UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-02192 | |||||

| BNY Mellon Sustainable U.S. Equity Fund, Inc. | ||||||

| (Exact name of Registrant as specified in charter) | ||||||

|

c/o BNY Mellon Investment Adviser, Inc. 240 Greenwich Street New York, New York 10286 |

||||||

| (Address of principal executive offices) (Zip code) | ||||||

|

Deirdre Cunnane, Esq. 240 Greenwich Street New York, New York 10286 |

||||||

| (Name and address of agent for service) | ||||||

| Registrant's telephone number, including area code: | (212) 922-6400 | |||||

|

Date of fiscal year end:

|

05/31 | |||||

| Date of reporting period: |

05/31/2023

|

|||||

FORM N-CSR

Item 1. Reports to Stockholders.

BNY Mellon Sustainable U.S. Equity Fund, Inc.

ANNUAL REPORT May 31, 2023 |

|

Save time. Save paper. View your next shareholder report online as soon as it’s available. Log into www.im.bnymellon.com and sign up for eCommunications. It’s simple and only takes a few minutes. |

The views expressed in this report reflect those of the portfolio manager(s) only through the end of the period covered and do not necessarily represent the views of BNY Mellon Investment Adviser, Inc. or any other person in the BNY Mellon Investment Adviser, Inc. organization. Any such views are subject to change at any time based upon market or other conditions and BNY Mellon Investment Adviser, Inc. disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for a fund in the BNY Mellon Family of Funds are based on numerous factors, may not be relied on as an indication of trading intent on behalf of any fund in the BNY Mellon Family of Funds. |

Not FDIC-Insured • Not Bank-Guaranteed • May Lose Value |

Contents

THE FUND

Information About the Approval of | |

FOR MORE INFORMATION

Back Cover

DISCUSSION OF FUND PERFORMANCE (Unaudited)

For the period from June 1, 2022, through May 31, 2023, as provided by portfolio manager Nick Pope of Newton Investment Management Limited (NIM), sub-adviser

Market and Fund Performance Overview

For the 12-month period ended May 31, 2023, the BNY Mellon Sustainable U.S. Equity Fund Inc. (the “fund”) produced a total return of .38% for Class A shares, −.34% for Class C shares, ..62% for Class I shares, .66% for Class Y shares and .58% for Class Z shares.1 In comparison, the fund’s benchmark, the S&P 500® Index (the “Index”), provided a total return of 2.93% for the same period.2

U.S. stocks gained ground during the reporting period as inflationary pressures eased, the U.S. Federal Reserve (the “Fed”) reduced the pace of interest-rate hikes, and economic growth remained positive. The fund underperformed the Index largely due to the fund’s positioning in the financials, materials, communication services and information technology sectors.

The Fund’s Investment Approach

The fund seeks long-term capital appreciation. To pursue its goal, the fund normally invests at least 80% of its net assets, plus any borrowings for investment purposes, in equity securities of U.S. companies that demonstrate attractive investment attributes with sustainable business practices and have no material unresolvable environmental, social and governance (ESG) issues. The fund invests principally in common stocks.

The fund may invest in the stocks of companies with any market capitalization but focuses on companies with market capitalizations of $5 billion or more at the time of purchase. The fund may invest up to 20% of its assets in the stock of foreign companies, including up to 10% in the securities of issuers in emerging-market countries, that demonstrate attractive investment attributes and sustainable business practices and have no material unresolvable ESG issues.

NIM seeks attractively priced companies (determined using both quantitative and qualitative fundamental analysis) with good products or services, strong management and strategic direction that have adopted, or are making progress toward, a sustainable business approach. These are companies that NIM believes should benefit from favorable long-term trends. NIM uses an investment process that combines investment themes with fundamental research and analysis to select stocks for the fund’s portfolio.

Equities Advance Despite Macroeconomic Concerns

Concerns regarding a shift in global monetary policy weighed on U.S. equities at the start of the reporting period, with stretched valuations a cause for concern in the face of hawkish central banks. Renewed COVID-19-related lockdowns in China also weighed on investor sentiment, given the negative implications for economic growth and supply chains. Investor hopes of a ‘pivot’ by the U.S. Federal Reserve (the “Fed”) on the interest-rate trajectory were dashed as it became increasingly clear that the central bank’s priority was to quash inflation rather than support the economy and financial asset prices.

2

At the start of 2023, share prices were lifted by positive sentiment regarding China’s reopening after the swift abandonment of its “zero-Covid-19” policy. However, as the year progressed, several issues took a toll on sentiment. January’s U.S. inflation numbers came in higher than expected, while headline employment data was also very robust, prompting the Fed to maintain its hawkish rhetoric. A reescalation of U.S.-China tensions put further pressure on risk assets. Another major challenge arose in early March, as signs of stress emerged within the U.S. banking sector, raising persistent concerns regarding U.S. regional banks. The U.S. debt ceiling impasse represented yet another temporary headwind for a period. Nevertheless, markets generally gained ground from mid-March through the end of the period as inflation moderated, and investors anticipated the cessation of interest-rate increases, while hoping the economy would avoid a major recession.

Several Sectors Detract from Relative Returns

Stock selection undermined the fund’s returns relative to the Index in the financials, materials, communication services and information technology sectors, with financials the most notable detractor by far. Despite regulatory intervention to stabilize the U.S. banking system in response to the collapse of Silicon Valley Bank and closure of Signature Bank, First Republic Bank shares came under significant pressure amid concerns regarding its ability to withstand continued deposit outflows. The negative impact of holdings in First Republic Bank alone accounted for a significant portion of the fund’s underperformance during the period. We moved swiftly to sell the fund’s position given a lack of clarity as to whether the bank would remain liquid amid a crisis of confidence in the regional banking sector. Another financial sector holding, Fidelity National Information Services, was also caught up in broader concerns around the health of the financial sector, with declines in the company’s stock exacerbated by a series of underwhelming earnings reports. After Fidelity announced plans to spin off its merchant solutions business, we gradually exited the fund’s position as it became apparent there would be a slower deleveraging than we had earlier anticipated.

More positively, lack of exposure to the energy and real estate sectors enhanced the fund’s relative performance, as did an overweight position in information technology. Positive stock selection further bolstered returns in industrials, consumer staples and health care. Pharmaceutical company Eli Lilly & Co. performed notably strongly, driven by positive news regarding its treatments for obesity and Alzheimer’s. Building products and services provider Trane Technologies PLC, a business for which the long-term outlook continues to be supported by decarbonization and energy efficiency trends, also emerged as one of the portfolio’s top contributors.

Remaining Focused on Sustainable and Resilient Businesses

The immediate path for interest rates remains the primary source of investor debate. While inflation remains elevated, tighter monetary policy has further scope to test the fragility of the financial system. As the economy adjusts to the effects of higher bond yields, liquidity and credit availability may face increased pressure. We believe markets are therefore likely to remain volatile over the short term, as the economy works through the consequences of the higher-yield environment.

In the face of these challenges, we remain focused on companies that our multi-dimensional research process identifies as having attractive sustainability credentials, durable returns and quality characteristics. As of May 31, 2023, the fund continues to hold its largest overweight

3

DISCUSSION OF FUND PERFORMANCE (Unaudited) (continued)

position in information technology, where several holdings have recently benefited from AI-driven momentum. We believe that the sector’s strong focus on providing innovation and solutions to global sustainability challenges creates a rich environment in which to find attractive long-term investments. The fund also continues to avoid the energy sector, where many companies feature business models inconsistent with a sustainable mandate, and largely incompatible with our focus on finding investments that are aligned with the transition to a lower carbon world. The fund also holds underweight exposure to the consumer discretionary sector, reflecting likely headwinds for the consumer due to rising borrowing costs and inflation. Lastly, lack of exposure to sizeable Index constituent Meta Platforms drives the fund’s underweight position in communication services.

June 15, 2023

1 Total return includes reinvestment of dividends and any capital gains paid and does not take into consideration the maximum initial sales charge in the case of Class A shares, or the applicable contingent deferred sales charges imposed on redemptions in the case of Class C shares. Had these charges been reflected, returns would have been lower. Past performance is no guarantee of future results. Share price and investment return fluctuate such that upon redemption, fund shares may be worth more or less than their original cost. The fund’s return reflects the absorption of certain fund expenses by BNY Mellon Investment Adviser, Inc. pursuant to an agreement in effect through September 30, 2023, at which time it may be extended, modified or terminated. Had these expenses not been absorbed, returns would have been lower.

2 Source: Lipper Inc. — The S&P 500® Index is widely regarded as the best single gauge of large-cap U.S. equities. The Index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. Investors cannot invest directly in any index.

Please note: the position in any security highlighted with italicized typeface was sold during the reporting period.

Equities are subject generally to market, market sector, market liquidity, issuer and investment style risks, among other factors, to varying degrees, all of which are more fully described in the fund’s prospectus.

Small and midsized company stocks tend to be more volatile and less liquid than larger company stocks as these companies are less established and have more volatile earnings histories.

Socially responsible portfolios can limit the number of investment opportunities available to the portfolio which may produce more modest gains than portfolios that are not subject to such special investment considerations.

Environmental, social and governance (ESG) managers may take into consideration factors beyond traditional financial information to select securities, which could result in relative investment performance deviating from other strategies or broad market benchmarks, depending on whether such sectors or investments are in or out of favor in the market. Further, ESG strategies may rely on certain values-based criteria to eliminate exposures found in similar strategies or broad market benchmarks, which could also result in relative investment performance deviating.

4

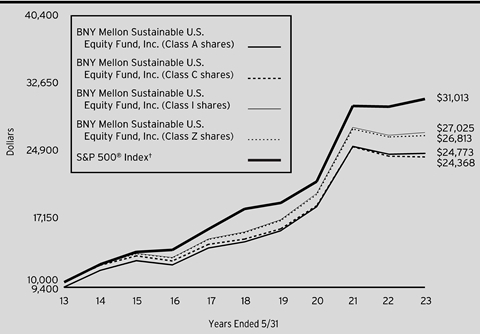

FUND PERFORMANCE (Unaudited)

Comparison of change in value of a $10,000 investment in Class A shares, Class C shares, Class I shares and Class Z shares of BNY Mellon Sustainable U.S. Equity Fund, Inc. with a hypothetical investment of $10,000 in the S&P 500® Index (the “Index”).

† Source: Lipper Inc.

Past performance is not predictive of future performance.

The above graph compares a hypothetical $10,000 investment made in Class A shares, Class C shares, Class I shares and Class Z shares of BNY Mellon Sustainable U.S. Equity Fund, Inc. on 5/31/13 to a hypothetical investment of $10,000 made in the Index on that date. All dividends and capital gain distributions are reinvested.

The fund’s performance shown in the line graph above takes into account the maximum initial sales charge on Class A shares and all other applicable fees and expenses on all classes. The Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

5

FUND PERFORMANCE (Unaudited) (continued)

Comparison of change in value of a $1,000,000 investment in Class Y shares of BNY Mellon Sustainable U.S. Equity Fund, Inc. with a hypothetical investment of $1,000,000 in the S&P 500® Index (the “Index”).

† Source: Lipper Inc.

†† The total return figures presented for Class Y shares of the fund reflect the performance of the fund’s Class Z shares for the period prior to 9/30/16 (the inception date for Class Y shares).

Past performance is not predictive of future performance.

The above graph compares a hypothetical $1,000,000 investment made in Class Y shares of BNY Mellon Sustainable U.S. Equity Fund, Inc. on 5/31/13 to a hypothetical investment of $1,000,000 made in the Index on that date. All dividends and capital gain distributions are reinvested

The fund’s performance shown in the line graph above takes into account all applicable fees and expenses of the fund’s Class Y shares. The Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and captures approximately 80% coverage of available market capitalization. Unlike a mutual fund, the Index is not subject to charges, fees and other expenses. Investors cannot invest directly in any index. Further information relating to fund performance, including expense reimbursements, if applicable, is contained in the Financial Highlights section of the prospectus and elsewhere in this report.

6

Average Annual Total Returns as of 5/31/2023 | ||||

| Inception | 1 Year | 5 Years | 10 Years |

Class A shares | ||||

with maximum sales charge (5.75%) | 8/31/99 | -5.41% | 9.80% | 9.50% |

without sales charge | 8/31/99 | .38% | 11.12% | 10.15% |

Class C shares | ||||

with applicable redemption charge † | 8/31/99 | -1.21% | 10.28% | 9.32% |

without redemption | 8/31/99 | -.34% | 10.28% | 9.32% |

Class I shares | 8/31/99 | .62% | 11.39% | 10.45% |

Class Y shares | 9/30/16 | .66% | 11.40% | 10.42%†† |

Class Z shares | 3/29/72 | .58% | 11.33% | 10.37% |

S&P 500® Index | 2.93% | 11.01% | 11.98% | |

† The maximum contingent deferred sales charge for Class C shares is 1% for shares redeemed within one year of the date of purchase.

†† The total return performance figures presented for Class Y shares of the fund reflect the performance of the fund’s Class Z shares for the period prior to 9/30/16 (the inception date for Class Y shares).

The performance data quoted represents past performance, which is no guarantee of future results. Share price and investment return fluctuate and an investor’s shares may be worth more or less than original cost upon redemption. Current performance may be lower or higher than the performance quoted. Go to www.im.bnymellon.com for the fund’s most recent month-end returns.

The fund’s performance shown in the graphs and table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. In addition to the performance of Class A shares shown with and without a maximum sales charge, the fund’s performance shown in the table takes into account all other applicable fees and expenses on all classes.

7

UNDERSTANDING YOUR FUND’S EXPENSES (Unaudited)

As a mutual fund investor, you pay ongoing expenses, such as management fees and other expenses. Using the information below, you can estimate how these expenses affect your investment and compare them with the expenses of other funds. You also may pay one-time transaction expenses, including sales charges (loads) and redemption fees, which are not shown in this section and would have resulted in higher total expenses. For more information, see your fund’s prospectus or talk to your financial adviser.

Review your fund’s expenses

The table below shows the expenses you would have paid on a $1,000 investment in BNY Mellon Sustainable U.S. Equity Fund, Inc. from December 1, 2022 to May 31, 2023. It also shows how much a $1,000 investment would be worth at the close of the period, assuming actual returns and expenses.

Expenses and Value of a $1,000 Investment |

| ||||||

Assume actual returns for the six months ended May 31, 2023 |

| ||||||

|

|

|

|

|

|

|

|

|

| Class A | Class C | Class I | Class Y | Class Z |

|

Expenses paid per $1,000† | $4.74 | $8.50 | $3.48 | $3.48 | $3.78 |

| |

Ending value (after expenses) | $1,021.60 | $1,018.10 | $1,023.00 | $1,023.30 | $1,023.10 |

| |

COMPARING YOUR FUND’S EXPENSES WITH THOSE OF OTHER FUNDS (Unaudited)

Using the SEC’s method to compare expenses

The Securities and Exchange Commission (“SEC”) has established guidelines to help investors assess fund expenses. Per these guidelines, the table below shows your fund’s expenses based on a $1,000 investment, assuming a hypothetical 5% annualized return. You can use this information to compare the ongoing expenses (but not transaction expenses or total cost) of investing in the fund with those of other funds. All mutual fund shareholder reports will provide this information to help you make this comparison. Please note that you cannot use this information to estimate your actual ending account balance and expenses paid during the period.

Expenses and Value of a $1,000 Investment |

| ||||||

Assuming a hypothetical 5% annualized return for the six months ended May 31, 2023 |

| ||||||

|

|

|

|

|

|

|

|

|

| Class A | Class C | Class I | Class Y | Class Z |

|

Expenses paid per $1,000† | $4.73 | $8.50 | $3.48 | $3.48 | $3.78 |

| |

Ending value (after expenses) | $1,020.24 | $1,016.50 | $1,021.49 | $1,021.49 | $1,021.19 |

| |

† | Expenses are equal to the fund’s annualized expense ratio of .94% for Class A, 1.69% for Class C, .69% for Class I, .69% for Class Y and .75% for Class Z, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). | ||||||

8

STATEMENT OF INVESTMENTS

May 31, 2023

Description | Shares | Value ($) | |||||

Common Stocks - 98.2% | |||||||

Banks - 2.9% | |||||||

JPMorgan Chase & Co. | 82,032 | 11,132,563 | |||||

Capital Goods - 3.6% | |||||||

Ingersoll Rand, Inc. | 130,531 | 7,395,886 | |||||

Trane Technologies PLC | 38,448 | 6,275,867 | |||||

13,671,753 | |||||||

Commercial & Professional Services - 1.7% | |||||||

Waste Management, Inc. | 40,974 | 6,634,510 | |||||

Consumer Discretionary Distribution & Retail - 5.1% | |||||||

Amazon.com, Inc. | 163,509 | a | 19,715,915 | ||||

Consumer Durables & Apparel - 2.5% | |||||||

NIKE, Inc., Cl. B | 91,199 | 9,599,607 | |||||

Consumer Staples Distribution - 2.8% | |||||||

Costco Wholesale Corp. | 20,798 | 10,639,425 | |||||

Financial Services - 5.5% | |||||||

Mastercard, Inc., Cl. A | 34,437 | 12,570,194 | |||||

The Goldman Sachs Group, Inc. | 27,099 | 8,777,366 | |||||

21,347,560 | |||||||

Food, Beverage & Tobacco - 4.6% | |||||||

Darling Ingredients, Inc. | 100,010 | a | 6,338,634 | ||||

PepsiCo, Inc. | 63,237 | 11,531,267 | |||||

17,869,901 | |||||||

Health Care Equipment & Services - 6.5% | |||||||

Boston Scientific Corp. | 179,772 | a | 9,254,663 | ||||

Edwards Lifesciences Corp. | 91,209 | a | 7,682,534 | ||||

The Cooper Companies, Inc. | 22,278 | 8,276,945 | |||||

25,214,142 | |||||||

Insurance - 4.2% | |||||||

Chubb Ltd. | 40,978 | 7,613,712 | |||||

The Progressive Corp. | 66,555 | 8,513,050 | |||||

16,126,762 | |||||||

Materials - 3.8% | |||||||

Albemarle Corp. | 30,649 | 5,931,501 | |||||

CF Industries Holdings, Inc. | 61,880 | 3,806,239 | |||||

Ecolab, Inc. | 29,123 | 4,806,751 | |||||

14,544,491 | |||||||

Media & Entertainment - 4.8% | |||||||

Alphabet, Inc., Cl. A | 151,411 | a | 18,603,870 | ||||

Pharmaceuticals, Biotechnology & Life Sciences - 9.7% | |||||||

AbbVie, Inc. | 67,508 | 9,313,404 | |||||

Danaher Corp. | 40,720 | 9,350,126 | |||||

Eli Lilly & Co. | 30,278 | 13,003,190 | |||||

9

STATEMENT OF INVESTMENTS (continued)

Description | Shares | Value ($) | |||||

Common Stocks - 98.2% (continued) | |||||||

Pharmaceuticals, Biotechnology & Life Sciences - 9.7% (continued) | |||||||

Merck & Co., Inc. | 51,737 | 5,712,282 | |||||

37,379,002 | |||||||

Semiconductors & Semiconductor Equipment - 7.8% | |||||||

Applied Materials, Inc. | 39,726 | 5,295,476 | |||||

NVIDIA Corp. | 29,766 | 11,261,668 | |||||

SolarEdge Technologies, Inc. | 18,795 | a | 5,353,380 | ||||

Texas Instruments, Inc. | 46,761 | 8,130,803 | |||||

30,041,327 | |||||||

Software & Services - 18.1% | |||||||

Accenture PLC, Cl. A | 33,645 | 10,292,678 | |||||

Ansys, Inc. | 12,113 | a | 3,919,646 | ||||

Intuit, Inc. | 24,945 | 10,454,948 | |||||

Microsoft Corp. | 87,178 | 28,628,383 | |||||

Roper Technologies, Inc. | 17,131 | 7,781,243 | |||||

Salesforce, Inc. | 39,234 | a | 8,764,091 | ||||

69,840,989 | |||||||

Technology Hardware & Equipment - 9.1% | |||||||

Apple, Inc. | 162,176 | 28,745,696 | |||||

TE Connectivity Ltd. | 51,471 | 6,304,168 | |||||

35,049,864 | |||||||

Transportation - 1.7% | |||||||

Norfolk Southern Corp. | 31,443 | 6,545,804 | |||||

Utilities - 3.8% | |||||||

CMS Energy Corp. | 112,724 | 6,535,738 | |||||

NextEra Energy, Inc. | 112,241 | 8,245,224 | |||||

14,780,962 | |||||||

Total Common Stocks (cost $265,557,392) | 378,738,447 | ||||||

1-Day | |||||||

Investment Companies - 1.8% | |||||||

Registered Investment Companies - 1.8% | |||||||

Dreyfus

Institutional Preferred Government Plus Money Market Fund, Institutional Shares | 5.19 | 6,872,055 | b | 6,872,055 | |||

Total Investments (cost $272,429,447) | 100.0% | 385,610,502 | |||||

Liabilities, Less Cash and Receivables | (.0%) | (38,842) | |||||

Net Assets | 100.0% | 385,571,660 | |||||

a Non-income producing security.

b Investment in affiliated issuer. The investment objective of this investment company is publicly available and can be found within the investment company’s prospectus.

10

Portfolio Summary (Unaudited) † | Value (%) |

Information Technology | 35.0 |

Health Care | 16.2 |

Financials | 12.6 |

Consumer Discretionary | 7.6 |

Consumer Staples | 7.4 |

Industrials | 7.0 |

Communication Services | 4.8 |

Utilities | 3.8 |

Materials | 3.8 |

Investment Companies | 1.8 |

100.0 |

† Based on net assets.

See notes to financial statements.

Affiliated Issuers | ||||||

Description | Value ($) 5/31/2022 | Purchases ($)† | Sales ($) | Value ($) 5/31/2023 | Dividends/ | |

Registered Investment Companies - 1.8% | ||||||

Dreyfus Institutional Preferred Government Plus Money Market Fund, Institutional Shares - 1.8% | 4,726,372 | 61,665,601 | (59,519,918) | 6,872,055 | 149,766 | |

† Includes reinvested dividends/distributions.

See notes to financial statements.

11

STATEMENT OF ASSETS AND LIABILITIES

May 31, 2023

|

|

|

|

|

|

|

|

|

| Cost |

| Value |

|

Assets ($): |

|

|

|

| ||

Investments in securities—See Statement of Investments |

|

|

| |||

Unaffiliated issuers | 265,557,392 |

| 378,738,447 |

| ||

Affiliated issuers |

| 6,872,055 |

| 6,872,055 |

| |

Dividends receivable |

| 279,406 |

| |||

Receivable for shares of Common Stock subscribed |

| 1,980 |

| |||

Prepaid expenses |

|

|

|

| 35,771 |

|

|

|

|

|

| 385,927,659 |

|

Liabilities ($): |

|

|

|

| ||

Due to BNY Mellon Investment Adviser, Inc. and affiliates—Note 3(c) |

| 247,229 |

| |||

Directors’ fees and expenses payable |

| 7,040 |

| |||

Payable for shares of Common Stock redeemed |

| 6,112 |

| |||

Other accrued expenses |

|

|

|

| 95,618 |

|

|

|

|

|

| 355,999 |

|

Net Assets ($) |

|

| 385,571,660 |

| ||

Composition of Net Assets ($): |

|

|

|

| ||

Paid-in capital |

|

|

|

| 258,979,430 |

|

Total distributable earnings (loss) |

|

|

|

| 126,592,230 |

|

Net Assets ($) |

|

| 385,571,660 |

| ||

Net Asset Value Per Share | Class A | Class C | Class I | Class Y | Class Z |

|

Net Assets ($) | 28,629,247 | 1,279,777 | 40,185,113 | 296,294 | 315,181,229 |

|

Shares Outstanding | 2,003,003 | 111,377 | 2,724,581 | 19,969 | 21,286,609 |

|

Net Asset Value Per Share ($) | 14.29 | 11.49 | 14.75 | 14.84 | 14.81 |

|

|

|

|

|

|

|

|

See notes to financial statements. |

|

|

|

|

|

|

12

STATEMENT OF OPERATIONS

Year Ended May 31, 2023

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Investment Income ($): |

|

|

|

| ||

Income: |

|

|

|

| ||

Cash dividends: |

| |||||

Unaffiliated issuers |

|

| 5,801,834 |

| ||

Affiliated issuers |

|

| 149,766 |

| ||

Interest |

|

| 18 |

| ||

Total Income |

|

| 5,951,618 |

| ||

Expenses: |

|

|

|

| ||

Management fee—Note 3(a) |

|

| 2,467,478 |

| ||

Shareholder servicing costs—Note 3(c) |

|

| 428,497 |

| ||

Professional fees |

|

| 102,498 |

| ||

Registration fees |

|

| 84,304 |

| ||

Prospectus and shareholders’ reports |

|

| 30,569 |

| ||

Directors’ fees and expenses—Note 3(d) |

|

| 21,101 |

| ||

Chief Compliance Officer fees—Note 3(c) |

|

| 19,799 |

| ||

Loan commitment fees—Note 2 |

|

| 10,624 |

| ||

Interest expense—Note 2 |

|

| 9,885 |

| ||

Distribution fees—Note 3(b) |

|

| 9,872 |

| ||

Custodian fees—Note 3(c) |

|

| 9,057 |

| ||

Miscellaneous |

|

| 24,599 |

| ||

Total Expenses |

|

| 3,218,283 |

| ||

Less—reduction in expenses due to undertaking—Note 3(a) |

|

| (51,281) |

| ||

Less—reduction in fees due to earnings credits—Note 3(c) |

|

| (38,383) |

| ||

Net Expenses |

|

| 3,128,619 |

| ||

Net Investment Income |

|

| 2,822,999 |

| ||

Realized and Unrealized Gain (Loss) on Investments—Note 4 ($): |

|

| ||||

Net realized gain (loss) on investments | 11,224,893 |

| ||||

Net change in unrealized appreciation (depreciation) on investments | (15,838,502) |

| ||||

Net Realized and Unrealized Gain (Loss) on Investments |

|

| (4,613,609) |

| ||

Net (Decrease) in Net Assets Resulting from Operations |

| (1,790,610) |

| |||

|

|

|

|

|

|

|

See notes to financial statements. | ||||||

13

STATEMENT OF CHANGES IN NET ASSETS

|

|

|

| Year Ended May 31, | |||||

|

|

|

| 2023 |

| 2022 |

| ||

Operations ($): |

|

|

|

|

|

|

|

| |

Net investment income |

|

| 2,822,999 |

|

|

| 2,210,241 |

| |

Net realized gain (loss) on investments |

| 11,224,893 |

|

|

| 46,412,997 |

| ||

Net

change in unrealized appreciation |

| (15,838,502) |

|

|

| (64,520,226) |

| ||

Net Increase

(Decrease) in Net Assets | (1,790,610) |

|

|

| (15,896,988) |

| |||

Distributions ($): |

| ||||||||

Distributions to shareholders: |

|

|

|

|

|

|

|

| |

Class A |

|

| (3,314,816) |

|

|

| (1,944,917) |

| |

Class C |

|

| (174,085) |

|

|

| (98,875) |

| |

Class I |

|

| (5,805,754) |

|

|

| (3,745,422) |

| |

Class Y |

|

| (2,036,728) |

|

|

| (1,317,100) |

| |

Class Z |

|

| (34,900,087) |

|

|

| (16,641,833) |

| |

Total Distributions |

|

| (46,231,470) |

|

|

| (23,748,147) |

| |

Capital Stock Transactions ($): |

| ||||||||

Net proceeds from shares sold: |

|

|

|

|

|

|

|

| |

Class A |

|

| 2,372,291 |

|

|

| 4,540,146 |

| |

Class C |

|

| 47,264 |

|

|

| 483,490 |

| |

Class I |

|

| 7,678,632 |

|

|

| 35,125,537 |

| |

Class Y |

|

| 4,114 |

|

|

| 404,208 |

| |

Class Z |

|

| 987,378 |

|

|

| 1,769,435 |

| |

Distributions reinvested: |

|

|

|

|

|

|

|

| |

Class A |

|

| 3,079,411 |

|

|

| 1,809,471 |

| |

Class C |

|

| 174,085 |

|

|

| 98,875 |

| |

Class I |

|

| 3,622,106 |

|

|

| 2,547,395 |

| |

Class Y |

|

| 1,977,367 |

|

|

| 1,279,161 |

| |

Class Z |

|

| 33,188,729 |

|

|

| 15,829,791 |

| |

Cost of shares redeemed: |

|

|

|

|

|

|

|

| |

Class A |

|

| (8,037,283) |

|

|

| (12,833,302) |

| |

Class C |

|

| (444,216) |

|

|

| (435,024) |

| |

Class I |

|

| (41,051,620) |

|

|

| (21,209,432) |

| |

Class Y |

|

| (18,142,839) |

|

|

| (8,387,316) |

| |

Class Z |

|

| (21,988,363) |

|

|

| (19,406,058) |

| |

Increase

(Decrease) in Net Assets | (36,532,944) |

|

|

| 1,616,377 |

| |||

Total Increase (Decrease) in Net Assets | (84,555,024) |

|

|

| (38,028,758) |

| |||

Net Assets ($): |

| ||||||||

Beginning of Period |

|

| 470,126,684 |

|

|

| 508,155,442 |

| |

End of Period |

|

| 385,571,660 |

|

|

| 470,126,684 |

| |

14

|

|

|

| Year Ended May 31, | |||||

|

|

|

| 2023 |

| 2022 |

| ||

Capital Share Transactions (Shares): |

| ||||||||

Class A |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 165,418 |

|

|

| 250,173 |

| |

Shares issued for distributions reinvested |

|

| 225,930 |

|

|

| 96,812 |

| |

Shares redeemed |

|

| (552,346) |

|

|

| (718,554) |

| |

Net Increase (Decrease) in Shares Outstanding | (160,998) |

|

|

| (371,569) |

| |||

Class C |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 4,121 |

|

|

| 30,302 |

| |

Shares issued for distributions reinvested |

|

| 15,826 |

|

|

| 6,358 |

| |

Shares redeemed |

|

| (35,892) |

|

|

| (28,931) |

| |

Net Increase (Decrease) in Shares Outstanding | (15,945) |

|

|

| 7,729 |

| |||

Class Ia,b |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 512,805 |

|

|

| 1,872,113 |

| |

Shares issued for distributions reinvested |

|

| 257,801 |

|

|

| 132,539 |

| |

Shares redeemed |

|

| (2,740,494) |

|

|

| (1,169,321) |

| |

Net Increase (Decrease) in Shares Outstanding | (1,969,888) |

|

|

| 835,331 |

| |||

Class Yb |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 279 |

|

|

| 20,739 |

| |

Shares issued for distributions reinvested |

|

| 139,842 |

|

|

| 66,175 |

| |

Shares redeemed |

|

| (1,277,145) |

|

|

| (488,033) |

| |

Net Increase (Decrease) in Shares Outstanding | (1,137,024) |

|

|

| (401,119) |

| |||

Class Za |

|

|

|

|

|

|

|

| |

Shares sold |

|

| 66,939 |

|

|

| 93,960 |

| |

Shares issued for distributions reinvested |

|

| 2,352,142 |

|

|

| 820,621 |

| |

Shares redeemed |

|

| (1,494,712) |

|

|

| (1,043,376) |

| |

Net Increase (Decrease) in Shares Outstanding | 924,369 |

|

|

| (128,795) |

| |||

|

|

|

|

|

|

|

|

|

|

a | During the period ended May 31, 2023, 6,239 Class Z shares representing $97,703 were exchanged for 6,263 Class I shares. | ||||||||

b | During the period ended May 31, 2023, 16,697 Class Y shares representing $232,667 were exchanged for 16,803 Class I shares and during the period ended May 31, 2022, 4,909 Class Y shares representing $72,747 were exchanged for 4,941 Class I shares. | ||||||||

See notes to financial statements. | |||||||||

15

FINANCIAL HIGHLIGHTS

The following tables describe the performance for each share class for the fiscal periods indicated. All information (except portfolio turnover rate) reflects financial results for a single fund share. Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all dividends and distributions at net asset value during the period, and redemption at net asset value on the last day of the period. Net asset value total return includes adjustments in accordance with accounting principles generally accepted in the United States of America and as such, the net asset value for financial reporting purposes and the returns based upon those net asset values may differ from the net asset value and returns for shareholder transactions. These figures have been derived from the fund’s financial statements.

Class A Shares | Year Ended May 31, | ||||||

2023 | 2022 | 2021 | 2020 | 2019 | |||

Per Share Data ($): | |||||||

Net asset value, beginning of period | 16.02 | 17.31 | 13.04 | 11.39 | 10.94 | ||

Investment Operations: | |||||||

Net investment incomea | .07 | .04 | .09 | .10 | .13 | ||

Net

realized and unrealized | (.09) | (.53) | 4.67 | 1.89 | .80 | ||

Total from Investment Operations | (.02) | (.49) | 4.76 | 1.99 | .93 | ||

Distributions: | |||||||

Dividends

from | (.04) | (.08) | (.10) | (.18) | (.18) | ||

Dividends

from net realized | (1.67) | (.72) | (.39) | (.16) | (.30) | ||

Total Distributions | (1.71) | (.80) | (.49) | (.34) | (.48) | ||

Net asset value, end of period | 14.29 | 16.02 | 17.31 | 13.04 | 11.39 | ||

Total Return (%)b | .38 | (3.50) | 37.09 | 17.40 | 8.66 | ||

Ratios/Supplemental Data (%): | |||||||

Ratio

of total expenses | 1.01 | .97 | .99 | 1.02 | 1.04 | ||

Ratio

of net expenses | .95 | .95 | .95 | .95 | .95 | ||

Ratio

of net investment income | .50 | .21 | .57 | .80 | 1.11 | ||

Portfolio Turnover Rate | 21.98 | 24.86 | 30.42 | 36.37 | 39.66 | ||

Net Assets, end of period ($ x 1,000) | 28,629 | 34,673 | 43,901 | 31,351 | 24,150 | ||

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

16

Class C Shares | Year Ended May 31, | ||||||

2023 | 2022 | 2021 | 2020 | 2019 | |||

Per Share Data ($): | |||||||

Net asset value, beginning of period | 13.28 | 14.51 | 10.99 | 9.60 | 9.26 | ||

Investment Operations: | |||||||

Net investment income (loss)a | (.03) | (.08) | (.02) | .01 | .04 | ||

Net

realized and unrealized | (.09) | (.43) | 3.93 | 1.58 | .67 | ||

Total from Investment Operations | (.12) | (.51) | 3.91 | 1.59 | .71 | ||

Distributions: | |||||||

Dividends

from | - | - | - | (.04) | (.07) | ||

Dividends

from net realized | (1.67) | (.72) | (.39) | (.16) | (.30) | ||

Total Distributions | (1.67) | (.72) | (.39) | (.20) | (.37) | ||

Net asset value, end of period | 11.49 | 13.28 | 14.51 | 10.99 | 9.60 | ||

Total Return (%)b | (.34) | (4.23) | 35.98 | 16.58 | 7.80 | ||

Ratios/Supplemental Data (%): | |||||||

Ratio

of total expenses | 1.87 | 1.80 | 1.83 | 1.82 | 1.81 | ||

Ratio

of net expenses | 1.70 | 1.70 | 1.70 | 1.70 | 1.70 | ||

Ratio

of net investment income (loss) | (.25) | (.54) | (.16) | .07 | .37 | ||

Portfolio Turnover Rate | 21.98 | 24.86 | 30.42 | 36.37 | 39.66 | ||

Net Assets, end of period ($ x 1,000) | 1,280 | 1,691 | 1,736 | 2,351 | 2,898 | ||

a Based on average shares outstanding.

b Exclusive of sales charge.

See notes to financial statements.

17

FINANCIAL HIGHLIGHTS (continued)

Class I Shares | Year Ended May 31, | ||||||

2023 | 2022 | 2021 | 2020 | 2019 | |||

Per Share Data ($): | |||||||

Net asset value, beginning of period | 16.50 | 17.80 | 13.38 | 11.68 | 11.22 | ||

Investment Operations: | |||||||

Net investment incomea | .11 | .09 | .13 | .14 | .16 | ||

Net

realized and unrealized | (.10) | (.55) | 4.81 | 1.94 | .80 | ||

Total from Investment Operations | .01 | (.46) | 4.94 | 2.08 | .96 | ||

Distributions: | |||||||

Dividends

from | (.09) | (.12) | (.13) | (.22) | (.20) | ||

Dividends

from net realized | (1.67) | (.72) | (.39) | (.16) | (.30) | ||

Total Distributions | (1.76) | (.84) | (.52) | (.38) | (.50) | ||

Net asset value, end of period | 14.75 | 16.50 | 17.80 | 13.38 | 11.68 | ||

Total Return (%) | .62 | (3.26) | 37.43 | 17.72 | 8.89 | ||

Ratios/Supplemental Data (%): | |||||||

Ratio

of total expenses | .73 | .70 | .72 | .72 | .74 | ||

Ratio

of net expenses | .70 | .70 | .70 | .70 | .70 | ||

Ratio

of net investment income | .75 | .47 | .81 | 1.04 | 1.36 | ||

Portfolio Turnover Rate | 21.98 | 24.86 | 30.42 | 36.37 | 39.66 | ||

Net Assets, end of period ($ x 1,000) | 40,185 | 77,438 | 68,681 | 35,247 | 14,261 | ||

a Based on average shares outstanding.

See notes to financial statements.

18

Class Y Shares | Year Ended May 31, | |||||||

2023 | 2022 | 2021 | 2020 | 2019 | ||||

Per Share Data ($): | ||||||||

Net asset value, beginning of period | 16.59 | 17.89 | 13.45 | 11.66 | 11.20 | |||

Investment Operations: | ||||||||

Net investment incomea | .12 | .09 | .07 | .14 | .16 | |||

Net

realized and unrealized | (.10) | (.55) | 4.89 | 1.93 | .80 | |||

Total from Investment Operations | .02 | (.46) | 4.96 | 2.07 | .96 | |||

Distributions: | ||||||||

Dividends

from | (.10) | (.12) | (.13) | (.12) | (.20) | |||

Dividends

from net realized | (1.67) | (.72) | (.39) | (.16) | (.30) | |||

Total Distributions | (1.77) | (.84) | (.52) | (.28) | (.50) | |||

Net asset value, end of period | 14.84 | 16.59 | 17.89 | 13.45 | 11.66 | |||

Total Return (%) | .66 | (3.24) | 37.38 | 17.70 | 8.90 | |||

Ratios/Supplemental Data (%): | ||||||||

Ratio

of total expenses | .69 | .67 | .74 | .71 | .71 | |||

Ratio

of net expenses | .69 | .67 | .70 | .70 | .70 | |||

Ratio

of net investment income | .76 | .49 | .57 | 1.13 | 1.35 | |||

Portfolio Turnover Rate | 21.98 | 24.86 | 30.42 | 36.37 | 39.66 | |||

Net Assets, end of period ($ x 1,000) | 296 | 19,199 | 27,882 | 205 | 317 | |||

a Based on average shares outstanding.

See notes to financial statements.

19

FINANCIAL HIGHLIGHTS (continued)

Class Z Shares | Year Ended May 31, | ||||||

2023 | 2022 | 2021 | 2020 | 2019 | |||

Per Share Data ($): | |||||||

Net asset value, beginning of period | 16.56 | 17.86 | 13.43 | 11.68 | 11.21 | ||

Investment Operations: | |||||||

Net investment incomea | .10 | .08 | .12 | .13 | .15 | ||

Net

realized and unrealized | (.09) | (.55) | 4.82 | 1.94 | .81 | ||

Total from Investment Operations | .01 | (.47) | 4.94 | 2.07 | .96 | ||

Distributions: | |||||||

Dividends

from | (.09) | (.11) | (.12) | (.16) | (.19) | ||

Dividends

from net realized | (1.67) | (.72) | (.39) | (.16) | (.30) | ||

Total Distributions | (1.76) | (.83) | (.51) | (.32) | (.49) | ||

Net asset value, end of period | 14.81 | 16.56 | 17.86 | 13.43 | 11.68 | ||

Total Return (%) | .58 | (3.29) | 37.38 | 17.65 | 8.81 | ||

Ratios/Supplemental Data (%): | |||||||

Ratio

of total expenses | .77 | .74 | .76 | .79 | .81 | ||

Ratio

of net expenses | .75 | .74 | .75 | .77 | .78 | ||

Ratio

of net investment income | .69 | .42 | .77 | 1.00 | 1.28 | ||

Portfolio Turnover Rate | 21.98 | 24.86 | 30.42 | 36.37 | 39.66 | ||

Net

Assets, | 315,181 | 337,126 | 365,956 | 284,793 | 262,053 | ||

a Based on average shares outstanding.

See notes to financial statements.

20

NOTES TO FINANCIAL STATEMENTS

NOTE 1—Significant Accounting Policies:

BNY Mellon Sustainable U.S. Equity Fund, Inc. (the “fund”), which is registered under the Investment Company Act of 1940, as amended (the “Act”), is a diversified open-end management investment company. The fund’s investment objective is to seek long-term capital appreciation. BNY Mellon Investment Adviser, Inc. (the “Adviser”), a wholly-owned subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”), serves as the fund’s investment adviser. Newton Investment Management Limited (the “Sub-Adviser”), an indirect wholly-owned subsidiary of BNY Mellon and an affiliate of the Adviser, serves as the sub-adviser.

Effective March 31, 2023, the Sub-Adviser, entered into a sub-sub-investment advisory agreement with its affiliate, Newton Investment Management North America, LLC (“NIMNA”), to enable NIMNA to provide certain advisory services to the Sub-Adviser for the benefit of the fund, including, but not limited to, portfolio management services. NIMNA is subject to the supervision of the Sub-Adviser and the Adviser. NIMNA is also an affiliate of the Adviser. NIMNA’s principal office is located at BNY Mellon Center, 201 Washington Street, Boston, MA 02108. NIMNA is an indirect subsidiary of BNY Mellon.

BNY Mellon Securities Corporation (the “Distributor”), a wholly-owned subsidiary of the Adviser, is the distributor of the fund’s shares. The fund is authorized to issue 700 million shares of $.001 par value Common Stock. The fund currently has authorized five classes of shares: Class A (100 million shares authorized), Class C (100 million shares authorized), Class I (150 million shares authorized), Class Y (150 million shares authorized) and Class Z (200 million shares authorized). Class A and Class C shares are sold primarily to retail investors through financial intermediaries and bear Distribution and/or Shareholder Services Plan fees. Class A shares generally are subject to a sales charge imposed at the time of purchase. Class A shares bought without an initial sales charge as part of an investment of $1 million or more may be charged a contingent deferred sales charge (“CDSC”) of 1.00% if redeemed within one year. Class C shares are subject to a CDSC imposed on Class C shares redeemed within one year of purchase. Class C shares automatically convert to Class A shares eight years after the date of purchase, without the imposition of a sales charge. Class I shares are sold primarily to bank trust departments and other financial service providers (including BNY Mellon and its affiliates), acting on behalf of customers having a qualified trust or an

21

NOTES TO FINANCIAL STATEMENTS (continued)

investment account or relationship at such institution, and bear no Distribution or Shareholder Services Plan fees. Class Y shares are sold at net asset value per share generally to institutional investors, and bear no Distribution or Shareholder Services Plan fees. Class Z shares are sold at net asset value per share to certain shareholders of the fund. Class Z shares generally are not available for new accounts and bear Shareholder Services Plan fees. Class I, Class Y and Class Z shares are offered without a front-end sales charge or CDSC. Other differences between the classes include the services offered to and the expenses borne by each class, the allocation of certain transfer agency costs and certain voting rights. Income, expenses (other than expenses attributable to a specific class), and realized and unrealized gains or losses on investments are allocated to each class of shares based on its relative net assets.

The Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) is the exclusive reference of authoritative U.S. generally accepted accounting principles (“GAAP”) recognized by the FASB to be applied by nongovernmental entities. Rules and interpretive releases of the SEC under authority of federal laws are also sources of authoritative GAAP for SEC registrants. The fund is an investment company and applies the accounting and reporting guidance of the FASB ASC Topic 946 Financial Services-Investment Companies. The fund’s financial statements are prepared in accordance with GAAP, which may require the use of management estimates and assumptions. Actual results could differ from those estimates.

The fund enters into contracts that contain a variety of indemnifications. The fund’s maximum exposure under these arrangements is unknown. The fund does not anticipate recognizing any loss related to these arrangements.

(a) Portfolio valuation: The fair value of a financial instrument is the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (i.e., the exit price). GAAP establishes a fair value hierarchy that prioritizes the inputs of valuation techniques used to measure fair value. This hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

Additionally, GAAP provides guidance on determining whether the volume and activity in a market has decreased significantly and whether such a decrease in activity results in transactions that are not orderly. GAAP requires enhanced disclosures around valuation inputs and techniques used during annual and interim periods.

22

Various inputs are used in determining the value of the fund’s investments relating to fair value measurements. These inputs are summarized in the three broad levels listed below:

Level 1—unadjusted quoted prices in active markets for identical investments.

Level 2—other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.).

Level 3—significant unobservable inputs (including the fund’s own assumptions in determining the fair value of investments).

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Changes in valuation techniques may result in transfers in or out of an assigned level within the disclosure hierarchy. Valuation techniques used to value the fund’s investments are as follows:

The fund’s Board of Directors (the “Board”) has designated the Adviser as the fund’s valuation designee, effective September 8, 2022, to make all fair value determinations with respect to the fund’s portfolio investments, subject to the Board’s oversight and pursuant to Rule 2a-5 under the Act.

Investments in equity securities are valued at the last sales price on the securities exchange or national securities market on which such securities are primarily traded. Securities listed on the National Market System for which market quotations are available are valued at the official closing price or, if there is no official closing price that day, at the last sales price. For open short positions, asked prices are used for valuation purposes. Bid price is used when no asked price is available. Registered investment companies that are not traded on an exchange are valued at their net asset value. All of the preceding securities are generally categorized within Level 1 of the fair value hierarchy.

Securities not listed on an exchange or the national securities market, or securities for which there were no transactions, are valued at the average of the most recent bid and asked prices. These securities are generally categorized within Level 2 of the fair value hierarchy.

Fair valuing of securities may be determined with the assistance of a pricing service using calculations based on indices of domestic securities and other appropriate indicators, such as prices of relevant American Depositary Receipts and futures. Utilizing these techniques may result in transfers between Level 1 and Level 2 of the fair value hierarchy.

23

NOTES TO FINANCIAL STATEMENTS (continued)

When market quotations or official closing prices are not readily available, or are determined not to accurately reflect fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the fund calculates its net asset value, the fund may value these investments at fair value as determined in accordance with the procedures approved by the Board. Certain factors may be considered when fair valuing investments such as: fundamental analytical data, the nature and duration of restrictions on disposition, an evaluation of the forces that influence the market in which the securities are purchased and sold, and public trading in similar securities of the issuer or comparable issuers. These securities are either categorized within Level 2 or 3 of the fair value hierarchy depending on the relevant inputs used.

For securities where observable inputs are limited, assumptions about market activity and risk are used and such securities are generally categorized within Level 3 of the fair value hierarchy.

The following is a summary of the inputs used as of May 31, 2023 in valuing the fund’s investments:

Level 1-Unadjusted Quoted Prices | Level 2- Other Significant Observable Inputs | Level 3-Significant Unobservable Inputs | Total | |||

Assets ($) | ||||||

Investments in Securities:† | ||||||

Equity Securities - Common Stocks | 378,738,447 | - | - | 378,738,447 | ||

Investment Companies | 6,872,055 | - | - | 6,872,055 | ||

† See Statement of Investments for additional detailed categorizations, if any.

(b) Securities transactions and investment income: Securities transactions are recorded on a trade date basis. Realized gains and losses from securities transactions are recorded on the identified cost basis. Dividend income is recognized on the ex-dividend date and interest income, including, where applicable, accretion of discount and amortization of premium on investments, is recognized on the accrual basis.

(c) Affiliated issuers: Investments in other investment companies advised by the Adviser are considered “affiliated” under the Act.

(d) Market Risk: The value of the securities in which the fund invests may be affected by political, regulatory, economic and social developments, and developments that impact specific economic sectors, industries or

24

segments of the market. The value of a security may also decline due to general market conditions that are not specifically related to a particular company or industry, such as real or perceived adverse economic conditions, changes in the general outlook for corporate earnings, changes in interest or currency rates, changes to inflation, adverse changes to credit markets or adverse investor sentiment generally. In addition, turbulence in financial markets and reduced liquidity in equity, credit and/or fixed-income markets may negatively affect many issuers, which could adversely affect the fund. Global economies and financial markets are becoming increasingly interconnected, and conditions and events in one country, region or financial market may adversely impact issuers in a different country, region or financial market. These risks may be magnified if certain events or developments adversely interrupt the global supply chain; in these and other circumstances, such risks might affect companies world-wide. Recent examples include pandemic risks related to COVID-19 and aggressive measures taken world-wide in response by governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines of large populations, and by businesses, including changes to operations and reducing staff.

ESG Investment Approach Risk: The fund’s incorporation of ESG considerations into its investment approach may cause it to make different investments than funds that invest principally in equity securities of U.S. companies that do not incorporate ESG considerations when selecting investments. Under certain economic conditions, this could cause the fund to underperform funds that do not incorporate ESG considerations. For example, the incorporation of ESG considerations may result in the fund forgoing opportunities to buy certain securities when it might otherwise be advantageous to do so or selling securities when it might otherwise be disadvantageous for the fund to do so. The incorporation of ESG considerations may also affect the fund’s exposure to certain sectors and/or types of investments, and may adversely impact the fund’s performance depending on whether such sectors or investments are in or out of favor in the market. The Sub-Adviser’s security selection process incorporates ESG data provided by third parties, which may be limited for certain companies and/or only take into account one or a few ESG related components. In addition, ESG data may include quantitative and/or qualitative measures, and consideration of this data may be subjective. Different methodologies may be used by the various data sources that provide ESG data. ESG data from third parties used by the Sub-Adviser as part of its proprietary ESG process often lacks standardization, consistency and transparency, and for certain companies such data may not be available, complete or accurate. The Sub-Adviser’s evaluation of ESG

25

NOTES TO FINANCIAL STATEMENTS (continued)

factors relevant to a particular company may be adversely affected in such instances. As a result, the fund’s investments may differ from, and potentially underperform, funds that incorporate ESG data from other sources or utilize other methodologies.

(e) Dividends and distributions to shareholders: Dividends and distributions are recorded on the ex-dividend date. Dividends from net investment income and dividends from net realized capital gains, if any, are normally declared and paid annually, but the fund may make distributions on a more frequent basis to comply with the distribution requirements of the Internal Revenue Code of 1986, as amended (the “Code”). To the extent that net realized capital gains can be offset by capital loss carryovers, it is the policy of the fund not to distribute such gains. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

(f) Federal income taxes: It is the policy of the fund to continue to qualify as a regulated investment company, if such qualification is in the best interests of its shareholders, by complying with the applicable provisions of the Code, and to make distributions of taxable income and net realized capital gain sufficient to relieve it from substantially all federal income and excise taxes.

As of and during the period ended May 31, 2023, the fund did not have any liabilities for any uncertain tax positions. The fund recognizes interest and penalties, if any, related to uncertain tax positions as income tax expense in the Statement of Operations. During the period ended May 31, 2023, the fund did not incur any interest or penalties.

Each tax year in the four-year period ended May 31, 2023 remains subject to examination by the Internal Revenue Service and state taxing authorities.

At May 31, 2023, the components of accumulated earnings on a tax basis were as follows: undistributed ordinary income $2,786,907, undistributed capital gains $11,002,564 and unrealized appreciation $112,802,759.

The tax character of distributions paid to shareholders during the fiscal years ended May 31, 2023 and May 31, 2022 were as follows: ordinary income $2,249,742 and $9,471,852, and long-term capital gains $43,981,728 and $14,276,295, respectively.

NOTE 2—Bank Lines of Credit:

The fund participates with other long-term open-end funds managed by the Adviser in a $823.5 million unsecured credit facility led by Citibank, N.A. (the “Citibank Credit Facility”) and a $300 million unsecured credit

26

facility provided by BNY Mellon (the “BNYM Credit Facility”), each to be utilized primarily for temporary or emergency purposes, including the financing of redemptions (each, a “Facility”). The Citibank Credit Facility is available in two tranches: (i) Tranche A is in an amount equal to $688.5 million and is available to all long-term open-ended funds, including the fund, and (ii) Tranche B is an amount equal to $135 million and is available only to BNY Mellon Floating Rate Income Fund, a series of BNY Mellon Investment Funds IV, Inc. In connection therewith, the fund has agreed to pay its pro rata portion of commitment fees for Tranche A of the Citibank Credit Facility and the BNYM Credit Facility. Interest is charged to the fund based on rates determined pursuant to the terms of the respective Facility at the time of borrowing.

The average amount of borrowings outstanding under the Facilities during the period ended May 31, 2023 was approximately $190,685 with a related weighted average annualized interest rate of 5.18%.

NOTE 3—Management Fee, Sub-Advisory Fee and Other Transactions with Affiliates:

(a) Pursuant to the management agreement (the “Agreement”) with the Adviser, the management fee is computed at an annual rate of .60% of the value of the fund’s average daily net assets and is payable monthly. Pursuant to the Agreement, if in any full fiscal year the aggregate expenses of Class Z shares (excluding taxes, interest expense, brokerage commissions, commitment fees on borrowings and extraordinary expenses) exceed 1½% of the value of the average daily net assets of Class Z shares, the fund may deduct from the fees paid to the Adviser, or the Adviser will bear such excess expense. During the period ended May 31, 2023, there was no expense reimbursement pursuant to the Agreement.

The Adviser has contractually agreed, from June 1, 2022 through September 30, 2023, to waive receipt of its fees and/or assume the direct expenses of the fund so that the direct expenses of none of the fund’s share classes (excluding Rule 12b-1 Distribution Plan fees, Shareholder Services Plan fees, taxes, interest expense, brokerage commission, commitment fees on borrowings and extraordinary expenses) exceed .70% of the value of the fund’s average daily net assets. On or after September 30, 2023, the Adviser may terminate this expense limitation at any time. The reduction in expenses, pursuant to the undertaking, amounted to $51,281 during the period ended May 31, 2023.

Pursuant to a sub-investment advisory agreement between the Adviser and the Sub-Adviser, the Sub-Adviser is responsible for the day-to-day management of the fund’s portfolio. The Adviser pays the Sub-Adviser a

27

NOTES TO FINANCIAL STATEMENTS (continued)

monthly fee at an annual percentage of the value of the fund’s average daily net assets. The Adviser has obtained an exemptive order from the SEC (the “Order”), upon which the fund may rely, to use a manager of managers approach that permits the Adviser, subject to certain conditions and approval by the Board, to enter into and materially amend sub-investment advisory agreements with one or more sub-advisers who are either unaffiliated with the Adviser or are wholly-owned subsidiaries (as defined under the Act) of the Adviser’s ultimate parent company, BNY Mellon, without obtaining shareholder approval. The Order also allows the fund to disclose the sub-advisory fee paid by the Adviser to any unaffiliated sub-adviser in the aggregate with other unaffiliated sub-advisers in documents filed with the SEC and provided to shareholders. In addition, pursuant to the Order, it is not necessary to disclose the sub-advisory fee payable by the Adviser separately to a sub-adviser that is a wholly-owned subsidiary of BNY Mellon in documents filed with the SEC and provided to shareholders; such fees are to be aggregated with fees payable to the Adviser. The Adviser has ultimate responsibility (subject to oversight by the Board) to supervise any sub-adviser and recommend the hiring, termination, and replacement of any sub-adviser to the Board.

During the period ended May 31, 2023, the Distributor retained $1,066 from commissions earned on sales of the fund’s Class A shares and $18 from CDSC fees on redemptions of the fund’s Class C shares.

(b) Under the Distribution Plan adopted pursuant to Rule 12b-1 under the Act, Class C shares pay the Distributor for distributing its shares at an annual rate of .75% of the value of its average daily net assets. The Distributor may pay one or more Service Agents in respect of advertising, marketing and other distribution services, and determines the amounts, if any, to be paid to Service Agents and the basis on which such payments are made. During the period ended May 31, 2023, Class C shares were charged $9,872 pursuant to the Distribution Plan.

(c) Under the Shareholder Services Plan, Class A and Class C shares pay the Distributor at an annual rate of .25% of the value of their average daily net assets for the provision of certain services. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding the fund, and services related to the maintenance of shareholder accounts. The Distributor may make payments to Service Agents (securities dealers, financial institutions or other industry professionals) with respect to these services. The Distributor determines the amounts to be paid to Service Agents. During the period ended May 31, 2023, Class A and Class C shares were charged

28

$73,940 and $3,291, respectively, pursuant to the Shareholder Services Plan.

Under the Shareholder Services Plan, Class Z shares reimburse the Distributor at an amount not to exceed an annual rate of ..25% of the value of Class Z shares’ average daily net assets for certain allocated expenses of providing personal services and/or maintaining shareholder accounts. The services provided may include personal services relating to shareholder accounts, such as answering shareholder inquiries regarding Class Z shares, and services related to the maintenance of shareholder accounts. During the period ended May 31, 2023, Class Z shares were charged $181,478 pursuant to the Shareholder Services Plan.

The fund has an arrangement with BNY Mellon Transfer, Inc., (the “Transfer Agent”), a subsidiary of BNY Mellon and an affiliate of the Adviser, whereby the fund may receive earnings credits when positive cash balances are maintained, which are used to offset Transfer Agent fees. For financial reporting purposes, the fund includes transfer agent net earnings credits, if any, as an expense offset in the Statement of Operations.

The fund has an arrangement with The Bank of New York Mellon (the “Custodian”), a subsidiary of BNY Mellon and an affiliate of the Adviser, whereby the fund will receive interest income or be charged overdraft fees when cash balances are maintained. For financial reporting purposes, the fund includes this interest income and overdraft fees, if any, as interest income in the Statement of Operations.

The fund compensates the Transfer Agent, under a transfer agency agreement, for providing transfer agency and cash management services for the fund. The majority of Transfer Agent fees are comprised of amounts paid on a per account basis, while cash management fees are related to fund subscriptions and redemptions. During the period ended May 31, 2023, the fund was charged $86,198 for transfer agency services. These fees are included in Shareholder servicing costs in the Statement of Operations. These fees were partially offset by earnings credits of $38,383.

The fund compensates the Custodian, under a custody agreement, for providing custodial services for the fund. These fees are determined based on net assets, geographic region and transaction activity. During the period ended May 31, 2023, the fund was charged $9,057 pursuant to the custody agreement.

During the period ended May 31, 2023, the fund was charged $19,799 for services performed by the fund’s Chief Compliance Officer and his staff. These fees are included in Chief Compliance Officer fees in the Statement of Operations.

29

NOTES TO FINANCIAL STATEMENTS (continued)

The components of “Due to BNY Mellon Investment Adviser, Inc. and affiliates” in the Statement of Assets and Liabilities consist of: management fee of $196,581, Distribution Plan fees of $813, Shareholder Services Plan fees of $25,425, Custodian fees of $4,800, Chief Compliance Officer fees of $5,070 and Transfer Agent fees of $25,370, which are offset against an expense reimbursement currently in effect in the amount of $10,830.

(d) Each board member also serves as a board member of other funds in the BNY Mellon Family of Funds complex. Annual retainer fees and attendance fees are allocated to each fund based on net assets.

NOTE 4—Securities Transactions:

The aggregate amount of purchases and sales of investment securities, excluding short-term securities, during the period ended May 31, 2023, amounted to $89,618,648 and $171,364,502, respectively.

At May 31, 2023, the cost of investments for federal income tax purposes was $272,807,743; accordingly, accumulated net unrealized appreciation on investments was $112,802,759, consisting of $125,441,990 gross unrealized appreciation and $12,639,231 gross unrealized depreciation.

30

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and the Board of Directors of BNY Mellon Sustainable U.S. Equity Fund, Inc.

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of BNY Mellon Sustainable U.S. Equity Fund, Inc. (the “Fund”), including the statement of investments, as of May 31, 2023, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the two years in the period then ended, the financial highlights for each of the five years in the period then ended and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund at May 31, 2023, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period then ended and its financial highlights for each of the five years in the period then ended, in conformity with U.S. generally accepted accounting principles.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of the Fund’s internal control over financial reporting. As part of our audits, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2023, by correspondence with the custodian, brokers and others; when replies were not received from brokers and others, we performed other auditing procedures. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

We have served as the auditor of one or more investment companies in the BNY Mellon Family of Funds since at least 1957, but we are unable to determine the specific year.

New York, New York

July

21, 2023

31

IMPORTANT TAX INFORMATION (Unaudited)

For federal tax purposes the fund hereby reports 100% of the ordinary dividends paid during the fiscal year ended May 31, 2023 as qualifying for the corporate dividends received deduction. Also, certain dividends paid by the fund may be subject to a maximum tax rate of 15%, as provided for by the Jobs and Growth Tax Relief Reconciliation Act of 2003. Of the distributions paid during the fiscal year, $2,249,742 represents the maximum amount that may be considered qualified dividend income. Shareholders will receive notification in early 2024 of the percentage applicable to the preparation of their 2023 income tax returns. Also, the fund hereby reports $1.6702 per share as a long-term capital gain distribution paid on December 5, 2022.

32

INFORMATION ABOUT THE APPROVAL OF THE FUND’S SUB-SUB-INVESTMENT ADVISORY AGREEMENT (Unaudited)

At a meeting of the fund’s Board held on March 1, 2023, the Board considered the approval of a delegation arrangement between Newton Investment Management Limited (the “Sub-Adviser” or “NIM”) and its affiliate, Newton Investment Management North America, LLC (“NIMNA”), which permits NIM, as the fund’s sub-investment adviser, to use the investment advisory personnel, resources and capabilities (“Investment Advisory Services”) available at its sister company, NIMNA, in providing the day-to-day management of the fund’s investments. In connection therewith, the Board considered the approval of a sub-sub-investment advisory agreement (the “SSIA Agreement”) between NIM and NIMNA, with respect to the fund. In considering the approval of the SSIA Agreement, the Board considered several factors that it believed to be relevant, including those discussed below. The Board did not identify any one factor as dispositive, and each Board member may have attributed different weights to the factors considered.

At the meeting, the Adviser and the Sub-Adviser recommended the approval of the SSIA Agreement to enable NIMNA to provide Investment Advisory Services to the Sub-Adviser for the benefit of the fund, including, but not limited to, portfolio management services, subject to the supervision of the Sub-Adviser and the Adviser. The recommendation for the approval of the SSIA Agreement was based on the following considerations, among others: (i) approval of the SSIA Agreement would permit the Sub-Adviser to use investment personnel employed primarily by NIMNA as primary portfolio managers of the fund and to use the investment research services of NIMNA in the day-to-day management of the fund’s investments; and (ii) there would be no material changes to the fund’s investment objective, strategies or policies, no reduction in the nature or level of services provided to the fund, and no increases in the management fee payable by the fund or the sub-advisory fee payable by the Adviser to the Sub-Adviser as a result of the delegation arrangement. The Board also considered the fact that the Adviser stated that it believed there were no material changes to the information the Board had previously considered at the most recent meeting in connection with the Board’s re-approval of the Management Agreement, pursuant to which the Adviser provides the fund with investment advisory and administrative services, and the Sub-Investment Advisory Agreement (together with the Management Agreement, the “Agreements”), pursuant to which NIMNA provides day-to-day management of the fund’s investments, other than the information about the delegation arrangement and NIMNA.

In determining whether to approve the SSIA Agreement, the Board considered the materials prepared by the Adviser and the Sub-Adviser received in advance of the meeting and other information presented at the meeting, which included: (i) a form of the SSIA Agreement; (ii) information regarding the delegation arrangement and how it is expected to enhance investment capabilities for the benefit of the fund; (iii) information regarding NIMNA; and (iv) an opinion of counsel that the proposed delegation arrangement would not result in an “assignment” of the Sub-Investment Advisory Agreement under the 1940 Act and the Investment Advisers Act of 1940, as amended,

33

INFORMATION ABOUT THE APPROVAL OF THE FUND’S SUB-SUB-INVESTMENT ADVISORY AGREEMENT (Unaudited) (continued)

and, therefore, did not require the approval of fund shareholders. The Board also considered the substance of discussions with representatives of the Adviser and the Sub-Adviser at the meeting in connection with the Board’s re-approval of the Agreements.