Report to Shareholders for the third quarter ended September 30, 2019

All financial figures are unaudited and presented in Canadian dollars unless noted otherwise. Production volumes are presented on a working-interest basis, before royalties, except for Libya, which is on an entitlement basis. Certain financial measures in this document are not prescribed by Canadian generally accepted accounting principles (GAAP). For a description of these non-GAAP financial measures, see the Non-GAAP Financial Measures Advisory section of Suncor Energy Inc.'s (Suncor or the company) Management's Discussion and Analysis dated October 30, 2019 (MD&A). See also the Advisories section of the MD&A. References to Oil Sands operations exclude Suncor's interests in Fort Hills and Syncrude.

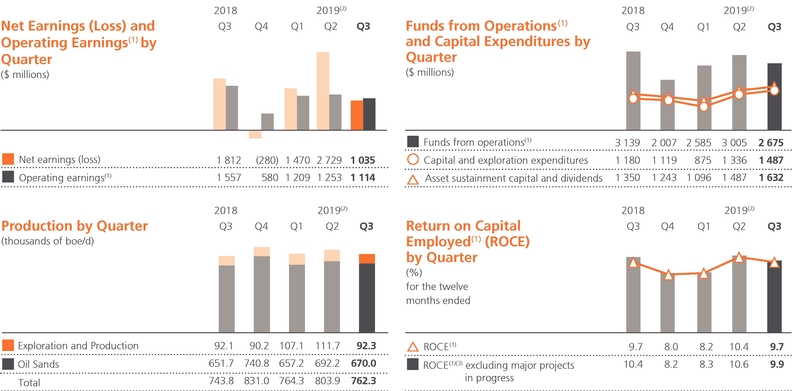

"Suncor generated $2.7 billion in funds from operations and $1.1 billion of operating earnings during the third quarter, reflecting the ability of our integrated business to deliver strong results across a wide range of market conditions," said Mark Little, president and chief executive officer. "We continue to demonstrate Suncor's ongoing commitment to shareholders by returning $1.4 billion in value through dividends and increased share repurchases."

- •

- Funds

from operations(1) were $2.675 billion ($1.72 per common share) in the third quarter of 2019, compared to $3.139 billion ($1.94 per common

share) in the prior year quarter, marking the ninth consecutive quarter above $2 billion. Cash flow provided by operating activities, which includes changes in non-cash working capital, was

$3.136 billion ($2.02 per common share) in the third quarter of 2019, compared to $4.370 billion ($2.70 per common share) in the prior year quarter.

- •

- Operating

earnings(1) were $1.114 billion ($0.72 per common share) in the third quarter of 2019, compared to operating earnings of $1.557 billion

($0.96 per common share) in the prior year quarter. Net earnings were $1.035 billion ($0.67 per common share) in the third quarter of 2019, compared to $1.812 billion ($1.12 per common

share) in the prior year quarter.

- •

- Total

Oil Sands production during the third quarter of 2019 increased to 670,000 barrels per day (bbls/d), from 651,700 bbls/d in the prior year quarter

despite being limited by mandatory production curtailments. The increase was primarily due to higher production at Syncrude, which increased to 162,300 bbls/d, from 106,200 bbls/d in the

prior year quarter, and Fort Hills, which increased to 85,500 bbls/d, from 69,400 bbls/d in the prior year quarter.

- •

- Reliable

operations in Refining and Marketing drove refinery utilization of 100% and crude throughput of 463,700 bbls/d. Total sales of refined petroleum products

increased to 572,000 bbls/d reflecting record retail volumes.

- •

- Suncor

announced a significant $1.4 billion investment in low-carbon power generation to replace coke-fired boilers with a new cogeneration facility at its Oil Sands

Base Plant which is expected to provide reliable steam generation while contributing to our environmental and incremental free funds flow(1) goals.

- •

- The company paid $650 million in dividends, repurchased 19.2 million of its common shares, representing 1.2% of the total outstanding common shares, for $756 million, and repaid $572 million of debt in the third quarter of 2019.

|

- (1)

- Funds

from operations, operating earnings, free funds flow and ROCE are non-GAAP financial measures. See page 5 for a reconciliation of net earnings to operating earnings. See

the Non-GAAP Financial Measures Advisory section of the MD&A.

- (2)

- Includes

the impact of the Government of Alberta's mandatory production curtailments.

- (3)

- ROCE excluding major projects in progress would have been 8.7% in the second quarter of 2019 and 8.0% in the third quarter of 2019 excluding the $1.116 billion deferred tax recovery for the Alberta corporate income tax rate change, which the company recorded in the second quarter of 2019.

Financial Results

Operating Earnings

Suncor's third quarter 2019 operating earnings were $1.114 billion ($0.72 per common share), compared to $1.557 billion ($0.96 per common share) in the prior year quarter. Highlights of the third quarter included higher overall crude oil production and refinery crude throughput as compared to the prior year quarter. Higher production at Syncrude and the ramp up of Fort Hills and Hebron production over the last year increased crude output during the third quarter of 2019, which was partially offset by planned maintenance, the impact of the Alberta government's mandatory production curtailments and an unplanned outage at Hibernia, which was resolved by the end of the third quarter. In addition, operating earnings were positively impacted by the realization of intersegment profit on inventory transfers, compared to the elimination of intersegment profit in the prior year quarter.

The decrease in operating earnings was primarily related to a weaker business environment, which drove lower overall crude price realizations and lower refining margins, as well as an increase in operating and transportation expenses.

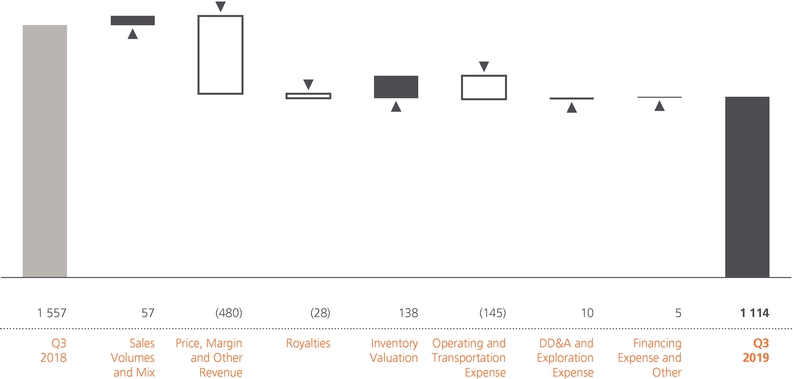

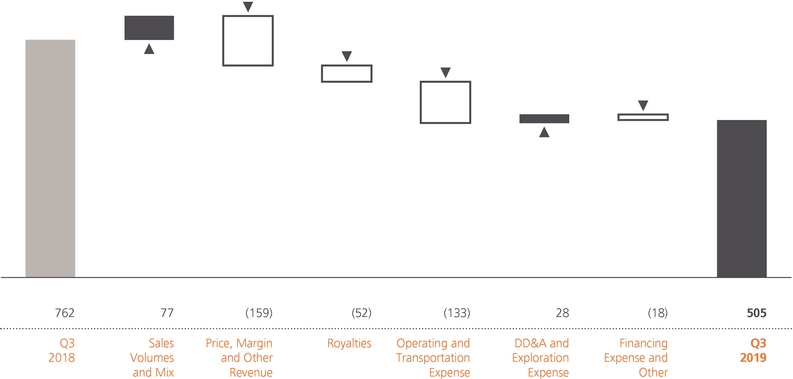

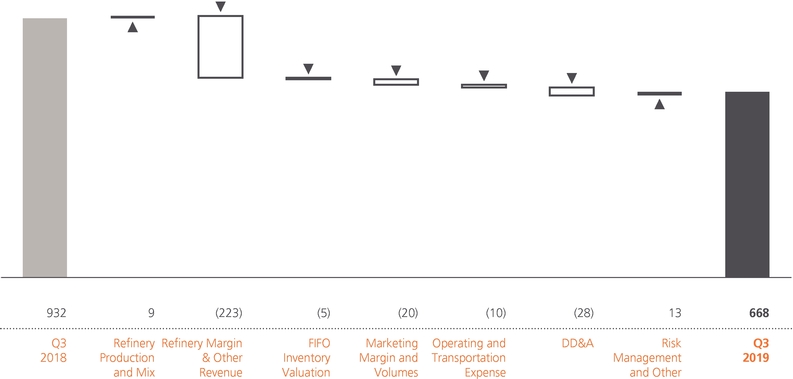

Bridge Analysis of Operating Earnings ($ millions)(1)

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of the MD&A.

Net Earnings

Net earnings were $1.035 billion ($0.67 per common share) in the third quarter of 2019, compared to net earnings of $1.812 billion ($1.12 per common share) in the prior year quarter. In addition to the factors impacting operating earnings discussed above, net earnings for the third quarter of 2019 included a $127 million unrealized after-tax foreign exchange loss on the revaluation of U.S. dollar denominated debt and an after-tax gain of $48 million in the Exploration and Production (E&P) segment related to the sale of certain non-core assets. Net earnings in the prior year quarter included an unrealized after-tax foreign exchange gain of $195 million on the revaluation of U.S. dollar denominated debt and an after-tax gain of $60 million on the sale of the company's interest in the Joslyn Oil Sands mining project.

Funds from Operations and Cash Flow Provided By Operating Activities

Funds from operations were $2.675 billion ($1.72 per common share) in the third quarter of 2019, compared to $3.139 billion ($1.94 per common share) in the third quarter of 2018, and were influenced by the same factors impacting operating earnings noted above.

Cash flow provided by operating activities was $3.136 billion ($2.02 per common share) for the third quarter of 2019, compared to $4.370 billion ($2.70 per common share) for the third quarter of 2018. In addition to the items noted in operating earnings above, cash flow provided by operating activities was further impacted by a lower source of cash associated with the company's working capital balances in the third quarter of 2019 as compared to the prior year quarter. The source of cash was due to a decrease in accounts receivable balances related to the decline in crude benchmark prices.

| 2 2019 THIRD QUARTER Suncor Energy Inc. | | |

Operating Results

Suncor's total upstream production was 762,300 barrels of oil equivalent per day (boe/d) during the third quarter of 2019, compared to 743,800 boe/d in the prior year quarter. The increase was primarily due to higher production at Syncrude and the ramp up of Fort Hills and Hebron production throughout 2018, partially offset by the impact of planned maintenance and mandatory production curtailments in the province of Alberta, which began January 1, 2019 and an unplanned outage at Hibernia, which was resolved by the end of the third quarter.

During the third quarter of 2019, the company was able to leverage its unique footprint and asset flexibility to maximize the value of its allotted barrels under the mandatory production curtailment program, focusing on higher value synthetic crude oil (SCO) production through the transfer of curtailment allotment credits among the company's assets. Given our planned maintenance, there was limited availability and opportunity to purchase production quotas from other operators in the quarter.

Oil Sands operations production was 422,200 bbls/d in the third quarter of 2019, compared to 476,100 bbls/d in the prior year quarter. The decrease in production was primarily due to planned upgrader maintenance and mandatory production curtailments in the province of Alberta, which resulted in a decrease in upgrader utilization to 91% in the third quarter of 2019, compared to 95% in the prior year quarter. Production of non-upgraded bitumen from the company's In Situ assets was 105,200 bbls/d in the third quarter of 2019, compared to 146,000 bbls/d in the prior year quarter, primarily impacted by mandatory production curtailments as the company maximized the production to the upgrader to produce higher value SCO barrels in the third quarter of 2019.

Oil Sands operations cash operating costs(1) per barrel increased to $26.60 in the third quarter of 2019, from $22.00 in the prior year quarter, primarily due to the impact of mandatory production curtailments and conscious changes in our production mix to maximize value, planned maintenance and an increase in contractor mining costs.

Suncor's share of production from Fort Hills averaged 85,500 bbls/d in the third quarter of 2019, compared to 69,400 bbls/d in the prior year quarter, with the increase in production attributable to the ramp up of operations, partially offset by mandatory production curtailments. Fort Hills cash operating costs(1) per barrel were $24.25 in the third quarter of 2019, compared to $33.45 in the prior year quarter, with the improvement attributable to the increase in production and a reduction in total Fort Hills cash operating costs.

Suncor's share of Syncrude production was 162,300 bbls/d in the third quarter of 2019, compared to 106,200 bbls/d in the prior year quarter. The increase in production was primarily due to planned maintenance in the current quarter having a smaller impact on production compared to the unplanned maintenance in the prior year quarter. Upgrader utilization at Syncrude was 80% in the third quarter of 2019, compared to 52% in the prior year quarter.

Syncrude cash operating costs(1) per barrel were $40.50 in the third quarter of 2019, a decrease from $63.85 in the prior year quarter, due primarily to the increase in production.

Production volumes at E&P were 92,300 boe/d in the third quarter of 2019, compared to 92,100 boe/d in the prior year quarter. Increased production from Hebron and Oda, which began production in the first quarter of 2019, was partially offset by an unplanned outage at Hibernia, which was resolved by the end of the third quarter, and natural declines at Golden Eagle and Buzzard.

Refinery crude throughput was 463,700 bbls/d and refinery utilization was 100% in the third quarter of 2019, which was comparable to 457,200 bbls/d and a refinery utilization rate of 99% in the prior year quarter.

Refined product sales increased in the third quarter of 2019 to 572,000 bbls/d, compared to 565,500 bbls/d in the prior year quarter, reflecting strong retail volumes.

"We continue to deliver on our commitment to operational excellence through reliable operations across our upstream assets and at our refineries where we achieved refinery utilization of 100%," said Little. "We had record retail sales and a solid performance in our upstream assets despite planned maintenance and the impact of the mandatory production curtailment."

- (1)

- Oil Sands operations cash operating costs, Fort Hills cash operating costs and Syncrude cash operating costs are non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of the MD&A.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 3 |

Strategy Update

Suncor remains focused on maximizing the return to our shareholders through the repurchase of 19.2 million common shares for $756 million under the company's normal course issuer bid and $650 million of dividends paid during the third quarter of 2019. The company also reduced debt by $572 million during the period. Suncor has returned $3.792 billion in dividends and share repurchases to shareholders, representing 46% of total funds from operations, and reduced its debt by $970 million in 2019, reflecting continued flexibility in the company's capital allocation strategy.

Suncor continues to advance projects and investments intended to incrementally and sustainably grow annual free funds flow by strategically investing in production growth of existing assets, and reducing operating and sustainment costs, while moving forward in the areas of safety, reliability and sustainability.

The company incurred $1.487 billion in capital expenditures, excluding capitalized interest in the third quarter of 2019, an increase from $1.180 billion in the prior year quarter. The increase was driven primarily by a more significant planned maintenance program at both Oil Sands operations and Syncrude.

During the third quarter of 2019, Suncor announced that it is replacing its coke-fired boilers with a cogeneration facility at its Oil Sands Base Plant. The facility will provide reliable steam generation required for Suncor's extraction and upgrading operations and is expected to reduce the company's greenhouse gas (GHG) emissions intensity associated with steam production at Oil Sands Base Plant by approximately 25%. The project is estimated to cost $1.4 billion and is expected to be in-service in the second half of 2023.

In the third quarter of 2019, construction on the interconnecting pipeline between Suncor's Oil Sands Base Plant and Syncrude continued in anticipation of an in-service date in the second half of 2020. The bi-directional pipeline is expected to enhance integration between these assets and increase reliability at Syncrude.

"The new cogeneration facility sanctioned this quarter represents meaningful progress towards our initiatives of reducing our greenhouse gas emissions intensity and increasing our structural free funds flow," said Little. "This project, together with the Syncrude interconnecting pipeline, autonomous haul trucks and tailings technology advancements, are expected to generate approximately half of our $2 billion of structural free funds flow target and underscores our commitment to deliver growth that is economically robust, sustainability minded and technologically progressive."

The company's continued focus on strategic production growth of existing assets includes developing step-out opportunities and asset extensions within our offshore business in the E&P segment. Drilling activity at Hebron is ongoing and production continues to ramp up. The seventh and eighth production wells came online during the third quarter and contributed to the asset reaching its nameplate production ahead of schedule. Other E&P activity in the third quarter included development drilling at Hibernia, Buzzard and Terra Nova, and development work on Fenja and the West White Rose Project.

Suncor remains committed to its goal to reduce total GHG emissions intensity by 30% by 2030 and continues to invest in low-carbon innovation aimed at lowering the company's carbon footprint. In the third quarter of 2019, the company finalized investments focused on clean technology and continued development of a network of fast-charging electric vehicle stations across Canada. Subsequent to the quarter, Suncor finalized an additional $50 million equity investment in Enerkem Inc., a waste-to-biofuels and chemicals producer. These investments, in addition to the sanctioning of the cogeneration assets, are critical projects that are expected to advance the company's sustainability and technology initiatives in the transition to a lower carbon world.

| 4 2019 THIRD QUARTER Suncor Energy Inc. | | |

Operating Earnings Reconciliation(1)

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Net earnings |

1 035 | 1 812 | 5 234 | 3 573 | ||||||

| | ||||||||||

Unrealized foreign exchange loss (gain) on U.S. dollar denominated debt |

127 | (195 | ) | (355 | ) | 352 | ||||

| | ||||||||||

Impact of income tax rate adjustment on deferred taxes(2) |

— | — | (1 116 | ) | — | |||||

| | ||||||||||

Gain on significant disposal(3) |

(48 | ) | (60 | ) | (187 | ) | (193 | ) | ||

| | ||||||||||

Operating earnings(1) |

1 114 | 1 557 | 3 576 | 3 732 | ||||||

| | | | | | | | | | | |

- (1)

- Operating

earnings is a non-GAAP financial measure. All reconciling items are presented on an after-tax basis. See the Non-GAAP Financial Measures Advisory section of the MD&A.

- (2)

- In

the second quarter of 2019, the company recorded a $1.116 billion deferred income tax recovery associated with the Government of Alberta's substantive enactment of

legislation for the staged reduction of the corporate income tax rate from 12% to 8% over the next four years.

- (3)

- The third quarter of 2019 included an after-tax gain of $48 million in the E&P segment related to the sale of certain non-core assets. The third quarter of 2018 included an after-tax gain of $60 million on the sale of the company's interest in the Joslyn Oil Sands mining project. In the second quarter of 2019, Suncor sold its 37% interest in Canbriam Energy Inc. for total proceeds and an equivalent gain of $151 million ($139 million after-tax), which had previously been written down to nil in the fourth quarter of 2018 following the company's assessment of forward natural gas prices and the impact on estimated future cash flows.

Corporate Guidance

Suncor has updated its production and other information in its 2019 corporate guidance, previously updated on July 24, 2019.

The total production outlook range has been updated from 780,000 – 820,000 boe/d to 780,000 – 790,000 boe/d to reflect the impact of production for the first nine months of 2019 and the planned fourth quarter production given the higher levels of mandatory production curtailment. Oil Sands operations production has been updated from 410,000 – 440,000 bbls/d to 410,000 – 425,000 bbls/d, Fort Hills production has been updated from 85,000 – 95,000 bbls/d to 85,000 – 90,000 bbls/d, and E&P production has been updated from 105,000 – 115,000 boe/d to 105,000 – 110,000 boe/d. As a result of the changes to the Oil Sands operations production range, the SCO sales range has narrowed from 315,000 – 335,000 bbls/d to 315,000 – 320,000 bbls/d.

Oil Sands operations cash operating costs per barrel have been updated to $27.00 – $28.00 from $24.00 – $26.50, reflecting mandatory production curtailment, the impact of conscious decisions taken to change the production mix to maximize the value of the barrels while operating under curtailment, and higher maintenance and contractor costs.

East Coast Canada royalties have been updated from 17% – 21% to 13% – 17%, with the decrease in royalty rates attributed to the change in production mix among the company's East Coast assets.

Suncor has also updated its full year business environment outlook assumptions for Brent Sullom Voe from US$66.00/bbl to US$63.00/bbl, WTI at Cushing from US$58.00/bbl to US$56.00/bbl, AECO – C Spot from $1.70/GJ to $1.50/GJ, New York Harbor 2-1-1 crack from US$19.00/bbl to US$20.00/bbl, and the Cdn$/US$ exchange rate from 0.76 to 0.75, due to changes in key forward curve pricing for the remainder of the year. For further details and advisories regarding Suncor's 2019 annual guidance, see www.suncor.com/guidance.

Measurement Conversions

Certain natural gas volumes in this report to shareholders have been converted to boe on the basis of one bbl to six mcf. See the Advisories section of the MD&A.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 5 |

MANAGEMENT'S DISCUSSION AND ANALYSIS

October 30, 2019

Suncor is an integrated energy company headquartered in Calgary, Alberta, Canada. We are strategically focused on developing one of the world's largest petroleum resource basins – Canada's Athabasca oil sands. In addition, we explore for, acquire, develop, produce and market crude oil in Canada and internationally; we transport and refine crude oil, and we market petroleum and petrochemical products primarily in Canada. We also operate a renewable energy business and conduct energy trading activities focused principally on the marketing and trading of crude oil, natural gas, byproducts, refined products, and power.

For a description of Suncor's segments, refer to Suncor's Management's Discussion and Analysis for the year ended December 31, 2018, dated February 28, 2019 (the 2018 annual MD&A).

This Management's Discussion and Analysis (MD&A) should be read in conjunction with Suncor's unaudited interim Consolidated Financial Statements for the three and nine months ended September 30, 2019, Suncor's audited Consolidated Financial Statements for the year ended December 31, 2018 and the 2018 annual MD&A.

Additional information about Suncor filed with Canadian securities regulatory authorities and the United States Securities and Exchange Commission (SEC), including quarterly and annual reports and Suncor's Annual Information Form dated February 28, 2019 (the 2018 AIF), which is also filed with the SEC under cover of Form 40-F, is available online at www.sedar.com, www.sec.gov and our website www.suncor.com. Information contained in or otherwise accessible through our website does not form part of this MD&A, and is not incorporated into this document by reference.

References to "we", "our", "Suncor", or "the company" mean Suncor Energy Inc., and the company's subsidiaries and interests in associates and jointly controlled entities, unless the context otherwise requires.

Table of Contents

Basis of Presentation

Unless otherwise noted, all financial information has been prepared in accordance with Canadian generally accepted accounting principles (GAAP), specifically International Accounting Standard (IAS) 34 Interim Financial Reporting as issued by the International Accounting Standards Board (IASB), which is within the framework of International Financial Reporting Standards (IFRS) as issued by the IASB.

Effective January 1, 2019, the company adopted IFRS 16 Leases (IFRS 16), which replaced the previous leasing standard IAS 17 Leases (IAS 17), and requires the recognition of all leases on the balance sheet, with optional exemptions for short-term leases where the term is twelve months or less and for leases of low value. IFRS 16 effectively removes the classification of leases as either finance or operating leases and treats all leases as finance leases for lessees. The accounting treatment for lessors remains essentially unchanged, with the requirement to classify leases as either finance or operating. Please refer to note 3 in the company's unaudited interim Consolidated Financial Statements for the three and nine months ended September 30, 2019 for further information. The company has selected the modified retrospective transition approach, electing to adjust opening retained earnings with no re-statement of comparative figures. As such, comparative information continues to be reported under IAS 17 and International Financial Reporting Interpretations Committee (IFRIC) 4.

All financial information is reported in Canadian dollars, unless otherwise noted. Production volumes are presented on a working-interest basis, before royalties, except for Libya, which is on an entitlement basis.

| 6 2019 THIRD QUARTER Suncor Energy Inc. | | |

Beginning in the first quarter of 2019, results from the company's Energy Trading business have been included within each of the respective operating business segments to which the respective trading activity relates. The Energy Trading business was previously reported within the Corporate, Energy Trading and Eliminations segment. Prior periods have been restated to reflect this change.

Also beginning in the first quarter of 2019, the company revised the classification of its capital expenditures into "asset sustainment and maintenance" and "economic investment" to better reflect the types of capital investments being made by the company. There is no impact to overall capital expenditures, and comparative periods have been restated to reflect this change. Refer to the Capital Investment Update section of this MD&A for further details.

References to Oil Sands operations exclude Suncor's interests in Fort Hills and Syncrude.

Non-GAAP Financial Measures

Certain financial measures in this MD&A – namely operating earnings (loss), funds from (used in) operations, return on capital employed (ROCE), Oil Sands operations cash operating costs, Fort Hills cash operating costs, Syncrude cash operating costs, refining margin, refining operating expense, free funds flow, discretionary free funds flow, and last-in, first-out (LIFO) inventory valuation methodology and related per share amounts – are not prescribed by GAAP. Operating earnings (loss) is defined in the Non-GAAP Financial Measures Advisory section of this MD&A and reconciled to the most directly comparable GAAP measures in the Consolidated Financial Information and Segment Results and Analysis sections of this MD&A. Oil Sands operations cash operating costs, Fort Hills cash operating costs, Syncrude cash operating costs and LIFO are defined in the Non-GAAP Financial Measures Advisory section of this MD&A and reconciled to the most directly comparable GAAP measures in the Segment Results and Analysis section of this MD&A. Funds from (used in) operations, ROCE, free funds flow, discretionary free funds flow, refining margin and refining operating expense are defined and reconciled, where applicable, to the most directly comparable GAAP measures in the Non-GAAP Financial Measures Advisory section of this MD&A.

Risk Factors and Forward-Looking Information

The company's financial and operational performance is potentially affected by a number of factors, including, but not limited to, the factors described within the Forward-Looking Information section of this MD&A. This MD&A contains forward-looking information based on Suncor's current expectations, estimates, projections and assumptions. This information is provided to assist readers in understanding the company's future plans and expectations and may not be appropriate for other purposes. Refer to the Forward-Looking Information section of this MD&A for information on the material risk factors and assumptions underlying our forward-looking information contained in this MD&A.

Measurement Conversions

Certain crude oil and natural gas liquids volumes have been converted to mcfe on the basis of one bbl to six mcf. Also, certain natural gas volumes have been converted to boe or mboe on the same basis. Any figure presented in mcfe, boe or mboe may be misleading, particularly if used in isolation. A conversion ratio of one bbl of crude oil or natural gas liquids to six mcf of natural gas is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio based on the current price of crude oil as compared to natural gas is significantly different from the energy equivalency of 6:1, conversion on a 6:1 basis may be misleading as an indication of value.

Common Abbreviations

For a list of abbreviations that may be used in this MD&A, refer to the Common Abbreviations section of this MD&A.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 7 |

- •

- Third quarter financial results

- •

- Suncor's

net earnings were $1.035 billion ($0.67 per common share) in the third quarter of 2019, compared to $1.812 billion ($1.12 per common share) in the

prior year quarter. In addition to the factors impacting operating earnings discussed below, net earnings for the third quarter of 2019 included a $127 million unrealized after-tax foreign

exchange loss on the revaluation of U.S. dollar denominated debt and an after-tax gain of $48 million in the Exploration and Production (E&P) segment related to a non-core asset sale.

Net earnings in the prior year quarter included an unrealized after-tax foreign exchange gain of $195 million on the revaluation of U.S. dollar denominated debt and an after-tax gain of

$60 million on the sale of the company's interest in the Joslyn Oil Sands mining project.

- •

- Suncor's

third quarter 2019 operating earnings(1) were $1.114 billion ($0.72 per common share), compared to $1.557 billion ($0.96 per common

share) in the prior year quarter, with the decrease in operating earnings primarily related to a weaker business environment resulting in a decrease in crude oil price realizations and lower refining

margins. Partially offsetting these were higher crude oil production, increased refinery crude throughput, and the impact of a weaker Canadian dollar on U.S. dollar denominated sales, as

detailed in the Segment Results and Analysis section of this MD&A.

- •

- Funds

from operations(1) were $2.675 billion ($1.72 per common share) in the third quarter of 2019, compared to $3.139 billion ($1.94 per common

share) in the third quarter of 2018, and were influenced primarily by the same factors impacting operating earnings noted above. Cash flow provided by operating activities, which includes changes in

non-cash working capital, was $3.136 billion ($2.02 per common share) for the third quarter of 2019, compared to $4.370 billion ($2.70 per common share) for the third quarter of 2018,

with both periods reflecting a source of cash from working capital.

- •

- Syncrude production increased to 162,300 bbls/d, compared to 106,200 bbls/d in the prior year quarter.

Production increased due to improved reliability, which was partially offset by planned maintenance and mandatory production curtailments, resulting in upgrader utilization of 80% in the third quarter

of 2019, compared to 52% in the prior year quarter.

- •

- Fort Hills production increased to 85,500 bbls/d compared to 69,400 bbls/d in the prior year quarter. The ramp

up of Fort Hills operations throughout 2018 drove the increase in production, which was partially offset by mandatory production curtailments. Fort Hills cash operating costs(1) per

barrel were $24.25 in the third quarter of 2019, compared to $33.45 in the prior year quarter, with the improvement attributable to the increase in production and a reduction in total cash operating

costs.

- •

- Refining and Marketing (R&M) achieved full refinery utilization. R&M delivered quarterly crude

throughput of

463,700 bbls/d and record refined product sales of 572,000 bbls/d in the third quarter of 2019, compared to 457,200 bbls/d and 565,500 bbls/d respectively, in the prior

year quarter. Refinery utilization averaged 100% for the quarter.

- •

- Ramp up of Hebron continues after completion of the seventh and eighth production wells. Production at

Hebron was

23,600 bbls/d in the third quarter of 2019, compared to 14,400 bbls/d in the prior year quarter, reaching nameplate production ahead of schedule.

- •

- Investment in low-carbon power cogeneration. In the third quarter of 2019, Suncor announced that it is

replacing its

coke-fired boilers with a new cogeneration facility at its Oil Sands Base Plant. The cogeneration units will provide reliable steam generation required for Suncor's extraction and upgrading operations

and are expected to reduce the greenhouse gas (GHG) emissions intensity associated with steam production at Base Plant by approximately 25%. The project is estimated to cost $1.4 billion and is

expected to be in-service in the second half of 2023.

- •

- Increased share repurchases and dividends. During the third quarter of 2019, the company

demonstrated its

flexible capital allocation program by taking advantage of market conditions to accelerate its share buybacks under its normal course issuer bid (NCIB). The company repurchased $756 million of

its common shares and paid $650 million to shareholders through dividends during the third quarter of 2019. In the third quarter of 2019, the company repurchased 19.2 million common

shares, representing 1.2% of the total outstanding common shares, compared to 16.8 million common shares in the third quarter of 2018, representing a 14% increase.

- •

- Reduction of debt. During the third quarter of 2019, the company continued to strengthen the balance sheet and repaid $572 million of debt, further improving the company's liquidity and balance sheet flexibility.

- (1)

- Non-GAAP financial measure. See the Non-GAAP Financial Measures Advisory section of this MD&A.

| 8 2019 THIRD QUARTER Suncor Energy Inc. | | |

3. CONSOLIDATED FINANCIAL INFORMATION(1)

Financial Highlights

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Net earnings (loss) |

||||||||||

| | ||||||||||

Oil Sands |

505 | 822 | 2 255 | 1 322 | ||||||

| | ||||||||||

Exploration and Production |

219 | 222 | 1 167 | 922 | ||||||

| | ||||||||||

Refining and Marketing |

668 | 932 | 2 442 | 2 392 | ||||||

| | ||||||||||

Corporate and Eliminations |

(357 | ) | (164 | ) | (630 | ) | (1 063 | ) | ||

| | | | | | | | | | | |

Total |

1 035 | 1 812 | 5 234 | 3 573 | ||||||

| | | | | | | | | | | |

Operating earnings (loss)(2) |

||||||||||

| | ||||||||||

Oil Sands |

505 | 762 | 1 345 | 1 262 | ||||||

| | ||||||||||

Exploration and Production |

171 | 222 | 910 | 789 | ||||||

| | ||||||||||

Refining and Marketing |

668 | 932 | 2 354 | 2 392 | ||||||

| | ||||||||||

Corporate and Eliminations |

(230 | ) | (359 | ) | (1 033 | ) | (711 | ) | ||

| | | | | | | | | | | |

Total |

1 114 | 1 557 | 3 576 | 3 732 | ||||||

| | | | | | | | | | | |

Funds from (used in) operations(2) |

||||||||||

| | ||||||||||

Oil Sands |

1 606 | 1 884 | 4 656 | 4 357 | ||||||

| | ||||||||||

Exploration and Production |

379 | 443 | 1 588 | 1 448 | ||||||

| | ||||||||||

Refining and Marketing |

885 | 1 122 | 3 070 | 2 925 | ||||||

| | ||||||||||

Corporate and Eliminations |

(195 | ) | (310 | ) | (1 049 | ) | (565 | ) | ||

| | | | | | | | | | | |

Total |

2 675 | 3 139 | 8 265 | 8 165 | ||||||

| | | | | | | | | | | |

Decrease (increase) in non-cash working capital |

461 | 1 231 | (148 | ) | (625 | ) | ||||

| | ||||||||||

Cash flow provided by operating activities |

3 136 | 4 370 | 8 117 | 7 540 | ||||||

| | | | | | | | | | | |

Capital and exploration expenditures(3) |

||||||||||

| | ||||||||||

Asset sustainment and maintenance |

966 | 753 | 2 201 | 2 693 | ||||||

| | ||||||||||

Economic investment |

521 | 427 | 1 497 | 1 438 | ||||||

| | | | | | | | | | | |

Total |

1 487 | 1 180 | 3 698 | 4 131 | ||||||

| | | | | | | | | | | |

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Discretionary free funds flow(2) |

1 043 | 1 789 | 4 050 | 3 668 | ||||||

| | | | | | | | | | | |

- (1)

- The

three and nine months ended September 30, 2018 have been restated to reflect the change to the company's segmented presentation of its Energy Trading business, with no

impact to overall consolidated results. The Energy Trading business is now included within each of the respective operating business segments to which the respective trading activity relates. Suncor's

Energy Trading business was previously reported within the Corporate, Energy Trading and Eliminations segment.

- (2)

- Non-GAAP

financial measures. See the Non-GAAP Financial Measures Advisory section of this MD&A. Discretionary free funds flow for the three and nine months ended September 30,

2018 have been restated for the impact of the change to the company's classification of asset sustainment and maintenance capital expenditures. Refer to the Capital and Investment Update section of

this MD&A for further details.

- (3)

- Excludes capitalized interest of $29 million in the third quarter of 2019 and $26 million in the third quarter of 2018 and reflects the company's revised capital expenditure classification. Refer to the Capital and Investment Update section of this MD&A for further details.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 9 |

Operating Highlights

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

|

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Production volumes by segment |

||||||||||

| | ||||||||||

Oil Sands (mbbls/d) |

670.0 | 651.7 | 673.1 | 591.0 | ||||||

| | ||||||||||

Exploration and Production (mboe/d) |

92.3 | 92.1 | 103.6 | 107.9 | ||||||

| | | | | | | | | | | |

Total (mboe/d) |

762.3 | 743.8 | 776.7 | 698.9 | ||||||

| | | | | | | | | | | |

Refinery utilization (%) |

100 | 99 | 94 | 91 | ||||||

| | ||||||||||

Refinery crude oil processed (mbbls/d) |

463.7 | 457.2 | 436.0 | 418.3 | ||||||

| | | | | | | | | | | |

Net Earnings

Suncor's consolidated net earnings for the third quarter of 2019 were $1.035 billion, compared to $1.812 billion for the prior year quarter. Net earnings were primarily affected by the same factors that influenced operating earnings described subsequently in this section of this MD&A.

Other items affecting net earnings over these periods included:

- •

- The

after-tax unrealized foreign exchange loss on the revaluation of U.S. dollar denominated debt was $127 million for the third quarter of 2019, compared to a

gain of $195 million for the third quarter of 2018.

- •

- The

third quarter of 2019 included an after-tax gain of $48 million in the E&P segment related to the sale of certain non-core assets.

- •

- The third quarter of 2018 included an after-tax gain of $60 million on the sale of the company's interest in the Joslyn Oil Sands mining project.

Operating Earnings Reconciliation(1)

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Net earnings |

1 035 | 1 812 | 5 234 | 3 573 | ||||||

| | ||||||||||

Unrealized foreign exchange loss (gain) on U.S. dollar denominated debt |

127 | (195 | ) | (355 | ) | 352 | ||||

| | ||||||||||

Impact of income tax rate adjustment on deferred taxes(2) |

— | — | (1 116 | ) | — | |||||

| | ||||||||||

Gain on significant disposal(3) |

(48 | ) | (60 | ) | (187 | ) | (193 | ) | ||

| | | | | | | | | | | |

Operating earnings(1) |

1 114 | 1 557 | 3 576 | 3 732 | ||||||

| | | | | | | | | | | |

- (1)

- Operating

earnings is a non-GAAP financial measure. All reconciling items are presented on an after-tax basis. See the Non-GAAP Financial Measures Advisory section of

this MD&A.

- (2)

- In

the second quarter of 2019, the company recorded a $1.116 billion deferred income tax recovery associated with the Government of Alberta's substantive enactment of

legislation for the staged reduction of the corporate income tax rate from 12% to 8% over the next four years.

- (3)

- The third quarter of 2019 included an after-tax gain of $48 million in the E&P segment related to the sale of certain non-core assets. In the second quarter of 2019, Suncor sold its 37% interest in Canbriam Energy Inc. (Canbriam) for total proceeds and an equivalent gain of $151 million ($139 million after-tax), which had previously been written down to nil in the fourth quarter of 2018 following the company's assessment of forward natural gas prices and the impact on estimated future cash flows. The equity interest in Canbriam was acquired during the first quarter of 2018 in exchange for the company's mineral landholdings in northeast British Columbia, at which time a gain of $133 million after-tax was recorded on the transaction. The third quarter of 2018 included an after-tax gain of $60 million on the sale of the company's interest in the Joslyn Oil Sands mining project.

| 10 2019 THIRD QUARTER Suncor Energy Inc. | | |

Bridge Analysis of Operating Earnings ($ millions)(1)

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this MD&A.

Suncor's third quarter 2019 operating earnings were $1.114 billion ($0.72 per common share), compared to $1.557 billion ($0.96 per common share) in the prior year quarter. Highlights of the third quarter included higher overall crude oil production and refinery crude throughput as compared to the prior year quarter. Higher production at Syncrude and the ramp up of Fort Hills and Hebron production over the last year increased crude output during the third quarter of 2019, which was partially offset by planned maintenance, the impact of the Alberta government's mandatory production curtailments and an unplanned outage at Hibernia, which was resolved by the end of the third quarter. In addition, operating earnings were positively impacted by the realization of intersegment profit on inventory transfers, compared to the elimination of intersegment profit in the prior year quarter.

The decrease in operating earnings was primarily related to a weaker business environment, which drove lower overall crude price realizations and lower refining margins, as well as an increase in operating and transportation expenses.

After-Tax Share-Based Compensation Expense by Segment

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Oil Sands |

15 | 8 | 53 | 63 | ||||||

| | ||||||||||

Exploration and Production |

2 | 1 | 6 | 6 | ||||||

| | ||||||||||

Refining and Marketing |

8 | 4 | 30 | 32 | ||||||

| | ||||||||||

Corporate and Eliminations |

27 | 19 | 107 | 130 | ||||||

| | | | | | | | | | | |

Total share-based compensation expense |

52 | 32 | 196 | 231 | ||||||

| | | | | | | | | | | |

The after-tax share-based compensation expense increased to $52 million during the third quarter of 2019, compared to an expense of $32 million during the prior year quarter, as a result of an increase in the company's share price through the period, compared to a decrease in the prior year quarter.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 11 |

Business Environment

Commodity prices, refining crack spreads and foreign exchange rates are important factors that affect the results of Suncor's operations.

|

Average for the three months ended September 30 |

Average for the nine months ended September 30 |

||||||||||

|

2019 | 2018 | 2019 | 2018 | ||||||||

| | | | | | | | | | | | | |

WTI crude oil at Cushing |

US$/bbl | 56.45 | 69.50 | 57.05 | 66.80 | |||||||

| | ||||||||||||

Dated Brent crude |

US$/bbl | 61.90 | 75.25 | 64.65 | 72.15 | |||||||

| | ||||||||||||

Dated Brent/Maya FOB price differential |

US$/bbl | 5.20 | 10.20 | 5.45 | 10.75 | |||||||

| | ||||||||||||

MSW at Edmonton |

Cdn$/bbl | 68.35 | 82.10 | 69.60 | 77.85 | |||||||

| | ||||||||||||

WCS at Hardisty |

US$/bbl | 44.20 | 47.35 | 45.30 | 44.90 | |||||||

| | ||||||||||||

Light/heavy crude oil differential for WTI at Cushing less WCS at Hardisty |

US$/bbl | (12.25 | ) | (22.15 | ) | (11.75 | ) | (21.90 | ) | |||

| | ||||||||||||

SYN-WTI differential |

US$/bbl | 0.40 | (0.90 | ) | (0.55 | ) | (1.00 | ) | ||||

| | ||||||||||||

Condensate at Edmonton |

US$/bbl | 52.00 | 66.80 | 52.80 | 66.30 | |||||||

| | ||||||||||||

Natural gas (Alberta spot) at AECO |

Cdn$/mcf | 0.95 | 1.20 | 1.50 | 1.50 | |||||||

| | ||||||||||||

Alberta Power Pool Price |

Cdn$/MWh | 46.85 | 54.45 | 57.55 | 48.40 | |||||||

| | ||||||||||||

New York Harbor 2-1-1 crack(1) |

US$/bbl | 20.45 | 20.25 | 20.45 | 19.20 | |||||||

| | ||||||||||||

Chicago 2-1-1 crack(1) |

US$/bbl | 17.05 | 20.00 | 17.95 | 16.75 | |||||||

| | ||||||||||||

Portland 2-1-1 crack(1) |

US$/bbl | 23.90 | 22.05 | 24.15 | 23.20 | |||||||

| | ||||||||||||

Gulf Coast 2-1-1 crack(1) |

US$/bbl | 20.00 | 19.35 | 19.85 | 18.20 | |||||||

| | ||||||||||||

Exchange rate |

US$/Cdn$ | 0.76 | 0.77 | 0.75 | 0.78 | |||||||

| | ||||||||||||

Exchange rate (end of period) |

US$/Cdn$ | 0.76 | 0.77 | 0.76 | 0.77 | |||||||

| | | | | | | | | | | | | |

- (1)

- 2-1-1 crack spreads are indicators of the refining margin generated by converting two barrels of WTI into one barrel of gasoline and one barrel of diesel. The company previously quoted 3-2-1 crack margin benchmarks based on wider use and familiarity with these benchmarks and, although the 3-2-1 crack spread is more commonly quoted, the company's refinery production is better aligned with a 2-1-1 crack spread, which better reflects the approximate composition of Suncor's overall refined product mix. The crack spreads presented here generally approximate the regions into which the company sells refined products through retail and wholesale channels.

Suncor's sweet SCO price realizations are influenced primarily by the price of WTI at Cushing and by the supply and demand for sweet SCO from Western Canada, which influences SCO differentials. Price realizations in the third quarter of 2019 for sweet SCO were unfavourably impacted by a decrease in WTI at Cushing to US$56.45/bbl, compared to US$69.50/bbl in the prior year quarter. Suncor also produces sour SCO, the price of which is influenced by various crude benchmarks, including, but not limited to, MSW at Edmonton and WCS at Hardisty, and which can also be affected by prices negotiated for spot sales. Prices for MSW at Edmonton decreased to $68.35/bbl compared to $82.10/bbl in the prior year quarter, and prices for WCS at Hardisty decreased to US$44.20/bbl in the third quarter of 2019, from US$47.35/bbl in the prior year quarter, which was less than the decrease in WTI as a result of narrowing heavy crude differentials in part due to mandatory production curtailments in Alberta. Sweet and sour SCO differentials in the third quarter of 2019 were favourable when compared to the third quarter of 2018.

Bitumen production that Suncor does not upgrade is blended with diluent or SCO to facilitate delivery on pipeline systems. Net bitumen price realizations are, therefore, influenced by both prices for Canadian heavy crude oil (WCS at Hardisty is a common reference), prices for diluent (Condensate at Edmonton) and SCO. Bitumen price realizations can also be affected by bitumen quality and spot sales. Bitumen prices were favourably impacted by narrower heavy crude oil differentials in the third quarter of 2019.

Suncor's price realizations for production from East Coast Canada and International assets are influenced primarily by the price for Brent crude, which decreased to US$61.90/bbl in the third quarter of 2019, compared to US$75.25/bbl in the prior year quarter.

| 12 2019 THIRD QUARTER Suncor Energy Inc. | | |

Suncor's refining margins are primarily influenced by industry benchmark crack spreads and although the 3-2-1 crack spread is more commonly quoted, the company's refinery production is better aligned with a 2-1-1 crack spread, which more appropriately reflects the company's refined product mix of gasoline and distillates. Benchmark crack spreads are industry indicators approximating the gross margin on a barrel of crude oil that is refined to produce gasoline and distillates. More complex refineries can earn greater refining margin by processing less expensive, heavier crudes. Crack spreads do not necessarily reflect the margins at a specific refinery. Crack spreads are based on current crude feedstock prices, whereas actual earnings are based on first-in, first-out (FIFO) inventory accounting where a delay exists between the time that feedstock is purchased and when it is processed and sold to a third party. A FIFO loss normally reflects a declining price environment for crude oil and finished products, whereas FIFO gains reflect an increasing price environment for crude oil and finished products. Specific refinery margins are determined by actual crude purchase costs, refinery configuration, production mix and realized prices for refined product sales in markets unique to each refinery.

The cost of natural gas used in Suncor's Oil Sands and Refining operations is primarily referenced to Alberta spot prices at AECO. The average AECO benchmark decreased to $0.95/mcf in the third quarter of 2019, from $1.20/mcf in the prior year quarter.

Excess electricity produced in Suncor's Oil Sands operations and at Fort Hills is sold to the Alberta Electric System Operator, with the proceeds netted against the cash operating cost per barrel metric. The Alberta power pool price decreased to an average of $46.85/MWh in the third quarter of 2019, compared to $54.45/MWh in the prior year quarter.

The majority of Suncor's revenues from the sale of oil and natural gas commodities are based on prices that are determined by or referenced to U.S. dollar benchmark prices, while the majority of Suncor's expenditures are realized in Canadian dollars. The Canadian dollar weakened in relation to the U.S. dollar during the third quarter of 2019, as the average exchange rate decreased to US$0.76 per one Canadian dollar from US$0.77 per one Canadian dollar in the prior year quarter. This rate decrease had a positive impact on price realizations for the company during the third quarter of 2019.

Suncor also has assets and liabilities, including approximately 65% of the company's debt, which are denominated in U.S. dollars and translated to Suncor's reporting currency (Canadian dollars) at each balance sheet date. A decrease in the value of the Canadian dollar, relative to the U.S. dollar, from the previous balance sheet date increases the amount of Canadian dollars required to settle U.S. dollar denominated obligations, while an increase in the value of the Canadian dollar, relative to the U.S. dollar, decreases the amount of Canadian dollars required to settle U.S. dollar denominated obligations.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 13 |

4. SEGMENT RESULTS AND ANALYSIS

OIL SANDS(1)

Financial Highlights

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Gross revenues |

4 601 | 4 815 | 13 922 | 12 594 | ||||||

| | ||||||||||

Less: Royalties |

(235 | ) | (161 | ) | (774 | ) | (331 | ) | ||

| | | | | | | | | | | |

Operating revenues, net of royalties |

4 366 | 4 654 | 13 148 | 12 263 | ||||||

| | | | | | | | | | | |

Net earnings |

505 | 822 | 2 255 | 1 322 | ||||||

| | ||||||||||

Impact of income tax rate adjustment on deferred taxes(2) |

— | — | (910 | ) | — | |||||

| | ||||||||||

Gain on significant disposal(3) |

— | (60 | ) | — | (60 | ) | ||||

| | | | | | | | | | | |

Operating earnings(4) |

505 | 762 | 1 345 | 1 262 | ||||||

| | | | | | | | | | | |

Funds from operations(4) |

1 606 | 1 884 | 4 656 | 4 357 | ||||||

| | | | | | | | | | | |

- (1)

- The

three and nine months ended September 30, 2018 have been restated to reflect the change to the company's segmented presentation of its Energy Trading business, with no

impact to overall consolidated results. The Energy Trading business is now included within each of the respective operating business segments to which the respective trading activity relates. Suncor's

Energy Trading business was previously reported within the Corporate, Energy Trading and Eliminations segment.

- (2)

- In

the second quarter of 2019, the company recorded a $910 million deferred income tax recovery in the Oil Sands segment associated with the Government of Alberta's substantive

enactment of legislation for the staged reduction of the corporate income tax rate from 12% to 8% over the next four years.

- (3)

- The

third quarter of 2018 included an after-tax gain of $60 million on the sale of the company's interest in the Joslyn Oil Sands mining project.

- (4)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this MD&A.

Bridge Analysis of Operating Earnings ($ millions)(1)

- (1)

- For an explanation of this bridge analysis, see the Non-GAAP Financial Measures Advisory section of this MD&A.

The Oil Sands segment had operating earnings of $505 million in the third quarter of 2019, compared to $762 million in the prior year quarter. The decrease was primarily due to lower benchmark crude prices, higher operating, selling and general expenses, and an increase in royalties. The decrease was partially offset by higher overall production volumes due to stronger Syncrude production and the ramp up of Fort Hills production, as well as higher bitumen crude price realizations due to mandatory production curtailments.

| 14 2019 THIRD QUARTER Suncor Energy Inc. | | |

Production Volumes(1)

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

(mbbls/d) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Upgraded product (SCO and diesel) |

325.3 | 338.5 | 326.5 | 291.1 | ||||||

| | ||||||||||

Internally consumed diesel(2) |

(8.3 | ) | (8.4 | ) | (8.7 | ) | (8.4 | ) | ||

| | | | | | | | | | | |

Total Oil Sands operations upgraded product |

317.0 | 330.1 | 317.8 | 282.7 | ||||||

| | ||||||||||

In Situ non-upgraded bitumen |

105.2 | 146.0 | 93.3 | 130.9 | ||||||

| | | | | | | | | | | |

Total Oil Sands operations production |

422.2 | 476.1 | 411.1 | 413.6 | ||||||

| | ||||||||||

Fort Hills bitumen |

85.5 | 69.4 | 84.4 | 56.9 | ||||||

| | ||||||||||

Internally upgraded bitumen from froth |

— | — | — | (1.7 | ) | |||||

| | | | | | | | | | | |

Total Fort Hills bitumen production |

85.5 | 69.4 | 84.4 | 55.2 | ||||||

| | ||||||||||

Syncrude (sweet SCO and diesel) |

164.7 | 107.6 | 180.1 | 124.3 | ||||||

| | ||||||||||

Internally consumed diesel(2) |

(2.4 | ) | (1.4 | ) | (2.5 | ) | (2.1 | ) | ||

| | | | | | | | | | | |

Total Syncrude production |

162.3 | 106.2 | 177.6 | 122.2 | ||||||

| | | | | | | | | | | |

Total Oil Sands production |

670.0 | 651.7 | 673.1 | 591.0 | ||||||

| | | | | | | | | | | |

- (1)

- Bitumen

production from Oil Sands Base is upgraded, while bitumen production from In Situ operations is either upgraded or sold directly to customers, including Suncor's own

refineries, with SCO and diesel yields of approximately 79% of bitumen feedstock input. Fort Hills finished bitumen is sold directly to customers and bitumen froth from Fort Hills can be sent to Oil

Sands Base for further processing into SCO. Essentially all of the bitumen produced at Syncrude is upgraded to sweet SCO and a small amount of diesel, at an approximate yield of 85%.

- (2)

- Both Oil Sands operations and Syncrude produce diesel, which is internally consumed in mining operations, and Fort Hills uses internally produced diesel from Oil Sands Base within its mining operations. Of the 8,300 bbls/d of internally consumed diesel at Oil Sands operations in the third quarter of 2019, 6,600 bbls/d was consumed at Oil Sands Base and 1,700 bbls/d, net, was consumed at Fort Hills. Oil Sands operations utilization rates are calculated net of Oil Sands Base internally consumed diesel, but inclusive of diesel consumed internally at Fort Hills. Syncrude utilization rates are calculated using intermediate sour production.

Oil Sands operations production decreased to 422,200 bbls/d in the third quarter of 2019, from 476,100 bbls/d in the prior year quarter, primarily due to planned maintenance and mandatory production curtailments in the province of Alberta, which resulted in upgrader utilization declining to 91% in the third quarter of 2019, compared to 95% in the prior year period. The company sought to minimize the impact of mandatory production curtailments by allocating curtailment allotment credits between Oil Sands assets on an opportunistic basis, as well as maximizing the production to the upgrader to produce higher value SCO barrels in the third quarter of 2019, resulting in decreased production of In Situ non-upgraded bitumen. Given our planned maintenance, there was limited availability and opportunity to purchase production quotas from other operators in the quarter.

Fort Hills production, net to Suncor, increased to 85,500 bbls/d of bitumen in the third quarter of 2019, compared to 69,400 bbls/d in the prior year quarter. The increase was due to the successful ramp up of operations throughout 2018, partially offset by the impact of mandatory production curtailments.

Suncor's share of Syncrude production was 162,300 bbls/d in the third quarter of 2019, compared to 106,200 bbls/d in the prior year quarter. The increase in production was primarily due to improved reliability at Syncrude, partially offset by planned maintenance that commenced in the quarter and the impact of mandatory production curtailments. Production in the prior year quarter was impacted by extended planned maintenance and a power disruption that occurred late in the second quarter of 2018.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 15 |

Sales Volumes

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

(mbbls/d) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Oil Sands operations sales volumes |

||||||||||

| | ||||||||||

Sweet SCO |

116.1 | 129.5 | 116.0 | 91.3 | ||||||

| | ||||||||||

Diesel |

20.1 | 34.7 | 24.7 | 29.2 | ||||||

| | ||||||||||

Sour SCO |

184.6 | 162.8 | 177.3 | 166.6 | ||||||

| | | | | | | | | | | |

Upgraded product |

320.8 | 327.0 | 318.0 | 287.1 | ||||||

| | ||||||||||

In Situ non-upgraded bitumen |

110.2 | 131.4 | 93.0 | 121.2 | ||||||

| | | | | | | | | | | |

Oil Sands operations |

431.0 | 458.4 | 411.0 | 408.3 | ||||||

| | ||||||||||

Fort Hills bitumen |

91.6 | 61.6 | 84.1 | 44.8 | ||||||

| | ||||||||||

Syncrude |

162.3 | 106.2 | 177.6 | 122.2 | ||||||

| | | | | | | | | | | |

Total |

684.9 | 626.2 | 672.7 | 575.3 | ||||||

| | | | | | | | | | | |

Sales volumes for Oil Sands operations were 431,000 bbls/d in the third quarter of 2019, compared to 458,400 bbls/d in the prior year quarter, and were influenced by the same factors influencing production as noted above, partially offset by a draw of crude inventory.

Bitumen sales at Fort Hills increased to 91,600 bbls/d, net to Suncor, in the third quarter of 2019, from 61,600 bbls/d in the prior year quarter, consistent with the increase in production combined with a draw of inventory.

Bitumen Production

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

|

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Oil Sands Base |

||||||||||

| | ||||||||||

Bitumen production (mbbls/d) |

301.0 | 323.4 | 289.8 | 252.2 | ||||||

| | ||||||||||

Bitumen ore mined (thousands of tonnes per day) |

460.3 | 449.6 | 431.1 | 366.5 | ||||||

| | ||||||||||

Bitumen ore grade quality (bbls/tonne) |

0.65 | 0.72 | 0.67 | 0.69 | ||||||

| | | | | | | | | | | |

In Situ |

||||||||||

| | ||||||||||

Bitumen production – Firebag (mbbls/d) |

194.6 | 211.0 | 184.1 | 206.2 | ||||||

| | ||||||||||

Steam-to-oil ratio – Firebag |

2.7 | 2.7 | 2.7 | 2.6 | ||||||

| | | | | | | | | | | |

Bitumen production – MacKay River (mbbls/d) |

23.1 | 37.1 | 31.5 | 35.6 | ||||||

| | ||||||||||

Steam-to-oil ratio – MacKay River |

2.9 | 2.8 | 3.0 | 2.9 | ||||||

| | | | | | | | | | | |

Total In Situ bitumen production (mbbls/d) |

217.7 | 248.1 | 215.6 | 241.8 | ||||||

| | | | | | | | | | | |

Total Oil Sands operations bitumen production (mbbls/d) |

518.7 | 571.5 | 505.4 | 494.0 | ||||||

| | | | | | | | | | | |

Fort Hills |

||||||||||

| | ||||||||||

Bitumen production (mbbls/d) |

85.5 | 69.4 | 84.4 | 56.9 | ||||||

| | ||||||||||

Bitumen ore mined (thousands of tonnes per day) |

126.1 | 114.1 | 134.0 | 91.2 | ||||||

| | ||||||||||

Bitumen ore grade quality (bbls/tonne) |

0.68 | 0.61 | 0.63 | 0.62 | ||||||

| | | | | | | | | | | |

Syncrude |

||||||||||

| | ||||||||||

Bitumen production (mbbls/d) |

194.4 | 130.9 | 211.2 | 148.8 | ||||||

| | ||||||||||

Bitumen ore mined (thousands of tonnes per day) |

313.5 | 213.3 | 341.9 | 241.5 | ||||||

| | ||||||||||

Bitumen ore grade quality (bbls/tonne) |

0.62 | 0.61 | 0.62 | 0.62 | ||||||

| | | | | | | | | | | |

Total Oil Sands bitumen production |

798.6 | 771.8 | 801.0 | 699.7 | ||||||

| | | | | | | | | | | |

| 16 2019 THIRD QUARTER Suncor Energy Inc. | | |

Bitumen production at Oil Sands operations decreased in the third quarter of 2019 to 518,700 bbls/d, compared to 571,500 bbls/d in the prior year quarter. The decrease was primarily due to planned upgrader maintenance and mandatory production curtailments.

Fort Hills bitumen production increased in the third quarter of 2019 to 85,500 bbls/d, net to Suncor, from 69,400 bbls/d in the prior year quarter. The increase was primarily due to a ramp up of production throughout 2018, partially offset by the impact of mandatory production curtailments.

Bitumen production at Syncrude in the third quarter of 2019 increased to 194,400 bbls/d, net to Suncor, from 130,900 bbls/d in the prior year quarter. The increase was primarily due to improved upgrader reliability, partially offset by planned maintenance and the impact of mandatory production curtailments.

Price Realizations

Net of transportation costs, but before royalties |

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($/bbl) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Oil Sands operations |

||||||||||

| | ||||||||||

SCO and diesel |

68.11 | 82.95 | 69.24 | 78.06 | ||||||

| | ||||||||||

Bitumen |

42.21 | 36.62 | 44.59 | 35.65 | ||||||

| | ||||||||||

Crude sales basket (all products) |

61.49 | 69.67 | 63.67 | 65.47 | ||||||

| | ||||||||||

Crude sales basket, relative to WTI |

(13.07 | ) | (20.59 | ) | (12.15 | ) | (20.17 | ) | ||

| | | | | | | | | | | |

Fort Hills bitumen |

48.50 | 53.43 | 51.74 | 51.44 | ||||||

| | | | | | | | | | | |

Syncrude – sweet SCO |

74.07 | 88.80 | 73.84 | 83.12 | ||||||

| | ||||||||||

Syncrude, relative to WTI |

(0.49 | ) | (1.46 | ) | (1.98 | ) | (2.52 | ) | ||

| | | | | | | | | | | |

Average price realizations at Oil Sands operations decreased to $61.49/bbl in the third quarter of 2019 from $69.67/bbl in the prior year quarter due to a decrease in the WTI benchmark, partially offset by narrower heavy crude oil differentials resulting from mandatory production curtailments in the province of Alberta, strengthening SCO differentials, and the impact of a weaker Canadian dollar.

Average price realizations for Fort Hills bitumen were $48.50/bbl in the third quarter of 2019 and were higher than In Situ bitumen realizations due to a higher proportion of sales being made in the U.S. mid-continent and the U.S. Gulf Coast, where Suncor is able to utilize its logistics network to access favourable pricing in the U.S. market, combined with the higher quality associated with paraffinic froth-treated bitumen produced at Fort Hills. Average price realizations were lower than the prior year quarter due to narrower location differentials in the third quarter of 2019.

Average price realizations at Syncrude decreased to $74.07/bbl in the third quarter of 2019 from $88.80/bbl in the prior year quarter due to the decrease in the WTI benchmark price, partially offset by the impact of a weaker Canadian dollar and narrower SCO differentials. Average Syncrude realizations were lower than the average quarterly benchmark due to a higher proportion of quarterly sales volumes occurring prior to planned maintenance, when the differential was at a discount.

Royalties

Royalties for the Oil Sands segment were higher in the third quarter of 2019 compared to the prior year quarter, primarily due to higher production at Syncrude.

Expenses and Other Factors

Oil Sands operating and transportation expenses for the third quarter of 2019 increased when compared to the prior year quarter, as described in detail below. See the reconciliation in the Cash Operating Costs section below for further details regarding cash operating costs and a breakdown of non-production costs by asset.

At Oil Sands operations, operating costs increased as a result of an increase in maintenance, contractor mining, and research and development costs.

At Fort Hills, operating costs in the third quarter of 2019 increased when compared to the prior year quarter primarily due to higher mining costs associated with increased production volumes, partially offset by a decrease in project startup expenses.

Suncor's share of Syncrude operating costs were comparable to the prior year quarter.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 17 |

Oil Sands transportation costs increased primarily as a result of higher overall production and sales volumes, as compared to the prior year quarter.

DD&A and impairment expenses and exploration expense for the third quarter of 2019 were lower compared to the prior year quarter as the prior year period included a write-down of certain assets no longer being utilized by the company, partially offset by additional depreciation associated with the transition to IFRS 16.

Cash Operating Costs

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions, except as noted) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Oil Sands Operating, selling and general expense (OS&G) |

2 009 | 1 855 | 6 042 | 5 579 | ||||||

| | | | | | | | | | | |

Oil Sands operations cash operating costs(1) reconciliation |

||||||||||

| | ||||||||||

Oil Sands operations OS&G |

1 156 | 1 006 | 3 496 | 3 133 | ||||||

| | ||||||||||

Non-production costs(2) |

(73 | ) | (15 | ) | (168 | ) | (96 | ) | ||

| | ||||||||||

Excess power capacity and other(3) |

(64 | ) | (50 | ) | (181 | ) | (157 | ) | ||

| | ||||||||||

Inventory changes |

19 | 28 | 16 | 11 | ||||||

| | | | | | | | | | | |

Oil Sands operations cash operating costs(1) |

1 038 | 969 | 3 163 | 2 891 | ||||||

| | ||||||||||

Oil Sands operations cash operating costs ($/bbl)(1) |

26.60 | 22.00 | 28.10 | 25.50 | ||||||

| | | | | | | | | | | |

Fort Hills cash operating costs(1) reconciliation |

||||||||||

| | ||||||||||

Fort Hills OS&G |

224 | 214 | 673 | 542 | ||||||

| | ||||||||||

Non-production costs(2) |

(23 | ) | (26 | ) | (95 | ) | (96 | ) | ||

| | ||||||||||

Inventory changes |

(10 | ) | 26 | 5 | 98 | |||||

| | | | | | | | | | | |

Fort Hills cash operating costs(1) |

191 | 214 | 583 | 543 | ||||||

| | ||||||||||

Fort Hills cash operating costs ($/bbl)(1) |

24.25 | 33.45 | 25.30 | 34.90 | ||||||

| | | | | | | | | | | |

Syncrude cash operating costs(1) reconciliation |

||||||||||

| | ||||||||||

Syncrude OS&G |

629 | 635 | 1 873 | 1 904 | ||||||

| | ||||||||||

Non-production costs(2) |

(24 | ) | (11 | ) | (62 | ) | (26 | ) | ||

| | | | | | | | | | | |

Syncrude cash operating costs(1) |

605 | 624 | 1 811 | 1 878 | ||||||

| | ||||||||||

Syncrude cash operating costs ($/bbl)(1) |

40.50 | 63.85 | 37.35 | 56.25 | ||||||

| | | | | | | | | | | |

- (1)

- Non-GAAP

financial measures. See the Non-GAAP Financial Measures Advisory section of this MD&A.

- (2)

- Significant

non-production costs include, but are not limited to, share-based compensation expense and research expenses. Non-production costs at Fort Hills also include, but are not

limited to, project startup costs, excess power revenue from cogeneration units and an adjustment to reflect internally produced diesel from Oil Sands operations at the cost of production.

- (3)

- Oil Sands operations excess power capacity and other includes, but is not limited to, the operational revenue impacts of excess power from a cogeneration unit and the natural gas expense recorded as part of a non-monetary arrangement involving a third-party processor.

Oil Sands operations cash operating costs(1) per barrel were $26.60 in the third quarter of 2019, compared to $22.00 in the prior year quarter, primarily as a result of the impact of the mandatory production curtailments and conscious changes in our production mix to maximize value, planned maintenance at Upgrader 2, which commenced late in the third quarter of 2019, and an increase in contractor mining costs. Total Oil Sands operations cash operating costs were $1.038 billion, compared to $969 million in the prior year quarter due to the same factors discussed above.

In the third quarter of 2019, non-production costs, which are excluded from Oil Sands operations cash operating costs, were higher than the prior year quarter, primarily due to an increase in research and development costs.

Fort Hills cash operating costs(1) per barrel averaged $24.25 in the third quarter of 2019, compared to $33.45 in the prior year quarter, reflecting the impact of higher production volumes in the current period and lower cash operating costs.

- (1)

- Non-GAAP financial measure. See the Non-GAAP Financial Measures Advisory section of this MD&A.

| 18 2019 THIRD QUARTER Suncor Energy Inc. | | |

Syncrude cash operating costs(1) per barrel were $40.50 in the third quarter of 2019, compared to $63.85 in the prior year quarter, with the decrease attributable to the increase in production noted above.

Results for the First Nine Months of 2019

Oil Sands net earnings were $2.255 billion for the first nine months of 2019, compared to $1.322 billion in the prior year period. In addition to the factors explained in operating earnings below, net earnings for the first nine months of 2019 included a one-time deferred income tax recovery of $910 million associated with a staged reduction to the Alberta corporate income tax rate of 1% each year from 2019 to 2022. Net earnings for the first nine months of 2018 included an after-tax gain on the sale of the company's interest in the Joslyn Oil Sands mining project of $60 million in the third quarter of 2018.

Oil Sands operating earnings(1) for the first nine months of 2019 were $1.345 billion, compared to $1.262 billion for the same period in 2018. Operating earnings improved as a result of increased production volumes, partially offset by an increase in operating, selling and general expenses, as detailed below. Production improved as a result of the ramp up of Fort Hills operations and higher production at Syncrude, partially offset by the impact of mandatory production curtailments in 2019. Both periods were impacted by planned upgrader maintenance.

Funds from operations(1) for the first nine months of 2019 were $4.656 billion for the Oil Sands segment, compared to $4.357 billion in the prior year period, with the increase primarily due to the same factors that influenced operating earnings noted above.

Oil Sands operations cash operating costs(1) per barrel averaged $28.10 for the first nine months of 2019, an increase from an average of $25.50 for the first nine months of 2018 due to the impact of mandatory production curtailments and conscious changes in our production mix to maximize value, and an increase in operating, selling and general expense related to higher contractor mining, commodity consumption, and maintenance costs.

Fort Hills cash operating costs(1) per barrel averaged $25.30 for the first nine months of 2019, compared to $34.90 for the same period of 2018, reflecting increased production, although production was limited by mandatory production curtailments.

Syncrude cash operating costs(1) per barrel averaged $37.35 for the first nine months of 2019, a decrease compared to $56.25 in the first nine months of 2018, due to an increase in production, although limited by mandatory production curtailments, with the prior year period impacted by a power disruption and extended planned maintenance, as well as a decrease in cash operating costs, which was primarily attributable to lower maintenance costs.

Planned Maintenance Update

Planned maintenance activity in the fourth quarter of 2019 includes maintenance events at Oil Sands operations Upgrader 2, Fort Hills and Syncrude. Planned maintenance at Fort Hills was completed subsequent to the third quarter. The impact of this maintenance is reflected in the company's 2019 guidance.

- (1)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this MD&A.

| | | 2019 THIRD QUARTER Suncor Energy Inc. 19 |

EXPLORATION AND PRODUCTION(1)

Financial Highlights

|

Three months ended September 30 |

Nine months ended September 30 |

||||||||

($ millions) |

2019 | 2018 | 2019 | 2018 | ||||||

| | | | | | | | | | | |

Gross revenues(2) |

681 | 875 | 2 461 | 2 823 | ||||||

| | ||||||||||

Less: Royalties(2) |

(32 | ) | (91 | ) | (219 | ) | (238 | ) | ||

| | | | | | | | | | | |

Operating revenues, net of royalties |

649 | 784 | 2 242 | 2 585 | ||||||

| | | | | | | | | | | |

Net earnings |

219 | 222 | 1 167 | 922 | ||||||

| | ||||||||||

Adjusted for: |

||||||||||

| | ||||||||||

Impact of income tax rate adjustment on deferred taxes(3) |

— | — | (70 | ) | — | |||||

| | ||||||||||

Gain on asset disposal(4) |

(48 | ) | — | (187 | ) | (133 | ) | |||

| | | | | | | | | | | |

Operating earnings(5) |

171 | 222 | 910 | 789 | ||||||

| | | | | | | | | | | |

Funds from operations(5) |

379 | 443 | 1 588 | 1 448 | ||||||

| | | | | | | | | | | |

- (1)

- The

three and nine months ended September 30, 2018 have been restated to reflect the change to the company's segmented presentation of its Energy Trading business, with no

impact to overall consolidated results. The Energy Trading business is now included within each of the respective operating business segments to which the respective trading activity relates. Suncor's

Energy Trading business was previously reported within the Corporate, Energy Trading and Eliminations segment.

- (2)

- Production,

revenues and royalties from the company's Libya operations have been presented in the E&P section of this MD&A on an entitlement basis and exclude an equal and offsetting

gross up of revenues and royalties of $65 million in the third quarter of 2019 and $74 million in the third quarter of 2018, which is required for presentation purposes in the company's

financial statements under the working-interest basis.

- (3)

- In

the second quarter of 2019, the company recorded a $70 million deferred income tax recovery in the E&P segment associated with the Government of Alberta's substantive

enactment of legislation for the staged reduction of the corporate income tax rate from 12% to 8% over the next four years.

- (4)

- The

third quarter of 2019 included an after-tax gain of $48 million in the E&P segment related to the sale of certain non-core assets. In the second quarter of 2019, Suncor

sold its 37% interest in Canbriam for total proceeds and an equivalent gain of $151 million ($139 million after-tax), which had previously been written down to nil in the fourth quarter

of 2018 following the company's assessment of forward natural gas prices and the impact on estimated future cash flows.

- (5)

- Non-GAAP financial measures. See the Non-GAAP Financial Measures Advisory section of this MD&A.

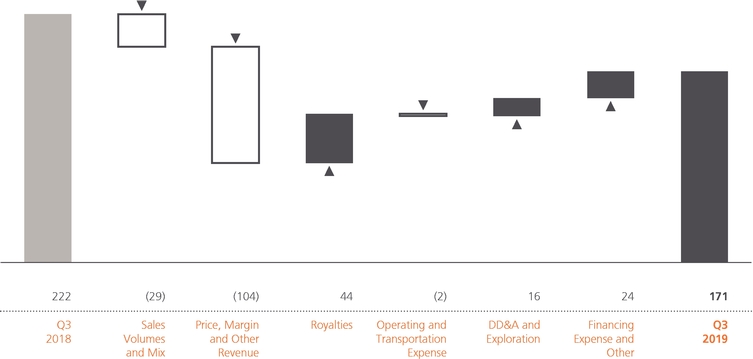

Bridge Analysis of Operating Earnings ($ millions)(1)

- (1)