Act File No. 333-155368

UNITED STATES SECURITIES AND EXCHANGE

COMMISSION

Washington, D.C. 20549

Post-Effective Amendment No. 5

to

FORM S-1

REGISTRATION STATEMENT

Under

THE SECURITIES ACT OF 1933

NATIONWIDE LIFE INSURANCE COMPANY

(Exact name of registrant as specified in its charter)

| OHIO |

6311 |

31-4156830

|

| (State or other jurisdiction of

incorporation or organization) |

(Primary Standard Industrial Classification

Code Number) |

(I.R.S. Employer

Identification Number) |

ONE NATIONWIDE PLAZA, COLUMBUS, OHIO 43215

(Address,

including zip code, and telephone number, including area code,

of registrant's principal executive offices)

Robert W. Horner, III

Vice President – Corporate Governance and

Secretary

One Nationwide

Plaza

Columbus, Ohio 43215

Telephone: (614) 249-7111

(Name, address, including zip code, and telephone number, including area code, of agent for service)

__________________________________________________

| |

Approximate date of commencement of proposed sale to the public: May 1,

2012 |

| If any of the securities being

registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. |

[X] |

| If this Form is filed to register

additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same

offering. |

[ ] |

| If this Form is a post-effective

amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. |

[ ] |

| If this Form is a post-effective

amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. |

[ ] |

| Indicate by check mark whether

the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of

the Exchange Act. |

[ ] |

| Large accelerated

filer |

[ ] |

| Accelerated filer

|

[ ] |

| Non-accelerated filer (Do not

check if a smaller reporting company) |

[X] |

| Smaller reporting

Company |

[ ] |

Select Retirement

INDIVIDUAL SUPPLEMENTAL IMMEDIATE FIXED INCOME

ANNUITY CONTRACT

Issued by

NATIONWIDE LIFE INSURANCE COMPANY

The date of this prospectus is May 1, 2012.

This prospectus describes Select Retirement, individual supplemental immediate fixed income annuity contracts (referred to as "Contracts") issued by Nationwide Life Insurance

Company ("Nationwide"), which are offered to investors with Morgan Stanley Smith Barney LLC, its affiliates, or any successors (collectively, "MSSB"). The Contract provides for guaranteed income for the life of a designated

person based on the Contract Owner's account at MSSB, provided all conditions specified in this prospectus are met, regardless of the actual performance or value of the investments in Your Account.

The Contract has no cash surrender value and does not provide a death benefit.

Prospective purchasers may apply to purchase a Contract through MSSB broker dealers who have entered into a selling agreement with Nationwide Investment Services Corporation

("NISC"), a subsidiary of Nationwide that acts as the general distributor of the Contracts sold through this prospectus.

This prospectus provides important information that a prospective purchaser

of a Contract should know before investing. Please read this prospectus carefully and keep it for future reference.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or passed upon the accuracy or

adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The Contracts described in this prospectus may not be available in all

state jurisdictions and, accordingly, representations made in this prospectus do not constitute an offering in such jurisdictions.

The Contract:

| · |

Is NOT a bank deposit |

| · |

Is NOT FDIC insured |

| · |

Is NOT insured or endorsed by a bank or any government agency |

| · |

Is NOT available in every state |

A purchase of this Contract is subject to certain risks. Please see the "Risk Factors" section on page

15. The Contract is novel and innovative. To date, the tax consequences of the Contract have not been addressed in binding published legal authorities; however, we understand that the Internal Revenue Service ("IRS") may

be considering tax issues associated with products similar to the Contracts, and there is no certainty as to what the IRS will conclude is the proper tax treatment for the Contracts. Consequently, you should consult a tax advisor before

purchasing a Contract.

For information on how to contact Nationwide, see "Contacting the Service Center" on page 37.

TABLE OF CONTENTS

| SUMMARY OF

THE

CONTRACTS

|

1

|

| Preliminary note regarding terms

used in this prospectus. |

|

| What is the

Contract? |

|

| How does the Contract generally

work? |

|

| How much will the Contract

cost? |

|

| What are the requirements to

purchase the Contract? |

|

| Is this Contract right for

you? |

|

| Who is Morgan Stanley Smith

Barney LLC? |

|

| What are the Eligible Portfolios

and how are they managed? |

|

| Can a Contract be purchased by

an Individual Retirement Account? |

|

| Can the Contract Owner cancel

the Contract? |

|

| Does the Contract contain any

type of spousal benefit? |

|

| Does the Contract contain any

kind of Guaranteed Lifetime Withdrawal Base increases? |

|

| RISK

FACTORS

|

15

|

| Your Account may perform well

enough that you may not receive any Guaranteed Lifetime Income Payments from Nationwide under the Contract. |

|

| Your Investment choices are

limited by the Contract. |

|

| You must remain invested in Your

Account at MSSB to maintain your Contract. |

|

| You may die before receiving

payments from us. |

|

| Early Withdrawals or Excess

Withdrawals will reduce or eliminate the Guarantee provided by your Contract. |

|

| The Contract Fee will reduce the

growth of Your Account. |

|

| Actions of your creditors may

reduce or eliminate the Guarantee provided by your Contract. |

|

| Your Guarantee may terminate if

MSSB no longer manages the Eligible Portfolios. |

|

| Nationwide determines that an

Eligible Portfolio is no longer eligible as an investment option under the Contract. |

|

| Additional deposits that

exceed $2,000,000 in Total Gross Deposits could suspend or terminate your Contract. |

|

| Nationwide's claims paying

ability. |

|

| Tax Consequences.

|

|

| YOUR

RELATIONSHIP WITH MSSB AND

NATIONWIDE

|

16

|

| The Contract. |

|

| Management of Your

Account. |

|

| THE

ACCUMULATION

PHASE

|

17

|

| What is the Guaranteed Lifetime

Withdrawal Base and how is it calculated? |

|

| Can the Guaranteed Lifetime

Withdrawal Base change during the Accumulation Phase? |

|

| What if the Account Value falls

to the Minimum Account Value before the Withdrawal Start Date

but your Guaranteed Lifetime Withdrawal Base is above zero? |

|

| THE WITHDRAWAL

PHASE

|

19

|

| What events trigger the

Withdrawal Phase? |

|

| What is the Withdrawal Start

Date and what does it mean? |

|

| What is the Guaranteed Lifetime

Withdrawal Amount and how is it calculated? |

|

| Can the Guaranteed Lifetime

Withdrawal Base change during the Withdrawal Phase? |

|

| Do Early Withdrawals and Excess

Withdrawals affect the Guaranteed Lifetime Withdrawal Amount

and the Guaranteed Lifetime Withdrawal Base differently? |

|

| What if the Account Value and

the Guaranteed Lifetime Withdrawal Base decline to zero due to

Excess Withdrawals during the Withdrawal Phase? |

|

| TRIGGERING THE

INCOME

PHASE

|

22

|

| What events will trigger the

Income Phase? |

|

| How is the Contract transitioned

into the Income Phase? |

|

| THE INCOME

PHASE

|

23

|

| How much will each Guaranteed

Lifetime Income Payment be? |

|

| Will the Guaranteed Lifetime

Income Payment ever increase or decrease? |

|

| How often are the Guaranteed

Lifetime Income Payments paid? |

|

| How long will the Guaranteed

Lifetime Income Payments be paid? |

| TERMS AND

CONDITIONS OF THE

CONTRACT

|

23

|

| What does it mean to have a

change in "terms and conditions" of the Contract? |

|

| How will a change to the terms

and conditions of the Contract affect an existing Contract? |

|

| SPOUSAL

CONTINUATION

OPTION

|

24

|

| What is the Spousal Continuation

Option? |

|

| Election of the Spousal

Continuation Option. |

|

| How much does the Spousal

Continuation Option cost? |

|

| Is it possible to pay for the

Spousal Continuation Option but not receive a benefit from it? |

|

| THE CONTRACT

FEE

|

25

|

| How much is the Contract

Fee? |

|

| When and how is the Contract Fee

assessed? |

|

| Will the Contract Fee be the

same amount from quarter to quarter? |

|

| Will advisory and other fees

impact the Account Value and the Guarantee under the Contract? |

|

| MANAGING

WITHDRAWALS FROM YOUR

ACCOUNT

|

26

|

| DEATH

PROVISIONS

|

27

|

| MARRIAGE

TERMINATION

PROVISIONS

|

28

|

| Marriage termination in the

Accumulation or Withdrawal Phases. |

|

| Marriage termination in the

Income Phase. |

|

| SUSPENSION AND

TERMINATION

PROVISIONS

|

29

|

| What does it mean to have a

suspended Contract? |

|

| What will cause a Contract to be

suspended? |

|

| What can be done to take the

Contract out of suspension? |

|

| Specific suspension events and

their cures. |

|

| What will cause a Contract to be

terminated? |

|

| FEDERAL INCOME

TAX

CONSIDERATIONS

|

32

|

| Taxation of Distributions from

the Contract. |

|

| Taxation of Eligible

Portfolios or Former Eligible Portfolios that are not held by an Individual Retirement Account. |

|

| Additional Medicare

Tax. |

|

| Section 1035

Exchanges. |

|

| Qualified Retirement

Plans. |

|

| Income Tax

Withholding. |

|

| State and Local Tax

Considerations. |

|

| Non-Resident

Aliens. |

|

| Payment of Advisory or Service

Fees. |

|

| Seek Tax Advice.

|

|

| MISCELLANEOUS

PROVISIONS

|

36

|

| Ownership of the

Contract. |

|

| Periodic communications to

Contract Owners. |

|

| Amendments to the

Contract. |

|

| Assignment. |

|

| Misstatements.

|

|

| DISTRIBUTION

(MARKETING) OF THE

CONTRACT

|

36

|

| LEGAL

OPINION

|

37

|

| ABOUT

NATIONWIDE

|

37

|

| CONTACTING THE

SERVICE

CENTER

EXPERTS

|

37

37 |

| DISCLOSURE OF

COMMISSION POSITION ON

INDEMNIFICATION

|

37

|

|

DEFINITIONS

|

38

|

| APPENDIX

A |

A-1 |

Available Information

Information about Nationwide and the product may also be reviewed and copied

at the SEC's Public Reference Room in Washington, D.C., or may be obtained, upon payment of a duplicating fee, by writing the Public Reference Section of the SEC at 100 F Street NE, Washington, D.C. 20549. Additional information on the

operation of the Public Reference Room may be obtained by calling the SEC at (202) 551-8090. The SEC also maintains a website (www.sec.gov) that contains the prospectus and other information.

Preliminary note regarding terms used in this

prospectus.

Certain terms used in this prospectus have specific and important meanings. Some are explained below. Others are explained as they appear in the

prospectus. Additionally, in the back of this prospectus, there is a "Definitions" provision containing definitions of all of the terms used in the prospectus.

| Ø |

"We," "us," "our," "Nationwide" or the "Company" means Nationwide Life Insurance

Company. |

| Ø |

"You" or "yours," "Owner" or "Contract Owner" means the owner of the

Contract. If more than one Owner is named, each Owner may also be referred to as a "joint owner." Joint owners are permitted only when they are spouses as recognized by applicable Federal law. |

| Ø |

"Your Account" means the unified managed account you own. As described

further below, "Select UMA" is a unified managed account investment advisory program offered by MSSB. MSSB offers Your Account through registered representatives and investment advisor representatives ("Financial Advisors") of

MSSB. You must purchase a Contract with the assistance of these Financial Advisors. Financial Advisors assist clients in analyzing whether the investment options are appropriate for the client. If your

Financial Advisor recommends a MSSB account to you, upon your request, MSSB will open Your Account. MSSB acts as introducing broker to Citigroup Global Markets Inc. ("CGMI"), which acts as clearing broker for Your

Account. The assets in Your Account are custodied at CGMI. |

The following is a summary of the Contract. Unless otherwise

noted, this prospectus assumes that you are the sole Contract Owner. You should read the entire prospectus in addition to this summary.

What is the Contract?

The Contract is an Individual Supplemental Immediate Fixed Income Annuity

Contract that is available for you to purchase if you open and own Your Account. If you own Your Account, then you and your Financial Advisor have determined that one or more MSSB investment options available in the Select UMA investment

advisory program is appropriate for you. The Contract is an optional feature available on Your Account for those investors who intend to use the assets in their account to provide income payments for retirement or other long-term

purposes.

Specifically, the Contract provides for annuity payments ("Guaranteed Lifetime Income Payments") to be paid to you under circumstances outlined below as long as you meet the

conditions of the Contract as described in this prospectus. If, or when, you are eligible and elect to take withdrawals ("Guaranteed Lifetime Withdrawals") from Your Account, and if, or when, the value of the assets in Your Account ("Your

Account Value") falls below a certain amount or you live to a certain age, you will receive Guaranteed Lifetime Income Payments from us for the rest of your life (the "Guarantee"). The amount of your Guaranteed Lifetime Withdrawals will

be based on a percentage of the value of Your Account when you first purchase the Contract (with adjustments for additions and withdrawals, the "Guaranteed Lifetime Withdrawal Base") and will vary based on Your Account Value and other actions you

take with regard to Your Account, as described in this prospectus.

The Contract also offers a Spousal Continuation Option available at the

time of application and a potential 5% increase (the 5% roll-up) in the Guaranteed Lifetime Withdrawal Base during the Accumulation Phase:

| · |

The Spousal Continuation Option allows, upon your death, your surviving spouse to

continue the Contract and receive all the rights and benefits associated with the Contract (see "Spousal Continuation Option," later in this prospectus). |

| · |

The Contract's potential 5% roll-up is calculated based on your original Guaranteed

Lifetime Withdrawal Base and may increase the Guaranteed Lifetime Withdrawal Base. This feature is only available during the Accumulation Phase (see "Can the Guaranteed Lifetime Withdrawal

Base change during the Accumulation Phase?," later in this prospectus). |

Guaranteed Lifetime Income Payments under your Contract are triggered if

the withdrawals (within the permitted limits of the Contract) and/or poor market performance reduce Your Account Value to $10,000 or less. Note: If a triggering event does not occur, you

will not receive any payments under this Contract and your Guarantee will have no value.

The Contract Guarantee is based on the age and life of the

Annuitant. For Non-Qualified Contracts, the Annuitant is you, the Contract Owner and the Owner of Your Account. If this Contract is issued to a trustee of a trust or a custodian of an Individual Retirement Account ("IRA"), you

must be the Annuitant, and if you elect the Spousal Continuation Option (discussed later in this prospectus), you and your spouse must be Co-Annuitants and your spouse must be listed as the beneficiary of Your Account.

It is important to note that the Contract itself has no cash surrender value because there are no assets attributable directly to it. All obligations under the

Contract to make Guaranteed Lifetime Income Payments to you are tied to Your Account. If you surrender your interest in or otherwise terminate Your Account, this Contract also terminates

and you will not receive any Guaranteed Lifetime Income Payments under this Contract.

1

The Contract may terminate and you may not receive any Guaranteed Lifetime Income Payments under this Contract if you terminate your Select UMA Account or if for any reason MSSB

no longer manages any Eligible Portfolios or Former Eligible Portfolios (as defined below) in the Select UMA program.

Payments under the Contract are backed only by the claims paying ability of

Nationwide and are not guaranteed by MSSB or any of its affiliates.

How does the Contract generally work?

The life of the Contract can generally be described as having three phases: an "Accumulation Phase," a "Withdrawal Phase," and an "Income Phase." Your Contract will

begin in the Accumulation Phase, and you must affirmatively elect to enter the Withdrawal Phase. After a triggering event (described below) occurs, you can elect to enter the Income Phase.

Accumulation Phase. During the Accumulation Phase, Your Account is just like any other advisory account at

MSSB, except that Your Account must be 100% invested in an "Eligible Portfolio" or "Former Eligible Portfolio." Eligible Portfolios are those Select UMA program investment models that contain certain permissible investments under the

Contract. A Former Eligible Portfolio is a previously permissible investment model that is no longer available to new Contract Owners. Please see "What are the Eligible

Portfolios and how are they managed?," later in this prospectus for more information on the Select UMA program and the Eligible Portfolios currently available for the Guarantee.

The Contract provides an increase in your Guaranteed Lifetime Withdrawal Base each Contract Anniversary (the anniversary of the date we issue your Contract) equal to the greatest

of:

| (a) |

The current Guaranteed Lifetime Withdrawal Base, adjusted for transactions in the

previous Contract Year that affected the Guaranteed Lifetime Withdrawal Base; |

| (b) |

Your Account Value as of that Contract Anniversary; or |

| (c) |

The original Guaranteed Lifetime Withdrawal Base with a 5% roll-up. This

is equal to the original Guaranteed Lifetime Withdrawal Base plus 5% of the original Guaranteed Lifetime Withdrawal Base for each Contract Anniversary that has been reached. An adjustment will be made to the calculations for transactions

that increase or decrease the Guaranteed Lifetime Withdrawal Base. |

The greatest of these three amounts will become your new Guaranteed

Lifetime Withdrawal Base at your next Contract Anniversary. The review of these three amounts is referred to as the "Annual Benefit Base Review." See "Can the Guaranteed

Lifetime Withdrawal Base change during the Accumulation Phase?," later in the prospectus for more information.

You may make Additional Deposits (payments applied to Your Account after

the Contract is issued), which will increase your Guaranteed Lifetime Withdrawal Base. Any withdrawals taken during the Accumulation Phase will reduce your Guaranteed Lifetime Withdrawal Base.

Withdrawal Phase. Anytime after you (and your spouse, if you elected the Spousal Continuation Option), reach

the age of 55, you may elect to begin the Withdrawal Phase. You must submit a Withdrawal Phase election form to us to enter the Withdrawal Phase. The day Nationwide receives your Withdrawal Phase election form indicating that

you are eligible and affirmatively elect to begin taking annual withdrawals of the Guaranteed Lifetime Withdrawal Amount is considered the "Withdrawal Start Date." Once the Contract is in the Withdrawal Phase, you can take annual

withdrawals up to a certain amount, the "Guaranteed Lifetime Withdrawal Amount," from Your Account without reducing your Guaranteed Lifetime Withdrawal Base and any potential Guaranteed Lifetime Income Payments.

Once you elect to begin taking Guaranteed Lifetime Withdrawals, you may withdraw up to 4%, the "Guaranteed Lifetime Withdrawal Percentage," of your Guaranteed Lifetime Withdrawal

Base from Your Account without reducing your Guaranteed Lifetime Withdrawal Base and any potential Guaranteed Lifetime Income Payments. When you (and your spouse, if you elected the Spousal Continuation Option) reach age 65, your

Guaranteed Lifetime Withdrawal Percentage increases to 5%. At that time, you may withdraw up to 5% of your Guaranteed Lifetime Withdrawal Base from Your Account without reducing your Guaranteed Lifetime Withdrawal Base and any potential

Guaranteed Lifetime Income Payments.

Income

Phase. If and when any of the following triggering events occur, the Contract will be eligible to begin the Income Phase:

| · |

Your Account Value, after the Withdrawal Start Date, falls below the greater of

$10,000 or the Guaranteed Lifetime Withdrawal Amount (the "Minimum Account Value"); or |

| · |

Your Account Value is invested in the Minimum Account Value Eligible Portfolio, as

discussed in the "Suspension and Termination Provisions" section later in this prospectus, and you reach the age of 55; or |

| · |

You, after the Withdrawal Start Date, affirmatively elect to begin the Income Phase

by submitting the appropriate administrative forms. |

2

At that time, you will instruct MSSB to transfer the remaining value in Your Account to us, and we will begin making annual guaranteed fixed annuity payments to you for as long

as you (or your spouse, if the Spousal Continuation Option, described herein, is elected) live. After this transition into the Income Phase, Your Account is closed and you no longer own interests in the Eligible Portfolio or Former

Eligible Portfolio. Rather, your ownership interest lies in the guaranteed stream of annuity payments - the Guaranteed Lifetime Income Payments - which Nationwide is obligated to provide. Note: It is possible that you may never receive Guaranteed Lifetime Income Payments if none of the triggering events occur. If you (and your spouse, if the Spousal Continuation Option is elected)

die before any of the triggering events occur, no benefit is payable under this Contract.

How much will the Contract cost?

Accumulation Phase and Withdrawal Phase. During both the Accumulation Phase and Withdrawal Phase, you will pay

a fee for the Contract (the "Contract Fee" or "Fee"), which will be deducted from Your Account Value on a quarterly basis. The Fee is calculated as a percentage (the "Contract Fee Percentage") of your Guaranteed Lifetime Withdrawal Base

(not Your Account Value) as of the end of the calendar quarter. Please see "The Contract Fee," for more information.

The Fee compensates us for the risk we assume in providing you Guaranteed Lifetime Income Payments. We intend to invest the fees as we invest

our General Account assets. We take into account the amount of Guaranteed Lifetime Income Payments and anticipated cash-flow requirements when making investments. Nationwide is not obligated to invest in accordance with any

particular investment objective, but will generally adhere to our overall investing philosophy.

The Fee is calculated as follows:

Contract Fee Percentage x (# of days in the quarter/365) x Guaranteed Lifetime Withdrawal Base as of quarter end

We reserve the right to increase the Contract Fee Percentage (up to a maximum of 1.45% of your Guaranteed Lifetime Withdrawal Base or 1.75% of your Guaranteed Lifetime Withdrawal

Base with the Spousal Continuation Option elected) and will provide written notice to you. We provide a two-year Contract Fee Percentage guarantee, during which time we will not increase the Contract Fee Percentage (if at all) before your

second Contract Anniversary. Please see "Terms and Conditions of the Contract," for more information.

Note: The Contract Fee is in addition to any charges that are imposed in connection with Your Account including advisory

and other charges imposed by your Financial Advisor, MSSB, or any of the investments that comprise Your Account. Any fees you pay that are deducted from Your Account Value, including the Contract Fee, will negatively affect the growth of

Your Account Value.

| Maximum Recurring Contract Fees | |

| (assessed on the first day of

each calendar quarter against the Guaranteed Lifetime Withdrawal Base as of the last day of the previous calendar quarter) | |

| Contract

Fee |

1.45%1 |

| Spousal

Continuation Option Fee |

0.30%2 |

| Total Contract Fee (including the Spousal Continuation Option)

|

1.75%3

|

Income Phase.

During the Income Phase, no Contract Fee is assessed.

Neither MSSB nor your Financial Advisor receives any compensation from

Nationwide directly associated with the sale of the Contracts or for administrative services associated with the Contract. In order to maintain your Contract, you must keep Your Account invested in an Eligible Portfolio or Former Eligible

Portfolio. MSSB and their Financial Advisors will receive annual advisory fees and other compensation relevant to services provided in connection with the Select UMA program as outlined in your client agreement (the "Client Agreement")

and as disclosed in the MSSB ADV (as defined below) during the Accumulation and Withdrawal Phases of the Contract.

What are the requirements to purchase the

Contract?

The Contract is only available for purchase by investors who elect and continue to invest, with the help of their Financial Advisor, in the Eligible Portfolios approved by

Nationwide and offered by MSSB in the Select UMA program. Upon such election, MSSB will open Your Account.

You, as the Owner of Your Account at MSSB, may purchase a Contract from

MSSB, which is also a broker-dealer, when you open Your Account. To purchase the Contract without the Spousal Continuation Option, the Annuitant must be between 45 and 75 at the time of application. To purchase the Contract

with the Spousal Continuation Option, the younger Annuitant must be between 45 and 80 and the older Annuitant must be 84 or younger at the time of application.

3

To purchase a Contract, the value of Your Account on the date of application must equal $50,000 or more. We reserve the right to refuse to accept Additional Deposits

made into Your Account for your Guaranteed Lifetime Withdrawal Base, including your initial deposit ("Total Gross Deposits") that exceed $2,000,000. Withdrawals do not impact the limit of $2,000,000 in Total Gross Deposits.

Please see the "Risk Factors" and "Suspension and Termination

Provisions," later in this prospectus.

Additionally, on the date of application (and continuously thereafter),

Your Account must be allocated to one of the Eligible Portfolios as discussed herein. Once you select an Eligible Portfolio, you may switch to another Eligible Portfolio, but Your Account Value must always remain invested in an Eligible

Portfolio in order to maintain the benefits and the Guarantee associated with the Contract. If Nationwide determines that an Eligible Portfolio is no longer eligible as an investment option, you may remain in the Former Eligible Portfolio

as indicated in the "Terms and Conditions of the Contract" section.

Note: IF AT ANY

TIME 100% OF YOUR ACCOUNT IS NOT INVESTED IN AN ELIGIBLE PORTFOLIO OR FORMER ELIGIBLE PORTFOLIO, YOUR CONTRACT WILL BE SUSPENDED AND MAY TERMINATE (see "Suspension and Termination

Provisions"). Ensuring that you continue to maintain Your Account and that it remains invested according to the terms of the Contract is your responsibility.

Is this Contract right for you?

This Contract is meant to protect your assets in the event market

fluctuations bring Your Account Value below the Minimum Account Value or in the event you outlive your assets. This Contract does NOT protect the actual investments in Your Account. For example, if you initially invest $600,000

in Your Account and the value of Your Account within that year falls to $400,000, we are not required to add $200,000 to Your Account. Instead, we guarantee that you will be able to withdraw, after reaching the age of 55, Guaranteed

Lifetime Withdrawal Amounts equal to 4% of $600,000 (instead of 4% of $400,000). We guarantee this even if such withdrawals bring Your Account Value to $0.

It is also important to understand, that even after you have reached age 55 and start taking Guaranteed Lifetime Withdrawals from Your Account, those withdrawals are made from

Your Account. We are required to start using our own money to make Guaranteed Lifetime Income Payments only when, and if, Your Account Value reaches the Minimum Account Value because of withdrawals within the limits of this Contract

and/or poor investment performance. We limit our risk of having to make Guaranteed Lifetime Income Payments by limiting the amount you may withdraw each year from Your Account without reducing your Guaranteed Lifetime Withdrawal Base. If the investment return on Your Account over time is sufficient to generate gains that can sustain systematic or periodic withdrawals equal to the Guaranteed Lifetime Withdrawal Amount, then Your Account

Value will never be reduced to the Minimum Account Value and we will never have to make Guaranteed Lifetime Income Payments to you.

There are many variables, however, other than average annual return on Your Account, that will determine whether the investments in Your Account, without the Contract, would have

generated enough gain over time to sustain systematic or periodic withdrawals equal to the Guaranteed Lifetime Withdrawals you would have received if you had purchased the Contract. Your Account Value may have declined over time before

beginning the Income Phase, which means that your investments would have to produce an even greater return after the Income Phase to make up for the investment losses before that date. Moreover, studies have shown that individual years of

negative annual average investment returns can have a disproportionate impact on the ability of your retirement investments to sustain systematic withdrawals over an extended period, depending on the timing of the poor investment

returns.

| |

Who is Morgan Stanley Smith Barney LLC? |

Morgan Stanley Smith Barney LLC ("MSSB LLC") is a financial services firm. MSSB LLC's principal activities include retail and institutional private client services,

including but not limited to providing advice with respect to financial markets, securities and commodities, and executing securities and commodities transactions as broker or dealer; securities underwriting and investment banking; investment

management (including fiduciary and administrative services); and trading and holding securities and commodities for its own account.

MSSB LLC is registered as a securities broker-dealer, investment advisor, and futures commission merchant. Affiliates of MSSB LLC are registered as commodity pool operators

and/or commodity trading advisors.

On January 13, 2009, Morgan Stanley and Citigroup Inc. agreed to a

transaction (the "Transaction") combining the Global Wealth Management Group of Morgan Stanley & Co. Incorporated and the Smith Barney division of CGMI into a new joint venture. The Transaction closed on May 31, 2009. The

joint venture now owns MSSB LLC, a recently formed investment advisor and broker-dealer that is registered with the Securities and Exchange Commission. CGMI (the clearing broker for Your Account) is an indirect wholly-owned subsidiary of

Citigroup Inc. For purposes of this prospectus, "MSSB" refers to MSSB LLC and its affiliates, or any successors. Nationwide is not affiliated with MSSB and does not manage Your Account.

4

| |

What are the Eligible Portfolios and how are they managed? |

Eligible Portfolios are those Select UMA asset allocation investment models ("Models") established by MSSB and approved by Nationwide, which contain certain permissible

investments under the Contract. Each of the Models available as an Eligible Portfolio corresponds to a specific investment risk profile. The Models are comprised of asset classes and asset class percentages established by

MSSB. You and your Financial Advisor select the actual investments within each asset class from a list of investment products ("Investment Products") created by MSSB and approved by Nationwide. These Investment Products can take the form

of Mutual Funds, Exchange Traded Funds and/or Separately Managed Accounts. You and your Financial Advisor may elect any combination of the permitted Investment Products to fulfill each asset class percentage:

Mutual Funds - A mutual fund is a professionally managed type of collective investment that pools money from many investors and invests it in stocks, bonds, short-term money

market instruments, and/or other securities. The mutual fund will have a fund manager that trades the pooled money on a regular basis, and is an open end investment company registered under the Investment Company Act of 1940.

Exchange Traded Funds ("ETFs") - An ETF is an investment vehicle traded on stock exchanges, much like stocks. An ETF holds assets such as stocks or bonds and trades at

approximately the same price as the net asset value of its underlying assets over the course of the trading day. Many ETFs track an index, such as the Dow Jones Industrial Average or the S&P 500.

Separately Managed Accounts ("SMAs") - A SMA is comprised of individual securities which an Overlay Manager will invest in for the client, based on an investment model provided

by one or more separately registered investment managers ("sub-managers"), which invests for the client based on their own investment decision. This differs from a mutual fund because the investor directly owns the securities instead of owning a

share in a pool of securities. Please see "Your Relationship with MSSB and Nationwide," for more information about the Overlay Manager.

MSSB selects the list of Investment Products available to you and your Financial Advisor from among those that MSSB can recommend based on MSSB's due diligence

research. MSSB bases its research on factors such as consistency with investment strategy and historical performance. The list of Investment Products that MSSB recommends will change when MSSB identifies additional Investment

Products that satisfy MSSB's research, or when MSSB determines that existing Investment Products no longer satisfy MSSB's research. Nationwide also reviews the list of available Investment Products to ensure that it is comfortable with

the risk that each Investment Product could generate. MSSB provides the list of available Investment Products to your Financial Advisor.

As the provider of the Guarantee under the Contracts, we maintain sole discretion as to which investment options will be permitted under the Contracts as Eligible

Portfolios. We only make available those Eligible Portfolios that we determine carry an acceptable amount of risk for Nationwide to manage the Guarantee. We monitor the risk that investments in Your Account will not generate

sufficient income for you to sustain your Guaranteed Lifetime Withdrawals during your lifetime. If, after making an Eligible Portfolio available, we subsequently determine that such Eligible Portfolio carries too much risk (the risk that

we will have to make Guaranteed Lifetime Income Payments), we will adjust the list of Eligible Portfolios, re-characterizing those portfolios that we determine to be too risky to continue offering as "Former Eligible Portfolios." We will

notify Contract Owners that originally selected a now Former Eligible Portfolio of their contractual options, which are described in the "Terms and Conditions of the Contract" section later in

this prospectus.

Four Step Investment Process

At or before the time of this Contract application, you and your Financial

Advisor will follow the process below to select your Eligible Portfolio:

Step 1: Set Investment

Objectives

Your Financial Advisor helps you establish your investment objectives for Your Account.

Step 2: Select Investment Model/Eligible Portfolio

Based on your investment objectives, your Financial Advisor recommends one Model for Your Account from the Models permitted as Eligible Portfolios. The Select UMA

program offers Models that are Eligible Portfolios and those that are not Eligible Portfolios. If you wish to receive the benefit of this Contract, you must select an Eligible Portfolio.

Step 3: Select Investment Products

Your Financial Advisor then works with you to select the specific Investment Products that will meet the requirement for each asset class and asset class percentage within the

Eligible Portfolio you selected.

Once you have (with the assistance of your Financial Advisor) selected the

Investment Products for each asset class in the Model you have chosen, the Overlay Manager will purchase the investments in a manner consistent with the Model and the Investment Products selected.

5

Step 4: Ongoing Review Process

Your Financial Advisor will contact you to determine whether short-term or long-term changes are needed in the Eligible Portfolio you selected. You may change to a

different Model from among the Models permitted as Eligible Portfolios, and you and your Financial Advisor may also change to other Investment Products from the Investment Products that are permitted for Eligible Portfolios.

Additionally, you may remain in a Former Eligible Portfolio as indicated in the "Terms and Conditions of the Contract"

section. If you move Your Account assets to a non-Eligible Portfolio (any Select UMA Model that is not an Eligible Portfolio) at any time, your Contract will be suspended. Please see "Suspension and Termination Provisions," later in this prospectus for more information. Note: Reallocating Your Account out of the Eligible Portfolio elected at the time of application

may have negative tax consequences. Please consult a qualified tax advisor for more information.

Eligible Portfolios Summary

The following tables reflect a summary of each Eligible Portfolio that is currently available for election under the Contract. The Eligible Portfolios are listed from

most conservative to least conservative. The target allocations may be changed by MSSB from time to time as provided in the Client Agreement and the MSSB ADV. MSSB monitors each Eligible Portfolio's holdings and will

periodically rebalance Your Account as provided in the Client Agreement to realign it with the current asset allocations for your Eligible Portfolio.

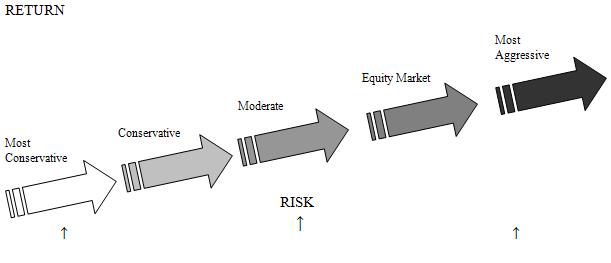

The value of your Eligible Portfolio will fluctuate over time. This means it will rise and fall in response to market events. Although past performance is

not a guarantee of future results, historically, investments that have had higher fluctuations have provided higher long term returns, along with higher risks of loss. The Return chart below shows that as you move up the risk ladder from

conservative investments to aggressive investments, you have the potential to receive higher long term returns but may also experience higher fluctuations in value.

| Capital Preservation oriented. Total return oriented, but may have higher current income. Suitable for short time horizon (3 to 5 years). |

Capital appreciation

oriented. Minimal income needs. Increasing equity exposure. Longer time horizon – at least a market cycle (5 years or more). |

Aggressive growth

oriented. No current income consideration. Greater volatility than broad stock market. Longest time horizon (10+ years). |

The target allocation categories listed below reflect investment asset

categories only, and not specific Investment Products. You and your Financial Advisor select the Investment Products to satisfy each Target Allocation. More explanation of each category follows the tables. The percentage ranges

shown are target ranges only, and may change if deemed appropriate by MSSB. Additionally, the index percentages used to establish the benchmark as determined by MSSB are provided for each Eligible Portfolio. The indices and

percentages provided by MSSB are established by MSSB based on the asset allocation of the selected Model. MSSB has determined that the benchmarks are appropriate for use as a gauge of performance of the associated Eligible

Portfolios. The indices work together to provide a blended performance percentage of how your Eligible Portfolio should perform. Your Financial Advisor will discuss how your Eligible Portfolio performed as compared to the

benchmark. Not every asset class is represented by a corresponding index. A summary of the referenced asset classes and indices follows the Eligible Portfolio tables.

6

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 1 w/o Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

|

0% |

0% |

0% |

0% |

0% |

0% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Core Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 100%

Fixed |

0% |

0% |

40

- 60% |

0

- 20% |

5

- 25% |

20

- 40% |

| Investment Strategy: Fixed Income- An all fixed income model for a most conservative investor that seeks conservative risk investments with minimal

market volatility. This investment strategy is most appropriate for investors with an investment time horizon of 1 to 3 years. Investment Objective: The investment objective for this Model has a primary emphasis on capital preservation. This Model is classified

to have low volatility. It is most suitable for an investor that is comfortable with minimal fluctuations in their portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 1 has 100% of the assets in fixed income or cash. Therefore, of all of the Eligible Portfolios, this portfolio provides the most conservative investment risk.

Benchmark: 70% BC Aggregate Bond (U.S. Fixed Income)/ 30% 90-Day

T-Bills (Cash) | ||||||

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 2 w/o Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 10% |

0

- 10% |

0

- 10% |

0

- 10% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Core Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 25%

Equity 75% Fixed |

0

- 20% |

0

- 10% |

30

- 50% |

0

- 20% |

0

- 20% |

5

- 25% |

| Investment Strategy: Global Balanced- A global balanced model with a higher emphasis on income for a conservative investor that seeks long term

growth through achieving a balance between income and capital growth globally. This investment strategy is most appropriate for investors with an investment time horizon of 3 to 5 years.

Investment Objective: The investment

objective for this Model has a primary emphasis on income with some capital growth. This Model is classified to have low volatility. It is most suitable for an investor that is comfortable with minimal fluctuations in their

portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time. Investment Risk: Fixed income is historically considered less risky than equities. Model 2 has 75% of the assets in fixed income or cash and 25% in

equities. Therefore, of all of the Eligible Portfolios, this portfolio provides a more aggressive investment risk than Model 1 and less aggressive than Models 3 and 4.

Benchmark: 18% Russell 1000 (U.S. Equity) / 7% MSCI EAFE

(International Equity)/ 60% BC Aggregate Bond (U.S. Fixed Income)/15% 90-Day T-Bills (Cash) | ||||||

7

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 3 w/o Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 15% |

0

- 15% |

0

- 10% |

0

- 10% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Core Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 40%

Equity 60% Fixed |

0

- 20% |

0

- 10% |

25

- 45% |

0

- 15% |

0

- 20% |

0

- 20% |

| Investment Strategy: Global Balanced- A global balanced

model utilizing equities, fixed income, and cash seeking some growth and moderate level of income for a moderate investor that seeks long term growth through achieving a balance between income and capital growth globally. This investment

strategy is most appropriate for investors with an investment time horizon of 3 to 5 years. Investment Objective: The investment objective for this Model has a primary emphasis on capital growth and income. This Model is classified to have

medium volatility. It is most suitable for an investor that is comfortable with fluctuations in their portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 3 has 60% of the assets in fixed income or cash and 40% in equities. Therefore, of all of the Eligible Portfolios, this portfolio provides a more aggressive investment risk than Models

1 and 2 and less aggressive than Model 4.

Benchmark: 28% Russell 3000 (U.S Equity)/ 12% MSCI EAFE

(International Equity)/ 50% BC Aggregate Bond (Fixed Income)/10% 90-Day T-Bills (Cash) | ||||||

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 4 w/o Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 15% |

0

- 15% |

0

- 15% |

0

- 15% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Core Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 50%

Equity 50% Fixed |

0

- 20% |

0

- 15% |

25

- 45% |

0

- 15% |

0

- 20% |

0

- 15% |

| Investment Strategy: Global Balanced- A global balanced model utilizing equities, fixed income, and cash seeking a

moderate level of growth and income for a moderate investor that seeks long term growth through achieving a balance between income and capital growth globally. This investment strategy is most

appropriate for investors with an investment time horizon of 5 to 7 years. Investment Objective: The investment objective for this Model has a primary emphasis on capital growth with some focus on income. This

Model is classified to have medium volatility. It is most suitable for an investor that is comfortable with fluctuations in their portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 4 has 50% of the assets in fixed income or cash and 50% in equities. Therefore, of all of the Eligible Portfolios, this portfolio provides the most aggressive investment

risk. Benchmark: 35% Russell 3000 (U.S. Equity)/ 15%

MSCI AC World x U.S. (International Equity)/ 50% BC Aggregate Bond (U.S. Fixed Income) | ||||||

8

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 1 w/ Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

|

0% |

0% |

0% |

0% |

0% |

0% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Municipal Bond Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 100%

Fixed |

0% |

0% |

40

- 60% |

0

- 20% |

5

- 25% |

20

- 40% |

| Investment Strategy: Fixed Income- An all fixed income model for a most conservative investor that seeks conservative risk investments, with

minimal market volatility. This investment strategy is most appropriate for investors with an investment time horizon of 1 to 3 years.

Investment Objective: The investment

objective for this Model has a primary emphasis on capital preservation. This Model is classified to have low volatility. It is most suitable for an investor that is comfortable with minimal fluctuations in their portfolio, and the

possibility of larger declines in value, in order to grow their portfolio over time. One of the primary reasons municipal bonds are considered separately from other types of bonds is their special ability to provide tax-exempt income.

Interest paid by the issuer (i.e., the municipality, state or local government) to bond holders is often exempt from all federal taxes, as well as state or local taxes depending on the state in which the issuer is located, subject to certain

restrictions. Therefore, for taxable accounts, it can be a tax advantage to invest in municipal bonds in lieu of core fixed income investments.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 1 has 100% of the assets in fixed income or cash. Therefore, of all of the Eligible Portfolios, this portfolio provides the most conservative investment risk.

Benchmark: 70% BC Municipal Bond (U.S. Fixed Income)/ 30% 90-Day

T-Bills (Cash) | ||||||

9

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 2 w/ Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 10% |

0

- 10% |

0

- 10% |

0

- 10% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Municipal Bond Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Duration Bond | |

| 25%

Equity 75% Fixed |

0

- 20% |

0

- 10% |

30

- 50% |

0

- 20% |

0

- 20% |

5

- 25% |

| Investment Strategy: Global Balanced- A global balanced model with a higher emphasis on income for a conservative investor that seeks long term

growth through achieving a balance between income and capital growth globally. This investment strategy is most appropriate for investors with an investment time horizon of 3 to 5 years.

Investment Objective: The investment

objective for this Model has a primary emphasis on income with some capital growth. This Model is classified to have low volatility. It is most suitable for an investor that is comfortable with minimal fluctuations in their portfolio, and

the possibility of larger declines in value, in order to grow their portfolio over time. One of the primary reasons municipal bonds are considered separately from other types of bonds is their special ability to provide tax-exempt income. Interest

paid by the issuer (i.e., the municipality, state or local government) to bond holders is often exempt from all federal taxes, as well as state or local taxes depending on the state in which the issuer is located, subject to certain

restrictions. Therefore, for taxable accounts, it can be a tax advantage to invest in municipal bonds in lieu of core fixed income investments.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 2 has 75% of the assets in fixed income or cash and 25% in equities. Therefore, of all of the Eligible Portfolios, this portfolio provides a slightly more aggressive investment risk than Model

1. Benchmark: 18% Russell 1000 (U.S. Equity)/ 7%

MSCI EAFE (International Equity)/ 60% BC Municipal Bond (U.S. Fixed Income) /15% 90-Day T-Bills (Cash) | ||||||

10

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 3 w/ Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 15% |

0

- 15% |

0

- 10% |

0

- 10% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Municipal Bond Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Term Bond | |

| 40%

Equity 60% Fixed |

0

- 20% |

0

- 10% |

25

- 45% |

0

- 15% |

0

- 20% |

0

- 20% |

| Investment Strategy: Global Balanced- A global balanced

model utilizing equities, fixed income, and cash seeking some growth and moderate level of income for a moderate investor that seeks long term growth through achieving a balance between income and capital growth globally. This investment

strategy is most appropriate for investors with an investment time horizon of 3 to 5 years. Investment Objective: The investment objective for this Model has a primary emphasis on capital growth and income. This Model is

classified to have medium volatility. It is most suitable for an investor that is comfortable with fluctuations in their portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time. One of the primary

reasons municipal bonds are considered separately from other types of bonds is their special ability to provide tax-exempt income. Interest paid by the issuer (i.e., the municipality, state or local government) to bond holders is often exempt from

all federal taxes, as well as state or local taxes depending on the state in which the issuer is located, subject to certain restrictions. Therefore, for taxable accounts, it can be a tax advantage to invest in municipal bonds in lieu of

core fixed income investments. Investment

Risk: Fixed income is historically considered less risky than equities. Model 3 has 60% of the assets in fixed income or cash and 40% in equities. Therefore, of all of the Eligible Portfolios, this portfolio provides

a more aggressive investment risk than Models 1 and 2 and less aggressive than Model 4. Benchmark: 28% Russell 3000 (U.S. Equity) / 12% MSCI EAFE (International Equity)/ 50% BC Municipal Bond (U.S. Fixed Income)/10% 90-Day T-Bills (Cash)

| ||||||

11

| Eligible Portfolio |

Target Allocations | |||||

| U.S. Equity | ||||||

| Select UMA Model 4 w/ Municipal Bonds |

U.S. Large Cap Value Equity |

U.S. Large Cap Growth Equity |

U.S. Mid Cap Value Equity |

U.S. Mid Cap Growth Equity |

U.S. Small Cap Value Equity |

U.S. Small Cap Growth Equity |

| 0

- 20% |

0

- 20% |

0

- 15% |

0

- 15% |

0

- 15% |

0

- 15% | |

| Composition |

International Equity |

U.S. Fixed Income |

International Fixed Income |

Cash | ||

| Developed International Equity |

Emerging Markets Equity |

U.S. Municipal Bond Fixed Income |

U.S. High Yield Fixed Income |

International Fixed Income |

Cash/U.S. Short Term Bond | |

| 50%

Equity 50% Fixed |

0

- 20% |

0

- 15% |

25

- 45% |

0

- 15% |

0

- 20% |

0

- 15% |

| Investment Strategy: Global Balanced- A global balanced model utilizing equities, fixed income, and cash seeking a moderate level of growth and

income for a moderate investor that seeks long term growth through achieving a balance between income and capital growth globally. This investment strategy is most appropriate for investors with an investment time horizon of 5 to 7

years. Investment

Objective: The investment objective for this Model has a primary emphasis on capital growth with some focus on income. This Model is classified to have medium volatility. It is most suitable for an investor that is

comfortable with fluctuations in their portfolio, and the possibility of larger declines in value, in order to grow their portfolio over time. One of the primary reasons municipal bonds are considered separately from other types of bonds

is their special ability to provide tax-exempt income. Interest paid by the issuer (i.e., the municipality, state or local government) to bond holders is often exempt from all federal taxes, as well as state or local taxes depending on the state in

which the issuer is located, subject to certain restrictions. Therefore, for taxable accounts, it can be a tax advantage to invest in municipal bonds in lieu of core fixed income investments.

Investment Risk: Fixed income is historically

considered less risky than equities. Model 4 has 50% of the assets in fixed income or cash and 50% in equities. Therefore, of all of the Eligible Portfolios, this portfolio provides the most aggressive investment

risk. Benchmark: 35% Russell 3000 (U.S. Equity)/ 15%

MSCI AC World x U.S. (International Equity)/ 50% BC Municipal Bond (U.S. Fixed Income) | ||||||

The Eligible Portfolios are made up of the following asset

classes. Investment Products are then chosen to represent the appropriate asset classes within each Eligible Portfolio. The available Investment Products are mutual funds, exchange traded funds and separately managed

accounts.

Asset Classes (listed in order of lowest historical risk to highest historical risk):

U.S. Short Duration Bond- This asset class is generally comprised of securities made up of United States

dollar-denominated Treasuries, government-related securities, and investment grade United States corporate securities. The duration of these bonds is typically between less than 1 year and 5 years.

U.S. Municipal Bond Fixed Income- This asset class is generally comprised of investment grade municipal

bonds.

U.S. Core Fixed Income- An asset class that is generally comprised of securities made up of United States

dollar-denominated Treasuries, government-related securities, and investment grade United States corporate securities.

U.S. High Yield Fixed

Income- An asset class that is generally comprised of fixed income securities that have below investment grade credit ratings and carry higher risks, but generally offer higher yields than investment-grade bonds.

International Fixed Income- An asset class that is generally comprised of securities made up of non-U.S. dollar

denominated Treasuries, international government-related securities, and investment grade international corporate securities.

U.S. Large Cap Value Equity- An asset class that is generally comprised of securities issued by U.S. companies with large

market capitalizations (typically $10 billion or more). These securities have the potential for long-term capital appreciation and are generally considered to be undervalued relative to a major unmanaged stock index based on

price-to-current earnings, book value, asset value, or other factors. In aggregate, the securities within this asset class will generally have below-average price-to-earnings ratios, price-to-book ratios, and three-year earnings growth

figures compared to the average of the U.S. diversified large-cap asset class.

12

U.S. Large Cap Growth Equity- An asset class that is generally comprised of securities issued by U.S. companies with large

market capitalizations (typically $10 billion or more). These securities have the potential for long-term capital appreciation and are generally defined as companies with expected long-term earnings growth rates significantly higher than

the earnings growth rates of the stocks represented in a major unmanaged stock index. In aggregate, the securities within this asset class will generally have above-average price-to-earnings ratios, price-to-book ratios, and three-year earnings

growth figures compared to the average of the U.S. diversified large-cap asset class.

U.S. Mid Cap Value Equity- An asset class that is generally comprised of securities issued by U.S. companies with market capitalizations typically in the $2 - $10 billion range. These securities have the

potential for long-term capital appreciation and are generally considered to be undervalued relative to a major unmanaged stock index based on price-to-current earnings, book value, asset value, or other factors. In aggregate, the

securities within this asset class will generally have below-average price-to-earnings ratios, price-to-book ratios, and three-year earnings growth figures compared to the average of the U.S. diversified mid-cap asset class.

U.S. Mid Cap Growth Equity- An asset class that is generally comprised of securities issued by U.S. companies with market

capitalizations typically in the $2 - $10 billion range. These securities have the potential for long-term capital appreciation and are generally defined as companies with expected long-term earnings growth rates significantly higher than

the earnings growth rates of the stocks represented in a major unmanaged stock index. In aggregate, the securities within this asset class will generally have above-average price-to-earnings ratios, price-to-book ratios, and three-year earnings

growth figures compared to the average of the U.S. diversified mid-cap asset class.

U.S. Small Cap Value

Equity- An asset class that is generally comprised of securities issued by U.S. companies with market capitalizations typically below $2 - $3 billion. These securities have the potential for long-term capital

appreciation and are generally considered to be undervalued relative to a major unmanaged stock index based on price-to-current earnings, book value, asset value, or other factors. In aggregate, the securities within this asset class will

generally have below-average price-to-earnings ratios, price-to-book ratios, and three-year earnings growth figures compared to the average of the U.S. diversified small-cap asset class.

U.S. Small Cap Growth Equity- An asset class that is generally

comprised of securities issued by U.S. companies with market capitalizations typically below $2 - $3 billion. These securities have the potential for long-term capital appreciation and are generally defined as companies with expected

long-term earnings growth rates significantly higher than the earnings growth rates of the stocks represented in a major unmanaged stock index. In aggregate, the securities within this asset class will generally have above-average price-to-earnings

ratios, price-to-book ratios, and three-year earnings growth figures compared to the average of the U.S. diversified small-cap asset class.

Developed International Equity- An asset class that is generally comprised of securities with primary trading markets

outside of the United States in developed international markets.

Emerging Markets Equity- An asset class that is generally comprised of securities with primary trading markets in developing countries outside of the U. S. that have low standards of democratic governments, free

market economies, industrialization, social programs, and human rights guarantees for its citizens.

The following indices are listed from the lowest historical risk to the

highest historical risk. Risk is defined as the long term historical standard deviation of each asset class, which measures the degree of volatility.

Benchmark Indices (listed in order of lowest risk to highest risk), which represent various asset classes:

90-Day T-Bills- Index that measures returns of three-month Treasury Bills. (Applicable to: Cash)

BC Municipal Bond- This index is representative of the tax-exempt bond market and is made up of investment grade municipal

bonds issued after December 31, 1990, having a remaining maturity of at least one year. (Applicable to: U.S. Fixed Income)

BC Aggregate Bond- This market value-weighted index measures fixed-rate, publicly placed, dollar-denominated, and

non-convertible investment grade debt issues. (Applicable to: U.S. Fixed Income)

Russell 1000- Index

that measures the performance of the large-cap segment of the U.S. equity universe. It is a subset of the Russell 3000® Index and includes approximately 1000 of the largest securities based on a combination of their market cap and current index

membership. The Russell 1000 represents approximately 92% of the U.S. market. The Russell 1000 Index is constructed to provide a comprehensive and unbiased barometer for the large-cap segment and is completely reconstituted annually to ensure new

and growing equities are reflected. (Applicable to: U.S. Equity)

Russell 3000- This

index measures the performance of the largest 3000 U.S. companies representing 98% of the investable U.S. equity market. (Applicable to: U.S. Equity)

13

MSCI All Country World- A free float-adjusted market capitalization weighted index that is designed to measure the equity

market performance of developed markets. As of June 2007 it consisted of the following 23 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland, Italy, Japan,

Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. (Applicable to: International Equity)

MSCI EAFE- The Morgan Stanley Capital International Europe, Australasia and Far East Index is a market-weighted index

composed of companies representative of the market structure of 20 developed market countries in Europe, Australasia and the Far East. (Applicable to: International Equity)

The Eligible Portfolios offered by MSSB are subject to the same risks faced by similar investment options available in the market, including, without limitation, market risk (the

risk of an overall down market), interest rate risk (the risk that rising or declining interest rates will hurt your investment returns), idiosyncratic risk (the risk that an individual asset will hurt your returns), and concentration risk (the risk

that due to concentrations in a certain segment of the market which performs poorly, your returns are lower than the overall market). The Eligible Portfolios may not achieve their respective investment objectives regardless of whether or not you

purchase the Contract.

Can a Contract be purchased by an Individual Retirement Account?

You may purchase a Contract for your IRA, Roth IRA, SEP IRA or Simple IRA (collectively, an "IRA"). You must designate yourself as the Annuitant of the IRA if your

custodian will be listed as the owner. The Contract is held within the IRA for your benefit. If you elect the Spousal Continuation Option (discussed herein), you and your spouse must be Co-Annuitants, and your spouse must be

listed as the sole beneficiary of Your Account.

For Contracts within an IRA, Nationwide makes Guaranteed Lifetime Income

Payments to the IRA unless otherwise directed by the trustee. Any IRA payments made to you are considered an IRA distribution and will be taxed as such. Distributions that you receive from your IRA with respect to the Contract

will generally be treated as ordinary taxable income. You should refer to your IRA disclosure documents and/or Internal Revenue Service Publication 590 for the rules applicable to IRAs and their distributions.

Can the Contract Owner cancel the Contract?

After you purchase and receive the Contract, you have up to 30 days to cancel your Contract. We call this the "Examination Period." In order to cancel your

Contract, you must provide us with the approved cancellation form (which can be obtained from the Service Center) at the Service Center within 30 days after receiving the Contract (or such longer period that your state may require). We

will then terminate your Contract and refund to Your Account the full amount of any Fee we have already assessed.

After the Examination Period has expired, you can cancel your Contract

by:

| · |

advising us and MSSB that you want to terminate the Contract; or |

| · |

liquidating all of the investments in Your Account; or |

| · |

terminating Your Account. |

If you cancel your Contract, before or after the examination period, a 30-day waiting period may be imposed before you can purchase another Contract for Your

Account.

There are other actions or inactions that can cause the Contract to terminate as well (see "Suspension and Termination

Provisions," for more information).

Does the Contract contain any type of spousal

benefit?

Yes. At the time of application, you may elect to add the Spousal Continuation Option to your Contract. The Spousal Continuation Option allows a surviving

spouse to continue to take withdrawals during the Withdrawal Phase and receive payments during the Income Phase, for the duration of his or her lifetime, provided that the conditions outlined in this prospectus are satisfied. In order to

elect the Spousal Continuation Option for Non-Qualified Contracts, you must be the owner of Your Account and list your spouse as Co-Annuitant of the Contract. If Your Account is held by an IRA, the sole beneficiary to the IRA must be your

spouse. There is a maximum Spousal Continuation Option Fee Percentage equal to a rate of 0.30% of the Guaranteed Lifetime Withdrawal Base associated with the Spousal Continuation Option. Currently, the Spousal Continuation

Option Fee Percentage is equal to a rate of 0.20% of the Guaranteed Lifetime Withdrawal Base.

14

Does the Contract contain any kind of Guaranteed Lifetime Withdrawal Base increases?

Yes. During both the Accumulation Phase and the Withdrawal Phase, the Contract contains an anniversary step-up feature, the "Annual Benefit Base Review" where if, on

any Contract Anniversary, Your Account Value exceeds the Guaranteed Lifetime Withdrawal Base, we will automatically increase your Guaranteed Lifetime Withdrawal Base to equal that Your Account

Value. Please see "What is the Guaranteed Lifetime Withdrawal Base and how is it calculated?," for more information.

Your Account may perform well enough that you may not

receive any Guaranteed Lifetime Income Payments from Nationwide under the Contract.

The assets in Your Account must be invested in accordance with one of the

designated Eligible Portfolios. The Eligible Portfolios, together with the limits on the amount you may withdraw annually without reducing your Guaranteed Lifetime Withdrawal Base, are intended to minimize the risk to us that we will be

required to make Guaranteed Lifetime Income Payments to you. Accordingly, the risk against which the Contract protects, i.e., that Your Account Value will be reduced below the Minimum Account Value by withdrawals and/or poor investment performance,

or that you will live beyond the age when Your Account Value is reduced below the Minimum Account Value, is likely to be small. In this case, you will have paid us fees for the life of your Contract and received no payments in

return.

Your investment choices are limited by the Contract.

The Guarantee associated with the Contract is contingent on your investments being allocated to one of the Eligible Portfolios or a Former Eligible Portfolio. The

Eligible Portfolios may be managed in a more conservative fashion than other investments available to you. If you do not purchase the Contract, it is possible that you may invest in other types of investments that experience higher growth

or lower losses, depending on the market, than the Eligible Portfolios experience.

You must remain invested in Your Account at MSSB to

maintain your Contract.

In order to receive any benefits under the Contract, you must maintain Your Account at MSSB and pay the annual advisory fees and other compensation associated with the Select UMA