Filed pursuant to Rule 424(b)(4)

Registration No. 333-265635

5,000,000 Ordinary Shares

![]()

Starbox Group Holdings Ltd.

This is an initial public offering of our ordinary shares, par value $0.001125 (“Ordinary Shares”). Prior to this offering, there has been no public market for our Ordinary Shares. The initial public offering price of our Ordinary Shares is $4.00 per share.

We have received the approval letter from Nasdaq to list our Ordinary Shares on the Nasdaq Capital Market under the symbol “STBX.”

Investing in our Ordinary Shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 8 to read about factors you should consider before buying our Ordinary Shares.

We are an “emerging growth company” as defined under the federal securities laws and will be subject to reduced public company reporting requirements. Please read the disclosures beginning on page 5 of this prospectus for more information.

| Per Share | Total

Without Over-Allotment Option | Total

With Over-Allotment Option | ||||||||||

| Initial public offering price | $ | 4.00 | $ | 20,000,000 | $ | 23,000,000 | ||||||

| Underwriters’ discounts(1) | $ | 0.28 | $ | 1,400,000 | $ | 1,610,000 | ||||||

| Proceeds to our company before expenses(2) | $ | 3.72 | $ | 18,600,000 | $ | 21,390,000 | ||||||

| (1) | Represents underwriting discounts equal to 7% per Ordinary Share. |

| (2) | In addition to the underwriting discounts listed above, we have agreed to issue, upon closing of this offering, warrants to Network 1 Financial Securities, Inc., as representative of the several underwriters (the “Representative”), exercisable after the date of issuance and for a five-year period after the date of commencement of sales of Ordinary Shares in this offering, entitling the representative to purchase 7% of the total number of Ordinary Shares sold in this offering (including any Ordinary Shares sold as a result of the exercise of the underwriters’ over-allotment option) at a per share price equal to 140% of the public offering price (the “Representative’s Warrants”). The registration statement of which this prospectus is a part also covers the Representative’s Warrants and the Ordinary Shares issuable upon the exercise thereof. See “Underwriting” for additional information regarding total underwriter compensation. |

This offering is being conducted on a firm commitment basis. The underwriters are obligated to take and pay for all of the Ordinary Shares if any such Ordinary Shares are taken. The underwriters expect to deliver the Ordinary Shares against payment in U.S. dollars in New York, New York on or about August 25, 2022.

Neither the Securities and Exchange Commission nor any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Prospectus dated August 22, 2022

TABLE OF CONTENTS

| i |

About this Prospectus

We and the underwriters have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the Ordinary Shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. For the avoidance of doubt, no offer or invitation to subscribe for Ordinary Shares is made to the public in the Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our business, financial condition, results of operations, and prospects may have changed since that date.

Conventions that Apply to this Prospectus

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “GETBATS website and mobile app” are to the GETBATS cash rebate website (www.getbats.com) and the GETBATS app operated by StarboxGB (defined below); | |

| ● | “Members” are to retail shoppers that have registered as a member on the GETBATS website and mobile app; | |

| ● | “Merchants” are to retail merchants (both online and offline) that have registered as a merchant on the GETBATS website and mobile app; | |

| ● | “MYR” are to the Malaysian ringgit, the legal currency of Malaysia; | |

| ● | “Nasdaq” are to the Nasdaq Stock Market LLC; | |

| ● | “Ordinary Shares” are to ordinary shares of Starbox Group (defined below), par value $0.001125 per share; | |

| ● | “Preferred Shares” are to preferred shares of Starbox Group, par value $0.001125 per share; | |

| ● | “SEC” are to the U.S. Securities and Exchange Commission; | |

| ● | “SEEBATS website and mobile app” are to the SEEBATS video streaming website (www.seebats.com) and the SEEBATS app operated by StarboxSB (defined below); | |

| ● | “Starbox Berhad” are to Starbox Holdings Berhad, a company limited by shares incorporated under the laws of Malaysia and a wholly owned subsidiary of Starbox Group; | |

| ● | “StarboxGB” are to Starbox Rebates Sdn. Bhd., a company limited by shares incorporated under the laws of Malaysia, which is a wholly owned subsidiary of Starbox Berhad; | |

| ● | “Starbox Group” are to Starbox Group Holdings Ltd., an exempted company limited by shares incorporated under the laws of the Cayman Islands; | |

| ● | “StarboxPB” are to Paybats Sdn. Bhd., a company limited by shares incorporated under the laws of Malaysia, which is a wholly owned subsidiary of Starbox Berhad; | |

| ● | “StarboxSB” are to StarboxTV Sdn. Bhd., a company limited by shares incorporated under the laws of Malaysia, which is a wholly owned subsidiary of Starbox Berhad; | |

| ● | “U.S. dollars,” “$,” and “dollars” are to the legal currency of the United States; and | |

| ● | “we,” “us,” “our,” “our Company,” or the “Company” are to one or more of Starbox Group and its subsidiaries, as the case may be. |

Unless the context indicates otherwise, all information in this prospectus assumes no exercise by the underwriters of their over-allotment option.

Starbox Berhad is a Malaysian holding company. Our business is conducted by our subsidiaries, StarboxPB, StarboxGB, and StarboxSB in Malaysia using MYR. Our consolidated financial statements are presented in U.S. dollars. In this prospectus, we refer to assets, obligations, commitments, and liabilities in our consolidated financial statements in U.S. dollars. These dollar references are based on the exchange rate of MYR to U.S. dollars, determined as of a specific date or for a specific period. Changes in the exchange rate will affect the amount of our obligations and the value of our assets in terms of U.S. dollars which may result in an increase or decrease in the amount of our obligations (expressed in dollars) and the value of our assets, including accounts receivable (expressed in dollars).

| ii |

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements included elsewhere in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks of investing in our Ordinary Shares, discussed under “Risk Factors,” before deciding whether to buy our Ordinary Shares.

Unless otherwise indicated, all share amounts and per share amounts in this prospectus have been presented giving effect to a reverse split of our Ordinary Shares and Preferred Shares at a ratio of 1-for-11.25 shares approved by our shareholders on June 8, 2022.

Overview

We are building a cash rebate, digital advertising, and payment solution business ecosystem targeting micro, small, and medium enterprises that lack the bandwidth to develop an in-house data management system for effective marketing. Through our subsidiaries in Malaysia, we connect retail merchants with retail shoppers to facilitate transactions through cash rebates offered by retail merchants, provide digital advertising services to advertisers, and provide payment solution services to merchants. Substantially all of our current operations are located in Malaysia.

Our cash rebate business is the foundation of the business ecosystem we are building. We have cooperated with retail merchants, which have registered on the GETBATS website and mobile app as “Merchants,” to offer cash rebates on their products or services, which have attracted retail shoppers to register on the GETBATS website and mobile app as “Members” in order to earn cash rebates for shopping online and offline. As the number of Members grows and sales of the existing Merchants increase, more retail merchants are willing to cooperate with us. As of March 31, 2022 and September 30, 2021 and 2020, the GETBATS website and mobile app had 613,509, 514,167, and 66,580 Members, respectively, and 799, 723, and 478 Merchants, respectively. During the six months ended March 31, 2022 and the fiscal years ended September 30, 2021 and 2020, we facilitated 188,718, 295,393, and 1,759 transactions through the GETBATS website and mobile app, respectively. We generate revenue by keeping an agreed-upon portion of the cash rebates offered by Merchants through the GETBATS website and mobile app.

Making use of the vast Member and Merchant data we have collected from the GETBATS website and mobile app, we help advertisers design, optimize, and distribute advertisements through online and digital channels. We primarily distribute advertisements through (i) our SEEBATS website and mobile app, on which viewers can watch movies and television series for free through over-the-top (“OTT”) streaming, which is a means of providing television and film content over the Internet at the request and to suit the requirements of the individual consumer, (ii) our GETBATS website and mobile app to its Members, and (iii) social media, mainly consisting of accounts of influencers and bloggers. During the six months ended March 31, 2022 and the fiscal years ended September 30, 2021 and 2020, we served 42, 25, and 2 advertisers, respectively. We generate revenue through service fees charged to the advertisers.

To diversify our revenue sources and supplement our cash rebates and digital advertising service businesses, we started to provide payment solution services to merchants in May 2021 by referring them to VE Services Sdn Bhd, a Malaysian Internet payment gateway company and a related-party entity controlled by one of our beneficial shareholders (“VE Services”). Pursuant to an appointment letter dated October 1, 2020 with VE Services (the “Appointment Letter”), we serve as its independent merchant recruitment and onboarding agent and refer merchants to VE Services for payment processing. We referred 14 and 11 merchants to VE Services during the six months ended March 31, 2022 and the fiscal year ended September 30, 2021, respectively. We generate insignificant revenue through commissions from VE Services for our referrals and such revenue has been reported as revenue from a related party in our consolidated financial statements.

For the six months ended March 31, 2022, we had total revenue of $2,922,413 and net income of $1,256,019. Revenue derived from digital advertising services, cash rebate services, and payment solution services accounted for approximately 99.63%, 0.19%, and 0.18% of our total revenue for the period, respectively.

For the fiscal years ended September 30, 2021 and 2020, we had total revenue of $3,166,228 and $153,863, respectively, and net income of $1,447,650 and a net loss of $205,154, respectively. Revenue derived from digital advertising services accounted for approximately 99.75% and 99.53% of our total revenue for those fiscal years, respectively. Revenue derived from cash rebate services accounted for approximately 0.20% and 0.47% of our total revenue for those fiscal years, respectively. Revenue derived from payment solution services accounted for approximately 0.05% and 0.00% of our total revenue for those fiscal years, respectively.

| 1 |

Competitive Strengths

We believe that the following competitive strengths have contributed to our success and differentiated us from our competitors:

| ● | business ecosystem comprising cash rebate, digital advertising, and payment solution services; | |

| ● | capability of providing targeted digital advertising services by leveraging our business data analysis technology; | |

| ● | solid advertiser base spanning a wide range of industries; and | |

| ● | visionary and experienced management team with strong technical and operational expertise. |

Growth Strategies

We intend to develop our business and strengthen brand loyalty by implementing the following strategies:

| ● | further expand our business scale and secure new advertisers; | |

| ● | further grow our Merchant and Member bases on the GETBATS website and mobile app; | |

| ● | continue to invest in and develop technologies relating to data analysis; and | |

| ● | expand our cash rebate and digital advertising services internationally. |

Summary of Risk Factors

Investing in our Ordinary Shares involves significant risks. You should carefully consider all of the information in this prospectus before making an investment in our Ordinary Shares. Below please find a summary of the principal risks we face, organized under relevant headings. These risks are discussed more fully in the section titled “Risk Factors.”

Risks Related to Our Business and Industry

Risks and uncertainties related to our business include, but are not limited to, the following:

| ● | if advertisers stop purchasing digital advertising services from us or decrease the amount they are willing to spend on marketing campaigns and promotional activities, or if we are unable to establish and maintain new relationships with advertisers, our business, financial condition, and results of operations could be materially adversely affected (see page 8 of this prospectus); | |

| ● | if we fail to retain and expand our Merchant and Member bases, our revenue and business will be harmed (see page 8 of this prospectus); | |

| ● | our limited operating history in rapidly evolving industries makes it difficult to accurately forecast our future operating results and evaluate our business prospects (see page 9 of this prospectus); | |

| ● | we have significantly unstable operating revenue, anticipate increases in our operating expenses in the future, and may not achieve or sustain profitability on a consistent basis. If we cannot achieve and sustain profitability, our business, financial condition, and operating results may be adversely affected (see page 10 of this prospectus); | |

| ● | the markets in which we operate are highly competitive, and we may not be able to compete successfully against existing or new competitors, which could reduce our market share and adversely affect our competitive position and financial performance (see page 10 of this prospectus); | |

| ● | our major clients generate a significant portion of our revenue. Any interruption in operations in such major clients may have an adverse effect on our business, financial condition, and results of operations (see page 11 of this prospectus); |

| 2 |

| ● | we have licensed all of the movies and television series on our SEEBATS website and mobile app from a third-party content provider. Any interruption in the operations of the content provider or our licensing partnership may have an adverse effect on our business, financial condition, and results of operations (see page 11 of this prospectus); | |

| ● | our payment solution service business relies on our cooperation with VE Services. Any interruption in the operations of VE Services or its cooperation with us may have an adverse effect on our business, financial condition, and results of operations (see page 11 of this prospectus); | |

| ● | if we fail to improve our services to keep up with the rapidly changing demands, preferences, advertising trends, or technologies in the digital advertising industry, our revenue and growth could be adversely affected (see page 12 of this prospectus); | |

| ● | our failure to anticipate or successfully implement new technologies could render our technologies or advertising services unattractive or obsolete and reduce our revenue and market share (see page 12 of this prospectus); | |

| ● | if we fail to manage our growth or execute our strategies and future plans effectively, we may not be able to take advantage of market opportunities or meet the demand of our advertisers (see page 13 of this prospectus); | |

| ● | the ongoing effects of the COVID-19 pandemic in Malaysia may have a material adverse effect on our business (see page 14 of this prospectus); | |

| ● | our business is geographically concentrated, which subjects us to greater risks from changes in local or regional conditions (see page 15 of this prospectus); | |

| ● | we may be unsuccessful in expanding and operating our business internationally, which could adversely affect our results of operations (see page 15 of this prospectus); | |

| ● | any negative publicity about us, our services, and our management may materially and adversely affect our reputation and business (see page 16 of this prospectus); and | |

| ● | if we sustain cyber-attacks or other privacy or data security incidents that result in security breaches, we could be subject to increased costs, liabilities, reputational harm, or other negative consequences (see page 17 of this prospectus). |

Risks Relating to this Offering and the Trading Market

In addition to the risks described above, we are subject to general risks and uncertainties relating to this offering and the trading market, including, but not limited to, the following:

| ● | there has been no public market for our Ordinary Shares prior to this offering, and you may not be able to resell our Ordinary Shares at or above the price you pay for them, or at all (see page 20 of this prospectus); | |

| ● | we do not intend to pay dividends for the foreseeable future (see page 22 of this prospectus); | |

| ● | because we are a foreign private issuer and are exempt from certain Nasdaq corporate governance standards applicable to U.S. issuers, you will have less protection than you would have if we were a domestic issuer (see page 24 of this prospectus); and | |

| ● | we are an “emerging growth company” within the meaning of the Securities Act, and if we take advantage of certain exemptions from disclosure requirements available to emerging growth companies, this will make it more difficult to compare our performance with other public companies (see page 25 of this prospectus). |

| 3 |

Our Securities

On June 8, 2022, our shareholders approved (i) a reverse split of our outstanding Ordinary Shares at a ratio of 1-for-11.25 shares, (ii) a reverse split of our authorized and unissued Preferred Shares at a ratio of 1-for-11.25 shares, (iii) an increase in our authorized share capital from $50,000 to $999,000, and (iv) an amendment and restatement of our memorandum and articles of association, in order to reflect the foregoing alterations to our share capital. The net effect of these corporate actions is that, with effect on and from June 8, 2022, our authorized share capital was changed to $999,000, divided into 883,000,000 Ordinary Shares of par value $0.001125 each and 5,000,000 Preferred Shares of par value $0.001125 each.

Unless otherwise indicated, all references to Ordinary Shares, options to purchase Ordinary Shares, share data, per share data, and related information have been retroactively adjusted, where applicable, in this prospectus to reflect the reverse split as if it had occurred at the beginning of the earlier period presented.

Corporate Information

Our principal executive offices are located at VO2-03-07, Velocity Office 2, Lingkaran SV, Sunway Velocity, 55100 Kuala Lumpur, Malaysia, and our phone number is +603 2781 9066. Our registered office in the Cayman Islands is located at the offices of Gold-In (Cayman) Co., Ltd., whose physical address is Suite 102, Cannon Place, North Sound Rd., George Town, Grand Cayman, Cayman Islands with postal address P.O. Box 712, Grand Cayman, KY1-9006, Cayman Islands, and the phone number of our registered office is +886-2-55820008. We maintain a corporate website at https://www.starboxholdings.com. The information contained in, or accessible from, our website or any other website does not constitute a part of this prospectus. Our agent for service of process in the United States is Cogency Global Inc., 122 East 42nd Street, 18th Floor, New York, NY 10168.

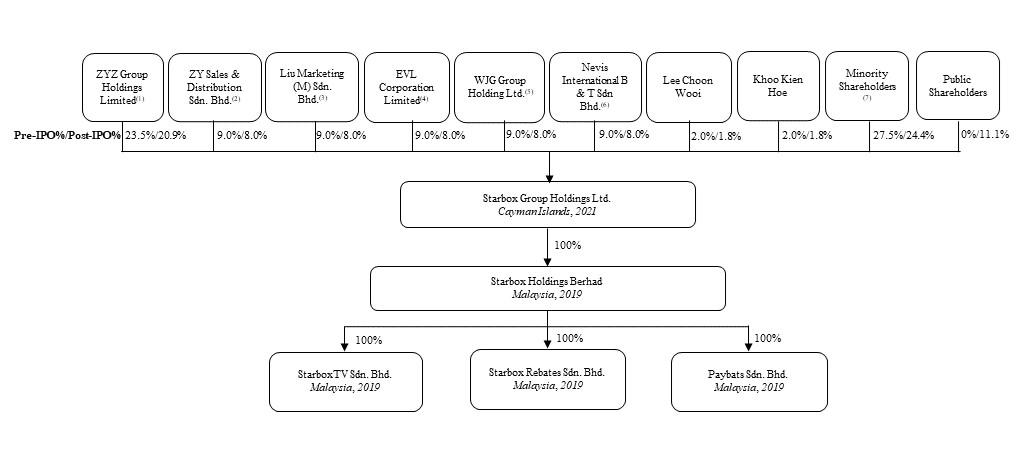

Corporate Structure

We are a Cayman Islands exempted company limited by shares incorporated on September 13, 2021. Exempted companies are Cayman Island companies conducting business mainly outside the Cayman Islands and, as such, are exempted from complying with certain provisions of the Companies Act (as amended) of the Cayman Islands (the “Cayman Companies Act”).

The following diagram illustrates our corporate structure upon completion of our initial public offering (“IPO”) based on 5,000,000 Ordinary Shares being offered, assuming no exercise of the underwriters’ over-allotment option. For more details on our corporate history, please refer to “Corporate History and Structure.”

| (1) | Represents 9,400,000 Ordinary Shares indirectly held by Choo Teck Hong, the 100% beneficial owner of ZYZ Group Holdings Limited, as of the date of this prospectus. | |

| (2) | Represents 3,600,000 Ordinary Shares indirectly held by Zhang Yong, the 100% beneficial owner of ZY Sales & Distribution Sdn. Bhd., as of the date of this prospectus. | |

| (3) | Represents 3,600,000 Ordinary Shares indirectly held by Liu Jun, the 100% beneficial owner of Liu Marketing (M) Sdn. Bhd., as of the date of this prospectus. | |

| (4) | Represents 3,600,000 Ordinary Shares indirectly held by Chen Han-Chen, the 100% beneficial owner of EVL Corporation Limited, as of the date of this prospectus. | |

| (5) | Represents 3,600,000 Ordinary Shares indirectly held by Wang Jian Guo, the 100% beneficial owner of WJG Group Holding Ltd., as of the date of this prospectus. | |

| (6) | Represents 3,600,000 Ordinary Shares indirectly held by Chen Xiaoping, the 100% beneficial owner of Nevis International B & T Sdn Bhd., as of the date of this prospectus. | |

| (7) | Represents an aggregate of 11,000,000 Ordinary Shares held by 10 shareholders, each one of which holds less than 5% of our Ordinary Shares, as of the date of this prospectus. |

| 4 |

Impact of the COVID-19 Pandemic on Our Operations and Financial Performance

The COVID-19 pandemic has adversely affected our business operations. Specifically, significant governmental measures implemented by the Malaysian government, including various stages of lockdowns, closures, quarantines, and travel bans, led to the store closure of some of our offline Merchants. As a result, our cash rebate service business was negatively affected to a certain extent, because the number of offline sales transactions between retail shoppers and retail merchants facilitated by us did not grow as much as we expected, leading to a lower amount of cash rebate service revenue than we expected during the six months ended March 31, 2022 and during the fiscal years ended September 30, 2021 and 2020. However, our digital advertising service revenue was not significantly affected by the COVID-19 pandemic, because more people have opted to use various online services since the beginning of the COVID-19 pandemic. As more advertisers used our digital advertising services through our websites and mobile apps and third-party social media channels to target their audiences, our revenue from digital advertising services increased significantly from fiscal year 2020 to fiscal year 2021 and during the six months ended March 31, 2022. However, any resurgence of the COVID-19 pandemic could negatively affect the execution of customer contracts and the collection of customer payments. The extent of any future impact of the COVID-19 pandemic on our business is still highly uncertain and cannot be predicted as of the date of this prospectus. Any potential impact to our operating results will depend, to a large extent, on future developments and new information that may emerge regarding the duration and severity of the COVID-19 pandemic and the actions taken by government authorities to contain the spread of the COVID-19 pandemic, almost all of which are beyond our control.

See “Risk Factors—Risks Related to Our Business and Industry—The ongoing effects of the COVID-19 pandemic in Malaysia may have a material adverse effect on our business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—COVID-19 Pandemic Affecting Our Results of Operations.”

Implications of Our Being an “Emerging Growth Company”

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the “JOBS Act.” An “emerging growth company” may take advantage of reduced reporting requirements that are otherwise applicable to larger public companies. In particular, as an emerging growth company, we:

| ● | may present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations; | |

| ● | are not required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives, which is commonly referred to as “compensation discussion and analysis”; | |

| ● | are not required to obtain an attestation and report from our auditors on our management’s assessment of our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; | |

| ● | are not required to obtain a non-binding advisory vote from our shareholders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on frequency,” and “say-on-golden-parachute” votes); | |

| ● | are exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and chief executive officer pay ratio disclosure; | |

| ● | are eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act; and | |

| ● | will not be required to conduct an evaluation of our internal control over financial reporting until our second annual report on Form 20-F following the effectiveness of our initial public offering. |

| 5 |

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under §107 of the JOBS Act.

Under the JOBS Act, we may take advantage of the above-described reduced reporting requirements and exemptions until we no longer meet the definition of an emerging growth company. The JOBS Act provides that we would cease to be an “emerging growth company” at the end of the fiscal year in which the fifth anniversary of our initial sale of common equity pursuant to a registration statement declared effective under the Securities Act of 1933, as amended (the “Securities Act”) occurred, if we have more than $1.07 billion in annual revenue, have more than $700 million in market value of our Ordinary Shares held by non-affiliates, or issue more than $1 billion in principal amount of non-convertible debt over a three-year period.

Foreign Private Issuer Status

We are a foreign private issuer within the meaning of the rules under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

| ● | we are not required to provide as many Exchange Act reports, or as frequently, as a domestic public company; | |

| ● | for interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that apply to domestic public companies; | |

| ● | we are not required to provide the same level of disclosure on certain issues, such as executive compensation; | |

| ● | we are exempt from provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; | |

| ● | we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents, or authorizations in respect of a security registered under the Exchange Act; and | |

| ● | we are not required to comply with Section 16 of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction. |

We will be required to file an annual report on Form 20-F within four months of the end of each fiscal year. Press releases relating to financial results and material events will also be furnished to the SEC on Form 6-K. However, the information we are required to file with or furnish to the SEC will be less extensive and less timely compared to that required to be filed with the SEC by U.S. domestic issuers. As a result, you may not be afforded the same protections or information that would be made available to you were you investing in a U.S. domestic issuer.

The Nasdaq listing rules provide that a foreign private issuer may follow the practices of its home country, which for us is the Cayman Islands, rather than the Nasdaq rules as to certain corporate governance requirements, including the requirement that the issuer have a majority of independent directors, the audit committee, compensation committee, and nominating and corporate governance committee requirements, the requirement to disclose third-party director and nominee compensation, and the requirement to distribute annual and interim reports. A foreign private issuer that follows a home country practice in lieu of one or more of the listing rules is required to disclose in its annual reports filed with the SEC each requirement that it does not follow and describe the home country practice followed by the issuer in lieu of such requirements. Although we do not currently intend to take advantage of these exceptions to the Nasdaq corporate governance rules, we may in the future take advantage of one or more of these exemptions. See “Risk Factors—Risks Relating to this Offering and the Trading Market—Because we are a foreign private issuer and are exempt from certain Nasdaq corporate governance standards applicable to U.S. issuers, you will have less protection than you would have if we were a domestic issuer.”

| 6 |

THE OFFERING

| Securities offered by us | 5,000,000 Ordinary Shares | |

| Over-allotment option | We have granted the underwriters an option, exercisable for 45 days from the date of this prospectus, to purchase up to an aggregate of 750,000 additional Ordinary Shares at the initial public offering price, less underwriting discounts. | |

| Price per Ordinary Share | The initial public offering price is $4.00 per Ordinary Share. | |

| Ordinary Shares outstanding prior to completion of this offering | 40,000,000 Ordinary Shares See “Description of Share Capital” for more information. | |

| Ordinary Shares outstanding immediately after this offering | 45,000,000 Ordinary Shares assuming no exercise of the underwriters’ over-allotment option and excluding 350,000 Ordinary Shares underlying the Representative’s Warrants

45,750,000 Ordinary Shares assuming full exercise of the underwriters’ over-allotment option and excluding 402,500 Ordinary Shares underlying the Representative’s Warrants | |

| Listing | We have received the approval letter from Nasdaq to have our Ordinary Shares listed on the Nasdaq Capital Market. | |

| Proposed Ticker symbol | “STBX” | |

| Transfer Agent | Transhare Corporation | |

| Use of proceeds | We intend to use the proceeds from this offering to expand our business into other countries in Southeast Asia, upgrade our software and system, and promote our brands in Malaysia. See “Use of Proceeds” on page 30 for more information. | |

| Lock-up | All of our directors and officers have agreed, subject to certain exceptions, not to sell, transfer, or dispose of, directly or indirectly, any of our Ordinary Shares or securities convertible into or exercisable or exchangeable for our Ordinary Shares for a period of 180 days after the date of this prospectus. See “Shares Eligible for Future Sale” and “Underwriting” for more information. | |

| Risk factors | The Ordinary Shares offered hereby involve a high degree of risk. You should read “Risk Factors” beginning on page 8 for a discussion of factors to consider before deciding to invest in our Ordinary Shares. |

| 7 |

An investment in our Ordinary Shares involves a high degree of risk. Before deciding whether to invest in our Ordinary Shares, you should consider carefully the risks described below, together with all of the other information set forth in this prospectus, including the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes. If any of these risks actually occurs, our business, financial condition, results of operations, or cash flow could be materially and adversely affected, which could cause the trading price of our Ordinary Shares to decline, resulting in a loss of all or part of your investment. The risks described below and discussed in other parts of this prospectus are not the only ones that we face. Additional risks not presently known to us or that we currently deem immaterial may also affect our business. You should only consider investing in our Ordinary Shares if you can bear the risk of loss of your entire investment.

Risks Related to Our Business and Industry

If advertisers stop purchasing digital advertising services from us or decrease the amount they are willing to spend on marketing campaigns and promotional activities, or if we are unable to establish and maintain new relationships with advertisers, our business, financial condition, and results of operations could be materially adversely affected.

A substantial majority of our revenue is derived from providing digital advertising services to retail merchant advertisers. Our digital advertising services are designed to help advertisers drive consumer demand, increase sales, and achieve operating efficiencies. Thus, our relationships with advertisers primarily depend on our ability to deliver quality advertising services at attractive volumes and prices. If advertisers are dissatisfied with the effectiveness of the advertising campaigns run through us, they may stop purchasing our digital advertising services or decrease the amount they are willing to spend on marketing campaigns and promotional activities. Our agreements with advertisers are largely short-term agreements, and advertisers may cease purchasing our digital advertising services at any time with no prior notice.

In addition to the quality of our digital advertising services, the willingness of retail merchant advertisers to spend their digital advertising budget through us, which is critical to our business and our ability to generate our revenue, can be influenced by a variety of factors, including:

| ● | macro-economic and social factors: domestic, regional, and global social, economic, and political conditions; economic and geopolitical challenges; and economic, monetary, and fiscal policies (such as concerns over a severe or prolonged slowdown in Malaysia’s economy and threats of political unrest); |

| ● | industry-related factors: the trends, preferences, and habits of audiences towards digital advertising and the development of varying forms of digital advertising and content; and |

| ● | advertiser-specific factors: an advertiser’s specific development strategies, business performance, financial condition, and sales and marketing plans. |

In view of the above, we cannot ensure you that our advertisers will continue to purchase our services or that we will be able to replace, in a timely and effective manner, departing advertisers with potential new and quality advertisers. Neither can we guarantee the amount of digital advertising services our advertisers will purchase from us, or that we will be able to attract new advertisers or increase the amount of revenue we earn from advertisers over time. If we are unable to maintain existing relationships with our advertisers or continue to expand our advertiser base, the demand for our advertising services will not grow and may even decrease, which could materially and adversely affect our revenue and profitability.

If we fail to retain and expand our Merchant and Member bases, our revenue and business will be harmed.

Our revenue is derived largely from the digital advertising services we provided primarily on our websites and mobile apps. The effectiveness of our digital advertising services, in turn, depends on (i) a large repository of Merchant and Member data we have been collecting from the GETBATS website and mobile app, which enables targeted marketing by leveraging our business data analysis technology; and (ii) the Internet traffic on our GETBATS website and mobile app and SEEBATS website and mobile app, where we place our advertisements, which largely decides the number of audiences who may view our advertisements. As such, maintaining and timely updating our composite database of Merchants and Members, and maintaining sufficiently high website traffic on the GETBATS website and mobile app and the SEEBATS website and mobile app are both vital to our business operations.

| 8 |

We must continue to retain and acquire Members on the GETBATS website and mobile app that purchase products or services through cash rebates offered by our Merchants, in order to maintain both the Internet traffic on the website and mobile app and our composite database for direct marketing. If our Members do not perceive the cash rebates offered through the GETBATS website and mobile app to be attractive or if we fail to introduce new and more relevant deals, we may not be able to retain or acquire Members at levels necessary to grow our business, which may not only affect the quality of our digital advertising services, but also comprise the number of audiences who may view our advertisements. This, in turn, may adversely affect the effectiveness of our digital advertising services, reduce our revenue from sales of digital advertising services, and thereby result in a material adverse impact on our financial performance and business prospects.

Moreover, we depend on our ability to attract and retain Merchants that are prepared to offer products or services with compelling cash rebates through our website and mobile app and provide our Members with a great experience. Our GETBATS website and mobile app currently feature cash rebates from retail merchants (both online and offline) in over 20 industries, such as automotive, beauty and health, books and media, electronics, fashion, food and beverages, groceries and pets, home and living, and sports and entertainment. After a merchant fills out an application form and agrees with our Merchant terms and conditions and the rate of blanket cash rebates, it becomes an authorized GETBATS Merchant and remains one indefinitely, unless the status is terminated by us or the Merchant by notice in writing. During the six months ended March 31, 2022 and the fiscal years ended September 30, 2021 and 2020, the GETBATS website and mobile app had 799, 723, and 478 Merchants, respectively, and had total transaction amount of $1,823,404, $2,501,913, and $74,867, respectively. For more details, see “Business—Cash Rebates—The Merchants.” If we are unsuccessful in our efforts to introduce services to Merchants as part of our cash rebates operating system, we will not experience a corresponding growth in our Merchant pool that is sufficient to offset the cost of these initiatives. We must continue to attract and retain Merchants to maintain our business ecosystem, where we leverage business data analysis technology to provide targeted advertisements based on our composite database of Merchants and Members on our website and mobile app. If new merchants do not find our marketing and promotional services effective, or if existing Merchants do not believe that utilizing our services provides them with a long-term increase in customers, revenue, or profits, they may stop making offers through our website and mobile app. In addition, we may experience attrition in our Merchants in the ordinary course of business, resulting from several factors, including losses to competitors and Merchant closures or bankruptcies. If we are unable to attract new merchants or if too many Merchants are unwilling to offer products or services with compelling cash rebates through our website and mobile app, we may not be able to retain or acquire Merchants in sufficient numbers to maintain our business ecosystem that relies both on our composite database of consumer spending behaviors and our website traffic. As a result, our business, financial condition, and results of operations may be adversely affected.

Our limited operating history in rapidly evolving industries makes it difficult to accurately forecast our future operating results and evaluate our business prospects.

As we launched our cash rebates and digital advertising services business in 2019, we only have a limited operating history. Members of our management team have been working together only for a short period of time and are still in the running-in period. They may still be in the process of exploring approaches to running our Company and reaching consensus among themselves, which may affect the efficiency and results of our operation. Due to our limited operating history, our historical growth rate may not be indicative of our future performance. Our future performance may be more susceptible to certain risks than a company with a longer operating history in a different industry. Many of the factors discussed below could adversely affect our business and prospects and future performance, including:

| ● | our ability to maintain, expand, and further develop our relationships with advertisers to meet their increasing demand; |

| ● | our ability to introduce and manage the development of new digital advertising services; |

| ● | the continued growth and development of the cash rebates industry and the digital advertising industry; |

| ● | our ability to keep up with the technological developments or new business models of the rapidly evolving cash rebates industry and digital advertising industry; |

| ● | our ability to attract and retain qualified and skilled employees; |

| ● | our ability to effectively manage our growth; and |

| ● | our ability to compete effectively with our competitors in the cash rebates industry and the digital advertising industry. |

| 9 |

We may not be successful in addressing the risks and uncertainties listed above, among others, which may materially and adversely affect our business, results of operations, financial condition, and future prospects.

We have significantly unstable operating revenue, anticipate increases in our operating expenses in the future, and may not achieve or sustain profitability on a consistent basis. If we cannot achieve and sustain profitability, our business, financial condition, and operating results may be adversely affected.

We have had significantly unstable and volatile operating revenue since our inception—specifically, our total revenue increased significantly by $2,803,270, or approximately 2,352.9%, to $2,922,413 for the six months ended March 31, 2022 from $119,143 for the six months ended March 31, 2021, primarily due to increased revenue from providing digital advertising services and cash rebate services to customers. As a result, we reported net income of $1,256,019 for the six months ended March 31, 2022, representing a significant increase of $1,445,370 from a net loss of $189,351 for the six months ended March 31, 2021. Our total revenue increased significantly by $3,012,365, or approximately 1,957.82%, to $3,166,228 for the fiscal year ended September 30, 2021 from $153,863 for the fiscal year ended September 30, 2020, primarily due to increased revenue from providing digital advertising services and cash rebate services to customers. As a result, we reported net income of $1,447,650 for the fiscal year ended September 30, 2021, representing a significant increase of $1,652,804 from a net loss of $205,154 for the fiscal year ended September 30, 2020. However, we cannot assure you that we will achieve or maintain profitability on a consistent basis. Our revenue growth may slow or our revenue may decline for a number of reasons, including reduced demand for our digital marketing services, increased competition, or our failure to capitalize on growth opportunities. Meanwhile, we expect our overall selling, general, and administrative expenses, including marketing expenses, salaries, and professional and business consulting expenses, to continue to increase in the foreseeable future, as we plan to hire additional personnel and incur additional expenses in connection with the expansion of our business operations. In addition, we also expect to incur significant additional legal, accounting, and other expenses as a newly public company. These efforts and additional expenses may be more costly than we currently expect, and there is no assurance that we will be able to maintain sufficient operating revenue to offset our operating expenses. Any failure to increase revenue or to manage our costs as we continue to grow and invest in our business would prevent us from achieving or maintaining profitability or maintaining positive operating cash flow at all, or on a consistent basis, which would cause our business, financial condition, and results of operations to suffer.

The markets in which we operate are highly competitive, and we may not be able to compete successfully against existing or new competitors, which could reduce our market share and adversely affect our competitive position and financial performance.

The cash rebates industry and the digital advertising industry in Malaysia are highly-competitive and rapidly evolving, with many new companies joining the competition in recent years and few leading companies. We compete directly with other cash rebate platforms for members and merchants and other providers of digital advertising services for advertisers and advertising revenue. Competition can be increasingly intensive and is expected to increase significantly in the future. Increased competition may result in price reductions for cash rebate offers and advertising services and thus reduced margins and loss of our market share. We compete for members, merchants, and advertisers on the following bases:

| ● | breadth of member and merchant bases; | |

| ● | brand recognition; | |

| ● | quality of services; | |

| ● | effectiveness of sales and marketing efforts; | |

| ● | creativity in design and contents of advertisements; | |

| ● | pricing and discount policies; and | |

| ● | hiring and retention of talented staff. |

| 10 |

Our competitors may operate with different business models, have different cost structures, and may ultimately prove to be more successful or more adaptable to new regulatory, technological, and other developments. They may in the future achieve greater market acceptance and recognition and gain a greater market share. It is also possible that potential competitors may emerge and acquire a significant market share. If existing or potential competitors develop or offer services that provide significant performance, price, creative optimization, or other advantages over those offered by us, our business, results of operations, and financial condition would be negatively affected. Our existing and potential competitors may enjoy competitive advantages over us, such as longer operating history, greater brand recognition, larger advertiser base, and significantly greater financial, technical, and marketing resources. In addition, our clients often have a vast array of advertising choices—for example, we compete with traditional forms of media, such as newspapers, magazines, and radio and television broadcast, for advertisers and advertising revenue. If we are unable to sustain sufficient interest in our digital advertising services in comparison to other advertising forms, including new forms of marketing campaigns and promotional activities that may emerge in the future, our business model may no longer be viable.

If we fail to compete successfully, we could lose out in acquiring Members and Merchants or procuring advertisers, which could result in an adverse impact on our financial performance and business prospects. We cannot assure you that our strategies will remain competitive or that they will continue to be successful in the future. Increasing competition may result in pricing pressure and loss of our market share, either of which could have a material adverse effect on our financial condition and results of operations.

Our major clients generate a significant portion of our revenue. Any interruption in operations in such major clients may have an adverse effect on our business, financial condition, and results of operations.

During the six months ended March 31, 2022 and during the fiscal years ended September 30, 2021 and 2020, we derived most of our revenue from a few clients. Specifically, for the six months ended March 31, 2022, one client accounted for approximately 19.2% of our total revenue. As of March 31, 2022, five clients accounted for approximately 15.4%, 13.3%, 11.8%, 11.8%, and 11.8% of our total accounts receivable, respectively. For the fiscal year ended September 30, 2021, three clients accounted for approximately 21.7%, 10.8%, and 10.8% of our total revenue, respectively. As of September 30, 2021, two clients accounted for approximately 52.6% and 26.3% of our total accounts receivable, respectively. For the fiscal year ended September 30, 2020, one client accounted for approximately 91.6% of our total revenue and approximately 85.4% of our total accounts receivable. All of these significant customers were advertisers who used our digital advertising services during the six months ended March 31, 2022 and the fiscal years ended September 30, 2021 and 2020. These clients are generally able to reduce or cancel spending on our services on short notice for any reason. There are a number of factors, including our performance, that could cause the loss of, or decrease in the volume of business from, a client. Even though we have a strong record of performance, we cannot assure you that we will continue to maintain the business cooperation with these clients at the same level, or at all. The loss of business from one or more of these significant clients could materially and adversely affect our revenue and profitability. Furthermore, if any significant advertiser terminates its relationship with us, we cannot assure you that we will be able to secure an alternative arrangement with comparable advertiser in a timely manner, or at all.

We have licensed all of the movies and television series on our SEEBATS website and mobile app from a third-party content provider. Any interruption in the operations of the content provider or our licensing partnership may have an adverse effect on our business, financial condition, and results of operations.

Our success will depend, in large part, on the website traffic on our SEEBATS website and mobile app, which in turn depends on our ability to continually provide attractive and entertaining movies and television series across various genres to meet the evolving needs of viewers. Currently, we have licensed all of the movies and television series on our SEEBATS website and mobile app from Shenzhen Yunshidian Information Technology Ltd., a third-party content provider (“Shenzhen Yunshidian”), pursuant to a Service and Licensing Agreement dated November 1, 2021. However, as the license will expire on October 31, 2023, and although we currently expect to renew the license when it expires, we cannot assure you that we will be able to maintain such license partnership at the same level, or at all. Such third-party content provider is subject to its own unique operational and financial risks, which are beyond our control. If the content provider breaches, terminates, or decides to not renew its licensing contract with us or experiences significant disruption to its operations, we will be required to find a substitute content provider for sufficient entertainment offerings in order to continually attract and retain viewers on our SEEBATS website and mobile app. If we are unable to do so in a timely or cost-effective manner, our SEEBATS website and mobile app could lose their appeal to our advertisers as a marketing platform due to the decreased website traffic. As a result, our business, financial condition, and results of operations may be adversely affected.

If the relevant Malaysian regulatory agency were to determine that a Film Distribution License was required for the operations of our SEEBATS website and mobile app prior to April 11, 2022, our business, financial condition, and results of operations could be adversely affected.

Pursuant to Section 22(1) of the Perbadanan Kemajuan Filem Nasional Malaysia Act 1981 (Unofficial Translation: the National Film Development Corporation Malaysia Act 1981) (the “FINAS Act”), “no person shall engage in any of the activities of production, distribution, or exhibition of films or any combination of those activities as specified in subsection 21(1) unless there is in force a license authorizing him to do the same.” Section 2 of the FINAS Act defines film distribution as “including the renting, hiring, and loaning of films for profit or otherwise, the importation and distribution of films produced abroad, and the distribution of films produced locally.” One of our subsidiaries, StarboxSB, operates our SEEBATS website and mobile app, on which viewers may watch movies and television series through OTT streaming, and StarboxSB obtained the Film Distribution License from the National Film Development Corporation Malaysia (the “FINAS”) on April 11, 2022. However, since we conducted our business operations through our SEEBATS website and mobile app without holding the Film Distribution License prior to April 11, 2022, we may be subject to penalty if the FINAS were to determine that a Film Distribution License was required. As of the date of this prospectus, we have not received any penalty notice from the relevant Malaysian regulatory agency.

Our Malaysia legal counsel, GLT Law, has advised us that, based on their understanding of the FINAS Act and their discussion with the Director of Licensing and Enforcement of the FINAS, StarboxSB is not required to obtain a Film Distribution License for “film distribution” for the following reasons: (i) as our SEEBATS website and mobile app allow viewers to access movies and television series through the Internet, this online streaming mode does not, at its strict interpretation, fall within the scope of “renting, hiring, and loaning of films” under the FINAS Act, and (ii) no enforcement actions are currently being taken towards online streaming service providers who do not have the Film Distribution License.

There remains uncertainty, however, inherent in relying on an opinion of counsel or the opinion of an officer at the relevant department in connection with whether we would be required to obtain a license under the FINAS Act for the business of StarboxSB. The issue of whether the Film Distribution License is required for the operations of our SEEBATS website and mobile app will be subject to future revisions of the FINAS Act and different interpretations by higher-level officers within FINAS. If FINAS were to determine that a Film Distribution License was required prior to April 11, 2022, FINAS may take enforcement action to collect from us the penalty and late fee charges in respect of unlicensed activities of StarboxSB prior to such date, which could adversely affect our business, financial condition, and results of operations. For details about the penalty for failure to comply with the FINAS Act, see “Regulations—Regulations Relating to Film Distribution.”

Our payment solution service business relies on our cooperation with VE Services. Any interruption in the operations of VE Services or its cooperation with us may have an adverse effect on our business, financial condition, and results of operations.

We provide payment solution services to merchants by referring them to VE Services for payment processing. As we merely act as a recruitment and onboarding agent during this type of transaction, our payment solution service business is highly dependent on the quality of the services provided by VE Services, and its ability to comply with the relevant laws and regulations. Since we do not have control over the operations of VE Services, if VE Services breaches the terms of its contracts with the relevant merchants, or the relevant laws and regulations, our payment solution services and our reputation may be severely impacted. In addition, if VE Services breaches or terminates the Appointment Letter with us or experiences significant disruption to its operations, we may lose our current payment solution service customers in the event that the customers discontinue the services provided by us, and we will be unable to continue providing payment solution services unless we find substitute payment solution service providers. As a result, our business, financial condition, and results of operations may be adversely affected.

| 11 |

If we fail to improve our services to keep up with the rapidly changing demands, preferences, advertising trends, or technologies in the digital advertising industry, our revenue and growth could be adversely affected.

We consider the digital advertising industry to be dynamic, as we face (i) constant changes in audiences’ interests, preferences, and receptiveness over different advertisement formats, (ii) evolution of the needs of advertisers in response to shifts in their business needs and marketing strategies, and (iii) innovations in the means on digital advertising. As a result, our success depends not only on our ability to offer proper choices of media, deliver effective optimization services, and provide creative advertising ideas, but also on our ability to adapt to rapidly changing online trends and technologies to enhance the quality of existing services and to develop and introduce new services to address advertisers’ changing demands.

We may experience difficulties that could delay or prevent the successful development, introduction, or marketing of our new services. Any new service or enhancement will need to meet the requirements of our existing and potential advertisers and may not achieve significant market acceptance. If we fail to keep pace with changing trends and technologies, continue to offer effective optimization services and creative advertising ideas to the satisfaction of our advertisers, or introduce successful and well-accepted services for our existing and potential advertisers, we may lose our advertisers and our revenue and growth could be adversely affected.

Our failure to anticipate or successfully implement new technologies could render our technologies or advertising services unattractive or obsolete and reduce our revenue and market share.

The majority of our revenue is derived from our digital advertising services, which in turn depend on our advanced business data analysis technology for advertisements. We have built a large repository of data regarding Merchants and Members through the GETBATS website and mobile app, where we facilitate transactions between Merchants and Members, in which Merchants offer certain cash rebates to incentivize or attract Members to shop online or offline. With the data collected through our cash rebate website and mobile app, we have utilized our business data analysis capabilities to better understand and anticipate consumer spending behaviors, which enables targeted advertisement delivery by Merchants.

With our digital advertising services primarily driven by a composite database of consumer spending behaviors, we operate in businesses that require sophisticated data collection, processing, and software for analysis and insights. Some of the digital advertising strategy technologies, which support the industry we serve, are changing rapidly. We will be required to continue to adapt to changing technologies, either by developing new services or by enhancing our existing services, to meet client demand. We need to invest significant resources, including financial resources, in research and development to keep pace with technological advances in order to make our digital advertising services competitive in the market. Our continued success will depend on our ability to anticipate and adapt to changing technologies, manage and process increasing amounts of data and information, and improve the performance, features, and reliability of our existing services in response to changing client and industry demand.

However, development activities are inherently uncertain, and our investment in research and development may not generate corresponding benefits. Given the fast pace with which the online marketing strategy technology has been and will continue to be developed, we may not be able to timely upgrade our business data analysis technology, or the algorithm or engines required thereby, in an efficient and cost-effective manner, or at all. New technologies in programming or operations could render our technologies or products or services that we are developing or expect to develop in the future obsolete or unattractive, thereby limiting our ability to recover the costs relating to the design, development, testing, or marketing of our digital advertising services, and resulting in a decline in our revenue and market share.

| 12 |

If we fail to retain and expand the user base for our payment solution service business or if our partner fails to implement and maintain a reliable and convenient payment solution system, our payment solution service business may not be successful, and our business, financial condition, and results of operations may be adversely affected.

We started to provide payment solution services to merchants in May 2021 by referring them to VE Services for payment processing. Since we have relatively limited operating history and experience regarding our payment solution service business, we may encounter difficulties as we advance our business operations, such as in marketing, selling, and deploying our payment services.

The payments industry is highly competitive. We compete against other payment solution service providers in the market, many of which have greater customer bases, volume, scale, resources, and market share than we do, which may provide significant competitive advantages. Because one of the biggest concerns for the payment solution users, is the system’s security vulnerabilities such as the threat of cyber-attacks and data breaches, users tend to choose an established brand having a relatively large market share and proven reputation. For that reason, we may incur substantial expenses in retaining and expanding our merchant user base through robust marketing campaigns and promotional activities, and we cannot assure you that these promotional efforts will be effective. To be competitive in the constantly evolving payments industry, we must keep pace with rapid technological developments to provide new and innovative payment solution services. Our payment solution service business relies, in large part, on VE Services for access to new or evolving payment technologies, but we cannot assure you that we will continue to maintain the business cooperation with it at the same level, or at all. In addition, we cannot predict the effects of technological changes on our business, which technological developments or innovations will become widely adopted, or how those technologies may be regulated. New services and technologies will continue to emerge and may render the technologies VE Services currently uses in its system obsolete. If we are unable to attract new merchant users in sufficient numbers or if VE Services fails to keep pace with the new payment technology to maintain a reliable and resilient payment system, our payment solutions service business may not be successful, leading to a waste of our substantial investment in promoting our payment solution service business as well as the diversion of management’s attention and resources. As a result, our business, financial condition, and results of operations may be adversely affected.

If we fail to manage our growth or execute our strategies and future plans effectively, we may not be able to take advantage of market opportunities or meet the demand of our advertisers.

Our business has grown substantially since our inception, and we expect it to continue to grow in terms of the scale and diversity of operations. For example, in order to diversify our business and revenue stream for future growth, we have utilized our cash rebate website and mobile app, in addition to our digital advertising service business, to facilitate transactions between Merchants and Members, in which Merchants offer certain cash rebates to incentivize or attract Members to shop online or offline, and we have provided payment solution services to Merchants. This expansion increases the complexity of our operations and may cause strain on our managerial, operational, and financial resources. We must continue to hire, train, and effectively manage new employees. If our new hires perform poorly or if we are unsuccessful in hiring, training, managing, and integrating new employees, our business, financial condition, and results of operations may be materially harmed. Our expansion will also require us to maintain the consistency of our service offerings to ensure that our market reputation does not suffer as a result of any deviations, whether actual or perceived, in the quality of our services.

Our future results of operations also depend largely on our ability to execute our future plans successfully. In particular, our continued growth may subject us to the following additional challenges and constraints:

| ● | we face challenges in recruiting, training, and retaining highly skilled personnel, including areas of sales and marketing, advertising concepts, optimization skills, and information technology for our growing operations; | |

| ● | we face challenges in responding to evolving industry standards and government regulations that impact our business and the cash rebates industry and the digital advertising industry in general, particularly in the areas of content dissemination; |

| 13 |

| ● | we may have limited experience for certain new service offerings, and our expansion into these new service offerings may not achieve broad acceptance among advertisers; | |

| ● | the execution of our future plan will be subject to the availability of funds to support the relevant capital investment and expenditures; and | |

| ● | the successful execution of our strategies is subject to factors beyond our control, such as general market conditions, economic, and political development in Malaysia and globally. |

All of these endeavors involve risks and will require significant management, financial, and human resources. We cannot assure you that we will be able to effectively manage our growth or to implement our strategies successfully. Besides, there is no assurance that the investment to be made by our Company as contemplated under our future plans will be successful and generate the expected return. If we are not able to manage our growth or execute our strategies effectively, or at all, our business, results of operations, and prospects may be materially and adversely affected.

The ongoing effects of the COVID-19 pandemic in Malaysia may have a material adverse effect on our business.

Our business operations could be materially and adversely affected by the ongoing COVID-19 pandemic. The COVID-19 pandemic has resulted in the implementation of significant governmental measures, including lockdowns, closures, quarantines, and travel bans, intended to control the spread of the virus. Such governmental actions, together with the further development of the COVID-19 pandemic, could materially disrupt our business and operations, slow down the overall economy, curtail consumer spending, and make it difficult to adequately staff our operations.

Specifically, in response to the COVID-19 pandemic and its spread, the Malaysian government has implemented intermittent lockdowns in various stages such as (i) imposing full movement control orders (“MCO”), under which, quarantines, travel restrictions, and the temporary closure of stores and facilities in Malaysia were made mandatory; (ii) easing MCO to a Conditional Movement Control Order (“CMCO”) under which most business sectors were allowed to operate under strict rules and Standard Operating Procedures mandated by the government of Malaysia; and (iii) further easing CMCO to Recovery Movement Control Order. On January 12, 2021, due to a resurgence of COVID-19 cases, the Malaysian government declared a state of emergency nationwide to combat COVID-19. On February 16, 2021, the government announced that a National COVID-19 Immunization Plan will be implemented for one year after February 2021, in which 80% of the Malaysian population will be vaccinated to achieve herd immunity. On March 5, 2021, lockdowns in most parts of the country were eased to a CMCO, however, COVID-19 cases in the country continued to rise. On May 12, 2021, the Malaysian government re-imposed a full lockdown order nationwide, until the earlier of when (i) daily COVID-19 infection cases in the country fall below 4,000; (ii) intensive care unit wards start operating at a moderate level; or (iii) 10% of the Malaysian population is fully vaccinated. The total number of COVID-19 cases in the country surpassed three million on February 13, 2022, and the number of daily cases hit a record high of 33,406 on March 5, 2022.

In response to efforts to contain the spread of COVID-19, we have implemented temporary measures and adjustments of work schemes to allow employees to work from home and collaborate remotely. We have taken measures to reduce the impact of the COVID-19 pandemic, including upgrading our telecommuting system, monitoring employees’ health on a daily basis, and optimizing the technology system to support potential growth in user traffic. The Malaysian government has recently eased its restrictive policies due to a decrease in COVID-19 infection cases. The government ended the nationwide state of emergency on August 1, 2021, and COVID-19 infection started to drop below the 10,000 mark daily, beginning October 3, 2021. Interstate and international travel restrictions were lifted, effective October 11, 2021, for residents who had been fully vaccinated against COVID-19, as the country achieved its target of inoculating 90% of its adult population. The government is preparing to shift into an endemic COVID-19 phase, where it will not impose wide lockdowns even if cases rise. As of March 3, 2022, over 78% of the country’s population had been fully vaccinated.

| 14 |

However, there have been occasional outbreaks of COVID-19 in various cities in Malaysia, and the Malaysian government may again take measures to keep COVID-19 in check. Consumers may have less disposable income and the merchants’ advertising budget may experience a general decline or fluctuate depending on factors beyond our control, such as the shelter-in-place restrictions due to the COVID-19 pandemic. Substantially all our revenue is concentrated in Malaysia. Consequently, our results of operations will likely be adversely, and may be materially, affected, to the extent that the COVID-19 pandemic or any other epidemic harms the Malaysia and global economy in general. Specifically, significant governmental measures implemented by the Malaysian government, including various stages of lockdowns, closures, quarantines, and travel bans, led to the store closure of some of our offline Merchants. As a result, our cash rebate service business was negatively affected to a certain extent, because the number of offline sales transactions between retail shoppers and retail merchants facilitated by us did not grow as much as we expected, leading to a lower amount of cash rebate service revenue than we expected during the six months ended March 31, 2022 and during the fiscal years ended September 30, 2021 and 2020. However, our digital advertising service revenue was not significantly affected by the COVID-19 pandemic, because more people have opted to use various online services since the beginning of the COVID-19 pandemic. As more advertisers used our digital advertising services through our websites and mobile apps and third-party social media channels to target their audiences, our revenue from digital advertising services increased significantly from fiscal year 2020 to fiscal year 2021 and during the six months ended March 31, 2022. However, any resurgence of the COVID-19 pandemic could negatively affect the execution of customer contracts and the collection of customer payments. The extent to which the COVID-19 pandemic may impact us will depend on future developments, which are highly uncertain and cannot be predicted, including new information on the effectiveness of the mitigation strategies, the duration, spread, severity, and recurrence of COVID-19 and any COVID-19 variants and related travel advisories and restrictions, and the efficacy of COVID-19 vaccines, which may also take an extended period of time to be widely and adequately distributed.

Our business is geographically concentrated, which subjects us to greater risks from changes in local or regional conditions.

Substantially all of our current operations are located in Malaysia. Due to this geographic concentration, our financial condition and operating results are subject to greater risks from changes in general economic and other conditions in Malaysia, than the operations of more geographically diversified competitors. These risks include:

| ● | changes in economic conditions and unemployment rates; | |

| ● | changes in laws and regulations; | |

| ● | changes in the competitive environment; and | |

| ● | adverse weather conditions and natural disasters. |

As a result of the geographic concentration of our business, we face a greater risk of a negative impact on our business, financial condition, results of operations, and prospects in the event that Malaysia is more severely impacted by any such adverse condition, as compared to other countries.

We may be unsuccessful in expanding and operating our business internationally, which could adversely affect our results of operations.

We plan to selectively launch our cash rebate and digital advertising services in other countries in Southeast Asia during the next three years, starting from markets such as the Philippines, Thailand, and Indonesia. For details, see “—Liquidity and Capital Resources” The entry and operation of our business in these markets could cause us to be subject to unexpected, uncontrollable, and rapidly changing events and circumstances outside Malaysia. As we grow our international operations in the future, we may need to recruit and hire new product development, sales, marketing, and support personnel in the countries in which we will launch our services or otherwise have a significant presence. Entry into new international markets typically requires the establishment of new marketing channels. Our ability to continue to expand into international markets involves various risks, including the possibility that our expectations regarding the level of returns we will achieve on such expansion will not be achieved in the near future, or ever, and that competing in markets with which we are unfamiliar may be more difficult than anticipated. If we are less successful than we expect in a new market, we may not be able to realize an adequate return on our initial investment and our operating results could suffer.

| 15 |

Our international operations may also fail due to other risks inherent in foreign operations, including:

| ● | varied, unfamiliar, unclear, and changing legal and regulatory restrictions, including different legal and regulatory standards applicable to digital advertising; | |

| ● | compliance with multiple and potentially conflicting regulations in other countries in Southeast Asia; | |

| ● | difficulties in staffing and managing foreign operations; | |

| ● | longer collection cycles; | |

| ● | different intellectual property laws that may not provide consistent and/or sufficient protections for our intellectual property; | |