|

Amendment No. 1 dated November 29, 2019 to the Pricing Supplement dated November 25, 2019 (To the Prospectus dated August 1, 2019, the Prospectus Supplement dated August 1, 2019 and the Underlying Supplement dated August 1, 2019) |

Filed Pursuant to Rule 424(b)(2) Registration No. 333–232144 |

|

|

$5,000,000 Callable Range Accrual Notes due November 30, 2027 Linked to the Performance of the S&P 500® Index Global Medium-Term Notes, Series A |

Terms used in this pricing supplement, but not defined herein, shall have the meanings ascribed to them in the prospectus supplement.

|

Issuer: |

Barclays Bank PLC |

|

Denominations: |

Minimum denomination of $1,000, and integral multiples of $1,000 in excess thereof |

|

Initial Valuation Date: |

November 25, 2019 |

|

Issue Date: |

November 29, 2019 |

|

Final Valuation Date:* |

November 24, 2027 |

|

Maturity Date:* |

November 30, 2027 |

|

Reference Asset: |

The S&P 500® Index (Bloomberg ticker symbol “SPX <Index>”) |

|

Valuation Dates:* |

The 25th of each month during the term of the Notes, beginning in December 2019, provided that the final Valuation Date will be the Final Valuation Date set forth above; provided further that if any such date is not a Scheduled Trading Day, the scheduled Valuation Date will be the next following Scheduled Trading Day |

|

Interest Payment Dates: |

With respect to each Valuation Date, the fifth business day following such Valuation Date, provided that the final Interest Payment Date shall be the Maturity Date |

|

Early Redemption at the Option of the Issuer: |

The Notes cannot be redeemed for the first year after the Issue Date. We may redeem the Notes (in whole but not in part) at our sole discretion without your consent at the Redemption Price set forth below on any Interest Payment Date prior to the Maturity Date, beginning with the Interest Payment Date following the twelfth Valuation Date, provided that we give at least five business days’ prior written notice to the trustee. No further amounts will be payable after they have been redeemed. If we exercise our redemption option, the Interest Payment Date on which we exercise such option will be referred to as the “Early Redemption Date.” |

|

Redemption Price: |

$1,000 per $1,000 principal amount Note, plus the Interest Payment (if any) that is payable on the relevant Interest Payment Date |

|

|

|

|

Payment at Maturity: |

If the Notes are not redeemed prior to scheduled maturity, and if you hold the Notes to maturity, you will receive on the Maturity Date (in each case, in addition to the final Interest Payment, if one is payable) a cash payment per $1,000 principal amount Note that you hold determined as follows:

§ If the Final Value of the Reference Asset is greater than or equal to the Buffer Value, you will receive a payment of $1,000 per $1,000 principal amount Note

§ If the Final Value of the Reference Asset is less than the Buffer Value, you will receive an amount per $1,000 principal amount Note calculated as follows:

$1,000 + [$1,000 × (Reference Asset Return + Buffer Percentage)]

If the Notes are not redeemed prior to scheduled maturity, and if the Final Value of the Reference Asset is less than the Buffer Value, you will lose 1.00% of the principal amount of your Notes for every 1.00% that the Reference Asset Return falls below -20.00%. You may lose up to 80.00% of the principal amount of your Notes at maturity.

Any payment on the Notes, including any repayment of principal, is not guaranteed by any third party and is subject to (a) the creditworthiness of Barclays Bank PLC and (b) the risk of exercise of any U.K. Bail-in Power (as described on page PS-2 of this pricing supplement) by the relevant U.K. resolution authority. If Barclays Bank PLC were to default on its payment obligations or become subject to the exercise of any U.K. Bail-in Power (or any other resolution measure) by the relevant U.K. resolution authority, you might not receive any amounts owed to you under the Notes. See “Consent to U.K. Bail-in Power” and “Selected Risk Considerations” in this pricing supplement and “Risk Factors” in the accompanying prospectus supplement for more information. |

|

|

|

|

Consent to U.K. Bail-in Power: |

Notwithstanding any other agreements, arrangements or understandings between Barclays Bank PLC and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority. See “Consent to U.K. Bail-in Power” on page PS–2 of this pricing supplement. |

[Terms of the Notes Continue on the Next Page]

|

|

|

Initial Issue Price(1) |

|

Price to Public |

|

Agent’s Commission(2) |

|

Proceeds to Barclays Bank PLC |

|

Per Note |

|

$1,000 |

|

100% |

|

4.00% |

|

96.00% |

|

Total |

|

$5,000,000 |

|

$5,000,000 |

|

$200,000 |

|

$4,800,000 |

(1) Because dealers who purchase the Notes for sale to certain fee-based advisory accounts may forgo some or all selling concessions, fees or commissions, the public offering price for investors purchasing the Notes in such fee-based advisory accounts may be between $960.00 and $1,000 per Note. Investors that hold their Notes in fee-based advisory or trust accounts may be charged fees by the investment advisor or manager of such account based on the amount of assets held in those accounts, including the Notes.

(2) Our estimated value of the Notes on the Initial Valuation Date, based on our internal pricing models, is $948.30 per Note. The estimated value is less than the initial issue price of the Notes. See “Additional Information Regarding Our Estimated Value of the Notes” on page PS–3 of this pricing supplement.

(3) Barclays Capital Inc. will receive commissions from the Issuer of $40.00 per $1,000 principal amount Note. Barclays Capital Inc. will use these commissions to pay selling concessions or fees (including custodial or clearing fees) to other dealers.

Investing in the Notes involves a number of risks. See “Risk Factors” beginning on page S–7 of the prospectus supplement and “Selected Risk Considerations” beginning on page PS–9 of this pricing supplement.

We may use this pricing supplement in the initial sale of Notes. In addition, Barclays Capital Inc. or another of our affiliates may use this pricing supplement in market resale transactions in any Notes after their initial sale. Unless we or our agent informs you otherwise in the confirmation of sale, this pricing supplement is being used in a market resale transaction.

The Notes will not be listed on any U.S. securities exchange or quotation system. Neither the U.S. Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these Notes or determined that this pricing supplement is truthful or complete. Any representation to the contrary is a criminal offense.

The Notes constitute our unsecured and unsubordinated obligations. The Notes are not deposit liabilities of Barclays Bank PLC and are not covered by the U.K. Financial Services Compensation Scheme or insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or deposit insurance agency of the United States, the United Kingdom or any other jurisdiction.

Terms of the Notes, Continued

|

Accrual Period: |

Each Accrual Period will begin on, and exclude, the preceding Valuation Date (or, if there is no preceding Valuation Date, the Initial Valuation Date) and end on, and include, the next Valuation Date |

|

|

|

|

Above Barrier Rate: |

0.42083% (equivalent to a rate of 5.05% per annum) |

|

|

|

|

Interest Payment: |

The Interest Payment payable on each Interest Payment Date, with respect to the relevant Accrual Period, will be calculated as follows:

$1,000 × Interest Rate

|

|

Interest Rate: |

With respect to each Accrual Period, an amount calculated as follows:

Above Barrier Rate × Accrual Factor

|

|

Accrual Factor: |

For any Accrual Period, the number of Scheduled Trading Days in that Accrual Period on which the Closing Value of the Reference Asset is greater than or equal to the Coupon Barrier Value, divided by the total number of Scheduled Trading Days in that Accrual Period |

|

|

|

|

Reference Asset Return: |

The performance of the Reference Asset from the Initial Value to the Final Value, calculated as follows:

Final Value – Initial Value

|

|

Initial Value: |

3,133.64, the Closing Value of the Reference Asset on the Initial Valuation Date (rounded to two decimal places) |

|

Buffer Value: |

2,506.91, 80.00% of the Initial Value (rounded to two decimal places) |

|

Final Value: |

The Closing Value of the Reference Asset on the Final Valuation Date (rounded to two decimal places) |

|

Coupon Barrier Value: |

2,506.91, which is 80.00% of the Initial Value (rounded to two decimal places) |

|

Buffer Percentage: |

20.00% |

|

Closing Value: |

The term “Closing Value” means the closing level of the Reference Asset, as further described under “Reference Assets—Indices—Special Calculation Provisions” in the prospectus supplement, rounded to two decimal places |

|

Scheduled Trading Day: |

The term “Scheduled Trading Day” has the meaning set forth under “Reference Assets—Indices—Market Disruption Events for Securities with an Index of Equity Securities as a Reference Asset” in the prospectus supplement |

|

Business Day Convention: |

Following |

|

Calculation Agent: |

Barclays Bank PLC |

|

CUSIP / ISIN: |

06747NQJ6 / US06747NQJ62 |

* Subject to postponement, as described under “Additional Terms of the Notes” in this pricing supplement.

![]()

ADDITIONAL DOCUMENTS RELATED TO THE OFFERING OF THE NOTES

You should read this pricing supplement together with the prospectus dated August 1, 2019, as supplemented by the prospectus supplement dated August 1, 2019 and the underlying supplement dated August 1, 2019, relating to our Global Medium-Term Notes, Series A, of which these Notes are a part. This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth under “Risk Factors” in the prospectus supplement and “Selected Risk Considerations” in this pricing supplement, as the Notes involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisors before you invest in the Notes.

You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

· Prospectus dated August 1, 2019:

http://www.sec.gov/Archives/edgar/data/312070/000119312519210880/d756086d424b3.htm

· Prospectus Supplement dated August 1, 2019:

http://www.sec.gov/Archives/edgar/data/312070/000095010319010190/dp110493_424b2-prosupp.htm

· Underlying Supplement dated August 1, 2019:

http://www.sec.gov/Archives/edgar/data/312070/000095010319010191/dp110497_424b2-underlying.htm

Our SEC file number is 1–10257. As used in this pricing supplement, “we,” “us” or “our” refers to Barclays Bank PLC.

Notwithstanding any other agreements, arrangements or understandings between us and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority.

Under the U.K. Banking Act 2009, as amended, the relevant U.K. resolution authority may exercise a U.K. Bail-in Power in circumstances in which the relevant U.K. resolution authority is satisfied that the resolution conditions are met. These conditions include that a U.K. bank or investment firm is failing or is likely to fail to satisfy the Financial Services and Markets Act 2000 (the “FSMA”) threshold conditions for authorization to carry on certain regulated activities (within the meaning of section 55B FSMA) or, in the case of a U.K. banking group company that is a European Economic Area (“EEA”) or third country institution or investment firm, that the relevant EEA or third country relevant authority is satisfied that the resolution conditions are met in respect of that entity.

The U.K. Bail-in Power includes any write-down, conversion, transfer, modification and/or suspension power, which allows for (i) the reduction or cancellation of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes; (ii) the conversion of all, or a portion, of the principal amount of, interest on, or any other amounts payable on, the Notes into shares or other securities or other obligations of Barclays Bank PLC or another person (and the issue to, or conferral on, the holder or beneficial owner of the Notes such shares, securities or obligations); and/or (iii) the amendment or alteration of the maturity of the Notes, or amendment of the amount of interest or any other amounts due on the Notes, or the dates on which interest or any other amounts become payable, including by suspending payment for a temporary period; which U.K. Bail-in Power may be exercised by means of a variation of the terms of the Notes solely to give effect to the exercise by the relevant U.K. resolution authority of such U.K. Bail-in Power. Each holder and beneficial owner of the Notes further acknowledges and agrees that the rights of the holders or beneficial owners of the Notes are subject to, and will be varied, if necessary, solely to give effect to, the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority. For the avoidance of doubt, this consent and acknowledgment is not a waiver of any rights holders or beneficial owners of the Notes may have at law if and to the extent that any U.K. Bail-in Power is exercised by the relevant U.K. resolution authority in breach of laws applicable in England.

For more information, please see “Selected Risk Considerations—You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

ADDITIONAL INFORMATION REGARDING OUR ESTIMATED VALUE OF THE NOTES

Our internal pricing models take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize, typically including volatility, interest rates, and our internal funding rates. Our internal funding rates (which are our internally published borrowing rates based on variables such as market benchmarks, our appetite for borrowing, and our existing obligations coming to maturity) may vary from the levels at which our benchmark debt securities trade in the secondary market. Our estimated value on the Initial Valuation Date is based on our internal funding rates. Our estimated value of the Notes may be lower if such valuation were based on the levels at which our benchmark debt securities trade in the secondary market.

Our estimated value of the Notes on the Initial Valuation Date is less than the initial issue price of the Notes. The difference between the initial issue price of the Notes and our estimated value of the Notes is a result of several factors, including any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees (including any structuring or other distribution related fees) to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

Our estimated value on the Initial Valuation Date is not a prediction of the price at which the Notes may trade in the secondary market, nor will it be the price at which Barclays Capital Inc. may buy or sell the Notes in the secondary market. Subject to normal market and funding conditions, Barclays Capital Inc. or another affiliate of ours intends to offer to purchase the Notes in the secondary market but it is not obligated to do so.

Assuming that all relevant factors remain constant after the Initial Valuation Date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market, if any, and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value on the Initial Valuation Date for a temporary period expected to be approximately six months after the Issue Date because, in our discretion, we may elect to effectively reimburse to investors a portion of the estimated cost of hedging our obligations under the Notes and other costs in connection with the Notes which we will no longer expect to incur over the term of the Notes. We made such discretionary election and determined this temporary reimbursement period on the basis of a number of factors, which may include the tenor of the Notes and/or any agreement we may have with the distributors of the Notes. The amount of our estimated costs which we effectively reimburse to investors in this way may not be allocated ratably throughout the reimbursement period, and we may discontinue such reimbursement at any time or revise the duration of the reimbursement period after the initial Issue Date of the Notes based on changes in market conditions and other factors that cannot be predicted.

We urge you to read the “Selected Risk Considerations” beginning on page PS–9 of this pricing supplement.

SELECTED PURCHASE CONSIDERATIONS

The Notes are not suitable for all investors. The Notes may be a suitable investment for you if all of the following statements are true:

· You do not seek an investment that produces fixed periodic interest or coupon payments or other non-contingent sources of current income, and you can tolerate receiving few or no interest payments over the term of the Notes in the event the Closing Value of the Reference Asset is less than the Coupon Barrier Value during any Accrual Period.

· You anticipate that the value of the Reference Asset will remain above the Coupon Barrier Value throughout the term of the Notes.

· You understand and accept the risks that (a) the amount of interest that you receive with respect to any Accrual Period will depend on the number of days in the Accrual Period on which the Closing Value of the Reference Asset equals or exceeds the Coupon Barrier Value, (b) that the interest payable with respect to any Accrual Period may be as low as zero and (c) accordingly, you may not receive any interest payments on your Notes.

· You are willing and able to accept the risk that you may lose up to 80.00% of the principal amount of your Notes.

· You do not anticipate that the Final Value of the Reference Asset will be less than the Buffer Value.

· You understand and are willing and able to accept the risks associated with an investment linked to the performance of the Reference Asset.

· You understand and accept that you will not be entitled to receive dividends or distributions that may be paid to holders of a Reference Asset or any securities to which a Reference Asset provides exposure, nor will you have any voting rights with respect to a Reference Asset or any securities to which a Reference Asset provides exposure.

· You are willing and able to accept the risk that the Notes may be redeemed prior to scheduled maturity and that you may not be able to reinvest your money in an alternative investment with comparable risk and yield.

· You can tolerate fluctuations in the price of the Notes prior to scheduled maturity that may be similar to or exceed the downside fluctuations in the value of the Reference Asset.

· You do not seek an investment for which there will be an active secondary market, and you are willing and able to hold the Notes to maturity if the Notes are not redeemed.

· You are willing and able to assume our credit risk for all payments on the Notes.

· You are willing and able to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority.

The Notes may not be a suitable investment for you if any of the following statements are true:

· You seek an investment that produces fixed periodic interest or coupon payments or other non-contingent sources of current income, and/or you cannot tolerate receiving few or no interest payments over the term of the Notes in the event the Closing Value of the Reference Asset is less than the Coupon Barrier Value during any Accrual Period.

· You seek an investment that provides for the full repayment of principal at maturity, and/or you are unwilling or unable to accept the risk that you may lose up to 80.00% of the principal amount of your Notes.

· You do not anticipate that the value of the Reference Asset will remain above the Coupon Barrier Value throughout the term of the Notes.

· You are unwilling or unable to accept the risk that the Interest Rate for any or all Accrual Periods may be less than the Above Barrier Rate (and may be as low as zero).

· You anticipate that the Final Value of the Reference Asset will be less than the Buffer Value.

· You are unwilling or unable to accept the risks associated with an investment linked to the performance of the Reference Asset.

· You seek an investment that entitles you to dividends or distributions on, or voting rights related to a Reference Asset or any securities to which a Reference Asset provides exposure.

· You are unwilling or unable to accept the risk that the Notes may be redeemed prior to scheduled maturity.

· You cannot tolerate fluctuations in the price of the Notes prior to scheduled maturity that may be similar to or exceed the downside fluctuations in the value of the Reference Asset.

· You seek an investment for which there will be an active secondary market, and/or you are unwilling or unable to hold the Notes to maturity if the Notes are not redeemed.

· You prefer the lower risk, and therefore accept the potentially lower returns, of fixed income investments with comparable maturities and credit ratings.

· You are unwilling or unable to assume our credit risk for all payments on the Notes.

· You are unwilling or unable to consent to the exercise of any U.K. Bail-in Power by any relevant U.K. resolution authority.

You must rely on your own evaluation of the merits of an investment in the Notes. You should reach a decision whether to invest in the Notes after carefully considering, with your advisors, the suitability of the Notes in light of your investment objectives and the specific information set out in this pricing supplement and the documents referenced under “Additional Documents Related to the Offering of the Notes” in this pricing supplement. Neither the Issuer nor Barclays Capital Inc. makes any recommendation as to the suitability of the Notes for investment.

ADDITIONAL TERMS OF THE NOTES

Market Disruption Events

The Final Valuation Date, the Maturity Date, the interest payments and the payment at maturity are subject to adjustment as described in the following paragraphs.

If, on the Final Valuation Date, a Market Disruption Event occurs or is continuing in respect of the Reference Asset, the Final Valuation Date will be postponed solely for the purpose of determining the payment at maturity (excluding the final Interest Payment, if any). If such postponement occurs, the Final Value shall be determined using the Closing Value on the first following Scheduled Trading Day on which no Market Disruption Event occurs or is continuing. In no event, however, will the Final Valuation Date be postponed by more than five Scheduled Trading Days. If the Calculation Agent determines that a Market Disruption Event occurs or is continuing on such fifth day, the Calculation Agent will determine the Final Value acting in good faith and in a commercially reasonable manner. If the Final Valuation Date is postponed, the Maturity Date will be postponed by the same number of business days from, but excluding the originally scheduled Final Valuation Date, to and including the actual Final Valuation Date.

The postponements described in the preceding paragraph will be solely for the purposes of determining the payment at maturity (excluding the final Interest Payment, if any). For purposes of determining the Interest Payment, if any, payable with respect to each Accrual Period (including the final Accrual Period), if the Reference Asset is subject to a Market Disruption Event on any Scheduled Trading Day during an Accrual Period, the Closing Value on such date will equal the Closing Value observed on the immediately preceding Scheduled Trading Day on which no Market Disruption Event occurred or was continuing. Accordingly, if the Final Valuation Date is subject to a Market Disruption Event, the Closing Value attributable to such date solely for purposes of the determining the Interest Payment that is payable on the related Interest Payment Date (the Maturity Date) will be equal to Closing Value observed on the immediately preceding Scheduled Trading Day on which no Market Disruption Event occurred or was continuing. For purposes of determining the Reference Asset Return and the payment at maturity, however, the Closing Value of the Reference Asset on the Final Valuation Date will be determined as described above.

For a description of what constitutes a Market Disruption Event with respect to the Reference Asset, see “Reference Assets—Indices—Market Disruption Events for Securities with an Index of Equity Securities as a Reference Asset” in the accompanying prospectus supplement.

Adjustments to the Reference Asset and the Notes

In addition, the Reference Asset and the Notes are subject to adjustment by the Calculation Agent under certain circumstances, as described under “Reference Assets—Indices—Adjustments Relating to Securities with an Index as a Reference Asset” in the accompanying prospectus supplement.

HYPOTHETICAL AMOUNTS PAYABLE ON THE NOTES

The examples below illustrate the various payments you may receive on the Notes in a number of different hypothetical scenarios. These examples are only hypothetical and do not indicate the actual payments or return you will receive on the Notes.

Hypothetical Example of the Interest Payment Payable on a Single Interest Payment Date

The following example demonstrates the calculation of the Interest Payment payable on a single hypothetical Interest Payment Date. The numbers appearing in this example are purely hypothetical and are provided for illustrative purposes only. This example does not take into account any tax consequences from investing in the Notes and make the following key assumptions:

§ Number of Scheduled Trading Days in the Accrual Period: 21

§ Number of Scheduled Trading Days in the Accrual Period on Which the Closing Value of the Reference Asset is Greater than or Equal to the Coupon Barrier Value: 14

Step 1: Calculate the Accrual Factor for the Relevant Accrual Period.

Because the Closing Value of the Reference Asset equals or exceeds the Coupon Barrier Value on 14 out of the 21 Scheduled Trading Days in the Accrual Period, the Accrual Factor is equal to 14/21, or 66.66667%.

Step 2: Calculate the Interest Rate for the Relevant Accrual Period.

Because the Accrual Factor is 66.66667%, the Interest Rate is equal to 0.28055%, calculated as follows:

Interest Rate = Accrual Factor × Above Barrier Rate

Interest Rate = 66.6667% × 0.42083% = 0.28055%

Step 3: Calculate the Interest Payment Payable for the Relevant Accrual Period.

Because the Interest Rate is equal to 0.28055%, the Interest Payment payable on the related Interest Payment Date is $2.8055 per $1,000 principal amount Note, calculated as follows:

Interest Payment = $1,000 × Interest Rate

Interest Payment = $1,000 × 0.28055% = $2.8055

Additional Examples of Interest Rate and Interest Payment Calculations

The following examples illustrate how the per annum Interest Rate and Interest Payment amount would be calculated for a given Accrual Period under different Accrual Factor scenarios. The numbers in the following examples have been rounded of reference and make the following key assumption:

§ Number of Scheduled Trading Days in Accrual Period: 21

The number of Scheduled Trading Days in the hypothetical Accrual Period has been chosen arbitrarily for illustrative purposes only. An actual Accrual Period may be comprised of more or less than 21 Scheduled Trading Days. These examples do not take into account any tax consequences of investing in the Notes.

|

Number of Scheduled Trading |

Accrual |

Interest Rate |

Interest Payment |

|

21 |

100.00000% |

0.42083% |

$4.2083 |

|

14 |

66.66667% |

0.28055% |

$2.8055 |

|

7 |

33.33333% |

0.14027% |

$1.4027 |

|

0 |

0.00000% |

0.00000% |

$0.00 |

Example 1: The Closing Value of the Reference Asset is greater than or equal to the Coupon Barrier Value on every Scheduled Trading Day during the Accrual Period.

In this case, the Accrual Factor is 100.00% and the Interest Rate for the Accrual Period is equal to the Above Barrier Rate, the maximum Interest Rate for any Accrual Period. Accordingly, you will receive an Interest Payment of $4.2083 per $1,000 principal amount Note that you hold, on the related Interest Payment Date, calculated as follows:

$1,000 × Interest Rate

$1,000 × 0.42083% = $4.2083

Example 2: The Closing Value is greater than or equal to the Coupon Barrier Value on seven Scheduled Trading Days during the Accrual Period.

In this case, the Accrual Factor is 33.33333% and the Interest Rate for the Accrual Period is equal to 33.33333% of the Above Barrier Rate, or 0.14027%. Accordingly, you will receive an Interest Payment of $1.4027 per $1,000 principal amount Note that you hold, calculated as follows:

$1,000 × Interest Rate

$1,000 × 0.14027% = $1.4027

Example 3: The Closing Value is less than the Coupon Barrier Value on every Scheduled Trading Day during the Accrual Period.

In this case, the Accrual Factor is 0.00% and the Interest Rate for the Accrual Period equal to zero. In other words, no interest would accrue on any Scheduled Trading Day in the Accrual Period and you would not receive any Interest Payment on the related Interest Payment Date.

Hypothetical Payment at Maturity (Excluding the Final Interest Payment on the Notes)

The following examples demonstrate how the payment (if any) at maturity on the Notes (excluding the final Interest Payment) will be calculated under various circumstances. The numbers set forth in the following examples are purely hypothetical and have been rounded for eases of reference. The following examples do not take into account any tax consequences of investing in the Notes and make the following key assumptions:

§ Hypothetical Initial Value of the Reference Asset: 100.00*

§ Hypothetical Buffer Value of the Reference Asset: 80.00* (80.00% of the hypothetical Initial Value set forth above)

§ You hold the Notes to maturity, and the Notes are NOT redeemed by us prior to scheduled maturity.

* The hypothetical Initial Value of 100.00 and the hypothetical Buffer Value of 80.00 has been chosen for illustrative purposes only. The actual Initial Value and Buffer Value are as set forth on the cover of this pricing supplement.

|

Final Value |

Reference Asset Return |

Payment at Maturity** |

|

150.00 |

50.00% |

$1,000.00 |

|

140.00 |

40.00% |

$1,000.00 |

|

130.00 |

30.00% |

$1,000.00 |

|

120.00 |

20.00% |

$1,000.00 |

|

110.00 |

10.00% |

$1,000.00 |

|

105.00 |

5.00% |

$1,000.00 |

|

100.00 |

0.00% |

$1,000.00 |

|

90.00 |

-10.00% |

$1,000.00 |

|

80.00 |

-20.00% |

$1,000.00 |

|

70.00 |

-30.00% |

$900.00 |

|

60.00 |

-40.00% |

$800.00 |

|

50.00 |

-50.00% |

$700.00 |

|

40.00 |

-60.00% |

$600.00 |

|

30.00 |

-70.00% |

$500.00 |

|

20.00 |

-80.00% |

$400.00 |

|

10.00 |

-90.00% |

$300.00 |

|

0.00 |

-100.00% |

$200.00 |

|

** per $1,000 principal amount Note, excluding any Interest Payment payable at maturity | ||

The following examples illustrate how the payments at maturity set forth in the table above are calculated:

Example 1: The Final Value of the Reference Asset is 110.00.

Because the Final Value of the Reference Asset is greater than or equal to the Buffer Value, you will receive a payment at maturity of $1,000 per $1,000 principal amount Note that you hold (plus the final Interest Payment).

Example 2: The Final Value of the Reference Asset is 90.00.

Because the Final Value of the Reference Asset is greater than or equal to the Buffer Value, you will receive a payment at maturity of $1,000 per $1,000 principal amount Note that you hold (plus the final Interest Payment).

Example 3: The Final Value of the Reference Asset is 50.00.

Because the Final Value of the Reference Asset is less than the Buffer Value, you will receive a payment at maturity of $700.00 per $1,000 principal amount Note that you hold (plus the final Interest Payment, if one is payable), calculated as follows:

$1,000 + [$1,000 × Reference Asset Return + Buffer Percentage]

$1,000 + [$1,000 × (-50.00% + 20.00%)] = $700.00

An investment in the Notes involves significant risks. Investing in the Notes is not equivalent to investing directly in the Reference Asset or its components. Some of the risks that apply to an investment in the Notes are summarized below, but we urge you to read the more detailed explanation of risks relating to the Notes generally in the “Risk Factors” section of the prospectus supplement. You should not purchase the Notes unless you understand and can bear the risks of investing in the Notes.

· Your Investment in the Notes May Result in a Significant Loss—The Notes differ from ordinary debt securities in that the Issuer will not necessarily repay the full principal amount of the Notes at maturity. If the Notes are not redeemed prior to scheduled maturity, and if the Final Value of the Reference Asset is less than the Buffer Value, you will lose an amount equal to 1.00% of the principal amount of your Notes for every 1.00% that the Reference Asset Return falls below -20.00%. You may lose up to 80.00% of the principal amount of your Notes.

· Potential Return is Limited to the Interest Payments, if Any—The return on the Notes is limited to the Interest Payments, if any, that may be payable during the term of the Notes. You will not participate in any appreciation in the value of the Reference Asset. You will not receive more than the principal amount of your Notes at maturity (plus the final Interest Payment, if one is payable in respect of the final Accrual Period) even if the Reference Asset has appreciated over the term of the Notes.

· The Amount of Interest Payments that you Receive May be Limited—Interest will accrue only on Scheduled Trading Days when the Closing Value of the Reference Asset equals or exceeds the Coupon Barrier Value. If the Closing Value of the Reference Asset falls below the Coupon Barrier Value on one or more Scheduled Trading Days during an Accrual Period, then the Interest Rate for that Accrual Period will decrease in proportion to the number of Scheduled Trading Days on which the Closing Value is less than the Coupon Barrier Value. It is possible that the Closing Value of the Reference Asset will be less than the Coupon Barrier Value for the entirety of an Accrual Period, in which case the Interest Rate for that Accrual Period will be zero.

· If the Notes Are Not Redeemed Prior to Scheduled Maturity, the Payment at Maturity (Excluding the Final Interest Payment, if Any) Will be Based Solely on the Closing Value of the Reference Asset on the Final Valuation Date—The Final Value will be based solely on the Closing Value of the Reference Asset on the Final Valuation Date. Accordingly, if the value of the Reference Asset drops on the Final Valuation Date, the payment at maturity on the Notes may be significantly less than it would have been had it been linked to the value of the Reference Asset at any time prior to such drop.

· Early Redemption and Reinvestment Risk—While the original term of the Notes is as indicated on the cover page of this pricing supplement, the Notes may be redeemed prior to maturity, as described above, and the holding period over which you may receive Interest Payments could be as short as approximately one year.

The Redemption Price, together with any Interest Payments that you may have received on or prior to the Early Redemption Date, may be less than the aggregate amount of payments that you would have received had the Notes not been redeemed. There is no guarantee that you would be able to reinvest the proceeds from an investment in the Notes in a comparable investment with a similar level of risk in the event the Notes are redeemed prior to the Maturity Date. No additional payments will be due after the Early Redemption Date. The fact that the Notes may be redeemed prior to maturity may also adversely impact your ability to sell your Notes and the price at which they may be sold.

It is more likely that we will redeem the Notes at our sole discretion prior to maturity to the extent that the expected interest payable on the Notes is greater than the interest that would be payable on other instruments issued by us of comparable maturity, terms and credit rating trading in the market. We are less likely to redeem the Notes prior to maturity when the expected interest payable on the Notes is less than the interest that would be payable on other comparable instruments issued by us, which includes when the level of the Reference Asset is less than the Coupon Barrier Value. Therefore, the Notes are more likely to remain outstanding when the expected interest payable on the Notes is less than what would be payable on other comparable instruments and when your risk of not receiving an Interest Payment is relatively higher.

· Credit of Issuer—The Notes are unsecured and unsubordinated debt obligations of the Issuer, Barclays Bank PLC, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Notes, including any repayment of principal, is subject to the ability of Barclays Bank PLC to satisfy its obligations as they come due and is not guaranteed by any third party. As a result, the actual and perceived creditworthiness of Barclays Bank PLC may affect the market value of the Notes, and in the event Barclays Bank PLC were to default on its obligations, you may not receive any amounts owed to you under the terms of the Notes.

· You May Lose Some or All of Your Investment If Any U.K. Bail-in Power Is Exercised by the Relevant U.K. Resolution Authority— Notwithstanding any other agreements, arrangements or understandings between Barclays Bank PLC and any holder or beneficial owner of the Notes, by acquiring the Notes, each holder and beneficial owner of the Notes acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority as set forth under “Consent to U.K. Bail-in Power” in this pricing supplement. Accordingly, any U.K. Bail-in Power may be exercised in such a manner as to result in you and other holders and beneficial owners of the Notes losing all or a part of the value of your investment in the Notes or receiving a different security from the Notes, which may be worth significantly less than the Notes and which may have significantly fewer protections than those typically afforded to debt securities. Moreover, the relevant U.K. resolution authority may exercise the U.K. Bail-in Power without providing any advance notice to, or requiring the consent of, the holders and the beneficial owners of the Notes. The exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes will not be a default or an Event of Default (as each term is defined in the senior debt securities indenture) and the trustee will not be liable for any action that the trustee takes, or abstains from taking, in either case, in accordance with the exercise of the U.K. Bail-in Power by the relevant U.K. resolution authority with respect to the Notes. See “Consent to U.K. Bail-in Power” in this pricing supplement as well as “U.K. Bail-in Power,” “Risk Factors—Risks Relating to the Securities Generally—Regulatory action in the event a bank or investment firm in the Group is failing or likely to fail could materially adversely affect the value of the securities” and “Risk Factors—Risks Relating to the Securities Generally—Under the terms of the securities, you have agreed to be bound by the exercise of any U.K. Bail-in Power by the relevant U.K. resolution authority” in the accompanying prospectus supplement.

· Contingent Repayment of Any Principal Amount Applies Only at Maturity or upon Any Redemption—You should be willing to hold your Notes to maturity or any redemption. Although the Notes provide for the contingent repayment of the principal amount of your Notes at maturity, provided that the Final Value of the Reference Asset is greater than or equal to the Buffer Value, or upon any redemption, if you sell your Notes prior to such time in the secondary market, if any, you may have to sell your Notes at a price that is less than the principal amount even if at that time the value of the Reference Asset has increased from the Initial Value. See “Many Economic and Market Factors Will Impact the Value of the Notes” below.

· Owning the Notes is Not the Same as Owning A Reference Asset or Any Securities to which A Reference Asset Provides Exposure—The return on the Notes may not reflect the return you would realize if you actually owned a Reference Asset or any securities to which a Reference Asset provides exposure. As a holder of the Notes, you will not have voting rights or rights to receive dividends or other distributions or any other rights that holders of a Reference Asset or any securities to which a Reference Asset provides exposure may have.

· The Reference Asset Reflects the Price Return of the Securities Composing the Reference Asset, Not the Total Return — The return on the Notes is based on the performance of the Reference Asset, which reflect changes in the market prices of the securities composing the Reference Asset. The Reference Asset is not a “total return” index that, in addition to reflecting those price returns, would also reflect dividends paid on the securities composing the Reference Asset. Accordingly, the return on the Notes will not include such a total return feature.

· Adjustments to the Reference Asset Could Adversely Affect the Value of the Notes—The sponsor of the Reference Asset may add, delete, substitute or adjust the securities composing the Reference Asset or make other methodological changes to the Reference Asset that could affect its value. The Calculation Agent will calculate the value to be used as the Closing Value of the Reference Asset in the event of certain material changes in or modifications to the Reference Asset. In addition, the sponsor of the Reference Asset may also discontinue or suspend calculation or publication of the Reference Asset at any time. Under these circumstances, the Calculation Agent may select a successor index that the Calculation Agent determines to be comparable to the Reference Asset or, if no successor index is available, the Calculation Agent will determine the value to be used as the Closing Value of the Reference Asset. Any of these actions could adversely affect the value of the Reference Asset and, consequently, the value of the Notes. See “Reference Assets—Indices—Adjustments Relating to Securities with an Index as a Reference Asset” in the accompanying prospectus supplement.

· Historical Performance of the Reference Asset Should Not Be Taken as Any Indication of the Future Performance of the Reference Asset Over the Term of the Notes—The value of the Reference Asset has fluctuated in the past and may, in the future, experience significant fluctuations. The historical performance of the Reference Asset is not an indication of the future performance of the Reference Asset over the term of the Notes. Therefore, the performance of the Reference Asset over the term of the Notes may bear no relation or resemblance to the historical performance of the Reference Asset.

· The Estimated Value of Your Notes is Lower Than the Initial Issue Price of Your Notes—The estimated value of your Notes on the Initial Valuation Date is lower than the initial issue price of your Notes. The difference between the initial issue price of your Notes and the estimated value of the Notes is a result of certain factors, such as any sales commissions to be paid to Barclays Capital Inc. or another affiliate of ours, any selling concessions, discounts, commissions or fees (including any structuring or other distribution related fees)to be allowed or paid to non-affiliated intermediaries, the estimated profit that we or any of our affiliates expect to earn in connection with structuring the Notes, the estimated cost which we may incur in hedging our obligations under the Notes, and estimated development and other costs which we may incur in connection with the Notes.

· The Estimated Value of Your Notes Might be Lower if Such Estimated Value Were Based on the Levels at Which Our Debt Securities Trade in the Secondary Market—The estimated value of your Notes on the Initial Valuation Date is based on a number of variables, including our internal funding rates. Our internal funding rates may vary from the levels at which our benchmark debt securities trade in the secondary market. As a result of this difference, the estimated value referenced above might be lower if such estimated value were based on the levels at which our benchmark debt securities trade in the secondary market.

· The Estimated Value of the Notes is Based on Our Internal Pricing Models, Which May Prove to be Inaccurate and May be Different from the Pricing Models of Other Financial Institutions—The estimated value of your Notes on the Initial Valuation Date is based on our internal pricing models, which take into account a number of variables and are based on a number of subjective assumptions, which may or may not materialize. These variables and assumptions are not evaluated or verified on an independent basis. Further, our pricing models may be different from other financial institutions’ pricing models and the methodologies used by us to estimate the value of the Notes may not be consistent with those of other financial institutions which may be purchasers or sellers of Notes in the secondary market. As a result, the secondary market price of your Notes may be materially different from the estimated value of the Notes determined by reference to our internal pricing models.

· The Estimated Value of Your Notes Is Not a Prediction of the Prices at Which You May Sell Your Notes in the Secondary Market, if any, and Such Secondary Market Prices, If Any, Will Likely be Lower Than the Initial Issue Price of Your Notes and May be Lower Than the Estimated Value of Your Notes—The estimated value of the Notes will not be a prediction of the prices at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions (if they are willing to purchase, which they are not obligated to do). The price at which you may be able to sell your Notes in the secondary market at any time will be influenced by many factors that cannot be predicted, such as market conditions, and any bid and ask spread for similar sized trades, and may be substantially less than our estimated value of the Notes. Further, as secondary market prices of your Notes take into account the levels at which our debt securities trade in the secondary market, and do not take into account our various costs related to the Notes such as fees, commissions, discounts, and the costs of hedging our obligations under the Notes, secondary market prices of your Notes will likely be lower than the initial issue price of your Notes. As a result, the price at which Barclays Capital Inc., other affiliates of ours or third parties may be willing to purchase the Notes from you in secondary market transactions, if any, will likely be lower than the price you paid for your Notes, and any sale prior to the Maturity Date could result in a substantial loss to you.

· The Temporary Price at Which We May Initially Buy The Notes in the Secondary Market And the Value We May Initially Use for Customer Account Statements, If We Provide Any Customer Account Statements At All, May Not Be Indicative of Future Prices of Your Notes—Assuming that all relevant factors remain constant after the Initial Valuation Date, the price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market (if Barclays Capital Inc. makes a market in the Notes, which it is not obligated to do) and the value that we may initially use for customer account statements, if we provide any customer account statements at all, may exceed our estimated value of the Notes on the Initial Valuation Date, as well as the secondary market value of the Notes, for a temporary period after the initial Issue Date of the Notes. The price at which Barclays Capital Inc. may initially buy or sell the Notes in the secondary market and the value that we may initially use for customer account statements may not be indicative of future prices of your Notes.

· We and Our Affiliates May Engage in Various Activities or Make Determinations That Could Materially Affect the Notes in Various Ways and Create Conflicts of Interest—We and our affiliates play a variety of roles in connection with the issuance of the Notes, as described below. In performing these roles, our and our affiliates’ economic interests are potentially adverse to your interests as an investor in the Notes.

In connection with our normal business activities and in connection with hedging our obligations under the Notes, we and our affiliates make markets in and trade various financial instruments or products for our accounts and for the account of our clients and otherwise provide investment banking and other financial services with respect to these financial instruments and products. These financial instruments and products may include securities, derivative instruments or assets that may relate to the Reference Asset or its components. In any such market making, trading and hedging activity, and other financial services, we or our affiliates may take positions or take actions that are inconsistent with, or adverse to, the investment objectives of the holders of the Notes. We and our affiliates have no obligation to take the needs of any buyer, seller or holder of the Notes into account in conducting these activities. Such market making, trading and hedging activity, investment banking and other financial services may negatively impact the value of the Notes.

In addition, the role played by Barclays Capital Inc., as the agent for the Notes, could present significant conflicts of interest with the role of Barclays Bank PLC, as issuer of the Notes. For example, Barclays Capital Inc. or its representatives may derive compensation or financial benefit from the distribution of the Notes and such compensation or financial benefit may serve as incentive to sell the Notes instead of other investments. Furthermore, we and our affiliates establish the offering price of the Notes for initial sale to the public, and the offering price is not based upon any independent verification or valuation.

In addition to the activities described above, we will also act as the Calculation Agent for the Notes. As Calculation Agent, we will determine any values of the Reference Asset and make any other determinations necessary to calculate any payments on the Notes. In making these determinations, the Calculation Agent may be required to make discretionary judgements relating to the Reference Asset, including determining whether a market disruption event has occurred or whether certain adjustments to the Reference Asset or other terms of the Notes are necessary, as further described in the accompanying prospectus supplement. In making these discretionary judgments, our economic interests are potentially adverse to your interests as an investor in the Notes, and any of these determinations may adversely affect any payments on the Notes.

· Lack of Liquidity—The Notes will not be listed on any securities exchange. Barclays Capital Inc. and other affiliates of Barclays Bank PLC intend to make a secondary market for the Notes but are not required to do so, and may discontinue any such secondary market making at any time, without notice. Barclays Capital Inc. may at any time hold unsold inventory, which may inhibit the development of a secondary market for the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily. Because other dealers are not likely to make a secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which Barclays Capital Inc. and other affiliates of Barclays Bank PLC are willing to buy the Notes. The Notes are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Notes to maturity.

· Tax Treatment—Significant aspects of the tax treatment of the Notes are uncertain. You should consult your tax advisor about your tax situation. See “Tax Considerations” below.

· Many Economic and Market Factors Will Impact the Value of the Notes—The value of the Notes will be affected by a number of economic and market factors that interact in complex and unpredictable ways and that may either offset or magnify each other, including:

o the market price of, dividend rate on and expected volatility of the Reference Asset and the components of the Reference Asset;

o the time to maturity of the Notes;

o interest and yield rates in the market generally;

o a variety of economic, financial, political, regulatory or judicial events;

o supply and demand for the Notes; and

o our creditworthiness, including actual or anticipated downgrades in our credit ratings.

INFORMATION REGARDING THE REFERENCE ASSET

S&P 500® Index

The Reference Asset consists of stocks of 500 companies selected to provide a performance benchmark for the U.S. equity markets. For more information about the Reference Asset, see “Indices—The S&P U.S. Indices” in the accompanying underlying supplement.

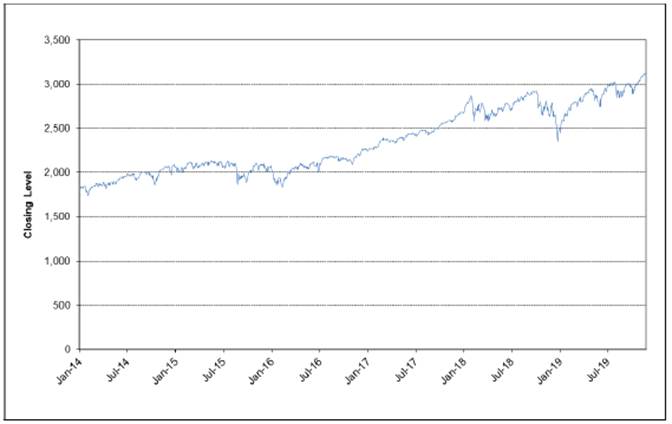

Historical Performance of the Reference Asset

The graph below sets forth the historical performance of the Reference Asset based on the daily Closing Values from January 2, 2009 through November 25, 2019. We obtained the Closing Values shown in the graph below from Bloomberg Professional® service (“Bloomberg”). We have not independently verified the accuracy or completeness of the information obtained from Bloomberg.

Historical Performance of the S&P 500® Index

PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS

TAX CONSIDERATIONS

You should review carefully the sections entitled “Material U.S. Federal Income Tax Consequences—Tax Consequences to U.S. Holders—Notes Treated as Prepaid Forward or Derivative Contracts with Associated Contingent Coupons” and, if you are a non-U.S. holder, “—Tax Consequences to Non-U.S. Holders,” in the accompanying prospectus supplement.

In determining our reporting responsibilities, if any, we intend to treat (i) the Notes for U.S. federal income tax purposes as prepaid forward contracts with associated contingent coupons and (ii) any Contingent Coupon payments as ordinary income, as described in the section entitled “Material U.S. Federal Income Tax Consequences—Tax Consequences to U.S. Holders—Notes Treated as Prepaid Forward or Derivative Contracts with Associated Contingent Coupons” in the accompanying prospectus supplement. Our special tax counsel, Davis Polk & Wardwell LLP, has advised that it believes this treatment to be reasonable, but that there are other reasonable treatments that the Internal Revenue Service (the “IRS”) or a court may adopt.

Sale, exchange or redemption of a Note. Assuming the treatment described above is respected, upon a sale or exchange of the Notes (including upon early redemption or redemption at maturity), you should recognize capital gain or loss equal to the difference between the amount realized on the sale or exchange and your tax basis in the Notes, which should equal the amount you paid to acquire the Notes (assuming Contingent Coupon payments are properly treated as ordinary income, consistent with the position referred to above). This gain or loss should be long-term capital gain or loss if you hold the Notes for more than one year, whether or not you are an initial purchaser of the Notes at the issue price. The deductibility of capital losses is subject to limitations. If you sell your Notes between the time you accrue any portion of a Contingent Coupon payment and the time it is paid, it is likely that you will be treated as receiving ordinary income equal to the accrued portion of the contingent coupon payment. Although uncertain, it is possible that proceeds received from the sale or exchange of your Notes that can be attributed to expected but not yet accrued portions of a Contingent Coupon payment could be treated as ordinary income. You should consult your tax advisor regarding this issue.

As noted above, there are other reasonable treatments that the IRS or a court may adopt, in which case the timing and character of any income or loss on the Notes could be materially affected. In addition, in 2007 the U.S. Treasury Department and the IRS released a notice requesting comments on the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. The notice focuses in particular on whether to require investors in these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments and the relevance of factors such as the nature of the underlying property to which the instruments are linked. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially affect the tax consequences of an investment in the Notes, possibly with retroactive effect. You should consult your tax advisor regarding the U.S. federal income tax consequences of an investment in the Notes, including possible alternative treatments and the issues presented by this notice.

Non-U.S. holders. Insofar as we have responsibility as a withholding agent, we do not currently intend to treat Contingent Coupon payments to non-U.S. holders (as defined in the accompanying prospectus supplement) as subject to U.S. withholding tax. However, non-U.S. holders should in any event expect to be required to provide appropriate Forms W-8 or other documentation in order to establish an exemption from backup withholding, as described under the heading “—Information Reporting and Backup Withholding” in the accompanying prospectus supplement. If any withholding is required, we will not be required to pay any additional amounts with respect to amounts withheld.

Treasury regulations under Section 871(m) generally impose a withholding tax on certain “dividend equivalents” under certain “equity linked instruments.” A recent IRS notice excludes from the scope of Section 871(m) instruments issued prior to January 1, 2021 that do not have a “delta of one” with respect to underlying securities that could pay U.S.-source dividends for U.S. federal income tax purposes (each an “Underlying Security”). Based on our determination that the Notes do not have a “delta of one” within the meaning of the regulations, our special tax counsel is of the opinion that these regulations should not apply to the Notes with regard to non-U.S. holders. Our determination is not binding on the IRS, and the IRS may disagree with this determination. Section 871(m) is complex and its application may depend on your particular circumstances, including whether you enter into other transactions with respect to an Underlying Security. You should consult your tax advisor regarding the potential application of Section 871(m) to the Notes.

SUPPLEMENTAL PLAN OF DISTRIBUTION

We have agreed to sell to Barclays Capital Inc. (the “Agent”), and the Agent has agreed to purchase from us, the principal amount of the Notes, and at the price, specified on the cover of this pricing supplement. The Agent commits to take and pay for all of the Notes, if any are taken.

VALIDITY OF THE NOTES

In the opinion of Davis Polk & Wardwell LLP, as special United States products counsel to Barclays Bank PLC, when the Notes offered by this pricing supplement have been executed and issued by Barclays Bank PLC and authenticated by the trustee pursuant to the indenture, and delivered against payment as contemplated herein, such Notes will be valid and binding obligations of Barclays Bank PLC, enforceable in accordance with their terms, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith) and possible judicial or regulatory actions giving effect to governmental actions or foreign laws affecting creditors’ rights, provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date hereof and is limited to the laws of the State of New York. Insofar as this opinion involves matters governed by English law, Davis Polk & Wardwell LLP has relied, with Barclays Bank PLC’s permission, on the opinion of Davis Polk & Wardwell London LLP, dated as of June 14, 2019, filed as an exhibit to a report on Form 6-K by Barclays Bank PLC on June 14, 2019, and this opinion is subject to the same assumptions, qualifications and limitations as set forth in such opinion of Davis Polk & Wardwell London LLP. In addition, this opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the indenture and its authentication of the Notes and the validity, binding nature and enforceability of the indenture with respect to the trustee, all as stated in the letter of Davis Polk & Wardwell LLP, dated June 14, 2019, which has been filed as an exhibit to the report on Form 6-K referred to above.