PROSPECTUS

June 21, 2022

Bluerock High Income Institutional Credit Fund

Class A Shares (IIMAX)

of Beneficial Interest

The Bluerock High Income Institutional Credit Fund (the “Fund”) is a continuously offered, non-diversified, closed-end management investment company that is operated as an interval fund. As an interval fund, the Fund will offer to repurchase at least 5% of the Fund’s shares on a quarterly basis in accordance with the Fund's repurchase policy, subject to certain conditions. See “Quarterly Repurchases of Shares” and “Repurchase Policy Risk.” Shares will be repurchased at the per-class net asset value per share determined as of the close of regular trading on the NYSE no later than the 14th day after the date the repurchase offer ends, or the next business day if the 14th day is not a business day. Shareholders will be notified in writing about each quarterly repurchase offer, how they may request that the Fund repurchase their shares and the date the repurchase offer ends. The time between the notification to shareholders and the Repurchase Request Deadline may vary from no more than 42 days to no less than 21 days. The first repurchase offer is expected to occur in September 2022 and will occur no later than two periodic intervals after the effective date of the Fund.

Investment Objective. The Fund’s primary investment objective is to generate high current income, while secondarily seeking attractive, long-term risk-adjusted returns, with low correlation to the broader markets.

Summary of Investment Strategy. The Fund pursues its investment objective by investing, directly or indirectly, in senior secured loans (“Senior Secured Loans”). The Fund may purchase Senior Secured Loans directly in the primary or secondary market and will invest in them indirectly by purchasing various tranches, including senior, junior or equity tranches, of entities that own a diversified pool of Senior Secured Loans known as Collateralized Loan Obligations, or “CLOs”, (collectively with Senior Secured Loans, “Target Securities”). The Fund will generally focus its investment activities on U.S. dollar-denominated loans that (i) are broadly syndicated (i.e. with multiple institutional lenders) and made to U.S. companies, (ii) are senior in the capital structure with a priority claim on assets and cash flow of the underlying borrower, (iii) are primarily secured by first priority liens on assets of the underlying borrowers, (iv) are rated BB+ or below, known as “below investment grade” or “junk”, or are unrated, (v) are floating rate to provide some protection against rising interest rates, (vi) may change over time but at origination represent 40%-60% of the enterprise value of the borrower, and (vii) in CLOs that own such loans and additionally (a) are diverse across issuers, industries and geographies, (b) have senior tranches with high credit ratings in order to maximize excess spread, (c) have attractive risk-adjusted spreads, and (d) are actively managed by experienced CLO collateral managers. Securities which are “below investment grade” or “junk” are predominantly speculative in nature. See “Below Investment Grade Risk.” A risk-adjusted return is a calculation of the profit or potential profit from an investment that takes into account the degree of risk that must be accepted in order to achieve it.

The Fund is newly organized and as a result it has no pricing and performance history. For the reasons set forth below, an investment in the Fund’s shares is not suitable for investors who cannot tolerate risk of loss or who require liquidity, other than liquidity provided through the Fund's repurchase policy:

| ● | Shares of the Fund will not be listed on any securities exchange or any secondary market, which makes them inherently illiquid. |

| ● | Shares of the Fund are not redeemable, but shall be subject to the repurchase offer provisions set forth below. |

| ● | Although the Fund will offer to repurchase at least 5% of the Fund’s shares on a quarterly basis in accordance with the Fund's repurchase policy, the Fund will not be required to repurchase shares at a shareholder's option nor will shares be exchangeable for units, interests or shares of any other security. |

| ● | The Fund is not required to extend, and shareholders should not expect the Fund’s Board of Trustees (the “Board” or the “Trustees”) to authorize, repurchase offers in excess of 5% of outstanding shares per quarter. |

| ● | The Fund will invest in CLOs, including in junior and equity tranches that may experience substantial losses, including due to actual defaults, decrease of market value due to collateral defaults and removal of subordinate tranches, market anticipation of defaults and investor aversion to CLO securities as a class. The risks of investing in CLOs depend largely on the tranche invested in and the type of the underlying debts and loans in the tranche of the CLO, in which the Fund invests. CLOs also carry risks including, but not limited to, interest rate risk and credit risk. Our investments in CLOs may be riskier and less transparent to us and our shareholders than direct investments in the underlying companies. |

| ● | Regardless of how the Fund performs, an investor may not be able to sell or otherwise liquidate his or her shares whenever such investor would prefer and will be significantly limited in his or her ability to reduce his or her exposure on any market downturn. |

| ● | The amount of distributions that the Fund may pay, if any, is uncertain. |

| ● | The Fund may pay distributions in significant part from sources that may not be available in the future and that are unrelated to the Fund’s performance, such as from offering proceeds, borrowings, and amounts from the Fund’s affiliates that are subject to repayment by investors. |

| ● | The Fund's distributions may be funded from unlimited amounts of offering proceeds or borrowings, which may constitute a return of capital and reduce the amount of capital available to the Fund for investment. Any capital returned to Shareholders through distributions will be distributed after payment of fees and expenses. |

| ● | A return of capital to Shareholders is a return of a portion of their original investment in the Fund, thereby reducing the tax basis of their investment. As a result from such reduction in tax basis, Shareholders may be subject to tax in connection with the sale of Shares, even if such Shares are sold at a loss relative to the Shareholder's original investment. |

Neither the SEC nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

This prospectus concisely provides you the information that a prospective investor should know about the Fund before investing in the shares of the Fund that are being offered through this prospectus. You are advised to read this prospectus carefully and to retain it for future reference. Additional information about the Fund, including the Fund’s Statement of Additional Information (“SAI”), dated June 21, 2022, has been filed with the SEC. Information regarding the Fund is available on the SEC’s website at http://www.sec.gov, including the SAI. The address of the SEC's website is provided solely for the information of prospective shareholders and is not intended to be an active link. The table of contents of the SAI appears on page 47 of this prospectus. The SAI is incorporated by reference into this prospectus (legally made a part of this prospectus). The SAI, Fund annual and semi-annual reports and other information and shareholder inquiries regarding the Fund are available free of charge and may be requested by writing the Fund c/o DST Systems PO Box 219445, Kansas City, MO 64121-9445 (the “Transfer Agent”), by calling the Transfer Agent toll-free at 1-844-819-8287, or by visiting the Fund’s website at http://www.bluerockfunds.com.

The Advisor. The Fund’s investment advisor is Bluerock Credit Fund Advisor, LLC (the “Advisor”), a registered advisor under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). The Advisor is a subsidiary of Bluerock Asset Management, LLC (“Bluerock”). Bluerock and its affiliates and principals have acquired or managed approximately $13.2 billion of assets as of March 31, 2022.

The Sub-Advisor. The Advisor has engaged WhiteStar Asset Management LLC (the “Sub-Advisor”) to serve as the Fund’s investment sub-adviser. The Sub-Advisor is a registered investment adviser under the Advisers Act and provides investment advisory services to its clients and has particular expertise in underwriting, managing and executing transactions with respect to senior secured loans, including on behalf of pooled investment vehicles that are CLOs. The Sub-Advisor is owned by Clearlake Strategic Partners, L.P., a Delaware limited partnership (an affiliate of Clearlake Capital Group, L.P. and collectively referred to herein as “Clearlake”), and by certain members of the Sub-Advisor’s management team. The Sub-Advisor acts as the credit and structured product arm of Clearlake. As of December 12, 2021, the Sub-Advisor and Clearlake, collectively had over $55 billion of assets under management focusing on credit, private equity and special situations.

Securities Offered. The Fund engages in a continuous offering of classes of shares of beneficial interest of the Fund, including Class A shares offered by this prospectus. The Fund and its Advisor have exemptive relief to offer multiple share classes. The Fund is authorized as a Delaware statutory trust to issue an unlimited number of shares and has registered an unlimited number of shares. The Fund is offering to sell, through its principal underwriter, ALPS Distributors, Inc. (the “Distributor”) on a continual basis under the terms of this prospectus, shares of beneficial interest at net asset value (“NAV”) per share of each share class, plus any applicable sales load. The initial NAV is $25.00 for Class A shares. The maximum sales load is 5.75% of the amount invested for Class A shares. Class C shares, Class F shares and Class I shares are not subject to sales charges. The minimum initial investment by a shareholder for Class A shares is $2,500 for regular accounts and $1,000 for retirement plan accounts, and a minimum subsequent investment of at least $100 for regular accounts and $50 for retirement plan accounts. The Fund also offers Class C, Class F and Class I shares, each by a separate prospectus. The Distributor is not required to sell any specific number or dollar amount of the Fund's shares, but will use best efforts to sell the shares. Monies received will be invested promptly and no arrangements have been made to place such monies in an escrow, trust or similar account. See “Plan of Distribution.”

The Fund’s shares have no history of public trading, nor is it intended that they will be listed on a public exchange at this time. No secondary market is expected to develop for the Fund’s shares, liquidity for the Fund’s shares will be provided only through quarterly repurchase offers for no less than 5% of the Fund’s shares and there is no guarantee that an investor will be able to sell all the shares that the investor desires to sell in the repurchase offer. Investing in the Fund’s shares involves substantial risks, including the risks set forth in the “Risk Factors” section of this prospectus.

| Per Class A Share | |

| Price to Public | Current NAV Plus Applicable Sales Load |

| Sales Load | 0%-5.75%(1) |

| Net Proceeds to Fund (Before Expenses)(2) | Amount Invested at Current Purchase Price Less Applicable Sales Load |

| (1) | Includes maximum selling commissions and dealer manager fees of 5.00% and 0.75%, respectively, of the Fund’s public offering price per Class A share. The Advisor or its affiliates, in the Advisor’s discretion and from their own resources (which may include the Advisor’s legitimate profits from the advisory fee it receives from the Fund), may pay additional compensation to brokers or dealers in connection with the sale and distribution of Fund shares. See “Plan of Distribution”. |

| (2) | The Fund anticipates that it will incur approximately $302,386 of offering-related expenses. |

For Class A shares, you will pay an upfront sales load of up to 5.75%, if you invest $100 in our Class A shares and pay the full upfront sales load, at least $94.25 but less than $100.00 of your investment will actually be used by us for investments. As a result, based on the initial public offering price of $25.00 per Class A share, you would have to experience a total return on your investment of 6.1% in Class A shares, in order to recover these expenses. However, other share classes can be more expensive over time than Class A shares because of the annual distribution and/or shareholder services fees imposed on other classes.

TABLE OF CONTENTS

| PROSPECTUS SUMMARY | 2 |

| SUMMARY OF FUND EXPENSES | 12 |

| FINANCIAL HIGHLIGHTS | 13 |

| USE OF PROCEEDS | 13 |

| THE FUND | 13 |

| INVESTMENT OBJECTIVE, POLICIES AND STRATEGIES | 13 |

| RISK FACTORS | 17 |

| MANAGEMENT OF THE FUND | 23 |

| DETERMINATION OF NET ASSET VALUE | 29 |

| CONFLICTS OF INTEREST | 30 |

| QUARTERLY REPURCHASES OF SHARES | 32 |

| DISTRIBUTION POLICY | 34 |

| DIVIDEND REINVESTMENT POLICY | 35 |

| U.S. FEDERAL INCOME TAX MATTERS | 36 |

| DESCRIPTION OF CAPITAL STRUCTURE AND SHARES | 37 |

| ANTI-TAKEOVER PROVISIONS IN THE DECLARATION OF TRUST | 38 |

| PLAN OF DISTRIBUTION | 39 |

| LEGAL MATTERS | 44 |

| REPORTS TO SHAREHOLDERS | 44 |

| INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM | 44 |

| ADDITIONAL INFORMATION | 44 |

| TABLE OF CONTENTS OF THE STATEMENT OF ADDITIONAL INFORMATION | 45 |

| NOTICE OF PRIVACY POLICY & PRACTICES | 46 |

PROSPECTUS SUMMARY

This summary does not contain all of the information that you should consider before investing in the shares. You should review the more detailed information contained or incorporated by reference in this prospectus and in the SAI, particularly the information set forth below under the heading “Risk Factors.”

The Fund

Bluerock High Income Institutional Credit Fund is a continuously offered, non-diversified, closed-end management investment company. See “The Fund.” The Fund is an interval fund that provides investor liquidity by offering to make quarterly repurchases of each class of shares at that class of shares’ net asset value, which will be calculated on a daily basis. See “Quarterly Repurchases of Shares” and “Determination of Net Asset Value.”

Investment Objective, Strategy and Policies

The Fund’s primary investment objective is to generate high current income, while secondarily seeking attractive, long-term risk-adjusted returns, with low correlation to the broader markets.

The Fund pursues its investment objective by investing, directly or indirectly, in senior secured loans (“Senior Secured Loans”). The Fund may purchase Senior Secured Loans directly in the primary or secondary market and will invest in them indirectly by purchasing various tranches, including senior, junior and equity tranches, of entities that own a diversified pool of Senior Secured Loans known as Collateralized Loan Obligations, or “CLOs”, (collectively with Senior Secured Loans, “Target Securities”). The Fund will generally focus its investment activities on U.S. dollar -denominated loans that (i) are broadly syndicated (i.e. with multiple institutional lenders) and made to U.S. companies, (ii) are senior in the capital structure with a priority claim on assets and cash flow of the underlying borrower, (iii) are primarily secured by first priority liens on assets of the underlying borrowers, (iv) are rated BB+ or below, known as “below investment grade” or “junk”, or are unrated (v) are floating rate to provide some protection against rising interest rates, (vi) may change over time but at origination represent 40%-60% of the enterprise value of the borrower, and (vii) in CLOs that own such loans and additionally (a) are diverse across issuers, industries and geographies, (b) have senior tranches with high credit ratings in order to maximize excess spread, (c) have attractive risk-adjusted spreads (i.e. spreads that are attractive after taking into account the risk associated with the underlying loan), and (d) are actively managed by experienced CLO collateral managers, including Trinitas Capital Management, LLC (“Trinitas”) or other advisers who may be associated with the Sub-Advisor. Securities which are “below investment grade” or “junk” are predominantly speculative in nature.

In a typical CLO, the capital structure would include approximately 90% debt of which over 85% is generally investment grade, with the remainder comprising the junior most CLO securities, typically referred to as the CLO’s junior debt tranche and equity tranche. Interest and principal repayment cashflows derived from the pool of Senior Secured Loans are allocated sequentially first to cover the operational and administrative costs of the CLO, second to the debt service of the highest-ranking debt tranche, third to the debt service of the next highest-ranking debt tranche and so on until all obligations of the CLO have been met, with all residual proceeds generally allocated to the equity tranche. This sequential cashflow allocation is usually referred to as the “payment waterfall.” The most subordinated tranche of securities is therefore the most sensitive to defaults and realized losses in relation to the underlying assets, and the most senior tranche is the least sensitive to them. The Fund’s investment portfolio will have significant investments in the equity and junior debt tranches of CLOs.

The investment committee for the Advisor (the “Investment Committee”) will formulate and implement a plan to construct and manage the Fund’s portfolio in accordance with its investment objective and strategies.

By investing in the Fund, the Advisor expects that the shareholders may realize the following potential benefits:

| ● | Access to Attractive Risk-Adjusted Returns from Institutional Private Credit Investments – The Fund will provide investors with exposure to private credit investments that are typically intended for large, institutional investors due to the large minimum investment size, which would limit the ability of individual, non-institutional investors to participate in such investments. The Fund invests in institutional private credit investments that offer what the Advisor and Sub-Advisor believe to be attractive risk-adjusted returns, with some downside protection provided by the senior secured nature of the underlying loans in which the Fund will invest either directly or indirectly. Senior secured loans generally have a first lien security interest in the assets of the underlying borrower, and have or share the most senior position in the borrower’s capital structure, meaning the holders of such loans will be paid before certain other creditors of the borrower and before all common equity holders in the event of a default, creating an “equity cushion” for such holders. |

2

| ● | Access to Relationship-Based Deal Flow – The Fund will have access to the Sub-Advisor’s substantial direct, long-standing relationships across market participants, including major U.S.-based CLO collateral managers and banks that originate and trade Target Securities, to identify investment opportunities. This comprehensive access to sourcing may offer strategic benefits, including a more efficient investment of Fund assets and the potential to identify investment opportunities before they are broadly marketed, enhancing the Fund’s ability to deliver attractive yields to investors. |

| ● | Substantial Platform and Resources with Seasoned Investment Professionals – The Fund will have access to the wider resources of the Advisor and the Sub-Advisor, respectively, including the Sub-Advisor’s established leveraged finance platform and proprietary quantitative approach to provide established underwriting and structuring capabilities to execute its investment strategy. We believe these personnel possess market knowledge, experience and industry relationships that enable them to identify potentially attractive investment opportunities in Target Securities and effectively manage the Fund’s portfolio. |

Under normal circumstances, the Fund invests at least 80% of its net assets (plus the amount of any borrowing for investment purposes) in Target Securities. The Fund may utilize leverage through borrowings for investment purposes or in order to satisfy repurchase requests. The Fund expects that such borrowings will be pursuant to a credit facility, however the Fund currently does not have access to a credit facility and there cannot be any assurance that the Fund will be able to obtain access to a credit facility. See “Leveraging Risk.” The Fund’s 80% investment policy may be changed upon 60 days’ advance notice to shareholders. The Fund’s SAI contains a list of all of the fundamental and non-fundamental investment policies of the Fund, under the heading “Investment Objective, Strategies and Policies.”

Investment Advisor

Bluerock Credit Fund Advisor, LLC is a Delaware limited liability company with its principal offices at 1345 Avenue of the Americas, 32nd Floor, New York, NY 10105. The Advisor was formed in November 2017 and is registered with the SEC as an investment adviser under the Advisers Act. The Advisor is a subsidiary of Bluerock Asset Management, LLC (“Bluerock”); Bluerock and its affiliates and principals have acquired or managed approximately $13.2 billion of assets as of March 31, 2022.

Sub-Advisor

WhiteStar Asset Management LLC is as a Delaware limited liability company with its principal offices at 200 Crescent Court, Suite 1175, Dallas, TX 75201. The Sub-Advisor was formed on February 28, 2013 and is a registered investment adviser under the Advisers Act. The Sub-Advisor provides investment advisory services to its clients and has particular expertise in underwriting, managing and executing transactions with respect to senior secured loans, including on behalf of pooled investment vehicles that are CLOs. The Sub-Advisor is owned by Clearlake Strategic Partners, L.P., a Delaware limited partnership (an affiliate of Clearlake Capital Group, L.P. and collectively referred to herein as “Clearlake”), and by certain members of the Sub-Advisor’s management team. The Sub-Advisor acts as the credit and structured product arm of Clearlake. The Sub-Advisor provides additional services associated with its asset management business, including trading, portfolio analysis, credit review and monitoring, asset valuation, and risk and compliance management to Trinitas. Trinitas provides investment advisory services, as a collateral manager and sponsor for pooled investment vehicles that are CLOs, including in connection with CLOs in which the Fund may invest. Certain investment professionals and other employees or officers of the Sub-Advisor may also be investment professionals or employees of other investment advisers, including Trinitas. Trinitas’ investment committee is currently comprised of individuals who are also investment professionals of both Trinitas and the Sub-Advisor. However, the Sub-Advisor and Trinitas have adopted policies and procedures to mitigate any conflicts of interest and any investments by the Fund in a CLO sponsored or managed by Trinitas will be approved by the Advisor’s Investment Committee, to further mitigate any potential conflict. As of December 12, 2021, the Sub-Advisor and Clearlake, had over $55 billion of assets under management focusing on credit, private equity and special situations.

3

The Sub-Advisor is responsible for selecting investments in accordance with the Fund’s investment objective, policies and restrictions. The Sub-Advisor also is responsible for trading portfolio securities and other investment instruments on behalf of the Fund and selecting broker-dealers to execute purchase and sale transactions, subject to the supervision of the Advisor and the Board. The Sub-Advisor is paid solely by the Advisor from its advisory fees. Shareholders do not pay the Sub-Advisor directly.

Advisor Fees

The Advisor is entitled to receive a fee consisting of two components — a base management fee and an incentive fee.

The base management fee is calculated and payable monthly in arrears at the annual rate of 1.75% of the average value of the Fund’s daily net assets during such period.

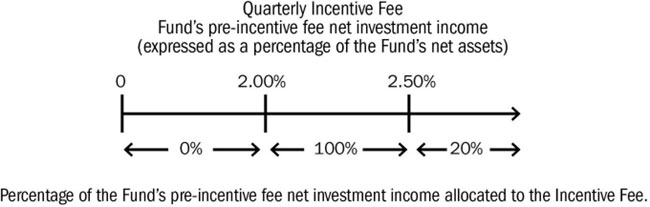

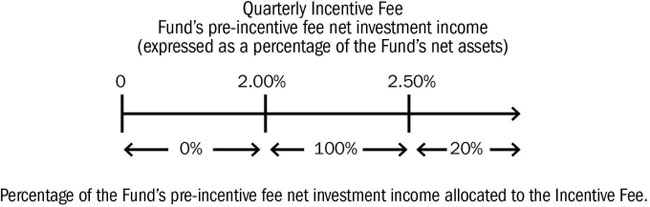

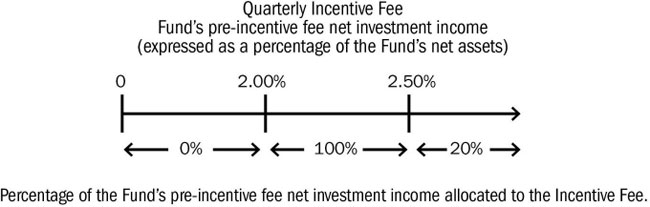

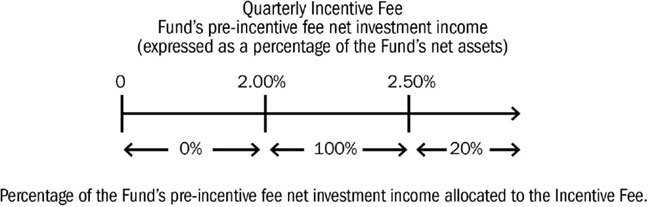

The incentive fee is calculated and payable quarterly in arrears in an amount equal to 20% of the Fund’s “pre-incentive fee net investment income” for the immediately preceding quarter, and is subject to a hurdle rate, expressed as a rate of return on the Fund’s net assets, equal to 2.0% per quarter (or an annualized hurdle rate of 8.0%), subject to a “catch-up” feature, which allows the Advisor to recover foregone incentive fees that were previously limited by the hurdle rate. For these purposes, “pre-incentive fee net investment income” means interest income, dividend income and any other income accrued during the calendar quarter, minus the Fund’s quarterly operating expenses (including the base management fee, expenses reimbursed to the Advisor or Sub-Advisor and any interest expenses and distributions paid on any issued and outstanding preferred shares, but excluding the incentive fee).

The calculation of the incentive fee on pre-incentive fee net investment income for each quarter is as follows:

| ● | No incentive fee is payable in any calendar quarter in which the Fund’s pre-incentive fee net investment income does not exceed the hurdle rate of 2.0% per quarter (or an annualized rate of 8.0%); |

| ● | 100% of the Fund’s pre-incentive fee net investment income, if any, that exceeds the hurdle rate but is less than or equal to 2.5% (the “Catch-Up”). The Catch-Up is intended to provide the Advisor with an incentive fee of 20.0% on all of the Fund’s pre-incentive fee net investment income when its pre-incentive fee net investment income reaches 2.5% in any calendar quarter; and |

| ● | 20.0% of the amount of the Fund’s pre-incentive fee net investment income, if any, that exceeds 2.5% in any calendar quarter (10.0% annualized) is payable to the Advisor once the hurdle rate is reached and the Catch-Up is achieved (20.0% of all pre-incentive fee net investment income thereafter will be allocated to the Advisor). |

Expense Limitation Agreement

The Advisor and the Fund have entered into an expense limitation and reimbursement agreement (the “Expense Limitation Agreement”) under which the Advisor has contractually agreed to waive the base management fees and/or reimburse the Fund for ordinary operating expenses the Fund incurs but only to the extent necessary to maintain the Fund's total annual operating expenses after fee waivers and/or reimbursement (exclusive of any incentive fee, taxes, interest, brokerage commissions, and extraordinary expenses, such as litigation or reorganization costs, but inclusive of organizational costs and offering costs), to the extent that such expenses exceed 2.60% per annum of the Fund's average daily net assets attributable to Class A shares (the “Expense Limitation”). For the avoidance of doubt, acquired fund fees and expenses are not operating costs and are therefore excluded from the Expense Limitation. In consideration of the Advisor’s agreement to limit the Fund's expenses, the Fund has agreed to repay the Advisor in the amount of any fees waived and Fund expenses paid or absorbed, subject to the limitations that: any waiver or reimbursement by the Advisor is subject to repayment by the Fund within the three years following the date the waiver or reimbursement occurred (provided the Advisor continues to serve as investment adviser to the Fund), if the Fund is able to make the repayment without exceeding the expense limitation then in effect or in effect at the time of the waiver and the repayment is approved by the Board of Trustees (the “Board”). The Expense Limitation Agreement will remain in effect at least until January 31, 2024, unless and until the Board approves its modification or termination. After January 31, 2024, the Expense Limitation Agreement may be renewed at the Advisor’s and Board's discretion. See “Management of the Fund.”

Administrator, Accounting Agent and Transfer Agent

ALPS Fund Services, Inc. (the “Administrator”) serves as the Fund’s administrator and accounting agent. DST Systems, Inc. serves as the transfer agent of the Fund. See “Management of the Fund.”

4

Distribution Fees

Class A shares are not subject to a distribution fee.

Closed-End Interval Fund Structure

Closed-end funds differ from open-end mutual funds in that closed-end funds do not typically redeem their shares at the option of the shareholder. Closed-end fund shares typically trade in the secondary market via a stock exchange. However, unlike other closed-end funds, the Fund is an “interval” fund whose shares will not be listed on a stock exchange and therefore will not have a secondary market. Instead, the Fund will provide limited liquidity to shareholders by offering to repurchase a limited amount of the Fund's shares (at least 5%) quarterly, which is discussed in more detail below. The Fund, similar to a mutual fund, is subject to continuous asset in-flows, but limited to out-flows through its quarterly repurchase offers.

Share Classes

The Fund offers four classes of shares: Class A, Class C, Class F and Class I shares. An investment in any share class of the Fund represents an investment in the same assets of the Fund. However, the sales loads, purchase restrictions, and ongoing fees and expenses for each share class are different. The loads, fees and expenses for Class A shares of the Fund are set forth in “Summary of Fund Expenses.” Not all share classes may be available in all states, or to all investors. If an investor has hired an intermediary and is eligible to invest in more than one class of shares, the intermediary may help determine which share class is appropriate for that investor. When selecting a share class, you should consider which share classes are available to you, how much you intend to invest, how long you expect to own shares, and the total costs and expenses associated with a particular share class.

Each investor’s financial considerations are different. You should speak with your financial advisor to help you decide which share class is best for you. Not all financial intermediaries offer all classes of shares and all share classes may not be available in every state. The Fund anticipates offering its Class A shares through a financial service intermediary platform. If your financial intermediary offers more than one class of shares, you should carefully consider which class of shares to purchase.

Repurchases of Shares

The Fund is an interval fund and, as such, has adopted a fundamental policy to make quarterly repurchase offers, at net asset value, of no less than 5% of the Fund’s shares outstanding. The first repurchase offer is expected to occur in September 2022 and will occur no later than two periodic intervals after the effective date of the Fund. There is no guarantee that shareholders will be able to sell all of the shares they desire to sell in a quarterly repurchase offer. Liquidity will be provided to shareholders only through the Fund's quarterly repurchases. See “Quarterly Repurchases of Shares.”

Investor Suitability

An investment in the Fund involves a considerable amount of risk. It is possible that you will lose some or all of your money invested. An investment in the Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the shares and should be viewed as a medium to long-term investment. Before making your investment decision, you should (i) consider the suitability of this investment with respect to your investment objectives and personal financial situation and (ii) consider factors such as your personal net worth, income, age, risk tolerance and liquidity needs. An investment in the Fund should not be viewed as a complete investment program.

Summary of Risks

Investing in the Fund involves risks, including the risk that you may receive little or no return on your investment, and that you may lose part or all of your investment. Before investing you should consider carefully the risks that you assume when you invest in the Fund's shares. See “Risk Factors.”

Market Risk. An investment in the Fund's shares is subject to investment risk, including the possible loss of the entire principal amount invested. The value of Fund investments, like other market investments, may move up or down, sometimes rapidly and unpredictably, which will subject shareholders to risk. In addition, the Fund is subject to the risk that geopolitical and other similar events will disrupt the economy on a national or global level. For instance, war, terrorism, market manipulation, government defaults, government shutdowns, political changes or diplomatic developments, public health emergencies (such as the spread of infectious diseases, pandemics and epidemics) and natural/environmental disasters can all negatively impact the securities markets.

5

The current novel coronavirus (COVID-19) global pandemic and the aggressive responses taken by many governments, including closing borders, restricting international and domestic travel, and the imposition of prolonged quarantines or similar restrictions, as well as the forced or voluntary closure of, or operational changes to, many retail and other businesses, have had negative impacts, and in many cases severe negative impacts, on markets worldwide. It is not known how long such impacts, or any future impacts of other significant events described above, will or would last, but there could be a prolonged period of global economic slowdown. Therefore, the Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. The foregoing could impair the Fund’s ability to maintain operational standards, disrupt the operations of the Fund and its service providers, adversely affect the performance, value and liquidity of the Fund’s investments, and negatively impact the Fund’s performance and your investment in the Fund. The value of your shares at any point in time may be worth less than the value of your original investment, even after taking into account any reinvestment of dividends and distributions.

Management Risk. Investments decisions regarding the relative attractiveness, value and potential appreciation of and returns on a particular investment, or allocation decisions with respect to the Fund’s portfolio, may prove to be incorrect, may not produce the desired results and/or may result in losses to the Fund and its shareholders. The Fund may be required to pay the Advisor incentive compensation for a quarter even if there is a decline in the value of the Fund’s portfolio or if the Fund incurs a net loss for that quarter because the Advisor and Sub-Advisor are entitled to receive incentive compensation on income regardless of any capital losses. The potential for the Advisor and Sub-Advisor to earn incentive fees under the Investment Advisory Agreement and Sub-Advisory Agreement, respectively, may create an incentive for it to enter into investments that are riskier or more speculative than would otherwise be in the Fund’s best interests.

Non-Diversification Risk. As a non-diversified fund, the Fund may invest more than 5% of its total assets in the securities of one or more issuers. The Fund’s performance may be more sensitive to any single economic, business, political or regulatory occurrence than the value of shares of a diversified investment company.

Debt Securities and Interest Rate Risks. Because the Fund invests primarily in debt-anchored instruments and securities, the value of your investment in the Fund may fluctuate with changes in interest rates. Typically, a rise in market interest rates will cause a decline in the value of fixed rate or other debt instruments. Market interest rates have been at historically low levels for a number of years, both in the United States and globally. It is difficult if not impossible to forecast future interest rates, but given their recent, historically low levels, there is a heightened risk that they may increase, perhaps substantially and perhaps in the near future. If market interest rates increase, there is a significant risk that the value of the Fund’s investment in fixed rate debt securities may fall, and that it may be more difficult for the Fund to raise capital. Related risks include credit risk (the debtor may default) and prepayment risk (the debtor may pay its obligation early, reducing the amount of interest payments).

Senior Secured Debt Risk. Senior secured debt typically will be secured by liens on the assets and/or cash flows of the borrower and holds the most senior position in its capital structure. Senior secured debt in most circumstances is initially fully collateralized by the borrower’s assets and thus it is repaid before unsecured debt and equity. Substantial increases in interest rates, however, may cause an increase in loan defaults as borrowers may lack resources to meet higher debt service requirements, or as a result of the impact on general business conditions caused by higher interest rates, and there can be no guaranty that secured senior debt, even if fully collateralized at origination, will be fully repaid after an event of default or if collateral values have fallen. Also, the security for the Fund’s senior secured debt investments may not be recognized for a variety of reasons, including the failure to make required filings by lenders, trustees or other responsible parties and, as a result, the Fund may not have priority over other creditors as anticipated.

Collateralized Loan Obligation (CLO) Risk. In addition to the general risks associated with investments in debt instruments and securities discussed herein, CLOs carry additional risks, including, but not limited to (i) the possibility that distributions from collateral will not be adequate to make interest or other payments; (ii) the quality of the collateral may decline in value or default; (iii) the possibility that the Fund’s investments in CLOs are subordinate to other classes or tranches thereof; and (iv) the complex structure of the CLO investment may not be fully understood at the time of investment and may produce disputes with the issuer, holders of senior tranches or other unexpected investment results.

6

In addition, CLOs and other structured products are often governed by a complex series of legal documents and contracts, which define the class or tranche of each investment, and may also increase the risk of dispute over the interpretation and enforceability of such documents relative to other types of investments. In a typical CLO, the capital structure would include approximately 90% debt, of which over 85% is generally investment grade, with the remainder comprising the junior most CLO securities, typically referred to as the CLO’s junior debt tranche and equity tranche. The Fund may acquire CLO investments in such equity and junior debt securities, which are subordinate to more senior tranches of the CLO. Such CLO equity and junior debt securities are therefore subject to increased risk of default relative to the holders of more senior tranches of the CLO. The Fund’s investment in equity tranches of CLO securities will be in the first loss position and junior debt tranches typically will be subordinate to more senior positions with respect to realized losses on the assets of the CLOs in which it is invested.

In connection with a primary issuance of a CLO, the structure of the CLO allows the CLO manager to purchase additional collateral (loans) for the CLO after the closing date of the Fund’s investment (the “Warehouse Period”). During the Warehouse Period, the price and availability of additional collateral may be adversely affected by a number of market factors, including price volatility and availability of investments suitable for the CLO, which could hamper the ability of the collateral manager to acquire additional collateral that will satisfy specified concentration limitations and allow the CLO to reach the initial par amount of collateral prior to its effective date. An inability or delay in reaching the target initial par amount of collateral may adversely affect the timing and amount of interest or principal payments received by the holders of the CLO debt securities and distributions of the CLO on equity securities and could result in early redemptions which may cause CLO debt and equity investors to receive less than face value of their investment, resulting in a loss.

The failure by a CLO in which the Fund invests to satisfy financial covenants, including with respect to adequate collateralization and/or interest coverage tests, could lead to a reduction in the CLO’s payments to the Fund. In the event that a CLO fails certain tests, holders of CLO senior debt may be entitled to additional payments that would, in turn, reduce the payments the holders of the junior debt tranche and the equity tranche would otherwise be entitled to receive. Separately, the Fund may incur expenses to the extent necessary to seek recovery upon default or to negotiate new terms, which may include the waiver of certain financial covenants, in connection with a defaulting CLO or any other investment the Fund may make. If any of these occur, it could adversely affect the Fund’s operating results and cash flows.

The Fund’s investments in Senior Secured Loans in CLOs may be riskier and less transparent to the Sub-Advisor than direct investments in the underlying companies. The Sub-Advisor cannot be certain that due diligence investigations with respect to any investment opportunity for the Fund will reveal or highlight all relevant facts (including fraud) that may be necessary or helpful in evaluating such investment opportunity, or that its due diligence investigations will result in investments for the Fund being successful. There is limited control of the administration and amendment of Senior Secured Loans in CLOs. Senior Secured Loans in CLOs may be sold and replaced resulting in a loss to the Fund.

The Fund’s CLO investments are exposed to leveraged credit risk. If certain minimum collateral value ratios and/or interest coverage ratios are not met by a CLO, primarily due to defaults under the Senior Secured Loans in which the CLO has invested, then cash flow that otherwise would have been available to pay distributions to the Fund on its CLO investments may instead be used to redeem senior tranches or to purchase additional collateral for all tranches, until the ratios again exceed the minimum required levels or any the senior tranches of CLO debt are repaid in full. The Fund’s investments in CLOs or Senior Secured Loans may prepay more quickly than expected, which could have an adverse impact on the Fund’s net assets and/or returns.

The Fund may recognize “phantom” taxable income (due to allocations of profits or cancellation of debt, which results in recognition of taxable income regardless of whether a corresponding amount of cash is actually received) from its investments in these subordinated tranches of CLOs and structured notes. The CLOs in which the Fund invests may constitute Passive Foreign Investment Companies (“PFICs”). If the Fund acquires shares in a PFIC (including in CLOs that are PFICs), the Fund may be subject to U.S. federal income tax on a portion of any “excess distribution” or gain from the disposition of such shares even if such income is distributed as a taxable dividend by the Fund to its shareholders. Certain elections may be available to mitigate or eliminate such tax on excess distributions, but such elections (if available) will generally require the Fund to recognize its share of the PFICs income for each year regardless of whether it receives any distributions from such PFICs. The Fund must nonetheless distribute such income to maintain its status as a RIC.

Covenant-Lite Loan Risk. The loans in which the Fund invests will include “covenant-lite loans.” Covenant-lite loans contain fewer maintenance covenants on the borrower than traditional loans (or no maintenance covenants at all) and fewer protections for the lender, such as terms that allow the lender to monitor the financial performance of the borrower and declare a default if certain criteria are breached.

7

Credit Risk. It is possible that the borrowers under the Senior Secured Loans may not make scheduled interest and/or principal payments on their loans and/or debt securities, which may result in losses or reduced cash flow to the Fund, either or both of which may cause the Net Asset Value of, or the distributions by, the Fund to decrease. In addition, the credit quality of securities held by the Fund may fall if the underlying borrowers’ financial condition deteriorates. This also may negatively impact the value of and the Fund’s returns on its investment in such securities.

Prepayment Risk. Debt securities may be subject to prepayment risk because borrowers are typically able to repay their debt obligations prior to maturity principal. Consequently, a debt security's maturity may be longer or shorter than anticipated. When interest rates fall, debt obligations tend to be refinanced or otherwise paid off more quickly than originally anticipated. If that occurs with respect to the Fund’s investments, the Fund may have to invest the prepaid proceeds in securities with lower yields. When interest rates rise, obligations will tend to be paid off by the obligor more slowly than anticipated, preventing the Fund from reinvesting at higher comparable or yields. For certain investments, lower-than-expected prepayment rates may expose investments in the junior tranches of CLOs to credit risks for longer periods of time.

LIBOR Risk. The Fund invests in Target Securities that may have floating or variable rate calculations for payment obligations or financing terms based on the London Interbank Offered Rate (LIBOR), which is the benchmark interest rate at which major global banks lend to one another in the international interbank market for short-term loans. It was originally anticipated that LIBOR would be discontinued by the end of 2021 and would cease to be published after that time. Although many LIBOR rates were phased out at the end of 2021 as originally intended, a selection of widely used USD LIBOR rates will continue to be published until June 2023 in order to assist with the transition to an alternative rate. The impact of the discontinuation of LIBOR and the transition to an alternative rate on the Fund's portfolio remains uncertain. There can be no guarantee that financial instruments that transition to an alternative reference rate will retain the same value or liquidity as they would otherwise have had.

On March 5, 2021, the United Kingdom’s Financial Conduct Authority (the “FCA”) announced that all LIBOR benchmarks related to sterling, euro, Swiss franc and Japanese yen and the 1-week and 2-month US dollar settings will permanently cease immediately after December 31, 2021, and the remaining US dollar settings will cease immediately after June 30, 2023. On March 15, 2022, President Biden signed the Adjustable Interest Rate (LIBOR) Act, which is intended to provide a transition from LIBOR to a Secured Overnight Financing Rate (“SOFR”) based rate for certain legacy contracts which lack adequate fallback provisions and would be difficult to amend. The LIBOR Act does not affect contracts which already contain benchmark replacement or alternate interest rate provisions and amends the Trust Indenture Act of 1939 to resolve potential conflicts between the provisions of that legislation and changes authorized under the LIBOR Act. The Board of Governors of the U.S. Federal Reserve System (the Fed) is charged with adopting regulations to implement the LIBOR Act and establish a replacement rate based on SOFR (including establishing spread adjustments for the one, three and six month interest period tenors). As an alternative to LIBOR, the Fed, in conjunction with the Alternative Reference Rates Committee, a steering committee comprised of large U.S. financial institutions, is considering replacing U.S. dollar LIBOR with a new index calculated by short-term repurchase agreements, backed by Treasury securities. Uncertainty related to the pending transition away from LIBOR may adversely affect the market for LIBOR-based securities. There are obstacles to converting certain securities and transactions to a new benchmark. Abandonment of or modifications to LIBOR could lead to significant short-term and long-term uncertainty, market instability, illiquidity in markets for instruments whose terms currently include LIBOR and could have adverse impacts on newly issued financial instruments and existing financial instruments which reference LIBOR. It remains uncertain how such changes would be implemented and the effects such changes would have on the Fund, issuers of instruments in which the Fund invests and financial markets generally. The CLOs in which the Fund invests in generally contemplate a scenario where LIBOR is no longer available by requiring the CLO administrator to calculate a replacement rate primarily through dealer polling on the applicable measurement date. However, there is uncertainty regarding the effectiveness of the dealer polling processes, including the willingness of banks to provide such quotations, which could adversely impact our net investment income. In addition, the effect of a phase out of LIBOR on U.S. senior secured loans, which are also the underlying assets of CLOs, is currently unclear. To the extent that any replacement rate utilized for senior secured loans differs from that utilized for a CLO that holds those loans, the CLO would experience an interest rate mismatch between its assets and liabilities, which could have an adverse impact on our net investment income and portfolio returns.

Investment Sourcing Risk. The results of the Fund’s operations depend on several factors, including its ability to originate or acquire target investments. The Fund’s ability to originate or acquire target investments will depend on a variety of factors, including the availability of opportunities for the origination or acquisition of target investments, its ability to raise capital or obtain adequate short and long-term financing to fund such originations and acquisitions and competition for such originations and acquisitions.

8

Risk Related to Potential Conflicts of Interest. The Advisor and Sub-Advisor will experience conflicts of interest in connection with the management of the Fund, including with respect to the allocation of their time and resources between the Fund and other investment activities; the allocation of investment opportunities by the Sub-Advisor; their compensation; services provided by the Advisor or Sub-Advisor to issuers in which the Fund invests; investments by the Fund in other clients of the Advisor or Sub-Advisor; and the formation of additional investment funds by the Advisor or Sub-Advisor. In addition, the Sub-Advisor’s investment professionals will, from time to time, acquire confidential or material, non-public information concerning an entity in which the Fund has invested, or propose to invest, and the possession of such information generally will limit their ability to buy or sell particular securities of such entity on behalf of the Fund, thereby limiting the investment opportunities or exit strategies available to the Fund. While the Sub-Advisor and Trinitas are not affiliates within the definition of the Investment Company Act of 1940, they may have certain employees or officers in common. The Sub-Advisor and Trinitas have policies in place to mitigate potential conflicts of interest and any investment in a CLO sponsored or managed by Trinitas will be approved by the Advisor’s Investment Committee. See “Conflicts of Interest” below.

Defaulted Securities Risk. Loans in which the Fund invests, including Senior Secured Loans in which the Fund indirectly invests through investments in CLOs, may fall into default. Defaulted loans/debt securities provide less liquidity to the Fund than performing loans and, for extended periods of time, may have a limited or no secondary market. Defaulted loans/debt securities may have low recovery values and borrowers or issuers in default of their debt obligations may seek bankruptcy protection, which may hinder or delay resolution of the Fund's collection efforts.

Below Investment Grade Risk. Lower-quality debt investments, known as “below investment grade” or “junk”, are speculative and present greater risk than investments of higher quality, including an increased risk of default. An economic downturn or period of rising interest rates could adversely affect the market for these investments and reduce the Fund’s ability to sell its investments. Additionally, high yield issuers may seek bankruptcy protection which will delay resolution of creditor claims and may eliminate or materially reduce liquidity. The Sub-Advisor’s assessment of an issuer’s credit quality may prove incorrect and the Fund could suffer losses.

Syndicated Loan Risk. The Fund may invest in syndicated loans, which are typically loans to corporate entities originated by one or more lenders, and then traded in the secondary market. The primary risk of a syndicated loan is the creditworthiness of the corporate borrower.

Issuer/Borrower Risk. The Fund’s investments in debt securities issued by a specific issuer or borrower may perform differently than the performance of credit markets in general, and therefore may be more volatile. Issuer-specific risks may include: the risk of poor management performance, excessive financial leverage, and reduced demand for the issuer’s goods and/or services. Additionally, borrowers experiencing financial difficulties could seek bankruptcy protection, which may limit or delay the Fund’s ability to obtain judgment or collect on defaulted loans.

Correlation Risk. Pursuant to the Fund’s investment objective, the Fund seeks to produce returns with low correlation to the broader financial markets. There is no guaranty that the Fund will succeed in achieving its investment objective or that the Fund will outperform the broader financial markets.

Liquidity Risk – Quarterly Repurchases. The Fund’s shares are not listed on any securities exchange and are not publicly traded. There currently is no secondary market for the Fund's shares and the Advisor does not expect that a secondary market will develop. Limited liquidity is provided to shareholders only through the Fund's quarterly repurchase offers, for no less than 5% of the Fund's shares outstanding at net asset value. There is no guarantee that all shareholders seeking liquidity will be able to sell all of the shares that they desire to sell in a quarterly repurchase offer.

Liquidity Risk – Underlying Investments. The Fund's investments, such as in Target Securities, are subject to liquidity risk. This liquidity risk exists because particular investments of the Fund may be difficult to sell, possibly preventing the Fund from selling them at an advantageous time or price, or possibly requiring the Fund to dispose of other investments at unfavorable times or prices, in order to satisfy its 5% quarterly repurchase obligations.

Leveraging Risk. The Fund is authorized to use leverage for investment purposes and to satisfy redemption requests. The use of leverage will cause the Fund to incur additional expenses and may significantly magnify the Fund's losses in the event of adverse performance of the Fund’s underlying investments.

Repurchase Policy Risk. Quarterly repurchases by the Fund of its shares typically will be funded from available cash or sales of portfolio securities. However, payment for repurchased shares may require the Fund to liquidate portfolio holdings early or at inopportune times, potentially resulting in losses, and may increase the Fund’s portfolio turnover. The Fund may take measures to attempt to avoid or minimize such potential losses and turnover, and instead of liquidating portfolio holdings, may borrow money to finance repurchases of shares. If the Fund borrows to finance repurchases, interest on any such borrowing will negatively affect shareholders who do not tender their shares in a repurchase offer by increasing the Fund’s expenses and reducing any net investment income.

9

Repurchase of shares will tend to reduce the number of outstanding shares and, depending upon the Fund’s investment performance, its net assets. A reduction in the Fund’s net assets may increase the Fund’s expense ratio, to the extent that additional shares are not sold. In addition, a repurchase of shares submitted by a shareholder will result in the recognition of taxable gain or loss in an amount equal to the difference between the amount realized and the shareholder’s tax basis in his or her Fund shares. Such gain or loss is treated as a capital gain or loss if the shares are held as capital assets. However, any loss realized upon the repurchase of shares within six months from the date of their purchase will be treated as a long-term capital loss to the extent of any amounts treated as capital gain dividends during such six-month period. All or a portion of any loss realized upon the repurchase of shares may be disallowed to the extent shares are purchased (including shares acquired by means of reinvested dividends) within 30 days before or after such repurchase.

Distribution Policy Risk. The Fund’s distribution policy is not designed to generate, and is not expected to result in, distributions to investors that equal a fixed percentage of the Fund’s current net asset value per share. Shareholders should not assume that the source of a distribution from the Fund is net profit. Shareholders should note that return of capital will reduce the tax basis of their shares and potentially increase the taxable gain, if any, upon disposition of their shares.

Minimal Capitalization Risk. The Fund is not obligated to raise any specific amount of capital prior to commencing operations. There is a risk that the amount of capital actually raised by the Fund through the offering of its shares may be insufficient to achieve profitability or allow the Fund to realize its investment objective. Therefore, an inability to raise substantial capital may significantly adversely affect the Fund’s financial condition, liquidity and results of operations, as well as its ability to comply with regulatory requirements. Further, if the Fund fails to achieve its estimated size and the Expense Limitation is not renewed, future expenses will be higher than expected.

No Operating History. The Fund is a closed-end investment company with no history of operations for potential investors to review. If the Fund commences operations under inopportune market or economic conditions, it may not be able to achieve its investment objective.

U.S. Federal Income Tax Matters

The Fund intends to elect to be treated and to qualify each year for taxation as a regulated investment company under Subchapter M of the Code. In order for the Fund to so qualify, it must, among other requirements, meet an income and asset diversification test each year. If the Fund so qualifies and satisfies the applicable distribution requirements, the Fund (but not its shareholders) will not be subject to federal income tax to the extent it distributes its investment company taxable income and net capital gains (the excess of net long-term capital gains over net short-term capital loss) in a timely manner to its shareholders in the form of dividends or capital gain distributions. The Code imposes a 4% nondeductible excise tax on regulated investment companies, such as the Fund, to the extent they do not meet certain distribution requirements by the end of each calendar year. The Fund anticipates meeting these distribution requirements. See “U.S. Federal Income Tax Matters.”

Distribution Policy

The Fund’s distribution policy is to make quarterly distributions to shareholders. The level of quarterly distributions (including any return of capital) is not fixed, but is expected to represent an annual rate of approximately 8.0% of the Fund’s current net asset value per share. Such distributions are accrued daily (Saturdays, Sundays and holidays included) and paid quarterly. This distribution policy is subject to change. The level of quarterly distributions (including any return of capital) is not fixed and all or a portion of a distribution may consist of a return of capital. Shareholders should not assume that the source of a distribution from the Fund is net profit.

Unless a shareholder elects otherwise, the shareholder's distributions will be reinvested in additional shares of the same class under the Fund's dividend reinvestment policy. Shareholders who elect not to participate in the Fund's dividend reinvestment policy will receive all distributions in cash paid to the shareholder of record (or, if the shares are held in street or other nominee name, then to such nominee). Distributions are made at the class level, so they may vary from class to class within the Fund. See “Dividend Reinvestment Policy.”

10

Custodian

UMB Bank, N.A (“Custodian”), with principal offices at 1010 Grand Boulevard, Kansas City, Missouri 64106, serves as the Fund’s custodian.

11

SUMMARY OF FUND EXPENSES

| Shareholder Transaction Expenses | Class A |

|

Maximum Sales Load (as a percent of offering price) |

5.75% |

| Maximum Early Withdrawal Charge (as a percent of original purchase price) | None1 |

| Annual Expenses (as a percentage of average net assets attributable to shares) |

|

| Base Management Fee | 1.75% |

| Incentive Fee2 | None |

| Other Expenses3,4 | 1.29% |

| Shareholder Servicing Expenses | 0.25% |

| Distribution Fee | None |

| Remaining Other Expenses4 | 1.04% |

| Total Annual Expenses3 | 3.04% |

| Fee Waiver and Reimbursement 3,5 | (0.44%) |

| Total Annual Expenses (after fee waiver and reimbursement) 3,5 | 2.60% |

| 1. | Class A shares that were purchased in amounts of $1,000,000 or more that have been held less than one year (365 days) from the purchase date will be subject to an early withdrawal charge of 1.00% of the original purchase price. |

| 2. | The Fund anticipates that it may generate income in a manner sufficient to result in the payment of an Incentive Fee to the Advisor during certain periods. However, the Incentive Fee is based on the Fund’s performance and will not be paid unless the Fund achieves certain performance targets. As a result, the Fund cannot accurately estimate the amount of Incentive Fees for the current fiscal year. The Fund expects the Incentive Fee the Fund pays to increase to the extent the Fund earns greater income through its investments in Target Securities. The Incentive Fee is calculated and payable quarterly in arrears in an amount equal to 20% of the Fund’s ‘‘pre-incentive fee net investment income’’ for the immediately preceding fiscal quarter, and is subject to a hurdle rate, expressed as a rate of return on the Fund’s net assets, equal to 2.00% per quarter, or an annualized hurdle rate of 8.00%, subject to a ‘‘catch-up’’ feature. See “Base Management Fee and Incentive Fee on page 26.” |

| 3. | Estimated for the current fiscal year. Other Expenses estimate directly impacts Total Annual Expenses, Fee Waiver and Reimbursement, and Total Annual Expenses (after fee waiver and reimbursement). |

| 4. | Other Expenses include all other operating expenses of the Fund, including research and risk management fees, offering and organizational expenses. |

| 5. | The Advisor and the Fund have entered into an expense limitation and reimbursement agreement (the “Expense Limitation Agreement”) under which the Advisor has contractually agreed to waive the base management fees and/or reimburse the Fund for ordinary operating expenses the Fund incurs but only to the extent necessary to maintain the Fund's total annual operating expenses after fee waivers and/or reimbursement (exclusive of any incentive fee, taxes, interest, brokerage commissions, and extraordinary expenses, such as litigation or reorganization costs, but inclusive of organizational costs and offering costs), to the extent that such expenses exceed 2.60% per annum of the Fund's average daily net assets attributable to Class A shares (the “Expense Limitation”). For the avoidance of doubt, acquired fund fees and expenses are not operating costs and are therefore excluded from the Expense Limitation. In consideration of the Advisor’s agreement to limit the Fund's expenses, the Fund has agreed to repay the Advisor in the amount of any fees waived and Fund expenses paid or absorbed, subject to the limitations that: any waiver or reimbursement by the Advisor is subject to repayment by the Fund within the three years following the date the waiver or reimbursement occurred (provided the Advisor continues to serve as investment adviser to the Fund), if the Fund is able to make the repayment without exceeding the expense limitation then in effect or in effect at the time of the waiver and the repayment is approved by the Board of Trustees (the “Board”). The Expense Limitation Agreement will remain in effect at least until January 31, 2024, unless and until the Board approves its modification or termination. After January 31, 2024, the Expense Limitation Agreement may be renewed at the Advisor’s and Board's discretion. See “Management of the Fund.” |

The above Summary of Fund Expenses table describes the fees and expenses that you may pay if you buy and hold shares of the Fund. More information about management fees, fee waivers and other expenses is available in Management of the Fund starting on page 23 of this prospectus.

The following example illustrates the hypothetical expenses that you would pay on a $1,000 investment assuming annual expenses attributable to shares remain unchanged and shares earn a 5% annual return. The below example gives effect to the Expense Limitation Agreement for only year one and no redemption by you.

12

| Share Class | 1 Year |

3 Years |

5 Years |

10 Years |

| Class A Shares | $82 | $142 | $204 | $370 |

Shareholders of Class A shares who choose to participate in repurchase offers by the Fund will not incur an early withdrawal charge, unless the repurchase is less than 365 days after purchase by a shareholder who purchased in amounts of $1,000,000 or more. However, if shareholders request repurchase proceeds be paid by wire transfer, such shareholders will be assessed an outgoing wire transfer fee at prevailing rates charged by the Administrator, currently $15. The purpose of the above table is to help a holder of shares understand the fees and expenses that such holder would bear directly or indirectly. The example should not be considered a representation of actual future expenses. Actual expenses may be higher or lower than those shown.

FINANCIAL HIGHLIGHTS

Because the Fund is newly formed and has no performance history as of the date of this Prospectus, a financial highlights table for the Fund has not been included in this Prospectus.

USE OF PROCEEDS

The net proceeds of the Fund’s continuous offering of shares, after payment of the sales load (if applicable) and other associated expenses, will be invested in accordance with the Fund's investment objective and policies (as stated below) as soon as practicable after receipt. The Fund pays organizational costs and its offering expenses incurred with respect to its initial and continuous offering. Pending investment of the net proceeds in accordance with the Fund's investment objective and policies, the Fund will invest in money market or short-term fixed-income mutual funds. Investors should expect, therefore, that before the Fund has fully invested the proceeds of the offering in accordance with its investment objective and policies, the Fund's assets would earn interest income at a modest rate. While the Fund does not anticipate a delay in the investment of additional net proceeds received from investors, it may take up to three months after completion of any offering to invest the net proceeds or otherwise utilize such proceeds, although such period may vary and depends on the size of additional offering proceeds and the availability of appropriate investment opportunities consistent with the Fund’s investment objectives and market conditions.

THE FUND

The Fund is a continuously offered, non-diversified, closed-end management investment company that is operated as an interval fund. The Fund was organized as a Delaware statutory trust on August 19, 2021. The Fund's principal office is located at 1345 Avenue of the Americas, 32nd Floor, New York, NY 10105, and its telephone number is (212) 843-1601.

INVESTMENT OBJECTIVE, POLICIES AND STRATEGIES

Investment Objective and Policies

The Fund’s primary investment objective is to generate high current income, while secondarily seeking attractive, long-term risk-adjusted returns with low correlation to the broader markets.

The Fund pursues its investment objective by investing, directly or indirectly, in senior secured loans (“Senior Secured Loans”). The Fund may purchase Senior Secured Loans directly in the primary or secondary market and will invest in them indirectly by purchasing various tranches, including senior, junior and equity tranches, of entities that own a diversified pool of Senior Secured Loans known as Collateralized Loan Obligations, or “CLOs”, (collectively with Senior Secured Loans, “Target Securities”). The Fund will generally focus its investment activities on U.S. dollar -denominated loans that (i) are broadly syndicated (i.e. with multiple institutional lenders) and made to U.S. companies, (ii) are senior in the credit structure with a priority claim on assets and cash flow of the underlying borrower, (iii) are primarily secured by first priority liens on assets of the underlying borrowers, (iv) are rated BB+ or below, known as “below investment grade” or “junk”, (v) are floating rate to provide some protection against rising interest rates, (vi) represent 40%-60%, at origination, of the enterprise value of the borrower, and (vii) in CLOs that own such loans and additionally (a) are diverse across issuers, industries and geographies, (b) have senior tranches with high credit ratings in order to maximize excess spread, (c) have attractive risk-adjusted spreads, and (d) are actively managed by experienced CLO collateral managers, including Trinitas or other advisers who may be associated with the Sub-Advisor. Securities which are “below investment grade” or “junk,” are predominantly speculative in nature.

13

In a typical CLO, the capital structure would include approximately 90% debt of which over 85% is generally investment grade, with the remainder comprising the junior most CLO securities, typically referred to as the CLO’s junior debt tranche and equity tranche. Interest and principal repayment cashflows derived from the pool of Senior Secured Loans are allocated sequentially first to cover the operational and administrative costs of the CLO, second to the debt service of the highest-ranking debt tranche, third to the debt service of the next highest-ranking debt tranche and so on until all obligations of the CLO have been met, with all residual proceeds generally allocated to the equity tranche. This sequential cashflow allocation is usually referred to as the “payment waterfall.” The most subordinated tranche of securities is therefore the most sensitive to defaults and realized losses in relation to the underlying assets, and the most senior tranche is the least sensitive to them. The Fund’s investment portfolio will have significant investments in the equity and junior debt tranches of CLOs.

The Investment Committee will formulate and implement a plan to construct and manage the Fund’s portfolio in accordance with its investment objective and strategies.

The Advisor expects that the Fund’s shareholders may realize the following potential benefits:

| ● | Access to Attractive Risk-Adjusted Returns from Institutional Private Credit Investments – The Fund will provide investors with exposure to private credit investments that are typically intended for large, institutional investors due to the large minimum investment size, which would limit the ability of individual, non-institutional investors to participate in such investments. The Fund invests in institutional private credit investments that offer what the Advisor and Sub-Advisor believe to be attractive risk-adjusted returns, with some downside protection provided by the senior secured nature of the underlying loans in which the Fund will invest either directly or indirectly. Senior secured loans generally have a first lien security interest in the assets of the underlying borrower, and have or share the most senior position in the borrower’s capital structure, meaning the holders of such loans will be paid before certain other creditors of the borrower and before all common equity holders in the event of a default, creating an “equity cushion” for such holders. |

| ● | Access to Relationship-Based Deal Flow – The Fund will have access to the Sub-Advisor substantial direct, long-standing relationships across market participants, including major U.S.-based CLO collateral managers and banks that originate and trade Target Securities, to identify investment opportunities. This comprehensive access to sourcing may offer strategic benefits, including a more efficient investment of Fund assets and the potential to identify investment opportunities before they are broadly marketed, enhancing the Fund’s ability to deliver attractive yields to investors. |

| ● | Substantial Platform and Resources with Seasoned Investment Professionals – The Fund will have access to the wider resources of the Advisor and the Sub-Advisor, respectively, including the Sub-Advisor’s established leveraged finance platform and proprietary quantitative approach to provide established underwriting and structuring capabilities to execute its investment strategy. We believe these personnel possess market knowledge, experience and industry relationships that enable them to identify potentially attractive investment opportunities in Target Securities and effectively manage the Fund’s portfolio. |

Fund's Target Investment Portfolio

The Advisor and Sub-Advisor intend to execute the Fund's investment strategy primarily by investing directly or indirectly in Senior Secured Loans or CLOs.

| ● | Senior Secured Loans: Senior Secured Loans are floating rate credit instruments structured primarily with first-priority liens on the assets of the borrower, including, but not limited to cash, receivables, inventory and PP&E, that serve as collateral in support of the repayment of such debt. Senior Secured Loans are predominately used to fund a company’s growth, financing their business, M&A-related transactions or capital expenditures. Senior Secured Loans typically have the highest priority in receiving payments, ahead of both bondholders and preferred stockholders. |

14

| ● | Collateralized Loan Obligations: Structurally, CLOs are actively managed special purpose vehicles that are formed to manage a portfolio of Senior Secured Loans. The loans within a CLO are predominately limited to Senior Secured Loans which meet specified credit and diversity criteria and are subject to concentration limitations in order to create an investment portfolio that is strategically diversified across different loans, borrowers, and industries, with limitations on non-U.S. borrowers. The Fund will seek to target CLOs comprised of broadly syndicated Senior Secured Loans made to large corporate borrowers, with loan sizes typically exceeding $500 million, which we believe are generally more liquid compared to loans to smaller middle-market borrowers. The Fund will invest in new issue transactions in the primary market and transactions in the secondary market. |

Investment Process

The Sub-Advisor assists the Advisor by providing ongoing research, recommendations and selecting investments for the Fund’s portfolio. The Sub-Advisor seeks to create an investment portfolio that generates current income while secondarily seeking attractive, long-term risk-adjusted returns, with low correlation to the broader markets, through a disciplined and rigorous investment analysis and due diligence process.

Proactive Sourcing and Identification Investment Opportunities. The Fund will utilize the Sub-Advisor’s leveraged finance platform and industry relationships to source investment opportunities. The Sub-Advisor has direct contact with and access to major U.S.-based banks and CLO collateral managers that originate and trade Senior Secured Loans and CLO interests.

Disciplined and Rigorous Investment Analysis and Due Diligence Process. The Sub-Advisor utilizes an integrated approach when investing in structured credit, enabling cross-collaboration between its senior secured loan team and its CLO investment team. This collaborative framework, which employs both “top-down” and “bottom-up” analyses, provides enhanced visibility into the Target Securities. The top-down analysis involves a macro analysis of relative asset valuations, long-term industry trends, business cycles, interest rate expectations, credit fundamentals, and technical factors to target specific industry sectors and asset classes in which to invest. The bottom-up analysis includes a rigorous analysis of the credit fundamentals and capital structure of each potential investment and a determination of relative value compared to alternative investments. Potential investments will be analyzed through a thorough review of the fundamentals of the economy in general and then the particular industry and the strengths and weaknesses of each individual credit. Under this approach, the credit performance of each asset will typically be subjected to stress tests to maximize the selection of investments with favorable risk adjusted returns.