Use these links to rapidly review the document

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES INDEX

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly period ended March 30, 2008 |

|

OR |

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to . |

|

Commission File Number: 1-14829

Molson Coors Brewing Company

(Exact name of registrant as specified in its charter)

| DELAWARE (State or other jurisdiction of incorporation or organization) |

84-0178360 (I.R.S. Employer Identification No.) |

|

1225 17th Street, Denver, Colorado, USA 1555 Notre Dame Street East, Montréal, Québec, Canada (Address of principal executive offices) |

80202 H2L 2R5 (Zip Code) |

|

303-279-6565 (Colorado) 514-521-1786 (Québec) (Registrant's telephone number, including area code) |

||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer," "accelerated filer," and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of April 25, 2008:

Class A

Common Stock—2,674,772 shares

Class B Common Stock—150,749,605 shares

Exchangeable shares:

As of April 25, 2008, the following number of exchangeable shares was outstanding for Molson Coors Canada, Inc.:

Class A

Exchangeable shares—3,314,096

Class B Exchangeable shares—24,795,839

In addition, the registrant has outstanding one share of special Class A voting stock, through which the holders of Class A exchangeable shares and Class B exchangeable shares of Molson Coors Canada Inc. (a subsidiary of the registrant), respectively, may exercise their voting rights with respect to the registrant. The special Class A and Class B voting stock are entitled to one vote for each of the exchangeable share classes, respectively, excluding shares held by the registrant or its subsidiaries, and generally vote together with the Class A common stock and Class B common stock, respectively, on all matters on which the Class A common stock and Class B common stock are entitled to vote. The trustee holder of the special Class A voting stock and the special Class B voting stock has the right to cast a number of votes equal to the number of then outstanding Class A exchangeable shares and Class B exchangeable shares, respectively.

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

INDEX

2

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(IN MILLIONS, EXCEPT PER SHARE DATA)

(UNAUDITED)

| |

Thirteen Weeks Ended |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||||||

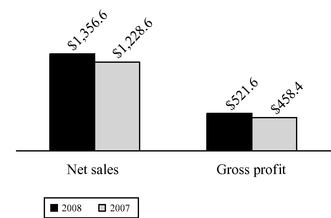

| Sales | $ | 1,816.2 | $ | 1,651.2 | ||||

| Excise taxes | (459.6 | ) | (422.6 | ) | ||||

| Net sales | 1,356.6 | 1,228.6 | ||||||

| Cost of goods sold | (835.0 | ) | (770.2 | ) | ||||

| Gross profit | 521.6 | 458.4 | ||||||

| Marketing, general and administrative expenses | (436.6 | ) | (396.8 | ) | ||||

| Special items, net | (7.3 | ) | (8.2 | ) | ||||

| Operating income | 77.7 | 53.4 | ||||||

| Interest expense, net | (23.9 | ) | (26.3 | ) | ||||

| Debt extinguishment costs | (12.4 | ) | — | |||||

| Other income, net | 4.6 | 1.2 | ||||||

| Income from continuing operations before income taxes and minority interests | 46.0 | 28.3 | ||||||

| Income tax benefit (expense) | 5.5 | (5.3 | ) | |||||

| Income from continuing operations before minority interests | 51.5 | 23.0 | ||||||

| Minority interests in net income of consolidated entities | (5.4 | ) | (3.8 | ) | ||||

| Income from continuing operations | 46.1 | 19.2 | ||||||

| Loss from discontinued operations, net of tax | (9.0 | ) | (14.8 | ) | ||||

| Net income | $ | 37.1 | $ | 4.4 | ||||

| Basic income (loss) per share: | ||||||||

| From continuing operations | $ | 0.25 | $ | 0.11 | ||||

| From discontinued operations | (0.05 | ) | (0.08 | ) | ||||

| Basic net income per share | $ | 0.20 | $ | 0.03 | ||||

| Diluted income (loss) per share: | ||||||||

| From continuing operations | $ | 0.25 | $ | 0.11 | ||||

| From discontinued operations | (0.05 | ) | (0.08 | ) | ||||

| Diluted net income per share | $ | 0.20 | $ | 0.03 | ||||

| Weighted average shares—basic | 181.0 | 176.1 | ||||||

| Weighted average shares—diluted | 184.5 | 178.2 | ||||||

See notes to unaudited condensed consolidated financial statements

3

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(IN MILLIONS)

(UNAUDITED)

| |

As of |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

December 30, 2007 |

||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 118.7 | $ | 377.0 | ||||

| Accounts receivable, net | 684.2 | 758.5 | ||||||

| Other receivables, net | 162.1 | 112.6 | ||||||

| Inventories: | ||||||||

| Finished, net | 171.7 | 164.0 | ||||||

| In process | 50.6 | 40.7 | ||||||

| Raw materials | 76.8 | 82.3 | ||||||

| Packaging materials, net | 83.9 | 82.6 | ||||||

| Total inventories, net | 383.0 | 369.6 | ||||||

| Other assets, net | 117.3 | 135.7 | ||||||

| Deferred tax assets | 18.0 | 17.9 | ||||||

| Discontinued operations | 5.7 | 5.5 | ||||||

| Total current assets | 1,489.0 | 1,776.8 | ||||||

| Properties, net | 2,643.4 | 2,696.2 | ||||||

| Goodwill | 3,257.9 | 3,346.5 | ||||||

| Other intangibles, net | 4,846.5 | 5,039.4 | ||||||

| Deferred tax assets | 292.3 | 336.9 | ||||||

| Notes receivable, net | 71.3 | 71.2 | ||||||

| Other assets | 191.4 | 179.5 | ||||||

| Discontinued operations | 4.6 | 5.1 | ||||||

| Total assets | $ | 12,796.4 | $ | 13,451.6 | ||||

See notes to unaudited condensed consolidated financial statements.

4

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(IN MILLIONS, EXCEPT PAR VALUE)

(UNAUDITED)

| |

As of |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

December 30, 2007 |

||||||

| Liabilities and stockholders' equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 310.5 | $ | 380.7 | ||||

| Accrued expenses and other liabilities | 1,018.8 | 1,189.1 | ||||||

| Deferred tax liabilities | 146.5 | 120.6 | ||||||

| Short-term borrowings and current portion of long-term debt | 34.4 | 4.3 | ||||||

| Discontinued operations | 41.1 | 40.8 | ||||||

| Total current liabilities | 1,551.3 | 1,735.5 | ||||||

| Long-term debt | 2,030.8 | 2,260.6 | ||||||

| Pension and post-retirement benefits | 637.4 | 677.8 | ||||||

| Derivative hedging instruments | 421.7 | 477.4 | ||||||

| Deferred tax liabilities | 571.6 | 605.4 | ||||||

| Unrecognized tax benefits | 267.4 | 285.9 | ||||||

| Other liabilities | 87.4 | 90.9 | ||||||

| Discontinued operations | 126.7 | 124.8 | ||||||

| Total liabilities | 5,694.3 | 6,258.3 | ||||||

| Minority interests | 45.1 | 43.8 | ||||||

| Stockholders' equity | ||||||||

| Capital stock: | ||||||||

| Preferred stock, non-voting, no par value (authorized: 25.0 shares; none issued) | — | — | ||||||

| Class A common stock, voting, $0.01 par value per share (authorized: 500.0 shares; issued and outstanding: 2.7 shares at March 30, 2008 and December 30, 2007) | — | — | ||||||

| Class B common stock, non-voting, $0.01 par value per share (authorized: 500.0 shares; issued and outstanding: 150.5 shares and 149.6 shares at March 30, 2008 and December 30, 2007, respectively) | 1.5 | 1.5 | ||||||

| Class A exchangeable shares (issued and outstanding: 3.3 shares at March 30, 2008 and December 30, 2007) | 124.7 | 124.8 | ||||||

| Class B exchangeable shares (issued and outstanding: 24.9 shares and 25.1 shares at March 30, 2008 and December 30, 2007, respectively) | 935.6 | 945.3 | ||||||

| Total capital stock | 1,061.8 | 1,071.6 | ||||||

| Paid-in capital | 3,096.2 | 3,022.5 | ||||||

| Retained earnings | 1,958.7 | 1,950.5 | ||||||

| Accumulated other comprehensive income | 940.3 | 1,104.9 | ||||||

| Total stockholders' equity | 7,057.0 | 7,149.5 | ||||||

| Total liabilities and stockholders' equity | $ | 12,796.4 | $ | 13,451.6 | ||||

See notes to unaudited condensed consolidated financial statements.

5

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(IN MILLIONS)

(UNAUDITED)

| |

Thirteen Weeks Ended |

||||||||

|---|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

|||||||

| Cash flows from operating activities: | |||||||||

| Net income | $ | 37.1 | $ | 4.4 | |||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||

| Depreciation and amortization | 82.3 | 83.4 | |||||||

| Share-based compensation | 38.6 | 6.7 | |||||||

| Gain on sale of properties and intangibles | (23.2 | ) | — | ||||||

| Deferred income taxes | (2.4 | ) | 1.1 | ||||||

| Equity in net income of unconsolidated affiliates | (5.9 | ) | (2.6 | ) | |||||

| Minority interest in net income of consolidated entities | 5.4 | 3.8 | |||||||

| Excess tax benefits from share-based compensation | (3.6 | ) | (15.8 | ) | |||||

| Change in current assets and liabilities and other | (263.5 | ) | (268.5 | ) | |||||

| Discontinued operations | 9.0 | 14.8 | |||||||

| Net cash used in operating activities | (126.2 | ) | (172.7 | ) | |||||

| Cash flows from investing activities: | |||||||||

| Additions to properties and intangible assets | (69.5 | ) | (107.0 | ) | |||||

| Proceeds from sales of properties and intangible assets | 28.3 | 1.0 | |||||||

| Proceeds from sale of investment securities, net | 22.8 | — | |||||||

| Investment in an unconsolidated affiliate | (7.0 | ) | — | ||||||

| Trade loan repayments from customers | 6.9 | 7.1 | |||||||

| Trade loans advanced to customers | (9.2 | ) | (5.2 | ) | |||||

| Other | 2.6 | 0.2 | |||||||

| Net cash used in investing activities | (25.1 | ) | (103.9 | ) | |||||

| Cash flows from financing activities: | |||||||||

| Exercise of stock options under equity compensation plans | 23.0 | 144.9 | |||||||

| Excess tax benefits from share-based compensation | 3.6 | 15.8 | |||||||

| Dividends paid | (28.9 | ) | (28.4 | ) | |||||

| Dividends paid to minority interest holders | (4.2 | ) | — | ||||||

| Payments on long-term debt and capital lease obligations | (180.6 | ) | (0.1 | ) | |||||

| Proceeds from short-term borrowings | 30.5 | 86.4 | |||||||

| Payments on short-term borrowings | (0.1 | ) | (66.1 | ) | |||||

| Net proceeds from revolving credit facilities | — | 60.2 | |||||||

| Change in overdraft balances and other | 39.1 | 0.7 | |||||||

| Settlements of debt-related derivatives | 12.0 | — | |||||||

| Net cash (used in) provided by financing activities | (105.6 | ) | 213.4 | ||||||

| Cash and cash equivalents: | |||||||||

| Net decrease in cash and cash equivalents | (256.9 | ) | (63.2 | ) | |||||

| Effect of foreign exchange rate changes on cash and cash equivalents | (1.4 | ) | 0.4 | ||||||

| Balance at beginning of year | 377.0 | 182.2 | |||||||

| Balance at end of period | $ | 118.7 | $ | 119.4 | |||||

See notes to unaudited condensed consolidated financial statements.

6

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES

On February 9, 2005, Adolph Coors Company merged with Molson Inc. (the "Merger"). In connection with the Merger, Adolph Coors Company became the parent of the merged Company and changed its name to Molson Coors Brewing Company. Unless otherwise noted in this report, any description of us includes Molson Coors Brewing Company ("MCBC" or the "Company"), principally a holding company, and its operating subsidiaries: Coors Brewing Company ("CBC"), operating in the United States ("U.S."); Coors Brewers Limited ("CBL"), operating in the United Kingdom ("U.K."); Molson Canada ("Molson"), operating in Canada; and our other corporate entities. Any reference to "Coors" means the Adolph Coors Company prior to the Merger. Any reference to Molson Inc. means Molson prior to the Merger. Any reference to "Molson Coors" means MCBC after the Merger.

Unless otherwise indicated, information in this report is presented in U.S. dollars ("USD" or "$").

Unaudited Condensed Consolidated Financial Statements

The accompanying unaudited condensed consolidated financial statements reflect all adjustments, consisting of normal recurring accruals, which are necessary for a fair statement of the financial position, results of operations and cash flows for the periods presented. The accompanying condensed consolidated financial statements include our accounts, the accounts of our majority-owned subsidiaries and certain variable interest entities of which we are the primary beneficiary. All intercompany transactions and balances have been eliminated in consolidation. These condensed consolidated financial statements should be read in conjunction with the consolidated financial statements, including the notes thereto, contained in our Annual Report on Form 10-K for the year ended December 30, 2007. The results of operations for the thirteen week period ended March 30, 2008, are not necessarily indicative of the results that may be achieved for the full fiscal year and cannot be used to indicate financial performance for the entire year.

The December 30, 2007 condensed consolidated balance sheet data was derived from audited financial statements, but does not include all disclosures required by accounting principles generally accepted in the United States of America ("U.S. GAAP").

Reporting Periods Presented

MCBC follows a 52/53 week fiscal reporting calendar. The first fiscal quarter of 2008 and 2007 consisted of 13 weeks ending on March 30, 2008 and April 1, 2007, respectively. Fiscal year 2008 and 2007 consist of 52 weeks ending on December 28, 2008 and December 30, 2007, respectively.

Since the Merger, the results from Brewers Retail Inc. ("BRI") are reported one month in arrears in the accompanying unaudited condensed consolidated financial statements.

Use of estimates

Our consolidated financial statements are prepared in accordance with U.S. GAAP. These accounting principles require us to make certain estimates, judgments and assumptions. We believe that the estimates, judgments and assumptions are reasonable, based on information available at the time they are made. To the extent there are material differences between these estimates and actual results, our consolidated financial statements may be affected.

7

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES (Continued)

Reclassifications

Certain prior period amounts have been reclassified to conform to the current period presentation.

Adoption of New Accounting Pronouncements

SFAS No. 157 "Fair Value Measurements"

In September 2006, the FASB issued SFAS No. 157, "Fair Value Measurements," ("SFAS 157") which is, in part, effective for us beginning in fiscal year 2008. This statement defines fair value, establishes a framework for measuring fair value and expands the related disclosure requirements. The statement indicates, among other things, that a fair value measurement assumes that the transaction to sell an asset or transfer a liability occurs in the principal market for the asset or liability or, in the absence of a principal market, the most advantageous market for the asset or liability. Subsequent to the issuance of SFAS 157, the FASB issued FASB Staff Positions ("FSP") 157-1, "Application of FASB Statement No. 157 to FASB Statement No. 13 and Other Accounting Pronouncements That Address Fair Value Measurements for Purposes of Lease Classification or Measurement under Statement 13" and FSP 157-2 "Effective Date of FASB Statement No. 157." FSP 157-1 excludes, in certain circumstances, SFAS 13 and other accounting pronouncements that address fair value measurements for purposes of lease classification or measurement under Statement 13 from the provision of SFAS 157. FSP 157-2 delays the effective date of SFAS 157 for all nonfinancial assets and nonfinancial liabilities, except those that are recognized or disclosed at fair value in the financial statements on a recurring basis. For the instruments subject to the effective date delay under FSP 157-2, the effective date to adopt the fair value provisions for us will be the first quarter of 2009.

The table below summarizes our assets and liabilities that are measured at fair value on a recurring basis as of March 30, 2008. Such assets include certain derivative instruments and our indemnity obligations related primarily to our discontinued operations from Kaiser (see Note 5). In addition, we have provided a reconciliation of the beginning and ending balances for the fair value of these indemnity obligations using significant unobservable inputs (Level 3—see definition below) in Note 11 "CONTINGENCIES—Kaiser and Other Indemnity Obligations." SFAS 157 establishes a hierarchy that prioritizes fair value measurements based on the types of inputs used for the various valuation techniques (market approach, income approach and cost approach). We utilize a combination of market and income approaches to value derivative instruments, and use an income approach for valuing our indemnity obligations. Our financial assets and liabilities are measured using inputs from the three levels of the fair value hierarchy. The three levels of the hierarchy are as follows:

Level 1—Inputs are unadjusted quoted prices in active markets for identical assets or liabilities that we have the ability to access at the measurement date.

Level 2—Inputs include quoted prices for similar assets and liabilities in active markets, quoted prices for identical or similar assets or liabilities in markets that are not active, inputs other than quoted prices that are observable for the asset or liability (i.e., interest rates, yield curves, etc.), and inputs that are derived principally from or corroborated by observable market data by correlation or other means (market corroborated inputs).

8

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES (Continued)

Level 3—Unobservable inputs that reflect our assumptions about the assumptions that market participants would use in pricing the asset or liability. We develop these inputs based on the best information available, including our own data.

The following presents our assets and liabilities that are measured at fair value based on a recurring basis:

| |

|

Fair Vaue Measurements at March 30, 2008 Using |

||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Total carrying value at March 30, 2008 |

Quoted prices in active markets (Level 1) |

Significant Other Observable Inputs (Level 2) |

Significant Unobservable Inputs (Level 3) |

||||||||||

| |

(In millions) |

|||||||||||||

| Derivatives assets | $ | 38.6 | $ | — | $ | 38.6 | $ | — | ||||||

| Derivatives liabilities | (427.7 | ) | — | (427.7 | ) | — | ||||||||

| Guarantees—indemnity obligations | (168.2 | ) | — | — | (168.2 | ) | ||||||||

| Total | $ | (557.3 | ) | $ | — | $ | (389.1 | ) | $ | (168.2 | ) | |||

In accordance with FSP 157-2, we will adopt in 2009 the fair value provisions of those financial assets and liabilities that are measured at fair value on a nonrecurring basis including goodwill, intangibles, and debt. Based on our evaluation of this statement, we do not believe the adoption of FSP 157-2, will have a significant impact on the determination or reporting of our financial results.

Following is a list of asset and liabilities that are recognized or disclosed at fair value for which, we will not apply the provisions of SFAS 157 until 2009:

- •

- Reporting

units, including Canada, U.S. and U.K., measured at fair value in the first step of our annual goodwill impairment testing,

- •

- Indefinite-lived

intangible assets measured at fair value in our annual impairment testing,

- •

- Other

long-lived assets held for sale and carried at fair value less costs to sell,

- •

- Asset

retirement obligations, and

- •

- Liabilities associated with restructuring or other exit activities.

SFAS No. 159 "The Fair Value Option for Financial Assets and Financial Liabilities. Including an amendment of FASB Statement No. 115"

In February 2007, the FASB issued Statement No. 159 ("SFAS 159") which permits entities an option to choose to measure many financial instruments and certain other items at fair value that are not currently required to be measured at fair value. The objective of this Statement is to reduce both complexity in accounting for financial instruments and the volatility in earnings caused by measuring related assets and liabilities using different measurement techniques. The fair value measurement provisions are elective and can be applied to individual financial instruments. SFAS 159 requires additional disclosures related to the fair value measurements included in the entity's financial statements. This Statement is effective for us as of the beginning of our 2008 fiscal year. We do not intend to adopt the fair value measurement provisions of SFAS 159.

9

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES (Continued)

New Accounting Pronouncements

SFAS No. 141R "Business Combinations"

In December 2007, the FASB issued SFAS No. 141 (revised 2007), "Business Combinations" ("SFAS 141R"), which replaces SFAS No. 141, "Business Combinations." Under the provisions of SFAS 141R, acquisition costs will generally be expensed as incurred; noncontrolling interests will be valued at fair value at the acquisition date; in-process research and development will be recorded at fair value as an indefinite-lived intangible asset at the acquisition date; restructuring costs associated with a business combination will generally be expensed subsequent to the acquisition date; and changes in deferred tax asset valuation allowances and income tax uncertainties after the acquisition date generally will affect income tax expense. SFAS 141R will be effective, on a prospective basis, for all business combinations for which the acquisition date is after the beginning of our fiscal year 2009, with the exception of the accounting for valuation allowances on deferred taxes and acquired tax contingencies for which the adoption is retrospective. We are currently evaluating the effects, if any, that SFAS 141R may have on our financial statements.

SFAS No. 160 "Noncontrolling interests in Consolidated Financial Statements"

In December 2007, the FASB issued Financial Accounting Standards No. 160, "Noncontrolling Interests in Consolidated Financial Statements—an amendment of ARB No. 51" ("SFAS 160") and is effective for us beginning in fiscal year 2009. This Statement requires the recognition of a noncontrolling interest, or minority interest, as equity in the consolidated financial statements and separate from the parent's equity. The amount of net income attributable to the noncontrolling interest will be included in consolidated net income on the face of the income statement. It also amends certain of ARB No. 51's consolidation procedures for consistency with the requirements of SFAS 141R, including procedures associated with the deconsolidation of a subsidiary. This statement also includes expanded disclosure requirements regarding the interests of the parent and its noncontrolling interest. We are currently evaluating this new statement and anticipate that while the adoption of SFAS 160 will require the reclassification of our reported minority interests to stockholders' equity, the statement will not have a significant impact on the reporting of our results of operations.

SFAS No. 161 "Disclosures about Derivative Instruments and Hedging Activities. Including an amendment of FASB Statement No. 133 "

In March 2008, the FASB issued SFAS No. 161, "Disclosures about Derivative Instruments and Hedging Activities—an amendment of FASB Statement No. 133," (SFAS "161") as amended and interpreted, which requires enhanced disclosures about an entity's derivative and hedging activities and thereby improves the transparency of financial reporting. Disclosing the fair values of derivative instruments and their gains and losses in a tabular format provides a more complete picture of the location in an entity's financial statements of both the derivative positions existing at period end and the effect of using derivatives during the reporting period. Entities are required to provide enhanced disclosures about (a) how and why an entity uses derivative instruments, (b) how derivative instruments and related hedged items are accounted for under Statement 133 and its related interpretations, and (c) how derivative instruments and related hedged items affect an entity's financial position, financial performance, and cash flows. SFAS No. 161 is effective for financial statements issued for fiscal years

10

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

1. BASIS OF PRESENTATION AND SIGNIFICANT ACCOUNTING POLICIES (Continued)

and interim periods beginning after November 15, 2008. Early adoption is permitted. The Company does not expect SFAS 161 to have a material impact on its financial statements.

Proposed Accounting Pronouncements

Proposed FASB Staff Position APB 14-a, "Accounting for Convertible Debt Instruments That May Be Settled in Cash Upon Conversion (Including Partial Cash Settlement)"

In August 2001, the FASB proposed FASB Staff Position APB 14-a, "Accounting for Convertible Debt Instruments That May Be Settled in Cash Upon Conversion (Including Partial Cash Settlement)" ("FSP APB 14-a"). The proposed FSP APB 14-a specifies that issuers of such instruments should separately account for the liability and equity components in a manner that will reflect the entity's nonconvertible debt borrowing rate on the instrument's issuance date when interest cost is recognized in subsequent periods. Our 2007 2.5% Convertible Senior Notes due July 30, 2013, are within the scope of the proposed FSP APB 14-a; therefore if FSP APB 14-a is issued as proposed, we would be required to record the debt portions of our 2.5% Convertible Senior Notes at their fair value on the date of issuance and amortize the discount into interest expense over the life of the debt. However, there would be no effect on our cash interest payments. If the FSP APB 14-a is issued as proposed, we expect the increase in non-cash interest expense recognized on our consolidated financial statements to be significant. As currently proposed, FSP APB 14-a will be effective for financial statements issued for fiscal years beginning after December 15, 2008, and would be applied retrospectively to all periods presented. FSP APB 14-a is expected to be issued as final by the FASB in May 2008.

2. BUSINESS SEGMENTS

During the first quarter of 2008, MCBC adjusted its operating and reporting structure to reflect a re-alignment of responsibility associated with certain developing beer markets. A summary of our revised operating segments is provided below:

Reportable segments

Canada

The Canada segment was not impacted by this reorganization and remains as described in our previously issued financial statements.

Effective January 1, 2008, Molson and Grupo Modelo, S.A.B. de C.V. established a joint venture Molson Modelo Imports ("MMI"), to import, distribute, and market the Modelo beer brand portfolio across all Canadian provinces and territories. Under the new arrangement, Molson's sales team will be responsible for selling the brands across Canada on behalf of the joint venture. The new alliance will enable Grupo Modelo to effectively tap into the resources and capabilities of Molson to achieve greater distribution coverage in the Western provinces of Canada. The MMI joint venture will be accounted for under the equity method.

United States ("U.S.")

Our beer business associated with Mexico, the Caribbean (other than Puerto Rico), and military sales outside the U.S. have had responsibility transferred from this operating segment to our new

11

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

2. BUSINESS SEGMENTS (Continued)

non-reportable segment called Global Brands and Market Development ("Global Markets"), discussed below. In addition, the results of Coors Global Properties which includes certain intellectual property, trademarks and brands, was re-aligned and is now included in the U.S. segment.

On October 9, 2007, MCBC and SABMiller plc (the investing companies) announced that they signed a letter of intent to combine the U.S. and Puerto Rico operations of their respective subsidiaries, Coors Brewing Company and Miller Brewing Company, in a joint venture ("MillerCoors"). The parties signed a definitive joint venture agreement on December 20, 2007 and expect the transaction to close in mid-2008.

Each party will contribute its business and related operating assets and certain liabilities into an operating joint venture company. The percentage interests in the profits of the joint venture will be 58% for SABMiller plc and 42% for MCBC. Voting interests will be shared 50%-50%, and each investing company will have equal board representation within the joint venture company. Each party to the joint venture has agreed not to transfer its economic or voting interests in the joint venture for a period of five years, and certain rights of first refusal will apply to any subsequent assignment of such interests.

The results and financial position of our U.S. segment will, in all material respects, be de-consolidated upon contribution to the joint venture, and our interest in the new combined operations will be accounted for by us under the equity method of accounting.

The proposed joint venture transaction has been submitted for antitrust review and clearance by the U.S. Department of Justice under the Hart-Scott-Rodino Act of 1976, as amended, and to certain other applicable governmental authorities.

United Kingdom ("U.K")

Our beer business in Asia markets and exports from the U.K. to continental Europe have had responsibility transferred to our non-reportable segment called Global Markets and Corporate, discussed below. As a result the segment previously carried as "Europe" has been renamed the U.K. segment. The segment includes the results of operations in the U.K. and our royalty arrangements in the Republic of Ireland.

Non-reportable segment and other business activities

Global Markets and Corporate

These results represent our unallocated corporate general and administrative costs, net interest costs associated with financing activities, and results of operations associated with certain global markets, including Mexico, the Caribbean (other than Puerto Rico), Asia and exports to continental Europe.

No single customer accounted for more than 10% of our sales. Net sales represent sales to third party external customers. Inter-segment revenues are insignificant and eliminated in consolidation. Prior period amounts have been reclassified to conform to the current operating segment structure described above.

12

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

2. BUSINESS SEGMENTS (Continued)

The following table sets forth net sales by segment:

| |

Thirteen Weeks Ended |

||||||

|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

|||||

| |

(In millions) |

||||||

| Canada(1) | $ | 383.6 | $ | 337.8 | |||

| U.S.(1) | 650.0 | 585.4 | |||||

| U.K.(1) | 310.5 | 291.7 | |||||

| Global Markets and Corporate(2) | 12.5 | 13.7 | |||||

| Consolidated | $ | 1,356.6 | $ | 1,228.6 | |||

- (1)

- Reportable

segment

- (2)

- Operating segment and other business activities that are not reportable

The following table sets forth income (loss) from continuing operations before income taxes and minority interests by segment:

| |

Thirteen Weeks Ended |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||||||

| |

(In millions) |

|||||||

| Canada(1) | $ | 62.7 | $ | 41.2 | ||||

| U.S.(1) | 69.9 | 45.5 | ||||||

| U.K.(1) | (4.1 | ) | (6.8 | ) | ||||

| Global Markets and Corporate(2) | (82.5 | ) | (51.6 | ) | ||||

| Consolidated | $ | 46.0 | $ | 28.3 | ||||

- (1)

- Reportable

segment

- (2)

- Operating segment and other business activities that are not reportable

The following table sets forth total assets by segment:

| |

As of |

||||||

|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

December 30, 2007 |

|||||

| |

(In millions) |

||||||

| Canada(1)(2) | $ | 6,977.1 | $ | 7,378.6 | |||

| U.S.(2) | 2,990.5 | 2,830.6 | |||||

| U.K.(2) | 2,723.1 | 2,867.3 | |||||

| Global Markets and Corporate(3) | 95.4 | 364.5 | |||||

| Discontinued operations | 10.3 | 10.6 | |||||

| Total assets | $ | 12,796.4 | $ | 13,451.6 | |||

- (1)

- The decrease is primarily due to foreign currency translation.

13

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

2. BUSINESS SEGMENTS (Continued)

- (2)

- Reportable

segment

- (3)

- Operating segment and other business activities that are not reportable

3. SHARE-BASED PAYMENTS

During the first quarters of 2008 and 2007, we issued the following awards related to Class B common shares to certain directors, officers, and other eligible employees, pursuant to the Molson Coors Brewing Company Incentive Compensation Plan ("MCIP"): restricted stock units ("RSU"), deferred stock units ("DSU"), performance share units ("PSU"), stock options, stock-only stock appreciation rights ("SOSAR"), and limited stock appreciation rights ("LOSAR").

PSU awards are earned over the estimated expected term to achieve projected financial targets, which were established on March 16, 2006 at the time of the initial grant. As of March 30, 2008, these financial targets were achieved for all PSU awards outstanding. As a result of achieving these financial targets we recognized the remaining $34.4 million expense before taxes in the first quarter of 2008 associated with the outstanding PSU awards. PSUs are granted at the market value of our stock on the date of the grant.

The following table summarizes components of the recorded equity-based compensation expense:

| |

Thirteen Weeks Ended |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||||||

| |

(In millions) |

|||||||

| Stock options, SOSARs and LOSARs | ||||||||

| Pre-tax compensation expense | $ | 1.6 | $ | 0.8 | ||||

| Tax (benefit) | (0.4 | ) | (0.2 | ) | ||||

| After-tax compensation expense | $ | 1.2 | $ | 0.6 | ||||

RSUs and DSUs |

||||||||

| Pre-tax compensation expense | $ | 2.6 | $ | 1.6 | ||||

| Tax (benefit) | (0.8 | ) | (0.5 | ) | ||||

| After-tax compensation expense | $ | 1.8 | $ | 1.1 | ||||

PSUs |

||||||||

| Pre-tax compensation expense | $ | 34.4 | $ | 4.3 | ||||

| Tax (benefit) | (10.0 | ) | (1.3 | ) | ||||

| After-tax compensation expense | $ | 24.4 | $ | 3.0 | ||||

Total after-tax compensation expense |

$ |

27.4 |

$ |

4.7 |

||||

4. SPECIAL ITEMS, NET

We have incurred charges or gains that are not indicative of our normal, recurring operations. As such, we have separately classified these costs as special operating items.

14

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

4. SPECIAL ITEMS, NET (Continued)

Summary of Special Items

The table below summarizes special items recorded in the first quarters of 2008 and 2007, by program:

| |

Thirteen Weeks Ended |

||||||

|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

|||||

| |

(In millions) |

||||||

| Canada—Restructuring and related costs associated with the Edmonton brewery closure | $ | 1.4 | $ | 4.1 | |||

| U.S.—Costs associated with the proposed MillerCoors joint venture | 16.2 | — | |||||

| U.S.—(Gain) on sale of distribution center | (24.2 | ) | — | ||||

| U.K.—Restructuring charge | 1.6 | 4.1 | |||||

| U.K.—Other, including certain exit costs | 0.5 | — | |||||

| Global Markets and Corporate—Costs associated with proposed MillerCoors joint venture | 5.5 | — | |||||

| Global Markets and Corporate—Transitional costs associated with outsourcing agreement | 6.3 | — | |||||

| Total special items | $ | 7.3 | $ | 8.2 | |||

Canada Segment

During the first quarter of 2008, the Canada segment recognized a charge of $1.4 million related to costs associated with the Edmonton brewery, which was closed in the third quarter of 2007. In the first quarter of 2007, the Canada segment began a restructuring program focused on labor savings across production and sales, general and administrative functions, and also targeted a reduction of overhead expenses. We recognized $4.1 million for severance and other related costs in the first quarter of 2007.

The following summarizes the activity in the Canada segment restructuring accruals:

| |

Severance and other employee-related costs |

||||

|---|---|---|---|---|---|

| |

(In millions) |

||||

| Balance at December 30, 2007 | $ | 4.2 | |||

| Charges incurred | — | ||||

| Payments made | (2.0 | ) | |||

| Foreign currency and other adjustments | (0.2 | ) | |||

| Balance at March 30, 2008 | $ | 2.0 | |||

U.S. Segment

The U.S. segment recognized on a net basis, a gain of $8.0 million associated with special items during the first quarter of 2008. During the first quarter of 2008 we sold our Boise, Idaho beer

15

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

4. SPECIAL ITEMS, NET (Continued)

distributorship, for $25.2 million resulting in a gain of $24.2 million. This gain was partially offset by $16.2 million of costs associated with the MillerCoors joint venture which primarily consists of employee retention costs. The retention accruals have not been included in the restructuring accruals table, presented below, as the activities do not represent restructuring or exit activities. The U.S. segment recognized no special items during the first quarter of 2007.

The following summarizes the activity in the U.S. segment restructuring accruals:

| |

Severance and other employee-related costs |

||||

|---|---|---|---|---|---|

| |

(In millions) |

||||

| Balance at December 30, 2007 | $ | 2.6 | |||

| Charges incurred | — | ||||

| Payments made | (2.5 | ) | |||

| Other adjustments | (0.1 | ) | |||

| Balance at March 30, 2008 | $ | — | |||

U.K. Segment

The U.K. segment recognized $2.1 million and $4.1 million of net special charges in the first quarters of 2008 and 2007, respectively. The 2008 and 2007 net charges were predominantly employee termination costs associated with supply chain and back-office restructuring efforts in the U.K. As of March 30, 2008, we had 348 employees whose employment was terminated under this restructuring plan since the inception of the programs in 2006.

The following summarizes the activity in the U.K. segment restructuring accruals:

| |

Severance and other employee-related costs |

||||

|---|---|---|---|---|---|

| |

(In millions) |

||||

| Balance at December 30, 2007 | $ | 2.5 | |||

| Charges incurred | 1.7 | ||||

| Payments made | (1.8 | ) | |||

| Foreign currency and other adjustments | — | ||||

| Balance at March 30, 2008 | $ | 2.4 | |||

Global Markets and Corporate

During the first quarter of 2008, Global Markets and Corporate recognized a $5.5 million charge associated with the proposed MillerCoors joint venture, consisting primarily of outside professional services. Additionally, in January 2008, we signed a contract with a third party service provider to outsource a significant portion of our general and administrative back office functions in all of our operating segments and in our corporate office. This outsourcing initiative is a key component of our Resources for Growth cost reduction program. During the quarter we incurred $6.3 million of external transition costs associated with this outsourcing initiative. We expect to incur additional costs

16

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

4. SPECIAL ITEMS, NET (Continued)

throughout the remainder of 2008. The Global Markets and Corporate segment recognized no special items in the first quarter of 2007.

5. DISCONTINUED OPERATIONS

In 2006, we sold our equity interest in the entity that comprised our previously-reported Brazil operating segment, Cervejarias Kaiser Brasil S.A. ("Kaiser") to FEMSA Cerveza S.A. de C.V. ("FEMSA"). As discussed in Note 11, we indemnified FEMSA with respect to certain tax and other liabilities. We have reflected the results of operations, financial position, and cash flows for the former Brazil segment in our financial statements as discontinued operations.

The loss from discontinued operations of $9.0 million and $14.8 million in the first quarters of 2008 and in 2007, respectively, were associated with changes in estimates of the carrying value of the indemnity related liabilities, foreign exchange gains and losses and accretion expense related to indemnities we provided to FEMSA with regard to contingent tax and other liabilities, which are discussed further in Note 11.

6. INCOME TAXES

Our effective tax rate for the first quarter of 2008 was approximately negative 12%, resulting in an income tax benefit. We anticipate that our full year effective tax rate will be in the range of 10% to 15%. Our first quarter effective tax rate is lower than our anticipated full year rate primarily due to reductions in unrecognized tax benefits.

Our tax rate is volatile and may fluctuate with changes in, among other things, the amount and source of income or loss, our ability to utilize foreign tax credits, changes in tax laws, and the movement of liabilities established pursuant to FIN 48 for uncertain tax positions as statutes of limitations expire or positions are otherwise effectively settled. We note that there are pending tax law changes in the U.S., U.K. and Canada that, if enacted, may impact our effective tax rate. The formation of the proposed MillerCoors joint venture could also impact our effective tax rate.

As of December 31, 2007 we had $286.2 million of unrecognized tax benefits. Since December 31, 2007, unrecognized tax benefits decreased by $13.2 million. This reduction is net of increases due to additional unrecognized tax benefits and interest accrued for the current year and decreases primarily due to fluctuation in foreign exchange rates, certain tax years closing or being effectively settled, and payments made to tax authorities with regard to unrecognized tax benefits during the first quarter of 2008. The net effect of such changes resulted in total unrecognized tax benefits of $273.0 million as of March 30, 2008.

We file income tax returns in most of the federal, state, and provincial jurisdictions in the U.S., U.K., Canada and the Netherlands. Tax years through 2004 are closed or have been effectively settled through examination in the U.S. The Internal Revenue Service has commenced examination of the 2005 and 2006 tax years and we expect the examination to conclude in late 2008. In addition, we have entered into the Compliance Assurance Process program whereby the Internal Revenue Service will be examining certain 2007 transactions in the current year. Tax years through 2003 are closed or have been effectively settled through examination in Canada. We are currently under examination for tax year 2004 in Canada and expect the examination to close during 2008. Tax years through 2001 are closed or

17

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

6. INCOME TAXES (Continued)

have been effectively settled through examination in the U.K. We are currently under examination for tax years 2002 through 2004 in the U.K. and expect the examinations to conclude during 2008. Tax years through 2006 are closed or have been effectively settled through examination in the Netherlands.

7. EARNINGS PER SHARE (EPS)

Basic net income per common share was computed using the weighted average number of shares of common stock outstanding during the period. All share and per share amounts for prior periods were adjusted to reflect the two for one stock split issued in the form of a dividend effective October 3, 2007. Diluted net income per share includes the additional dilutive effect of our potentially dilutive securities, which include certain stock options, LOSARs, SOSARs, RSUs, PSUs and DSUs, calculated using the treasury stock method. Diluted net income per share could also be impacted by our convertible debt and related warrants outstanding if they were in the money.

The following summarizes the effect of dilutive securities on diluted EPS:

| |

Thirteen Weeks Ended |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||||||

| |

(In millions, except per share amounts) |

|||||||

| Income from continuing operations | $ | 46.1 | $ | 19.2 | ||||

| Loss from discontinued operations, net of tax | (9.0 | ) | (14.8 | ) | ||||

| Net income | $ | 37.1 | $ | 4.4 | ||||

Weighted average shares for basic EPS |

181.0 |

176.1 |

||||||

| Effect of dilutive securities: | ||||||||

| Stock options, LOSARs and SOSARs | 2.0 | 2.0 | ||||||

| RSUs, PSUs and DSUs | 1.5 | 0.1 | ||||||

| Weighted average shares for diluted EPS | 184.5 | 178.2 | ||||||

Basic income (loss) per share: |

||||||||

| From continuing operations | $ | 0.25 | $ | 0.11 | ||||

| From discontinued operations | (0.05 | ) | (0.08 | ) | ||||

| Basic net income per share | $ | 0.20 | $ | 0.03 | ||||

Diluted income (loss) per share: |

||||||||

| From continuing operations | $ | 0.25 | $ | 0.11 | ||||

| From discontinued operations | (0.05 | ) | (0.08 | ) | ||||

| Diluted net income per share | $ | 0.20 | $ | 0.03 | ||||

Dividends per share |

$ |

0.16 |

$ |

0.16 |

||||

18

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

7. EARNINGS PER SHARE (EPS) (Continued)

The following anti-dilutive securities were excluded from the computation of the effect of dilutive securities on earnings per share for the following periods:

| |

Thirteen Weeks Ended |

|||

|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||

| |

(In millions, except per share amounts) |

|||

| Stock options, SOSARs and RSUs(1) | 0.2 | 0.2 | ||

| PSUs—2.1 million outstanding at April 1, 2007(2) | — | 2.1 | ||

| Shares issuable upon assumed conversion of the 2.5% Convertible Senior Notes to issue Class B common shares, 10.5 million at March 30, 2008(3) | 10.5 | — | ||

| Warrants to issue Class B common shares, 10.5 million at March 30, 2008(3) | 10.5 | — | ||

| 21.2 | 2.3 | |||

- (1)

- Exercise

prices exceed the average market price of the common shares or are anti-dilutive due to the impact of the unrecognized compensation cost on the

calculation of assumed proceeds in the application of the treasury stock method.

- (2)

- All

necessary conditions required to be satisfied were not met during 2007.

- (3)

- We issued $575 million of senior convertible notes in June 2007. The impact of a net share settlement of the conversion amount at maturity will begin to dilute earnings per share when our stock price reaches $54.76. The impact of stock that could be issued to settle share obligations we could have under the warrants we issued simultaneously with the convertible notes issuance will begin to dilute earning per share when our stock price reaches $70.09. The potential receipt of MCBC stock from counterparties under our purchased call options when and if our stock price is between $54.76 and $70.09 would be anti-dilutive and excluded from any calculations of earnings per share.

8. GOODWILL AND OTHER INTANGIBLES

The following summarizes the change in goodwill for the thirteen weeks ended March 30, 2008 (in millions):

| Balance at December 30, 2007 | $ | 3,346.5 | |||

| Deferred tax purchase accounting adjustments | (0.1 | ) | |||

| Foreign currency translation | (88.5 | ) | |||

| Balance at March 30, 2008 | $ | 3,257.9 | |||

19

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

8. GOODWILL AND OTHER INTANGIBLES (Continued)

The following summarizes goodwill allocated between our reportable segments as follows:

| |

As of |

||||||

|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

December 30, 2007 |

|||||

| |

(In millions) |

||||||

| Canada | $ | 979.2 | $ | 1,066.5 | |||

| United States | 1,346.8 | 1,347.0 | |||||

| United Kingdom | 931.9 | 933.0 | |||||

| Consolidated | $ | 3,257.9 | $ | 3,346.5 | |||

The following table presents details of our intangible assets, other than goodwill, as of March 30, 2008:

| |

Useful life |

Gross |

Accumulated amortization |

Net |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(Years) |

(In millions) |

||||||||||

| Intangible assets subject to amortization: | ||||||||||||

| Brands | 3 - 35 | $ | 312.7 | $ | (124.2 | ) | $ | 188.5 | ||||

| Distribution rights | 2 - 23 | 350.4 | (164.5 | ) | 185.9 | |||||||

| Patents and technology and distribution channels | 3 - 10 | 35.3 | (21.5 | ) | 13.8 | |||||||

| Other | 5 - 34 | 11.7 | (5.4 | ) | 6.3 | |||||||

| Intangible assets not subject to amortization: | ||||||||||||

| Brands | Indefinite | 3,433.9 | — | 3,433.9 | ||||||||

| Distribution networks | Indefinite | 989.2 | — | 989.2 | ||||||||

| Other | Indefinite | 28.9 | — | 28.9 | ||||||||

| Total | $ | 5,162.1 | $ | (315.6 | ) | $ | 4,846.5 | |||||

The following table presents details of our intangible assets, other than goodwill, as of December 30, 2007:

| |

Useful life |

Gross |

Accumulated amortization |

Net |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

(Years) |

(In millions) |

||||||||||

| Intangible assets subject to amortization: | ||||||||||||

| Brands | 3 - 35 | $ | 320.3 | $ | (121.2 | ) | $ | 199.1 | ||||

| Distribution rights | 2 - 23 | 363.4 | (164.9 | ) | 198.5 | |||||||

| Patents and technology and distribution channels | 3 - 10 | 35.4 | (20.7 | ) | 14.7 | |||||||

| Other | 5 - 34 | 11.7 | (5.3 | ) | 6.4 | |||||||

| Intangible assets not subject to amortization: | ||||||||||||

| Brands | Indefinite | 3,561.1 | — | 3,561.1 | ||||||||

| Distribution networks | Indefinite | 1,030.5 | — | 1,030.5 | ||||||||

| Other | Indefinite | 29.1 | — | 29.1 | ||||||||

| Total | $ | 5,351.5 | $ | (312.1 | ) | $ | 5,039.4 | |||||

20

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

8. GOODWILL AND OTHER INTANGIBLES (Continued)

The incremental change in the gross carrying amounts of intangibles from December 30, 2007 to March 30, 2008, is primarily due to the impact of foreign exchange rates, as a significant amount of intangibles are denominated in foreign currencies.

Based on foreign exchange rates as of March 30, 2008, the estimated future amortization expense of finite-lived intangible assets is as follows for the next five years:

| |

Amount |

||

|---|---|---|---|

| |

(In millions) |

||

| 2008—remaining | $ | 34.1 | |

| 2009 | $ | 45.5 | |

| 2010 | $ | 45.3 | |

| 2011 | $ | 41.8 | |

| 2012 | $ | 31.3 | |

Amortization expense of intangible assets was $11.5 million and $14.9 million for the thirteen weeks ended March 30, 2008 and April 1, 2007, respectively.

9. DEBT AND OTHER CREDIT ARRANGMENTS

On February 7, 2008, we announced a tender for repurchase of any and all principal amount of our remaining 6.375% $225 million Senior Notes due 2012, with the tender period running through February 14, 2008. The amount actually repurchased was $180.4 million. The net costs of $12.4 million related to this extinguishment of debt and termination of related interest rate swaps was recorded in the first quarter of 2008. The net debt extinguishment costs comprised a $21.4 million payment to settle the notes at fair value given interest rates at the time of extinguishment, a $1.7 million write-off of the proportionate amount of unamortized discount, issuance fees and transaction costs, offset by a $10.7 million gain from the termination of the interest rate swap associated with the extinguished debt. The debt extinguishment was funded by existing cash resources.

10. EMPLOYEE RETIREMENT AND POST-EMPLOYMENT PLANS

We offer defined benefit retirement plans in Canada, the United States and the United Kingdom that cover substantially all of our employees. Additionally, we offer other postretirement benefits to the

21

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

10. EMPLOYEE RETIREMENT AND POST-EMPLOYMENT PLANS (Continued)

majority of our Canadian and U.S. employees. The net periodic pension costs under retirement plans and other postretirement benefits were as follows:

| |

Thirteen Weeks Ended March 30, 2008 |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Canada plans |

U.S. plans |

U.K. plan |

Consolidated |

||||||||||

| |

(In millions) |

|||||||||||||

| Defined Benefit Plans | ||||||||||||||

| Service cost | $ | 8.4 | $ | 4.2 | $ | 7.0 | $ | 19.6 | ||||||

| Interest cost | 24.6 | 14.9 | 33.9 | 73.4 | ||||||||||

| Expected return on plan assets | (31.3 | ) | (17.5 | ) | (39.8 | ) | (88.6 | ) | ||||||

| Administrative Expenses | 0.6 | 0.3 | 1.3 | 2.2 | ||||||||||

| Amortization of prior service cost (benefit) | 0.3 | (0.1 | ) | (0.5 | ) | (0.3 | ) | |||||||

| Amortization of net actuarial loss | — | 2.0 | 0.3 | 2.3 | ||||||||||

| Less expected participant contributions | (0.7 | ) | — | (1.2 | ) | (1.9 | ) | |||||||

| Net periodic pension cost | $ | 1.9 | $ | 3.8 | $ | 1.0 | $ | 6.7 | ||||||

| Other Postretirement Benefits | ||||||||||||||

| Service cost—benefits earned during the period | $ | 2.5 | $ | 0.6 | $ | — | $ | 3.1 | ||||||

| Interest cost on projected benefit obligation | 4.1 | 2.4 | — | 6.5 | ||||||||||

| Amortization of prior service cost | — | 0.1 | — | 0.1 | ||||||||||

| Amortization of net actuarial loss | 0.1 | 1.0 | — | 1.1 | ||||||||||

| Net periodic postretirement benefit cost | $ | 6.7 | $ | 4.1 | $ | — | $ | 10.8 | ||||||

| |

Thirteen Weeks Ended April 1, 2007 |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Canada plans |

U.S. plans |

U.K. plan |

Consolidated |

||||||||||

| |

(In millions) |

|||||||||||||

| Defined Benefit Plans | ||||||||||||||

| Service cost | $ | 7.8 | $ | 4.3 | $ | 9.9 | $ | 22.0 | ||||||

| Interest cost | 20.3 | 14.3 | 28.0 | 62.6 | ||||||||||

| Expected return on plan assets | (25.5 | ) | (17.5 | ) | (39.6 | ) | (82.6 | ) | ||||||

| Amortization of prior service cost (benefit) | 0.4 | — | (1.6 | ) | (1.2 | ) | ||||||||

| Amortization of net actuarial loss | — | 3.5 | 1.3 | 4.8 | ||||||||||

| Less expected participant contributions | (0.9 | ) | — | (2.6 | ) | (3.5 | ) | |||||||

| Net periodic pension cost (benefit) | $ | 2.1 | $ | 4.6 | $ | (4.6 | ) | $ | 2.1 | |||||

| Other Postretirement Benefits | ||||||||||||||

| Service cost—benefits earned during the period | $ | 2.1 | $ | 0.7 | $ | — | $ | 2.8 | ||||||

| Interest cost on projected benefit obligation | 3.3 | 2.0 | — | 5.3 | ||||||||||

| Amortization of prior service cost | — | 0.1 | — | 0.1 | ||||||||||

| Amortization of net actuarial loss | 0.3 | 0.8 | — | 1.1 | ||||||||||

| Net periodic postretirement benefit cost | $ | 5.7 | $ | 3.6 | $ | — | $ | 9.3 | ||||||

During the first quarter of 2008, employer contributions paid to the defined benefit plans were $24.9 million, $.3 million, and $6.4 million for Canada, U.S. and U.K. plans, respectively. Expected

22

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

10. EMPLOYEE RETIREMENT AND POST-EMPLOYMENT PLANS (Continued)

total fiscal year 2008 employer contributions to Canada, U.S. and U.K. defined benefits plans are approximately $158.6 million.

11. CONTINGENCIES

Kaiser and Other Indemnity Obligations

Kaiser

As discussed in Note 5, we sold our entire equity interest in Kaiser during 2006 to FEMSA. The terms of the sale agreement require us to indemnify FEMSA for certain exposures related to tax, civil and labor contingencies arising prior to FEMSA's purchase of Kaiser. First, we provided a full indemnity for any losses Kaiser may incur with respect to tax claims associated with certain previously utilized purchased tax credits. The maximum potential claims amount in this regard, including estimated accumulated legal, penalties and interest, was $396 million as of March 30, 2008. Our estimate of the fair value of the indemnity liability associated with the purchased tax credits recorded as of March 30, 2008 was $118.6 million, $4.9 million of which was classified as a current liability and $113.7 million of which was classified as non-current. Our fair value estimates consider a number of scenarios for the ultimate resolution of these issues, the probabilities of which are influenced not only by legal developments in Brazil but also by management's intentions with regard to various alternatives that could present themselves leading to the ultimate resolution of these issues. Our indemnity obligations related to previously purchased tax credits increased by $1.8 million during the first quarter of 2008. The liabilities are also impacted by changes in estimates regarding amounts that could be paid, the timing of such payments and adjustments to the probabilities assigned to various scenarios.

We also provided indemnity related to all other tax, civil and labor contingencies existing as of the date of sale. In this regard, however, FEMSA assumed their full share of all of these contingent liabilities that had been previously recorded and disclosed by us prior to the sale on January 13, 2006. However, we may have to provide indemnity to FEMSA if those contingencies settle at amounts greater than those amounts previously recorded or disclosed by us. We will be able to offset any indemnity exposures in these circumstances with amounts that settle favorably to amounts previously recorded. Our exposure related to these indemnity claims is capped at the amount of the sales price of our 68% equity interest of Kaiser, which was $68 million. As a result of these contract provisions, our fair value estimates include not only probability-weighted potential cash outflows associated with indemnity provisions, but also probability-weighted cash inflows that could result from favorable settlements, which could occur through negotiation or settlement programs that could arise from the federal or any of the various state governments in Brazil. The recorded fair value of the total tax, civil and labor indemnity liability was $39.0 million as of March 30, 2008, $26.0 million of which is classified as a current liability and $13.0 million of which is classified as non-current.

Future settlement procedures and related negotiation activities associated with these contingencies are largely outside of our control and will be handled by FEMSA. Indemnity obligations related to purchased tax credits must be settled upon notification of FEMSA's settlement. Due to the uncertainty involved with the ultimate outcome and timing of these contingencies, significant adjustments to the carrying values of the indemnity obligations have resulted in the past and could result in the future. These liabilities are denominated in Brazilian reals and have been stated at present value and will,

23

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

11. CONTINGENCIES (Continued)

therefore, be subject in the future to foreign exchange gains or losses and to accretion cost, both of which will be recognized in the discontinued operations section of the statement of operations.

Other

Molson Canada owns a 19.9% common ownership interest in the Montréal Canadiens professional hockey club (the "Club") and as well as Board representation at the Club and related entities. The shareholders of the Club (the majority owner and Molson Canada) and the National Hockey League ("NHL") are parties to a consent agreement, which requires the purchaser and Molson to abide by funding requirements included in the terms of the shareholders' agreement. In addition, Molson Canada continues to be a guarantor of the majority owner's obligations under a land lease. We have evaluated our risk exposure related to these financial guarantees and recorded the fair values of these indemnities accordingly.

The table below provides a summary of indemnity obligations measured at fair value using significant unobservable inputs (see Note 1) from December 30, 2007, through March 30, 2008:

| |

Indemnity Obligations |

|||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Kaiser purchased tax credits indemnity reserve |

Kaiser tax, civil and labor indemnity reserve |

Indemnities associated with Montréal Canadiens |

Total indemnity reserves |

||||||||||

| |

(In millions) |

|||||||||||||

| Balance at December 30, 2007 | $ | 116.8 | $ | 38.2 | $ | 11.0 | $ | 166.0 | ||||||

| Gains included in earnings(1) | (0.6 | ) | (0.1 | ) | — | (0.7 | ) | |||||||

| Foreign exchange transaction loss included in earnings(1) | 7.3 | 2.4 | — | 9.7 | ||||||||||

| Foreign exchange translation gain included in other comprehensive income | (4.9 | ) | (1.5 | ) | (0.4 | ) | (6.8 | ) | ||||||

| Balance at March 30, 2008 | $ | 118.6 | $ | 39.0 | $ | 10.6 | $ | 168.2 | ||||||

- (1)

- All losses included in earnings are unrealized and were associated with amounts that were carried on the balance sheet at the beginning and the end of the quarter.

Current liabilities associated with discontinued operations also include current tax liabilities of $10.2 million. Included in current and non-current assets associated with discontinued operations on the balance sheet are $5.7 million and $4.6 million, respectively, of deferred tax assets associated with the indemnity liabilities.

Litigation and Other Disputes

Beginning in May 2005, several purported shareholder class actions were filed in the United States and Canada, including federal courts in Delaware and Colorado and provincial courts in Ontario and Quebec, alleging, among other things, that the Company and its affiliated entities, including Molson Inc., and certain officers and directors misled stockholders in connection with the Merger. The Colorado case has since been transferred to Delaware and consolidated with those cases. The Quebec

24

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

11. CONTINGENCIES (Continued)

Superior Court heard arguments in October 2007 regarding the plaintiffs' motion to authorize a class in that case. We opposed the motion.

During the first quarter of 2008, the Company agreed in principle with counsel for plaintiffs in all pending securities cases in Delaware, Quebec, and Ontario to settle all such claims on a worldwide basis. Pursuant to the settlement, the Company would pay $6 million in settlement, which amounts would be paid by the Company's insurance carrier. The Company anticipates that the agreement in principle will be formalized shortly in a definitive agreement. That agreement will be subject to approval in the various courts in which the cases are pending. This agreement in principle does not settle one remaining case in Delaware. That case seeks to recover on behalf of certain Molson Coors employees who invested in Company securities around the same time through two employee retirement savings plans. The complaint in that case essentially relies on the same allegations as the other shareholder lawsuits. We have asked the court to dismiss that lawsuit.

We are involved in other disputes and legal actions arising in the ordinary course of our business. While it is not feasible to predict or determine the outcome of these proceedings, in our opinion, based on a review with legal counsel, none of these disputes and legal actions is expected to have a material impact on our consolidated financial position, results of operations or cash flows. However, litigation is subject to inherent uncertainties, and an adverse result in these or other matters, for example, including the above-described advertising practices case, may arise from time to time that may harm our business.

Environmental

When we determine that it is probable that a liability for environmental matters or other legal actions exists and the amount of the loss is reasonably estimable, an estimate of the future costs are recorded as a liability in the financial statements. Costs that extend the life, increase the capacity or improve the safety or efficiency of Company-owned assets or are incurred to mitigate or prevent future environmental contamination may be capitalized. Other environmental costs are expensed when incurred.

From time to time, we have been notified that we are or may be a potentially responsible party (PRP) under the Comprehensive Environmental Response, Compensation and Liability Act or similar state laws for the cleanup of other sites where hazardous substances have allegedly been released into the environment. We cannot predict with certainty the total costs of cleanup, our share of the total cost, the extent to which contributions will be available from other parties, the amount of time necessary to complete the cleanups or insurance coverage.

We are one of a number of entities named by the Environmental Protection Agency (EPA) as a PRP at the Lowry Superfund site. This landfill is owned by the City and County of Denver (Denver) and is managed by Waste Management of Colorado, Inc. (Waste Management). In 1990, we recorded a pretax charge of $30 million, a portion of which was put into a trust in 1993 as part of a settlement with Denver and Waste Management regarding the then-outstanding litigation. Our settlement was based on an assumed remediation cost of $120 million (in 1992 adjusted dollars). We are obligated to pay a portion of future costs, if any, in excess of that amount.

Waste Management provides us with updated annual cost estimates through 2032. We reviewed these cost estimates in the assessment of our accrual related to this issue. We use certain assumptions

25

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

11. CONTINGENCIES (Continued)

that differ from Waste Management's estimates to assess our expected liability. Our expected liability (based on the $120 million threshold being met) is based on our best estimates available.

The assumptions used are as follows:

- •

- trust

management costs are included in projections with regard to the $120 million threshold, but are expensed only as incurred;

- •

- income

taxes, which we believe are not an included cost, are excluded from projections with regard to the $120 million threshold;

- •

- a

2.5% inflation rate for future costs; and

- •

- certain operations and maintenance costs were discounted using a 4.70% risk-free rate of return.

Based on these assumptions, the present value and gross amount of the costs at March 30, 2008, are approximately $2.3 million and $3.8 million, respectively. Accordingly, we believe that the existing liability is adequate as of March 30, 2008. We did not assume any future recoveries from insurance companies in the estimate of our liability, and none are expected.

Considering the estimates extend through the year 2032 and the related uncertainties at the site, including what additional remedial actions may be required by the EPA, new technologies and what costs are included in the determination of when the $120 million threshold is reached the estimate of our liability may change as further facts develop. We cannot predict the amount of any such change, but additional accruals in the future are possible.

We are aware of groundwater contamination at some of our properties in Colorado resulting from historical, ongoing or nearby activities. There may also be other contamination of which we are currently unaware.

In October 2006 we were notified by the EPA that we are a PRP, along with approximately 60 other parties, at the Cooper Drum site in southern California. Certain of Molson's former non-beer business operations, which were discontinued and sold in the mid-1990s prior to the Merger, were involved at this site. We responded to the EPA with information regarding our past involvement with the site. We are not yet able to estimate any potential liability associated with this site.

While we cannot predict the eventual aggregate cost for environmental and related matters in which we are currently involved, we believe that any payments, if required, for these matters would be made over a period of time in amounts that would not be material in any one year to our operating results, cash flows or our financial or competitive position. We believe adequate reserves have been provided for losses that are probable and estimable.

26

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE THIRTEEN WEEKS ENDED MARCH 30, 2008 (Continued)

12. OTHER COMPREHENSIVE (LOSS) INCOME

The following summarizes the components of other comprehensive (loss) income:

| |

Thirteen Weeks Ended |

|||||||

|---|---|---|---|---|---|---|---|---|

| |

March 30, 2008 |

April 1, 2007 |

||||||

| |

(In millions) |

|||||||

| Net income | $ | 37.1 | $ | 4.4 | ||||

| Other comprehensive (loss) income: | ||||||||

| Foreign currency translation adjustments, net of tax | (199.7 | ) | 55.2 | |||||

| Currency effect on pension liability | 2.5 | (1.0 | ) | |||||

| Amortization of net prior service costs and net actuarial losses, net of tax | 2.2 | 2.4 | ||||||

| Unrealized gain on derivative instruments, net of tax | 29.6 | 11.3 | ||||||

| Reclassification adjustment—derivative instruments, net of tax | 0.8 | (1.4 | ) | |||||

| Total other comprehensive (loss) income | (164.6 | ) | 66.5 | |||||

| Comprehensive (loss) income | $ | (127.5 | ) | $ | 70.9 | |||

13. SUPPLEMENTAL GUARANTOR INFORMATION

MCBC (Parent Guarantor and 2007 Issuer) issued $575.0 million of 2.5% Convertible Senior Notes due July 30, 2013 in a registered offering on June 15, 2007. The convertible notes are guaranteed on a senior unsecured basis by CBC (2002 Issuer), Molson Coors International, LP and Molson Coors Capital Finance ULC (together the 2005 Issuers) and certain significant subsidiaries (Subsidiary Guarantors).

On May 7, 2002, the 2002 Issuer completed a public offering of $850.0 million principal amount of 6.375% Senior notes due 2012. During the first quarter of 2008, $180.4 million of the Senior notes was extinguished by using existing cash resources (see Note 9). During the third quarter of 2007, $625.0 million of the Senior notes was extinguished by the proceeds received from the 2.5% Convertible Senior Notes issued June 15, 2007 and cash on hand. The remaining outstanding Senior notes are guaranteed on a senior and unsecured basis by the Parent Guarantor and 2007 Issuer, 2005 Issuers and Subsidiary Guarantors. The guarantees are full and unconditional and joint and several.

On September 22, 2005, the 2005 Issuers completed a public offering of $1.1 billion principal amount of Senior notes composed of USD $300 million 4.85% notes due 2010 and CAD $900.0 million 5.00% notes due 2015. The notes were issued with registration rights and are guaranteed on a senior and unsecured basis by Parent Guarantor and 2007 Issuer, 2002 Issuer and Subsidiary Guarantors. The guarantees are full and unconditional and joint and several. Funds necessary to meet the 2005 Issuers' debt service obligations are provided in large part by distributions or advances from MCBC's other subsidiaries, including Molson, a non-guarantor. Under certain circumstances, contractual and legal restrictions, as well as our financial condition and operating requirements, could limit the 2005 Issuers ability to obtain cash for the purpose of meeting its debt service obligation, including the payment of principal and interest on the notes.

27

MOLSON COORS BREWING COMPANY AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS