As filed with the Securities and Exchange Commission on June 13, 2024.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact Name of Registrant as Specified in Its Charter)

| 8900 | 85-4359258 | |||

| (State or jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

780 Lynnhaven Parkway

Suite 400

Virginia Beach, Virginia 23452

Telephone: (757) 734-5464

(Address, Including Zip Code, and Telephone Number, Including

Area Code, of Registrant’s Principal Executive Offices)

The Crone Law Group, PC

One East Liberty

Suite 600

Reno, Nevada 89501

Telephone: 646-861-7891

(Name, address, including zip code, and telephone

number,

including area code, of agent for service)

Copies to:

Mark E. Crone, Esq. Joe Laxague, Esq. Cassi Olson, Esq. The Crone Law Group, PC 420 Lexington Avenue Suite 2446 New York, NY 10170 (775) 234-5221 |

Ross Carmel, Esq. Jeffrey P. Wofford, Esq. Sichenzia Ross Ference Carmel LLP 1185 Avenue of the Americas, 31st Floor New York, NY, 10036 (212) 930-9700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer: ☐ | Accelerated filer: ☐ | |

| Smaller reporting company: | ||

| Emerging Growth Company: |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion. Dated June 13, 2024

PROSPECTUS

INSPIRE VETERINARY PARTNERS, INC.

Up

to [ ] Units, Each Unit Consisting of One Share of Class A Common Stock or One Pre-Funded

Warrant to Purchase One Share of Class A Common Stock

One Warrant to Purchase One Share of Class A Common Stock

Up to [ ] shares of Class A Common Stock underlying the Warrants

Up to [ ] shares of Class A Common Stock underlying the Pre-Funded Warrants

Inspire Veterinary Partners, Inc. (“Inspire” or the “Company”) is offering to [ ] units (the “Units”), each Unit consisting of one share of the Company’s Class A common stock, $0.001 par value per share and one warrant (“Warrant”) to purchase one share of Class A common stock for gross proceeds of up to $12 million before deduction of placement agent commissions and offering expenses, in a reasonable best-efforts offering. We currently estimate that the public offering price will be between $2.00 to $2.50 per Unit.

The Units have no stand-alone rights and will not be certificated or issued as stand-alone securities. The Warrants will have an exercise price of $[ ] (100% of the public offering price per Unit) and will be exercisable for a period of six months commencing upon issuance. The Class A common Stock and Pre-Funded Warrants can each be purchased in this offering only with the accompanying Warrants that are part of a Unit, but the components of the Units will be immediately separable and will be issued separately in this offering. A holder of a Warrant may not exercise any portion of a Warrant to the extent that the holder, together with its affiliates and any other person or entity acting as a group, would own more than 4.99% (or, at the election of the investor, 9.99%) of our outstanding shares of Class A common stock after exercise, as such ownership percentage is determined in accordance with the terms of the Warrants, except that upon notice from the holder to us, the holder may waive such limitation up to a percentage, not in excess of 9.99%. To better understand the terms of the Warrants, you should carefully read the “Description of Capital Stock” section on page 86 of this prospectus.

We are also offering to each purchaser of Units that would otherwise result in the purchaser’s beneficial ownership exceeding 4.99% of our outstanding Class A common stock immediately following the consummation of this offering, the opportunity to purchase Units consisting of one pre-funded warrant (in lieu of one share of Class A Common Stock, each a “Pre-Funded Warrant”). Subject to limited exceptions, a holder of Pre-Funded Warrants will not have the right to exercise any portion of its Pre-Funded Warrants if the holder, together with its affiliates, would beneficially own in excess of 4.99% (or, at the election of the holder, such limit may be increased to up to 9.99%) of the number of Class A common stock outstanding immediately after giving effect to such exercise. Each Pre-Funded Warrant will be exercisable for one share of Class A Common Stock. The purchase price of each Unit including a Pre-Funded Warrant will be [ ], and the remaining exercise price of each Pre-Funded Warrant will equal $0.001 per share. The Pre-Funded Warrants will be immediately exercisable (subject to the beneficial ownership cap) and may be exercised at any time until all of the Pre-Funded Warrants are exercised in full. For each Unit including a Pre-Funded Warrant we sell (without regard to any limitation on exercise set forth therein), the number of Units including a share of Class A common stock we are offering will be decreased on a one-for-one basis.

The securities are expected to be issued in a single closing. We expect this offering to be completed not later than two business days following the commencement of sales in this offering (the effective date of the registration statement of which this prospectus forms a part) and we will deliver all securities to be issued in connection with this offering delivery versus payment/receipt versus payment upon receipt of investor funds received by us. Accordingly, neither we nor the placement agent have made any arrangements to place investor funds in an escrow account or trust account since the placement agent will not receive investor funds in connection with the sale of the securities offered hereunder.

We have engaged Spartan Capital Securities, LLC (“Spartan” or “Placement Agent”) as our exclusive Placement Agent to use its reasonable best efforts to solicit offers to purchase our securities in this offering. The Placement Agent has no obligation to purchase any of the securities from us or to arrange for the purchase or sale of any specific number or dollar amount of our Class A common stock, Warrants or Pre-Funded Warrants. Because there is no minimum offering amount required as a condition to closing in this offering, the actual public offering amount, Placement Agent’s fee and proceeds to us, if any, are not presently determinable and may be substantially less than the total maximum offering amounts set forth above and throughout this prospectus. We have agreed to pay the Placement Agent the Placement Agent’s fee and other compensation and reimbursement of expenses set forth in the table below.

We have granted Spartan, as Placement Agent, an option, exercisable for 45 days from the closing date of this offering, to purchase up to [ ] additional shares of Class A Common Stock, representing 15% of the shares of Class A Common Stock sold in the offering, and/or up to [ ] Pre-Funded Warrants, representing 15% of the Pre-funded Warrants sold in the offering, and/or up to [ ] Warrants, representing 15% of the Warrants sold in the offering (the “Over-Allotment Option”). The underwriter may exercise the over-allotment option with respect to shares of Class A common stock only, Pre-Funded Warrants only, Warrants only, or any combination thereof.

We expect to receive up to $12 million in aggregate gross proceeds from sales of our Units pursuant to this prospectus. We expect to use the net proceeds from sales of our Class A common stock, Warrants and Pre-Funded Warrants, if any, in this offering for general working capital. See “Use of Proceeds.”

Our Class A Common Stock is listed on The Nasdaq Capital Market (“Nasdaq”) under the symbol “IVP.” On May 8, 2024, last reported trading date for our Class A common stock, the closing price of our Class A common stock was $3.63 per share. There is no established public trading market for the Warrants or Pre-Funded Warrants, and we do not intend to list the Warrants or Pre-Funded Warrants on any national securities exchange or trading system. Without an active trading market, the liquidity of the Warrants or Pre-Funded Warrants will be limited.

| Per Unit | Total | |||||||

| Public offering price | $ | $ | ||||||

| Placement Agent fees (1) | $ | $ | ||||||

| Proceeds to Inspire Veterinary Partners, Inc. before expenses(2) | $ | $ | ||||||

| (1) | We have agreed to pay the Placement Agent a cash fee equal to 8.0% of the gross proceeds raised in this offering. We have also agreed to reimburse the Placement Agent for certain of its offering related expenses, including non-accountable expenses in an amount equal to 1.0% of the aggregate gross proceeds raised in this offering, and legal fees and other out-of-pocket expenses in the amount of up to $125,000. See “Plan of Distribution” for a description of the compensation to be received by the Placement Agent. |

| (2) | The amount of offering proceeds to us presented in this table does not give effect to any exercise of the Warrants or the Pre-Funded Warrants. |

We will also pay any fees and expenses incurred in registering the Units (including the Class A common stock, Warrants, the Class A Common Stock underlying the Warrants and Pre-Funded Warrants, and the Class A Common Stock underlying the Pre-Funded Warrants) under the U.S. Securities Act of 1933, as amended (the “Securities Act”), including legal and accounting fees, if any. See “Plan of Distribution” beginning on page 93 of this prospectus for more information.

We are an “emerging growth company” as defined in Section 2(a) of the Securities Act, and are subject to reduced public company reporting requirements. This prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

Investing in our Class A common stock involves risks. You should carefully read the “Risk Factors” beginning on page 14 of this prospectus before deciding to invest in shares of our Class A common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Spartan Capital Securities, LLC

The date of this prospectus is , 2024.

TABLE OF CONTENTS

We and the underwriters have not authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus. We do not take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front of this prospectus only, regardless of the time of delivery of this prospectus or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

i

PROSPECTUS SUMMARY

This summary highlights information contained in more detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our Class A common stock. You should carefully read this prospectus in its entirety before investing in our Class A common stock, including the sections titled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Cautionary Statement Regarding Forward-Looking Statements,” and our consolidated financial statements and the accompanying notes thereto included elsewhere in this prospectus.

Unless the context requires otherwise, references to “Inspire Veterinary,” the “Company,” “we,” “us,” and “our,” refer to Inspire Veterinary Partners, Inc. and its consolidated subsidiaries. On April 22, 2024, we amended our Amended and Restated Articles of Incorporation to effect a reverse stock split of our authorized and issued and outstanding shares of Class A common stock by a ratio of 1-for-100 (the “Reverse Stock Split”). The Reverse Stock Split was effected on May 8, 2024. Unless expressly stated in this registration statement, all share and per share information included herein has been adjusted to account for the Reverse Stock Split.

About Inspire Veterinary Partners

Inspire Veterinary owns and operates veterinary hospitals throughout the United States. The Company specializes in small animal general practice hospitals which serve all manner of companion pets, emphasizing canine and feline breeds and including equine care. As the Company expands, it expects to acquire additional veterinary hospitals, including general practice, mixed animal facilities, and critical and emergency care.

The Company completed its initial public offering on August 31, 2023 and its shares of Class A common stock are quoted on The Nasdaq Capital Market under the symbol “IVP.”

As of the date of this prospectus, the Company currently has fourteen veterinary hospitals located in ten states. Inspire Veterinary has expanded and plans to further expand through acquisitions of existing hospitals which have the financial track record, marketplace advantages and future growth potential. Because the Company leverages a leadership and support structure which is distributed throughout the United States, acquisitions are not centralized to one geographic area.

Services provided at the Company’s hospitals include preventive care for companion animals consisting of annual health exams which include: parasite control; dental health; nutrition and body condition counseling; neurological examinations; radiology; bloodwork; skin and coat health and many breed specific preventive care services. Surgical offerings include all soft tissue procedures such as spays and neuters, mass removals, splenectomies and can also include gastropexies, orthopedic procedures and other types of surgical offerings based on a doctor’s training. In many locations additional means of care and alternative procedures are also offered such as acupuncture, chiropractic and various other health and wellness offerings.

Corporate Information

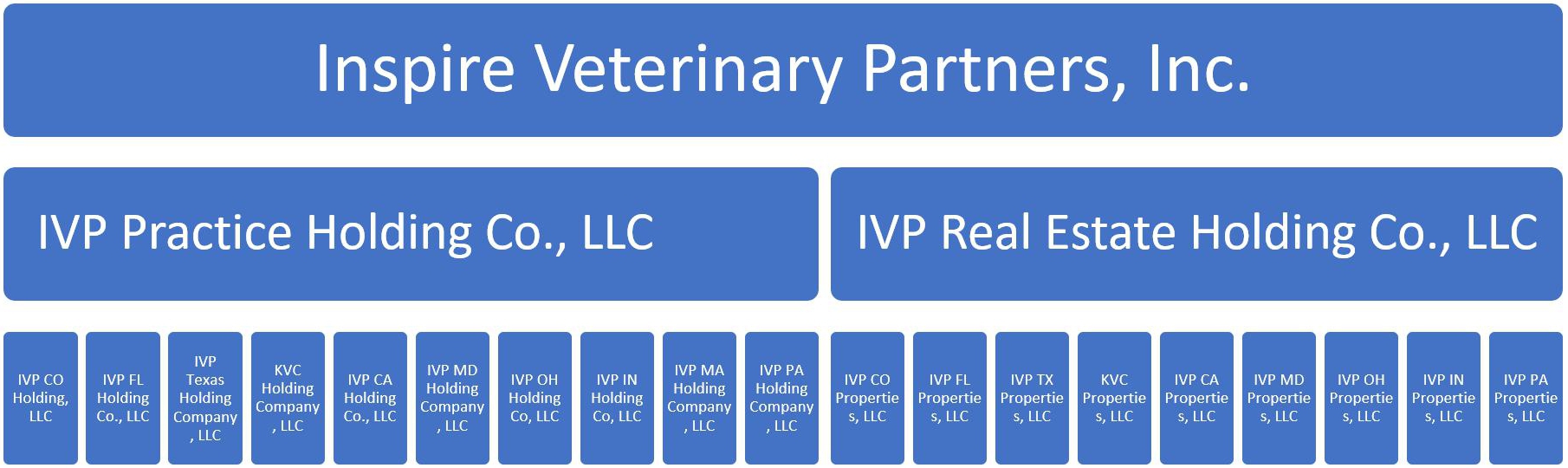

Inspire was incorporated as a corporation in the state of Delaware in 2020. In June 2022, the Company converted into a Nevada c-corporation. The Company has two consolidating holding companies: IVP Practice Holdings Co., LLC and IVP Real Estate Co., LLC. Each of IVP Practice Holdings Co., LLC and IVP Real Estate Co., LLC are passive intermediate holding companies with no employees, no operations and no assets other than the equity in the respective subsidiaries.

The Company’s principal executive offices are located at 780 Lynnhaven Parkway, Suite 400, Virginia Beach, Virginia 23452. Our telephone number is (757) 734-5464. Our website address is www.inspirevet.com. Information contained on our website or connected thereto does not constitute part of, and is not incorporated by reference into, this prospectus or the registration statement of which it forms a part.

Recent Developments

On March 26, 2024 Inspire Veterinary entered into a securities purchase agreement (the “Purchase Agreement”) with certain investors. Pursuant to the Purchase Agreement, Inspire Veterinary issued to certain investors two Increasing OID Senior Notes (each a “Note” and collectively the “Notes”) each for $250,000. The Notes have a maturity date of the earlier of December 26, 2024 or the consummation of a capital raise (the “Maturity Date”).

The Purchase Agreement contains a number of representations and warranties by Inspire Veterinary and the investors which are qualified by materiality or Material Adverse Effect as defined in the Purchase Agreement. The representations and warranties are customary for transactions of this nature and are subject to specified exceptions and qualification. The Purchase Agreement also contains customary confidentiality and indemnification provisions.

1

The Notes contain an original issue discount (“OID”) which shall be: (i) fifteen percent (15%) if the Notes are satisfied and paid in full on or before the forty-fifth (45th) day after the Original Issue Date (as such term is defined in the Notes), (ii) twenty percent (20%) if the Notes are satisfied and paid in full after such 45th day but on or before the ninetieth (90th) day after the Original Issue Date, and (iii) thirty percent (30%) after such 90th day. The Notes can be prepaid at any time prior to the Maturity Date without any penalties.

The Notes must be repaid in full from any future capital raises (debt, equity or any other form of capital raise) of Inspire Veterinary. All of the funds raised must be used to repay the Notes until the Notes are repaid in full.

The Notes are convertible into shares of Class A common stock of Inspire Veterinary, in full or in part, at any time after issuance at the discretion of the noteholder at a fixed conversion price of $0.03 per share (the “Fixed Conversion Price”).

If the Notes are not repaid by the Maturity Date the default provisions are as follow: (i) The Face Value (as such term is defined in the Notes) of the Notes will increase by 20% (to a 50% OID -- $1,000,000 Face Value); (ii) the conversion price of the Notes will become convertible at the lower of (a) the Fixed Conversion Price or (b) 20% discount to a 3-Day volume-weighted average price (the “Default Conversion Price”).

Inspire Veterinary must keep enough shares of Class A common stock in reserve in order to facilitate the conversion of the Notes at the Default Conversion Price. Additionally, Inspire Veterinary agrees to lower the floor price of the existing Series A Preferred Stock to $0.01.

In the event a noteholder agrees to release the funds to the Inspire Veterinary prior to the floor price on the Series A Preferred Stock being officially lowered and Inspire Veterinary then fails to officially lower the floor price within 7 calendar days, the Notes will be immediately considered in default.

The use of proceeds from the Notes will be used for general corporate purposes and acquisitions.

Nasdaq Delisting Notifications

On March 8, 2024, we received a staff determination from Nasdaq to delist the Company’s securities from the Nasdaq Capital Market (the “Staff Determination”). The Staff Determination was issued because, as of March 7, 2024, the Company’s securities had a closing bid price of $0.10 or less for at least ten consecutive trading days. Accordingly, the Company is subject to the provisions contemplated under Listing Rule 5810(c)(3)(A)(iii) (the “Low Priced Stocks Rule”). The Company appealed the Staff Determination, however, to a Hearings Panel by filing a hearing request with Nasdaq.

In addition, on April 11, 2024, we received a staff determination from Nasdaq notifying the Company that, based on the Company’s stockholders’ equity of ($788,259) as reported in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 as filed with the Securities and Exchange Commission, the Company does not meet the alternatives of market value of listed securities or net income from continuing operations. As such, the Company no longer complies with Nasdaq listing rules regarding minimal stockholder’s equity for continued listing. Accordingly, this matter serves as an additional basis for delisting the Company’s securities from Nasdaq. The Company’s hearing date with the Nasdaq Hearings Panel was held on May 14, 2024.

In order to address the bid price deficiency, on April 15, 2024, our board of directors approved a reverse stock split of the Company’s authorized and issued and outstanding shares of Class A common stock, par value $0.0001 per share (the “Common Stock”), at a ratio of 1 for 100 (the “Reverse Stock Split”). The Reverse Stock Split was effective on May 8, 2024. On the effective date, every one hundred (100) shares of Class A Common Stock issued and outstanding or held as treasury stock was automatically reclassified into one (1) new share of Common Stock. The total number of shares of Class A Common Stock authorized for issuance was reduced by a corresponding proportion from 100,000,000 shares to 1,000,000 shares.

We believe that the Reverse Split will allow us to regain compliance with both the Low Priced Stocks Rule and the Bid Price Rule. In addition, we believe that the raising of additional equity capital, including the additional equity capital to be raised in this offer, will allow us to regain compliance with the shareholder’s equity requirement for continued listing on Nasdaq.

2

On June 6, 2024, the Company received a letter from the Panel indicating that our request for continued on Nasdaq was granted subject to the following: (i) on or before June 15, 2024, the Company shall file a registration statement with the Securities and Exchange Commission for a public offering that will be led by Spartan Capital Securities, LLC, and (ii) on or before September 4, 2024, we shall demonstrate compliance with Listing Rule 5550(b)(1).

Additionally, we were advised that September 4, 2024, represents the full extent of the Panel’s discretion to grant continued listing while we are non-compliant with the Exchange’s Listing Rules. It is a requirement during the exception period that we provide prompt notification of any significant events that occur during this time that may affect our compliance with Nasdaq requirements.

There can be no assurance, however, that the Company will be able to regain compliance with the Bid Price Rule and the Low Priced Stocks Rule or that it will be able to regain compliance with the minimum shareholder’s equity rule.

Increase of Authorized

On April 26, 2024, the holders of a majority of the issued and outstanding voting securities of the Company (the “Majority Stockholders”), approved, by written consent an amendment to the Company’s Articles of Incorporation to increase the total number of authorized shares of Class A Common Stock to one hundred million (100,000,000) shares (the “Amendment”). The effectiveness of the Majority Stockholders’ approval of the Amendment shall automatically take effect on June 16, 2024.

Richard Frank Employment Agreement

We entered into an employment agreement (the “Employment Agreement”) with Richard Frank, the Company’s current Chief Financial Officer. Mr. Frank’s appointment as Chief Financial Officer had previously become effective upon consummation of Inspire’s initial public offering on August 31, 2023 and his Employment Agreement is effective as of January 1, 2024. The Employment Agreement provides for an initial one-year term with the ability to renew, upon the affirmative vote of the board of directors of the Company, for successive one-year terms. The Employment Agreement provides that Mr. Frank will receive a base salary of $210,000 per annum. The base salary will be reviewed at the end of each fiscal year and any recommended changes will be subject to approval of the board of directors of the Company. Mr. Frank is eligible for annual bonuses subject to satisfaction of both a “Revenue Target” and a “Profit Target”, as further described in the Employment Agreement. The Employment Agreement contains certain non-disclosure and confidentiality provisions applicable to Mr. Frank for the benefit of the Company. Mr. Frank has also agreed, during the term of his employment and for a two-year period following the termination of his employment not to solicit for employment any employee or any person who was employed by the Company within the prior six months. Mr. Frank is also barred from soliciting any clients or certain former clients of the Company for a period of two years following the termination of his employment with the Company. The Company has the right to terminate Mr. Frank’s employment immediately for cause upon certain specified acts, and he may be entitled to severance payments in certain circumstances.

Charles Keiser Consulting Agreement

On March 6, 2024, we entered into a consulting agreement (the “Consulting Agreement”) with Charles “Chuck” Keiser, DVM, an experienced professional of veterinary medicine and the business of veterinary medicine, and a former member of the board of directors of the Company, pursuant to which we agreed to compensate Dr. Keiser for certain consulting services that he has provided to the Company relating to veterinary medicine business support and other related activities. As consideration for Dr. Keiser’s consulting services, Inspire agreed to issue to Dr. Kesier $151,695.60 worth of restricted shares of Class A common stock of the Company, which resulted in the issuance of 18,659 shares of Class A common stock based on the closing price of $0.0813 per share on the last trading day immediately prior to the date of the Consulting Agreement, as quoted on The Nasdaq Capital Market. The Consulting Agreement contains certain non-disclosure and confidentiality provisions applicable to Dr. Keiser for the benefit of the Company. Dr. Keiser released the Company from any and all claims he may have had against the Company.

The Consulting Agreement terminated upon delivery of the shares to Dr. Keiser on March 7, 2024.

General Release

On March 6, 2024, Inspire entered into a general release agreement with Kenneth Seth Lundquist, DVM, Charles “Chuck” Keiser, DVM, and Don I. Williamson, Jr. DVM, and the Estate of Gregory Armstrong (each, a “Releasor” and collectively, the “Releasors”), pursuant to which the Company agreed to issue to each Releasor $5,000 worth of restricted shares of Class A common stock of the Company, which resulted in the issuance of 615 shares of Class A common stock to each Releasor, based on the closing price of $0.0813 per share on the last trading day immediately prior to the date of the General Release Agreement, as quoted on The Nasdaq Capital Market. As partial consideration for the issuance of the shares pursuant to the General Release Agreement, each Releasor agreed to release Inspire from all potential, pending, or alleged claims, issues or complaints, whether asserted or which could be asserted by the Releasors against the Company, including any such claims, issues or complaints arising from or in connection with Inspire Veterinary’s previous acquisition from the Releasors of their ownership interest in Kauai Veterinary Clinic, Inc., located in Lihue, Hawaii, and associated real estate.

3

The Tumim Transaction

On November 30, 2023, we entered into a common stock purchase agreement (the “Purchase Agreement”) with Tumim Stone Capital LLC (“Tumim”), pursuant to which Tumim committed to purchase, subject to certain conditions and limitations, up to $30.0 million of shares of Class A common stock, at our direction from time to time, subject to the satisfaction of the terms and conditions in the Purchase Agreement. Also, on the same date, we entered into a registration rights agreement (the “Registration Rights Agreement”) with Tumim, pursuant to which we agreed to file with the U.S. Securities and Exchange Commission (the “Commission”) a registration statement to register for resale under the Securities Act of 1933, as amended (the “Securities Act”), the shares of our Class A common stock that may be issued to Tumim under the Purchase Agreement. We and Tumim subsequently agreed in a letter agreement (the “Letter Agreement”) to certain amendments to the Purchase Agreement and the Registration Rights Agreement relating to the commitment shares and initial registration statement filing deadline, as reflected below.

Our sales of Class A common stock to Tumim, if any, will be subject to certain limitations, and may occur from time-to-time in Inspire Veterinary’s sole discretion, over the period commencing once certain customary conditions are satisfied, including securing effectiveness of a resale registration statement with the Commission, and ending on the first day of the month following the 24-month anniversary of the date on which the resale registration statement is declared effective by the Commission. Tumim has no right to require Inspire to sell any shares of Class A common stock to Tumim, but Tumim is obligated to purchase shares of Class A common stock pursuant to a valid purchase notice delivered by Inspire, subject to certain conditions and limitations.

Purchase Price

The shares of Class A common stock to be issued by Inspire and purchased by Tumim will be sold at a purchase price equal to 95% of the lowest daily volume-weighted average price of the Class A common stock on Nasdaq (or any other eligible national stock exchange, as applicable) during the three consecutive trading days immediately following the trading date on which a valid purchase notice is delivered to Tumim by Inspire. Such purchase price will be adjusted for reorganization, recapitalization, non-cash dividend, stock split, reverse stock split or other similar transaction by Inspire with respect to its Class A common stock.

Actual sales of shares of Class A common stock to Tumim will depend on a variety of factors to be determined by Inspire from time-to-time, including, among other things, market conditions, the trading price of the Class A common stock, and the working capital needs, if any, of the Company.

The net proceeds from sales, if any, under the Purchase Agreement to Inspire will depend on the frequency and prices at which Inspire sells shares of Class A common stock to Tumim. Inspire expects that any proceeds received by Inspire from such sales to Tumim will be used for working capital and general corporate purposes.

Purchase Limits

Pursuant to the Purchase Agreement, Inspire may not require Tumim to purchase, and Tumim will have no obligation to purchase, in any single transaction, shares of Class A common stock in excess of a number equal to the lowest of:

| (i) | 100% of the average daily trading volume in the Class A common stock on Nasdaq (or any other eligible national stock exchange, as applicable) for the five consecutive trading days immediately prior to the trading date on which a valid purchase notice is delivered to Tumim, |

| (ii) | a 30% discount to the daily trading volume in the Class A common stock on Nasdaq (or any other eligible national stock exchange, as applicable), and |

| (iii) | $2.0 million divided by the volume-weighted average price for the Class A common stock on the trading day immediately prior to the trading date on which a valid purchase notice is delivered to Tumim. |

Consistent with applicable Nasdaq rules, Inspire may not issue to Tumim more than 12,143 shares of its Class A common stock (the “Exchange Cap”), which number of shares is equal to 19.99% of the shares of the Company’s Class A common stock issued and outstanding immediately prior to the execution of the Purchase Agreement, unless Inspire obtains stockholder approval to issue shares of its Class A common stock in excess of such limit in accordance with applicable rules of Nasdaq or any other applicable national stock exchange.

4

However, the Exchange Cap will not apply to the extent that and for so long as the average price of all shares of Class A common stock purchased pursuant to the Purchase Agreement is equal to or greater than $0.4954, which was the official closing price of the Class A common stock on Nasdaq on the date of signing the Purchase Agreement.

Moreover, Inspire may not issue or sell any shares of Class A common stock to Tumim which, when aggregated with all other shares of the Company’s Class A common stock then beneficially owned by Tumim and its affiliates (as calculated pursuant to Section 13(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and Rule 13d-3 promulgated thereunder), would result in Tumim beneficially owning more than 4.99% of the issued and outstanding shares of the Company’s Class A common stock (the “Beneficial Ownership Limitation”), unless such limit is increased or waived by Tumim.

Commitment Shares

Pursuant to the terms of the Purchase Agreement, as consideration for Tumim’s irrevocable commitment to purchase shares of the Company’s Class A common stock, we became obligated to issue to Tumim a number of shares of Class A common stock (the “Commitment Shares”) equal to $600,000 divided by the average daily volume-weighted average price for the Class A common stock on Nasdaq during the five (5) consecutive trading days ending on the trading date immediately prior to Inspire Veterinary’s filing of a resale registration statement covering Tumim’s resales pursuant to the Registration Rights Agreement described below. The Commitment Shares are due on the trading day immediately following the date the resale registration statement is declared effective by the Commission.

If the number of Commitment Shares due to Tumim would exceed the Beneficial Ownership Limitation, then we will become obligated to issue to Tumim a pre-funded warrant (the “Tumim pre-funded warrant”) to purchase shares of Class A common stock (the “Warrant Shares”), with an exercise price equal to $0.0001 per share, in an amount equal to the difference between $600,000 and the value of the Commitment Shares issued below the Beneficial Ownership Limitation, calculated using the same pricing mechanism as the pricing mechanism used to determine the Commitment Shares paid as Class A common stock. For each share of Class A common stock which may be exercised as a Warrant Share upon exercise of the Tumim pre-funded warrant, the number of shares of Class A common stock to be issued as Commitment Shares will be decreased on a one-for-one basis.

If the aggregate number of Commitment Shares and Warrant Shares due to Tumim would exceed the Exchange Cap, and the Company has not obtained stockholder approval for the issuance of Class A common stock in excess of the Exchange Cap in accordance with the applicable rules of Nasdaq (or any eligible substitute exchange) by May 24, 2024, then the Company shall be obligated to pay to Tumim an amount in cash equal to $600,000 minus the value of the shares of Class A common stock issuable to Tumim as Commitment Shares and the value of the Warrant Shares issuable upon exercise of the Tumim pre-funded warrant.

In certain other circumstances, including our failure to file registration statements with respect to the shares of Class A common stock issuable to Tumim under the Purchase Agreement or the failure of such registration statements to be declared effective by the Commission within certain deadlines, Inspire may become obligated to pay to Tumim a cash fee equal to $600,000 in lieu of issuing such shares of Class A common stock and Warrant Shares, under the terms and subject to the conditions described more fully in the Purchase Agreement, as amended.

The Registration Rights Agreement

Pursuant to the Registration Rights Agreement, we are required to file an initial resale registration statement on Form S-1 with the Commission permitting the resale of the Commitment Shares, the Warrant Shares, and certain other shares of Class A common stock issued to Tumim pursuant to the Purchase Agreement by no later than January 31, 2024. The Registration Rights Agreement also obligates Inspire in some circumstances and subject to certain conditions, to file additional resale registration statements to permit the resale of shares of Class A common stock issued to Tumim pursuant to the Purchase Agreement. Such registration statements are required to identify Tumim as the “Selling Stockholder”. Such registration statements are required to permit the resale of such shares of Class A common stock of the Company held by Tumim pursuant to Rule 415 under the Securities Act.

Also pursuant to the Registration Rights Agreement, Inspire is required to use its commercially reasonable efforts to have each registration statement declared effective by the Commission as soon as reasonably practicable, but in no event later than May 28, 2024 (with respect to this initial resale registration statement), which is the 180th calendar day following the date of signing of the Registration Rights Agreement, or the 180th calendar day following the date on which the Company was required to file any such additional registration statement, in each case if such registration statement is subject to comment by the Commission, or the 75th calendar day after the date of signing the Registration Rights Agreement with respect to the initial registration statement or the 75th calendar day after the date on which the Company was required to any additional registration statement, in each case if such registration statement is not subject to comment by the Commission.

5

On February 13, 2024, we issued a warrant (the “Warrant”) to purchase up to 16,549 shares of Class A common stock of the Company, par value $0.0001 per share (the “Warrant Shares”), to Tumim pursuant to the Purchase Agreement and the Letter Agreement. Inspire issued the shares and the Warrant in fulfilment of its obligation to issue “Commitment Shares” to Tumim.

We issued the shares and the Warrant to Tumim pursuant to a privately negotiated transaction exempt from registration pursuant to Rule 506(b) of Regulation D under the Securities Act of 1933, as amended. We did not receive any proceeds with respect to the issuance of the Commitment Shares or the Warrant and do not expect to receive any material proceeds from Tumim’s exercise, if any, of the Warrant for the purchase of Warrant Shares.

The Valley Veterinary Services Acquisition

On November 8, 2023, pursuant to an asset purchase agreement, dated October 27, 2023 (the “Asset Purchase Agreement”), by and among the Company, IVP PA Holding Company, LLC (“Acquisition Sub”), a Delaware limited liability company and wholly-owned subsidiary of the Company and Valley Veterinary Service, Inc., a Pennsylvania corporation (the “Seller”), Michelle Bartus, VMD and Peter Nelson, VMD (the “Owners” and together with the Seller, the “Seller Parties”), the Company completed the acquisition of Valley Veterinary Services animal hospital.

The aggregate purchase consideration for the Valley Veterinary Services animal hospital practice was $1,400,000 plus certain assumed liabilities, with the purchase consideration consisting of $1,000,000 paid in cash plus 408,163 restricted shares of the Company’s Class A common stock which was equal to the quotient obtained by dividing $400,000 by the official closing price of one share of Class A common stock as reported by the Nasdaq Capital Market on the trading date immediately prior to the closing.

Pursuant to the Asset Purchase Agreement, Acquisition Sub acquired substantially all of the assets comprising the veterinary clinic operating under the name “Valley Veterinary Service”, including all equipment and other tangible personal property, inventory, customer deposits, prepaid expenses, permits, licenses, franchises, variances, business contracts and equipment leases, books and records, telephone numbers, yellow pages listings, internet websites, electronic mail addresses (including, without limitation, any and all content therein), and social media sites and accounts, goodwill and intangible assets and other proprietary rights relating to the veterinary practice. The acquisition excluded certain assets, including certain excess cash, patient and medical records and files to the extent non-transferable by applicable law, personal licenses held by individual veterinary professionals, and other stipulated assets. Also pursuant to the Asset Purchase Agreement, Acquisition Sub assumed liabilities arising from business contracts that may arise after the closing.

Series A Preferred Stock Issuance

On January 2, 2024, we issued 200 shares of our Series A preferred stock to Target Capital 1, LLC (“Target”), an existing investor and holder of certain shares of our previously issued and outstanding Series A preferred stock, for gross proceeds of $200,000. The issuance and sale of the Series A preferred stock to Target was consummated in a privately negotiated transaction exempt from registration pursuant to Rule 506(b) of Regulation D under the Securities Act. We expect to use the proceeds of the sale of the Series A preferred stock for general working capital purposes.

Series A Preferred Stock Conversions

Between November 14, 2023 and January 29, 2024, our existing holders of the previously issued and outstanding shares of Series A preferred stock converted an aggregate of 4,166 shares of Series A preferred stock for 166,169 shares of Class A common stock, in each case pursuant to the terms of the Certificate of Designations relating to such Series A preferred stock.

“Best-Efforts” Offering of Class A Common Stock

On January 26, 2024, the Company filed an amended registration statement on Form S-1/A to register our public offering and sale, on a reasonable best-efforts basis, of up to 265,816 shares of Class A common stock at an assumed offering price of $0.188 (the “Best-Efforts Offering”), for anticipated gross proceeds of approximately $5,000,000. As of the date of this prospectus, the registration statement relating to the Best-Efforts Offering has not been declared effective by the Commission, and we have not yet consummated the Best-Efforts Offering. There can be no assurance that we will sell all or any of the shares of Class A common stock pursuant to the Best-Efforts Offering. Spartan Capital Securities, LLC (“Spartan”) has agreed to act as our exclusive placement agent in connection with the Best-Efforts Offering.

6

Best-Efforts Offering Spartan Agent’s Warrant

In connection with their role as placement agent in the Best-Efforts Offering, we agreed to issue to Spartan a warrant (the “Best-Efforts Offering Spartan Warrant”) to purchase a number of shares of Class A common stock equal to 4.0% of the aggregate number of shares of Class A common stock sold in the Best-Efforts Offering, subject to certain conditions.

The Best-Efforts Offering Spartan Warrant will be issuable upon the consummation of the issuance of shares of Class A common stock pursuant to the Best-Efforts Offering, and will be exercisable at any time and from time to time, in whole or in part, at Spartan’s option during the four and a half-year period following such issuance of Best-Efforts Offering Spartan Warrant. The Best-Efforts Offering Spartan Warrant will be exercisable at a price per share equal to 110% of the price per share of the Class A common stock sold pursuant to the Best-Efforts Offering. We have also agreed to provide Spartan with registration rights for the shares of Class A common stock underlying the Best-Efforts Offering Spartan Warrant (including a one-time demand registration right and customary piggyback rights, subject and pursuant to a registration rights agreement to-be-agreed upon by the parties), cashless exercise and customary anti-dilution provisions.

The issuance of the Best-Efforts Offering Spartan Warrant and the issuance, if any, of restricted shares of Class A common stock upon exercise of such warrants are expected to be consummated in a privately negotiated transaction exempt from registration pursuant to Section 4(a)(2) of the Securities Act. There are no anticipated proceeds from the issuance of the Best-Efforts Offering Spartan Warrant.

Best-Efforts Offering Lock-Ups

In connection with the Best-Efforts Offering, we have agreed that, without the prior written consent of Spartan, we will not, for a period of 360 days after our entry into the placement agent agreement with respect to the Best-Efforts Offering, offer, pledge, sell, contract to sell, sell any option or contract to purchase, purchase any option or contract to sell, grant any option, right or warrant to purchase, lend, or otherwise transfer or dispose of any capital stock of the Company, or agree to or engage in certain related or similar transactions, other than with respect to certain exempt securities issuances.

Also in connection with the Best-Efforts Offering, our directors and executive officers and holders of 5% or more of Class A common stock will not, for a period of ninety days after the effective date of the registration statement on Form S-1 relating to the Best-Efforts Offering, offer, sell, agree to offer or sell, solicit offers to purchase, pledge, encumber, assign, borrow or otherwise dispose of any Class A common stock, or grant any call option or purchase any put option with respect to the same, or agree to or engage in certain related or similar transactions, or otherwise publicly disclose the intention to do so, subject to certain customary exceptions.

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended and as modified by the Jumpstart Our Business Startups Act of 2012 (“JOBS Act”). We have elected to use this extended transition period for complying with new or revised accounting standards that have different effective dates for public and private companies. We will remain an emerging growth company under the JOBS Act until the earliest of (a) the last day of our first fiscal year following the fifth anniversary of our initial public offering, which was consummated on August 31, 2023, (b) the last date of our fiscal year in which we have total annual gross revenue of at least $1.07 billion, (c) the date on which we are deemed to be a “large accelerated filer” under the rules of the SEC with at least $700.0 million of outstanding securities held by non-affiliates, (d) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the previous three year, or (e) the date on which we affirmatively and irrevocably opts out of the extended transition period provided in the JOBS Act.

We are also a “smaller reporting company” as defined in the Exchange Act. We may continue to be a smaller reporting company even after we are no longer an emerging growth company. We may take advantage of certain of the scaled disclosures available to smaller reporting companies and will be able to take advantage of these scaled disclosures for so long as the market value of our Class A common stock held by non-affiliates is less than $250.0 million measured on the last business day of our second fiscal quarter, or our annual revenue is less than $100.0 million during the most recently completed fiscal year and the market value of our Class A common stock held by non-affiliates is less than $700.0 million measured on the last business day of our second fiscal quarter.

As a result of being an emerging growth company and a smaller reporting company, the information and financial statements in this prospectus and that we provide to our investors in the future may be different than what you might receive from other public reporting companies.

7

SUMMARY OF RISK FACTORS

Risks Related to our Business

| ● | We have a limited operating history, are not profitable and may never become profitable. |

| ● | If our business plan is not successful, we may not be able to continue operations as a going concern and our shareholders may lose their entire investment in us. |

| ● | If we fail to attract and keep senior management, we may be unable to successfully integrate acquisitions, scale our offerings of veterinary services, and deliver enhanced customer services, which may impact our results of operations and financial results. |

| ● | We may need to raise additional capital to achieve our goals. |

| ● | The Company incurs significant increased expenses and administrative burdens as a public company, which could have an adverse effect on its business, financial condition and results of operations. |

| ● | If we fail to manage our growth effectively, our brand, business and operating results could be harmed. |

| ● | We may seek to grow our business through acquisitions of, or investments in, new or complementary businesses, and facilities, or through strategic alliances, and the failure to manage these acquisitions or strategic alliances, or to integrate them with our existing business, could have a material adverse effect on us. |

| ● | We may seek to raise additional funds in the future through debt financing which may impose operational restrictions on our business and may result in dilution to existing or future holders of our common shares. |

| ● | We may acquire other businesses that may be unsuccessful and could adversely dilute your ownership of our company. |

| ● | We have generated net operating loss carryforwards for U.S. income tax purposes, but our ability to use these net operating losses may be limited by our inability to generate future taxable income. |

| ● | Our management does not have experience as senior management of a public company or ensuring compliance with public company obligations, and fulfilling these obligations will be expensive and time consuming, which may divert management’s attention from the day-to-day operation of its business. |

| ● | Failure to maintain effective internal controls over financial reporting could have a material adverse effect on the Company’s business, operating results and stock price. |

8

| ● | We may incur successor liabilities due to conduct arising prior to the completion of the various acquisitions. |

| ● | Purchasing real estate with hospital acquisitions brings additional complexity and cost. |

| ● | Our estimate of the size of our addressable market may prove to be inaccurate. |

| ● | We may be unable to execute our growth strategies successfully or manage and sustain our growth, and as a result, our business may be adversely affected. |

| ● | We may experience difficulties recruiting and retaining skilled veterinarians due to shortages that could disrupt our business. |

| ● | Negative publicity arising from claims that we do not properly care for animals we handle could adversely affect how we are perceived by the public and reduce our sales and profitability. |

| ● | Our quarterly operating results may fluctuate due to the timing of expenses, veterinary facility acquisitions, veterinary facility closures, and other factors. |

| ● | The COVID-19 outbreak has previously disrupted our business, and any future outbreak of a health epidemic or other adverse public health developments could materially and adversely affect our business and operating results. |

| ● | Our continued success is largely dependent on positive perceptions of our company. |

| ● | Our business may be harmed if our computer network containing employee or other information is compromised, which could adversely affect our results of operations. |

| ● | Labor disputes may have an adverse effect on our operations. |

| ● | We may be subject to personal injury, workers’ compensation, discrimination, harassment, wrongful termination, wage and hour, and other claims in the ordinary course of business. |

| ● | A decline in consumer spending or a change in consumer preferences or demographics could reduce our sales or profitability and adversely affect our business. |

| ● | Our reputation and business may be harmed if our or our vendors’ computer network security or any of the databases containing customer, employee, or other personal information maintained by us or our third-party providers is compromised, which could materially adversely affect our results of operations. |

| ● | The animal health industry is highly competitive. |

| ● | We may be unable to adequately protect our intellectual property rights. |

| ● | We may be subject to litigation. |

| ● | Natural disasters and other events beyond our control could harm our business. |

9

Risks Related to Government Regulation

| ● | Various government regulations could limit or delay our ability to develop and commercialize our services or otherwise negatively impact our business. |

| ● | Changes in laws or regulations, or a failure to comply with any laws and regulations, may adversely affect our business, investments and results of operations. |

| ● | Failure to comply with governmental regulations or the expansion of existing or the enactment of new laws or regulations applicable to our veterinary services could adversely affect our business and our financial condition or lead to fines, litigation, or our inability to offer veterinary products or services in certain states. |

| ● | We may fail to comply with various state or federal regulations covering the dispensing of prescription pet medications, including controlled substances, through our veterinary services businesses, which may subject us to reprimands, sanctions, probations, fines, or suspensions. |

| ● | We are subject to environmental, health, and safety laws and regulations that could result in costs to us. |

Risks Related to our Common Shares

| ● | We have received a listing deficiency notice from Nasdaq regarding our Class A common stock. |

| ● | It is not possible to predict the actual number of shares we will sell under the Purchase Agreement, or the actual gross proceeds resulting from those sales. We may not have access to the full amount available under the Purchase Agreement with Tumim. |

| ● | Investors who buy shares at different times will likely pay different prices. |

| ● | If securities or industry analysts do not publish research or reports about our company, or if they issue adverse or misleading opinions regarding us or our stock, our stock price and trading volume could decline. |

| ● | We do not intend to pay cash dividends for the foreseeable future. |

| ● | Our shares will be subordinate to all of our debts and liabilities, which increases the risk that you could lose your entire investment. |

| ● | Our board of directors may designate and issue shares of new classes of stock, including the issuance of up to 157,000 additional shares of Class B common stock, that could be superior to or adversely affect you as a holder of our Class A common stock. Although a majority of our board of directors are independent, our non-independent directors, officers, and their affiliates control approximately [37.2]% of the voting power of our outstanding common stock prior to this offering. |

| ● | The trading price of our Class A common stock is volatile, which could result in substantial losses to investors. |

| ● | The sale or availability for sale of substantial amounts of our Class A common stock could adversely affect their market price. |

| ● | We are an “emerging growth company” and a “smaller reporting company” and we cannot be certain if the reduced disclosure requirements applicable to emerging growth companies and a smaller reporting companies will make our Class A common stock less attractive to investors. |

| ● | We may be deemed a “controlled company” within the meaning of the rules of Nasdaq and, as a result, may qualify for, but do not intend to rely on, exemptions from certain corporate governance requirements. |

| ● | Sales of a significant number of shares of our Class A common stock in the public markets, or the perception that such sales could occur, could depress the market price of our Class A common stock. |

10

THE OFFERING

| Units offered | [ ] Units(1) on a reasonable best efforts basis. Each Unit will consist of one share of Class A common stock (or Pre-Funded Warrant to purchase one share of our Class A common stock in lieu thereof) and one Warrant to purchase one share of Class A common stock. The Units have no stand-alone rights and will not be certificated or issued as stand-alone securities. The shares of Class A common stock and Warrants can only be purchased together in this offering (other than pursuant to the underwriter’s option to purchase additional Units), but the components of the Units will be immediately separable and will be issued separately in this offering. |

| Warrants offered | Each Unit includes one share of Class A common stock and one Warrant to purchase one share of Class A common stock exercisable at a price of $[ ] (100% of the public offering price per Unit) and will be exercisable for a period of six months commencing upon issuance. See “Description of Capital Stock –Warrants Offered in this Offering” | |

| Pre-Funded Warrants | We are also offering to certain purchasers whose purchase of Units in this offering would otherwise result in the purchaser, together with its affiliates and certain related parties, beneficially owning more than 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding Class A common stock immediately following the consummation of this offering, the opportunity to purchase, if such purchasers so choose, in lieu of Units including shares of Class A common stock, Units including Pre-Funded Warrants in lieu of shares of Class A common stock that would otherwise result in any such purchaser’s beneficial ownership exceeding 4.99% (or, at the election of the purchaser, 9.99%) of our outstanding Class A common stock. The purchase price of each Unit including a Pre-Funded Warrant will be equal to [ ], and the exercise price of each Pre-Funded Warrant will be $0.001 per share.

Each Pre-Funded Warrant will be exercisable for one share of our Class A common stock and will be exercisable at any time after its original issuance until exercised in full. |

| Offering price | [ ] per Unit |

| Class A common stock outstanding before this offering | 958,033 shares of Class A common stock |

| Class B common stock outstanding | 38,915 shares of Class B common stock.

|

| Class A common stock outstanding after this offering †† | [ ] shares of Class A common stock.

| |

| Over-allotment option | We have granted Spartan, as Placement Agent, an option, exercisable for 45 days from the closing date of this offering, to purchase up to [ ] additional shares of Class A Common Stock, representing 15% of the shares of Common Stock sold in the offering, and/or up to [ ] Pre-Funded Warrants, representing 15% of the Pre-funded Warrants sold in the offering, and/or up to [ ] Warrants, representing 15% of the Warrants sold in the offering (the “Over-Allotment Option”). The underwriter may exercise the over-allotment option with respect to shares of common stock only, Pre-Funded Warrants only, Warrants only, or any combination thereof |

| Use of proceeds | We expect to receive up to $12 million in aggregate gross proceeds from this offering. We expect to use the net proceeds from this offering for general working capital. See “Use of Proceeds.” |

| Risk factors | Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 14 and the other information included in this prospectus for a discussion of factors you should consider carefully before deciding to invest in our securities. |

| Nasdaq symbol for our Class A common stock | “IVP” |

| Transfer Agent | VStock Transfer, LLC |

| † | The number of shares of our Class A common stock to be outstanding immediately prior to this offering is comprised of 958,033 shares of our Class A common stock issued and outstanding as the date of this prospectus and excludes shares that are potentially issuable: |

| ● | upon the exercise of warrants outstanding as of the date of this prospectus (1); |

11

| ● | upon the conversion of shares of Series A preferred stock outstanding as of the date of this prospectus(2); |

| ● | to Tumim under the Purchase Agreement (including the Commitment Shares); and |

| ● | upon the conversion of 38,915 shares of Class B common stock(3) outstanding as of the date of this prospectus. |

| †† | The number of shares of our Class A common stock to be outstanding following this offering of a fully-diluted basis consist of: |

| ● | 28,540 shares of Class A common stock that are potentially issuable upon the exercise of warrants outstanding as of the date of this prospectus(1); |

| ● | 103,318 shares of Class A common stock that are potentially issuable upon conversion of 264 shares of Series A preferred stock(2) outstanding as of the date of this prospectus; the holders of Series A preferred stock have the right to vote as-if-converted, on all matters submitted to a vote of holders of the Company’s Class A common stock, including the election of directors, and all other matters as required by law, subject to the certain limits on beneficial ownership contained in the Certificate of Designations relating to the Series A preferred stock; |

| ● | [ ] shares of Class A common stock (low-range) or [ ] shares of Class A common stock (high-range) that are potentially issuable pursuant to this offering; and |

| ● | 38,915 shares of Class A common stock that are potentially issuable upon conversion of 38,915 shares of Class B common stock(3) outstanding as of the date of this prospectus. |

| 1) | Shares that are potentially issuable upon exercise of warrants include: |

| ● | 500 shares of Class A common stock issued to our Chair, President and Chief Executive Officer Kimball Carr in connection with his personal guaranty of certain loans to the Company; |

| ● | 19,624 shares of Class A common stock that are potentially issuable upon exercise of warrants issued in connection with the initial public offering and held by Spartan Capital Securities, LLC, the underwriter in our initial public offering; |

| ● | 120 shares of Class A common stock that are potentially issuable upon exercise of warrants held by Exchange Listing, LLC, pursuant to a capital market advisory agreement (the “Advisory Agreement”), dated as of December 28, 2021; and |

| ● | 8,296 shares of Class A common stock that are potentially issuable upon exercise of the New Warrants held by Target Capital 1, LLC, Dragon Dynamic Catalytic Bridge SAC Fund and 622 Capital LLC (the “New Warrant Holders”). |

| 2) | [ ] shares of Class A common stock are issuable upon conversion of [ ] shares of Series A preferred stock, $0.0001 par value. Each share of Series A preferred stock may convert, at the option of the holders at any time and from time, into a number of shares of Class A common stock equal to the stated value divided by a conversion price. The conversion price is equal to 60% of the dollar volume-weighted average price for shares for the Company’s Class A common stock for the three trading days immediately preceding the date of the conversion. However, the conversion price can never be less than $0.25 per-share. |

| 3) | Each share of Class B common stock entitles the holder of record to twenty-five (25) votes on all matters submitted to a vote of stockholders and is convertible into one share of Class A Common Stock at the option of the holder. |

Unless otherwise indicated, this prospectus reflects and assumes the following:

| ● | no exercise of outstanding options or warrants described above; |

| ● | no exercise of the Warrants, Pre-Funded Warrant, which, if sold, would reduce the number of Units that we are offering on a one-for-one basis, and ; and |

| ● | no exercise by the Placement Agent of the Placement Agent Warrant. |

| ● | No exercise by the Placement Agent of the Overallotment Option |

12

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Forward-looking statements are based upon our current assumptions, expectations and beliefs concerning future developments and their potential effect on our business. In some cases, you can identify forward-looking statements by the following words: “may,” “will,” “could,” “would,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “approximately,” “estimate,” “predict,” “project,” “potential,” “continue,” “ongoing,” or the negative of these terms or other comparable terminology, although the absence of these words does not necessarily mean that a statement is not forward-looking. This information may involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by any forward-looking statements.

We cannot predict all of the risks and uncertainties. Accordingly, such information should not be regarded as representations that the results or conditions described in such statements or that our objectives and plans will be achieved and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. These forward-looking statements are found at various places throughout this prospectus and include information concerning possible or assumed future results of our operations, including statements about potential acquisition or merger targets; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future acquisitions, future cash needs, future operations, business plans and future financial results, and any other statements that are not historical facts.

All forward-looking statements speak only as of the date of this prospectus. We undertake no obligation to update any forward-looking statements or other information contained herein. Shareholders and potential investors should not place undue reliance on these forward-looking statements. Although we believe that our plans, intentions and expectations reflected in or suggested by the forward-looking statements in this report are reasonable, we cannot assure stockholders and potential investors that these plans, intentions or expectations will be achieved.

These forward-looking statements represent our intentions, plans, expectations, assumptions ‘and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. Considering these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this prospectus. All subsequent written and oral forward-looking statements concerning other matters addressed in this prospectus and attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to herein.

Except to the extent required by law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, a change in events, conditions, circumstances or assumptions underlying such statements, or otherwise.

13

RISK FACTORS

Investing in our Class A common stock involves a high degree of risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the accompanying notes thereto included elsewhere in this prospectus, before deciding whether to invest in our Class A common stock. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of or that we deem immaterial may also become important factors that adversely affect our business. The realization of any of these risks and uncertainties could have a material adverse effect on our reputation, business, financial condition, results of operations, growth and future prospects, as well as our ability to accomplish our strategic objectives. In that event, the market price of our Class A common stock could decline and you could lose part or all of your investment.

Unless the context otherwise requires, references in this section to “we,” “us,” “our,” “Inspire Veterinary” and the “Company” refer to Inspire Veterinary Partners, Inc.

Risks Related to our Business

We have a limited operating history, are not profitable and may never become profitable.

We have not generated any net profits to date, and we expect to continue to incur significant acquisition related costs and other expenses. Our net loss for the twelve months ended December 31, 2023 was $14,792,886 and for the years ended December 31, 2022 and 2021 was $(4,911,926) and $(1,331,062), respectively. Our accumulated deficit as of December 31, 2023 was $21,215,257. As of December 31, 2023, we had total stockholders’ equity of approximately $788,259. We expect to continue to incur net losses for the foreseeable future, as we continue our development and acquisition of veterinary hospitals and related veterinary servicing activities. If we fail to achieve or maintain profitability, then we may be unable to continue our operations at planned levels and be forced to reduce or cease operations.

If our business plan is not successful, we may not be able to continue operations as a going concern and our shareholders may lose their entire investment in us.

As discussed in the Notes to Financial Statements included in this Registration Statement, as of December 31, 2023, we had $378,961 cash and restricted cash.

If we fail to raise sufficient capital pursuant to the Purchase Agreement, we will have to explore other financing activities to provide us with the liquidity and capital resources we need to meet our working capital requirements and to make capital investments in connection with ongoing operations. We cannot give assurance that we will be able to secure the necessary capital when needed. Consequently, we raise substantial doubt that we will be able to continue operations as a going concern, and our independent auditors included an explanatory paragraph regarding this uncertainty in their report on our financial statements for the year ended December 31, 2023. Our ability to continue as a going concern is dependent upon our generating cash flow sufficient to fund operations and reducing operating expenses. Our business plans may not be successful in addressing the cash flow issues. If we cannot continue as a going concern, our shareholders may lose their entire investment in us. If we fail to raise sufficient capital, we will have to explore other financing activities to provide us with the liquidity and capital resources we need to meet our working capital requirements and to make capital investments in connection with ongoing operations. We cannot give assurance that we will be able to secure the necessary capital when needed. Consequently, we raise substantial doubt that we will be able to continue operations as a going concern, and our independent auditors included an explanatory paragraph regarding this uncertainty in their report on our financial statements for the years ended December 31, 2023 and 2022. Our ability to continue as a going concern is dependent upon our generating cash flow sufficient to fund operations and reducing operating expenses. Our business plans may not be successful in addressing the cash flow issues. If we cannot continue as a going concern, our shareholders may lose their entire investment in us.

If we fail to attract and keep senior management, we may be unable to successfully integrate acquisitions, scale our offerings of veterinary services, and deliver enhanced customer services, which may impact our results of operations and financial results.

Our success depends in part on our continued ability to attract, retain and motivate highly qualified management and senior personnel. We are highly dependent upon our senior management, particularly Kimball Carr, our Chair, President and Chief Executive Officer, and Richard Frank, our Chief Executive Officer. The loss of services of any of these individuals could negatively impact our ability to successfully integrate acquisitions, scale our employee roster, and deliver enhanced veterinary services, which may impact our results of operations and financial results. Although we have entered an employment agreement with Kimball Carr, our Chair, President and Chief Executive Officer, for one 3-year term (automatically extending for one-year terms thereafter) there can be no assurance that Mr. Carr or any other senior executive officer will extend their terms of service.

14

We may need to raise additional capital to achieve our goals.

We currently incur operate at a net loss and a comprehensive loss and anticipate incurring additional expenses as a public company. We are also seeking to identify potential complementary acquisition opportunities in the veterinary services and animal health sectors. Some of our anticipated future expenditures will include: costs of identifying additional potential acquisitions; costs of obtaining regulatory approvals; and costs associated with marketing and selling our services. We also may incur unanticipated costs. Because the outcome of our development activities and commercialization efforts is inherently uncertain, the actual amounts necessary to successfully complete the development and commercialization of our existing or future veterinary services s may be greater or less than we anticipate.

As a result, we will need to obtain additional capital to fund the development of our business. We have no master agreements or arrangements with respect to any financings, and any such financings may result in dilution to our shareholders, the imposition of debt covenants and repayment obligations or other restrictions that may adversely affect our business or the value of our common shares.

Additional funds may not be available when we need them on terms that are acceptable to us, or at all. If adequate funds are not available to us on a timely basis, we may be required to delay, limit, reduce or terminate one or more of our veterinary service programs or any future commercialization efforts.

The Company incurs significant increased expenses and administrative burdens as a public company, which could have an adverse effect on its business, financial condition and results of operations.