Table of Contents

As filed with the Securities and Exchange Commission on July 19, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Lanvin Group Holdings Limited

(Exact Name of Registrant as Specified in Its Charter)

| Cayman Islands | Not Applicable | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification Number) |

4F, 168 Jiujiang Road,

Carlowitz & Co, Huangpu District

Shanghai, 200001, China

Tel: +86-21-6315-3873

(Address and Telephone Number of Registrant’s Principal Executive Offices)

Puglisi & Associates

850 Library Avenue, Suite 204

Newark, Delaware 19711

Tel: +1 (302) 738-6680

(Name, Address and Telephone Number of Agent For Service)

Copies to:

Howie Farn, Esq.

Freshfields Bruckhaus Deringer

55th Floor, One Island East,

Taikoo Place

Quarry Bay

Hong Kong

Tel: +852 2913 2797

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box. ☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a registration statement pursuant to General Instruction I.C. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.C. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated July 19, 2024

PRELIMINARY PROSPECTUS

Lanvin Group Holdings Limited

42,712,386 Ordinary Shares

We may from time to time in one or more offerings offer and sell up to an aggregate of 42,712,386 of our ordinary shares, par value $0.000001 per share (“Ordinary Shares”).

We will provide specific terms of any offering in a supplement to this prospectus. Any prospectus supplement may also add, update, or change information contained in this prospectus. You should carefully read this prospectus and the applicable prospectus supplement as well as the documents incorporated or deemed to be incorporated by reference in this prospectus before you purchase any of the securities offered hereby.

These securities may be offered and sold in the same offering or in separate offerings; to or through underwriters, dealers, and agents; or directly to purchasers. The names of any underwriters, dealers, or agents involved in the sale of our securities, their compensation and any options to purchase additional securities granted to them will be described in the applicable prospectus supplement. For a more complete description of the plan of distribution of these securities, see the section entitled “Plan of Distribution” beginning on page 31 of this prospectus.

Our Ordinary Shares are listed on the New York Stock Exchange, or NYSE, under the trading symbols “LANV”. On July 18, 2024, the closing price for our Ordinary Shares on the NYSE was $1.57 per share.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 and have elected to comply with certain reduced public company reporting requirements. In addition, we are a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company disclosure and reporting requirements. See “Our Company—Implications of Being a Foreign Private Issuer and a Controlled Company.”

We are a Cayman Islands holding company, and our operations are conducted by our subsidiaries organized in various jurisdictions including China. The securities offered herein are our securities, not securities of such operating subsidiaries. We may face various legal and operational risks and uncertainties associated with having a portion (approximately 12.5% of our revenues in 2023) of our operations conducted in China through our Chinese subsidiaries. For example, we may be subject to complex and evolving laws and regulations in China. The PRC government has indicated an intent to exert more oversight and control over offerings that are conducted overseas by and/or foreign investment in China-based issuers, including regulatory uncertainties related to the use of variable interest entities, tightened supervision over China-based issuers listed overseas, oversight on cybersecurity and data security, and expanded efforts in anti-monopoly enforcement. Although we do not use any variable interest entities, we may face risks associated with regulatory approvals on offerings conducted overseas by, and foreign investment in, China-based issuers and oversight on cybersecurity and data privacy, which may impact our ability to conduct certain businesses in China, accept foreign investments, or list on a U.S. or other foreign exchange outside of China. These risks could result in a material adverse change in our operations and the value of our securities, significantly limit or completely hinder our ability to offer, or continue to offer, securities to investors or cause the value of such securities to significantly decline.

We may be subject to the risk of trading prohibitions under the Holding Foreign Companies Accountable Act, or the HFCA Act. Our independent auditor, Grant Thornton Zhitong Certified Public Accountants LLP, is an independent registered accounting firm based in the mainland of China. Pursuant to the HFCA Act and related regulations, if we have filed an audit report issued by a registered public accounting firm that the Public Company Accounting Oversight Board (the “PCAOB”) has determined is unable to inspect and investigate

Table of Contents

completely for two consecutive years, the Securities and Exchange Commission, or the SEC, will prohibit our securities from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. However, there can be no assurance that the PCAOB will continue to have such access. Should PRC authorities fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination, which may affect our ability to maintain the listing of our securities on the U.S. national securities exchanges, including the NYSE, and the trading of them in the over-the-counter trading market. A delisting would substantially impair your ability to sell or purchase our securities when you wish to do so, and the risk and uncertainty associated with a potential delisting would have a negative impact on the price of our securities. For details, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Our Securities—Our ability to maintain the listing of our securities on the NYSE may be dependent on the PCAOB’s continued access to inspect our independent auditors” in our annual report on Form 20-F for the year ended December 31, 2023 (the “2023 Form 20-F”), which is incorporated herein by reference.

Investing in our securities involves a high degree of risk. Before buying any securities, you should carefully read the discussion of material risks of investing in our securities in “Risk Factors” beginning on page 9 of this prospectus and the other information included in or incorporated by reference in the prospectus and the applicable prospectus supplements.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2024

Table of Contents

| II | ||||

| III | ||||

| IV | ||||

| VI | ||||

| 1 | ||||

| 9 | ||||

| 10 | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| 24 | ||||

| 31 | ||||

| 34 | ||||

| ENFORCEMENT OF CIVIL LIABILITIES AND AGENT FOR SERVICE OF PROCESS IN THE UNITED STATES |

35 | |||

| 36 | ||||

| 37 | ||||

| 38 |

You should rely only on the information contained in this prospectus, as well as the information incorporated by reference into this prospectus and any applicable prospectus supplement or amendment or any free writing prospectus prepared by or on our behalf. We have not authorized any other person to provide you with different or additional information. We do not take responsibility for, nor can we provide assurance as to the reliability of, any other information that others may provide. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. The information contained in this prospectus, as well as the information incorporated by reference into this prospectus and any applicable prospectus supplement or amendment, is accurate only as of the date of the applicable document or such other date stated in the applicable document, and our business, financial condition, results of operations and/or prospects may have changed since those dates.

Except as otherwise set forth in this prospectus, we have not taken any action to permit a public offering of these securities outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of these securities and the distribution of this prospectus outside the United States.

-I-

Table of Contents

This prospectus is part of a registration statement on Form F-3 that we filed with the SEC using a “shelf” registration process. Under this shelf registration process, we may, from time to time, offer and sell any combination of the securities described in this prospectus in one or more offerings.

Information on our website is not included or incorporated by reference in this prospectus.

We will bear our costs, fees and expenses incurred in effecting the registration of the securities covered by this prospectus, including, without limitation, all registration and filing fees, NYSE listing fees and fees and expenses of our counsel and our independent registered public accountants.

To the extent required, we will deliver a prospectus supplement with this prospectus to update the information contained in this prospectus. The prospectus supplement may also add, update or change information included in this prospectus. You should read both this prospectus and any applicable prospectus supplement, together with additional information described below under the caption “Where You Can Find More Information” and “Incorporation of Certain Documents by Reference.” We have not, authorized anyone to provide you with information different from that contained in this prospectus.

No offer of these securities will be made in any jurisdiction where the offer is not permitted.

Throughout this prospectus, unless otherwise designated, the terms “we,” “us,” “our,” “Lanvin Group,” “the Company” and “our Company” refer to Fosun Fashion Group (Cayman) Limited, or FFG, and its consolidated subsidiaries, prior to the consummation of the Business Combination and to Lanvin Group Holdings Limited (“LGHL”) and its consolidated subsidiaries following the Business Combination, as the context requires. The term “PCAC” refers to Primavera Capital Acquisition Corporation prior to the consummation of the Business Combination.

-II-

Table of Contents

INCORPORATION OF CERTAIN DOCUMENTS BY REFERENCE

The SEC allows us to incorporate by reference in this prospectus the information we file with it, which means that we can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be part of this prospectus, and information filed subsequently with the SEC will automatically update and supersede earlier information.

We have filed with the SEC a registration statement on Form F-3 relating to the securities covered by this prospectus. This prospectus is a part of the registration statement and omits some of the information contained in the registration statement in accordance with SEC rules and regulations. You should review the information in, and exhibits to, the registration statement for further information on us and the securities being offered. Statements in this prospectus concerning any document we have filed or will file as an exhibit to the registration statement or that we have otherwise filed with the SEC are not intended to be comprehensive and are qualified in their entirety by reference to these filings. You should review the complete document to evaluate these statements. You may review a copy of the registration statement at the SEC’s internet site, as described under “Where You Can Find More Information” in this prospectus.

We incorporate by reference in this prospectus the following information:

| • | our annual report on Form 20-F for the fiscal year ended December 31, 2023, originally filed with the SEC on April 30, 2024; |

| • | exhibits 99.1 and 99.2 to our current report on Form 6-K, furnished to the SEC on April 30, 2024; |

| • | the description of Ordinary Shares contained in our registration statement on Form 8-A filed on December 14, 2022 pursuant to Section 12 of the Securities, together with all amendments and reports filed for the purpose of updating that description; |

| • | any future annual reports on Form 20-F that we file with the SEC after the date of this prospectus and prior to the termination of the offering of the securities offered by this prospectus; and |

| • | any future reports on Form 6-K (or portions thereof) that we furnish to the SEC after the date of this prospectus only to the extent that such reports expressly state that they are (or such portions are) incorporated by reference in this prospectus. |

You should not assume that the information in this prospectus, any prospectus supplement or any document incorporated by reference is accurate or complete at any date other than the date mentioned on those documents.

Copies of all documents incorporated by reference in this prospectus, other than exhibits to those documents unless such exhibits are specially incorporated by reference in this prospectus, will be provided at no cost to each person, including any beneficial owner, who receives a copy of this prospectus on the written or oral request of that person made to Lanvin Group Holdings Limited, 4F, 168 Jiujiang Road, Carlowitz & Co, Huangpu District, Shanghai, 200001, China, Tel. +86-21-6315-3873.

We file reports, including annual reports on Form 20-F, and other information with the SEC pursuant to the rules and regulations of the SEC that apply to foreign private issuers. You can read our SEC filings, including the registration statement of which this prospectus forms a part, over the internet at the SEC’s website at www.sec.gov and at our website at https://ir.lanvin-group.com/.

-III-

Table of Contents

Unless otherwise stated or unless the context otherwise requires in this prospectus:

“Amended Articles” means the amended and restated memorandum and articles of association of the Company.

“Amended and Restated Meritz Relationship Agreement” means the relationship agreement, as amended and restated on December 1, 2023, entered into between LGHL and Meritz and setting forth certain rights and obligations of LGHL and Meritz as the holder of Ordinary Shares (as amended by a side letter between the parties dated April 30, 2024), which modified the previous relationship agreement dated October 19, 2022.

“Aspex” means Aspex Master Fund, an investor in PCAC’s forward purchase units.

“Business Combination” or “Transactions” means the Mergers and the other transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of March 23, 2022 and as amended October 17, 2022, October 20, 2022, October 28, 2022 and December 2, 2022, by and among PCAC, FFG, LGHL, Lanvin Group Heritage I Limited (“Merger Sub 1”) and Lanvin Group Heritage II Limited (“Merger Sub 2”).

“Cayman Companies Act” means the Companies Act (As Revised) of the Cayman Islands as the same may be amended from time to time.

“China” and the “PRC” means the People’s Republic of China, including the mainland of China, the Hong Kong Special Administrative Region, the Macao Special Administrative Region and Taiwan. Only in the context of describing PRC laws, the PRC laws do not include any law, regulation, statute, rule, order, decree, notice, and supreme court’s judicial interpretation or other legislation of the Hong Kong Special Administrative Region, the Macao Special Administrative Region or Taiwan.

“Convertible Preference Share” means the convertible preference share, par value $0.000001 per share, of the Company, which is convertible into an aggregate number of up to 15,000,000 Non-Voting Ordinary Shares and/or Ordinary Shares (subject to adjustment as a result of any share subdivision or consolidation of the shares of LGHL) at the election of Meritz upon the occurrence of certain events, and was repurchased by the Company from Meritz on December 14, 2023.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Fosun Group” means Fosun International and its affiliates.

“Fosun International” or “Fosun” means Fosun International Limited, a company incorporated in Hong Kong with limited liability.

“founder shares” or “PCAC Class B ordinary shares” means Class B ordinary shares of PCAC, par value US$0.0001 per share initially purchased by the Sponsor, which is Primavera Capital Acquisition LLC, the sponsor of PCAC, in a private placement prior to PCAC’s initial public offering.

“Investor Rights Agreement” means the investor rights agreement in substantially the form attached as an exhibit to the Business Combination Agreement.

“IRS” means the Internal Revenue Service of the United States.

-IV-

Table of Contents

“Mergers” means each of: (i) the merger of PCAC with and into Merger Sub 1, with Merger Sub 1 surviving such merger (the “Initial Merger”); (ii) the merger of Merger Sub 2 with and into FFG, with FFG surviving such merger (FFG is referred to for the periods from and after the second merger effective time as the “Surviving Company”) (the “Second Merger”); and (iii) the subsequent merger of Merger Sub 1 as the surviving company of the Initial Merger with and into the Surviving Company as the surviving company of the Second Merger, with the Surviving Company surviving such merger. Pursuant to the Mergers, prior unitholders, shareholders and warrant holders of PCAC and FFG received securities of LGHL, and the surviving company became a wholly owned subsidiary of LGHL.

“Meritz” means Meritz Securities Co., Ltd, a Korean incorporated investment fund.

“Non-Voting Ordinary Shares” means the non-voting ordinary shares, par value $0.000001 per share, of the Company, that have no voting right but otherwise rank pari passu with Ordinary Shares.

“Ordinary Shares” means ordinary shares, par value $0.000001 per share, of the Company.

“PIPE Investors” means certain investors who subscribed for Ordinary Shares on a private placement basis concurrently with the execution of the Business Combination Agreement.

“Securities Act” means the Securities Act of 1933, as amended.

“Warrants” means (i) Public Warrants, which means the 20,699,969 warrants issued by LGHL as part of the Business Combination and listed on NYSE, each of which is exercisable for one Ordinary Share at an exercise price of $11.50 per share, in accordance with its terms, and (ii) Private Placement Warrants, which means the 11,280,000 warrants originally issued by LGHL on a private placement basis, each exercisable for one Ordinary Share at an exercise price of $11.50 per share, which are substantially identical to Public Warrants, subject to certain limited exceptions.

“€,” “EUR” and “Euro” each means the currency introduced at the start of the third stage of European Economic and Monetary Union pursuant to the Treaty on the Functioning of the European Union, as amended.

“$”, “USD” and “U.S. dollar” each means the currency in dollars of the United States of America. “U.S.” means the United States of America.

-V-

Table of Contents

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This prospectus includes trademarks, tradenames and service marks, certain of which belong to us and others that are the property of other organizations. Solely for convenience, some of the trademarks, service marks, logos and trade names referred to in this prospectus are presented without the “®” and “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks and trade names. This prospectus contains additional trademarks, service marks and trade names of others. All trademarks, service marks and trade names appearing in prospectus are, to our knowledge, the property of their respective owners. We do not intend our use or display of other companies’ trademarks, service marks, copyrights or trade names to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

-VI-

Table of Contents

Overview

We are a global luxury fashion group with five portfolio brands, namely Lanvin, Wolford, Sergio Rossi, St. John and Caruso.

| • | Founded in 1889, Lanvin is one of the oldest French couture houses still in operation, offering products ranging from apparel to leather goods, footwear, and accessories. |

| • | Wolford, founded in 1950, is one of the largest luxury skinwear brands in the world, offering luxury legwear and bodywear, with a recent successful diversification into leisurewear and athleisure. |

| • | Sergio Rossi is a highly recognized Italian shoemaker brand and has been a household name for luxury shoes since 1951. |

| • | St. John is a classic, timeless and sophisticated American luxury womenswear house founded in 1962. |

| • | Caruso has been a premier menswear manufacturer in Europe since 1958. |

In addition to our current five portfolio brands, we are also actively looking at potential add-on acquisitions as part of our growth strategy. Our goal is to build a leading global luxury group with unparalleled access to Asia, and to provide customers with excellent products that reflect our brands’ tradition of fine craftsmanship with exclusive design content and a style that preserves the exceptional manufacturing quality for which those brands are known. This is consistently achieved through the sourcing of superior raw materials, the careful finish of each piece, and the way the apparel products are manufactured and delivered to our customers.

Our products are sold through an extensive network of around 1,100 points of sale (“POSs”) including approximately 280 directly operated retail stores (across our five portfolio brands) as of December 31, 2023. We distribute our products worldwide via our retail and outlet stores, our wholesale customers and e-commerce platforms. Taking into account our DTC (including both directly-operated stores and e-commerce sites) and wholesale channels, we are present in more than 80 countries.

Summary of Risk Factors

Investing in our securities entails a high degree of risk. You should carefully consider such risks before deciding to invest in our securities. Below please find a summary of the principal risks we face, organized under relevant headings. These risks are discussed more fully in “Item 3. Key Information—D. Risk Factors” in our 2023 Form 20-F, which is incorporated herein by reference.

Risks Relating to Our Business and Industry

| • | We have incurred significant losses in the past and anticipate that we will continue to incur losses for the current year and upcoming future years. |

| • | The re-branding to Lanvin Group is being challenged by the minority shareholders of Arpège SAS. Arpège SAS, one of our subsidiaries, holds our Lanvin brand portfolio including the “Lanvin” brand name. We cannot predict the outcome of such challenge and may have to discontinue the use by us, at the group holding company level, of the Lanvin brand name. |

| • | The success of our luxury fashion businesses depends on the value of our brands and, if the value of any of those brands were to diminish, our business could be adversely affected. |

| • | We face risks related to health epidemics, pandemics and similar outbreaks, such as the COVID-19 pandemic, which has had and may continue to have a material adverse impact on our business, financial condition and results of operations. |

-1-

Table of Contents

| • | The long-term growth of our business depends on the successful execution of our strategic initiatives and we may not be able to continue to develop and grow our businesses. |

| • | Our growth depends, in part, on our continued retail expansion, and we may not be successful in undertaking such expansion. |

| • | Our business is heavily dependent on the ability and desire of consumers to shop. |

| • | Our inability to effectively execute our e-commerce strategy could materially adversely affect the reputation of our brands and our revenue and our operating results may be harmed. |

| • | We utilize a range of marketing, advertising, and other initiatives to increase existing customers’ spending and to acquire new customers; if the costs of advertising or marketing increase, or if our initiatives fail to achieve their desired impact, we may be unable to grow the business profitably. |

| • | Failure to accurately forecast consumer demand could lead to excess inventories or inventory shortages, which could result in decreased operating margins, reduced cash flows, and harm to our business. |

| • | We are dependent on suppliers for our products and raw materials, which poses risks to our business operations. |

| • | We face intense competition in the personal luxury goods industry. |

| • | A data security or privacy breach could damage our reputation and our relationships with our customers or employees, expose us to litigation risk, and adversely affect our business. |

| • | We are exposed to the risk that personal information of our customers, employees and other parties collected in the course of our operations may be damaged, lost, stolen, divulged or processed for unauthorized purposes. |

| • | Significant inflation could adversely affect our results of operations and financial condition. |

| • | If one or more of our distribution facilities or those of our distribution partners experience operational difficulties or becomes inoperable, it could have a material adverse effect on our business, results of operations and financial condition. |

| • | Our revenues and operating results are affected by the seasonal nature of our business and cyclical trends in consumer spending. |

| • | Our potential inability to find suitable new targets to drive inorganic business growth and the risk that any acquisitions we do complete may not be successful in achieving intended benefits, cost savings and synergies. |

| • | If our trademarks and intellectual property or other proprietary rights are not adequately protected to prevent use or appropriation by third parties, the value of our brand and other intangible assets may be diminished, and our business may be adversely affected. |

| • | We are subject to legal and regulatory risk. |

| • | Changes to taxation or the interpretation or application of tax laws could have an adverse impact on our results of operations and financial condition. |

| • | We are exposed to fluctuations in currency exchange rates. |

| • | We operate in many countries around the world and, accordingly, we are exposed to various international business, regulatory, social and political risks. |

| • | There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations, and changes in laws, rules and regulations in China could adversely affect us. |

| • | If we were to become subject to the oversight, discretion or control of PRC government authorities over overseas offerings of securities and/or foreign investments, it may result in a material adverse |

-2-

Table of Contents

| change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline, which would materially affect the interests of the investors. |

| • | Changes in tax laws, regulations and policies in jurisdictions in which we operate may materially and adversely affect our results of operations and financial condition. |

| • | Because of the costs and difficulties inherent in managing cross-border business operations, our results of operations may be negatively impacted. |

| • | The conflict in Ukraine and sanctions and export controls imposed in response to the conflict, including on Russia and Belarus, may adversely affect our business and other escalating global trade tensions, wars and conflicts, and the adoption or expansion of economic sanctions, export controls, or other trade restrictions could negatively affect us. |

| • | We rely to a significant extent on dividends and other distributions on equity paid by our principal operating subsidiaries to fund offshore cash and financing requirements. Any limitation on the ability of our operating subsidiaries to make payments to us could have a material adverse effect on our ability to conduct our business. |

Risks Relating to Our Securities

| • | The trading price of our securities has been and is likely to continue to be volatile, which could result in substantial losses to holders of our securities. |

| • | Sales of a substantial number of our securities in the public market by our existing securityholders could cause the price of our Ordinary Shares and Warrants to fall. |

| • | A certain number of our Warrants will become exercisable for our Ordinary Shares, which would increase the number of shares eligible for future resale in the public market and result in dilution to our shareholders. |

| • | The trading price of our securities has been and is likely to continue to be volatile, which could result in substantial losses to holders of our securities |

| • | If securities or industry analysts do not publish research, publish inaccurate or unfavourable research or cease publishing research about us, our share price and trading volume could decline significantly. |

| • | Future resales of our Ordinary Shares issued to Fosun and its affiliates may cause the market price of our securities to drop significantly, even if our business is doing well.. |

| • | Our ability to maintain the listing of our securities on the NYSE may be dependent on the PCAOB’s continued access to inspect our independent auditors. |

| • | You may face difficulties in protecting your interests, and your ability to protect your rights through U.S. courts may be limited, because we are incorporated under the laws of the Cayman Islands, we conduct substantially all of our operations, and a majority of our directors and executive officers reside, outside of the United States. The ability of U.S. authorities to bring actions for violations of U.S. securities laws and regulations against us and our directors and executive officers may be limited, and accordingly you may not be afforded the same protection as provided to investors in U.S. domestic companies. |

| • | The exercise price of our Warrants can fluctuate under certain circumstances which, if triggered, can potentially result in material dilution of our then existing shareholders. |

| • | Certain rights granted to Meritz in the Amended and Restated Meritz Relationship Agreement could limit the funds available to us or potentially result in dilution of our then existing shareholders. |

-3-

Table of Contents

| • | Fosun, being our controlling shareholder, has substantial influence over us and Fosun’s interests may not be aligned with the interests of our other shareholders, and Fosun losing control of us may materially and adversely impact us and our Securities. |

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in the JOBS Act, and we will remain an “emerging growth company” until the earliest to occur of (i) the last day of the fiscal year (a) following the fifth anniversary of the closing of the Business Combination, (b) in which we have total annual gross revenue of at least $1.07 billion or (c) in which we are deemed to be a large accelerated filer, which means the market value of our shares held by non-affiliates exceeds $700 million as of the last business day of our prior second fiscal quarter, we have been subject to Exchange Act reporting requirements for at least 12 calendar months; and filed at least one annual report, and (ii) the date on which we issued more than $1.0 billion in non-convertible debt during the prior three-year period. We intend to take advantage of exemptions from various reporting requirements that are applicable to most other public companies, whether or not they are classified as “emerging growth companies,” including, but not limited to, an exemption from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that our independent registered public accounting firm provide an attestation report on the effectiveness of our internal control over financial reporting and reduced disclosure obligations regarding executive compensation.

In addition, Section 102(b)(1) of the JOBS Act exempts “emerging growth companies” from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period, which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of our financial statements with certain other public companies difficult or impossible because of the potential differences in accounting standards used.

Implications of Being a Foreign Private Issuer and a Controlled Company

We are subject to the information reporting requirements of the Exchange Act that are applicable to “foreign private issuers,” and under those requirements we file reports with the SEC. As a foreign private issuer, we are not subject to the same requirements that are imposed upon U.S. domestic issuers by the SEC. Under the Exchange Act, we are subject to reporting obligations that, in certain respects, are less detailed and less frequent than those of U.S. domestic reporting companies. For example, we are not required to issue quarterly reports, proxy statements that comply with the requirements applicable to U.S. domestic reporting companies, or individual executive compensation information that is as detailed as that required of U.S. domestic reporting companies. We also have four months after the end of each fiscal year to file our annual reports with the SEC and are not required to file current reports as frequently or promptly as U.S. domestic reporting companies. Furthermore, our officers, directors and principal shareholders are exempt from the requirements to report transactions in our equity securities and from the short-swing profit liability provisions contained in Section 16 of the Exchange Act. As a foreign private issuer, we are also not subject to the requirements of Regulation FD (Fair Disclosure) promulgated under the Exchange Act. These exemptions and leniencies reduce the frequency and scope of information and protections available to you in comparison to those applicable to shareholders of U.S. domestic reporting companies.

We are a “controlled company” within the meaning of the NYSE listing rules as Fosun International owns more than 50% of our voting power as of the date of this prospectus. Under these rules, a “controlled company” will be permitted to elect to not comply with certain corporate governance requirements. Currently, we do not

-4-

Table of Contents

plan to utilize the exemptions available for controlled companies, but will rely on the exemption available for foreign private issuers to follow our home country governance practices instead.

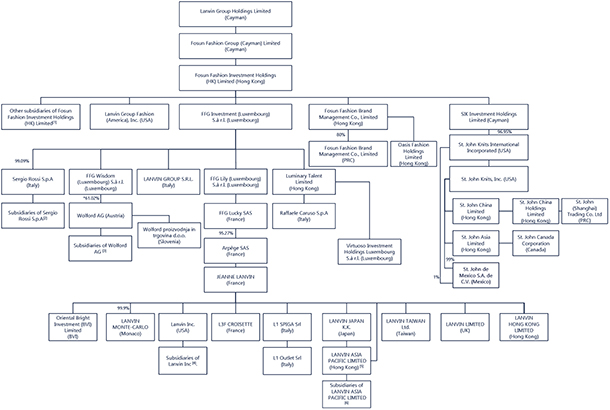

Our Organizational Structure

The following diagram depicts an organizational structure of the Company as of the date hereof. Except as otherwise specified, equity interests depicted in this diagram are held as to 100%.

PRC Permissions and Approvals

We conduct a portion (approximately 12.5% of our revenues in 2023) of our operations in China, and as of the date of this prospectus, we have obtained all requisite permissions and approvals that are material to our operations in China. However, there can be no assurance that we will be able to maintain such permissions and approvals in the future. In addition, laws and regulations in China may change quickly with little advance notice, and the Chinese government may intervene or influence our operations in China at any time. As a result, we may be required to obtain additional permissions and approvals in the future. There can be no assurance that such permissions and approvals can be obtained in a timely manner, or at all, and our business, results of operations and financial condition could be materially and adversely affected.

Under the PRC laws, rules and regulations currently in effect, no prior permission or approval from PRC government authority is required for the transactions completed pursuant to the Business Combination Agreement, including but not limited to the listing of our securities on the NYSE. However, the Chinese government has recently indicated that it may exert more control over offerings conducted overseas and foreign investment in China-based issuers. In particular, on February 17, 2023, the China Securities Regulatory Commission, or the CSRC, released the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies, or the Trial Measures, which came into effect on March 31, 2023. The Trial Measures will apply to overseas securities offerings and/or listings conducted by (i) companies incorporated in

-5-

Table of Contents

the PRC, or PRC domestic companies, directly and (ii) companies incorporated overseas with operations primarily in the mainland of China and valued on the basis of interests in PRC domestic companies, or indirect offerings. An equity or equity linked securities offering by an overseas company will be deemed an indirect offering if (i) more than 50% of such overseas company’s consolidated revenues, total profit, total assets or net assets that are derived from its audited consolidated financial statements for the most recently completed fiscal year are attributable to PRC domestic companies, and (ii) any of the following three circumstances applies: key components of its operations are carried out in the mainland of China; its principal places of business are located in the mainland of China; or the majority of the senior management members in charge of operation and management are citizens of the mainland of China or domiciled in the mainland of China.

The Trial Measures requires filings with the CSRC within three business days after the submission of an initial public offering or listing application overseas, or three business days after the completion of a follow-on offering in the same overseas market. If a company that should have been subject to the Trial Measures (i) has completed overseas offering and listing prior to the effectiveness of the Trial Measures; or (ii) (a) has its registration statement declared effective by the SEC prior to the effectiveness of the Trial Measures, and (b) while it is not necessary to fulfill any other regulatory procedures requested by the overseas regulators or overseas stock exchanges, will further complete its overseas offering and listing by September 30, 2023, such company is not required to file for such offering immediately, but should file as required if it is involved in follow-on offerings and other matters that require filing.

Our subsidiaries established in the mainland of China accounted for less than 50% of our consolidated revenues, total profit, total assets and net assets in 2021, 2022 and 2023. The main parts of our business activities are not conducted in the mainland of China. As a result, despite the fact that our principal executive offices are located in Shanghai, our principal places of business are not located in the mainland of China. Most of the senior managers in charge of our business operation and management are not citizens of the mainland of China or domiciled in the mainland of China. Hence, the likelihood that this offering will constitute an indirect overseas offering by a PRC domestic company under the Trial Measures is low, based on our assessment. We have therefore not filed materials pursuant to the Trial Measures. However, the interpretation, application and enforcement of the Trial Measures are still evolving, and it remains uncertain whether the requirements under the Trial Measures are applicable to this offering. If the offering by us pursuant to this registration statement is deemed an indirect offering by the CSRC, we will need to fulfil filing obligations pursuant to the Trial Measures.

On December 28, 2021, the Cyberspace Administration of China, together with certain other government authorities, promulgated the Revised Cybersecurity Review Measures that took effect from February 15, 2022, pursuant to which online platform operators holding over one million users’ information must apply for a cybersecurity review before listing abroad, and operators of “critical information infrastructure” that intend to purchase internet products and services that will or may affect national security must apply for a cybersecurity review. Furthermore, the competent government authorities may also initiate a cybersecurity review against the relevant operators where the authorities believe that the network product or service or data processing activities affect or may affect national security. However, the scope of potential operators of “critical information infrastructure” remains unclear. In addition, the scope of network product or service or data processing activities that will or may affect national security is also unclear and subject to regulatory interpretation. As of the date of this prospectus (i) we had not been informed by any PRC governmental authority of any requirement to apply for a cybersecurity review; (ii) we did not hold or process personal information of over one million users; and (iii) we had not received any investigation, notice, warning, or sanctions from applicable government authorities in relation to national security. Nonetheless, the interpretation and implementation of the Revised Cybersecurity Review Measures is subject to uncertainties, and the relevant laws and regulations may also change in the future.

As a result of such regulatory development, government authorities in China could conduct a cybersecurity review over our PRC domestic subsidiaries, which may have a material adverse effect on our business, results of operations and financial condition. See “Item 3. Key Information—D. Risk Factors—Risks Relating to Our Business and Industry—If we were to become subject to the oversight, discretion or control of PRC government authorities over of securities and/or foreign investments, it may result in a material adverse change in our

-6-

Table of Contents

operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors and cause the value of our securities to significantly decline, which would materially affect the interests of the investors” in our 2023 Form 20-F.

We are an offshore holding company and have operations in the mainland of China conducted by our PRC domestic subsidiaries. We may make loans to our PRC domestic subsidiaries subject to the approval from or registration with the governmental authorities and other limitations in the future. These include foreign exchange loan registrations and maximum statutory limit of the loan amount (which is either the difference between the registered capital and the total investment amount of the concerned company or the upper limit calculated based on the formula prescribed in the prevailing regulations). There can be no assurance that such permissions and approvals can be obtained in a timely manner, or at all, and our business, results of operations and financial condition could be materially and adversely affected.

Permissions and Approvals on Transfer and Repatriation of Cash within Our Group

We transfer cash to our subsidiaries through capital injections and shareholder loans. Subject to the cash needs of the subsidiaries, shareholders’ loans as granted may be capitalized (as equity) or repaid.

Cash in the subsidiaries may also be repatriated to us via dividend distribution. Nevertheless, no cash repatriation by way of distribution/dividends was made to us prior to our Business Combination or to LGHL as of the date of this prospectus.

Our principal subsidiaries, being our portfolio brands, are based mainly in the U.S. (Delaware) and Europe including Italy, France and Austria. We are subject to certain restrictions or limitations regarding distribution of earnings from the portfolio brands to us, which may in turn limit the cash available to make distributions to our shareholders. For our operating subsidiaries that are Delaware corporations, to which the Delaware General Corporation Law (DGCL) applies, the power and authority to declare dividends/distributions resides with the board of directors of the corporation. Further, the DGCL permits distributions out of either a surplus or net profits (subject to certain limitations). In addition, specific provisions under credit agreements or the relevant subsidiary’s bylaws may impose specific restrictions or approval requirements regarding dividend payment (including a contingent obligation or otherwise). For our Italian subsidiaries, no distribution may be made unless a reserve fund accumulated from net profits reach at least 20% of the relevant subsidiary’s share capital. Our subsidiaries in Italy also face other general restrictions to the shareholders’ right to an earnings distribution. In Austria, our subsidiaries cannot issue a dividend unless the validly adopted financial statements for a financial year show a balance sheet profit, which represents the maximum amount of capital available for the distribution of profits. Loans by us to our subsidiaries in Austria are considered equity substitution if we are in a crisis, and will only be repaid if we are fully restructured.

For our portfolio brands, the cash needs of the brands’ subsidiaries are provided as necessary in the form of shareholder loans or capital injections from us or the relevant parent brand entity. Payments from local subsidiaries to their parent brands are typically for purchase of inventories from the parent brand, and generally do not face any foreign exchange or capital control limitations. However, dividends and loan repayments may face similar restrictions as mentioned above.

Dividends repatriated or paid from our Chinese subsidiaries must be made from retained earnings as per such subsidiary’s financial statements prepared in accordance with Chinese accounting rules. Additionally, each of our Chinese subsidiaries must set aside a statutory reserve fund of at least 50% of its registered capital before it may pay dividends, and a 10% withholding tax or other reduced rate withholding tax under the China-Hong Kong treaty may be applied to the dividends repatriated from our Chinese subsidiaries. Also, approval from or registration with appropriate Chinese government authorities is required where RMB is to be converted into foreign currency and remitted outside of China to pay capital expenses such as the repayment of loans denominated in foreign currencies. However, we do not expect Chinese subsidiaries to declare any dividends or pay capital expenses to our portfolio brands in the near future.

-7-

Table of Contents

We made capital injections of EUR50.0 million in 2021, EUR50.0 million in 2022 and EUR27.0 million in 2023 into Lanvin brand portfolio through Arpège SAS, as well as EUR7.9 million in Raffaele Caruso S.p.A. in 2021. We also made an advance payment of EUR1.0million in Raffaele Caruso S.p.A in 2023. Caruso also received a shareholder loan of EUR2.5 million, EUR5.5 million and EUR1.0 million from us in 2021, 2022 and 2023, respectively. We have waived part of the repayment of shareholder loan by Caruso. In 2023, we paid EUR11.78 million for the subscription of Wolford shares. In addition, Wolford AG received shareholder loans of EUR10.0 million, EUR22.5 million, and EUR10.8 million from us in 2021, 2022 and 2023, respectively. In 2021, 2022 and 2023, we issued shareholder loans of $35.8 million, $25.5 million and $12.5 million, respectively, to St. John. After we acquired Sergio Rossi in 2021, Sergio Rossi S.p.A received capital injections of EUR5.0 million, EUR13.0 million and EUR11.0 million in 2021, 2022 and 2023, respectively. In 2023, Sergio Rossi S.p.A received a shareholder loan of EUR3.5million from us. We have also made capital injections and intercompany loans totaling RMB1.1 million, $3.7 million and $2.5 million to our Chinese subsidiaries in 2021, 2022 and 2023, respectively.

Other than the loan repayment of $1.0 million by St. John to us in August 2023, none of our direct subsidiaries made any dividends, distributions, or repayments to us in 2021, 2022 and 2023. We have also not made any transfers, dividends, or distributions to our shareholders as of the date of this annual report other than the cash dividend of $1.0 million and $1.0 million paid to Meritz in 2022 and 2023, respectively. On March 30, 2023, Jeanne Lanvin S.A. (“JLSA”) as the borrower, LGHL as the guarantor and Meritz as the lender entered into a facility agreement, pursuant to which Meritz made available to JLSA a facility in the sum of JPY3,714.4 million (the “Facility”). In 2023, a total of JPY502.3 million under the Facility was repaid to Meritz, including both principal and interest. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Meritz Private Placement” and “Item 7. Major Shareholders and Other Related Party Transactions—B. Related Party Transactions—Other Related Party Transactions—Shareholder Loans” in our 2023 Form 20-F.

The Holding Foreign Companies Accountable Act

We may be subject to the risk of trading prohibitions under the HFCA Act. Our independent auditor, Grant Thornton Zhitong Certified Public Accountants LLP, is an independent registered accounting firm based in the mainland of China. Pursuant to the HFCA Act and related regulations, if we have filed an audit report issued by a registered public accounting firm that the PCAOB has determined is unable to inspect and investigate completely for two consecutive years, the SEC will prohibit our securities from being traded on a national securities exchange or in the over-the-counter trading market in the United States. On December 15, 2022, the PCAOB issued a report that vacated its December 16, 2021 determination and removed mainland China and Hong Kong from the list of jurisdictions where it is unable to inspect or investigate completely registered public accounting firms. However, there can be no assurance that the PCAOB will continue to have such access. Should PRC authorities fail to facilitate the PCAOB’s access in the future, the PCAOB may consider the need to issue a new determination, which may affect our ability to maintain the listing of our securities on the U.S. national securities exchanges, including the NYSE, and the trading of them in the over-the-counter trading market. A delisting would substantially impair your ability to sell or purchase our securities when you wish to do so, and the risk and uncertainty associated with a potential delisting would have a negative impact on the price of our securities. For details, see “Item 3. Key Information—D. Risk Factors—Risks Relating to Our Securities—Our ability to maintain the listing of our securities on the NYSE may be dependent on the PCAOB’s continued access to inspect our independent auditors” in our 2023 Form 20-F.

Corporate Information

We are a holding limited company incorporated under the laws of the Cayman Islands. Our principal executive office is at 4F, 168 Jiujiang Road, Carlowitz & Co, Huangpu District, Shanghai, 200001, China and our telephone number is +86-21-6315-3873. Our website is https://lanvin-group.com. The information contained in, or accessible through, our website does not constitute a part of, nor incorporated by reference into, this prospectus or our other filings with the SEC, and should not be relied upon.

The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers, such as we, that file electronically, with the SEC at www.sec.gov.

-8-

Table of Contents

Investing in our securities involves a high degree of risk. Before making a decision to invest in our securities, you should carefully consider all risk factors described in the documents incorporated by reference in this prospectus, including the risk factors discussed under the heading “Item 3. Key Information—D. Risk Factors” in our 2023 Form 20-F for the year ended December 31, 2023 which is incorporated by reference in this prospectus and in similar sections in subsequent filings incorporated by reference in this prospectus, and any information in the applicable prospectus supplement. See “Incorporation of Certain Documents by Reference.” If any of such risks occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that case, the market price or liquidity of our securities could decline, and you could lose some or all of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations.

-9-

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and any prospectus supplement contain forward-looking statements. Forward-looking statements include all statements that are not historical statements of fact and statements regarding, but not limited to, our expectations, hopes, beliefs, intention or strategies of regarding the future. You can identify these statements by forward-looking words such as “may,” “expect,” “predict,” “potential,” “anticipate,” “contemplate,” “believe,” “estimate,” “intend,” “plan,” “future,” “outlook,” “project,” “will,” “would” and “continue” or similar words. You should read statements that contain these words carefully because they:

| • | changes adversely affecting the business in which we are engaged; |

| • | our projected financial information, anticipated growth rate, profitability and market opportunity may not be an indication of our actual results or our future results; |

| • | management of growth; |

| • | the impact of health epidemics, pandemics and similar outbreaks, including the COVID-19 pandemic on our business; |

| • | our ability to safeguard the value, recognition and reputation of our brands and to identify and respond to new and changing customer preferences; |

| • | the ability and desire of consumers to shop; |

| • | our ability to successfully implement our business strategies and plans; |

| • | our ability to effectively manage our advertising and marketing expenses and achieve desired impact; |

| • | our ability to accurately forecast consumer demand; |

| • | high levels of competition in the personal luxury products market; |

| • | disruptions to our distribution facilities or our distribution partners; |

| • | our ability to negotiate, maintain or renew our license agreements; |

| • | our ability to protect our intellectual property rights; |

| • | our ability to attract and retain qualified employees and preserve craftmanship skills; |

| • | our ability to develop and maintain effective internal controls; |

| • | general economic conditions; |

| • | the result of future financing efforts; and |

| • | other factors discussed elsewhere in this prospectus, including the section entitled “Risk Factors” and the documents incorporated by reference in this prospectus. |

In addition, statements that “we believe” and other similar statements reflect our belief and opinions on the relevant subject. These statements are based upon information available to us as of the date of this prospectus, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherent uncertain and investors are cautioned not to unduly rely upon these statements.

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this prospectus. All forward-looking statements included herein are expressly qualified in their entirety by the cautionary statements contained or referred to in this section as well as any other cautionary statements contained herein. Except to the extent required by applicable laws and regulations, we undertake no obligations to update these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events. In light of these risks and uncertainties, you should keep in mind that any event described in a forward-looking statement made in this prospectus or elsewhere might not occur.

-10-

Table of Contents

Table of Contents

We have never declared or paid any cash dividend on our Ordinary Shares. We currently intend to retain any future earnings and do not expect to pay any dividends on our Ordinary Shares in the foreseeable future. Any future determination to pay dividends on our Ordinary Shares would be at the discretion of our board of directors, subject to applicable laws, and would depend on our financial condition, results of operations, capital requirements, general business conditions, and other factors that our board of directors may deem relevant.

-12-

Table of Contents

The following table sets forth our consolidated capitalization as of December 31, 2023.

You should read this table in conjunction with our consolidated financial statements and the related notes as of December 31, 2022 and 2023, and for each of the three years ended December 31, 2023, which are contained in our 2023 Form 20-F and incorporated by reference in this prospectus.

| As of December 31, 2023 |

||||

| (€ in thousands) | ||||

| Cash and cash equivalents |

28,130 | |||

|

|

|

|||

| Total equity |

165,628 | |||

| Debt: |

||||

| Non-current borrowings |

32,381 | |||

| Current borrowings |

35,720 | |||

| Total indebtedness |

68,101 | |||

|

|

|

|||

| Total capitalization |

233,729 | |||

|

|

|

|||

We entered into a side letter with Meritz on April 30, 2024, which modified the Amended and Restated Meritz Relationship Agreement. Pursuant to the side letter, we agreed to repurchase from Meritz 5,245,648 Ordinary Shares in aggregate for a total purchase price of $20.0 million. Such share repurchase will be based on the following schedule: 1,328,704 Ordinary Shares on April 30, 2024 for $5.0 million, (ii) 1,318,129 Ordinary Shares on June 28, 2024 for $5.0 million, (iii) 1,305,220 on July 31, 2024 for $5.0 million and (iv) 1,293,595 on August 30, 2024 for $5.0 million. We completed the repurchase of 1,328,704 Ordinary Shares on April 30, 2024 and 1,318,129 Ordinary Shares on June 28, 2024 from Meritz. See “Item 5. Operating and Financial Review and Prospects—B. Liquidity and Capital Resources—Meritz Private Placement” in our 2023 Form 20-F.

-13-

Table of Contents

A summary of the material provisions governing our share capital is described below. This summary is not complete and should be read together with our Amended Articles, a copy of which is incorporated by reference in this registration statement.

We are a Cayman Islands exempted company incorporated with limited liability and our affairs are governed by the Amended Articles, the Cayman Companies Act, and the common law of the Cayman Islands.

Our authorized share capital is $50,000 divided into 49,984,999,999 Ordinary Shares with a par value of $0.000001 each, 15,000,000 Non-Voting Ordinary Shares with a par value of $0.000001 each and one Convertible Preference Share with a par value of $0.000001. As of July 15, 2024, there were 142,374,619 Ordinary Shares issued and outstanding. As of the same date, no Non-Voting Ordinary Shares was issued. On December 14, 2023, we repurchased the Convertible Preference Share from Meritz. All Ordinary Shares issued and outstanding as of the date of this prospectus are fully paid and non-assessable.

The Amended Articles became effective on December 14, 2022. The following are summaries of material provisions of the Amended Articles and the Cayman Companies Act insofar as they relate to the material terms of our securities.

Exempted Company

We are a Cayman Islands exempted company incorporated with limited liability. The Cayman Companies Act distinguishes between ordinary resident companies and exempted companies. Any company that is registered in the Cayman Islands but conducts business mainly outside of the Cayman Islands may apply to be registered as an exempted company. The requirements for an exempted company are essentially the same as for an ordinary company exempt for the exemptions and privileges listed below:

| • | an exempted company does not have to file an annual return of its shareholders with the Registrar of Companies of the Cayman Islands; |

| • | an exempted company’s register of members is not open to inspection; |

| • | an exempted company does not have to hold an annual general meeting; |

| • | an exempted company may issue no par value shares; |

| • | an exempted company may obtain an undertaking against the imposition of any future taxation (such undertakings are usually given for 20 years in the first instance); |

| • | an exempted company may register by way of continuation in another jurisdiction and be deregistered in the Cayman Islands; |

| • | an exempted company may register as a limited duration company; and |

| • | an exempted company may register as a segregated portfolio company. |

Ordinary Shares

General

All of our issued and outstanding ordinary shares are fully paid and non-assessable.

Our shareholders who are non-residents of the Cayman Islands may freely hold and vote their ordinary shares. The Amended Articles prohibit us from issuing bearer or negotiable shares. We may not issue share to bearer and Ordinary Shares are issued in registered form, which will be issued when registered in our register of members.

-14-

Table of Contents

Dividends

The holders of our Ordinary Shares are entitled to receive such dividends as may be declared by the board of directors subject to the Amended Articles and the Cayman Companies Act. In addition, our shareholders may by ordinary resolution declare a dividend, but no dividend may exceed the amount recommended by the board of directors. Under Cayman Islands law, dividends may be paid only out of profits (including retained earnings), or out of the share premium account (subject to a solvency test being met immediately following the payment of the dividend). No dividend may be declared and paid unless our directors determine that we have funds lawfully available for such purpose and that, immediately after the payment, we will be able to pay our debts as they fall due in the ordinary course of business.

Register of Members

Under Cayman Islands law, we must keep a register of members and there must be entered therein:

| • | the names and addresses of the members, together with a statement of the shares held by each member, and such statement shall confirm (i) the amount paid or agreed to be considered as paid, on the shares of each member, (ii) the number and category of shares held by each member, and (iii) whether each relevant category of shares held by a member carries voting rights under the articles of association of the company, and if so, whether such voting rights are conditional; |

| • | the date on which the name of any person was entered on the register as a member; and |

| • | the date on which any person ceased to be a member. |

Under Cayman Islands law, the register of members is prima facie evidence of the matters set out therein (i.e., the register of members will raise a presumption of fact on the matters referred to above unless rebutted) and a member registered in the register of members will be deemed as a matter of Cayman Islands law to have legal title to the shares as set against its name in the register of members.

If the name of any person is, without sufficient cause, entered in or omitted from the register of members, or if default is made or unnecessary delay takes place in entering on the register the fact of any person having ceased to be a member, the person or member aggrieved or any member or our Company itself may apply to the Grand Court of the Cayman Islands for an order that the register be rectified, and the Court may either refuse such application or it may, if satisfied of the justice of the case, make an order for the rectification of the register.

Voting Rights

Voting at any meeting of shareholders will be decided by poll and not by way of a show of hands. A poll shall be taken in such manner as the chair directs, and the result of the poll shall be deemed to be the resolution of the meeting.

Subject to any rights and restrictions for the time being attached to any share, every shareholder and every person representing a shareholder by proxy shall have one vote for each share of which they or the person represented by proxy is the holder.

All questions submitted to a meeting shall be decided by an ordinary resolution except where a greater majority is required by the Amended Articles or by the Cayman Companies Act. In the case of an equality of votes, the chair of the meeting shall be entitled to a second or casting vote. All resolutions of the shareholders shall be passed at a general meeting duly convened and held in accordance with the Amended Articles and resolutions of shareholders in writing in lieu of a general meeting shall not be permitted.

-15-

Table of Contents

An ordinary resolution to be passed by the shareholders will require a simple majority of votes cast, including by all holders of a specific class of shares, if applicable, while a special resolution will require not less than two-thirds of votes cast.

General Meetings and Shareholder Proposals

As a Cayman Islands exempted company, we are not obliged by the Cayman Companies Act to call

shareholders’ annual general meetings. The Amended Articles provide that our board of directors may convene a general meeting at any time whenever they see fit, but does not compel us to convene an annual general meeting.

Separate general meetings of the holders of a class or series of shares may be called by a majority of the entire board of directors (unless otherwise specifically provided by the terms of issue of the shares of such class or series).

Cayman Islands law provides limited rights for shareholders to requisition a general meeting. However, additional rights may be provided in a company’s articles of association. The Amended Articles allow our shareholders holding at least ten percent of the paid up voting share capital of the Company to requisition a shareholder’s meeting.

A quorum required for a meeting of shareholders consists of any one or more shareholders holding at least one-third (1/3) of the paid up voting share capital present and entitled to vote at that meeting shall form a quorum or, if a corporation or other non-natural person, by its duly authorized representative. In the ordinary course, advance notice of at least seven clear days’ notice in writing is required for the convening of our annual general meeting and other shareholders meetings.

Transfer of Ordinary Shares

Subject to applicable laws, including securities laws, the NYSE rules and the restrictions contained in the Amended Articles and to any lock-up agreements to which a shareholder may be a party, any shareholders may transfer all or any of their Ordinary Shares by an instrument of transfer in the usual or common form or in a form prescribed by the NYSE rules or any other form approved by the board of directors.

Subject to the NYSE rules and to any rights and restrictions for the time being attached to any Ordinary Share, the board of directors shall not unreasonably decline to register any transfer of Ordinary Shares and if the board of directors refuses to register a transfer our Company shall, within two months after the date on which the instrument of transfer was lodged with our Company, send to each of the transferor and the transferee notice of the refusal, including the relevant reason for such refusal.

Issuance of Additional Shares

The board of directors may issue additional ordinary shares from time to time as the board of directors shall determine, to the extent of available authorized but unissued shares.

Liquidation

On the winding up, if the assets available for distribution amongst the shareholders shall be more than sufficient to repay the whole of the share capital at the commencement of the winding up, the surplus shall be distributed amongst the shareholders in proportion to the par value of the shares held by them at the commencement of the winding up, subject to a deduction from those shares in respect of which there are monies due, of all monies payable to us for unpaid calls or otherwise. If our assets available for distribution are

-16-

Table of Contents

insufficient to repay the whole of the share capital, such assets shall be distributed so that, as nearly as may be, the losses are borne by our shareholders in proportion to the par value of the shares held by them. We are a Cayman Islands exempted company incorporated with limited liability, and under the Cayman Companies Act, the liability of our members is limited to the amount, if any, unpaid on the shares respectively held by them. The Amended Articles contains a declaration that the liability of our members is so limited.

Calls on Ordinary Shares and Forfeiture of Ordinary Shares

Our board of directors may from time to time make calls upon shareholders for any amounts unpaid on their Ordinary Shares. The Ordinary Shares that have been called upon and remain unpaid are, after a notice period, subject to forfeiture.

Redemption, Repurchase and Surrender of Ordinary Shares

Subject to the provisions of the Cayman Companies Act, we may issue shares on terms that such shares are subject to redemption or are liable to be redeemed, at our option or at the option of the holders thereof. The redemption of such shares will be effected in such manner and upon such other terms as we may, by ordinary resolution of the shareholders or the board of directors, determine before the issue of the shares.

We may also repurchase any of our shares provided that the manner and terms of such purchase have been approved by our board of directors, or by the shareholders by ordinary resolution, or are otherwise authorized by the Amended Articles. The premium (if any) payable in respect of any shares being redeemed or purchased may be paid out of profits, out of the share premium account or out of the proceeds of a fresh issue of shares made for the purposes of the redemption or purchase. Alternatively, as authorized under the Amended Articles, we may make a payment in respect of the redemption or purchase of its own shares out of capital provided that immediately following the date on which the payment out of capital is proposed to be made, we shall be able to pay its debts as they fall due in the ordinary course of business. In addition, under the Cayman Companies Act no such share may be redeemed or repurchased (a) unless it is fully paid up, (b) if such redemption or repurchase would result in there being no issued shares outstanding (excluding any shares held in treasury), or (c) if we have commenced liquidation. In addition, we may accept the surrender of any fully paid share for no consideration.

Variation of Rights of Shares

Subject to the Amended Articles, if at any time the share capital is divided into different classes of shares, the rights attached to any such class may, subject to any rights or restrictions for the time being attached to any class, be varied or abrogated without the consent of the holders of the issued shares of that class where such variation or abrogation is considered by the directors not to have a material adverse effect upon such rights. Otherwise, any such variation or abrogation will be made only with the consent in writing of the holders of not less than two-thirds of the issued shares of that class, or with the approval of a resolution passed by a majority of not less than two-thirds of the votes cast at a separate meeting of the holders of the shares of that class.

The rights conferred upon the holders of the shares of any class issued with preferred or other rights shall not, subject to any rights or restrictions for the time being attached to the shares of that class, be deemed to be materially adversely varied or abrogated by, inter alia, the creation, allotment or issue of further shares ranking pari passu with or subsequent to them or the redemption or purchase of any shares of any class by us.

General Meeting of Shareholders