As filed with the Securities and Exchange Commission on September 20, 2024

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CBL INTERNATIONAL LIMITED

(Exact Name of Registrant as Specified in Its Charter)

| Cayman Islands | 5172 | Not Applicable | ||

| (State

or other jurisdiction of incorporation or organization) |

(Primary

Standard Industrial Classification Code Number) |

(I.R.S.

Employer Identification Number) |

Level 23-2 Permata Sapura

Kuala Lumpur City Centre

50088 Kuala Lumpur

Malaysia

Tel: + 60 3 2706 8280

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

Tel: (212) 947-7200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Kathleen L. Deutsch, Esq.

Nelson Mullins Riley & Scarborough LLP

360 S. Rosemary Avenue, Suite 1410

West Palm Beach, FL 33401

Tel: (561) 366-5320

APPROXIMATE DATE OF COMMENCEMENT OF PROPOSED SALE TO THE PUBLIC: From time to time after the effective date of this registration statement.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box. ☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a registration statement pursuant to General Instruction I.C. or a post-effective amendment thereto that shall become effective on filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.C. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for comply with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated September 20, 2024.

PRELIMINARY PROSPECTUS

CBL INTERNATIONAL LIMITED

Up to 2,500,000 Ordinary Shares

Offered by the Selling Securityholder

This prospectus relates to the offer and sale from time to time in one or more offerings by the selling securityholder named in this prospectus or their permitted transferees (collectively, the “selling securityholders”) of up to 2,500,000 ordinary shares, par value of $0.0001 per share (“Ordinary Shares”) of CBL International Limited, an exempted company incorporated with limited liability in the Cayman Islands (the “Company”) issued to such securityholders in connection with the closing on August 22, 2024, of a private placement offering.

This prospectus also covers any additional securities that may become issuable by reason of share splits, share dividends or other similar transactions.

We are registering the securities described above for resale pursuant to the selling securityholders’ registration rights under the stock purchase agreement between us and the selling securityholders. Our registration of the securities covered by this prospectus does not mean that any selling securityholder will offer or sell, as applicable, any of the securities. The selling securityholders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the selling securityholders may sell the Ordinary Shares in the section entitled “Plan of Distribution.”

We will not receive any proceeds from the sale of Ordinary Shares by the selling securityholders pursuant to this prospectus. However, we may pay certain expenses, other than any underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus. We will pay certain expenses associated with the registration of the securities covered by this prospectus, as described in the section entitled “Plan of Distribution.”

INVESTING IN OUR SECURITIES INVOLVES RISKS. SEE THE “RISK FACTORS” ON PAGE 6 OF THIS PROSPECTUS AND ANY SIMILAR SECTION CONTAINED IN THE APPLICABLE PROSPECTUS SUPPLEMENT AND ANY DOCUMENTS INCORPORATED BY REFERENCE THEREIN CONCERNING FACTORS YOU SHOULD CONSIDER BEFORE INVESTING IN OUR SECURITIES.

Our Ordinary Shares are listed on The Nasdaq Capital Market (“Nasdaq”) under the symbol “BANL.” On September 17, 2024, the closing sale price as reported on Nasdaq of our Ordinary Shares was $0.6364 per share.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is ____________ , 2024.

TABLE OF CONTENTS

This prospectus is part of a registration statement on Form F-3 that we filed with the U.S. Securities and Exchange Commission, or the SEC, using a “shelf” registration process. By using a shelf registration statement, the selling securityholders may sell Ordinary Shares as described in this prospectus, from time to time, in one or more offerings as described in this prospectus. To the extent permitted by law, we may file or authorize one or more prospectus supplements or free writing prospectuses to be provided to you that may contain material information relating to these offerings. The prospectus supplement or free writing prospectus may also add, update or change information contained in this prospectus with respect to that offering. If there is any inconsistency between the information in this prospectus and the applicable prospectus supplement or free writing prospectus, you should rely on the prospectus supplement or free writing prospectus, as applicable. Before purchasing any securities, you should carefully read both this prospectus and the applicable prospectus supplement (and any applicable free writing prospectuses), together with the additional information described under the heading “Where You Can Find More Information; Incorporation by Reference.”

Neither we, nor the selling securityholders, have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus, any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. We and the selling securityholders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We and the selling securityholders will not make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus and the applicable prospectus supplement to this prospectus is accurate only as of the date on its respective cover, that the information appearing in any applicable free writing prospectus is accurate only as of the date of that free writing prospectus, and that any information incorporated by reference is accurate only as of the date of the document incorporated by reference, unless we indicate otherwise. Our business, financial condition, results of operations and prospects may have changed since those dates. This prospectus incorporates by reference, and any prospectus supplement or free writing prospectus may contain and incorporate by reference, market data and industry statistics and forecasts that are based on independent industry publications and other publicly available information. Although we believe these sources are reliable, we do not guarantee the accuracy or completeness of this information and we have not independently verified this information. In addition, the market and industry data and forecasts that may be included or incorporated by reference in this prospectus, any prospectus supplement or any applicable free writing prospectus may involve estimates, assumptions and other risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” contained in this prospectus, the applicable prospectus supplement and any applicable free writing prospectus, and under similar headings in other documents that are incorporated by reference into this prospectus. Accordingly, investors should not place undue reliance on this information.

On July 22, 2024, the Company entered into a securities purchase agreement (the “SPA”) with the selling shareholder named herein (the “PIPE Investor”), pursuant to which the PIPE Investor subscribes for, and the Company agreed to issue to such PIPE Investor, an aggregate of 2,500,000 Ordinary Shares at $0.55 per share for gross proceeds of approximately $1,375,000 on August 22, 2024, when closing occurred.

When we refer to “CBL International,” “we,” “our,” “us” and the “Company” in this prospectus, we mean CBL International Limited, an exempted company incorporated with limited liability in the Cayman Islands, and its consolidated subsidiaries, unless otherwise specified. When we refer to “you,” we mean the potential holders of the Ordinary Shares.

| 1 |

WHERE YOU CAN FIND MORE INFORMATION; INCORPORATION BY REFERENCE

Available Information

We file reports, proxy statements and other information with the SEC. The SEC maintains a website that contains reports, proxy and information statements and other information about issuers, such as us, who file electronically with the SEC. The address of that website is http://www.sec.gov.

Our website address is https://www.banle-intl.com. The information on our website, however, is not, and should not be deemed to be, a part of this prospectus.

This prospectus and any prospectus supplement are part of a registration statement that we filed with the SEC and do not contain all of the information in the registration statement. The full registration statement may be obtained from the SEC or us, as provided below. Other documents establishing the terms of the offered securities are or may be filed as exhibits to the registration statement or documents incorporated by reference in the registration statement. Statements in this prospectus or any prospectus supplement about these documents are summaries and each statement is qualified in all respects by reference to the document to which it refers. You should refer to the actual documents for a more complete description of the relevant matters. You may inspect a copy of the registration statement through the SEC’s website, as provided above.

Incorporation by Reference

The SEC’s rules allow us to “incorporate by reference” information into this prospectus, which means that we can disclose important information to you by referring you to another document filed separately with the SEC. The information incorporated by reference is deemed to be part of this prospectus, and subsequent information that we file with the SEC will automatically update and supersede that information. Any statement contained in this prospectus or a previously filed document incorporated by reference will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus or a subsequently filed document incorporated by reference modifies or replaces that statement.

This prospectus and any accompanying prospectus supplement incorporate by reference the documents set forth below that have previously been filed with the SEC:

| ● | Our Annual Report on Form 20-F for the year ended December 31, 2023 (the “2023 Annual Report”), filed with the SEC on April 18, 2024; |

| ● | Our Current Reports on Form 6-K furnished to the SEC on April 24, 2024/April 24, 2024, July 22, 2024 and September 12, 2024 (the September 12, 2024 Form 6-K is referred to as the “2024 Interim Results”); |

| ● | The information contained in our Current Reports on Form 6-K furnished to the SEC on April 18, 2024 (excluding Exhibit 99.1 thereto), April 24, 2024 (excluding Exhibits 99.1 and 99.2 thereto), May 13, 2024 (excluding Exhibit 99.1 thereto), May 15, 2024 (excluding Exhibit 99.1 thereto), July 15, 2024 (excluding Exhibit 99.1 thereto), and July 19, 2024, and (excluding Exhibit 99.1 thereto); and |

| ● | The description of our Ordinary Shares contained in our registration statement on Form 8-A filed with the SEC on March 22, 2023 and any amendment or report filed with the SEC for the purpose of updating the description. |

All reports and other documents we subsequently file pursuant to Section 13(a), 13(c), 14 or 15(d) of the Securities Exchange Act of 1934, as amended, which we refer to as the “Exchange Act” in this prospectus, prior to the termination of this offering, including all such documents we may file with the SEC after the date of the initial registration statement and prior to the effectiveness of the registration statement, but excluding any information furnished to, rather than filed with, the SEC, will also be incorporated by reference into this prospectus and deemed to be part of this prospectus from the date of the filing of such reports and documents. We may also incorporate by reference part or all of any reports on Form 6-K that we subsequently furnish to the SEC prior to the completion or termination of any offering by identifying in such Forms 6-K that such Form 6-K, or certain parts or exhibits of such Form 6-K, are being incorporated by reference into this prospectus, and any Form 6-K (or parts thereof) so identified shall be deemed to be incorporated by reference in this prospectus and to be a part of this prospectus from the date of submission of such document.

You may request a free copy of any of the documents incorporated by reference in this prospectus by writing or telephoning us at the following address:

CBL International Limited

Level 23-2 Permata Sapura

Kuala Lumpur City Centre

50088 Kuala Lumpur

Malaysia

Teck Lim Chia, Chief Executive Officer

Telephone: +60 3 2706 8280

Email: wchia@cbl-grp.com

Exhibits to the filings will not be sent, however, unless those exhibits have specifically been incorporated by reference in this prospectus or any accompanying prospectus supplement.

| 2 |

Overview

We were incorporated on February 8, 2022 in the Cayman Islands as a holding company to own our operating companies. We are an established marine fuel logistics company providing a one-stop solution for vessel refueling, which is referred to as a bunkering facilitator in the bunkering industry. We facilitate vessel refueling between ship operators, local physical distributors and oil traders by purchasing marine fuel, including both fossil fuel and sustainable fuel, from our suppliers and arranging for the marine fuel to be delivered by the local physical suppliers to our customers. We rely on the permits and licenses of our local physical suppliers for the delivery of marine fuel at each port. Since the establishment of our Group in 2015, container liner operators have been identified as our primary target customers. Container liner operators provide liner services which operate on a schedule with a fixed port rotation and fixed frequency, which is similar to bus operation under which buses go on fixed routes and calling at fixed stops for passengers to board and alight. Knowing the nature of the business of our target customers, we continually look to broaden our operations by (a) expanding our servicing network to cover more ports; (b) providing more value-added services to meet our existing and potential customers’ growing demands with high-quality vessel refueling services; and (c) expanding biofuel and other sustainable fuel supply capabilities to meet the evolving emission reduction needs of our customers.

Our operations are based in Malaysia, Hong Kong, Singapore and Ireland. We do not conclude and book any transactions in China. All of our transactions for vessel refueling services were concluded, and revenue was booked under our subsidiaries established in Malaysia, Hong Kong, Singapore, and Ireland. Although we deliver our services through our suppliers mainly in Hong Kong and China, most of our customers are international container liner operators from outside of Hong Kong and China. Our customers’ operational routes determine our bunkering service delivery locations. Of our five largest customers from whom we generated 73.5% of our total revenue for fiscal year 2022, there are two Taiwanese companies, two Singaporean companies and one Japanese company. For fiscal year 2023, 70.3% of our total revenue was generated from two Taiwanese companies, one Irish company, one Singaporean company and one Malaysian company; whilst for the six months ended June 30, 2024, the five largest customers who contributed 66.7% in the aggregate of our total revenue consisted of two Taiwanese companies, one Malaysian company, one Hong Kong company and one Irish company.

We act as a bunkering facilitator and leverage on our close business relationships with parties amongst our supply network in the value chain to provide one-stop solution for vessel refueling. Our services mainly involve (i) making vessel refueling options available to our customers at various ports along their voyages; (ii) arranging vessel refueling activities at competitive pricing (iii) coordinating vessel refueling to meet our customers’ schedule during their various port visits; (iv) providing trade credit to our customers in relation to vessel refueling; (v) arranging local physical delivery of marine fuel to meet our customers’ schedule; (vi) handling unforeseeable circumstances faced by our customers and providing contingency solutions to our customers in a timely manner; (vii) fulfilling special requests from our customers in relation to vessel refueling; and (viii) handling disputes, mainly in relation to quality and quantity issues on marine fuel, if any.

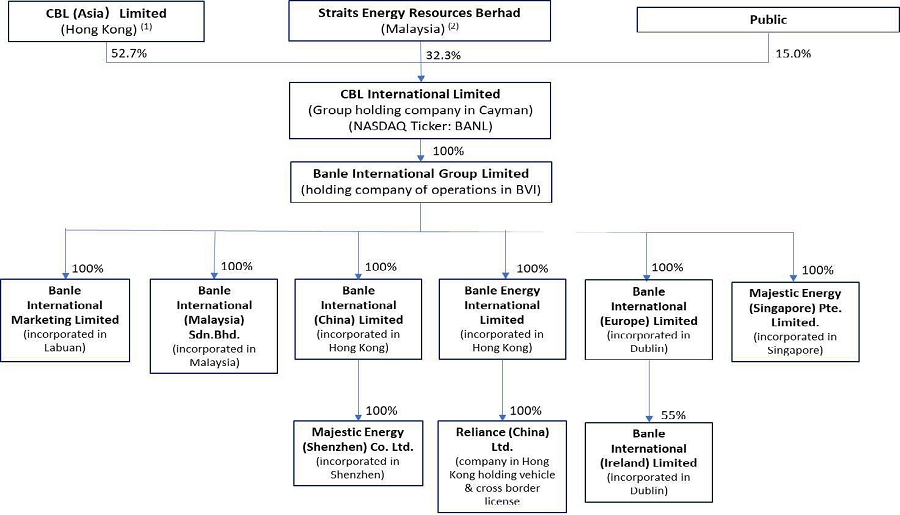

The subsidiaries of the Company, referred to as “the Group,” are listed as follows:

| Entity Name | Place of Incorporation | Percentage

of ownership |

Principal activities | |||

| CBL International Limited | Cayman Islands | Parent | Ultimate holding Company | |||

| Banle International Group Limited (“Banle BVI”) | British Virgin Islands | 100% by CBL International | Investment holding | |||

| Banle International Marketing Limited | Labuan, Malaysia | 100% by Banle BVI | Marketing service | |||

| Banle International (Malaysia) Sdn. Bhd. | Kuala Lumpur, Malaysia | 100% by Banle BVI | Sales and distribution of marine fuel | |||

| Banle Energy International Limited (“Banle HK”) | Hong Kong | 100% by Banle BVI | Sales and distribution of marine fuel | |||

| Reliance (China) Limited | Hong Kong | 100% by Banle HK | Business management | |||

| Banle International (China) Limited (“Banle China”) | Hong Kong | 100% by Banle BVI | Investment holding | |||

| Majestic Energy (Shenzhen) Co. Limited | PRC | 100% by Banle China | Investment holding (Dormant) | |||

| Majestic Energy (Singapore) Pte Limited | Singapore | 100% by Banle BVI | Sales and distribution of marine fuel | |||

| Banle International (Europe) Limited (“Banle Europe”) | Ireland | 100% by Banle BVI | Business management | |||

| Banle International (Ireland) Limited | Ireland | 55% by Banle Europe | Sales and distribution of marine fuel |

| 3 |

The following diagram illustrates our corporate structure:

(1) CBL (Asia) Limited is a limited liability company incorporated in Hong Kong which is owned as to 51% by Mr. Teck Lim Chia, our Chairman and Chief Executive Officer, 44% by Ms. Xiaoling Lu and 5% by Mr. Yuan He.

(2) Straits Energy Resources Berhad, or Straits, is a Malaysian company whose shares are listed on the ACE Market of Bursa Malaysia Securities Berhad (stock code: 0080).

August 2024 PIPE

On July 22, 2024, the Company entered into a Securities Purchase Agreement (the “SPA”) for a private placement (the “Private Placement”) with the PIPE Investor pursuant to which, the PIPE Investor agreed to purchase 2,500,000 Ordinary Shares of the Company (the “PIPE Shares”), par value $0.0001 per share, at a purchase price of $0.55 per share.

Upon the closing of the Private Placement on August 22, 2024, the PIPE Shares were issued, and the Company received gross proceeds of approximately $1.375 million before deducting any offering expenses payable by the Company. The net proceeds will be used to fund network development, alternative energy and biofuel supply development, future acquisitions as well as working capital and general corporate purposes.

Corporate Information

We are registered with the Registrar of Companies in the Cayman Islands under registration number CT-387046. Our principal executive offices are located at Level 23-2 Permata Sapura, Kuala Lumpur City Centre, 50088 Kuala Lumpur, Malaysia, and our telephone number is +60-3-2706-8280. The address of our website is https://www.banle-intl.com. Information contained on, or available through, our website does not constitute part of, and is not deemed incorporated by reference into, this prospectus. Our agent for service of process in the United States is Cogency Global Inc., located at 122 East 42nd Street, 18th Floor, New York, NY 10168.

| 4 |

| Issuer | CBL International Limited | |

| Resale of Ordinary Shares | 2,500,000 Ordinary Shares that were issued to the PIPE Investor in connection with the closing of a private placement offering pursuant to the SPA, including any additional securities that may become issuable by reason of share splits, share dividends or other similar transactions. | |

| Use of Proceeds | All of the Ordinary Shares offered by the selling securityholders pursuant to this prospectus will be sold by the selling securityholders for their respective accounts. We will not receive any of the proceeds from such sales. |

| 5 |

Investment in any securities offered pursuant to this prospectus and the applicable prospectus supplement involves risks. Before deciding whether to invest in our securities, you should carefully consider the risk factors described in our most recent 2023 Annual Report incorporated by reference into this prospectus and in our updates, if any, to those risk factors in our reports on Form 6-K incorporated by reference into this prospectus and all other information contained or incorporated by reference into this prospectus, as updated by our subsequent filings under the Exchange Act, and the risk factors and other information contained in the applicable prospectus supplement and any applicable free writing prospectus. The occurrence of any of these risks might cause you to lose all or part of your investment in the offered securities. There may be other unknown or unpredictable economic, business, competitive, regulatory or other factors that could have material adverse effects on our future results. Past financial performance may not be a reliable indicator of future performance, and historical trends should not be used to anticipate results or trends in future periods. If any of these risks actually occurs, our business, financial condition, results of operations or cash flow could be seriously harmed. This could cause the trading price of our securities to decline, resulting in a loss of all or part of your investment. Please also carefully read the section entitled “Cautionary Note Regarding Forward-Looking Statements” included herein and included in our most recent Annual Report on Form 20-F and our updates, if any, to that section in our reports on Form 6-K incorporated by reference into this prospectus.

| 6 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. Forward-looking statements provide our current expectations or forecasts of future events. Forward-looking statements include statements about our expectations, beliefs, plans, objectives, intentions, assumptions and other statements that are not historical facts. Words or phrases such as “anticipate,” “believe,” “can,” “continue,” “could,” “estimate,” “expect,” “forecast,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “possible,” “potential,” “predict,” “project,” “target,” “should,” “will” and “would,” or similar words or phrases, or the negatives of those words or phrases, may identify forward-looking statements, but the absence of these words does not necessarily mean that a statement is not forward-looking. Examples of forward-looking statements in this prospectus include, but are not limited to, statements concerning our operations, cash flows, financial position and dividend policy.

Forward-looking statements appear in a number of places in this prospectus including, without limitation, in the sections titled “Operating and Financial Review and Prospects,” and “Information on the Company” included in our 2023 Annual Report and 2024 Interim Results. These forward-looking statements include statements relating to:

| ● | our goal and strategies; |

| ● | our expansion plans; |

| ● | our future business development, financial condition and results of operations; |

| ● | expected changes in our revenues, costs or expenditures; |

| ● | the trends in, and size of, the bunkering markets in which we operate; |

| ● | our expectations regarding demand for, and market acceptance of, our products and services; |

| ● | our expectations regarding our relationships with customers, suppliers, third-party service providers, strategic partners and other stakeholders; |

| ● | competition in our industry; |

| ● | laws, regulations, and policies relating to the bunkering industry in the markets in which we operate; and |

| ● | general economic and business conditions. |

The risks and uncertainties include, but are not limited to:

| ● | future operating or financial results may fluctuate; |

| ● | expectations regarding the strength of future growth of the shipping industry, including the rates of annual demand and supply growth; |

| ● | geo-political events such as the conflict in Ukraine and the recent escalation of the Israel-Gaza conflict; |

| ● | the potential disruption of shipping routes, including due to low water levels in the Panama Canal and ongoing attacks by Houthis in the Red Sea; |

| ● | the length and severity of the ongoing outbreak of the novel coronavirus (COVID-19) around the world and governmental responses thereto; |

| ● | the overall health and condition of the U.S. and global financial markets; |

| 7 |

| ● | our financial condition and liquidity, including our ability to obtain additional financing to fund capital expenditures, vessel acquisitions and for other general corporate purposes and our ability to meet our financial covenants and repay our borrowings; |

| ● | our expectations relating to dividend payments and expectations of our ability to make such payments including the availability of cash and the impact of constraints under our loan agreements and financing arrangements; |

| ● | future acquisitions, business strategy and expected capital spending; |

| ● | general market conditions and shipping industry trends, including charter rates and factors affecting supply and demand; |

| ● | assumptions regarding interest rates and inflation; |

| ● | changes in the rate of growth of global and various regional economies; |

| ● | estimated future capital expenditures needed to preserve our capital base; |

| ● | our ability to capitalize on our management’s and directors’ relationships and reputations in the shipping industry to our advantage; |

| ● | changes in governmental and classification societies’ rules and regulations or actions taken by regulatory authorities; |

| ● | expectations about the availability of insurance on commercially reasonable terms; |

| ● | changes in laws and regulations (including environmental rules and regulations); |

| ● | potential liability from future litigation; and |

| ● | other important factors described from time to time in the reports we file with the SEC. |

These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described herein and in the “Risk Factors”, “Operating and Financial Review and Prospects” and elsewhere in our 2023 Annual Report and our 2024 Interim Results. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the future events and trends discussed in this report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements. CBL expressly disclaims any obligation or undertaking to release publicly any update or revision to any forward-looking statements contained herein to reflect any change in our expectations with respect to any such statement, or any change in events, conditions or circumstances on which any such statement is based.

You should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We are under no duty to update any of these forward-looking statements after the date of this report or to conform these statements to actual results or revised expectations.

| 8 |

All of the Ordinary Shares offered by the selling securityholders pursuant to this prospectus will be sold by the selling securityholders for their respective accounts. We will not receive any of the proceeds from such sales. We will pay certain expenses associated with the registration of the securities covered by this prospectus, as described in the section titled “Plan of Distribution.”

| 9 |

CAPITALIZATION AND INDEBTEDNESS

The following table sets forth our cash and cash equivalents and capitalization and indebtedness as of June 30, 2024 on:

| ● | an actual basis; and |

| ● | as adjusted to give effect to the issuance of 2,500,000 Ordinary Shares in connection with the PIPE. |

The information in this table should be read in conjunction with the financial statements and notes thereto and other financial information incorporated by reference in this prospectus and any prospectus supplement and the information under “Operating and Financial Review and Prospects” in our 2023 Annual Report and in our 2024 Interim Results, which are incorporated into this prospectus by reference. Our historical results do not necessarily indicate our expected results for any future periods.

| As of June 30, 2024 | ||||||||

| Actual (unaudited) | As Adjusted (unaudited) | |||||||

| Cash and cash equivalent | $ | 9,687,716 | $ | 10,992,716 | ||||

| Short-term lease liabilities | $ | 186,490 | $ | 186,490 | ||||

| Long-term lease liabilities | $ | 100,176 | $ | 100,176 | ||||

| Shareholders’ equity: | ||||||||

| Ordinary shares, $0.0001 par value, 500,000,000 shares authorized, 25,000,000 shares issued and outstanding as of June 30, 2024, 27,500,000 shares issued and outstanding as of September 20, 2024 | $ | 2,500 | $ | 2,750 | ||||

| Additional paid-in capital | $ | 12,536,087 | $ | 13,840,837 | ||||

| Retained earnings | $ | 11,226,987 | $ | 11,226,987 | ||||

| Total shareholders’ equity | $ | 23,765,574 | $ | 25,070,574 | ||||

| Total capitalization and indebtedness | $ | 24,052,240 | $ | 25,357,240 | ||||

| 10 |

We are an exempted company incorporated in the Cayman Islands with limited liability and our affairs are be governed by our Second Amended and Restated Memorandum of Association, the Cayman Islands Companies Act and the common law of the Cayman Islands.

Our current authorized share capital is US$50,000 divided into 500,000,000 Ordinary Shares, par value $0.0001 per share. All of our outstanding Ordinary Shares are validly issued, fully paid and non-assessable. Our Ordinary Shares are not redeemable and do not have any preemptive rights. As of the date of this prospectus, there are 27,500,000 Ordinary Shares issued and outstanding.

A reorganization of the Company’s legal entity structure was completed in August 2022. The reorganization involved the incorporation of CBL International Limited in February 2022, and the acquisition of Banle BVI by CBL International in August 2022. This transaction was treated as a recapitalization of the Company under common control and the financial statements give a retroactive effect to this transaction.

Banle BVI was set up in July 2020 with 50,000 shares at $1.00 per share issued to Mr. Chia, our Chairman and CEO. In February 2021, Banle BVI issued 490,323 shares in total, comprised of 304,000 shares issued to CBL (Asia) Limited (“CBL (Asia)”) and 186,323 shares to Straits Energy Resources Berhad (“Straits”). The 50,000 shares originally issued to Mr. Chia were surrendered and cancelled at the same time.

CBL International was incorporated in the Cayman Islands with limited liability on February 8, 2022, and was wholly owned by Mr. Chia, holding 50,000 shares of par value of $0.01 per share. In March 2022, each issued and unissued share was subdivided into 100 shares of par value of $0.0001 per share, and the authorized share capital became US$50,000 divided into 500,000,000 shares with $0.0001 par value per share. The number of shares held by Mr. Chia increased from 50,000 of par value of $0.01 per share to 5,000,000 of par value of $0.0001 each.

In August 2022, CBL (Asia) and Straits, as sellers, and CBL International, as purchaser, entered into a sale and purchase agreement, pursuant to which CBL International acquired the entire issued share capital of Banle BVI from its existing shareholders, CBL (Asia) and Straits, in consideration of which CBL International issued and allotted 13,175,000 shares and 8,075,000 shares, credited as fully paid, to CBL (Asia) and Straits, respectively. Upon completion of issuance and allotment of the shares to CBL (Asia) and Straits, the 5,000,000 shares of CBL International issued to Mr. Chia were surrendered and cancelled; and CBL International became the 100% shareholder of Banle BVI; CBL International being owned 62% by CBL (Asia) and 38% by Straits.

On March 23, 2023, the Company consummated the initial public offering of 3,325,000 ordinary shares, par value of $0.0001 per share at a price of $4.00 per share (the “Offering”), The Company’s underwriters exercised their over-allotment option in part for an additional 425,000 ordinary shares on March 27, 2023 (“Over-allotment Option”). The Over-allotment Option was closed with the Offering. Upon completion of the Offering, the ordinary share capital of the Company became $2,500, representing 25,000,000 shares of par value of $0.0001 per share.

Upon completion of issuance of the shares under the Offering, CBL International was effectively owned 52.7% by CBL (Asia), 32.3% by Straits and 15.0% by public shareholders.

| 11 |

This prospectus relates to the possible offer and sale from time to time of up to 2,500,000 Ordinary Shares, including any additional securities that may become issuable by reason of share splits, share dividends or other similar transactions. The PIPE Investor acquired Ordinary Shares pursuant to the SPA.

The selling securityholders may from time to time offer and sell any or all of the Ordinary Shares set forth below pursuant to this prospectus. When we refer to the “selling securityholders” in this prospectus, we mean the persons listed in the table below, and the pledgees, donees, transferees, assignees, successors and others who later are permitted to come to hold any of the selling securityholders’ interest in our securities after the date of this prospectus.

The following table is prepared based on information provided to us by the PIPE Investor. It sets forth the name and address of the PIPE Investor, the aggregate number of Ordinary Shares that the PIPE Investor may offer pursuant to this prospectus, and the beneficial ownership of the PIPE Investor both before and after the offering. We have based percentage ownership prior to this offering on 27,500,000 Ordinary Shares outstanding as of September 1, 2024.

The individuals and/or entities listed below have beneficial ownership over their respective securities. The SEC has defined “beneficial ownership” of a security to mean the possession, directly or indirectly, of voting power and/or investment power over such security. A shareholder is also deemed to be, as of any date, the beneficial owner of all securities that such shareholder has the right to acquire within 60 days after that date through (i) the exercise of any option, warrant or right, (ii) the conversion of a security, (iii) the power to revoke a trust, discretionary account or similar arrangement, or (iv) the automatic termination of a trust, discretionary account or similar arrangement. In computing the number of shares beneficially owned by a person and the percentage ownership of that person, Ordinary Shares subject to options or other rights (as set forth above) held by that person that are currently exercisable, or will become exercisable within 60 days thereafter, are deemed outstanding, while such shares are not deemed outstanding for purposes of computing percentage ownership of any other person.

We cannot advise you as to whether the selling securityholders will in fact sell any or all of such Ordinary Shares. In addition, the selling securityholders may sell, transfer or otherwise dispose of, at any time and from time to time, the Ordinary Shares in transactions exempt from the registration requirements of the Securities Act after the date of this prospectus, subject to applicable law.

Selling securityholder information for each additional selling securityholder, if any, will be set forth by prospectus supplement to the extent required prior to the time of any offer or sale of such selling securityholder’s securities pursuant to this prospectus. Any prospectus supplement may add, update, substitute, or change the information contained in this prospectus, including the identity of each selling securityholder and the number of Ordinary Shares registered on its behalf. A selling securityholder may sell all, some or none of such securities in this offering. See the section titled “Plan of Distribution.”

| Name of Selling Securityholder | Ordinary Shares Beneficially Owned Prior to the Offering | As a % of Ordinary Shares Outstanding | Number of Ordinary Shares Being Offered | Ordinary Shares Beneficially Owned After the Ordinary Shares are Sold | ||||||||||||||||

| Shares | Percent | |||||||||||||||||||

| Asian Strategy Limited | 2,500,000 | 9.1 | % | 2,500,000 | — | — | ||||||||||||||

| 12 |

MATERIAL U.S. FEDERAL INCOME AND FOREIGN TAX CONSEQUENCES

Material U.S. Federal Income Tax Consequences

General

The following is a summary of the material U.S. federal income tax consequences of owning and disposing of our ordinary shares. The discussion below of the U.S. federal income tax consequences to “U.S. Holders” will apply to a beneficial owner of our shares that is for U.S. federal income tax purposes:

| 1. | an individual citizen or resident of the U.S.; | ||

| 2. | a corporation (or other entity treated as a corporation) that is created or organized (or treated as created or organized) in or under the laws of the U.S., any state thereof or the District of Columbia; | ||

| 3. | an estate whose income is includible in gross income for U.S. federal income tax purposes regardless of its source; or | ||

| 4. | a trust if: | ||

| a) | a U.S. court can exercise primary supervision over the trust’s administration and one or more U.S. persons are authorized to control all substantial decisions of the trust; or | ||

| b) | it has a valid election in effect under applicable U.S. Treasury regulations to be treated as a U.S. person. | ||

If a beneficial owner of our shares is not described as a U.S. Holder and is not an entity treated as a partnership or other pass-through entity for U.S. federal income tax purposes, such owner will be considered a “Non-U.S. Holder.” The U.S. federal income tax consequences applicable specifically to non-U.S. Holders is described below under the heading “Tax Consequences to Non-U.S. Holders of Ordinary Shares.”

This summary is based on the Internal Revenue Code of 1986, as amended, or the Code, its legislative history, existing and proposed Treasury regulations promulgated thereunder, published rulings and court decisions, all as currently in effect. These authorities are subject to change or different interpretations, possibly on a retroactive basis.

This discussion does not address all aspects of U.S. federal income taxation that may be relevant to us or to any particular Holder of our shares based on such Holder’s individual circumstances. In particular, this discussion considers only Holders that own our shares as capital assets within the meaning of Section 1221 of the Code. This discussion also does not address the potential application of the alternative minimum tax or the U.S. federal income tax consequences to Holders that are subject to special rules, including:

| 1. | financial institutions or financial services entities; | |

| 2. | broker-dealers; | |

| 3. | taxpayers who have elected mark-to-market accounting; | |

| 4. | tax-exempt entities; | |

| 5. | governments or agencies or instrumentalities thereof; | |

| 6. | insurance companies; | |

| 7. | regulated investment companies; |

| 13 |

| 8. | real estate investment trusts; | |

| 9. | certain expatriates or former long-term residents of the U.S.; | |

| 10. | persons that actually or constructively own 5% or more of our voting shares; | |

| 11. | persons that acquired our shares pursuant to the exercise of employee stock options, in connection with employee stock incentive plans or otherwise as compensation; | |

| 12. | persons that hold our shares as part of a straddle, constructive sale, hedging, conversion or other integrated transaction; or | |

| 13. | persons whose functional currency is not the U.S. Dollars. |

This discussion does not address any aspect of U.S. federal non-income tax laws, such as gift or estate tax laws, or state, local or non-U.S. tax laws. Additionally, this discussion does not consider the tax treatment of partnerships or other pass-through entities or persons who hold our securities through such entities. If a partnership (or other entity classified as a partnership for U.S. federal income tax purposes) is the beneficial owner of our shares, the U.S. federal income tax treatment of a partner in the partnership will generally depend on the status of the partner and the activities of the partnership. This discussion also assumes that any distribution made (or deemed made) regarding our shares and any consideration received (or deemed received) by a Holder connected with selling or other disposition of such shares will be in U.S. Dollars.

We have not sought, and will not seek, a ruling from the Internal Revenue Service (the “IRS”), or an opinion of counsel as to any U.S. federal income tax consequence described herein. The IRS may disagree with one or more aspects of the discussion herein, and its determination may be upheld by a court. Moreover, there can be no assurance that future legislation, regulations, administrative rulings or court decisions will not adversely affect the accuracy of the statements in this discussion.

BECAUSE OF THE COMPLEXITY OF THE TAX LAWS AND BECAUSE THE TAX CONSEQUENCES TO THE COMPANY OR TO ANY PARTICULAR HOLDER OF OUR SECURITIES MAY BE AFFECTED BY MATTERS NOT DISCUSSED HEREIN, EACH HOLDER OF OUR SECURITIES IS URGED TO CONSULT WITH ITS TAX ADVISOR REGARDING THE SPECIFIC TAX CONSEQUENCES OF THE OWNERSHIP AND DISPOSITION OF OUR SECURITIES, INCLUDING THE APPLICABILITY AND EFFECT OF STATE, LOCAL AND NON-U.S. TAX LAWS, AS WELL AS U.S. FEDERAL TAX LAWS AND APPLICABLE TAX TREATIES.

Tax Consequences to U.S. Holders of Ordinary Shares

Taxation of Distributions Paid on Ordinary Shares

Subject to the passive foreign investment company, or PFIC, rules discussed below, a U.S. Holder generally will be required to include in gross income as ordinary income the amount of any cash dividend paid on our ordinary shares. A cash distribution on such shares will be treated as a dividend for U.S. federal income tax purposes to the extent the distribution is paid out of our current or accumulated earnings and profits (as determined for U.S. federal income tax purposes). Such dividend will not be eligible for the dividends-received deduction generally allowed to domestic corporations regarding dividends received from other domestic corporations. Any distributions in excess of such earnings and profits generally will be applied against and reduce the U.S. Holder’s basis in its ordinary shares and, to the extent in excess of such basis, will be treated as gain from the sale or exchange of such ordinary shares.

Non-corporate U.S. Holders of our Ordinary Shares should expect that dividends may be taxed at the lower applicable long-term capital gains rate (see “— Taxation on the Disposition of Ordinary Shares” below) provided that:

| 1. | our ordinary shares are readily tradable on an established securities market in the U.S. or, in the event we are deemed to be a Chinese “resident enterprise” under the Enterprise Income Tax (EIT) Law, we are eligible for the benefits of the Agreement between the Government of the United States of America and the Government of the People’s Republic of China for the Avoidance of Double Taxation and the Prevention of Tax Evasion regarding Taxes on Income, or the “U.S.-PRC Tax Treaty” as a “qualified foreign corporation” under Section 1(h)(11)(C)(i)(II) of the Code; |

| 14 |

| 2. | we are not a PFIC, as discussed below, for either the taxable year in which the dividend was paid or the preceding taxable year; and | |

| 3. | certain holding period requirements are met. Under the Code, long-term capital gains recognized by non-corporate U.S. Holders are generally subject to U.S. federal income tax at a reduced rate of tax. Capital gain or loss will constitute long-term capital gain or loss if the U.S. Holder’s holding period for the Ordinary Shares exceeds one year. |

Subject to certain exceptions, a qualified foreign corporation is any foreign corporation that is either (i) incorporated in a possession of the U.S., or (ii) eligible for benefits of a comprehensive income tax treaty with the U.S. that includes an exchange of information program.

If we are not able to maintain listing on Nasdaq, it is anticipated that our ordinary shares will be quoted and traded only on the OTC Bulletin Board. In that case, any dividends paid on our ordinary shares would not qualify for the lower rate unless we are deemed to be a Chinese “resident enterprise” under the EIT Law and are eligible for the benefits of the U.S.-PRC Tax Treaty.

U.S. Holders should consult their own tax advisors regarding the availability of the lower rate for any dividends paid regarding our ordinary shares.

If PRC taxes apply to dividends paid to a U.S. Holder on our ordinary shares, such U.S. Holder may be entitled to a reduced rate of PRC tax under the U.S-PRC Tax Treaty. In addition, direct PRC taxes may be treated as foreign taxes eligible for credit against such Holder’s U.S. federal income tax liability (subject to certain limitations). U.S. Holders should consult their own tax advisors regarding the creditability of any such PRC tax and their eligibility for the benefits of the U.S.-PRC Tax Treaty.

Taxation on the Disposition of Ordinary Shares

Upon a sale or other taxable disposition of our ordinary shares, and subject to the PFIC rules discussed below, a U.S. Holder should recognize capital gain or loss in an amount equal to the difference between (i) the sum of the amount of cash and the fair market value of any property received in such disposition and (ii) the U.S. Holder’s adjusted tax basis in the ordinary shares.

Capital gains recognized by U.S. Holders generally are subject to U.S. federal income tax at the same rate as ordinary income, except that long-term capital gains recognized by non-corporate U.S. Holders are generally subject to U.S. federal income tax at a maximum rate of 20% for taxable years beginning on and after January 1, 2013. Capital gain or loss will constitute long-term capital gain or loss if the U.S. Holder’s holding period for the ordinary shares exceeds one year. The deductibility of capital losses is subject to various limitations.

If PRC taxes would otherwise apply to any gain from the disposition of our ordinary shares by a U.S. Holder, such U.S. Holder may be entitled to a reduction in or elimination of such taxes under the U.S.-PRC Tax Treaty. Certain PRC taxes that are paid by a U.S. Holder regarding such gain may be treated as foreign taxes eligible for credit against such Holder’s U.S. federal income tax liability (subject to certain limitations which could reduce or eliminate the available tax credit). U.S. Holders should consult their own tax advisors regarding the creditability of any such PRC tax and their eligibility for the benefits of the U.S.-PRC Tax Treaty.

U.S. Holders that are individuals, estates or trusts and whose income exceeds certain thresholds generally will be subject to a 3.8% Medicare contribution tax on unearned income, including, among other things, cash dividends on, and capital gains from the sale or other taxable disposition of, our ordinary shares, subject to certain limitations and exceptions. U.S. Holders should consult their own tax advisors regarding the effect, if any, of such tax on their ownership and disposition of our ordinary shares.

| 15 |

Passive Foreign Investment Company Rules

Certain adverse U.S. federal income tax consequences could apply to a U.S. Holder if a foreign corporation, or any of its subsidiaries, is treated as a PFIC for any taxable year during which the U.S. Holder holds its securities. A foreign (i.e., non-U.S.) corporation will be a PFIC if at least 75% of its gross income in a taxable year of the foreign corporation, including its pro rata share of the gross income of any corporation in which it is considered to own at least 25% of the shares by value, is passive income. Alternatively, a foreign corporation will be a PFIC if at least 50% of its assets in a taxable year of the foreign corporation, ordinarily determined based on fair market value and averaged quarterly over the year, including its pro rata share of the assets of any corporation in which it is considered to own at least 25% of the shares by value, are held for the production of, or produce, passive income. Passive income generally includes dividends, interest, rents and royalties (other than certain rents or royalties derived from the active conduct of a trade or business) and gains from the disposition of passive assets.

Although PFIC status is determined on an annual basis and generally cannot be determined until the end of a taxable year, based on the nature of our current and expected income and the current and expected value and composition of our assets, we do not presently expect to be a PFIC for our current taxable year or the foreseeable future. However, there can be no assurance given in this regard because the determination of whether we are or will become a PFIC is a fact-intensive inquiry made on an annual basis that depends, in part, upon the composition of our income and assets. In addition, there can be no assurance that the IRS will agree with our conclusion or that the IRS would not successfully challenge our position.

If we are determined to be a PFIC and a U.S. Holder did not make either a timely qualified electing fund, or QEF, election for our first taxable year as a PFIC in which the U.S. Holder held (or was deemed to hold) ordinary shares, or a mark-to-market election, as described below, such Holder generally will be subject to special rules regarding:

| 1. | any gain recognized by the U.S. Holder on the sale or other disposition of its ordinary shares; and | |

| 2. | any “excess distribution” made to the U.S. Holder (generally, any distributions to such U.S. Holder during a taxable year of the U.S. Holder that are greater than 125% of the average annual distributions received by such U.S. Holder regarding the ordinary shares during the three preceding taxable years of such U.S. Holder or, if shorter, such U.S. Holder’s holding period for the ordinary shares). |

Under these rules:

| 1. | the U.S. Holder’s gain or excess distribution will be allocated ratably over the U.S. Holder’s holding period for the ordinary shares; | |

| 2. | the amount allocated to the U.S. Holder’s taxable year in which the U.S. Holder recognized the gain or received the excess distribution, or to the period in the U.S. Holder’s holding period before the first day of our first taxable year in which we are a PFIC, will be taxed as ordinary income; | |

| 3. | the amount allocated to other taxable years (or portions thereof) of the U.S. Holder and included in its holding period will be taxed at the highest tax rate in effect for that year and applicable to the U.S. Holder; and | |

| 4. | the interest charge generally applicable to underpayments of tax will be imposed regarding the tax attributable to each such year of the U.S. Holder. |

In general, a U.S. Holder may avoid the PFIC tax consequences described above in respect to our ordinary shares by making a timely QEF election to include in income its pro rata share of our net capital gains (as long-term capital gain) and other earnings and profits (as ordinary income), on a current basis, in each case whether or not distributed, in the taxable year of the U.S. Holder in which or with which our taxable year ends. There can be no assurance, however, that we will pay current dividends or make other distributions sufficient for a U.S. Holder who makes a QEF election to satisfy the tax liability attributable to income inclusions under the QEF rules, and the U.S. Holder may have to pay the resulting tax from its other assets. A U.S. Holder may make a separate election to defer the payment of taxes on undistributed income inclusions under the QEF rules, but if deferred, any such taxes will be subject to an interest charge.

| 16 |

The QEF election is made on a shareholder-by-shareholder basis and, once made, can be revoked only with the consent of the IRS. A U.S. Holder generally makes a QEF election by attaching a completed IRS Form 8621 (Return by a Shareholder of a Passive Foreign Investment Company or Qualified Electing Fund), including the information provided in a PFIC annual information statement, to a timely filed U.S. federal income tax return for the tax year to which the election relates.

Retroactive QEF elections generally may be made only by filing a protective statement with such return and if certain other conditions are met or with the consent of the IRS. To comply with the requirements of a QEF election, a U.S. Holder must receive certain information from us. Upon request from a U.S. Holder, we will endeavor to provide to the U.S. Holder no later than 90 days after the request such information as the IRS may require, including a PFIC annual information statement, in order to enable the U.S. Holder to make and maintain a QEF election. However, there is no assurance that we will have timely knowledge of our status as a PFIC in the future or of the required information to be provided.

If a U.S. Holder has made a QEF election regarding our ordinary shares, and the special tax and interest charge rules do not apply to such shares (because of a timely QEF election for our first taxable year as a PFIC in which the U.S. Holder holds (or is deemed to hold) such shares), any gain recognized on the appreciation of our ordinary shares generally will be taxable as capital gain and no interest charge will be imposed. As discussed above, U.S. Holders of a QEF are currently taxed on their pro rata shares of its earnings and profits, whether or not distributed. In such case, a subsequent distribution of such earnings and profits that were previously included in income generally should not be taxable as a dividend to those U.S. Holders who made a QEF election. The tax basis of a U.S. Holder’s shares in a QEF will be increased by amounts that are included in income, and decreased by amounts distributed but not taxed as dividends, under the above rules. Similar basis adjustments apply to property if by reason of holding such property the U.S. Holder is treated under the applicable attribution rules as owning shares in a QEF.

A determination as to our PFIC status will be made annually. But, an initial determination that our Company is a PFIC will generally apply for subsequent years to a U.S. Holder who held ordinary shares while we were a PFIC, whether or not we meet the test for PFIC status in those years. A U.S. Holder who makes the QEF election discussed above for our first taxable year as a PFIC in which the U.S. Holder holds (or is deemed to hold) our ordinary shares, however, will not be subject to the PFIC tax and interest charge rules discussed above in respect to such shares. In addition, such U.S. Holder will not be subject to the QEF inclusion regime regarding such shares for any taxable year of ours that ends within or with a taxable year of the U.S. Holder and in which we are not a PFIC. But, if the QEF election is not effective for each of our taxable years in which we are a PFIC and the U.S. Holder holds (or is deemed to hold) our ordinary shares, the PFIC rules discussed above will continue to apply to such shares unless the Holder makes a purging election, and pays the tax and interest charge regarding the gain inherent in such shares attributable to the pre-QEF election period.

Alternatively, if a U.S. Holder, at the close of its taxable year, owns shares in a PFIC that are treated as marketable stock, the U.S. Holder may make a mark-to-market election regarding such shares for such taxable year. If the U.S. Holder makes a valid mark-to-market election for the first taxable year of the U.S. Holder in which the U.S. Holder holds (or is deemed to hold) shares in us and for which we are determined to be a PFIC, such Holder generally will not be subject to the PFIC rules described above in respect to its ordinary shares. Instead, in general, the U.S. Holder will include as ordinary income each year the excess, if any, of the fair market value of its ordinary shares at the end of its taxable year over the adjusted basis in its ordinary shares. The U.S. Holder also will be allowed to take an ordinary loss regarding the excess, if any, of the adjusted basis of its ordinary shares over the fair market value of its ordinary shares at the end of its taxable year (but only to the extent of the net amount of previously included income as a result of the mark-to-market election). The U.S. Holder’s basis in its ordinary shares will be adjusted to reflect any such income or loss amounts, and any further gain recognized on a sale or other taxable disposition of the ordinary shares will be treated as ordinary income.

The mark-to-market election is available only for stock that is regularly traded on a national securities exchange that is registered with the SEC, or on a foreign exchange or market that the IRS determines has rules sufficient to establish that the market price represents a legitimate and sound fair market value. We became listed on the NASDAQ Stock Market in March 2023, but if we are not able to maintain such a listing, our ordinary shares may be quoted and traded only on the OTC Bulletin Board. If our ordinary shares were to be quoted and traded only on the OTC Bulletin Board, such shares may not currently qualify as marketable stock for purposes of the election. U.S. Holders should consult their own tax advisors regarding the availability and tax consequences of a mark-to-market election in respect to our ordinary shares under their particular circumstances.

| 17 |

If we are a PFIC and, at any time, have a foreign subsidiary that is classified as a PFIC, U.S. Holders generally would be deemed to own a portion of the shares of such lower-tier PFIC, and generally could incur liability for the deferred tax and interest charge described above if we receive a distribution from, or dispose of all or part of our interest in, the lower-tier PFIC. Upon request, we will endeavor to cause any lower-tier PFIC to provide to a U.S. Holder no later than 90 days after the request the information that may be required to make or maintain a QEF election regarding the lower-tier PFIC. However, there is no assurance that we will have timely knowledge of the status of any such lower-tier PFIC or will be able to cause the lower-tier PFIC to provide the required information. U.S. Holders are urged to consult their own tax advisors regarding the tax issues raised by lower-tier PFICs.

If a U.S. Holder owns (or is deemed to own) shares during any year in a PFIC, such Holder may have to file an IRS Form 8621 (whether or not a QEF election or mark-to-market election is made).

The rules dealing with PFICs and with the QEF and mark-to-market elections are very complex and are affected by various factors in addition to those described above. Accordingly, U.S. Holders of our ordinary shares should consult their own tax advisors concerning the application of the PFIC rules to our ordinary shares under their particular circumstances.

Tax Consequences to Non-U.S. Holders of Ordinary Shares

Dividends paid to a non-U.S. Holder in respect to its ordinary shares generally will not be subject to U.S. federal income tax, unless the dividends are effectively in connection with the non-U.S. Holder’s conduct of a trade or business within the U.S. (and, if required by an applicable income tax treaty, are attributable to a permanent establishment or fixed base that such Holder maintains in the U.S.).

In addition, a non-U.S. Holder generally will not be subject to U.S. federal income tax on any gain attributable to a sale or other disposition of our ordinary shares, unless such gain is effectively in connection with its conduct of a trade or business in the U.S. (and, if required by an applicable income tax treaty, is attributable to a permanent establishment or fixed base that such Holder maintains in the U.S.) or the non-U.S. Holder is an individual who is present in the U.S. for 183 days or more in the taxable year of sale or other disposition and certain other conditions are met (in which case, such gain from U.S. sources generally is subject to tax at a 30% rate or a lower applicable tax treaty rate).

Dividends and gains that are effectively in connection with the non-U.S. Holder’s conduct of a trade or business in the U.S. (and, if required by an applicable income tax treaty, are attributable to a permanent establishment or fixed base in the U.S.) generally will be subject to tax in the same manner as for a U.S. Holder and, in the case of a non-U.S. Holder that is a corporation for U.S. federal income tax purposes, may also be subject to an additional branch profits tax at a 30% rate or a lower applicable tax treaty rate.

Backup Withholding and Information Reporting

In general, information reporting for U.S. federal income tax purposes should apply to distributions made on our ordinary shares within the U.S. to a non-corporate U.S. Holder and to the proceeds from sales and other dispositions of our ordinary shares by a non-corporate U.S. Holder to or through a U.S. office of a broker. Payments made (and sales and other dispositions effected at an office) outside the U.S. will be subject to information reporting in limited circumstances. In addition, backup withholding of United States federal income tax, currently at a rate of 24%, generally will apply to dividends paid on our ordinary shares to a non-corporate U.S. Holder and the proceeds from sales and other dispositions of shares by a non-corporate U.S. Holder, in each case who:

| 1. | fails to provide an accurate taxpayer identification number; | |

| 2. | is notified by the IRS that backup withholding is required; or | |

| 3. | in certain circumstances, fails to comply with applicable certification requirements. |

| 18 |

A non-U.S. Holder generally may eliminate the requirement for information reporting and backup withholding by providing certification of its foreign status, under penalties of perjury, on a duly executed applicable IRS Form W-8 or by otherwise establishing an exemption.

Backup withholding is not an additional tax. Rather, the amount of any backup withholding will be allowed as a credit against a U.S. Holder’s or a non-U.S. Holder’s U.S. federal income tax liability and may entitle such Holder to a refund, provided that certain required information is timely furnished to the IRS. Holders are urged to consult their own tax advisors regarding the application of backup withholding and the availability of and procedure for obtaining an exemption from backup withholding in their particular circumstances.

For taxable years beginning after March 18, 2010, individual U.S. Holders may be required to report ownership of our ordinary shares and certain related information on their individual federal income tax returns in certain circumstances. Generally, this reporting requirement will apply if: (1) the ordinary shares are held in an account of the individual U.S. Holder maintained with a “foreign financial institution”; or (2) the ordinary shares are not held in an account maintained with a “financial institution,” as such terms are defined in the Code. The reporting obligation will not apply to an individual, however, unless the total aggregate value of the individual’s foreign financial assets exceeds $50,000 during a taxable year.

For clarification, this reporting requirement should not apply to ordinary shares held in an account with a U.S. brokerage firm. Not complying with this reporting requirement, if it applies, will result in substantial penalties. In certain circumstances, additional tax and other reporting requirements may apply. U.S. Holders of our ordinary shares are advised to consult with their own tax advisors concerning all such reporting requirements.

Cayman Islands Taxation

The Cayman Islands currently levies no taxes on individuals or corporations based upon profits, income, gains or appreciation and there is no taxation in the nature of inheritance tax or estate duty. There are no other taxes likely to be material to the Company or its shareholders levied by the Government of the Cayman Islands except for stamp duties which may be applicable on instruments executed in or brought within Cayman Islands. The Cayman Islands is not party to any double-tax treaties that are applicable to any payments made to or by the Company save and except that the Cayman Islands is a party to a double tax treaty entered into with the United Kingdom in 2010. There are no exchange control regulations or currency restrictions in the Cayman Islands.

People’s Republic of China Taxation

Pursuant to the Arrangement between China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and Tax Evasion on Income, or the Tax Arrangement, where a Hong Kong resident enterprise which is considered a non-PRC tax resident enterprise directly holds at least 25% of a PRC enterprise, the withholding tax rate in respect of the payment of dividends by such PRC enterprise to such Hong Kong resident enterprise is reduced to 5% from a standard rate of 10%, subject to approval of the PRC local tax authority. Pursuant to the Notice of the State Administration of Taxation on the Issues concerning the Application of the Dividend Clauses of Tax Agreements, or Circular 81, a resident enterprise of the counter-party to such Tax Arrangement should meet the following conditions, among others, in order to enjoy the reduced withholding tax under the Tax Arrangement: (i) it must directly own the required percentage of equity interests and voting rights in such PRC resident enterprise; and (ii) it should directly own such percentage in the PRC resident enterprise anytime in the 12 months prior to receiving the dividends. Furthermore, the Administrative Measures for Non-Resident Enterprises to Enjoy Treatments under Tax Treaties, or the Administrative Measures, which became effective in January 2020, requires that non-resident enterprises adopt the process of “self-assessment, declaration of entitlement, and bookkeeping for inspection” with the relevant tax authority in order to enjoy the reduced withholding tax rate under the tax treaties. There are also other conditions for enjoying such reduced withholding tax rate according to other relevant tax rules and regulations.

| 19 |

Hong Kong Taxation

The taxation of income and capital gains of holders of ordinary shares is subject to the laws and practices of Hong Kong and of jurisdictions in which holders of ordinary shares are resident or otherwise subject to tax. The following summary of certain relevant taxation provisions under Hong Kong law is based on current law and practice, is subject to changes therein and does not constitute legal or tax advice. The discussion does not deal with all possible tax consequences relating to an investment in the ordinary shares. Accordingly, each prospective investor (particularly those subject to special tax rules, such as banks, dealers, insurance companies and tax-exempt entities) should consult its own tax advisor regarding the tax consequences of an investment in the ordinary shares. The discussion is based upon laws and relevant interpretations thereof in effect as of the date of this report, all of which are subject to change. There is no reciprocal tax treaty in effect between Hong Kong and the United States.

Tax on Dividends

Under the current practices of the Hong Kong Inland Revenue Department, no tax is payable in Hong Kong in respect of dividends paid by us as a company incorporated in Cayman Islands.

Profits Tax

No tax is imposed in Hong Kong in respect of capital gains from the sale of shares. Trading gains from the sale of shares by persons carrying on a trade, profession or business in Hong Kong where such gains are derived from or arise in Hong Kong from such trade, profession or business will be chargeable to Hong Kong profits tax, which is currently imposed at the rate of 16.5% and 15% on corporations and unincorporated businesses, respectively, and at a maximum rate of 15% on individuals. Liability for Hong Kong profits tax may thus arise in respect of trading gains from sales of shares realized by persons carrying on a business or trading or dealing in securities in Hong Kong.

Malaysia Taxation

Income Tax Act 1967

Pursuant to the Income Tax Act 1967 (“ITA 1967”), income tax shall be charged for each year of assessment upon the income of any person accruing in or derived from Malaysia or received in Malaysia from outside Malaysia. Section 7 of ITA 1967 defines tax resident, amongst others, as an individual who has been residing in Malaysia for 182 days or more of the tax year.

A company will be a tax resident in Malaysia if its management and control of business are exercised in Malaysia.

Resident companies with a paid-up capital of RM2,500,000 or more and non-resident companies are subject to a tax rate of 24% with effect from the year of assessment 2020. In cases of resident companies with a paid-up capital of less than RM2,500,000 and gross business income of not more than RM50,000,000, they are taxed at the rate of 15% for the first RM150,000, 17% on the next RM450,000 and 24% for any sum in excess of RM600,000.

Withholding Tax

Malaysia imposes a withholding tax on certain payments to non-residents, including, without limitation, royalties, technical fees, installation fees and rental of movable property. The rate of withholding tax is generally between 10% and 15% unless there is a double-taxation agreement between Malaysia and the country of the non-resident, in which case, the withholding tax rate may be reduced.

Taxes on Dividends

There is no further income tax on dividends received from a Malaysian company. Tax imposed on the company’s profits will be the final tax and dividends distributed to the Shareholders will not be subject to further tax.

| 20 |

This prospectus relates to the offer and sale from time to time by the selling securityholder or their permitted transferees (collectively, the “selling securityholders”) of up to 2,500,000 Ordinary Shares issued to certain securityholders in connection with the closing of a private placement offering pursuant to the SPA. This prospectus also covers any additional securities that may become issuable by reason of share splits, share dividends or other similar transactions. All of the Ordinary Shares offered by the selling securityholders pursuant to this prospectus will be sold by the selling securityholders for their respective accounts. We will not receive any of the proceeds from such sales.

The selling securityholders will pay any underwriting discounts and commissions and expenses incurred by the selling securityholders for brokerage, accounting, tax or legal services or any other expenses incurred by the selling securityholders in disposing of the securities. Unless otherwise agreed with the selling securityholders, we will bear all other costs, fees and expenses incurred in effecting the registration of the securities covered by this prospectus, including, without limitation, all registration and filing fees, Nasdaq listing fees and fees and expenses of our counsel and our independent registered public accountants.

The securities beneficially owned by the selling securityholders covered by this prospectus may be offered and sold from time to time by the selling securityholders. The selling securityholders will act independently of us in making decisions with respect to the timing, manner and size of each sale. Such sales may be made on one or more exchanges or in the over-the-counter market or otherwise, at prices and under terms then prevailing or at prices related to our then current market price or in negotiated transactions. Each selling securityholder reserves the right to accept and, together with its respective agents, to reject, any proposed purchase of securities to be made directly or through agents. The selling securityholders and any of their permitted transferees may sell their securities offered by this prospectus on any stock exchange, market or trading facility on which the securities are traded or in private transactions.

The selling securityholders may use any one or more of the following methods when selling the securities offered by this prospectus:

| ● | purchases by a broker-dealer as principal and resale by such broker-dealer for its own account pursuant to this prospectus; |

| ● | ordinary brokerage transactions and transactions in which the broker solicits purchasers; |

| ● | block trades in which the broker-dealer so engaged will attempt to sell the securities as agent but may position and resell a portion of the block as principal to facilitate the transaction; |

| ● | an over-the-counter distribution in accordance with the rules of Nasdaq; |