Confidential Draft No. 4 as confidentially submitted to the Securities and Exchange Commission on December 2, 2022. This draft registration statement has not been publicly filed with the Securities and Exchange Commission and all information herein remains strictly confidential.

Registration No. 333- [●]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MED EIBY HOLDING CO., LIMITED

(Exact name of Registrant as specified in its charter)

Not

Applicable

(Translation of Registrant’s name into English)

| Cayman Islands | 5047 | Not Applicable | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification Number) |

8th Floor, Yifang Building, No. 315 Shuangming Avenue,

Dongzhou Community, Guangming Street, Guangming District,

Shenzhen, Guangdong, People’s Republic of China, 518107.

0755-

26416184

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

[*]

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Ying Li, Esq. Guillaume de Sampigny, Esq. Lisa Forcht, Esq. Hunter Taubman Fischer & Li LLC New York, NY 10005 |

Benjamin Tan, Esq. Sichenzia Ross Ference LLP 1185 Avenue of the Americas, 31st Floor, New York, NY 10036 212-930-9700 |

Approximate date of commencement of proposed sale to the public: as soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company x

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ¨

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered |

Proposed maximum offering price per share(1) |

Proposed maximum aggregate offering price(2) |

Amount of registration fee |

||||||||||||

| Ordinary Shares, par value US$0.001 per share(5) | US$ | US$ | US$ | |||||||||||||

| Underwriter’s warrants(3) | US$ | US$ | US$ | |||||||||||||

| Ordinary Shares underlying underwriter’s warrants(4) | US$ | US$ | US$ | |||||||||||||

| Total Registration Fee | US$ | |||||||||||||||

| (1) | There is no current market for the securities or price at which the shares are being offered. Estimated solely for the purpose of determining the amount of registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended (the “Securities Act”). |

| (2) | Pursuant to Rule 416 under the Securities Act, there is also being registered hereby an indeterminate number of additional Ordinary Shares of the Registrant as may be issued or issuable because of stock splits, stock dividends, stock distributions, and similar transactions. |

| (3) | No fee required pursuant to Rule 457(g) of the Securities Act. |

| (4) | Representing Ordinary Shares underlying underwriter’s warrants to purchase up to an aggregate of 7% of the Ordinary Shares sold in the offering, at an exercise price equal to the public offering price. As estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act, the proposed maximum aggregate offering price of the underwriter’s warrants is [$__________]. The Ordinary Shares underlying the underwriter’s warrants are exercisable within five years from the issuance. For additional information regarding our arrangement with the underwriter, please see “Underwriting” beginning on page 184. |

| (5) | Includes (a) [ ] Ordinary Shares; and (b) up to 15% of the total number of Ordinary Shares to be offered by us pursuant to this offering that may be purchased by the underwriter pursuant to its over-allotment option to purchase additional shares. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION

PRELIMINARY PROSPECTUS, DATED [*], 2022

[___] Ordinary Shares

MED EIBY HOLDING CO., LIMITED

This is an initial public offering, or the “offering,” of [__] ordinary shares, par value US$0.001 per share (each, an “Ordinary Share,” and, collectively, the “Ordinary Shares”) of MED EIBY Holding Co., Limited, a Cayman Islands exempted company with limited liability whose principal place of business is in Shenzhen, the People’s Republic of China, on a firm commitment basis.

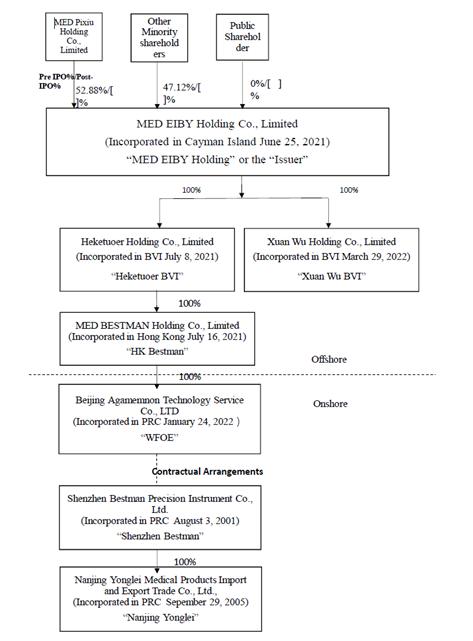

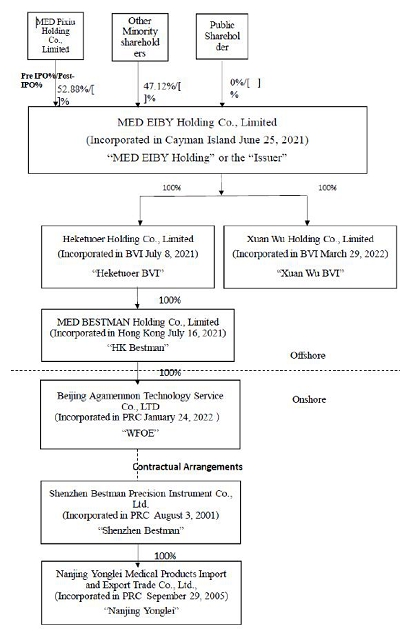

Throughout this prospectus, unless the context indicates otherwise, the terms “we,” “our,” and “our Company,” only refers to MED EIBY Holding Co., Limited, the Cayman Islands holding company, the term “the WFOE” or “our WFOE” refers to Beijing Agamemnon Technology Service Co., Ltd, a limited liability company organized under the laws of the People’s Republic of China (the “PRC”), the terms “Shenzhen Bestman,” or “the VIE” refers to Shenzhen Bestman Precision Instrument Co., Ltd., a limited liability company organized under the laws of the PRC, the term “Nanjing Yonglei” refers to Nanjing Yonglei Medical Products Import and Export Trade Co., Ltd., a PRC wholly-owned subsidiary of the VIE, and the term “the PRC operating entities” refers to the VIE and its subsidiary, Nanjing Yonglei.

Prior to this offering, there has been no public market for our Ordinary Shares. We expect that the initial public offering price of our Ordinary Share will be [*] per Ordinary Share. Currently no public market exists for the Ordinary Share.

We expect to list the Ordinary Shares on the Nasdaq Capital Market (“Nasdaq”) under the symbol “BSME.” At this time, Nasdaq has not yet approved our application to list our Ordinary Shares. The closing of this offering is conditioned upon Nasdaq’s final approval of our listing application, and there is no guarantee or assurance that our Ordinary Shares will be approved for listing on Nasdaq.

Investing in our Ordinary Shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 23 to read about factors you should consider before buying our Ordinary Shares.

We are a holding company incorporated in the Cayman Islands and not a Chinese operating company. The Ordinary Shares offered in this offering are shares of our offshore holding company instead of shares of the VIE or its subsidiary in China. As a holding company with no material operations of our own, the majority of our operations are conducted through the PRC operating entities. Due to PRC legal restrictions on foreign ownership in certain internet-related businesses we may explore and operate in the future, we do not have any equity ownership of the VIE. We control and receive the economic benefits of the VIE and its subsidiary business operations through certain contractual arrangements (the “VIE Agreements”) which enable us to consolidate the financial results of the VIE and its subsidiary in our consolidated financial statements for accounting purposes only because we met the conditions under the United States generally accepted accounting principles, or U.S. GAAP, to consolidate the VIE.

Under U.S. GAAP, the Company is deemed to have a controlling financial interest in, and be the primary beneficiary of, the VIE for accounting purposes, because pursuant to the VIE Agreements, the VIE shall pay service fees in an amount equivalent to all of its net income to our WFOE, while WFOE has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance, has the obligation to absorb the expected losses of the VIE, and has the right to receive substantially all of the economic benefits of the VIE. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of WFOE and, ultimately, the Company. As such, the Company is deemed to be the primary beneficiary of the VIE for accounting purposes and must consolidate the VIE because it met the conditions under U.S. GAAP to consolidate the VIE.

The VIE structure involves unique risks to investors and the VIE Agreements have not been tested in a court of law in China as of the date of this prospectus. Through the VIE Agreements among our WFOE, the VIE, and Shenzhen Bestman’s shareholders (the “VIE Shareholders”), we are regarded as the primary beneficiary of Shenzhen Bestman and its subsidiary, Nanjing Yonglei, for accounting purposes, and, therefore, we are able to consolidate the financial results of Shenzhen Bestman and Nanjing Yonglei in our consolidated financial statements in accordance with U.S. GAAP.

However, the VIE structure cannot completely replicate a foreign investment in China-based companies, as the investors will not, and may never directly, hold equity interests in the PRC operating entities. Instead, the VIE structure provides contractual exposure to foreign investment in us. The VIE Agreements may not be as effective as direct ownership in providing operational control over Shenzhen Bestman and Nanjing Yonglei. See “Risk Factors — Risks Related to Our Corporate Structure — If the PRC government determines that the contractual arrangements constituting part of the VIE structure do not comply with PRC regulations, or if these regulations change or are interpreted differently in the future, we may be unable to assert our contractual rights over the assets of the VIE and its subsidiary, and our Ordinary Shares may decline in value or become worthless.” For a description of the VIE contractual arrangements, see “Corporate History and Structure — Our VIE Agreements.” As a result of our use of the VIE structure, you may never directly hold equity interests in the VIE and its subsidiary.

Because we do not directly hold equity interests in the VIE and its subsidiary, we are subject to risks and uncertainties of the interpretations and applications of PRC laws and regulations, including but not limited to, regulatory review of overseas listing of PRC companies through special purpose vehicles, and the validity and enforcement of our VIE Agreements. Further, given that PRC laws and regulations governing the validity of the VIE Agreements are uncertain and the relevant government authorities and the PRC courts have broad discretion in interpreting these laws and regulations, if the PRC government authorities or the PRC courts deems that our contractual arrangements with the VIE do not comply with PRC regulatory restrictions on foreign investment in the relevant industries, or if these regulations or the interpretation of existing regulations change or are interpreted differently in the future, we could be subject to severe penalties or be forced to relinquish our interests in those operations. We are also subject to the risks and uncertainties about any future actions of the PRC government in this regard that could disallow the VIE structure, or deem the VIE Structure to be illegal, either in whole or in part, which would likely result in a loss of our consolidated VIE and cause a material change or disruption in our operations, and the value of our Ordinary Shares may depreciate significantly or become worthless. The VIE Agreements have not been tested in a court of law in China as of the date of this prospectus. See “Risk Factors — Risks Relating to Doing Business in the PRC” and “Risk Factors — Risks Related to our Corporate Structure.”

All of the PRC operating entities’ operations are located in “mainland China,” that is, excluding the Hong Kong Special Administrative Region (“Hong Kong”) and the Macau Special Administrative Region (“Macau”). As at the date of this prospectus, we do not have any Macau subsidiary and our sole Hong Kong subsidiary, MED BESTMAN Holding Co., Limited (“HK Bestman”), has historically been and will continue to be designated as an investment holding company only and we do not intend it to conduct any business operations through such entity.

Hong Kong was established as a special administrative region of the PRC in accordance with Article 31 of the Constitution of the PRC. The Basic Law of the Hong Kong Special Administrative Region of the PRC (the “Basic Law”) was adopted and promulgated on April 4, 1990 and became effective on July 1, 1997, when the PRC resumed the exercise of sovereignty over Hong Kong. Pursuant to the Basic Law, Hong Kong is authorized by the National People’s Congress of the PRC to exercise a high degree of autonomy and enjoy executive, legislative, and independent judicial power, under the principle of “one country, two systems,” and the PRC laws and regulations shall not be applied in Hong Kong except for those listed in Annex III of the Basic Law (which is confined to laws relating to national defense, foreign affairs, and other matters that are not within the scope of autonomy of Hong Kong). While the National People’s Congress of the PRC has the power to amend the Basic Law, the Basic Law also expressly provides that no amendment to the Basic Law shall contravene the established basic policies of the PRC regarding Hong Kong. As a result, national laws of the PRC not listed in Annex III of the Basic Law do not apply to our Hong Kong subsidiary, HK Bestman. However, there is no assurance that certain PRC laws and regulations, including existing laws and regulations and those enacted or promulgated in the future, will not be applicable to HK Bestman due to change in the current political arrangements between mainland China and Hong Kong or other unforeseeable reasons. The application of such laws and regulations may have a material adverse impact on HK Bestman, as relevant authorities may impose fines and penalties upon HK Bestman, delay or restrict the repatriation of the proceeds from this offering into mainland China and Hong Kong, and any failure by us to fully comply with any such new regulatory requirements may significantly limit or completely hinder our ability to offer or continue to offer our Ordinary Shares, cause significant disruption to our business operations, and severely damage our reputation, which would materially and adversely affect our financial condition and results of operations and cause our Ordinary Shares to significantly decline in value or in extreme cases, become worthless.

As of the date of this prospectus, no cash transfer nor transfer of other assets has occurred among our Company, our subsidiaries, and the consolidated VIE. As of the date of this prospectus, none of our subsidiaries or consolidated VIE have made any dividends or distributions to our Company. As of the date of this prospectus, neither we nor any of our subsidiaries have ever paid dividends or made distributions to U.S. investors. See “Prospectus Summary — Selected Condensed Consolidated Financial Schedule of Med Eiby Holding Co., Limited parent, VIE and Non-VIE.” We intend to retain most, if not all, of our available funds and any future earnings after this offering to the development and growth of our business. We do not expect to pay dividends or to distribute earnings or settle amounts owed under the VIE agreements in the foreseeable future after this offering. In the future, cash proceeds raised from overseas financing activities, including this offering, may be transferred by us to our WFOE via capital contribution or shareholder loans, as the case may be. However, any proceeds we transfer to our WFOE, either as a shareholder loan or as an increase in registered capital, are subject to approval by, registration with, or information reporting to, relevant governmental authorities in mainland China. Pursuant to the relevant PRC regulations on Foreign Invested Enterprises in China, capital contributions to our mainland China subsidiary are subject to the information report with the Ministry of Commerce, or MOFCOM, or its respective local branches and registration with a local bank authorized by the State Administration of Foreign Exchange, or the SAFE. In addition, any foreign loan procured by our WFOE cannot exceed statutory limits and is required to be registered with the SAFE or its respective local branches. Any medium or long-term loan to be provided by us to the VIE must be registered with the National Development and Reform Commission, or NDRC, and the SAFE or its local branches. Further, we are subject to governmental control of currency conversion and, in certain cases, the control of the remittance of currency out of China. As a result, such governmental control may limit our ability to utilize our revenues effectively. The approval by the SAFE is required to use cash generated from the operations of our mainland China subsidiary and VIE to pay off their respective debts in a currency other than Renminbi owed to entities outside China, or to make other capital expenditure payments outside mainland China in a currency other than Renminbi. See “Risk Factors — Risks Related to Doing Business in China — PRC regulation of loans to and direct investment in the PRC operating entities by offshore holding companies and governmental control of currency conversion may delay us from using the proceeds of this offering, to make loans or additional capital contributions to our WFOE, which could materially and adversely affect our liquidity and our ability to fund and expand our business” and “Risk Factors — Risks Related to Doing Business in China — Governmental control of currency conversion may limit our ability to utilize our revenues effectively and affect the value of your investment.”

In addition, our Ordinary Shares may be prohibited from trading on a national exchange under the Holding Foreign Companies Accountable Act if the Public Company Accounting Oversight Board (United States) (the “PCAOB”) is unable to inspect our auditors for three consecutive years beginning in 2022. Our auditor, Marcum Asia CPAs LLP, is headquartered in New York, New York, and has been inspected by the PCAOB on a regular basis, with the last inspection in 2020, and, as of the date of this prospectus, was not included in the list of PCAOB Identified Firms in the PCAOB Determination Report issued in December 16, 2021. If trading in our Ordinary Shares is prohibited under the Holding Foreign Companies Accountable Act in the future because the PCAOB determines that it cannot inspect or fully investigate our auditor at such future time, Nasdaq may determine to delist our Ordinary Shares and trading in our Ordinary Shares could be prohibited. On June 22, 2021, the U.S. Senate passed the Accelerating Holding Foreign Companies Accountable Act, which, if passed by the U.S. House of Representatives and signed into law, would reduce the period of time for foreign companies to comply with PCAOB audits to two consecutive years instead of three, thus reducing the time period for triggering the prohibition on trading. On August 26, 2022, China Securities Regulatory Commission, or the CSRC, the Ministry of Finance of the PRC (the “MOF”), and the PCAOB signed a Statement of Protocol (the “Protocol”), governing inspections and investigations of audit firms based in mainland China and Hong Kong. The Protocol remains unpublished and is subject to further explanation and implementation. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. The PCAOB is required to reassess its determinations by the end of 2022 and there are uncertainties as to whether the PCAOB will determine it is still unable to inspect or investigate completely registered public accounting firms in mainland China and Hong Kong. See “Risk Factors — Risks Related to This Offering and the Ordinary Shares — Recent joint statement by the SEC and the PCAOB, rule changes by Nasdaq, and the Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our continued listing or future offerings of our securities in the U.S.”

Recent statements by the Chinese government have indicated an intent to exert more oversight and control over offerings that are conducted overseas and/or foreign investments in China based issuers. Any future action by the Chinese government expanding the categories of industries and companies whose foreign securities offerings are subject to government review could significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless. See “Risk Factors — Risks Related to Doing Business in China — There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations. The Chinese government may choose to exert more oversight and control over offerings that are conducted overseas and/or foreign investment in China based issuers, such action may significantly limit or completely hinder our ability to offer or continue to offer Ordinary Shares to investors and cause the value of our Ordinary Shares to significantly decline or be worthless.”

Our business is subject to various government regulations and regulatory interference in China. We may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. Furthermore, recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas. The Chinese government recently initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over Chinese-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement. Pursuant to the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the Opinions, which were made available to the public on July 6, 2021, the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies have been emphasized. Subsequently, on December 24, 2021, the CSRC released the Administrative Provisions of the State Council Regarding the Overseas Issuance and Listing of Securities by Domestic Enterprises (Draft for Comments) (the “Draft Administrative Provisions”) and the Measures for the Overseas Issuance of Securities and Listing Record-Filings by Domestic Enterprises (Draft for Comments) (the “Draft Filing Measures”, collectively with the Draft Administrative Provisions, the “Draft Rules Regarding Overseas Listing”), which stipulate that Chinese-based companies, or the issuer, shall fulfill the filing procedures after the issuer makes an application for initial public offering and listing in an overseas market, and certain overseas offering and listing such as those that constitute a threat to or endanger national security, as reviewed and determined by competent authorities under the State Council in accordance with law, may be prohibited under the Draft Rules Regarding Overseas Listing. Furthermore, on April 2, 2022, the CSRC published the Provisions on Strengthening the Management of Confidentiality and Archives Related to the draft Overseas Issuance of Securities and Overseas Listing by Domestic Companies (draft for public comments), or the Draft Archives Rules, which stipulate that relevant approval, filing, reporting and other regulatory procedures are required in relation to the disclosure, provision and transmission of materials, working papers, archives that contain relevant state secrets or that have a sensitive impact (i.e. may be detrimental to national security or the public interest if divulged) by the domestic listing companies, securities companies and securities service institution to recipients outside the PRC such as the overseas listing regulatory authorities. In addition, on December 28, 2021, the Cyberspace Administration of China published the Measures for Cybersecurity Review, or Cybersecurity Review Measures, which stipulate that if an operator has personal information of over one million users and intends to be listed in a foreign country, it must be subject to the cybersecurity review. As advised by our PRC counsel, Han Kun Law Offices, as of the date of this prospectus, we or the PRC operating entities are not directly subject to those regulatory actions or statements currently in effect, as we or the PRC operating entities have not implemented any monopolistic behaviors and our business does not involve the process of user data, implicate cybersecurity, or involve any other types of restricted industry. As further advised by our PRC counsel, as of the date of this prospectus, no effective laws or regulations in the PRC explicitly require our Company, the VIE or its subsidiary to seek approvals from the CSRC or any other PRC governmental authorities for our overseas listing plan, however, since these statements and regulatory actions by the PRC government are newly published or remain as drafts for public comments only, and official guidance and related implementation rules have not been issued, it is highly uncertain what the potential impact such modified or new laws and regulations will have on our or the PRC operating entities’ daily business operation, the ability to accept foreign investments and listing on U.S. exchanges. The Standing Committee of the National People’s Congress (the “SCNPC”) or other PRC regulatory authorities may in the future promulgate laws, regulations or implementing rules that require our Company, the VIE or its subsidiary to obtain regulatory approval from Chinese authorities before listing in the U.S. Although as of the date of this prospectus, our Company, the VIE and its subsidiary have not been involved in any investigations on cybersecurity review initiated by any PRC regulatory authority, nor has any of them received any inquiry, notice or sanction in such respect, it is uncertain whether or when we might be required to obtain permission from any PRC governmental authority to list our shares overseas, and even if such permission is obtained, whether it will be later denied or rescinded, which could significantly limit or completely hinder our ability to offer or continue to offer our Ordinary Shares to investors and could cause the value of our Ordinary Shares to significantly decline or be worthless. See “Risk Factors — Risks Related to Our Corporate Structure.”

We are an “emerging growth company” under applicable U.S. federal securities laws and are eligible for reduced public company reporting requirements. See “Prospectus Summary — Implications of Being an Emerging Growth Company.”

Following the completion of this offering, our founder, Mr. Yong Bai, will beneficially own [*] Ordinary Shares, representing [*]% of the total voting power of our issued and outstanding share capital immediately following the completing of this offering assuming the underwriter does not exercise its over-allotment option, or [*]% of our total voting power if the underwriter exercises its over-allotment option in full. As such, we will be deemed a “controlled company” under Nasdaq listing rules 5615(c). However, even if we are deemed to be a “controlled company,” we do not intend to avail ourselves of the corporate governance exemptions afforded to a “controlled company” under the Nasdaq listing rules. See “Risk Factors” and “Management — Controlled Company.”

This prospectus does not constitute, and there will not be, an offering of securities to the public in the Cayman Islands.

| Per Share | Total

Without Over-Allotment Option | Total

With Over-Allotment Option | ||||||||||

| Initial public offering price | US$ | US$ | US$ | |||||||||

| Underwriting discounts (1) | US$ | US$ | US$ | |||||||||

| Proceeds to our Company before expenses (2) | US$ | US$ | US$ | |||||||||

| (1) | See “Underwriting” in this prospectus for more information regarding our arrangements with Boustead Securities, LLC (the “Underwriter”). |

| (2) | We expect our total cash expenses for this offering (including cash expenses payable to the Underwriter for their out-of-pocket expenses) to be approximately $[●], exclusive of the above discounts. In addition, we will pay additional items of value in connection with this offering that are viewed by the Financial Industry Regulatory Authority, or FINRA, as underwriting compensation. These payments will further reduce proceeds available to us before expenses. See “Underwriting.” |

The Underwriter is selling [ ] Ordinary Shares (or [●] Ordinary Shares if the Underwriter exercises its over-allotment option in full) in this Offering on a firm commitment basis. The Underwriter is obligated to take and pay for all of the Ordinary Shares if any such Ordinary Shares are taken. We have granted the Underwriter an option for a period of [45] days after the closing of this offering to purchase up to 15% of the total number of the Ordinary Shares to be offered by us pursuant to this offering (excluding Ordinary Shares subject to this option), solely for the purpose of covering over-allotments, at the public offering price less the underwriting discounts. If the Underwriter exercises the option in full, the total underwing discounts payable will be $[*] based on an assumed offering price of $[*] per Ordinary Share, and the total gross proceeds to us, before underwriting discounts and expenses, will be $[*].

We have agreed to issue to the Underwriter share purchase warrants, exercisable commencing [●] days immediately following the effective date of the registration statement of which this prospectus forms a part for a period of [●] years after the effective date of the offering, to purchase Ordinary Shares equal to [●]% of the total number of Ordinary Shares sold in this offering at a per share price equal to [●]% of the public offering price (the “Underwriter Warrants”). The registration statement of which this prospectus is a part also covers the Underwriter Warrants and the Ordinary Shares issuable upon the exercise thereof.

The Underwriter expects to deliver the Ordinary Shares against payment in U.S. dollars to purchasers on or about [ ], 2022.

Neither the United States Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated [*], 2022

TABLE OF CONTENTS

About this Prospectus

We and the Underwriter have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by us or on our behalf or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the Ordinary Shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted or where the person making the offer or sale is not qualified to do so or to any person to whom it is not permitted to make such offer or sale. For the avoidance of doubt, no offer or invitation to subscribe for Ordinary Shares is made to the public in the Cayman Islands. The information contained in this prospectus is current only as of the date on the front cover of the prospectus. Our business, financial condition, results of operations, and prospects may have changed since that date.

Conventions that Apply to this Prospectus

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “BVI” are to the British Virgin Islands; | |

| ● | “China” or the “PRC” refers to the People’s Republic of China; in this prospectus, any PRC laws, rules, regulations, statutes, notices, circulars and judicial interpretations or the like refer to those PRC laws, rules, regulations, statutes, notices, circulars and judicial interpretations or the like currently in force, published for comments (if specifically stated) or being promulgated but have not come into effect (if specifically stated) and publicly available in mainland China as of the date of this prospectus; | |

| ● | “Heketuoer BVI” are to Heketuoer Holding Co., Limited, a BVI business company incorporated with limited liability under the laws of the BVI on July 8, 2021; | |

| ● | “Hong Kong” are to the Hong Kong Special Administrative Region of the People’s Republic of China; | |

| ● | “HK Bestman” are to MED BESTMAN Holding Co., Limited, a limited liability company incorporated in Hong Kong on July 16, 2021; | |

| ● | “HK$” and “Hong Kong dollars” are to the legal currency of Hong Kong; | |

| ● | “mainland China” are to the People’s Republic of China, geographically, for the purposes of this prospectus only, excluding Taiwan, the Hong Kong Special Administrative Region and the Macau Special Administrative Region; | |

| ● | “Nanjing Yonglei” and “Yonglei” are to Nanjing Yonglei Medical Products Import and Export Trade Co., Ltd., a limited liability company incorporated in the PRC on September 29, 2005; | |

| ● | “the PRC operating entities” and “PRC operating entities” are to the VIE, Shenzhen Bestman, and its subsidiary, Nanjing Yonglei; | |

| ● | “the VIE” or “Shenzhen Bestman” are to Shenzhen Bestman Precision Instrument Co., Ltd., a limited liability company incorporated in the PRC on August 3, 2001; | |

| ● | “RMB” and “Renminbi” are to the legal currency of China; | |

| ● | “SCNPC” are to Standing Committee of the National People’s Congress; | |

| ● | “shares,” “Shares,” or “Ordinary Shares” are to the ordinary shares of the Company, par value US$0.001 per share; | |

| ● | “SMEs” are to small and medium enterprises; | |

| ● | “US$,” “$” and “U.S. dollars” are to the legal currency of the United States; | |

| ● | “we,” “us,” “Company,” “our” or “MED EIBY Holding” are to MED EIBY Holding Co., Limited, a Cayman Islands exempted company incorporated in the Cayman Islands on June 25, 2021 and its predecessor entity; and |

1

| ● | “WFOE,” “our WFOE” are to Beijing Agamemnon Technology Service Co., LTD, a limited liability company incorporated in the PRC on January 24, 2022; and | |

| ● | “Xuan Wu Holding” are to Xuan Wu Holding Co., Limited, a BVI business company incorporated with limited liability under the laws of the BVI on March 29, 2022. |

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements appearing elsewhere in this prospectus. In addition to this summary, we urge you to read the entire prospectus carefully, especially the risks of investing in our Ordinary Shares discussed under “Risk Factors,” before deciding whether to buy our Ordinary Shares. This prospectus contains information from an industry report commissioned by us and prepared by Frost & Sullivan (Beijing) Inc., Shanghai Branch Co., an independent research firm, to provide information regarding our industry and market position in China.

Our Corporate Structure

We are a holding company incorporated in the Cayman Islands and not a Chinese operating company. As a holding company with no material operations of our own, the majority of our operations are conducted through the PRC operating entities in mainland China pursuant to the VIE Agreements. The VIE Agreements were entered into by and among our WFOE, the VIE, and the VIE’s shareholders (together the “VIE Shareholders,” and each a “VIE Shareholder”) and include the Powers of Attorney, Equity Pledge Agreement, Exclusive Business Cooperation Agreement, Exclusive Option Agreement, and a Spousal Consent Letter. Due to PRC legal restrictions on foreign ownership in certain internet-related businesses we may explore and operate in the future, we do not have any equity ownership of the VIE. We control and receive the economic benefits of the VIE’s business operations through the VIE Agreements, and we consolidate the VIE for accounting purposes only because we met the conditions under U.S. GAAP to consolidate the VIE. Pursuant to the VIE Agreements, the VIE shall pay service fees in an amount equivalent to all of its net income to our WFOE, while WFOE has the power to direct the activities of the VIE that can significantly impact the VIE’s economic performance, has the obligation to absorb the expected losses of the legal entity, and has the right to receive substantially all of the economic benefits of the VIE. Such contractual arrangements are designed so that the operations of the VIE are solely for the benefit of WFOE and, ultimately, the Company. As such, under U.S. GAAP, the Company is deemed to have a controlling financial interest in, and be the primary beneficiary of, the VIE for accounting purposes and must consolidate the VIE. However, the VIE Agreements have not been tested in a court of law and may not be effective in providing control over the VIE. We are, therefore, subject to risks due to the uncertainty of the interpretation and application of the laws and regulations of the PRC regarding the VIE and the VIE structure. For a description of the VIE Agreements, see “Corporate History and Structure — Our VIE Agreements.” See also “Risk Factors – Risks Related to Our Corporate Structure.”

Our Ordinary Shares in this offering are shares of our offshore holding company in the Cayman Islands instead of shares of the operating entities. The VIE structure provides contractual exposure to foreign investment in China-based companies where Chinese law prohibits direct foreign investment in the operating companies. As a result, you may never directly hold equity interests in the operating entities.

2

The following diagram illustrates our corporate structure, including our significant subsidiary, the VIE and its subsidiary, as of the date of this prospectus and upon the completion of this offering based on proposed number of [*] Ordinary Shares being offered. For more detail on our corporate history, please refer to “Corporate History and Structure.”

As more stringent criteria have been imposed by the SEC and the PCAOB recently, our securities may be prohibited from trading if our auditor cannot be fully inspected. On December 16, 2021, the PCAOB issued its determination that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in mainland China or Hong Kong. This list does not include our auditor, Marcum Asia CPAs LLP. While our auditor is based in the U.S. and is registered with PCAOB and subject to PCAOB inspection, in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor because of a position taken by an authority in a foreign jurisdiction, then such lack of inspection could cause our securities to be delisted from the stock exchange. On August 26, 2022, CSRC, the MOF, and the PCAOB signed a Protocol, governing inspections and investigations of audit firms based in mainland China and Hong Kong. The Protocol remains unpublished and is subject to further explanation and implementation. Pursuant to the fact sheet with respect to the Protocol disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. The PCAOB is required to reassess its determinations by the end of 2022 and there are uncertainties as to whether the PCAOB will determine it is still unable to inspect or investigate completely registered public accounting firms in mainland China and Hong Kong. See “Risk Factors — Risks Related to This Offering and the Ordinary Shares — Recent joint statement by the SEC and the PCAOB, rule changes by Nasdaq, and the Holding Foreign Companies Accountable Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB. These developments could add uncertainties to our continued listing or future offerings of our securities in the U.S.”

Risks associated with our corporate structure and VIE contractual arrangements

Because we do not directly hold equity interests in the VIE and its subsidiary, we are subject to risks and uncertainties of the interpretations and applications of PRC laws and regulations, including but not limited to, regulatory review of overseas listing of PRC companies through special purpose vehicles, and the validity and enforcement of our VIE Agreements. We are also subject to the risks and uncertainties about any future actions of the PRC government in this regard that could disallow the VIE structure, which would likely result in a material change in our operations, and the value of our Ordinary Shares may depreciate significantly or become worthless. The VIE Agreements have not been tested in a court of law in China as of the date of this prospectus.

3

We are the primary beneficiary of Shenzhen Bestman and its subsidiary, Nanjing Yonglei, for accounting purposes, and, therefore, we are able to consolidate the financial results of Shenzhen Bestman and Nanjing Yonglei in our consolidated financial statements in accordance with U.S. GAAP. The contractual arrangements may not be as effective as direct ownership in providing operational control. For instance, the VIE and the VIE Shareholders could breach their contractual arrangements with us by, among other things, failing to conduct its operations in an acceptable manner or taking other actions that are detrimental to our interests. The VIE Shareholders may not act in the best interests of our Company or may not perform their obligations under these contracts. Such risks exist throughout the period in which we intend to operate certain portions of our business through the contractual arrangements with the VIE. In the event that the VIE or the VIE Shareholders fail to perform their respective obligations under the contractual arrangements, we may have to incur substantial costs and expend additional resources to enforce such arrangements. In addition, even if legal actions are taken to enforce such arrangements, there is uncertainty as to whether the courts of the PRC would recognize or enforce judgments of U.S. courts against us or such persons predicated upon the civil liability provisions of the securities laws of the United States or any state. See “Risk Factors — Risks Related to Our Corporate Structure — We rely on contractual arrangements with the VIE and the VIE Shareholders for a large portion of our business operations. These arrangements may not be as effective as direct ownership in providing operational control. Any failure by the VIE or the VIE Shareholders to perform their obligations under such contractual arrangements would have a material and adverse effect on our business.”

Our business is subject to various government regulations and regulatory interference in China. As of the date of this prospectus, except as disclosed in this prospectus and except for those that would not be reasonably expected to have a material adverse effect on our business operation, the PRC operating entities have obtained all material permissions and approvals required by Chinese authorities for our business operation under the current applicable laws in effect, including (i) business licenses; (ii) PRC medical device production and operation licenses; (iii) Class I and II medical device qualifications, including record filings for Class I products and registration certificates for Class II products; (iv) internet drug information service qualification licenses; (v) foreign trade business operators registrations; (vi) medical device advertisement approvals; and (vii) hygiene licenses for enterprises producing disinfection products and relevant record filings for such products.

As advised by our PRC counsel, other than those requisite for a domestic company in China to engage in the businesses similar to ours, our Company, the VIE and its subsidiary are not required to obtain any permission from Chinese governmental authorities, including the CSRC, Cyberspace Administration of China or any other governmental authorities that is required to approve our current business operations in China. However, if our Company, the VIE and its subsidiary do not receive or maintain the approvals, or we inadvertently conclude that such approvals are not required, or applicable laws, regulations, or interpretations change such that our Company, the VIE and its subsidiary are required to obtain approvals in the future, we may be subject to investigations by competent governmental authorities, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless.

We may incur increased costs necessary to comply with existing and newly adopted laws and regulations or penalties for any failure to comply. Furthermore, given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas, it is still uncertain how PRC governmental authorities will regulate overseas listing in general and whether we are required to obtain any specific prior approvals or ex-post record-filling approvals. As of the date of this prospectus, our Company, the VIE and its subsidiary have not been involved in any investigations on cybersecurity review initiated by any PRC regulatory authority, nor has any of them received any inquiry, notice or sanction in such respect, it is uncertain whether or when we might be required to obtain permission from any PRC governmental authority to list our shares overseas, and even if such permission is obtained, whether it will be later denied or rescinded, which could significantly limit or completely hinder our ability to offer or continue to offer our Ordinary Shares to investors and could cause the value of our Ordinary Shares to significantly decline or be worthless. See “Risk Factors — Risks Related to Our Corporate Structure — The SCNPC or PRC regulatory authorities may in the future promulgate laws, regulations or implementing rules that require us, our subsidiaries, the VIE or its subsidiary to obtain regulatory approval from Chinese authorities before or after listing in the U.S.” and “Risk Factors — Risks Related to Our Corporate Structure — If the PRC government determines that the contractual arrangements constituting part of the VIE structure do not comply with PRC regulations, or if these regulations change or are interpreted differently in the future, we may be unable to assert our contractual rights over the assets of the VIE and its subsidiary, and our Ordinary Shares may decline in value or become worthless.”

On December 24, 2021, the CSRC released the Draft Administrative Provisions and the Draft Filing Measures, both of which had a comment period that expired on January 23, 2022. The Draft Administrative Provisions and Draft Filing Measures regulate the administrative system, record-filing management, and other related rules in respect of the direct or indirect overseas issuance of listed and traded securities by “domestic enterprises”. The Draft Administrative Provisions specify that the CSRC has regulatory authority over the “overseas securities offering and listing by domestic enterprises”, and requires “domestic enterprises” to complete filing procedures with the CSRC if they wish to list overseas. The Draft Filing Measures provide supporting rules for the Draft Administrative Provisions by specifying the primary filing procedures for overseas offerings and listing by “domestic enterprises”. Among other things, if a domestic enterprise intends to indirectly offer and list securities in an overseas market, the record-filing obligation is with a major operating entity incorporated in the PRC and such filing obligation shall be completed within 3 working days after the overseas listing application is submitted. The required filing materials for an initial public offering and listing shall include, but are not limited to: regulatory opinions, record-filing, approval and other documents issued by competent regulatory authorities of relevant industries (if applicable); and security assessment opinion issued by relevant regulatory authorities (if applicable). On April 2, 2022, the CSRC published the Draft Archives Rules, for public comments. In the overseas listing activities of domestic companies, domestic companies, as well as securities companies and securities service institutions providing relevant securities services thereof, should establish a sound system of confidentiality and archival work, shall not disclose state secrets, or harm the state and public interests.

4

As advised by our PRC counsel, as of the date of this prospectus, we are not required to obtain any permission from any PRC governmental authorities to offer securities to foreign investors. We have been closely monitoring regulatory developments in China regarding any necessary approvals from the CSRC or other PRC governmental authorities required for overseas listings, including this offering. As of the date of this prospectus, we have not received any inquiry, notice, warning, sanctions or regulatory objection to this offering from the CSRC or other PRC governmental authorities. However, there remains significant uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities. Although we endeavor to comply with all the applicable laws and regulations, if the PRC operating entities (i) do not receive or maintain applicable permissions or approvals for our operation and to offer the securities being registered to foreign investors, or (ii) inadvertently conclude that such permissions or approvals are not required, or applicable laws, regulations, or interpretations change and the PRC operating entities are required to obtain permissions or approvals in the future, the PRC operating entities’ business operation may be materially affected and\or we may lose our consolidated VIE, which conducts the PRC operating entities’ manufacturing operations, holds significant assets and accounts for significant revenues, and have to modify such structure to comply with regulatory requirements. There can be no assurance that we or the PRC operating entities can achieve this without material disruption to the PRC operating entities’ business. Therefore, it may significantly limit or completely hinder our ability to offer or continue to offer securities to investors and could cause the value of such securities to significantly decline or be worthless. See “Risk Factors — Risks Related to Our Corporate Structure — The SCNPC or PRC regulatory authorities may in the future promulgate laws, regulations or implementing rules that require us, our subsidiaries, the VIE or its subsidiary to obtain regulatory approval from Chinese authorities before or after listing in the U.S.,” “Risk Factors — Risks Related to Our Corporate Structure — The Opinions recently issued by the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council and the New Overseas Listing Rules promulgated by the CSRC may subject us to additional compliance requirements in the future.” and “Risk Factors — Risks Related to Our Corporate Structure — If the PRC government determines that the contractual arrangements constituting part of the VIE structure do not comply with PRC regulations, or if these regulations change or are interpreted differently in the future, we may be unable to assert our contractual rights over the assets of the VIE and its subsidiary, and our Ordinary Shares may decline in value or become worthless.”

The Draft Administrative Provisions, the Draft Filing Measures and the Draft Archives Rules are in the process of being formulated and it remains unclear on how they will be interpreted, amended and implemented by CSRC and relevant PRC governmental authorities. Thus, it is still uncertain how PRC governmental authorities will regulate overseas listing in general and whether we are required to obtain any specific prior approvals or ex-post record-filing approvals. Furthermore, if the CSRC or other regulatory agencies later promulgate new rules or explanations requiring that we obtain their prior approvals or ex-post record-filings for this offering and any follow-on offering, we may be unable to obtain such approvals or record-filings, which could significantly limit or completely hinder our ability to offer or continue to offer securities to our investors. We may face sanctions by the CSRC or other PRC regulatory agencies for failure to seek CSRC approval or record-filings for this offering. These sanctions may include fines and penalties on our operations in the PRC, limitations on the operating privileges of the PRC operating entities in the PRC, delays in or restrictions on the repatriation of the proceeds from this offering into the PRC, restrictions on or prohibition of the payments or remittance of dividends by our mainland China subsidiary, or other actions that could have a material and adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our Ordinary Shares. The CSRC or other PRC regulatory agencies may also take actions requiring us, or making it advisable for us, to halt this offering before the settlement and delivery of the Ordinary Shares that we are offering. Consequently, if you engage in market trading or other activities in anticipation of and prior to the settlement and delivery of the Ordinary Shares we are offering, you would be doing so at the risk that the settlement and delivery may not occur. Any uncertainties or negative publicity regarding such approvals or record-filings requirements could have a material adverse effect on our ability to complete this offering or any follow-on offering of our securities or the market for and market price of our Ordinary Shares.

As of the date of this prospectus, our Company, the VIE and its subsidiary have not received any inquiry, notice, warning or sanctions regarding our planned overseas listing from the CSRC or any other PRC governmental authorities. However, it is still uncertain how the potential impact such modified or new laws and regulations will have on the daily operations of the PRC operating entities, the ability to accept foreign investments and list on a U.S. exchange.

Our Mission

Our mission is to become a world-leading medical device manufacturer and provide high-quality medical devices to protect human health.

Overview

The PRC operating entities are a provider and manufacturer of Class I and II medical devices. Specifically, Nanjing Yonglei exports Class I and II medical devices and Shenzhen Bestman manufactures Class I and II medical devices.

Shenzhen Bestman has Class I and II medical devices qualifications, including record filings for Class I products, registration certificates for Class II products, and medical device production and operation licenses in mainland China.

Class I, II, and III medical devices are defined by the National Medical Products Administration of China according to their risk levels under the Regulations on the Supervision and Administration of Medical Devices (2021 Revision), Article 6 of which sets out as follows:

| ● | “Medical Devices of Class I” means the medical devices with low risks, whose safety and effectiveness can be ensured through routine administration. |

| ● | “Medical Devices of Class II” means the medical devices with moderate risks, which shall be strictly controlled and administered to ensure their safety and effectiveness. |

5

| ● | “Medical Devices of Class III” means the medical devices with relatively high risks, which shall be strictly controlled and administered through special measures to ensure their safety and effectiveness. |

The National Medical Products Administration of the State Council, or the NMPA, is responsible for developing the classification rules for medical devices and maintaining catalogues of classified devices. Based on information on the production, distribution and use of medical devices, the NMPA analyzes and evaluates the risk levels of medical devices and adjusts the classification rules and classification catalogues.

The PRC operating entities have provided hospitals, pharmacies, medical equipment companies, and individual customers for over 20 years with more than 567,000 Class I and Class II medical device products for domestic and international sales.

Shenzhen Bestman mainly manufactures and sells Class I and II medical devices under its own brands. Specifically, Shenzhen Bestman mainly focuses on the manufacturing, sales and distributions of its own-produced medical devices, such as fetal dopplers, fetal/maternal monitors, ultrasonic vascular doppler detectors, vine finders, and feeding pumps, etc.

Nanjing Yonglei mainly sells Class I and II medical devices manufactured by Shenzhen Bestman and other medical devices sourced from other Chinese manufacturers to its overseas customers. Specifically, Nanjing Yonglei focuses on exporting medical devices.

The PRC operating entities sell their products both domestically and internationally. Besides significant domestic sales in China, the PRC operating entities’ export sales have expanded to more than 100 countries across the world. In 2003, Shenzhen Bestman obtained an ISO-9001 certificate and, in 2005, it received an ISO-13485 certificate. As of the date of this prospectus, both the ISO-9001 and ISO-13484 certificates are effective. The current effective ISO-13485 certificate will expire on September 27, 2024, and the current effective ISO-9001 certificate will expire on September 14, 2024.

In addition, Shenzhen Bestman’s product, fetal doppler (models: BF-500B, BF-500+, and BF500++), received United States Food and Drug Administration’s, or the FDA’s, approvals in 2010. The most recent registration renewal was in November 2021 and will be valid through December 31, 2022. Shenzhen Bestman expects to renew its registration in November 2022. If Shenzhen Bestman successfully renews the registration, such registration will be valid through December 2023. However, we cannot assure you that Shenzhen Bestman will successfully renew this registration.

Our Sales Ecosystem

The PRC operating entities’ distribution network covers major global markets. Internationally, the PRC operating entities mainly export medical devices through exporting distributors. Currently, the PRC operating entities cooperate with approximately 1,646 exporting distributors, who are responsible for distributing their products to end users across the world.

Our Revenue Model

The PRC operating entities generate revenues through: 1) manufacturing and sales of Class I and II medical devices under their own brands, i.e. the brands owned by Shenzhen Bestman; and 2) resales of Class I, II and III medical devices sourced from other manufacturers. For the fiscal year ended June 30, 2021, the PRC operating entities recognized approximately $2,775,632 in revenues, of which Shenzhen Bestman’s own brand sales accounted for 32%, and the resales of sourced medical devices from other manufactures accounted for 68%. For the fiscal year ended June 30, 2022, the PRC operating entities recognized approximately $3,386,258, in revenues, of which Shenzhen Bestman’s own brand sales accounted for 31%, and the resales of sourced medical devices from other manufactures accounted for 69%.

The PRC operating entities’ medical devices reach end users both domestically and internationally. For the fiscal year ended June 30, 2021, our total sales to domestic direct end users and domestic distributor customers accounted for 19% of our revenues. For the fiscal year ended June 30, 2021, our sales to overseas distributing customers accounted for 81% of our revenues. For fiscal years ended June 30, 2022, our total sales to domestic direct end users and domestic distributor customers accounted for 23% of our revenues. For the fiscal year ended June 30, 2022, our sales to overseas distributing customers accounted for 77%, of our revenues.

The PRC operating entities’ overseas distributors are mainly from Nigeria and Cameroon. For the fiscal year ended June 30, 2021 revenue contributed by distributors from Nigeria accounted for 28%, and revenue contributed by distributors from Cameroon accounted for 28%. For the fiscal year ended June 30, 2022, revenue contributed by distributors from Nigeria accounted for 30%, and revenue contributed by distributors from Cameroon accounted for 23%.

The PRC operating entities sell medical devices through their direct sales force, including ecommerce platforms, and distributors. For the fiscal year ended June 30, 2021, the PRC operating entities’ sales through direct sale channels accounted for 2% of our revenues, and the PRC operating entities’ sales through distributors accounted for 98% of our revenues, of which domestic distributors accounted for 16%, and exporting distributors accounted for 82% of our revenues. For the fiscal year ended June 30, 2022, the PRC operating entities’ sales through direct sale channels accounted for 3%, of our revenues, and the sales through distributors accounted for 97%, of our revenue, of which domestic distributors accounted for 20%, and exporting distributors accounted for 77%, of our revenues.

6

Competitive Strengths

We believe that the following strengths contribute to our success and are the differentiating factors that set us apart from our peers:

| ● | Strong brand and experienced management team. |

| ● | Large distribution, sales, and service network for medical devices. |

| ● | Competitive position maintained by high quality standard systems. |

| ● | Close cooperation between departments. |

| ● | Market-driven research and development allow for continual improvement and long-term client loyalty. |

7

Our Growth Strategies

We will continue to adhere to our business principle of providing high-quality and safe products to our consumers. We believe that our pursuit of this goal will lead to sustainable growth driven by our capacity expansion based on market demand, enabling us to solidify our position in the industry, and create long-term value for shareholders and employees. We intend to pursue the following strategies:

| ● | Strengthen our market position by gaining additional market share. |

| ● | Continue to invest in our research and development department. |

| ● | Strengthen our quality control system and uphold our commitment to product quality. |

| ● | Expand our sales and distribution network. |

| ● | Enhance our ability to attract, incentivize and retain talented professionals. |

Summary of Significant Risk Factors

An investment in our Ordinary Shares is subject to a number of risks, including risks relating to the business and industry of the PRC operating entities, risks related to our corporate structure, risks related to doing business in China, and risks related to our Ordinary Shares and this offering. You should carefully consider all of the information in this prospectus before making an investment in the Ordinary Shares. The following list summarizes some, but not all, of these risks. Please read the information in the section titled “Risk Factors” for a more thorough description of these and other risks.

8

Risks Related to the Business and Industry of the PRC Operating Entities

| ● | The PRC operating entities pay close attention to quality control, monitoring each step in the process from procurement to production and from warehouse to delivery. Yet, maintaining consistent product quality depends significantly on the effectiveness of the PRC operating entities’ quality control system, which in turn depends on a number of factors, including, but not limited to, the design of the PRC operating entities’ quality control system, employee training to ensure that the PRC operating entities’ employees adhere to and implement such quality control policies and procedures, and the effectiveness of monitoring any potential violation of such quality control policies and procedures. There can be no assurance that the PRC operating entities’ quality control system will always prove to be effective. See “Failure to maintain the quality and safety of the PRC operating entities’ products could have a material and adverse effect on our financial condition and results of operations” of this prospectus; | |

| ● | The quality of the PRC operating entities’ products is critical to the success of the PRC operating entities’ business, and such quality, to a large extent, depends on the effectiveness of the PRC operating entities’ quality control system. The PRC operating entities have developed a rigorous quality control system that enables them to monitor each stage of the production process. However, the PRC operating entities still cannot eliminate all risks of errors, defects or failures. Failure to detect quality defects in the PRC operating entities’ products could result in patient injury, customer dissatisfaction, or other problems that could seriously harm the PRC operating entities’ reputation and business, expose the PRC operating entities to liability, and adversely affect our revenues and profitability. See “Any failure to maintain effective quality control over the PRC operating entities’ products and services could materially adversely affect the PRC operating entities’ business” of this prospectus; | |

| ● | The PRC operating entities face an inherent risk of liability claims or complaints from their customers. Although, the PRC operating entities take those complaints and claims seriously and endeavor to reduce such complaints by implementing various remedial measures, the PRC operating entities cannot assure you that they can successfully prevent or address all complaints as and when they occur. Any complaints or claims against the PRC operating entities, even if meritless and unsuccessful, may divert management’s attention and other resources from the PRC operating entities’ business and adversely affect the PRC operating entities’ business and operations. Customers may lose confidence in the PRC operating entities and their brand, which may adversely affect the PRC operating entities’ business and results of operations. See “We may experience significant liability claims or complaints from customers, litigation, and regulatory investigations and proceedings relating to medical device safety, or adverse publicity involving the PRC operating entities’ products, which could adversely affect our financial condition and results of operations” of this prospectus; | |

| ● | The PRC operating entities do not have long term contracts with their suppliers. Their suppliers can reduce the quantities of products they sell to the PRC operating entities, or cease selling products to the PRC operating entities. Such reductions or terminations could have a material adverse impact on the PRC operating entities’ revenues, profits and financial condition, even if the PRC operating entities maintain an alternative suppliers list. See “The PRC operating entities do not have long term contracts with their suppliers and the suppliers can reduce order quantities or terminate their sales to the PRC operating entities” of this prospectus; | |

| ● | Currently, the PRC operating entities’ products are primarily produced at their factory located in Shenzhen, China. The products also rely on the PRC operating entities’ suppliers to provide raw materials and components. Nevertheless, natural disasters or other unanticipated catastrophic events, including storms, fires, explosions, earthquakes, terrorist attacks and wars, as well as changes in governmental planning for the land where the PRC operating entities’ factory or their suppliers’ factories are located could significantly impair the PRC operating entities’ ability to manufacture products and operate their business. Catastrophic events could also destroy the inventories stored in and those suppliers' factories. The occurrence of any catastrophic event could result in the temporary or long-term closure of manufacturing facilities, and may severely disrupt the PRC operating entities’ business operations. See “Any disruption of the operation of the PRC operating entities or the operation of the PRC operating entities’ suppliers could materially and adversely affect the PRC operating entities’ business and results of operations” of this prospectus; | |

| ● | The PRC operating entities rely on a combination of trademark, fair trade practice, patent, copyright and trade secret protection laws in China, as well as confidentiality procedures and contractual provisions, to protect their intellectual property rights. In the event that the PRC operating entities resort to litigation to enforce their intellectual property rights, such litigation could result in substantial costs and a diversion of their managerial and financial resources. We can provide no assurance that the PRC operating entities will prevail in such litigation. In addition, the PRC operating entities’ trade secrets may be leaked or otherwise become available to, or be independently discovered by, their competitors. Any failure in protecting or enforcing the PRC operating entities’ intellectual property rights could have a material adverse effect on our business, financial condition and results of operations. See “The PRC operating entities may not be able to prevent others from unauthorized use of their intellectual property, which could harm their business and competitive position” of this prospectus); | |

| ● | Global pandemics, epidemics in China or elsewhere in the world, or fear of the spread of contagious diseases, such as Ebola virus disease (EVD), coronavirus disease 2019 (COVID-19), Middle East respiratory syndrome (MERS), severe acute respiratory syndrome (SARS), H1N1 flu, H7N9 flu, and avian flu, as well as hurricanes, earthquakes, tsunamis, or other natural disasters could disrupt the PRC operating entities’ business operations, reduce or restrict the PRC operating entities’ supply of products, incur significant costs to protect their employees and facilities, or result in regional or global economic distress, which may materially and adversely affect the PRC operating entities’ business, financial condition, and results of operations. Actual or threatened war, terrorist activities, political unrest, civil strife, and other geopolitical uncertainty could have a similar adverse effect on the PRC operating entities’ business, financial condition, and results of operations. See “Pandemics and epidemics, natural disasters, terrorist activities, political unrest, and other outbreaks could disrupt the PRC operating entities’ delivery and operations, which could materially and adversely affect their business, financial condition, and results of operations” of this prospectus; | |

| ● | The PRC operating entities sell medical devices internationally. Although the PRC operating entities take measures to minimize risks inherent to their international sales, certain risks may have a negative effect on their profitability and operating results, impair the performance of the PRC operating entities’ foreign sales or otherwise disrupt their business. See “The PRC operating entities’ international sales are subject to a variety of risks that could adversely affect their profitability and operating results” of this prospectus; |

9

| ● | The medical devices the PRC operating entities manufacture and sell are closely related to human health, which is subject to strict supervision by relevant PRC authorities. The related national government authorities have issued a series of regulatory guidelines and industry policies to ensure the healthy development of the industry. In recent years, as China further deepens the reform of its medical and health system, relevant government departments have successively implemented a series of regulations and policies regarding industry standards, bidding, price formation mechanisms, circulation systems and other related fields, which have brought wide and profound impact on the livelihood and development of pharmaceutical companies. See “Failure to keep up with the changes in domestic industry policies or standards could have a material and adverse effect on the PRC operating entities’ reputation, financial condition, and results of operations” of this prospectus); and | |

| ● | The PRC operating entities have established and improved their internal control system against unfair business practices, to prevent, minimize and\or eliminate employees and customers improper behaviors in the medical device sales transactions, including unauthorized rebates. There can be no assurance that the PRC operating entities’ existing internal control system will be adequate to prevent, minimize and/or eliminate such improper transactions, that the PRC operating entities will be able to effectively implement their internal control polices, or that they will be able to perfect their internal control system to eliminate such improper transactions. See “If the PRC operating entities’ employees or customers are involved in improper medical device sales transactions, it could adversely affect the PRC operating entities’ reputation, financial conditions and results of operations” of this prospectus. |

Risks Related to Our Corporate Structure

| ● | We are a Cayman Islands exempted company and our mainland China subsidiary, namely our WFOE, is a foreign-invested enterprise. We have relied, and expect to continue relying, on contractual arrangements with the VIE and the VIE Shareholders to operate our business in China. We conduct our operations in the PRC mainly through the VIE and its subsidiary pursuant to the VIE Agreement. The VIE Agreements are designed so that the operations of the VIE are solely for the benefit of WFOE and ultimately, the Company. As such, under U.S. GAAP, the Company is deemed to have a controlling financial interest in, and be the primary beneficiary of, the VIE for accounting purposes only and must consolidate the VIE because we met the conditions under U.S. GAAP to consolidate the VIE.

The VIE Agreements may not be as effective as direct ownership in providing operational control. For example, the VIE and the VIE Shareholders could breach their contractual arrangements with us by, among other things, failing to conduct its operations in an acceptable manner or taking other actions that are detrimental to our interests. See “We rely on contractual arrangements with the VIE and the VIE Shareholders for a large portion of our business operations. These arrangements may not be as effective as direct ownership in providing operational control. Any failure by the VIE or the VIE Shareholders to perform their obligations under such contractual arrangements would have a material and adverse effect on our business” of this prospectus; | |