|

Barclays Bank PLC Market Linked Securities |

Filed Pursuant to Rule 433 Registration Statement No. 333-265158

|

|

Market Linked Securities—Auto-Callable with Contingent Coupon with Memory Feature and Contingent Downside Principal at Risk Securities Linked to the Class C Common Stock of Dell Technologies Inc. due August 27, 2027 Term Sheet dated August 29, 2024 to Preliminary Pricing Supplement dated August 29, 2024 (the “PPS”) |

Summary of Terms

| Issuer | Barclays Bank PLC |

| Market Measure | Class C common stock of Dell Technologies Inc. (Bloomberg ticker symbol “DELL UN<Equity>”) (the “Underlying Stock”) |

| Pricing Date | August 30, 2024 |

| Issue Date | September 5, 2024 |

| Final Calculation Day | August 24, 2027 |

| Stated Maturity Date | August 27, 2027 |

| Principal Amount | $1,000 per security |

| Contingent Coupon Payments | On each contingent coupon payment date, you will receive a contingent coupon payment at a per annum rate equal to the contingent coupon rate if the stock closing price of the Underlying Stock on the related calculation day is greater than or equal to the coupon threshold price, as well as the amounts of all contingent coupon payments, if any, that would have been paid on a previous contingent coupon payment date had the stock closing price of the Underlying Stock on the related calculation day been greater than or equal to the coupon threshold price and that have not been previously paid (without interest on amounts previously unpaid) (“unpaid contingent coupon payments”). Each “contingent coupon payment,” if any, will be calculated per security as follows: ($1,000 × contingent coupon rate)/4. |

| Contingent Coupon Payment Dates | Quarterly, on the third business day following each calculation day; provided that the contingent coupon payment date with respect to the final calculation day will be the stated maturity date |

| Contingent Coupon Rate | At least 16.55% per annum, to be determined on the pricing date |

| Automatic Call | If the stock closing price of the Underlying Stock on any of the calculation days from November 2024 to May 2027, inclusive, is greater than or equal to the starting price, the securities will be automatically called, and on the related call settlement date you will be entitled to receive a cash payment per security in U.S. dollars equal to the principal amount plus the contingent coupon payment and any unpaid contingent coupon payments otherwise due. The securities will not be subject to automatic call until the first calculation day, which is approximately three months after the issue date. |

| Calculation Days | Quarterly, on the 24th day of each February, May, August and November, commencing November 2024 and ending August 2027, provided that the August 2027 calculation day will be the final calculation day |

| Call Settlement Date | The contingent coupon payment date immediately following the applicable calculation day |

| Maturity Payment Amount (per security) |

The maturity payment amount will equal: · if the ending price is greater than or equal to the downside threshold price: $1,000; or · if the ending price is less than the downside threshold price: $1,000 × performance factor |

| Performance Factor | The ending price divided by the starting price |

Summary of Terms (continued)

| Starting Price | The stock closing price of the Underlying Stock on the pricing date |

| Ending Price | The stock closing price of the Underlying Stock on the final calculation day |

| Coupon Threshold Price | 70% of the starting price |

| Downside Threshold Price | 60% of the starting price |

| Calculation Agent | Barclays Bank PLC |

| Denominations | $1,000 and any integral multiple of $1,000 |

| CUSIP/ISIN | 06745UVC1 / US06745UVC16 |

| Agent Discount | Up to 2.325%; dealers, including those using the trade name Wells Fargo Advisors (WFA), may receive a selling concession of 1.75% and WFA may receive a distribution expense fee of 0.075%. Selected dealers may receive a fee of up to 0.35% for marketing and other services. |

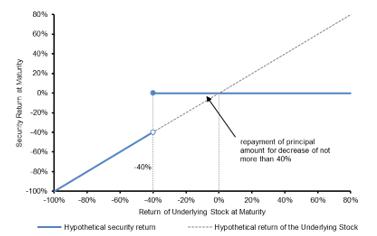

Hypothetical Payout Profile (maturity payment amount)

If the securities are not automatically called prior to stated maturity and the ending price is less than the downside threshold price, you will lose more than 40%, and possibly all, of the principal amount of your securities at stated maturity.

Any return on the securities will be limited to the sum of your contingent coupon payments, if any. You will not participate in any appreciation of the Underlying Stock.

Any payment on the securities, including any repayment of principal, is subject to the creditworthiness of Barclays Bank PLC and is not guaranteed by any third party.

Notwithstanding and to the exclusion of any other term of the securities or any other agreements, arrangements or understandings between Barclays Bank PLC and any holder or beneficial owner of the securities (or the trustee on behalf of the holders of the securities), by acquiring the securities, each holder and beneficial owner of the securities acknowledges, accepts, agrees to be bound by, and consents to the exercise of, any U.K. Bail-in Power by the relevant U.K. resolution authority. See “Consent to U.K. Bail-in Power” in the PPS.

The issuer’s estimated value of the securities on the pricing date, based on its internal pricing models, is expected to be between $934.70 and $964.70 per security. The estimated value is expected to be less than the original offering price of the securities. See “Additional Information Regarding Our Estimated Value of the Securities” in the PPS.

Investors should carefully review the accompanying PPS, product supplement, prospectus supplement and prospectus before making a decision to invest in the securities.

http://www.sec.gov/Archives/edgar/data/312070/000095010324012784/dp217237

_424b2-6336wfpps.htm

| The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See “Selected Risk Considerations” in this term sheet and the accompanying PPS and “Risk Factors” in the accompanying product supplement and prospectus supplement. |

| This term sheet does not provide all of the information that an investor should consider prior to making an investment decision. |

| The securities constitute our unsecured and unsubordinated obligations. The securities are not deposit liabilities of Barclays Bank PLC and are not covered by the U.K. Financial Services Compensation Scheme or insured by the U.S. Federal Deposit Insurance Corporation or any other governmental agency or deposit insurance agency of the United States, the United Kingdom or any other jurisdiction. |

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Underlying Stock. You should carefully review the risk disclosures set forth under the “Risk Factors” sections of the prospectus supplement and product supplement and the “Selected Risk Considerations” section in the accompanying PPS. The risks set forth below are discussed in detail in the “Selected Risk Considerations” section in the accompanying PPS.

| · | If The Securities Are Not Automatically Called Prior to Stated Maturity, You May Lose Some Or All Of The Principal Amount Of Your Securities At Stated Maturity. |

| · | The Securities Do Not Provide For Fixed Payments Of Interest And You May Receive No Contingent Coupon Payments On One Or More Contingent Coupon Payment Dates, Or Even Throughout The Entire Term Of The Securities. |

| · | Your Potential Return On The Securities Will Be Different Depending On The Sequence Of Calculation Days On Which The Stock Closing Price Of The Underlying Stock Is Greater Than Or Equal To The Coupon Threshold Price (If Any) |

| · | You May Be Fully Exposed To The Decline In The Underlying Stock From The Starting Price, But Will Not Participate In Any Positive Performance Of The Underlying Stock. |

| · | Higher Contingent Coupon Rates Are Associated With Greater Risk. |

| · | You Will Be Subject To Reinvestment Risk. |

| · | Any Payment On The Securities Will Be Determined Based On The Stock Closing Prices Of The Underlying Stock On The Dates Specified. |

| · | Owning The Securities Is Not The Same As Owning The Underlying Stock. |

| · | No Assurance That The Investment View Implicit In The Securities Will Be Successful. |

| · | The U.S. Federal Income Tax Consequences Of An Investment In The Securities Are Uncertain. |

| · | The Securities Are Subject To The Credit Risk Of Barclays Bank PLC. |

| · | You May Lose Some Or All Of Your Investment If Any U.K. Bail-In Power Is Exercised By The Relevant U.K. Resolution Authority. |

| · | There Are Risks Associated With Single Equities. |

| · | We Cannot Control Actions By The Underlying Stock Issuer. |

| · | We And Our Affiliates Have No Affiliation With The Underlying Stock Issuer And Have Not Independently Verified Its Public Disclosure Of Information. |

| · | You Have Limited Anti-dilution Protection. |

| · | The Securities May Become Linked To The Common Stock Of A Company Other Than The Original Underlying Stock Issuer. |

| · | The Historical Performance Of The Underlying Stock Is Not An Indication Of Its Future Performance. |

| · | Potentially Inconsistent Research, Opinions Or Recommendations By Barclays Capital Inc., Wells Fargo Securities, LLC Or Their Respective Affiliates. |

| · | We, Our Affiliates And Any Other Agent And/Or Participating Dealer May Engage In Various Activities Or Make Determinations That Could Materially Affect Your Securities In Various Ways And Create Conflicts Of Interest. |

| · | The Securities Will Not Be Listed On Any Securities Exchange And We Do Not Expect A Trading Market For The Securities To Develop. |

| · | The Value Of The Securities Prior To Maturity Will Be Affected By Numerous Factors, Some Of Which Are Related In Complex Ways. |

| · | The Estimated Value Of Your Securities Is Expected To Be Lower Than The Original Offering Price Of Your Securities. |

| · | The Estimated Value Of Your Securities Might Be Lower If Such Estimated Value Were Based On The Levels At Which Our Debt Securities Trade In The Secondary Market. |

| · | The Estimated Value Of The Securities Is Based On Our Internal Pricing Models, Which May Prove To Be Inaccurate And May Be Different From The Pricing Models Of Other Financial Institutions. |

| · | The Estimated Value Of Your Securities Is Not A Prediction Of The Prices At Which You May Sell Your Securities In The Secondary Market, If Any, And Such Secondary Market Prices, If Any, Will Likely Be Lower Than The Original Offering Price Of Your Securities And May Be Lower Than The Estimated Value Of Your Securities. |

| · | The Temporary Price At Which We May Initially Buy The Securities In The Secondary Market And The Value We May Initially Use For Customer Account Statements, If We Provide Any Customer Account Statements At All, May Not Be Indicative Of Future Prices Of Your Securities. |

| Barclays Bank PLC has filed a registration statement (including a prospectus) with the SEC for the offering to which this term sheet relates. Before you invest, you should read the prospectus dated May 23, 2022, the prospectus supplement dated June 27, 2022, the product supplement no. WF-1 dated October 17, 2022, the PPS and other documents Barclays Bank PLC has filed with the SEC for more complete information about Barclays Bank PLC and this offering. You may get these documents and other documents Barclays Bank PLC has filed for free by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Barclays Bank PLC or any agent or dealer participating in this offering will arrange to send you each of these documents if you request them by calling your Barclays Bank PLC sales representative, such dealer or toll-free 1-888-227-2275 (Extension 2-3430). A copy of each of these documents may be obtained from Barclays Capital Inc., 745 Seventh Avenue—Attn: US InvSol Support, New York, NY 10019. |

As used in this term sheet, “we,” “us” and “our” refer to Barclays Bank PLC. Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.