UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended | |||||

| Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from __________ to __________ | |||||

Commission File Number: 1-7891

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (952 ) 887-3131

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: NONE

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☒ Yes ☐ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

As of January 31, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of voting and non-voting common stock held by non-affiliates of the registrant was $7,523,208,549 (based on the closing price of $62.35 as reported on the New York Stock Exchange as of that date).

As of September 8, 2023, 121,242,187 shares of the registrant’s common stock, par value $5.00 per share, were outstanding.

Documents Incorporated by Reference

DONALDSON COMPANY, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| Page | ||||||||

PART I

Item 1. Business

The Company

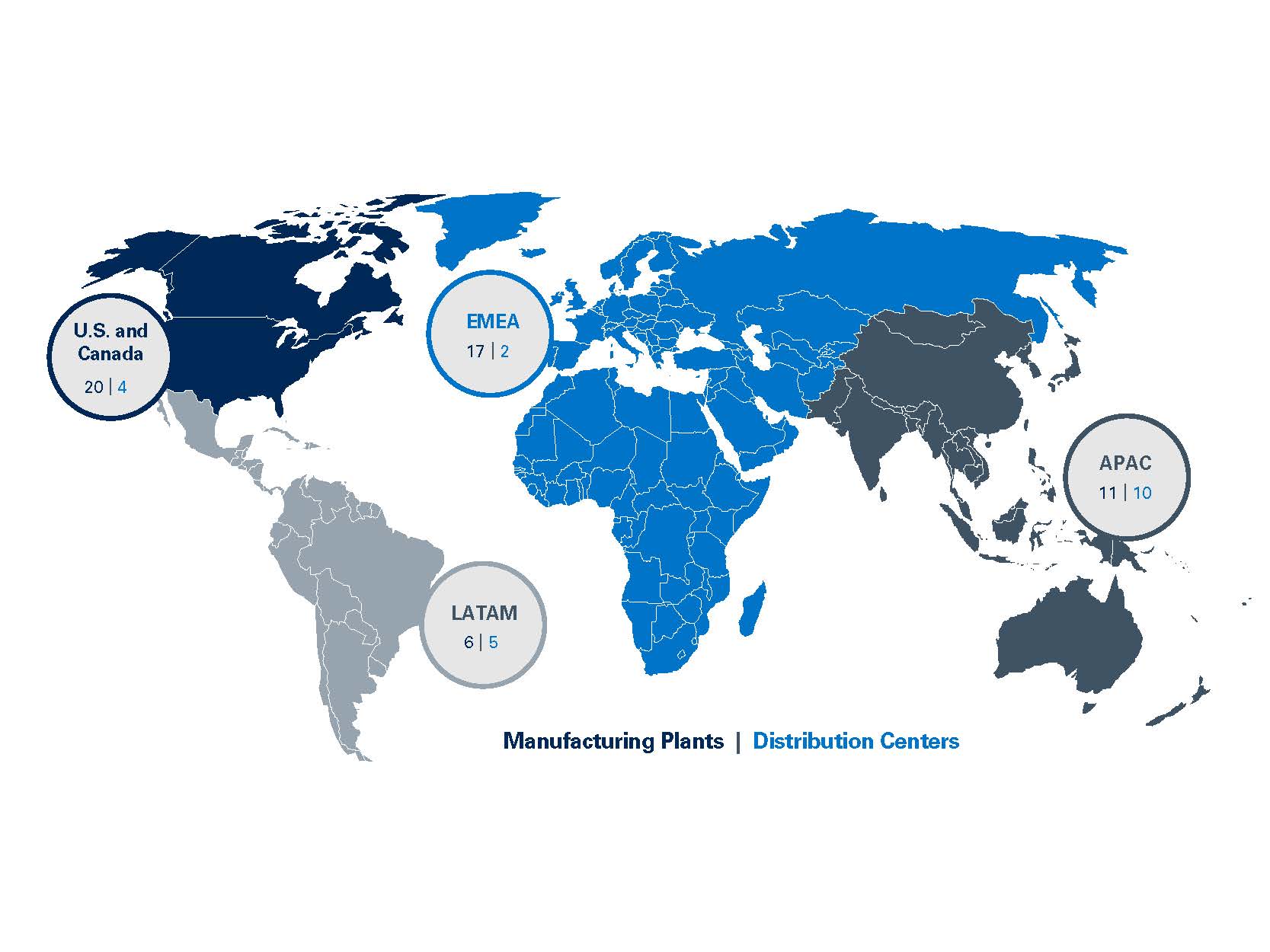

Founded in 1915, Donaldson Company, Inc. (the Company or Donaldson) is a global leader in technology-led filtration products and solutions, serving a broad range of industries and advanced markets. Donaldson’s diverse skilled employees at over 150 locations, 75 of which are manufacturing and/or distribution centers, on six continents partner with customers — from small business owners to the world’s largest original equipment manufacturer (OEM) brands — to solve complex filtration challenges. Customers choose Donaldson’s filtration solutions due to their stringent performance requirements and need for reliability.

Donaldson’s four regions and their contributing share of fiscal year 2023 revenue are as follows: the U.S. and Canada 42.7%; Europe, Middle East and Africa (EMEA) 29.4%; Asia Pacific (APAC) 17.7%; and Latin America (LATAM) 10.2%. Below are the Company’s manufacturing and distribution centers by region.

Strategic Priorities

The company has three primary strategic priorities to drive profitable growth. Below are each of the priorities and areas of focus related to each priority.

Extend Market Access - Grow Addressable Market by Extending Presence Across Adjacencies

•Significantly grow presence in bioprocessing via acquisitions with newly created stand-alone Life Sciences segment

•Strengthen position across alternative power solutions through increased focus and introduction of innovative and differentiated products

Expand Technologies and Solutions - Leverage Foundational Filtration Capabilities to Expand Best-in-class Technology and Service Offerings

1

•Expand Industrial Solutions connected service offerings while transitioning from a subscription model to a service model to gain additional aftermarket share

•Broaden battery vent offering to capture growing electronic vehicle (EV) opportunities

•Enhance digital experience through stronger data integration and navigation capabilities

Pursue Strategic Acquisitions - Accelerate Long-term Growth Through Strategic Acquisitions in High-margin Areas

•Strengthen presence in bioprocessing with disruptive technologies

•Penetrate underserved markets and expand service offerings

Reportable Segments

The Company’s reportable segments are Mobile Solutions, Industrial Solutions and Life Sciences.

The Mobile Solutions segment represents 63.4% of net sales, is organized based on a combination of customers and products and consists of the Off-Road, On-Road and Aftermarket business units. Within these business units, products consist of replacement filters for both air and liquid filtration applications and filtration housings for new equipment production and systems related to exhaust and emissions. Applications include air filtration systems, fuel, lube and hydraulic systems, emissions systems and sensors, indicators and monitoring systems. Mobile Solutions sells to original equipment manufacturers (OEMs) in the construction, mining, agriculture and transportation end markets and to independent distributors and OEM dealer networks.

The Industrial Solutions segment represents 29.6% of net sales, is organized based on product type and consists of the Industrial Air Filtration, Industrial Gasses, Industrial Hydraulics, Power Generation and Aerospace and Defense business units. Within our industrial portfolio, Donaldson provides the widest product offering in the market to industrial customers consisting of equipment, ancillary components, replacement parts, performance monitoring and service globally, that cost-effectively enhances productivity and manufacturing efficiency. Industrial Air Filtration, Industrial Gasses and Industrial Hydraulics products consist of dust, fume and mist collectors, compressed air and industrial gasses purification systems, hydraulic and lubricated rotating filtration applications as well as gas and liquid filtration for industrial processes. Power Generation products consist of air inlet systems and filtration sold to gas compression, power generation and natural gas liquification industries. Aerospace and Defense products consist of air, fuel, lubrication and hydraulic filtration for fixed-wing and rotorcraft aerospace applications and ground defense vehicle and naval platforms. Industrial Solutions businesses sell through multiple channels which include OEMs, distributors and direct-to-consumer in some markets.

The Life Sciences segment represents 7.0% of net sales and is organized by end market, including the Bioprocessing, Food and Beverage, Medical Device, Vehicle Electrification, Microelectronics and Disk Drive business units. Our products include gas and liquid filtration, bioprocessing equipment (including bioreactors, fermenters and filtration skids), bioprocessing consumables, (including membrane chromatography devices, reagents and filters) and specialized air and gas filtration systems for hard disk drive, semiconductor and electric vehicle applications. Life Sciences primarily sells to large OEMs and directly to various end users requiring cell growth, separation, purification, high purity filtration and device protection.

2

Diverse Product Groups

The Company sells a diverse group of products within each segment and the business units within the segments. Below are the diverse product groups across the Company’s three segments represented as a percentage of total fiscal 2023 net sales.

Mobile Solutions

Air Filtration

Air filtration systems are vital for safeguarding engine components against abrasive wear caused by dust particles. These systems play a pivotal role in supporting agricultural, construction and mining machinery, as well as commercial vehicles. Donaldson's air filtration solutions are globally renowned, featuring the standard in pleated cellulose filters. The company also offers advanced air filtration technologies, including PowerCore® and Ultra-Web®. PowerCore® filtration technology surpasses standard pleated cellulose filters in efficiency and compactness, making it the preferred choice for OEMs’ engines and equipment. Ultra-Web® media technology delivers robust filtration in the harshest environments, such as high-temperature and humid conditions frequently encountered by diesel, turbine, hybrid and other powered engines. Our Ultra-Web® HD media technology further enhances our fine fiber performance by ensuring consistent inter-fiber spacing at a microscopic level. This makes it ideal for extreme fine dust environments, commonly found in mining and high soot industries.

Fuel and Lube

Fuel and lube systems achieve optimal operations when contaminants are removed. The various components of the engine impacted include fuel injectors, valves, pumps, bearings and actuators. Fuel filters include primary and secondary particulate filters, coalescing fuel water separators, barrier fuel water separators and all-in-one filtration systems. The Company’s technology includes Synteq®™ XP filtration technology, which offers significantly higher fuel system protection and longer life under dynamic application conditions compared to commercially available alternatives. In addition, Donaldson’s Synteq® DRY and Synteq® XP coalescing technologies remove significantly more water in real-world conditions than current barrier or coalescing filters on the market. Fuel and lube filtration supports agricultural, construction and mining machinery and commercial vehicles.

Hydraulic

Hydraulic products provide filtration solutions typically for the same equipment that is filtered by fuel and lube systems. Applications include a suction strainer to protect the pump, high pressure filters, a charge pump or transmission filter, a return-line filter prior to the reservoir and a breather filter located on the reservoir.

3

The Duramax® filter, the Company’s primary mobile hydraulics filter, is renowned for its achievement of higher pressure in a spin-on configuration, allowing it to be designed on systems where other more costly, harder-to-service options were previously used. The Duramax® filter is combined with Synteq®™ XP media, a synthetic option for high performance. Hydraulics Systems supports agricultural, construction and mining machinery and transportation markets.

Emissions

Emissions products include sound-reducing mufflers used on machinery and vehicles, diesel-powered machinery and commercial vehicles. Emission control systems include diesel particulate filters, exhaust fluid mixers and catalytic reduction substrates to reduce emissions of particulate matter, nitrogen oxides and other greenhouse gases. Emissions products support agricultural, construction and mining machinery industries, as well as transportation markets.

Industrial Solutions

Industrial Air Filtration

Industrial air filtration equipment collects particles through an innovative bag house, or a cartridge style collector, which provides higher air-to-media capacity. Customers are supported through a global network of channel partners and service centers, which provide a quality customer experience during the design, installation, use, maintenance and repair of the equipment. Technology and features are continually added, such as the Internet-of-Things technology branded as iCue™, which is being integrated into product design to further improve product performance and better connect Donaldson with its end market customers, enabling additional service opportunities. Donaldson expanded its presence in the industrial service market with its acquisition in 2022 of Pearson Arnold Industrial Services (PAIS) headquartered in the U.S. PAIS provides equipment, parts and services for dust, mist and fume collection systems, industrial fans and compressed air systems.

Industrial dust, fume and mist collectors and filters are used within major industries including metals, mining, transportation, chemicals, food and beverage, pharmaceuticals and construction materials. For example, materials transformed in manufacturing, such as metal grinding, plasma cutting, mixing and welding, can create air contamination that can inhibit the production environment, which can be collected and filtered by Donaldson’s products.

Industrial Gasses

Industrial gasses provides solutions for challenging industrial gas purification objectives with premium filtration, drying and purification products. This includes delivering dust and particle collectors for air compressors at the inlet and output of air compressors and lube, fuel and air/oil separators used in a manufacturing environment.

Major product categories include dryers, compressed air, gasses and steam. Filtration involved in liquids, sterile and condensation management are part of the portfolio as well. Industrial gasses products are used within major industries including metals, mining, transportation, chemicals and construction materials.

Industrial Hydraulics

Industrial hydraulics helps to solve customers’ toughest contamination challenges with premium filtration products for hydraulics and lubrication. Hydraulic oil is adversely affected by contaminants such as wear metals, particulate, water and oxidation by-products. Contaminated fluid reduces performance and shortens lives of various system components including valves, pumps, bearings and actuators. Industrial hydraulic applications include steel mills, paper mills, refineries, oil and gas exploration, plastic molding, general manufacturing and power generation. Industrial hydraulics also supports the OEM fluid power and lubrication systems that support those industries.

Power Generation

Power generation provides leading OEMs air inlet equipment systems that deliver filtration and air handling performance. Power Generation filtration components are custom-engineered air intake systems for gas turbines and industrial compressors, for both new and retrofit applications. Aftermarket filters and parts are used in a variety of applications including cartridge filters, panel and compact filters, pulse systems, inlet hood components, filter retention hardware and accessories. Power Generation filtration components are in power plants, oil and gas delivery systems, other industrial applications and refining and processing machinery.

Aerospace and Defense

Aerospace and defense products are specifically designed to protect critical systems from contamination to ensure proper and efficient operation. The filtration portfolio includes engine intake, cabin air, avionics air, fuel, lubrication and hydraulics. Applications are found on fixed wing aircraft, helicopters, ground defense vehicles, weapons systems and naval vessels.

Life Sciences

Food and Beverage

4

Donaldson’s food and beverage business provides filtration solutions that enable process and product integrity for food and beverage manufacturing and support development of sustainable foods. Key products and applications include sterile liquid, air and steam filtration, compressed air dryers, bioreactors and fermenters and tangential and direct flow filtration.

Other Life Sciences

Bioprocessing Equipment and Consumables

Donaldson’s bioprocessing business provides equipment and consumables to support the development and production of biologic drugs and genetic medicines, including mAbs mRNA and cell and gene therapies, along with many other applications that use a bioprocessing workflow.

In fiscal year 2023, Donaldson acquired Isolere Bio, Inc. (Isolere), headquartered in Durham, North Carolina and Univercells Technologies (UTEC), headquartered in Nivelles, Belgium.

•Isolere is an early-stage biotechnology company that has developed novel and proprietary IsoTag™ reagents used for the purification and streamlined manufacturing of biopharmaceuticals. Aimed initially at the purification of viral vectors used for cell and gene therapies, IsoTag™ reagents are designed to substantially improve product quality and purity with faster timelines compared to competing solutions.

•UTEC is a global producer of innovative biomanufacturing solutions for cell and gene therapy research, development and commercial manufacturing. UTEC’s product offering includes the unique scale-X™ single-use structured fixed-bed bioreactor for the intensified production of viruses used in cell and gene therapy, viral vaccines and other therapeutics. In addition, UTEC’s automated NevoLine™ Upstream platform incorporates industry-standard filtration to provide integrated up-and mid-stream processing capabilities in a single unit, driving productivity improvements, a reduction in operational footprints and greater consistency of results.

During fiscal year 2022, the Company acquired Solaris Biotechnology S.r.l. (Solaris), headquartered in Porto Mantovano, Italy and Purlogics LLC (Purlogics) headquartered in Greenville, South Carolina.

•Solaris designs and manufactures bioprocessing equipment, including bioreactors, fermenters and tangential flow filtration systems for use in pharma, food and beverage and many other applications that require bioprocess technology.

•Purilogics is an early-stage biotechnology company that has developed novel and proprietary Purexa membrane chromatography products used for the purification and streamlined manufacturing of biopharmaceuticals. Aimed initially at the purification of pDNA, mRNA and mAbs, Purilogics’ platform is able to address a wide range of biologics. Purilogics’ Purexa membranes have significant competitive advantages over traditional resin and monolith technologies, enabling improved productivity, speed and production costs.

Vehicle Electrification and Medical Device

Vehicle electrification and medical device equipment provide a broad range of filters that protect devices and enclosures from pressure fluctuation, liquids and harmful contaminants. Key products include battery, powertrain and headlight vents for electric vehicles as well as venting solutions for hearing aids, ostomy bags and implantable devices.

Microelectronics

Microelectronics delivers product filtration solutions for gas phase molecular contamination at fabrication, tool and point-of-use locations. It offers protection and filtering for a broad spectrum of contaminants that can degrade tools, affect critical processes and impact production yield, which enables increased processing speeds and miniaturization of semiconductors. Key products/applications include lithography process air filtration, point-of-use chemical filtration, compressed air dryers and liquid filtration.

Disk Drive

Disk drive delivers products that have advanced materials and absorbent technologies to control moisture and contaminants in microenvironments. Disk drive filters work in the background to help protect critical components in cloud computing: streaming, storage, sharing, gaming and business-to-business interaction. Key products/applications include particle filters, chemical filters and relative humidity control.

Key Growth Drivers

The key growth drivers within each segment are as follows:

•Mobile Solutions

◦Providing solutions to customers to address their higher performance requirements

5

◦Utilization of technology to improve efficiencies and fuel economies in all end markets

◦Increased activity in construction, agriculture and mining markets driven by expansion in living standards

•Industrial Solutions

◦Complementing automation trends through expanded connectivity applications

◦Industrial equipment designed for optimized energy consumption and carbon footprint reduction

◦Growing operational efficiency needs to reduce costs associated with maintenance and downtime

•Life Sciences

◦Increasing need for cell and gene therapy as well as membrane applications for disease treatment and cures

◦Growing customer preference for sustainable food and materials

◦Continued cloud demand and growing automation trends

Competition

Principal methods of competition in the Mobile Solutions, Industrial Solutions and Life Sciences segments are technology, innovation, price, geographic coverage, service and product performance. The Company participates in a number of highly competitive filtration markets in all segments. Donaldson believes it is a market leader within many of its product lines, specifically within its Off-Road and On-Road product lines for OEMs and in the Aftermarket business for replacement filters. The Mobile Solutions segment’s principal competitors include several large global competitors and many regional competitors, especially in the Aftermarket business. The Industrial Solutions segment’s principal competitors vary from country to country and range from large global competitors to a significant number of smaller competitors who compete in a specific geographical region or in a limited number of product applications. The Life Sciences segment’s principal competitors include several large global competitors as well as niche players in the individual markets served by the segment.

Raw Materials

The principal raw materials the Company uses are steel, filter media and petrochemical-based products including plastic, rubber and adhesive products. Purchased raw materials represent approximately 70% of the Company’s cost of sales. On an ongoing basis, the Company enters into selective supply arrangements with certain of its suppliers that allow the Company to reduce volatility in its costs. The Company strives to recover or offset all material cost increases through selective price increases to its customers and the Company’s cost reduction initiatives, which include material substitution, process improvement and product redesigns.

Manufacturing and Backlog

Backlog is one of many indicators of business conditions in the Company’s markets. However, it is not always indicative of future results for a number of reasons, including the timing of the receipt of orders, as well as product mix. Backlog orders expected to be delivered within 90 days as of July 31, 2023 and 2022 were $576.4 million and $658.5 million, respectively.

Seasonality

Many of the Company’s end markets are generally stronger in the second half of the Company’s fiscal year. In addition, the first half of the fiscal year contains more holiday periods, which typically include more customer plant closures.

Diversification

The Company’s results of operations are affected by conditions in the global economic and geopolitical environment. Under most economic conditions, the Company’s market diversification between the regions and various end markets it serves and diversification through its OEM and replacement parts customers has helped to limit the impact of weakness in any one product line, market or geography on the consolidated operating results of the Company.

Intellectual Capital

Research and Development

Investment in research and development strengthens the Company’s material science capabilities and supports development of new and improved products and solutions. Research and development expenses include scientific research costs such as salaries, facility costs, testing, technical information technology and administrative expenditures. Research and development expenses are for the application of scientific advances to the development of new and improved products and their uses. Substantially all research and development is performed in-house. During the years ended July 31, 2023, 2022 and 2021, the Company spent $78.1 million, $69.1 million and $67.8 million, respectively, on research and development activities, which was 2.3%, 2.1% and 2.4% of net sales, respectively.

6

Intellectual Property

The Company owns a broad range of intellectual property rights relating to its products and services, which it considers in the aggregate to constitute a valuable asset. These include patents, trade secrets, trademarks, copyrights and other forms of intellectual property rights in the U.S. and a number of foreign countries. The Company protects its innovations arising from research and development through patent filings and owns a portfolio of over 2,800 issued patents, including utility and design patents. The Company also owns various trademarks related to its products and services including Donaldson® and the turbo D logo, Ultra-Web®, PowerCore®, Downflo®, Torit®, Synteq® XP, LifeTec®, iCue™ and Tetratex®, among others. No single intellectual property right is responsible for protecting the Company’s products.

Government Regulations

Donaldson is subject to a wide variety of local, state and federal governmental laws and regulations in the U.S., as well as the laws and regulations of other countries in which Donaldson conducts business, including securities laws, tax laws, data privacy, employment and pension-related laws, competition laws, U.S. and foreign export and trade laws, the Foreign Corrupt Practices Act ("FCPA") and similar worldwide anti-bribery laws, government procurement regulations and laws governing improper business practices. Donaldson strives to comply with applicable laws and regulations. We have robust internal controls, quality management systems, and management systems related to compliance that govern our internal actions and mitigate our risk of non-compliance. We also have safeguards established to identify non-compliance concerns through internal and external audits and risk assessments, as well as an ethics helpline reporting system. Failure to comply with these regulations, however, could lead to fines and other penalties.

We are subject to local, state, federal and international environmental, safety and health laws and regulations concerning, among other things, emissions to air; discharges to water; the generation, handling, storage, transportation, treatment and disposal of waste materials; and the use of raw materials and goods such as iron, steel aluminum, electricity, natural gas and hydrogen. The operation of manufacturing plants unavoidably entails environmental, safety and health risks, and we could incur material unanticipated costs or liabilities in the future if any of these risks were realized in ways or to an extent that we did not anticipate.

We believe that we operate in compliance, in all material respects, with applicable environmental laws and regulations. Compliance with environmental laws and regulations requires continuing management effort and expenditures. We have incurred, and will continue to incur, costs and capital expenditures to comply with these laws and regulations and to obtain and maintain the necessary permits and licenses. We believe that the cost of complying with environmental laws and regulations will not have a material effect on our results of operations, financial condition or cash flows but cannot assure that material compliance-related costs and expenses may not arise in the future. For example, future adoption of new or amended environmental laws, regulations or requirements or other circumstances could require us to incur costs and expenses that may have a material effect, but cannot be presently anticipated.

We believe that policies, practices and procedures have been properly designed to prevent unreasonable risk of material environmental damage arising from our operations. In fiscal 2023, the Company did not experience any material effect on its capital expenditures, results of operations or financial condition due to compliance with government rules regulating the discharge of materials into the environment or otherwise relating to the protection of the environment, nor does it expect such impact during fiscal 2024.

We are also required to comply with increasingly complex and changing laws and regulations enacted to protect business and personal data in the U.S. and other jurisdictions regarding privacy, data protection and data security, including those related to the collection, storage, use, transmission and protection of personal information and other consumer, customer, vendor or employee data. Such privacy and data protection laws and regulations, including with respect to the European Union’s General Data Protection Regulation ("GDPR"), the Brazilian General Data Protection Law, and the California Consumer Privacy Act of 2018 ("CCPA"), and the interpretation and enforcement of such laws and regulations, are continuously developing and evolving and there is significant uncertainty with respect to how compliance with these laws and regulations may evolve and the costs and complexity of future compliance.

For a discussion of the risks associated with these laws and regulations, see Part I, Item 1A, "Risk Factors."

Human Capital Resources

As of July 31, 2023, the Company had approximately 13,000 full time employees, of which 56% were in production related roles. When necessary, the Company’s production facilities augment their resources utilizing contingent labor. For over 100 years, the Company has been making a difference with customers, employees, investors, suppliers and communities through a collaborative and diverse workplace where every employee matters. The Company prides itself on providing innovative technologies and solutions backed by talented and dedicated employees guided by its core values.

7

Core Values

The Company’s purpose is to advance filtration for a cleaner world. The principles that guide this purpose are as follows:

•act with integrity - deliver on commitments and be accountable for actions;

•engage and empower people - have a richly diverse and inclusive culture and provide opportunities for people to grow, build successful careers and make meaningful contributions;

•deliver for customers - understand, anticipate and prioritize customers’ needs, delivering differentiated products and solutions that enable their success;

•cultivate innovation - pursue innovation in everything from continuous improvement in processes to breakthrough solutions that create value and competitive advantage;

•operate safely and sustainably - committed to safety in the workplace, being good stewards of natural resources and reducing environmental impacts; and

•enrich communities - share time, resources and talent to make a positive impact.

Culture

The Company is comprised of a diverse global team. With a broad base of capabilities, cultures and perspectives, employees reflect the communities they serve. The Company promotes a collaborative workplace. By working together, the Company’s employees can better understand and meet the customers’ needs. Every role is recognized and individuals’ contributions have a direct impact. The Company fosters learning and growth. To help employees continue to learn and succeed in their careers, while keeping pace with a rapidly changing global marketplace, the Company provides multiple learning opportunities and programs, including online courses and customized development plans.

Diversity, Equity and Inclusion

The Company values and welcomes employees’ unique views and contributions, knowing that together the global team can better understand and meet the needs of its customers and communities. The Company participates in outreach efforts for organizations focused on diversity and supporting educational opportunities to underserved students and communities.

Benefits

The Company is committed to the health, wealth and work-life balance of employees and offers competitive financial compensation packages that may include both base pay and bonus elements in addition to competitive benefits packages to help support individuals and their families. To support the health and well-being of employees in the U.S. and their dependents, the Company offers subsidized health insurance and also provides an employee assistance program. In other parts of the world, the Company offers social programs specific to the countries in which it operates. To help employees provide and prepare for the future, the Company provides several other financial and non-financial benefits.

Employment

The Company attracts a qualified workforce through an inclusive and accessible recruiting process that utilizes online recruiting platforms, campus outreach, internships, recruitment vendor partners, job fairs and other recruitment tools. The Company seeks to retain employees by offering competitive wages, benefits and training opportunities, as well as promoting a safe and healthy workplace. The Company is committed to treating all applicants and employees with the same high level of respect regardless of their gender, ethnicity, religion, national origin, age, marital status, political affiliation, sexual orientation, veteran status, gender identity, disability or other protected status. It is the Company’s policy to comply with all applicable state, local and international laws governing non-discrimination in employment in every location where it operates. This compliance includes terms and conditions of employment, which cover recruiting, hiring, placement, promotion, termination, layoff, recall, transfer, leaves of absence, compensation and training.

Health and Safety

The Company empowers its employees and provides the knowledge and tools needed to make safe decisions and mitigate risks. Every employee is responsible for identifying and managing exposure to health and safety hazards and harmful environmental impacts. A variety of training methods are available to fulfill these requirements, including online learning, training, coaching or mentoring and group discussions and activities.

Community Service

Generations of the Company’s employees and their families give their time, energy and aid to various philanthropic efforts, addressing the needs of our local communities and helping transform lives. Organizations are supported in partnership with the Donaldson Foundation and through numerous volunteer events.

8

Available Information

The Company makes its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other information, including amendments to those reports, available free of charge through its website at ir.donaldson.com, as soon as reasonably practicable after it electronically files such material with, or furnishes such material to, the Securities and Exchange Commission (SEC). These filings are available on the SEC’s website at www.sec.gov. Also available on the Company’s website are corporate governance documents, including the Company’s Code of Business Conduct and Business Conduct Help Line, Corporate Governance Guidelines, Director Independence Standards, Audit Committee Charter, Human Resources Committee Charter and Corporate Governance Committee Charter. The information contained on the Company’s website is not incorporated by reference into this Annual Report and should not be considered as part of this report.

Executive Officers

Our executive officers of the Company as of August 31, 2023 were as follows:

| Name | Age | Positions and Offices Held | First Calendar Year Appointed as an Executive Officer | |||||||||||||||||

| Amy C. Becker | 58 | Chief Legal Officer and Corporate Secretary | 2014 | |||||||||||||||||

| Guillermo Briseño | 56 | President, Industrial Solutions | 2022 | |||||||||||||||||

| Tod E. Carpenter | 64 | Chairman, President and Chief Executive Officer | 2008 | |||||||||||||||||

| Andrew Dahlgren | 52 | President, Life Sciences | 2022 | |||||||||||||||||

| Sheila G. Kramer | 64 | Chief Human Resources Officer | 2015 | |||||||||||||||||

| Richard B. Lewis | 51 | President, Mobile Solutions | 2017 | |||||||||||||||||

| Scott J. Robinson | 56 | Chief Financial Officer | 2015 | |||||||||||||||||

| Thomas R. Scalf | 57 | President, Enterprise Operations and Supply Chain | 2014 | |||||||||||||||||

Ms. Becker was appointed to Chief Legal Officer and Corporate Secretary in November 2022. Ms. Becker joined the Company in 1998 and held positions as Senior Counsel and Assistant Corporate Secretary; Assistant General Counsel; and Vice President, General Counsel and Secretary. Prior to joining the Company, Ms. Becker was an attorney for Dorsey and Whitney, LLP from 1991 to 1995 and was a Project Manager and Corporate Counsel for Harmon, Ltd. from 1995 to 1998.

Mr. Briseño was appointed President, Industrial Solutions in November 2022. Mr. Briseño joined the Company in 2003 and has held various positions, including IAF District Manager; IFS Latin America Business Manager; Industrial Sales Director Latin America; Managing Director Latin America; and Vice President, Latin America.

Mr. Carpenter was appointed Chairman, President and Chief Executive Officer in November 2017. Mr. Carpenter joined the Company in 1996 and has held various positions, including Director of Operations, Gas Turbine Systems; General Manager, Gas Turbine Systems; General Manager, Industrial Filtration Systems; Vice President, Global Industrial Filtration Systems; Vice President, Europe and Middle East; and Senior Vice President, Engine Products. Mr. Carpenter was appointed Chief Operating Officer in April 2014 and President and Chief Executive Officer in April 2015.

Mr. Dahlgren was appointed President, Life Sciences in November 2022. Mr. Dahlgren joined the Company in 1994 and has held various positions, including Manager Business Development, Disk Drive; Director of Business Development, IVS, Semiconductor, Fuel Cell; General Manager, Engine Air; General Manager, GTS; Vice President, GTS and Special Applications; and Vice President, Asia Pacific.

Ms. Kramer was appointed Chief Human Resources Officer in November 2022. Ms. Kramer joined the Company in 2015 as Vice President, Human Resources. Prior to joining the Company, Ms. Kramer was Vice President, Human Resources for Taylor Corporation, a print and graphics media company, from 2013 until September 2015. Prior to that, Ms. Kramer spent 22 years at Lifetouch, Inc. in various human resources roles, including Corporate Vice President, Human Resources from 2009 to 2013.

Mr. Lewis was appointed President, Mobile Solutions in November 2022. Mr. Lewis joined the Company in 2002 and has held various positions, including Plant Manager; Director of Operations; General Manager, Liquid Filtration; General Manager, Operations; Vice President, Global Operations; and Senior Vice President, Global Operations.

Mr. Robinson was appointed Chief Financial Officer and joined the Company in 2015. Prior to joining the Company, Mr. Robinson was the Chief Financial Officer for Imation Corp., a global data storage and information security company, from 2014 to 2015. During his 11 years with Imation Corp., he also served as the Investor Relations Officer, Corporate Controller and Chief Accounting Officer.

9

Mr. Scalf was appointed President, Enterprise Operations and Supply Chain in November 2022. Mr. Scalf joined the Company in 1989 and has held various positions, including Plant Manager; Manager, Site Integration; Director of Operations; General Manager, Exhaust and Emissions; General Manager, Industrial Filtration Solutions Americas; Vice President, Global Industrial Air Filtration; and Senior Vice President, Engine Products.

Item 1A. Risk Factors

The Company’s (we, our or us) business is subject to various risks and uncertainties. The following discussion outlines what we believe to be the risk factors that could materially and adversely affect our business, reputation, financial condition and results of operations. These risk factors should be considered with the Company’s cautionary comments related to forward-looking statements when evaluating information provided in this Annual Report. Risks not currently known to the Company, or which the Company currently believes are immaterial, may also impair the Company’s business, reputation, financial condition and results of operations. The Company periodically reviews its strategies, processes and controls with respect to risk identification, assessment and mitigation with the audit committee of the Company’s board of directors.

Macroeconomic and Geopolitical Risks

Global Operations - we have a broad footprint and global operations may present challenges.

We have operations throughout the world. Our stability, growth and profitability are subject to a number of risks of doing business globally including the following:

•political and military events, including the rise of nationalism and support for protectionist policies;

•tariffs, trade barriers and other trade restrictions;

•legal and regulatory requirements, including import, export, defense regulations, anti-corruption laws and foreign exchange controls;

•potential difficulties in staffing and managing local operations;

•credit risk of local customers and distributors;

•deterioration in economic conditions, including the effect of inflation on our customers and suppliers;

•difficulties in protecting our intellectual property; and

•local economic, political and social conditions.

Due to the global reach of our operations, our business is subject to a complex system of commercial and trade laws, regulations and policies, including those related to data privacy, trade compliance, anti-corruption and anti-bribery. We experience exposure to and costs of complying with, these laws and regulations. Our global subsidiaries, joint venture partners and affiliates are governed by laws, rules and business practices that differ from those of the U.S. Our compliance programs may not adequately prevent or deter our employees, agents, distributors, suppliers and other third parties with whom we do business from violating laws, regulations or standards. We may incur defense costs, fines, penalties, damage to our reputation and business disruptions, which could result in an adverse effect on our results of operations, financial condition and cash flows.

Business Disruption - unexpected events, including natural disasters, may increase our cost of doing business or disrupt our operations.

There could be an occurrence of one or more unexpected events, including a terrorist attack, war or civil unrest, a weather event, a natural disaster, a climate-related event, a pandemic or other catastrophe in countries in which we operate or in which our suppliers are located. Such an event could result in physical damage to and complete or partial closure of one or more of our headquarters, manufacturing facilities or distribution centers, temporary or long-term disruption in the supply of component products from some local and international suppliers, disruption in the transport of our products to customers and disruption of information systems. Existing insurance coverage may not provide protection for all costs that may arise from any such event. Any disruption in our operations could have an adverse impact on our ability to meet our customer needs or may require us to incur additional expense in order to produce sufficient inventory. Certain unexpected events could adversely impact our business, results of operations, financial condition and cash flows.

10

Operational Risks

Supply Chain - unavailable raw materials, significant demand fluctuations and material cost inflation have and could continue to have an impact on our sales and cost of sales.

We obtain raw materials, including steel, filter media, petroleum-based products and other components from third-party suppliers. We often concentrate our sourcing of some materials from one supplier or a few suppliers. We rely, in part, on our suppliers to ensure they meet required quality and delivery standards. An unanticipated delay in delivery by our suppliers could result in the inability to deliver our products on time and to meet the expectations of our customers. We have experienced and could continue to experience, an increase in the costs of doing business, including increasing raw material prices and transportation costs, which have and could continue to have an adverse impact on our business, results of operations, financial condition and cash flows.

Personnel - our success has been and could in the future be affected, if we are not able to attract, engage, train and retain qualified personnel.

Our success depends in large part on our ability to identify, recruit, engage, train and retain highly skilled, qualified and diverse personnel globally and successfully execute management transitions at leadership levels of the Company. There is competition for talent with market-leading skills and capabilities in new technologies. Additionally, in some locations we have experienced labor shortages causing significant wage inflation and workplace availability. We may not be able to attract and retain qualified personnel and it may be difficult for us to compete effectively, which could adversely impact our business, results of operations, financial condition and cash flows.

Operations - complexity of manufacturing could cause inability to meet demand and result in the loss of customers.

Our ability to fulfill customer orders is dependent on our manufacturing and distribution operations. Although we forecast demand, additional plant capacity takes significant time to bring online and thus, unexpected or extreme changes in demand could result in longer lead times. We cannot guarantee we will be able to adjust manufacturing capacity, in the short-term, to meet higher customer demand. Efficient operations require streamlining processes to maintain or reduce lead times, which we may not be capable of achieving. Unacceptable levels of service for key customers may result if we are not able to fulfill orders on a timely basis or if product quality, warranty or safety issues result from compromised production. We may not be able to adjust our production schedules to reflect changes in customer demand on a timely basis. Due to the complexity of our manufacturing operations, we may be unable to timely respond to fluctuations in demand, which could adversely impact our business, results of operations, financial condition and cash flows.

Products - maintaining a competitive advantage requires consistent investment with uncertain returns.

We operate in highly competitive markets and have numerous competitors that are already be well-established in those markets. We expect our competitors to continue to improve the design and performance of their products and to introduce new products that could be competitive in both price and performance. We believe we have certain technological advantages over our competitors, but maintaining these advantages requires us to consistently invest in research and development, sales and marketing and customer service and support. There is no guarantee we will be successful in maintaining these advantages and we could encounter the commoditization of our key products. We make investments in new technologies that address increased performance and regulatory requirements around the globe. There is no guarantee we will be successful in completing development or achieving sales of these products or that the margins on such products will be acceptable. A competitor’s successful product innovation could reach the market before ours or gain broader market acceptance, which could adversely impact our business, results of operations, financial condition and cash flows.

Evolving Customer Needs - disruptive technologies may threaten our growth in certain industries.

Certain industry market trends guide decisions we make in operating the Company and our growth could be threatened by disruptive technologies. We may be adversely impacted by changes in technology that could reduce or eliminate the demand for our products. These risks include wider adoption of technologies providing alternatives to diesel engines such as electrification of equipment or other alternative power solutions. Such disruptive innovation could create new markets and displace existing companies and products, resulting in significantly negative consequences for the Company. If we do not properly address future customer needs, we may be slower to adapt to such disruption, which could adversely impact our business, results of operations, financial condition and cash flows.

11

Competition - we participate in highly competitive markets with pricing pressure.

The businesses and product lines in which we participate are very competitive and we risk losing business based on a wide range of factors, including price, technology, performance, reliability and availability, geographic coverage and customer service. Our customers continue to seek technological innovation, productivity gains, competitive prices, reliability and availability from us and their other suppliers. Additionally, we sell through a variety of channels (e.g., OEM, dealer, distributor and eCommerce) in a diverse set of highly competitive filtration markets. The variability complicates the supply chain, affects working capital needs, requires balance between relationships and drives a more targeted sales force. As a result of these and other factors, we may not be able to compete effectively, which could adversely impact our business, results of operations, financial condition and cash flows.

Customer Concentration and Retention - a number of our customers operate in similar cyclical industries. Changes in economic conditions in these industries could impact our sales.

No customer accounted for 10% or more of our net sales in fiscal 2023, 2022 or 2021. However, a number of our customers are concentrated in similar cyclical industries (e.g., construction, agriculture, mining, oil and gas, transportation, power generation and disk drive), resulting in additional risk based on their respective economic conditions. Our success is also dependent on retaining key customers, which requires us to successfully manage relationships and anticipate the needs of our customers in the channels in which we sell our products. Changes in economic conditions could materially and adversely impact our business, results of operations, financial condition and cash flows.

Productivity Improvements - if we do not successfully manage productivity improvements, we may not realize the expected benefits.

Our financial projections assume certain ongoing productivity improvements as a key component of our business strategy to, among other things, contain operating expenses, maintain competitiveness, increase operating efficiencies and align manufacturing capacity to demand. We may not be able to realize the expected benefits and cost savings if we do not successfully execute these plans while continuing to invest in business growth. Such cost savings may not otherwise be realized or other difficulties could be encountered, which could adversely impact our business, results of operations, financial condition and cash flows.

Environmental, Social and Governance (ESG) - achieving commitments could result in additional costs and our inability to achieve them could have an adverse impact on our reputation and performance.

We periodically communicate our strategies, commitments and targets related to ESG matters, including greenhouse gas (GHG) emissions and diversity, equity and inclusion through the issuance of our ESG report. Although we intend to meet these strategies, commitments and targets, we may be unable to achieve them due to impacts on resources, operational costs and technological advancements. In addition, standards and processes for measuring and reporting GHG emissions and other sustainability metrics may change over time, result in inconsistent data or result in significant revisions to our strategies, commitments and targets, or our ability to achieve them. Any scrutiny of our carbon emissions or other sustainability disclosures, our failure to achieve related strategies, commitments and targets or failure to meet sustainability requirements could negatively impact our reputation as well as the demand for our products and adversely affect our business, results of operations, financial condition and cash flow.

Acquisitions, Divestitures and Other Strategic Transactions - the execution of our acquisitions, divestitures and other strategic transactions may not provide the desired return on investment.

We have made and continue to pursue acquisitions and divestitures and may pursue joint ventures, strategic investments and other similar strategic transactions. Acquisitions, joint ventures and strategic investments could negatively impact our profitability and financial condition due to operating and integration inefficiencies, the incurrence of debt, contingent liabilities and amortization of expenses related to intangible assets. There are also a number of other risks involved in acquisitions including the potential loss of key customers or employees, difficulties in assimilating the acquired operations and the diversion of management’s time and attention away from other business matters. Further, during the pendency of a proposed transaction, we may be subject to risks related to a decline in the business and the risk the transaction may not close. Divestitures may involve significant challenges and risks, such as difficulty separating out portions of our business or the potential loss of revenue or negative impacts on margins. The divestitures may also result in ongoing financial or legal proceedings, such as retained liabilities, which could have an adverse impact on our business, results of operations, financial condition and cash flows.

12

Cybersecurity Risks

Cybersecurity Risks - vulnerability of our information technology systems and security.

We have many information technology systems that are important to the operation of our business, some of which are managed by third parties. These systems are used to process, transmit and store electronic information and to manage or support a variety of business processes and activities, which are critical to our operations. We could encounter difficulties in developing new systems, maintaining and upgrading our existing systems, managing access to these systems and preventing information security breaches. Additionally, we collect and store sensitive data, including intellectual property and proprietary business information, in data centers and on information technology networks.

Our data is subject to a variety of U.S. and international laws and regulations that pertain to the collection and handling of personal information. The laws require us to notify governmental authorities and affected individuals of data breaches involving certain personal information. These laws include the European GDPR and the CCPA. Regulatory litigation or actions that could impose significant penalties may be brought against us in the event of a breach of data or alleged non-compliance with such laws and regulations.

Information technology security threats are increasing in frequency and sophistication; to date, none of the threats faced by the Company have been material. We have invested in protection to prevent these threats; however, there can be no assurance our efforts will prevent all potential failures, cybersecurity attacks or breaches of our systems. These threats pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. Should such an attack succeed, it could lead to the compromise of confidential information, manipulation and destruction of data, defective products, production downtimes and operation disruptions. The occurrence of any of these events could adversely affect our reputation and could result in litigation, regulatory action, potential liability, increased costs and operational consequences of implementing further data protection matters. The Company maintains insurance coverage for various cybersecurity and business continuity risks, however, there can be no guarantee all costs or losses incurred will be fully insured. Vulnerabilities could lead to significant additional expenses and an adverse effect on our reputation, business, results of operations, financial condition and cash flows.

Legal and Regulatory Risks

Intellectual Property - demand for our products may be affected by new entrants that copy our products and/or infringe on our intellectual property.

The ability to protect and enforce intellectual property rights varies across jurisdictions. Where possible, we seek to preserve our intellectual property rights through patents. These patents have a limited life and, in some cases, have expired or will expire in the near future. Competitors and others may also initiate litigation to challenge the validity of our intellectual property rights or allege that we infringe their intellectual property rights. We may be required to pay substantial damages if it is determined our products infringe on their intellectual property rights. We may also be required to develop an alternative, non-infringing product that could be costly and time-consuming, or acquire a license on terms that are unfavorable to us.

Protecting or defending against such claims could significantly increase our costs and divert management’s time and attention away from other business matters, which could adversely impact our business, results of operations, financial condition and cash flows.

Legal and Regulatory - costs associated with lawsuits, investigations or complying with laws and regulations.

We are subject to many laws and regulations in the jurisdictions in which we operate. We routinely incur costs in order to comply with these laws and regulations. We may be adversely impacted by new or changing laws and regulations that affect both our operations and our ability to develop and sell products that meet our customers’ requirements. We are involved in various product liability, product warranty, intellectual property, environmental claims and other legal proceedings that arise in and outside of the ordinary course of our business. We are subject to increasingly stringent laws and regulations in the countries in which we operate, including those governing the environment (e.g., emissions to air; discharges to water; and the generation, handling, storage, transportation, treatment and disposal of waste materials; and the use of raw materials and goods such as iron, steel aluminum, electricity, natural gas and hydrogen) and data protection and privacy. It is not possible to predict the outcome of investigations and lawsuits and we could incur judgments, fines or penalties or enter into settlements of lawsuits and claims that could have an adverse effect on our reputation, business, results of operations, financial condition and cash flows in any particular period. In addition, we may not be able to maintain our insurance at a reasonable cost or in sufficient amounts to protect us against any losses.

13

Financial Risks

Currency - an unfavorable fluctuation in foreign currency exchange rates could impact our results of operations.

We have operations in many countries, with a substantial portion of our annual revenue earned in currencies other than the U.S. dollar. We face transactional and translational risks associated with the fluctuations in foreign currency exchange rates. Transactional risk arises from changes in the value of cash flows denominated in different currencies. This can be caused by supply chains that cross borders resulting in revenues and costs being in different currencies. Translational risk arises from the remeasurement of our financial statements. In addition, decreased value of local currency may make it difficult for some of our customers, distributors and end users to purchase our products. Each of our subsidiaries reports its results of operations and financial position in its relevant functional currency, which is then translated into U.S. dollars. This translated financial information is included in our Consolidated Financial Statements. Significant fluctuations of the U.S. dollar in comparison to the foreign currencies of our subsidiaries during discrete periods may have a negative impact on our business, results of operations, financial condition and cash flows.

Liquidity - changes in the capital and credit markets may negatively affect our ability to access financing to support strategic initiatives.

Disruption of the global financial and credit markets may have an effect on our long-term liquidity and financial condition. There can be no assurance the cost or availability of future borrowings will not be impacted by future capital market disruptions. Some of our existing borrowings contain covenants to maintain certain financial ratios that, under certain circumstances, could restrict our ability to incur additional indebtedness, make investments and other restricted payments, create liens and sell assets.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

The Company’s corporate headquarters and corporate research facilities are located in Minneapolis, Minnesota. The Company also has administrative and engineering offices, as well as research facilities in the regions of EMEA, APAC and LATAM. The Company’s manufacturing and distribution activities are located throughout the world and the Company considers its properties to be suitable for their present purposes, well-maintained and in good operating condition.

Item 3. Legal Proceedings

The Company records provisions when it is probable a liability has been incurred and the amount of the loss can be reasonably estimated. Claims and litigation are reviewed quarterly and provisions are taken or adjusted to reflect the status of a particular matter. The Company believes the estimated liability in its Consolidated Financial Statements for claims or litigation is adequate and appropriate for the probable and estimable outcomes. Liabilities recorded were not material to the Company’s financial position, results of operations or liquidity. The Company believes it is remote that the settlement of any of the currently identified claims or litigation will be materially in excess of what is accrued.

Item 4. Mine Safety Disclosures

Not applicable.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’s common stock, par value $5.00 per share, is traded on the New York Stock Exchange under the symbol “DCI.” As of September 8, 2023, there were 1,168 registered stockholders of common stock.

To determine the appropriate level of dividend payouts, the Company considers recent and projected performance across key financial metrics, including earnings, cash flow from operations and total debt.

14

Information in connection with purchases made by, or on behalf of, the Company or any affiliated purchaser of the Company, of shares of the Company’s common stock during the three months ended July 31, 2023 was as follows:

| Period | Total Number of Shares Purchased | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs | ||||||||||||||||||||||

| May 1 - May 31, 2023 | 176,000 | $ | 63.80 | 176,000 | 3,104,805 | |||||||||||||||||||||

| June 1 - June 30, 2023 | 187,091 | $ | 60.40 | 187,091 | 2,917,714 | |||||||||||||||||||||

| July 1 - July 31, 2023 | — | $ | — | — | 2,917,714 | |||||||||||||||||||||

| Total | 363,091 | $ | 62.05 | 363,091 | 2,917,714 | |||||||||||||||||||||

On May 31, 2019, the Board of Directors authorized the repurchase of up to 13.0 million shares of the Company’s common stock. This repurchase authorization is effective until terminated by the Board of Directors. The Company has remaining authorization to repurchase 2.9 million shares under this plan. There were no repurchases of common stock made outside of the Company’s current repurchase authorization during the three months ended July 31, 2023. While not considered repurchases of shares, the Company does at times withhold shares that would otherwise be issued under stock-based awards to cover the withholding of taxes due as a result of exercising stock options or payment of stock-based awards.

The table set forth in Part III, Item 12, “Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters” of this Annual Report is also incorporated herein by reference.

15

The graph below compares the cumulative total stockholder return on the Company’s common stock for the last five fiscal years with the cumulative total return of the Standard & Poor’s (S&P) 500 Stock Index and the S&P Industrial Machinery Index. The graph and table assume the investment of $100 in each of the Company’s common stock and the specified indexes at the beginning of the applicable period and assume the reinvestment of all dividends.

COMPARISON OF FIVE YEAR CUMULATIVE TOTAL RETURN

Among Donaldson Company Inc., the S&P 500 Index

and the S&P Industrial Machinery Index

| As of July 31, | ||||||||||||||||||||||||||||||||||||||

| 2018 | 2019 | 2020 | 2021 | 2022 | 2023 | |||||||||||||||||||||||||||||||||

| Donaldson Company, Inc. | $ | 100.00 | $ | 106.43 | $ | 104.74 | $ | 145.55 | $ | 121.51 | $ | 142.53 | ||||||||||||||||||||||||||

| S&P 500 Stock Index | $ | 100.00 | $ | 107.99 | $ | 120.90 | $ | 164.96 | $ | 157.31 | $ | 177.78 | ||||||||||||||||||||||||||

| S&P Industrial Machinery Index | $ | 100.00 | $ | 107.28 | $ | 112.27 | $ | 162.08 | $ | 139.66 | $ | 174.48 | ||||||||||||||||||||||||||

Item 6. [Reserved]

Reserved.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

In the second quarter of fiscal 2023, the Company established a new segment reporting structure which resulted in three reportable segments: Mobile Solutions, Industrial Solutions and Life Sciences. We have reflected this change in all historical periods presented. See Note 19. Segment Reporting in the Notes to Consolidated Financial Statements, included in Item 8 of Part II in this Annual Report for further detail of this change.

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (MD&A) provides a comparison of the Company’s results of operations, liquidity and capital resources for the years ended July 31, 2023 and 2022, as well as revenue and segment specific comparisons for 2021. A discussion of the changes in the Company’s results of operations and liquidity and capital resources for the year ended July 31, 2022 from July 31, 2021 for non-segment specific comparisons can be found in Part II, “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” of the Company’s Annual Report on Form 10-K for the year ended July 31, 2022 (the “2022 Annual Report”), which was filed with the SEC on September 23, 2022.

16

The MD&A should be read in conjunction with the Company’s Consolidated Financial Statements and Notes included in Item 8 of this Annual Report. This discussion contains forward-looking statements that involve risks and uncertainties. The Company’s actual results could differ materially from those anticipated in these forward-looking statements as a result of various factors, including those discussed elsewhere in this Annual Report, particularly Item 1A, “Risk Factors” and in the Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995.

Throughout this MD&A, the Company refers to measures used by management to evaluate performance, including a number of financial measures that are not defined under generally accepted accounting principles (GAAP) in the U.S. Excluding foreign currency translation from net sales and net earnings (i.e. constant currency) are not measures of financial performance under GAAP; however, the Company believes they are useful in understanding its financial results and provide comparable measures for understanding the operating results of the Company between different fiscal periods. Reconciliations within this MD&A provide more details on the use and derivation of these measures.

Overview

Founded in 1915, Donaldson Company, Inc. is a global leader in technology-led filtration products and solutions, serving a broad range of industries and advanced markets. Donaldson’s diverse skilled employees at over 150 locations, 75 of which are manufacturing and/or distribution centers, on six continents partner with customers — from small business owners to the world’s largest original equipment manufacturer (OEM) brands — to solve complex filtration challenges. Customers choose Donaldson’s filtration solutions due to their stringent performance requirements and need for reliability.

The Company’s operating segments are Mobile Solutions, Industrial Solutions and Life Sciences. The Mobile Solutions segment is organized based on a combination of customers and products and consists of the Off-Road, On-Road and Aftermarket business units. Within these business units, products consist of replacement filters for both air and liquid filtration applications and filtration housings for new equipment production and systems related to exhaust and emissions. Applications include air filtration systems, fuel, lube and hydraulic systems, emissions systems and sensors, indicators and monitoring systems. Mobile Solutions sells to OEMs in the construction, mining, agriculture and transportation end markets and to independent distributors and OEM dealer networks.

The Industrial Solutions segment is organized based on product type and consists of the Industrial Air Filtration, Industrial Gasses, Industrial Hydraulics, Power Generation and Aerospace and Defense business units. Within our Industrial Solutions portfolio, Donaldson provides a wide product offering in the market to industrial customers consisting of equipment, ancillary components, replacement parts, performance monitoring and service globally, that cost-effectively enhance productivity and manufacturing efficiency. Industrial Air Filtration, Industrial Gasses and Industrial Hydraulics products consist of dust, fume and mist collectors, compressed air and industrial gasses purification systems, hydraulic and lubricated rotating equipment applications as well as gas and liquid filtration for industrial processes. Power Generation products consist of air inlet systems and filtration sold to gas compression, power generation and natural gas liquification industries. Aerospace and Defense products consist of air, fuel, lubrication and hydraulic filtration for fixed-wing and rotorcraft aerospace applications and ground defense vehicle and naval platforms. Industrial Solutions sells through multiple channels which include OEMs, distributors and direct-to-consumer in some markets.

The Life Sciences segment is organized by end market and consists of the Bioprocessing Equipment and Consumables, Food and Beverage, Vehicle Electrification and Medical Device, Microelectronics and Disk Drive business units. Within these business units, products consist of micro-environment gas and liquid filtration for food and beverage and industrial processes, bioprocessing equipment, including bioreactors and fermenters, bioprocessing consumables including chromatography devices, reagents and filters, polytetrafluoroethylene membrane-based products, as well as specialized air and gas filtration systems for applications including hard disk drives, semiconductor manufacturing, sensors, battery systems and powertrain components. Life Sciences primarily sells to large OEMs and directly to various end users requiring cell growth, separation, purification, high purity filtration and device protection.

The Company’s results of operations are affected by conditions in the global economic and geopolitical environment. Under most economic conditions, the Company’s market diversification between its diesel engine end markets, its global end markets, its diversification through technology and its OEM and replacement parts customers has helped to limit the impact of weakness in any one product line, market or geography on the consolidated operating results of the Company.

Operating Environment

Inflation

While inflation was not significant in the fourth quarter or the twelve months of fiscal 2023, as compared to the prior year, the Company continues to experience the effects of the prior year inflation related to raw materials and other expenses, including labor and energy. These inflationary pressures have had an adverse impact on the Company’s profit margins throughout the twelve months of fiscal 2023 when compared to the prior year, however they have been generally mitigated by pricing actions primarily implemented in the prior year.

17

Consolidated Results of Operations

Operating Results

Operating results were as follows (in millions, except per share amounts):

| Year Ended July 31, | ||||||||||||||||||||||||||

| 2023 | % of net sales | 2022 | % of net sales | |||||||||||||||||||||||

| Net sales | $ | 3,430.8 | $ | 3,306.6 | ||||||||||||||||||||||

| Cost of sales | 2,270.2 | 66.2 | % | 2,239.2 | 67.7 | % | ||||||||||||||||||||

| Gross profit | 1,160.6 | 33.8 | 1,067.4 | 32.3 | ||||||||||||||||||||||

| Selling, general and administrative | 602.3 | 17.6 | 554.8 | 16.8 | ||||||||||||||||||||||

| Research and development | 78.1 | 2.3 | 69.1 | 2.1 | ||||||||||||||||||||||

| Operating expenses | 680.4 | 19.8 | 623.9 | 18.9 | ||||||||||||||||||||||

| Operating income | 480.2 | 14.0 | 443.5 | 13.4 | ||||||||||||||||||||||

| Interest expense | 19.2 | 0.6 | 14.9 | 0.4 | ||||||||||||||||||||||

| Other income, net | (7.7) | (0.2) | (9.8) | (0.3) | ||||||||||||||||||||||

| Earnings before income taxes | 468.7 | 13.7 | 438.4 | 13.3 | ||||||||||||||||||||||

| Income taxes | 109.9 | 3.2 | 105.6 | 3.2 | ||||||||||||||||||||||

| Net earnings | $ | 358.8 | 10.5 | % | $ | 332.8 | 10.1 | % | ||||||||||||||||||

| Net earnings per share (EPS) – diluted | $ | 2.90 | $ | 2.66 | ||||||||||||||||||||||

Geographic Net Sales by Origination

Net sales, generally disaggregated by location where the customer’s order was received, were as follows (in millions):

| Year Ended July 31, | ||||||||||||||||||||||||||

| 2023 | % of net sales | 2022 | % of net sales | |||||||||||||||||||||||

| U.S. and Canada | $ | 1,464.7 | 42.7 | % | $ | 1,336.8 | 40.5 | % | ||||||||||||||||||

| Europe, Middle East and Africa (EMEA) | 1,007.8 | 29.4 | 963.6 | 29.1 | ||||||||||||||||||||||

| Asia Pacific (APAC) | 608.8 | 17.7 | 669.0 | 20.2 | ||||||||||||||||||||||

| Latin America (LATAM) | 349.5 | 10.2 | 337.2 | 10.2 | ||||||||||||||||||||||

| Total Company | $ | 3,430.8 | 100.0 | % | $ | 3,306.6 | 100.0 | % | ||||||||||||||||||

Impact of Foreign Currency Translation on Net Sales

Net sales were impacted by fluctuations in foreign currency exchange rates. The impact was as follows (in millions):

| Year Ended July 31, | ||||||||||||||

| 2023 | 2022 | |||||||||||||

| Prior year net sales | $ | 3,306.6 | $ | 2,853.9 | ||||||||||

| Change in net sales excluding translation | 237.6 | 539.8 | ||||||||||||

Impact of foreign currency translation(1) | (113.4) | (87.1) | ||||||||||||

| Current year net sales | $ | 3,430.8 | $ | 3,306.6 | ||||||||||

(1)The impact of foreign currency translation was calculated by translating current fiscal year foreign currency net sales into U.S. dollars using the average foreign currency exchange rates for the prior fiscal year.

Net Sales

Net sales for the year ended July 31, 2023 increased $124.2 million, or 3.8% from fiscal 2022, reflecting higher sales in the Mobile Solutions segment of $48.3 million, or 2.3% and the Industrial Solutions segment of $113.7 million, or 12.6%, and decreased sales in the Life Sciences segment of $37.8 million, or 13.5%. Foreign currency translation decreased net sales by $113.4 million, reflecting decreases in the Mobile Solutions, Industrial Solutions and Life Sciences segments of $73.8 million, $26.8 million and $12.7 million, respectively. In fiscal 2023, the Company’s net sales increased primarily from higher pricing, partially offset by a negative impact from foreign currency translation.