UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 29, 2007

Commission File Number 1-5480

Textron Inc.

(Exact name of registrant as specified in its charter)

|

Delaware |

|

05-0315468 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

40 Westminster Street, Providence, RI |

|

02903 |

|

(Address of principal executive offices) |

|

(zipcode) |

Registrant’s Telephone Number, Including Area Code: (401) 421-2800

Securities registered pursuant to Section 12(b) of the Act:

|

Title of Each Class |

|

Name of Each Exchange on Which Registered |

|

Common Stock — par value $0.125 |

|

New York Stock Exchange |

|

|

|

Chicago Stock Exchange |

|

|

|

|

|

$2.08 Cumulative Convertible Preferred Stock, |

|

New York Stock Exchange |

|

Series A — no par value |

|

|

|

|

|

|

|

$1.40 Convertible Preferred Dividend Stock, Series B |

|

New York Stock Exchange |

|

(preferred only as to dividends) — no par value |

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes x. No o.

Indicate by check mark if registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o. No x.

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x. No o.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

(Check one):

|

Large accelerated filer x |

Accelerated filer o |

|

Non-accelerated filer o |

Smaller reporting company o |

(Do not check if a smaller reporting company)

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o. No x.

The aggregate market value of the registrant’s Common Stock held by non-affiliates at June 30, 2007 was approximately $13,742,545,000 based on the New York Stock Exchange closing price for such shares on that date. The registrant has no non-voting common equity.

At February 9, 2008, 248,688,866 shares of Common Stock were outstanding.

Documents Incorporated by Reference

Part III of this Report incorporates information from certain portions of the registrant’s Proxy Statement for its Annual Meeting of Shareholders to be held on April 23, 2008.

PART I

Item 1. Business

Textron Inc. is a multi-industry company that leverages its global network of aircraft, industrial and finance businesses to provide customers with innovative solutions and services around the world. We have approximately 44,000 employees in 34 countries. Textron Inc. was founded in 1923 and reincorporated in Delaware on July 31, 1967. Unless otherwise indicated, references to “Textron Inc.,” the “Company,” “we,” “our” and “us” in this Annual Report on Form 10-K refer to Textron Inc. and its consolidated subsidiaries.

We operate our business through four operating segments. Three of our operating segments represent our manufacturing businesses: Bell, Cessna and Industrial. Our fourth segment consists of our Finance business. A description of the business of each of our segments is set forth below. Our business segments include operations that are unincorporated divisions of Textron Inc. and others that are separately incorporated subsidiaries. Financial information by business segment and geographic area appears in Note 20 to the Consolidated Financial Statements on pages 73 through 75 of this Annual Report on Form 10-K. The following description of our business should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on pages 15 through 32 of this Annual Report on Form 10-K. Information included in this Annual Report on Form 10-K refers to our continuing businesses unless otherwise indicated.

Bell Segment

The Bell segment is comprised of Bell Helicopter and Textron Systems.

Bell Helicopter is one of the leading suppliers of helicopters, tiltrotor aircraft, and helicopter-related spare parts and services in the world. Bell Helicopter manufactures for both military and commercial applications. Revenues for Bell Helicopter accounted for approximately 19%, 20% and 21% of our total revenues in 2007, 2006 and 2005, respectively.

Bell Helicopter supplies advanced military helicopters and support to the U.S. Government and to military customers outside the U.S. Bell Helicopter is one of the leading suppliers of helicopters to the U.S. Government and, in association with The Boeing Company, the only supplier of military tiltrotor aircraft. Bell Helicopter’s three major U.S. Government programs are for the V-22 tiltrotor aircraft, the H-1 helicopters and the Armed Reconnaissance Helicopter (“ARH”).

Bell Helicopter is teamed with The Boeing Company to develop, produce and support the V-22 Osprey tiltrotor aircraft for the U.S. Department of Defense. Tiltrotor aircraft are designed to provide the benefits of both helicopters and fixed-wing aircraft. The U.S. Government has issued contracts for 113 production V-22 aircraft through production Lot 11, of which 78 have been delivered as of the end of 2007. The U.S. Government’s program of record for the V-22 calls for a total of 458 production units.

The U.S. Marine Corps H-1 helicopter program includes an advanced attack model and a utility model, the AH-1Z and UH-1Y, respectively, both of which were designed to have 84% parts commonality between them. Through Low Rate Initial Production (“LRIP”) contracts, the U.S. Government has contracted for the production of 26 UH-1Y aircraft and eight AH-1Z aircraft, of which 10 were delivered by the end of 2007. Phase II of the H-1 Operational Evaluation (“OPEVAL”) is scheduled to commence in the first half of 2008; successful completion of OPEVAL is required prior to our receiving authorization for full-rate production. The U.S. Government’s program of record for the H-1 program calls for a total of 280 production units.

Bell Helicopter currently is working under a U.S. Government System Development and Demonstration contract for development of the ARH. During 2007, after uncertainty about whether the U.S. Government would continue with the ARH program, the U.S. Army agreed to restructure the program. Bell continues to work with the U.S. Army to finalize details of the restructure and anticipates that initial LRIP contract awards will be granted in mid-2008. The U.S. Government’s program of record for the ARH currently calls for a total of 368 production units; however, based upon communications from the U.S. Army, we expect that the U.S. Government will increase production requirements to 512 units during 2008.

Bell Helicopter also is a leading supplier of commercially certified helicopters and support to corporate, offshore petroleum exploration and development, utility, charter, police, fire, rescue and emergency medical helicopter operators. Bell Helicopter produces a variety of commercial aircraft types, including light single and twin engine helicopters and medium twin engine helicopters, along with other related products. The

1

commercial helicopters currently offered by Bell include the 206, 407 and 412; in addition, the 429 is expected to be certified in the 2008-2009 time-frame.

Bell Helicopter’s Customer Support and Service division provides post-sale service and support to its customers for its installed base of approximately 13,000 helicopters and tiltrotors through a network of five Bell-owned service centers, over 130 independent service centers and seven parts distribution centers that are located throughout the world. Collectively, these service centers offer logistics support, including parts, support equipment, technical data, training devices, pilot and maintenance training, component repairs, engine repair and overhaul, aircraft modifications, post-sale customizing, accessory manufacturing, contractor maintenance, field service and product support engineering.

Bell Helicopter competes against a number of competitors based in the U.S. and other countries for its helicopter business, and its parts and support business competes against numerous competitors around the world. Competition is based primarily on price, product quality and reliability, product support, contract performance and reputation.

Textron Systems is a primary supplier to the defense, aerospace and general aviation markets, providing approximately 10%, 9% and 8% of Textron’s revenues in 2007, 2006 and 2005, respectively. Textron Systems’ principal strategy is to address the U.S. Department of Defense’s emphasis on network centric warfare by leveraging advances in information technology in the development and production of networked sensors, weapons and the associated algorithms and software. Textron Systems manufactures precision weapons, airborne and ground-based surveillance systems, sophisticated intelligence and situational awareness software, armored vehicles and turrets, reciprocating piston aircraft engines, and aircraft and missile control actuators, valves and related components. While Textron Systems sells most of its products to U.S. customers, it also sells certain products to customers outside the U.S. through sales representatives and distributors located in various global locations. Textron Systems includes HR Textron, Lycoming Engines, Overwatch Geospatial Operations, Overwatch Tactical Operations, Textron Defense Systems, Textron Marine & Land Systems, and AAI Corporation.

Textron Systems has produced approximately 900 armored security vehicles (“ASV”) for the U.S. Army since inception of the current U.S. Army contract in June 2005. This contract calls for more than 750 additional units through May 2009. The ASVs currently are deployed in locations around the globe, particularly in Iraq and Afghanistan, serving various missions, including convoy escorts, patrolling, checkpoints, forward operating base patrol, urban operations, reconnaissance and surveillance patrols, and tactical overwatch for civilian and military police operations.

Textron Systems is a tier-one supplier of unattended ground sensors and intelligent munitions systems for the U.S. Army’s Future Combat System. Textron Systems also is the U.S. Air Force’s prime contractor for the Sensor Fuzed Weapon and a subcontractor to The Boeing Company for tail actuation systems on the Joint Direct Attack Munition and the next generation Small Diameter Bomb.

In November 2007, we acquired United Industrial Corporation, which operates through its wholly owned subsidiary, AAI Corporation (“AAI”). AAI is a leading provider of intelligent aerospace and defense systems, including: tactical unmanned aircraft systems (“UAS”), training and simulation systems, automated aircraft test and maintenance equipment, armament systems, aviation ground support equipment, countersniper detection systems, and logistical, engineering and supply chain services. AAI adds important capabilities to our existing aerospace and defense businesses and advances our strategy to deliver broader and more integrated solutions to our customers. As a part of Textron Systems, AAI remains the prime system integrator for the U.S. Army’s premier tactical UAS, the Shadow®, which includes the One System® Ground Control Station — the U.S. Army’s standard for interoperability of manned and unmanned airborne assets.

Textron Systems competes against a number of competitors in the U.S. and other countries on the basis of technology, contract performance, price, product quality and reliability, product support and reputation.

Cessna Segment

Based on unit sales, Cessna Aircraft Company is the world’s largest manufacturer of general aviation aircraft. Cessna currently has four major product lines: Citation business jets, Caravan single engine turboprops, Cessna single engine piston aircraft, and aftermarket services. Revenues in the Cessna segment accounted for approximately 38%, 36% and 35% of our total revenues in 2007, 2006 and 2005, respectively.

The family of business jets currently produced by Cessna includes the Mustang, Citation CJ1+, Citation CJ2+, Citation CJ3, Citation CJ4, Citation Encore+, Citation XLS+, Citation Sovereign and Citation X. The Citation X is the world’s fastest business jet with a maximum operating speed of Mach 0.92. First customer deliveries of the Citation XLS+ and Citation CJ4 are scheduled to commence in late 2008 and 2010, respectively.

2

The Cessna Caravan is the world’s best selling utility turboprop. Caravans are offered in four models: the Grand Caravan, the Super Cargomaster, the Caravan 675 and the Caravan Amphibian. Caravans are used in the U.S. primarily for overnight express package shipments and for personal transportation. International uses of Caravans include humanitarian flights, tourism and freight transport.

Cessna offers 10 models in its single engine piston product line, which include the four-place Skyhawk, Skyhawk SP, Skyhawk TD, Skylane, Turbo Skylane, Cessna 350, Cessna 400, six-place Stationair, Turbo Stationair, and the recently announced two-place Light Sport Aircraft, the Model 162 SkyCatcher. First customer deliveries of the SkyCatcher are scheduled to commence in late 2009. In December 2007, Cessna purchased certain assets of Columbia Aircraft Manufacturing Corporation, a producer of high-performance single engine aircraft, including two low-wing, composite four-place aircraft, which now are branded as the Cessna 350 and Cessna 400. Cessna also recently announced its plan to develop the Citation Columbus, a wide-body, eight-passenger business jet designed for intercontinental travel. Cessna is targeting Federal Aviation Administration certification by the end of 2013, with deliveries beginning in 2014.

The Citation family of aircraft currently is supported by 10 Citation Service Centers owned or operated by Cessna, along with authorized independent service stations and centers located in more than 18 countries throughout the world. The Wichita Citation Service Center is the world’s largest general aviation maintenance facility. Cessna-owned Service Centers provide customers with 24-hour service and maintenance. Cessna also provides around-the-clock parts support for Citation aircraft. Cessna Caravan and single engine piston customers receive product support through independently owned service stations and around-the-clock parts support through Cessna.

Cessna markets its products worldwide primarily through its own sales force, as well as through a network of authorized independent sales representatives, depending upon the product line. Cessna has several competitors in various market segments. Cessna’s aircraft compete with other aircraft that vary in size, speed, range, capacity, handling characteristics and price. Cessna operates a business jet fractional ownership business through a joint venture called CitationShares. Cessna’s current ownership interest in CitationShares is 88%. This business offers shares of Citation aircraft for operation throughout the contiguous U.S. and in Canada, Mexico, Central America, the Caribbean and Bermuda. CitationShares also has a limited advance purchase jet aircraft charter product called the Vector Jetcard.

Industrial Segment

The Industrial segment includes our Kautex, Fluid & Power, Greenlee, E-Z-GO and Jacobsen businesses.

Kautex, headquartered in Bonn, Germany, is a leading global designer and manufacturer of blow-molded fuel systems and other blow-molded parts for automobile original equipment manufacturers and, to a lesser extent, other industrial customers. Revenues of Kautex accounted for approximately 13%, 13% and 15% of our total revenues in 2007, 2006 and 2005, respectively. Kautex operates plants near its major customers all around the world. Kautex also is a leading supplier of windshield and headlamp washer systems in the original equipment automobile market. In North America, Kautex produces metal fuel fillers and engine camshafts for the automotive market. In Europe, Kautex produces bottles and plastic containers for food, household, laboratory and industrial uses. Kautex also manufactures blow-molded fuel systems for the all-terrain vehicle and watercraft markets and tanks for selective catalytic reduction systems used to reduce emissions from diesel engines. In 2007, Kautex announced that it has received the first production order for fuel systems using its new next generation fuel system manufacturing process, which is designed to reduce emissions from fuel systems and lower manufacturing costs. Kautex has a number of competitors worldwide, some of whom are owned by the automotive original equipment manufacturers that comprise Kautex’s targeted customer base. Competition typically is based on a number of factors, including price, product quality and reliability, prior experience and available manufacturing capacity.

Fluid & Power designs and manufactures four product lines: Gear Technologies, Industrial Pumps, Polymer Systems and Hydraulics. Gear Technologies includes industrial gears, mechanical transmission systems, worm gear speed reducers, screwjacks, gear motors and gear sets under the David Brown, Benzlers, Cone Drive and Radicon brand names, primarily for the defense, industrial and mining industries. Industrial Pumps includes centrifugal and reciprocating pumps for the oil, gas, petrochemical, nuclear and desalinization industries under the Union brands. Polymer Systems includes industrial pumps, extrusion equipment and screen changers for the polymer industry under the Maag brand name. Hydraulics includes hydraulic pumps, valves, pilot controls and power takeoffs under the David Brown, Hydreco and Powauto brands. These products are sold to a variety of customers, including original equipment manufacturers, engineering contractors, governments, distributors and end users. Fluid & Power faces competition from other manufacturers based primarily on price, product quality and reliability, and product support.

3

Greenlee designs and manufactures powered equipment, electrical test and measurement instruments, hand and hydraulic powered tools, and electrical and fiber optic connectors under the Greenlee, Fairmont, Klauke, Progressive and Tempo brand names. The products principally are used in the electrical construction and maintenance, telecommunications and plumbing industries. Greenlee distributes its products through a global network of sales representatives and distributors and sells its products directly to home improvement retailers and original equipment manufacturers. Through a joint venture, Greenlee also sells hand and powered tools for the plumbing and mechanical industries in North America. In December 2007, Greenlee acquired Paladin Tools, a provider of tools and accessories for the telecommunications, data communications and wiring industries. The Greenlee businesses face competition from numerous manufacturers based primarily on price and product quality and reliability.

E-Z-GO designs and manufactures golf cars and off-road utility vehicles powered by electric and internal combustion engines under the E-Z-GO name, as well as multipurpose utility vehicles under the E-Z-GO and Cushman brand names. In the fourth quarter of 2007, E-Z-GO introduced its new energy-efficient RXV golf car, which it expects will provide reduced energy and maintenance costs for its customers. E-Z-GO’s commercial customers consist primarily of golf courses, resort communities and municipalities, as well as commercial and industrial users such as airports and factories. E-Z-GO’s golf cars and off-road utility vehicles also are sold in the consumer market. Sales are made through a network of distributors and directly to end users. E-Z-GO has two major competitors for golf cars and several other competitors for off-road utility vehicles. Competition is based primarily on price, product quality and reliability, product support and reputation.

Jacobsen designs and manufactures professional turf-maintenance equipment and specialized turf-care vehicles. Major brand names include Ransomes, Jacobsen and Cushman. Jacobsen’s commercial customers consist primarily of golf courses, resort communities, sporting venues and municipalities. Sales are made through a network of distributors and dealers. Jacobsen has two major competitors for professional turf-maintenance equipment and several other competitors for specialized turf care. Competition is based primarily on price, product quality and reliability, and product support.

Finance Segment

Our Finance segment consists of Textron Financial Corporation, a diversified commercial finance company with core operations in six markets:

|

· |

Asset-Based Lending provides revolving credit facilities secured by receivable and inventory, related equipment and real estate term loans, and factoring programs across a broad range of manufacturing and service industries; |

|

|

|

|

· |

Aviation Finance provides financing for new and used Cessna business jets, single engine turboprops, piston-engine airplanes, Bell helicopters and other general aviation aircraft; |

|

|

|

|

· |

Distribution Finance primarily offers inventory finance programs for dealers of products manufactured by Textron and for dealers of a variety of other household, housing, leisure, agricultural and technology products; |

|

|

|

|

· |

Golf Finance primarily makes mortgage loans for the acquisition and refinancing of golf courses and provides term financing for E-Z-GO golf cars and Jacobsen turf-care equipment; |

|

|

|

|

· |

Resort Finance primarily extends loans to developers of vacation interval resorts, secured principally by notes receivable and interval inventory; and |

|

|

|

|

· |

Structured Capital primarily engages in long-term leases of large-ticket equipment and real estate, primarily with investment grade lessees. |

Textron Financial Corporation’s financing activities are confined almost exclusively to secured lending and leasing to commercial markets. Textron Financial Corporation’s services are offered primarily in North America. However, Textron Financial Corporation finances certain Textron products worldwide, principally Bell helicopters and Cessna aircraft. Textron Financial Corporation also finances many of the sales at E-Z-GO and Jacobsen.

In 2007, 2006 and 2005, our Finance segment paid our manufacturing segments $1.2 billion, $1.0 billion and $0.8 billion, respectively, related to the sale of Textron-manufactured products that it financed. Our Cessna and Industrial segments also received proceeds in those years of $27 million, $63 million and $41 million, respectively, from the sale of equipment from their manufacturing operations to Textron Financial Corporation for use under operating lease agreements.

4

The commercial finance environment in which Textron Financial Corporation operates is highly fragmented and extremely competitive. Textron Financial Corporation is subject to competition from various types of financing institutions, including banks, leasing companies, insurance companies, commercial finance companies and finance operations of equipment vendors. Competition within the commercial finance industry is primarily focused on price, term, structure and service.

Textron Financial Corporation’s largest business risk is the collectibility of its finance receivable portfolio. See “Finance Portfolio Quality” in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” on page 23 for a detailed discussion of the credit quality of this portfolio.

Backlog

Our backlog at the end of 2007 and 2006 is summarized below:

|

|

|

December 29, |

|

December 30, |

|

||

|

(In millions) |

|

2007 |

|

2006 |

|

||

|

U.S. Government: |

|

|

|

|

|

||

|

Bell Helicopter |

|

$ |

2,805 |

|

$ |

2,363 |

|

|

Textron Systems |

|

2,092 |

|

1,152 |

|

||

|

Other |

|

1 |

|

7 |

|

||

|

Total U.S. Government Backlog |

|

4,898 |

|

3,522 |

|

||

|

Commercial: |

|

|

|

|

|

||

|

Bell Helicopter |

|

1,004 |

|

756 |

|

||

|

Cessna |

|

12,583 |

|

8,467 |

|

||

|

Other |

|

771 |

|

613 |

|

||

|

Total Commercial Backlog |

|

14,358 |

|

9,836 |

|

||

|

Total Backlog |

|

$ |

19,256 |

|

$ |

13,358 |

|

At December 29, 2007, approximately 97% of the U.S. Government backlog was funded. Unfunded backlog represents the award value of U.S. Government contracts received, generally related to cost-plus type contracts, in excess of the funding formally appropriated by the U.S. Government. The U.S. Government is obligated only up to the funded amount of the contract. Additional funding is appropriated as the contract progresses.

Cessna’s backlog includes approximately $2.0 billion in orders from a major fractional jet customer. Orders from this fractional aircraft operator are included in backlog when the customer enters into a definitive master agreement and has established preliminary delivery dates for the aircraft. Preliminary delivery dates are subject to change through amendment to the master agreement. Final delivery dates are established approximately 12 to 18 months prior to delivery. Orders from other commercial customers, which cover a wide spectrum of industries, are included in backlog upon the customer entering into a definitive purchase order and receipt of required deposits.

Approximately 56% of our total backlog at December 29, 2007 represents orders that are not expected to be filled in 2008, including $1.2 billion in orders for the new Citation CJ4 aircraft with first customer deliveries scheduled for 2010.

U.S. Government Contracts

In 2007, approximately 19% of our consolidated revenues were generated by or resulted from contracts with the U.S. Government. This business is subject to competition, changes in procurement policies and regulations, the continuing availability of funding which is dependent upon congressional appropriations, national and international priorities for defense spending, world events, and the size and timing of programs in which we may participate.

Our contracts with the U.S. Government generally may be terminated by the U.S. Government for convenience or if we default in whole or in part by failing to perform under the terms of the applicable contract. If the U.S. Government terminates a contract for convenience, we normally will be entitled to payment for the cost of contract work performed before the effective date of termination plus reasonable profit on such work, adjusted to reflect any rate of loss had the contract been completed, plus reasonable costs of settlement of the work terminated. If, however, the U.S. Government terminates a contract for default, generally: (a) we will be paid the contract price for completed supplies delivered and accepted, an agreed-upon amount for manufacturing materials delivered and accepted and for the protection and preservation of property, and for partially completed products accepted by the U.S. Government; (b) the U.S. Government will not be liable for our costs with respect to unaccepted items

5

and will be entitled to repayment of advance payments and progress payments related to the terminated portions of the contract; and (c) we may be liable for excess costs incurred by the U.S. Government in procuring undelivered items from another source.

Research and Development

Information regarding our research and development expenditures is contained in Note 16 to the Consolidated Financial Statements on page 70 of this Annual Report on Form 10-K.

Patents and Trademarks

We own, or are licensed under, numerous patents throughout the world relating to products, services and methods of manufacturing. Patents developed while under contract with the U.S. Government may be subject to use by the U.S. Government. We also own or license active trademark registrations and pending trademark applications in the U.S. and in various foreign countries or regions, as well as trade names and service marks. While our intellectual property rights in the aggregate are important to the operation of our business, we do not believe that any existing patent, license, trademark or other intellectual property right is of such importance that its loss or termination would have a material adverse effect on our business taken as a whole. Some of these trademarks, trade names and service marks are used in this Annual Report on Form 10-K and other reports, including: AAI; AB Benzlers; AH-1Z; APCO; BA609; Bell/Agusta Aerospace Company, LLC; Bell Helicopter; Benzlers; Bravo; Cadillac Gage; Caravan; Caravan 675; Caravan Amphibian; Cessna; Cessna 350; Cessna 400; Citation; Citation Encore+; CitationShares; Citation X; Citation XLS+; Citation Sovereign; CJ1; CJ1+; CJ2; CJ2+; CJ3; CJ4; Cone Drive; Cushman; David Brown; Eclipse; Excel; E-Z-GO; Fairmont; Fly Smart; Fly Bell; Gear Technologies; Global Technology Center; Grand Caravan; Greenlee; H-1; HR Textron; Huey II; Hydraulics; Hydreco; Jacobsen; Kautex; Kiowa Warrior; Klauke Progressive; Lycoming; Maag; McCauley; Modular Affordable Product Lines; Mustang; Next Generation Fuel System; Overwatch Systems; Paladin; PDCue; Polymer Systems; Powauto; Power Advantage; ProParts; Quick Draw Loan; Radicon; Ransomes; Rothenberger LLC; RXV; Sensor Fuzed Weapon; SHADOW; Sovereign; SkyBOOKS; SkyPLUS; SkyCatcher; Skyhawk; Skyhawk SP; Skyhawk TD; Skylane; ST 4X4; Stationair; Super Cargomaster; SuperCobra; SYMTX; TDCue; Tempo; Textron; Textron Business Services; Textron Business Systems; Textron Defense Systems; Textron Financial Corporation; Textron Fluid & Power; Textron Marine & Land Systems; Textron Six Sigma; Textron Systems; Turbo Skylane; Turbo Stationair; UAV SYSTEMS SPECIALIST; UH-1Y; Union Pump; US Helicopter; V-22 Osprey; Vector; Vector Jetcard; XLS; 429; 429 Global Ranger; and 429 Light Twin. These marks and their related trademark designs and logotypes (and variations of the foregoing) are trademarks, trade names or service marks of Textron Inc., its subsidiaries, affiliates or joint ventures.

Environmental Considerations

Our operations are subject to numerous laws and regulations designed to protect the environment. Compliance with these laws and expenditures for environmental control facilities has not had a material effect on our capital expenditures, earnings or competitive position. Additional information regarding environmental matters is contained in Note 15 to the Consolidated Financial Statements on pages 69 and 70 of this Annual Report on Form 10-K.

Employees

At December 29, 2007, we had approximately 44,000 employees.

Available Information

We make available free of charge on our Internet website (www.textron.com) our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission.

Forward-Looking Information

Certain statements in this Annual Report on Form 10-K and other oral and written statements made by us from time to time are forward-looking statements, including those that discuss strategies, goals, outlook or other non-historical matters, or project revenues, income, returns or other financial measures. These forward-looking statements speak only as of the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those contained in the statements, including the following: (a) changes in worldwide economic and political conditions that impact demand for our products, interest rates and foreign exchange rates; (b) the interruption of production at our facilities or our customers or suppliers; (c) performance issues with key suppliers, subcontractors and business partners; (d) our ability to perform as anticipated and to control costs under contracts with the U.S. Government; (e) the U.S. Government’s ability to unilaterally modify or terminate its contracts with us for the U.S. Government’s convenience or for our failure to perform, to change applicable procurement and accounting policies, and, under certain circumstances, to suspend or debar us as a contractor eligible to receive future contract awards; (f) changing priorities or reductions

6

in the U.S. Government defense budget, including those related to Operation Iraqi Freedom, Operation Enduring Freedom and the Global War on Terrorism; (g) changes in national or international funding priorities, U.S. and foreign military budget constraints and determinations, and government policies on the export and import of military and commercial products; (h) legislative or regulatory actions impacting defense operations; (i) the ability to control costs and successful implementation of various cost-reduction programs; (j) the timing of new product launches and certifications of new aircraft products; (k) the occurrence of slowdowns or downturns in customer markets in which our products are sold or supplied or where Textron Financial Corporation offers financing; (l) changes in aircraft delivery schedules or cancellation of orders; (m) the impact of changes in tax legislation; (n) the extent to which we are able to pass raw material price increases through to customers or offset such price increases by reducing other costs; (o) our ability to offset, through cost reductions, pricing pressure brought by original equipment manufacturer customers; (p) our ability to realize full value of receivables; (q) the availability and cost of insurance; (r) increases in pension expenses and other postretirement employee costs; (s) Textron Financial Corporation’s ability to maintain portfolio credit quality; (t) Textron Financial Corporation’s access to debt financing at competitive rates; (u) uncertainty in estimating contingent liabilities and establishing reserves to address such contingencies; (v) risks and uncertainties related to acquisitions and dispositions; (w) the efficacy of research and development investments to develop new products; (x) the launching of significant new products or programs which could result in unanticipated expenses; (y) bankruptcy or other financial problems at major suppliers or customers that could cause disruptions in our supply chain or difficulty in collecting amounts owed by such customers; and (z) difficulties or unanticipated expenses in connection with the consummation or integration of acquisitions, potential difficulties in employee retention following the acquisition and risks that the acquisition does not perform as planned or disrupts our current plans and operations or that anticipated synergies and opportunities will not be realized.

Item 1A. Risk Factors

Our business, financial condition and results of operations are subject to various risks, including those discussed below, which may affect the value of our securities. The risks discussed below are those that we believe currently are the most significant, although additional risks not presently known to us or that we currently deem less significant also may impact our business, financial condition or results of operations, perhaps materially.

We have customer concentration with the U.S. Government.

During 2007, we derived approximately 19% of our revenues from sales to a variety of U.S. Government entities. Our U.S. Government revenues have continued to grow both organically and through acquisitions, such as our recent acquisition of UIC. Our ability to compete successfully for and retain U.S. Government business is highly dependent on technical excellence, management proficiency, strategic alliances, cost-effective performance, and the ability to recruit and retain key personnel. Our revenues from the U.S. Government largely result from contracts awarded to us under various U.S. Government programs, primarily defense-related programs. The funding of these programs is subject to congressional appropriation decisions. Although multiple-year contracts may be planned in connection with major procurements, Congress generally appropriates funds on a fiscal year basis even though a program may continue for several years. Consequently, programs often are only partially funded initially, and additional funds are committed only as Congress makes further appropriations. The reduction or termination of funding, or changes in the timing of funding, for a U.S. Government program in which we provide products or services would result in a reduction or loss of anticipated future revenues attributable to that program, and could have a negative impact on our results of operations. While the overall level of U.S. defense spending has increased in recent years for numerous reasons, including increases in funding of operations in Iraq and Afghanistan and the U.S. Department of Defense’s military transformation initiatives, we can give no assurance that such spending will continue to grow or not be reduced. Significant changes in national and international priorities for defense spending could impact the funding, or the time of funding, of our programs, which could negatively impact our results of operations and financial condition.

U.S. Government contracts may be terminated at any time and may contain other unfavorable provisions.

The U.S. Government typically can terminate or modify any of its contracts with us either for its convenience or if we default by failing to perform under the terms of the applicable contract. A termination arising out of our default could expose us to liability and have an adverse effect on our ability to compete for future contracts and orders.

If any of our contracts are terminated by the U.S. Government, our backlog would be reduced, in accordance with contract terms, by the expected value of the remaining work under such contracts, and our financial condition and results of operations could be adversely affected. In addition,

7

on those contracts for which we are teamed with others and are not the prime contractor, the U.S. Government could terminate a prime contract under which we are a subcontractor, irrespective of the quality of our products and services as a subcontractor.

As a U.S. Government contractor, we are subject to a number of procurement rules and regulations.

We must comply with and are affected by laws and regulations relating to the formation, administration and performance of U.S. Government contracts. These laws and regulations, among other things, require certification and disclosure of all cost and pricing data in connection with contract negotiation, define allowable and unallowable costs and otherwise govern our right to reimbursement under certain cost-based U.S. Government contracts and restrict the use and dissemination of classified information and the exportation of certain products and technical data. Our U.S. Government contracts contain provisions that allow the U.S. Government to unilaterally suspend us from receiving new contracts pending resolution of alleged violations of procurement laws or regulations, reduce the value of existing contracts, issue modifications to a contract and control and potentially prohibit the export of our products, services and associated materials. A violation of specific laws and regulations could result in the imposition of fines and penalties or the termination of our contracts and, under certain circumstances, suspension or debarment from future contracts for a period of time. These laws and regulations affect how we do business with our customers and, in some instances, impose added costs on our business.

Cost overruns on U.S. Government contracts could subject us to losses or adversely affect our future business.

Contract and program accounting require judgment relative to assessing risks, estimating contract revenues and costs, and making assumptions for schedule and technical issues. Due to the size and nature of many of our contracts, the estimation of total revenues and cost at completion is complicated and subject to many variables. Assumptions have to be made regarding the length of time to complete the contract because costs include expected increases in wages and prices for materials. Incentives or penalties related to performance on contracts are considered in estimating sales and profit rates and are recorded when there is sufficient information for us to assess anticipated performance. Estimates of award fees also are used in estimating sales and profit rates based on actual and anticipated awards. Because of the significance of these estimates, it is likely that different amounts could be recorded if we used different assumptions or if the underlying circumstances were to change. Changes in underlying assumptions, circumstances or estimates may adversely affect our future financial results of operations.

Under fixed-price contracts, we receive a fixed price irrespective of the actual costs we incur, and, consequently, any costs in excess of the fixed price are absorbed by us. Under time and materials contracts, we are paid for labor at negotiated hourly billing rates and for certain expenses. Under cost reimbursement contracts, which are subject to a contract-ceiling amount, we are reimbursed for allowable costs and paid a fee, which may be fixed or performance based. However, if our costs exceed the contract ceiling or are not allowable under the provisions of the contract or applicable regulations, we may not be able to obtain reimbursement for all such costs. Under each type of contract, if we are unable to control costs we incur in performing under the contract, our financial condition and results of operations could be adversely affected. Cost overruns also may adversely affect our ability to sustain existing programs and obtain future contract awards.

Delays in aircraft delivery schedules or cancellation of orders may adversely affect our financial results.

Aircraft customers, including sellers of fractional share interests, may respond to weak economic conditions by delaying delivery of orders or canceling orders. Weakness in the economy may result in fewer hours flown on existing aircraft and, consequently, lower demand for spare parts and maintenance. Weak economic conditions also may cause reduced demand for used business jets or helicopters. We may accept used aircraft on trade-in that would be subject to fluctuations in the fair market value of the aircraft while in inventory. Reduced demand for new and used aircraft, spare parts and maintenance can have an adverse effect on our financial results of operations.

Developing new products and technologies entails significant risks and uncertainties.

Delays or cost overruns in the development and acceptance of new products, or certification of new aircraft products and other products, could affect our financial results of operations. These delays could be caused by unanticipated technological hurdles, production changes to meet customer demands, unanticipated difficulties in obtaining required regulatory certifications of new aircraft products, coordination with joint venture partners or failure on the part of our suppliers to deliver components as agreed. We also could be adversely affected if the general efficacy of our research and development investments to develop products is less than expected. Furthermore, because of the lengthy research and development cycle involved in bringing certain of our products to market, we cannot predict the economic conditions that will exist when any new product is complete. A reduction in capital spending in the aerospace or defense industries could have a significant effect on the demand for new products and technologies under development, which could have an adverse effect on our financial performance or results of operations.

8

We have entered, and expect to continue to enter, into joint venture, teaming and other arrangements, and these activities involve risks and uncertainties.

We have entered, and expect to continue to enter, into joint venture, teaming and other arrangements, and these activities involve risks and uncertainties, including the risk of the joint venture or related business partner failing to satisfy its obligations, which may result in certain liabilities to us for guarantees and other commitments, the challenges in achieving strategic objectives and expected benefits of the business arrangement, the risk of conflicts arising between us and our partners and the difficulty of managing and resolving such conflicts, and the difficulty of managing or otherwise monitoring such business arrangements.

We may make acquisitions and dispositions that increase the risks of our business.

We may enter into acquisitions or dispositions in the future in an effort to enhance shareholder value. Acquisitions or dispositions involve a certain amount of risks and uncertainties that could result in our not achieving expected benefits. With respect to acquisitions, such risks include difficulties in integrating newly acquired businesses and operations in an efficient and cost-effective manner; challenges in achieving expected strategic objectives, cost savings and other benefits; the risk that the acquired businesses’ markets do not evolve as anticipated and that the technologies acquired do not prove to be those needed to be successful in those markets; the risk that we pay a purchase price that exceeds what the future results of operations would have merited; and the potential loss of key employees of the acquired businesses. With respect to dispositions, the decision to dispose of a business or asset may result in a writedown of the related assets if the fair market value of the assets, less costs of disposal, is less than the book value. In addition, we may encounter difficulty in finding buyers or alternative exit strategies at acceptable prices and terms and in a timely manner. We may also underestimate the costs of retained liabilities or indemnification obligations. In addition, unanticipated delays or difficulties in effecting acquisitions or dispositions may divert the attention of our management and resources from our existing operations.

Our operations could be adversely affected by interruptions of production that are beyond our control.

Our business and financial results may be affected by certain events that we cannot anticipate or that are beyond our control, such as natural disasters and national emergencies that could curtail production at our facilities and cause delayed deliveries and canceled orders. In addition, we purchase components and raw materials and information technology and other services from numerous suppliers, and, even if our facilities are not directly affected by such events, we could be affected by interruptions at such suppliers. Such suppliers may be less likely than our own facilities to be able to quickly recover from such events and may be subject to additional risks such as financial problems that limit their ability to conduct their operations.

Our business could be adversely affected by strikes or work stoppages and other labor issues.

Approximately 14,000 of our employees, or 32% of our total employees, are unionized. As a result, we may experience work stoppages, which could negatively impact our ability to manufacture our products on a timely basis, resulting in strain on our relationships with our customers and a loss of revenues. In addition, the presence of unions may limit our flexibility in responding to competitive pressures in the marketplace, which could have an adverse effect on our financial results of operations.

In addition to our workforce, the workforces of many of our customers and suppliers are represented by labor unions. Work stoppages or strikes at the plants of our key customers could result in delayed or canceled orders for our products. Work stoppages and strikes at the plants of our key suppliers could disrupt our manufacturing processes. Any of these results could adversely affect our financial results of operations.

Our international business is subject to the risks of doing business in foreign countries.

Our international business exposes us to certain unique and potentially greater risks than our domestic business, and our exposure to such risks may increase if our international business continues to grow. Our international business is subject to local government regulations and procurement policies and practices, including regulations relating to import-export control, investments, exchange controls and repatriation of earnings or cash settlement challenges, as well as to varying currency, geopolitical and economic risks. We also are exposed to risks associated with using foreign representatives and consultants for international sales and operations and teaming with international subcontractors and suppliers in connection with international programs.

Our Finance borrowing group’s business is dependent on its continuing access to the capital markets.

Our financings are conducted through two borrowing groups: Finance and Manufacturing. Our Finance group consists of Textron Financial Corporation and its subsidiaries, which are the entities through which we operate in the Finance segment. Our Finance group relies on its access to the capital markets to fund asset growth, fund operations, and meet debt obligations and other commitments. This group raises funds through

9

commercial paper borrowings, issuances of medium-term notes and other term debt securities, and syndication and securitization of receivables. Additional liquidity is provided to our Finance group through bank lines of credit. Much of the capital markets funding is made possible by the maintenance of credit ratings that are acceptable to investors. If the credit ratings of our Finance group were to be lowered, it might face higher borrowing costs, a disruption of its access to the capital markets or both. Our Finance group also could lose access to financing for other reasons, such as a general disruption of the capital markets. Any disruption of our Finance group’s access to the capital markets could adversely affect its business and our profitability.

If our Finance group is unable to maintain portfolio credit quality, our financial performance could be adversely affected.

A key determinant of financial performance of our Finance group is its ability to maintain the quality of loans, leases and other credit products in its finance asset portfolios. Portfolio quality may adversely be affected by several factors, including finance receivable underwriting procedures, collateral quality, geographic or industry concentrations, or general economic downturns. Any inability by our Finance group to successfully collect its finance receivable portfolio and to resolve problem accounts may adversely affect our cash flow, profitability and financial condition.

We are subject to legal proceedings and other claims.

We are subject to legal proceedings and other claims arising out of the conduct of our business, including proceedings and claims relating to private transactions; government contracts; lack of compliance with applicable laws and regulations; production partners; product liability; employment; and environmental, safety and health matters. Under federal government procurement regulations, certain claims brought by the U.S. Government could result in our being suspended or debarred from U.S. Government contracting for a period of time. On the basis of information presently available, we do not believe that existing proceedings and claims will have a material effect on our financial position or results of operations. However, litigation is inherently unpredictable, and we could incur judgments or enter into settlements for current or future claims that could adversely affect our financial position or our results of operations in any particular period.

The levels of our reserves are subject to many uncertainties and may not be adequate to cover writedowns or losses.

In addition to reserves at our Finance group, we establish reserves in our Manufacturing group to cover uncollectible accounts receivable, excess or obsolete inventory, fair market value writedowns on used aircraft and golf cars, recall campaigns, warranty costs and litigation. These reserves are subject to adjustment from time to time depending on actual experience and are subject to many uncertainties, including bankruptcy or other financial problems at key customers.

In the case of litigation matters for which reserves have not been established because the loss is not deemed probable, it is reasonably possible such matters could be decided against us and could require us to pay damages or make other expenditures in amounts that are not presently estimable.

The effect on our financial results of many of these factors depends, in some cases, on our ability to obtain insurance covering potential losses at reasonable rates.

Currency, raw material price and interest rate fluctuations may adversely affect our results.

We are exposed to a variety of market risks, including the effects of changes in foreign currency exchange rates, raw material prices and interest rates. We monitor and manage these exposures as an integral part of our overall risk management program. In some cases, we purchase derivatives or enter into contracts to insulate our financial results of operations from these fluctuations. Nevertheless, changes in currency exchange rates, raw material prices and interest rates can have substantial adverse effects on our financial results of operations.

We may be unable to effectively mitigate pricing pressures.

In some markets, particularly where we deliver component products and services to original equipment manufacturers, we face ongoing customer demands for price reductions, which sometimes are contractually obligated. In some cases, we are able to offset these reductions through technological advances or by lowering our cost base through improved operating and supply chain efficiencies. However, if we are unable to effectively mitigate future pricing pressures, our financial results of operations could be adversely affected.

Failure to perform by our subcontractors or suppliers could adversely affect our performance.

We rely on other companies to provide raw materials, major components and subsystems for our products. Subcontractors also perform services that we provide to our customers in certain circumstances. We depend on these subcontractors and vendors to meet our contractual obligations to our customers. Our ability to meet our obligations to our customers may be adversely affected if suppliers do not provide the agreed-upon supplies or perform the agreed-upon services in compliance with customer requirements and in a timely and cost-effective manner. Such events

10

may adversely affect our financial results of operations or damage our reputation and relationships with our customers. The risk of these adverse effects may be greater in circumstances where we rely on only one or two subcontractors or suppliers for a particular product or service.

The increasing costs of certain employee and retiree benefits could adversely affect our results.

Our earnings and cash flow may be impacted by the amount of income or expense we expend or record for employee benefit plans. This is particularly true for our pension plans, which are dependent on actual plan asset returns and factors used to determine the value and current costs of plan benefit obligations.

In addition, medical costs are rising at a rate faster than the general inflation rate. Continued medical cost inflation in excess of the general inflation rate increases the risk that we will not be able to mitigate the rising costs of medical benefits. Increases to the costs of pension and medical benefits could have an adverse effect on our financial results of operations.

Unanticipated changes in our tax rates or exposure to additional income tax liabilities could affect our profitability.

We are subject to income taxes in both the U.S. and various foreign jurisdictions, and our domestic and international tax liabilities are subject to the allocation of income among these different jurisdictions. Our effective tax rates could be adversely affected by changes in the mix of earnings in countries with differing statutory tax rates, changes in the valuation of deferred tax assets and liabilities or changes in tax laws, which could affect our profitability. In particular, the carrying value of deferred tax assets is dependent on our ability to generate future taxable income. In addition, the amount of income taxes we pay is subject to audits in various jurisdictions, and a material assessment by a tax authority could affect our profitability.

Item 1B. Unresolved Staff Comments

None

Item 2. Properties

On December 29, 2007, we operated a total of 77 plants located throughout the U.S. and 56 plants outside the U.S. We own 68 plants and lease the remainder for a total manufacturing space of approximately 22.2 million square feet.

We also own or lease offices, warehouse and other space at various locations. We consider the productive capacity of the plants operated by each of our business segments to be adequate. In general, our facilities are in good condition, are considered to be adequate for the uses to which they are being put and are substantially in regular use.

Item 3. Legal Proceedings

We are subject to actual and threatened legal proceedings and other claims arising out of the conduct of our business. These proceedings include claims relating to private transactions, government contracts, lack of compliance with applicable laws and regulations, production partners, product liability, employment, and environmental, safety and health matters. Some of these legal proceedings seek damages, fines or penalties in substantial amounts or remediation of environmental contamination. Under federal government procurement regulations, certain claims brought by the U.S. Government could result in our suspension or debarment from U.S. Government contracting for a period of time. On the basis of information presently available, we do not believe that existing proceedings and claims will have a material effect on our financial position or results of operations.

Item 4. Submission of Matters to a Vote of Security Holders

No matters were submitted to a vote of our security holders during the last quarter of the period covered by this Annual Report on Form 10-K.

11

Executive Officers of the Registrant

The following table sets forth certain information concerning our executive officers as of February 20, 2008. All of our executive officers are members of our Management Committee and Transformation Leadership Team.

|

Name |

|

Age |

|

Current Position with Textron Inc. |

|

Lewis B. Campbell |

|

61 |

|

Chairman, President and Chief Executive Officer; Director |

|

Kenneth C. Bohlen |

|

55 |

|

Executive Vice President and Chief Innovation Officer |

|

John D. Butler |

|

60 |

|

Executive Vice President Administration and Chief Human Resources Officer |

|

Ted R. French |

|

53 |

|

Executive Vice President and Chief Financial Officer |

|

Mary L. Howell |

|

55 |

|

Executive Vice President Government Affairs, Strategy and Business Development, International, Communications and Investor Relations |

|

Terrence O’Donnell |

|

63 |

|

Executive Vice President and General Counsel |

Mr. Campbell joined Textron in September 1992 as Executive Vice President and Chief Operating Officer. He was named Chief Executive Officer in July 1998 and was appointed Chairman of our Board of Directors in February 1999. Mr. Campbell served as President and Chief Operating Officer from January 1994 to July 1998 and reassumed the position of President in September 2001. Mr. Campbell has been a Director of Textron since January 1994 and is Chairman of our International Advisory Council.

Mr. Bohlen joined Textron in November 1999 as Senior Vice President and Chief Information Officer and became Executive Vice President and Chief Innovation Officer in April 2000.

Mr. Butler joined Textron in July 1997 as Executive Vice President and Chief Human Resources Officer and became Executive Vice President Administration and Chief Human Resources Officer in January 1999.

Mr. French joined Textron in December 2000 as Executive Vice President and Chief Financial Officer of Textron Inc. and assumed the additional position of Chairman and Chief Executive Officer of Textron Financial Corporation in January 2004.

Ms. Howell has been Executive Vice President Government Affairs, Strategy and Business Development, International, Communications and Investor Relations since October 2000 and serves on our International Advisory Council. Ms. Howell joined Textron in 1980 and became an Executive Vice President in August 1995.

Mr. O’Donnell joined Textron as Executive Vice President and General Counsel in March 2000. Mr. O’Donnell is a Senior Partner in the Washington, D.C.-based law firm of Williams & Connolly, which he first joined in 1977. From 1989 to 1992, he served as General Counsel of the U.S. Department of Defense.

PART II

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The principal market on which our common stock is traded is the New York Stock Exchange under the symbol “TXT.” Our stock also is traded on the Chicago Stock Exchange. At December 29, 2007, there were approximately 15,000 record holders of Textron common stock. On July 18, 2007, our Board of Directors approved a two-for-one split of our common stock effected in the form of a 100% stock dividend. The additional shares resulting from the stock split were distributed on August 24, 2007 to shareholders of record on August 3, 2007. Prior period per share data has been restated to reflect this stock split. The high and low common stock prices per share as reported on the New York Stock Exchange, and the dividends paid per share are provided in the following table:

12

|

|

|

2007 |

|

2006 |

|

||||||||||||||

|

|

|

High |

|

Low |

|

Dividends |

|

High |

|

Low |

|

Dividends |

|

||||||

|

First quarter |

|

$ |

49.10 |

|

$ |

44.08 |

|

$ |

0.194 |

|

$ |

47.20 |

|

$ |

37.88 |

|

$ |

0.194 |

|

|

Second quarter |

|

56.91 |

|

45.35 |

|

0.194 |

|

49.05 |

|

41.25 |

|

0.194 |

|

||||||

|

Third quarter |

|

63.13 |

|

53.01 |

|

0.23 |

|

46.56 |

|

40.55 |

|

0.194 |

|

||||||

|

Fourth quarter |

|

73.38 |

|

62.58 |

|

0.23 |

|

49.19 |

|

44.09 |

|

0.194 |

|

||||||

Issuer Repurchases of Equity Securities

|

Fourth Quarter |

|

Total |

|

Average |

|

Total

Number |

|

Maximum |

|

|

|

Month 1 (September 30, 2007 – November 3, 2007) |

|

8,134 |

* |

$ |

66.04 |

|

— |

|

22,749,000 |

|

|

Month 2 (November 4, 2006 – December 1, 2007) |

|

— |

|

— |

|

— |

|

22,749,000 |

|

|

|

Month 3 (December 2, 2007 – December 29, 2007) |

|

962 |

* |

70.61 |

|

— |

|

22,749,000 |

|

|

|

Total |

|

9,096 |

|

66.53 |

|

— |

|

|

|

|

* Amount represents the number of shares we received as payment for the exercise price of employee stock options, which are not included in the publicly announced plan.

** On July 18, 2007, our Board of Directors approved a new plan authorizing the repurchase of up to 24 million shares of our common stock. The plan has no expiration date.

Stock Performance Graph

The following graph compares the change in value of $100 invested on December 31, 2002 in Textron common stock, the Standard & Poor’s 500 Stock Index and a market-weighted peer group index. The values calculated assume dividend reinvestment. Our peer group consists of the following 17 companies, which operate in the various industries in which we conduct business: The Boeing Company, Crane Co., Dover Corporation, General Dynamics Corporation, Honeywell International, Inc., Illinois Tool Works Inc., ITT Industries, Inc., Johnson Controls Inc., Lockheed Martin Corporation, Millipore Corporation, Northrop Grumman Corporation, Pall Corp., Parker Hannifin Corp., Raytheon Company, Rockwell Automation, Inc., Tyco International LTD. and United Technologies Corporation.

13

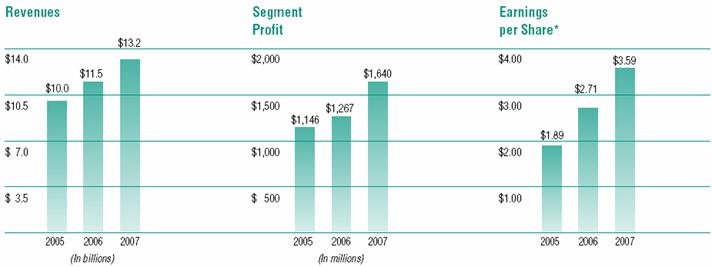

Item 6. Selected Financial Data

|

(Dollars in millions, except per share amounts and where otherwise noted) |

|

2007 |

|

2006 |

|

2005 |

|

2004 |

|

2003 |

|

||||||

|

Revenues |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Bell |

|

$ |

3,915 |

|

$ |

3,408 |

|

$ |

2,881 |

|

$ |

2,254 |

|

$ |

2,348 |

|

|

|

Cessna |

|

5,000 |

|

4,156 |

|

3,480 |

|

2,473 |

|

2,299 |

|

||||||

|

Industrial |

|

3,435 |

|

3,128 |

|

3,054 |

|

3,046 |

|

2,836 |

|

||||||

|

Finance |

|

875 |

|

798 |

|

628 |

|

545 |

|

572 |

|

||||||

|

Total revenues |

|

$ |

13,225 |

|

$ |

11,490 |

|

$ |

10,043 |

|

$ |

8,318 |

|

$ |

8,055 |

|

|

|

Segment profit |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Bell |

|

$ |

335 |

|

$ |

249 |

|

$ |

368 |

|

$ |

250 |

|

$ |

234 |

|

|

|

Cessna |

|

865 |

|

645 |

|

457 |

|

267 |

|

199 |

|

||||||

|

Industrial |

|

218 |

|

163 |

|

150 |

|

194 |

|

150 |

|

||||||

|

Finance |

|

222 |

|

210 |

|

171 |

|

139 |

|

122 |

|

||||||

|

Total segment profit |

|

1,640 |

|

1,267 |

|

1,146 |

|

850 |

|

705 |

|

||||||

|

Special charges |

|

— |

|

— |

|

(118 |

) |

(59 |

) |

(77 |

) |

||||||

|

Gain on sale of businesses |

|

— |

|

— |

|

— |

|

— |

|

15 |

|

||||||

|

Corporate expenses and other, net |

|

(253 |

) |

(202 |

) |

(199 |

) |

(157 |

) |

(123 |

) |

||||||

|

Interest expense, net |

|

(87 |

) |

(90 |

) |

(90 |

) |

(94 |

) |

(96 |

) |

||||||

|

Income taxes |

|

(385 |

) |

(269 |

) |

(223 |

) |

(165 |

) |

(109 |

) |

||||||

|

Distributions on preferred securities, net of income taxes |

|

— |

|

— |

|

— |

|

— |

|

(13 |

) |

||||||

|

Income from continuing operations |

|

$ |

915 |

|

$ |

706 |

|

$ |

516 |

|

$ |

375 |

|

$ |

302 |

|

|

|

Per share of common stock** |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Income from continuing operations — basic |

|

$ |

3.66 |

|

$ |

2.76 |

|

$ |

1.93 |

|

$ |

1.36 |

|

$ |

1.11 |

|

|

|

Income from continuing operations — diluted |

|

$ |

3.59 |

|

$ |

2.71 |

|

$ |

1.89 |

|

$ |

1.34 |

|

$ |

1.10 |

|

|

|

Dividends declared |

|

$ |

0.85 |

|

$ |

0.78 |

|

$ |

0.70 |

|

$ |

0.66 |

|

$ |

0.65 |

|

|

|

Book value at year-end |

|

$ |

13.99 |

|

$ |

10.51 |

|

$ |

12.55 |

|

$ |

13.45 |

|

$ |

13.40 |

|

|

|

Common stock price: High |

|

$ |

73.38 |

|

$ |

49.19 |

|

$ |

40.02 |

|

$ |

37.31 |

|

$ |

28.85 |

|

|

|

|

Low |

|

$ |

44.08 |

|

$ |

37.88 |

|

$ |

32.92 |

|

$ |

25.42 |

|

$ |

13.42 |

|

|

|

Year-end |

|

$ |

71.62 |

|

$ |

46.88 |

|

$ |

38.49 |

|

$ |

36.90 |

|

$ |

28.59 |

|

|

Common shares outstanding (In thousands)** |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Basic average |

|

249,792 |

|

255,098 |

|

267,062 |

|

274,674 |

|

271,750 |

|

||||||

|

Diluted average* |

|

254,826 |

|

260,444 |

|

272,892 |

|

280,339 |

|

274,434 |

|

||||||

|

Year-end |

|

250,061 |

|

251,192 |

|

260,370 |

|

270,746 |

|

274,476 |

|

||||||

|

Financial position |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Total assets |

|

$ |

19,956 |

|

$ |

17,550 |

|

$ |

16,499 |

|

$ |

15,875 |

|

$ |

15,171 |

|

|

|

Manufacturing group debt |

|

$ |

2,148 |

|

$ |

1,800 |

|

$ |

1,934 |

|

$ |

1,770 |

|

$ |

2,008 |

|

|

|

Finance group debt |

|

$ |

7,311 |

|

$ |

6,862 |

|

$ |

5,420 |

|

$ |

4,783 |

|

$ |

4,407 |

|

|

|

Mandatorily redeemable preferred securities — Finance group |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

— |

|

$ |

26 |

|

|

|

Shareholders’ equity |

|

$ |

3,507 |

|

$ |

2,649 |

|

$ |

3,276 |

|

$ |

3,652 |

|

$ |

3,690 |

|

|

|

Manufacturing group debt-to-capital (net of cash) |

|

32 |

% |

29 |

% |

26 |

% |

25 |

% |

30 |

% |

||||||

|

Manufacturing group debt-to-capital |

|

38 |

% |

40 |

% |

37 |

% |

33 |

% |

35 |

% |

||||||

|

Investment data |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Capital expenditures, including capital leases |

|

$ |

423 |

|

$ |

447 |

|

$ |

380 |

|

$ |

294 |

|

$ |

289 |

|

|

|

Depreciation |

|

$ |

298 |

|

$ |

271 |

|

$ |

284 |

|

$ |

265 |

|

$ |

260 |

|

|

|

Research and development |

|

$ |

814 |

|

$ |

786 |

|

$ |

692 |

|

$ |

574 |

|

$ |

573 |

|

|

|

Other data |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

Number of employees at year-end |

|

44,000 |

|

40,000 |

|

37,000 |

|

34,000 |

|

31,000 |

|

||||||

|

Number of common shareholders at year-end |

|

15,000 |

|

16,000 |

|

17,000 |

|

18,000 |

|

19,000 |

|

||||||

* Diluted average common shares outstanding assumes full conversion of outstanding preferred stock and exercise of stock options.

** All prior periods presented have been restated to reflect a two-for-one stock split in 2007.

14

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Business Overview

2007 was an exceptional year in many respects. We experienced strong sales and organic growth, particularly in our aerospace and defense businesses. Cessna set a new record with 773 jet orders, while demand for commercial helicopters remained strong with Bell Helicopter recording 268 orders. Our aircraft and defense backlog increased to $18.8 billion, up 45% from a year ago.

We strategically acquired businesses to complement our core growth areas, the most significant of which was the acquisition of United Industrial Corporation (“UIC”). UIC, operating through its wholly owned subsidiary, AAI Corporation (“AAI”), is a leading provider of intelligent aerospace and defense systems, including unmanned aircraft and ground control stations, aircraft and satellite test equipment, training systems and countersniper devices. In addition to AAI, we acquired certain assets of CAV-Air LLC, a helicopter maintenance and service center; Columbia Aircraft Manufacturing Corporation, which produces high-performance, single engine aircraft; and Paladin Tools, a provider of tools and accessories for the telecommunications industry. We paid approximately $1.1 billion in cash for these four acquisitions.

We also made considerable investments in innovation, new product development and capacity expansion across our businesses, including the continued development of our commercial aircraft product offerings, with the Bell Model 429 and the Cessna CJ4.

In our Finance segment, we generated significant growth in our managed finance receivables, while portfolio quality statistics remained relatively stable.