UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

INVESTMENT COMPANY ACT FILE NUMBER 811-22684

DAXOR CORPORATION

(Exact name of registrant as specified in charter)

109 Meco Lane

Oak Ridge, TN 37830

(Address of principal executive offices) (Zip code)

Michael Feldschuh

109 Meco Lane

Oak Ridge, TN 37830

(Name and address of agent for service)

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: 212-330-8500

DATE OF FISCAL YEAR END: DECEMBER 31

DATE OF REPORTING PERIOD: JANUARY 1, 2023 to DECEMBER 31, 2023

Daxor Corporation

Financial Statements

For the Year Ended

December 31, 2023

Table of Contents

March 15, 2024

Dear Fellow Shareholder:

It is my pleasure to report on Daxor’s results for the year ended December 31, 2023.

As of December 31, 2023, Daxor’s net assets were $34,010,384 or $7.08 per share as compared to $28,969,469 , or $6.75 per share at December 31, 2022. The increase in the net asset value is primarily due to the continued appreciation in value in the operating division. The valuation of the operating division increased $6,000,000 to $32,000,000 at December 31, 2023. For the year ended December 31, 2023, Daxor had net dividend income of $157,378 and net realized gains on investment activity of $603,774. There was a net decrease in the unrealized appreciation on investments of $885,199 as we sold positions during 2023 and the prior period’s significant unrealized gains unwound into the gains for the period. Included in the Net Increase in Net Assets Resulting From Operations of $280,640 is non-cash stock based compensation expense of $631,701, in an effort to provide incentive to employees, officers, agents and consultants through proprietary interest in the company. Daxor invested $4,552,380 in the operating division to continue its research and development, sales and overhead for our 2024 product launch, ramping the commercial sales teams, as well as production facilities for our next generation blood volume analyzers.

We maintain a diversified securities portfolio comprised primarily of electric utility company common and preferred stocks. With regard to the performance of these investment securities, utilities were a low-performing sector of the market, particularly in the first half of 2023. In the first half of 2023, the economy delivered better-than-feared results, with continued—albeit moderating—growth led by resilient consumer spending amid ongoing labor market strength. As inflationary pressures eased, the Fed slowed the pace of monetary tightening, which encouraged investors, as did stronger-than-expected earnings reports. In late summer, markets stumbled again in the face of the increasing likelihood that the Fed would maintain rates at elevated levels for longer than previously expected, due to rising energy prices, sustained wage pressures, and the broad persistence of above-target inflation. By the end of the third quarter, macroeconomic and political developments added to investor unease. Then the equity markets bounced back in November as the 10-year US Treasury yield pulled back and many of the aforementioned issues were resolved. Oil prices retreated into the fourth quarter on rising demand concerns and disagreement within OPEC over production quotas.

As has often been the case over the last five years, utilities were a low-performing sector of the market. The geopolitical tailwinds that drove investors to the safe haven of utilities in 2022 dissipated and were replaced by the much stronger headwind of rising interest rates. As rates retreated into the fourth quarter of 2023, however, utilities got a bit of a break and advanced in line with the broader market.

Daxor has been reporting as an investment company under the Investment Company Act of 1940 since January 1, 2012. See the Notes to the Financial Statements of Form N-CSR for further information on Daxor’s strategies and goals regarding its investments in publicly traded securities to help fund its diagnostic operations. Because of its significant holding of publicly traded securities, the SEC currently classifies Daxor as a closed-end investment management company with a fully-owned medical operating division; however, the primary focus of management is on our operational objectives. Daxor anticipates that as the value of the operating company continues to increase as a percentage of assets owned, it will be eligible to file under its previous designation as an operating company and report as an operating company, and will take steps to accomplish this result.

Any shareholder who is interested in learning more about our medical instrumentation and biotechnology operations should visit our website at www.daxor.com or contact our investor relations representative Bret Shapiro of CORE IR at 516-222-2560 for more detailed information. We periodically issue press releases regarding research reports and placements of the BVA-100 Blood Volume Analyzer in hospitals.

Go Paperless with E-Delivery

In order to sign up for electronic delivery of shareholder reports and prospectuses, please send an email to info@daxor.com. If you do not hold your account directly with Daxor, please contact the firm that holds your account about electronic delivery.

Cordially Yours,

Michael Feldschuh

CEO and President

| 1 |

Item 1. Schedule of Investments

Daxor Corporation

Schedule of Investments

December 31, 2023

| Shares | Fair Value | |||||||

| Common Stock - (United States) – 7.30% | ||||||||

| Industrials – 0.01% | ||||||||

| Wabtec | 13 | $ | 1,650 | |||||

| Materials – 0.31% | ||||||||

| Enbridge Inc. | 2,952 | 106,331 | ||||||

| Electric Utilities – 6.98% | ||||||||

| Avangrid, Inc. | 7,000 | 226,870 | ||||||

| Avista Corporation | 6,000 | 214,440 | ||||||

| CenterPoint Energy, Inc. | 1,000 | 28,570 | ||||||

| Centrus Energy Corp. (1) | 1 | 54 | ||||||

| CMS Energy Corporation | 3,500 | 203,245 | ||||||

| DTE Energy Company | 2,000 | 220,520 | ||||||

| Edison International | 4,000 | 285,960 | ||||||

| Entergy Corporation | 3,500 | 354,165 | ||||||

| Evergy Inc. | 4,297 | 224,303 | ||||||

| Eversource Energy | 2,000 | 123,440 | ||||||

| Exelon Corporation | 2,100 | 75,390 | ||||||

| FirstEnergy Corp. | 3,800 | 139,308 | ||||||

| Pinnacle West Capital Corporation | 3,000 | 215,520 | ||||||

| Xcel Energy, Inc. | 1,000 | 61,910 | ||||||

| Total Electric Utilities | 2,373,695 | |||||||

| Total Common Stock (Cost $816,921) – 7.30% | $ | 2,481,676 | ||||||

| Shares | Fair Value | |||||||

| Preferred Stock - (United States) – 1.06% | ||||||||

| Banking – 1.06% | ||||||||

| Bank of America Corp 7.250% Series L | 300 | $ | 361,584 | |||||

| Total Preferred Stock (Cost $193,985) – 1.06% | $ | 361,584 | ||||||

| Total Investments in Securities (Cost $1,010,906) – 8.36% | $ | 2,843,260 | ||||||

| Investment in Operating Division (Cost $41,494,302) - (United States) – 94.09% (2) | $ | 32,000,000 | ||||||

| Dividends receivable – 0.04% | $ | 14,198 | ||||||

| Other Assets – 0.03% | $ | 11,684 | ||||||

| Total Assets – 102.52% | $ | 34,869,142 | ||||||

| Total Liabilities - (2.52%) | $ | (858,758 | ) | |||||

| Net Assets – 100.00% | $ | 34,010,384 | ||||||

| (1) | Non-income producing security |

| (2) | The Fair Value of the operating division was determined by using significant unobservable inputs. |

The accompanying notes are an integral part of these financial statements.

| 2 |

Daxor Corporation

Schedule of Investments – (Continued)

December 31, 2023

At December 31, 2023, the net unrealized appreciation on investment in securities, options and securities borrowed of $1,832,354 was composed of the following:

| Aggregate gross unrealized appreciation for which there was an excess of value over cost | $ | 1,837,512 | ||

| Aggregate gross unrealized depreciation for which there was an excess of cost over value | (5,158 | ) | ||

| Net unrealized appreciation | $ | 1,832,354 |

At December 31, 2023, the net unrealized (depreciation) on investment in operating division was composed of the following:

| Net unrealized (depreciation) on investment in operating division | $ | (9,494,302 | ) |

Portfolio Analysis

December 31, 2023

| Percentage | ||||

| of Net Assets | ||||

| Common Stock (United States) | ||||

| Industrials | 0.01 | % | ||

| Materials | 0.31 | % | ||

| Electric Utilities | 6.98 | % | ||

| Total Common Stock | 7.30 | % | ||

| Preferred Stock (United States) | ||||

| Banking | 1.06 | % | ||

| Total Investments in Securities | 8.36 | % | ||

The accompanying notes are an integral part of these financial statements.

| 3 |

Summary of Liabilities

December 31, 2023

| Accounts payable and accrued expenses – (0.03)% | (103,099 | ) | ||

| Margin loans payable - (2.22)% | (755,659 | ) | ||

| Total Liabilities - (2.52)% | $ | (858,758 | ) |

The accompanying notes are an integral part of these financial statements.

| 4 |

Daxor Corporation

Statement of Assets and Liabilities

December 31, 2023

| Assets: | ||||

| Investments in securities, at fair value (cost of $1,010,906) | $ | 2,843,260 | ||

| Investment in operating division, at fair value (cost of $41,494,302) | 32,000,000 | |||

| Dividends receivable | 14,198 | |||

| Prepaid taxes and other assets | 11,684 | |||

| Total Assets | 34,869,142 | |||

| Liabilities: | ||||

| Margin loans payable | 755,659 | |||

| Accounts payable and accrued expenses | 103,099 | |||

| Total Liabilities | 858,758 | |||

| Commitments (Note 15) | ||||

| Net Assets | $ | 34,010,384 | ||

| Net Asset Value, (10,000,000 shares authorized, 5,316,530 issued and 4,806,347 shares outstanding of $0.01 par value capital stock outstanding) | $ | 7.08 | ||

| Net Assets consist of: | ||||

| Capital paid in | $ | 13,744,205 | ||

| Total distributable earnings | 25,093,122 | |||

| Treasury Stock | (4,826,943 | ) | ||

| Net Assets | $ | 34,010,384 | ||

The accompanying notes are an integral part of these financial statements.

| 5 |

Daxor Corporation

For the Year Ended December 31, 2023

| Investment Income: | ||||

| Dividend income (net of foreign withholding taxes of $1,985) | $ | 157,378 | ||

| Other income | 6,044 | |||

| Total Investment Income | 163,422 | |||

| Expenses: | ||||

| Stock based compensation expense | 631,701 | |||

| Investment administrative charges | 128,666 | |||

| Audit and tax preparation fees | 139,496 | |||

| Professional fees | 39,200 | |||

| Transfer agent fees | 48,409 | |||

| Interest expense | 49,102 | |||

| Other taxes | 12,403 | |||

| Total Expenses | 1,048,977 | |||

| Net Investment (Loss) | (885,555 | ) | ||

| Realized and Unrealized Gain (Loss) on Investments and Other items: | ||||

| Net realized gain from investments in securities | 603,774 | |||

| Net change in unrealized (depreciation) on investments | (885,199 | ) | ||

| Net change in unrealized (depreciation) in operating division | (32,375,445 | ) | ||

| Adjustment to opening cost of investments in operating division (See Note 4) | 33,823,065 | |||

| Net Realized and Unrealized Gain on Investments | 1,166,195 | |||

| Income tax (benefit) | 0 | |||

| Net Increase in Net Assets Resulting From Operations | $ | 280,640 |

The accompanying notes are an integral part of these financial statements.

| 6 |

Daxor Corporation

Statement of Changes in Net Assets

Year Ended December 31, 2023 | Year Ended December 31, 2022 | |||||||

| Increase in Net Assets Resulting from Operations | ||||||||

| Net investment (loss) | $ | (885,555 | ) | $ | (972,974 | ) | ||

| Net realized gain from investments in securities | 603,774 | 2,736,375 | ||||||

| Net realized (loss) from options | - | (56,954 | ) | |||||

| Net change in unrealized (depreciation) appreciation on investments, options and securities borrowed | (885,199 | ) | (2,763,895 | ) | ||||

| Net change in unrealized (depreciation) appreciation in operating division | (32,375,445 | ) | 9,500,000 | |||||

| Adjustment to opening cost of investment in operating division (See Note 4) | 33,823,065 | - | ||||||

| Realized (loss) on investment in operating division | - | (3,264,419 | ) | |||||

| Net Increase in Net Assets Resulting From Operations | 280,640 | 5,178,133 | ||||||

| Capital Share Issuances: | ||||||||

| Increase in net assets resulting from stock-based compensation | 631,701 | 786,642 | ||||||

| Gross proceeds from sale of treasury stock | 4,529,840 | 2,099,975 | ||||||

| Issuance costs from the sale of treasury stock | (401,266 | ) | (248,000 | ) | ||||

| Net Increase in Net Assets Resulting From Capital Share Issuances | 4,760,275 | 2,638,617 | ||||||

| Total Net Increase in Net Assets | 5,040,915 | 7,816,750 | ||||||

| Net Assets: | ||||||||

| Beginning of Period | 28,969,469 | 21,152,719 | ||||||

| End of Period | $ | 34,010,384 | $ | 28,969,469 | ||||

The accompanying notes are an integral part of these financial statements.

| 7 |

Daxor Corporation

For the Year Ended December 31, 2023

| Cash flows from operating activities: | ||||

| Net increase in net assets resulting from operations | $ | 280,640 | ||

| Adjustment to reconcile net increase in net assets resulting from operations to net cash used in operating activities: | ||||

| Net realized gain from investments in securities | (603,774 | ) | ||

| Net change in unrealized depreciation on investments | 885,199 | |||

| Net change in unrealized depreciation in operating division | 32,375,445 | |||

| Adjustment to opening cost of investment in operating division (See Note 4) | (33,823,065 | ) | ||

| Current year investment in operating division | (4,552,380 | ) | ||

| Proceeds from sales of securities | 2,746,121 | |||

| Purchase of securities | (1,647,577 | ) | ||

| Stock based compensation expense | 631,701 | |||

| Changes in operating assets and liabilities: | ||||

| Decrease in dividends receivable | 3,035 | |||

| Prepaid taxes and other assets | 8,923 | |||

| Increase in accrued expenses | 40,664 | |||

| Net cash used in operating activities | (3,655,068 | ) | ||

| Cash flows from financing activities: | ||||

| Proceeds from margin loan payable | 4,112,901 | |||

| Repayment of margin loan payable | (4,586,407 | ) | ||

| Gross proceeds from the sale of treasury stock | 4,529,840 | |||

| Issuance costs on the sale of treasury stock | (401,266 | ) | ||

| Net cash provided by financing activities | 3,655,068 | |||

| Net change in cash and restricted cash | $ | - | ||

| Cash and restricted cash at beginning of the period | - | |||

| Cash and restricted cash at end of the period | $ | - | ||

| Supplemental Disclosures of Cash Flow Information: | ||||

| Cash paid during the year for: | ||||

| Income Taxes (State income taxes) | $ | 13,803 | ||

| Interest on margin loan payable | $ | 49,102 | ||

The accompanying notes are an integral part of these financial statements.

| 8 |

Daxor Corporation

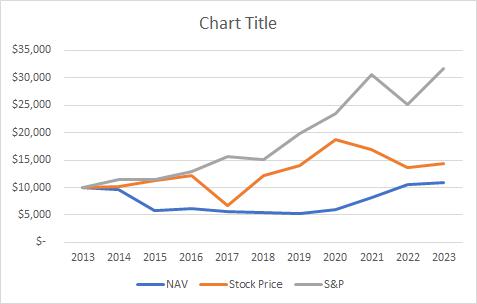

The table below sets forth certain financial data for weighted average shares of stock outstanding for each year and for one share of capital stock outstanding throughout the years presented: “Net investment (loss) income,” “Net realized and unrealized gain (loss) from investments,” “Net loss and unrealized appreciation of operating division,” “stock based compensation expense,” “sale of treasury stock” and “cost relief of treasury stock sold”. We used weighted average shares outstanding for these items because of the increase in outstanding shares in 2023 and 2022, and we believe the use of weighted average shares outstanding best reflects the impact of the share increases on the calculation of these items. The total investment return does not reflect sales load.

| Year

Ended December 31, 2023 | Year

Ended December 31, 2022 | |||||||

| Net Asset Value Per Share, Beginning of Year | $ | 6.75 | $ | 5.24 | ||||

| Income (loss) from operations: | ||||||||

| Net investment (loss) income | (0.19 | ) | (0.24 | ) | ||||

| Net realized and unrealized gain (loss) from investments, options and securities borrowed | (0.06 | ) | (0.02 | ) | ||||

| Net loss and unrealized appreciation of operating division | 0.31 | 1.53 | ||||||

| Other (1) | 0.08 | (0.40 | ) | |||||

| Total income from Operations | 0.14 | 0.87 | ||||||

| Capital share issuances : | ||||||||

| Increase in net assets from stock based compensation | 0.15 | 0.19 | ||||||

| Increase from sale of treasury stock | 0.89 | 0.45 | ||||||

| (Decrease) from cost relief of treasury stock sold | (0.85 | ) | - | |||||

| Increase in Net Asset Value Per Share | 0.33 | 1.51 | ||||||

| Net Asset Value Per Share, End of Year | $ | 7.08 | $ | 6.75 | ||||

| Market Price Per Share of Common Stock, Beginning of Year | $ | 9.16 | $ | 11.29 | ||||

| Market Price Per Share of Common Stock, End of Year | $ | 9.60 | $ | 9.16 | ||||

| Change in Price Per Share of Common Stock | $ | 0.44 | $ | (2.13 | ) | |||

| Total Investment Return | 4.80 | % | (18.87 | )% | ||||

| Weighted Average Shares Outstanding | 4,631,255 | 4,083,847 | ||||||

| Ratios/Supplemental Data | ||||||||

| Net assets, End of Period (in 000’s) | $ | 34,010 | $ | 28,969 | ||||

| Ratio of total expenses to average net assets | 3.32 | % | 5.86 | % | ||||

| Ratio of net investment (loss) income after income taxes to average net assets | (2.80 | )% | (4.73 | )% | ||||

| Portfolio turnover rate | 46.07 | % | 0 | % | ||||

| (1) | Primarily due to the increase in Daxor shares outstanding for the years 2023 and 2022 |

The accompanying notes are an integral part of these financial statements.

| 9 |

Daxor Corporation

Financial Highlights (continued)

| Year Ended December 31, 2021 | Year Ended December 31, 2020 | Year Ended December 31, 2019 | ||||||||||

| Net Asset Value Per Share, Beginning of Year | $ | 3.89 | $ | 3.41 | $ | 3.49 | ||||||

| Income (loss) from operations: | ||||||||||||

| Net investment (loss) income | (0.20 | ) | (0.08 | ) | (0.03 | ) | ||||||

| Net realized and unrealized gain from investments, options and securities borrowed | 0.21 | (0.32 | ) | 0.59 | ||||||||

| Net loss and unrealized appreciation (depreciation) of operating division | 1.16 | 0.11 | (0.69 | ) | ||||||||

| Other | 0.00 | 0.01 | 0.00 | |||||||||

| Total income (loss) from Investment Operations | 1.17 | (0.28 | ) | (0.13 | ) | |||||||

| Capital share issuances : | ||||||||||||

| Increase in net assets from stock based compensation | 0.18 | 0.06 | 0.05 | |||||||||

| Increase from sale of treasury stock and exercise of stock options | - | 0.70 | 0.00 | |||||||||

| Increase/(Decrease) in Net Asset Value Per Share | 1.35 | 0.48 | (0.08 | ) | ||||||||

| Net Asset Value Per Share, End of Year | $ | 5.24 | $ | 3.89 | $ | 3.41 | ||||||

| Market Price Per Share of Common Stock, Beginning of Year | $ | 12.50 | $ | 9.40 | $ | 8.20 | ||||||

| Market Price Per Share of Common Stock, End of Year | 11.29 | 12.50 | 9.40 | |||||||||

| Change in Price Per Share of Common Stock | $ | (1.21 | ) | $ | 3.10 | $ | 1.20 | |||||

| Total Investment Return | (9.68 | )% | 32.98 | % | 14.63 | % | ||||||

| Weighted Average Shares Outstanding | 4,036,660 | 3,935,902 | 3,746,858 | |||||||||

| Ratios/Supplemental Data | ||||||||||||

| Net assets, End of Year (in 000’s) | $ | 21,153 | $ | 15,675 | $ | 12,766 | ||||||

| Ratio of total expenses to average net assets | 7.29 | % | 5.79 | % | 4.26 | % | ||||||

| Ratio of net investment (loss) income after income taxes to average net assets | (5.44 | )% | (3.53 | )% | (1.12 | )% | ||||||

| Portfolio turnover rate | 0.00 | % | 12.54 | % | 0.00 | % | ||||||

The accompanying notes are an integral part of these financial statements.

| 10 |

Daxor Corporation

December 31, 2023

1. Organization and Investment Objective

Daxor Corporation (the “Company”) is registered under the Investment Company Act of 1940, as amended, as a diversified, closed-end management investment company.

The Company qualifies as a “controlled company” under Nasdaq rules, as the estate of Joseph Feldschuh, M.D. controls more than 50% of the Company’s voting power, as evidenced by the Company’s ownership records. The estate owns 53.1% of the outstanding shares. As a result, the estate has the ability to control the outcome on any matter requiring the approval of shareholders of the Company.

The Company’s investment goals, objectives and principal strategies are as follows:

| A. | The Company’s investment goals and objectives are capital preservation, maintaining returns on capital with a high degree of safety and generating income from dividends and option sales to help offset operating losses from the Company’s operating division. |

| B. | In order to achieve these goals, the Company maintains a diversified securities portfolio comprised primarily of electric utility company common and preferred stocks. The Company also sells covered calls on portions of its portfolio and also sells puts on stocks it is willing to own. It also sells uncovered calls and may have net short positions in common stock up to 15% of the value of the portfolio. The net short position is the total fair market value of the Company’s short positions reduced by the amount due to the Company from the broker. If the amount due from the broker is more than the fair market value of the short positions, the Company will have a net receivable from the broker. The Company’s investment policy is to maintain a minimum of 80% of its portfolio in equity securities of utility companies. The Board of Directors has authorized this minimum to be temporarily lowered to 70% when Company management deems it to be necessary. Investments in utilities are primarily in electric companies. Investments in non-utility stocks will generally not exceed 20% of the value of the portfolio. |

2. Significant Accounting Policies

Basis of Presentation and Use of Estimates

The Company is unique in nature, as it reports as a closed-end investment company but its focus and operations are as a medical device manufacturing, company. For measurement of its investments in securities, the Company follows accounting and reporting guidance in the Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 946 (ASC 946). The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), including, but not limited to, ASC 946, as stated above. GAAP requires the use of estimates made by management. Management believes that estimates and valuations are appropriate; however, actual results may differ from those estimates, and the valuations reflected in the accompanying financial statements may differ from the value ultimately realized upon sale or maturity.

The following is a summary of significant accounting policies consistently followed by the Company in the preparation of its financial statements.

Valuation of Investments

The Company carries its investments in securities at fair value and utilizes various methods to measure the fair value of its investments on a recurring basis. Fair value is an estimate of the exit price, representing the amount that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants (i.e., the exit price at the measurement date). Fair value measurements are not adjusted for transaction costs. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

Level 1 - Unadjusted quoted prices in active markets for identical assets and liabilities that the Company has the ability to access.

Level 2 - Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 - Unobservable inputs for an asset or liability, to the extent relevant observable inputs are not available; representing the Company’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available (ASC Topic 820).

| 11 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

2. Significant Accounting Policies - (continued)

Valuations of Investments (continued)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

Investments in securities, securities borrowed and put and call options that are freely traded and are listed on a national securities exchange are valued at the last reported sales price on the last business day of the year; securities traded on the over-the-counter market and listed securities for which no sale was reported on that date are valued at the mean between the last reported bid and asked prices.

The Company establishes valuation processes and procedures to ensure that the valuation techniques for investments that are categorized within Level 3 of the fair value hierarchy are fair, consistent, and verifiable. At December 31, 2023, the Company has no Level 3 investments. If the money that is advanced to the operating division from sales of our investment securities to fund our operations were treated as an investment, even though it is not, then it would be a Level 3 investment. The Company’s Audit Committee oversees the valuation process of the Company’s Level 3 investments. The Audit Committee is comprised of members of the Company’s Board of Directors and is responsible for the valuation processes and procedures and evaluating the overall fairness and consistent application of the valuation policies. For this valuation process, the Audit Committee meets semi-annually or as needed, and, in conjunction with reports from an independent valuation company, determines the valuations of the Company’s Level 3 investments. Valuations determined by the Audit Committee are required to be supported by the independent valuation company whose reports may include information such as market data, third-party pricing sources, industry accepted pricing models, counterparty prices, or other appropriate methods. On an annual basis, the Company engages the services of an independent valuation company to perform an independent review of the valuation of the Company’s operating division on a standalone basis, and may adjust its valuation based on the recommendations from the valuation firm.

The Company is not a party to any advisory services agreements and as such has no related liabilities.

| 12 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

2. Significant Accounting Policies - (continued)

Valuation of Derivative Instruments

The Company accounts for derivative instruments under FASB ASC 815, “Derivatives and Hedging,” which establishes accounting and reporting standards requiring that derivative instruments be recorded in the Statement of Assets and Liabilities at fair value. The changes in the fair values of derivatives are included in the Statements of Operations as a component of net realized and unrealized loss from investments.

Investment Transactions and Income and Expenses

Investment transactions are accounted for on the trade date. Realized gains and losses on sales of investments are calculated on the basis of identifying the specific securities delivered. Dividend income and expense are recorded on the ex-dividend date, and interest income is recognized on the accrual basis. Expenses are recorded on an accrual basis. Realized gains and loses are net of transaction fees.

Investments in Operating Division Transactions

Investment in operating division transactions are accounted for using the accrual method of accounting. The net change in unrealized appreciation (depreciation) in the operating division is based on the results of the valuation of the operating division, performed annually under the guidance of Topic 820, Fair Value Measurement, compared to the underlying cost of the investment in the operating division. The cost of the operating division is based on the original cost of the purchase of the assets of the operating division and subsequent capital infusions into the investment in the operating division.

Distributions

Net investment income and net realized gains are accumulated within the Company and used to pay expenses, to make additional investments or held in cash as a reserve and at the discretion of the Company, to pay dividends to shareholders.

Revenue Recognition

ACS Topic 606, Revenue from Contracts with Customers, requires that an entity recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The guidance requires an entity to follow a five-step model to (a) identify the contract(s) with a customer, (b) identify the performance obligations in the contract, (c) determine the transaction price, (d) allocate the transaction price to the performance obligations in the contract, and (e) recognize revenue when the entity satisfies a performance obligation.

Income Taxes

The Company accounts for income taxes under the provisions of FASB ASC 740, “Income Taxes.” This pronouncement requires recognition of deferred tax assets and liabilities for the estimated future tax consequences of events attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases and operating loss and tax credit carryforwards. Deferred tax assets and liabilities are measured using enacted tax rates in effect for the year in which the differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of changes in tax rates is recognized in the Statement of Operations in the period in which the enactment rate changes. Deferred tax assets and liabilities are reduced through the establishment of a valuation allowance at such time as, based on available evidence, it is more likely than not that the deferred tax assets will not be realized.

The Company accounts for uncertainties in income taxes under the provisions of FASB ASC 740-10-05, “Accounting for Uncertainties in Income Taxes”. The ASC clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements. The ASC prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. The ASC provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosure and transition.

| 13 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

2. Significant Accounting Policies - (continued)

Treasury Stock

Treasury stock is recorded under the cost method and shown as a reduction of net assets.

3. Fair Value Measurements of Investments, Financial Instruments and Related Risks

The following tables summarize the inputs used as of December 31, 2023 for the Company’s assets and liabilities measured at fair value on a recurring basis at December 31, 2023, categorized by the above mentioned fair value hierarchy and also by denomination. As noted above, the valuation of the Company’s operating division on a standalone basis is determined on a yearly basis.

| Assets | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Common Stocks | $ | 2,481,676 | $ | - | $ | - | $ | 2,481,676 | ||||||||

| Preferred Stocks | 361,584 | - | - | 361,584 | ||||||||||||

| Operating division | - | - | 32,000,000 | 32,000,000 | ||||||||||||

| Total | $ | 2,843,260 | $ | - | $ | 32,000,000 | $ | 34,843,260 | ||||||||

The Company purchases equity securities in the form of common and preferred stocks, primarily in the utility sector and these comprise the investment securities held by the Company. The common and preferred stocks are recorded at fair value at the unadjusted closing quoted price on active securities markets.

Purchased call and put options: When the Company purchases an option, an amount equal to the premium paid by the Company is recorded as an investment on the Statement of Assets and Liabilities, the value of which is marked-to-market to reflect the current market value of the option purchased. If the purchased option expires, the Company realizes a loss equal to the amount of premium paid. When an instrument is purchased or sold through the exercise of an option, the related premium paid is added to the basis of the instrument acquired or deducted from the proceeds of the instrument sold. The risk associated with purchasing put and call options is limited to the premium paid.

Written call and put options: When the Company writes (sells) an option, an amount equal to the premium received by the Company is recorded as an obligation on the Statement of Assets and Liabilities, the value of which is marked-to-market to reflect the current market value of the written option. If the written option expires, the Company realizes a gain equal to the amount of premium received. When an instrument is purchased or sold through the exercise of an option, the related premium received is adjusted to the basis of the instrument acquired or the instrument sold. The risk associated with writing options is based on the difference between the strike price of the option and current market price of the underlying security less premium received. See Note 8 for further discussion of Investment and Market Risk Factors and risks of written call and put options. The Company did not invest in option instruments during 2023.

Securities sold short: The Company may sell securities that it does not own, and it will therefore be obligated to purchase such securities at a future date. The value of the open short position is recorded as a liability, and the Company records an unrealized gain or loss to the extent of the difference between the proceeds received and the value of the open short position. The Company records a realized gain or loss when a short position is closed out. By entering into short sales, the Company bears the market risk of increases in the value of the security sold short in excess of the proceeds received. Possible losses from short sales differ from losses that could be incurred from purchases of securities because losses from short sales may be unlimited whereas losses from purchases cannot exceed the total amount invested. See Note 1 regarding the Company’s investment goals and its use of covered positions and Note 8 for further discussion of Investment and Market Risk Factors.

During the year ended December 31, 2023, the Company realized proceeds of $2,746,121 from the sale of investment securities, with the proceeds being used to fund the Company’s operating division.

All transfers are recognized by the Company at the end of each reporting period. Transfers between Levels 2 and 3 (if any) generally relate to whether significant unobservable inputs are used for the fair value measurements. See Note 2 – Significant Accounting Policies for additional information related to the fair value hierarchy and valuation techniques and inputs. During the year ended December 31, 2023 there were no transfers between Levels.

| 14 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

3. Fair Value Measurements of Investments, Financial Instruments and Related Risks (continued)

The following table is a reconciliation of the beginning and ending balances for the Company’s assets measured at fair value on a recurring basis using significant unobservable inputs (Level 3) during the year ended December 31, 2023:

| Balance at | ||||

| December 31, 2023 | ||||

| Balance, December 31, 2022 | $ | 26,000,000 | ||

| Net change in unrealized (depreciation) on operating division | (32,375,445 | ) | ||

| Adjustment to opening cost of investment in operating division | 33,823,065 | |||

| Current year investment in operating division | 4,552,380 | |||

| Balance, December 31, 2023 | $ | 32,000,000 | ||

The Company’s Level 3 asset consists of the operating division at fair value and requires significant judgment due to the absence of quoted market prices, inherent lack of liquidity, heavy reliance on Level 3 inputs, and the long-term nature of such investments. The medical operating division is not a subsidiary or a separate legal entity, and forms part of Daxor. Since the Company’s operating division has not generated significant revenue and has incurred substantial operating losses. Due to these substantial losses, the operating division has been dependent on funding from the sale of, or earnings on, the Company’s investment securities, or proceeds from our margin facility to sustain operations. The primary assets of the operating division are primarily located in Oak Ridge, Tennessee and were initially valued at transaction value for identified assets (property and equipment, land, buildings and laboratory equipment), less accumulated depreciation adjusted for advances to the operating division, business operations and activity and realized losses. Based on Company initiatives started in 2016 and through 2023, related to potential partnerships, joint ventures, product development, marketing and other operations of the operating division, the Company hired an independent valuation company to perform a valuation of the operating division on a standalone basis. The Company updated the initial 2016 valuation and subsequent valuations at December 31, 2017 through December 31, 2023, using the blended Income and Market Approaches as defined in Statement of Financial Accounting Standards (“SFAS”) SFAS 157 (ASC Topic 820). Based on the valuation approaches, we determined a valuation of $32,000,000 at December 31, 2023. In determining the Income Approach value range, the Gordon Growth Model valuation technique was used with a discount rate of 20.0% and long-term growth rate of 3.0%. Significant increases (decreases) in these unobservable inputs in isolation could result in significant changes in fair value measurements. The Income Approach was weighted 35% split between the Gordon Growth model at 15% weight and the Exit Multiple at 20% weight, given the current financial performance and expectations as to longer-term revenue growth and profitability, and a Market Approach method split between Arm’s Length evidence at 30% and public trades weight at 35% for a total weight of 65% for the Market Approach. The Company has effected Arm’s Length transactions in which it sold shares and raised $4.5 million, for the Company resulting in a market valuation of approximately $41 million. Management has reviewed and assessed this valuation and concluded the valuation is reasonable.

| Fair Value | Valuation | Valuation | Unobservable | Range of Inputs | ||||||||||

| Asset | December 31, 2023 | Approach | Techniques | Inputs | (Weighted Average) | |||||||||

| Operating | ||||||||||||||

| Division | $ | 32,000,000 | Income | Discounted | Discount Rate | 20 | % | |||||||

| Approach | Cash | Long Term | 3 | % | ||||||||||

| Flow | Growth Rate | |||||||||||||

| (Gordon Growth) | Forecasted EBITDA | (101%)- 3.1 | % | |||||||||||

| Income | Discounted | Discount Rate | 20 | % | ||||||||||

| Approach | Cash | Long Term | 3 | % | ||||||||||

| Flow | Growth Rate | |||||||||||||

| (Exit Multiple) | Exit Multiple | 3.25 | % | |||||||||||

| Forecasted EBITDA | (101%)- 3.1 | % | ||||||||||||

| Market | Arm’s Length | N/A | N/A | |||||||||||

| Approach | Evidence | |||||||||||||

4. Revision of Opening Balance – Cost of Operating Division

For the year ended December 31, 2023, the company revised its method to account for the cost basis of the operating division by including the cumulative capital infusions made into the investment in the in the operating division to comply with ASC 946, Investment Companies. The Company increased the opening balance of the cost of the investment in the operating division by $33,823,065 for a revised beginning balance total of $36,941,922. The capital infusions in the investment in the operating division of $4,552,380 for the year ended December 31, 2023, are included in the accounting cost basis of the operating division as of December 31, 2023 of $41,494,302.

5. Derivative Instruments

The Company may write call and put options in order to generate additional investment income as part of its investment strategy.

| 15 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

5. Derivative Instruments - (continued)

For the period ended December 31, 2023, the Company did not trade in derivatives.

6. Income Taxes (Benefit)

The net income tax expense (benefit) for the period ended December 31, 2023 is comprised of the following:

| Current Income Tax Expense (Benefit): | ||||

| Federal | $ | - | ||

| State and local | - | |||

| Total current income tax expense (benefit) | - | |||

| Deferred Tax Expense: | ||||

| Federal | $ | - | ||

| State and local | - | |||

| Total deferred tax expense | - | |||

| Net income tax (benefit) | $ | - |

The Company has a net operating loss carryforward of approximately $32,147,367 at December 31, 2023. Approximately $16,744,764 of these losses relates to years prior to 2018 and will begin to expire in 2033. Approximately $15,402,603 of these losses relates to the years 2018 through 2023, and will not expire, but are subject to limitations on usage.

The following table sets forth the net operating loss carryforwards by state and local jurisdiction at December 31, 2023:

| Amount | Expiration Date | |||||

| New York State | $ | 2,926,396 | 2035 to Indefinite | |||

| New York City | $ | 1,275,431 | Indefinite | |||

| California | $ | 3,653,556 | 2039 to Indefinite | |||

| Tennessee | $ | 8,684,666 | Expires 2027-2037 | |||

| South Carolina | $ | 10,471,340 | Expires 2026-2037 | |||

At December 31, 2023, the Company had no material unrecognized tax benefits and no adjustments to liabilities or operations were required. The Company does not expect that its unrecognized tax benefits will materially increase within the next twelve months. The Company recognizes interest and penalties related to uncertain tax positions in investment administrative expenses. As of December 31, 2023, the Company has not recorded any provisions for accrued interest and penalties related to uncertain tax positions.

| 16 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

6. Income Taxes (Benefit) - (continued)

In certain cases, the Company’s uncertain tax positions are related to tax years that remain subject to examination by the relevant tax authorities. The Company files federal, state and local income tax returns in jurisdictions with varying statutes of limitations. The 2020 through 2022 tax years generally remain subject to examination by federal, state and local tax authorities.

Under Internal Revenue Code Section 542, a company is defined as a Personal Holding Company (“PHC”) if it meets both an ownership test and an income test. The ownership test is met if a company has five or fewer shareholders that own more than 50% of the company, which is applicable to Daxor. The income test is met if PHC income items such as dividends, interest and rents exceed 60% of adjusted ordinary gross income. Adjusted ordinary income is defined as all items of income except capital gains. For the year ended December 31, 2023, more than 60% of Daxor’s adjusted gross income came from items defined as PHC income.

Determining the PHC tax liability requires computing Daxor’s “undistributed PHC income” and taxing such PHC income at the statutory rate of 20%. Undistributed PHC income is current year taxable income of the Company, exclusive of the net operating loss carry forward deduction that is allowed for regular tax purposes. The Company incurred no liability for PHC for the period ended December 31, 2023 due to the net operating losses applied to realized gains incurred during the year.

| Computed expected provision at statutory rates | (21.0 | )% | ||

| State taxes | (0.8 | )% | ||

| Non-deductible/non-taxable and other items | 26.2 | % | ||

| Dividend received deduction and other items | (4.4 | )% | ||

| Effective income tax (benefit) rate | 0.0 | % |

The Company is not a party to any advisory services agreements and as such has no related liabilities.

7. Deferred Income Taxes

Deferred income taxes result from differences in the recognition of gains and losses on marketable securities, stock options, as well as from carryforwards of the Company’s net operating losses of approximately $32,147,367 at December 31, 2023, and tax credits of approximately $1,793,281 in research tax credits for tax purposes. At December 31, 2023 the aggregate cost of investments for federal income tax purposes was $4,129,762.

| 17 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

7. Deferred Income Taxes - (continued)

The significant components of deferred tax assets and liabilities are reflected in the following table:

| Unrealized losses on investments in securities | $ | (432,967 | ) | |

| Unrealized loss on investment in operating division | (6,823,748 | ) | ||

| Net operating loss carryforward | 8,150,527 | |||

| Business tax credits carried forward | 1,793,281 | |||

| Others | 77,685 | |||

| Deferred Income Tax Available for use | 2,764,779 | |||

| Valuation allowance | (2,764,779 | ) | ||

| Net Deferred Tax Asset | $ | - |

Realization of deferred tax assets is dependent on future earnings. Due to the uncertainty of the realization of its net deferred tax assets, the Company has provided a valuation allowance. In assessing the potential to realize the deferred tax asset, management considers whether it is more likely than not that some or perhaps all of the deferred tax assets will be realized. The ultimate realization of deferred tax assets is dependent upon the generation of future taxable income during the periods in which these temporary differences become deductible. Management considers the scheduled reversal of deferred tax liabilities, projected future taxable income and tax planning strategies in making their assessment. The Company recorded a valuation allowance of $2,764,779 at December 31, 2023. The valuation allowance increased $176,643 from December 31, 2022. If the Company becomes profitable before the expiration of the loss carryforwards, it would have the ability to utilize them in order to offset any taxable income.

8. Investment and Market Risk Factors

The Company enters into investments in securities, call and put options and securities borrowed and/or financial instruments that may have off-balance sheet risks, where the potential loss due to changes in the market (market risk), failure of counterparty to perform on the transaction risk (credit risk) and other risk elements, such as interest rate risk, exceeds the value and/or obligations of such financial instruments. It is the Company’s general policy to mitigate such risks by transacting with established counterparties. The Company transacts with and custodies investment assets at UBS Financial Services, Inc. (the “Broker”).

The Company’s investments in securities arise from investments in long common and preferred stocks, selling common stocks short and transacting in put and call (naked and covered) options. These investments are subject to equity risks of increases and decreases in market exchange prices such as on the Nasdaq stock exchange.

| 18 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

8. Investment and Market Risk Factors - (continued)

The Company is subject to certain inherent risks arising from its investing activities of selling securities short and writing put and call options. Selling securities short creates an obligation to purchase the securities at an unknown future date, subject to the Company’s discretion, at the then prevailing future market prices. Securities borrowed create the risk that the ultimate obligation may exceed the liability reflected in these financial statements.

The Company collects premiums and the opportunity to create option premium income when writing put and call options if the options expire out-of-the-money. Writing put and call options gives the option buyer the right to exercise the option against the option writer. Writing put options obligates the writer to purchase the stock at the strike price if the stock’s current market price is below the strike price prior to expiration of the put option. The potential loss in writing a put option is the strike price less the premium collected if the stock price falls to zero. Writing call options obligates the writer to sell the stock at the strike price if the stock’s current market price is greater than the strike price prior to expiration of the call option. The potential loss in writing a naked call option is unlimited as the rise of a stock price is unlimited. The potential loss in writing a covered call is limited to the strike price less the cost of the underlying security the Company holds in the portfolio. The Company endeavors to write covered calls but may also write naked calls.

Cash receivable from the Broker (if any) and margin loans payable reflect accounts with the Broker. Margin loan payable represents obligations to the Broker for leveraging investments in securities. Investments in securities are collateral for the margin loan payable. The Company does not have the right of setoff nor netting agreements between brokers.

The Company’s investments may be subject to changes in interest rates as they may affect equity and option markets. Interest rate risk refers to the fluctuations in value of fixed-income securities resulting from the inverse relationship between price and yield. For example, an increase in general interest rates will tend to reduce the market value of already issued fixed-income investments, and a decline in general interest rates will tend to increase their value. In addition, debt securities with longer maturities, which tend to have higher yields, are subject to potentially greater fluctuations in value from changes in interest rates than obligations with shorter maturities.

The Company is subject to volatility risk which refers to the magnitude of the movement, but not the direction of the movement, in a financial instrument’s price over a defined time period. Large increases or decreases in a financial instrument’s price over a relative time period typically indicate greater volatility risk, while small increases or decreases in its price typically indicate lower volatility risk.

Legal, tax and regulatory changes continue to occur in the United States and globally; additionally, regulatory environments, as a whole, continue to evolve and change. The effect of any future legal, tax and/or regulatory changes are unknown and could be substantial and adverse.

9. Portfolio Administrative Expenses

The Company reported $128,666 of portfolio administrative expenses, which are included in investment administrative charges on the Statement of Operations for the year ended December 31, 2023. These charges represent a portion of the payroll and related expenses of two (2) employees for services performed for the Company.

| 19 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

10. Margin Loan

The Company has total margin loan payable at December 31, 2023 of $755,659. This loan is secured by the Company’s investments in marketable securities. The interest expense on the margin loans for the year ended December 31, 2023 was $49,102. The ability of the Company to incur margin debt at any given time is based on the current amount outstanding and the market value of the portfolio of marketable securities. There are no set repayment terms for the Company’s margin loan.

The following table summarizes the margin loan activity for the year ended December 31, 2023:

| Balance at 12/31/23 | Interest

rate at 12/31/23 | Maximum

amount outstanding during the year | Average

amount outstanding during the year | Weighted

average interest rate during the year | ||||||||

| $ | 755,659 | 6.551% | $ | 2,438,635 | $828,138 | 5.995% | ||||||

The Company’s investment in securities detailed in Schedule 1 serves as collateral for the margin facility with the Broker.

11. Capital Stock

At December 31, 2023, there were 10,000,000 shares of $0.01 par value capital stock authorized. The paid-in capital of $13,744,205 at December 31, 2023 consists of the following amounts:

| Additional Paid-in Capital in excess of par value of common stock | $ | 13,691,039 | ||

| Common Stock | 53,166 | |||

| Total Paid-in Capital | $ | 13,744,205 |

12. Treasury Stock

The Company’s Board of Directors from time to time has authorized the repurchase of shares of the Company’s common stock in the open market usually as funds are available and if the stock is trading at a price which management feels is undervalued. The Company did not repurchase any shares of the Company during the year ended December 31, 2023.

Treasury stock at December 31, 2023:

| Treasury Stock at repurchase price | $ | 4,826,943 | ||

| Treasury Stock shares | 510,183 |

During the year 2023, the Company sold 464,599 shares out of Treasury shares at a price of $9.75 per share. Gross proceeds from the sale were $4,529,840. Net proceeds to the Company were $4,128,572. The Net Asset Value (“NAV”) per share was approximately $6.39 per share as compared to (gross value) $9.75 at the time the Treasury shares were sold.

13. Dividends

In 2008, management instituted a policy of paying dividends when funds are available. The Company did not declare a dividend for the year ended December 31, 2023.

| 20 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

14. Stock Options

In June 2019, the Board of Directors of the Company approved the Daxor Corporation 2020 Incentive Compensation Plan (the “2020 Plan”). In April 2020, the Company received exemptive relief from the Securities & Exchange Commission (“SEC”) and the 2020 Plan was given approval to become operational effective in April, 2020. The 2020 Plan was approved by shareholders of the Company on June 25, 2020. In addition to Stock Options, awards under the 2020 Plan can consist of Stock Appreciation Rights, Restricted Stock, Restricted Stock Units, Deferred Stock Units, Cash Awards and Bonus Stock (collectively, “Stock Awards”). The 2020 Plan is an effort to provide incentive to employees, officers, agents, consultants, and independent contractors through proprietary interest. The Board of Directors acts as the Plan Administrator, and may issue these Stock Awards at its discretion.

The 2020 Plan replaced the 2004 Stock Option Plan.

The maximum number of shares that may be issued under the 2020 Plan is 250,000 or 5% of the Company’s outstanding shares, whichever is greater. The Company has obtained approval from shareholders to increase the number of shares available for issuance from 250,000 shares to 400,000 shares (or such lesser amount as may be determined by the Company), subject to the SEC granting an exemptive order to permit the operation of the 2020 Plan as amended, and the SEC may not elect to grant such order. Under the provisions of the 2020 Plan, the exercise price of any stock options issued is a minimum of 100% of the closing market price of the Company’s stock on the grant date of the option. Previously, the Company issued options to various employees under the previous 2004 Stock Option Plan and the Stock Option Plan that was also administered by the Board of Directors. All issuances have varying vesting and expiration timelines. As of December 31, 2023, the 2020 Plan had 308,774 options outstanding and 167,833 were exercisable. The 2004 Stock Option Plan has 26,166 options outstanding and 26,166 are exercisable. The Company has not granted options under the 2004 Stock Option Plan since August 2018. The 2004 Stock Option Plan ceased operation upon approval of the 2020 Plan, although stock options that were awarded under the 2004 Plan that have not expired are still eligible to be exercised.

At December 31, 2023, there was $1,298,113 of unvested stock-based compensation expense to recognize. The Company recognized $631,701 of stock-based compensation expense, which is included in investment administrative charges in the Statement of Operations for the year ended December 31, 2023. There was no aggregate intrinsic value at December 31, 2023 as the closing price of the Company’s stock was lower than the average exercise price of the underlying options. The intrinsic value is calculated based on the difference between the closing market price of the Company’s common stock and the exercise price of the underlying options.

To calculate the option-based compensation, the Company used the Black-Scholes option-pricing model. The Company’s determination of fair value of option-based awards on the date of grant using the Black-Scholes model is affected by the Company’s stock price as well as assumptions regarding a number of subjective variables. These variables include, but are not limited to, the Company’s expected stock price volatility over the term of the awards, risk-free interest rate, and the expected life of the options. The risk-free interest rate is based on a treasury instrument whose term is consistent with the expected life of the stock options. The expected volatility, holding period of options are based on historical experience.

For the year ended December 31, 2023, 127,112 stock options were granted to employees, Directors and outside consultants from the 2020 Plan with a weighted average exercise price of $9.67. The stock options granted during the year ended December 31, 2023 from the 2020 Plan are still outstanding and 167,833 stock options have vested as of December 31, 2023.

The fair values of stock options granted in the twelve month period ended December 31, 2023 were estimated using the Black-Scholes option-pricing model with the following assumptions for the year ended December 31, 2023.

| 2023 | ||||

| Risk free rate | 4.89 | % | ||

| Expected life (in years) | 4.50 | |||

| Expected volatility | 55.11 | % | ||

| Dividend yield | 0.00 | % | ||

| Weighted Average grant date fair value per share | $ | 9.66 | ||

| 21 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

14. Stock Options - (continued)

The details of option activity for the 2020 Plan for the year ended December 31, 2023 are as follows:

| Number

of Shares | Weighted

Average Exercise Price | |||||||

| Outstanding and Exercisable, January 1, 2023 | 256,501 | $ | 13.77 | |||||

| Granted | 127,112 | $ | 9.67 | |||||

| Canceled | (74,839 | ) | $ | (13.55 | ) | |||

| Expired | - | - | ||||||

| Outstanding at December 31, 2023 | 308,774 | $ | 12.08 | |||||

The following tables summarize information concerning currently outstanding and exercisable options at December 31, 2023:

| Range

of Exercise Prices | Number Outstanding at December 31, 2023 | Weighted

Average Remaining Contractual Life at December 31, 2023 | Weighted Average Exercise Price at December 31, 2023 | |||||||||||

| $ | 7.84 - $18.95 | 308,774 | 4.5 years | $ | 12.08 | |||||||||

| Range

of Exercise Prices -Vested | Number Exercisable at December 31, 2023 -Vested | Weighted Average Exercise Price at December 31, 2023 -Vested | ||||||||

| $ | 9.41 - $14.11 | 167,833 | $ | 13.16 | ||||||

The details of employee option activity for the 2004 Stock Option Plan for the year ended December 31, 2023 is as follows:

| Number

of Shares | Weighted Average Exercise Price | |||||||

| Outstanding and Exercisable, January 1, 2023 | 147,066 | $ | 8.47 | |||||

| Granted | - | - | ||||||

| Exercised | (13,500 | ) | $ | (4.72 | ) | |||

| Expired | (64,650 | ) | $ | (9.09 | ) | |||

| Canceled | (42,750 | ) | $ | (8.43 | ) | |||

| Outstanding at December 31, 2023 | 26,166 | $ | 8.92 | |||||

The following tables summarize information concerning currently outstanding and exercisable options from the 2004 Stock Option Plan at December 31, 2023:

| Range

of Exercise Prices | Number Outstanding at December 31, 2023 | Weighted Average Remaining Contractual Life at December 31, 2023 | Weighted Average Exercise Price at December 31, 2023 | |||||||||||

| $ | 7.75 - $9.46 | 26,166 | 0.38 years | $ | 8.92 | |||||||||

| Range

of Exercise Prices -Vested | Number Exercisable at December 31, 2023 -Vested | Weighted

Average December 31, 2023 -Vested | ||||||||

| $ | 7.75 - $9.46 | 26,166 | $ | 8.92 | ||||||

| 22 |

Daxor Corporation

Notes to Financial Statements

December 31, 2023

14. Stock Options - (continued)

The following table summarizes information about restricted stock and stock awards transactions:

| Year

Ended December 31, 2023 | Weighted Average Grant Date Fair Value | |||||||

| Unvested at the beginning of the period | 9,813 | $ | 10.98 | |||||

| Awards granted | 28,556 | $ | 9.23 | |||||

| Vested | (31,297 | ) | $ | (11.25 | ) | |||

| Unvested at the end of period | 7,071 | $ | 9.83 | |||||

15. Commitments

There are no commitments for the Company as of this date.

16. Registration Statement

The Company has filed a Form N-2 Registration Statement under the Securities Act of 1933, which permits the Company to raise additional equity capital by issuing additional shares of common stock from time to time in varying amounts and by different offering methods, at prices and on terms to be determined by market conditions at the time of offering. During any 12-month period, the aggregate market value of securities the Company may offer may not exceed one third of the aggregate market value of voting and non-voting common equity held by persons who are not affiliates of the Company. The Registration Statement became effective July 16, 2021.

17. Capital Share Transaction

The Statement of Changes in Net Assets discloses the value of shares issued as stock-based compensation, the dollar amounts received for shares sold, and the increase in net assets from the issuance of stock for the past two years, and such information is incorporated herein by reference. The table below shows the number of shares issued as stock-based compensation, and the number of shares sold for the past two years. No shares were issued to shareholders in reinvestment of dividends, and no shares were redeemed during the past two years.

For the Year Ended December 31, 2023 | For the Year Ended December 31, 2022 (unaudited) | |||||||

| Shares issued stock-based compensation | 50,684 | 31,018 | ||||||

| Shares sold | 464,599 | 221,050 | ||||||

| Shares reinvested from distributions | - | - | ||||||

| Shares redeemed | - | - | ||||||

| Net increase | 515,283 | 252,068 | ||||||

18. Subsequent Events

Nothing to report as of this date

| 23 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Shareholders of Daxor Corporation

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Daxor Corporation (the “Company”), including the schedule of investments, as of December 31, 2023, and the related statements of operations, changes in net assets, cash flows, and financial highlights for the year ended December 31, 2023, and the related notes to the financial statements (collectively, the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2023, and the results of its operations, changes in net assets, cash flows and financial highlights for the year ended December 31, 2023, in conformity with accounting principles generally accepted in the United States of America.

The financial statements of the Company as of and for the year ended December 31, 2022 and the financial highlights for each of the periods ended on or prior to December 31, 2022 (not presented herein, other than the statement of changes in net assets and the financial highlights) were audited by other auditors whose report dated March 1, 2023 expressed an unqualified opinion on those financial statements and financial highlights.

Basis for Opinion

These financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on the Company’s financial statements based on our audit. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audit in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Company is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audit, we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audit included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of December 31, 2023, by correspondence with the custodian and others. Our audit also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audit provides a reasonable basis for our opinion.

Emphasis of Matter

As discussed in Note 4 to the financial statements, the Company revised its method to account for the cost basis of the operating division by including the cumulative capital infusions made into the investment in the operating division to comply with Accounting Standards Codification 946, Investment Companies. Our opinion is not modified with respect to that matter.

| /s/ Citrin Cooperman & Company, LLP | |

| New York, New York | |

| March 15, 2024 |

We have served as the Company’s auditor since 2023.

| 24 |

Daxor Corporation

Investment Products Offered

| ● | Are not FDIC Insured |

| ● | May Lose Value |

| ● | Are Not Bank Guaranteed |

The investment return and principal value of an investment in Daxor Corporation will fluctuate in part as the prices of the individual securities in which it invests fluctuate, so that your shares, when sold, may be worth more or less than their original cost. You should consider the investment objectives, risks, charges and expenses of Daxor and Daxor’s operating business carefully before investing. For a free copy of the Company’s definitive prospectus (when available), which contains this and other information, call the Company at 212- 330-8500.

This shareholder report must be preceded or accompanied by the Company’s prospectus for individuals who are not current shareholders of the Company.

Voting Proxies on Portfolio Securities

A description of the policies and procedures that the Company uses to determine how to vote proxies relating to portfolio securities owned by the Company and the Company’s proxy voting record for the 12-month period ended June 30, 2023 are available (i) without charge, upon request, by calling 1-212-330-8500 and (ii) on the Securities and Exchange Commission’s website: www.sec.gov.

Disclosure of Portfolio Holdings

The SEC has adopted the requirement that all investment companies file a complete schedule of investments with the SEC for their first and third fiscal quarters on Form N-PORT. The Company’s Form N-PORT for March 31, 2023, and September 30, 2023 reporting portfolio securities held by the Company, are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the public reference room may be obtained by calling 800-SEC-0330.

Shareholder Vote

The Company’s Annual Meeting was held July 11, 2023. At the Annual Meeting, the following directors were elected for terms expiring at the annual meeting of shareholders to be held in 2024 by the votes indicated:

| For | Withheld | Broker Non-votes | ||||||||||

| James Lombard (See Note) | 3,498,907 | 87,254 | - | |||||||||

| Henry D. Cremisi, MD | 3,500,783 | 85,378 | - | |||||||||

| Edward Feuer | 3,500,783 | 85,378 | - | |||||||||

| Joy Goudie, Esq. | 3,500,783 | 85,378 | - | |||||||||

| Michael Feldschuh | 3,505,372 | 80,789 | - | |||||||||

| Jonathan Feldschuh | 3,485,491 | 100,670 | - | |||||||||

| Caleb DesRosiers, Esq. | 3,508,783 | 77,378 | - | |||||||||

NOTE: Mr. James Lombard passed away on October 17, 2023.

The following reflects the voting results for matters other than the election of directors brought for vote at the Annual Meeting:

| For | Against | Abstain | Broker Non-votes | |||||||||||||

| Ratification of Steven Zelin & Associates C.P.A. as Daxor Corporation’s independent registered public accounting firm (1) | 3,568,964 | 16,671 | 526 | 0 | ||||||||||||

Since the filing of the Proxy Statement the Company has chosen Citrin Cooperman & Company, LLP as the audit firm for 2023. Steven Zelin & Associates C.P.A continues to prepare the Company’s tax returns.

| 25 |

Rule 8b-16 under the Investment Company Act of 1940, as amended, requires that we disclose certain information to stockholders in our annual report. That disclosure is included in this report as provided below:

Dividend Reinvestment Plan

Daxor does not maintain a dividend reinvestment plan.

Information Investment Objectives and Policies

Daxor’s investment objectives and policies are provided below. There have not been any material changes to the investment objectives and policies that have not been approved by shareholders.

Our objective is to support and expand our operating businesses, through organic growth (i.e., the rate of business expansion through internal enhancement of the business and operations as opposed to mergers, acquisitions and takeovers). The company is not primarily engaged in the business of investing, reinvesting, owning, holding or trading in securities. Funds in excess of the company’s business needs are placed in instruments designed to maximize capital preservation and assure liquidity. The foregoing policies may be changed without a shareholder vote.

We concentrate our investments in the utility industry and have an investment policy that calls for a minimum of 80% of the company’s investment portfolio to consist of electric utility stocks. The Board of Directors has authorized this minimum to be temporarily lowered to 70% when management deems it to be necessary. At least once a year, the company reviews its investment strategy, and more frequently as needed, at board meetings.

The investment portfolio primarily consists of electric utility companies which are publicly traded common and preferred stock. In addition to receiving income from dividends from the securities held in the investment portfolio, we also have an investment policy of selling puts on stocks that we are willing to own. Such options usually have a maturity of less than 1 year. The company will also sell covered calls on securities within its investment portfolio. Covered calls involve stocks, which usually do not exceed 15% of the value of the company’s portfolio.

We will, at times, sell naked or uncovered calls, as well as, engage in short sales as part of an income strategy, and to a lesser extent a strategy to mitigate risk. Our net short position will usually amount to less than 15% of the company’s portfolio value.

At this time, investments in debt instruments and foreign securities are not a principal investment strategy, and we expect any such investments to be minimal.

Our management expects that our investment portfolio will continue to consist primarily of publicly traded common and preferred stocks of electric utilities. The percentage of investments other than electric utilities is expected to remain at less than 20% of the investment portfolio.

With regard to the non-principal investments for the investment portfolio, we are flexible in how we may allocate our investments. We may allocate the non-principal investments among the following types of securities, in proportions which reflect the judgment of our management of the potential returns and risks of such securities:

| ● | Common stocks and other equity securities (including common stocks, preferred stocks, convertible preferred stocks, warrants, options and American Depository Receipts); | |

| ● | Bonds and other debt securities (including U.S. Treasury Notes and Bonds, investment grade corporate debt securities, convertible debt securities and debt securities below investment grade); and | |

| ● | Money market instruments. |

| 26 |

Principal Risk Factors

Daxor’s principal risk factors are provided below. There have not been any material changes to the principal risk factors.

Investment Portfolio Risks

Market Risks

Loss of money is a risk of investing in the company. The net asset value of the company can be expected to change daily and you may lose money. There is no guarantee that the performance of our investment portfolio will be positive over any period of time, either short-term or long-term. Market risk may affect a single issuer, industry, sector of the economy, or the market as a whole.

U.S. and international markets have experienced significant periods of volatility in recent years due to a number of economic, political and global macro factors, including the impact of the coronavirus (COVID-19) as a global pandemic and related public health issues, the ongoing military conflict between Russia and Ukraine, military conflict between Israel and Hamas, the growth concerns in the U.S. and overseas, uncertainties regarding interest rates, trade tensions and the threat of tariffs imposed by the U.S. and other countries. Health crises and related political, social and economic disruptions caused by the spread of the recent coronavirus outbreak may exacerbate other pre-existing political, social and economic risks in certain countries. It is not possible to know the extent of these impacts, and they may be short term or may last for an extended period of time. These developments as well as other events, could result in further market volatility and negatively affect security prices, the liquidity of certain securities and the normal operations of securities exchanges and other markets, despite government efforts to address market disruptions.

Equity Investments