File No. 2-9455

811-0523

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 [X]

Pre-Effective Amendment No. [__]

Post-Effective Amendment No. 163 [X]

and/or

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 [X]

Amendment No. 163 [X]

(Check appropriate box or boxes.)

The Dreyfus Fund Incorporated

(Exact Name of Registrant as Specified in Charter)

c/o The Dreyfus Corporation

200 Park Avenue, New York, New York 10166

(Address of Principal Executive Offices) (Zip Code)

Registrant's Telephone Number, including Area Code: (212) 922-6000

John Pak, Esq.

200 Park Avenue

New York, New York 10166

(Name and Address of Agent for Service)

It is proposed that this filing will become effective (check appropriate box)

__ immediately upon filing pursuant to paragraph (b)

X on May 1, 2013 pursuant to paragraph (b)

____ days after filing pursuant to paragraph (a)(1)

__ on (date) pursuant to paragraph (a)(1)

____ days after filing pursuant to paragraph (a)(2)

__ on (date) pursuant to paragraph (a)(2) of Rule 485

If appropriate, check the following box:

__ this post-effective amendment designates a new effective date for a previously filed post-effective amendment.

The Dreyfus Fund Incorporated

|

|

Prospectus May 1, 2013 |

||

Ticker Symbol: DREVX

|

As with all mutual funds, the Securities and Exchange Commission has not approved or disapproved |

|

Contents

Fund Summary |

Buying and Selling Shares |

|

General Policies |

|

Distributions and Taxes |

|

Services for Fund Investors |

|

Financial Highlights |

See back cover.

Fund Summary

The fund seeks long-term capital growth consistent with the preservation of capital. Current income is a secondary investment objective.

This table describes the fees and expenses that you may pay if you buy and hold shares of the fund.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

|||

Management fees |

0.65 |

||

Other expenses |

0.10 |

||

Total annual fund operating expenses |

0.75 |

||

Example

The Example is intended to help you compare the cost of investing in the fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the fund for the time periods indicated and then redeem all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the fund's operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

1 Year |

3 Years |

5 Years |

10 Years |

$77 |

$240 |

$417 |

$930 |

Portfolio Turnover

The fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund's performance. During the most recent fiscal year, the fund's portfolio turnover rate was 56.38% of the average value of its portfolio.

To pursue its goals, the fund primarily invests in common stocks issued by U.S. companies. The fund may invest up to 20% of its assets in foreign securities (i.e., issued by companies organized under the laws of countries other than the U.S.).

In choosing stocks, the fund's portfolio managers focus on large-capitalization companies with strong positions in their industries and a catalyst that can trigger a price increase (such as a corporate restructuring or change in management). The portfolio managers use fundamental analysis to create a broadly diversified portfolio comprised of growth stocks, value stocks and stocks that exhibit characteristics of both investment styles. The portfolio managers attempt to measure a security's instrinsic value by analyzing "real" data (company financials, economic outlook, etc.) and other factors (management, industry conditions, competition, etc.) and select stocks based on value, growth and financial profile.

An investment in the fund is not a bank deposit. It is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. It is not a complete investment program. The fund's share price fluctuates, sometimes dramatically, which means you could lose money.

1

· Risks of stock investing. Stocks generally fluctuate more in value than bonds and may decline significantly over short time periods. There is the chance that stock prices overall will decline because stock markets tend to move in cycles, with periods of rising prices and falling prices. The market value of a stock may decline due to general weakness in the stock market or because of factors that affect the company or its particular industry.

· Growth and value stock risk. By investing in a mix of growth and value companies, the fund assumes the risks of both. Investors often expect growth companies to increase their earnings at a certain rate. If these expectations are not met, investors can punish the stocks inordinately, even if earnings do increase. In addition, growth stocks typically lack the dividend yield that can cushion stock prices in market downturns. Value stocks involve the risk that they may never reach their expected full market value, either because the market fails to recognize the stock's intrinsic worth, or the expected value was misgauged. They also may decline in price even though in theory they are already undervalued.

· Large cap stock risk. To the extent the fund invests in large capitalization stocks, the fund may underperform funds that invest primarily in the stocks of lower quality, smaller capitalization companies during periods when the stocks of such companies are in favor.

· Market sector risk. The fund may significantly overweight or underweight certain companies, industries or market sectors, which may cause the fund's performance to be more or less sensitive to developments affecting those companies, industries or sectors.

· Foreign investment risk. To the extent the fund invests in foreign securities, the fund's performance will be influenced by political, social and economic factors affecting investments in foreign issuers. Special risks associated with investments in foreign issuers include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political and economic instability and differing auditing and legal standards. Investments denominated in foreign currencies are subject to the risk that such currencies will decline in value relative to the U.S. dollar and affect the value of these investments held by the fund.

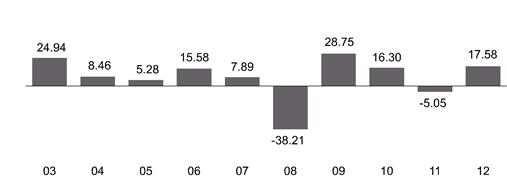

The following bar chart and table provide some indication of the risks of investing in the fund. The bar chart shows changes in the performance of the fund's shares from year to year. The table compares the average annual total returns of the fund's shares to those of a broad measure of market performance. The fund's past performance (before and after taxes) is not necessarily an indication of how the fund will perform in the future. More recent performance information may be available at www.dreyfus.com.

Year-by-Year Total Returns as of 12/31 each year (%) |

|

|

Best Quarter Worst Quarter |

After-tax returns are calculated using the historical highest individual federal marginal income tax rates, and do not reflect the impact of state and local taxes. Actual after-tax returns depend on the investor's tax situation and may differ from those shown, and the after-tax returns shown are not relevant to investors who hold their shares through tax-deferred arrangements such as 401(k) plans or individual retirement accounts.

Average Annual Total Returns (as of 12/31/12) |

|||

1 Year |

5 Years |

10 Years |

|

Fund returns before taxes |

17.58% |

0.65% |

6.28% |

Fund returns after taxes on distributions |

17.36% |

0.39% |

5.67% |

Fund returns after taxes on distributions and sale of fund shares |

11.72% |

0.49% |

5.42% |

S&P 500® Index reflects no deduction for fees, expenses or taxes |

15.99% |

1.66% |

7.10% |

2

The fund's investment adviser is The Dreyfus Corporation. Sean P. Fitzgibbon, David Sealy and Barry K. Mills are the fund's primary portfolio managers, positions they have held since May 2005, February 2010 and February 2010, respectively. Mr. Fitzgibbon is a senior managing director, research analyst and the head of the global core equity team at The Boston Company Asset Management, LLC (TBCAM), an affiliate of The Dreyfus Corporation. Mr. Sealy is a portfolio manager at TBCAM. Mr. Mills is a senior managing analyst at TBCAM. Each primary portfolio manager also is an employee of The Dreyfus Corporation.

In general, the fund's minimum initial investment is $2,500 and the minimum subsequent investment is $100. You may sell (redeem) your shares on any business day by calling 1-800-DREYFUS (inside the U.S. only) or by visiting www.dreyfus.com. If you invested in the fund through a third party, such as a bank, broker-dealer or financial adviser, or in a 401(k) or other retirement plan, you may mail your request to sell shares to Dreyfus Institutional Department, P.O. Box 9882, Providence, Rhode Island 02940-8082. If you invested directly through the fund, you may mail your request to sell shares to Dreyfus Shareholder Services, P.O. Box 9879, Providence, Rhode Island 02940-8079.

The fund's distributions are taxable as ordinary income or capital gains, except when your investment is through an IRA, 401(k) plan or other tax-advantaged investment plan (in which case you may be taxed upon withdrawal of your investment from such account).

If you purchase shares through a broker-dealer or other financial intermediary (such as a bank), the fund and its related companies may pay the intermediary for the sale of fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the fund over another investment. Ask your salesperson or visit your financial intermediary's website for more information.

3

Fund Details

The fund seeks long-term capital growth consistent with the preservation of capital. Current income is a secondary investment objective. To pursue its goals, the fund primarily invests in common stocks issued by U.S. companies, including to a limited degree, those issued in initial public offerings (IPOs). The fund may invest up to 20% of its assets in foreign securities (i.e., securities issued by companies organized under the laws of countries other than the U.S.).

In choosing stocks, the fund's portfolio managers focus on large-capitalization companies with strong positions in their industries and a catalyst that can trigger a price increase (such as a corporate restructuring or change in management). The portfolio managers use fundamental analysis to create a broadly diversified portfolio comprised of growth stocks, value stocks and stocks that exhibit characteristics of both investment styles. The portfolio managers attempt to measure a security's intrinsic value by analyzing "real" data (company financials, economic outlook, etc.) and other factors (management, industry conditions, competition, etc.), and select stocks based on:

· value, or how a stock is priced relative to its perceived intrinsic worth

· growth, in this case the sustainability or growth of earnings or cash flow

· financial profile, which measures the financial health of the company

The fund typically sells a security when the portfolio managers believe that there has been a negative change in the fundamental factors surrounding the company, the company has become fully valued, the company has lost favor in the current market or economic environment, or a more attractive opportunity has been identified.

Although not a principal investment strategy, the fund may, but is not required to, use derivatives, such as options, futures and options on futures (including those relating to stocks, indexes, foreign currencies and interest rates), as a substitute for investing directly in an underlying asset, to increase returns, or as part of a hedging strategy. The fund also may engage in short-selling, typically for hedging purposes, such as to limit exposure to a possible market decline in the value of its portfolio securities.

An investment in the fund is not a bank deposit. It is not insured or guaranteed by the FDIC or any other government agency. It is not a complete investment program. The value of your investment in the fund will fluctuate, sometimes dramatically, which means you could lose money.

· Risks of stock investing. Stocks generally fluctuate more in value than bonds and may decline significantly over short time periods. There is the chance that stock prices overall will decline because stock markets tend to move in cycles, with periods of rising prices and falling prices. The market value of a stock may decline due to general market conditions that are not related to the particular company, such as real or perceived adverse economic conditions, changes in the outlook for corporate earnings, changes in interest or currency rates, or adverse investor sentiment generally. A security's market value also may decline because of factors that affect a particular industry, such as labor shortages or increased production costs and competitive conditions within an industry, or factors that affect a particular company, such as management performance, financial leverage, and reduced demand for the company's products or services.

· Growth and value stock risk. By investing in a mix of growth and value companies, the fund assumes the risks of both. Investors often expect growth companies to increase their earnings at a certain rate. If these expectations are not met, investors can punish the stocks inordinately, even if earnings do increase. In addition, growth stocks typically lack the dividend yield that can cushion stock prices in market downturns. Value stocks involve the risk that they may never reach their expected full market value, either because the market fails to recognize the stock's intrinsic worth, or the expected value was misgauged. They also may decline in price even though in theory they are already undervalued.

· Large cap stock risk. To the extent the fund invests in large capitalization stocks, the fund may underperform funds that invest primarily in the stocks of lower quality, smaller capitalization companies during periods when the stocks of such companies are in favor.

4

· Market sector risk. The fund may significantly overweight or underweight certain companies, industries or market sectors, which may cause the fund's performance to be more or less sensitive to developments affecting those companies, industries or sectors.

· Foreign investment risk. To the extent the fund invests in foreign securities, the fund's performance will be influenced by political, social and economic factors affecting investments in foreign issuers. Special risks associated with investments in foreign issuers include exposure to currency fluctuations, less liquidity, less developed or less efficient trading markets, lack of comprehensive company information, political and economic instability and differing auditing and legal standards. Investments denominated in foreign currencies are subject to the risk that such currencies will decline in value relative to the U.S. dollar and affect the value of these investments held by the fund.

In addition to the principal risks described above, the fund is subject to the following additional risks.

· IPO risk. The prices of securities purchased in IPOs can be very volatile. The effect of IPOs on the fund's performance depends on a variety of factors, including the number of IPOs the fund invests in relative to the size of the fund and whether and to what extent a security purchased in an IPO appreciates or depreciates in value. As a fund's asset base increases, IPOs often have a diminished effect on such fund's performance.

· Derivatives risk. A small investment in derivatives could have a potentially large impact on the fund's performance. The use of derivatives involves risks different from, or possibly greater than, the risks associated with investing directly in the underlying assets. Derivatives can be highly volatile, illiquid and difficult to value, and there is the risk that changes in the value of a derivative held by the fund will not correlate with the underlying instruments or the fund's other investments. Derivative instruments, such as options, futures and options on futures, also involve the risk that a loss may be sustained as a result of the failure of the counterparty to the derivative instruments to make required payments or otherwise comply with the derivative instruments' terms. Many of the regulatory protections afforded participants on organized exchanges for futures contracts and exchange-traded options, such as the performance guarantee of an exchange clearing house, are not available in connection with over-the-counter derivative transactions. Certain types of derivatives, including over-the-counter transactions, involve greater risks than the underlying obligations because, in addition to general market risks, they are subject to illiquidity risk, counterparty risk, credit risk and pricing risk. Because many derivatives have a leverage component, adverse changes in the value or level of the underlying asset, reference rate or index can result in a loss substantially greater than the amount invested in the derivative itself. Certain derivatives have the potential for unlimited loss, regardless of the size of the initial investment. The fund may be required to segregate liquid assets in connection with the purchase of derivative instruments.

· Leverage risk. The use of leverage, such as entering into futures contracts, and lending portfolio securities, may magnify the fund's gains or losses.

· Short sale risk. The fund may make short sales, which involves selling a security it does not own in anticipation that the security's price will decline. Short sales expose the fund to the risk that it will be required to buy the security sold short (also known as "covering" the short position) at a time when the security has appreciated in value, thus resulting in a loss to the fund.

· Other potential risks. The fund may lend its portfolio securities to brokers, dealers and other financial institutions. In connection with such loans, the fund will receive collateral from the borrower equal to at least 100% of the value of loaned securities. If the borrower of the securities fails financially, there could be delays in recovering the loaned securities or exercising rights to the collateral.

Under adverse market conditions, the fund could invest some or all of its assets in U.S. Treasury securities and money market securities. Although the fund would do this for temporary defensive purposes, it could reduce the benefit from any upswing in the market. During such periods, the fund may not achieve its investment objectives.

The investment adviser for the fund is The Dreyfus Corporation (Dreyfus), 200 Park Avenue, New York, New York 10166. Founded in 1947, Dreyfus manages approximately $240 billion in 168 mutual fund portfolios. For the past fiscal year, the fund paid Dreyfus a management fee at the annual rate of 0.65% of the fund's average daily net assets. A discussion regarding the basis for the board's approving the fund's management agreement with Dreyfus is available in the fund's annual report for the fiscal year ended December 31, 2012. Dreyfus is the primary mutual fund business of The Bank of New York Mellon Corporation (BNY Mellon), a global financial services company focused on helping clients manage and service their financial assets, operating in 36 countries and serving more than 100 markets. BNY Mellon is a leading investment management and investment services company, uniquely focused to help clients manage and move their financial assets in the rapidly changing global marketplace. BNY Mellon has $26.2 trillion in assets under custody and administration and $1.4 trillion in assets under management. BNY Mellon is the corporate brand of The

5

Bank of New York Mellon Corporation. BNY Mellon Investment Management is one of the world's leading investment management organizations, and one of the top U.S. wealth managers, encompassing BNY Mellon's affiliated investment management firms, wealth management services and global distribution companies. Additional information is available at www.bnymellon.com.

The Dreyfus asset management philosophy is based on the belief that discipline and consistency are important to investment success. For each fund, Dreyfus seeks to establish clear guidelines for portfolio management and to be systematic in making decisions. This approach is designed to provide each fund with a distinct, stable identity.

Sean P. Fitzgibbon, David Sealy and Barry K. Mills are the fund's primary portfolio managers. Mr. Fitzgibbon has been a primary portfolio manager of the fund since May 2005. Mr. Fitzgibbon is a senior managing director, research analyst and the head of the global core equity team at The Boston Company Asset Management, LLC (TBCAM), a Dreyfus affiliate, where he has been employed since 1991. He also has been employed by Dreyfus since October 2004. Mr. Sealy has been a portfolio manager of the fund since June 2005 and a primary portfolio manager of the fund since February 2010. Mr. Sealy is a portfolio manager at TBCAM, where he has been employed since 2005. He also has been employed by Dreyfus since June 1997. Mr. Mills has been a portfolio manager of the fund since June 2005 and a primary portfolio manager of the fund since February 2010. Mr. Mills is senior managing analyst at TBCAM, where he has been employed since June 2005. He also has been employed by Dreyfus since 1999.

The fund's Statement of Additional Information (SAI) provides additional portfolio manager information, including compensation, other accounts managed and ownership of fund shares.

MBSC Securities Corporation (MBSC), a wholly owned subsidiary of Dreyfus, serves as distributor of the fund and of the other funds in the Dreyfus Family of Funds. Any Rule 12b-1 fees and shareholder services fees, as applicable, are paid to MBSC for financing the sale and distribution of fund shares and for providing shareholder account service and maintenance, respectively. Dreyfus or MBSC may provide cash payments out of its own resources to financial intermediaries that sell shares of funds in the Dreyfus Family of Funds or provide other services. Such payments are separate from any sales charges, 12b-1 fees and/or shareholder services fees or other expenses that may be paid by a fund to those intermediaries. Because those payments are not made by fund shareholders or the fund, the fund's total expense ratio will not be affected by any such payments. These payments may be made to intermediaries, including affiliates, that provide shareholder servicing, sub-administration, recordkeeping and/or sub-transfer agency services, marketing support and/or access to sales meetings, sales representatives and management representatives of the financial intermediary. Cash compensation also may be paid from Dreyfus' or MBSC's own resources to intermediaries for inclusion of a fund on a sales list, including a preferred or select sales list or in other sales programs. These payments sometimes are referred to as "revenue sharing." From time to time, Dreyfus or MBSC also may provide cash or non-cash compensation to financial intermediaries or their representatives in the form of occasional gifts; occasional meals, tickets or other entertainment; support for due diligence trips; educational conference sponsorships; support for recognition programs; technology or infrastructure support; and other forms of cash or non-cash compensation permissible under broker-dealer regulations. In some cases, these payments or compensation may create an incentive for a financial intermediary or its employees to recommend or sell shares of the fund to you. Please contact your financial representative for details about any payments they or their firm may receive in connection with the sale of fund shares or the provision of services to the fund.

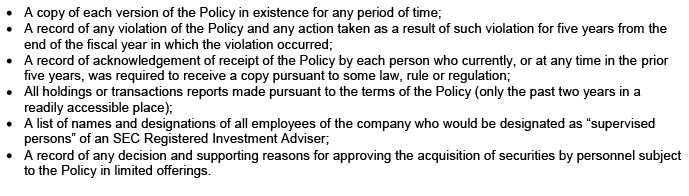

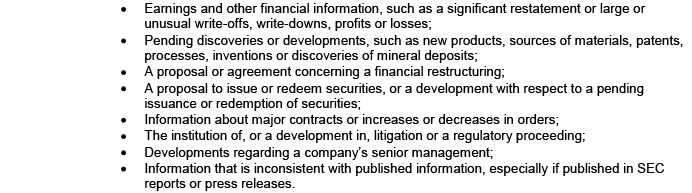

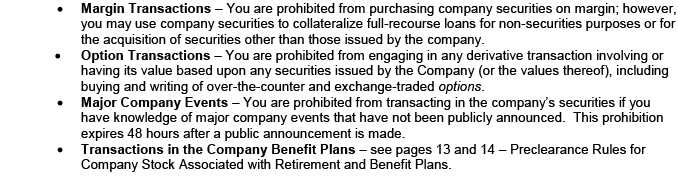

The fund, Dreyfus and MBSC have each adopted a code of ethics that permits its personnel, subject to such code, to invest in securities, including securities that may be purchased or held by the fund. Each code of ethics restricts the personal securities transactions of employees, and requires portfolio managers and other investment personnel to comply with the code's preclearance and disclosure procedures. The primary purpose of the respective codes is to ensure that personal trading by employees does not disadvantage any fund managed by Dreyfus or its affiliates.

6

Shareholder Guide

You pay no sales charges to invest in shares of the fund. Your price for shares is the net asset value (NAV) per share, which is generally calculated as of the close of trading on the New York Stock Exchange (NYSE) (usually 4:00 p.m. Eastern time) on days the NYSE is open for regular business.

Your order will be priced at the next NAV calculated after your order is received in proper form by the fund's transfer agent or other authorized entity. When calculating NAVs, Dreyfus values equity investments on the basis of market quotations or official closing prices. Dreyfus generally values fixed-income investments based on values supplied by an independent pricing service approved by the fund's board. The pricing service's procedures are reviewed under the general supervision of the board. If market quotations or prices from a pricing service are not readily available, or are determined not to reflect accurately fair value, the fund may value those investments at fair value as determined in accordance with procedures approved by the fund's board. Fair value of investments may be determined by the fund's board, its pricing committee or its valuation committee in good faith using such information as it deems appropriate under the circumstances. Under certain circumstances, the fair value of foreign equity securities will be provided by an independent pricing service. Using fair value to price investments may result in a value that is different from a security's most recent closing price and from the prices used by other mutual funds to calculate their net asset values. Foreign securities held by a fund may trade on days when the fund does not calculate its NAV and thus may affect the fund's NAV on days when investors will not be able to purchase or sell (redeem) fund shares.

Investments in certain types of thinly traded securities may provide short-term traders arbitrage opportunities with respect to the fund's shares. For example, arbitrage opportunities may exist when trading in a portfolio security or securities is halted and does not resume, or the market on which such securities are traded closes before the fund calculates its NAV. If short-term investors in the fund were able to take advantage of these arbitrage opportunities, they could dilute the NAV of fund shares held by long-term investors. Portfolio valuation policies can serve to reduce arbitrage opportunities available to short-term traders, but there is no assurance that such valuation policies will prevent dilution of the fund's NAV by short-term traders. While the fund has a policy regarding frequent trading, it too may not be completely effective to prevent short-term NAV arbitrage trading, particularly in regard to omnibus accounts. Please see "Shareholder Guide— General Policies" for further information about the fund's frequent trading policy.

Orders to buy and sell shares received by an authorized entity (such as a bank, broker-dealer or financial adviser, or 401(k) or other retirement plan that has entered into an agreement with the fund's distributor) by the close of trading on the NYSE and transmitted to the distributor or its designee by the close of its business day (usually 5:15 p.m. Eastern time) will be based on the NAV determined as of the close of trading on the NYSE that day.

How to Buy Shares

By Mail.

Regular Accounts. To open a regular account, complete an application and mail it, together with a check payable to The Dreyfus Family of Funds, to the appropriate address below. To purchase additional shares in a regular account, mail a check payable to The Dreyfus Family of Funds (with your account number on your check), together with an investment slip, to the appropriate address below.

IRA Accounts. To open an IRA account or make additional investments in an IRA account, be sure to specify the fund name and the year for which the contribution is being made. When opening a new account include a completed IRA application, and when making additional investments include an investment slip. Make checks payable to The Dreyfus Family of Funds, and mail to the appropriate address below.

Mailing Address. If you are investing directly through the fund, mail to:

Dreyfus Shareholder Services

P.O. Box 9879

Providence, Rhode Island 02940-8079

7

If you are investing through a third party, such as a bank, broker-dealer or financial adviser, or in a 401(k) or other retirement plan, mail to:

Dreyfus Institutional Department

P.O. Box 9882

Providence, Rhode Island 02940-8082

Electronic Check or Wire. To purchase shares in a regular or IRA account by wire or electronic check, please call 1-800-DREYFUS (inside the U.S. only) for more information.

Dreyfus TeleTransfer. To purchase additional shares in a regular or IRA account by Dreyfus TeleTransfer, which will transfer money from a pre-designated bank account, request the account service on your application. Call us at 1-800-DREYFUS (inside the U.S. only) or visit www.dreyfus.com to request your transaction.

Automatically. You may purchase additional shares in a regular or IRA account by selecting one of Dreyfus' automatic investment services made available to the fund on your account application or service application. See "Services for Fund Investors."

The minimum initial and subsequent investment for regular accounts is $2,500 and $100, respectively. The minimum initial investment for IRAs is $750, with no minimum subsequent investment. The minimum initial investment for educational savings accounts is $500, with no minimum subsequent investment. Investments made through Dreyfus TeleTransfer are subject to a $100 minimum and a $150,000 maximum. All investments must be in U.S. dollars. Third-party checks, cash, travelers' checks or money orders will not be accepted. You may be charged a fee for any check that does not clear.

How to Sell Shares

You may sell (redeem) shares at any time. Your shares will be sold at the next NAV calculated after your order is received in proper form by the fund's transfer agent or other authorized entity. Any certificates representing fund shares being sold must be returned with your redemption request. Your order will be processed promptly and you will generally receive the proceeds within a week.

Before selling shares recently purchased by check, Dreyfus TeleTransfer or Automatic Asset Builder, please note that:

· if you send a written request to sell such shares, the fund may delay sending the proceeds for up to eight business days following the purchase of those shares

· the fund will not process wire, telephone, online or Dreyfus TeleTransfer redemption requests for up to eight business days following the purchase of those shares

By Mail – Regular Account. To redeem shares in a regular account by mail, send a letter of instruction that includes your name, your account number, the name of the fund, the dollar amount to be redeemed and how and where to send the proceeds. Mail your request to the appropriate address below.

By Mail – IRA Accounts. To redeem shares in an IRA account by mail, send a letter of instruction that includes all of the same information for regular accounts and indicate whether the distribution is qualified or premature and whether the 10% TEFRA should be withheld. Mail your request to the appropriate address below.

Mailing Address. If you invested directly through the fund, mail to:

Dreyfus Shareholder Services

P.O. Box 9879

Providence, Rhode Island 02940-8079

If you invested through a third party, such as a bank, broker-dealer or financial adviser, or in a 401(k) or other retirement plan, mail to:

Dreyfus Institutional Department

P.O. Box 9882

Providence, Rhode Island 02940-8082

A medallion signature guarantee is required for some written sell orders. These include:

· amounts of $10,000 or more on accounts whose address has been changed within the last 30 days

· requests to send the proceeds to a different payee or address

· amounts of $100,000 or more

8

A medallion signature guarantee helps protect against fraud. You can obtain one from most banks or securities dealers, but not from a notary public. For joint accounts, each signature must be guaranteed. Please call to ensure that your medallion signature guarantee will be processed correctly.

Telephone or Online. To redeem shares call Dreyfus at 1-800-DREYFUS (inside the U.S. only), or for regular accounts visit www.dreyfus.com to request your transaction.

A check will be mailed to your address of record or you may request a wire or electronic check (Dreyfus TeleTransfer). For wires or Dreyfus TeleTransfer, be sure that the fund has your bank account information on file. Proceeds will be wired or sent by electronic check to your bank account.

You may speak to a Dreyfus representative to request that redemption proceeds be paid by check and mailed to your address of record (maximum $250,000 per day). You may also request that redemption proceeds be sent to your bank by wire (minimum $1,000) or by Dreyfus TeleTransfer (minimum $500). There is a $100,000 per day limit on redemption requests made online through dreyfus.com or through the Dreyfus Express® automated account access system.

Automatically. You may sell shares in a regular account by calling 1-800-DREYFUS (inside the U.S. only) for instructions on how to establish the Dreyfus Automatic Withdrawal Plan. You may sell shares in an IRA account by calling the above number for instructions on automatic withdrawals.

Unless you decline teleservice privileges on your application, the fund's transfer agent is authorized to act on telephone or online instructions from any person representing himself or herself to be you and reasonably believed by the transfer agent to be genuine. You may be responsible for any fraudulent telephone or online order as long as the fund's transfer agent takes reasonable measures to confirm that instructions are genuine.

If you invest through a financial intermediary (rather than directly through the fund), the policies may be different than those described herein. Banks, brokers, 401(k) plans, financial advisers and financial supermarkets may charge transaction fees and may set up different minimum investments or limitations on buying or selling shares. Please consult your financial representative.

The fund is designed for long-term investors. Frequent purchases, redemptions and exchanges may disrupt portfolio management strategies and harm fund performance by diluting the value of fund shares and increasing brokerage and administrative costs. As a result, Dreyfus and the fund's board have adopted a policy of discouraging excessive trading, short-term market timing and other abusive trading practices (frequent trading) that could adversely affect the fund or its operations. Dreyfus and the fund will not enter into arrangements with any person or group to permit frequent trading.

The fund also reserves the right to:

· change or discontinue its exchange privilege, or temporarily suspend the privilege during unusual market conditions

· change its minimum or maximum investment amounts

· delay sending out redemption proceeds for up to seven days (generally applies only during unusual market conditions or in cases of very large redemptions or excessive trading)

· "redeem in kind," or make payments in securities rather than cash, if the amount redeemed is large enough to affect fund operations (for example, if it exceeds 1% of the fund's assets)

· refuse any purchase or exchange request, including those from any individual or group who, in Dreyfus' view, is likely to engage in frequent trading

More than four roundtrips within a rolling 12-month period generally is considered to be frequent trading. A roundtrip consists of an investment that is substantially liquidated within 60 days. Based on the facts and circumstances of the trades, the fund may also view as frequent trading a pattern of investments that are partially liquidated within 60 days.

Transactions made through Automatic Investment Plans, Automatic Withdrawal Plans, Dreyfus Auto-Exchange Privileges, automatic non-discretionary rebalancing programs, and minimum required retirement distributions generally are not considered to be frequent trading. For employer-sponsored benefit plans, generally only participant-initiated exchange transactions are subject to the roundtrip limit.

Dreyfus monitors selected transactions to identify frequent trading. When its surveillance systems identify multiple roundtrips, Dreyfus evaluates trading activity in the account for evidence of frequent trading. Dreyfus considers the investor's trading history in other accounts under common ownership or control, in other Dreyfus Funds and BNY

9

Mellon Funds and, if known, in nonaffiliated mutual funds and accounts under common control. These evaluations involve judgments that are inherently subjective, and while Dreyfus seeks to apply the policy and procedures uniformly, it is possible that similar transactions may be treated differently. In all instances, Dreyfus seeks to make these judgments to the best of its abilities in a manner that it believes is consistent with shareholder interests. If Dreyfus concludes the account is likely to engage in frequent trading, Dreyfus may cancel or revoke the purchase or exchange on the following business day. Dreyfus may also temporarily or permanently bar such investor's future purchases into the fund in lieu of, or in addition to, canceling or revoking the trade. At its discretion, Dreyfus may apply these restrictions across all accounts under common ownership, control or perceived affiliation.

Fund shares often are held through omnibus accounts maintained by financial intermediaries, such as brokers and retirement plan administrators, where the holdings of multiple shareholders, such as all the clients of a particular broker, are aggregated. Dreyfus' ability to monitor the trading activity of investors whose shares are held in omnibus accounts is limited. However, the agreements between the distributor and financial intermediaries include obligations to comply with the terms of this prospectus and to provide Dreyfus, upon request, with information concerning the trading activity of investors whose shares are held in omnibus accounts. If Dreyfus determines that any such investor has engaged in frequent trading of fund shares, Dreyfus may require the intermediary to restrict or prohibit future purchases or exchanges of fund shares by that investor.

Certain retirement plans and intermediaries that maintain omnibus accounts with the fund may have developed policies designed to control frequent trading that may differ from the fund's policy. At its sole discretion, the fund may permit such intermediaries to apply their own frequent trading policy. If you are investing in fund shares through an intermediary (or in the case of a retirement plan, your plan sponsor), please contact the intermediary for information on the frequent trading policies applicable to your account.

To the extent that the fund significantly invests in foreign securities traded on markets that close before the fund calculates its NAV, events that influence the value of these foreign securities may occur after the close of these foreign markets and before the fund calculates its NAV. As a result, certain investors may seek to trade fund shares in an effort to benefit from their understanding of the value of these foreign securities at the time the fund calculates its NAV (referred to as price arbitrage). This type of frequent trading may dilute the value of fund shares held by other shareholders. Dreyfus has adopted procedures designed to adjust closing market prices of foreign equity securities under certain circumstances to reflect what it believes to be their fair value.

To the extent that the fund significantly invests in thinly traded securities, certain investors may seek to trade fund shares in an effort to benefit from their understanding of the value of these securities (referred to as price arbitrage). Any such frequent trading strategies may interfere with efficient management of the fund's portfolio to a greater degree than funds that invest in highly liquid securities, in part because the fund may have difficulty selling these portfolio securities at advantageous times or prices to satisfy large and/or frequent redemption requests. Any successful price arbitrage may also cause dilution in the value of fund shares held by other shareholders.

Although the fund's frequent trading and fair valuation policies and procedures are designed to discourage market timing and excessive trading, none of these tools alone, nor all of them together, completely eliminates the potential for frequent trading.

Small Account Policies

To offset the relatively higher costs of servicing smaller accounts, the fund charges regular accounts with balances below $2,000 an annual fee of $12. The fee will be imposed during the fourth quarter of each calendar year.

The fee will be waived for: any investor whose aggregate Dreyfus mutual fund investments total at least $25,000; IRA accounts; Education Savings Accounts; accounts participating in automatic investment programs; and accounts opened through a financial institution.

If your account falls below $500, the fund may ask you to increase your balance. If it is still below $500 after 45 days, the fund may close your account and send you the proceeds.

The fund earns dividends, interest and other income from its investments, and distributes this income (less expenses) to shareholders as dividends. The fund also realizes capital gains from its investments, and distributes these gains (less any losses) to shareholders as capital gain distributions. The fund normally pays dividends quarterly and capital gain distributions annually. Fund dividends and capital gain distributions will be reinvested in the fund unless you instruct the fund otherwise. There are no fees or sales charges on reinvestments.

Distributions paid by the fund are subject to federal income tax, and may also be subject to state or local taxes (unless you are investing through a tax-advantaged retirement account). For federal tax purposes, in general, certain fund

10

distributions, including distributions of short-term capital gains, are taxable as ordinary income. Other fund distributions, including dividends from certain U.S. companies and certain foreign companies and distributions of long-term capital gains, generally are taxable as qualified dividends and capital gains, respectively.

High portfolio turnover and more volatile markets can result in significant taxable distributions to shareholders, regardless of whether their shares have increased in value. The tax status of any distribution generally is the same regardless of how long you have been in the fund and whether you reinvest your distributions or take them in cash.

If you buy shares of a fund when the fund has realized but not yet distributed income or capital gains, you will be "buying a dividend" by paying the full price for the shares and then receiving a portion back in the form of a taxable distribution.

Your sale of shares, including exchanges into other funds, may result in a capital gain or loss for tax purposes. A capital gain or loss on your investment in the fund generally is the difference between the cost of your shares and the amount you receive when you sell them.

The tax status of your distributions will be detailed in your annual tax statement from the fund. Because everyone's tax situation is unique, please consult your tax adviser before investing.

Automatic Services

Buying or selling shares automatically is easy with the services described below. With each service, you select a schedule and amount, subject to certain restrictions. If you purchase shares through a third party, the third party may impose different restrictions on these services and privileges, or may not make them available at all. For information, call your financial representative or 1-800-DREYFUS (inside the U.S. only).

Dreyfus Automatic Asset Builder® permits you to purchase fund shares (minimum of $100 and maximum of $150,000 per transaction) at regular intervals selected by you. Fund shares are purchased by transferring funds from the bank account designated by you.

Dreyfus Payroll Savings Plan permits you to purchase fund shares (minimum of $100 per transaction) automatically through a payroll deduction.

Dreyfus Government Direct Deposit permits you to purchase fund shares (minimum of $100 and maximum of $50,000 per transaction) automatically from your federal employment, Social Security or other regular federal government check.

Dreyfus Dividend Sweep permits you to automatically reinvest dividends and distributions from the fund into another Dreyfus Fund (not available for IRAs).

Dreyfus Auto-Exchange Privilege permits you to exchange at regular intervals your fund shares for shares of other Dreyfus Funds.

Dreyfus Automatic Withdrawal Plan permits you to make withdrawals (minimum of $50) on a specific day each month, quarter or semi-annual or annual period, provided your account balance is at least $5,000.

Exchange Privilege

Generally, you can exchange shares worth $500 or more (no minimum for retirement accounts) into shares of the same class, or another class in which you are eligible to invest, of another fund in the Dreyfus Family of Funds. You can request your exchange by contacting your financial representative. Be sure to read the current prospectus for any fund into which you are exchanging before investing. Any new account established through an exchange generally will have the same privileges as your original account (as long as they are available). There is currently no fee for exchanges, although you may be charged a sales load when exchanging into any fund that has one.

Your exchange request will be processed on the same business day it is received in proper form, provided that each fund is open at the time of the request. If the exchange is accepted at a time of day after one or both of the funds is closed (i.e., at a time after the NAV for the fund has been calculated for that business day), the exchange will be processed on the next business day. See the SAI for more information regarding exchanges.

Dreyfus TeleTransfer Privilege

To move money between your bank account and your Dreyfus Fund account with a phone call (for regular or IRA accounts) or online (for regular accounts only), use the Dreyfus TeleTransfer privilege. You can set up Dreyfus TeleTransfer on your account by providing bank account information and following the instructions on your

11

application, or contacting your financial representative. Shares held in an Education Savings Account may not be redeemed through the Dreyfus TeleTransfer privilege.

Account Statements

Every Dreyfus Fund investor automatically receives regular account statements. You will also be sent a yearly statement detailing the tax characteristics of any dividends and distributions you have received.

Dreyfus Express® Voice-Activated Account Access

You can easily manage your Dreyfus accounts, check your account balances, purchase fund shares, transfer money between your Dreyfus Funds, get price and yield information, and much more, by calling 1-800-DREYFUS (inside the U.S. only). Certain requests require the services of a representative.

Dreyfus Advisor Services

For investors with a minimum of $100,000 or more in investable assets, Dreyfus Advisor Services is a personalized asset management service. We welcome the opportunity to discuss what we can do, specifically for you. For more information, contact an advisor at 1-800-896-2645.

Retirement Plans

Dreyfus offers a variety of retirement plans, including traditional and Roth IRAs and Education Savings Accounts. Here's where you call for information:

· For traditional, rollover and Roth IRAs and Education Savings Accounts, call 1-800-DREYFUS (inside the U.S. only)

· For SEP-IRAs, Keogh accounts, 401(k) and 403(b) accounts, call 1-800-358-0910

12

These financial highlights describe the performance of the fund's shares for the fiscal periods indicated. "Total return" shows how much your investment in the fund would have increased (or decreased) during each period, assuming you had reinvested all dividends and distributions. These financial highlights have been audited by Ernst & Young LLP, an independent registered public accounting firm, whose report, along with the fund's financial statements, is included in the annual report, which is available upon request.

Year Ended December 31, |

|||||

2012 |

2011 |

2010 |

2009 |

2008 |

|

Per Share Data ($): |

|||||

Net asset value, beginning of period |

8.44 |

8.99 |

7.80 |

6.14 |

10.25 |

Investment Operations: |

|||||

Investment income--neta |

.12 |

.10 |

.07 |

.08 |

.13 |

Net realized and unrealized gain (loss) on investments |

1.36 |

(.55) |

1.19 |

1.67 |

(3.98) |

Total from Investment Operations |

1.48 |

(.45) |

1.26 |

1.75 |

(3.85) |

Distributions: |

|||||

Dividends from investment income--net |

(.12) |

(.10) |

(.07) |

(.09) |

(.13) |

Dividends from net realized gain on investments |

- |

- |

- |

- |

(.13) |

Total Distributions |

(.12) |

(.10) |

(.07) |

(.09) |

(.26) |

Net asset value, end of period |

9.80 |

8.44 |

8.99 |

7.80 |

6.14 |

Total Return (%) |

17.58 |

(5.05) |

16.30 |

28.75 |

(38.21) |

Ratios/Supplemental Data (%): |

|||||

Ratio of total expenses to average net assets |

.75 |

.77 |

.78 |

.80 |

.76 |

Ratio of net expenses to average net assets |

.75 |

.77 |

.78 |

.79 |

.75 |

Ratio of net investment income to average net assets |

1.30 |

1.11 |

.84 |

1.18 |

1.48 |

Portfolio Turnover Rate |

56.38 |

67.60 |

60.06 |

77.88 |

76.31 |

Net Assets, end of period ($ x 1,000) |

1,010,371 |

940,107 |

1,041,526 |

966,117 |

815,876 |

aBased on average shares outstanding at each month. |

|||||

13

For More Information

The Dreyfus Fund Incorporated

SEC file

number: 811-0523

More information on this fund is available free upon request, including the following:

Annual/Semiannual Report

Describes the fund's performance, lists portfolio holdings and contains a letter from the fund's manager discussing recent market conditions, economic trends and fund strategies that significantly affected the fund's performance during the last fiscal year. The fund's most recent annual and semiannual reports are available at www.dreyfus.com.

Statement of Additional Information (SAI)

Provides more details about the fund and its policies. A current SAI is available at www.dreyfus.com and is on file with the Securities and Exchange Commission (SEC). The SAI is incorporated by reference (and is legally considered part of this prospectus).

Portfolio Holdings

Dreyfus funds generally disclose their complete schedule of portfolio holdings monthly with a 30-day lag at www.dreyfus.com under Products and Performance. Complete holdings as of the end of the calendar quarter are disclosed 15 days after the end of such quarter. Dreyfus money market funds generally disclose their complete schedule of holdings daily. The schedule of holdings for a fund will remain on the website until the fund files its Form N-Q or Form N-CSR for the period that includes the dates of the posted holdings.

A complete description of the fund's policies and procedures with respect to the disclosure of the fund's portfolio securities is available in the fund's SAI.

To Obtain Information

By telephone. Call 1-800-DREYFUS (inside the U.S. only)

By mail.

The

Dreyfus Family of Funds

144 Glenn Curtiss Boulevard

Uniondale, NY 11556-0144

By E-mail. Send your request to info@dreyfus.com

On the Internet. Certain fund documents can be viewed online or downloaded from:

SEC: http://www.sec.gov

Dreyfus: http://www.dreyfus.com

You can also obtain copies, after paying a duplicating fee, by visiting the SEC's Public Reference Room in Washington, DC (for information, call 1-202-551-8090) or by E-mail request to publicinfo@sec.gov, or by writing to the SEC's Public Reference Section, Washington, DC 20549-1520.

© 2013

MBSC Securities Corporation |

|

STATEMENT OF ADDITIONAL INFORMATION

August 1, 2012, as revised or amended September 1, 2012, October 1, 2012, December 1, 2012, February 1, 2013, March 1, 2013, April 1, 2013 and May 1, 2013

This Statement of Additional Information (SAI), which is not a prospectus, supplements and should be read in conjunction with the current prospectus of each fund listed below, as such prospectuses may be revised from time to time. To obtain a copy of a fund's prospectus, please call your financial adviser, or write to the fund at 144 Glenn Curtiss Boulevard, Uniondale, New York 11556-0144, visit www.dreyfus.com, or call 1-800-DREYFUS (inside the U.S. only).

The most recent annual report and semi-annual report to shareholders for each fund are separate documents supplied with this SAI, and the financial statements, accompanying notes and report of the independent registered public accounting firm appearing in the annual report are incorporated by reference into this SAI. All classes of a fund have the same fiscal year end and prospectus date. Capitalized but undefined terms used in this SAI are defined in the Glossary at the end of this SAI.

|

Fund |

Abbreviation |

Share Class/Ticker |

Fiscal Year End* |

Prospectus Date |

|

Dreyfus Institutional Cash Advantage Funds |

ICAF |

|||

|

Dreyfus Institutional Cash Advantage Fund |

DICAF |

Administrative Advantage/DDTXX |

April 30th |

September 1st |

|

Participant Advantage/DPTXX |

||||

|

Institutional Advantage/DADXX |

||||

|

Investor Advantage/DIVXX |

||||

|

Dreyfus Institutional Preferred Money Market Funds |

IPMMF |

|||

|

Dreyfus Institutional Preferred Money Market Fund |

DIPMMF |

Prime/N/A |

March 31st |

August 1st |

|

Reserve/DRSXX |

||||

|

Dreyfus Institutional Preferred Plus Money Market Fund |

DIPPMMF |

N/A |

March 31st |

August 1st |

|

Dreyfus Institutional Reserves Funds |

IRF |

|||

|

Dreyfus Institutional Reserves Money Fund |

DIRMF |

Institutional/DSVXX |

December 31st |

May 1st |

|

Hamilton/DSHXX |

||||

|

Agency/DRGXX |

||||

|

Premier/DERXX |

||||

|

Classic/DLSXX |

||||

|

Dreyfus Institutional Reserves Treasury Fund |

DIRTF |

Institutional/DNSXX |

December 31st |

May 1st |

|

Hamilton/DHLXX |

||||

|

Agency/DGYXX |

||||

|

Premier/DRRXX |

||||

|

Classic/DSSXX |

||||

|

Dreyfus Institutional Reserves Treasury Prime Fund |

DIRTPF |

Institutional/DUPXX |

December 31st |

May 1st |

|

Hamilton/DHMXX |

||||

|

| ||||

|

Premier/DMEXX |

||||

|

|

Fund |

Abbreviation |

Share Class/Ticker |

Fiscal Year End* |

Prospectus Date |

Dreyfus Investment Grade Funds, Inc. |

DIGF |

|||

Dreyfus Inflation Adjusted Securities Fund |

DIASF |

Institutional/DIASX |

July 31st |

December 1st |

Investor/DIAVX |

||||

Dreyfus Intermediate Term Income Fund |

DITIF |

Class A/DRITX |

July 31st |

December 1st |

Class C/DTECX |

||||

Class I/DITIX |

||||

Dreyfus Short Term Income Fund |

DSTIF |

Class D/DSTIX |

July 31st |

December 1st |

Class P/DSHPX |

||||

|

||||

Dreyfus Liquid Assets, Inc. |

DLA |

Class 1/DLAXX |

December 31st |

May 1st |

Class 2/DLATX |

||||

Dreyfus Opportunity Funds |

DOF |

|||

Dreyfus Natural Resources Fund |

DNRF |

Class A/DNLAX |

September 30th |

February 1st |

Class C/DLDCX |

||||

Class I/DLDRX |

||||

Dreyfus Premier Short-Intermediate Municipal Bond Fund |

PSIMBF |

|||

Dreyfus Short-Intermediate Municipal Bond Fund |

DSIMBF |

Class A/DMBAX |

March 31st |

August 1st |

Class D/DSIBX |

||||

Class I/DIMIX |

||||

Dreyfus Short-Intermediate Government Fund |

SIGF |

DSIGX |

November 30th |

April 1st |

Dreyfus Worldwide Dollar Money Market Fund, Inc. |

WDMMF |

DWDXX |

October 31st |

March 1st |

The Dreyfus Fund Incorporated |

DF |

DREVX |

December 31st |

May 1st |

The Dreyfus Third Century Fund, Inc. |

DTCF |

Class A/DTCAX |

May 31st |

October 1st |

Class C/DTCCX |

||||

Class I/DRTCX |

||||

Class Z/DRTHX |

||||

* Certain information provided in this SAI is indicated to be as of the end of a fund's last fiscal year or during a fund's last fiscal year. The term "last fiscal year" means the most recently completed fiscal year, except that, for funds with fiscal years ended March 31st and April 30th, "last fiscal year" means the fiscal year ended in the immediately preceding calendar year.

TABLE OF CONTENTS

PART I

BOARD INFORMATION |

|

Information About Each Board Member's Experience, Qualifications, Attributes or Skills |

|

Committee Meetings |

|

Board Members' and Officers' Fund Share Ownership |

|

Board Members' Compensation |

|

OFFICERS |

|

CERTAIN PORTFOLIO MANAGER INFORMATION |

|

MANAGER'S COMPENSATION |

|

SALES LOADS, CDSCS AND DISTRIBUTOR'S COMPENSATION |

|

OFFERING PRICE |

|

RATINGS OF MUNICIPAL BONDS |

|

Ratings of Corporate Debt Securities |

|

SECURITIES OF REGULAR BROKERS OR DEALERS |

|

COMMISSIONS |

|

PORTFOLIO TURNOVER VARIATION |

|

SHARE OWNERSHIP |

PART II

HOW TO BUY SHARES |

|

Investment Minimums |

|

Purchase of Institutional Money Funds |

|

Dreyfus TeleTransfer Privilege |

|

Reopening an Account |

|

Information Regarding the Offering of Share Classes |

|

Class A |

|

Right of Accumulation |

|

HOW TO REDEEM SHARES |

|

Wire Redemption Privilege |

|

SHAREHOLDER SERVICES |

|

DISTRIBUTION PLANS, SERVICE PLANS AND SHAREHOLDER SERVICES PLANS |

|

INVESTMENTS, INVESTMENT TECHNIQUES AND RISKS |

|

Funds other than Money Market Funds |

|

Money Market Funds |

|

INVESTMENT RESTRICTIONS |

|

Fundamental Policies |

|

Nonfundamental Policies |

|

Policies Related to Fund Names |

|

DIVIDENDS AND DISTRIBUTIONS |

|

INFORMATION ABOUT THE FUNDS' ORGANIZATION AND STRUCTURE |

CERTAIN EXPENSE ARRANGEMENTS AND OTHER DISCLOSURES |

|

COUNSEL AND INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM |

PART III

ADDITIONAL INFORMATION ABOUT HOW TO BUY SHARES |

|

Investment Minimums |

|

Purchase of Institutional Money Funds and Cash Management Funds |

|

In-Kind Purchases |

|

Information Pertaining to Purchase Orders |

|

Federal Funds |

|

Dreyfus TeleTransfer Privilege |

|

Reopening an Account |

|

Multi-Class Funds |

|

Converting Shares |

|

Taxpayer ID Number |

|

Frequent Purchases and Exchanges (non-money market funds only) |

|

ADDITIONAL INFORMATION ABOUT HOW TO REDEEM SHARES |

|

Redemption Fee |

|

Contingent Deferred Sales Charge - Multi-Class Funds |

|

Class C |

|

Waiver of CDSC |

|

Redemption Through an Authorized Entity |

|

Checkwriting Privilege |

|

Wire Redemption Privilege |

|

Redemption through Compatible Automated Facilities |

|

Dreyfus TeleTransfer Privilege |

|

Reinvestment Privilege |

|

Share Certificates; Medallion Signature Guarantees |

|

Redemption Commitment |

|

Suspension of Redemptions |

|

ADDITIONAL INFORMATION ABOUT SHAREHOLDER SERVICES |

|

Exchanges |

|

Fund Exchanges |

|

Dreyfus Auto-Exchange Privilege |

|

Dreyfus Automatic Asset Builder® |

|

Dreyfus Government Direct Deposit Privilege |

|

Dreyfus Payroll Savings Plan |

|

Dreyfus Dividend Options |

|

Dreyfus Dividend Sweep |

|

Dreyfus Dividend ACH |

|

Automatic Withdrawal Plan |

|

Letter of Intent - Class A Shares |

|

Corporate Pension/Profit-Sharing and Retirement Plans |

|

ADDITIONAL INFORMATION ABOUT DISTRIBUTION PLANS, SERVICE PLANS AND SHAREHOLDER SERVICES PLANS |

|

ADDITIONAL INFORMATION ABOUT INVESTMENTS, |

|

INVESTMENT TECHNIQUES AND RISKS |

|

All Funds other than Money Market Funds |

|

Equity Securities |

|

Common Stock |

|

Preferred Stock |

|

Convertible Securities |

Warrants |

|

IPOs |

|

Fixed-Income Securities |

|

U.S. Government Securities |

|

Corporate Debt Securities |

|

Ratings of Securities; Unrated Securities |

|

High Yield and Lower-Rated Securities |

|

Zero Coupon, Pay-In-Kind and Step-Up Securities |

|

Inflation-Indexed Securities |

|

Variable and Floating Rate Securities |

|

Participation Interests and Assignments |

|

Mortgage-Related Securities |

|

Asset-Backed Securities |

|

Collateralized Debt Obligations |

|

Municipal Securities |

|

Taxable Investments (municipal or other tax-exempt funds only) |

|

Funding Agreements |

|

Real Estate Investment Trusts (REITs) |

|

Money Market Instruments |

|

Bank Obligations |

|

Repurchase Agreements |

|

Commercial Paper |

|

Foreign Securities |

|

Emerging Markets |

|

Brazil |

|

Certain Asian Emerging Market Countries |

|

India |

|

Depositary Receipts and New York Shares |

|

Sovereign Debt Obligations |

|

Eurodollar and Yankee Dollar Investments |

|

Investment Companies |

|

Private Investment Funds |

|

Exchange-Traded Funds (ETFs) |

|

Exchange-Traded Notes |

|

Derivatives |

|

Futures Transactions |

|

Options |

|

Swap Transactions |

|

Credit Linked Securities |

|

Credit Derivatives |

|

Structured Securities and Hybrid Instruments |

|

Participatory Notes |

|

Custodial Receipts |

|

Combined Transactions |

|

Future Developments |

|

Foreign Currency Transactions |

|

Commodities |

|

Short-Selling |

|

Lending Portfolio Securities |

|

Borrowing Money |

|

Borrowing Money for Leverage |

|

Reverse Repurchase Agreements |

|

Forward Commitments |

|

Forward Roll Transactions |

|

Illiquid Securities |

|

Illiquid Securities Generally |

Section 4(2) Paper and Rule 144A Securities |

|

Non-Diversified Status |

|

Investments in the Technology Sector |

|

Investments in the Real Estate Sector |

|

Investments in the Natural Resources Sector |

|

Money Market Funds |

|

Ratings of Securities |

|

Treasury Securities |

|

U.S. Government Securities |

|

Repurchase Agreements |

|

Bank Obligations |

|

Bank Securities |

|

Floating and Variable Rate Obligations |

|

Participation Interests |

|

Asset-Backed Securities |

|

Commercial Paper |

|

Investment Companies |

|

Foreign Securities |

|

Municipal Securities |

|

Derivative Products |

|

Stand-By Commitments |

|

Taxable Investments (municipal or other tax-exempt funds only) |

|

Illiquid Securities |

|

Borrowing Money |

|

Reverse Repurchase Agreements |

|

Forward Commitments |

|

Interfund Borrowing and Lending Program |

|

Lending Portfolio Securities |

|

RATING CATEGORIES |

|

S&P |

|

Long-Term Issue Credit Ratings |

|

Short-Term Issue Credit Ratings |

|

Municipal Short-Term Note Ratings Definitions |

|

Moody's |

|

Long-Term Obligation Ratings and Definitions |

|

Short-Term Ratings |

|

U.S. Municipal Short-Term Debt and Demand Obligation Ratings |

|

Fitch |

|

Corporate Finance Obligations — Long-Term Rating Scales |

|

Structured, Project & Public Finance Obligations — Long-Term Rating Scales |

|

Short-Term Ratings Assigned to Obligations in Corporate, Public and Structured Finance |

|

DBRS |

|

Long Term Obligations |

|

Commercial Paper and Short Term Debt |

|

ADDITIONAL INFORMATION ABOUT THE BOARD |

|

Boards' Oversight Role in Management |

|

Board Composition and Leadership Structure |

|

Additional Information About the Boards and Their Committees |

|

MANAGEMENT ARRANGEMENTS |

|

The Manager |

|

Sub-Advisers |

|

Portfolio Allocation Manager |

|

Portfolio Managers and Portfolio Manager Compensation |

|

Certain Conflicts of Interest with Other Accounts |

Code of Ethics |

|

Distributor |

|

Transfer and Dividend Disbursing Agent and Custodian |

|

DETERMINATION OF NAV |

|

Valuation of Portfolio Securities (funds other than money market funds) |

|

Valuation of Portfolio Securities (money market funds only) |

|

Calculation of NAV |

|

Expense Allocations |

|

NYSE and Transfer Agent Closings |

|

ADDITIONAL INFORMATION ABOUT DIVIDENDS AND DISTRIBUTIONS |

|

Funds Other Than Money Market Funds |

|

Money Market Funds |

|

TAXATION |

|

Taxation of the Funds |

|

Taxation of Fund Distributions (Funds Other Than Municipal or Other Tax-Exempt Funds) |

|

Sale, Exchange or Redemption of Shares |

|

PFICs |

|

Non-U.S. Taxes |

|

Foreign Currency Transactions |

|

Financial Products |

|

Payments with Respect to Securities Loans |

|

Securities Issued or Purchased at a Discount and Payment-in-Kind Securities |

|

Inflation-Indexed Treasury Securities |

|

Certain Higher-Risk and High Yield Securities |

|

Funds Investing in Municipal Securities (Municipal or Other Tax-Exempt Funds) |

|

Investing in Mortgage Entities |

|

Tax-Exempt Shareholders |

|

Backup Withholding |

|

Foreign (Non-U.S.) Shareholders |

|

The Hiring Incentives to Restore Employment Act |

|

Possible Legislative Changes |

|

Other Tax Matters |

|

PORTFOLIO TRANSACTIONS |

|

Trading the Funds' Portfolio Securities |

|

Soft Dollars |

|

IPO Allocations |

|

Disclosure of Portfolio Holdings |

|

SUMMARY OF THE PROXY VOTING POLICY, PROCEDURES AND GUIDELINES OF THE DREYFUS FAMILY OF FUNDS |

|

ADDITIONAL INFORMATION ABOUT THE FUNDS' STRUCTURE; FUND SHARES |

|

AND VOTING RIGHTS |

|

Massachusetts Business Trusts |

|

Fund Shares and Voting Rights |

|

GLOSSARY |

PART I

Information About Each Board Member's Experience, Qualifications, Attributes or Skills

Board members for the funds, together with information as to their positions with the funds, principal occupations and other board memberships during the past five years, are shown below. The address of each board member is 200 Park Avenue, New York, New York 10166.

Independent Board Members

Name |

Principal Occupation During Past 5 Years |

Other Public Company Board Memberships During Past 5 Years |

Joseph S. DiMartino |

Corporate Director and Trustee |

CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small and medium size companies, Director (1997 - present) The Newark Group, a provider of a national market of paper recovery facilities, paperboard mills and paperboard converting plants, Director (2000 - 2010) Sunair Services Corporation, a provider of certain outdoor-related services to homes and businesses, Director (2005 - 2009) |

Clifford

L. Alexander, Jr. |

President of Alexander & Associates, Inc., a management consulting firm (1981 - present) |

N/A |

Whitney I. Gerard |

Partner in the law firm of Chadbourne & Parke LLP |

N/A |

Nathan Leventhal |

Chairman of the Avery Fisher Artist Program (1997 - present) Commissioner, NYC Planning Commission (2007 - 2011) |

Movado Group, Inc., Director (2003 - present) |

|

||

George L. Perry |

Economist and Senior Fellow at The Brookings Institution |

N/A |

Benaree Pratt Wiley |

Principal, The Wiley Group, a firm specializing in strategy and business development (2005 - present) |

CBIZ (formerly, Century Business Services, Inc.), a provider of outsourcing functions for small and medium size companies, Director (2008 - present) |

1 Each of the Independent Board Members serves on the board's audit, nominating, compensation and litigation committees.

I-1

Interested Board Member1

Name |

Principal Occupation During Past 5 Years |

Other Public Company Board Memberships During Past 5 Years |

Gordon

J. Davis |

Partner in the law firm of Venable LLP (2012 - present) Partner in the law firm of Dewey & LeBoeuf LLP (1994 - 2012) |

Consolidated Edison, Inc., a utility company, Director (1997 - present) The Phoenix Companies, Inc., a life insurance company, Director (2000 - present) |

1 Mr. Davis is deemed to be an Interested Board Member of DIGF, WDMMF and DTCF as a result of his affiliation with Venable LLP, which provides legal services to these funds.

2 Mr. Davis serves on the audit, nominating, compensation and litigation committees for each fund except DIGF, WDMMF and DTCF.

The following table shows the year each board member joined each fund's board.

Independent Board Members |

Interested Board Member |

|||||||

Fund |

Joseph S. DiMartino |

Clifford L. Alexander |

Whitney I. Gerard |

Nathan Leventhal |

George L. Perry |

Benaree Pratt Wiley |

Gordon J. Davis |

|

ICAF |

2002 |

2002 |

2003 |

2009 |

2003 |

2009 |

2012 |

|

IPMMF |

1997 |

1997 |

2003 |

2009 |

2003 |

2009 |

2012 |

|

IRF |

2008 |

2008 |

2008 |

2009 |

2008 |

2009 |

2012 |

|

DIGF |

1995 |

2003 |

1993 |

2009 |

1992 |

2009 |

2012 |

|

DLA |

1995 |

2003 |

1973 |

2009 |

1989 |

2009 |

2012 |

|

DOF |

2000 |

2000 |

2003 |

2009 |

2003 |

2009 |

2012 |

|

PSIMBF |

1995 |

2003 |

1989 |

2009 |

1990 |

2009 |

2012 |

|

SIGF |

1995 |

2003 |

1989 |

2009 |

1990 |

2009 |

2012 |

|

WDMMF |

1995 |

2003 |

1989 |

2009 |

1990 |

2009 |

2012 |

|

DF |

1995 |

2003 |

1973 |

2009 |

1989 |

2009 |

2012 |

|

DTCF |

1995 |

1981 |

2003 |

2009 |

2003 |

2009 |

2012 |

|

Each board member has been a Dreyfus Family of Funds board member for over ten years. Additional information about each board member follows (supplementing the information provided in the table above) that describes some of the specific experiences, qualifications, attributes or skills that each board member possesses which the board believes has prepared them to be effective board members. The board believes that the significance of each board member's experience, qualifications, attributes or skills is an individual matter (meaning that experience that is important for one board member may not have the same value for another) and that these factors are best evaluated at the board level, with no single board member, or particular factor, being indicative of board effectiveness. However, the board believes that board members need to have the ability to critically review, evaluate, question and discuss information provided to them, and to interact effectively with fund management, service providers and counsel, in order to exercise effective business judgment in the performance of their duties; the board believes that its members satisfy this standard. Experience relevant to having this ability may be achieved through a board member's educational background; business, professional training or practice (e.g., medicine, accounting or law), public service or academic positions; experience from service as a board member (including the board for the funds) or as an executive of investment funds, public companies or significant private or not-for-profit entities or other organizations; and/or other life experiences. The charter for the board's nominating committee contains certain other

I-2

factors considered by the committee in identifying and evaluating potential board member nominees. To assist them in evaluating matters under federal and state law, the board members are counseled by their independent legal counsel, who participates in board meetings and interacts with the Manager, and also may benefit from information provided by the Manager's counsel; counsel to the funds and to the board have significant experience advising funds and fund board members. The board and its committees have the ability to engage other experts as appropriate. The board evaluates its performance on an annual basis.

Independent Board Members

· Joseph S. DiMartino – Mr. DiMartino has been the Chairman of the Board of the funds in the Dreyfus Family of Funds for over 15 years. From 1971 through 1994, Mr. DiMartino served in various roles as an employee of Dreyfus (prior to its acquisition by a predecessor of BNY Mellon in August 1994 and related management changes), including portfolio manager, President, Chief Operating Officer and a director. He ceased being an employee or director of Dreyfus by the end of 1994. From July 1995 to November 1997, Mr. DiMartino served as Chairman of the Board of The Noel Group, a public buyout firm; in that capacity, he helped manage, acquire, take public and liquidate a number of operating companies. From 1986 to 2010, Mr. DiMartino served as a Director of the Muscular Dystrophy Association.