UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

OR

For

the Fiscal Year Ended

OR

OR

Date of event requiring this shell company report ________

For the transition period from __________ to __________

Commission

file number

(Exact Name of registrant as specified in its charter)

Not

Applicable

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(65)

8304 8372

(Address of principal executive offices)

Email:

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| The |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

| None |

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

| None |

(Title of Class)

Indicate

the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered

by the annual report: as of October 31, 2022,

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ☐

If this

report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section

13 or 15(d) of the Securities Exchange Act of 1934. **Yes ☐ No

If

this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13

or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate

by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2)

has been subject to such filing requirements for the past 90 days. **Yes ☐

Indicate

by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule

405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit such files). **Yes ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Emerging growth company |

If

an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant

has elected not to use the extended transition period for complying with any new or revised financial accounting standards † provided

pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. **Yes ☐ No ☒

If

securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant

included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☒ | International Financial Reporting Standards as issued By the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

☐ No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. **Yes ☐ No ☐

Table of Contents

i

INTRODUCTION

FREQUENTLY USED TERMS

Unless otherwise indicated, “we,” “us,” “our,” “Caravelle,” and “the Company” and similar terminology refer to Caravelle International Group, an exempted company incorporated under the laws of the Cayman Islands, and its subsidiaries subsequent to the Business Combination (defined below).

“Amended and Restated Registration Rights Agreement” means the amended and restated registration rights agreement that certain holders of ordinary shares of the Caravelle, certain holders of Pacifico Common Stock, and the holders of the Private Units entered into at the Closing.

“BDI” means the Baltic Dry Index, an index of the daily average of charter rates for key routes published by the Baltic Exchange Limited.

“Business Combination” means the Mergers and the other Transactions to be consummated under the Merger Agreement.

“Caravelle” means Caravelle International Group, a Cayman Islands exempted company.

“Caravelle Board” means the board of directors of Caravelle.

“Caravelle Group” means Caravelle Group Co., Ltd prior to the consummation of the Business Combination.

“Caravelle Ordinary Share(s)” means Ordinary Share(s) of Caravelle, par value $0.0001 per share.

“Chardan” means Chardan Capital Markets LLC.

“Closing” means the closing of the Business Combination.

“Code” means the Internal Revenue Code.

“Combined Company” means Caravelle and its consolidated subsidiaries after the consummation of the Business Combination.

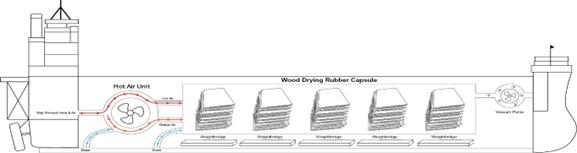

“CO-Tech” means new carbon neutral ocean technology. The CO-Tech business is an innovative integration of ocean shipping, wood drying, and carbon trading businesses.

“Earnout Shares” means initial earnout shares and subsequent earnout shares.

“Founder Shares” refer to the 1,437,500 shares of common stock held or controlled by Pacifico’s insiders prior to the IPO.

“GAAP” means accounting principles generally accepted in the United States of America.

“IFRS” means the International Financial Reporting Standards.

“Incentive Plan” means Caravelle 2022 Share Incentive Plan.

“Initial Merger” means the merger of Merger Sub 1 with and into Caravelle Group.

“Initial Stockholders” means the stockholders who hold the Founder Shares.

“IPO” means Pacifico’s initial public offering.

“Lock-up Agreements” means the lock-up agreements that certain holders of Caravelle Group ordinary shares and certain holders of Pacifico Common Stock executed contemporaneously with the execution of the Merger Agreement.

“Merger” means SPAC Merger and Initial Merger.

“Merger Agreement” means certain Agreement and Plan of Merger (as may be amended, supplemented or otherwise modified from time to time) entered into by Caravelle, Merger Sub 1, Merger Sub 2 and Caravelle Group on April 5, 2022 and amended by the Amended and Restated Agreement and Plan of Merger dated August 15, 2022.

ii

“Merger Sub 1” means Pacifico International Group, a Cayman Islands exempted company and a direct wholly owned subsidiary of Caravelle.

“Merger Sub 2” means Pacifico Merger Sub 2 Inc., a Delaware corporation and a direct wholly owned subsidiary of Caravelle.

“Nasdaq” means The Nasdaq Stock Market LLC.

“Pacifico” means Pacifico Acquisition Corp.

“Pacifico Common Stock” means shares of common stock of Pacifico.

“Pacifico Rights” means rights of Pacifico.

“Pacifico securities” means Pacifico Units, Pacifico Common Stock (excluding any redeemed shares) and Pacifico Rights.

“Pacifico Units” means units of Pacifico.

“Private Units” means the 307,500 units of Pacifico that the Sponsor and Chardan purchased at a price of $10.00 per Private Unit for an aggregate purchase price of $3,075,000 in a private placement.

“Public Shares” means shares of common stock of Pacifico sold as part of the Public Units in the IPO.

“Public Units” means units of Pacifico sold in the IPO.

“SEC” means the United States Securities and Exchange Commission.

“Securities Act” means the United States Securities Act of 1933, as amended.

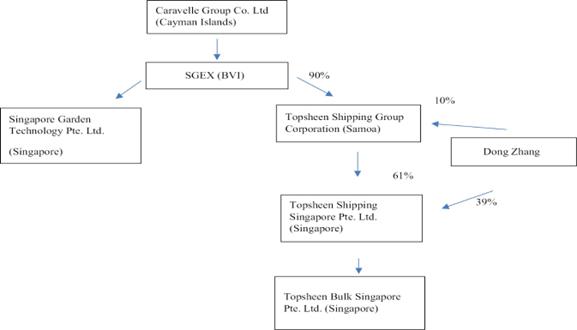

“SGEX” means SGEX Group Co., Ltd.

“Singapore Garden” means Singapore Garden Technology Pte. Ltd.

“Singapore Subsidiary” means either Topsheen Shipping Singapore Pte. Ltd., Topsheen Bulk Singapore Pte. Ltd. or Singapore Garden Technology Pte. Ltd. (collectively, the “Singapore Subsidiaries”).

“SPAC Merger” means the merger of Merger Sub 2 with and into Pacifico.

“Sponsor” means Pacifico Capital LLC.

“TBS” means Topsheen Bulk Shipping Pte. Ltd.

“Transactions” means, collectively, the Mergers and each of the other transactions contemplated by the Merger Agreement or any of the ancillary agreements.

“TSGC” means Topsheen Shipping Group Corporation.

“TSS” means Topsheen Shipping Singapore Pte. Ltd.

“Topsheen Companies” means TBS, TSGC, and TSS.

“Trust Account” means Pacifico’s U.S.-based trust account with American Stock Transfer & Trust Company, LLC for the benefit of Pacifico’s public stockholders.

iii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F (including information incorporated by reference herein, “this Report”) is being filed by Caravelle.

This Report contains or may contain forward-looking statements as defined in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”) that involve significant risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements include information about our possible or assumed future results of operations or our performance. Words such as “expects,” “intends,” “plans,” “believes,” “anticipates,” “estimates,” and variations of such words and similar expressions are intended to identify the forward-looking statements. The risk factors and cautionary language in this Report provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described in our forward-looking statements, including among other things, the items identified in “Item 3.D. — Risk Factors” section of this Report.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Report. Although we believe that the expectations reflected in such forward-looking statements are reasonable, there can be no assurance that such expectations will prove to be correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates which are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. Actual results may differ materially from those expressed or implied by such forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statements contained in this Report, or the documents to which we refer readers in this Report, to reflect any change in our expectations with respect to such statements or any change in events, conditions or circumstances upon which any statement is based.

iv

EXPLANATORY NOTE

On April 5, 2022, Pacifico Acquisition Corp. entered into that certain Agreement and Plan of Merger which was amended by the Amended and Restated Agreement and Plan of Merger dated August 15, 2022, by and among Caravelle International Group (“Caravelle”), Pacifico International Group, a Cayman Islands exempted company and a direct wholly-owned subsidiary of Caravelle (“Merger Sub 1”), Pacifico Merger Sub 2 Inc., a Delaware corporation and a direct wholly-owned subsidiary of Caravelle (“Merger Sub 2”), and Caravelle Group Co., Ltd, a Cayman Islands exempted company (“Caravelle Group”), pursuant to which (a) Merger Sub 1 merged with and into Caravelle Group, and Caravelle Group became the surviving corporation of the Initial Merger and a direct wholly owned subsidiary of Caravelle, and (b) following confirmation of the effectiveness of the Initial Merger, Merger Sub 2 merged with and into Pacifico, and Pacifico became the surviving corporation of the SPAC Merger and a direct wholly owned subsidiary of Caravelle.

On December 16, 2022, Caravelle consummated the Business Combination pursuant to the terms of the Merger Agreement and Caravelle Group became a wholly owned subsidiary of Caravelle. On December 19, 2022, Caravelle’s ordinary shares commenced trading on Nasdaq under the symbol “CACO.”

As a result of the Business Combination, among other things, (i) all outstanding ordinary shares of Caravelle Group were cancelled in exchange for 50,000,000 ordinary shares of Caravelle, (ii) each outstanding unit of Pacifico (the “Pacifico Unit”) was automatically detached, (iii) each unredeemed outstanding share of common stock of Pacifico (the “Pacifico Common Stock”) was cancelled in exchange for the right to receive one (1) Ordinary Share of Caravelle, (iv) every ten (10) outstanding rights of Pacifico (the “Pacifico Rights”) were contributed in exchange for one (1) Ordinary Share of Caravelle, and were cancelled and cease to exist, and (v) each unit purchase option of Pacifico (the “Pacifico UPO”) was automatically cancelled in exchange for one (1) unit purchase option of Caravelle (the “UPO”).

Caravelle was determined to be the accounting acquirer given that the original shareholders of Caravelle Group effectively controlled the combined entity after the Business Combination. Pacifico is treated as the acquired company for financial reporting purposes. This determination is primarily based on the fact that subsequent to the Business Combination, Caravelle’s shareholders have a majority of the voting power of the combined company, Caravelle comprised all of the ongoing operations of the combined entity, Caravelle comprised a majority of the governing body of the combined company, and Caravelle’s senior management comprised all of the senior management of the combined company. Accordingly, for accounting purposes, the Business Combination is accounted for as a reverse recapitalization, which is equivalent to the issuance of shares by Caravelle for the net assets of Pacifico, accompanied by a recapitalization. Caravelle is determined as the predecessor, and the historical financial statements of Caravelle Group became Caravelle’s historical financial statements, with retrospective adjustments to give effect of the reverse recapitalization. The share and per share data is retrospectively restated to give effect to the reverse recapitalization. Net assets of Pacifico were stated at historical costs. No goodwill or other intangible assets were recorded. Operations prior to the Business Combination were those of the Caravelle Group.

v

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

A. Directors and Senior Management

Not applicable.

B. Advisors

Not applicable.

C. Auditors

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. Selected Financial Data

See “Item 18. Financial Statements.”

B. Capitalization and indebtedness

Not applicable.

C. Reasons for the offer and use of proceeds

Not applicable.

D. Risk factors

Investing in the securities of Caravelle involves a high degree of risk. In addition to the other information contained in this Report, including the matters addressed under the headings “Cautionary Note Regarding Forward-Looking Statements,” “Item 5. Operating and Financial Review and Prospects”, and the consolidated financial statements and related notes contained herein, you should carefully consider the following risk factors presented in this Report. The risks associated with Caravelle are discussed below, and many of these risks may have various ramifications. Therefore, the information below should be viewed as a starting point for understanding the significant risks relating to Caravelle, and not as a limitation on the potential impact of the matters discussed. The business, results of operations, financial condition and prospects of Caravelle could also be harmed by risks and uncertainties that are not presently known to us or that we currently believe are not material. If any of the risks actually occur, the business, results of operations, financial condition and prospects of Caravelle could be materially and adversely affected. Unless otherwise indicated, references to business being harmed in these risk factors include harm to business, reputation, brand, financial condition, results of operations and future prospects.

Summary of Risk Factors

The following summary description sets forth an overview of the material risks we are exposed to in the normal course of our business activities. The summary does not purport to be complete and is qualified in its entirety by reference to the full risk factor discussion immediately following this summary description. We encourage you to read the full risk factor discussion carefully. The occurrence of one or more of the events or circumstances described in this section, alone or in combination with other events or circumstances, may have a material adverse effect on our business, cash flows, financial condition and results of operations.

1

Risks Related to the International Shipping Industry

| ● | The cyclical nature of the shipping industry could have an adverse effect on Caravelle’s business. |

| ● | Caravelle’s profitability and growth depend on the demand for shipping vessels and global economic conditions, and the impact of consumer confidence and consumer spending on shipping volume and charter rates. Charter hire rates for shipping vessels may experience volatility or increase, which would, in turn, adversely affect Caravelle’s profitability. |

| ● | Outbreaks of epidemic and pandemic diseases, and governmental responses thereto, could adversely affect Caravelle’s business. The COVID-19 pandemic, and measures to contain its spread, have impacted the markets in which Caravelle operates and could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations. |

| ● | If global economic conditions weaken, particularly in the Asia Pacific region, it could have a material adverse effect on Caravelle’s business, financial condition and results of operations. |

| ● | An increase in trade protectionism globally could have a material adverse impact on Caravelle’s business and, in turn, could cause a material adverse impact on Caravelle’s business, financial condition, results of operations and cash flows. |

| ● | Caravelle operates in a highly competitive international shipping industry and if Caravelle does not compete successfully with new entrants or established companies with greater resources, its shipping business growth and results of operations may be adversely affected. |

| ● | Increases in marine fuel prices could increase Caravelle’s operating costs. |

| ● | Increases in port fees and stevedoring expenses could increase Caravelle’s operating costs. |

| ● | World events, including terrorist attacks and regional conflict, could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations. |

| ● | Acts of piracy on ocean-going vessels may have a material adverse effect on Caravelle’s business, financial condition, cash flows, and results of operations. |

| ● | Increased inspection procedures and tighter import and export controls could increase costs and disrupt Caravelle’s business. |

| ● | Caravelle’s freights may call on ports located in countries that are subject to restrictions imposed by the United States, United Kingdom, United Nations or other governments. |

Risks Related to Caravelle’s International Shipping Business

| ● | Caravelle operates carriers worldwide and, as a result, its business has inherent operational risks, which may reduce its revenue or increase its expenses, and Caravelle may not be adequately covered by insurance. |

| ● | Caravelle charters vessels mostly from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer. |

| ● | Labor interruptions could disrupt Caravelle’s business. |

| ● | Failure to comply with the U.S. Foreign Corrupt Practices Act and other anti-bribery legislation in other jurisdictions could result in fines, criminal penalties, contract terminations and an adverse effect on Caravelle’s business. |

| ● | The smuggling of drugs or other contraband onto Caravelle’s freight may lead to governmental claims against Caravelle. |

| ● | Caravelle needs to maintain its relationships with local shipping agents, port and terminal operators. |

Risks related to Caravelle’s CO-Tech Business

| ● | Caravelle’s CO-Tech business has no operating history, and its project growth might not be realized. |

2

| ● | Caravelle’s yet to be launched CO-Tech business sector has no operating history and no revenues, and there is no past performance with which to evaluate Caravelle’s ability to achieve its business objectives. |

| ● | Caravelle’s forecast regarding its CO-Tech business relies in large part upon assumptions and analyses developed by its management. If these assumptions and analyses prove to be incorrect, its actual operating results could suffer. |

| ● | Caravelle expects its operating expenses to increase significantly in the future, which may impede its ability to achieve profitability. |

| ● | Caravelle is dependent upon its proprietary intellectual properties. |

| ● | Caravelle’s CO-Tech model is in the early stages and it may not become profitable within twelve months after the closing of the Business Combination, if at all. |

| ● | Caravelle purchases its CO-Tech equipment from New Galion Group (HK) Co Ltd (“New Galion”) and purchases a vessel from Beijing Hanpu Technology Co., Ltd, both of which are controlled by Dr. Guohua Zhang, Caravelle’s Chief Executive Officer. In addition, Caravelle will rent vessels for the CO-Tech business from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer. |

| ● | Supply and distribution chain disruptions could adversely affect Caravelle’s business. |

| ● | Caravelle depends on third parties for logging and transportation services and increases in the costs or decreases in the availability of quality service providers could adversely affect its business. |

| ● | In the new CO-Tech wood desiccation business, the revenue and profit may be subject to high volatility because the need for wood desiccation service is determined by the market’s supply of timber and demand for wood products, and such markets are cyclical and competitive. |

| ● | Caravelle’s growth depends on the continued growth of the need for wood desiccation, wood vinegar, and further development of the carbon trading market. |

| ● | Caravelle may not be able to obtain the necessary certification from the classification societies. |

| ● | Caravelle depends on the core technologies licensed by Dr. Guohua Zhang, in the CO-Tech business, thus, if Dr. Zhang revokes such license, Caravelle’s business will be substantially affected. |

| ● | Caravelle currently lacks employees with adequate training and experience to carry out the CO-Tech business on-board. |

Risks related to Caravelle’s Overall Business

| ● | It is not certain if Caravelle will be classified as a Singapore tax resident. |

| ● | The ability of Caravelle’s subsidiaries and consolidated affiliated entities in Singapore and Samoa to distribute dividends to Caravelle may be subject to restrictions under Singapore and Samoa laws. |

| ● | Caravelle may require additional capital to implement its business strategy, including to develop its business in carbon neutral shipping and to expand its traditional international shipping business, and it may need to raise additional funds in the future. |

| ● | Caravelle may require additional capital to implement its business strategy, including to develop its business in carbon neutral shipping and to expand its traditional international shipping business, and it may need to raise additional funds in the future. |

| ● | Caravelle’s business depends upon certain employees who may not necessarily continue to work for us. |

| ● | Caravelle might not obtain and maintain sufficient insurance coverage, which could expose Caravelle to significant costs and business disruption. |

| ● | Caravelle may be subject to litigation that, if not resolved in its favor, could have a material adverse effect on its business, financial condition, cash flows and results of operations. |

| ● | The requirements of being a public company have increased certain of Caravelle’s costs and require significant management focus. |

3

| ● | Because Caravelle generates most of the revenues in United States dollars but incurs a portion of the expenses in other currencies, exchange rate fluctuations could hurt the results of operations. |

| ● | Global inflationary pressures could negatively impact Caravelle’s results of operations and cash flows. |

| ● | Failure to comply with the U.S. sanction laws could result in fines, criminal penalties, and an adverse effect on Caravelle’s business. |

| ● | Security breaches and disruptions to Caravelle’s information technology infrastructure (cyber-security) could interfere with its operations and expose it to liability, which could have a material adverse effect on its business, financial condition, cash flows and results of operations. |

| ● | Caravelle is leveraged, which could limit its ability to execute its business strategy and Caravelle may be unable to comply with its covenants in its credit facilities that impose operating and financial restrictions on it, which could result in a default under the terms of these agreements. |

Risks Related to Caravelle

| ● | No public market for Caravelle’s shares and uncertainty in the development of an active trading market for Caravelle’s shares; |

| ● | Price volatility of Caravelle’s shares; |

| ● | Sale or availability for sale of substantial amounts of Caravelle’s shares; |

| ● | Potential dilution for existing shareholders upon Caravelle’s issuance of additional shares; |

| ● | Potential treatment of Caravelle as a passive foreign investment company; |

| ● | Potential treatment of Caravelle as a U.S. corporation for U.S. federal income tax purposes; and |

| ● | Exemptions from requirements applicable to other public companies due to Caravelle’s status as an emerging growth company. |

Risks Related to Caravelle’s Business

In addition to the other information included in this Report, the considerations listed below could have a material adverse effect on Caravelle’s business, financial condition or results of operations, cash flows, or ability to pay dividends, future prospects, or financial performance. The risks set forth below comprise all material risks currently known to Caravelle. These factors should be considered carefully, together with the information and financial data set forth in this Report.

Risks Related to the International Shipping Industry

The cyclical nature of the shipping industry could have an adverse effect on Caravelle’s business.

Historically, the financial performance of the shipping industry has been cyclical, with volatility in profitability and asset values resulting from changes in the supply of, and demand for, international maritime shipping services. The level of shipping capacity is a function of the number and size of vessels in the world fleet, their deployment, the delivery of new vessels and the scrapping of older vessels. The demand for international maritime shipping services is influenced by, among other factors, global and regional economic conditions, currency exchange rates, the globalization of manufacturing, fluctuation in the levels of global and regional international trade, regulatory developments and changes in seaborne and other transportation patterns. Changes in the demand for international maritime shipping services are difficult to predict. Decreases in such demand and/or increases in international maritime shipping capacity could lead to significantly lower freight rates, reduced volume, or a combination of the two, which would have a material adverse effect on Caravelle’s business, financial condition and results of operations.

Caravelle’s profitability and growth depend on the demand for shipping vessels and global economic conditions, and the impact of consumer confidence and consumer spending on shipping volume and charter rates. Charter hire rates for shipping vessels may experience volatility or increase, which would, in turn, adversely affect Caravelle’s profitability.

The ocean-going shipping industry is both cyclical and volatile in terms of charter hire rates and profitability. Charter rates are impacted by various factors, including supplies of vessels, the level of global trade, exports from one part of the world to the other parts, demand for the seaborne transportation cargoes, and shipping capacity. High demand for shipping capacity and lower supply of shipping capacity could result in higher charter rates, which may adversely affect Caravelle’s profitability. The factors affecting the supply and demand for shipping vessels are outside of the control of Caravelle, and the nature, timing and degree of changes in industry conditions are unpredictable. The Baltic Dry Index, or the BDI, an index of the daily average of charter rates for key routes published by the Baltic Exchange Limited, which has long been viewed as the main benchmark to monitor the movements of the vessel charter market and the performance of the entire shipping market, declined approximately 97.5% from its high of 11,793 in May 2008 to 290 on February 10, 2016, and has remained volatile since then. During the year ended December 31, 2021, the BDI rose to an average of 4,948 from an average of 1,066 in the previous year. For the month of December 2022, the daily average BDI was 1,466. A significant increase in charter rates would adversely affect Caravelle’s profitability, cash flows and ability to pay dividends.

4

Factors that influence demand for shipping capacity include:

| ● | supply and demand for products suitable for maritime shipping; |

| ● | changes in global production of products transported by ships; |

| ● | the distance that cargo products are to be moved by sea; |

| ● | the globalization and deglobalization of manufacturing; |

| ● | global and regional economic and political conditions; |

| ● | developments and disruptions in international trade; |

| ● | changes in seaborne and other transportation patterns, including changes in the distances over which cargoes are transported and the speed of vessels; |

| ● | environmental and other regulatory developments; and |

| ● | currency exchange rates. |

Factors that influence the supply of shipping capacity include:

| ● | the number of new building deliveries; |

| ● | the scrapping rate of older shipping vessels; |

| ● | the price of steel and other raw materials; |

| ● | changes in environmental and other regulations that may limit the useful life of shipping vessels; |

| ● | the number of shipping vessels that are out of service; and |

| ● | port congestion. |

Outbreaks of epidemic and pandemic diseases, and governmental responses thereto, could adversely affect Caravelle’s business. The COVID-19 pandemic, and measures to contain its spread, have impacted the markets in which Caravelle operates and could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations.

The COVID-19 pandemic and measures to contain its spread, continues to negatively impact regional and global economies and trade patterns in markets in which Caravelle operates, the way Caravelle operates its business, and the businesses of its customers and suppliers. Governments in affected countries have been imposing travel bans, quarantines and other emergency public health measures and a number of countries have implemented lockdown measures. Companies, including Caravelle, are also taking precautions, such as requiring employees to work remotely, and imposing travel restrictions. These restrictions have had an adverse impact on global economic conditions, resulted in turmoil in the shipping, credit and other markets which affect Caravelle, and introduced new risks to Caravelle’s operations, some of which may not yet have become evident to Caravelle. As a result of these measures, Caravelle’s chartered ships may not be able to call on ports, or may be restricted from departing from ports, and the duration of voyages may increase in order to accommodate mandatory minimum periods between port calls which could increase Caravelle’s costs and delay the due date for payment of freight to Caravelle. In addition, Caravelle may experience severe operational disruptions and delays, unavailability of normal port infrastructure and services including limited access to equipment, critical goods and personnel, closure of ports and customs offices, disruptions to crew change, quarantine of ships and/or crew, counterparty credit risk, limitations on sources of cash and liquidity, as well as disruptions in the supply chain and industrial production which may lead to reduced cargo supply and/or the demand for such cargo and thus to a decline in the demand for Caravelle’s services, among other potential consequences. Ongoing prevention and mitigation measures, and negative economic and trade impacts of the COVID-19 outbreak could materially and adversely affect Caravelle’s future operations, its business, financial condition and cash flows. The extent of the COVID-19 outbreak’s effect on Caravelle’s operational and financial performance will depend on future developments, including the duration, spread and intensity of the outbreak, the emergence of new variants, the development, availability, distribution and effectiveness of vaccines and treatments, the imposition of protective public safety measures and the impact on the global economy, all of which are uncertain and difficult to predict considering the rapidly evolving situation. As a result, the ultimate severity of the COVID-19 pandemic is uncertain at this time and therefore Caravelle cannot predict the impact it may have on its future operations, which impact could be material and adverse.

5

If global economic conditions weaken, particularly in the Asia Pacific region, it could have a material adverse effect on Caravelle’s business, financial condition and results of operations.

Global economic conditions impact worldwide demand for various goods and, thus, shipping. In particular, Caravelle anticipates a significant number of the port calls made by its freight will continue to involve the loading or unloading of cargos in ports in the Asia Pacific region. As a result, negative changes in economic conditions in any Asia Pacific country can have a significant impact on the demand for international maritime shipping. However, if the pace in growth in the Asia Pacific region experiences slower or negative economic growth in the future, this may impose negative impact on the international maritime shipping demand.

An increase in trade protectionism globally could have a material adverse impact on Caravelle’s business and, in turn, could cause a material adverse impact on Caravelle’s business, financial condition, results of operations and cash flows.

Caravelle’s operations are exposed to the risk that increased trade protectionism globally could adversely affect Caravelle’s business. Governments may turn to trade barriers to protect or revive their domestic industries in the face of foreign imports, thereby depressing the demand for shipping. Restrictions on imports, including in the form of tariffs, could have a major impact on global trade and demand for shipping. Trade protectionism in the markets that Caravelle serves may cause an increase in the cost of exported goods, the length of time required to deliver goods and the risks associated with exporting goods and, as a result, a decline in the volume of exported goods and demand for shipping.

Caravelle’s shipping business is deployed on routes involving seaborne trade in and out of emerging markets, and Caravelle’s shipping and business revenue may be derived from the shipment of goods from Asia to various overseas export markets. Any reduction in or hindrance to the output of Asia-based exporters could have a material adverse effect on the growth rate of Asia’s exports and on Caravelle’s business.

Caravelle operates in a highly competitive international shipping industry and if Caravelle does not compete successfully with new entrants or established companies with greater resources, its shipping business growth and results of operations may be adversely affected.

The worldwide international maritime shipping business is highly competitive. Barriers to entry are relatively low for existing shipping companies wishing to enter, or expand their presence in, a new market or new trade lane. Carriers compete based on price, frequency of service, transit time, port coverage, service reliability, vessel availability, inland operations, quality of customer service, value added services and other customer requirements. There is strong competition in the international markets and trade lanes that Caravelle currently operates in, and Caravelle expects that current competitive pressures within the international maritime shipping industry will continue.

Increases in marine fuel prices could increase Caravelle’s operating costs.

In fiscal years 2020 and 2021, the cost of marine fuel accounted for about 25.3% and 24.3% of Caravelle’s total operating costs. For the fiscal year ended October 31, 2022, the cost of marine fuel accounted for about 21.9% of Caravelle’s total operating costs. The cost of marine fuel is subject to many economic and political factors which are beyond Caravelle’s control. The price and supply of fuel are unpredictable and fluctuate based on events outside its control, including geopolitical developments, supply of and demand for oil and gas, actions by the Organization of the Petroleum Exporting Countries, or OPEC, and other oil and gas producers, war and unrest in oil producing countries and regions, regional production patterns and environmental concerns. In February 2022, crude oil prices increased to a new seven year high impacted by the Russia-Ukraine conflict and the sanctions and other measures imposed on Russia by the United Kingdom, European Union, the United States and other countries. Sanctions and trade restrictions have increased uncertainty in global energy markets and fuel may become much more expensive in the future, which could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations.

6

Increases in port fees and stevedoring expenses could increase Caravelle’s operating costs.

Pursuant to relevant terminal port agreements entered into between Caravelle and the relevant stevedoring companies, stevedoring expenses are charged by the relevant stevedoring companies to each shipping company for the use of its labor and the stevedoring facilities. Any increase in such fees and expenses could adversely affect the business, results of operations and financial condition of Caravelle in the event that it is not able to increase freight rates or otherwise recover such fees and expenses increases from its customers.

World events, including terrorist attacks and regional conflict, could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations.

Past terrorist attacks, as well as the threat of future terrorist attacks around the world, continue to cause uncertainty in the world’s financial markets and may affect its business, operating results and financial condition. Continuing conflicts and recent developments in Ukraine, Russia, Azerbaijan, North Korea, Myanmar, the Middle East, including Iran, Iraq, Syria, the Persian Gulf, Yemen, North Africa and the Gulf of Guinea, and the presence of the United States or other armed forces in the Middle East, may lead to additional acts of terrorism and armed conflict around the world, which may contribute to further economic instability in the global financial markets. Recently, government leaders have declared that their countries may turn to trade barriers to protect or revive their domestic industries in the face of foreign imports. War in a country in which a material supplier or customer of Caravelle is located could impact that supply to Caravelle or its ability to earn revenue from that customer. In the past, political conflicts have also resulted in attacks on vessels, mining of waterways and other efforts to disrupt international shipping. Restrictions on imports, including in the form of tariffs, have had and could have a major impact on global trade and demand for shipping. Any of these occurrences could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations.

Acts of piracy on ocean-going vessels may have a material adverse effect on Caravelle’s business, financial condition, cash flows, and results of operations.

Acts of piracy have historically affected ocean-going vessels trading in regions of the world such as the South China Sea, the Indian Ocean, in the Gulf of Aden off the coast of Somalia and, in more recent times, the Gulf of Guinea. Sea piracy incidents continue to occur, particularly in the Gulf of Aden off the coast of Somalia, in the Gulf of Guinea and the west coast of Africa, with carriers vulnerable to such attacks. Acts of piracy may result in death or injury to persons or damage to property. In addition, crew costs, including costs of employing on-board security guards, could increase in such circumstances. Caravelle may not be adequately insured to cover losses from these incidents, which could have a material adverse effect on its business, financial condition, cash flows and results of operations.

Increased inspection procedures and tighter import and export controls could increase costs and disrupt Caravelle’s business.

International shipping is subject to various security and customs inspection and related procedures in countries of origin and destination and trans-shipment points. Inspection procedures may result in the seizure of contents of Caravelle’s vessels, delays in the loading, offloading, trans-shipment or delivery and the levying of customs duties, fines or other penalties against Caravelle. It is possible that changes to inspection procedures could impose additional financial and legal obligations on Caravelle. Changes to inspection procedures could also impose additional costs and obligations on Caravelle and may, in certain cases, render the shipment of certain types of cargo uneconomical or impractical. Any such changes or developments could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations.

7

Caravelle’s freights may call on ports located in countries that are subject to restrictions imposed by the United States, United Kingdom, United Nations or other governments.

Although Caravelle does not expect that its freights will call on ports located in countries subject to sanctions and embargoes imposed by the U.S. government and other authorities or countries identified by the U.S. government or other authorities as state sponsors of terrorism, from time to time on charterers’ instructions, Caravelle’s freights may call on ports located in such countries in the future. The U.S. sanctions and embargo laws and regulations vary in their application, as they do not all apply to the same covered persons or proscribe the same activities, and such sanctions and embargo laws and regulations may be amended or strengthened over time. Although Caravelle believes that it is in compliance with all applicable sanctions and embargo laws and regulations, and intends to maintain such compliance, there can be no assurance that it will be in compliance in the future, particularly as the scope of certain laws may be unclear and may be subject to changing interpretations. Any such violation could result in a severe adverse impact on Caravelle’s ability to access U.S. capital markets.

Risks Related to Caravelle’s International Maritime Shipping Business

Caravelle operates carriers worldwide and, as a result, its business has inherent operational risks, which may reduce its revenue or increase its expenses, and Caravelle may not be adequately covered by insurance.

The international shipping industry is an inherently risky business involving global operations of ocean-going freights. Cargoes carried by Caravelle are at risk of being damaged or lost because of events such as marine disasters, bad weather, mechanical failures, human error, environmental accidents, war, terrorism, piracy and other circumstances or events. In addition, transporting cargoes across a wide variety of international jurisdictions creates a risk of business interruptions due to political circumstances in foreign countries, hostilities, labor strikes and boycotts, the potential for changes in tax rates or policies, and the potential for government expropriation of the cargos carried by Caravelle. Any of these events may result in loss of revenue, increased costs and decreased cash flows to Caravelle.

Changing economic, regulatory and political conditions in some countries, including political and military conflicts, have from time to time resulted in attacks on vessels, mining of waterways, piracy, terrorism, labor strikes and boycotts. These hazards may result in death or injury to persons, loss of revenue or property, payment of ransoms, environmental damage, higher insurance rates, market disruptions, and interference with shipping routes (such as delay or rerouting), which may have a material adverse effect on Caravelle’s business.

Caravelle charters vessels mostly from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer.

Caravelle charters vessels mostly from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer. If Topsheen Shipping Limited terminates its business relationship with Caravelle, Caravelle has the risk that it might not be able to secure adequate vessel replacement in a timely manner or it is required to pay a higher charter rate for comparable vessel replacement, which could have a material adverse effect on Caravelle’s business, financial condition, cash flows and results of operations. Mr. Dong Zhang may have conflicts of interest with Caravelle or its shareholders, and Mr. Dong Zhang may not act in the best interests of Caravelle or may not perform the obligations under these contracts. For example, Topsheen Shipping Limited could breach its contractual arrangements with Caravelle by, among other things, failing to provide vessels at the price or timing previously agreed upon, or entering into agreements with Caravelle’s competitors.

More generally, since Mr. Dong Zhang is a related party to Caravelle, the agreement between Caravelle and the entities he controls might not have been negotiated at arm’s length. It is possible the agreement is more favorable to Mr. Dong Zhang’s controlled entities than is industry standard, due to the possible conflicts of interest described above. On the other hand, it is also possible that the agreement is more favorable to Caravelle than is industry standard, in which case Caravelle may be unable to enter into agreements on similarly favorable terms with other vessel suppliers if Mr. Dong Zhang’s controlled entities terminate or change the agreement terms.

Labor interruptions could disrupt Caravelle’s business.

Caravelle could be subject to industrial action or other labor unrest that could prevent or hinder its operations from being carried out normally. If not resolved in a timely and cost-effective manner, such business interruptions could have a material adverse effect on its business, financial condition, cash flows and results of operations.

8

Failure to comply with the U.S. Foreign Corrupt Practices Act and other anti-bribery legislation in other jurisdictions could result in fines, criminal penalties, contract terminations and an adverse effect on Caravelle’s business.

Caravelle operates in a number of countries throughout the world, including countries known to have a reputation for corruption. Caravelle is committed to doing business in accordance with applicable anti-corruption laws. However, Caravelle is subject to the risk that persons and entities employed or engaged by Caravelle or their agents may take actions that are determined to be in violation of such anti-corruption laws, including the U.S. Foreign Corrupt Practices Act of 1977, or the “FCPA.” Any such violation could result in substantial fines, sanctions, civil and/or criminal penalties, or curtailment of operations in certain jurisdictions, and might adversely affect Caravelle’s business, results of operations or financial condition. In addition, actual or alleged violations could damage Caravelle’s reputation and ability to do business. Furthermore, detecting, investigating, and resolving actual or alleged violations is expensive and can consume significant time and attention of Caravelle’s senior management.

The smuggling of drugs or other contraband onto Caravelle’s freight may lead to governmental claims against Caravelle.

Caravelle’s freights may call in ports where smugglers attempt to hide drugs and other contraband on vessels, with or without the knowledge of crew members. To the extent Caravelle’s freights are found with contraband, whether with or without the knowledge of any of its crew, Caravelle may face reputational damage and governmental or other regulatory claims which could have a material adverse effect on its business, financial condition, cash flows and results of operations.

Caravelle needs to maintain its relationships with local shipping agents, port and terminal operators.

Caravelle’s shipping business is dependent upon its relationships with local shipping agents, port and terminal operators operating in the ports where its customers ship and unload their products. Caravelle believes that these relationships will remain critical to its success in the future and the loss of one or more of which could materially and negatively impact its ability to retain and service its customers. Caravelle cannot be certain that it will be able to maintain and expand its existing local shipping agent, port and terminal operator relationships or enter into new relationships, or that new or renewed relationships will be available on commercially reasonable terms. If Caravelle is unable to maintain and expand its existing local shipping agent, port and terminal operator relationships, renew existing relationships, or enter into new relationships, Caravelle may lose customers or cause delays in the ports in which it operates, which could have a material adverse effect on its business, financial condition, cash flows and results of operations.

Risks Related to Caravelle’s CO-Tech Business

Caravelle’s CO-Tech business has no operating history and its project growth might not be realized.

Caravelle was founded in 2021 and to date, has not started the commercialization of its CO-Tech business. Although Caravelle expects to launch the CO-Tech business in the fourth quarter of 2023, there is no assurance Caravelle will be able to secure reliable sources of wood supply and customers to successfully grow its CO-Tech business as it projected.

Furthermore, even if Caravelle achieves a stable wood desiccation, carbon trading, and sale of wood vinegar business operation as it has projected for its CO-Tech businesses, it faces significant risks and barriers in the relevant industries, including the continuous expansion of the carbon-trading markets around the world, application of wood vinegar, client base, marketing channels, pricing policies, talent management, value-added service packages and sustained technological advancement. If Caravelle fails to address any or all of these risks and barriers to entry and growth, its business and results of operation may be materially and adversely affected.

Given Caravelle’s limited operating history, the likelihood of its success must be evaluated, especially in light of the risks, expenses, complications, delays and the competitive environment in which it operates. There is, therefore, no assurance that Caravelle’s business plan will prove successful. Caravelle will continue to encounter risks and difficulties frequently experienced by early-stage commercial companies, including in scaling its infrastructure and headcount, and may encounter unforeseen expenses, difficulties or delays in connection with its growth. In addition, its new CO-Tech business may not be able to become profitable as quickly as its traditional ocean shipping business has. There is no assurance Caravelle will continue to be able to generate revenue, raise additional capital when required or operate profitably.

9

Caravelle’s yet to be launched CO-Tech business sector has no operating history and no revenues, and there is no past performance on which to evaluate Caravelle’s ability to achieve its business objectives.

Caravelle has yet to launch its carbon neutral shipping business and has been in the testing stage up to the date of this Report. Currently, Caravelle anticipates to formally commence its carbon neutral shipping business in the fourth quarter of 2023. Because of the lack of operating history, you have no past performance with which to evaluate Caravelle’s ability to achieve its business objective for the CO-Tech business sector.

Caravelle’s forecast regarding its CO-Tech business relies in large part upon assumptions and analyses developed by its management. If these assumptions and analyses prove to be incorrect, its actual operating results could suffer.

Caravelle’s forecast regarding its CO-Tech business relies in large part upon assumptions and analyses developed by its management and reflects current estimates of future performance. Whether actual operating and financial results and business developments will be consistent with Caravelle’s expectations and assumptions as reflected in the forecast depends on a number of factors, many of which are outside Caravelle’s control, including, but not limited to:

| ● | whether it can obtain sufficient capital to sustain and grow its business; | |

| ● | its ability to manage growth; | |

| ● | whether it can manage relationships with key suppliers; | |

| ● | demand for its products and services; | |

| ● | the timing and cost of new and existing marketing and promotional efforts; | |

| ● | competition, including established and future competitors; | |

| ● | its ability to retain existing key management, to integrate recent hires and to attract, retain and motivate qualified personnel; | |

| ● | the overall strength and stability of domestic and international economies; and | |

| ● | regulatory, legislative and political changes. |

Specifically, Caravelle’s forecast regarding its CO-Tech business is based on projected purchase prices, demand in market, costs for wood to be dried, logistics, sales, marketing and service, and its projected number of orders for the desiccated wood. Any of these factors could turn out to be different from those anticipated. Unfavorable changes in any of these or other factors, most of which are beyond Caravelle’s control, could materially and adversely affect its business, prospects, financial results and results of operations.

Caravelle expects its operating expenses to increase significantly in the future, which may impede its ability to achieve profitability.

Caravelle expects to further incur significant operating costs which will impact its profitability, including research and development expenses as it improves its operations in wood desiccation on vessels or applies its CO-Tech model in other industries, capital expenditures in adding wood desiccation components to vessels, general and administrative expenses as it scales its operations, and sales, marketing, and distribution expenses as it builds its brand and markets its new business model and expands its CO-Tech business.

Caravelle’s ability to become profitable in the future will not only depend on its ability to successfully market its products and services, but also to control costs. Ultimately, Caravelle may not be able to adequately control costs associated with its operations for reasons outside its control, including the cost of raw materials and fuel costs. Substantial increases in such costs could increase Caravelle’s cost of revenue and its operating expenses, and could reduce its margins. Additionally, unforeseen events such as the current ongoing global pandemic could adversely affect supply chains, impacting Caravelle’s ability to control and manage costs. Additionally, currency fluctuations, tariffs or shortages in petroleum and other economic or political conditions could result in significant increases in freight charges and raw material costs. If Caravelle fails to continue to design, develop, manufacture, market, sell and service its CO-Tech business sector, including providing service in a cost-efficient manner, its margins, profitability, and prospects would be materially and adversely affected.

10

The rate at which Caravelle may incur costs and losses in future periods compared to current levels may increase significantly, as it:

| ● | continues to develop the CO-Tech system and remote-control platform; |

| ● | develops and equips the vessels it employs with the CO-Tech system, and to secure manufacturing capabilities; |

| ● | builds up inventories of parts and components for the CO-Tech system; |

| ● | develops and expands its design, development, maintenance, servicing and repair capabilities; and |

| ● | increases its sales and marketing activities. |

These efforts may be more expensive than Caravelle currently anticipates, and these efforts may not result in increases in revenues. Any cost overruns that deviate from Caravelle’s estimates may materially and adversely affect its business prospects, financial condition and results of operations.

Caravelle is dependent upon its proprietary intellectual properties.

Caravelle considers its patents, copyrights, trademarks, trade names, internet domain names and other intellectual property assets crucial to its ability to develop and protect new technology, grow its business and enhance Caravelle’s brand recognition. Caravelle has invested significant resources to develop its intellectual property assets. Failure to successfully maintain or protect these assets could harm Caravelle’s business. The steps Caravelle has taken to protect its intellectual property rights may not be adequate or prevent theft and use of its trade secrets by others or prevent competitors from copying its newly developed technology. If Caravelle is unable to protect its proprietary rights or if third parties independently develop or gain access to similar technology, Caravelle’s business, revenue, reputation and competitive position could be harmed. For example, the measures Caravelle takes to protect its intellectual property from unauthorized use by others may not be effective for various reasons, including the following:

| ● | any patent applications Caravelle submits may not result in the issuance of patents; |

| ● | the scope of Caravelle’s issued patents may not be broad enough to protect its proprietary rights; |

| ● | Caravelle’s issued patents may be challenged and/or invalidated by its competitors or others; |

| ● | the costs associated with enforcing patents, confidentiality and invention agreements and/or other intellectual property rights may make aggressive enforcement impracticable; |

| ● | current and future competitors may circumvent Caravelle’s patents; |

| ● | Caravelle’s in-licensed patents may be invalidated, or the owners of these patents may breach their license arrangements; and |

| ● | even if Caravelle obtains a favorable outcome in litigation asserting its rights, Caravelle may not be able to obtain an adequate remedy, especially in the context of unauthorized persons copying or reverse engineering Caravelle’s products or technology. |

Caravelle may need to resort to litigation to enforce its intellectual property rights if its intellectual property rights are infringed or misappropriated, which could be costly and time-consuming. Additionally, the protection of Caravelle’s intellectual property rights in different jurisdictions may vary in their effectiveness. Caravelle has little patent coverage anywhere in the world except China. Implementation and enforcement of Chinese intellectual property-related laws historically has been considered to be deficient and ineffective. Moreover, with Caravelle’s licensed-in patents limited mostly to those issued in China, Caravelle may find it impossible to prevent competitors from copying its patented advancements in vehicles manufactured and sold elsewhere.

Despite Caravelle’s efforts to protect its proprietary rights, third parties may still attempt to copy or otherwise obtain and use its intellectual property or seek court declarations that such third parties’ intellectual property does not infringe upon Caravelle’s intellectual property rights, or they may be able to independently develop technologies that are the same as or similar to Caravelle’s technologies.

11

We may be subject to intellectual property infringement claims or other allegations, which may be time-consuming and result in substantial costs and removal of data or technology from our system.

Companies, organizations or individuals, including our competitors, may hold or obtain patents, trademarks or other proprietary rights that would prevent, limit or interfere with our ability to make, use, develop, sell or market our products, which could make it more difficult for us to operate our business. We may not be aware of all the intellectual property infringement assertions from third parties surrounding our current or future products, which could materially impair our ability to commercialize our products. Any analysis performed may not identify all the third-party intellectual property that is potentially relevant, including intellectual property that is not publicly available for review, and would not prevent third parties from bringing intellectual property infringement claims.

From time to time, we may need to defend ourselves against intellectual property infringement or trade secret misappropriation claims, and companies holding patents, copyrights, trademarks or other intellectual property rights may bring suits alleging infringement of such rights by us or our employees or otherwise assert their rights and urge us to purchase licenses. Any such intellectual property infringement claim could result in costly litigation and divert management’s attention and resources.

If we or our employees are determined to have infringed upon a third party’s intellectual property rights, we may be required to do one or more of the following:

| ● | cease offering products and solutions that incorporate or use the challenged intellectual property; |

| ● | pay substantial damages; |

| ● | seek a license from the holder of the infringed intellectual property right, which license may not be available on reasonable terms or at all; |

| ● | redesign our products and solutions or relevant services, which would result in significant cost; or |

| ● | establish and maintain alternative branding for our products and solutions or services. |

In the event of a successful claim of infringement against us and our failure or inability to obtain a license to the infringed technology or other intellectual property right, our business, prospects, financial condition and results of operation could be materially and adversely affected. In addition, any litigation or claims, whether valid or not, could result in substantial costs, negative publicity and diversion of resources and management attention.

Caravelle purchases its CO-Tech equipment from New Galion Group (HK) Co Ltd (“New Galion”) and purchases a vessel from Beijing Hanpu Technology Co., Ltd., both of which are controlled by Dr. Guohua Zhang, Caravelle’s Chief Executive Officer, and will rent vessels for the CO-Tech business from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer.

Caravelle purchases its CO-Tech equipment from New Galion and purchases a vessel from Beijing Hanpu Technology Co., Ltd, both of which are controlled by Dr. Guohua Zhang, Caravelle’s Chief Executive Officer. In addition, Caravelle will rent vessels for the CO-Tech business from Topsheen Shipping Limited, a company controlled by Mr. Dong Zhang, Caravelle’s Chief Shipping Officer. If New Galion or Topsheen Group Limited terminates its business relationship with or fails to deliver on time the equipment or vessels for Caravelle, Caravelle might not be able to secure adequate replacement equipment or vessels in a timely manner or may be required to pay a higher price for such replacement, which could have a material adverse effect on Caravelle’s business, financial condition, cash flows and the results of the CO-Tech business operations. Mr. Dong Zhang may have conflicts of interest with Caravelle or its shareholders, and Mr. Dong Zhang and New Galion may not act in the best interests of Caravelle or may not perform their obligations under these contracts. For example, New Galion could breach it contractual arrangements with Caravelle by, among other things, failing to provide the equipment at the price or timing previously agreed upon, or failing the technical standards as agreed upon. It is unclear whether Caravelle could find an alternative provider for the CO-Tech equipment. Caravelle also purchased a vessel for testing and trial operation of the CO-Tech business from Beijing Hanpu Technology Co., Ltd. (“Hanpu”), a company controlled by Dr. Guohua Zhang, Caravelle’s Chief Executive Officer. Caravelle believes such transactions were entered into at a fair market price.

More generally, since Mr. Dong Zhang is a related party to Caravelle, the agreement between Caravelle and the entities he controls might not have been negotiated at arm’s length. It is possible the agreement is more favorable to Mr. Dong Zhang’s controlled entities than is industry standard, due to the possible conflicts of interest described above. On the other hand, it is also possible that the agreement is more favorable to Caravelle than is industry standard, in which case Caravelle may be unable to enter into agreements on similarly favorable terms with other vessel suppliers if Mr. Dong Zhang’s controlled entities terminate or change the agreement terms.

12

Caravelle’s CO-Tech model is in the early stages and it may not become profitable within twelve months after the closing of the Business Combination, if at all.

Caravelle’s CO-Tech business has not yet commenced operation and has not recognized any revenue as of the date of this Report. Caravelle’s future business depends in large part on its ability to execute its plans to develop, manufacture, market, sell and deliver desiccated wood using its CO-Tech model.

Although Caravelle originally planned to commence operation of its first vessel using the CO-Tech model in early 2022, it experienced delays caused by China’s COVID-related lockdown measures, and it may experience further significant delays due to reasons such as lack of funding, supply shortages, design defects, talent gaps, and/or force majeure. For example, Caravelle relies on third-party suppliers for the provision of wet wood to be processed. To the extent Caravelle’s suppliers experience any delays in providing or developing necessary raw materials, or if they experience quality issues, Caravelle could experience delays in delivering on its timelines.

Supply and distribution chain disruptions could adversely affect Caravelle’s business.

Caravelle’s ability to generate revenue from either selling dried wood or providing wood desiccation services in its new CO-Tech business may be materially adversely impacted by supply chain disruptions. Such disruptions include the shutdown of forest farms, shortage of labor, and increased price of timber. Although the CO-Tech business has a short supply chain consisting of upstream timber seller and forest farms, and the supply chain has recovered to pre-pandemic levels, there is no guarantee that Caravelle will not be subject to impact caused by future shutdowns or other disruptions. To secure wood supply and reduce impact of price volatilities, Dr. Guohua Zhang has established cordial long-term relationships with timber suppliers in Africa and Southeast Asia. For example, Singapore Garden has entered into an agreement with Honest Timber Gabon Co. Ltd. securing its wood supply, under which Honest Timber Gabon Co. Ltd. agrees to sell an aggregate of 400,000 cubic meters of wood between 2022 and 2026.

Caravelle depends on third parties for logging and transportation services and increases in the costs or decreases in the availability of quality service providers could adversely affect its business.

The upstream and downstream business chain of its CO-Tech sector depends on logging and transportation services provided by third parties, both domestically and internationally, including by railroad, trucks, or ships. If any of its transportation providers were to fail to deliver timber supply or logs to Caravelle or its clients, or fails to deliver in a timely manner, or were to damage timber supply or logs during transport, Caravelle may be unable to reach the expected profit level. During the global financial crisis and subsequent downturn in U.S. housing starts, timber harvest volumes declined significantly. As a result, many logging contractors, particularly cable logging operators in the western U.S., permanently shut down their operations. As harvest levels have returned to higher levels with the recovery in housing starts, this shortage of logging contractors has resulted in sharp increases in logging costs and more limited availability of logging contractors. It is expected that the supply of qualified logging contractors will be affected by the availability of debt financing for equipment purchases as well as the availability of adequately trained loggers. As housing continues to recover, harvest levels are expected to increase, placing more pressure on the existing supply of logging contractors. Any significant failure or unavailability of third-party logging or transportation providers, or increases in transportation rates or fuel costs, may result in higher logging costs, the inability to capitalize on stronger log prices to the extent logging contractors cannot be secured at a competitive cost, or decreased demand for Caravelle’s desiccation service. Such events could harm its reputation, negatively affect its customer relationships and adversely affect its business.

In the new CO-Tech wood desiccation business, the revenue and profit may be subject to high volatility because the need for wood desiccation service is determined by the market’s supply of timber and demand for wood products, and such markets operates are cyclical and competitive.

The performance of Caravelle’s CO-Tech sector depends on the state of the housing, construction, and home improvement markets. The pricing of its products is dependent on customers’ perceptions of the market and therefore can be volatile.

At times, the price for any one or more of the products Caravelle produces or to which Caravelle’s desiccation services contribute may fall below its cash production costs, requiring Caravelle to either incur short-term losses on product sales, decreased income generated by services, or suspend operations. Therefore, its profitability with respect to these wood products depends, in significant part, on the market’s supply of timber and demand for wood products, and managing its cost structure, particularly raw materials and ship chartering costs, which represent the largest components of its operating costs. Caravelle has limited control of the foregoing, and as a result, its profitability and cash flow may fluctuate materially in response to changes in the supply and demand of the wood product industry.

13

Caravelle’s growth depends on the continued growth of the need for wood desiccation, wood vinegar, and further development of the carbon trading market.

Currently, a substantial portion of Caravelle’s projected income in the CO-Tech business comes from the provision of wood desiccation service and sale of desiccated wood, the sale of wood vinegar, and the trade of Carbon Emission Abatement (“CEA”) on the coming carbon trading markets. However, there is no guarantee that the need for desiccated wood will remain or grow beyond the current level, nor is there a guarantee that the productivity of desiccated wood will remain bottlenecked under the traditional model. The projected income from the sale of wood vinegar is premised upon the wider application of wood vinegar in agriculture, healthcare, and other industries. Caravelle also expects to derive a substantial amount of future revenue from the CEA generated from the CO-Tech business model. If any of the previous assumptions fail to realize, Caravelle’s profitability may be substantially undermined.

Caravelle may not be able to obtain the necessary certification from the classification societies.

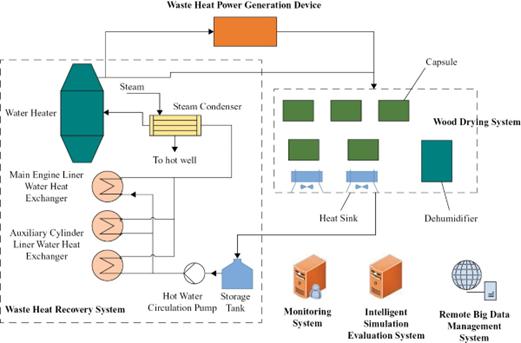

Caravelle has obtained an Approval in Principle from one of the leading classification societies, Det Norske Veritas (DNV), on the design of a waste heat recovery and utilization system. However, Caravelle must obtain Product Approval from DNV for its on-board wood desiccation system as well as Ship Inspection Approval for each of the vessels on-board wood desiccation system is installed before such a vessel may start its maritime voyage. Currently, Caravelle expects to receive these approvals for its first vessel with the on-board wood desiccation system in the fourth quarter of 2023. However, there is no guarantee that Caravelle will receive such approvals, or obtain these approvals in a timely manner for it to launch its CO-Tech business when anticipated.

Caravelle depends on the core technologies licensed by Dr. Guohua Zhang, in the CO-Tech business. Thus, if Dr. Zhang revokes such license, Caravelle’s business will be substantially affected.

The CO-Tech business model under which Caravelle currently operates is reliant upon the 14 patents held or under prosecution by Dr. Guohua Zhang, as well as other know-how and trade secrets originally invented by Dr. Guohua Zhang. If Dr. Zhang discontinues such license of patents or provision of trade secrets to Caravelle, Caravelle’s CO-Tech business sector will be substantially affected.

Caravelle currently lacks employees with adequate training and experience to carry out the CO-Tech business on-board.

To operate the CO-Tech wood desiccation during maritime shipping, Caravelle needs crews and employees on-board. As the CO-Tech wood desiccation is a new business that involves novel technologies, Caravelle must provide adequate training to its crews and employees to operate. While Caravelle believes it will have sufficient number of crews and employees with the required skills and experience when it launches its CO-Tech wood desiccation business, there is a risk that Caravelle may not able to recruit new crews and employees, or to provide adequate training for newly recruited crews and employees, to carry out the on-board operations when Caravelle expands its CO-Tech business, which takes financing, time, and other resources to achieve. If Caravelle fails to obtain and train an adequate number of such qualified employees, the CO-Tech business may not be as successful as Caravelle anticipates.

Risk related to Caravelle’s Overall Business

It is not certain if Caravelle will be classified as a Singapore tax resident.