UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

For the transition period from to

OR

Date of event requiring this shell company report

Commission file number:

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

State of

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Chief Executive Officer

HUB Cyber Security Ltd.

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered, pursuant to Section 12(b) of the Act

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each

of the issuer’s classes of capital stock or common stock as of the close of the period covered by the annual report. As of December 31,

2023, the registrant had 11,938,363 ordinary shares outstanding, no par value. As of August 13, 2024, the registrant had

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Note—Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |

| ☒ | Emerging growth company |

If an emerging growth company that prepares its

financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition

period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the

Exchange Act.

Indicate by check mark whether the registrant

has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial

reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared

or issued its audit report.

If securities are registered pursuant to Section

12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction

of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| ☐ U.S. GAAP | ☒ | | ☐ Other |

If “Other” has been checked in response to the previous question indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No

CONTENTS

i

ii

ABOUT THIS ANNUAL REPORT

Except where the context otherwise requires or where otherwise indicated in this Annual Report, the terms “HUB Cyber Security Ltd.,”, “HUB,” the “Company,” “we,” “us,” “our,” “our company” and “our business” refer to HUB Cyber Security Ltd. and its subsidiaries.

All references in this Annual Report to “Business Combination” refer to the transactions effected under the merger agreement, dated as of March 23, 2022 (the “Merger Agreement”), by and among Mount Rainier Acquisition Corp., a Delaware corporation (“RNER”), HUB and Rover Merger Sub, Inc., a Delaware corporation and wholly owned subsidiary of HUB (“Merger Sub”). Pursuant to the Merger Agreement, Merger Sub merged with and into RNER, with RNER surviving the merger. Upon consummation of the Business Combination and the other transactions contemplated by the Merger Agreement on February 28, 2023, RNER became a wholly owned subsidiary of HUB.

All references in this Annual Report to “Israeli currency” and “NIS” refer to New Israeli Shekels, the terms “dollar,” “USD” or “$” refer to U.S. dollars and the terms “€” or “euro” refer to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

All information in this Annual Report on Form 20-F relating to shares or price per share reflects the 1-for-10 reverse share split effected by us on December 14, 2023.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Our financial statements have been prepared in accordance with International Financial Reporting Standards as issued by the IASB (“IFRS”). We present our consolidated financial statements in U.S. dollars.

Our fiscal year ends on December 31 of each year. References to fiscal 2021 and 2021 are references to the fiscal year ended December 31, 2021, references to fiscal 2022 and 2022 are references to the fiscal year ended December 31, 2022, and references to fiscal 2023 and 2023 are references to the fiscal year ended December 31, 2023.

Market and Industry Data

Unless otherwise indicated, information contained in this Annual Report concerning our industry and the regions in which we operate, including our general expectations and market position, market opportunity, market share and other management estimates, is based on information obtained from various independent publicly available sources and other industry publications, surveys and forecasts, which we believe to be reliable based upon our management’s knowledge of the industry. We assume liability for the accuracy and completeness of such information to the extent included in this Annual Report. Such assumptions and estimates of our future performance and growth objectives and the future performance of our industry and the markets in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those discussed under the headings “Cautionary Statement Regarding Forward-Looking Statements” Item 3.D. “Key Information—Risk Factors” and Item 5. “Operating and Financial Review and Prospects” in this Annual Report.

Certain monetary amounts, percentages and other figures included in this Annual Report have been subject to rounding adjustments. Certain other amounts that appear in this Annual Report may not sum due to rounding. Revenue shown throughout this Annual Report is revenue from continuing operations, unless otherwise stated.

Unless otherwise noted, in this Annual Report we cite a source the first time a statement relying upon that source is made, and do not include citations subsequently when that statement is repeated.

Trademarks

This Annual Report contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this Annual Report may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

iii

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

In addition to historical facts, this Annual Report contains forward-looking statements within the meaning of Section 27A of the U.S. Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”) and the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements are principally contained in the sections entitled Item 3.D. “Key Information—Risk Factors,” Item 4. “Information on the Company,” and Item 5. “Operating and Financial Review and Prospects.” In some cases, these forward-looking statements can be identified by words or phrases such as “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “plan,” “anticipate,” “intend,” “seek,” “believe,” “estimate,” “predict,” “potential,” “continue,” “contemplate,” “possible” or similar words. Statements regarding our future results of operations and financial position, growth strategy and plans and objectives of management for future operations, including, among others, expansion in new and existing markets, are forward-looking statements.

Forward-looking statements involve a number of risks, including potential impairments, uncertainties and assumptions, and actual results or events may differ materially from those projected or implied in those statements. Important factors that could cause such differences include, but are not limited to:

| ● | Our previously disclosed internal investigation was initiated to review allegations of misappropriation of Company funds and other potential fraudulent actions regarding the use of Company funds by a former senior officer of the Company. As a result of or in connection with the matters that were the subject of the investigation, we may become subject to certain regulatory scrutiny, which could have a material adverse effect on our business, financial condition and results of operation. |

| ● | We are a company with a history of net losses and anticipate that we may incur net losses for the foreseeable future. Moreover, our independent registered public accounting firm’s report, contained herein, includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern, indicating the possibility that we may not be able to continue to operate in the future. |

| ● | We have identified material weaknesses in our internal control over financial reporting. If our remediation of the material weaknesses is not effective, or we fail to develop and maintain effective internal controls over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable laws and regulations could be impaired. |

| ● | The circumstances that led to the failure to file our Annual Report on time, and our efforts to assess and remediate those matters have caused and may continue to cause substantial delays in our SEC filings. |

| ● | We are not currently in compliance with the continued listing standards of Nasdaq and our failure to meet the continued listing requirements of Nasdaq could result in a delisting of our securities. |

| ● | We have financed our operations and certain capital needs through various debt, convertible debt and equity issuances. Our existing and future debt obligations could impair our liquidity and financial condition. We are currently in default under certain of our debt obligations. If we are unable to negotiate a solution for the payment of our outstanding debt or otherwise meet our debt obligations, the lenders could foreclose on our assets which could cause us to curtail or cease operations or have an adverse impact on our business, results of operations and financial condition and the price of our ordinary shares. |

| ● | We need to raise additional funds in the near future in order to execute our business plan and these funds may not be available to us when we need them. If we cannot raise additional funds when we need them, our business, prospects, financial condition and operating results could be negatively affected. |

| ● | An inability to attract new customers, retain existing customers and sell additional services to customers could adversely impact our revenue and results of operations. |

| ● | The termination of, or material changes to, our relationships with key vendors and customers could materially adversely affect our business, financial condition and operating results, which could be exacerbated due to our reliance on a small number of vendors for a significant portion of our distribution and offerings in our Professional Services division. |

| ● | Actions that we have taken to reduce costs and rebalance investments may not result in anticipated savings or operational efficiencies, could result in total costs and expenses that are greater than expected, and could disrupt our business. |

| ● | Our limited operating history in the fields of secured data fabric and confidential computing makes it difficult to evaluate our business and future prospects and increases the risk of your investment. |

| ● | The network security market is rapidly evolving within the increasingly challenging cyber threat landscape. If our solutions fail to adapt to market changes and demands, sales may not continue to grow or may decline. |

| ● | Our reputation and business could be harmed based on real or perceived shortcomings, defects or vulnerabilities in our solutions or if our customers experience security breaches, which could have a material adverse effect on our business, reputation and operating results. |

iv

| ● | Our ability to introduce new products, features, integrations and enhancements is dependent on adequate research and development resources. |

| ● | We currently have and target many customers that are large corporations and government entities, which are subject to a number of challenges and risks, such as increased competitive pressures, administrative delays and additional approval requirements. |

| ● | We may not be able to convert our customer orders in backlog or pipeline into revenue. |

| ● | A shortage of components or manufacturing capacity could cause a delay in our ability to fulfill orders or increase our manufacturing costs. |

| ● | Our management team has limited experience managing a U.S. listed public company. |

| ● | Our business relies on the performance of, and we face stark competition for, highly skilled personnel, including our management, other key employees and qualified employees, and the loss of one or more of such personnel or of a significant number of our team members or the inability to attract and retain executives and qualified employees we need to support our operations and growth, could harm our business. |

| ● | Changes in tax laws or exposure to additional income tax liabilities could affect our future net profitability. |

| ● | As a cybersecurity provider, if any of our systems, our customers’ cloud or on-premises environments, or our internal systems are breached or if unauthorized access to customer or third-party data is otherwise obtained, public perception of our business may be harmed, and we may lose business and incur losses or liabilities. |

| ● | Undetected defects and errors may increase our costs and impair the market acceptance of our products and solutions. |

| ● | We may not be able to adequately protect or enforce our intellectual property rights or prevent unauthorized parties from copying or reverse engineering our products or technology. Our efforts to protect and enforce our intellectual property rights and prevent third parties from violating our rights may be costly. |

| ● | The dynamic regulatory environment around privacy and data protection may limit our offering or require modification of our products and services, which could limit our ability to attract new customers and support our existing customers and increase our operational expenses. We could also be subject to investigations, litigation, or enforcement actions alleging that we fail to comply with the regulatory requirements, which could harm our operating results and adversely affect our business. |

| ● | Our actual or perceived failure to adequately protect personal data could subject us to sanctions and damages and could harm our reputation and business. |

| ● | We may be required to indemnify our directors and officers in certain circumstances. |

| ● | A market for our securities may not develop or be sustained, which would adversely affect the liquidity and price of our securities. |

| ● | We are subject to a number of securities class actions and other litigations and could be subject to additional litigation in the United States, Israel or elsewhere that could negatively impact our business, including resulting in substantial costs and liabilities. |

| ● | Class action litigation due to stock price volatility or other factors could cause us to incur substantial costs and divert management’s attention and resources. |

| ● | If our estimates or judgments relating to our critical accounting policies are based on assumptions that change or prove to be incorrect, our operating results could fall below expectations of securities analysts and investors, resulting in a decline in our stock price. |

v

| ● | Provisions of Israeli law and our articles of association may delay, prevent or make difficult an acquisition of us, prevent a change of control, and negatively impact our share price. |

| ● | Our ordinary shares and warrants may not continue to be listed on a national securities exchange, which could limit investors’ ability to make transactions in such securities and subject us to additional trading restrictions. |

| ● | If securities or industry analysts do not publish or cease publishing research or reports about us, our business, or our market, or if they change their recommendations regarding our ordinary shares adversely, then the price and trading volume of our ordinary shares could decline. |

| ● | As we are a “foreign private issuer” and intend to follow certain home country corporate governance practices, our shareholders may not have the same protections afforded to shareholders of companies that are subject to all Nasdaq corporate governance requirements. |

| ● | The listing of our securities on Nasdaq did not benefit from the process undertaken in connection with an underwritten initial public offering, which could result in diminished investor demand, inefficiencies in pricing and a more volatile public price for our securities. |

| ● | Conditions in Israel, including the current war between Israel and Hamas, could materially and adversely affect our business. |

| ● | It may be difficult to enforce a U.S. judgment against us, our officers and directors and the Israeli experts named in this Annual Report in Israel or the United States, or to assert U.S. securities laws claims in Israel or serve process on our officers and directors and these experts. |

| ● | We may issue additional ordinary shares or other equity securities without seeking approval of our shareholders, which would dilute the ownership interests represented by our ordinary shares and may depress the market price of our ordinary shares. |

Our estimates and forward-looking statements are mainly based on our current expectations and estimates of future events and trends which affect or may affect our business, operations and industry. Although we believe that these estimates and forward-looking statements are based upon reasonable assumptions, they are subject to numerous risks and uncertainties.

These forward-looking statements are subject to a number of known and unknown risks, uncertainties, other factors and assumptions, including the risks described in Item 3.D “Key Information—Risk Factors” and elsewhere in this Annual Report.

You should not rely on forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition and operating results. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in the section titled “Risk factors” and elsewhere in this Annual Report. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report. The results, events and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Annual Report. While we believe that information provides a reasonable basis for these statements, that information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements. We qualify all of our estimates and forward-looking statements by these cautionary statements.

The forward-looking statements made in this Annual Report relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report to reflect events or circumstances after the date of this Annual Report or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments.

vi

PART I

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

Item 3. Key Information

A. [Reserved.]

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

You should carefully consider the risks described below before making an investment decision. Additional risks not presently known to us or that we currently deem immaterial may also impair our business operations. Our business, financial condition or results of operations could be materially and adversely affected by any of these risks. The trading price and value of our ordinary shares could decline due to any of these risks, and you may lose all or part of your investment. This Annual Report also contains forward-looking statements that involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks faced by us described below and elsewhere in this Annual Report. See “Cautionary Statement Regarding Forward-Looking Statements” on page iv of this Annual Report. Such risks include, but are not limited to:

Risks Relating to the Internal Investigation,

Our Ability to Continue as a Going Concern, Our Internal

Controls and Related Matters

Our previously disclosed internal investigation was initiated to review allegations of misappropriation of Company funds and other potential fraudulent actions regarding the use of Company funds by a former senior officer of the Company. As a result of or in connection with the matters that were the subject of the investigation, we may become subject to certain regulatory scrutiny. We are unable to predict the effectiveness of any remediation measures recommended by the Special Committee. In addition, we have incurred and may continue to incur substantial costs in connection with the internal investigation, which could have a material adverse effect on our business, financial condition and results of operations.

As previously disclosed in our Report on Form 6-K on April 20, 2023, our board of directors appointed a Special Committee of Independent Directors (the “Special Committee”) to oversee an internal investigation (the “Internal Investigation”) in order to review certain allegations of misappropriation of Company funds and other potential fraudulent actions regarding the use of Company funds by a former senior officer of ours. During the course of the Internal Investigation, the Special Committee, together with its outside advisers, believed that it found sufficient evidence to support a determination that Mr. Eyal Moshe, our former Chief Executive Officer and President of U.S. operations and former member of the board of directors, and Ms. Ayelet Bitan, our former Chief of Staff and wife of Mr. Moshe, misappropriated (from a Company bank account over which Mr. Moshe had sole signatory rights) a total of approximately NIS 2 million (approximately $582,000) for personal use. Further, in certain instances, evidence reviewed by the Special Committee demonstrated that Mr. Moshe authorized payments to contractors without either (i) proper documentation and signatory approval; or (ii) required budget and expense reports. The employment of Eyal Moshe, was terminated effective July 24, 2023 for cause and Mr. Moshe resigned from our board on August 15, 2023. Additionally we commenced two legal actions in Israel against Ms. Bitan and against Mr. Moshe to dispute their requests for severance payments in accordance with Israeli law in connection with these determinations by the Special Committee.

1

Additionally, the Special Committee believed that it found sufficient evidence to determine that, one of our controllers, with the permission of Mr. Moshe, used Company credit cards for personal use in the amount of approximately NIS 400,000 (approximately $110,000). These personal expenses were neither factored into the controller’s payroll nor properly documented in our financial books and records. Additionally, Mr. Moshe approved a bonus of NIS 250,000 to the controller. However, this bonus was not paid to the controller but instead was paid to a third-party at the controller’s direction. Prior to the commencement of legal proceedings, we reached a settlement with the controller whereby the amount of the bonus in the amount of NIS 250,000 plus VAT was repaid to us and all his options and RSUs were cancelled.

The Internal Investigation is complete, although we continue to pursue recovery of the misappropriated funds. These events regarding the Special Committee and Internal Investigation are the subject of possible regulatory review and expose us and our directors and officers to possible investigations and possible enforcement actions by regulators both in Israel and the United States, including the Israel Securities Authority (“ISA”), Israel Tax Authority, U.S. Securities and Exchange Commission (“SEC”), the Nasdaq Stock Market LLC (“Nasdaq”) and/or U.S. Department of Justice (“DOJ”). We have provided certain information and documentation to certain regulatory authorities and is prepared to respond to any regulatory inquiry it may receive. Our management and our board of directors do not currently believe there are any impacts on our financial statements. If we were to be subject to an investigation or enforcement action from a regulatory agency it could have a material adverse effect on our business, financial position and results of operations.

If any federal authorities were to ultimately determine that we violated any laws or regulations, we may be exposed to a broad range of civil and criminal sanctions including, but not limited to, injunctive relief, disgorgement, fines, penalties, modifications to business practices including the termination or modification of existing business relationships, the imposition of compliance programs and the retention of a monitor to oversee future compliance by us, which could be costly and burdensome to our management, and could adversely impact our business, prospects, reputation, financial condition, liquidity, results of operations or cash flows. Even if an inquiry or investigation does not result in any adverse determinations, it potentially could create negative publicity and give rise to third-party litigation or other actions, which could also have a material adverse effect on our business, financial condition, results of operations and cash flows.

The Special Committee is neither a civil nor a criminal a court of law and no court has yet substantiated the findings of the Special Committee. It is possible that a court of law may find differently than the Special Committee has, which could expose us to counterclaims from Mr. Moshe, Ms. Bitan or others. Additionally, while we have informed Mr. Moshe that he has been summarily dismissed as an employee, Mr. Moshe resigned from our board of directors.

We have commenced legal actions in Israel against Ms. Bitan and against Mr. Moshe to dispute their requests for severance payments in accordance with Israeli law. Two actions were undertaken against Ms. Bitan. In the initial action, the court granted an injunction preventing her from accessing her accumulated severance package. In the second action, it was requested that the court order that these sums be returned to the Company. In the action against Mr. Moshe, the court was requested to grant an injunction against accessing the accumulated severance package and to order the return of the sums to us. These actions are time limited, so the initial action against Ms. Bitan was initiated prior to the completion of the Special Committee Report and as such was based upon the limited information known at that time. The preliminary hearing in both of these cases is set for the coming months and both will be heard in front of the same judge who granted the injunction against Ms. Bitan. For further details please refer to Item 8. “Financial Information—Consolidated Statements and Other Financial Information—Legal and Arbitration Proceedings” below.

There can be no assurance that Mr. Moshe, Ms. Bitan or others will not bring forth any claims or commence any litigation against us in connection with Mr. Moshe’s dismissal, his resignation from the board, our challenging Ms. Bitan’s severance payments or the publication of the Special Committee’s findings from the Internal Investigation.

Further, we incurred substantial costs and diverted management resources in connection with the Internal Investigation, and the Internal Investigation itself caused us to fail to timely file our Annual Reports on Form 20-F for the fiscal years ended December 31, 2022 and 2023 with the SEC. We may also incur material costs associated with our indemnification arrangements with our current and former directors and certain of our officers, as well as other indemnitees related to law suits or regulatory proceedings that have arisen and may arise in the future from the Internal Investigation.

2

Our reported material weaknesses in internal control over financial reporting subjects us to additional litigation and regulatory examinations, investigations, proceedings or court orders, including additional cease and desist orders, the suspension of trading of our securities, delisting of our securities, the assessment of civil monetary penalties and other equitable remedies. In addition, the remediation of the material weaknesses (set forth below in Item 15. “Controls and Procedures”) will require us to incur additional costs and to divert management resources in the upcoming periods, which could adversely affect our business, financial condition, results of operations, and growth prospects.

We are a company with a history of net losses and anticipate that we may incur net losses for the foreseeable future and may never be profitable. Moreover, our independent registered public accounting firm’s report, contained herein, includes an explanatory paragraph that expresses substantial doubt about our ability to continue as a going concern, indicating the possibility that we may not be able to continue to operate in the future.

We have incurred net losses in each year since our inception, including net losses of $86.6 million, $80.0 million and $13.4 million in the years ended December 31, 2023, 2022, and 2021, respectively. In addition, we may continue to incur net losses for the foreseeable future, and we may not achieve or maintain profitability in the future. Because the market for our network security solutions and products is rapidly evolving and has not yet reached widespread adoption, it is difficult for us to predict our future results of operations or the limits of our market opportunity. We cannot be certain when, if ever, we will become profitable. Even if we were to become profitable, we might not be able to sustain such profitability on a quarterly or annual basis.

Primarily because of our losses incurred to date, our expected continued future losses, our default on existing debt facilities and limited cash balances, our independent registered public accounting firm has included in its report an explanatory paragraph expressing substantial doubt about our ability to continue as a going concern. We are generating negative cash flow, requiring constant and immediate cash injections to continue to operate, failing to meet obligations as they become due, including financial, suppliers debts and other ordinary course of operations costs. In addition, and as a result of our ongoing operating losses, we had outstanding liabilities that could not be met by our revenues, including payments due to our debt holders, vendors and service providers, and since May 2024, we have been unable to make required deposits in employee pension and severance funds or to pay required withholding taxes on employee compensation payment. We are currently negotiating with our debt holders with whom we are currently in default to extend the term of their notes or to convert the same into our ordinary shares. In addition, we are currently negotiating with Comsec creditors to achieve with them debt arrangement in light of two applications that were submitted to court to declare the Company and Comsec as insolvent. For more information about those application please refer to Item 8. “Financial Information—Consolidated Statements and Other Financial Information—Legal and Arbitration Proceedings” below. Our ability to continue as a going concern is contingent upon, among other factors, the sale of ordinary shares to obtain additional funding to support our operations and/or obtaining alternate financing and the ability to cure our outstanding defaults or that these obligations may be negotiated on terms that are favorable to us, if at all. Management currently believes that it will be necessary for us to secure additional funds to continue our existing business operations and to fund our obligations We have raised and will continue to seek to raise additional funds during 2024 through a variety of equity and/or debt financing arrangements; however, there can be no assurance that we will be able to obtain funds on commercially acceptable terms, if at all. If we cannot generate sufficient revenues, reduce cost and/or secure additional financing on acceptable terms, we may be required to, among other things, alter our business strategy, significantly curtail or discontinue operations or obtain funds by entering into financing agreements on unattractive terms. See “—We will be required to raise additional funds in the near future in order to execute our business plan and these funds may not be available to us when we need them. If we cannot raise additional funds when we need them, our business, prospects, financial condition and operating results could be negatively affected” below for additional information.

3

We have identified material weaknesses in our internal control over financial reporting. If our remediation of the material weaknesses is not effective, or we fail to develop and maintain effective internal controls over financial reporting, our ability to produce timely and accurate financial statements or comply with applicable laws and regulations could be impaired.

As described above, we appointed the Special Committee to oversee an internal investigation related to alleged misappropriation of Company funds and other potentially fraudulent actions regarding the use of Company funds by a former senior officer of the Company. As such, when preparing the financial statements that are included in this Annual Report, our management determined that we have material weaknesses in our internal control over financial reporting as of December 31, 2023 and 2022, which had not been remedied as of December 31, 2023. A material weakness is a deficiency, or combination of deficiencies, in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of our annual or interim consolidated financial statements will not be prevented or detected on a timely basis.

The material weaknesses as of December 31, 2023 identified include, but are not limited to:

| ● | Lack of sufficient number of personnel with an appropriate level of knowledge and experience in accounting for complex or non-routine transactions; |

| ● | The fact that our policies and procedures with respect to the review, supervision and monitoring of our accounting and reporting functions were either not designed, not properly put in place or not operating effectively; |

| ● | Deficiencies in the design and operations of the procedures relating to the timely closing of financial books at the quarter and fiscal year end; |

| ● | Insufficient oversight of certain signatory rights relating to our financial accounts; |

| ● | Ineffective design and implementation of Information Technology General Controls (“ITGC”). The Company’s ITGC deficiencies included improperly designed controls pertaining to change management and user access rights over systems that are critical to the Company’s system of financial reporting; and |

| ● | Incomplete segregation of duties in certain types of transactions and processes (excluding monetary transactions, where there is a clear distinction between the preparer and the signer vis-a-vis financial institutions). |

As a result of the material weaknesses, management has concluded that our internal control over financial reporting was ineffective as of each of December 31, 2023 and 2022.

Under the Companies Law, the board of directors is required to appoint an internal auditor recommended by the audit committee. Our current internal auditor is Joseph Ginossar of Fahn Kanne, an affiliate of Grant Thornton International. The role of the internal auditor is to examine, among other things, whether the company’s actions comply with applicable law and proper business procedures. The internal auditor may not be an interested party, a director or an officer of the company, or a relative of any of the foregoing, nor may the internal auditor be our independent accountant or a representative thereof.

Further, there can be no guarantee that the Internal Investigation and subsequent inquiries revealed all instances of inaccurate disclosure or other deficiencies, or that other existing or past inaccuracies or deficiencies will not be revealed in the future. Our failure to correct these deficiencies or our failure to discover and address any other deficiencies could result in inaccuracies in our financial statements and could also impair our ability to comply with applicable financial reporting requirements and related regulatory filings on a timely basis. As a result, our business, financial condition, results of operations and prospects, as well as the trading price of our ordinary shares and warrants, may be materially adversely affected.

4

We, together with any additional remediation actions to be suggested by the Special Committee, have taken and will continue to take the following actions to remediate these material weaknesses:

| ● | the hiring of additional accounting and finance resources with public company experience to assist in the expansion and effectiveness of the existing risk assessment, management processes and the design and implementation of controls responsive to those deficiencies; |

| ● | broadening the scope and improving the effectiveness of existing ITGC for identity and access management, segregation of duties, change management, data governance and program development; |

| ● | the implementation of enhanced corporate policies and practices including with respect to gifts, loans, conflicts of interest and workplace conduct; |

| ● | engaging internal and external resources to assist us with remediation and monitoring remediation progress; and |

| ● | delivering periodic training to our team members, including but not limited to technology and accounting staff, on the responsibilities of officers and leaders related to workplace conduct and various compliance issues and internal controls over financial reporting. |

We cannot assure you the measures we are taking to remediate the material weaknesses will be sufficient or that they will prevent future material weaknesses. Additional material weaknesses or failure to maintain effective internal control over financial reporting could cause us to fail to meet our reporting obligations as a public company and may result in a restatement of our financial statements for prior periods. In addition, these deficiencies could cause investors to lose confidence in our reported financial information, limiting our access to capital markets, adversely affecting our operating results and leading to declines in the trading price of our ordinary shares and warrants.

Our independent registered public accounting firm is not required to attest to the effectiveness of our internal control over financial reporting until after we are no longer an “emerging growth company” as defined in the JOBS Act. At such time, our independent registered public accounting firm may issue a report that is adverse in the event our internal controls over financial reporting do not operate effectively. If we are not able to complete our initial assessment of our internal controls and otherwise implement the requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) in a timely manner or with adequate compliance, our independent registered public accounting firm may not be able to certify as to the effectiveness of our internal controls over financial reporting. Any failure to implement and maintain effective internal control over financial reporting also could adversely affect the results of periodic management evaluations and annual independent registered public accounting firm attestation reports regarding the effectiveness of our internal control over financial reporting that we will eventually be required to include in its periodic reports that are filed with the SEC. If we are unable to remediate our existing material weaknesses or identify additional material weaknesses and are unable to comply with the requirements of Section 404 in a timely manner or assert that our internal control over financial reporting is effective, or if our independent registered public accounting firm is unable to express an opinion as to the effectiveness of our internal control over financial reporting once we are no longer an emerging growth company, investors may lose confidence in the accuracy and completeness of the financial reports and the market price of our ordinary shares and warrants could be negatively affected, and we could become subject to investigations by Nasdaq, the SEC or other regulatory authorities, which could require additional financial and management resources. For more information regarding these remedial actions and enhancement measures, see “Item 15. Controls and Procedures—Material Weaknesses in Internal Control Over Financial Reporting”.

The circumstances that led to the failure to file our Annual Report on time, and our efforts to assess and remediate those matters have caused and may continue to cause substantial delays in our SEC filings.

Our ability to resume a timely filing schedule with respect to our SEC reporting is subject to a number of contingencies, including whether and how quickly we are able to effectively remediate the identified material weaknesses in our internal control over financial reporting. Our filing of our Annual Report has been delayed and we cannot assure you we will be able to timely make our future filings.

In cases where we delay our filings, investors will need to evaluate certain decisions with respect to our ordinary shares and warrants in light of our lack of current financial information. Accordingly, any investment in our ordinary shares and/or warrants may involve a greater degree of risk than other companies who are current on their public filings. Our lack of current public information may have an adverse impact on investor confidence, which could lead to a reduction in our share price or restrictions on our abilities to obtain financing in the public market, among others.

5

We are not currently in compliance with the continued listing standards of Nasdaq and our failure to meet the continued listing requirements of Nasdaq could result in a delisting of our securities.

If we fail to satisfy the continued listing requirements of Nasdaq such as the corporate governance requirements or the minimum closing bid price requirement, Nasdaq will take steps to delist our securities. We did not timely file this Annual Report and the per share price of our ordinary shares has declined below the minimum bid price threshold required for continued listing on Nasdaq. Such a delisting would likely have a negative effect on the price of the securities and would impair shareholders’ ability to sell or purchase the securities when they wish to do so as well as adversely affect our ability to issue additional securities and obtain additional financing in the future.

On May 20, 2024, we received a notification letter from the Listing Qualifications Department of Nasdaq stating that we were not in compliance with the requirements of Nasdaq Listing Rule 5250(c)(1) (the “Reporting Rule”) as a result of not having timely filed this Annual Report with the SEC. Under the Nasdaq rules, the Company had 60 calendar days, or until July 19, 2024, to file this Annual Report or to submit to Nasdaq a plan to regain compliance with the Nasdaq Listing Rules. On July 19, 2024, we submitted a plan of compliance to achieve and sustain compliance with the Reporting Rule. Following submission of this plan of compliance, Nasdaq has determined to grant an exception to enable us to regain compliance with the aforesaid rule, subject to our filing of the Annual Report with the SEC on or before August 19, 2024.

On July 19, 2024, we submitted a plan of compliance to achieve and sustain compliance with the Reporting Rule. Following submitting this plan of compliance, we received an extension from Nasdaq to file this Report until August 19, 2024.

On July 16, 2024, we received a deficiency notice from Nasdaq informing us that our ordinary shares have failed to comply with the $1.00 minimum bid price required for continued listing under Nasdaq Listing Rule 5450(a)(1) (the “Minimum Bid Price Requirement”) based upon the closing bid price of our ordinary shares for the 30 consecutive business days prior to the date of the deficiency notice. The Deficiency notice did not result in the immediate delisting of our ordinary shares from Nasdaq. In accordance with Nasdaq Listing Rule 5810(c)(3)(A), we were given 180 calendar days from, or until January 13, 2025, to regain compliance with the Minimum Bid Price Requirement. If at any time before January 13, 2025, the bid price of our ordinary shares closes at $1.00 per share or more for a minimum of 10 consecutive business days, then Nasdaq will provide written confirmation that we have regained compliance.

Furthermore, we expect to receive a further deficiency notice from Nasdaq following the filing of this Annual Report due to our failure to meet the financial standards for continued listing on the Nasdaq Global Market.

In the event of a delisting, we can provide no assurance that any action taken by us to restore compliance with listing requirements would allow our securities to become listed again, stabilize the market price or improve the liquidity of our securities, prevent our securities from dropping below the Minimum Bid Price Requirement or prevent future non-compliance with Nasdaq’s listing requirements. Additionally, if our securities are not listed on, or become delisted from, Nasdaq for any reason, and are quoted on the OTC Bulletin Board, an inter-dealer automated quotation system for equity securities that is not a national securities exchange, the liquidity and price of HUB’s securities may be more limited than if it were quoted or listed on Nasdaq or another national securities exchange as the liquidity that Nasdaq provides would no longer be available to investors. Shareholders may be unable to sell their securities unless a market can be established or sustained, and we could face a lengthy process to re-list the ordinary shares, if at all.

We have previously financed our operations and certain capital needs through various debt, convertible debt and equity issuances. Our existing and future debt obligations could impair our liquidity and financial condition. We are currently in default under certain of our debt obligations. If we are unable to negotiate a solution for the payment of our outstanding debt or otherwise meet our debt obligations, the lenders could foreclose on our assets which could cause us to curtail or cease operations or have an adverse impact on our business, results of operations and financial condition and the price of our ordinary shares.

We are currently in default under certain of our debt and convertible obligations totaling approximately $82 million in debt (the “Outstanding Debt”). Upon an event of default under the Outstanding Debt, the holders of such debt may exercise all rights and remedies available under the terms of the notes or applicable laws. Some of the Outstanding Debt is payable through conversion into our ordinary shares, but we currently are unable to make such payments in ordinary shares due to our failure to timely file our Annual Report, our failure to register the ordinary shares issuable upon conversion and the current trading price of our ordinary shares.

6

We are currently in discussions with holders of the Outstanding Debt regarding possible solutions for the payment of the Outstanding Debt, including the possible extension of the outstanding obligations and, in some cases, maturity date of the Outstanding Debt. However, there can be no assurance that our discussions will be successful and, if we are not successful in finding an acceptable resolution to the existing default or the impending event of default, the holders of the Outstanding Debt will be able to seek judgement for the full amount due and may seek to foreclose on our assets, which would adversely affect our business or possibly force us to cease operations and commence liquidation proceedings. Our debt and financial obligations:

| ● | could impair our liquidity; |

| ● | could make it more difficult for us to satisfy our other obligations; |

| ● | could require us to dedicate cash flow to payments on our debt and financial obligations, which would reduce the availability of our cash flow to fund working capital, capital expenditures and other corporate requirements; |

| ● | could impose restrictions on our ability to incur other indebtedness, grant liens on our assets, and could impede us from obtaining additional financing in the future for working capital, capital expenditures, acquisitions and general corporate purposes; |

| ● | could adversely affect our ability to enter into strategic transactions, public or private equity offerings, and similar agreements, or require us to obtain the consent to enter into such transactions; |

| ● | could make us more vulnerable in the event of a downturn in our business prospects and could limit our flexibility to plan for, or react to, changes in our industry and markets; and |

| ● | could place us at a competitive disadvantage when compared to our competitors. |

| ● | could cease operation and liquidate risk. |

The Outstanding Debt could enable the lenders to foreclose on certain of our assets and could significantly diminish the market value and marketability of our ordinary shares and could result in the acceleration of other payment obligations or default under other contracts or possibly force us to cease operations and commence liquidation proceedings. In addition, the conversion of some or all of the Outstanding Debt into ordinary shares will dilute the ownership interests of our existing shareholders. Any sales in the public market of our ordinary shares issuable upon such conversion could adversely affect prevailing market prices of our ordinary shares. In addition, the existence of the Outstanding Debt may encourage short selling by market participants because the conversion of the Outstanding Debt would likely depress the price of our ordinary shares.

We will need to raise additional funds in the near future in order to execute our business plan and these funds may not be available to us when we need them. If we cannot raise additional funds when we need them, our business, prospects, financial condition and operating results could be negatively affected.

We require additional capital in the future in order to fund our growth strategy or to respond to technological advancements, competitive dynamics or technologies, customer demands, business opportunities, challenges, acquisitions or unforeseen circumstances. We may also determine to raise equity or debt financing for other reasons. For example, in order to further enhance business relationships with current or potential customers or partners, we may issue equity or equity-linked securities to such current or potential customers or partners.

We may not be able to timely secure additional debt or equity financing on favorable terms, or at all. If we raise additional funds through the issuance of equity or convertible debt or other equity-linked securities, our existing shareholders could experience significant dilution. In addition, any debt financing obtained by us in the future, whether in the form of a credit facility or otherwise, could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions. If we are unable to obtain adequate financing or financing on terms satisfactory to us when we require it, our ability to continue to grow or support our business and to respond to business challenges could be significantly limited. In addition, because our decision to issue debt or equity in the future will depend on market conditions and other factors beyond our control, we cannot predict or estimate the amount, timing, nature or success of our future capital raising efforts.

7

Risks Related to Our Business and Industry

An inability to attract new customers, retain existing customers and sell additional services to customers could adversely impact our revenue and results of operations.

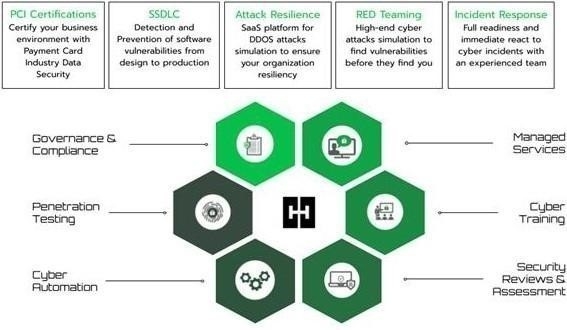

Currently, we generate the majority of our revenues from our Professional Services division, which, among other services, enables enterprise clients to identify, manage and respond to cybersecurity threats with comprehensive, bundled solutions that provide a crucial layer of protection for organizations as well as a means to manage associated risk and compliance. More recently, we have bundled solutions under a package approach called HUB Guard that includes dashboards providing scoring on the customer’s cyber resiliency.

The ability to maintain or increase our revenues and achieve profitability may be impacted by a number of factors, including our ability to attract new customers, retain existing customers and sell our professional services to additional customers. We may incur higher customer acquisition or retention costs as we seek to grow our customer base and expand our markets. Moreover, to the extent we are unable to retain and sell additional services to existing customers, including as part of our initiative to address existing accounts that have substandard margins, our revenue and results of operations may decrease. For example, our Professional Services division had a large contract with a governmental agency in Israel, which expired in December 2023. The loss of business from any of our major customers, whether by the cancellation of existing contracts, the failure to obtain renewal of these contracts or win new business or lower overall demand for our services, could materially and adversely impact our revenue and results of operations.

The termination of, or material changes to, our relationships with key vendors could materially adversely affect our business, financial condition and operating results, which could be exacerbated due to our reliance on a small number of vendors for a significant portion of our distribution and offerings in our Professional Services division.

We contract to purchase from specific vendors a significant portion of our distribution and offerings for our Professional Services division. For the year ended December 31, 2023, two vendors accounted for approximately 80% of inventory purchases. These vendors decided to terminate their relationships with our subsidiary and ceased supplying products. We have reached settlement with one vendor and we are negotiating settlement with the second one as well. Those vendors are associated with the Company’s discontinued operation for the period ended December 31,2023.

Actions that we have taken to reduce costs and rebalance investments may not result in anticipated savings or operational efficiencies, could result in total costs and expenses that are greater than expected, and could disrupt our business.

Beginning in March 2023, we began implementing a plan to reduce our workforce in order to become more efficient in our costs and to optimize facilities-related costs. We adopted this plan to improve operational efficiencies and align our investments more closely with our strategic priorities. We may incur additional expenses associated with the reduction in our workforce not contemplated by our plan such as employment litigation costs, which may have an impact on other areas of our liabilities and obligations and contribute to losses in future periods. We may not realize, in full or in part, the anticipated benefits and savings from our plan due to unforeseen difficulties, delays or unexpected costs. If we are unable to realize the expected operational efficiencies and cost savings, our operating results and financial condition would be adversely affected.

Furthermore, ongoing implementation of our plan and reductions in force may be disruptive to our operations. For example, our workforce reduction could result in attrition beyond planned staff reductions, increased difficulties in our day-to-day operations and reduced employee morale. If employees who were not affected by the few rounds of reduction in force seek alternative employment, we could incur unplanned additional expense to ensure adequate resourcing and fail to attract and retain qualified management, sales and marketing personnel who are critical to our business. Our failure to do so could harm our business and our future performance.

8

Our limited operating history in the field of secured data fabric and confidential computing makes it difficult to evaluate our business and prospects and increases the risk of your investment.

We began operations in 1984 as A.L.D. Advanced Logistics Development Ltd. (“ALD”) and are engaged in developing and marketing quality management software tools and solutions. HUB Cyber Security Ltd (today HUB Cyber Security TLV) was founded in 2017 by veterans of the elite Unit 8200 and Unit 81 of the Israeli Defense Forces, with vast experience and proven track records in setting up and commercializing start-ups in a multi-disciplinary environment. HUB merged with ALD in June 2021 and began trading on the Tel Aviv Stock Exchange (the “TASE”). Following the merger with ALD, we have developed unique technology and products in the field of confidential computing, which is a rapidly evolving industry. Further, significant portions of our growth have been through mergers with, and acquisitions, of other companies. As a result, there is limited information that investors can use in evaluating our business, strategy, operating plan, results, and prospects. While we currently derive most of our revenues from our Professional Services division, we intend to derive most of our revenues in the future from the delivery of technology and products, including our secured data fabric and confidential computing protection solutions. It is difficult to predict future revenues and appropriately budget for expenses, and we have limited insight into trends that may emerge and affect our business. To date, we have only derived a small portion of our historical revenues from technology and product-oriented solutions, including our confidential computing solution. In addition, we have encountered and expect to continue to encounter risks and uncertainties frequently experienced by growing companies in rapidly evolving industries, such as the risks and uncertainties described herein. As a result, if we do not address these risks successfully, or if the assumptions we use to plan and operate our business are incorrect or change, our results of operations could differ materially from our expectations, and our business, financial condition, and results of operations could be materially adversely affected.

The network security market is rapidly evolving within the increasingly challenging cyber threat landscape. If our solutions fail to adapt to market changes and demands, sales may not continue to grow or may decline.

We offer a combined hardware and software solutions that provides end-to-end data protection across all phases of data storage and processing. If customers do not recognize the benefit of our solutions as a critical layer of an effective security strategy, our revenues may fail to grow or otherwise decline. Security solutions such as ours create a protective envelope around each data processing component to protect data while it is being processed. However, advanced cyber attackers are skilled at adapting to new technologies and developing new methods of gaining access to organizations’ sensitive data and technology assets, including those of IT and cybersecurity providers. The techniques they use to access or sabotage networks or applications or to disrupt operations (for example, via ransomware) change frequently and are frequently not recognized until launched against a target. In addition, the COVID-19 pandemic significantly impacted online behavior and the security of businesses and individuals, and we have observed a significant increase in cyber-attack activity since the beginning of the pandemic. We expect that our customers, and thereby our solutions, will face new and increasingly sophisticated methods of attack, particularly due to the increased use by attackers of tools and techniques that are designed to circumvent security controls, to avoid detection and to remove or obfuscate evidence. We face significant challenges in ensuring that our solutions effectively identify and respond to sophisticated attacks while avoiding disruption to our customers’ businesses. As a result, we must continually modify and improve our products and solutions in response to market and technology trends and evolvement, including obtaining interoperability with existing or newly introduced technologies and systems, to ensure we are meeting market needs and continuing to provide valuable solutions that can be deployed in a variety of IT environments. If we fail to identify and respond to new and increasingly complex methods of attack or to update our solutions to detect or prevent such threats in time to protect our customers’ critical business data, the integrity of our solutions and reputation, as well as our business and operating results, could suffer.

We cannot guarantee that we will be able to anticipate future market needs and opportunities or be able to develop or acquire product enhancements or new products or solutions to meet such needs or opportunities in a timely manner or at all. Additionally, we cannot guarantee that we will be able to comply with new regulatory requirements (see “Item 3.D. “Key Information—Risk Factors—Risks Related to Our Legal and Regulatory Environment—The dynamic regulatory environment around privacy and data protection may limit our offering or require modification of our products and services, which could limit our ability to attract new customers and support our existing customers and increase our operational expenses. We could also be subject to investigations, litigation, or enforcement actions alleging that we fail to comply with the regulatory requirements, which could harm our operating results and adversely affect our business.”). Furthermore, new technologies and solutions that may be introduced into the market may make our solutions obsolete, lowering the demand for our products and reducing our sales. Even if we are able to anticipate, develop and commercially introduce new features and solutions and ongoing enhancements to our existing solutions, there can be no assurance that such enhancements or new solutions will achieve widespread market acceptance. Delays in developing, completing or delivering new or enhanced solutions could cause our offerings to be less competitive, impair customer acceptance of our solutions and result in delayed or reduced revenue.

9

Our reputation and business could be harmed based on real or perceived shortcomings, defects or vulnerabilities in our solutions or if our customers experience security breaches, which could have a material adverse effect on our business, reputation and operating results.

Network security products, solutions and services such as ours are complex in development, design and deployment and may contain errors, bugs, misconfigurations or vulnerabilities that are potentially incapable of being remediated or detected until after their deployment, if at all. Any real or perceived errors, bugs, design failures, defects, vulnerabilities, misconfigurations in our solutions or untimely or insufficient remediation thereof, could cause our solutions to not meet specifications, be vulnerable to security attacks or fail to secure networks or applications which could negatively impact customer operations and consequently harm our business and reputation.

In addition, we may suffer significant adverse publicity and reputational harm if our solutions are associated, or are believed to be associated with, or fail to reasonably protect against, a security attack or a breach at a high-profile customer. Moreover, any actual or perceived cyber-attack, other security breach, exposure or theft of ours or our customers’ data, regardless of whether the breach or theft is attributable to the failure of our solutions, could:

| ● | adversely affect the market’s perception of our solutions, |

| ● | cause current or potential customers to look to our competitors for alternatives, |

| ● | require us to expend significant financial resources to analyze, correct or eliminate any vulnerabilities, and |

| ● | lead to investigations, litigation, fines and penalties, any of which could have a material adverse effect on our operations, financial condition and reputation. |

Furthermore, security breaches or defects in our solutions could result in loss or alteration of, or unauthorized access to, customers’ data and compromise our customers’ networks and applications that are secured by our solutions. If such a security breach results in the disruption or loss of availability, integrity or confidentiality of customers’ data, we could incur significant liability to our customers and to businesses or individuals whose information was being handled by our customers, in addition to regulatory agencies. There can be no assurance that limitation of liability, indemnification or other protective provisions that we attempt to include in our contracts would be applicable, enforceable or adequate in connection with a security breach, or would otherwise protect us from any such liabilities or damages with respect to any particular claim.

There is no guarantee that our solutions will be free of flaws or vulnerabilities. Our customers may also misuse or improperly install our solutions, which could result in vulnerabilities to a breach or theft of business data.

Competition in the market for cybersecurity and other technology solutions, in general, is intense. If we are unable to compete effectively, our business, financial condition and results of operations could be harmed.

The network security solutions market in which we operate is characterized by intense competition, constant innovation, rapid adoption of different technological solutions and services, and evolving security threats. We compete with a multitude of companies that offer a broad array of network security products and that employ different approaches and delivery models to address these evolving threats.

Our primary competitors in the network security industry consist of Cisco Systems, Inc., Juniper Networks, Inc., Fortinet Inc., Check Point Software Technologies Ltd. and Palo Alto Networks, Inc., as well as companies that have network security capabilities as part of broader IT solutions offerings, such as Microsoft Corporation, McAfee, Inc., International Business Machines Corporation, Hewlett-Packard Enterprise Company and FireEye, Inc. Competitors in the data fabric market include Atlan, IBM, Oracle, Talend, SAP, Informatica, Cloudera, TIBCO, Amazon Web Services and data.world.

10

In addition, IT security spending is spread across a wide variety of solutions and strategies, including, for example, endpoint, network and cloud security, vulnerability management and identity and access management. Organizations continually evaluate their security priorities and investments and may allocate their IT security budgets to other solutions and strategies and may not adopt or expand use of our solutions. Accordingly, we may also compete for budgetary reasons with additional vendors that offer threat protection solutions in adjacent or complementary markets to ours.

Most of our competitors have greater financial, personnel and other resources than we have, which may limit our ability to effectively compete with them. We also expect to continue to face additional competition as new participants enter the market or extend their portfolios into related technologies. Current and future participants may also be able to respond more quickly to new or emerging technologies and changes in customer demands and to devote greater resources to the development, promotion and sale of their products than we can. Larger companies with substantial resources, brand recognition and sales channels may form alliances with or acquire competing security solutions and emerge as significant competitors.

Competition may result in lower prices or reduced demand for our solutions and a corresponding reduction in our ability to recover costs, which may impair our ability to achieve, maintain and increase profitability. Furthermore, the dynamic market environment poses a challenge in predicting market trends and expected growth. We cannot assure you that we will be able to implement our business strategy in a manner that will allow us to be competitive. If any of our competitors offer products or services that are more competitive than ours, we could lose market share and our business, financial condition and results of operations could be materially and adversely affected as a result.

Our ability to introduce new products, features, integrations and enhancements is dependent on adequate research and development resources.

To remain competitive, we must maintain adequate research and development resources, such as the appropriate personnel and development technology, to meet the demands of the market. If we are unable to offer high level and new services in our Professional Services division, develop new products, features, integrations and enhancements internally due to certain constraints, such as employee turnover, a lack of management ability or a lack of other research and development resources, our business may be harmed. Moreover, research and development projects can be technically challenging and expensive. The nature of these research and development cycles may cause us to experience delays between the time we incur expenses associated with research and development and the time we are able to offer compelling features, integrations and enhancements and generate revenue, if any, from such investment. If we expend a significant amount of resources on research and development and our efforts do not lead to the successful introduction or competitive improvement of products, features, integrations and enhancements, it could harm our business, results of operations and financial condition. For example, we are in the process of developing our “single chip” solution, which is a complicated process and there is no assurance that we will be able to successfully release this solution as planned. In addition, our failure to maintain adequate research and development resources or to compete effectively with the research and development programs of our competitors may harm our business, results of operations and financial condition.

If we are unable to acquire large enterprise customers for our security solutions or sell additional products and services to our existing customers, our future revenues and operating results will be harmed.

Our success and continued growth will depend in part on our ability to convince large enterprises to adopt our technologies and solutions and selling incremental or new solutions to existing customers. If we are unable to succeed in such efforts, we will likely be unable to generate revenue growth at desired or projected rates.

In addition, competition in the industry may lead us to acquire fewer new customers or result in our providing more favorable commercial terms to new or existing customers. Macro-economic effects may also affect our ability to maintain our customer base and expand it.

Additional factors that impact our ability to acquire new customers or sell additional products and services to our existing customers include the consumption of their past purchases, a reduction in the perceived need for network security, the size of our prospective and existing customers’ IT budgets, the utility and efficacy of our solution offerings, whether proven or perceived, changes in our pricing models, and general economic conditions. These factors may have a material negative impact on future revenues and operating results.

11

We currently have and target many customers that are large corporations and government entities, which are subject to a number of challenges and risks, such as increased competitive pressures, administrative delays and additional approval requirements.