As filed with the Securities and Exchange Commission on January 31, 2023

Registration Statement No. 333-264195

UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

TO

FORM

FOR REGISTRATION

UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

(Exact name of registrant as specified in its governing instruments)

5847 San Felipe, Suite 4675

Houston,

TX 77057

Tel: (832-804-9680)

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

John

R. Krugh

1800 Bering Drive, Suite 350

Houston, Texas 77057

Tel: (713-255-0266)

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Steve Kronengold

SRK Kronengold Law Offices

7 Oppenheimer

Rehovot, Israel

Telephone No.: +972-8-936-0999

Facsimile No.: +972-8-936-6000

Approximate

date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | Smaller reporting company | ||||

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION,

DATED January 31, 2023

PROSPECTUS

Shares

Maple X, Inc.

Common Stock

Maple X, Inc. is a recently incorporated Texas corporation that operates in Texas in the field of land development for residential and commercial construction. We purchase undeveloped land, and engage in the planning, development, and construction of necessary infrastructure, and then we sell ready-to-build lots to homebuilders, construction companies and real estate developers. We will be externally managed and advised by Maple Development Group, LLC (the “Manager”), a Texas limited liability company controlled by the same shareholders who control the Company. The Company is controlled by four individuals, Uri Frisch, an Israeli citizen and resident, Roi Marsiano, an Israeli citizen and resident, Michael Sabo, a U.S. citizen and resident, and Itiel Kaplan, a dual U.S.-Israeli citizen and a U.S. resident (the “Controlling Shareholders”), who are projected to own in the aggregate at least 70% of the Company following this offering.

This is our initial public offering. No public market currently exists for our common stock.

Currently, no public market exists for our common stock. We intend to apply to list our common stock on the Tel Aviv Stock Exchange (the “TASE”) under the symbol “ ”. We are offering all of the shares of common stock sold in this offering to the public in Israel at a price per share of Israeli new shekels (“ILS”), which we refer to as the Offering Price. We are not conducting an offering to the public in the United States. We expect to engage Orion Underwriting and Issuances Ltd. (“Orion”) to serve as the pricing underwriters for purposes of Section 1 of the Israeli Securities Law of 1968 and regulations thereunder (the “Israeli Securities Law”), which means underwriters who participate in determining the price per share at which shares of our common stock will be offered to the public. As described in more detail in the “Plan of Distribution”, we will conduct the offering of shares of our common stock through a non-uniform offering with the price per share to be determined by the pricing underwriters in agreement with us based on the process for evaluating institutional investor demand known as book-building. We expect to appoint , a member of the TASE, to also act as our offering coordinator.

We are an “emerging growth company” under U.S. federal securities laws and will be subject to reduced public company reporting requirements. You should consider the risks described in “Risk Factors” beginning on page 12 of this prospectus for risks relevant to an investment in our common stock.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting and/or distribution commissions | $ | $ | ||||||

| Proceeds, to us, before expenses | $ | $ | ||||||

| (1) | As converted from ILS to U.S. dollars (“USD”) at the representative exchange rate of ILS per USD, as published by the Bank of Israel on its website on , 2022. |

| (2) | The initial gross proceeds from the sale of our shares of common stock are estimated based upon the Offering Price assuming the maximum number of shares of common stock offered in this offering are sold. |

Neither the United States Securities and Exchange Commission nor any state or non-U.S. securities commission or authority has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We will conduct a non-uniform offering, and Orion, together with any other underwriters, will commit to purchase up to 25% of shares of our common stock offered by this prospectus pursuant to an underwriting agreement.. The remaining 75% of shares of common stock offered by this prospectus will be offered by the underwriters on a best-efforts basis. We expect to complete the offering within seventy-five (75) days from the date of this prospectus. For more details, please see the “Plan of Distribution” below.

The underwriters expect to deliver the shares on or about , 2023.

The date of this prospectus is , 2023.

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus or any free writing prospectus prepared by us. We have not, and the underwriters have not, authorized any other person to provide you with different or additional information. If anyone provides you with different or additional information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the cover of this prospectus. Our business, financial condition, liquidity, results of operations and prospects may have changed since that date.

Market Data

We use market data, demographic data, industry forecasts and industry projections throughout this prospectus. Unless otherwise indicated, we have obtained such market and industry data from publicly available industry and governmental publications. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information.

Unless otherwise indicated or the context otherwise requires, all references in this prospectus to “Maple X”, “we”, “our”, “us”, and “Company” refer to Maple X, Inc., a Texas corporation, together with its consolidated subsidiaries, after giving effect to the formation transactions described in this prospectus. For additional information about the formation transactions, see “Structure and Formation of Our Company”.

Certain dollar figures in this prospectus are expressed in, or have been converted from, Israeli new shekels (“ILS”). Unless otherwise stated, all such amounts were converted from ILS to USD at the representative exchange rate of ILS per USD, as published by the Bank of Israel on its website on , 2023.

i

PROSPECTUS SUMMARY

The following summary highlights information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in our common stock. You should read the entire prospectus carefully, including the section entitled “Risk Factors,” as well as the financial statements and related notes included elsewhere in this prospectus, before making an investment decision.

Unless otherwise indicated, the information contained in this prospectus (i) reflects the completion of the formation transactions, as described below under the caption “Structure and Formation of Our Company”, (ii) assumes that the shares of our common stock to be sold in this offering are sold at $ per share, which is the USD equivalent of the Offering Price set forth on the front cover of this prospectus, and (iii) presents all property-level information as of December 31, 2021, unless otherwise indicated, on a pro forma basis for the formation transactions.

Our Company

We are a recently incorporated Texas corporation that operates in Texas in the field of land development for residential and commercial construction. We purchase undeveloped land, and engage in the planning, development, and construction of necessary infrastructure, and then we sell read-to-build lots of land to homebuilders, construction companies and real estate developers. Our focus is on land development for residential and commercial construction targeted to the middle-class.

Our strategy is to focus on acquiring appropriate properties; engaging in planning, engineering supervision, and development of these properties; and then selling the developed land to homebuilders and commercial contractors. We undertake horizontal development of undeveloped land in vibrant, supply-constrained markets, in circumstances where we believe we will be able to leverage our management team’s experience and relationships to generate strong risk-adjusted returns for our stockholders.

Our initial portfolio is comprised of 12 projects that are in the process of development planning and design. Our projects are in various pre-planning, planning and development stages, and consist of approximately 1,366 acres and more than 4,240 lots ready for the construction of single-family homes, as well as land parcels amounting to approximately 1,056 acres intended for value appreciation purposes and future development for residential and commercial use. In addition, on January 6, 2023 we completed the sale of the Maple Heights property, which included approximately 211 acres and about 900 lots for the construction of housing units . In addition to our initial portfolio, we maintain an acquisition pipeline of additional prospective investments, focused on assets in high growth metropolitan areas with close proximity to mass transportation, healthcare, and social infrastructure.

The Company is controlled by four individuals, Uri Frisch, an Israeli citizen and resident, Roi Marsiano, an Israeli citizen and resident, Michael Sabo, a U.S. citizen and resident, and Itiel Kaplan, a dual U.S.-Israeli citizen and a U.S. resident (the “Controlling Shareholders”), who are projected to own in the aggregate at least 70% of the Company following this offering.

Fields of Activity

The Company focuses on two fields of activity, development for master planned communities, and real estate investment.

Master Planned Communities

Most of the Company’s projects may be characterized as being in the field of master planned communities. Master planned communities are a form of development envisioned and delivered as a self-contained, unified community, with clear boundaries and a full range of land uses, employment opportunities, and public facilities and services. Master planned communities are frequently built on the edge of existing metropolitan areas.

There is no single, accepted definition to describe master planned communities. Most master planned communities will have a consistent design character, while allowing for some varieties of design styles, home sizes, prices, and lot sizes to cater to multiple segments of the market and allow space for the diversity that can help create the feel of community. Master planned communities are frequently developed by a single-development entity, though many developers will allow separate builders to create smaller subdivisions so that each one is unique and offers residents something different from the others.

As part of a master planned community, an entire neighborhood is planned, including all the services and infrastructure required to create an actual community, such as public services, schools, retail and recreational areas, parks and swimming pools, sport centers, and sometimes even employment centers. Master planned communities are widescale projects which may include up to tens of thousands of residents and require several years for development. They are often developed in phases, such that in each phase of the project the relevant infrastructures and public areas for that particular phase are developed.

1

Real Estate Investment

In addition to projects for master planned communities, the Company acquires undeveloped properties for investment and value appreciation. These properties are not part of projects for master planned communities. The Company may hold these properties and resell them in the future after their value has increased or the Company may engage in infrastructure development, similar to the Company’s activities in the master planned communities field.

The Company’s activities in the field of real estate investment are complementary to its activities in the field of development for master planned communities. The Company’s real estate investment projects may relate to land that is proximate to the land that forms part of a project for a master planned community, or the land may be separate and independent from a project for a master planned community.

See the section of this prospectus entitled “Description of Business and Properties” for more detail on the Company’s activities.

Our Manager

Although we will directly retain a CEO, Itiel Kaplan, and a CFO, Ilanit Halperin, we will be externally managed and advised by Maple Development Group, LLC, a Texas limited liability company formed in 2019 (the “Manager”), which is majority owned and controlled by the same individuals who are the controlling shareholders of the Company: Uri Frisch, an Israeli citizen and resident, Roi Marsiano, an Israeli citizen and resident, Michael Sabo, a U.S. citizen and resident, and Itiel Kaplan, a dual U.S.-Israeli citizen and a U.S. resident (the “Controlling Shareholders”). Prior to or in connection with this offering, we will enter into a management agreement with our Manager pursuant to which our Manager will assist our CEO with the management of our business and affairs and with the day-to-day operations of the Company. A team of real estate professionals acting through our Manager will make all the decisions regarding the selection, negotiation, financing, and disposition of our investments, subject to direction provided by our Board of Directors and the limitations in our operating agreements.

Our Manager will also provide asset management, marketing, investor relations, and other administrative services on our behalf with the goal of maximizing our operating cash flow and preserving our invested capital.

Our Manager will be entitled to the following fees:

| ● | An annual fee equal to 1% of the net asset value (NAV) of the Company’s properties, to be paid by us. |

| ● | A development fee equal to 5% of the development costs of each of our properties, to be paid monthly by the applicable Property Company. The development fee is paid monthly in equal monthly installments in accordance with the business plan for the particular project, with a true-up upon project completion. |

| ● | In addition, the Company will reimburse the Manager for reasonable business expenses. |

| ● | The Company will pay the insurance premiums for insurance for the Manager. |

We estimate that the approximate, aggregate maximum fees to be paid to our Manager in 2022 for asset management, marketing, and other administrative services and related out-of-pocket and other reimbursements (assuming that the we do not acquire any additional properties or projects) will total $1,025,600.

Attractive Risk-Adjusted Returns Supported by Strong Long-Term Market Dynamics

We believe attractive risk-adjusted returns in real estate investments can be achieved by: (i) acquiring undeveloped properties in vibrant markets with high income growth; and (ii) developing and selling these properties to homebuilders and commercial contractors.

We intend to acquire properties primarily in locations where demand outstrips supply and that have a potential for further growth.

See the section of this prospectus entitled “Market Opportunity” for more detail on these attractive supply and demand dynamics.

2

Our Initial Properties

We currently have an ownership interest in twelve properties. In January 2022, we obtained an ownership interest in the Maple Heights property by acquiring from the Controlling Shareholders their 50% interest in Maple Heights GP, LLC, a Delaware limited liability company that has a 10% ownership interest in the Maple Heights property. On January 6, 2023, we completed the sale of the Maple Heights Property. Our twelve properties (as well as the Maple Heights property) are listed in the tables below (the “Owned Properties”).

Master Planned Community Properties

| Name of Property | Location | Ownership Percentage in the Property | Profit Participation Percentage (including Promote Allocation*) | Status / Stage | Size (Acres) | Residential Lots | Acquisition Date | Purchase Price | Debt as of 9/30/2022 | Projected Completion Date | ||||||||||||||||||||

| Maple View | Alvin, Brazoria County, TX | 5 | % | 33.4%

right to profits | Planning and Permits | 235 | 800 | 12/29/2021 | $ | 3,529,215 | $ | 2,128,041 | 3/31/2028 | |||||||||||||||||

| Maple Grove | Pattison, Waller Country, TX | 5 | % | 38.4% right to profits | Planning and Permits | 257 | 1,000 | 12/8/2021 | $ | 9,004,854 | $ | 3,516,891 | 3/31/2028 | |||||||||||||||||

| Pecan Ranch | Bonney, Brazoria County, TX | 5 | % | 36.8% right to profits | Planning and Permits | 169 | 500 | 12/10/2021 | $ | 3,700,728 | $ | 2,220,043 | 9/30/2026 | |||||||||||||||||

| Maple Heights† | Porter, Montgomery County, TX | 5 | % | 28.6% right to profits | Parcels are being sold | 211 (158.5 acres have been sold as of 7/31/22) | N/A Parcels are being sold “as is.” | 6/27/2019 | $ | 8,000,000 | $ | 1,198,000 | 01/6/2023 | |||||||||||||||||

| Maple Woods | Hockley, TX | 5 | % | 36.9% right to profits | Planning and Permits | 142 | 450 | 4/15/2022 & 09/13/2022 |

$ | 4,614,685 | $ | 2,752,500 | ‡ | 12/31/2026 | ||||||||||||||||

| Maple Reserve | Waller County, TX | 5 | % | 35.6% right to profits | Planning and Permits | 374 | 1,000 | 7/5/2022 | $ | 13,846,721 | $ | 10,000,000 | ‡ | 07/01/2029 | ||||||||||||||||

| Maple Park | Brookshire TX | 5 | % | 35.8% right to profits | Planning and Permits | 155 | 425 | 12/12/2022 | $ | 6,180,000 | $ | 3,000,000 | ‡ | 10/31/2027 | ||||||||||||||||

| (*) | The Promote Allocation is an added percentage linked to the profitability of each project and is determined according to the waterfall distribution terms in the relevant operating agreement. The calculated percentage is subject to change based on the property’s profitability. |

| (†) | The Maple Heights property appears in this table even though it is no longer part the Company’s portfolio of properties. In January 2022, the Company acquired from the Controlling Shareholders their 50% interest in Maple Heights GP, LLC, a Delaware limited liability company that has a 10% ownership interest in the Maple Heights property. On January 6, 2023, the Company completed the sale of the Maple Heights property. |

| (‡) | Debt as of December 31, 2022 |

Investment Properties

| Name of Property | Location | Ownership Percentage in the Property | Profit Participation Percentage | Status / Stage | Size (Acres) | Land Use | Acquisition Date | Purchase Price | Debt as of 9/30/2022 | Projected Completion Date | ||||||||||||||||||||

| Maple Farms | Sandy Point, Brazoria County, TX | 25.5 | % | 47.5% right to profits | Planning | 770 | TBD | 12/17/2021 | $ | 10,015,018 | $ | 3,000,000 | Long Term Hold | |||||||||||||||||

| Pecan Ranch West | Bonney, Brazoria County, TX | 100 | % | 100% | Planning | 74 | TBD | 11/15/2021 | $ | 1,596,000 | $ | 1,217,000 | Long Term Hold | |||||||||||||||||

| Pecan Ranch North | Bonney, Brazoria County, TX | 100 | % | 100% | Planning | 148 | TBD | 12/10/2021 | $ | 2,855,001 | $ | 2,855,000 | Long Term Hold | |||||||||||||||||

| Pecan Ranch Square | Bonney, Brazoria County, TX | 100 | % | 100% | Planning | 41 | Commercial | 12/10/2021 | $ | 917,277 | $ | 1,096,000 | Long Term Hold | |||||||||||||||||

| Maple Grove Square | Angleton, Brazoria County, TX | 100 | % | 100% | Planning | 15 | Commercial | 12/8/2021 | $ | 534,186.24 | $ | 662,000 | Long Term Hold | |||||||||||||||||

| Maple Reserve Square | Waller County, TX | 100 | % | 100% | Planning | 7 | Commercial | 7/5/2022 | $ | 260,454 | 260,454 | Long Term Hold | ||||||||||||||||||

3

Our Acquisition Pipeline

In addition to the twelve initial properties, as of the date of this prospectus, we have entered into purchase and sale agreements to acquire six additional properties from third parties, three of which have been terminated, and three of which are currently undergoing due diligence activities. While these purchase and sale agreements are binding, during the inspection period for each property we have the right to terminate the agreement for any reason. The estimated aggregate acquisition costs for these properties total approximately $15,949,393. The following table provides additional details regarding the six additional properties:

| Location | Size (Acres) |

Purchase Price | Purchaser | Date of Agreement | Inspection Period End Date | Projected Closing Date per Contract | ||||||||||

| Beasley, TX | 180 | $ | 6,300,000 | Manager | March 2022 | February 13, 2023 | March 13, 2023 | |||||||||

| Martindale, TX | 110.4 | $ | 4,021,200 | Manager | November 2021 | June 21, 2022 | Terminated | |||||||||

| San Antonio, TX | 173 | $ | 5,190,000 | Manager | February 2022 | July 14, 2022 | Terminated | |||||||||

| San Antonio, TX | 15 | $ | 1,501,550 | Manager | February 2022 | June 14, 2022 | Terminated | |||||||||

| Conroe, TX | 171 | $ | 6,000,000 | Maple X, Inc. | July 2022 | February 13, 2023 | March 13, 2023 | |||||||||

| Waller , TX | 103 | $ | 3,649,393 | Maple X Inc. | January 2023 | June 10, 2023 | June 25, 2023 | |||||||||

The two San Antonio property transactions and the Martindale property transaction have been terminated. The remaining three investments are under review, and we have not completed our due diligence. There can be no assurance that we will close these potential acquisition transactions. If we do not acquire these properties or projects, we will be out-of-pocket the earnest money deposits and the costs associated with our due diligence activities, which costs are not material.

Market Opportunity

Our activities are currently focused on the real estate market in the greater Houston metropolitan area.

In recent years, Texas has experienced positive migration inflows into the state, due in part to significant employment opportunities afforded by the gas and oil, construction, and service sectors. The energy industry is a core industry in the state’s economy, as Texas is the leading state in the US in the production of gas and oil (4.3% of gross oil production and 26% of the natural gas production), as well as a producer of wind energy (28% of wind energy production). Approximately 600,000 workers are employed in the energy sector in Texas. (Source: https://www.energy.gov/sites/default/files/2021-09/Texas%20Energy%20Sector%20Risk%20Profile.pdf).

In addition, the state of Texas is home to 49 Fortune 500 companies (Source: https://fortune.com), and, according to CNBC, in 2021 Texas was voted one of the 5 “Best States for Business” in the US (Source: https://www.cnbc.com/2021/07/13/americas-top-states-for-business.html). Although in 2020, in light of Covid-19, economic indices recorded a certain downturn, Texas recorded a recovery in 2021 as reflected by an increase in the GDP growth rate (3.7% as of the end of the third quarter of 2021) (Source: U.S. Bureau of Economic Analysis (BEA), https://www.bea.gov/), as well as a decline in the unemployment rate, which was approximately 5% as of the end of 2021, compared to 7.2% in the same period during 2020 (Source: https://www.bls.gov/regions/southwest/texas.htm#eag).

Accordingly, the real estate market in Texas has recorded significant growth in recent years, as reflected by the volume of sale transactions of residential real estate. In 2020, despite Covid-19, approximately 393,618 residential properties were sold (a figure slightly higher than said figure in 2019, pre-Covid-19), and as of the third quarter of 2021, the number of properties sold in Texas was approximately 313,508, compared to approximately 290,000 properties sold in the same period of 2020 (representing an increase of approximately 8%). The median price in such transactions increased by approximately 16.9%, to approximately US$310,000 (Source: https://www.texasrealestate.com/market-research/quarterly-housing-report/). As of November 2021, the housing price index in Texas has increased by 18.6%, as compared with the same period in 2020 (Source: https://www.recenter.tamu.edu/articles/technical-report/Texas-Housing-Insight).

Despite the recent positive migration inflows into the state, given the large territory of Texas, the population density is low, at approximately 105.2 people per square mile (26th among US states in terms of density). This fact, combined with the topographic characteristics of the state (most of which is flat), suggest a widespread supply of land in the state suitable for construction. To meet the demand for residential real estate in Texas, over the last several years the number of permits for the construction of single-family properties in the state has increased each year, with approximately 167,699 construction permits for single-family properties being issued in 2021, as compared to approximately 159,066 in 2020 (Source: https://www.recenter.tamu.edu/data/building-permits/#!/state/Texas).

The Houston metropolitan area is the largest city in the State of Texas and the fourth largest city in the US. The city itself has a population of approximately 2.3 million people, while the population of the metropolitan area is estimated to be approximately 7 million people. Over the last decade, an increase of approximately 20% was recorded in the population of the metropolitan area (Source: https://issuu.com/zondaevents/docs/2022_tx_belfiore_report_proof1), while 2021 alone recorded a growth of approximately 1.24%. (Source: https://worldpopulationreview.com/us-cities/houston-tx-population).

4

The Houston metropolitan area is enjoying high employment rates. In 2021, the unemployment rate in the city was approximately 4.8%, and approximately 151,800 jobs were added in the metropolitan area, a figure reflecting an increase of 5.1% as compared with 2020 (Source: https://www.bls.gov/regions/southwest/tx_houston_msa.htm#eag).

Concurrently with the population growth and the high employment rate in the Houston metropolitan area, the real estate sector has also been characterized by ongoing growth and development. A combination of increased demand for housing and a lack of supply has led to a reduced average time to sell a house (from 48 days to 39 days) as of 2021, as well as an increase of approximately 9.3% in the number of acquisition transactions of residential units in the metropolitan area during January 2022, as compared with the same period in 2021 (an increase of approximately 61.2% as compared with January 2017). The increase in the demand for housing is also reflected in the increase in the median price of single-family homes, which as of January 2022 was approximately US$310,000 per unit (an increase of approximately 41.6% over the past five years) (Source: https://www.houston.org/houston-data/monthly-update-home-sales), and in the increase in the number of permits provided for the construction of single-family properties (approximately 3,887 construction permits provided in November 2021). In this regard, among Texas districts, the Houston metropolitan area was ranked at the top of the list of localities providing permits for the construction of single-family properties (Source: https://www.recenter.tamu.edu/articles/technical-report/Texas-Housing-Insight among Texas districts).

Summary Risk Factors

An investment in shares of our common stock involves a high degree of risk. If any of the factors enumerated below or in the section entitled “Risk Factors” occurs, our business, financial condition, liquidity, results of operations and prospects could be materially and adversely affected. In that case, the market price of our common stock could decline, and you may lose some or all of your investment. Some of the more significant risks relating to this offering and an investment in our common stock include:

| ● | our ability to consummate the formation transactions; |

| ● | our lack of prior operating history; |

| ● | our ability to consummate the acquisition and development of our properties in the time frame, on the terms, or in the manner we currently anticipate; |

| ● | the impact of development and construction delays and cost overruns; |

| ● | the risks related to the illiquidity of real estate investments; |

| ● | the impact of potential declines in real estate valuations and impairment charges; |

| ● | our exposure to adverse economic or regulatory developments in the municipalities in which our properties are located; |

| ● | the impact of pandemics such as the recent outbreak of novel coronavirus (“COVID-19”) or other sudden or unforeseen events that disrupt the economy; |

| ● | our ability to properly value our investments; |

| ● | the impact on our business from delays in our locating suitable investments; |

| ● | the impact of competition for a limited supply of properties for us to acquire and/or develop; |

| ● | the impact of potential conflicts of interest between us and our Manager and their affiliates; |

| ● | our ability to make distributions to our stockholders; and |

| ● | the lack of a public market for shares of our common stock. |

Our Formation and Operating Structure

We were formed as a Texas limited liability corporation on October 14, 2021. On March 21, 2022, we filed a certificate of conversion with the Texas Secretary of State to convert the Company from a LLC into a Texas corporation. As part of the conversion from a LLC to an Inc., the membership interests of our Controlling Shareholders in the LLC were converted into an aggregate of 100 shares of common stock in the incorporated company.

We commenced our activities in the fourth quarter of 2021 by acquiring eight properties located in the greater Houston metropolitan area. In January 2022, we obtained from the Controlling Shareholders the Controlling Shareholders’ 50% interest in Maple Heights GP, LLC, a Delaware limited liability company that has a 10% ownership interest in the Maple Heights property.

5

Prior to or in connection with this offering, we will engage in certain formation transactions intended to establish our operating and capital structure.

| ● | We will enter into a management agreement with our Manager. |

| ● | We will amend and restate our certificate of formation and our bylaws. |

| ● | We will issue shares of our common stock to our Controlling Shareholders to reflect an aggregate 75% ownership interest in the Company (post-offering). |

| ● | We intend to issue shares of our common stock in this offering. |

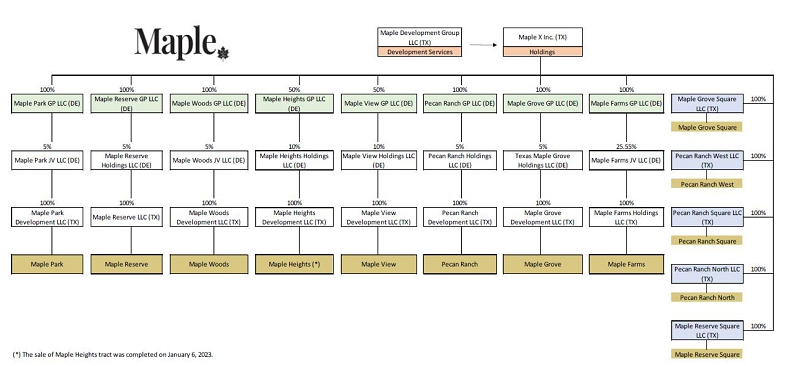

Upon completion of the formation transactions, substantially all of our operations will be conducted through our Manager, and all of our assets will be held by single purpose entities, typically a LLC or a LP, established by the Company for each project which hold, directly or indirectly, the title in each property (each a “Property Company”).

Our interests in our Property Companies will generally entitle us to share in cash distributions from, and in the profits and losses of, our Property Companies, in accordance with the terms of each Property Company’s operating agreement. See the section of this prospectus entitled “Operating Agreements” for more detail on the distribution of profits.

The following diagram illustrates our organizational structure:

Owned Properties Diagram

Our Financing Strategy

We are undertaking this offering to become a publicly traded company in order to provide us with substantial access to capital and capital flexibility as we pursue our business plan.

We do not currently expect to use permanent, company-level debt. We finance our activities by having our subsidiary companies raise capital in equity investment transactions and obtain acquisition loans and development loans to acquire and develop the properties.

See the section of this prospectus entitled “Our Financing” for more detail on how we finance our business activities.

We may engage in other forms of capital raising available to other public real estate companies such as conducting offerings of common equity.

6

Our Management Agreement

Upon completion of this offering and the formation transactions, we will enter into a management agreement with our Manager. Pursuant to this agreement, our Manager will manage the day-to-day operations of our company in accordance with our investment guidelines, which may be modified or supplemented by our board of directors from time to time.

The following is a summary of the fees and expense reimbursements that we will pay to our Manager.

Manager Compensation

Our Manager will be entitled to the following fees:

| ● | An annual fee equal to 1% of the net asset value (NAV) of the Company’s properties, to be paid by us. |

| ● | A development fee equal to 5% of the development costs of each of our properties, to be paid monthly by the applicable Property Company. The development fee is paid monthly in equal monthly installments in accordance with the business plan for the particular project, with a true-up upon project completion. |

| ● | In addition, the Company will reimburse the Manager for reasonable business expenses. |

| ● | The Company will pay the insurance premiums for insurance for the Manager. |

We estimate that the approximate, aggregate maximum fees to be paid to our Manager in 2022 for asset management, marketing, and other administrative services and related out-of-pocket and other reimbursements (assuming that the we do not acquire any additional properties or projects) will total $1,025,600.

Our Tax Status

We have elected to be treated as a corporation for U.S. federal income tax purposes. We will be subject to certain U.S. federal, state and local taxes on our income and property. See “U.S. Federal Income Tax Considerations”.

Our Distribution Policy

As of the date of this registration statement, the Company has not adopted a dividend distribution policy, and since its incorporation in 2021, the Company has not distributed any dividends.

Any distributions we make will be at the sole discretion of our board of directors and will depend upon a number of factors, including our actual and projected financial condition, liquidity, results of operations, cash flow generated by our operations, operating expenses, debt service requirements, capital expenditure requirements, prohibitions and other limitations under our financing arrangements, our taxable income, restrictions on making distributions under applicable law, and such other factors as our board of directors deems relevant.

We anticipate that our distributions generally will be taxable as ordinary income to our stockholders, although a portion of the distributions may constitute a return of capital or may be designated by us as qualified dividend income or capital gain.

For so long as the Company’s securities are traded on the TASE and an applicable exemption under the Israeli Securities Law does not apply, pursuant to our charter, distributions of dividends by us to our stockholders will be made in accordance with Texas law and the requirements of the Israeli Companies Law and the regulations promulgated thereunder applicable to the distribution of dividends.

Emerging Growth Company Status

We are an “emerging growth company”, as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies”, including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We have not yet made a decision as to whether we will take advantage of any or all of these exemptions in the future. If we do take advantage of any of these exemptions, we do not know if some investors will find our common stock less attractive as a result, which may result in a less active trading market for our common stock and more volatility in our share price.

7

In addition, the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies.

We will remain an “emerging growth company” until the earliest to occur of (i) the last day of the fiscal year during which our total annual revenue equals or exceeds $1.07 billion (subject to adjustment for inflation), (ii) the last day of the fiscal year following the fifth anniversary of this offering, (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

Smaller Reporting Company

We also qualify as a “smaller reporting company” under Rule 12b-2 of the Exchange Act, which is defined as a company with a public equity float of less than $250 million. To the extent that we remain a smaller reporting company at such time as we are no longer an emerging growth company, we will still have reduced disclosure requirements for our public filings, some of which are similar to those of an emerging growth company, including not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act and the reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements.

Our Corporate Information

We were originally incorporated as a Texas LLC in 2021. In March 2022, the Company became a Texas corporation. Our principal executive offices are located at 5847 San Felipe Street, Suite 4675, Houston, TX 77057. Our telephone number is 832-804-9680. We do not currently have a website, but we will establish one upon the closing of this offering. Information contained on, or accessible through, our website is not incorporated by reference into and does not constitute a part of this prospectus or any other reports or documents we file with or furnish to the Securities and Exchange Commission (the “SEC”). Any reference to our website in this prospectus is an inactive textual reference only. Any other website references (URL’s) in this Registration Statement are also inactive textual references only and are not active hyperlinks. The contents of our website is not part of this prospectus, and you should not consider the contents of our website in making an investment decision with respect to our common shares.

8

The Offering

| Common stock offered by us | shares of common stock | |

| Common stock to be outstanding after this offering | Shares (1) | |

| Use of proceeds | Assuming we sell all of the shares of common stock offered in this offering at an offering price per share of ILS (approximately $ as of , 2022), which is the Offering Price set forth on the cover of this prospectus, we estimate that the net proceeds to us from this offering will be approximately $ million, after deducting underwriting and/or distribution commissions and other estimated expenses payable by us. We may use up to $ of the net proceeds from this offering to develop or redevelop other properties, which may include properties in our acquisition pipeline, and for general corporate and working capital purposes. See “Use of Proceeds.” | |

| Listing | We intend to apply to list our common stock on the TASE under the symbol “ ”. Our common stock will not be listed on a national securities exchange in the United States. | |

| Risk factors | Investing in our common stock involves risks. You should carefully read and consider the information set forth under “Risk Factors” beginning on page 12 of this prospectus and all other information in this prospectus before making a decision to invest in our common stock. |

| (1) | Includes shares of our common stock to be issued in this offering. |

9

Summary Selected Historical and Pro-Forma Financial Information

Set forth below is summary selected financial information and other data presented on (i) a historical basis for our Company and its subsidiaries, and (ii) a pro forma basis for our Company after giving effect to the completion of the formation transactions and the other adjustments described in the unaudited pro forma condensed combined consolidated financial statements beginning on page F-42 of the prospectus.

The Company’s initial portfolio is comprised of a total of nine properties. For more information regarding the formation transactions, please see “Structure and Formation of Our Company.”

The Company’s historical combined balance sheet data as of December 31, 2021, and historical combined operating data for the year ended December 31, 2021, have been derived from the Company’s audited historical combined financial statements included elsewhere in this prospectus. The historical combined financial data included below and set forth elsewhere in this prospectus are not necessarily indicative of our future performance. Our pro forma financial information is not necessarily indicative of what our actual financial position and results of operations would have been had the formation transactions and other adjustments described occurred as of the date and for the period indicated, nor does it purport to represent our future financial position or results of operations.

You should read the following summary selected historical and pro-forma financial and other data together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business and Properties” and the historical and pro forma financial statements and related notes appearing elsewhere in this prospectus.

Operating Data (U.S. dollars in thousands):

| As of December 31, 2021 | As of Sept. 30, 2022 | |||||||||||||||

| Maple X Inc. (Audited) | Maple Heights GP (Audited) | Pro Forma (Unaudited) | Maple X Inc. (Unaudited) | |||||||||||||

| Revenues | - | 4,978 | 4,978 | 10,830 | ||||||||||||

| Cost of revenues | - | (3,951 | ) | (3,951 | ) | (6,278 | ) | |||||||||

| Gross profit | - | 1,027 | 1,027 | 4,552 | ||||||||||||

| General and administrative expenses | (5 | ) | (12 | ) | (17 | ) | (1,147 | ) | ||||||||

| Operating loss | (5 | ) | 1,015 | 1,010 | 3,405 | |||||||||||

| Financing expenses, net | (22 | ) | (104 | ) | (126 | ) | (597 | ) | ||||||||

| Net income (loss) | (27 | ) | 911 | 884 | 2,808 | |||||||||||

10

Balance Sheet Data (U.S. dollars in thousands):

| As of December 31, 2021 | As of Sept. 30, 2022 | |||||||||||||||

| Maple X Inc. (Audited) | Maple Heights GP (Audited) | Pro Forma (Unaudited) | Maple X Inc. (Unaudited) | |||||||||||||

| A s s e t s | ||||||||||||||||

| Current Assets | ||||||||||||||||

| Cash and cash equivalents | 2,125 | 417 | 2,542 | 4,549 | ||||||||||||

| Restricted cash | 912 | 98 | 1,010 | 466 | ||||||||||||

| Prepaid expenses and other assets | 50 | - | 50 | 490 | ||||||||||||

| Land inventory | 17,072 | 9,214 | 26,286 | 40,989 | ||||||||||||

| T o t a l Current assets | 20,159 | 9,729 | 29,888 | 46,494 | ||||||||||||

| Non-current Assets | ||||||||||||||||

| Real estate properties | 16,266 | - | 16,266 | 16,969 | ||||||||||||

| T o t a l non-current assets | 16,266 | - | 16,266 | 16,969 | ||||||||||||

| T o t a l assets | 36,425 | 9,729 | 46,154 | 63,463 | ||||||||||||

| Liabilities and Shareholders’ Equity | ||||||||||||||||

| Current Liabilities | ||||||||||||||||

| Current liabilities - Mortgage and other loans | 9,962 | 3,468 | 13,430 | 25,391 | ||||||||||||

| Current liabilities - Loans from related parties | 1,488 | - | 1,488 | 1,210 | ||||||||||||

| Other current liabilities | 314 | 12 | 326 | 1,015 | ||||||||||||

| T o t a l current liabilities | 11,764 | 3,480 | 15,244 | 27,616 | ||||||||||||

| Non-current Liabilities | ||||||||||||||||

| Loans from related parties | 4,227 | - | 4,227 | 4,315 | ||||||||||||

| T o t a l non-current liabilities | 4,227 | - | 4,227 | 2,721 | ||||||||||||

| 7,036 | ||||||||||||||||

| T o t a l liabilities | 15,991 | 3,480 | 19,471 | |||||||||||||

| 34,652 | ||||||||||||||||

| Shareholders’ Equity | (27 | ) | 322 | 295 | ||||||||||||

| Non-controlling interests | 20,461 | 5,927 | 26,388 | (1,278 | ) | |||||||||||

| Total Shareholders’ Equity | 20,434 | 6,249 | 26,683 | 30,089 | ||||||||||||

| T o t a l liabilities and stockholders’ equity | 36,425 | 9,729 | 46,154 | 28,811 | ||||||||||||

11

RISK FACTORS

Investing in our common stock involves risks. Before you invest in our common stock, you should carefully consider the risk factors below together with all of the other information included in this prospectus. If any of the risks discussed in this prospectus were to occur, our business, financial condition, liquidity, cash flows, results of operations and prospects and our ability to service our debt and make distributions to our stockholders could be materially and adversely affected (which we refer to collectively as “materially and adversely affecting us” or having “a material adverse effect on us” and comparable phrases), the market price of our common stock could decline significantly, and you could lose all or part of your investment in our common stock. Some statements in this prospectus, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section in this prospectus entitled “Special Note Regarding Forward-Looking Statements.”

Risks Related to Our Business and Properties

We barely have an operating history, and the prior performance of our Company and Maple Heights GP, LLC may not be indicative of our future results.

We are a recently formed company and barely have an operating history. We currently have an ownership interest in twelve properties. Even though our Controlling Shareholders, our Manager, and Maple Heights GP, LLC have substantial experience in real estate investments, you should not assume that our performance will be similar to the past performance of other real estate investment opportunities sourced by these individuals or companies. Our lack of an operating history significantly increases the risk and uncertainty you face in making an investment in our common stock.

The illiquidity of real estate investments could significantly impede our ability to respond to changing economic, financial, and investment conditions or changes in the operating performance of our properties, which could adversely affect our business, financial condition, results of operations and cash flows.

Real estate investments are relatively illiquid and this lack of liquidity may limit our ability to react promptly to changes in the economy or other conditions. Significant expenditures associated with real estate investments, such as secured mortgage payments, real estate taxes, insurance and maintenance costs, are generally not reduced when circumstances cause a reduction in the value of the property. As a result of the illiquidity of the real estate investments, we may not be able to sell a property or properties quickly or on favorable terms in response to changing economic, financial and investment conditions or changes in the property’s operating performance when it otherwise may be prudent to do so. We cannot predict whether we will be able to sell any property we desire to sell for the price or on the terms set by us or whether any price or other terms offered by a prospective purchaser would be acceptable to us. We also cannot predict the length of time needed to find a willing purchaser and to close the sale of a property. We may be required to expend funds to correct defects or to make improvements before a property can be sold, and we cannot provide any assurances that we will have funds available to correct such defects or to make such improvements. Our inability to dispose of assets at opportune times or on favorable terms could materially and adversely affect our business, financial condition, results of operations and cash flows. In addition, properties that we own may be subject to takings or eminent domain by the government, which could adversely affect our business, financial condition, results of operations and our ability to make distributions on, and the value of, our common stock.

In addition, our ability to dispose of properties could be constrained by their tax attributes. Properties which we own for a significant period of time may have low tax bases. If we dispose of these properties outright in taxable transactions, we may be required to pay tax on that gain, which, in turn, would impact our cash flow and increase our leverage. To dispose of low basis properties efficiently, we may from time to time use like-kind exchanges, which qualify for non-recognition of taxable gain, but can be difficult to consummate and result in the property for which the disposed assets are exchanged inheriting their low tax bases and other tax attributes.

Our long-term growth depends in part on successfully identifying and consummating acquisitions of additional properties and the failure to make such acquisitions could materially impede our growth.

We intend to continue to develop and acquire properties from time to time consistent with our investment strategy as long as we believe such properties offer an attractive total return opportunity, even if real estate markets are not as favorable as they have been in the recent past. Except for the properties in our initial portfolio, you will have no prior opportunity to evaluate the economic merits or the terms of our investments before making a decision to invest in our common stock. We can provide no assurances that we will be successful in identifying attractive properties or that, once identified, we will be successful in consummating an acquisition.

We expect to finance future acquisitions through a combination of the use of retained cash flows, bank loan borrowings and offerings of equity and debt securities, which may not be available on advantageous terms, or at all. We may also acquire properties in exchange for partnership interests in our subsidiary partnerships. We may spend significant time and money on potential acquisitions, including those that we do not consummate. Any delay or failure on our part to identify, negotiate, finance on favorable terms, consummate and integrate such acquisitions could materially impede our growth. If we are unsuccessful in locating suitable investments, other than the properties in our initial portfolio, we may ultimately decide to liquidate. In the event we are unable to timely locate suitable investments, we may be unable or limited in our ability to make distributions on our common stock and we may not be able to meet our business objectives.

12

Potential declines in real estate valuations and impairment charges could materially and adversely affect our business, financial condition and results of operations.

We will continuously monitor events and changes in circumstances, including those resulting from an economic downturn that could indicate that the carrying value of the real estate and related intangible assets in which we have an ownership interest may not be recoverable. Examples of such indicators may include a significant decrease in market price, a significant adverse change in the extent or manner the property is being used or in its physical condition, an accumulation of costs significantly in excess of the amount originally expected for the acquisition or development or a history of operating or cash flow losses. When such impairment indicators exist, we review an estimate of the future undiscounted net cash flows (excluding interest charges) expected to result from the real estate investment’s use and eventual disposition and compare it to the carrying value of the property. We consider factors such as future operating income, trends and prospects, leasing demand, competition and other factors. If our future undiscounted net cash flow evaluation indicates that we are unable to recover the carrying value of a real estate investment, an impairment loss is recorded to the extent that the carrying value exceeds the estimated fair value of the property. These losses have a direct impact on our net income because recording an impairment loss results in an immediate negative adjustment to net income. The evaluation of anticipated cash flows is highly subjective and is based on numerous assumptions, including future operating income and property operating expenses and capital requirements that could differ materially from actual results in future periods. A worsening real estate market may cause us to re-evaluate the assumptions used in our impairment analysis. Impairment charges could adversely affect our business, financial condition, results of operations and our ability to make distributions on, and the value of, our common stock.

Projections of expected future cash flows require management to make assumptions to estimate future operating income, property operating expenses and the number of years the property is held for investment, among other factors. The subjectivity of assumptions used in the future cash flow analysis, including discount and capitalization rates, could result in an incorrect assessment of the property’s fair value and, therefore, could result in the misstatement of the carrying value of our related intangible assets on our balance sheet and our results of operations. Adverse market and economic conditions and market volatility will likely make it difficult to value the future properties owned by us, as well as the value of our intangible assets. As a result of adverse market and economic conditions and market volatility, there may be significant uncertainty in the valuation, or in the stability of, the cash flows, discount rates and other factors related to such assets that could result in a substantial decrease in their value.

Adverse economic or regulatory developments in the municipalities and states in which we are invested could negatively affect our business, results of operations and financial condition, and ability to make distributions on our common stock.

Our business is dependent on the condition of the economy in the municipalities and states in which we are invested. Following the completion of the formation transactions and this offering, the nine properties in our initial portfolio will be located in the Houston, Texas greater metropolitan area. This concentration may expose us to greater economic risks than if we owned a more geographically diverse portfolio. We will be susceptible to adverse developments in the economic and regulatory environments of the municipalities in which we are invested (such as business layoffs or downsizing, industry slowdowns, relocations of businesses, rent control, variations in AMI, social unrest, increases in real estate and other taxes, costs of complying with governmental regulations or increased regulation). In addition, we will be subject to similar localized economic conditions with respect to our future investments. Such adverse developments could materially reduce the value of our real estate portfolio, and thus adversely affect our business, financial condition, results of operations, and our ability to make distributions on, and the value of, our common stock.

If we overestimate the value or income-producing ability or incorrectly price the risks of our investments, we may experience losses.

Analysis of the value or income-producing ability of the properties in our initial portfolio or any property we may acquire in the future is highly subjective and may be subject to error. Our Manager will value our potential investments based on yields and risks, taking into account estimated future losses on select commercial real estate equity investments, and the estimated impact of these losses on expected future cash flows and returns. In the event that we underestimate the risks relative to the price we pay for a particular investment, we may experience losses with respect to such investment.

Rent control and other changes in similar laws as well as variations in area median income (AMI) could adversely affect our operations.

The value of our properties may be adversely affected by changes in (i) rent control or rent stabilization laws or other similar residential landlord/tenant laws, or (ii) variations in AMI. Such changes could limit our ability to sell our properties to homebuilders. Depending on the nature of such laws or regulations or variations in AMI and the number of projects that become subject to any such resulting restrictions on rent increases, our revenues and net income could be adversely affected.

13

We may suffer from delays in locating suitable investments, which could limit our ability to make distributions on our common stock and lower the overall return on your investment.

We will rely upon our Manager’s real estate professionals to identify suitable investments. To the extent that our Manager’s real estate professionals face competing demands upon their time in instances when we have capital ready for investment, we may face delays in execution. Additionally, the current market for properties that meet our investment objectives is often competitive. Except for the properties in our initial portfolio, you will have no prior opportunity to evaluate the terms of transactions or other economic or financial data concerning our future investments. You must rely entirely on the oversight and management ability of our Manager. We cannot be sure that our Manager will be successful in obtaining suitable investments on financially attractive terms. Furthermore, since we plan to acquire properties prior to the start of the development process, it will typically take several months to complete development and sell the properties to homebuilders and commercial contractors. Therefore, you may suffer delays in the receipt of distributions on our common stock attributable to those particular properties.

There may be a limited supply of undeveloped property assets for us to acquire and/or develop in our existing or target markets, and we will have to compete for opportunities with companies that are larger and have more resources than we do.

We intend to focus our acquisition and development efforts primarily on properties in attractive U.S. urban and suburban markets. As a result of our strategic focus on these locations and assets, there may be a limited supply of existing properties or vacant land that matches our selection criteria. We will have significant competition with respect to our acquisition of properties and other investments with many other companies, including REITs, insurance companies, commercial banks, private investment funds, hedge funds, specialty finance companies, online investment platforms and other investors, many of which may have greater resources and name recognition than us. Consequently, we may not be able to compete successfully for investments. When we enter new markets or expand in markets where we and our Manager have only a limited presence and limited experience, we face competition from local real estate developers and market participants who may have more established local knowledge and relationships than we do. Such competition is significant, and our failure to successfully compete for the limited supply of properties or locations that match our selection criteria could materially and adversely affect our ability to grow.

In addition, the number of entities and the amount of funds competing for suitable investments may increase. If we acquire properties and other investments at higher prices than our competitors and/or by using less-than-ideal capital structures, our returns will be lower and the value of our assets may not increase or may decrease significantly below the amount we paid for such assets. If such events occur, you may experience a lower return on your investment in our common stock.

Furthermore, there may be changes in laws or regulations, or the interpretation thereof, impacting the availability or value of federal or state tax credits and other development incentives. Any decrease in the supply of these designated properties or the availability of tax credits or other development incentives, or any decrease in the investment value of tax credits or incentives, could further limit the availability or appeal of properties or locations in our target markets, which could materially and adversely affect our ability to grow, or cause us to alter our current strategy.

Our assets will be subject to the risks typically associated with real estate investments.

Our assets will be subject to the risks typically associated with real estate investments. The value of real estate may be adversely affected by a number of risks, including:

| ● | natural disasters such as hurricanes, earthquakes and floods; |

| ● | acts of war or terrorism, including the consequences of terrorist attacks, such as those that occurred on September 11, 2001; |

| ● | adverse changes in national and local economic and real estate conditions |

| ● | the impact of pandemics such as the recent outbreak of COVID-19 or other sudden or unforeseen events that disrupt the economy; |

14

| ● | an oversupply of (or a reduction in demand for) space in the areas where particular properties are located and the attractiveness of particular properties to prospective homebuilders and commercial contractors; |

| ● | changes in governmental laws and regulations, fiscal policies, and zoning ordinances and the related costs of compliance and the potential for liability under applicable laws; |

| ● | costs of remediation and liabilities associated with environmental conditions affecting properties; and |

| ● | the potential for uninsured or underinsured property losses. |

The value of real estate properties is typically affected significantly by their ability to generate cash flow and net income, which in turn depends on the potential amount of rental or other income that can be generated net of expenses required to be incurred with respect to the property. Many expenditures associated with properties (such as operating expenses and capital expenditures) cannot be reduced when there is a reduction in income from the properties. These factors may have a material adverse effect on the value that we can realize from our assets and our business, financial condition and results of operations, and on our ability to make distributions on, and the value of, our common stock could be adversely affected.

Actual or threatened epidemics, pandemics, outbreaks, or other public health crises may have an adverse impact on the profitability of the properties in our portfolio.

Our business could be materially and adversely affected by the risks, or the public perception of the risks, related to an epidemic, pandemic, outbreak, or other public health crisis, such as the recent outbreak of COVID-19. As a result of shutdowns, quarantines, actual viral health issues or loss of employment, we may be hindered in the operation of our business. In addition, we may incur costs in protecting our investment and completing development of our properties. Additionally, local and national authorities may expand or extend certain measures imposing restrictions on our ability to enforce contractual obligations. Local and national authorities may also reduce or discontinue stimulus and relief programs, implemented in response to such events, which may be providing benefits to our business partners and purchasers of our properties which may impact their ability to make their payments. Due to the COVID-19 pandemic, we have also incurred, and we may in the future as a result of COVID-19 or other epidemics, pandemics, outbreaks or other public health crises incur, an increase in operating expenses related to cleaning and sanitization supplies and temporary increases in our labor costs. In addition, our ability to complete the ground-up development or refurbishment of the properties in our initial portfolio may be inhibited due to social distancing or other restrictions implemented in response to such events. Restrictions inhibiting our employees’ ability to meet with existing and potential business partners and homebuilders may in the future further disrupt our ability to implement our business plan which could adversely impact our business. We may also face an increased risk of cyber attacks due to an increased reliance on remote working as a result of an epidemic, pandemic, outbreak or other public health crisis. In addition, the deterioration of global economic conditions and increases in unemployment as a result of an epidemic, pandemic, outbreak or other public health crisis may ultimately decrease pricing across our portfolio as potential homebuilders and commercial contractors reduce the scope of their activities.

Epidemics, pandemics, outbreaks or other public health crises have caused, and may cause in the future, severe economic, market and other disruptions worldwide. Market fluctuations may affect our ability to obtain necessary funds for our operations from lenders. In addition, we may be unable to obtain financing for the acquisition of investments on satisfactory terms, or at all.

The ultimate extent of the impact of any epidemic, pandemic, outbreak or other public health crisis, including the COVID-19 pandemic, on our business, financial condition and results of operations will depend on future developments, which are highly uncertain, and cannot be predicted, including new information that may emerge concerning the severity of such epidemic, pandemic, outbreak or other public health crisis and actions taken to contain or prevent their further spread, among others. These and other potential impacts of an epidemic, pandemic, outbreak or other public health crisis, such as the COVID-19 pandemic, could therefore materially and adversely affect our business, financial condition and results of operations.

15

Design, development, and construction risks could adversely impact our profitability.

We intend to acquire, invest in, and develop a portfolio of residential and commercial real estate properties. These activities may expose us to a number of risks that may increase our construction costs and decrease our profitability, including the following:

| ● | construction delays or cost overruns; |

| ● | problems with the construction companies we hire to develop our properties and with their subcontractors, including delays in performance, defective performance, failure to perform and contract disputes, including disputes regarding change orders; |

| ● | increased labor costs, labor shortages or labor disruptions; |

| ● | increased construction commodity prices, particularly lumber, steel and concrete; |

| ● | costs to address or remediate unforeseen or concealed structural deficiencies, termite damage or damage from other pests, environmental, health or safety hazards and other unanticipated problems not contemplated in a project’s budget; |

| ● | inability to obtain, or delays in obtaining, necessary zoning, land-use, building, licenses, and other required permits, authorizations, inspections and approvals; |

| ● | opposition from local community or political groups; |

| ● | damage or alleged damage to adjacent property owners; |

| ● | health and safety incidents, site accidents and structural failures, which may cause significant property damage, personal injury, or loss of life; |

| ● | other difficulties related to construction in urban areas such as the need for heightened security measures, higher crime rates, vagrancy, parking and access constraints, protests, civil unrest, interruptions or failure of utilities; |

| ● | difficulties complying with complex building codes and other local regulations; and |

| ● | incurrence of costs related to the abandonment of development opportunities we pursue and subsequently deem unfeasible. |

Our inability to successfully implement our development, redevelopment, architecture and design and construction strategy could adversely affect our results of operations and our ability to satisfy our financial obligations.

Ongoing requirements for capital improvements may reduce our profitability and adversely impact our liquidity.

Acquisitions and development of properties require significant capital expenditures, and properties that we acquire may need significant development and capital improvements at the time of acquisition or later. All of our properties require capital expenditures for development and upgrades to remain competitive. We will have ongoing needs for development and capital improvements with respect to the properties that we own. We may need to make developments and capital improvements to comply with applicable laws and regulations, to remain competitive with other properties and to maintain the economic value of our properties.

We may also undertake other developments, expansions or additions of new features at our existing properties that involve significant capital expenditures. We may not be able to fund developments and capital improvements solely from cash provided from our operating activities. Consequently, we will rely upon the availability of debt or equity capital to fund developments and improvements. Consequently, our ability maximize the value of our portfolio may be limited if we cannot obtain satisfactory debt or equity financing, which will depend on market conditions and our future performance. The costs of development and capital improvements we are required or choose to make could reduce the funds available for other purposes and may reduce our profitability and adversely impact our liquidity.

16

Many real estate costs are fixed, even if the value of our properties in the initial portfolio or any properties we acquire in the future decreases.

Many real estate costs, such as real estate taxes, insurance premiums, and maintenance costs, are not reduced when a property is not occupied, or other circumstances cause a reduction in property values. Even though our properties are not fully developed, we will still be obligated to pay real estate taxes, insurance premiums, and maintenance costs. In addition, any property we acquire in the future will not produce revenues immediately, and any such property’s operating cash flow may be insufficient to pay the operating expenses and, if financed with debt, the debt service associated with these new properties. If we are unable to offset real estate costs with sufficient revenues from our operations, our business, financial condition and results of operations and our ability to make distributions on, and the value of, our common stock.

Increased competition and increased affordability of apartment homes could limit our ability to sell the properties we may acquire or develop.

The undeveloped properties that we plan on developing for residential use in our initial portfolio and any additional undeveloped properties we may acquire or develop will compete with numerous alternatives in attracting homebuilders and commercial contractors, including other developed properties. Competitive housing and commercial space in a particular area and an increase in the affordability of owner occupied single and multifamily homes and commercial space due to, among other things, declining housing and commercial rental prices, oversupply, mortgage interest rates and tax incentives and government programs to promote home ownership, could adversely affect our ability to sell our properties to homebuilders and commercial contractors.

Actions of any joint venture partners that we may have in the future could reduce the returns on joint venture investments.

We may enter into joint ventures to acquire properties and other assets. We may also develop other properties we may acquire in the future in joint ventures or in partnerships, or other co-ownership arrangements. Such investments may involve risks not otherwise present with other methods of investment, including, for example, the following risks:

| ● | that our co-venturer or partner in an investment could become insolvent or bankrupt; |

| ● | that such co-venturer or partner may at any time have economic or business interests or goals that are or that become inconsistent with our business interests or goals; |

| ● | that such co-venturer or partner may be in a position to take action contrary to our instructions or requests or contrary to our policies or objectives; or |

| ● | that disputes between us and our co-venturer or partner may result in litigation or arbitration that would increase our expenses and prevent our officers and directors from focusing their time and effort on our operations. |

Any of the above might subject a property to liabilities in excess of those contemplated and adversely affect our business, financial condition and results of operations and our ability to make distributions on, and the value of, our common stock.

Our projects may encounter significant opposition from local community or political groups or unions, which may damage our goodwill and reputation and adversely affect our financial condition and results of operations.