As filed with the Securities and Exchange Commission on February 27, 2023.

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 2 TO FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Qilun Group Inc.

(Exact name of Registrant as specified in its charter)

| Cayman Islands | 5190 | Not applicable | ||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification Number) |

Room 2201, Modern International Building, No. 3038, Jintian Road, Gangxia Community, Futian Street Futian District, Shenzhen City, Guangdong Province People’s Republic of China +86-755-83985414 |

| (Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices) |

Mark E. Crone, Esq. The Crone Law Group, PC 420 Lexington Avenue, Suite 2446 New York, NY 10170 (646) 861-7891 |

| (Name, address, including zip code, and telephone number, including area code, of agent for service) |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on the Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

COPIES OF COMMUNICATIONS TO:

| Mark Crone, Esq. | Florence Chan, Esq. | |

| Mason Allen, Esq. | Ogier | |

| The Crone Law Group P.C. | 11th Floor, Central Tower | |

| 420 Lexington Ave, Suite 2446 | 28 Queen's Road Central, Central | |

| New York, NY 10170 | Hong Kong 999077 | |

| Phone: (646) 861-7891 | Phone: (852) 36566061 |

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OF 1933 OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SECTION 8(a), MAY DETERMINE.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the United States Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting any offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated , 2023

QILUN GROUP INC.

16,550,000 Ordinary Shares

This prospectus relates to the offer and resale of an aggregate 16,550,000 Ordinary Shares, $0.0001 par value (the “Shares”), of Qilun Group Inc. (the “Company,” “Qilun,” “we,” or “our”), all of which were issued by us in a private placement transaction pursuant to securities purchase agreements (each a “Purchase Agreement”) at a purchase price of $0.20 per share. The holders of the shares are each referred to herein as a “Selling Stockholder” and collectively as the “Selling Stockholders.”

There is currently no public trading market for the Shares. The offering is contingent on obtaining a listing or quotation of the Shares on an existing public market. We expect the selling stockholders to sell at an initial fixed price of $0.20 per Share upon listing or quotation on an existing public trading market, and thereafter at prevailing market prices or privately negotiated prices.

The Selling Stockholders, or their respective transferees, pledgees, donees or other successors-in-interest, may sell the Shares through public or private transactions at prevailing market prices, at prices related to prevailing market prices or at privately negotiated prices. The Selling Stockholders may sell any, all or none of the securities offered by this prospectus, and we do not know when or in what amount the Selling Stockholders may sell their Shares hereunder following the effective date of this registration statement. We provide more information about how a Selling Stockholder may sell its Shares in the section titled “Plan of Distribution” on page 82.

We are registering the Shares on behalf of the Selling Stockholders, to be offered and sold by them from time to time. We will not receive any proceeds from the sale of the Shares by the Selling Stockholders in the offering described in this prospectus. We have agreed to bear all of the expenses incurred in connection with the registration of the Shares. The Selling Stockholders will pay or assume discounts, commissions, fees of underwriters, selling brokers or dealer managers and similar expenses, if any, incurred for the sale of the Shares.

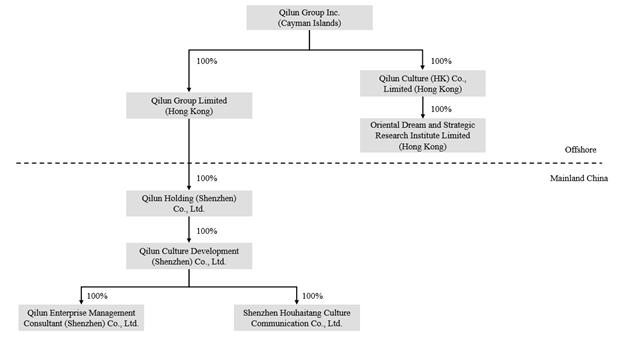

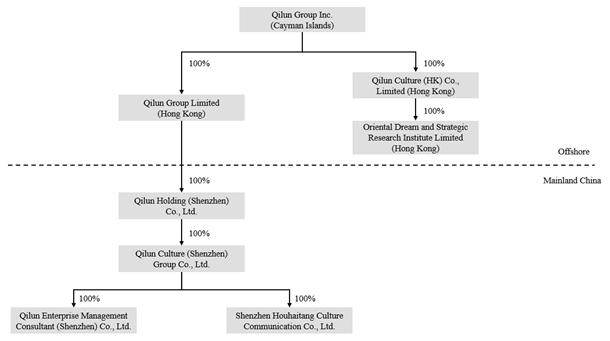

Qilun is an exempted company with limited liability incorporated under the laws of the Cayman Islands on May 24, 2022. The Company is the 100% owner of the Company’s Hong Kong operating subsidiary: Qilun Culture (HK) Co., Limited (“Qilun Culture (HK)”), a limited company that was organized under the laws of Hong Kong on November 12, 2021. Qilun Culture (HK) is the 100% owner of Oriental Dream and Strategic Research Institute Limited, a limited company that was organized under the laws of Hong Kong on October 31, 2022. The Company is also the 100% owner of Qilun Group Limited (“Qilun Group (HK)”), a limited company that was organized under the laws of Hong Kong on June 14, 2022. Qilun Group (HK) is the 100% owner of the Company’s intermediate holding company Qilun Holding (Shenzhen) Co., Ltd. (“Qilun Holding (Shenzhen)”), a PRC company organized under the laws of the People’s Republic of China (the “PRC”) on August 29, 2022. Qilun Holding (Shenzhen) is the 100% owner of the Company’s PRC operating subsidiary: Qilun Culture (Shenzhen) Group Co., Ltd. (“Qilun Culture (Shenzhen)”), a limited company organized under the laws of the PRC on February 26, 2021. Qilun Culture (Shenzhen) was wholly acquired by Qilun Holding (Shenzhen) in October 2022. Qilun Culture (Shenzhen) is the 100% owner of the Company’s PRC operating subsidiaries:

| 1. | Shenzhen Houhaitang Culture Communication Co., Ltd. (“Shenzhen Houhaitang”), a limited company organized under the laws of the PRC on March 31, 2014, and wholly acquired by Qilun Culture (Shenzhen) on December 31, 2021; and | |

| 2. | Qilun Enterprise Management Consultant (Shenzhen) Co., Ltd. (“Qilun Enterprise Management Consultant”), a limited company organized under the laws of the PRC on December 7, 2021. |

Investing in our ordinary shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 10 to read about factors you should consider before buying our ordinary shares.

We are both an “emerging growth company” and a “foreign private issuer” as defined under applicable U.S. securities laws and are eligible for reduced public company reporting requirements. Please read the disclosures beginning on page 7 of this prospectus for more information.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2023.

We are not a Chinese operating company but a Cayman Islands holding company. We have no material operations of our own and conduct substantially all of the operations through the operating entities in China and, to a more limited extent, in the special administrative region of Hong Kong. We currently have no operations in Hong Kong but may conduct strategy and management consulting, industry research reports, senior management training and certification courses in the future in that special administrative region. Investors in our ordinary shares are purchasing equity interests in the Cayman Islands holding company, and not in the Chinese or Hong Kong operating entities. Investors in our ordinary shares may never hold equity interests in the Chinese or Hong Kong operating entities. Our operating structure involves unique risks to investors. The Chinese regulatory authorities could disallow our operating structure, which would likely result in a material change in our operations and/or a material change in the value of our ordinary shares, and could cause the value of our ordinary shares to significantly decline or become worthless. See “Risk Factors — Risks Related to Doing Business in China — If the Chinese government chooses to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless” beginning on page 18 of this prospectus. In addition, Chinese regulatory authorities could change the rules and regulations regarding foreign ownership in the Chinese cultural and creative art collectibles, art house decorations and artwork home goods industries. The same legal, regulatory, operating and investment risks applicable to our operations in China also apply to any operations which way may conduct in the special administrative regions of Hong Kong and Macau.

As used in this prospectus, terms such as “the Company,” “we,” “us,” “our company,” or “our” refer to Qilun Group Inc., unless the context suggests otherwise, and when describing Qilun Group Inc.’s consolidated financial information, also includes the Chinese operating entities. We directly hold 100% equity interests in the operating entities in China, and we do not currently use a variable interest entity (“VIE”) structure. See “Our History and Corporate Structure” beginning on page 36 of this prospectus.

As of the date of this prospectus, we have not maintained any cash management policies that dictate the purpose, amount and procedure of fund transfers among our Cayman Islands holding company, our subsidiaries, or investors. Rather, the funds can be transferred in accordance with the applicable laws and regulations. We will rely on dividends paid by our operating subsidiaries in the PRC and, possibly in the future, our formed but not yet operational subsidiary in Hong Kong, to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating subsidiaries by the PRC government to transfer cash or assets could have a material and adverse effect on our business. To the extent cash in the business is in accounts located in the PRC or Hong Kong, or held at a PRC or Hong Kong operating entity, the cash may not be available to fund operations or for other use outside of the PRC or Hong Kong due to interventions in or the imposition of restrictions and limitations by the PRC government on the ability of you or your subsidiaries to transfer cash outside of the PRC or Hong Kong. See “Risk Factors — We rely on dividends and other distributions on equity paid by the operating entities to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets could have a material and adverse effect on our business.” and “Prospectus Summary — Cash Transfers and Dividend Distributions.” As of the date of this prospectus, the Cayman Islands holding company has not declared or paid dividends or made distributions to the Chinese operating entities or to investors in the past, nor any dividends or distributions were made by a Chinese operating entity to the Cayman Islands holding company. Our Director has complete discretion on whether to distribute dividends, subject to applicable laws. We do not have any current plan to declare or pay any cash dividends on our ordinary shares in the foreseeable future after this offering. See “Risk Factors — Risks Related to This Offering and the Shares — We currently do not expect to pay dividends in the foreseeable future after this offering and you must rely on price appreciation of our ordinary shares for return on your investment” beginning on page 30 of this prospectus. Subject to certain contractual, legal and regulatory restrictions, cash and capital contributions may be transferred among our Cayman Islands holding company and the Chinese operating entities. If needed, the Cayman Islands holding company can transfer cash to the Chinese operating entities through loans and/or capital contributions, and the Chinese operating entities can transfer cash to our Cayman Islands holding company through loans and/or issuing dividends or other distributions. There are limitations on the ability to transfer cash between the Cayman Islands holding company, the Chinese operating entities or investors. Cash transfers from the Cayman Islands holding company to the Chinese operating entities are subject to the applicable PRC laws and regulations on loans and direct investment. See the Consolidated Financial Statements of the Company beginning on page F-1 and “Risk Factors — Risks Related to Doing Business in China — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us to make loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business” beginning on page 22 of this prospectus. If any of the operating entities incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to the Cayman Islands holding company. Cash transfers from the Chinese operating entities to the Cayman Islands holding company are also subject to the current PRC regulations, which permit the Chinese operating entities to pay dividends to their shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. See “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by the operating entities to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets could have a material and adverse effect on our business” beginning on page 22 of this prospectus. Cash transfers from the Cayman Islands holding company to the investors are subject to the restrictions on the remittance of Renminbi into and out of China and governmental control of currency conversion. See “Risk Factors — Risks Related to Doing Business in China — Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment” beginning on page 25 of this prospectus. Additionally, to the extent cash or assets in the business is in China or a Chinese operating entity, the funds or assets may not be available to fund operations or for other use outside of China due to interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets.

As substantially all of our operations are conducted by the operating entities in China. We currently have no operations in Hong Kong but may conduct strategy and management consulting, industry research reports, senior management training and certification courses in the future in that special administrative region. We are subject to the associated legal and operational risks, including risks related to the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United States regulations, which risks could result in a material change in our operations and/or cause the value of our ordinary shares to significantly decline or become worthless, and affect our ability to offer or continue to offer securities to investors. Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, and adopting new measures to extend the scope of cybersecurity reviews. According to our PRC legal counsel, DeHeng Law Offices (Shenzhen), as of the date of this prospectus, our PRC subsidiaries have received from PRC authorities all requisite licenses, permissions or approvals needed to engage in the businesses currently conducted in China and neither we nor the operating entities have been subject to any investigation, or received any notice, warning, or sanction from the China Securities Regulatory Commission (the “CSRC”), the Cyberspace Administration of China (the “CAC”), or other applicable government authorities related to this offering. In addition, neither we nor the operating entities have been involved in any review, investigation, enquiry, penalty, or other legal proceedings initiated by the CSRC, the CAC, or other applicable governmental or regulatory authorities or third parties in relation to this offering. However, since these statements and regulatory actions by the PRC government authorities are newly published and the official guidance and related implementation rules have not been issued, it is highly uncertain what the potential impact such modified or new laws and regulations will have on operations of the operating entities, the ability to accept foreign investments and list on an U.S. stock exchange. The PRC government authorities may in the future promulgate laws, regulations or implementing rules that requires our company, or any of our subsidiaries to obtain regulatory approval from Chinese authorities before listing in the U.S. See “Risk Factors — Risks Related to Doing Business in China” beginning on page 18 of this prospectus for a discussion of these legal and operational risks.

Pursuant to the Holding Foreign Companies Accountable Act (“HFCAA”), the Public Company Accounting Oversight Board (the “PCAOB”) issued a Determination Report on December 16, 2021 which found that the PCAOB is unable to inspect or investigate completely registered public accounting firms headquartered in: (1) mainland China of the People’s Republic of China because of a position taken by one or more authorities in mainland China; and (2) Hong Kong, a Special Administrative Region and dependency of the PRC, because of a position taken by one or more authorities in Hong Kong. In addition, the PCAOB’s report identified the specific registered public accounting firms which are subject to these determinations. Our registered public accounting firm, Assentsure PAC, is not headquartered in mainland China or Hong Kong and was not identified in this report as a firm subject to the PCAOB’s determination. Notwithstanding the foregoing, if the PCAOB is not able to fully conduct inspections of our auditor’s work papers in China, you may be deprived of the benefits of such inspection which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities may be prohibited under the HFCAA.

On August 26, 2022, the China Securities Regulatory Commission (“CSRC”), the Ministry of Finance of China, and the PCAOB signed a protocol governing inspections and investigations of audit firms based in China and Hong Kong. which could prevent China-based, U.S.-listed firms from being delisted pursuant to the HFCAA. On December 15, 2022, the PCAOB issued a new Determination Report which: (1) vacated the December 16, 2021 Determination Report; and (2) concluded that the PCAOB has been able to conduct inspections and investigations completely in the PRC in 2022. The December 15, 2022 Determination Report cautions, however, that authorities in the PRC might take positions at any time that would prevent the PCAOB from continuing to inspect or investigate completely. As required by the HFCAA, if in the future the PCAOB determines it no longer can inspect or investigate completely because of a position taken by an authority in the PRC, the PCAOB will act expeditiously to consider whether it should issue a new determination. If the PCAOB is not able to fully conduct inspections of our auditor’s work papers in China, you may be deprived of the benefits of such inspection which could result in limitation or restriction to our access to the U.S. capital markets and trading of our securities may be prohibited under the HFCAA. Under the HFCAA, our securities may be prohibited from trading on the Nasdaq or other U.S. stock exchanges if our auditor is not inspected by the PCAOB for three consecutive years, and this ultimately could result in our Ordinary Shares being delisted. Furthermore, on June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act (“AHFCAA”), which became law on December 29, 2023, and amends the HFCAA and requires the SEC to prohibit an issuer’s securities from trading on any U.S. stock exchanges if its auditor is not subject to PCAOB inspections for two consecutive years instead of three. See “Risk Factors — Risks Related to This Offering and the Shares — Although the audit report included in this prospectus was issued by Singapore auditors who are currently inspected by the PCAOB, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, investors would be deprived of the benefits of such inspection and our ordinary shares may be delisted or prohibited from trading” beginning on page 24 of this prospectus.

There has been no market for our securities and a public market may not develop, or, if any market does develop, it may not be sustained. We intend to seek quotation of our ordinary shares on the OTCQB after effectiveness of the registration statement of this prospectus. Quotation of our ordinary shares on the OTCQB will require a market maker filing an application to quote our ordinary shares and approval of that application. We do not have a market maker willing to file the necessary application for quoting our shares on the OTCQB as of the date of this prospectus. There is a risk that no public market will develop for our Shares.

Table of Contents

You should rely only on the information contained in this prospectus. Neither we, nor the Selling Stockholders have authorized anyone to provide information different from that contained in this prospectus. The Selling Stockholders are offering to sell, and seeking offers to buy, Shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our Shares.

Conventions that Apply to this Prospectus

Our financial statements have been prepared in accordance with generally accepted accounting principles in the United States (“US GAAP”). We present our consolidated financial statements in U.S. dollars.

Our fiscal year ends on December 31 of each year. References to fiscal 2021 are references to the fiscal year ended December 31, 2021 and references to fiscal 2020 are references to the fiscal year ended December 31, 2020. Some amounts in this prospectus may not total due to rounding. All percentages have been calculated using unrounded amounts.

Throughout this prospectus, we provide a number of key performance indicators used by our management and often used by competitors in our industry. These and other key performance indicators are discussed in more detail in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” We define certain terms used in this prospectus as follows:

Unless otherwise indicated or the context otherwise requires, references in this prospectus to:

| ● | “Shares” are to our Ordinary Shares, $0.0001 par value per share; | |

| ● | “China” or the “PRC” are to the People’s Republic of China, excluding, for the purposes of this prospectus only, Hong Kong, Macau and Taiwan; | |

| ● | Depending on the context, “we,” “us,” “our company,” “our,”, “the Company”, and “Qilun” refer to Qilun Group Inc., an exempted company with limited liability incorporated under the laws of the Cayman Islands company, its subsidiaries, Qilun Group (HK), Qilun Culture (HK), Qilun Holding (Shenzhen), Qilun Culture (Shenzhen), Qilun Enterprise Management Consultant, and Shenzhen Houhaitang; | |

| ● | “Qilun Group (HK)” are to the wholly owned subsidiary of Qilun Group Inc., Qilun Group Limited, a limited company that was organized under the laws of Hong Kong; | |

| ● | “Qilun Culture (HK)” are to the wholly owned subsidiary of Qilun Group Inc., Qilun Culture (HK) Co., Limited, a limited company that was organized under the laws of Hong Kong; | |

| ● | “Qilun Holding (Shenzhen)” are to the wholly owned subsidiary of Qilun Group (HK), Qilun Holding (Shenzhen) Co., Ltd., a PRC limited liability company; | |

| ● | “Qilun Culture (Shenzhen)” are to the wholly owned subsidiary of Qilun Holding (Shenzhen), Qilun Culture (Shenzhen) Group Co., Ltd. (previously known as Qilun Culture Development (Shenzhen) Co., Ltd.), a PRC limited liability company; | |

| ● | “Qilun Enterprise Management Consultant” are to the wholly owned subsidiary of Qilun Culture (Shenzhen), Qilun Enterprise Management Consultant (Shenzhen) Co., Ltd., a PRC limited liability company; | |

| ● | “RMB” or “Renminbi” are to the legal currency of the People’s Republic of China; | |

| ● | “Shenzhen Houhaitang” are to the wholly owned subsidiary of Qilun Culture (Shenzhen), Shenzhen Houhaitang Culture Communication Co., Ltd., a PRC limited liability company; | |

| ● | “OD&SR Institute” are to the wholly owned subsidiary of Qilun Culture (HK), Oriental Dream and Strategic Research Institute Limited, a limited company that was organized under the laws of Hong Kong; | |

| ● | “Yuan” or “¥” are to the primary unit of account of the Renminbi (RMB), the legal currency of the People’s Republic of China; and | |

| ● | “US$,” “U.S. dollars,” “$,” or “dollars” are to the legal currency of the United States. | |

Our reporting currency is the U.S. Dollar. The functional currency of the Company in the PRC is the Renminbi.

This disclosure contains translations of certain Renminbi amounts into U.S. dollar amounts at specified rates solely for the convenience of the reader. The relevant exchange rates are listed below:

| For

the Year Ended December 31, 2021 | For

the Year Ended December 31, 2020 | |||||||

| Year ended USD: RMB exchange rate | 6.3614 | 6.5326 | ||||||

| Average yearly USD: RMB: exchange rate | 6.4518 | 6.6020 | ||||||

Market and industry data

Unless otherwise indicated, information in this prospectus concerning economic conditions, our industry, our markets and our competitive position is based on a variety of sources, information from independent industry analysts and publications, as well as our own estimates and research.

Our estimates are derived from publicly available information released by third-party sources, as well as data from our internal research, which we believe to be reasonable. None of the independent industry publications used in this prospectus were prepared on our behalf.

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements appearing elsewhere in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks of investing in our Shares discussed under “Risk Factors,” before deciding whether to invest in our Shares.

Our Business

General

Qilun is in the business of the research, development, design, outsourced production and sales of Chinese cultural and creative art collectibles, art house decorations and artwork home goods. As a pioneer of an innovative brand of new Chinese culture, the Company partners with famous artists and brand experts from all over the world to explore the practice and product application value of this new emerging Chinese culture.

In the process of research, development and design, the Company integrates many Chinese cultural elements and the intellectual property of well-known artists, including original and reproduced paintings and other visual arts, home decorations, home goods and other products. Our products are distributed and sold in a variety of provinces and regions across China.

The Company believes its cultural and creative products are grounded in Chinese cultural themes which derive market value through creative transformation and presentation of such cultural themes. Our value-added products rely on the wisdom, skills and talents of our content-creating designers and artists. We derive success through the commercial development and application of our creative counterparties’ intellectual property.

Our Products and Services

Our principal product lines consist of:

| ● | Original paintings and calligraphy artwork – original paintings and calligraphy artworks made by our partner artists (each original painting or calligraphy artwork is unique); | |

| ● | High-quality reproductions – high-quality reproductions of original painting and calligraphy artworks produced with high resolution reproduction technologies (in which the quality of the reproduction is highly comparable to the original artwork while the retail price is much lower than the price of the original artwork); | |

| ● | Art house decorations – interior decorations reflecting the Company’s innovative Chinese cultural elements, inspired by Chinese traditions, including decorative swords, scales, tea pots and tea cups; | |

| ● | Artwork home goods – home goods including bookmarks, notebooks, mugs and other goods that are used in daily life; | |

| ● | Retail sales of books – the Company sells books published by third-party publishers to retail customers; and | |

| ● | Services – the Company provides ancillary research, design, planning, exhibition installation, video recording and production services. |

| 1 |

The Company takes efforts to develop new types of art house decorations and artwork home goods.

Key Growth Strategies

Key components of our growth strategy include the following:

| ● | Cooperating with more artists, artwork designers and content-creators to increase our intellectual property and proprietary brands; | |

| ● | Expanding our product lines to cater to demands of different types of customers; and | |

| ● | Enhancing our brand through various online and offline promotion programs and activities. |

Our Strengths

We are dedicated to the development, design, production and sales of high quality products that reflect our innovative brand of new Chinese culture, inspired by five thousand years of Chinese tradition. Our competitive strengths include:

| ● | Discovery of leading designers and artists: We have gathered leading designers and artists of high-end luxury brands in the cultural and creative arts industry, and have developed deep cooperation with our content-creator counterparties. In cooperation with these artists, we have created a series of proprietary brands including: |

| ○ | Baihua Huagui Map, | |

| ○ | Baihua National gift purple sand, and | |

| ○ | Zen calligraphy and cultural creation. |

We believe our proprietary brands and products are widely loved by our customers. The Company currently has close relationships with multiple artists and have collaborated with additional artists in China through licensing or collaborative arrangements.

| ● | Strong intellectual property creation and operations: We have applied for patent rights or other intellectual property protection for every creative product created by the Company and our creative counterparties. With the support of our strong high-end intellectual property creation and operations, we continue to attract leading artists to establish long-term commercial and creative relationships with us, effectively forming a virtuous circle from intellectual property creation to intellectual property operations. As a promoter of the Chinese cultural and creative industries, we have promoted the commercialization of high-end cultural and creative products in China and formed what we believe to be a large and loyal fan community. | |

| ● | Mission focused management team: Our management team is a leading factor in the development of China’s high-end cultural and creative products industry. We believe the management team’s insights into market trends and industry trends, as well as the creation of cultural and creative intellectual property and operations, are the main reasons why Qilun Culture has grown rapidly and occupies a leading position in the industry in the southern region of China. The management team is highly experienced in the industry, with an average of over 15 years of brand management experience. |

Our Challenges

The Company notes the following operational, marketing, and strategic challenges:

| ● | Our limited operating history makes it difficult to assess the business and prospects in our highly competitive, rapidly evolving and customer-oriented market. | |

| ● | Failure to attract, maintain and enhance relationships with designer, creator and artist counterparties, as well as retail- and commercial distributors and merchants, will adversely affect profitability and operations. | |

| ● | Failure to meet the needs of consumers and attract and retain consumers, or failure to adapt products or business models to the changing needs of such consumers, may have a material adverse impact on the business. | |

| ● | Our past growth rate is not necessarily an indicator of our future performance, and our success depends on our ability to execute our business strategy. | |

| ● | The business, operating results and financial condition may be adversely affected by the COVID-19 pandemic. |

| 2 |

Future Business Plans

Based on market feedback and consumer recognition, we plan to develop new products and services lines, and to partner with more well-known artists and content creators. We expect to improve our sales network to effectively reach our target customers and provide a superb purchase experience for high-end retail consumers.

RISK FACTOR SUMMARY

Risks Related to Our Business

| ● | Our operating history may not be indicative of our future growth or financial results and we may not be able to sustain our historical growth rates. | |

| ● | The global economy and the financial markets may negatively affect our business and clients, as well as the supply of and demand for works of art. | |

| ● | The demand for art and collectibles is unpredictable, which may cause significant variability in our results of operations. | |

| ● | As an artwork company and creator and distributor of cultural and creative collectibles and artisanal home goods, we cannot guarantee that we will be able to design and develop products that are popular with consumers or that we will be able to maintain the popularity of our successful products. | |

| ● | Despite our marketing efforts, we may not be able to promote and maintain our brand in an effective and cost-efficient way and our business and results of operations may be harmed accordingly. | |

| ● | We operate in a highly competitive industry and may lose market share or experience margin erosion if we are unable to compete effectively. | |

| ● | Fraudulent activity in our marketplace could negatively impact our operating results, brand and reputation and cause the use of our services to decrease. |

Risks Relating to Our Operations

| ● | Our limited operating history and our volatile historical results of operations could make it difficult for us to forecast our business and assess the seasonality and volatility in our business. | |

| ● | The ongoing global coronavirus COVID-19 outbreak had caused significant disruptions in our business, which we expect will materially and adversely affect our results of operations and financial condition. | |

| ● | We have engaged in transactions with related parties, and such transactions present possible conflicts of interest that could have an adverse effect on our business and results of operations. | |

| ● | We may not be able to successfully expand into new cities or markets or expand within cities or markets where we already have a presence. | |

| ● | Failure to monitor the quality of our products could adversely affect our business. | |

| ● | We face the risk of fluctuations in the cost, availability and quality of our raw materials, which could adversely affect our results of operations. | |

| ● | We do not have long term contracts with our suppliers and they can reduce order quantities or terminate their sales to us at any time. | |

| ● | Due to the nature of our business, valuable works of art are stored at our facilities. Such works of art could be subject to damage or theft, which could have a material adverse effect on our operations, reputation and brand. | |

| ● | The relative lack of public company experience of our management team may put us at a competitive disadvantage. | |

| ● | Increases in labor costs in the PRC may adversely affect our business and results of operations. | |

| ● | If we are unable to build and maintain sufficient sales and distribution network to meet increasing demand of our products, our ability to execute on our business plan as outlined in this prospectus will be impaired. |

| 3 |

Risks Related to Our Corporate Structure

| ● | You may face difficulties in protecting your interests, and your ability to protect your rights through U.S. courts may be limited, because we are incorporated under Cayman Islands law. | |

| ● | Recently introduced economic substance legislation of the Cayman Islands may impact the Company or its operations. | |

| ● | Certain judgments obtained against us by our shareholders may not be enforceable. |

Risks Related to Doing Business in China and Hong Kong

| ● | Because all of our operations are in China, our business is subject to the complex and rapidly evolving laws and regulations there. The Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our Shares. — See “Risks Related to Doing Business in China and Hong Kong — Because all of our operations are in China and Hong Kong, our business is subject to the complex and rapidly evolving laws and regulations there. The Chinese government may exercise significant oversight and discretion over the conduct of our business and may intervene in or influence our operations at any time, which could result in a material change in our operations and/or the value of our Shares” on page 18 for more information. | |

| ● | If the Chinese government chooses to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless. — See “Risks Related to Doing Business in China and Hong Kong —If the Chinese government chooses to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers, such action could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of such securities to significantly decline or be worthless” on page 18 for more information. | |

| ● | The uncertainties in the PRC legal system may subject our structure to different interpretations or enforcement challenges, or subject us to severe penalties or force us to relinquish our interests in our operations. — See “Risks Related to Doing Business in China and Hong Kong — The uncertainties in the PRC legal system may subject our structure to different interpretations or enforcement challenges, or subject us to severe penalties or force us to relinquish our interests in our operations” on page 19 for more information. | |

| ● | Recent greater oversight by the Cyberspace Administration of China (the “CAC”) over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact our business and our offering. — See “Risks Related to Doing Business in China and Hong Kong — Recent greater oversight by the Cyberspace Administration of China (the “CAC”) over data security, particularly for companies seeking to list on a foreign exchange, could adversely impact our business and our offering” on page 19 for more information. | |

| ● | Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and operations. — See “Risks Related to Doing Business in China and Hong Kong — Changes in China’s economic, political or social conditions or government policies could have a material adverse effect on our business and operations” on page 20 for more information. | |

| ● | Non-compliance with labor-related laws and regulations of the PRC may have an adverse impact on our financial condition and results of operation. — See “Risks Related to Doing Business in China and Hong Kong — Non-compliance with labor-related laws and regulations of the PRC may have an adverse impact on our financial condition and results of operation” on page 20 for more information. | |

| ● | Uncertainties with respect to the PRC legal system could adversely affect us. — See “Risks Related to Doing Business in China and Hong Kong — Uncertainties with respect to the PRC legal system could adversely affect us” on page 21 for more information. | |

| ● | You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our management named in the prospectus based on foreign laws. — See “Risks Related to Doing Business in China and Hong Kong — You may experience difficulties in effecting service of legal process, enforcing foreign judgments or bringing actions in China against us or our management named in the prospectus based on foreign laws” on page 22 for more information. | |

| ● | We may rely on dividends and other distributions on equity paid by the operating entities to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets could have a material and adverse effect on our business. — See “Risks Related to Doing Business in China and Hong Kong — We may rely on dividends and other distributions on equity paid by the operating entities to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets could have a material and adverse effect on our business” on page 22 for more information. | |

| ● | PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from making loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business. — See “Risks Related to Doing Business in China and Hong Kong — PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from making loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business” on page 22 for more information. | |

| ● | We may be exposed to liabilities under the Foreign Corrupt Practices Act and Chinese anti-corruption laws. — See “Risks Related to Doing Business in China and Hong Kong — We may be exposed to liabilities under the Foreign Corrupt Practices Act and Chinese anti-corruption laws” on page 23 for more information. | |

| ● | Restrictions on the remittance of Renminbi into and out of China and governmental control of currency conversion may limit our ability to pay dividends and other obligations, and affect the value of your investment. — See “Risks Related to Doing Business in China and Hong Kong — Restrictions on the remittance of Renminbi into and out of China and governmental control of currency conversion may limit our ability to pay dividends and other obligations, and affect the value of your investment” on page 23 for more information. | |

| ● | Although the audit report included in this prospectus was issued by Singapore auditors who are currently inspected by the PCAOB, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, investors would be deprived of the benefits of such inspection and our ordinary shares may be delisted or prohibited from trading. — See “Risks Related to Doing Business in China and Hong Kong — Although the audit report included in this prospectus was issued by Singapore auditors who are currently inspected by the PCAOB, if it is later determined that the PCAOB is unable to inspect or investigate our auditor completely, investors would be deprived of the benefits of such inspection and our ordinary shares may be delisted or prohibited from trading” on page 24 for more information. | |

| ● | Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment. — See “Risks Related to Doing Business in China and Hong Kong — Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment” on page 25 for more information. | |

| ● | Certain PRC regulations may make it more difficult for us to pursue growth through acquisitions. — See “Risks Related to Doing Business in China and Hong Kong — Certain PRC regulations may make it more difficult for us to pursue growth through acquisitions” on page 25 for more information. | |

| ● | PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’ ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us. — See “Risks Related to Doing Business in China and Hong Kong — PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’ ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us” on page 26 for more information. | |

| ● | Failure to make adequate contributions to various employee benefit plans and withhold individual income tax on employees’ salaries as required by PRC regulations may subject us to penalties. — See “Risks Related to Doing Business in China and Hong Kong — Failure to make adequate contributions to various employee benefit plans and withhold individual income tax on employees’ salaries as required by PRC regulations may subject us to penalties” on page 27 for more information. | |

| ● | Any failure to comply with PRC regulations regarding the registration requirements for employee stock incentive plans may subject the PRC plan participants or us to fines and other legal or administrative sanctions. — See “Risks Related to Doing Business in China and Hong Kong — Any failure to comply with PRC regulations regarding the registration requirements for employee stock incentive plans may subject the PRC plan participants or us to fines and other legal or administrative sanctions” on page 27 for more information. | |

| ● | U.S. regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China. — See “Risks Related to Doing Business in China and Hong Kong — U.S. regulatory bodies may be limited in their ability to conduct investigations or inspections of our operations in China” on page 27 for more information. | |

| ● | If we are classified as a PRC resident enterprise for PRC income tax purposes, such classification could result in unfavorable tax consequences to us and our non-PRC shareholders. If we are classified as a PRC resident enterprise for PRC income tax purposes, such classification could result in unfavorable tax consequences to us and our non-PRC shareholders. — See “Risks Related to Doing Business in China and Hong Kong — If we are classified as a PRC resident enterprise for PRC income tax purposes, such classification could result in unfavorable tax consequences to us and our non-PRC shareholders. If we are classified as a PRC resident enterprise for PRC income tax purposes, such classification could result in unfavorable tax consequences to us and our non-PRC shareholders” on page 27 for more information. | |

| ● | We face uncertainty with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies. — See “Risks Related to Doing Business in China and Hong Kong — We face uncertainty with respect to indirect transfers of equity interests in PRC resident enterprises by their non-PRC holding companies” on page 28 for more information. |

| 4 |

Risks Related to This Offering and the Shares

| ● | There has been no public market for our Shares prior to this offering, and you may not be able to resell the Shares at or above the price you paid, or at all. | |

| ● | The market price for the Shares may be volatile. | |

| ● | If securities or industry analysts do not publish research or reports about our business, or if they adversely change their recommendations regarding the Shares, the market price for the Shares and trading volume could decline. | |

| ● | We currently do not expect to pay dividends in the foreseeable future after this offering and you must rely on price appreciation of our ordinary shares for return on your investment. | |

| ● | Substantial future sales or perceived potential sales of Shares in the public market could cause the price of the Shares to decline. | |

| ● | The approval and/or other requirements of the CSRC or other PRC government authorities may be required in connection with this offering under PRC rules, regulations or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval. | |

| ● | We may need additional capital and may sell additional Shares or other equity securities or incur indebtedness, which could result in additional dilution to our shareholders or increase our debt service obligations. | |

| ● | Certain existing shareholders have substantial influence over our company and their interests may not be aligned with the interests of our other shareholders. | |

| ● | We are a foreign private issuer within the meaning of the rules under the Exchange Act, and as such we are exempt from certain provisions applicable to U.S. domestic public companies. | |

| ● | We will incur increased costs as a result of being a public company. | |

| ● | If we fail to establish and maintain proper internal financial reporting controls, our ability to produce accurate financial statements or comply with applicable regulations could be impaired. |

Corporate History and Structure

The Company is an exempted company with limited liability incorporated under the laws of the Cayman Islands on May 24, 2022. The Company is the 100% owner of the Company’s Hong Kong operating subsidiary: Qilun Culture (HK), a limited company that was organized under the laws of Hong Kong on November 12, 2021, and is the 100% owner of the Company’s Hong Kong holding subsidiary: Qilun Group (HK), a limited company that was organized under the laws of Hong Kong on June 14, 2022.

Qilun Culture (Shenzhen) is the 100% owner of the Company’s PRC operating subsidiaries:

| 1. | Shenzhen Houhaitang, a limited company organized under the laws of the PRC on March 31, 2014, and wholly acquired by Qilun Culture (Shenzhen) on December 31, 2021; and | |

| 2. | Qilun Enterprise Management Consultant, a limited company organized under the laws of the PRC on December 7, 2021. |

Qilun Culture (HK) was wholly-owned by Qilun Culture (Shenzhen) since its incorporation; on August 24, 2022, 100% equity of Qilun Culture (HK) was transferred from Qilun Culture (Shenzhen) to the Company. Qilun Culture (HK) is the 100% owner of OD&SR Institute, a limited company that was organized under the laws of Hong Kong on October 31, 2022.

Qilun Culture (Shenzhen) was wholly acquired by Qilun Holding (Shenzhen) in October 2022. Qilun Culture (Shenzhen) has been in the business of the research, development, design, outsourced production and sales of Chinese cultural and creative art collectibles and artwork home goods since inception.

Shenzhen Houhaitang has been in the business of retail sales of books since its acquisition by Qilun Culture (Shenzhen).

The Company did not have any significant corporate transactions since inception and capital expenditures and divestitures during the previous three years.

| 5 |

The following diagram illustrates our corporate structure, including our holding company, as of the date of this prospectus:

* Each of Qilun Holding (Shenzhen) Co., Ltd., Qilun Culture (Shenzhen) Group Co., Ltd., Qilun Enterprise Management Consultant (Shenzhen) Co., Ltd. and Shenzhen Houhaitang Culture Communication Co., Ltd. are organized under the laws of the PRC. The other listed entities are organized under the laws of the indicated jurisdictions.

Cash Transfers and Dividend Distributions

As of the date of this prospectus, our Cayman Islands holding company has not declared or paid dividends or made distributions to the Chinese operating entities or to investors in the past, nor any dividends or distributions were made by a Chinese operating entity to the Cayman Islands holding company. Our sole director Ruowen Li has complete discretion on whether to distribute dividends, subject to applicable laws. We do not have any current plan to declare or pay any cash dividends on our ordinary shares in the foreseeable future after this offering. See “Risk Factors — Risks related to Our Shares and This Offering — We currently do not expect to pay dividends in the foreseeable future after this offering and you must rely on price appreciation of our ordinary shares for return on your investment” beginning on page 30 of this prospectus. Subject to certain contractual, legal and regulatory restrictions, cash and capital contributions may be transferred among our Cayman Islands holding company and the Chinese operating entities. If needed, our Cayman Islands holding company can transfer cash to the Chinese operating entities through loans and/or capital contributions, and the Chinese operating entities can transfer cash to our Cayman Islands holding company through loans and/or issuing dividends or other distributions. There are limitations on the ability to transfer cash between the Cayman Islands holding company, the Chinese operating entities or investors. Cash transfers from the Cayman Islands holding company to the Chinese operating entities are subject to the applicable PRC laws and regulations on loans and direct investment. See “Risk Factors — Risks Related to Doing Business in China — PRC regulations of loans and direct investment by offshore holding companies to PRC entities may delay or prevent us from using the proceeds of our offshore financing to make loans or additional capital contributions to the operating entities, which could materially and adversely affect our liquidity and business” beginning on page 22 of this prospectus. If any of the operating entities incurs debt on its own behalf in the future, the instruments governing such debt may restrict their ability to pay dividends to us. Cash transfers from the Chinese operating entities to the Cayman Islands holding company are subject to the current PRC regulations, which permit the Chinese operating entities to pay dividends to their shareholders only out of their accumulated profits, if any, determined in accordance with PRC accounting standards and regulations. See “Risk Factors — Risks Related to Doing Business in China — We may rely on dividends and other distributions on equity paid by the operating entities to fund any cash and financing requirements we may have, and any interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets could have a material and adverse effect on our business” beginning on page 22 of this prospectus. Cash transfers from the Cayman Islands holding company to the investors is subject to the restrictions on the remittance of Renminbi into and out of China and governmental control of currency conversion. See “Risk Factors — Risks Related to Doing Business in China — Restrictions on the remittance of Renminbi into and out of China and governmental control of currency conversion may limit our ability to pay dividends and other obligations, and affect the value of your investment” beginning on page 23 of this prospectus. Additionally, to the extent cash or assets in the business is in China or a Chinese operating entity, the funds or assets may not be available to fund operations or for other use outside of China due to interventions in or the imposition of restrictions and limitations on the ability of our company or the operating entities by the PRC government to transfer cash or assets.

The Company does not have a specific cash transfer policy among its subsidiaries. The cash transfers made to date consist of:

| ● | Shenzhen Houhaitang Culture Communication Co., Ltd. loaned $131,746 to Qilun Culture Development (Shenzhen) Co., Ltd.; | |

| ● | Shenzhen Houhaitang Culture Communication Co., Ltd. sold products in the amount of $71,121 to Qilun Culture Development (Shenzhen) Co., Ltd.; and | |

| ● | Qilun Culture Development (Shenzhen) Co., Ltd. made a payment of $27,899 on behalf of Qilun Enterprise Management Consultant (Shenzhen) Co., Ltd. |

The cash transfers were made occasionally at the discretion of management and were not routine. There has been no transfers, dividends or distributions made to date between the holding company and its subsidiaries or to investors. The Company has no intentions to distribute earnings now and in the foreseeable future. See the Consolidated Financial Statements of the Company beginning on page F-1.

As of the date of this prospectus, we have not maintained any cash management policies that dictate the purpose, amount and procedure of fund transfers among our Cayman Islands holding company, our subsidiaries, or investors. Rather, the funds can be transferred in accordance with the applicable laws and regulations.

| 6 |

Corporate Information

Our principal executive offices are located at Room 2201, Modern International Building, No. 3038, Jintian Road, Gangxia Community, Futian Street, Futian District, Shenzhen City, Guangdong Province, People’s Republic of China. Our telephone number at this address is +86-755-83985414. Our registered office in the Cayman Islands is 4th Floor, Harbour Place, 103 South Church Street, P.O. Box 10240, Grand Cayman KY1-1002, Cayman Islands and is currently located at the office of 4th Floor, Harbour Place, 103 South Church Street, P.O. Box 10240, Grand Cayman KY1-1002, Cayman Islands, which may be changed from time to time at the discretion of our director. Our agent for service of process in the United States is The Crone Law Group P.C., 420 Lexington Avenue, Suite 2446, New York, NY 10170.

Investors should contact us for any inquiries through the address and telephone number of our principal executive offices. Our website is http://qilungroup.com.cn/. The information contained on our website is not a part of this prospectus.

Regulatory Permission

As substantially all of our operations are conducted by our PRC Subsidiaries in China, we are subject to the associated legal and operational risks, including risks related to the legal, political and economic policies of the Chinese government, the relations between China and the United States, or Chinese or United States regulations, which risks could result in a material change in our operations and/or cause the value of our ordinary shares to significantly decline or become worthless, and affect our ability to offer or continue to offer securities to investors. Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, and adopting new measures to extend the scope of cybersecurity reviews.

On July 6, 2021, the relevant PRC government authorities made public the Opinions on Strictly Cracking Down Illegal Securities Activities, which provided that the administration and supervision of overseas-listed China-based companies will be strengthened, and the special provisions of the State Council on overseas issuance and listing of shares by such companies will be revised, clarifying the responsibilities of domestic industry competent authorities and regulatory authorities. However, the Opinions on Strictly Cracking Down Illegal Securities Activities were only issued recently, leaving uncertainties regarding the interpretation and implementation of these opinions. It is possible that any new rules or regulations may impose additional requirements on us. As of the date of this prospectus, neither we nor our PRC Subsidiaries have been subject to any investigation, or received any notice, warning, or sanction from applicable government authorities related to this offering. In addition, neither we nor our PRC Subsidiaries have been involved in any review, investigation, enquiry, penalty, or other legal proceedings initiated by applicable governmental or regulatory authorities or third parties in relation to this offering.

The Regulations on Mergers and Acquisitions of Domestic Companies by Foreign Investors, or the M&A Rules, adopted by six PRC regulatory agencies in 2006 and amended in 2009, requires an overseas special purpose vehicle formed for listing purposes through acquisitions of PRC domestic companies and controlled by PRC companies or individuals to obtain the approval of the China Securities Regulatory Commission, or the CSRC, prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. According to our PRC legal counsel, DeHeng Law Offices (Shenzhen), we will not be required to submit an application to the CSRC for the approval under the M&A Rules for an offering because (i) the CSRC currently has not issued any definitive rule or interpretation concerning whether offerings like ours are subject to this regulation; and (ii) we did not acquire any equity interests or assets of a “PRC domestic company” as such terms are defined under the M&A Rules. However, our PRC legal counsel, DeHeng Law Offices (Shenzhen), has further advised us that there remains some uncertainty as to how the M&A Rules will be interpreted or implemented in the context of an overseas offering and its opinions summarized above are subject to any new laws, rules and regulations or detailed implementations and interpretations in any form relating to the M&A Rules.

On December 24, 2021, the CSRC, together with other relevant government authorities in China issued the Provisions of the State Council on the Administration of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments), and the Measures for the Filing of Overseas Securities Offering and Listing by Domestic Companies (Draft for Comments) (together, “Draft Overseas Listing Regulations”). The Draft Overseas Listing Regulations require that a PRC domestic enterprise seeking to issue and list its shares overseas shall complete the filing procedures with the CSRC. Such overseas securities issuance and listing include direct and indirect issuance and listing. Where an enterprise, whose principal business activities are conducted in China, seeks to issue and list its shares in the name of an overseas entity, such practice is deemed as an indirect overseas issuance and listing in the meaning of the Draft Overseas Listing Regulations. The Draft Overseas Listing Regulations, if enacted, may subject us to additional compliance requirements in the future, and we cannot assure you that we will be able to get the clearance of filing procedures under the Draft Overseas Listing Regulations on a timely basis, or at all. For instance, if we complete any offering under this prospectus after the enactment of the Draft Overseas Listing Regulations, we may be required to submit additional filings.

On December 28, 2021, the Cyberspace Administration of China (the “CAC”) jointly with the relevant authorities formally published Measures for Cybersecurity Review (2021) which took effect on February 15, 2022 and replace the former Measures for Cybersecurity Review (2020). Measures for Cybersecurity Review (2021) stipulates that operators of critical information infrastructure purchasing network products and services, and online platform operator (together with the operators of critical information infrastructure, the “Operators”) carrying out data processing activities that affect or may affect national security, shall conduct a cybersecurity review, any online platform operator who controls more than one million users’ personal information must go through a cybersecurity review by the cybersecurity review office if it seeks to be listed in a foreign country. Given that: (i) we do not possess personal information on more than one million users in our business operations; and (ii) data processed in our business does not have a bearing on national security and thus may not be classified as core or important data by the authorities, our PRC legal counsel, DeHeng Law Offices (Shenzhen), has advised that this offering would not be required to apply for a cybersecurity review under the Measures for Cybersecurity Review (2021).

According to the Notice by the General Office of the State Council of Comprehensively Implementing the List-based Management of Administrative Licensing Items (No. 2 [2022] of the General Office of the State Council) and its attachment, the List of Administrative Licensing Items Set by Laws, Administrative Regulations, and Decisions of the State Council (2022 Edition), as of the date of this prospectus, our PRC subsidiaries have received from PRC authorities all requisite licenses, permissions or approvals needed to engage in the businesses currently conducted in China. As of the date of this prospectus, neither we nor our PRC Subsidiaries (i) are required to obtain permissions from any PRC authorities to operate or issue our ordinary shares to foreign investors, (ii) are subject to permission requirements from the CSRC, the CAC or any other entity that is required to approve our PRC Subsidiaries’ operations, or (iii) have received or were denied such permissions by any PRC authorities.

However, since these statements and regulatory actions by the PRC government authorities are newly published and the official guidance and related implementation rules have not been issued, it is highly uncertain what the potential impact such modified or new laws and regulations will have on operations of our PRC Subsidiaries, the ability to accept foreign investments and quote on the OTCQB. If the CSRC, CAC or other regulatory agencies in the future promulgate laws, regulations or implementing rules requiring that we obtain their approvals for this offering and any follow-on offering, there is no assurance that we can obtain the approval, authorizations, or complete required procedures or other requirements in a timely manner, or at all. In the event that we or our PRC subsidiaries (i) do not receive or maintain any requisite permissions or approvals, (ii) inadvertently conclude that such permissions or approvals are not required, or (iii) applicable laws, regulations, or interpretations change and we are required to obtain such permissions or approvals in the future, we and our subsidiaries may be subject to sanctions imposed by the relevant PRC regulatory authority, including fines and penalties, revocation of the licenses and suspension of these entities’ business, restrictions or limitations on our ability to pay dividends outside of China, regulatory orders, including injunctions requiring the our subsidiaries to cease business operation, litigation or adverse publicity, the delisting of our securities on the OTCQB, and other forms of sanctions, which may result in a material change in the operations of our operating entities, significantly limit or completely hinder our ability to offer or continue to offer securities to our investors and the securities currently being offered may substantially decline in value and be worthless. See “Risk Factors — Risks Related to Doing Business in China” beginning on page 18 of this prospectus for a discussion of these legal and operational risks.

Implications of Being an Emerging Growth Company

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended, or the JOBS Act. As long as we remain an emerging growth company, we may rely on exemptions from some of the reporting requirements applicable to public companies that are not emerging growth companies. These exemptions include: (1) being permitted to provide only two years of selected financial data (rather than five years) and only two years of audited financial statements (rather than three years), in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; (2) not being required to comply with the auditor attestation requirements of the Sarbanes-Oxley Act of 2002 in the assessment of our internal control over financial reporting; and (3) not being required to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards. We have taken, and may continue to take, advantage of some of these exemptions until we are no longer an emerging growth company. The JOBS Act also provides that an emerging growth company does not need to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards. However, we have elected to “opt out” of this provision and, as a result, we will comply with new or revised accounting standards as required when they are adopted for public companies. This decision to opt out of the extended transition period under the JOBS Act is irrevocable.

We will remain an emerging growth company until the earliest of: (1) the last day of our fiscal year during which we have total annual gross revenues of at least $1.07 billion; (2) the last day of our fiscal year following the fifth anniversary of the completion of our initial public offering; (3) the date on which we have, during the previous three-year period, issued more than $1.00 billion in non-convertible debt; or (4) the date on which we become a “large accelerated filer” under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), which would occur if we have been a public company for at least 12 months and the market value of our Shares held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter. We will not be entitled to the above exemptions if we cease to be an emerging growth company.

Implications of Our Foreign Private Issuers Status

Because we are a foreign private issuer under the Exchange Act, we are exempt from certain provisions of the securities rules and regulations in the United States that are applicable to U.S. domestic issuers, including: (i) the rules under the Exchange Act requiring the filing of quarterly reports on Form 10-Q or current reports on Form 8-K with the SEC; (ii) the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; (iii) the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and (iv) the selective disclosure rules by issuers of material nonpublic information under Regulation FD.

We will be required to file an annual report on Form 20-F within four months of the end of each fiscal year. In addition, if we are successful at having our shares quoted on the OTCQB, we will publish our results on a quarterly basis through press releases, distributed pursuant to the rules and regulations of the OTCQB. Press releases relating to financial results and material events will also be furnished to the SEC on Form 6-K. However, the information we are required to file with or furnish to the SEC will be less extensive and less timely compared to that required to be filed with the SEC by U.S. domestic issuers. As a result, you may not be afforded the same protections or information, which would be made available to you, were you investing in a U.S. domestic issuer.

| 7 |

The Offering

| Ordinary Shares Offered by Selling Stockholders: | 16,550,000 Ordinary Shares (the “Shares”)

| |

Ordinary Shares Issued and Outstanding After Completion of this Offering:

Use of Proceeds: |

116,550,000

We will not receive any of the proceeds from the sale of Shares by the Selling Stockholders pursuant to this prospectus. The Selling Stockholders will pay any agent’s commissions and expenses they incur for brokerage, accounting, tax or legal services or any other expenses that they incur in disposing of Shares. We will bear all other costs, fees and expenses incurred in effecting the registration of the Shares covered by this prospectus and any prospectus supplement. | |

Market for our Ordinary Shares:

|

There is no market for our securities. Our Shares are not traded on any exchange or quoted on the OTCQB. After the effective date of the registration statement relating to this prospectus, we hope to have a market maker file an application for our shares to be eligible for quotation on the OTCQB. We do not yet have a market maker who has agreed to file such application.

There is no assurance that a trading market will develop, or, if developed, that it will be sustained. Consequently, a purchaser of our Shares may find it difficult to resell the securities offered herein should the purchaser desire to do so when eligible for public resale. |

| Risk Factors: | See “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our Shares. | |

| Listing: | We intend to apply to quote our Shares on the OTCQB. There is no assurance that we will be successful at having our shares quoted. | |

| Transfer Agent | Equity Stock Transfer, LLC. |

| 8 |

SUMMARY CONSOLIDATED FINANCIAL DATA