|

JPMorgan Chase Financial Company LLC Fully and Unconditionally Guaranteed by JPMorgan Chase & Co. Market Linked Securities |

Filed Pursuant to Rule 433 Registration Statement Nos. 333-270004 and 333-270004-01 |

|

|

|

Market Linked Securities— Auto-Callable with Leveraged Upside Participation and Contingent Downside Principal at Risk Securities Linked to the Lowest Performing of the Russell 2000® Index and the Nikkei 225 Index due July 29, 2027 Fact Sheet dated July 10, 2024 to Preliminary Pricing Supplement dated July 10, 2024 |

Summary of Terms

| Issuer: | JPMorgan Chase Financial Company LLC |

| Guarantor: | JPMorgan Chase & C0. |

| Indices: | Russell 2000® Index and the Nikkei 225 Index |

| Pricing Date1: | July 26, 2024 |

| Issue Date1: | July 31, 2024 |

| Final Calculation Day1, 2: | July 26, 2027 |

| Stated Maturity Date1, 2: | July 29, 2027 |

| Principal Amount: | $1,000 per security (100% of par) |

| Automatic Call: | If the closing level of the lowest performing Index on the call date is greater than or equal to its starting level, the securities will be automatically called, and on the call settlement date, investors will receive the principal amount plus the call premium. |

| Call Premium: | At least 23.50% of the principal amount (the actual call premium will be provided in the pricing supplement) |

| Call Date1, 2: | July 31, 2025 |

| Call Settlement Date: | Three business days after the call date |

| Maturity Payment Amount: |

If the securities are not automatically called on the call date, the “maturity payment amount” per security will equal: If the ending level of the lowest performing Index on the final calculation day is greater than its starting level: $1,000 + ($1,000 × index return of the lowest performing Index on the final calculation day × upside participation rate); If the ending level of the lowest performing Index on the final calculation day is less than or equal to its starting level, but greater than or equal to its threshold level: $1,000; or If the ending level of the lowest performing Index on the final calculation day is less than its threshold level: $1,000 + ($1,000 × index return of the lowest performing Index on the final calculation day) |

| Lowest Performing Index | On the call date or the calculation date, the Index with the lowest index return on that day |

| Starting Level: | For each Index, its closing level on the pricing date |

| Ending Level: | For each Index, its closing level on the final calculation day |

| Upside Participation Rate: | 150.00% |

| Threshold Level: | For each Index, 75% of its starting level |

| Index Return: | For the call date or the final calculation day and for each Index: (closing level on that day – starting level) / starting level |

| Calculation Agent: | J.P. Morgan Securities LLC (“JPMS”) |

| Denominations: | $1,000 and any integral multiple of $1,000 |

| CUSIP: | 48135PGP0 |

| Fees and Commissions: | Up to 2.575% for Wells Fargo Securities, LLC (“WFS”); WFS has advised us that dealers, including Wells Fargo Advisors (“WFA”), may receive 2.00% of WFS’s fee, and WFA may also receive a distribution expense fee of 0.075%. In addition, with respect of certain securities sold in this offering, JPMS may pay a fee of up to 0.25% to selected dealers in consideration for marketing and other services in connection with the distribution of the securities to other dealers. |

| Tax Considerations: | See the preliminary pricing supplement. |

|

1 Subject to change 2 Subject to postponement | |

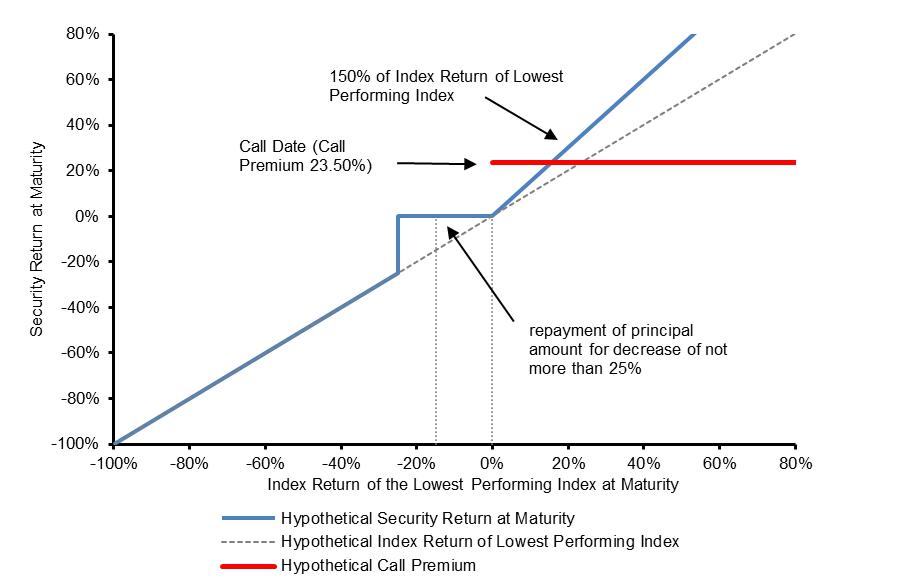

Hypothetical Payout Profile*

*Assumes a call premium equal to the lowest possible call premium that may be determined on the pricing date

If the securities are automatically called, the positive return on the securities will be limited to the call premium, even if the closing level of the lowest performing Index on the call date significantly exceeds its starting level. If the securities are automatically called, you will not have the opportunity to participate in any appreciation of the lowest performing Index on the final calculation day at the upside participation rate.

If the securities are not automatically called and the ending level of the lowest performing Index on the final calculation day is less than its threshold level, you will have full downside exposure to the decrease in the level of that Index from its starting level and you will lose more than 25%, and possibly all, of the principal amount of your securities at maturity.

The securities are unsecured and unsubordinated obligations of JPMorgan Chase Financial Company LLC, which we refer to as JPMorgan Financial, the payment on which is fully and unconditionally guaranteed by JPMorgan Chase & Co. Any payment on the securities is subject to the credit risk of JPMorgan Financial, as issuer of the securities, and the credit risk of JPMorgan Chase & Co., as guarantor of the securities.

If the securities priced on the date of the accompanying preliminary pricing supplement, the estimated value of the securities would be approximately $950.70 per security. The estimated value of the securities, when the terms of the securities are set, will be provided in the pricing supplement and will not be less than $940.00 per security. See “The Estimated Value of the Securities” in the preliminary pricing supplement for additional information.

Preliminary Pricing Supplement: http://www.sec.gov/Archives/edgar/data/19617/000121390024060440/

ea177232_424b2.htm

The securities have complex features and investing in the securities involves risks not associated with an investment in conventional debt securities. See “Risk Factors” in the accompanying prospectus supplement and the accompanying product supplement, Annex A to the accompanying prospectus addendum and “Selected Risk Considerations” in the accompanying preliminary pricing supplement.

The securities are not bank deposits, are not insured by the Federal Deposit Insurance Corporation or any other governmental agency and are not obligations of, or guaranteed by, a bank.

THIS FACT SHEET DOES NOT PROVIDE ALL OF THE INFORMATION THAT AN INVESTOR SHOULD CONSIDER PRIOR TO MAKING AN INVESTMENT DECISION. This fact sheet should be read in conjunction with the accompanying preliminary pricing supplement, prospectus, prospectus supplement, prospectus addendum, product supplement and underlying supplement.

Selected Risk Considerations

The risks set forth below are discussed in detail in the “Selected Risk Considerations” section in the accompanying preliminary pricing supplement, the “Risk Factors” sections in the accompanying prospectus supplement and product supplement and Annex A to the accompanying prospectus addendum. Please review the risk disclosure carefully.

|

· If the Securities Are Not Automatically Called and the Ending Level of the Lowest Performing Index on the Final Calculation Day Is Less Than Its Threshold Level, You Will Lose More Than 25%, and Possibly All, of the Principal Amount of Your Securities at Maturity. · If the Securities Are Automatically Called, the Return on the Securities Will Be Limited to the Call Premium. · You Will Be Subject to Reinvestment Risk. · The Securities Are Subject to the Credit Risks of JPMorgan Financial and JPMorgan Chase & Co. · As a Finance Subsidiary, JPMorgan Financial Has No Independent Operations and Has Limited Assets. · You Are Exposed to the Risk of Decline in the Level of Each Index. · Your Payment at Maturity Will Be Determined by the Lowest Performing Index. · You Will Be Subject to Risks Resulting from the Relationship Between the Indices. · The Benefit Provided by the Threshold Level May Terminate on the Final Calculation Day. · No Interest or Dividend Payments or Voting Rights · Lack of Liquidity · The Final Terms and Estimated Valuation of the Securities Will Be Provided in the Pricing Supplement. · The Tax Consequences of an Investment in the Securities Are Uncertain. · Potential Conflicts · The Estimated Value of the Securities Will Be Lower Than the Original Issue Price (Price to Public) of the Securities. · The Estimated Value of the Securities Does Not Represent Future Values of the Securities and May Differ from Others’ Estimates. · The Estimated Value of the Securities Is Derived by Reference to an Internal Funding Rate. · The Value of the Securities as Published by JPMS (and Which May Be Reflected on Customer Account Statements) May Be Higher Than the Then-Current Estimated Value of the Securities for a Limited Time Period.

|

· Secondary Market Prices of the Securities Will Likely Be Lower Than the Original Issue Price of the Securities. · Many Economic and Market Factors Will Impact the Value of the Securities. · An Investment in the Securities Is Subject to Risks Associated with Small Capitalization Stocks with Respect to the Russell 2000® Index. · The Securities Are Subject to Non-U.S. Securities Risk with Respect to the Nikkei 225 Index. · No Direct Exposure to Fluctuations in Foreign Exchange Rates with Respect to the Nikkei 225 Index. · Any Payment on the Securities Will Depend upon the Performance of Each Index and Therefore the Securities Are Subject to the Risks Associated with each Index, as Discussed in the Accompanying Pricing Supplement and Product Supplement.

|

SEC Legend: JPMorgan Chase Financial Company LLC and JPMorgan Chase & Co. have filed a registration statement (including a prospectus) with the SEC for any offerings to which these materials relate. Before you invest, you should read the prospectus in that registration statement and the other documents relating to this offering that JPMorgan Chase Financial Company LLC and JPMorgan Chase & Co. has filed with the SEC for more complete information about JPMorgan Chase Financial Company LLC and JPMorgan Chase & Co. and this offering. You may get these documents without cost by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, JPMorgan Chase Financial Company LLC and JPMorgan Chase & Co., any agent or any dealer participating in this offering will arrange to send you the prospectus and each prospectus supplement as well as any product supplement, underlying supplement and preliminary pricing supplement if you so request by calling toll-free 1-866-535-9248.

As used in this fact sheet, “we,” “us” and “our” refer to JPMorgan Financial Company LLC. Wells Fargo Advisors is a trade name used by Wells Fargo Clearing Services, LLC and Wells Fargo Advisors Financial Network, LLC, members SIPC, separate registered broker-dealers and non-bank affiliates of Wells Fargo & Company.