Table of Contents

Delaware |

1400 |

87-3426517 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

| J. Eric Johnson, Esq. Winston & Strawn LLP 800 Capitol Street, Suite 2400 Houston, TX 77002 (713) 651-2647 |

Chantel Jordan, Esq. General Counsel 5E Advanced Materials, Inc. 19500 State Highway 249, Suite 125 Houston, Texas 77070 (346) 439-9656 |

Large accelerated filer |

☐ |

Accelerated filer |

☐ | |||

☒ |

Smaller reporting company |

|||||

Emerging growth company |

||||||

Table of Contents

The information in this prospectus is not complete and may be changed. These securities may not be resold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION DATED OCTOBER 11, 2022 |

5E ADVANCED MATERIALS, INC.

Up to 4,581,534 Shares of Common Stock Issuable Upon Conversion of Convertible Notes

This prospectus relates to the offer and sale of up to 4,581,534 shares (the “Resale Shares”) of common stock, par value $0.01 per share (the “Common Stock”) of 5E Advanced Materials, Inc. (the “Company”) issuable upon the conversion of amounts outstanding (including principal and accrued interest thereon) under convertible notes (the “Convertible Notes”) issued pursuant to a convertible note purchase agreement (the “Note Purchase Agreement”), dated August 11, 2022, between the selling shareholder named herein (the “Selling Shareholder”), the guarantors signatory thereto, and Alter Domus (US) LLC as collateral agent (the “Collateral Agent”).

We will not receive any proceeds from the sale of the Resale Shares by the Selling Shareholder. We will pay the expenses associated with the sale of securities pursuant to this prospectus.

We are registering the Resale Shares pursuant to the Selling Shareholder’s registration rights under a registration rights agreement, dated August 26, 2022, between us and the Selling Shareholder (the “Registration Rights Agreement”). Our registration of the Resale Shares does not mean that the Selling Shareholder will sell any of the securities offered hereby. The Selling Shareholder may offer and sell the Resale Shares in a number of different ways and at varying prices. We provide more information about how the Resale Shares may be sold in the section entitled “Plan of Distribution.”

You should read this prospectus and any amendment carefully before you purchase any securities being offered hereby.

Our Common Stock is listed on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “FEAM”. On October 7, 2022, the closing price of our Common Stock was $10.16.

Investing in our shares of Common Stock involves substantial risks. See “Risk Factors” beginning on page 20 of this prospectus to read about important factors you should consider before purchasing such shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2022.

Table of Contents

TABLE OF CONTENTS

| 1 | ||||

| 2 | ||||

| 8 | ||||

| 20 | ||||

| 59 | ||||

| 60 | ||||

| 61 | ||||

| 62 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

63 | |||

| 68 | ||||

| 81 | ||||

| 92 | ||||

| CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

93 | |||

| 94 | ||||

| 98 | ||||

| 103 | ||||

| 105 | ||||

| 106 | ||||

| 108 | ||||

| 109 | ||||

| MATERIAL UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS FOR NON-U.S. HOLDERS OF OUR COMMON STOCK |

113 | |||

| 117 | ||||

| 121 | ||||

| 122 | ||||

| 122 | ||||

| 122 | ||||

| F-1 | ||||

Table of Contents

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”). The Selling Shareholder may, from time to time, sell the securities offered by it described in this prospectus. We will not receive any proceeds from the sale by the Selling Shareholder of the securities offered by it described in this prospectus.

Neither we nor the Selling Shareholder have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Shareholder take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Shareholder will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

You should read this prospectus and any post-effective amendment, if any, to the registration statement together with the additional information to which we refer you in the sections of this prospectus entitled “Where You Can Find More Information.”

Unless the context indicates otherwise, references in this prospectus to the “Company,” “5E,” “we,” “us,” “our” and similar terms refer to 5E Advanced Materials, Inc. and its subsidiaries.

TRADEMARKS AND TRADE NAMES

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

SELECTED DEFINITIONS

| • | “ABR” refers to American Pacific Borates Limited, a company incorporated under the laws of Australia. |

| • | “ASX” refers to the Australian Securities Exchange. |

| • | “CDI” refers to a CHESS Depositary Interest. |

| • | “Company” refers to 5E Advanced Materials, Inc., a Delaware corporation. |

| • | “Corporations Act” refers to the Australian Corporations Act, 2001 (Cth). |

| • | “Exchange Act” means the Securities Exchange Act of 1934, as amended. |

| • | “Nasdaq” refers to The Nasdaq Global Select Market. |

| • | “Reorganization” refers to the transactions pursuant to which, among other things, we (i) issued (a) to eligible shareholders of ABR either one share of our Common Stock for every ten ordinary shares of ABR or one CDI over our Common Stock for every one ordinary share of ABR, in each case, as held on the Scheme record date and (b) to ineligible shareholders proceeds from the sale of the CDIs to which they would otherwise be entitled by a broker appointed by ABR, who sold the CDIs in accordance with the terms of a sale facility agreement and remitted the proceeds to ineligible |

1

Table of Contents

| shareholders, (ii) cancelled each of the outstanding options to acquire ordinary shares of ABR and issued replacement options representing the right to acquire shares of our Common Stock on the basis of a one replacement option for every ten existing ABR options held, (iii) maintained an ASX listing for its CDIs, with each CDI representing 1/10th of a share of Common Stock, (iv) delisted ABR’s ordinary shares from the ASX, and (v) became the parent company to ABR. |

| • | “Scheme” refers to a statutory Scheme of Arrangement under Australian law under Part 5.1 of the Corporations Act. |

| • | “SEC” means the U.S. Securities and Exchange Commission. |

| • | “Securities Act” means the Securities Act of 1933, as amended. |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains various forward-looking statements relating to our future financial performance and results, financial condition, business strategy, plans, goals and objectives, including certain projections, milestones, targets, business trends and other statements that are not historical facts. These statements constitute forward-looking statements within the meaning of the safe harbor provisions of the U.S. Private Securities Litigation Reform Act of 1995. These forward-looking statements generally are identified by the words “believe” “project,” “expect,” “anticipate,” “estimate,” “intend,” “budget,” “target,” “aim,” “strategy,” “estimate,” “plan,” “guidance,” “outlook,” “intend,” “may,” “should,” “could,” “will,” “would,” “will be,” “will continue,” “will likely result” and similar expressions, although not all forward-looking statements contain these identifying words. Forward-looking statements reflect our beliefs and expectations based on current estimates and projections. Forward-looking statements include, but are not limited to, statements concerning:

| • | The timing, completion and estimated production capacity of our proposed small-scale boron facility (“SSBF”) and proposed large-scale complex; |

| • | The outputs from our proposed SSBF and their impact on future estimates and potential studies regarding our proposed large-scale complex; |

| • | Unanticipated costs or delays associated with our proposed SSBF; |

| • | Use of our injection-recovery wells for extraction once our proposed SSBF and large-scale complex is complete; |

| • | Our ability to successfully and economically extract boron and lithium from colemanite; |

| • | The quantities of resources we expect to be able to extract and our production capabilities; |

| • | The timing of completing and the expected ability of our proposed SSBF facility to serve as a foundation for future design, engineering and cost optimization for our proposed large-scale complex; |

| • | Our ability to secure the requisite funding for the successful engineering, development, construction, completion and operation of our proposed facilities; |

| • | The timing and viability of achieving initial commercial production; |

| • | Our ability to commercialize our output and to enter into commercial agreements; |

| • | The total addressable market for materials we intend on producing and selling, including its current size, growth trajectory and the underlying factors that may drive growth in the overall market size; |

| • | The cost and availability of natural gas and electricity; |

| • | Our ability to timely and successfully reach anticipated full commercial production capacity; |

| • | Our ability to achieve and maintain profitability and to develop and maintain positive cash flow from our proposed operating activities; |

2

Table of Contents

| • | Our ability to enter into and deliver product under binding supply agreements; |

| • | Our ability to acquire and maintain the necessary mining licenses, permits and access rights; |

| • | Our ability to acquire and maintain the necessary mineral property interests and related water rights; |

| • | The demand for borates and lithium and the market for their end-use applications; and |

| • | Our ability to develop downstream advanced materials capabilities. |

These forward-looking statements are subject to a number of risks and uncertainties, including:

| • | Our limited operating history in the borates and lithium industries and no revenue from our proposed extraction operations at our properties; |

| • | Our need for substantial additional financing to execute our business plan and our ability to access capital and the financial markets; |

| • | Our status as an exploration stage company dependent on a single project with no known mineral reserves and the inherent uncertainty in estimates of mineral resources; |

| • | Our lack of history in mineral production and the significant risks associated with achieving our business strategies, including our downstream processing ambitions; |

| • | We have incurred significant net operating losses to date and we anticipate incurring continued losses for the foreseeable future; |

| • | Risks and uncertainties relating to the development of Fort Cady (“Fort Cady” or the “Project”); |

| • | Risks related to our ability to prepare and update further technical and economic analysis of Fort Cady, and the timing thereof; |

| • | Our dependence on a single project; |

| • | Risks related to our ability to achieve and maintain profitability and to develop positive cash flow from our operating activities; |

| • | Risks, including changes in technology, that could adversely affect the demand for end use applications that require borates, lithium, and related minerals and compounds; |

| • | Our long-term success is dependent on our ability to enter into and deliver product under supply agreements; |

| • | Risks related to estimates of our total addressable market; |

| • | The costs and availability of natural gas, electricity, and water; |

| • | Uncertain global economic conditions and the impact this may have on our business and plans; |

| • | Risks associated with our ongoing investment in Fort Cady; |

| • | Risks associated with the required infrastructure at Fort Cady; |

| • | Risks related to the titles of our mineral property interests and related water rights; |

| • | Any restrictions on our ability to obtain, recycle, and dispose of water on site; |

| • | Risks related to the portion of Fort Cady that we lease from a third party; |

| • | Risks related to land use restrictions on our properties; |

| • | Risks related to volatility in prices or demand for borates, lithium, and other minerals; |

| • | Fluctuations in the U.S. dollar relative to other currencies; |

| • | Risks related to mineral exploration and development; |

3

Table of Contents

| • | Risks related to equipment shortages and supply chain disruptions; |

| • | Risks associated with any of our customers, suppliers, or any third parties not implementing ethical or legal business practices in compliance with applicable laws and regulations; |

| • | Competition from new or current competitors in the mineral exploration and mining industry; |

| • | Risks associated with consolidation in the markets in which we operate and expect to operate; |

| • | Risks related to compliance with environmental and regulatory requirements, reclamation requirements, the potential generation and disposal of hazardous waste, climate change, and the proposed SEC rules on climate-related disclosures; |

| • | Risks related to our ability to acquire and maintain necessary mining licenses, permits, or access rights; |

| • | Litigation risk; |

| • | Risks related to our main operations being located in California and our engagement with local communities; |

| • | Risks relating to our investment in the Salt Wells North project area and the Salt Wells South project area (together, the “Salt Wells Projects”) located in Nevada; |

| • | Our dependence on key management and third parties; |

| • | Risks related to potential acquisitions, joint ventures, and other investments; |

| • | Risks related to public health threats, including the novel coronavirus, that may continue to cause disruptions to our operations or may have a material adverse effect on our development plans and financial results; |

| • | Information technology risks; |

| • | Risks and costs relating to the Reorganization; |

| • | Risks related to the possible dilution of our Common Stock; |

| • | Risks related to our stock price and trading volume volatility; |

| • | Risks relating to the development of an active trading market for our Common Stock; |

| • | Risks related to our status as an emerging growth company; |

| • | Risks related to technology systems and security breaches; |

| • | A shortage of skilled technicians and engineers; |

| • | Risks related to technology systems and security breaches; |

| • | Our facilities of operations could be adversely affected by outside events outside of our control, such as natural disasters, climate change, wars, or health epidemics or pandemics; |

| • | Risks and uncertainties related to the COVID-19 pandemic; |

| • | Our increased costs as a result of being a U.S. listed public company; |

| • | Strategic actions, including acquisitions and dispositions of investments, including but not limited to integrations of acquiring investments; |

| • | Risks associated with our Convertible Notes; |

| • | Risk of insufficient cash flow to service the Convertible Notes; |

| • | Risk of foreclosure on our assets if we default on the Convertible Notes; |

| • | Risk of dilution of the ownership interest of our existing stockholders if the Convertible Notes are converted; |

4

Table of Contents

| • | Risk of adverse impact on the price of our Common Stock if the Convertible Notes are converted; |

| • | Risks associated with limitations on our ability to raise money through equity offerings and to incur additional indebtedness imposed by the Note Purchase Agreement; and |

| • | Any other risks described elsewhere in this prospectus or the documents incorporated herein by reference. |

While we believe these expectations, and the estimates and projections on which they are based, are reasonable and were made in good faith, these statements are subject to numerous risks and uncertainties. Forward-looking statements involve known and unknown risks, uncertainties and other important factors, which include, but are not limited to, the risks described under the heading “Risk Factor Summary” and “Risk Factors,” any of which could cause our actual results, performance or achievements, or industry results, to differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements. Therefore, you should not rely on any of these forward-looking statements.

These forward-looking statements speak only as of the date of this prospectus and we undertake no obligation to correct, update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except to the extent required under federal securities laws. You are advised, however, to consult any additional disclosures we make in our reports to the SEC. All subsequent written and oral forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements contained in this prospectus.

CAUTIONARY NOTE REGARDING RESERVES

Unless otherwise indicated, all mineral resource and mineral reserve estimates included in this prospectus have been prepared in accordance with, and are based on the relevant definitions set forth in, the SEC’s Mining Disclosure Rules and Regulation S-K 1300 (each as defined below). Mining disclosure in the United States was previously required to comply with SEC Industry Guide 7 (the “SEC Industry Guide 7”) under the Exchange Act. In accordance with the SEC’s Final Rule 13-10570, Modernization of Property Disclosure for Mining Registrant, the SEC has adopted final rules, effective February 25, 2019, to replace SEC Industry Guide 7 with new mining disclosure rules (the “Mining Disclosure Rules”) under sub-part 1300 of Regulation S-K of the Securities Act (“Regulation S-K 1300”). Regulation S-K 1300 replaces the historical property disclosure requirements included in SEC Industry Guide 7. Regulation S-K 1300 uses the Committee for Mineral Reserves International Reporting Standards (“CRIRSCO”)-based classification system for mineral resources and mineral reserves and accordingly, under Regulation S-K 1300, the SEC now recognizes estimates of “Measured Mineral Resources,” “Indicated Mineral Resources” and “Inferred Mineral Resources,” and require SEC-registered mining companies to disclose in their SEC filings specified information concerning their mineral resources, in addition to mineral reserves. In addition, the SEC has amended its definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” to be substantially similar to international standards. The SEC Mining Disclosure Rules more closely align SEC disclosure requirements and policies for mining properties with current industry and global regulatory practices and standards, including the Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves, referred to as the “JORC Code.” While the SEC now recognizes “Measured Mineral Resources,” “Indicated Mineral Resources” and “Inferred Mineral Resources” under the SEC Mining Disclosure Rules, investors should not assume that any part or all of the mineral deposits in these categories will be converted into a higher category of mineral resources or into mineral reserves.

5

Table of Contents

The following terms, as defined in Regulation S-K 1300, apply within this prospectus:

| Measured Mineral Resource (“Measured” or “Measured Mineral Resource”) |

that part of a mineral resource for which quantity and grade or quality are estimated on the basis of conclusive geological evidence and sampling. The level of geological certainty associated with a measured mineral resource is sufficient to allow a qualified person to apply modifying factors in sufficient detail to support detailed mine planning and final evaluation of the economic viability of the deposit. Because a measured mineral resource has a higher level of confidence than the level of confidence of either an indicated mineral resource or an inferred mineral resource, a measured mineral resource may be converted to a proven mineral reserve or to a probable mineral reserve. | |

| Indicated Mineral Resource (“Indicated” or “Indicated Mineral Resource”) |

that part of a mineral resource for which quantity and grade or quality are estimated on the basis of adequate geological evidence and sampling. The level of geological certainty associated with an indicated mineral resource is sufficient to allow a qualified person to apply modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Because an indicated mineral resource has a lower level of confidence than the level of confidence of a measured mineral resource, an indicated mineral resource may only be converted to a probable mineral reserve. | |

| Inferred Mineral Resource (“Inferred” or “Inferred Mineral Resource”) |

that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. The level of geological uncertainty associated with an inferred mineral resource is too high to apply relevant technical and economic factors likely to influence the prospects of economic extraction in a manner useful for evaluation of economic viability. Because an inferred mineral resource has the lowest level of geological confidence of all mineral resources, which prevents the application of the modifying factors in a manner useful for evaluation of economic viability, an inferred mineral resource may not be considered when assessing the economic viability of a mining project, and may not be converted to a mineral reserve. | |

| Probable Mineral Reserve (“Probable” or “Probable Mineral Reserve”) |

the economically mineable part of an indicated and, in some cases, a measured mineral resource. | |

| Proven Mineral Reserve (“Proven” or “Proven Mineral Reserve”) |

the economically mineable part of a measured mineral resource and can only result from conversion of a measured mineral resource. | |

6

Table of Contents

We retained Millcreek Mining Group to prepare an independent technical report on Fort Cady, dated February 7, 2022 (the “Initial Assessment Report”). The purpose of the Initial Assessment Report is to support the disclosure of mineral resource estimates for Fort Cady. The Initial Assessment Report was prepared in accordance with the SEC’s Mining Disclosure Rules and Regulation S-K Subpart 1300 and Item 601(b)(96) (technical report summary). The Initial Assessment Report is discussed in Business and Properties and filed as Exhibit 96.1 to the registration statement on Form S-1 of which this prospectus is a part.

UNLESS OTHERWISE EXPRESSLY STATED, NOTHING CONTAINED IN THIS PROSPECTUS IS, NOR DOES IT PURPORT TO BE, A TECHNICAL REPORT SUMMARY PREPARED BY A QUALIFIED PERSON PURSUANT TO AND IN ACCORDANCE WITH THE REQUIREMENTS OF SUBPART 1300 OF SECURITIES EXCHANGE COMMISSION REGULATION S-K.

CAUTIONARY NOTE REGARDING EXPLORATION STAGE COMPANIES

We are an exploration stage company and do not currently have any known mineral reserves and cannot expect to have known mineral reserves unless and until an appropriate technical and economic study is completed for Fort Cady or any of our other properties that shows Proven or Probable Mineral Reserves as defined by Regulation S-K 1300. We currently do not have any Proven or Probable Mineral Reserves. There can be no assurance that Fort Cady or any of our other properties contains or will contain any such SEC-compliant Proven or Probable Mineral Reserves or that, even if such reserves are found, the quantities of any such reserves warrant continued operations or that we will be successful in economically recovering them.

CAUTIONARY NOTE REGARDING EMERGING GROWTH COMPANY STATUS

Section 102(b)(1) of the Jumpstart Our Business Startups Act (“JOBS Act”) exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard, until such time we are no longer considered to be an emerging growth company. At times, we may elect to adopt a new or revised standard early.

CAUTIONARY NOTE REGARDING INDUSTRY AND MARKET DATA

This prospectus includes information concerning our industry and the markets in which we will operate that is based on information from various sources including public filings, internal company sources, various third-party sources and management estimates. Our management estimates regarding our position, share and industry size are derived from publicly available information and its internal research, and are based on a number of key assumptions made upon reviewing such data and our knowledge of such industry and markets, which we believe to be reasonable. While we believe the industry, market and competitive position data included in this prospectus is reliable and is based on reasonable assumptions, such data is necessarily subject to a high degree of uncertainty and risk and is subject to change due to a variety of factors, including those described in “Cautionary Note Regarding Forward-Looking Statements,” “Risk Factors” and elsewhere in this prospectus. These and other factors could cause results to differ materially from those expressed in the estimates included in this prospectus. We have not independently verified any data obtained from third-party sources and cannot assure you of the accuracy or completeness of such data.

7

Table of Contents

PROSPECTUS SUMMARY

This summary highlights selected information appearing elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that may be important to you. To understand this offering fully, you should read this entire prospectus carefully, including the information set forth under the heading “Risk Factors” and our financial statements.

The Company

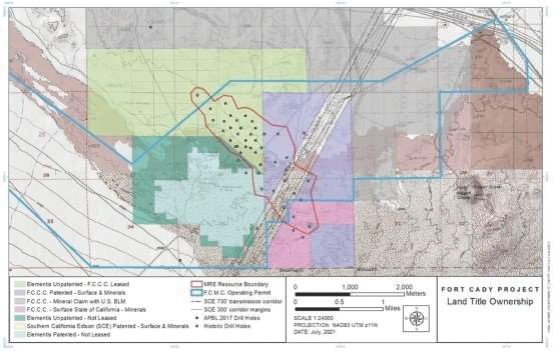

We are an exploration stage company focused on becoming a vertically integrated global leader and supplier of boron specialty and advanced materials, complemented by lithium carbonate production capabilities. Our mission is to become a supplier of these critical materials to industries addressing global decarbonization, food security, and production of domestic supply. Our business strategy and objectives are to develop capabilities ranging from upstream extraction and product sales of boric acid, lithium carbonate and potentially other co-products, to downstream boron advanced material processing and development. Our business is based on our large domestic boron and lithium resource in Southern California, and we intend to leverage this asset once commercially operational to internally supply our proposed downstream advanced material development activities overtime.

We hold 100% of the rights—either through ownership or leasehold interest—in Fort Cady through our wholly owned subsidiary, 5E Boron Americas, LLC (f/k/a Fort Cady (California) Corporation) (“5E Boron Americas”). Through a multi-phased approach, we plan to develop Fort Cady into a large-scale boron and lithium complex. Fort Cady is based on a conventional colemanite deposit, which is a hydrated calcium borate mineral found in evaporite deposits, and we believe it is one of the largest known new conventional boron deposits globally. The deposit hosts a mineral resource from which we intend to extract and process into boric acid, boron advanced materials, lithium carbonate, and potentially other co-products. These materials are scarce in resource, currently subject to supply risk as a large portion of their consumption in the United States is sourced from foreign producers and are essential for supporting critical industries. If and when Fort Cady is successfully developed, we believe that we can become an important supplier helping address supply security for these materials in the United States. The importance of Fort Cady and its mineral resource has been recognized by it being designated as Critical Infrastructure by the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency. Fort Cady is also expected to serve as an important supply source of boric acid that we intend to process and develop into boron specialty and advanced materials over time.

Our Strengths

We believe the following key strengths will help us toward our goal of becoming an important supplier of boron specialty and advanced materials, complemented by lithium carbonate production capabilities:

Strategically Positioned to Benefit from Expected Substantial Demand Growth as Decarbonization Efforts Intensify and Future Facing Markets Develop. We are an exploration-stage company aiming to develop a materials resource of high-quality borates and other key materials, such as lithium, currently positioned as inputs into key technologies and industries that address climate change, support decarbonization, and support food and domestic security sectors. We believe factors such as government regulation and incentives and capital investments across industries will drive demand for end-use applications like solar and wind energy infrastructure, neodymium-ferro-boron magnets, lithium-ion batteries, and other critical material applications. We expect any such growth in demand to increase the need for borates and other advanced materials that we seek to produce. In addition, products with future facing applications, including in the semi-conductor, life sciences, aerospace, military and automotive markets, are also expected to drive demand growth. As a result of our broader focus on the boron specialty and advanced materials rather than specific end use applications, we believe we can be well-positioned to be an important domestic supplier to a number of different sectors benefitting from their expected growth.

8

Table of Contents

Attractive Geographic Location with a Potential to Address Global Supply Challenges and National Security Concerns. Over the last year, the United States has taken action to reinforce existing supply chains and access to critical materials, while working to secure the domestic supply. In February 2022, Fort Cady was designated as Critical Infrastructure by the Department of Homeland Security’s Cybersecurity and Infrastructure Security Agency, which we believe is a testament to its potential importance as a U.S.-based source of boron, lithium and other materials. This designation supports our goal of playing an important role in providing critical materials domestically, while simultaneously addressing the currently challenged global supply chain. The global boron market is exposed to potential supply risks. There are currently only two major global suppliers (Eti Maden and Rio Tinto Borax) who together represented approximately 85% of total supply in 2021, with Eti Maden representing approximately 60% of global supply in 2021. Similarly, there are only a small number of domestic lithium carbonate suppliers today in the United States. Fort Cady is located in Southern California and, if successfully commercialized, we expect it will have the ability to supply U.S. markets and industries with these two key materials, and thereby help reduce reliance on foreign sources. Our plans to develop U.S.-based downstream capabilities are similarly expected to allow us to onshore additional components of the overall boron supply chain that have historically been concentrated in Asia and other foreign regions.

Fort Cady is Based on one of the Largest Known New Conventional Boron Deposits in the World and Includes a Complementary Lithium Resource that has the Potential to Enable Us to Become an Important Participant in the U.S. Lithium Market. The Fort Cady deposit is a rare colemanite borate deposit, and we believe it is one of the largest known new deposits of colemanite globally. The Initial Assessment Report prepared for us estimates a combined 97.55 million tons of Measured Mineral Resource plus Indicated Mineral Resource at Fort Cady, with a grade of 6.53% for boron oxide (B2O3) and 324 parts per million for lithium. The mineral resource estimate also identified 11.43 million tons of Inferred Mineral Resource with a grade of 6.40% boron oxide and 324 parts per million for lithium. Across the three mineral resource categories there is an estimated 108.98 million tons grading 6.52% for boron oxide and 324 parts per million for lithium. The Initial Assessment Report estimated total contained mineral resource across all resource categories equal to 12.62 million tons of boric acid equivalent at a 5% cut-off grade. We believe that the complementary lithium resource at Fort Cady, if successfully developed, has the potential to enable us to become an important participant in the U.S. lithium market. We believe the size and quality of our Fort Cady resource also positions us to become a long-term supplier, if and when the site becomes operational.

We Believe Our Approach for Developing and Commercializing Fort Cady, along with our Orientation towards Decarbonization-Enabling Materials and Industries can Position us Well to Focus On Important Sustainability Initiatives. We believe that the boron and lithium materials we plan on producing will support industries and applications that enable decarbonization and emission reduction, such as electric vehicles and green energy. These industries are important contributors and supporters of the United Nations Sustainability Development Goals (“SDG’s”), which include accelerating a net-zero future, promoting sustainable infrastructure, improving global nutrition and health as well as promoting innovation. Further, we believe that our extraction techniques will help us create a set of infrastructure that is aligned with the industries we plan on supporting. Our method of in-situ extraction is expected to source hot water from our hydrology wells while providing for closed loop water recycling which we expect will help reduce overall water consumption and provide for efficient energy management. In-situ extraction is also traditionally associated with less above ground land disturbance than traditional resource extraction methods, while using less fossil fuels. Given our early stage of development, we believe we have a clean sheet opportunity to develop and grow our business and a potential sustainability advantage, including building a diverse board of directors and leadership team as well as creating strong corporate governance policies, in each case focused on sustainability matters. Our focus will be to have a positive impact on the prosperity of local communities by supporting job creation, providing specialized training, targeting local procurement and investment, all of which are important given the local community near Fort Cady is designated an economic development zone by the State of California. Finally, we expect to collaborate on technology and material development with universities and research institutions across the United

9

Table of Contents

States and abroad with the overall objective of driving innovation, including with respect to boron advanced materials.

Our Strategy

Our strategy is founded on leveraging our large mineral resource, related proposed infrastructure project, project development and advanced materials expertise to develop a vertically integrated business focused on boron specialty and advanced materials, complemented by lithium production capabilities. We intend to thoughtfully develop our business over time in a systematic manner, starting with the development and construction of our SSBF to support ongoing design work, engineering and cost optimization for our proposed large-scale complex that we believe will provide us with the ability to commercially produce salable products including boric acid and lithium carbonate, while opportunistically developing downstream boron advanced material processing capabilities to extract greater value out of the boron supply chain.

Key elements of our strategy include:

Develop and Commercialize Fort Cady to Produce an Economical and Secure Supply of Boron and Lithium and Focusing on a more Environmentally Friendly In-Situ Extraction Process as Compared to Traditional Mining. Our initial objective is to develop our Fort Cady boron and lithium resource and achieve a commercial extraction volume of borates, lithium and other co-products safely, profitably with a focus on a more environmentally friendly in-situ extraction process as compared to traditional mining. The SSBF, which we began constructing in April 2022, is expected to serve as a foundation for future design, engineering, and cost optimization of our planned large-scale complex. If and when Fort Cady is fully operational in accordance with our current plan, we believe that we can have an opportunity to be a long-term supplier of boric acid and lithium carbonate, and Fort Cady can serve as an important internal supply source for our development of downstream specialty and advanced materials.

Establish Competitive Market Positions in High Value, High Margin Markets for Boron Specialty and Advanced Materials and Lithium that Address Decarbonization, Food Security, and production of Domestic Supply. We are seeking to establish competitive market positions in high value in use, high margin, and high technology boron specialty and advanced materials and lithium markets. We believe that as a result of the global push to address climate change and achieve decarbonization, as well as increasing challenges related to food security and geopolitical instability, key sectors such as electric vehicle manufacturing, clean energy infrastructure, food and fertilizers, and domestic security, will experience significant growth in the future. As a result, these sectors are expected to require secure and substantial new supplies of key inputs such as boron and lithium to support their growth. Assuming the successful commercial completion of our large-scale complex, we believe we will have the opportunity to become one of the largest suppliers of boric acid and lithium carbonate in the domestic U.S. and international markets. Over time, we plan on developing downstream boron advanced materials capabilities to convert boric acid into boron advanced materials. These boron advanced materials may support higher technology applications across the fields of semi-conductors, life sciences, aerospace, military and automotive markets and would allow us to extract greater value from our processes and supply chain. Downstream boron advanced materials capabilities may be developed over time through a combination of internal research and development, commercial partnerships or joint ventures with other organizations or research institutions, or via the acquisition of intellectual property related to processing and manufacturing.

Sign Offtake Agreements and Develop Commercial Partnerships to Expand High-Performance Boron and Lithium Product Capabilities and Embed Ourselves in Customer Supply Chains. As part of the commercialization plans for Fort Cady, we plan on dedicating resources for marketing efforts to establish commercial offtake agreements for the sale of boric acid and lithium carbonate. We believe sales of these materials will support our strategy of achieving a durable revenue base, which can be used to fund subsequent

10

Table of Contents

incremental capacity plans at Fort Cady and generate cash necessary for investments in downstream boron advanced materials capabilities. As we develop our downstream materials business, we plan to collaborate with customers and partners to support their development of high-performance applications in the areas of clean energy infrastructure, electric transportation, and high-grade fertilizers among other end uses. These commercial partnerships are expected to be an important element of embedding us within global supply chains and positioning us as an essential supplier of boron specialty and advanced materials. We intend to invest in research and development initiatives with an aim to support our customers’ product development and create intellectual property for us.

Potentially Diversify our Sources of Supply. Initially, we will rely on production from Fort Cady to support materials sales and downstream materials processing capability development. We have the opportunity to expand our supply of resources as a result of our earn-in right to acquire a 100% interest (“Earn-In Agreement”) in the Salt Wells Projects in the State of Nevada, a land package that is considered a prospective area for borates and lithium deposits. Pursuant to the Earn-In Agreement, we may acquire a 100% interest in the Salt Wells Projects which has the potential to serve as a second pillar of high-quality borates and lithium supply to us. We plan on assessing new resources that offer the potential to provide economically viable alternative sources of borates or other essential materials.

Recent Developments

Henri Tausch Departure

On September 28, 2022, the Board of Directors (the “Board”) accepted the resignation of Henri Tausch as President, Chief Executive Officer and as a member of the Board, effective as of October 31, 2022. The Board is engaged in a search and review of permanent Chief Executive Officer candidates. In the interim, Mr. Anthony Hall will lead the Company effective November 1, 2022 until the appointment of a new CEO is confirmed.

Note Purchase Agreement

On August 11, 2022, we entered into the Note Purchase Agreement with the Selling Shareholder and the other parties signatory thereto. The Convertible Notes issued pursuant to the Note Purchase Agreement bear interest at a rate of 4.50% per annum, payable semi-annually, or 6.00% per annum if the Company elects to pay such interest through the delivery of additional Convertible Notes, and are convertible into 4,581,534 shares of Common Stock at a conversion price of $17.60 per share of Common Stock in accordance with the terms of the Note Purchase Agreement. The Convertible Notes mature on August 15, 2027.

We are registering the Resale Shares issuable upon the conversion of the Convertible Notes in this prospectus pursuant to the Selling Shareholder’s registration rights under the Registration Rights Agreement entered in connection with the closing of the Note Purchase Agreement.

Corporate Update

In March 2022 we executed a research agreement with Georgetown University that aims to enhance the performance of permanent magnets through increased usage of boron. We believe the potential benefits of this agreement include creating intellectual property and commercialization pathways for us as it pertains to the manufacturing of boron enhanced permanent magnets.

Our team in California and Texas continues to grow with several new hires across operations, administration, and finance, including a former key employee with over 19 years of experience at Albemarle Corporation that spans across multiple disciplines including process design, purchasing, M&A, and general management. As of June 2022, the majority of our administrative and operational personnel have transitioned to

11

Table of Contents

the U.S. and we hired a Chief Accounting Officer with over 29 years of experience. We anticipate a step-up in hiring as we work towards mechanical completion and operation of the SSBF.

In light of the recent Presidential Executive Orders and U.S. government initiatives, we have increased our government affairs effort by engaging a specialized management consulting firm in May 2022 to pursue federal, state, and local funding opportunities. We have continued to advance our efforts around environmental, sustainability and governance (“ESG”), and have been working with a North American sustainability consulting firm to develop our ESG strategy and future reporting framework.

In May 2022 we signed a non-binding letter of intent with Rose Mill Co. (“Rose Mill”) for the joint research and development of boron advanced materials applications across a number of industrial and military fields. In June 2022, we signed a non-binding letter of intent with Corning International for the supply of boron and lithium materials, technical collaboration to develop advanced materials and potential financial accommodations in support of a commercial agreement. We continue to advance discussions with other customers for boron advanced materials.

SSBF Update

The SSBF is our proposed smaller scale boron facility which is expected to serve as a foundation for future design, engineering, and cost optimization for our large-scale complex at Fort Cady focused on boron and lithium. Once successfully completed, the SSBF will be an essential step in the overall Fort Cady development plan and is expected to serve as our initial extraction and processing facility. In recent months, we have made progress on planning and procurement of long lead item equipment for our SSBF, with major equipment either already on-site or scheduled for delivery. Detailed engineering, including our hazard analysis, instrument designs, piping isometrics, and structural and foundation design, was substantially completed by March 2022 and the progress of detailed engineering provided us the opportunity to engage in a competitive bidding process for the SSBF construction contract. In April 2022, we awarded the construction contract to a contractor. Assuming no unexpected delays in construction, supply chain issues or availability of labor, we are targeting completing the construction of the SSBF around the end of the 2022 calendar year at an engineered estimated test production capacity of approximately 2,000 tons per year of boric acid. This facility is being designed to process a pregnant leach solution (“PLS”) containing boron and lithium extracted from colemanite. Assuming the timely and successful construction and operation of the SSBF, production from our SSBF is primarily intended to provide PLS and process intelligence that will help us to more effectively detail engineer our proposed large-scale complex and estimate capital expenditures required to build our large-scale complex. It is possible that a portion of the output from our SSBF may be used to support customer origination efforts for eventual offtake and qualification and may be used for commercial sales and to progress our advanced materials development. The extraction of the PLS is expected to occur through our injection-recovery wells, and we completed four such wells by May 2022. As of June 30, 2022, we had no lost time injuries for any of our sites during the calendar year 2022, and we will continue to prioritize the safety and well-being of personnel. While the total cost is subject to change, we currently estimate the total cost of the SSBF (including the drilling and installation costs for our injection recovery wells of $3.4 million) to be between $45 million and $55 million, of which $25.6 million had been spent (including costs for our injection recovery wells of $3.4 million) as of June 30, 2022, and the remainder is expected to be incurred prior to March 31, 2023.

Fort Cady

Our previous development plans were focused on boron and sulphate of potash (“SOP”) and developing a large-scale complex under a phased development process. During the 2022 fiscal year, we have changed the focus of our business plan and have worked with our external engineering partners on an updated process design for our proposed large-scale complex at Fort Cady. Our Initial Assessment Report added further definition to our

12

Table of Contents

large boron resource and established the existence of a lithium mineral resource that we believe could provide us with potential lithium carbonate production. Due to the current favorable market backdrop and growing importance of critical materials, we now intend to focus primarily on further defining our boron and lithium resources, and to work towards developing a large-scale boron and lithium complex for the extraction of boric acid and lithium carbonate. A focus on boron and lithium extraction and related end markets is aligned with our mission to become a global leader in enabling industries addressing decarbonization, food security, and production of domestic supply and our focus on high value in use materials and applications.

The SSBF is expected to serve as a foundation for future design, engineering, and cost optimization for our large-scale complex. We believe that the successful completion of the SSBF is an important path to obtaining critical information that will help enable us to optimize the efficiency, output and economic profile of our large-scale complex. As such, we expect to incorporate value engineering and cost structure optimization into the continued technical and economic analysis of the proposed large-scale complex, and to provide project updates, rather than completing a bankable feasibility study in fiscal year 2022. We have begun to progress plans for the proposed large-scale complex processing plant, including defining infrastructure, material balance and process flow diagrams, co-generation, as well as the integration of a sulfuric acid plant, and are developing a priced equipment list for process equipment needed for full-scale operations. Notwithstanding the proposed scope changes to Fort Cady and our large-scale complex focused on boron and lithium, we continue to target, assuming timely and successful construction and operation of the SSBF, and obtaining the requisite funding for construction, the potential for initial commercial production in 2025. We also intend to develop downstream boron specialty and advanced materials capabilities and anticipate using internally generated boric acid to supply downstream processing activities.

As a result of the change in project scope, enhanced focus on boron and lithium, and current favorable market backdrop for these materials, we have also refined our anticipated phased development approach for the large-scale complex at Fort Cady, which differs from our February 2021 Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves (“JORC Code”) report. We are currently targeting a boric acid production capacity of approximately 250,000 tons per year once our proposed large-scale complex at Fort Cady commences initial operations. In addition, based on currently expected engineering and process design, once in full production, we believe Fort Cady could potentially produce up to 500,000 tons per year of boric acid. We will consider the pacing and timing of any potential incremental capacity additions above the initial target of 250,000 tons per year, and we expect this to be an economic decision based on factors including go-forward supply and demand fundamentals, pricing, and further engineering work to be conducted over time. We also intend to leverage our anticipated internal supply of borates to produce boron specialty and advanced materials and additional lithium carbonate. However, further analysis is required with respect to the potential for boron advanced materials, with the successful completion and operation of the SSBF expected to provide key operational input for this analysis. Additionally, early estimates by us currently target a lithium carbonate production capacity of up to several thousand tons per year upon completion of our proposed large-scale complex, and we expect the successful completion and operation of the SSBF to provide further information on this point. If we successfully meet the aforementioned early estimates of lithium carbonate production capacity, this could allow us to become an important participant in the U.S. lithium carbonate market. Given currently high lithium prices and electric vehicle growth forecasted by third-party analysts, we believe that an ability to produce a co- product of lithium carbonate could have a positive impact on our business.

The proposed large-scale complex is being designed and engineered to regenerate a significant portion of hydrochloric acid, which we expect to increase efficiencies and reduce our emphasis on SOP to produce feedstock hydrochloric acid. While production of SOP remains in our long-term plans, we believe we can implement the Mannheim process to produce SOP during later phases of Fort Cady when capacity for boric acid production exceeds 250,000 tons per year. Our short to medium term plan focuses on the production of boric acid, boron advanced materials, and lithium carbonate where we currently see favorable market pricing and high

13

Table of Contents

value in use. We believe that a focus on boron and lithium could be an important step towards creating a more durable, less seasonal business compared to a more traditional commodity-driven fertilizer focused business.

The continued technical and economic analysis described above with respect to our proposed large-scale complex and overall business strategy, has been determined by us to be a currently more cost effective and time efficient way to proceed. This continued technical and economic analysis of the proposed large-scale complex is subject to change and may lead to a separate technical study, an update to our Initial Assessment Report or a more comprehensive study. However, we cannot assure you of the form and scope of this continued technical and economic analysis, and it is possible that we will conclude that the completion of any such further studies (including a bankable feasibility study) may not be commercially reasonable, necessary or possible at all.

In May 2022, we announced a change in project scope compared to our previous business plans. Our new business plan includes:

| • | a focus on boron and lithium extraction (as opposed to boron and SOP under our previous plans); |

| • | revisions to the proposed processing facility design (including a targeted increase of the overall long- term potential production capacity to approximately 500,000 tons pa of boric acid compared to approximately 450,000 tons pa of boric acid under our previous plans); and |

| • | a modified sequencing of our project development timeline to include the initial SSBF followed by the development of our proposed large-scale complex (as opposed to only developing the large-scale complex under our previous plans), with the expectation that operating data to be obtained from the SSBF will be important in determining the future design, engineering and cost optimization for our large-scale complex, as well as the expected total capital expenditures and ongoing required operating expenditures related thereto. |

These project scope changes, taken together with cost inflation, have resulted in a material increase to our previously estimated capital expenditure budget required to complete our proposed large-scale complex. As a result, we currently expect a material increase to our capital expenditure budget compared to the previously published estimates and our internal cost estimates. In addition, the capital expenditures related to our proposed large-scale complex continue to be subject to change as our technical and economic analysis progresses. Such changes could also be material, including without limitation as a result of potential future price increases for major equipment or labor, and future operating data from our SSBF which may result in changes in the design and engineering of our proposed large-scale complex. The foregoing factors may lead to materially higher costs, delays or the inability to complete our proposed large-scale complex as planned or on commercially reasonable terms or at all. Furthermore, it could take several months or longer for the operating data from the operational SSBF to be sufficiently calibrated and reliable to provide reasonable input into the future design, engineering and cost optimization for our large-scale complex, as well as the expected total capital expenditures and ongoing required operating expenditures related thereto. As a result, depending on the timing, nature, quality and specificity of the data we receive from the operational SSBF, we may require significant additional capital before we can progress the development of our proposed large-scale complex. Such additional capital may be needed to fund further detailed engineering work necessary to prepare a feasibility study (if any), including engineering work to define, with a reasonable degree of certainty, the capital expenditures required for our proposed large- scale complex and in particular related to equipment and drilling. We may also need additional capital for continued operation of the SSBF to obtain test and flow data required to complete such detailed engineering work. As a result, we can provide no assurance that we will be able to meet our expected timelines, capital expenditure and costs estimates with respect to our SSBF and large-scale complex and we may need significant additional capital to pursue our operating plans, which capital may not be available to us on commercially reasonable terms or at all.

14

Table of Contents

Corporate Information

We were incorporated in the State of Delaware on September 23, 2021 for the purposes of effecting the Reorganization. Our principal executive offices are located at 19500 State Highway 249, Suite 125, Houston, Texas, and our telephone number is (346) 439-9656. We maintain a website on the Internet at http://www.5eadvancedmaterials.com. Information contained on the website does not constitute a part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

Implications of Being an Emerging Growth Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies. These exemptions include:

| • | the option to present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations in this prospectus; |

| • | not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002; |

| • | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements (i.e., an auditor discussion and analysis); |

| • | not being required to submit certain executive compensation matters to shareholder advisory votes, such as “say-on-pay,” “say-on-frequency,” and “say-on-golden parachutes;” and |

| • | not being required to disclose certain executive compensation related items such as the correlation between executive compensation and performance and comparisons of the chief executive officer’s compensation to median employee compensation. |

As a result, some investors may find our Common Stock less attractive. The result may be a less active trading market for our Common Stock, and the price of our Common Stock may become more volatile. Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 13(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to avail ourselves of this exemption and, as a result, our financial statements may not be comparable to the financial statements of issuers who are required to comply with the effective dates for new or revised accounting standards that are applicable to public companies. Section 107 of the JOBS Act provides that we can elect to opt out of the extended transition period at any time, which election is irrevocable.

We will remain an emerging growth company until the earliest to occur of: (i) the last day of the fiscal year in which we have more than $1.235 billion in annual revenue; (ii) the date we qualify as a “large accelerated filer,” as defined in Rule 12b-2 under the Exchange Act, with at least $700 million of equity securities held by non-affiliates; (iii) the issuance, in any three-year period, by us of more than $1.0 billion in non-convertible debt securities; and (iv) the last day of the fiscal year ending after the fifth anniversary of our initial public offering.

Even after we no longer qualify as an emerging growth company, we may continue to qualify as a “smaller reporting company,” which would allow us to take advantage of many of the same exemptions from disclosure

15

Table of Contents

requirements including reduced disclosure obligations regarding executive compensation in this prospectus supplement and our periodic reports and proxy statements, if either (i) the market value of our stock held by non-affiliates is less than $250 million or (ii) our annual revenue is less than $100 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700 million.

Summary Risk Factors

An investment in shares of our Common Stock involves a high degree of risk. If any of the factors below or in the section entitled “Risk Factors” occurs, our business, financial condition, liquidity, results of operations, and prospects could be materially and adversely affected.

| • | We have incurred significant net operating losses since our inception and we will incur continued losses for the foreseeable future; |

| • | Our future performance is difficult to evaluate because we have no or only a limited operating history in the minerals industry and no revenue from our proposed extraction operations at our properties, which may negatively impact our ability to achieve our business objectives. |

| • | If we do not obtain additional financing and maintain sufficient funds to continue our ongoing development and proposed operations, our proposed business may be at risk or the execution of our business plan may be delayed. |

| • | Our inability to timely and successfully complete and operate the SSBF, and our inability to complete further technical and economic studies (including a bankable feasibility study) with respect to Fort Cady, may have a material adverse impact on Fort Cady. |

| • | There are risks associated with our Convertible Notes. |

| • | Servicing our debt requires a significant amount of cash, and we may not have sufficient cash flow from our business to pay our debt. |

| • | Our obligations to the purchaser under the Convertible Notes, and any additional convertible notes, are secured by a security interest in substantially all of our assets, and if we default on those obligations, the purchaser could foreclose on our assets. |

| • | We may not be able to compete the SSBF on our current targeted timeline which would impact the successful construction of our proposed large-scale complex and potential for initial commercial production targeted in 2025. |

| • | We have invested and plan to continue to invest significant amounts of capital in Fort Cady on exploration and development activities, which involve many uncertainties and future operating risks that could prevent us from realizing profits. |

| • | We have no history of mineral production and we may not be able to successfully achieve our business strategies, including our downstream processing ambitions. |

| • | We may be unable to develop or acquire certain intellectual property required to implement our business strategy successfully. |

| • | Third parties may claim that we infringe on their proprietary intellectual property rights, and resulting litigation may be costly, result in diversion of management’s time and efforts, require us to pay damages or prevent us from marketing our future products. |

| • | All of our business activities are now in the exploration stage and there can be no assurance that our exploration efforts will result in commercial development. |

16

Table of Contents

| • | We are an exploration stage company with no known Proven or Probable Mineral Reserves, our estimates of resources and mineralized material are inherently uncertain and subject to change, and the volume and grade of ore actually recovered may vary from our estimates. |

| • | Estimates relating to the development of Fort Cady and mine plan are uncertain and we may incur higher costs and lower economic returns than estimated. |

| • | We depend on a single mining project. |

| • | Our long-term success will depend ultimately on our ability to achieve and maintain profitability and to develop positive cash flow from our proposed operating activities. |

| • | Our growth depends upon the continued growth in demand for end use and future facing applications that require borates, lithium, and related minerals and compounds we expect to produce |

| • | Changes in technology or other developments could adversely affect demand for lithium compounds or result in preferences for substitute products. |

| • | Our growth depends upon the continued growth in demand for electric vehicles with high performance lithium compounds. |

| • | Our long-term success will depend on our ability to enter into and deliver product under supply agreements. |

| • | If the estimates and assumptions we use to determine the size of our total addressable market are inaccurate, including its current size, growth trajectory, and the underlying factors that may drive future growth in overall market size, particularly for boron where there is limited third party published research and market forecasting, our future growth rate may be adversely affected, and the potential growth of our business may be limited. |

| • | The cost and availability of electricity and natural gas are subject to volatile market conditions. |

| • | Uncertain global economic conditions could have a material adverse effect on our business, financial condition, results of operations or prospects, including the pricing of our products. |

| • | We are subject to anti-bribery, anti-corruption, and anti-money laundering laws, including the U.S. Foreign Corrupt Practices Act, as well as export control laws, customs laws, sanctions laws and other laws governing our operations. If we fail to comply with these laws, we could be subject to civil or criminal penalties, other remedial measures and legal expenses, which could adversely affect our business, results of operations and financial condition. |

| • | Inadequate infrastructure may constrain our future mining operations, including at Fort Cady. |

| • | Title to mineral properties and related water rights is a complex process and we may suffer a material adverse effect in the event the Fort Cady property or other properties that we may acquire are determined to have title deficiencies. |

| • | Restrictions on our ability to obtain, recycle and dispose of water may impact our ability to execute our development plans in a timely or cost-effective manner. |

| • | The development, construction and proposed operation of our properties and projects is subject to various environmental and operational regulations, and risks relating to land use restrictions and potential opposition from landowners, environmental groups and other third parties, all of which could adversely affect or prevent our ability to grow. |

| • | The mining industry is historically a cyclical industry and market fluctuations in the prices of borates, lithium, and lithium byproducts and other minerals could adversely affect our business. |

17

Table of Contents

| • | Fluctuations in the value of the United States dollar relative to other currencies may adversely affect our business. |

| • | We face risks relating to mining, exploration, and mine construction, if warranted, on our properties. |

18

Table of Contents

The Offering

The Selling Shareholder is offering for resale the Resale Shares. The Resale Shares consist of 4,581,534 shares of our Common Stock underling the Convertible Notes.

As of October 3, 2022, there were 43,364,172 shares of our Common Stock outstanding, of which 38,114,775 shares were held by non-affiliates. If the Selling Shareholder converts the Convertible Notes, the ownership position of our shareholders prior to the conversion or exercise would be diluted. If the Selling Shareholder converts the Convertible Notes into all of the 4,581,534 shares being offered for resale by this prospectus and such shares are resold to non-affiliates, such shares would represent 9.56% of the total number of shares held by non-affiliates after the offering (assuming the issuance of no additional shares). The number of shares ultimately offered for resale by the Selling Shareholder depends upon the amount of the Convertible Notes that are converted and the conversion price used for such conversions.

| Shares of Common Stock Offered Hereby |

4,581,534 |

| Common Stock Outstanding(1) |

43,364,172 shares. |

| Common Stock Outstanding after the Offering |

47,945,706 shares, assuming the conversion of the Convertible Notes into all 4,581,534 underlying shares registered hereby. |

| Interest Rate |

The rate of interest on the Convertible Notes is 4.50% per annum payable semi-annually, or 6.00% per annum if we elect to pay such interest through the delivery of additional Convertible Notes. |

| Nasdaq Global Select Market Symbol |

Our shares of Common Stock are traded under the symbol “FEAM.” |

| Use of Proceeds |

We will not receive any proceeds from the Resale Shares by the Selling Shareholder. |

| We have received net proceeds of approximately $55,841,000 under the Note Purchase Agreement. |

| Risk Factors |

See “Risk Factors” and other information included in this prospectus for a discussion of factors you should consider before investing in our securities. |

| Dividend Policy |

We have not paid any cash dividends on our Common Stock to date. The payment of cash dividends in the future will be dependent upon our revenues and earnings, if any, capital requirements, and general financial condition. The payment of any cash dividends will be within the discretion of our Board of Directors. |

| (1) | As of October 3, 2022 and does not include (i) 6,202,732 shares of Common Stock underlying restricted stock awards and stock options granted as of October 3, 2022 or (ii) any shares of Common Stock underlying the Convertible Notes. |

19

Table of Contents

RISK FACTORS

Investing in our securities involves risks. Before you make a decision to buy our securities, in addition to the risks and uncertainties discussed above under “Cautionary Note Regarding Forward-Looking Statements,” you should carefully consider the specific risks set forth herein. If any of these risks actually occur, it may materially harm our business, financial condition, liquidity and results of operations. As a result, the market price of our securities could decline, and you could lose all or part of your investment. Additionally, the risks and uncertainties described in this prospectus are not the only risks and uncertainties that we face. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may become material and adversely affect our business.

Risks Relating to Our Business

We have incurred significant net operating losses since our inception and anticipate that we will incur continued losses for the foreseeable future.

We had an accumulated deficit of $107.4 million as of June 30, 2022, and we expect to incur significant discovery and development expenses in the foreseeable future related to the completion of exploration, development and commercialization of Fort Cady. As a result, we expect we will continue to sustain substantial operating and net losses, and it is possible that we will never be able to sustain or develop the revenue levels necessary to attain profitability. If we are unable to raise sufficient capital when needed, our business, financial condition and results of operations could be materially and adversely affected, and we may need to modify our operational plans. In addition, if we were unable to raise sufficient capital in the future, it may be determined that we would be unable to continue as a going concern, which could have a further material adverse impact on our business and financial condition.

Our future performance is difficult to evaluate because we have no or only a limited operating history in the minerals industry and no revenue from our proposed extraction operations at our properties, which may negatively impact our ability to achieve our business objectives.

Although the Fort Cady deposit was identified over 50 years ago and significant work has been undertaken to refine the resource estimate and development plan since that time, including by our immediate predecessor, ABR, which undertook significant development activities to develop the resource estimate and mine plan for Fort Cady, we have not realized any revenues to date from the sale of mineral products. To date, our operating cash flow needs have been financed primarily through equity financing and not through cash flows derived from our operations.

We do not currently produce any material, nor do we currently sell any materials that may be derived from our properties. As a result, our revenues are expected to be determined, to a large degree, by the success of our construction and operation of the SSBF, development of our proposed large-scale complex at Fort Cady, subsequent operating activities as well as ongoing commercial and marketing efforts to establish offtake contracts for material products. Our revenues will also be substantially impacted by the prevailing prices for boric acid and its derivatives, lithium carbonate, HCl, SOP and gypsum, to the extent that these products can be successfully extracted. At the present time, a recovery process for lithium has not been developed and will likely not be addressed until recovery of boric acid is operational. Furthermore, preliminary work regarding the recovery of SOP has been completed, but a determination has not been made as to whether or when SOP production will be included in the planned operations at Fort Cady. For the products that we aim to successfully produce in the future, market prices are dictated by supply and demand, and we cannot predict or control the price we will receive for boric acid and its derivatives, lithium carbonate, HCl, SOP and gypsum. Although management has identified currently favorable market conditions concerning the supply and demand of boric acid, boron advanced materials and lithium carbonate, future market conditions may be significantly less favorable as a result of numerous factors, including many that are beyond the scope of our control.

20

Table of Contents