the Netherlands (NYSE: PHG, AEX: PHI) is a diversified health and well-being company, focused on improving people’s lives through timely innovations. As a world leader in

healthcare, lifestyle and lighting, Philips integrates technologies and design into people-centric solutions, based on fundamental customer insights and the brand promise of “sense and simplicity.” Headquartered in the Netherlands, Philips employs approximately 122,000 employees with sales and services in more than 100 countries worldwide. With sales of EUR 22.6 billion in 2011, the company is a market leader in cardiac care, acute care and home healthcare, energy efficient lighting solutions and new lighting applications, as well as lifestyle products for personal well-being and pleasure with strong leadership positions in male shaving and grooming, portable entertainment and oral healthcare. News from Philips is located at www.philips.com/newscenter.

Forward-looking statements

This document contains certain forward-looking statements with respect to the financial condition, results of operations and business of Philips and certain of the plans and objectives of Philips with respect to these items, in particular the sector sections “Miscellaneous”. Examples of forward-looking statements include statements made about our strategy, estimates of sales growth, future EBITA and future developments in our organic business. By their nature, these statements involve risk and uncertainty because they relate to future events and circumstances and there are many factors that could cause actual results and developments to differ materially from those expressed or implied by these statements.

These factors include but are not limited to domestic and global economic and business conditions, the successful implementation of our strategy and our ability to realize the benefits of this strategy, our ability to develop and market new products, changes in legislation, legal claims, changes in exchange and interest rates, changes in tax rates, pension costs and actuarial assumptions, raw materials and employee costs, our ability to identify and complete successful acquisitions and to integrate those acquisitions into our business, our ability to successfully exit certain businesses or restructure our operations, the rate of technological changes, political, economic and other developments in countries where Philips operates, industry consolidation and competition. As a result, Philips’ actual future results may differ materially from the plans, goals and expectations set forth in such forward looking statements. For a discussion of factors that could cause future results to differ from such forward-looking statements, see the Risk management chapter included in our Annual Report 2010 and the “Risk and uncertainties” section in our semi-annual financial report for the six months ended July 3, 2011.

Third-party market share data

Statements regarding market share, including those regarding Philips’ competitive position, contained in this document are based on outside sources such as research institutes, industry and dealer panels in combination with management estimates. Where information is not yet available to Philips, those statements may also be based on estimates and projections prepared by outside sources or management. Rankings are based on sales unless otherwise stated.

Use of non-GAAP information

In presenting and discussing the Philips Group’s financial position, operating results and cash flows, management uses certain non-GAAP financial measures. These non-GAAP financial measures should not be viewed in isolation as alternatives to the equivalent IFRS measures and should be used in conjunction with the most directly comparable IFRS measures. A reconciliation of such measures to the most directly comparable IFRS measures is contained in this document. Further information on non-GAAP measures can be found in our Annual Report 2010.

Use of fair-value measurements

In presenting the Philips Group’s financial position, fair values are used for the measurement of various items in accordance with the applicable accounting standards. These fair values are based on market prices, where available, and are obtained from sources that are deemed to be reliable. Readers are cautioned that these values are subject to changes over time and are only valid at the balance sheet date. When quoted prices or observable market data do not exist, we estimated the fair values using appropriate valuation models and unobservable inputs. They require management to make significant assumptions with respect to future developments, which are inherently uncertain and may therefore deviate from actual developments. Critical assumptions used are disclosed in our 2010 financial statements. Independent valuations may have been obtained to support management’s determination of fair-values.

All amounts in millions of euros unless otherwise stated; data included are unaudited. Financial reporting is in accordance with IFRS, unless otherwise stated. This document comprises regulated information within the meaning of the Dutch Financial Markets Supervision Act ‘Wet op het Financieel Toezicht’.