UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

OR

For

the fiscal year ended

OR

OR

For the transition period from to

Commission

file number:

(Exact name of Registrant as specified in its charter)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The Nasdaq Stock Market LLC ( |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer’s

classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |||

| Emerging growth company |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided

pursuant to Section 13(a) of the Exchange Act.

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | International Financial Reporting Standards as issued | Other ☐ | ||

| by the International Accounting Standards Board ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934).

☐ Yes

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☐ Yes ☐ No

Table of Contents

i

INTRODUCTION

Except where the context otherwise requires and for purposes of this annual report only the term:

| ● | “17 Uno BVI” refers to 17 Uno Limited, a company incorporated under the laws of British Virgin Islands; |

| ● | “AE” refers to an account executive, being licensed representative accredited to I Win Securities to carry out regulated activities, who is self-employed and only entitled to share the brokerage income from the clients referred by him/her; |

| ● | “AUM” refers to the amount of assets under management; |

| ● | “BSS” refers to the Broker Supplied System, being a front office solution either developed in-house by the Stock Exchange Participant or a third-party software package acquired from commercial vendors, enabling the Stock Exchange Participant to connect its trading facilities to the Open Gateway to conduct trading; |

| ● | “CAGR” refers to compounded annual growth rate, the year-on-year growth rate over a specific period of time; |

| ● | “China” or the “PRC” refer to the People’s Republic of China, including Hong Kong and Macau; |

| ● | “Code of Conduct” refers to the Code of Conduct for Persons Licensed by or Registered with the Securities and Futures Commission of Hong Kong; |

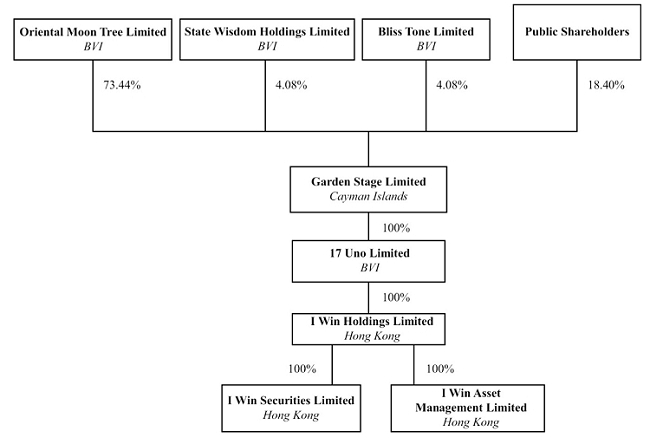

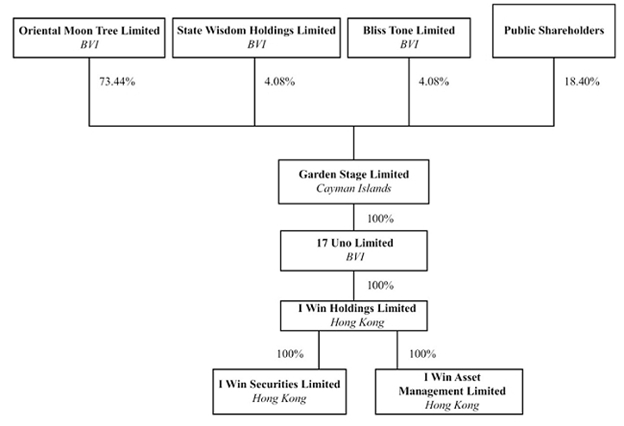

| ● | “Controlling Shareholder” refers to Oriental Moon Tree Limited, a company incorporated under the laws of British Virgin Islands; |

| ● | “FY 2024”, “FY 2023” “FY2022” are to fiscal year ended March 31, 2024, March 31, 2023, March 31, 2022, respectively; |

| ● | “Garden Stage” or “Company” are to Garden Stage Limited, an exempted company incorporated with limited liability in the Cayman Islands on August 11, 2022; |

| ● | “HKD” or “HK$” refer to the legal currency of Hong Kong. |

| ● | “HKSCC” refers to the Hong Kong Securities Clearing Company Limited |

| ● | “HKSFC” refers to the Securities and Futures Commission of Hong Kong; |

| ● | “Hong Kong” refers to the Hong Kong Special Administrative Region of the People’s Republic of China for the purposes of this annual report only; |

| ● | “I Win Asset Management” refers to I Win Asset Management Limited, a company with limited liability under the laws of Hong Kong; |

| ● | “I Win Holdings HK” refers to I Win Holdings Limited, a company with limited liability under the laws of Hong Kong; |

| ● | “I Win Securities” refers to I Win Securities Limited, a company with limited liability under the laws of Hong Kong; |

| ● | “Licensed Representative(s)” refers to an individual who is granted a license under section 120(1) or 121(1) of the SFO to carry on one or more than one regulated activity; |

| ● | “Listing Rules” refers to the Rules Governing the Listing of Securities on the Stock Exchange of Hong Kong, as amended, supplemented or otherwise modified from time to time; |

| ● | “Mainland China” refers to the mainland of the People’s Republic of China; excluding Taiwan and the special administrative regions of Hong Kong and Macau for the purposes of this annual report only; |

| ● | “Ordinary Shares” refers to the ordinary shares of the Garden Stage Limited, par value of US$0.0001 per share; |

| ● | “Open Gateway” refers to a Windows-based device provided by the Stock Exchange and installed at the Stock Exchange Participants’ office to facilitate electronic interface of the Automatic Order Matching and Execution System of the Stock Exchange with front office systems operated by the Stock Exchange Participant; |

| ● | “Operating Subsidiaries” refers to I Win Securities and I Win Asset Management, the indirectly wholly-owned subsidiaries of Garden Stage, unless otherwise specified |

| ● | “PRC government” or “Chinse government” are to the government of Mainland China for the purposes of this annual report only; |

| ● | “Responsible Officer(s)” or “RO” refer to a Licensed Representative who is also approved as a responsible officer under section 126 of the SFO to supervise one or more than one regulated activity of the licensed corporation to which he/she is accredited; |

ii

| ● | “SEC” refers to the United States Securities and Exchange Commission; |

| ● | “SFO” refers to the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong), as amended, supplemented or otherwise modified from time to time; |

| ● | “Stock Exchange” or “SEHK” refer to the Stock Exchange of Hong Kong Limited; |

| ● | “Stock Exchange Trading Right” refers to the right to be eligible to trade on or through the Stock Exchange as a Stock Exchange Participant and entered as such a right in a list, register or roll kept by the Stock Exchange; |

| ● | “Stock Exchange Participant(s)” refers to corporation(s) licensed to carry on Type 1 (dealing in securities) regulated activity under the SFO who, in accordance with the rules of the Stock Exchange, may trade on or through the Stock Exchange and whose name(s) is/are entered in a list, register or roll kept by the Stock Exchange as person(s) who may trade on or through the Stock Exchange; |

| ● | “US$” or “U.S. dollars” refer to the legal currency of the United States; and |

| ● | “we,” “us,” “our,” “the Company” and “Garden Stage” are to Garden Stage Limited, an exempted company incorporated with limited liability in the Cayman Islands on August 11, 2022, and does not include its subsidiaries, 17 Uno BVI, I Win Holdings HK, I Win Securities, and I Win Asset Management. Where appropriate, we shall refer to the subsidiaries by their legal names, collectively as “our subsidiaries”, or “Operating Subsidiaries” when we refer to our operating entities, as the case may be, and clearly identify the entity in which investors are purchasing an interest; |

Garden Stage is a holding company with operations conducted in Hong Kong through its Operating Subsidiaries, using Hong Kong dollars. The reporting currency is U.S. dollars. Assets and liabilities denominated in foreign currencies are translated at year-end exchange rates, income statement accounts are translated at average rates of exchange for the year and equity is translated at historical exchange rates. Any translation gains or losses are recorded in other comprehensive income (loss). Gains or losses resulting from foreign currency transactions are included in net income. The conversion of Hong Kong dollars into U.S. dollars are based on the exchange rates set forth in the H.10 statistical release of the Board of Governors of the Federal Reserve System. Unless otherwise noted, all translations from Hong Kong dollars to U.S. dollars and from U.S. dollars to Hong Kong dollars in this annual report were made at an average rate of HKD 7.8252 to USD 1.00, HKD 7.8392 to USD 1.00 and HKD 7.7843 to USD 1.00 for FY 2024, FY2023 and FY 2022, respectively.

We obtained the industry and market data used in this annual report or any document incorporated by reference from industry publications, research, surveys and studies conducted by third parties and our own internal estimates based on our management’s knowledge and experience in the markets in which we operate. We did not, directly or indirectly, sponsor or participate in the publication of such materials, and these materials are not incorporated in this annual report other than to the extent specifically cited in this annual report. We have sought to provide current information in this annual report and believe that the statistics provided in this annual report remain up-to-date and reliable, and these materials are not incorporated in this annual report other than to the extent specifically cited in this annual report.

iii

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to us. All statements other than statements of historical facts are forward-looking statements. These statements relate to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

You can identify forward-looking statements by terms such as “may,” “could,” “will,” “should,” “would,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “project” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements include, but are not limited to, statements about:

| ● | future financial and operating results, including revenues, income, expenditures, cash balances and other financial items; |

| ● | our ability to execute our growth, expansion and acquisition strategies, including our ability to meet our goals; |

| ● | current and future economic and political conditions; |

| ● | our expectations regarding demand for and market acceptance of our subsidiaries’ services; |

| ● | our expectations regarding the expansion of our subsidiaries’ client base; |

| ● | our subsidiaries’ relationships with their business partners; |

| ● | competition in our industries; |

| ● | relevant government policies and regulations relating to our industries; |

| ● | our ability to obtain and maintain all necessary government certifications, approvals, and/or licenses to conduct our business; |

| ● | ability to managing our growth effectively; |

| ● | our capital requirements and our ability to raise any additional financing which we may require; |

| ● | our subsidiaries’ ability to protect their intellectual property rights and secure the right to use other intellectual property that they deem to be essential or desirable to the conduct of their business; |

| ● | the dependence on our senior management and key employees; and |

| ● | our ability to hire and retain qualified management personnel and key employees in order to develop our subsidiaries’ business; |

| ● | overall industry and market performance; |

| ● | any recurrence of the COVID-19 pandemic and scope of related government orders and restrictions and the extent of the impact of the COVID-19 pandemic on the global economy, impact it may have on our operations, the demand for our products and services, and economic activity in general; |

| ● | other assumptions described in this annual report underlying or relating to any forward-looking statements. |

You should read this annual report and the documents that we refer to in this annual report and have filed as exhibits to this annual report completely and with the understanding that our actual future results may be materially different from what we expect. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed under the heading “Risk Factors” and elsewhere in this annual report. If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee of future performance.

You should not rely upon forward-looking statements as predictions of future events. The forward-looking statements made in this annual report relate only to events or information as of the date on which the statements are made in this annual report. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

We would like to caution you not to place undue reliance on these forward-looking statements and you should read these statements in conjunction with the risk factors disclosed in “Item 3. Key Information—3.D. Risk Factors.” Those risks are not exhaustive. We operate in an evolving environment. New risks emerge from time to time and it is impossible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ from those contained in any forward-looking statement. We do not undertake any obligation to update or revise the forward-looking statements except as required under applicable law. You should read this annual report and the documents that we reference in this annual report completely and with the understanding that our actual future results may be materially different from what we expect.

iv

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable for annual reports on Form 20-F.

Item 2. Offer Statistics and Expected Timetable

Not applicable for annual reports on Form 20-F.

Item 3. Key Information

3.A. [Reserved]

3.B. Capitalization and Indebtedness

Not applicable for annual reports on Form 20-F.

3.C. Reasons for the Offer and Use of Proceeds

Not applicable for annual reports on Form 20-F.

3.D. Risk Factors

You should carefully consider the following risk factors, together with all of the other information included in this Annual Report. Investment in our securities involves a high degree of risk. You should carefully consider the risks described below together with all of the other information included in this Annual Report before making an investment decision. The risks and uncertainties described below represent our known material risks to our business. If any of the following risks actually occurs, our business, financial condition or results of operations could suffer. In that case, you may lose all or part of your investment.

Risks Related to Doing Business in the Jurisdictions in which the Operating Subsidiaries Operate

All of our operations are in Hong Kong. However, due to the long arm application of the current PRC laws and regulations, the PRC government may exercise significant direct oversight and discretion over the conduct of our business and may intervene or influence our operations, which could result in a material change in our operations and/or the value of our Ordinary Shares. Our Operating Subsidiaries in Hong Kong may be subject to laws and regulations of the Mainland China, which may impair our ability to operate profitably and result in a material negative impact on our operations and/or the value of our Ordinary Shares. Furthermore, the changes in the policies, regulations, rules, and the enforcement of laws of the PRC may also occur quickly with little advance notice and our assertions and beliefs of the risk imposed by the PRC legal and regulatory system cannot be certain.

Our Operating Subsidiaries are located and operates its business in Hong Kong, a special administrative region of the PRC. The Operating Subsidiaries do not have operation in Mainland China and is not regulated by any regulator in Mainland China. As a result, the laws and regulations of the Mainland China do not currently have any material impact on our business, financial condition and results of operation. Furthermore, except for the Basic Law of the Hong Kong Special Administrative Region of the People’s Republic of China (“Basic Law”), national laws of the Mainland China do not apply in Hong Kong unless they are listed in Annex III of the Basic Law and applied locally by promulgation or local legislation. National laws that may be listed in Annex III are currently limited under the Basic Law to those which fall within the scope of defense and foreign affairs as well as other matters outside the limits of the autonomy of Hong Kong. National laws and regulations relating to data protection, cybersecurity and the anti-monopoly have not been listed in Annex III and so do not apply directly to Hong Kong.

1

However, due to long arm provisions under the current Mainland China laws and regulations, there remain regulatory and legal uncertainty with respect to the implementation of laws and regulations of Mainland China to Hong Kong. As a result, there is no guarantee that the PRC government may not choose to implement the laws of the Mainland China to Hong Kong and exercise significant direct influence and discretion over the operation of our operating subsidiary in the future and, it will not have a material adverse impact on our business, financial condition and results of operations, due to changes in laws, political environment or other unforeseeable reasons.

In the event that we or our Hong Kong Operating Subsidiaries were to become subject to laws and regulations of Mainland China, the legal and operational risks associated in Mainland China may also apply to our operations in Hong Kong, and we face the risks and uncertainties associated with the legal system in the Mainland China, complex and evolving Mainland China laws and regulations, and as to whether and how the recent PRC government statements and regulatory developments, such as those relating to data and cyberspace security and anti-monopoly concerns, would be applicable to companies like our operating subsidiary and us, given the substantial operations of our operating subsidiary in Hong Kong and the PRC government may exercise significant oversight over the conduct of business in Hong Kong.

The laws and regulations in the Mainland China are evolving, and their enactment timetable, interpretation, enforcement, and implementation involve significant uncertainties, and may change quickly with little advance notice, along with the risk that the PRC government may intervene or influence our operating subsidiary’s operations at any time could result in a material change in our operations and/or the value of our securities. Moreover, there are substantial uncertainties regarding the interpretation and application of Mainland China laws and regulations including, but not limited to, the laws and regulations related to our business and the enforcement and performance of our arrangements with customers in certain circumstances. The laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness and interpretation of newly enacted laws or regulations, including amendments to existing laws and regulations, may be delayed, and our business may be affected if we rely on laws and regulations which are subsequently adopted or interpreted in a manner different from our understanding of these laws and regulations. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business.

The laws, regulations, and other government directives in the Mainland China may also be costly to comply with, and such compliance or any associated inquiries or investigations or any other government actions may:

| ● | delay or impede our development; |

| ● | result in negative publicity or increase our operating costs; |

| ● | require significant management time and attention; |

| ● | cause devaluation of our securities or delisting; and, |

| ● | subject us to remedies, administrative penalties and even criminal liabilities that may harm our business, including fines assessed for our current or historical operations, or demands or orders that we modify or even cease our business operations. |

The PRC government may intervene or influence the Hong Kong operations of an offshore holding company, such as ours, at any time. The PRC government may exert more control over offerings conducted overseas and/or foreign investment in Hong Kong-based issuers. If the PRC government exerts more oversight and control over offerings that are conducted overseas and/or foreign investment in Hong Kong-based issuers and we were to be subject to such oversight and control, it may result in a material adverse change to our subsidiaries’ business operations, including our subsidiaries’ operations in Hong Kong.

As a company mainly conducting business in Hong Kong, a special administrative region of China and our subsidiaries’ clients include mainland China residents, our subsidiaries’ business and our prospects, financial condition, and results of operations may be influenced to a significant degree by political, economic, and social conditions in China generally. The PRC government may intervene or influence the operations in mainland China of an offshore holding company at any time, which, if extended to our subsidiaries’ operations in Hong Kong, could result in a material adverse change to our subsidiaries’ operations. The PRC government has recently indicated an intent to exert more oversight and control over listings conducted overseas and/or foreign investment in issuers based in mainland China. For instance, on July 6, 2021, the relevant PRC governmental authorities promulgated the Opinions on Strictly Cracking Down on Illegal Securities Activities, which emphasized the need to strengthen the supervision over overseas listings by companies in mainland China. We cannot assure you that the oversight will not be extended to companies operating in Hong Kong like us and any such action may significantly limit or completely hinder our ability to offer or continue to offer our securities to investors, result in a material adverse change to our subsidiaries’ business operations, including our subsidiaries’ Hong Kong operations, and damage our reputation.

2

Our subsidiaries’ business, our financial condition and results of operations, and/or the value of our Ordinary Shares or our ability to offer or continue to offer securities to investors may be materially and adversely affected by existing or future PRC laws and regulations which may become applicable to our subsidiaries.

We have no operations in Mainland China. However, our Operating Subsidiaries are located and operate in Hong Kong, a special administrative region of the PRC, there is no guarantee that if certain existing or future PRC laws become applicable to our subsidiaries, it will not have a material adverse impact on our subsidiaries’ business, financial condition and results of operations and/or our ability to offer or continue to offer securities to investors.

Except for the Basic Law of the Hong Kong Special Region of the People’s Republic of China (“Basic Law”), national laws of mainland China (“National Laws”) do not apply in Hong Kong unless they are listed in Annex III of the Basic Law and applied locally by promulgation or local legislation. National Laws that may be listed in Annex III are currently limited under the Basic Law to those which fall within the scope of defense and foreign affairs as well as other matters outside the limits of the autonomy of Hong Kong. PRC laws and regulations relating to data protection, cyber security and the anti-monopoly have not been listed in Annex III and thus they may not apply directly to Hong Kong.

The PRC laws and regulations are evolving, and their enactment timetable, interpretation and implementation involve significant uncertainties. To the extent any PRC laws and regulations become applicable to our subsidiaries, we may be subject to the risks and uncertainties associated with the legal system in mainland China, including with respect to the enforcement of laws and the possibility of changes of rules and regulations with little or no advance notice.

We may also become subject to the PRC laws and regulations to the extent our subsidiaries commence business and customer facing operations in mainland China as a result of any future acquisition, expansion or organic growth. There is no guarantee that this will continue to be the case in the future in relation to the continued listing of our securities on a securities exchange outside of the PRC, or even when such permission is obtained, it will not be subsequently denied or rescinded. It remains uncertain as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offering and other capital markets activities and due to the possibility that laws, regulations, or policies in the PRC could change rapidly in the future, it remains uncertain whether the PRC government will adopt additional requirements or extend the existing requirements to apply to our operating subsidiary located in Hong Kong. It is also uncertain whether the Hong Kong government will be mandated by the PRC government, despite the constitutional constraints of the Basic Law, to control over offerings conducted overseas and/or foreign investment of entities in Hong Kong, including our operating subsidiary. Any actions by the PRC government to exert more oversight and control over offerings (including businesses whose primary operations are in Hong Kong) that are conducted overseas and/or foreign investments in Hong Kong-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline or be worthless.

If we and/or our subsidiaries were to be required to comply with cybersecurity, data privacy, data protection, or any other PRC laws and regulations related to data and we and/or our subsidiaries cannot comply with such PRC laws and regulations, our subsidiaries’ business, financial condition, and results of operations may be materially and adversely affected.

We may be subject to a variety of cybersecurity, data privacy, data protection, and other PRC laws and regulations related to data, including those relating to the collection, use, sharing, retention, security, disclosure, and transfer of confidential and private information, such as personal information and other data. These laws and regulations apply not only to third-party transactions, but also to transfers of information within our organization. These laws and regulations may restrict our subsidiaries’ business activities and require us and/or our subsidiaries to incur increased costs and efforts to comply, and any breach or noncompliance may subject us and/or our subsidiaries to proceedings against such entity(ies), damage our reputation, or result in penalties and other significant legal liabilities, and thus may materially and adversely affect our subsidiaries’ business and our financial condition and results of operations.

3

As the laws and regulations related to cybersecurity, data privacy, and data protection in mainland China where our subsidiaries do not have operations are relatively new and evolving, and their interpretation and application may be uncertain, it is still unclear if we and/or our subsidiaries may become subject to such new laws and regulations.

The PRC Data Security Law, or the Data Security Law, which was promulgated by the Standing Committee of the National People’s Congress on June 10, 2021 and took effect on September 1, 2021, requires data collection to be conducted in a legitimate and proper manner, and stipulates that, for the purpose of data protection, data processing activities must be conducted based on data classification and hierarchical protection system for data security. According to Article 2 of the Data Security Law, it applies to data processing activities within the territory of mainland China as well as data processing activities conducted outside the territory of mainland China which jeopardize the national interest or the public interest of China or the rights and interest of any PRC organization and citizens. Any entity failing to perform the obligations provided in the Data Security Law may be subject to orders to correct, warnings and penalties including ban or suspension of business, revocation of business licenses or other penalties. As of the date of this Annual Report, we do not have any operation or maintain any office or personnel in mainland China, and we have not conducted any data processing activities which may endanger the national interest or the public interest of China or the rights and interest of any Chinese organization and citizens. Therefore, we do not believe that the Data Security Law is applicable to us.

On August 20, 2021, the Standing Committee of the National People’s Congress of China promulgated the Personal Information Protection Law, which integrates the scattered rules with respect to personal information rights and privacy protection and took effect on November 1, 2021. According to Article 3 of the Personal Information Protection Law, it is applied not only to personal information processing activities carried out in the territory of mainland China but also to personal information processing activities outside the mainland China for the purpose of offering products or services to domestic natural persons in the territory of mainland China. The offending entities could be ordered to correct, or to suspend or terminate the provision of services, and face confiscation of illegal income, fines or other penalties. As our subsidiaries’ services are provided in Hong Kong, Cayman Islands, British Virgin Islands and the U.S. rather than in the mainland China to clients worldwide, including but not limited to clients of mainland China who visit our offices in these locations, we take the view that we and our subsidiaries are not subject to the Personal Information Protection Law.

On July 7, 2022, the Cyberspace Administration of China (the “CAC”) issued the Measures for Security Assessment of Outbound Data Transfer, or the Measures, which took effect on September 1, 2022. According to the Measures, in addition to the self-risk assessment requirement for provision of any data outside mainland China, a data processor shall apply to the competent cyberspace department for data security assessment and clearance of outbound data transfer in any of the following events: (i) outbound transfer of important data by a data processor; (ii) outbound transfer of personal information by an operator of critical information infrastructure or a data processor which has processed more than one million users’ personal data; (iii) outbound transfer of personal information by a data processor which has made outbound transfers of more than one hundred thousand users’ personal information or more than ten thousand users’ sensitive personal information cumulatively since January 1 of the previous year; (iv) such other circumstances where ex-ante security assessment and evaluation of cross-border data transfer is required by the CAC. As of the date of this Annual Report, we and our subsidiaries have not collected, stored, or managed any personal information in mainland China. therefore, we believe that the Measures is not applicable to us.

However, given the recency of the issuance of the above PRC laws and regulations related to cybersecurity and data privacy, we and our subsidiaries still face uncertainties regarding the interpretation and implementation of these laws and regulations and we could not rule out the possibility that any PRC governmental authorities may subject us and/or our subsidiaries to such laws and regulations in the future. If they are deemed to be applicable to us and/or our subsidiaries, we cannot assure you that we and our subsidiaries will be compliant with such new regulations in all respects, and we and/or our subsidiaries may be ordered to rectify and terminate any actions that are deemed illegal by the PRC governmental authorities and become subject to fines and other government sanctions, which may materially and adversely affect our subsidiaries’ business and our financial condition and results of operations.

4

If we and/or our subsidiaries were to be required to obtain any permission or approval from or complete any filing procedure with the China Securities Regulatory Commission (the “CSRC”), the CAC, or other PRC governmental authorities in connection with the initial public offering (“IPO”) or future follow-on offerings under PRC laws, we and/or our subsidiaries may be fined or subject to other sanctions, and our subsidiaries’ business and our reputation, financial condition, and results of operations may be materially and adversely affected.

The Cybersecurity Review Measures jointly promulgated by the CAC and other relevant PRC governmental authorities on December 28, 2021 required that, among others, “critical information infrastructure” or network platform operators holding over one million users’ personal information to apply for a cybersecurity review before any public offering on a foreign stock exchange. However, this regulation is recently issued and there remain substantial uncertainties about its interpretation and implementation.

As of the date of this Annual Report, we and our subsidiaries do not have any business operation or maintain any office or personnel in mainland China. We and our subsidiaries have not collected, stored, or managed any personal information in mainland China. Based on the assessment conducted by the management, we believe that we and our subsidiaries are not currently required to proactively apply to a cybersecurity review for our IPO or follow-on offerings overseas, on the basis that (i) our subsidiaries are incorporated in Hong Kong, the British Virgin Islands, and other jurisdictions outside of mainland China and operate in Hong Kong without any subsidiary or variable interest entities (“VIE”) structure in mainland China, and we do not maintain any office or personnel in mainland China; (ii) except for the Basic Law, the National Laws do not apply in Hong Kong unless they are listed in Annex III of the Basic Law and applied locally by promulgation or local legislation, and National Laws that may be listed in Annex III are currently limited under the Basic Law to those which fall within the scope of defense and foreign affairs as well as other matters outside the limits of the autonomy of Hong Kong, and PRC laws and regulations relating to data protection and cyber security have not been listed in Annex III as the date of this Annual Report; (iii) our data processing activities are solely carried out by our overseas entities outside of mainland China for the purpose of offering products or services in Hong Kong and other jurisdictions outside of mainland China; (iv) we and our subsidiaries do not control more than one millions users’ personal information as of the date of this Annual Report; (v) as of the date of this Annual Report, we and our subsidiaries have not received any notice of identifying us as critical information infrastructure from any relevant PRC governmental authorities; and (vi) as of the date of this Annual Report, none of us or our subsidiaries have been informed by any PRC governmental authority of any requirement for a cybersecurity review.

Additionally, we believe that we and our subsidiaries are compliant with the regulations and policies that have been issued by the CAC to date and there was no material change to these regulations and policies since our IPO. However, regulatory requirements on cybersecurity and data security in the mainland China are constantly evolving and can be subject to varying interpretations or significant changes, which may result in uncertainties about the scope of our responsibilities in that regard, and there can be no assurance that the relevant PRC governmental authorities, including the CAC, would reach the same conclusion as us. We will closely monitor and assess the implementation and enforcement of the Cybersecurity Review Measures. If the Cybersecurity Review Measures mandates clearance of cybersecurity and/or data security regulators and other specific actions to be completed by companies like us, we may face uncertainties as to whether we can meet such requirements timely, or at all.

On February 17, 2023, the CSRC promulgated the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Measures”) and five supporting guidelines, which took effect on March 31, 2023. The Trial Measures requires companies in mainland China that seek to offer and list securities overseas, both directly and indirectly, to fulfill the filing procedures with the CSRC. According to the Trial Measures, the determination of the “indirect overseas offering and listing by companies in mainland China” shall comply with the principle of “substance over form” and particularly, an issuer will be required to go through the filing procedures under the Trial Measures if the following criteria are met at the same time: (i) 50% or more of the issuer’s operating revenue, total profits, total assets or net assets as documented in its audited consolidated financial statements for the most recent accounting year are accounted for by companies in mainland China; and (ii) the main parts of the issuer’s business activities are conducted in mainland China, or its main places of business are located in mainland China, or the senior managers in charge of its business operation and management are mostly Chinese citizens or domiciled in mainland China. On the same day, the CSRC held a press conference for the release of the Trial Measures and issued the Notice on Administration for the Filing of Overseas Offering and Listing by Domestic Companies, which clarifies that (i) on or prior to the effective date of the Trial Measures, companies in mainland China that have already submitted valid applications for overseas offering and listing but have not obtained approval from overseas regulatory authorities or stock exchanges shall complete the filing before the completion of their overseas offering and listing; and (ii) companies in mainland China which, prior to the effective date of the Trial Measures, have already obtained the approval from overseas regulatory authorities or stock exchanges and are not required to re-perform the regulatory procedures with the relevant overseas regulatory authority or stock exchange, but have not completed the indirect overseas listing, shall complete the overseas offering and listing before September 30,2023, and failure to complete the overseas listing within such six-month period will subject such companies to the filing requirements with the CSRC.

5

Based on the assessment conducted by the management, we are not subject to the Trial Measures, because we are incorporated in the Cayman Islands and our subsidiaries are incorporated in Hong Kong, the British Virgin Islands and other regions outside of mainland China and operate in Hong Kong without any subsidiary or VIE structure in mainland China, and we do not have any business operations or maintain any office or personnel in mainland China. However, as the Trial Measures and the supporting guidelines are newly published, there exists uncertainty with respect to the implementation and interpretation of the principle of “substance over form”. As of the date of this Annual Report, there was no material change to these regulations and policies since our IPO If our offering, including the IPO and future follow-on offerings, and listing were later deemed as “indirect overseas offering and listing by companies in mainland China” under the Trial Measures, we may need to complete the filing procedures for our offering, including the IPO and future follow-on offerings, and listing. If we are subject to the filing requirements, we cannot assure you that we will be able to complete such filings in a timely manner or even at all.

Since these statements and regulatory actions are new, it is also highly uncertain in the interpretation and the enforcement of the above cybersecurity and overseas listing laws and regulation. There is no assurance that the relevant PRC governmental authorities would reach the same conclusion as us. If we and/or our subsidiaries are required to obtain approval or fillings from any governmental authorities, including the CAC and/or the CSRC, in connection with the listing or continued listing of our securities on a stock exchange outside of Hong Kong or mainland China, it is uncertain how long it will take for us and/or our subsidiaries to obtain such approval or complete such filing, and, even if we and our subsidiaries obtain such approval or complete such filing, the approval or filing could be rescinded. Any failure to obtain or a delay in obtaining the necessary permissions from or complete the necessary filing procedure with the PRC governmental authorities to conduct offerings or list outside of Hong Kong or mainland China may subject us and/or our subsidiaries to sanctions imposed by the PRC governmental authorities, which could include fines and penalties, suspension of business, proceedings against us and/or our subsidiaries, and even fines on the controlling shareholder and other responsible persons, and our subsidiaries’ ability to conduct our business, our ability to invest into mainland China as foreign investments or accept foreign investments, or our ability to list on a U.S. or other overseas exchange may be restricted, and our subsidiaries’ business, and our reputation, financial condition, and results of operations may be materially and adversely affected.

If the Chinese government chooses to extend the oversight and control over offerings that are conducted overseas and/or foreign investment in mainland China-based issuers to Hong Kong-based issuers, such action may significantly limit or completely hinder our ability to offer or continue to offer Ordinary Shares to investors and cause the value of our Ordinary Shares to significantly decline or be worthless.

Recent statements, laws and regulations by the Chinese government, including the Measures for Cybersecurity Review (2021), the PRC Personal Information Protection Law and the Trial Measures, have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China-based issuers. It is uncertain whether the Chinese government will adopt additional requirements or extend the existing requirements to apply to our Operating Subsidiaries located in Hong Kong. We could be subject to approval or review of Chinese regulatory authorities to pursue future offerings. Any future action by the PRC government expanding the categories of industries and companies whose foreign securities offerings are subject to review by the CSRC or CAC or filing with the CSRC could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless.

The enforcement of laws and rules and regulations in the PRC can change quickly with little advance notice. Additionally, the PRC laws and regulations and the enforcement of such that apply or are to be applied to Hong Kong can change quickly with little or no advance notice. As a result, the Hong Kong legal system embodies uncertainties which could limit the availability of legal protections, which could result in a material change in our Operating Subsidiaries’ operations and/or the value of the securities we are offering.

As one of the conditions for the handover of the sovereignty of Hong Kong to China, China accepted conditions such as Hong Kong’s Basic Law. The Basic Law ensured Hong Kong will retain its currency (the Hong Kong Dollar), legal system, parliamentary system, and people’s rights and freedom for fifty years from 1997. This agreement has given Hong Kong the freedom to function with a high degree of autonomy. The Special Administrative Region of Hong Kong is responsible for its domestic affairs, including, but not limited to, the judiciary and courts of last resort, immigration, and customs, public finance, currencies, and extradition. Hong Kong continues using the English common law system. However, if the PRC government attempts to alter its agreement to allow Hong Kong to function autonomously, this could potentially impact Hong Kong’s common law legal system and may in turn bring about uncertainty in, for example, the enforcement of our contractual rights. This could, in turn, materially and adversely affect our Operating Subsidiaries’ business and operations. Additionally, intellectual property rights and confidentiality protections in Hong Kong may not be as effective as in the United States or other countries. Accordingly, we cannot predict the effect of future developments in the Hong Kong legal system, including the promulgation of new laws, changes to existing laws or the interpretation or enforcement thereof, or the pre-emption of local regulations by national laws. These uncertainties could limit the legal protections available to us, including the ability to enforce agreements with the customers.

6

There are political risks associated with conducting business in Hong Kong.

All of our operations are in Hong Kong. Accordingly, the business operations and financial conditions of our Operating Subsidiaries will be affected by the political and legal developments in Hong Kong. Any adverse economic, social and/or political conditions, material social unrest, strike, riot, civil disturbance or disobedience, as well as significant natural disasters, may affect the market and may adversely affect our operations. Given the relatively small geographical size of Hong Kong, any of such incidents may have a widespread effect on our business operations, which could in turn adversely and materially affect our business, results of operations and financial condition.

Hong Kong is a special administrative region of the PRC and the basic policies of the PRC regarding Hong Kong are reflected in the Basic Law, namely, Hong Kong’s constitutional document, which provides Hong Kong with a high degree of autonomy and executive, legislative and independent judicial powers, including that of final adjudication under the principle of “one country, two systems”. However, there is no assurance that there will not be any changes in the political arrangement between PRC and Hong Kong and the economic, political and legal environment in Hong Kong in the future. Since all of our operations are based in Hong Kong, any change of such political arrangements may pose an immediate threat to the stability of the economy in Hong Kong, thereby directly and adversely affecting our results of operations and financial positions.

Based on certain recent development including the Law of the People’s Republic of China on Safeguarding National Security in the Hong Kong Special Administrative Region issued by the Standing Committee of the PRC National People’s Congress in June 2020, the U.S. State Department has indicated that the United States no longer considers Hong Kong to have significant autonomy from China and former President Trump signed an executive order and Hong Kong Autonomy Act, or HKAA, to remove Hong Kong’s preferential trade status and to authorize the U.S. administration to impose blocking sanctions against individuals and entities who are determined to have materially contributed to the erosion of Hong Kong’s autonomy. The United States may impose the same tariffs and other trade restrictions on exports from Hong Kong that it places on goods from Mainland China. These and other recent actions may represent an escalation in political and trade tensions involving the U.S, China and Hong Kong, which could potentially harm our business. It is difficult to predict the full impact of the HKAA on Hong Kong and companies with operations in Hong Kong like us. Furthermore, legislative or administrative actions in respect of China-U.S. relations could cause investor uncertainty for affected issuers, including us, and the market price of our Ordinary Shares could be adversely affected.

The enactment of Law of the PRC on Safeguarding National Security in the Hong Kong Special Administrative Region (the “Hong Kong National Security Law”) could impact our Hong Kong subsidiaries.

On June 30, 2020, the Standing Committee of the PRC National People’s Congress adopted the Hong Kong National Security Law. This law defines the duties and government bodies of the Hong Kong National Security Law for safeguarding national security and four categories of offences - secession, subversion, terrorist activities, and collusion with a foreign country or external elements to endanger national security - and their corresponding penalties. On July 14, 2020, the former U.S. President Donald Trump signed the Hong Kong Autonomy Act, or HKAA, into law, authorizing the U.S. administration to impose blocking sanctions against individuals and entities who are determined to have materially contributed to the erosion of Hong Kong’s autonomy. On August 7, 2020 the U.S. government imposed HKAA-authorized sanctions on eleven individuals, including former HKSAR chief executive Carrie Lam. On October14, 2020, the U.S. State Department submitted to relevant committees of Congress the report required under HKAA, identifying persons materially contributing to “the failure of the Government of China to meet its obligations under the Joint Declaration or the Basic Law.” The HKAA further authorizes secondary sanctions, including the imposition of blocking sanctions, against foreign financial institutions that knowingly conduct a significant transaction with foreign persons sanctioned under this authority. The imposition of sanctions may directly affect the foreign financial institutions as well as any third parties or customers dealing with any foreign financial institution that is targeted.

On March 19, 2024, the Legislative Council of Hong Kong passed the Safeguarding National Security bill. The Safeguarding National Security Ordinance (effective on March 23, 2024) was enacted according to the Article 23 of the Basic Law of the Hong Kong Special Administrative Region which stipulates that Hong Kong shall enact laws on its own to prohibit any act of treason, secession, sedition, subversion against the central people’s government, or theft of state secrets. The Safeguarding National Security Ordinance mainly covers five types of offences: treason, insurrection, offences in connection with state secrets and espionage, sabotage endangering national security and related activities, and external interference and organizations engaging in activities endangering national security. It is difficult to predict the full impact of the Hong Kong National Security Law and HKAA and the Safeguarding National Security Ordinance on Hong Kong and companies located in Hong Kong. If our Hong Kong subsidiaries are determined to be in violation of the Hong Kong National Security Law or the HKAA or the Safeguarding National Security Ordinance, by competent authorities, our business operations, financial position and results of operations could be materially and adversely affected.

7

Our subsidiaries may be subject to restrictions on paying dividends or making other payments to us, which may restrict their ability to satisfy liquidity requirements, conduct business and pay dividends to holders of our ordinary shares.

We are a holding company incorporated in the Cayman Islands with operations in Hong Kong. Accordingly, most of our cash is maintained in Hong Kong dollars. We rely in part on dividends from our Hong Kong subsidiaries for our cash and financing requirements, such as the funds necessary to service any debt we may incur.

There is currently no restriction or limitation under the laws of Hong Kong on the conversion of Hong Kong dollars into foreign currencies and the transfer of currencies out of Hong Kong and the foreign currency regulations of mainland China do not currently have any material impact on the transfer of cash between us and our Hong Kong subsidiaries. However, there is a possibility that certain PRC laws and regulations, including existing laws and regulations and those enacted or promulgated in the future were to become applicable to our Hong Kong subsidiaries in the future and the PRC government may prevent our cash maintained in Hong Kong from leaving or restrict the deployment of the cash into our business or for the payment of dividends in the future. Any such controls or restrictions, if imposed in the future and to the extent cash is generated in our Hong Kong subsidiaries and to the extent assets (other than cash) in our business are located in Hong Kong or held by a Hong Kong entity and may need to be used to fund operations outside of Hong Kong, may adversely affect our ability to finance our cash requirements, service debt or make dividend or other distributions to our shareholders. Furthermore, there can be no assurance that the PRC government will not intervene or impose restrictions on our ability to transfer or distribute cash within our organization, which could result in an inability or prohibition on making transfers or distributions to entities outside of Hong Kong and adversely affect our business.

The Hong Kong regulatory requirement of prior approval for the transfer of shares in excess of a certain threshold may restrict future takeovers and other transactions.

Section 132 of Securities and Futures Ordinance (Cap. 157 of the laws of Hong Kong) (the “SFO”) requires prior approval from the HKSFC for any company or individual to become a substantial shareholder of a HKSFC-licensed corporation in Hong Kong. Under the SFO, a person will be a “substantial shareholder” of a licensed company if he, either alone or with associates, has an interest in, or is entitled to control the exercise of, the voting power of more than 10% of the total number of issued shares of the licensed corporation, or exercises control of 35% or more of the voting power of a company that controls more than 10% of the voting power of the licensed company. Further, all potential parties who will be the new substantial shareholder(s) of the HKSFC-licensed subsidiaries, which are I Win Securities and I Win Asset Management, are required to seek prior approval from the HKSFC. This regulatory requirement may discourage, delay or prevent a change in control of Garden Stage, which could deprive the holders of our Ordinary Shares the opportunity to receive a premium for their Ordinary Shares as part of a future sale and may reduce the price of our Ordinary Shares upon the consummation of a future proposed business combination.

Risks Relating to our Ordinary Shares

Our corporate actions will be substantially controlled by our Controlling Shareholder, Oriental Moon Tree Limited, which will have the ability to control or exert significant influence over important corporate matters that require approval of shareholders, which may deprive you of an opportunity to receive a premium for your Ordinary Shares and materially reduce the value of your investment.

Oriental Moon Tree Limited, our Controlling Shareholder, beneficially owns 73.44% of our total issued and outstanding Ordinary Shares as of the date of this annual report. Accordingly, Oriental Moon Tree Limited will have significant influence in determining the outcome of any corporate transaction or other matter submitted to the shareholders for approval, including mergers, consolidations, election of directors and other significant corporate actions. Ms. Kam Yan Karen, LAU, through Courageous Wealth Limited, owns 64% of the equity interest in Oriental Moon Tree Limited, and she is the sole director of Oriental Moon Tree Limited. Ms. Kam Yan Karen, LAU is deemed as the beneficial owner of all Ordinary Shares held by Oriental Moon Tree Limited. Ms. Kam Yan Karen, LAU will be able to control the management and affairs of Garden Stage through Oriental Moon Tree Limited. This concentration of ownership may also discourage, delay or prevent a change in control of our company, which could deprive our shareholders of an opportunity to receive a premium for their shares as part of a sale of our company and might reduce the price of our Ordinary Shares. These actions may be taken even if they are opposed by our other shareholders.

8

The PCAOB may be unable to inspect or fully investigate our auditors as required under the Holding Foreign Companies Accountable Act,

or the HFCAA, as amended. If the PCAOB is unable to conduct such inspections for two consecutive years, the SEC will prohibit the trading

of our shares. The delisting of our shares, or the threat of their being delisted, may materially and adversely affect the value of your

investment. Additionally, the inability of the PCAOB to conduct inspections of our auditors would deprive our investors of the benefits

of such inspections.

On April 21, 2020, SEC Chairman Jay Clayton and PCAOB Chairman William D. Duhnke III, along with other senior SEC staff, released a joint statement highlighting the risks associated with investing in companies based in or have substantial operations in emerging markets including China. The joint statement emphasized the risks associated with lack of access for the PCAOB to inspect auditors and audit work papers in China and higher risks of fraud in emerging markets.

On May 18, 2020, Nasdaq filed three proposals with the SEC to (i) apply a minimum offering size requirement for companies primarily operating in a “Restrictive Market”, (ii) adopt a new requirement relating to the qualification of management or board of directors for Restrictive Market companies, and (iii) apply additional and more stringent criteria to an applicant or listed company based on the qualifications of the company’s auditors.

On May 20, 2020, the U.S. Senate passed the Holding Foreign Companies Accountable Act (“HFCAA”), requiring a foreign company to certify it is not owned or controlled by a foreign government if the PCAOB is unable to audit specified reports because the company uses a foreign auditor not subject to PCAOB inspection. If the PCAOB is unable to inspect the company’s auditors for three consecutive years, the issuer’s securities are prohibited to trade on a national securities exchange or in the over-the-counter trading market in the U.S. On December 2, 2020, the U.S. House of Representatives approved the HFCAA. On December 18, 2020, the HFCAA was signed into law.

On March 24, 2021, the SEC announced that it had adopted interim final amendments to implement congressionally mandated submission and disclosure requirements of the HFCAA. The interim final amendments will apply to registrants that the SEC identifies as having filed an annual report on Forms 10-K, 20-F, 40-F or N-CSR with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that the PCAOB has determined it is unable to inspect or investigate completely because of a position taken by an authority in that jurisdiction. The SEC will implement a process for identifying such a registrant and any such identified registrant will be required to submit documentation to the SEC establishing that it is not owned or controlled by a governmental entity in that foreign jurisdiction, and will also require disclosure in the registrant’s annual report regarding the audit arrangements of, and governmental influence on, such a registrant.

On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”), which was signed into law on December 29, 2022, amending the HFCAA and requiring the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchange if its auditor is not subject to PCAOB inspections for two consecutive years instead of three consecutive years.

On September 22, 2021, the PCAOB adopted a final rule implementing the HFCAA, which provides a framework for the PCAOB to use when determining, as contemplated under the HFCAA, whether the PCAOB is unable to inspect or investigate completely registered public accounting firms located in a foreign jurisdiction because of a position taken by one or more authorities in that jurisdiction.

On December 2, 2021, the SEC issued amendments to finalize rules implementing the submission and disclosure requirements in the HFCAA. The rules apply to registrants that the SEC identifies as having filed an annual report with an audit report issued by a registered public accounting firm that is located in a foreign jurisdiction and that PCAOB is unable to inspect or investigate completely because of a position taken by an authority in foreign jurisdictions.

On December 16, 2021, the PCAOB issued a report on its determinations that it is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, which determinations were vacated on December 15, 2022.

9

On August 26, 2022, the PCAOB announced that it had signed a Statement of Protocol (the “SOP”) with the China Securities Regulatory Commission and the Ministry of Finance of China. The SOP, together with two protocol agreements governing inspections and investigations (together, the “SOP Agreement”), establishes a specific, accountable framework to make possible complete inspections and investigations by the PCAOB of audit firms based in mainland China and Hong Kong, as required under U.S. law.

On December 15, 2022, the PCAOB announced that it was able to secure complete access to inspect and investigate PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong completely in 2022. The PCAOB Board vacated its previous 2021 determinations that the PCAOB was unable to inspect or investigate completely registered public accounting firms headquartered in mainland China and Hong Kong. However, whether the PCAOB will continue to be able to satisfactorily conduct inspections of PCAOB-registered public accounting firms headquartered in mainland China and Hong Kong is subject to uncertainties and depends on a number of factors out of our and our auditor’s control. The PCAOB continues to demand complete access in mainland China and Hong Kong moving forward and is making plans to resume regular inspections in early 2023 and beyond, as well as to continue pursuing ongoing investigations and initiate new investigations as needed. The PCAOB has also indicated that it will act immediately to consider the need to issue new determinations with the HFCAA if needed.

J&S Associate PLT (“J&S”), the independent registered public accounting firm that issues the audit report for the fiscal year ended March 31, 2024 and 2023 included in this annual report, is currently subject to PCAOB inspections and the PCAOB is thus able to inspect J&S Associate PLT. J&S Associate PLT is headquartered in Malaysia, and has recently been inspected by the PCAOB. Our former auditor, Marcum Asia CPAs LLP (“Marcum Asia”), the independent registered public accounting firm that issued the audit report for the fiscal year ended March 31, 2022 included in this annual report, as an auditor of companies that are traded publicly in the United States and a firm registered with the PCAOB, was subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess Friedman’s compliance with applicable professional standards. Our auditors are not headquartered in mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. Therefore, we believe that, as of the date of this annual report, our auditors are not subject to the PCAOB determinations.

Our ability to retain an auditor subject to PCAOB inspection and investigation, including but not limited to inspection of the audit working papers related to us, may depend on the relevant positions of U.S. and Chinese regulators. With respect to audits of companies with operations in China, such as the Company, there are uncertainties about the ability of our auditor to fully cooperate with a request by the PCAOB for audit working papers in China without the approval of Chinese authorities. Whether the PCAOB will be able to conduct inspections of our auditor, including but not limited to inspection of the audit working papers related to us, in the future is subject to substantial uncertainty and depends on a number of factors out of our, and our auditor’s, control. If our shares and shares are prohibited from trading in the United States, there is no certainty that we will be able to list on a non-U.S. exchange or that a market for our shares will develop outside of the United States. Such a prohibition would substantially impair your ability to sell or purchase our shares when you wish to do so, and the risk and uncertainty associated with delisting would have a negative impact on the price of our shares. Also, such a prohibition would significantly affect our ability to raise capital on terms acceptable to us, or at all, which would have a material adverse impact on our business, financial condition, and prospects.

The trading price of our Ordinary Shares may be volatile, which could result in substantial losses to you. Such volatility, including any stock run-ups, may be unrelated to our actual or expected operating performance and financial condition or prospects, making it difficult for prospective investors to assess the rapidly changing value of our Ordinary Shares.

The trading price of our Ordinary Shares is likely to be volatile and could fluctuate widely due to factors beyond our control. This may happen due to broad market and industry factors, such as performance and fluctuation in the market prices or underperformance or deteriorating financial results of other listed companies based in Hong Kong and Mainland China. The securities of some of these companies have experienced significant volatility since their initial public offerings, including, in some cases, substantial price declines in the trading price of their securities. The trading performances of other Hong Kong and Chinese companies’ securities after their offerings may affect the attitudes of investors towards Hong Kong-based, U.S.-listed companies, which consequently may affect the trading performance of our Ordinary Shares, regardless of our actual operating performance. In addition, any negative news or perceptions about inadequate corporate governance practices or fraudulent accounting, corporate structure or matters of other Hong Kong and Chinese companies may also negatively affect the attitudes of investors towards Hong Kong and Chinese companies in general, including us, regardless of whether we have conducted any inappropriate activities. Furthermore, securities markets may from time to time experience significant price and volume fluctuations that are not related to our operating performance, which may have a material and adverse effect on the trading price of our Ordinary Shares.

10

In addition to the above factors, the price and trading volume of our Ordinary Shares may be highly volatile due to multiple factors, including the following:

| ● | regulatory developments affecting us or our industry; |

| ● | variations in our revenues, profit, and cash flow; |

| ● | the general market reactions and financial market fluctuation due to the continuous Russo-Ukraine conflicts; |

| ● | changes in the economic performance or market valuations of other financial services firms; political, social and economic conditions of the PRC and Hong Kong; |

| ● | actual or anticipated fluctuations in our quarterly results of operations and changes or revisions of our expected results; |

| ● | fluctuations of exchange rates among Hong Kong dollar, Renminbi, and the U.S. dollar; |

| ● | changes in financial estimates by securities research analysts; |

| ● | detrimental negative publicity about us, our services, our officers, directors, Controlling Shareholder, other beneficial owners, our business partners, or our industry; |

| ● | announcements by us or our competitors of new service offerings, acquisitions, strategic relationships, joint ventures, capital raisings or capital commitments; |

| ● | additions to or departures of our senior management; |

| ● | litigation or regulatory proceedings involving us, our officers, directors, or Controlling Shareholder; |

| ● | release or expiry of lock-up or other transfer restrictions on our outstanding Ordinary Shares; and |

| ● | sales or perceived potential sales of additional Ordinary Shares. |

Any of these factors may result in large and sudden changes in the volume and price at which our Ordinary Shares will trade.

Recently, there have been instances of extreme stock price run-ups followed by rapid price declines and strong stock price volatility with a number of recent initial public offerings, especially among companies with relatively smaller public floats. As a relatively small-capitalization company with relatively small public float, we may experience greater stock price volatility, extreme price run-ups, lower trading volume and less liquidity than large-capitalization companies. In particular, our Ordinary Shares may be subject to rapid and substantial price volatility, low volumes of trades and large spreads in bid and ask prices. Such volatility, including any stock-run up, may be unrelated to our actual or expected operating performance, financial conditions or prospects, making it difficult for prospective investors to assess the rapidly changing value of our Ordinary Shares.

In addition, if the trading volumes of our Ordinary Shares are low, persons buying or selling in relatively small quantities may easily influence prices of our Ordinary Shares. This low volume of trades could also cause the price of our Ordinary Shares to fluctuate greatly, with large percentage changes in price occurring in any trading day session. Holders of our Ordinary Shares may also not be able to readily liquidate their investment or may be forced to sell at depressed prices due to low volume trading. Broad market fluctuations and general economic and political conditions may also adversely affect the market price of our Ordinary Shares. As a result of this volatility, investors may experience losses on their investment in our Ordinary Shares. A decline in the market price of our Ordinary Shares also could adversely affect our ability to issue additional shares of Ordinary Shares or other securities and our ability to obtain additional financing in the future. No assurance can be given that an active market in our Ordinary Shares will develop or be sustained. If an active market does not develop, holders of our Ordinary Shares may be unable to readily sell the shares they hold or may not be able to sell their shares at all.

11

In the past, shareholders of public companies have often brought securities class action suits against those companies following periods of instability in the market price of their securities. If we were involved in a class action suit, it could divert a significant amount of our management’s attention and other resources from our business and operations and require us to incur significant expenses to defend the suit, which could harm our results of operations. Any such class action suit, whether or not successful, could harm our reputation and restrict our ability to raise capital in the future. In addition, if a claim is successfully made against us, we may be required to pay significant damages, which could have a material adverse effect on our financial conditions and results of operations.

If securities or industry analysts do not publish or publish inaccurate or unfavorable research about our business, or if they adversely change their recommendations regarding our Ordinary Shares, the market price for our Ordinary Shares and trading volume could decline.

The trading market for our Ordinary Shares will depend in part on the research and reports that securities or industry analysts publish about us or our business. If research analysts do not establish and maintain adequate research coverage or if one or more of the analysts who covers us downgrades our Ordinary Shares or publishes inaccurate or unfavorable research about our business, the market price for our Ordinary Shares would likely decline. If one or more of these analysts cease coverage of the Company or fail to publish reports on us regularly, we could lose visibility in the financial markets, which, in turn, could cause the market price or trading volume for our Ordinary Shares to decline.

Because the amount, timing, and whether or not we distribute dividends at all is entirely at the discretion of our board of directors, you must rely on price appreciation of our Ordinary Shares for return on your investment.