UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2020

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-33998

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

( | ||||||||||||||

| (Registrant’s telephone number, including area code) | ||||||||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Trading Symbol(s) | ||||||||

| (Title of each class registered) | (Name of each exchange on which registered) | |||||||

Securities registered pursuant to Section 12(g) of the Act:

None

(Title of class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by a check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of February 10, 2021, 38,476,002 shares of the Registrant’s Common Stock were outstanding. As of June 30, 2020 (based upon the closing sale price for such date on the Nasdaq Global Select Market), the aggregate market value of the shares held by non-affiliates of the Registrant was $4,543,867,580 .

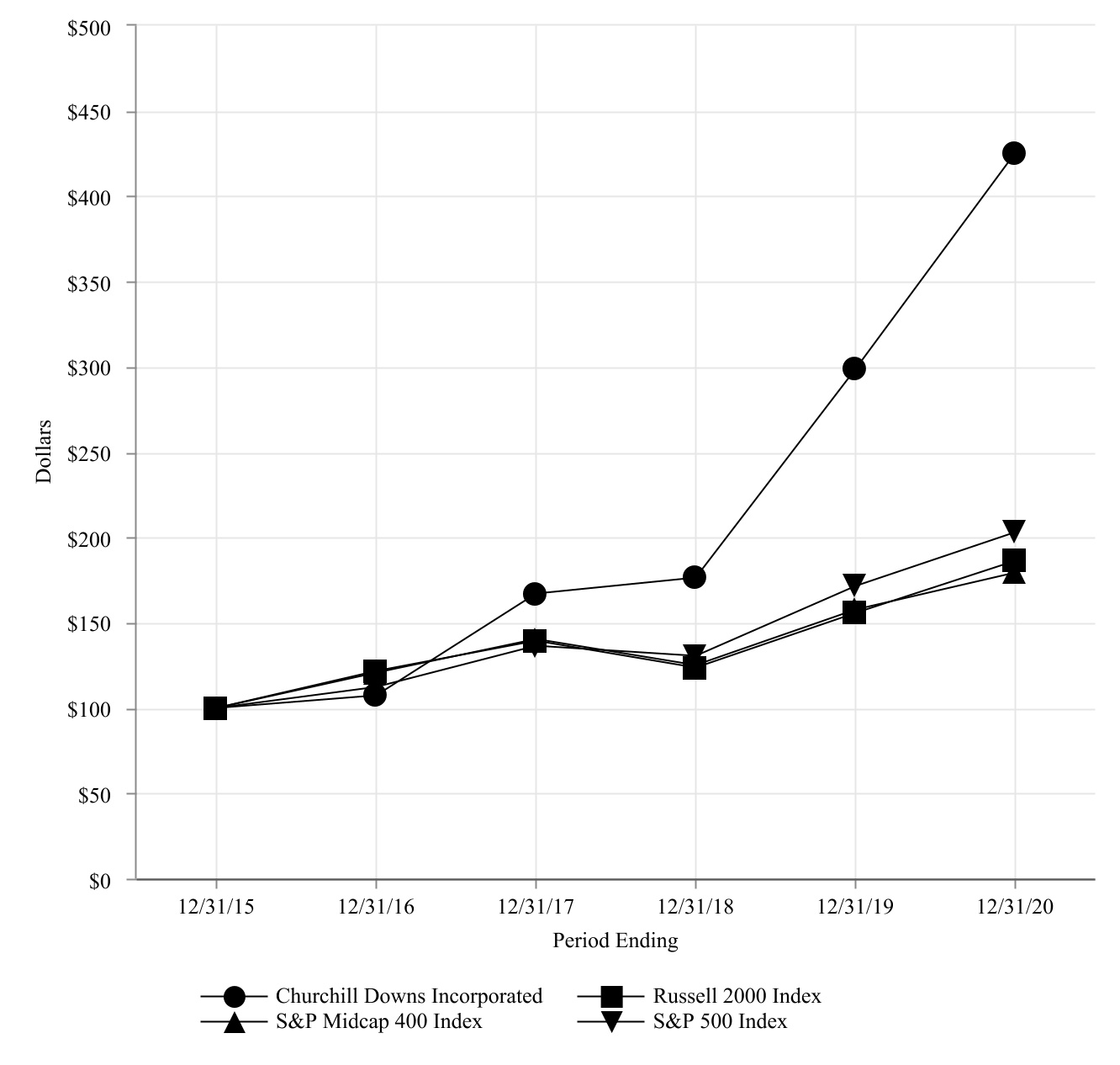

CHURCHILL DOWNS INCORPORATED

INDEX TO ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2020

Principal Accountant Fees and Services | ||||||||

2

Cautionary Statement Regarding Forward-Looking Information

This Annual Report on Form 10-K ("Report") including the information incorporated by reference herein, contains various "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The Private Securities Litigation Reform Act of 1995 (the "Act") provides certain "safe harbor" provisions for forward-looking statements. All forward-looking statements made in this Report are made pursuant to the Act. The reader is cautioned that such forward-looking statements are based on information available at the time and/or management’s good faith belief with respect to future events, and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in the statements. Forward-looking statements speak only as of the date the statement was made. We assume no obligation to update forward-looking information to reflect actual results, changes in assumptions or changes in other factors affecting forward-looking information. Forward-looking statements are typically identified by the use of terms such as "anticipate", "believe", "could", "estimate", "expect", "intend", "may", "might", "plan", "predict", "project", "seek", "should", "will", and similar words, although some forward-looking statements are expressed differently. Although we believe that the expectations reflected in such forward-looking statements are reasonable, we can give no assurance that such expectations will prove to be correct. Important factors that could cause actual results to differ materially from expectations include the factors described in Item 1A. Risk Factors, of this Report.

3

PART I

ITEM 1.BUSINESS

Overview

Churchill Downs Incorporated (the "Company", "we", "us", "our") is an industry-leading racing, online wagering and gaming entertainment company anchored by our iconic flagship event, the Kentucky Derby. We own and operate three pari-mutuel gaming entertainment venues with approximately 3,050 historical racing machines ("HRMs") in Kentucky. We also own and operate TwinSpires, one of the largest and most profitable online wagering platforms for horse racing, sports and iGaming in the U.S and we have seven retail sportsbooks. We are also a leader in brick-and-mortar casino gaming in eight states with approximately 11,000 slot machines and video lottery terminals ("VLTs") and 200 table games. We were organized as a Kentucky corporation in 1928, and our principal executive offices are located in Louisville, Kentucky.

Impact of the COVID-19 Global Pandemic

In March 2020, the World Health Organization declared the COVID-19 outbreak a global pandemic. Considerable uncertainty still surrounds the potential effects of the COVID-19 virus, and the extent of and effectiveness of responses taken on international, national and local levels. Measures taken to limit the impact of COVID-19, including shelter-in-place orders, social distancing measures, travel bans and restrictions, and business and government shutdowns, have resulted and continue to result in significant negative economic impacts in the U.S. and in relation to our business. Although vaccines are now available, their distribution is currently limited and there can be no assurance that these vaccines will be successful in ending the COVID-19 global pandemic. The long-term impact of COVID-19 on the U.S. and world economies and continuing impact on our business remains uncertain, the duration and scope of which cannot currently be predicted.

In response to the measures taken to limit the impact of COVID-19 described above, and for the protection of our employees, customers, and communities, we temporarily suspended operations at our properties in March 2020. In May 2020, we began to reopen our properties with patron restrictions and gaming limitations. One property temporarily suspended operations again in July 2020 and reopened in August 2020, and three properties temporarily suspended operations again in December 2020 and reopened in January 2021.

We implemented a number of initiatives to facilitate social distancing and enhanced cleaning, such as increased frequency of cleaning and sanitizing of all high-touch surfaces, mandatory temperature checks of all guests and team members upon entry and required training for all team members on safety protocols. Certain amenities at our properties have continued to be suspended, including food buffets and valet services, and certain restaurants and food outlets. A summary of the temporary closures and the current status of each property is provided in Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations contained within this Report.

Business Segments

For financial reporting purposes, we aggregate our operating segments into three reportable segments as follows: Churchill Downs, Online Wagering and Gaming. Our operating segments reflect the internal management reporting used by our chief operating decision maker to evaluate results of operations and to assess performance and allocate resources. Financial information about these segments is set forth in Part II, Item 8. Financial Statements and Supplementary Data, Note 21 of notes to consolidated financial statements contained within this Report. Further discussion of financial results by segment is provided in Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations contained within this Report.

We conduct our business through these reportable segments and report net revenue and operating expense associated with these reportable segments in Part II, Item 8. Financial Statements and Supplementary Data, contained within this Report.

Churchill Downs

The Churchill Downs segment includes live and historical pari-mutuel racing related revenue and expenses at Churchill Downs Racetrack and Derby City Gaming.

Churchill Downs Racetrack is the home of the Kentucky Derby and conducts live racing during the year. Derby City Gaming is an HRM facility that operates under the Churchill Downs pari-mutuel racing license at the auxiliary training facility for Churchill Downs Racetrack in Louisville, Kentucky.

Churchill Downs Racetrack and Derby City Gaming earn commissions primarily from pari-mutuel wagering on live races at Churchill Downs and on historical races at Derby City Gaming; simulcast fees earned from other wagering sites; admissions, personal seat licenses, sponsorships, television rights, and other miscellaneous services (collectively "racing event-related services"), as well as food and beverage services.

4

Churchill Downs Racetrack

Churchill Downs Racetrack is located in Louisville, Kentucky and is an internationally known thoroughbred racing operation best known as the home of our iconic flagship event, the Kentucky Derby. We have conducted thoroughbred racing continuously at Churchill Downs Racetrack since 1875. The Kentucky Derby is the longest continuously held annual sporting event in the U.S. and is the first race of the annual series of races for 3-year-old thoroughbreds known as the Triple Crown.

The demographic profile of our guests, global television viewership and long-running nature of this iconic event are attractive to sponsors and corporate partners, especially those with similar luxury and/or marquee brands. The Kentucky Derby Week generated the tenth consecutive year of earnings growth in 2019. The 2020 Kentucky Derby Week results were severely impacted by the rescheduling of the 146th Kentucky Derby from the first weekend in May to the first weekend in September and without spectators due to the COVID-19 global pandemic.

We conducted 70 live race days in 2018, 74 live racing days in 2019 and 65 live race days, including 41 spectator-free live race days, in 2020. In 2021, we anticipate conducting up to 71 live race days with spectators.

Churchill Downs Racetrack is located on 175 acres and has a one-mile dirt track, a 7/8-mile turf track, a stabling area, and a variety of areas, structures, and buildings that provide seating for our patrons. We also own 83 acres of land at our auxiliary training facility, which is five miles from Churchill Downs Racetrack. The facilities at Churchill Downs Racetrack accommodate seating for approximately 59,000 guests. Churchill Downs Racetrack has one of the largest 4K video boards in the world sitting 80 feet above the ground and measuring 171 feet wide by 90 feet tall. This video board provides views of the finish line and the entire race for on-track guests, including those in the infield and guests along the entire front side of the racetrack. The facility also has permanent lighting in order to accommodate night races. We have a saddling paddock, and the stable area has barns sufficient to accommodate 1,400 horses and a 114-room dormitory for backstretch personnel. The Churchill Downs Racetrack facility also includes a simulcast wagering facility.

In April 2020, we completed a state-of-the-art equine medical center and quarantine barns on the backside area of Churchill Downs Racetrack which reinforces our ongoing commitment to equine and jockey safety and supports our long-term international growth strategy.

In 2002, we transferred title of the Churchill Downs Racetrack facility to the City of Louisville, Kentucky and entered into a 30-year lease for the facility as part of the financing of improvements to the Churchill Downs Racetrack facility. We can re-acquire the facility at any time for $1.00 subject to the terms of the lease.

Derby City Gaming

In September 2018, we opened Derby City Gaming, an 85,000 square-foot, state-of-the-art HRM facility at the Churchill Downs Racetrack auxiliary training facility in Louisville, Kentucky. On September 3, 2020, Derby City Gaming opened a new 8,000 square-foot outdoor gaming patio on the south side of the property. Derby City Gaming operates under the Churchill Downs Racetrack pari-mutuel racing license, and has approximately 1,225 HRMs, a simulcast center, and a dining facility.

Online Wagering

The Online Wagering segment includes the revenue and expenses for the TwinSpires Horse Racing and the TwinSpires Sports and Casino businesses. Both businesses are headquartered in Louisville, Kentucky.

TwinSpires Horse Racing

TwinSpires Horse Racing operates the online horse racing wagering business for TwinSpires.com, BetAmerica.com, and other white-label platforms; facilitates high dollar wagering by international customers (through Velocity); and provides the Bloodstock Research Information Services platform for horse race statistical data.

TwinSpires is one of the largest and most profitable legal online horse racing wagering platforms in the U.S. TwinSpires accepts pari-mutuel wagers through advance deposit wagering ("ADW") from customers residing in certain states who establish and fund an account from which these customers may place wagers via telephone, mobile applications or through the Internet. This business is licensed as a multi-jurisdictional simulcasting and interactive wagering hub in the state of Oregon. This business also offers customers streaming video of live horse races, as well as replays, and an assortment of racing and handicapping information.

BetAmerica.com is an online wagering business licensed under TwinSpires and also offers wagering on horse racing throughout the U.S. We also provide technology services to third parties, and we earn commissions from white label ADW products and services. Under these arrangements, we typically provide an ADW platform and related operational services while the third-party typically provides a brand name, marketing and limited customer functions.

5

TwinSpires Sports and Casino

Our TwinSpires Sports and Casino business operates our sports betting and casino iGaming platform in multiple states, including Colorado, Indiana, Michigan, Mississippi, New Jersey, and Pennsylvania. The TwinSpires Sports and Casino business includes the mobile and online sports betting and casino iGaming results and the results of our three retail sportsbooks in Colorado, Indiana and Michigan which utilize a third party's casino license. The results of the two retail sportsbooks at our Mississippi properties, our retail sportsbook at Presque Isle in Pennsylvania and the retail and online BetRivers sportsbook at Rivers Des Plaines, are included in the Gaming segment.

In August 2020, the Company announced the entry into multi-year agreements with GAN Limited ("GAN") and Kambi Group PLC ("Kambi") to provide player account management, casino platform, sports trading and risk management services (collectively, the "GAN / Kambi Platforms"). The Company has transitioned the Mississippi properties to the new Kambi platform and has launched in Michigan with the new GAN / Kambi Platforms. We plan to transition the remaining properties to the new GAN / Kambi Platforms in the first half of 2021.

On September 24, 2020, the Company opened a retail sportsbook at Bronco Billy's Casino in Cripple Creek, Colorado, and on September 25, 2020, the Company opened a retail sportsbook at Island Resort & Casino in Harris, Michigan. The Company launched its mobile and online sportsbook and casino app in Michigan on January 22, 2021 and plans to launch its mobile sportsbook and casino app in Pennsylvania and its mobile sportsbook app in Indiana, subject to regulatory approvals, in the first half of 2021.

On January 5, 2021, the Company announced the transition from the BetAmerica brand to the TwinSpires brand for the Company's sports betting and casino platforms. The Company launched the TwinSpires sportsbook and casino app in Michigan under the TwinSpires brand in January 2021 and the existing Company's sportsbook and casino apps will transition to the TwinSpires brand in the first half of 2021.

Gaming

The Gaming segment includes revenue and expenses for the casino properties and associated racetrack or jai alai facilities which support the casino license. The Gaming segment has approximately 11,000 slot machines and VLTs and 200 table games located in eight states.

The Gaming segment revenue and Adjusted EBITDA includes the following properties:

◦Calder Casino and Racing ("Calder")

◦Fair Grounds Slots, Fair Grounds Race Course, and Video Services, LLC ("VSI") (collectively, "Fair Grounds and VSI")

◦Harlow’s Casino Resort and Spa ("Harlow's")

◦Ocean Downs Casino and Racetrack ("Ocean Downs")

◦Oxford Casino and Hotel ("Oxford")

◦Presque Isle Downs and Casino ("Presque Isle")

◦Riverwalk Casino Hotel ("Riverwalk")

◦Lady Luck Casino Nemacolin ("Lady Luck Nemacolin") management agreement

The Gaming segment Adjusted EBITDA also includes the Adjusted EBITDA related to the Company’s equity investments in the following:

◦61.3% equity investment in Rivers Casino Des Plaines ("Rivers Des Plaines")

◦50% equity investment in Miami Valley Gaming and Racing ("MVG")

The Gaming segment generates revenue and expenses from slot machines, table games, VLTs, video poker, retail sports betting, ancillary food and beverage services, hotel services, commission on pari-mutuel wagering, racing event-related services, and other miscellaneous operations.

Calder

Calder is located on 170 acres of land in Miami Gardens, Florida near Hard Rock Stadium, home of the Miami Dolphins. Calder owns and operates a 106,000 square-foot casino with approximately 1,100 slot machines and two dining facilities. Calder also has a fronton for jai alai performances, and a one-mile dirt track, a 7/8-mile turf track, barns and stabling facilities for thoroughbred horse racing.

In February 2018, Calder was issued a jai alai permit by the Department of Business & Professional Regulation ("DBPR") Division of Pari-Mutuel Wagering ("DPW") in Florida. Calder received a jai alai license in May 2018 and conducted live summer jai alai performances in May and June 2019 for the State of Florida's 2018-2019 fiscal year and in August and September 2019 for the 2019-2020 fiscal year. In 2021, in order to attract better jai alai players and operate efficiently, Calder

6

is planning to conduct jai alai performances in the summer 2021 for the 2020-2021 fiscal year and for the 2021-2022 fiscal year.

In October 2018, the State of Florida DPW issued two separate Final Orders Granting Declaratory Statement in response to two separate Petitions for Declaratory Statements submitted by Calder regarding jai alai. One of the Declaratory Statements was appealed but affirmed by the First District Court of Appeals in September 2019.

There are pending administrative challenges filed by various organizations, including Florida Horsemen's Benevolent and Protective Association, Inc., the Florida Thoroughbred Breeders’ & Owners’ Association, Ocala Breeders’ Sales, and SCF, Inc., related to jai alai and the location of the casino with respect to the racing facility.

We have an agreement with the Stronach Group ("TSG") that expires on April 15, 2021 under which we permit TSG to operate and manage Calder's racetrack and certain other racing and training facilities and to provide live horse racing under Calder's racing permits. During the term of the agreement, TSG pays Calder a racing services fee and is responsible for the direct and indirect costs of maintaining the racing premises, including the training facilities and applicable barns, and TSG receives the associated revenue from the operation.

Fair Grounds and VSI

Fair Grounds Slots and Fair Grounds Race Course are located on 145 acres in New Orleans, Louisiana. Fair Grounds Slots owns and operates a 33,000 square-foot slot facility with approximately 600 slot machines, two concession areas, a bar, a simulcast facility, and other amenities. The Fair Grounds Race Course consists of a one-mile dirt track, a 7/8-mile turf track, a grandstand, and a stabling area. The facility includes clubhouse and grandstand seating for approximately 5,000 guests, a general admissions area, and dining facilities. The stable area consists of barns that can accommodate approximately 1,900 horses and living quarters for approximately 130 people. Fair Grounds Race Course also operates pari-mutuel wagering in thirteen off-track betting facilities ("OTBs") and VSI is the owner and operator of approximately 1,000 video poker machines in twelve OTBs in Louisiana.

Harlow’s

Harlow’s is located on 85 acres of leased land in Greenville, Mississippi. Harlow’s owns and operates a 33,000 square-foot casino with approximately 700 slot machines, 15 table games, a retail sportsbook, a 105-room hotel, a 5,600 square-foot multi-functional event center, and four dining facilities.

Ocean Downs

Ocean Downs is located on 167 acres near Ocean City, Maryland. Ocean Downs owns and operates a 70,000 square-foot casino with approximately 900 VLTs, 18 table games, and three dining facilities. Ocean Downs also conducts approximately 40 live harness racing days each year.

Oxford

Oxford is located on 97 acres in Oxford, Maine. Oxford owns and operates a 27,000 square-foot casino with approximately 950 slot machines, 30 table games, a 100-room hotel, and three dining facilities.

Presque Isle

Presque Isle is located on 270 acres in Erie, Pennsylvania. Presque Isle owns and operates a 153,000 square-foot casino with approximately 1,550 slot machines, 34 table games, a retail sportsbook, a poker room, and four dining facilities. Presque Isle also conducts 100 live thoroughbred racing days each year.

Riverwalk

Riverwalk is located on 22 acres in Vicksburg, Mississippi. Riverwalk owns and operates a 25,000 square-foot casino with approximately 650 slot machines, 15 table games, a retail sportsbook, a five-story 80-room hotel, and two dining facilities.

Lady Luck Nemacolin

On March 8, 2019, the Company assumed the management of Lady Luck Nemacolin, which is located in Farmington, Pennsylvania, approximately one mile from the Nemacolin Woodlands Resort. Lady Luck Nemacolin operates the casino with approximately 600 slot machines, 27 table games, and a dining facility.

Rivers Des Plaines

Rivers Des Plaines is located on 21 acres in Des Plaines, Illinois. Rivers Des Plaines owns and operates a 140,000 square-foot casino with approximately 1,000 slot machines and 69 table games, seven dining and entertainment facilities, and an approximate 5,000 square-foot state-of-the-art BetRivers Sports Bar. In December 2019, Rivers Des Plaines became the first land-based casino in Illinois and, in the third quarter of 2020, completed the expansion of the parking garage. We acquired

7

61.3% equity ownership in Midwest Gaming Holdings, LLC ("Midwest Gaming"), the parent company of Rivers Des Plaines, in March 2019.

Miami Valley Gaming

MVG is located on 120 acres in Lebanon, Ohio. MVG owns and operates a 186,000 square-foot casino with approximately 1,950 VLTs, four dining facilities, a racing simulcast center, and a 5/8-mile harness racetrack. We have a 50% equity investment in MVG.

All Other

We have aggregated the following businesses as well as certain corporate operations, and other immaterial joint ventures in "All Other" to reconcile to consolidated results:

•Oak Grove Racing, Gaming & Hotel ("Oak Grove")

•Newport Racing & Gaming ("Newport")

•Turfway Park

•Arlington International Racecourse ("Arlington")

•United Tote

•Corporate

Oak Grove

Oak Grove is located on 240 acres in Oak Grove, Kentucky, which is approximately one-hour north of Nashville, Tennessee. Oak Grove owns and operates a 5/8-mile harness racing track and completed the first racing meet in October 2019. On September 18, 2020, the Company opened the simulcast and HRM facility with approximately 1,325 HRMs, event center and food and beverage venues. The 128-room hotel opened on October 15, 2020. The 1,200-person grandstand, 3,000-person capacity outdoor amphitheater and stage, a state-of-the-art equestrian center, and a recreational vehicle park at Oak Grove will open in early 2021. Effective as of September 11, 2020, the Company purchased the remaining noncontrolling interest in WKY Development, LLC, a joint venture that owns Oak Grove, from Keeneland Association, Inc. for $3.0 million. The Company no longer reports a noncontrolling interest associated with Oak Grove in the accompanying consolidated financial statements.

Newport

On October 2, 2020, the Company opened Newport, located in Newport, Kentucky, after investing approximately $32.0 million to create a premier entertainment experience as an extension of Turfway Park. Newport has a pari-mutuel simulcast area, a 17,000 square-foot gaming floor with approximately 500 HRMs, and a feature bar.

Turfway Park

Turfway Park is located on 197 acres in Florence, Kentucky. In 2020, the Company approved the final design plans for the HRM and grandstand facility at Turfway Park. The final plans reflect $200 million of project capital, which includes the Turfway Park Acquisition costs and other previously approved capital. The final plans provide for a 155,000 square foot facility including a grandstand, sports bar, food offerings, and up to 1,200 historical racing machines. The Company has spent approximately $58.5 million of the planned project capital as of December 31, 2020 to acquire the business and associated land and to demolish the existing grandstand, prepare the site for the next phase of the development, and install a new Tapeta synthetic racetrack.

Arlington

Arlington is located on 326 acres in Arlington Heights, Illinois. Arlington owns and operates a thoroughbred racing operation with nine OTBs. Arlington has a 1 1/8-mile synthetic track, a one-mile turf track and a 5/8-mile training track. The facility includes a grandstand, clubhouse, and suite seating for 7,500 guests, and dining facilities. The stable area consists of barns that can accommodate 2,200 horses and living quarters for 550 people. On February 23, 2021, we launched a process to sell the 326 acres at Arlington Park. The Company is committed to running Arlington Park's 2021 race dates from April 30, 2021 to September 25, 2021.

8

United Tote

United Tote manufactures and operates pari-mutuel wagering systems for racetracks, OTBs and other pari-mutuel wagering businesses. United Tote provides totalisator services which accumulate wagers, record sales, calculate payoffs and display wagering data to patrons who wager on horse races. United Tote has contracts to provide totalisator services to a number of third-party racetracks, OTBs and other pari-mutuel wagering businesses and also provides these services at our facilities.

Corporate

Corporate includes miscellaneous and other revenue, compensation expense, professional fees and other general and administrative expense not allocated to our segments.

Competition

Overview

We operate in a highly competitive industry with a large number of participants, some of which have financial and other resources that are greater than ours. The industry faces competition from a variety of sources for discretionary consumer spending, including spectator sports, fantasy sports and other entertainment and gaming options. Our brick-and-mortar casinos compete with traditional and Native American casinos, video lottery terminals, state-sponsored lotteries and other forms of legalized gaming in the U.S. and other jurisdictions.

Legalized gambling is currently permitted in various forms in many states and Canada. Other jurisdictions could legalize gambling in the future, and established gaming jurisdictions could award additional gaming licenses or permit the expansion of existing gaming operations. If additional gaming opportunities become available near our racing or gaming operations, such gaming operations could have a material adverse impact on our business.

In May 2018, the United States Supreme Court struck down the 1992 Professional and Amateur Sports Protection Act, which had effectively banned sports wagering in most states. Removal of the ban gives states the authority to authorize sports wagering.

Churchill Downs

In 2020, approximately 28,000 thoroughbred horse races were conducted in the U.S., which was down 24% compared to 2019 due to the impact of almost all of the racetracks across the U.S. being closed for a portion of the year as a result of the COVID-19 global pandemic. Of these races, Churchill Downs Racetrack hosted approximately 650 races, or 2.4% of the total thoroughbred horse races in the U.S. As a content provider, we compete for wagering dollars in the simulcast market with other racetracks conducting races at or near the same times as our races. As a racetrack operator, we also compete for horses with other racetracks running live racing meets at or near the same time as our races. Our ability to compete is substantially dependent on the racing calendar, number of horses racing and purse sizes. In recent years, competition has increased as more states legalize gaming and allow slot machines at racetracks with mandatory purse contributions. Derby City Gaming competes with regional casinos in the area and other forms of legal and illegal gaming.

Online Wagering

TwinSpires Horse Racing

Our TwinSpires Horse Racing business competes with other ADW businesses for both customers and racing content, as well as brick-and-mortar racetracks, casinos, OTBs, and other forms of legal and illegal sports betting.

TwinSpires Sports and Casino

Our TwinSpires Sports and Casino business competes for customers with retail, mobile and online offerings from commercial brick-and-mortar casinos and racetracks. We also compete with daily fantasy sports gaming companies that are expanding into mobile and online sports betting and iGaming, international sports betting businesses looking to expand into the U.S. market, and other forms of legal and illegal sports betting and iGaming operations.

Gaming

Our Gaming properties operate in highly competitive environments and primarily compete for customers with other casinos in the surrounding regional gaming markets. Our Gaming properties compete to a lesser extent with state-sponsored lotteries, off-track wagering, card parlors, online gambling, and other forms of legalized gaming in the U.S.

9

Human Capital

We believe our human capital is material to our operations and core to the long-term success of the Company as an industry-leading racing, online wagering and gaming entertainment company anchored by our iconic flagship event - The Kentucky Derby. Our focus is on attracting innovative and collaborative team members who want to build their skills in a successful and growing set of businesses focused on creating unique experiences for our guests.

Our People

As of December 31, 2020, we had a total of approximately 7,000 team members, of which 4,000 are full-time employees. As of December 31, 2020, the Churchill Downs segment had 1,900 team members, the Online Wagering segment had 240 team members; and the Gaming segment had 2,200 team members. Nearly one-quarter of the Churchill Downs segment team members are full-time employees and nearly all of the Online Wagering and Gaming segment team members are full-time employees. The Company’s corporate staff consists of approximately 180 full-time employees. The number of seasonal employees fluctuates significantly through the course of the year primarily due to the seasonal nature of our businesses. We have the highest level of seasonal team members during the second quarter when we run the Kentucky Derby.

As a result of the COVID-19 global pandemic and the closing of our gaming properties, a significant number of our team members were furloughed beginning in March 2020. The Company provided health, dental, vision and life insurance benefits to furloughed full-time employees through July 31, 2020 and for an additional three months if a full-time employee was re-furloughed as a result of a subsequent property closure period or business capacity limitations. As of December 31, 2020, approximately 500 full-time employees were covered by 16 collective bargaining agreements. We have experienced no material interruptions of operations due to disputes with our team members.

Diversity and Inclusion

We believe that a diverse workforce fosters innovation and cultivates a high performance culture that leverages the unique perspectives of every team member to profitably grow our businesses. The Company’s Board of Directors’ and executive management team is diverse based on gender and race and also have diverse experiences that individually and collectively create a high-performance culture focused on executing our strategic priorities to effectively and efficiently protect and grow our businesses.

We believe diversity and inclusion helps the Company attract the best talent to grow our businesses and enables our businesses to attract and delight customers and consumers. The Kentucky Derby is a pillar of our community that provides the opportunity for our team members and the community to raise significant funding for charities that support important aspects of our broader communities including fostering diversity and inclusion, food, shelter, education, and health related non-profits. The Company also provides donations to non-profit organizations that support these initiatives within our communities.

Talent Acquisition, Development and Retention

We invest in attracting, developing and retaining our team members. Our philosophy is to communicate a clear purpose and strategy, set challenging goals, drive accountability, continuously assess, develop, and advance talent, and to embrace a leadership-driven talent strategy. Our Company enables team members to grow in their current roles as well as to have opportunities to build new skills in other parts of the Company. We review talent and succession plans with our Chief Executive Officer and Board of Directors periodically throughout the year. The process focuses on accelerating talent development, strengthening succession pipelines, and advancing diversity in gender, race and experience for our most critical roles.

Compensation, Benefits, Safety and Wellness

We strive to offer market competitive salaries and wages for our team members and we offer comprehensive health and retirement benefits to eligible employees. Our core health and welfare benefits are supplemented with specific programs to manage or improve common health conditions and to provide a variety of voluntary benefits and paid time away from work programs. We also provide a number of innovative programs designed to promote physical, emotional and financial well-being. Our commitment to the safety of our employees, customers, and community remains a top priority and we have safety programs at all of our properties to facilitate identification and implementation of safety practices. Refer to our discussion above under "Overview", for additional information on actions we have taken to facilitate social distancing and enhanced cleaning in order to protect our employees, customers, and communities as a result of the COVID-19 global pandemic.

Governmental Regulations and Potential Legislative Changes

We are subject to various federal, state, local, and international laws and regulations that affect our businesses. The ownership, operation and management of our Churchill Downs, Online Wagering, and Gaming segments, as well as our other operations, are subject to regulation under the laws and regulations of each of the jurisdictions in which we operate. The ownership, operation and management of our businesses and properties are also subject to legislative actions at both the federal and state level.

10

Churchill Downs Regulations

Horse racing is a highly regulated industry. In the U.S., individual states control the operations of racetracks located within their respective jurisdictions with the intent of, among other things, protecting the public from unfair and illegal gambling practices, generating tax revenue, licensing racetracks and operators and preventing organized crime from being involved in the industry. Although the specific form may vary, states that regulate horse racing generally do so through a horse racing commission or other gambling regulatory authority. In general, regulatory authorities perform background checks on all racetrack owners prior to granting the necessary operating licenses. Horse owners, trainers, jockeys, drivers, stewards, judges, and backstretch personnel are also subject to licensing by governmental authorities. State regulation of horse races extends to virtually every aspect of racing and usually extends to details such as the presence and placement of specific race officials, including timers, placing judges, starters, and patrol judges.

The total number of days on which each racetrack conducts live racing fluctuates annually according to each calendar year and the determination of applicable regulatory authorities.

In the U.S., interstate pari-mutuel wagering on horse racing is subject to the Interstate Horseracing Act of 1978, as amended in 2000 ("IHA"). Through the IHA, racetracks can commingle wagers from different racetracks and wagering facilities and broadcast horse racing events to other licensed establishments.

Kentucky

In Kentucky, horse racing tracks and HRM facilities are subject to the licensing and regulation of the Kentucky Horse Racing Commission ("KHRC"), which is responsible for overseeing horse racing and regulating the state equine industry and overseeing the annual licensing and operations of HRMs in Kentucky. Licenses to conduct live thoroughbred and standardbred racing meets, to participate in simulcasting, and to accept advance deposit wagers from Kentucky residents are approved annually by the KHRC based upon applications submitted by the racetracks in Kentucky.

Derby City Gaming is subject to extensive state and local laws and is subject to licensing and regulatory control by the KHRC. Changes in Kentucky laws or regulations may limit or otherwise materially affect the types of HRMs that may be conducted and such changes, if enacted, could have an adverse impact on our Kentucky HRM operations. The failure to comply with the rules and regulations of the KHRC could have a material adverse impact on our business.

TwinSpires Regulations and Potential Legislative Changes

TwinSpires is licensed in Oregon under a multi-jurisdictional simulcasting and interactive wagering totalisator hub license issued by the Oregon Racing Commission and in accordance with Oregon law and the IHA. We also hold advance deposit wagering licenses in certain other states where required. Changes in the form of new legislation or regulatory activity at the state or federal level could adversely impact our mobile and online ADW business.

Sports Betting and iGaming Regulations and Potential Legislative Changes

Federal

In May 2018, the United States Supreme Court struck down the 1992 Professional and Amateur Sports Protection Act, which had effectively banned sports wagering in most states. Removal of the ban gives states the authority to authorize sports wagering. States have begun authorizing sports betting, which we believe will have a positive impact on our business.

In January 2019, the Department of Justice’s Office of Legal Counsel ("DJOLC") issued a revised legal opinion regarding the scope of the Interstate Wire Act of 1961 (the "Wire Act"). Under the 2019 revised opinion, the DJOLC stated that the Wire Act applied to all forms of gaming that crosses state lines, including online gambling and online lottery. The new opinion overturned a DJOLC opinion from 2011 which stated the Wire Act applied only to sports betting. In June 2019, a federal district court judge in New Hampshire ruled that the Wire Act applies only to gambling activities on sporting events and does not prohibit other forms of gambling conducted over the internet, including online casino gaming and in January 2021, the U.S. Court of Appeals for the First Circuit affirmed this decision.

Gaming Regulations and Potential Legislative Changes

Casino laws are generally designed to protect casino consumers and the viability and integrity of the casino industry. Casino laws may also be designed to protect and maximize state and local revenue derived through taxes and licensing fees imposed on casino industry participants as well as to enhance economic development and tourism. To accomplish these public policy goals, casino laws establish procedures to ensure that participants in the casino industry meet certain standards of character and fitness. Casino laws also require casino industry participants to:

•Ensure that unsuitable individuals and organizations have no role in casino operations,

•Establish procedures designed to prevent cheating and fraudulent practices,

11

•Establish and maintain responsible accounting practices and procedures,

•Maintain effective controls over financial practices, including establishment of minimum procedures for internal fiscal affairs and the safeguarding of assets and revenue,

•Maintain systems for reliable record keeping,

•File periodic reports with casino regulators,

•Ensure that contracts and financial transactions are commercially reasonable, reflect fair market value and are arms-length transactions,

•Establish programs to promote responsible gambling and inform patrons of the availability of help for problem gambling, and

•Enforce minimum age requirements.

Typically, a state regulatory environment is established by statute and administered by a regulatory agency with broad discretion to regulate the affairs of owners, managers and persons with financial interests in casino operations. Among other things, casino authorities in the various jurisdictions in which we operate:

•Adopt rules and regulations under the implementing statutes,

•Interpret and enforce casino laws,

•Impose disciplinary sanctions for violations, including fines and penalties,

•Review the character and fitness of participants in casino operations and make determinations regarding suitability or qualification for licensure,

•Grant licenses for participation in casino operations,

•Collect and review reports and information submitted by participants in casino operations,

•Review and approve transactions, such as acquisitions or change-of-control transactions of casino industry participants, securities offerings and debt transactions engaged in by such participants, and

•Establish and collect fees and taxes.

Any change in the laws or regulations of a casino jurisdiction could have a material adverse impact on our casino operations.

Licensing and Suitability Determinations

Gaming laws require us, each of our subsidiaries engaged in casino operations, certain of our directors, officers and employees, and in some cases, certain of our shareholders, to obtain licenses from casino authorities. Licenses typically require a determination that the applicant qualifies or is suitable to hold the license. Gaming authorities have very broad discretion in determining whether an applicant qualifies for licensing or should be deemed suitable. Criteria used in determining whether to grant a license to conduct casino operations, while varying between jurisdictions, generally include consideration of factors such as the good character, honesty and integrity of the applicant; the financial stability, integrity and responsibility of the applicant, including whether the operation is adequately capitalized in the state and exhibits the ability to maintain adequate insurance levels; the quality of the applicant’s casino facilities; the amount of revenue to be derived by the applicable state from the operation of the applicant’s casino; the applicant’s practices with respect to minority hiring and training; and the effect on competition and general impact on the community.

In evaluating individual applicants, casino authorities consider the individual’s business experience and reputation for good character, the individual’s criminal history and the character of those with whom the individual associates.

Many casino jurisdictions limit the number of licenses granted to operate casinos within the state and some states limit the number of licenses granted to any one casino operator. Licenses under casino laws are generally not transferable without approval. Licenses in most of the jurisdictions in which we conduct casino operations are granted for limited durations and require renewal from time to time. There can be no assurance that any of our licenses will be renewed. The failure to renew any of our licenses could have a material adverse impact on our casino operations.

Casino authorities may investigate any subsidiary engaged in casino operations and may investigate any individual who has a material relationship to or material involvement with any of these entities to determine whether such individual is suitable or should be licensed as a business associate of a casino licensee. Our officers, directors and certain key employees must file applications with the casino authorities and may be required to be licensed, qualify or be found suitable in many jurisdictions. Gaming authorities may deny an application for licensing for any cause that they deem reasonable. Qualification and suitability determinations require submission of detailed personal and financial information followed by a thorough investigation. The

12

applicant must pay all the costs of the investigation. Changes in licensed positions must be reported to casino authorities. Casino authorities have the ability to deny a license, qualification or finding of suitability and have jurisdiction to disapprove a change in a corporate position.

If one or more casino authorities were to find that an officer, director or key employee fails to qualify or is unsuitable for licensing or unsuitable to continue having a relationship with us, we would be required to sever all relationships with such person. Casino authorities may also require us to terminate the employment of any person who refuses to file appropriate applications.

In many jurisdictions, certain of our shareholders may be required to undergo a suitability investigation similar to that described above. Many jurisdictions require any person who acquires beneficial ownership of more than a certain percentage of our voting securities, typically 5%, to report the acquisition to casino authorities, and casino authorities may require such holders to apply for qualification or a finding of suitability. Most casino authorities, however, allow an "institutional investor" to apply for a waiver. An "institutional investor" is generally defined as an investor acquiring and holding voting securities in the ordinary course of business as an institutional investor, and not for the purpose of causing, directly or indirectly, the election of a member of our board of directors, any change in our corporate charter, bylaws, management, policies or operations, or those of any of our casino affiliates, or the taking of any other action which casino authorities find to be inconsistent with holding our voting securities for investment purposes only. Even if a waiver is granted, an institutional investor generally may not take any action inconsistent with their status when the waiver was granted without once again becoming subject to the foregoing reporting and application obligations.

Any person who fails or refuses to apply for a finding of suitability or a license within the prescribed period after being advised it is required by casino authorities may be denied a license or found unsuitable, as applicable. Any shareholder found unsuitable or denied a license and who holds, directly or indirectly, any beneficial ownership of our voting securities beyond such period of time as may be prescribed by the applicable casino authorities may be guilty of a criminal offense. We may be subject to disciplinary action if, after we receive notice that a person is unsuitable to be a shareholder or to have any other relationship with us or any of our subsidiaries, we:

(i) pay that person any dividend or interest upon our voting securities,

(ii) allow that person to exercise, directly or indirectly, any voting right conferred through securities held by that person,

(iii) pay remuneration in any form to that person for services rendered or otherwise, or

(iv) fail to pursue all lawful efforts to require such unsuitable person to relinquish voting securities including, if necessary, the immediate purchase of said voting securities for cash at fair market value.

Violations of Gaming Laws

If we violate applicable casino laws, our casino licenses could be limited, conditioned, suspended or revoked by casino authorities, and we and any other persons involved could be subject to substantial fines. A supervisor or conservator can be appointed by casino authorities to operate our casino properties, or in some jurisdictions, take title to our casino assets in the jurisdiction, and under certain circumstances, income generated during such appointment could be forfeited to the applicable state or states. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions. As a result, violations by us of applicable casino laws could have a material adverse impact on our casino operations.

Some casino jurisdictions prohibit certain types of political activity by a casino licensee, officers, directors and key employees. A violation of such a prohibition may subject the offender to criminal and/or disciplinary action.

Reporting and Record-keeping Requirements

We are required periodically to submit detailed financial and operating reports and furnish any other information that casino authorities may require. Under federal law, we are required to record and submit detailed reports of currency transactions involving greater than $10,000 at our casinos and racetracks as well as any suspicious activity that may occur at such facilities. Failure to comply with these requirements could result in fines or cessation of operations. We are required to maintain a current stock ledger that may be examined by casino authorities at any time. If any securities are held in trust by an agent or by a nominee, the record holder may be required to disclose the identity of the beneficial owner to casino authorities. A failure to make such disclosure may be grounds for finding the record holder unsuitable. Gaming authorities may require certificates for our securities to bear a legend indicating that the securities are subject to specified casino laws.

Review and Approval of Transactions

Substantially all material loans, leases, sales of securities and similar financing transactions must be reported to and in some cases approved by casino authorities. We may not make a public offering of securities without the prior approval of certain

13

casino authorities. Changes in control through merger, consolidation, stock or asset acquisitions, management or consulting agreements, or otherwise are subject to receipt of prior approval of casino authorities. Entities seeking to acquire control of us or one of our subsidiaries must satisfy casino authorities with respect to a variety of stringent standards prior to assuming control. Gaming authorities may also require controlling shareholders, officers, directors and other persons having a material relationship or involvement with the entity proposing to acquire control, to be investigated and licensed as part of the approval process relating to the transaction.

License Fees and Gaming Taxes

We pay substantial license fees and taxes in many jurisdictions in connection with our casino operations which are computed in various ways depending on the type of gambling or activity involved. Depending upon the particular fee or tax involved, these fees and taxes are payable with varying frequency. License fees and taxes are based upon such factors as a percentage of the casino revenue received; the number of gambling devices and table games operated; or a one-time fee payable upon the initial receipt of license and fees in connection with the renewal of license. In some jurisdictions, casino tax rates are graduated such that the tax rates increase as casino revenue increases. Tax rates are subject to change, sometimes with little notice, and such changes could have a material adverse impact on our casino operations.

Operational Requirements

In most jurisdictions, we are subject to certain requirements and restrictions on how we must conduct our casino operations. In certain states, we are required to give preference to local suppliers and include minority and women-owned businesses and organized labor in construction projects to the maximum extent practicable. We may be required to give employment preference to minorities, women and in-state residents in certain jurisdictions. Our ability to conduct certain types of games, introduce new games or move existing games within our facilities may be restricted or subject to regulatory review and approval. Some of our operations are subject to restrictions on the number of gaming positions we may have, and the maximum wagers allowed to be placed by our customers.

Specific State Gaming Regulations and Potential Legislative Changes

Florida

The ownership and operation of casino gaming facilities in the State of Florida is subject to extensive state and local regulation, primarily by the DBPR, within the executive branch of Florida’s state government. The DBPR is charged with the regulation of Florida’s pari-mutuel, card room and slot gaming industries, as well as collecting and safeguarding associated revenue due to the state. The DBPR has been designated by the Florida legislature as the state compliance agency with the authority to carry out the state’s oversight responsibilities in accordance with the provisions outlined in the compact between the Seminole Tribe of Florida and the State of Florida. Changes in Florida laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Florida gaming operation. The laws and regulations of Florida are based on policies of maintaining the health, welfare and safety of the general public and protecting the gaming industry from elements of organized crime, illegal gambling activities and other harmful elements, as well as protecting the public from illegal and unscrupulous gaming to ensure the fair play of devices. The failure to comply with the rules and regulations of the DBPR could have a material adverse impact on our business.

In Florida, licenses to conduct live thoroughbred racing and jai alai, and to participate in simulcast wagering are approved by the DPW, which is responsible for overseeing the network of state offices located at every pari-mutuel wagering facility, as well as issuing the permits necessary to operate a pari-mutuel wagering facility. The DPW also issues annual licenses for thoroughbred, standardbred, and quarter horse races, as well as jai alai, but does not approve the specific live race days.

Illinois

The ownership and operation of casino gaming facilities in the State of Illinois is subject to extensive state and local regulation and is subject to licensing and regulatory control by the Illinois Gaming Board (the "IGB"). The IGB assures the integrity of gambling and gaming in Illinois through regulatory oversight of riverboat and casino gaming, video gaming and sports wagering in Illinois. Changes in Illinois laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Illinois gaming operations. The failure to comply with the rules and regulations of the IGB could have a material adverse impact on our business.

On June 30, 2020, legislation was signed into law by the Governor of Illinois that provides financial relief to the gaming industry. The legislation amends the existing law to allow the lower privilege tax on table games for existing casinos effective as of July 1, 2020 instead of when a newly authorized casino begins operations. The legislation also provides cash flow relief for existing casinos by extending the payment deadline for new gaming positions from July 1, 2020 to July 1, 2021 and extends the payment period and waives interest for reconciliation payments related to the new gaming positions. The legislation delays the payment deadline for the initial sports wagering license from July 1, 2020 to July 1, 2021 and also establishes a lower

14

privilege tax schedule for a new casino in the Chicago area, which has been authorized but not yet opened. We believe the legislation will have a positive impact on our business operations.

Louisiana

The manufacturing, distribution, servicing and operation of video draw poker devices in Louisiana are subject to the Louisiana Video Draw Poker Devices Control Law and the rules and regulations promulgated thereunder. The manufacturing, distribution, servicing and operation of video poker devices and slot machines are governed by the Louisiana Gaming Control Board (the "Louisiana Board") which oversees all licensing for all forms of legalized gaming in Louisiana. The Video Gaming Division and the Slots Gaming Division of the Gaming Enforcement Section of the Office of the State Police within the Department of Public Safety and Corrections performs the video poker and slots gaming investigative functions for the Louisiana Board. The laws and regulations of Louisiana are based on policies of maintaining the health, welfare and safety of the general public and protecting the gaming industry from elements of organized crime, illegal gambling activities and other harmful elements, as well as protecting the public from illegal and unscrupulous gaming to ensure the fair play of devices. The Louisiana Board also regulates slot machine gaming at racetrack facilities pursuant to the Louisiana Pari-Mutuel Live Racing Facility Economic Redevelopment and Gaming Control Act. Changes in Louisiana laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Louisiana gaming operations. LSRC also issues licenses required for Fair Grounds to operate slot machines at the racetrack and video poker devices at their OTBs. The failure to comply with the rules and regulations of the Louisiana Board or the LSRC could have a material adverse impact on our business.

In Louisiana, licenses to conduct live thoroughbred and quarter horse racing and to participate in simulcast wagering are approved by the Louisiana State Racing Commission ("LSRC"). The LSRC is responsible for overseeing the awarding of licenses for the conduct of live racing meets, the conduct of thoroughbred and quarter horse racing, the types of wagering that may be offered by pari-mutuel facilities and the disposition of revenue generated from wagering. Off-track wagering is also regulated by the LSRC. Louisiana law requires live thoroughbred racing at a licensed racetrack for at least 80 days over a 20-week period each year to maintain the license and to conduct slot operations.

Louisiana law requires live quarter horse racing to be conducted at the racetrack with the addition of the slot machines at Fair Grounds. We conducted quarter horse racing at Fair Grounds for 10 days in each of 2018 and 2019. In 2020, we obtained approval from the LSRC to move the 10 days of quarter horse racing to Evangeline Downs. We expect to conduct quarter horse racing for 10 days in 2021.

Effective July 15, 2020, legislation was signed into law by the Governor of Louisiana that exempts the tax on promotional play up to $5.0 million for casinos. We believe the legislation will have a positive impact on our business operations.

Maine

The ownership and operation of casino gaming facilities in the State of Maine is subject to extensive state and local regulation and is subject to licensing and regulatory control by the Maine Gambling Control Board (the "MGCB"). The laws, regulations and supervisory procedures of the MGCB are based upon declarations of public policy that are concerned with, among other things: (1) the regulation, supervision and general control over casinos and the ownership and operation of slot machines and table games; (2) the investigation of complaints made regarding casinos; (3) the establishment and maintenance of responsible accounting practices and procedures; (4) the maintenance of effective controls over the financial practices of licensees, including the establishment of minimum procedures for internal fiscal affairs and the safeguarding of assets and revenue and providing for reliable record keeping; and (5) the prevention of cheating and fraudulent practices. The regulations are subject to amendment and interpretation by the MGCB. Changes in Maine laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Maine gaming operations. The failure to comply with the rules and regulations of the MGCB could have a material adverse impact on our business.

Maryland

The ownership and operation of casino gaming facilities in the State of Maryland is subject to extensive state and local regulation and is subject to licensing and regulatory control by the Maryland Lottery and Gaming Control Commission (“MLGCC”), with staff assistance from the Maryland Lottery and Gaming Control Agency (“MLGCA”). The MLGCA oversees all internal controls, auditing, security, surveillance, background investigations, licensing and accounting procedures for each casino in the State of Maryland, including Ocean Downs. Changes in Maryland laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Maryland gaming operations. The failure to comply with the rules and regulations of the MLGCC could have a material adverse impact on our business.

15

Mississippi

The ownership and operation of casino gaming facilities in the State of Mississippi is subject to extensive state and local regulation, including the Mississippi Gaming Commission (the "Mississippi Commission"). The laws, regulations and supervisory procedures of the Mississippi Commission are based upon declarations of public policy that are concerned with, among other things: (1) the prevention of unsavory or unsuitable persons from having direct or indirect involvement with gaming at any time or in any capacity; (2) the establishment and maintenance of responsible accounting practices and procedures; (3) the maintenance of effective controls over the financial practices of licensees, including the establishment of minimum procedures for internal fiscal affairs and the safeguarding of assets and revenue, providing for reliable record keeping and requiring the filing of periodic reports with the Mississippi Commission; (4) the prevention of cheating and fraudulent practices; (5) providing a source of state and local revenue through taxation and licensing fees; and (6) ensuring that gaming licensees, to the extent practicable, employ Mississippi residents. The regulations are subject to amendment and interpretation by the Mississippi Commission. Changes in Mississippi laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Mississippi gaming operations. The failure to comply with the rules and regulations of the Mississippi Commission could have a material adverse impact on our business.

Ohio

In 2012, the Governor of Ohio signed an Executive Order which authorized the Ohio Lottery Commission (the "OLC") to amend and adopt rules necessary to implement a video lottery program at Ohio’s seven horse racing facilities. The ownership and operation of VLT facilities in the State of Ohio is subject to extensive state and local regulation. The laws, regulations and supervisory procedures of the OLC include: (1) regulating the licensing of video lottery sales agents, key gaming employees and VLT manufacturers; (2) collecting and disbursing VLT revenue; and (3) maintaining compliance in regulatory matters. Changes in Ohio laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Ohio gaming operations. The failure to comply with the rules and regulations of the OLC could have a material adverse impact on our business.

Pennsylvania

The ownership and operation of casino gaming facilities in the Commonwealth of Pennsylvania are subject to extensive state and local regulation and are subject to licensing and regulatory control by the Pennsylvania Gaming Control Board ("PGCB") as well as other agencies. The PGCB regulates, oversees and enforces all matters related to gaming activity in Pennsylvania, including, without limitation, operations, internal controls, accounting procedures, auditing, security, surveillance, licensing, background investigations and compliance of each casino in the state. Changes in Pennsylvania laws or regulations may limit or otherwise materially affect the types of gaming that may be conducted and such changes, if enacted, could have an adverse impact on our Pennsylvania gaming operations. The failure to comply with the rules and regulations of the PGCB could have a material adverse impact on our business.

In Pennsylvania, licenses to conduct live thoroughbred racing, to participate in simulcast wagering and to accept advance deposit wagers from Pennsylvania residents are approved by the Pennsylvania State Horse Racing Commission (“PSHRC”). The PSHRC regulates the operations of horse racing, the conduct of pari-mutuel wagering and the promotion and marketing of horse racing in Pennsylvania. As a Category 1 slot machine licensee, Presque Isle is required to conduct live racing on at least 100 days each calendar year. The PSHRC approved Presque Isle for 100 live race days in 2021.

Other Specific State Regulations and Potential Legislative Changes

Kentucky

On February 22, 2021, the Governor of the Commonwealth of Kentucky signed into law Senate Bill 120 which creates a statutory definition of pari-mutuel wagering that includes historical horse racing approved by the KHRC and addresses the Supreme Court of Kentucky's opinion in The Kentucky Horse Racing Commission, et al v. The Family Trust Foundation of Kentucky, Inc. regarding the KHRC's historical racing regulations and the validity of operating HRMs pursuant to a license issued by KHRC. For more information, please refer to Item 3, Legal Proceedings. Following this action, we do not believe that any further rulings in this litigation will impact our ability to operate HRM facilities in Kentucky.

Illinois

In Illinois, licenses to conduct live thoroughbred racing and to participate in simulcast wagering are approved by the Illinois Racing Board ("IRB"). The IRB appointed Arlington the dark host track for 60 simulcast host days in 2019 and 2020. Arlington was also awarded 155 live host days in 2019 and 2020.

16

Environmental Matters

We are subject to various federal, state and local environmental laws and regulations that govern activities that may have adverse environmental effects, such as discharges to air and water, as well as the management and disposal of solid, animal and hazardous wastes and exposure to hazardous materials. These laws and regulations, which are complex and subject to change, include the United States Environmental Protection Agency ("EPA") and state laws and regulations that address the impacts of manure and wastewater generated by Concentrated Animal Feeding Operations ("CAFO") on water quality, including, but not limited to, storm and sanitary water discharges. CAFO and other water discharge regulations include permit requirements and water quality discharge standards. Enforcement of these regulations has been receiving increased governmental attention. Compliance with these and other environmental laws can, in some circumstances, require significant capital expenditures. We may incur future costs under existing and new laws and regulations pertaining to storm water and wastewater management at our racetracks. Violations can result in significant penalties and, in some instances, interruption or cessation of operations.

In the ordinary course of our business, we may receive notices from regulatory agencies regarding our compliance with CAFO regulations that may require remediation at our facilities. On December 6, 2013, we received a notice from the EPA regarding alleged CAFO non-compliance at Fair Grounds Race Course. On October 21, 2019, we reached an agreement in principle, subject to final agreement and regulatory and court approval. If approved, the agreement will include a $2.8 million penalty, which is included in accrued expense and other current liabilities in our accompanying consolidated balance sheet as of December 31, 2020.

We also are subject to laws and regulations that create liability and cleanup responsibility for releases of hazardous substances into the environment. Under certain of these laws and regulations, a current or previous owner or operator of property may be liable for the costs of remediating hazardous substances or petroleum products on its property, without regard to whether the owner or operator knew of, or caused, the presence of the contaminants, and regardless of whether the practices that resulted in the contamination were legal at the time the contamination occurred. The presence of, or failure to remediate properly, such substances may materially adversely affect the ability to sell or rent such property or to borrow funds using such property as collateral. The owner of a property may be subject to claims by third parties based on damages and costs resulting from environmental contamination emanating from the property.

Marks and Internet Properties

We hold numerous state and federal service mark registrations on specific names and designs in various categories including the entertainment business, apparel, paper goods, printed matter, housewares and glass. We license the use of these service marks and derive revenue from such license agreements.

Available Information

Our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, proxy statements and other Securities and Exchange Commission ("SEC") filings, and any amendments to those reports and any other filings that we file with or furnish to the SEC under the Securities Exchange Act of 1934 are made available free of charge on our website (www.churchilldownsincorporated.com) as soon as reasonably practicable after we electronically file the materials with the SEC and are also available at the SEC’s website at www.sec.gov.

17

ITEM 1A.RISK FACTORS

Our operations and financial results are subject to various risks and uncertainties, including those described below, that could adversely affect our business, financial condition, results of operations, cash flows, and the trading price of our common stock.

Economic and External Risks

The current novel coronavirus (COVID-19) global pandemic has adversely affected, and could continue to adversely affect our business, financial condition and financial results. Other major public health issues could adversely affect our business, financial condition and financial results in the future

In March 2020, the World Health Organization declared the COVID-19 outbreak a global pandemic. Considerable uncertainty still surrounds the potential effects of the COVID-19 virus, and the extent of and effectiveness of responses taken on international, national and local levels. Measures taken to limit the impact of COVID-19, including shelter-in-place orders, social distancing measures, travel bans and restrictions, and business and government shutdowns, have resulted and some continue to result in significant negative economic impacts in the U.S. and in relation to our business. The long-term impact of COVID-19 on the U.S. and world economies and continued impact on our business remains uncertain, the duration and scope of which cannot currently be predicted.

Our operating results depend, in large part, on revenues derived from customers visiting our casinos and racetracks. In March 2020, we announced the temporary suspension of operations of all of our wholly-owned gaming properties, certain wholly-owned racing operations, and the two casino properties related to our equity investments. Starting in mid-February, U.S. and international sporting events were cancelled, which reduced our sports betting options for our customers. Horse racing content for wagering on TwinSpires also decreased, although handle increased as our customers wagered more on the content that was available. Although vaccines are now available, distribution is currently limited and there can be no assurance that these vaccines will be successful in ending the COVID-19 global pandemic.

In May 2020, we began to reopen our properties with patron restrictions and gaming limitations. One property temporarily suspended operations again in July 2020 after reopening and reopened in August 2020, and three properties suspended operations in December 2020 and reopened in January 2021. We implemented a number of initiatives to facilitate social distancing and enhanced cleaning, such as increased frequency of cleaning and sanitizing of all high-touch surfaces, mandatory temperature checks of all guests and team members upon entry and required training for all team members on safety protocols. Certain amenities at our properties continue to be suspended, including food buffets and valet services, and certain restaurants and food outlets. We cannot predict how soon our casino and racetrack properties will be able to return to customary operations. Our ability to return to our customary operations will depend, in part, on the actions of a number of governmental bodies over which we have no control. Once all restrictions are lifted, it is unclear how quickly customers will return to our casinos and racetracks, which may be a function of continued concerns over safety and decreased consumer spending due to economic conditions, including job losses.

Certain non-furloughed employees continue to work remotely. An extended period of remote work arrangements could strain business continuity plans, introduce operational risk (including but not limited to cybersecurity risks) and may impair our ability to manage our business. We also outsource certain business activities to third parties. As a result, we rely upon the successful implementation and execution of the business continuity planning of such entities in the current environment. While we seek to monitor the business continuity activities of these third parties, successful implementation and execution of their business continuity strategies are largely outside our control. If one or more of the third parties to whom we outsource certain business activities experience operational failures or business disruption as a result of the impacts from the spread of COVID-19, or claim that they cannot perform, it may have negative effects on our business and financial condition.

The Company reduced planned maintenance and project capital expenditures for 2020 as a result of the temporary property and operations closures and prioritized capital investments based on the highest near-term return opportunities in order to maintain financial flexibility.