As filed with the Securities and Exchange Commission on June 10, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact name of Registrant as specified in its charter) |

The Netherlands |

| 3823 |

| N/A |

(State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

Robert-Bosch-Str. 32-36,

72250

Freudenstadt, Germany

Tel: +49 7441 538 0

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

Tel: 1 (800) 221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications

sent to agent for service, should be sent to:

Axel Wittmann

George Hacket

Junghofstrasse 14

60311 Frankfurt, Germany

+49 (69) 7199 1528

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act.

† | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities, nor a solicitation of an offer to buy these securities, in any jurisdiction where the offer, solicitation, or sale is not permitted.

PRELIMINARY — SUBJECT TO COMPLETION, DATED JUNE 10, 2024

SCHMID Group N.V.

Up to 36,010,890 Ordinary Shares

Up to 21,000,000 Ordinary Shares Issuable Upon Exercise of Warrants

Up to 9,750,000 Warrants

This prospectus relates to the issuance from time to time by us of an aggregate of up to 21,000,000 of our ordinary shares with a nominal value €0.01 per share (“Ordinary Shares”), including (i) up to 9,750,000 Ordinary Shares issuable upon conversion of 9,750,000 warrants (the “Private Warrants”) originally issued by Pegasus Digital Mobility Acquisition Corp. (“Pegasus”) in a private placement transaction in connection with the initial public offering of Pegasus, and converted into warrants to purchase Ordinary Shares at the closing of the Business Combination (as defined below) at an exercise price of $11.50 per Ordinary Share, and (ii) up to 11,250,000 Ordinary Shares that are issuable upon the exercise of 11,250,000 warrants (the “Public Warrants” and, together with the Private Warrants, the “Warrants”) originally issued to public shareholders of Pegasus in its IPO, and converted into warrants to purchase Ordinary Shares at the closing of the Business Combination at an exercise price of $11.50 per Ordinary Share.

This prospectus also relates to offer and resale from time to time by the selling securityholders or their permitted transferees and certain other investors (collectively, the “selling securityholders”) of (i) 57,010,890 Ordinary Shares including (a) up to 35,888,325 of our Ordinary Shares issued to certain selling securityholders in connection with the Business Combination (including 5,000,000 non-vested earn-out shares), (b) up to 122,565 Ordinary Shares to be issued to certain selling securityholders under non-redemption and investment agreements that were entered into before the Business Combination, and (c) up to 21,000,000 of our Ordinary Shares to be issued upon the exercise of our Warrants, and (ii) up to 9,750,000 Private Warrants.

This prospectus provides you with a general description of such securities and the general manner in which the selling securityholders may offer or sell the securities. More specific terms of any securities that the selling securityholders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

All of the Ordinary Shares and Private Warrants offered by the selling securityholders pursuant to this prospectus will be sold by the selling securityholders for their respective accounts. We will not receive any proceeds from the sale of Ordinary Shares or Private Warrants by the selling securityholders or the issuance of Ordinary Shares by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the Warrants. However, we will pay the expenses, other than any underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

We are registering the securities described above for resale pursuant to, among other things, the selling securityholders’ registration rights under certain agreements between us and the selling securityholders. Our registration of the securities covered by this prospectus does not mean that either we or the selling securityholders will issue, offer or sell, as applicable, any of the securities. The selling securityholders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the selling securityholders may sell the Ordinary Shares or Private Warrants in the section entitled “Plan of Distribution.”

We will pay certain expenses associated with the registration of the securities covered by this prospectus, as described in the section entitled “Plan of Distribution.”

Our Ordinary Shares and Public Warrants are listed on The Nasdaq Global Select Market (“Nasdaq”) under the symbols “SHMD” and “SHMD.W,” respectively. On June 6, 2024, the closing sale price as reported on Nasdaq of our Ordinary Shares was $4.22 per share and of our Public Warrants was $0.46 per warrant.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus and any amendments or supplements carefully before you make your investment decision.

We are an “emerging growth company” as that term is defined in the Jumpstart Our Business Startups Act of 2012 and, as such, are subject to reduced public company reporting requirements.

Our principal executive offices are located at Robert-Bosch-Str. 32-36, 72250 Freudenstadt, Germany.

Investing in our securities involves a high degree of risk. Before buying any securities, you should carefully read the discussion of material risks of investing in our securities in “Risk Factors” of this prospectus.

We are a “foreign private issuer” as defined in the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are exempt from certain rules under the Exchange Act that impose certain disclosure obligations and procedural requirements for proxy solicitations under Section 14 of the Exchange Act. In addition, our officers, directors and principal shareholders are exempt from the reporting and “short-swing” profit recovery provisions under Section 16 of the Exchange Act. Moreover, we are not required to file periodic reports and financial statements with the U.S. Securities and Exchange Commission as frequently or as promptly as U.S. companies whose securities are registered under the Exchange Act. Additionally, the NASDAQ rules allow foreign private issuers to follow home country practices in lieu of certain of the NASDAQ’s corporate governance rules. As a result, our shareholders may not have the same protections afforded to shareholders of companies that are subject to all the NASDAQ corporate governance requirements.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2024

TABLE OF CONTENTS

i

You should rely only on the information contained in this prospectus, any amendment or supplement to this prospectus or any free writing prospectus prepared by us or on our behalf. Neither we, nor the selling securityholders, have authorized any other person to provide you with different or additional information. Neither we, nor the selling securityholders, take responsibility for, nor can we provide assurance as to the reliability of, any other information that others may provide. The selling securityholders are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this prospectus is accurate only as of the date of this prospectus or such other date stated in this prospectus, and our business, financial condition, results of operations and/or prospects may have changed since those dates.

Except as otherwise set forth in this prospectus, neither we nor the selling securityholders have taken any action to permit a public offering of these securities outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of these securities and the distribution of this prospectus outside the United States.

ii

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form F-1 that we filed with the United States Securities and Exchange Commission (the “SEC”) using a “shelf” registration process. Under this shelf registration process, the selling securityholders may, from time to time, offer and sell any combination of the securities described in this prospectus in one or more offerings.

We will not receive any proceeds from the sale of Ordinary Shares or Private Warrants to be offered by the selling securityholders pursuant to this prospectus, but we will receive proceeds from Warrants or Specified Options exercised in the event that such Warrants or Specified Options are exercised for cash. We will pay the expenses, other than underwriting discounts and commissions, if any, associated with the sale of our Ordinary Shares and Private Warrants pursuant to this prospectus. To the extent required, we and the selling securityholders, as applicable, will deliver a prospectus supplement with this prospectus to update the information contained in this prospectus. The prospectus supplement may also add, update or change information included in this prospectus. You should read both this prospectus and any applicable prospectus supplement, together with additional information described below under the caption “Where You Can Find More Information.” We have not, and the selling securityholders have not authorized anyone to provide you with information different from that contained in this prospectus. The information contained in this prospectus is accurate only as of the date on the front cover of the prospectus. You should not assume that the information contained in this prospectus is accurate as of any other date.

No offer of these securities will be made in any jurisdiction where the offer is not permitted.

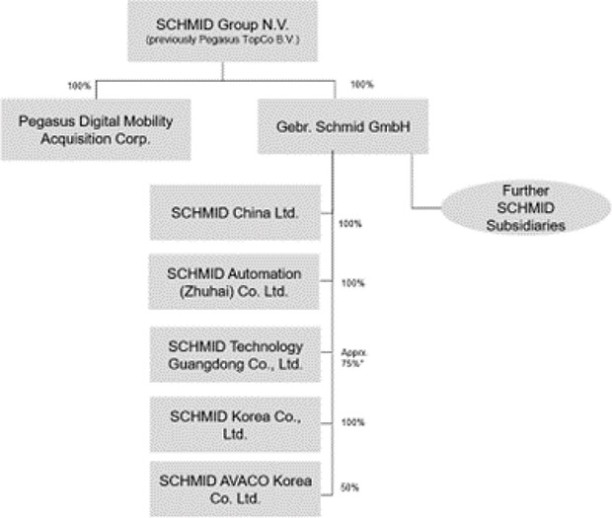

On April 30, 2024 (the “Closing Date”), SCHMID Group N.V. (“SCHMID”, “Schmid Group” or the “Company”), closed the previously announced business combination (the “Business Combination”) pursuant to the Business Combination Agreement, dated as of May 31, 2023, as amended by a first amendment agreement dated September 26, 2023 (the “Business Combination Agreement”) and a second amendment agreement dated January 29, 2024, by and among Pegasus Digital Mobility Acquisition Corp., a Cayman Islands exempted company (“Pegasus”), Gebr. Schmid GmbH, a German limited liability company, Pegasus TopCo B.V., a Dutch private liability company (which was converted into a Dutch public limited liability company, and renamed SCHMID Group N.V., prior to the closing of the Business Combination) (“TopCo” when referring to the company prior to the Business Combination and “SCHMID” following the Closing), and Pegasus MergerSub Corp., a Cayman Islands limited liability company and wholly-owned subsidiary of the Schmid Group (“Merger Sub”). References made to Schmid Group pertaining to occurrences predating the Business Combination closing, refer to Gebr. Schmid GmbH, which was the predecessor to SCHMID Group N.V. at the top of the group’s structure.

On the Closing Date, several transactions were completed pursuant to the Business Combination Agreement, including:

| ● | SCHMID issued 99 new ordinary shares to its shareholder Pegasus; |

| ● | The shareholders of Gebr. Schmid GmbH, Anette Schmid, Christian Schmid and a Community of Heirs (the“Schmid Shareholders”) purchased all 100 SCHMID shares from Pegasus at nominal value; |

| ● | The Schmid Shareholders subscribed to 28,725,000 SCHMID shares and an additional 5,000,000 earn-out shares at €0.01 nominal value and in consideration contributed 100% of the Gebr. Schmid GmbH shares by transferring them to SCHMID; |

| ● | SCHMID changed its legal form from a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) to a Dutch public limited liability company (naamloze vennootschap) and was renamed SCHMID Group N.V.; |

| ● | SCHMID issued shares in exchange for each Pegasus Class A and B share outstanding (a total of 1,461,537 reigstered shares for Pegasus Class A shares and 5,625,000 former Pegasus Class B shares which were converted to registered Pegasus Class A shares prior to the Business Combination), and issued 1,406,361 shares to XJ Harbour HK Limited (“XJ Harbour”); |

| ● | SCHMID issued further shares in the amount of 756,964 shares to Pegasus Digital Mobility Sponsor LLC, the sponsor of Pegasus (the “Sponsor”), as payment for approximately USD 8.6 million in liabilities which SCHMID assumed before the closing by a debt assumption agreement between Pegasus, the Sponsor and SCHMID; and |

| ● | Pegasus merged with Merger Sub, with Pegasus as the surviving company and, after giving effect to the merger becoming a direct, wholly-owned subsidiary of SCHMID. |

1

Prior to the Business Combination, SCHMID Group N.V. did not conduct any material activities other than those incident to its formation and the matters contemplated by the Business Combination Agreement, such as the making of certain required securities law filings, and the establishment of Merger Sub. Upon the closing of the Business Combination, SCHMID Group N.V. became the direct parent of Schmid, a Germany-based technology provider with extensive expertise in high-tech manufacturing processes.

Unless the context indicates otherwise, the terms “SCHMID,” the “Company,” “we,” “us” and “our” refer to SCHMID Group N.V. (f/k/a Pegasus TopCo B.V.) after conversion into a Dutch public limited liability company and Pegasus TopCo B.V. prior to the conversion into a Dutch public liability company.

CONVENTIONS WHICH APPLY TO THIS PROSPECTUS

In this prospectus, unless otherwise specified or the context otherwise requires:

| ● | “$,” “USD” and “U.S. dollar” each refer to the United States dollar; and |

| ● | “€,” “EUR” and “Euro” each refer to the Euro. |

The exchange rate used for conversion between U.S. dollars and Euros is based on the ECB euro reference exchange rate published by the European Central Bank.

IMPORTANT INFORMATION ABOUT U.S. GAAP, IFRS AND NON-IFRS FINANCIAL MEASURES

SCHMID’s audited financial statements included in this prospectus are prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). This prospectus includes certain references to financial measures that were not prepared in accordance with IFRS, including Adjusted EBITDA. The presentation of this non-IFRS information is not meant to be considered in isolation or as a substitute for SCHMID’s consolidated financial results prepared in accordance with IFRS.

IFRS differs in certain material respects from U.S. generally accepted accounting principles (“US GAAP”) and, as such, e.GO’s financial statements are not comparable to the financial statements of U.S. companies prepared in accordance with U.S. GAAP.

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

The SCHMID name, logos and other trademarks and service marks of SCHMID appearing in this prospectus are the property of SCHMID. Solely for convenience, some of the trademarks, service marks, logos and trade names referred to in this prospectus are presented without the ® and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names. This prospectus contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks, copyrights or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

MARKET, INDUSTRY AND OTHER DATA

Unless otherwise indicated, information contained in this prospectus concerning our industry and the markets in which we operate, including our general expectations and market position, market opportunity and market size estimates, is based on information from independent industry analysts, third-party sources and management estimates. Management estimates are derived from publicly available information released by independent industry analysts and third-party sources, as well as data from our internal research, and are based on assumptions made by us based on such data and our knowledge of such industry and market, which we believe to be reasonable. In addition, while we believe the market opportunity information included in this prospectus is reliable and is based on reasonable assumptions, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the heading “Risk Factors.”

2

FREQUENTLY USED TERMS AND BASIS OF PRESENTATION

Unless otherwise stated in this registration statement on Form F-1 or the context otherwise requires, references to:

“Annual Report” means the annual report of the Company on Form 20-F.

“Board” means the board of directors of the Company.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated May 31, 2023, by and among TopCo, Merger Sub, Pegasus and Gebr. Schmid GmbH, as amended by that First Amendment to Business Combination Agreement dated as of September 26, 2023 and as amended by the Second Amendment to Business Combination Agreement dated as of January 29, 2024, and as it may be further amended from time to time.

“Ordinary Shares” means the shares of the Company.

“Closing Date” means April 30, 2024, the date of the closing of the Business Combination.

“Company” means SCHMID Group N.V.

“Continental” means Continental Stock Transfer & Trust Company, the transfer agent and warrant agent of the Company.

“Earn out shares” means the 5,000,000 shares issued and not yet vested to Anette Schmid and Christian Schmid, transferrable per the terms of the Earn-Out Agreement.

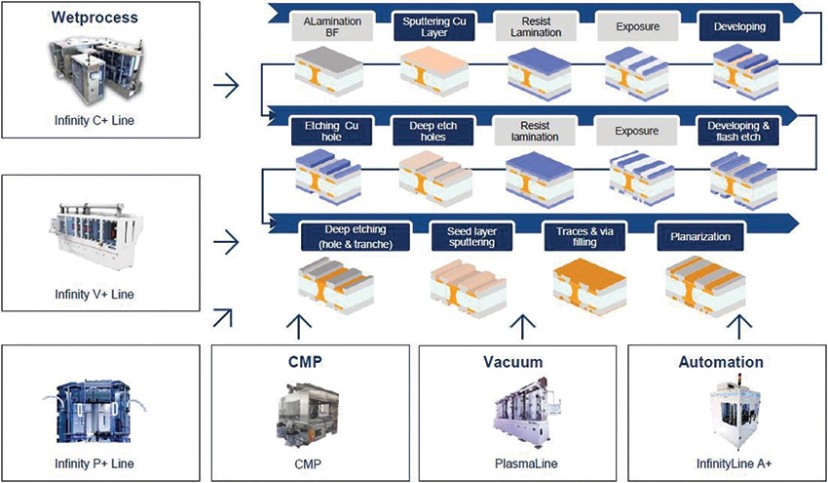

“ET” means embedded traces, a process which we believe the next level technology for high-end PCBs & Substrates.

“EBITDA” means earnings before interest, taxes, depreciation, and amortization.

“EU” means the European Union.

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“FCPA” means U.S. Foreign Corrupt Practices Act.

“GDPR” means the European General Data Protection Regulation.

“IAS” means the International Accounting Standard.

“IASB” means the International Accounting Standards Board. “IBR” means the incremental borrowing rate.

“IFRS” means the International Financial Reporting Standards as issued by the IASB.

“mSAP” means modified semi additive processes.

“MergerSub” means Pegasus MergerSub Corp., a Cayman Islands exempted company.

“NASDAQ” means the Nasdaq Stock Exchange in New York.

“NYSE” means the New York Stock Exchange.

“OEMs” means original equipment manufacturers.

“Pegasus” means Pegasus Digital Mobility Acquisition Corp., a Cayman Islands exempted company.

“Private Placement Warrants” means the 9,750,000 warrants originally issued in the private placement that occurred concurrently with the closing of Pegasus’s IPO.

3

“Public Warrants” means the 11,250,000 public warrants, each of which is a warrant to purchase one Pegasus Class A Ordinary Share at a price of $11.50 per share, subject to adjustment in accordance with the Warrant Agreement.

“Warrants” means collectively the Pegasus Public Warrants and the Pegasus Private Placement Warrants.

“PCB” means printed circuit board.

“R&D” Means research and development.

“RMB” means the Chinese Renminbi.

“SAP” means semi-additive processes.

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002.

“Schmid” or “SCHMID” means SCHMID Group N.V.

“SEC” means the United States Securities and Exchange Commission.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“Sponsor” means Pegasus Digital Mobility Sponsor LLC., a Cayman Islands limited liability company, which is the sponsor of Pegasus.

“TopCo” means Pegasus TopCo B.V., a Dutch private liability company (besloten vennootschap met beperkte aansprakelijkheid) which has been converted and renamed to SCHMID Group N.V. on April 30, 2024.

“XJ Harbour” means XJ Harbour HK Limited.

4

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains or may contain forward-looking statements that involve significant risks and uncertainties.

Statements contained in this prospectus, other than statements of historical fact, including statements about SCHMID’s expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts are forward-looking statements. Words or phrases such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” “will” and “would,” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. Examples of forward-looking statements in this prospectus include, but are not limited to, statements regarding SCHMID’s operations, cash flows, financial position and dividend policy.

Forward-looking statements are subject to risks and uncertainties. The risks and uncertainties include, but are not limited to:

| ● | our future financial condition and operating results; |

| ● | our ability to remain in compliance with financial covenants under our financing arrangements; |

| ● | our ability to extend, renew or refinance our existing debt; |

| ● | our liquidity and losses from operations and projected cash flows and related impact on our ability to continue as a going concern; |

| ● | our growth, expansion and acquisition prospects and strategies, the success of such strategies, and the benefits we believe can be derived from such strategies; |

| ● | our ability to effectively manage our inventory and inventory reserves; |

| ● | impairments of our goodwill or other intangible assets; |

| ● | changes in consumer spending patterns and overall levels of consumer spending; |

| ● | our ability to further upgrade our information technology systems and infrastructure, including our accounting processes and functions; |

| ● | our ability to continue to remedy weaknesses in our internal controls; |

| ● | costs as a result of operating as a public company; |

| ● | our assumptions regarding interest rates and inflation; |

| ● | changes affecting currency exchange rates; |

| ● | continuing business disruptions arising from the on-going war in Ukraine and in the aftermath of the coronavirus pandemic; |

| ● | our financial condition and ability to obtain financing in the future to implement our business strategy and fund capital expenditures, acquisitions and other general corporate activities; |

| ● | estimated future capital expenditures needed to preserve our capital base; |

| ● | changes in general economic conditions in the Federal Republic of Germany (“Germany”), and the European Union, the United States of America and the People’s Republic of China, including changes in the unemployment rate, the level of energy and consumer prices, wage levels, etc.; |

| ● | the market acceptance of our products by our customers and our ability to adapt to technological changes; |

5

| ● | the growth in the market for Embedded Traces technology in our products; |

| ● | changes in our competitive environment and in our competition level; |

| ● | the occurrence of accidents, terrorist attacks, natural disasters, fires, environmental damage, or systemic delivery failures; |

| ● | our inability to attract and retain qualified personnel, consultants and collaborators; |

| ● | changes in laws and regulations; |

| ● | our expectations relating to dividend payments and forecasts of our ability to make such payments; and |

| ● | other factors discussed in “Risk Factors” in this prospectus. |

Forward-looking statements are subject to known and unknown risks and uncertainties and are based on potentially inaccurate assumptions that could cause actual results to differ materially from those expected or implied by the forward-looking statements.

Actual results could differ materially from those anticipated in forward-looking statements for many reasons, including the factors described under the section titled “Risk Factors” in this prospectus. Accordingly, you should not rely on these forward-looking statements, which speak only as of the date of this prospectus. We undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this prospectus or to reflect the occurrence of unanticipated events. You should, however, review the factors and risks we describe in the reports we will file from time to time with the SEC after the date of this prospectus.

In addition, statements that “Schmid believes” or “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date such statements are made. And while we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information.

These statements are inherently uncertain, and you are cautioned not to unduly rely on these statements.

Although we believe the expectations reflected in the forward-looking statements were reasonable at the time made, we cannot guarantee future results, level of activity, performance or achievements. Moreover, neither SCHMID nor any other person assumes responsibility for the accuracy or completeness of any of these forward-looking statements. You should carefully consider the cautionary statements contained or referred to in this section in connection with the forward-looking statements contained in this prospectus and any subsequent written or oral forward-looking statements that may be issued by SCHMID or persons acting on our behalf. Our actual results, performance or achievements could differ materially from those contemplated, expressed or implied in this registration statement. You should not place undue reliance on these forward-looking statements. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements set forth in this prospectus. Also, these forward-looking statements represent our estimates and assumptions only as of the date such forward-looking statements are made. Except as required by law, we assume no obligation to update any forward-looking statements publicly, whether as a result of new information, future events or otherwise.

6

SUMMARY OF PROSPECTUS

This summary highlights certain information about us, this offering and selected information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in the securities covered by this prospectus. For a more complete understanding of our company and this offering, we encourage you to read and consider carefully the more detailed information in this prospectus, and any related prospectus supplement, including the information set forth in the section titled “Risk Factors” in this prospectus, and any related prospectus supplement in their entirety before making an investment decision. Unless otherwise stated or the context otherwise indicates, references to the “Company”, “we”, “our”, “us”, “SCHMID” or the “SCHMID Group” refer to SCHMID Group N.V., together with its subsidiaries.

Our Company

We are a global supplier of equipment, software and services for various industries such as printed circuit board (“PCB”), substrate manufacturing, photovoltaics, and glass and energy storage with a focus on the highest end of this market in terms of technology and performance. We are a long-established, fifth generation family-controlled business that was founded in 1864 in Freudenstadt, Germany as an iron foundry and has a tradition of being at forefront of technology.

Throughout the almost 160 years of our operations, we have maintained sustainable operations by developing our products following trends on the market. We have been developing machines for the electronic industry since the 1960s, photovoltaic solutions since the early 2000s and energy storage for the last seven years. We focus on a modular product portfolio of machinery to use in the manufacturing of high-end PCB equipment and semiconductor packaging devices which include common flexible circuit fabrication techniques such as subtractive, semi-additive processes (“SAP”) and modified semi additive processes (“mSAP”). We are a global supplier of capital equipment, software and services for the PCB and substrate manufacturing industry. We focus on the highest end of the market in terms of technology and performance. We do not only develop production techniques and build machines ourselves, we are also extensively working with our customers on joint research & development projects for the next generation of electronics and photovoltaics products.

We produce our products in two manufacturing sites, one in Germany and one in China. In addition, we have built up an extensive service and sales network in five centers in the US, Europe, and Asia. In addition to our sale and service centers and two manufacturing sites, in South Korea we also work with our partners in the SCHMID Avaco Korea, Co. Ltd. which we account for using the equity method. We also provide customer service through which we assist our customers with machinery and software upgrades, spare parts, logistics, customer training in multiple languages, on-site management, maintenance contracts and project management.

We have developed and applied for patents for the embedded traces (“ET”), PCB and substrate production processes that allow a significant increase in manufacturing precision as well as enhanced design features while also achieving cost savings compared to traditional processes and reduce the CO2 emissions of the overall production processes. We believe that our ET technology will gain a significant share of the high-end PCB and substrate market as it has substantial advantages in technology capabilities, cost and to reduce emissions, as well as water consumption for production processes (greener production processes). We believe these innovative production processes create a sustainable competitive advantage that helps us contract with new customers and allows us to continue to grow our market share and capitalize on the overall positive market growth trends.

Our customers include large, global original equipment manufacturers (“OEMs”) from the semi-conductor and consumer electronics industry and companies that are part of the supply chain of such global companies.

We have a research and development focused business model. We develop and build innovative machines and systems for wet- & vacuum processing in various industries spanning high-end electronics such as PCB and organic packaging, photovoltaics and special glass applications as well as other high-tech industries. We employ more than 150 scientists, engineers and development personnel to focus on new technologies and processes out of a total of approximately 800 employees (by headcount) globally. As a result, we consistently invest a significant amount in R&D. Our science, engineering and development staff work in close collaboration with our customers to jointly develop high-value solutions. Such collaboration may reduce commercial risk, given that solutions are specifically developed for customers. The remainder of our R&D investment is focused on developing next-generation technologies, often as part of a collaborative process with our customers. In addition, we work with universities and leading research institutes such as the Fraunhofer Institute for Solar Energy Systems.

7

We expect to continue to invest in the future focusing on three primary areas: (i) growth for ET projects, which have higher working capital needs compared to other technologies; (ii) strategic investments in automation solutions, such as the next generation of fully automatic factories; and (iii) software insourcing for semiconductor equipment communication standard (“SECS/GEM”), which can allow for more reliable data exchange and which will allow us to offer our own software as the interface to our customers’ software solutions.

Pegasus TopCo B.V. was incorporated as a Dutch private limited liability corporation (besloten vennootschap met beperkte aansprakelijkheid) on February 7, 2023, and converted to a Dutch public limited liability company (naamloze vennootschap) and renamed SCHMID Group N.V. on April 30, 2024. As part of the Business Combination, the Company changed its legal form to a public limited liability company (naamloze vennootschap). The address of the registered office of the Company is Robert-Bosch-Str. 32-36, 72250 Freudenstadt, Germany, and the telephone number of Schmid Group is +49 7441 538 0.

Recent Developments

Closing of the Business Combination

On April 30, 2024 (the “Closing Date”), we closed our previously announced business combination (the “Business Combination”) pursuant to the Business Combination Agreement, dated as of May 30, 2023, as amended by a first amendment agreement dated September 26, 2023 and a second amendment agreement dated January 29, 2024, by and among Pegasus Digital Mobility Acquisition Corp., a Cayman Islands exempted company (“Pegasus”), Gebr. Schmid GmbH, a German limited liability company, Pegasus TopCo B.V., a Dutch private liability company (which was converted into a Dutch public limited liability company, and renamed SCHMID Group N.V., prior to the closing of the Business Combination) (“TopCo”), and Pegasus MergerSub Corp., a Cayman Islands limited liability company and wholly-owned subsidiary of the Schmid Group (“MergerSub”) (the “Business Combination Agreement”). References made to Schmid Group pertaining to occurrences predating the Business Combination closing, refer to Gebr. Schmid GmbH, which was the predecessor to SCHMID Group N.V. at the top of the group’s structure.

On the Closing Date, several transactions were completed pursuant to the Business Combination Agreement, including:

| ● | TopCo issued 99 new ordinary shares to its shareholder Pegasus; |

| ● | The shareholders of Schmid, Anette Schmid, Christian Schmid and a Community of Heirs (the “Schmid Shareholders”) purchased all 100 TopCo shares from Pegasus at nominal value; |

| ● | The Schmid Shareholders subscribed to 28,725,000 TopCo shares and an additional 5,000,000 earn-out shares at €0.01 nominal value and in consideration contributed 100% of the Gebr. Schmid shares by transferring them to TopCo; |

| ● | TopCo changed its legal form from a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) to a Dutch public limited liability company (naamloze vennootschap) and was renamed SCHMID Group N.V.; |

| ● | The Schmid Group issued shares in exchange for each Pegasus Class A and B share outstanding (a total of 1,461,537 reigstered shares for Pegasus Class A shares and 5,625,000 former Pegasus Class B shares which were converted to registered Pegasus Class A shares prior to the Business Combination), and issued 1,406,361 shares to XJ Harbour HK Limited (“XJ Harbour”); |

| ● | The Schmid Group issued further shares in the amount of 756,964 shares to Pegasus Digital Mobility Sponsor Corp., the sponsor of Pegasus (the “Sponsor”), as payment for approximately USD 8.6 million in liabilities which TopCo assumed before the closing by a debt assumption agreement between Pegasus, the Sponsor and TopCo; and |

| ● | Pegasus merged with Merger Sub, with Pegasus as the surviving company and, after giving effect to the merger, becoming a direct, wholly-owned subsidiary of SCHMID Group. |

Prior to the Business Combination, SCHMID Group N.V. did not conduct any material activities other than those incident to its formation and the matters contemplated by the Business Combination Agreement, such as the making of certain required securities

8

law filings, and the establishment of Merger Sub. Upon the closing of the Business Combination, SCHMID Group N.V. became the direct parent of Schmid, a Germany-based technology provider with extensive expertise in high-tech manufacturing processes.

Ordinary Shares, and warrants to purchase one Ordinary Share at a price of $11.50, subject to adjustment, Public Warrants (“Public Warrants”), began trading on the Nasdaq Global Select Market (“Nasdaq”) under the symbols “SHMD” and “SHMD.W”, respectively, on May 1, 2024.

Implications of Being an Emerging Growth Company and a Foreign Private Issuer

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (“JOBS Act”). As an emerging growth company, we intend to take advantage of exemptions from various reporting requirements that are applicable to most other public companies. The exemptions include, but are not limited to:

| ● | an exemption from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that our independent registered public accounting firm provide an attestation report on the effectiveness of our internal control over financial reporting; |

| ● | reduced disclosure obligations regarding executive compensation; and |

| ● | not being required to hold a nonbinding advisory vote on executive compensation or seek shareholder approval of any golden parachute payments not previously approved. |

We will remain an “emerging growth company” until the earliest to occur of (i) the last day of the fiscal year (a) following the fifth anniversary of the closing of the Business Combination, (b) in which we have total annual gross revenue of at least $1.07 billion or (c) in which we are deemed to be a large accelerated filer, which means the market value of equity securities held by our non-affiliates exceeds $700 million as of the last business day of our prior second fiscal quarter, and (ii) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period.

We are also considered a “foreign private issuer” subject to reporting requirements under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), as a non-U.S. company with foreign private issuer status. As a “foreign private issuer,” we will be subject to different U.S. securities laws than domestic U.S. issuers. The rules governing the information that we must disclose differ from those governing U.S. corporations pursuant to the Exchange Act. This means that, even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| ● | the rules under the Exchange Act prescribing the furnishing and content of proxy statements to shareholders and requirements that the proxy statements conform to Schedule 14A of the proxy rules promulgated under the Exchange Act; |

| ● | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| ● | the sections of the Exchange Act requiring insiders (i.e., officers, directors and holders of more than 10% of our issued and outstanding equity securities) to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; |

| ● | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission (the “SEC”) of quarterly reports on Form 10-Q containing unaudited financial and other specified information, or current reports on Form 8-K, upon the occurrence of specified significant events; and |

| ● | the SEC rules on disclosure of compensation on an individual basis unless individual disclosure is required in our home country (the Netherlands) and is not otherwise publicly disclosed by us. |

We may take advantage of these exemptions until such time as we are no longer a foreign private issuer. We would cease to be a foreign private issuer at such time as more than 50% of our outstanding voting securities are held by U.S. residents and any of the following three circumstances applies: (i) the majority of our executive officers or directors are U.S. citizens or residents, (ii) more than 50% of our assets are located in the United States or (iii) our business is administered principally in the United States.

9

We may choose to take advantage of some but not all of these reduced reporting requirements of which we have taken advantage of in this prospectus. Accordingly, the information contained herein may be different from the information you receive from our competitors that are U.S. domestic filers, or other U.S. domestic public companies in which you have made an investment.

Risk Factors Summary

Our business faces significant risks and uncertainties. You should carefully consider all of the information set forth in this prospectus and in other documents we file with or furnish to the SEC, including the following risk factors, before deciding to invest in or to maintain an investment in our securities. Our business, as well as our reputation, financial condition, results of operations and share price, could be materially adversely affected by any of these risks, as well as other risks and uncertainties not currently known to us or not currently considered material. These risks include, among others, the following:

| ● | SCHMID’s ability to maintain the listing of our securities on the NASDAQ; |

| ● | Our ability to implement business plans, operating models, forecasts, and other expectations and identify and realize additional business opportunities; |

| ● | SCHMID faces intense competition in the markets and industries in which it operates, and Schmid’s competitiveness depends on being successful in new product development and to market its embedded traces technology. |

| ● | The reputation of SCHMID’s brand is an important company asset and is key to SCHMID’s ability to remain a trusted supplier of specialty products, equipment and services. |

| ● | SCHMID’s profitability could suffer if its cost management strategies are unsuccessful, or SCHMID’s competitors develop an advantageous cost structure that SCHMID cannot match. |

| ● | SCHMID’s direct customers and their direct and indirect customers face numerous competitive challenges, which may materially adversely affect their business and as a result SCHMID’s business. |

| ● | SCHMID’s revenue, earnings, and other operating results have fluctuated in the past and may fluctuate in the future due to the nature of its business. |

| ● | Any disruptions to SCHMID’s supply chain, significant increases in material costs, or shortages of critical components, could adversely affect SCHMID’s business and result in increased costs. |

| ● | Most of SCHMID’s revenue is derived from the electronics business which subjects its revenues and profitability to fluctuations and developments in one global area of business. |

| ● | Economic, financial, geopolitical, epidemiological, or other conditions could result in business disruptions which could seriously harm SCHMID’s future revenue and financial condition and increase SCHMID’s costs and expenses. |

| ● | SCHMID’s operations and assets in foreign jurisdictions may be subject to significant political and economic uncertainties. |

| ● | SCHMID’s management has limited experience in operating a public company. |

| ● | SCHMID’s ability to obtain additional capital on commercially reasonable terms may be limited. |

| ● | SCHMID is generally subject to substantial regulation and laws and unfavorable changes to, or its failure to comply with, these regulations and/or laws could substantially harm its business and operating results. |

| ● | Failure of information security and privacy concerns could subject SCHMID to penalties, damage SCHMID’s reputation and brand, and harm SCHMID’s business and results of operations. |

| ● | SCHMID may be unable to successfully execute its growth initiatives, business strategies, or operating plans. |

10

| ● | SCHMID’s know-how and innovations, which it relies on for its current and future business, may not be adequately protected. |

| ● | SCHMID’s patent applications may not be successful, which may have a material adverse effect on SCHMID’s ability to prevent others from commercially exploiting products similar to SCHMID’s products. |

Corporate Information

We were incorporated as a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid) under the name Pegasus TopCo B.V. on February 7, 2023, solely for the purpose of effectuating the Business Combination. Prior to the Business Combination, Pegasus TopCo B.V. did not conduct any material activities other than those incident to its formation and certain matters related to the Business Combination, such as the making of certain required securities law filings.

Our name was changed from Pegasus TopCo B.V. to SCHMID Group N.V. when we converted into a Dutch public limited liability company (naamloze vennootschap) on April 30, 2024, in connection with the closing of the Business Combination.

We are registered in the Commercial Register of the Netherlands Chamber of Commerce (Kamer van Koophandel) under number 89188276. Our official seat (statutaire zetel) is in Amsterdam, the Netherlands and the mailing and business address of our principal executive office is Robert-Bosch-Str. 32-36, 72250 Freudenstadt, Federal Republic of Germany. Our telephone number is Tel: +49 7441 538 0.

We maintain a website at schmid-group.com, where we regularly post copies of our press releases as well as additional information about us.

Our filings with the SEC are available free of charge through the website as soon as reasonably practicable after being electronically filed with or furnished to the SEC. Information contained in our website is not a part of, nor incorporated by reference into, this prospectus or our other filings with the SEC, and should not be relied upon.

All trademarks, service marks and trade names appearing in this prospectus are the property of their respective holders. Use or display by us of other parties’ trademarks, trade dress, or products in this prospectus is not intended to, and does not, imply a relationship with, or endorsements or sponsorship of, us by the trademark or trade dress owners.

11

THE OFFERING

Issuer | SCHMID Group N.V. | |

Ordinary Shares that may be offered and sold from time to time by the Selling Securityholders | We are registering for resale 57,010,890 of our Ordinary ordinary shares consisting of up to (i) 9,750,000 Ordinary Shares issuable upon conversion of our 9,750,000 Private Warrants, (ii) up to 11,250,000 Ordinary Shares issuable upon the exercise of 11,250,000 Public Warrants and (iii) up to 36,010,890 Ordinary Shares held by Selling Shareholders, Permitted Transferees and certain investors. | |

Ordinary Shares outstanding prior to exercise of all Warrants and after the exercise of all Warrants (assuming all Warrants are exercised on a cash-basis) | As of June 10, 2024, we had 42,974,862 Ordinary Shares outstanding and have to issue a further 122,565 shares to three investors which have committed to subscribe for such shares before the Business Combination but have not yet received new Ordinary Shares. The number of Ordinary Shares outstanding prior to this offering excludes the up to 21,000,000 Ordinary Shares which are issuable upon the exercise of the Warrants. | |

Exercise Price of Warrants | Warrants: $11.50 per share, subject to adjustments described therein | |

Redemption | The Warrants are redeemable in certain circumstances. See “Description of Securities” for further discussion. | |

Offering price | The Ordinary Shares offered by this prospectus may be offered and sold at prevailing market prices, privately negotiated prices or such other prices as the Selling Shareholders may determine. See the section titled “Plan of Distribution”. | |

Use of Proceeds | All of the Ordinary Shares offered by the Selling Shareholders pursuant to this prospectus will be sold by the Selling Shareholders for their respective accounts. We will not receive any of the proceeds from such sales. We will receive up to an aggregate of approximately $241.5 million from the exercise of the Warrants, assuming the exercise in full of all of the Warrants for cash. We expect to use the net proceeds from the exercise of the Warrants for general corporate purposes. See “Use of Proceeds.” | |

Transfer restrictions | Pursuant to the Business Combination Agreement and related agreements, certain Selling Shareholders who received Ordinary Shares in connection with the Business Combination agreed not to sell, transfer, pledge or otherwise dispose of such shares for certain periods. See the section titled “Shares Eligible for Future Sale.” |

12

Dividend policy | We have never declared or paid any cash dividends and have no plan to declare or pay any dividends on our Ordinary Shares in the foreseeable future. We currently intend to retain any earnings for future operations and expansion. Under Dutch law, we may only pay dividends and other distributions from our reserves to the extent our shareholders’ equity (eigen vermogen) exceeds the sum of our paid-in and called-up share capital plus the reserves we must maintain under Dutch law or our articles of association (the “Articles of Association”) and (if it concerns a distribution of profits) after adoption of our statutory annual accounts by the general meeting from which it appears that such dividend distribution is allowed. Subject to those restrictions, any future determination to pay dividends or other distributions from our reserves will be at the discretion of our board of directors and will depend upon a number of factors, including our results of operations, financial condition, future prospects, contractual restrictions, restrictions imposed by applicable law and other factors we deem relevant. See the section titled “Dividend Policy.” | |

Market for our Ordinary Shares | Our ordinary shares are listed on Nasdaq under the symbol “SHMD” and our Public Warrants are listed under the symbol “SHMD.W” | |

Risk factors | Investing in our securities involves a high degree of risk. See “Risk Factors” in this prospectus for a description of certain of the risks you should consider before investing in our ordinary shares |

13

SUMMARY CONSOLIDATED HISTORICAL AND OTHER FINANCIAL INFORMATION

Summary Historical Financial Data of Gebr. Schmid GmbH

The following table shows summary historical financial information of SCHMID for the periods and as of the dates indicated. The summary historical financial information of SCHMID as of and for the years ended December 31, 2023, 2022 and 2021 was derived from the audited historical financial statements of SCHMID included elsewhere in this prospectus.

The following summary historical financial information should be read together with the consolidated financial statements and accompanying notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” appearing elsewhere in this prospectus. The summary historical financial information in this section is not intended to replace our consolidated financial statements and the related notes. Our historical results are not necessarily indicative of our future results.

The financial information contained in this section relates to SCHMID, prior to and without giving pro-forma effect to the impact of the Business Combination and, as a result, the results reflected in this section may not be indicative of the results of SCHMID going forward after giving effect to the Business Combination. See the section entitled “Unaudited Pro Forma Condensed Combined Financial Information” included elsewhere in this prospectus.

14

SCHMID — Combined Statements of Profit or Loss and

Other Comprehensive Income (Loss) for the years ended

December 31, 2023, 2022 and 2021

in € thousand |

| Note |

| 2023 |

| 2022 |

| 2021 |

Revenue |

| 7 |

| 90,246 |

| 95,058 |

| 39,481 |

Cost of sales |

| 7 |

| (63,849) |

| (61,721) |

| (30,506) |

Gross profit |

| 26,397 |

| 33,337 |

| 8,975 | ||

Selling |

| 8 |

| (12,577) |

| (11,369) |

| (7,851) |

General administration |

| 9 |

| (12,538) |

| (6,973) |

| (6,298) |

Research and development |

| 10 |

| (5,148) |

| (4,818) |

| (2,733) |

Other income |

| 11 |

| 15,985 |

| 3,375 |

| 1,924 |

Other expenses |

| 12 |

| (2,620) |

| (2,988) |

| (4,779) |

(Impairment) / Reversal on impairment on financial assets |

| 13 |

| 22,696 |

| 3,091 |

| 3,333 |

Operating profit (loss) |

| 32,195 |

| 13,654 |

| (7,427) | ||

Finance income |

|

| 19,685 |

| 5,758 |

| 3,360 | |

Finance expenses |

| (10,091) |

| (17,746) |

| (18,014) | ||

Financial result |

| 14 | 9,594 |

| (11,988) |

| (14,654) | |

Share of profit (loss) in joint ventures |

| 15 |

| (1,057) |

| — |

| — |

Income (loss) before income tax |

| 40,732 |

| 1,667 |

| (22,082) | ||

Income tax benefit (expense) |

| 16 |

| (2,778) |

| 1,924 |

| (5,195) |

Net income (loss) for the period |

| 37,954 |

| 3,591 |

| (27,277) |

15

SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION

The following summary unaudited pro forma condensed combined statement of financial position as of December 31, 2023 (the “Summary Pro Forma Information”) combines the historical statement of financial position of Schmid and the historical balance sheet of Pegasus on a pro forma basis as if the Business Combination and related transactions had been consummated on December 31, 2023. The unaudited pro forma condensed combined statement of profit or loss for the year ended December 31, 2023 combines the historical statement of profit or loss of Schmid and the historical statements of operations of Pegasus for such periods on a pro forma basis as if the Business Combination and related transactions had been consummated on January 1, 2023, the beginning of the earliest period presented.

The unaudited pro forma condensed combined financial information has been presented for illustrative purposes only and is not necessarily indicative of the financial position and results of profit or loss that would have been achieved had the Business Combination and related transactions occurred on the dates indicated. Further, the unaudited pro forma condensed combined financial information may not be useful in predicting the future financial condition and results of profit or loss of the post-combination company. The actual financial position and results of profit or loss may differ significantly from the pro forma amounts reflected herein due to a variety of factors. The unaudited pro forma adjustments represent management’s estimates based on information available as of the date of the unaudited pro forma condensed combined financial information and is subject to change as additional information becomes available and analyses are performed. This information should be read together with Schmid’s and Pegasus’s audited financial statements and related notes, as applicable, and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and other financial information in the prospectus, which are incorporated herein by reference.

16

Summary Unaudited Pro Forma Condensed Combined Financial Information (in Euro thousands, except per share data)

Year Ended | Year Ended | |||||||||||||||

| Schmid (IFRS, |

| Pegasus (US |

| IFRS Policy and |

| Transaction |

|

|

| Pro Forma | |||||

Revenue | 90,246 | € | € | € | € | 9,506 | ||||||||||

Cost of sales | (63,849) | — | (63,849) | |||||||||||||

Gross Profit | 26,397 | — | — | — | 26,397 | |||||||||||

Selling | (12,577) | — | — | — | (12,577) | |||||||||||

General administration | (12,538) | (751) | — | 155 | BB | (87,424) | ||||||||||

(4,184) | CC | |||||||||||||||

(70,106) | DD | |||||||||||||||

Research and development | (5,148) | — | — | — | (5,148) | |||||||||||

Other income | 15,985 | — | — | — | 15,985 | |||||||||||

Other expenses | (2,620) | — | — | — | (2,620) | |||||||||||

Listing fee amortization expense | — | (89) | — | — | (89) | |||||||||||

Legal and accounting expense | — | (4,957) | — | — | (4,957) | |||||||||||

Insurance expense | — | (181) | — | — | (181) | |||||||||||

(Impairment) / Reversal on impairment on financials assets | 22,696 | — | — | — | 22,696 | |||||||||||

Operating profit (loss) | 32,195 | (5,978) | — | (74,135) | (47,918) | |||||||||||

Finance income | 19,685 | — | — | — | 19,685 | |||||||||||

Interest and dividend income on cash and marketable securities held in Trust Account | — | 4,851 | — | (4,851) | AA | — | ||||||||||

Change in fair value of warrant liabilities | — | (1,251) | — | (204) | EE | (1,455) | ||||||||||

Loss on foreign exchange conversion | — | (33) | — | — | (33) | |||||||||||

Finance expense | (10,091) | — | — | (1,508) | FF | (11,599) | ||||||||||

Financial result | 9,594 | 3,567 | — | (6,563) | 6,598 | |||||||||||

Share of profit(loss) in joint venture | (1,057) | — | — | — | — | |||||||||||

Income (loss) before income tax | 40,732 | (2,411) | — | (80,698) | (42,378) | |||||||||||

Income tax expense | (2,778) | — | — | — | (2,778) | |||||||||||

Net income (loss) for the period | 37,954 | (2,411) | — | (80,698) | (45,156) | |||||||||||

17

RISK FACTORS

Investing in our Ordinary Shares or Warrants involves a high degree of risk. In addition to the other information set forth in this prospectus, you should carefully consider the risk factors discussed below when considering an investment in our Ordinary Shares or Warrants and any risk factors that may be set forth in the applicable prospectus supplement, as well as the other information contained in this prospectus and any applicable prospectus supplement. If any of the following risks occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that case, the market price of our Ordinary Shares and Public Warrants could decline and you could lose some or all of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations.

Risks Related to Our Business, Technology, and Industry

In the markets and industries in which we operate, we face intense competition and our failure to compete successfully in product development may have an adverse effect on our business, financial condition, and results of operations.

The electronic and photovoltaic industries in which we operate are highly competitive. We encounter competition from numerous and varied competitors in all areas of our business, especially in photovoltaics. For example, the photovoltaic industry includes large Chinese players who often dominate equipment manufacturing as the market is highly commoditized, price driven and under the focus of the Chinese government, which seeks to implement favorable industry policy for local producers. Further, we face competition not only from competitors who manufacture similar products, but also those who may offer a variety of other alternative products. Additionally, industry consolidation may result in larger, more homogeneous, and potentially stronger competitors in the markets in which we compete in the future.

We compete primarily on the basis of product quality, innovation, technology, brand reputation as well as through the services and support we offer. Our competitors may continue to develop their existing portfolios of products, introduce new products and enhance their existing products, which could cause a decline in market acceptance of our products. Our competitors may also improve their manufacturing processes or expand their manufacturing capacity, which could make it more difficult or costly for us to compete successfully. In addition, our competitors could enter into exclusive arrangements with our existing or potential customers or suppliers, which could limit our ability, or make it significantly more costly, to acquire necessary raw materials or to generate sales.

Some of our competitors may have or may obtain greater financial, technical, and marketing resources than we do. This would allow them to devote greater resources to promoting and selling certain products. Unlike many of our competitors who specialize in a single or limited number of product lines, we have a portfolio of businesses and must allocate resources across those businesses. As a result, we may invest less in certain areas of our business than our competitors invest which may lead to a competitive disadvantage.

Further, because some of our competitors are small divisions of large, international businesses, these competitors may have access to greater resources than we do and may therefore be better able to withstand a change in conditions within our industry or the economy as a whole.

Some of our competitors may also incur fewer expenses than we do in creating, marketing, and selling certain products and may face fewer risks in introducing new products to the market. This circumstance results from the nature of our business model, which is based on providing innovative and high-quality products, and therefore may require us to spend a proportionately greater amount on R&D than some of our competitors. If our pricing, marketing resources or other factors are not sufficiently competitive, or if there is an adverse reaction to our product decisions, we may lose market share in certain areas, which could adversely affect our business, financial condition, and results of operations.

Additionally, competitors could benefit from favorable tax regimes or additional governmental grants and subsidies. Certain of our competitors in various countries in which we do business, including China, may be owned by or affiliated with members of local governments and political entities. These competitors may receive special treatment with respect to regulatory compliance and product registration, while certain of our products, including those based on new technologies, may be delayed or even prevented from entering into the local market.

Escalating trade tensions, for example between the United States and China, can also lead to restrictions on the import and export of certain goods and technologies to or from certain countries. Further, additional trade import taxes can create disruption in competitiveness. Disruption in the global supply chain due to an escalation of trade tensions, the outbreak of war, a disease epidemic or other unexpected situation can cause certain services, goods and materials to be unavailable or in limited supply and can further

18

limit production capability and result in an inability to produce equipment for customers within an acceptable timeframe and at the needed volume. Such disruptions can have a material impact on our business, results of operations and financial condition, in time and in the needed volume.

We are currently in the process of patenting the technology for embedded traces (“ET”) which we believe is the next level technology for high-end PCBs & substrates. We believe we are the only participant in the market that is currently able to supply equipment for ET production and our best estimate, based on third-party data from a leading international consultancy firm, assumes that the ET market for high-end PCB equipment will grow substantially in 2024. If competitors concentrate on the ET as well and develop either better or more cost competitive processes and machinery, we could fail to capture the growth we expect in the ET market, which could have a material adverse effect on our business, financial condition, and results of operations.

The reputation of our brand is an important company asset and is key to our ability to remain a trusted supplier of specialty products, equipment and services.

We have maintained a strong reputation in the electronics and photovoltaics industries for more than 160 years. Our products, equipment and services are associated with long-lasting and reliable high quality.

The reputation of our brand is an important company asset and is key to our ability to remain a trusted supplier of specialty products, equipment and services and to attract and retain customers. Negative publicity regarding our company or actual, alleged, or perceived issues regarding one of our products or services, particularly given the high cost-of-failure nature of our products and services, could harm our relationships with customers and may adversely affect our credibility and our business.

Our business is dependent on the continued acceptance by our customers of our existing products and services and the value placed on them. If these products and services do not maintain market acceptance, our revenues may decrease. A portion of our sales originate from our worldwide customer-oriented services, which is an important element of our business. If we do not devote sufficient resources or are otherwise unsuccessful in assisting our customers effectively with the products sold to them, we could adversely affect our ability to retain existing customers and could discourage prospective customers from adopting our services. We may be unable to respond quickly enough to accommodate short-term increases in demand for customer support. We may also be unable to modify the nature, scope and delivery of our customer support to compete with changes in the support services provided by our competitors. Increased demand for customer support, without corresponding revenue, could increase costs and adversely affect our business, results of operations and financial condition.

We are also continually investing in new product development to expand our offerings beyond our traditional products and services. Market acceptance of any new products or services may be affected by customer confusion surrounding our introduction of new products and services. Our expansion into new offerings may present increased risks and efforts to expand beyond our traditional products and services may not succeed. However, if we do not continue to innovate and provide innovative machinery and technological solutions that are competitive within our industry, we may lose customers, and our revenues and results of operations could suffer.

Through our products, we have established ourselves as one of the leaders in quality and innovation in the markets in which we operate. For that reason, our customers are willing to pay above market prices for our machinery and technological solutions. If we do not continue to innovate and provide innovative machinery and technological solutions that are competitive within our industry, our customers may no longer be willing to pay above market price for our machinery and technological solutions or may move to our competitors. Our customers moving to our competitors could have a material adverse effect on our business, financial condition, and results of operations.

In addition, our business is subject to constant and rapid technological change, product obsolescence, price erosion, evolving standards, and raw material price fluctuations. The industry is currently affected by localization and a shift in customers’ businesses. In particular, there is currently a reorganization of the global supply chain underway, with a focus on decreasing dependency on China. The trends and characteristics in these industries may cause significant fluctuations in our results of operations and cash flows and have a material adverse effect on our financial condition. Our growth and success depend upon our ability to enhance our existing products and services and to develop and introduce new products and services to keep pace with such changes and developments and to meet changing customer needs and preferences. However, newer products or services may not achieve market acceptance if current or potential customers do not value the benefits of using our products, do not achieve favorable results using our products, use their budgets for different products, experience difficulties in using our products, or believe that our products are not cutting edge or do not add as much value as our competition’s products. If these newer products and services do not achieve market acceptance, there could

19

be a material adverse effect on our business, financial condition, and results of operations and our profitability could decline. Additionally, changes, including technological changes, in our customers’ products or processes may make our specialty machines unnecessary or reduce the quantity of our specialty machines needed for a given product or process, which would reduce the demand for such. We have had, and may continue to have, customers who find alternative materials or processes and therefore no longer require our products, which could have a material adverse effect on our business, financial condition, and results of operations. Further, our plans for operating our business and leading further growth include adding new products and services. These investments could contribute to losses, and we cannot guarantee whether or when any of these plans will be successful with customers or result in an improvement in profits for our business.

In addition, we may fail to anticipate the impact of new and emerging technology or changes in trends, fail to accurately determine market demand for new products and services, experience cost overruns, delays in delivery or performance problems, or create market confusion by making changes to our existing products and services. If we are not successful in obtaining acceptance for new products or services, demand for our products and services may decline and/or we may not be able to grow our business or growth may occur more slowly than we anticipate. Some of our current or future products or services could also be rendered obsolete as a result of competitive offerings or market shifts. Furthermore, if our customers deviate from the envisaged timeline for the introduction of new technology, the sales of our newer products could be adversely affected. Failure to anticipate or quickly adapt to changes in our customers’ product introduction timelines could have a material adverse effect on our business, financial condition, and results of operations.

Our profitability could suffer if our cost management strategies are unsuccessful, or our competitors develop an advantageous cost structure that we cannot match.

Our ability to improve or maintain our profitability is dependent on our ability to successfully manage our costs. Our cost management strategies include maintaining appropriate alignment between the price of raw materials, the demand for our offerings and our resource capacity and maintaining or improving our sales and marketing and general and administrative costs as a percentage of revenues. If our cost management efforts are not successful, our efficiency may suffer, and we may not achieve desired levels of profitability. In addition, we may not be able to implement our cost management efforts in a manner that permits us to realize the cost savings we anticipate in the time, manner, or amount we currently expect, or at all due to a variety of risks, including, but not limited to, difficulties in integrating shared services within our business, higher than expected employee severance or retention costs, higher than expected overhead expenses, delays in the anticipated timing of activities related to our cost savings plans, and other unexpected costs associated with operating our business. If we are not effective in managing our operating costs in response to changes in demand or pricing, or if we are unable to absorb or pass on increases in the compensation of our employees or costs of raw materials, we may not be able to invest in our business in an amount necessary to achieve our planned rates of growth, and our business, financial condition, and results of operations could be materially adversely affected.