Securities Act of 1933 Registration No. 002-77909

Investment Company Act of 1940 Registration No. 811-03480

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 x

o Pre-Effective Amendment No. ______

x Post-Effective Amendment No. 85

and

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 x

x Amendment No. 85

Fidelity Oxford Street Trust

(Exact Name of Registrant as Specified in Charter)

245 Summer Street, Boston, Massachusetts 02210

(Address of Principal Executive Offices)(Zip Code)

Registrant’s Telephone Number: 617-563-7000

Marc Bryant, Secretary

245 Summer Street

Boston, Massachusetts 02210

(Name and Address of Agent for Service)

It is proposed that this filing will become effective on May 25, 2017 pursuant to paragraph (b) at 5:30 p.m. Eastern Time.

| Fidelity® Commodity Strategy Fund |

| Class/Ticker |

| F/ FIHTX |

Shares are offered only to certain other Fidelity® funds and accounts.

Prospectus

May 25, 2017

|

The Securities and Exchange Commission and the Commodity Futures Trading Commission have not approved or disapproved these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense. | 245 Summer Street, Boston, MA 02210 |

Contents

|

Fund Summary |

Fidelity® Commodity Strategy Fund |

|

|

Fund Basics |

Investment Details |

|

|

Valuing Shares |

||

|

Shareholder Information |

Additional Information about the Purchase and Sale of Shares |

|

|

Account Policies |

||

|

Dividends and Capital Gain Distributions |

||

|

Tax Consequences |

||

|

Fund Services |

Fund Management |

|

|

Fund Distribution |

||

|

Appendix |

Prior Performance of a Similar Fund |

Fund Summary

Fund/Class:

Fidelity® Commodity Strategy Fund/F

Investment Objective

The fund seeks to provide investment returns that correspond to the performance of the commodities market.

Fee Table

The following table describes the fees and expenses that may be incurred when you buy and hold shares of the fund.

Shareholder fees

| (fees paid directly from your investment) | None |

Annual Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

| Management fee | 0.40% | |

| Distribution and/or Service (12b-1) fees | None | |

| Other expenses(a) | 0.00% | |

| Acquired fund fees and expenses(b),(c) | 0.08% | |

| Total annual operating expenses | 0.48% | |

| Fee waiver and/or expense reimbursement(c) | 0.08% | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 0.40% |

(a) Based on estimated amounts for the current fiscal year.

(b) Acquired fund fees and expenses based on estimated amounts for the current fiscal year.

(c) The fund may invest in a wholly-owned subsidiary. The subsidiary has entered into a separate contract with Geode Capital Management, LLC (Geode) for the management of its portfolio pursuant to which the subsidiary pays Geode a fee at an annual rate of 0.30% of its net assets. The subsidiary also pays certain other expenses including custody fees. Geode has contractually agreed to waive the fund's management fee in an amount equal to the management fee paid to Geode by the subsidiary. This arrangement will remain in effect for at least one year from the effective date of the prospectus, and will remain in effect thereafter as long as Geode's contract with the subsidiary is in place. If Geode's contract with the subsidiary is terminated, Geode, in its sole discretion, may discontinue the arrangement.

This example helps compare the cost of investing in the fund with the cost of investing in other funds.

Let's say, hypothetically, that the annual return for shares of the fund is 5% and that your shareholder fees and the annual operating expenses for shares of the fund are exactly as described in the fee table. This example illustrates the effect of fees and expenses, but is not meant to suggest actual or expected fees and expenses or returns, all of which may vary. For every $10,000 you invested, here's how much you would pay in total expenses if you sell all of your shares at the end of each time period indicated:

| 1 year | $41 |

| 3 years | $128 |

Portfolio Turnover

The fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual operating expenses or in the example, affect the fund's performance.

Principal Investment Strategies

- Normally investing in commodity-linked derivative instruments, short-term investment-grade debt securities, cash, and cash equivalents.

- Investing up to 25% of assets in a wholly-owned subsidiary that invests in commodity-linked total return swaps based on the value of commodities or commodities indexes and in other commodity-linked derivative instruments.

- Managing the fund to track an index chosen to represent the commodities market, as well as short-term investment-grade debt securities, which as of the fund's inception was the Bloomberg Commodity Index Total Return℠.

- Investing in domestic and foreign issuers.

- Engaging in commodity-linked derivatives transactions that have a leveraging effect on the fund.

- Investing in Fidelity's central funds (specialized investment vehicles used by Fidelity® funds to invest in particular security types or investment disciplines).

Principal Investment Risks

- Interest Rate Changes. Interest rate increases can cause the price of a debt security to decrease.

- Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market.

- Financial Services Exposure. Changes in government regulation and interest rates and economic downturns can have a significant negative effect on issuers in the financial services sector, including the price of their securities or their ability to meet their payment obligations.

- Subsidiary Risk. Investment in an unregistered subsidiary is not subject to the investor protections of the Investment Company Act of 1940 (1940 Act) and is subject to the risks associated with investing in derivatives and commodity-linked investing in general. Changes in tax and other laws could negatively affect investments in the subsidiary.

- Prepayment. The ability of an issuer of a debt security to repay principal prior to a security's maturity can cause greater price volatility if interest rates change.

- Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. A decline in the credit quality of an issuer or a provider of credit support or a maturity-shortening structure for a security can cause the price of a security to decrease.

- Leverage Risk. Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly.

- Commodity-Linked Investing. The value of commodities and commodity-linked investments may be affected by the performance of the overall commodities markets as well as weather, political, tax, and other regulatory and market developments. Commodity-linked investments may be more volatile and less liquid than the underlying commodity, instruments, or measures.

In addition, the fund is considered non-diversified and can invest a greater portion of assets in securities of a smaller number of individual issuers than a diversified fund. As a result, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a more diversified fund.

An investment in the fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You could lose money by investing in the fund.

Performance

Performance history will be available for the fund after the fund has been in operation for one calendar year.

Visit www.fidelity.com for more recent performance information.

Investment Adviser

Geode Capital Management, LLC (Geode) (the Adviser) is the fund's manager.

Portfolio Manager(s)

Bobe Simon (senior portfolio manager) has managed the fund since May 2017.

Louis Bottari (portfolio manager) has managed the fund since May 2017.

Eric Matteson (portfolio manager) has managed the fund since May 2017.

Patrick Waddell (portfolio manager) has managed the fund since May 2017.

Purchase and Sale of Shares

Shares are offered only to certain other Fidelity® funds and accounts.

The price to sell one share is its net asset value per share (NAV). Shares will be sold at the NAV next calculated after an order is received in proper form.

The fund is open for business each day the New York Stock Exchange (NYSE) is open.

There is no purchase minimum for Class F shares.

Tax Information

Distributions you receive from the fund are subject to federal income tax and generally will be taxed as ordinary income or capital gains, and may also be subject to state or local taxes, unless you are investing through a tax-advantaged retirement account (in which case you may be taxed later, upon withdrawal of your investment from such account).

Payments to Broker-Dealers and Other Financial Intermediaries

The fund, the Adviser, Fidelity Management & Research Company (FMR), Fidelity Distributors Corporation (FDC), and/or their affiliates may pay intermediaries, which may include retirement plan sponsors, administrators, or service-providers (who may be affiliated with the Adviser, FMR, or FDC), for the sale of fund shares and related services. These payments may create a conflict of interest by influencing your intermediary and your investment professional to recommend the fund over another investment. Ask your investment professional or visit your intermediary's web site for more information.

Fund Basics

Investment Details

Investment Objective

Fidelity® Commodity Strategy Fund seeks to provide investment returns that correspond to the performance of the commodities market.

Principal Investment Strategies

The Adviser normally expects to invest the fund's assets in commodity-linked derivative instruments, short-term investment-grade debt securities, cash, and cash equivalents. Commodities are assets that have physical properties, such as oil and other energy products, metals, and agricultural products. Commodity-linked derivative instruments include commodity-linked notes; total return swaps, options, and forward contracts based on the value of commodities or commodities indexes; and commodity futures. The fund intends to provide exposure to the commodities market but will not be managed to take delivery of physical commodities. The fund may divest of commodity-linked derivative instruments to avoid delivery.

The fund seeks to track the performance of an index chosen by the Adviser to represent the commodities market, as well as short-term investment-grade debt securities. As of the fund's inception, the Adviser was using the Bloomberg Commodity Index Total Return℠ to represent the commodities market.

The Adviser may invest up to 25% of the fund's assets in a wholly-owned subsidiary of the fund organized under the laws of the Cayman Islands (the Subsidiary). The Subsidiary is managed by the same investment adviser as the fund. The Subsidiary is expected to invest directly in total return swaps based on the value of commodities or commodities indexes and in other commodity-linked derivative instruments, including options and forward contracts based on the value of commodities or commodities indexes, and commodity futures. The Subsidiary will not be managed to take delivery of physical commodities, and may divest of certain commodity-linked derivative instruments (namely commodity futures) to avoid delivery.

The Adviser may invest the fund's assets in securities of foreign issuers in addition to securities of domestic issuers.

Because the fund is considered non-diversified, the Adviser may invest a significant percentage of the fund's assets in a single issuer.

In addition to the principal investment strategies discussed above, the fund may also lend securities to broker-dealers or other institutions to earn income. When the Adviser believes that suitable commodity-linked derivative instruments are not available, or during other unusual market conditions, the Adviser may leave all or a significant portion of the fund's assets invested in cash, cash equivalents, or short-term investment-grade debt securities.

If the Adviser's strategies do not work as intended, the fund may not achieve its objective.

Description of Principal Security Types

Debt securities are used by issuers to borrow money. The issuer usually pays a fixed, variable, or floating rate of interest, and must repay the amount borrowed, usually at the maturity of the security. Some debt securities, such as zero coupon bonds, do not pay current interest but are sold at a discount from their face values. Debt securities include corporate bonds, government securities, repurchase agreements, money market securities, mortgage and other asset-backed securities, loans and loan participations, and other securities believed to have debt-like characteristics, including hybrids and synthetic securities.

Money market securities are high-quality, short-term securities that pay a fixed, variable, or floating interest rate. Securities are often specifically structured so that they are eligible investments for a money market fund. For example, in order to satisfy the maturity restrictions for a money market fund, some money market securities have demand or put features, which have the effect of shortening the security's maturity. Money market securities include bank certificates of deposit, bankers' acceptances, bank time deposits, notes, commercial paper, and U.S. Government securities. Certain issuers of U.S. Government securities, including Fannie Mae, Freddie Mac, and the Federal Home Loan Banks, are sponsored or chartered by Congress but their securities are neither issued nor guaranteed by the U.S. Treasury.

Commodity-linked derivative instruments are indexed to all or part of a commodities index or to a single commodity. Commodity-linked derivative instruments include debt securities and other investments whose maturity values, interest rates, or returns are determined by reference to a commodities index and are designed to provide exposure to the entire index, and may include other investments that provide exposure to less than the entire commodities index or to a single commodity. Commodity-linked derivative instruments may be positively or negatively indexed, meaning their maturity value may be structured to increase or decrease as commodity values change.

Derivatives are investments whose values are tied to an underlying asset, instrument, currency, or index. Derivatives include futures, options, forwards, and swaps, such as interest rate swaps (exchanging a floating rate for a fixed rate), total return swaps (exchanging a floating rate for the total return of an index, security, or other instrument or investment) and credit default swaps (buying or selling credit default protection).

Forward-settling securities involve a commitment to purchase or sell specific securities when issued, or at a predetermined price or yield. Payment and delivery take place after the customary settlement period.

Central funds are special types of investment vehicles created by Fidelity for use by Fidelity® funds and other advisory clients. Central funds incur certain costs related to their investment activity (such as custodial fees and expenses), but do not pay additional management fees. The investment results of the portions of the fund's assets invested in the central funds will be based upon the investment results of those funds.

Principal Investment Risks

Many factors affect the fund's performance. The fund's share price and yield change daily based on changes in market conditions and interest rates and in response to other economic, political, or financial developments. The fund's reaction to these developments will be affected by the types and maturities of securities in which the fund invests, the financial condition, industry and economic sector, and geographic location of an issuer, and the fund's level of investment in the securities of that issuer. In addition, because the fund may invest a significant percentage of assets in a single issuer, the fund's performance could be closely tied to that one issuer and could be more volatile than the performance of more diversified funds. When you sell your shares they may be worth more or less than what you paid for them, which means that you could lose money by investing in the fund.

The following factors can significantly affect the fund's performance:

Interest Rate Changes. Debt securities, including money market securities, have varying levels of sensitivity to changes in interest rates. In general, the price of a debt security can fall when interest rates rise and can rise when interest rates fall. Securities with longer maturities and certain types of securities, such as the securities of issuers in the financial services sector, can be more sensitive to interest rate changes, meaning the longer the maturity of a security, the greater the impact a change in interest rates could have on the security's price. Short-term and long-term interest rates do not necessarily move in the same amount or the same direction. Short-term securities tend to react to changes in short-term interest rates, and long-term securities tend to react to changes in long-term interest rates. Securities with floating interest rates can be less sensitive to interest rate changes, but may decline in value if their interest rates do not rise as much as interest rates in general. Securities whose payment at maturity is based on the movement of all or part of an index and inflation-protected debt securities may react differently from other types of debt securities.

Foreign Exposure. Foreign securities, securities issued by U.S. entities with substantial foreign operations, and entities providing credit support or a maturity-shortening structure that are located in foreign countries can involve additional risks relating to political, economic, or regulatory conditions in foreign countries. These risks include fluctuations in foreign exchange rates; withholding or other taxes; trading, settlement, custodial, and other operational risks; and the less stringent investor protection and disclosure standards of some foreign markets. All of these factors can make foreign investments more volatile than U.S. investments. In addition, foreign markets can perform differently from the U.S. market.

Global economies and financial markets are becoming increasingly interconnected, which increases the possibilities that conditions in one country or region might adversely impact issuers or providers in, or foreign exchange rates with, a different country or region.

Industry Exposure. Market conditions, interest rates, and economic, regulatory, or financial developments could significantly affect a single industry or a group of related industries, and the securities of companies in that industry or group of industries could react similarly to these or other developments. In addition, from time to time, a small number of companies may represent a large portion of a single industry or a group of related industries as a whole, and these companies can be sensitive to adverse economic, regulatory, or financial developments.

The commodities industries can be significantly affected by the level and volatility of commodity prices; the rate of commodity consumption; world events including international monetary and political developments; import controls, export controls, and worldwide competition; exploration and production spending; and tax and other government regulations and economic conditions.

Financial Services Exposure. Financial services companies are highly dependent on the supply of short-term financing and can be sensitive to changes in government regulation and interest rates and to economic downturns in the United States and abroad. These events can significantly affect the price of issuers’ securities as well as their ability to make payments of principal or interest or otherwise meet obligations on securities or instruments for which they serve as guarantors or counterparties.

Subsidiary Risk. The investments held by the Subsidiary are generally similar to those that are permitted to be held by the fund and, therefore, the Subsidiary is subject to risks similar to those of the fund, including the risks associated with investing in derivatives and commodity-linked investing in general. Because the Subsidiary is organized under Cayman Islands law and is not registered under the 1940 Act, the Subsidiary is not subject to the investor protections of the 1940 Act. The fund relies on a private letter ruling received by other Fidelity® funds from the Internal Revenue Service with respect to its investment in the Subsidiary. Changes in U.S. or Cayman Islands laws could result in the inability of the fund and/or the Subsidiary to operate as described in this prospectus.

Prepayment. Many types of debt securities, including mortgage securities, are subject to prepayment risk. Prepayment risk occurs when the issuer of a security can repay principal prior to the security's maturity. Securities subject to prepayment can offer less potential for gains during a declining interest rate environment and similar or greater potential for loss in a rising interest rate environment. In addition, the potential impact of prepayment features on the price of a debt security can be difficult to predict and result in greater volatility.

Issuer-Specific Changes. Changes in the financial condition of an issuer or counterparty, changes in specific economic or political conditions that affect a particular type of security or issuer, and changes in general economic or political conditions can increase the risk of default by an issuer or counterparty, which can affect a security's or instrument's credit quality or value. Entities providing credit support or a maturity-shortening structure also can be affected by these types of changes, and if the structure of a security fails to function as intended, the security could decline in value.

Leverage Risk. Derivatives and forward-settling securities involve leverage because they can provide investment exposure in an amount exceeding the initial investment. Leverage can magnify investment risks and cause losses to be realized more quickly. A small change in the underlying asset, instrument, or index can lead to a significant loss. Assets segregated to cover these transactions may decline in value and are not available to meet redemptions. Forward-settling securities also involve the risk that a security will not be issued, delivered, or paid for when anticipated. Government legislation or regulation could affect the use of these transactions and could limit a fund's ability to pursue its investment strategies.

Commodity-Linked Investing. The performance of commodities, commodity-linked swaps, futures, notes, and other commodity-related investments may depend on the performance of individual commodities and the overall commodities markets and on other factors that affect the value of commodities, including weather, political, tax, and other regulatory and market developments. Commodity-linked instruments may be leveraged. For example, the price of a three-times leveraged commodity-linked note may change by a magnitude of three for every percentage change (positive or negative) in the value of the underlying index. Commodity-linked investments may be hybrid instruments that can have substantial risk of loss with respect to both principal and interest. Commodity-linked investments may be more volatile and less liquid than the underlying commodity, instruments, or measures, and may be subject to the credit risks associated with the issuer or counterparty. As a result, returns of commodity-linked investments may deviate significantly from the return of the underlying commodity, instruments, or measures. In addition, the regulatory and tax environment for commodity linked derivative instruments is evolving, and changes in the regulation or taxation of such investments may have a material adverse impact on the fund. Funds and advisers subject to Commodity Futures Trading Commission (CFTC) regulation are subject to additional regulatory requirements and may incur additional costs.

In response to market, economic, political, or other conditions, a fund may temporarily use a different investment strategy for defensive purposes. If the fund does so, different factors could affect its performance and the fund may not achieve its investment objective.

Fundamental Investment Policies

The following is fundamental, that is, subject to change only by shareholder approval:

Fidelity® Commodity Strategy Fund seeks to provide investment returns that correspond to the performance of the commodities market.

Valuing Shares

The fund is open for business each day the NYSE is open.

NAV is the value of a single share. Fidelity normally calculates NAV as of the close of business of the NYSE, normally 4:00 p.m. Eastern time. The fund's assets normally are valued as of this time for the purpose of computing NAV. Fidelity calculates NAV separately for each class of shares of a multiple class fund.

NAV is not calculated and the fund will not process purchase and redemption requests submitted on days when the fund is not open for business. The time at which shares are priced and until which purchase and redemption orders are accepted may be changed as permitted by the Securities and Exchange Commission (SEC).

To the extent that the fund's assets are traded in other markets on days when the fund is not open for business, the value of the fund's assets may be affected on those days. In addition, trading in some of the fund's assets may not occur on days when the fund is open for business.

NAV is calculated using the values of the underlying central funds in which the fund invests. Shares of underlying central funds are valued at their respective NAVs. Other assets are valued primarily on the basis of market quotations, official closing prices, or information furnished by a pricing service. Certain short-term securities are valued on the basis of amortized cost. If market quotations, official closing prices, or information furnished by a pricing service are not readily available or, in FMR's opinion, are deemed unreliable for a security, then that security will be fair valued in good faith by FMR in accordance with applicable fair value pricing policies. For example, if, in FMR’s opinion, a security’s value has been materially affected by events occurring before a fund’s pricing time but after the close of the exchange or market on which the security is principally traded, then that security will be fair valued in good faith by FMR in accordance with applicable fair value pricing policies. Fair value pricing will be used for high yield debt securities when available pricing information is determined to be stale or for other reasons not to accurately reflect fair value.

Arbitrage opportunities may exist when trading in a portfolio security or securities is halted and does not resume before a fund calculates its NAV. These arbitrage opportunities may enable short-term traders to dilute the NAV of long-term investors. Securities trading in overseas markets present time zone arbitrage opportunities when events affecting portfolio security values occur after the close of the overseas markets but prior to the close of the U.S. market. Fair valuation of a fund's portfolio securities can serve to reduce arbitrage opportunities available to short-term traders, but there is no assurance that fair value pricing policies will prevent dilution of NAV by short-term traders.

Fair value pricing is based on subjective judgments and it is possible that the fair value of a security may differ materially from the value that would be realized if the security were sold.

Shareholder Information

Additional Information about the Purchase and Sale of Shares

As used in this prospectus, the term "shares" generally refers to the shares offered through this prospectus.

Frequent Purchases and Redemptions

The fund may reject for any reason, or cancel as permitted or required by law, any purchase orders, including transactions deemed to represent excessive trading, at any time.

Excessive trading of fund shares can harm shareholders in various ways, including reducing the returns to long-term shareholders by increasing costs to the fund (such as brokerage commissions or spreads paid to dealers who sell money market instruments), disrupting portfolio management strategies, and diluting the value of the shares in cases in which fluctuations in markets are not fully priced into the fund's NAV.

Because the fund is primarily offered for investment only to certain other Fidelity® funds, the potential for excessive or short-term disruptive purchases and sales is reduced. Accordingly, the Board of Trustees has not adopted policies and procedures designed to discourage excessive trading of fund shares and the fund accommodates frequent trading.

The fund has no limit on purchase transactions but may in its discretion restrict, reject, or cancel any purchases that, in the Adviser's opinion, may be disruptive to the management of the fund or otherwise not be in the fund's interests.

The fund reserves the right at any time to restrict purchases or impose conditions that are more restrictive on excessive trading than those stated in this prospectus.

The fund has no exchange privilege with any other fund.

Buying Shares

Eligibility

Shares are generally available only to investors residing in the United States.

Shares are offered only to certain other Fidelity® funds and accounts.

Price to Buy

The price to buy one share is its NAV. Shares are sold without a sales charge.

Shares will be bought at the NAV next calculated after an order is received in proper form.

Orders by funds of funds for which Fidelity serves as investment manager will be treated as received by the fund at the same time that the corresponding orders are received in proper form by the funds of funds.

The fund may stop offering shares completely or may offer shares only on a limited basis, for a period of time or permanently.

When you place an order to buy shares, note the following:

- All wires must be received in proper form by Fidelity at the fund's designated wire bank before the close of the Federal Reserve Wire System on the day of purchase or you could be liable for any losses or fees the fund or Fidelity has incurred or for interest and penalties.

- Under applicable anti-money laundering rules and other regulations, purchase orders may be suspended, restricted, or canceled and the monies may be withheld.

Selling Shares

The price to sell one share is its NAV.

Shares will be sold at the NAV next calculated after an order is received in proper form. Normally, redemptions will be processed by the next business day, but it may take up to seven days to pay the redemption proceeds if making immediate payment would adversely affect the fund.

Orders by funds of funds for which Fidelity serves as investment manager will be treated as received by the fund at the same time that the corresponding orders are received in proper form by the funds of funds.

When you place an order to sell shares, note the following:

- Redemptions may be suspended or payment dates postponed when the NYSE is closed (other than weekends or holidays), when trading on the NYSE is restricted, or as permitted by the SEC.

- Redemption proceeds may be paid in securities or other property rather than in cash if the Adviser determines it is in the best interests of the fund.

- Under applicable anti-money laundering rules and other regulations, redemption requests may be suspended, restricted, canceled, or processed and the proceeds may be withheld.

Account Policies

Fidelity will send monthly account statements detailing fund balances and all transactions completed during the prior month.

You may be asked to provide additional information in order for Fidelity to verify your identity in accordance with requirements under anti-money laundering regulations. Accounts may be restricted and/or closed, and the monies withheld, pending verification of this information or as otherwise required under these and other federal regulations.

Dividends and Capital Gain Distributions

The fund earns dividends, interest, and other income from its investments, and distributes this income (less expenses) to shareholders as dividends. The fund also realizes capital gains from its investments, and distributes these gains (less any losses) to shareholders as capital gain distributions.

The fund normally pays dividends and capital gain distributions in September and December.

Any dividends and capital gain distributions will be automatically reinvested in additional shares.

Tax Consequences

As with any investment, your investment in the fund could have tax consequences for you. If you are not investing through a tax-advantaged retirement account, you should consider these tax consequences.

Taxes on Distributions Distributions you receive from the fund are subject to federal income tax, and may also be subject to state or local taxes.

For federal tax purposes, certain of the fund's distributions, including dividends and distributions of short-term capital gains, are taxable to you as ordinary income, while certain of the fund's distributions, including distributions of long-term capital gains, are taxable to you generally as capital gains. A percentage of certain distributions of dividends may qualify for taxation at long-term capital gains rates (provided certain holding period requirements are met). Because the fund's income is primarily derived from interest and the investment in the Subsidiary, dividends from the fund generally will not qualify for the long-term capital gains tax rates available to individuals.

If you buy shares when a fund has realized but not yet distributed income or capital gains, you will be "buying a dividend" by paying the full price for the shares and then receiving a portion of the price back in the form of a taxable distribution.

Any taxable distributions you receive from the fund will normally be taxable to you when you receive them.

Taxes on Transactions

Your redemptions may result in a capital gain or loss for federal tax purposes. A capital gain or loss on your investment in the fund generally is the difference between the cost of your shares and the price you receive when you sell them.Fund Services

Fund Management

The fund is a mutual fund, an investment that pools shareholders' money and invests it toward a specified goal.

Adviser

Geode. The Adviser is the fund's manager. The address of the Adviser is One Post Office Square, 20th Floor, Boston, Massachusetts 02109.

As of December 31, 2016, the Adviser had approximately $254.7 billion in discretionary assets under management.

As the manager, the Adviser chooses the fund's investments and places orders to buy and sell the fund's investments. The Adviser is registered with the Commodity Futures Trading Commission as a commodity pool operator (CPO) and commodity trading advisor (CTA), and is a member of the National Futures Association in such capacities. The Adviser acts as CPO and CTA of the fund and the Subsidiary.

FMR, at 245 Summer Street, Boston, Massachusetts 02210, is responsible for handling the business affairs for the fund.

Portfolio Manager(s)

Bobe Simon is senior portfolio manager of the fund, which he has managed since May 2017. He also manages other funds. Since joining Geode in 2005, Mr. Simon has worked as a portfolio manager and senior portfolio manager.

Louis Bottari is portfolio manager of the fund, which he has managed since May 2017. He also manages other funds. Since joining Geode in 2008, Mr. Bottari has worked as an assistant portfolio manager and portfolio manager.

Eric Matteson is portfolio manager of the fund, which he has managed since May 2017. He also manages other funds. Since joining Geode in 2010, Mr. Matteson has worked as an assistant portfolio manager and portfolio manager.

Patrick Waddell is portfolio manager of the fund, which he has managed since May 2017. He also manages other funds. Since joining Geode in 2004, Mr. Waddell has worked as an assistant portfolio manager, portfolio manager, and senior portfolio manager.

The statement of additional information (SAI) provides additional information about the compensation of, any other accounts managed by, and any fund shares held by the portfolio managers.

Advisory Fee(s)

The fund pays a management fee to the Adviser. The management fee is calculated and paid to the Adviser every month. The Adviser pays all of the other expenses of the fund with certain exceptions.

The fund's annual management fee rate is 0.40% of its average net assets.

The Subsidiary has entered into a separate contract with the Adviser for the management of its portfolio pursuant to which the Subsidiary pays the Adviser a fee at an annual rate of 0.30% of its net assets. The Adviser has contractually agreed to waive the fund's management fee in an amount equal to the management fee paid to the Adviser by the Subsidiary. This arrangement may not be discontinued by the Adviser as long as its contract with the Subsidiary is in place.

The Adviser pays FMR an administration fee for handling the business affairs for the fund.

The basis for the Board of Trustees approving the management contract for the fund will be included in the fund's annual report for the fiscal period ending July 31, 2017, when available.

From time to time, the Adviser, FMR, or affiliates may agree to reimburse or waive certain fund expenses while retaining the ability to be repaid if expenses fall below the specified limit prior to the end of the fiscal year.

Reimbursement or waiver arrangements can decrease expenses and boost performance.

Fund Distribution

The fund is composed of multiple classes of shares. All classes of the fund have a common investment objective and investment portfolio.

Distribution and Service Plan(s)

Class F has adopted a Distribution and Service Plan pursuant to Rule 12b-1 under the 1940 Act that recognizes that the Adviser or FMR may use its revenues, including management fees paid to the Adviser by the fund, or fees paid to FMR out of such management fees, as well as past profits or its resources from any other source to pay FDC for expenses incurred in connection with providing services intended to result in the sale of Class F shares and/or shareholder support services. The Adviser or FMR, directly or through FDC, may pay significant amounts to intermediaries that provide those services. Currently, the Board of Trustees of the fund has authorized such payments for Class F shares.

If payments made by the Adviser or FMR to FDC or to intermediaries under the Distribution and Service Plan were considered to be paid out of Class F's assets on an ongoing basis, they might increase the cost of your investment and might cost you more than paying other types of sales charges.

No dealer, sales representative, or any other person has been authorized to give any information or to make any representations, other than those contained in this prospectus and in the related SAI, in connection with the offer contained in this prospectus. If given or made, such other information or representations must not be relied upon as having been authorized by the fund or FDC. This prospectus and the related SAI do not constitute an offer by the fund or by FDC to sell shares of the fund to or to buy shares of the fund from any person to whom it is unlawful to make such offer.

Appendix

Prior Performance of a Similar Fund

Because Fidelity® Commodity Strategy Fund was new when this prospectus was printed, its performance history is not included. However, Fidelity® Commodity Strategy Fund has an investment objective, policies, and strategies that are substantially similar to certain other funds and accounts which are also managed by Geode. Below you will find information about the prior performance of a composite of these funds and accounts (historical composite), not the performance of Class F of Fidelity® Commodity Strategy Fund.

The components of the historical composite may have different expenses and be sold through different distribution channels than Class F of Fidelity® Commodity Strategy Fund. Historical composite returns are based on past results and are not an indication of future performance. Geode also may manage other similar funds and accounts that have better or worse performance than the historical composite, and are not included in the historical composite due to factors such as differences in their policies and/or portfolio management strategies.

The performance of the historical composite does not represent the past performance of Class F of Fidelity® Commodity Strategy Fund and is not an indication of the future performance of Class F of Fidelity® Commodity Strategy Fund or Geode. You should not assume that Class F of Fidelity® Commodity Strategy Fund will have the same performance as the historical composite. The performance of Class F of Fidelity® Commodity Strategy Fund may be better or worse than the performance of the historical composite due to, among other things, differences in portfolio holdings, sales charges, expenses, asset sizes, and cash flows between Class F of Fidelity® Commodity Strategy Fund and the components of the historical composite. Some components of the historical composite are not subject to certain legal restrictions imposed on the Fidelity Commodity Strategy Fund, including the diversification requirements, specific tax restrictions and investment limitations imposed by the 1940 Act and Subchapter M of the Internal Revenue Code. The returns of Class F of Fidelity® Commodity Strategy Fund would differ from the returns of the historical composite to the extent that Class F of Fidelity® Commodity Strategy Fund and the components of the historical composite do not have the same expenses.

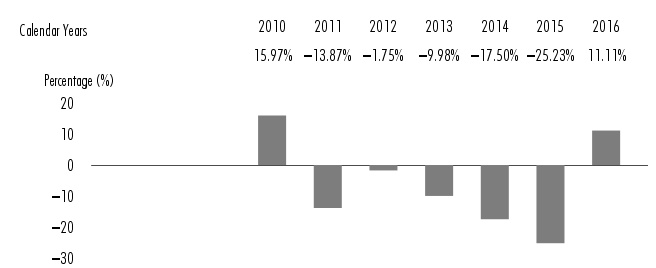

The following information illustrates the changes in the performance of the historical composite from year to year, and compares the performance of the historical composite to the performance of a securities market index over various periods of time.

Year-by-Year Returns*

| During the periods shown in the chart: | Returns | Quarter ended |

| Highest Quarter Return | 15.55% | December 31, 2010 |

| Lowest Quarter Return | (14.52)% | September 30, 2015 |

| Year-to-Date Return | (2.54)% | March 31, 2017 |

Average Annual Returns*

| For the periods ended December 31, 2016 | Past 1 year | Past 5 years | Life of Composite(a) |

| Composite | 11.11% | (9.53)% | (6.10)% |

| Bloomberg Commodity Index Total Return (reflects no deduction for fees, expenses, or taxes) | 11.77% | (8.95)% | (5.46)% |

(a) From October 31, 2009

* Historical composite returns are net of advisory fees and other expenses (as applicable) but reflect no deduction for taxes.Bloomberg Commodity Index Total Return℠ measures the performance of the commodities market. It consists of exchange-traded futures contracts on physical commodities that are weighted to account for the economic significance and market liquidity of each commodity. When available, the performance of each class of Fidelity® Commodity Strategy Fund will also be compared to the performance of Bloomberg Commodity Index Total Return.

IMPORTANT INFORMATION ABOUT OPENING A NEW ACCOUNT

To help the government fight the funding of terrorism and money laundering activities, the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act of 2001 (USA PATRIOT ACT), requires all financial institutions to obtain, verify, and record information that identifies each person or entity that opens an account.

For investors other than individuals: When you open an account, you will be asked for the name of the entity, its principal place of business and taxpayer identification number (TIN) and may be requested to provide information on persons with authority or control over the account such as name, residential address, date of birth and social security number. You may also be asked to provide documents, such as drivers' licenses, articles of incorporation, trust instruments or partnership agreements and other information that will help Fidelity identify the entity.

You can obtain additional information about the fund. A description of the fund's policies and procedures for disclosing its holdings is available in its SAI and on Fidelity's web sites. The SAI also includes more detailed information about the fund and its investments. The SAI is incorporated herein by reference (legally forms a part of the prospectus). A financial report will be available once the fund has completed its first annual or semi-annual period. The fund's annual and semi-annual reports also include additional information. The fund's annual report includes a discussion of the fund's holdings and recent market conditions and the fund's investment strategies that affected performance.

For a free copy of any of these documents or to request other information or ask questions about the fund, call Fidelity at 1-800-835-5092. In addition, existing investors may visit the web site at www.401k.com for a free copy of a prospectus, SAI, or annual or semi-annual report or to request other information.

The SAI, the fund's annual and semi-annual reports and other related materials are available from the Electronic Data Gathering, Analysis, and Retrieval (EDGAR) Database on the SEC's web site (http://www.sec.gov). You can obtain copies of this information, after paying a duplicating fee, by sending a request by e-mail to publicinfo@sec.gov or by writing the Public Reference Section of the SEC, Washington, D.C. 20549-1520. You can also review and copy information about the fund, including the fund's SAI, at the SEC's Public Reference Room in Washington, D.C. Call 1-202-551-8090 for information on the operation of the SEC's Public Reference Room.

Investment Company Act of 1940, File Number, 811-03480

FDC is a member of the Securities Investor Protection Corporation (SIPC). You may obtain information about SIPC, including the SIPC brochure, by visiting www.sipc.org or calling SIPC at 202-371-8300.

Fidelity and Fidelity Investments & Pyramid Design are registered service marks of FMR LLC. © 2017 FMR LLC. All rights reserved.

Any third-party marks that may appear above are the marks of their respective owners.

| 1.9879556.101 | CSZ-F-PRO-0517 |

| Fidelity® Commodity Strategy Fund |

| Class/Ticker |

| Fidelity® Commodity Strategy Fund/ FYHTX |

Shares are offered only to certain other Fidelity® funds and accounts.

In this prospectus, the term "shares" (as it relates to the fund) means the class of shares offered through this prospectus.

Prospectus

May 25, 2017

|

The Securities and Exchange Commission and the Commodity Futures Trading Commission have not approved or disapproved these securities or determined if this prospectus is accurate or complete. Any representation to the contrary is a criminal offense. | 245 Summer Street, Boston, MA 02210 |

Contents

|

Fund Summary |

Fidelity® Commodity Strategy Fund |

|

|

Fund Basics |

Investment Details |

|

|

Valuing Shares |

||

|

Shareholder Information |

Additional Information about the Purchase and Sale of Shares |

|

|

Account Policies |

||

|

Dividends and Capital Gain Distributions |

||

|

Tax Consequences |

||

|

Fund Services |

Fund Management |

|

|

Fund Distribution |

||

|

Appendix |

Prior Performance of a Similar Fund |

Fund Summary

Fund/Class:

Fidelity® Commodity Strategy Fund/Fidelity® Commodity Strategy Fund

Investment Objective

The fund seeks to provide investment returns that correspond to the performance of the commodities market.

Fee Table

The following table describes the fees and expenses that may be incurred when you buy and hold shares of the fund.

Shareholder fees

| (fees paid directly from your investment) | None |

Annual Operating Expenses

(expenses that you pay each year as a % of the value of your investment)

| Management fee | 0.40% | |

| Distribution and/or Service (12b-1) fees | None | |

| Other expenses(a) | 0.20% | |

| Acquired fund fees and expenses(b),(c) | 0.08% | |

| Total annual operating expenses | 0.68% | |

| Fee waiver and/or expense reimbursement(c) | 0.08% | |

| Total annual operating expenses after fee waiver and/or expense reimbursement | 0.60% |

(a) Based on estimated amounts for the current fiscal year.

(b) Acquired fund fees and expenses based on estimated amounts for the current fiscal year.

(c) The fund may invest in a wholly-owned subsidiary. The subsidiary has entered into a separate contract with Geode Capital Management, LLC (Geode) for the management of its portfolio pursuant to which the subsidiary pays Geode a fee at an annual rate of 0.30% of its net assets. The subsidiary also pays certain other expenses including custody fees. Geode has contractually agreed to waive the fund's management fee in an amount equal to the management fee paid to Geode by the subsidiary. This arrangement will remain in effect for at least one year from the effective date of the prospectus, and will remain in effect thereafter as long as Geode's contract with the subsidiary is in place. If Geode's contract with the subsidiary is terminated, Geode, in its sole discretion, may discontinue the arrangement.

This example helps compare the cost of investing in the fund with the cost of investing in other funds.

Let's say, hypothetically, that the annual return for shares of the fund is 5% and that your shareholder fees and the annual operating expenses for shares of the fund are exactly as described in the fee table. This example illustrates the effect of fees and expenses, but is not meant to suggest actual or expected fees and expenses or returns, all of which may vary. For every $10,000 you invested, here's how much you would pay in total expenses if you sell all of your shares at the end of each time period indicated:

| 1 year | $61 |

| 3 years | $192 |

Portfolio Turnover

The fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual operating expenses or in the example, affect the fund's performance.

Principal Investment Strategies

- Normally investing in commodity-linked derivative instruments, short-term investment-grade debt securities, cash, and cash equivalents.

- Investing up to 25% of assets in a wholly-owned subsidiary that invests in commodity-linked total return swaps based on the value of commodities or commodities indexes and in other commodity-linked derivative instruments.

- Managing the fund to track an index chosen to represent the commodities market, as well as short-term investment-grade debt securities, which as of the fund's inception was the Bloomberg Commodity Index Total Return℠.

- Investing in domestic and foreign issuers.

- Engaging in commodity-linked derivatives transactions that have a leveraging effect on the fund.

- Investing in Fidelity's central funds (specialized investment vehicles used by Fidelity® funds to invest in particular security types or investment disciplines).

Principal Investment Risks

- Interest Rate Changes. Interest rate increases can cause the price of a debt security to decrease.

- Foreign Exposure. Foreign markets can be more volatile than the U.S. market due to increased risks of adverse issuer, political, regulatory, market, or economic developments and can perform differently from the U.S. market.

- Financial Services Exposure. Changes in government regulation and interest rates and economic downturns can have a significant negative effect on issuers in the financial services sector, including the price of their securities or their ability to meet their payment obligations.

- Subsidiary Risk. Investment in an unregistered subsidiary is not subject to the investor protections of the Investment Company Act of 1940 (1940 Act) and is subject to the risks associated with investing in derivatives and commodity-linked investing in general. Changes in tax and other laws could negatively affect investments in the subsidiary.

- Prepayment. The ability of an issuer of a debt security to repay principal prior to a security's maturity can cause greater price volatility if interest rates change.

- Issuer-Specific Changes. The value of an individual security or particular type of security can be more volatile than, and can perform differently from, the market as a whole. A decline in the credit quality of an issuer or a provider of credit support or a maturity-shortening structure for a security can cause the price of a security to decrease.

- Leverage Risk. Leverage can increase market exposure, magnify investment risks, and cause losses to be realized more quickly.

- Commodity-Linked Investing. The value of commodities and commodity-linked investments may be affected by the performance of the overall commodities markets as well as weather, political, tax, and other regulatory and market developments. Commodity-linked investments may be more volatile and less liquid than the underlying commodity, instruments, or measures.

In addition, the fund is considered non-diversified and can invest a greater portion of assets in securities of a smaller number of individual issuers than a diversified fund. As a result, changes in the market value of a single investment could cause greater fluctuations in share price than would occur in a more diversified fund.

An investment in the fund is not a deposit of a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency. You could lose money by investing in the fund.

Performance

Performance history will be available for the fund after the fund has been in operation for one calendar year.

Visit www.fidelity.com for more recent performance information.

Investment Adviser

Geode Capital Management, LLC (Geode) (the Adviser) is the fund's manager.

Portfolio Manager(s)

Bobe Simon (senior portfolio manager) has managed the fund since May 2017.

Louis Bottari (portfolio manager) has managed the fund since May 2017.

Eric Matteson (portfolio manager) has managed the fund since May 2017.

Patrick Waddell (portfolio manager) has managed the fund since May 2017.

Purchase and Sale of Shares

Shares are offered only to certain other Fidelity® funds and accounts.

The price to sell one share is its net asset value per share (NAV). Shares will be sold at the NAV next calculated after an order is received in proper form.

The fund is open for business each day the New York Stock Exchange (NYSE) is open.

The fund has no minimum investment requirement.

Tax Information

Distributions you receive from the fund are subject to federal income tax and generally will be taxed as ordinary income or capital gains, and may also be subject to state or local taxes, unless you are investing through a tax-advantaged retirement account (in which case you may be taxed later, upon withdrawal of your investment from such account).

Payments to Broker-Dealers and Other Financial Intermediaries

The fund, the Adviser, Fidelity Management & Research Company (FMR), Fidelity Distributors Corporation (FDC), and/or their affiliates may pay intermediaries, which may include retirement plan sponsors, administrators, or service-providers (who may be affiliated with the Adviser, FMR, or FDC), for the sale of fund shares and related services. These payments may create a conflict of interest by influencing your intermediary and your investment professional to recommend the fund over another investment. Ask your investment professional or visit your intermediary's web site for more information.

Fund Basics

Investment Details

Investment Objective

Fidelity® Commodity Strategy Fund seeks to provide investment returns that correspond to the performance of the commodities market.

Principal Investment Strategies

The Adviser normally expects to invest the fund's assets in commodity-linked derivative instruments, short-term investment-grade debt securities, cash, and cash equivalents. Commodities are assets that have physical properties, such as oil and other energy products, metals, and agricultural products. Commodity-linked derivative instruments include commodity-linked notes; total return swaps, options, and forward contracts based on the value of commodities or commodities indexes; and commodity futures. The fund intends to provide exposure to the commodities market but will not be managed to take delivery of physical commodities. The fund may divest of commodity-linked derivative instruments to avoid delivery.

The fund seeks to track the performance of an index chosen by the Adviser to represent the commodities market, as well as short-term investment-grade debt securities. As of the fund's inception, the Adviser was using the Bloomberg Commodity Index Total Return℠ to represent the commodities market.

The Adviser may invest up to 25% of the fund's assets in a wholly-owned subsidiary of the fund organized under the laws of the Cayman Islands (the Subsidiary). The Subsidiary is managed by the same investment adviser as the fund. The Subsidiary is expected to invest directly in total return swaps based on the value of commodities or commodities indexes and in other commodity-linked derivative instruments, including options and forward contracts based on the value of commodities or commodities indexes, and commodity futures. The Subsidiary will not be managed to take delivery of physical commodities, and may divest of certain commodity-linked derivative instruments (namely commodity futures) to avoid delivery.

The Adviser may invest the fund's assets in securities of foreign issuers in addition to securities of domestic issuers.

Because the fund is considered non-diversified, the Adviser may invest a significant percentage of the fund's assets in a single issuer.

In addition to the principal investment strategies discussed above, the fund may also lend securities to broker-dealers or other institutions to earn income. When the Adviser believes that suitable commodity-linked derivative instruments are not available, or during other unusual market conditions, the Adviser may leave all or a significant portion of the fund's assets invested in cash, cash equivalents, or short-term investment-grade debt securities.

If the Adviser's strategies do not work as intended, the fund may not achieve its objective.

Description of Principal Security Types

Debt securities are used by issuers to borrow money. The issuer usually pays a fixed, variable, or floating rate of interest, and must repay the amount borrowed, usually at the maturity of the security. Some debt securities, such as zero coupon bonds, do not pay current interest but are sold at a discount from their face values. Debt securities include corporate bonds, government securities, repurchase agreements, money market securities, mortgage and other asset-backed securities, loans and loan participations, and other securities believed to have debt-like characteristics, including hybrids and synthetic securities.

Money market securities are high-quality, short-term securities that pay a fixed, variable, or floating interest rate. Securities are often specifically structured so that they are eligible investments for a money market fund. For example, in order to satisfy the maturity restrictions for a money market fund, some money market securities have demand or put features, which have the effect of shortening the security's maturity. Money market securities include bank certificates of deposit, bankers' acceptances, bank time deposits, notes, commercial paper, and U.S. Government securities. Certain issuers of U.S. Government securities, including Fannie Mae, Freddie Mac, and the Federal Home Loan Banks, are sponsored or chartered by Congress but their securities are neither issued nor guaranteed by the U.S. Treasury.

Commodity-linked derivative instruments are indexed to all or part of a commodities index or to a single commodity. Commodity-linked derivative instruments include debt securities and other investments whose maturity values, interest rates, or returns are determined by reference to a commodities index and are designed to provide exposure to the entire index, and may include other investments that provide exposure to less than the entire commodities index or to a single commodity. Commodity-linked derivative instruments may be positively or negatively indexed, meaning their maturity value may be structured to increase or decrease as commodity values change.

Derivatives are investments whose values are tied to an underlying asset, instrument, currency, or index. Derivatives include futures, options, forwards, and swaps, such as interest rate swaps (exchanging a floating rate for a fixed rate), total return swaps (exchanging a floating rate for the total return of an index, security, or other instrument or investment) and credit default swaps (buying or selling credit default protection).

Forward-settling securities involve a commitment to purchase or sell specific securities when issued, or at a predetermined price or yield. Payment and delivery take place after the customary settlement period.

Central funds are special types of investment vehicles created by Fidelity for use by Fidelity® funds and other advisory clients. Central funds incur certain costs related to their investment activity (such as custodial fees and expenses), but do not pay additional management fees. The investment results of the portions of the fund's assets invested in the central funds will be based upon the investment results of those funds.

Principal Investment Risks

Many factors affect the fund's performance. The fund's share price and yield change daily based on changes in market conditions and interest rates and in response to other economic, political, or financial developments. The fund's reaction to these developments will be affected by the types and maturities of securities in which the fund invests, the financial condition, industry and economic sector, and geographic location of an issuer, and the fund's level of investment in the securities of that issuer. In addition, because the fund may invest a significant percentage of assets in a single issuer, the fund's performance could be closely tied to that one issuer and could be more volatile than the performance of more diversified funds. When you sell your shares they may be worth more or less than what you paid for them, which means that you could lose money by investing in the fund.

The following factors can significantly affect the fund's performance:

Interest Rate Changes. Debt securities, including money market securities, have varying levels of sensitivity to changes in interest rates. In general, the price of a debt security can fall when interest rates rise and can rise when interest rates fall. Securities with longer maturities and certain types of securities, such as the securities of issuers in the financial services sector, can be more sensitive to interest rate changes, meaning the longer the maturity of a security, the greater the impact a change in interest rates could have on the security's price. Short-term and long-term interest rates do not necessarily move in the same amount or the same direction. Short-term securities tend to react to changes in short-term interest rates, and long-term securities tend to react to changes in long-term interest rates. Securities with floating interest rates can be less sensitive to interest rate changes, but may decline in value if their interest rates do not rise as much as interest rates in general. Securities whose payment at maturity is based on the movement of all or part of an index and inflation-protected debt securities may react differently from other types of debt securities.

Foreign Exposure. Foreign securities, securities issued by U.S. entities with substantial foreign operations, and entities providing credit support or a maturity-shortening structure that are located in foreign countries can involve additional risks relating to political, economic, or regulatory conditions in foreign countries. These risks include fluctuations in foreign exchange rates; withholding or other taxes; trading, settlement, custodial, and other operational risks; and the less stringent investor protection and disclosure standards of some foreign markets. All of these factors can make foreign investments more volatile than U.S. investments. In addition, foreign markets can perform differently from the U.S. market.

Global economies and financial markets are becoming increasingly interconnected, which increases the possibilities that conditions in one country or region might adversely impact issuers or providers in, or foreign exchange rates with, a different country or region.

Industry Exposure. Market conditions, interest rates, and economic, regulatory, or financial developments could significantly affect a single industry or a group of related industries, and the securities of companies in that industry or group of industries could react similarly to these or other developments. In addition, from time to time, a small number of companies may represent a large portion of a single industry or a group of related industries as a whole, and these companies can be sensitive to adverse economic, regulatory, or financial developments.

The commodities industries can be significantly affected by the level and volatility of commodity prices; the rate of commodity consumption; world events including international monetary and political developments; import controls, export controls, and worldwide competition; exploration and production spending; and tax and other government regulations and economic conditions.

Financial Services Exposure. Financial services companies are highly dependent on the supply of short-term financing and can be sensitive to changes in government regulation and interest rates and to economic downturns in the United States and abroad. These events can significantly affect the price of issuers’ securities as well as their ability to make payments of principal or interest or otherwise meet obligations on securities or instruments for which they serve as guarantors or counterparties.

Subsidiary Risk. The investments held by the Subsidiary are generally similar to those that are permitted to be held by the fund and, therefore, the Subsidiary is subject to risks similar to those of the fund, including the risks associated with investing in derivatives and commodity-linked investing in general. Because the Subsidiary is organized under Cayman Islands law and is not registered under the 1940 Act, the Subsidiary is not subject to the investor protections of the 1940 Act. The fund relies on a private letter ruling received by other Fidelity® funds from the Internal Revenue Service with respect to its investment in the Subsidiary. Changes in U.S. or Cayman Islands laws could result in the inability of the fund and/or the Subsidiary to operate as described in this prospectus.

Prepayment. Many types of debt securities, including mortgage securities, are subject to prepayment risk. Prepayment risk occurs when the issuer of a security can repay principal prior to the security's maturity. Securities subject to prepayment can offer less potential for gains during a declining interest rate environment and similar or greater potential for loss in a rising interest rate environment. In addition, the potential impact of prepayment features on the price of a debt security can be difficult to predict and result in greater volatility.

Issuer-Specific Changes. Changes in the financial condition of an issuer or counterparty, changes in specific economic or political conditions that affect a particular type of security or issuer, and changes in general economic or political conditions can increase the risk of default by an issuer or counterparty, which can affect a security's or instrument's credit quality or value. Entities providing credit support or a maturity-shortening structure also can be affected by these types of changes, and if the structure of a security fails to function as intended, the security could decline in value.

Leverage Risk. Derivatives and forward-settling securities involve leverage because they can provide investment exposure in an amount exceeding the initial investment. Leverage can magnify investment risks and cause losses to be realized more quickly. A small change in the underlying asset, instrument, or index can lead to a significant loss. Assets segregated to cover these transactions may decline in value and are not available to meet redemptions. Forward-settling securities also involve the risk that a security will not be issued, delivered, or paid for when anticipated. Government legislation or regulation could affect the use of these transactions and could limit a fund's ability to pursue its investment strategies.

Commodity-Linked Investing. The performance of commodities, commodity-linked swaps, futures, notes, and other commodity-related investments may depend on the performance of individual commodities and the overall commodities markets and on other factors that affect the value of commodities, including weather, political, tax, and other regulatory and market developments. Commodity-linked instruments may be leveraged. For example, the price of a three-times leveraged commodity-linked note may change by a magnitude of three for every percentage change (positive or negative) in the value of the underlying index. Commodity-linked investments may be hybrid instruments that can have substantial risk of loss with respect to both principal and interest. Commodity-linked investments may be more volatile and less liquid than the underlying commodity, instruments, or measures, and may be subject to the credit risks associated with the issuer or counterparty. As a result, returns of commodity-linked investments may deviate significantly from the return of the underlying commodity, instruments, or measures. In addition, the regulatory and tax environment for commodity linked derivative instruments is evolving, and changes in the regulation or taxation of such investments may have a material adverse impact on the fund. Funds and advisers subject to Commodity Futures Trading Commission (CFTC) regulation are subject to additional regulatory requirements and may incur additional costs.

In response to market, economic, political, or other conditions, a fund may temporarily use a different investment strategy for defensive purposes. If the fund does so, different factors could affect its performance and the fund may not achieve its investment objective.

Fundamental Investment Policies

The following is fundamental, that is, subject to change only by shareholder approval:

Fidelity® Commodity Strategy Fund seeks to provide investment returns that correspond to the performance of the commodities market.

Valuing Shares

The fund is open for business each day the NYSE is open.

NAV is the value of a single share. Fidelity normally calculates NAV as of the close of business of the NYSE, normally 4:00 p.m. Eastern time. The fund's assets normally are valued as of this time for the purpose of computing NAV. Fidelity calculates NAV separately for each class of shares of a multiple class fund.

NAV is not calculated and the fund will not process purchase and redemption requests submitted on days when the fund is not open for business. The time at which shares are priced and until which purchase and redemption orders are accepted may be changed as permitted by the Securities and Exchange Commission (SEC).

To the extent that the fund's assets are traded in other markets on days when the fund is not open for business, the value of the fund's assets may be affected on those days. In addition, trading in some of the fund's assets may not occur on days when the fund is open for business.

NAV is calculated using the values of the underlying central funds in which the fund invests. Shares of underlying central funds are valued at their respective NAVs. Other assets are valued primarily on the basis of market quotations, official closing prices, or information furnished by a pricing service. Certain short-term securities are valued on the basis of amortized cost. If market quotations, official closing prices, or information furnished by a pricing service are not readily available or, in FMR's opinion, are deemed unreliable for a security, then that security will be fair valued in good faith by FMR in accordance with applicable fair value pricing policies. For example, if, in FMR’s opinion, a security’s value has been materially affected by events occurring before a fund’s pricing time but after the close of the exchange or market on which the security is principally traded, then that security will be fair valued in good faith by FMR in accordance with applicable fair value pricing policies. Fair value pricing will be used for high yield debt securities when available pricing information is determined to be stale or for other reasons not to accurately reflect fair value.

Arbitrage opportunities may exist when trading in a portfolio security or securities is halted and does not resume before a fund calculates its NAV. These arbitrage opportunities may enable short-term traders to dilute the NAV of long-term investors. Securities trading in overseas markets present time zone arbitrage opportunities when events affecting portfolio security values occur after the close of the overseas markets but prior to the close of the U.S. market. Fair valuation of a fund's portfolio securities can serve to reduce arbitrage opportunities available to short-term traders, but there is no assurance that fair value pricing policies will prevent dilution of NAV by short-term traders.

Fair value pricing is based on subjective judgments and it is possible that the fair value of a security may differ materially from the value that would be realized if the security were sold.

Shareholder Information

Additional Information about the Purchase and Sale of Shares

As used in this prospectus, the term "shares" generally refers to the shares offered through this prospectus.

Frequent Purchases and Redemptions

The fund may reject for any reason, or cancel as permitted or required by law, any purchase orders, including transactions deemed to represent excessive trading, at any time.

Excessive trading of fund shares can harm shareholders in various ways, including reducing the returns to long-term shareholders by increasing costs to the fund (such as brokerage commissions or spreads paid to dealers who sell money market instruments), disrupting portfolio management strategies, and diluting the value of the shares in cases in which fluctuations in markets are not fully priced into the fund's NAV.

Because the fund is primarily offered for investment only to certain other Fidelity® funds, the potential for excessive or short-term disruptive purchases and sales is reduced. Accordingly, the Board of Trustees has not adopted policies and procedures designed to discourage excessive trading of fund shares and the fund accommodates frequent trading.

The fund has no limit on purchase transactions but may in its discretion restrict, reject, or cancel any purchases that, in the Adviser's opinion, may be disruptive to the management of the fund or otherwise not be in the fund's interests.

The fund reserves the right at any time to restrict purchases or impose conditions that are more restrictive on excessive trading than those stated in this prospectus.

The fund has no exchange privilege with any other fund.

Buying Shares

Eligibility

Shares are generally available only to investors residing in the United States.

Shares are offered only to certain other Fidelity® funds and accounts.

Price to Buy

The price to buy one share is its NAV. Shares are sold without a sales charge.

Shares will be bought at the NAV next calculated after an order is received in proper form.

Orders by funds of funds for which Fidelity serves as investment manager will be treated as received by the fund at the same time that the corresponding orders are received in proper form by the funds of funds.