As filed with the Securities and Exchange Commission on March 16, 2022.

Registration No. 333-262065

Delaware | | | 4924 | | | 87-2878691 |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification Number) |

| | | With copies to: | | | ||

Andrew L. Fabens Hillary H. Holmes Gibson, Dunn & Crutcher LLP 811 Main Street, Suite 3000 Houston, TX 77002 (346) 718-6600 | | | Alisa Newman Hood Executive Vice President, General Counsel and Secretary Excelerate Energy, Inc. 2445 Technology Forest Blvd., Level 6 The Woodlands, TX 77381 (832) 813-7100 | | | Michael Kaplan Pedro Bermeo Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10022 (212) 450-4000 |

Large accelerated filer ☐ | | | Accelerated filer ☐ |

Non-accelerated filer ☒ | | | Smaller reporting company ☐ |

| | | Emerging growth company ☒ |

PROSPECTUS | | |

| | | Per Share | | | Total | |

Initial public offering price | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | $ | | | $ |

Proceeds, before expenses, to us | | | $ | | | $ |

(1) | See “Underwriting (Conflicts of Interest)” for a description of all underwriting compensation payable in connection with this offering. |

Barclays | | | J.P. Morgan | | | Morgan Stanley |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

• | LNG-to-power developers. In many of our markets, we compete with other LNG-to-power companies, including New Fortress Energy and AES. Our investment strategy is focused on leveraging our FSRU expertise and local operational experience and relationship development to drive the expansion of incremental |

• | Large LNG producers. When compared to major LNG producers such as Qatargas, Shell, ExxonMobil, BP and Total Energies, we believe we are better positioned to open and expand new markets given our expertise in the downstream portion of the LNG value chain. Our focus is on helping LNG producers expand the reach of their LNG supply beyond their traditional markets, resulting in less price pressure and better portfolio diversification. In close collaboration with Qatargas, we succeeded in bringing regasified LNG to Pakistan and Bangladesh, which triggered a dramatic displacement of coal fired plants from the government’s energy plans. Additionally, we are collaborating with ExxonMobil on a feasibility study in Albania of an opportunity for them to provide LNG and for us to develop the LNG terminal, power generation facilities and pipeline interconnections necessary to make the importation of LNG viable, illustrating how we can provide value to LNG producers while capturing integrated markets downstream. |

• | FSRU / LNG carrier owners. As the owner and operator of the largest FSRU fleet employed for regasification in the industry, we compete with FSRU and LNG carrier (“LNGC”) owners such as New Fortress Energy (following its acquisition of Hygo Energy Transition and Golar LNG Partners), Hoegh LNG and GasLog. We distinguish ourselves by providing customers the ability to expand our service as their energy demands increase. This flexible approach, focused on optimizing services by swapping smaller FSRUs for larger ones, performing technical upgrades and offering seasonal service when required, fosters trust and long-term relationships with our customers. We believe the fundamentals supporting the FSRU business model require operators to focus on reliability, value and service, combined with disciplined expansion and growth. |

• | Experienced LNG Leader and Proven Ability to Execute. We are an admired player within the LNG industry with significant experience across the value chain. Our experienced team and proven LNG solutions, including the industry's largest FSRU fleet employed for regasification, more than 2,200 STS transfers of LNG with over 40 LNG operators and the development or operation of 15 LNG import terminals, make us a market leader and a trusted partner for countries who seek to improve their access to energy. We have nearly two decades of development, construction and operational experience, making us one of the most accomplished, reliable and capable LNG companies in the industry. Our team’s in-depth experience and local presence enable us to support energy hubs by sourcing and aggregating LNG from the global market for delivery downstream, ensuring the long-term stability, reliability, and independence of customers’ energy supply. |

• | Positioned to Meet Growing Global Demand for Cleaner Energy. According to the International Energy Agency’s (“IEA”) most recent semi-annual Electricity Market Report, global electricity demand rebounded strongly in 2021, growing by close to 6% over the prior year, and is expected to increase by approximately 3% annually in 2022 and 2023. With the demand for power generation growing worldwide, direct access to diverse, affordable and reliable energy sources such as LNG has become a critical enabler for economic growth and improving the quality of life across the globe. LNG provides an abundant, competitive and cleaner energy source to meet the world’s growing demand for power. It is also an efficient means to displace coal, which is a higher carbon intensity fuel compared to natural gas. Despite its advantages, LNG access is not readily available in many emerging markets due to the complexity of LNG import projects. We have an established reputation for developing and operating complex LNG solutions and are a trusted operator with a strong track record of bringing reliability, resiliency and flexibility to energy systems. |

• | Full-Service, Integrated LNG Business Model Provides Competitive Advantage. As market dynamics and the energy needs of customers have evolved over time, we embraced the opportunity to expand beyond our FSRU business. Today, we are addressing the need for increased access to LNG with our fully integrated business model that manages the LNG supply chain from procurement until final delivery to end users. We plan to help our customers meet their growing energy demand by providing an array of products, including LNG terminal services, natural gas supply procurement and distribution, LNG-to-power projects |

• | Well-Established FSRU Business Supported by Dependable Revenue Base. We own and operate the largest FSRU fleet employed for regasification in the industry. The success of our well established FSRU business is highlighted by our ability to secure long-term, take-or-pay contracts that generate consistent revenue and cash flow with minimal exposure to commodity price volatility. Our ability to swap FSRUs between projects makes our baseline revenue more predictable and minimizes redeployment risk. Further, we minimize the initial commitments for integrated offers through the initial use of existing, smaller capacity FSRUs while our customers’ markets evolve. Most of our existing customers have benefited from this scalability, which has resulted in better project returns and higher customer loyalty. This strength has allowed us to capture downstream markets such as Brazil, where our successful FSRU services with Petrobras opened the door to accessing gas sales through the lease of the Bahia Regasification Terminal from Petrobras. Our profitable FSRU and LNG marketing and supply businesses also provide us with valuable connectivity to global downstream markets. With our expansive global presence, we are well positioned to deliver integrated natural gas and power solutions, giving our customers access to cleaner, reliable and affordable energy. |

• | Understanding of LNG Market Dynamics Allows for Portfolio Optimization. We leverage our expertise and understanding of LNG market dynamics to create significant value though our LNG marketing and supply business. Our worldwide market access and ability to buy LNG from major LNG producers and traders gives us the chance to capture additional value via portfolio optimization and provides incremental cash flow. Even more importantly, our access to diverse, uncorrelated markets, including New England and Brazil, generates valuable arbitrage opportunities. We are structuring our business to be able to maximize this extra value from LNG supply to gas sales agreements (“GSA”) and power purchase agreements (“PPA”). Our strategy of integrating LNG supply, natural gas sales and terminal operations, gives us the ability to optimize our FSRU fleet utilization. |

• | Proven Management Team. Our management team has experience in all aspects of the LNG value chain and a strong balance of technical, commercial, operational, financial, legal and management skills. Steven Kobos, our President and Chief Executive Officer, has over 27 years of experience working on complex energy and infrastructure development projects and general maritime operations, specifically LNG shipping, FSRUs, chartering of vessels, shipbuilding contracts, operational agreements and related project finance and tax matters, and he has helped establish Excelerate as a growing and profitable international energy company. Daniel Bustos, our Executive Vice President and Chief Commercial Officer, has over 24 years of experience leading commercial development of oil and gas projects across the globe, with a particular focus on LNG, and is responsible for the commercial development of our LNG import projects, expansion of our customer base and the buildout of our global network of regional offices. Dana Armstrong, our Executive Vice President and Chief Financial Officer, provides oversight of all global financial reporting, financial planning and analysis, accounting, treasury, tax, financial systems and internal controls and has led both public and private multinational companies within the energy and biotechnology industries over her 25-year career. Calvin Bancroft, our Executive Vice President and Chief Operating Officer, has over 40 years of experience in the shipping industry, with recognized expertise in maritime security, chartering, supply chain management and operational logistics. Alisa Newman Hood, our Executive Vice President and General Counsel, has 20 years of worldwide legal, government relations and energy policy experience. Amy Thompson, our Executive Vice President and Chief Human Resources Officer, has over 22 years of human resources experience in global oil field services organizations and has held various leadership roles in the United States and the Middle East. |

• | Continue to develop our existing, diversified regasification business, supported by our large purpose-built FSRU fleet. Our current markets are essential to maintaining our solid foundation of revenues and providing new opportunities for downstream growth. Our persistent market presence helps |

• | Pursue opportunities downstream of existing markets. With established terminals, existing markets provide opportunities for us to structure end-to-end natural gas supply products and cleaner power solutions for our customers. We expect the organic growth of our business to be accompanied by strategic acquisitions for new or existing projects, in order to enhance our growth trajectory. As we integrate new infrastructure assets downstream of our floating LNG terminals, we will be required to make investments in new products and technologies to ensure that we are positioned for success in a lower-carbon energy future. We anticipate that increasing global demand for electricity generation, more efficient access to natural gas and decarbonization initiatives will be the primary drivers of opportunity, and we intend to diversify our product portfolio responsibly and in a manner that reinforces our broader goals of improving access to cleaner, more affordable and reliable energy, creating sustainable growth and combatting climate change. Our local teams will be key to expanding and diversifying our commercial, technical and financial expertise in our existing markets. |

• | Utilize our global presence to enter new, growing markets. We plan to use our existing markets as a springboard into new countries and regions. Our ability to cultivate meaningful partnerships and successfully acquire equity interests in projects will be a determining factor in how quickly we are able to achieve critical mass in new markets. We are currently developing a set of integrated LNG projects in |

• | Create a sizable, diversified LNG procurement portfolio. Our expansion downstream will offer us the opportunity to establish valuable access to a worldwide network of natural gas markets. Our network of supply and charter contracts and reputation with major LNG producers provide us with ample opportunities to grow our LNG portfolio on competitive terms. This diversified portfolio will give us the opportunity to better manage the typical uncertainties of local demand (weather seasonality, economic cycles, availability of renewables, etc.), while capturing arbitrage opportunities. For example, we have already demonstrated the value of accessing the New England market in a flexible way. With the addition of new market access points in Asia, Europe, Africa and South America, we can capture value from our LNG procurement portfolio, above the margins generated in individual markets. Finally, this LNG portfolio will help further enhance our competitive edge for new opportunities, allowing us to offer more flexible and cost-effective products to new customers. |

• | Maintain our disciplined investment philosophy. As we grow our business, we are committed to maintaining our disciplined investment philosophy and prudent approach to project development. We have established a proven track record of investing in the right projects which has resulted in higher project returns and consistent earnings results. We also strive to negotiate the terms of our contracts in a manner that seeks to minimize any potential commodity risk. It is our aim to have an industry leading portfolio of high-return growth opportunities that will support sustainable and profitable growth for years to come. We expect our contract portfolio to evolve over time to include long-term contracts as well as shorter-term agreements that will create opportunities to capture additional upside. |

• | our ability to enter into contracts with customers and our customers’ failure to perform their contractual obligations; |

• | customer termination rights in our contracts; |

• | the risks inherent in operating our FSRUs and other LNG infrastructure assets; |

• | the technical complexity of our FSRUs and LNG import terminals and related operational problems; |

• | cancellations, time delays, unforeseen expenses and other complications while developing our projects; |

• | our inability to develop a project successfully and our customers’ failure to fulfill their payment obligations to us following our capital investment in a project; |

• | the failure of our regasification terminals and other facilities to operate as expected or be completed; |

• | our need for substantial expenditures to maintain and replace, over the long-term, the operating capacity of our fleet, regasification terminals and associated assets, pipelines and downstream infrastructure; |

• | our reliance on our engineering, procurement and construction (“EPC”) contractors and other contractors for the successful completion of our energy-related infrastructure; |

• | shortages of qualified officers and crew impairing our ability to operate or increasing the cost of crewing our vessels; |

• | uncertainty related to construction costs, development timelines, third-party subcontractors and equipment manufacturers required to perform our development services; |

• | our ability to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the design, construction and operation of our facilities and provision of our services; |

• | our ability to maintain relationships with our customers and existing suppliers, source new suppliers for LNG and critical components of our projects and complete building out our supply chain; |

• | our ability to connect with third-party pipelines, power plants and other facilities that provide gas receipt and delivery downstream of our integrated terminals; |

• | our ability to purchase or receive physical delivery of LNG in sufficient quantities to satisfy our delivery obligations under GSAs or at attractive prices; |

• | changes in the demand for and price of LNG and natural gas and LNG regasification capacity; |

• | the competitive market for LNG regasification services; |

• | fluctuations in hire rates for FSRUs; |

• | infrastructure constraints and community and political group resistance to existing and new LNG and natural gas infrastructure over concerns about the environment, safety and terrorism; |

• | outbreaks of epidemic and pandemic diseases and governmental responses thereto; |

• | our ability to access financing sources on favorable terms; |

• | our debt level and finance lease liabilities, which may limit our flexibility in obtaining additional financing, refinancing credit facilities upon maturity; |

• | volatility of the global financial markets and uncertain economic conditions; |

• | our financing agreements, which include financial restrictions and covenants and are secured by certain of our vessels; |

• | compliance with various international treaties and conventions and national and local environmental, health, safety and maritime conduct laws that affect our operations; |

• | our dependence upon distributions from our subsidiaries to pay dividends, if any, taxes and other expenses and make payments under the Tax Receivable Agreement; |

• | the requirement that we pay over to the TRA Beneficiaries (as defined below) most of the tax benefits we receive; |

• | payments under the Tax Receivable Agreement being accelerated and/or significantly exceeding the tax benefits, if any, that we actually realize; |

• | the possibility that EELP will be required to make distributions to us and the other partners of EELP; |

• | the material weaknesses identified in our internal control over financial reporting; |

• | Kaiser having the ability to direct the voting of a majority of the voting power of our common stock, and his interests may conflict with those of our other stockholders; and |

• | our ability to pay dividends on our Class A common stock. |

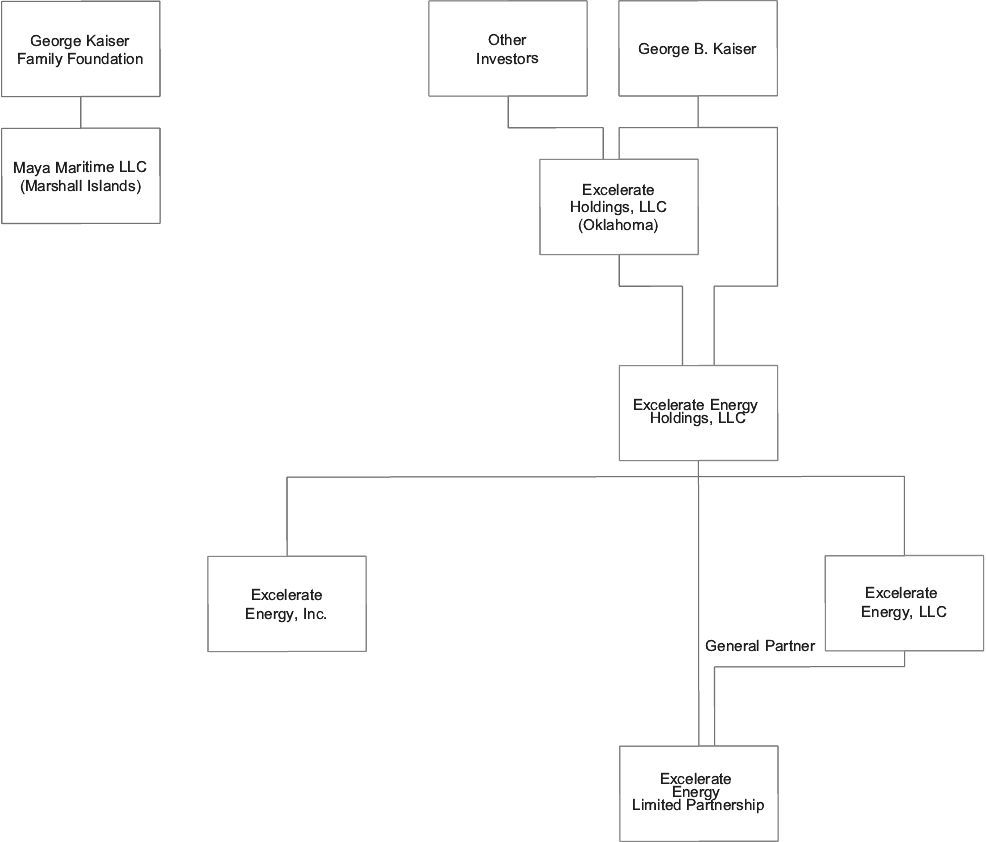

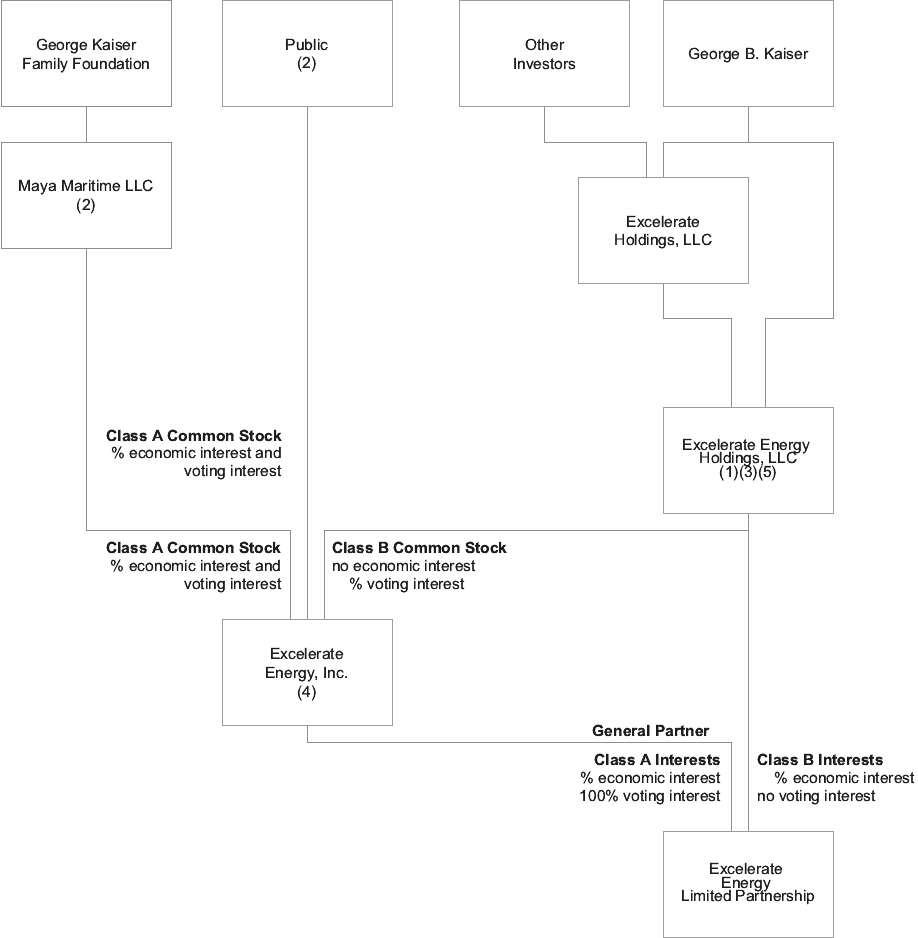

(1) | At the closing of this offering, EE Holdings will own Class B interests of EELP and shares of Class B common stock of Excelerate. |

(2) | Each share of Class A common stock of Excelerate will be entitled to one vote and will vote together with the Class B common stock as a single class, except as provided in our amended and restated certificate of incorporation or required by law. See “Description of Capital Stock—Common Stock—Class A Common Stock.” |

(3) | Each share of Class B common stock is entitled to one vote and will vote together with the Class A common stock as a single class, except as provided in our amended and restated certificate of incorporation or required by law. The Class B common stock will have no economic rights in Excelerate. See “Description of Capital Stock—Common Stock—Class B Common Stock.” |

(4) | Excelerate will, directly or indirectly, own all of the Class A interests of EELP after the Reorganization, which upon the completion of this offering will represent the right to receive approximately % of the distributions made by EELP. While this interest represents a minority of economic interests in EELP, it represents 100% of the voting interests, and Excelerate (or its subsidiary) will be admitted as the general partner of EELP in connection with the Reorganization. As a result, Excelerate will operate and control all of EELP’s business and affairs and will be required to consolidate its financial results into Excelerate’s financial statements. |

(5) | At the closing of the offering, EE Holdings will own all of the outstanding shares of Class B common stock and all of the outstanding Class B interests of EELP, which upon the completion of this offering will represent the right to receive approximately % of the distributions made by EELP. No person will have any voting rights in EELP on account of the Class B interests, except for the right to approve amendments to the EELP Limited Partnership Agreement (as defined herein) that adversely affect the rights of holders of Class B interests. However, through ownership of shares of Class B common stock, EE Holdings will control a majority of the voting power of the common stock of Excelerate, the general partner (or sole owner of the general partner) of EELP and will therefore have indirect control over EELP. Class B interests of EELP may be exchanged for shares of our Class A common stock or, at our election, for cash, subject to certain restrictions pursuant to the EELP Limited Partnership Agreement described in “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate Energy, Inc.—EELP Limited Partnership Agreement.” When a Class B interest is exchanged for a share of our Class A common stock or, at our election, for cash, it will result in the automatic cancellation of the corresponding number of shares of our Class B common stock and, therefore, will decrease the aggregate voting power of EE Holdings. Any beneficial holder exchanging Class B interests must ensure that the applicable corresponding number of shares of Class B common stock are delivered to us for cancellation as a condition of exercising its right to exchange Class B interests for shares of our Class A common stock or, at our election, for cash. After a Class B interest is surrendered for exchange, it will not be available for reissuance. |

• | being permitted to provide only two years of audited financial statements, in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; |

• | not being required to comply with the auditor attestation requirements in the assessment of our internal control over financial reporting under the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, for up to five years or until we no longer qualify as an emerging growth company; |

• | not being required to comply with any requirement that may be adopted by the Public Company Accounting Oversight Board (“PCAOB”) regarding mandatory audit firm rotation or a supplement to the auditor’s report providing additional information about the audit and the financial statements; |

• | reduced disclosure obligations regarding executive compensation pursuant to the rules applicable to smaller reporting companies, which means we do not have to include a compensation discussion and analysis and certain other disclosures regarding our executive compensation; and |

• | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and obtaining stockholder approval of any golden parachute payments not previously approved. |

• | approximately $ million of the net proceeds of this offering to fund our growth strategy, including our projects in Brazil at the Bahia Regasification Terminal, Albania at the Vlora LNG Terminal, the Philippines at the Filipinas LNG Gateway, and Bangladesh at the Payra LNG Terminal; |

• | approximately $ million of the net proceeds of this offering to fund in part EELP's purchase of the Foundation Vessels in connection with the Reorganization; and |

• | approximately $ million of the net proceeds of this offering to pay the expenses incurred by us in connection with this offering and the Reorganization. |

• | shares of Class A common stock issuable upon exercise of the underwriters’ option to purchase additional shares; |

• | shares of Class A common stock issuable under our Excelerate Energy, Inc. Long-Term Incentive Plan (the “LTI Plan”), including: |

(i) | shares of Class A common stock underlying restricted stock units and stock options to be granted to certain employees and our independent directors pursuant to the LTI Plan in connection with this offering, which restricted stock units will vest ratably over a three-year period and which stock options will have an exercise price per share equal to the public offering price in this offering; and |

(ii) | additional shares of Class A common stock to be reserved for future issuance of awards under the LTI Plan; and |

• | shares of Class A common stock reserved for issuance upon exchange of the Class B interests of EELP (and the cancellation of the corresponding shares of Class B common stock) that will be outstanding immediately after this offering. |

| | | Year Ended December 31, | ||||

(In thousands) | | | 2021 | | | 2020 |

Statements of Operations Data: | | | | | ||

Revenues | | | | | ||

FSRU and terminal services | | | $468,030 | | | $430,843 |

Gas sales | | | 420,525 | | | — |

Total revenues | | | 888,555 | | | 430,843 |

Operating expenses | | | | | ||

Cost of revenue and vessel operating expenses | | | 192,723 | | | 150,478 |

Direct cost of gas sales | | | 390,518 | | | — |

Depreciation and amortization | | | 104,908 | | | 104,167 |

Selling, general and administrative | | | 47,088 | | | 42,942 |

Restructuring, transition and transaction expenses | | | 13,974 | | | — |

Total operating expenses | | | 749,211 | | | 297,587 |

Operating income | | | 139,344 | | | 133,256 |

Other income (expense) | | | | | ||

Interest expense | | | (31,892) | | | (37,460) |

Interest expense – related party | | | (48,922) | | | (51,970) |

Earnings from equity-method investment | | | 3,263 | | | 3,094 |

Other income, net | | | 564 | | | (92) |

Income before income taxes | | | 62,357 | | | 46,828 |

Provision for income taxes | | | (21,168) | | | (13,937) |

Net income | | | 41,189 | | | 32,891 |

Less net income attributable to non-controlling interests | | | 3,035 | | | 2,622 |

Less net income attributable to non-controlling interests – ENE Onshore | | | (2,964) | | | (8,484) |

Net income attributable to EELP | | | $41,118 | | | $38,753 |

Additional financial data: | | | | | ||

Gross Margin | | | $200,406 | | | $176,198 |

Adjusted Gross Margin | | | 305,314 | | | 280,366 |

Adjusted EBITDA | | | 262,053 | | | 240,425 |

Adjusted EBITDAR | | | 291,051 | | | 256,197 |

Capital expenditures | | | 36,091 | | | 41,258 |

| | | As of December 31, | ||||

(In thousands) | | | 2021 | | | 2020 |

Balance Sheets Data: | | | | | ||

Property and equipment, net | | | $1,433,169 | | | $1,501,528 |

Total assets | | | 2,500,736 | | | 2,255,724 |

Long-term debt (includes current portion) | | | 233,415 | | | 262,424 |

Long-term debt (includes current portion) – related party | | | 198,313 | | | 427,193 |

Total liabilities | | | 1,496,810 | | | 1,484,563 |

| | | Year Ended December 31, | ||||

(In thousands) | | | 2021 | | | 2020 |

Statements of Cash Flow Data: | | | | | ||

Net cash provided by (used in): | | | | | ||

Operating activities | | | $141,613 | | | $108,964 |

Investing activities | | | (36,091) | | | (41,258) |

Financing activities | | | $(124,097) | | | $(31,438) |

| | | Year Ended December 31, | ||||

(In thousands) | | | 2021 | | | 2020 |

FSRU and terminal services revenues | | | $468,030 | | | $430,843 |

Gas sales revenues | | | 420,525 | | | — |

Cost of revenue and vessel operating expenses | | | 192,723 | | | 150,478 |

Direct cost of gas sales | | | 390,518 | | | — |

Depreciation and amortization expense | | | 104,908 | | | 104,167 |

Gross Margin | | | 200,406 | | | 176,198 |

Depreciation and amortization expense | | | 104,908 | | | 104,167 |

Adjusted Gross Margin | | | $305,314 | | | $280,365 |

| | | Year Ended December 31, | ||||

(In thousands) | | | 2021 | | | 2020 |

Net income | | | $41,189 | | | $32,891 |

Interest expense | | | 80,814 | | | 89,430 |

Provision for income taxes | | | 21,168 | | | 13,937 |

Depreciation and amortization expense | | | 104,908 | | | 104,167 |

Restructuring, transition and transaction expenses | | | 13,974 | | | — |

Adjusted EBITDA | | | 262,053 | | | 240,425 |

Vessel and infrastructure rent expense | | | 28,998 | | | 15,772 |

Adjusted EBITDAR | | | $291,051 | | | $256,197 |

• | at the end of a specified time period following certain events of force majeure or the outbreak of war; |

• | extended unexcused service interruptions or deficiencies; |

• | loss of or requisition of the FSRU; |

• | the occurrence of an insolvency event; and |

• | the occurrence of certain uncured, material breaches. |

• | marine disasters; |

• | piracy; |

• | environmental incidents; |

• | bad weather; |

• | mechanical failures; |

• | grounding, fire, explosions and collisions; |

• | human error; and |

• | war and terrorism. |

• | death or injury to persons, loss of property or damage to the environment, natural resources or protected species, and associated costs; |

• | delays in taking delivery of an LNG cargo or discharging regasified LNG, as applicable; |

• | suspension or termination of customer contracts, and resulting loss of revenues; |

• | governmental fines, penalties or restrictions on conducting business; |

• | higher insurance rates; and |

• | damage to our reputation and customer relationships generally. |

• | the cost of labor and materials; |

• | customer requirements; |

• | fleet and project size; |

• | the cost of replacement vessels; |

• | length of charters; |

• | governmental regulations and maritime self-regulatory organization standards relating to safety, security or the environment; |

• | competitive standards; and |

• | operating conditions, including adverse weather events, sea currents and natural disasters impacting performance, required maintenance and repair intervals and spending. |

• | design and engineer each of our facilities to operate in accordance with specifications; |

• | engage and retain third-party subcontractors and procure equipment and supplies; |

• | respond to difficulties such as equipment failure, delivery delays, schedule changes and failures to perform by subcontractors, some of which are beyond their control; |

• | attract, develop and retain skilled personnel, including engineers; |

• | post required construction bonds and comply with the terms thereof; |

• | manage the construction process generally, including coordinating with other contractors and regulatory agencies; and |

• | maintain their own financial condition, including adequate working capital. |

• | additions to competitive regasification capacity; |

• | insufficient or oversupply of natural gas liquefaction or export capacity worldwide; |

• | insufficient LNG tanker capacity; |

• | weather conditions and natural disasters; |

• | reduced demand and lower prices for natural gas over an extended period; |

• | higher LNG prices, which could make other fuels more competitive in the markets where we operate; |

• | increased natural gas production deliverable by pipelines in the markets where we operate, which could suppress demand for LNG; |

• | decreased oil and natural gas exploration activities, including shut-ins and possible proration, which have begun and may continue to decrease the production of natural gas available for liquefaction; |

• | cost improvements that allow competitors to offer LNG regasification services at reduced prices; |

• | changes in supplies of, and prices for, alternative energy sources, such as coal, oil, nuclear, hydroelectric, wind and solar energy, which may reduce the demand for natural gas; |

• | changes in regulatory, tax or other governmental policies regarding imported or exported LNG, natural gas or alternative energy sources, which may reduce the demand for imported LNG or natural gas in the markets where we operate; |

• | political conditions; |

• | adverse relative demand for LNG compared to other markets; |

• | changes in economic conditions of countries where we operate or purchase or sell LNG and natural gas; and |

• | cyclical trends in general business and economic conditions that cause changes in the demand for natural gas. |

• | FSRU experience and quality of ship operations; |

• | shipping industry relationships and reputation for customer service and safety; |

• | technical ability and reputation for operation of highly specialized vessels, including FSRUs; |

• | quality and experience of seafaring crew; |

• | financial stability; |

• | construction management experience, including (i) relationships with shipyards and the ability to secure suitable berths and (ii) the ability to obtain on-time delivery of new FSRUs according to customer specifications; |

• | willingness to accept operational and other risks, such as allowing customer termination rights for extended operational failures and force majeure events; |

• | the ability to commence operations quickly; and |

• | price competitiveness. |

• | limited downstream infrastructure limiting the development of new or expanded import terminals; |

• | local community resistance to proposed or existing LNG facilities based on safety, environmental or security concerns; |

• | any significant explosion, spill or similar incident involving an LNG facility or vessel involved in the LNG transportation, storage and regasification industry, including an FSRU or LNGC; and |

• | labor or political unrest affecting existing or proposed sites for LNG regasification terminals. |

• | inability to achieve our target costs or our target pricing for long-term contracts; |

• | failure to develop cost-effective logistics solutions; |

• | failure to manage expanding operations in the projected time frame; |

• | failure to win new bids or contracts on the terms, size and within the time frame we need to execute our business strategy; |

• | inability to attract and retain personnel in a timely and cost-effective manner; |

• | failure of investments in technology and machinery, such as regasification technology, to perform as expected; |

• | increases in competition which could increase our costs and undermine our profits; |

• | inability to source LNG in sufficient quantities and/or at economically attractive prices; |

• | failure to anticipate and adapt to new trends in the energy sector of the countries where we operate; |

• | increases in operating costs, including the need for repairs and maintenance, capital improvements, insurance premiums, general taxes, real estate taxes and utilities or other costs that affect our profit margins; |

• | inability to raise significant additional debt and equity capital in the future to implement our strategy as well as to operate and expand our business; |

• | general economic, political and business conditions in the United States, Argentina, Bangladesh, Brazil, Israel, Pakistan, the UAE and in the other geographic areas in which we operate or intend to operate; |

• | inflation, depreciation of the currencies of the countries in which we operate and fluctuations in interest rates; |

• | failure to obtain approvals from governmental regulators and relevant local authorities for the construction and operation of potential future projects and other relevant approvals; |

• | existing and future governmental laws and regulations; |

• | inability, or failure, of any customer or contract counterparty to perform their contractual obligations to us; or |

• | uncertainty regarding the timing, pace and extent of an economic recovery in the United States, the other jurisdictions in which we operate and elsewhere, which in turn will likely affect demand for crude oil and natural gas. |

• | crew changes have been canceled or delayed due to port authorities denying or delaying disembarkation, a high potential of infection in countries where crew changes may otherwise have taken place, and the inability to repatriate crew members due to lack of international air transport or denial of re-entry by crew members’ home countries that have closed their borders; |

• | the inability to complete scheduled engine overhauls, routine maintenance work and management of equipment malfunctions; |

• | shortages or a lack of access to required spare parts for our vessels, and delays in repairs to, or scheduled or unscheduled maintenance or modifications or dry docking of, our vessels, as a result of a lack of berths available at shipyards from a shortage in labor at shipyards or contractors or due to other business disruptions; |

• | necessity to find new, remote means to complete vessel inspections and related certifications by class societies, customers or government agencies; and |

• | disruptions to our business from, or additional costs related to, new regulations, directives or practices implemented in response to the pandemic, such as travel restrictions, increased inspection regimes, hygiene measures (such as quarantining and physical distancing) or increased implementation of remote working arrangements. |

• | managing crew rotations depending on the duration and severity of Covid-19 in countries from which our crews are sourced as well as any restrictions in place at ports in which our vessels call; |

• | providing financial support to Excelerate Technical Management (“ETM”) employees while on shore leave; |

• | under maritime standards and the Maritime Labour Convention, on a case-by-case basis, providing financial assistance to seafarers on shore as necessary; |

• | arranging to accept delivery of additional spare parts and critical supplies where possible in our supply chains; |

• | postponing or cancelling planned engine overhaul and routine maintenance services where possible, and arranging for remote servicing of equipment when possible; |

• | cancelling non-critical boardings, limiting visits to vettings inspectors, pilots, critical service engineers and port officials where allowed and implementing procedures and mitigation controls on board to limit the risk of human-to-human transmission from visiting personnel; |

• | more extensively using remote ship visits by our management and support functions; |

• | monitoring applicable local legislation and social distancing guidelines related to minimizing human-to-human transmission, IT systems and network capacity and financial reporting systems and internal controls over financial reporting; |

• | providing mental health support for our seafarers and global workforce through membership in organizations providing hotline support and introducing a forum for virtual sharing and collaboration on mental health concerns; and |

• | permitting flexible working arrangements for our people, encouraging full vaccination status of all employees/seafarers and postponing non-critical projects. |

• | prevailing economic conditions in the LNG, natural gas and energy markets; |

• | a substantial or extended decline or increase in demand for LNG; |

• | increases in the supply of vessel capacity; |

• | the size and age of a vessel; |

• | the remaining term on existing time charters; and |

• | the cost of retrofitting or modifying existing vessels, as a result of technological advances in vessel design or equipment, changes in applicable environmental or other regulations or standards, customer requirements or otherwise. |

• | general market conditions; |

• | the duration and effects of the Covid-19 pandemic; |

• | the market’s perception of our growth potential; |

• | our current debt levels; |

• | our current and expected future earnings; |

• | restrictions in our customer contracts to pledge or place debt on our assets; |

• | risk allocation requirements for limited recourse financing vehicles; |

• | creditworthiness of potential customers; |

• | our cash flow; and |

• | the market price per share of our Class A common stock. |

• | our ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be limited, or such financing may not be available on favorable terms; |

• | we will need a substantial portion of our cash flows to make principal and interest payments on our debt, reducing the funds that would otherwise be available for operations and future business opportunities; |

• | our debt level may make us vulnerable to competitive pressures or a downturn in our business or the economy generally; and |

• | our debt level may limit our flexibility in responding to changing business and economic conditions. |

• | merge into, or consolidate with, any other entity or sell, or otherwise dispose of, all or substantially all of our assets; |

• | make or pay dividends; |

• | incur additional indebtedness; |

• | incur or make any capital expenditures; or |

• | materially amend or terminate our customer contract for the vessel that secures the financing. |

• | the likelihood that an active trading market for shares of our Class A common stock will develop or be sustained; |

• | the liquidity of any such market; |

• | the ability of our stockholders to sell their shares of Class A common stock; or |

• | the price that our stockholders may obtain for their Class A common stock. |

• | institute a more comprehensive compliance function, including for financial reporting and disclosures; |

• | continue to prepare and distribute periodic public reports in compliance with our obligations under federal securities laws; |

• | comply with rules promulgated by the NYSE; |

• | continue to prepare and distribute periodic public reports in compliance with our obligations under federal securities laws; |

• | enhance our investor relations function; |

• | establish new internal policies, such as those relating to insider trading; and |

• | involve and retain to a greater degree outside counsel and accountants in the above activities. |

• | we did not design and maintain effective controls over period end financial reporting processes and procedures, controls over significant accounts and disclosures to achieve complete, accurate and timely |

• | we did not design and maintain effective controls over the proper timing of revenue recognition for dry-dock revenue contracts; |

• | we did not design and maintain effective controls to analyze compliance with non-financial debt covenants and conditions; and |

• | we did not design and maintain effective controls to verify the completeness and accuracy of our income tax provision. |

• | our operating and financial performance; |

• | quarterly variations in the rate of growth of our financial indicators, such as net income per share, net income and revenues; |

• | the public reaction to our press releases, our other public announcements and our filings with the SEC; |

• | strategic actions by our competitors; |

• | changes in revenue or earnings estimates, or changes in recommendations or withdrawals of research coverage, by equity research analysts; |

• | market and industry perception of our success, or lack thereof, in pursuing our growth strategies; |

• | introductions or announcements of new products offered by us or significant acquisitions, strategic partnerships, joint ventures or capital commitments by us or our competitors and the timing of such introductions or announcements; |

• | our ability to effectively manage our growth; |

• | the impact of pandemics on us and the national and global economies; |

• | speculation in the press or investment community; |

• | the failure of research analysts to cover our Class A common stock; |

• | whether investors or securities analysts view our stock structure unfavorably, particularly the significant voting control of our executive officers, directors and their affiliates; |

• | our ability or inability to raise additional capital through the issuance of equity or debt or other arrangements and the terms on which we raise it; |

• | additional shares of our Class A common stock being sold into the market by us or our existing stockholders, or the anticipation of such sales, including if existing stockholders sell shares into the market when applicable “lock-up” periods end; |

• | changes in accounting principles, policies, guidance, interpretations or standards; |

• | additions or departures of key management personnel; |

• | actions by our stockholders; |

• | changes in operating performance and stock market valuations of companies in our industry, including our vendors and competitors; |

• | trading volume of our Class A common stock; |

• | price and volume fluctuations in the overall stock market, including as a result of trends in the economy as a whole and those resulting from natural disasters, severe weather events, terrorist attacks and responses to such events; |

• | lawsuits threatened or filed against us; |

• | domestic and international economic, legal and regulatory factors unrelated to our performance; |

• | privacy or cybersecurity breaches, data theft or other security incidents or failure to comply with applicable data privacy laws, rules and regulations; |

• | our ability to obtain, maintain, protect, defend and enforce our intellectual property; and |

• | the realization of any risks described under this “Risk Factors” section. |

• | providing for two classes of stock; |

• | authorizing the issuance of “blank check” preferred stock that could be issued by our board of directors to increase the number of outstanding shares and thwart a takeover attempt; |

• | from and after such time as EE Holdings (including its permitted transferees) ceases to beneficially own at least 40% of the combined voting power of our then-outstanding capital stock entitled to vote generally in director elections (the “Trigger Date”), establishing a classified board of directors, with each class serving three-year staggered terms, so that not all members of our board of directors are elected at one time; |

• | from and after such time as our board is classified, providing that directors can be removed only for cause and only by the affirmative vote of at least 662∕3% of the voting power of the stock outstanding and entitled to vote on the election of directors, voting together as a single class; |

• | prohibiting the use of cumulative voting for the election of directors; |

• | from and after the Trigger Date, eliminating the ability of stockholders to call special meetings and prohibiting stockholder action by written consent and instead requiring stockholder actions to be taken at a meeting of our stockholders; |

• | from and after the Trigger Date, providing that only the board can fill vacancies on the board of directors; |

• | from and after the Trigger Date, requiring the approval of the holders of at least 662∕3% of voting power of the stock outstanding and entitled to vote thereon, voting together as a single class, to amend or repeal our bylaws and certain provisions of our certificate of incorporation; |

• | establishing advance notice provisions for stockholder proposals and nominations for elections to the board of directors to be acted upon at meetings of stockholders; and |

• | providing that the board of directors is expressly authorized to adopt, or to alter or repeal, our bylaws. |

• | a majority of such company’s board of directors consist of independent directors; |

• | such company have a nominating and governance committee that is composed entirely of independent directors with a written charter addressing such committee’s purpose and responsibilities; |

• | such company have a compensation committee that is composed entirely of independent directors with a written charter addressing such committee’s purpose and responsibilities; and |

• | such company conduct an annual performance evaluation of the nominating and governance and compensation committees. |

• | prevailing economic and market conditions in the natural gas and energy markets; |

• | negative global or regional economic or political conditions, particularly in LNG-consuming regions, which could reduce energy consumption or its growth; |

• | declines in demand for LNG or the services of LNGCs or FSRUs or; |

• | increases in the supply of LNGC capacity operating in the spot market or the supply of FSRUs; |

• | marine disasters; war, piracy or terrorism; environmental accidents; or inclement weather conditions; |

• | mechanical failures or accidents involving any of our vessels; and |

• | drydock scheduling and capital expenditures. |

• | our ability to enter into contracts with customers and our customers’ failure to perform their contractual obligations; |

• | customer termination rights in our contracts; |

• | the risks inherent in operating our FSRUs and other LNG infrastructure assets; |

• | the technical complexity of our FSRUs and LNG import terminals and related operational problems; |

• | cancellations, time delays, unforeseen expenses and other complications while developing our projects; |

• | our inability to develop a project successfully and our customers’ failure to fulfill their payment obligations to us following our capital investment in a project; |

• | the failure of our regasification terminals and other facilities to operate as expected or be completed; |

• | our need for substantial expenditures to maintain and replace, over the long-term, the operating capacity of our fleet, regasification terminals and associated assets, pipelines and downstream infrastructure; |

• | our reliance on our EPC contractors and other contractors for the successful completion of our energy-related infrastructure; |

• | shortages of qualified officers and crew impairing our ability to operate or increasing the cost of crewing our vessels; |

• | uncertainty related to construction costs, development timelines, third-party subcontractors and equipment manufacturers required to perform our development services; |

• | our ability to obtain and maintain approvals and permits from governmental and regulatory agencies with respect to the design, construction and operation of our facilities and provision of our services; |

• | our ability to maintain relationships with our customers and existing suppliers, source new suppliers for LNG and critical components of our projects and complete building out our supply chain; |

• | our ability to connect with third-party pipelines, power plants and other facilities that provide gas receipt and delivery downstream of our integrated terminals; |

• | our ability to purchase or receive physical delivery of LNG in sufficient quantities to satisfy our delivery obligations under GSAs or at attractive prices; |

• | changes in the demand for and price of LNG and natural gas and LNG regasification capacity; |

• | the competitive market for LNG regasification services; |

• | fluctuations in hire rates for FSRUs; |

• | infrastructure constraints and community and political group resistance to existing and new LNG and natural gas infrastructure over concerns about the environment, safety and terrorism; |

• | outbreaks of epidemic and pandemic diseases and governmental responses thereto; |

• | our ability to access financing sources on favorable terms; |

• | our debt level and finance lease liabilities, which may limit our flexibility in obtaining additional financing, refinancing credit facilities upon maturity; |

• | the effects of international conflicts, including sanctions, retaliatory measures and changes in the availability and prices of LNG, natural gas and oil resulting from the invasion of Ukraine by Russia, on our business, customers, industry and outlook; |

• | volatility of the global financial markets and uncertain economic conditions, including as a result of the invasion of Ukraine by Russia; |

• | our financing agreements, which include financial restrictions and covenants and are secured by certain of our vessels; |

• | compliance with various international treaties and conventions and national and local environmental, health, safety and maritime conduct laws that affect our operations; |

• | our dependence upon distributions from our subsidiaries to pay dividends, if any, taxes and other expenses and make payments under the Tax Receivable Agreement; |

• | the requirement that we pay over to the TRA Beneficiaries most of the tax benefits we receive; |

• | payments under the Tax Receivable Agreement being accelerated and/or significantly exceeding the tax benefits, if any, that we actually realize; |

• | the possibility that EELP will be required to make distributions to us and the other partners of EELP; |

• | the material weaknesses identified in our internal control over financial reporting; |

• | Kaiser having the ability to direct the voting of a majority of the voting power of our common stock, and his interests may conflict with those of our other stockholders; |

• | our ability to pay dividends on our Class A common stock; |

• | our status as an emerging growth company; |

• | the possibility that circumstances preclude any of our director nominees from joining our board of directors; |

• | other risks and uncertainties inherent in our business; and |

• | other risks, uncertainties and factors set forth in this prospectus, including those set forth under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business.” |

• | EE Holdings will amend and restate the limited partnership agreement of EELP (the “EELP Limited Partnership Agreement”) whereby, all of the outstanding interests of EELP will be recapitalized into Class B interests and EELP will be authorized to issue Class A interests. Subject to certain limitations, the EELP Limited Partnership Agreement will permit Class B interests to be exchanged for shares of Class A common stock on a one-for-one basis or, at Excelerate’s election, for cash. See “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate Energy, Inc.—The EELP Limited Partnership Agreement.” |

• | Excelerate will amend and restate its certificate of incorporation to, among other things, provide for Class A common stock and Class B common stock. See “Description of Capital Stock.” |

• | Excelerate will contribute shares of Class A common stock with a fair market value of $ to EELP in exchange for an equal number of Class A interests in EELP. |

• | In exchange for (i) shares of Class A common stock with a fair market value (based on the public offering price) of $ (which is equal to shares of Class A common stock assuming a public offering price equal to the midpoint of the price range set forth on the cover of this prospectus), (ii) a cash payment of $ and (iii) $ of deemed value for future payments under the Tax Receivable Agreement, EELP will purchase from Maya Maritime LLC, a wholly owned subsidiary of the Foundation, the Foundation Vessels pursuant to a securities purchase agreement. Each $1.00 increase or decrease in the assumed initial public offering price of $ per share of Class A common stock (the midpoint of the price range set forth on the cover of this prospectus) would increase or decrease the number of shares of Class A common stock exchanged for the Foundation Vessels by approximately shares, which would increase or decrease the Foundation’s indirect ownership percentage of our Class A common stock by approximately %. |

• | Excelerate will sell to the underwriters in this offering shares of our Class A common stock (assuming no exercise of the underwriters’ option to purchase additional shares). |

• | Excelerate will issue to EE Holdings and Excelerate Energy, LLC, in the aggregate, all of our outstanding shares of Class B common stock. In connection with the issuance of Class B common stock to EELP, Excelerate (or a wholly owned subsidiary of Excelerate) will be admitted as the general partner of EELP. Excelerate Energy, LLC will distribute to EE Holdings, all of its Class B common stock and Class B interests. |

• | EE Holdings will contribute Excelerate Energy, LLC to EELP and Excelerate Energy, LLC will be dissolved. |

• | Excelerate will enter into the Tax Receivable Agreement for the benefit of the TRA Beneficiaries, pursuant to which Excelerate will pay 85% of the amount of the net cash tax savings, if any, that Excelerate is deemed to realize as a result of (i) certain increases in the tax basis of assets of EELP and its subsidiaries resulting from exchanges of EELP partnership interests in the future, (ii) certain tax attributes of EELP and subsidiaries of EELP (including the existing tax basis of assets owned by EELP or its subsidiaries and the tax basis of the Foundation Vessels) that exist as of the time of this offering or may exist at the time when Class B interests of EELP are exchanged for shares of Class A common stock, and (iii) certain other tax benefits related to Excelerate entering into the Tax Receivable Agreement, including tax benefits attributable to payments that Excelerate makes under the Tax Receivable Agreement. See “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate Energy, Inc.—Tax Receivable Agreement.” |

• | We will enter into the Registration Rights Agreement to provide for certain rights and restrictions after the offering. See “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate Energy, Inc.—Registration Rights Agreement.” |

• | approximately $ million of the net proceeds of this offering to fund our growth strategy, including our projects in Brazil at the Bahia Regasification Terminal, Albania at the Vlora LNG Terminal, the Philippines at the Filipinas LNG Gateway and Bangladesh at the Payra LNG Terminal; |

• | approximately $ million of the net proceeds of this offering to fund in part EELP's purchase of the Foundation Vessels in connection with the Reorganization; |

• | approximately $ million to pay the expenses incurred by us in connection with this offering and the Reorganization; and |

• | other than as set forth below, the remainder for working capital and other general corporate purposes. |

| | | As of December 31, 2021 | ||||

(in thousands, except per share amounts and interest data) | | | Historical EELP | | | Pro Forma Excelerate |

Cash and cash equivalents: | | | $72,786 | | | $ |

Debt and finance leases: | | | | | ||

Debt facilities | | | 233,415 | | | |

Debt facilities – related party | | | 198,313 | | | |

Finance lease liabilities | | | 251,658 | | | |

Finance lease liabilities – related party | | | 226,619 | | | |

New credit facility | | | — | | | |

Total debt and finance leases: | | | $910,005 | | | |

Partners’ / stockholders’ equity: | | | | | ||

Equity interest | | | 1,135,769 | | | |

Related party note receivable | | | (6,759) | | | |

Accumulated other comprehensive loss | | | (9,178) | | | |

Retained Earnings | | | — | | | |

Non-controlling interest | | | 14,376 | | | |

Non-controlling interest – ENE Onshore | | | (130,282) | | | |

Class A common stock (no shares authorized, issued and outstanding, actual; shares authorized, shares issued and outstanding, pro forma) | | | — | | | |

Class B common stock (no shares authorized, issued and outstanding, actual; shares authorized, shares issued and outstanding, pro forma) | | | — | | | |

Additional paid-in capital | | | — | | | |

Total consolidated partners’ / stockholders’ equity: | | | 1,003,926 | | | |

Total capitalization: | | | $1,913,931 | | | $ |

(in thousands) | | | |

Pro forma tangible assets | | | $ |

Pro forma liabilities | | | |

Pro forma net tangible book value after this offering | | | $ |

Less: | | | |

Proceeds from offering net of underwriting discounts | | | |

Offering expenses | | | |

Pro forma net tangible book value as of December 31, 2021 | | | $ |

Assumed initial public offering price per share | | | | | $ | |

Pro forma net tangible book value per share as of December 31, 2021 | | | $ | | | |

Increase in pro forma net tangible book value per share attributable to new investors | | | $ | | | |

Pro forma net tangible book value per share after the offering | | | | | $ | |

Dilution in pro forma net tangible book value per share to new investors | | | | | $ |

| | | Shares purchased(1) | | | Total consideration(2) | | | Average price per share | |||||||

| | | Number | | | % | | | Number | | | % | | |||

Existing stockholders | | | | | % | | | (3) | | | % | | | $ | |

New investors(4) | | | | | % | | | | | % | | | $ | ||

Total | | | | | 100% | | | $ | | | 100% | | | $ | |

(1) | If the underwriters exercise their option to purchase additional shares in full, our existing stockholders would own approximately % and our new investors would own approximately % of the total number of shares of our Class A common stock outstanding after this offering. |

(2) | If the underwriters exercise their option to purchase additional shares in full, the total consideration paid by our new investors would be approximately $ (or %). |

(3) | Existing stockholder past contributions to EELP not included. |

(4) | Reflects the issuance to Maya Maritime LLC of shares of Class A common stock (assuming a public offering price equal to the midpoint of the price range set forth on the cover of this prospectus), which serves as a portion of the consideration for EELP's acquisition of the Foundation Vessels. |

• | the Reorganization as described in “Organizational Structure”; |

• | the acquisition of the Foundation Vessels; |

• | the intended use of proceeds from this offering as described in “Use of Proceeds”; |

• | the Tax Receivable Agreement as described in the “Organizational Structure” and “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate—Tax Receivable Agreement” sections in this prospectus; |

• | the issuance of shares of our Class A common stock to the investors in this offering in exchange for net proceeds of approximately $ (based on an assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus), after deducting underwriting discounts and commissions but before offering expenses; |

• | the payment of fees and expenses related to this offering and the application of the net proceeds from the sale of Class A common stock in this offering to purchase Class A interests directly from EELP, at a purchase price per Class A interest equal to the initial public offering price per share of Class A common stock less the underwriting discount, with such Class A interests representing % of the outstanding interests of EELP; and |

• | the provision for corporate income taxes on the balance sheet and income statement of Excelerate that will be taxable as a corporation for U.S. federal and state income tax purposes. |

| | | | | Transaction Adjustments | | | |||||||||

| | | EELP Historical Consolidated | | | Vessel Acquisition Adjustments | | | Reorganization Adjustments | | | Offering Adjustments | | | Excelerate Condensed Consolidated | |

| | | (in thousands) | |||||||||||||

Assets | | | | | | | | | | | |||||

Current assets | | | | | | | | | | | |||||

Cash and cash equivalents | | | $72,786 | | | (2) | | | | | (9) | | | $ | |

Current portion of restricted cash | | | 2,495 | | | | | | | | | ||||

Accounts receivable, net | | | 260,535 | | | | | | | | | ||||

Accounts receivable, net – related-party | | | 11,140 | | | | | | | | | ||||

Inventories | | | 105,020 | | | | | | | | | ||||

Current portion of net investments in sales-type leases | | | 12,225 | | | | | | | | | ||||

Other current assets | | | 26,194 | | | (1) | | | | | (11) | | | ||

Total current assets | | | 490,395 | | | | | | | | | ||||

Restricted cash | | | 15,683 | | | | | | | | | ||||

Property and equipment, net | | | 1,433,169 | | | (2) | | | | | | | |||

Operating lease right-of-use assets | | | 106,225 | | | | | | | | | ||||

Net investments in sales-type leases | | | 412,908 | | | | | | | | | ||||

Investment in equity method investee | | | 22,051 | | | | | | | | | ||||

Deferred tax assets | | | — | | | (3) | | | (7)(10) | | | | | ||

Other assets | | | 20,305 | | | (1) | | | | | | | |||

Total assets | | | $2,500,736 | | | | | | | | | ||||

Liabilities and Stockholders’ Equity | | | | | | | | | | | |||||

Current liabilities | | | | | | | | | | | |||||

Accounts payable | | | $303,651 | | | | | | | | | ||||

Accounts payable to related party | | | 7,937 | | | | | | | | | ||||

Accrued liabilities and other liabilities | | | 105,034 | | | | | | | | | ||||

Deferred revenue | | | 9,653 | | | (1) | | | | | | | |||

Current portion of long-term debt | | | 19,046 | | | | | | | | | ||||

Current portion of long-term debt – related party | | | 7,096 | | | | | | | | | ||||

Current portion of operating lease liabilities | | | 30,215 | | | | | | | | | ||||

Current portion of finance lease liabilities | | | 21,903 | | | | | | | | | ||||

Current portion of finance lease liabilities – related party | | | 15,627 | | | (4) | | | | | | | |||

Total current liabilities | | | 520,162 | | | | | | | | | ||||

Derivative liabilities | | | 2,999 | | | | | | | | | ||||

Long-term debt, net | | | 214,369 | | | | | | | | | ||||

Long-term debt, net – related party | | | 191,217 | | | | | | | | | ||||

Operating lease liabilities | | | 77,936 | | | | | | | | | ||||

Finance lease liabilities | | | 229,755 | | | | | | | | | ||||

Finance lease liabilities – related party | | | 210,992 | | | (4) | | | | | | | |||

TRA liability | | | — | | | (3) | | | (7)(10) | | | | | ||

Asset retirement obligations | | | 34,929 | | | | | | | | | ||||

Other long-term liabilities | | | 14,451 | | | | | | | | | ||||

Total liabilities | | | 1,496,810 | | | | | | | | | ||||

Partners’ / stockholders’ equity | | | | | | | | | | | |||||

Class A common stock, $0.001 par value | | | — | | | (5) | | | | | (9) | | | ||

Class B common stock, $0.001 par value | | | — | | | | | (7)(8) | | | | | |||

| | | | | | | | | | | ||||||

Additional paid in capital | | | — | | | (3)(5)(6) | | | (6)(7) | | | (9)(11) | | | |

Equity interest | | | 1,135,769 | | | | | (8) | | | | | |||

Related party note receivable | | | (6,759) | | | | | | | | | ||||

Accumulated other comprehensive loss | | | (9,178) | | | | | | | | | ||||

Retained Earnings | | | | | (2) | | | | | | | ||||

Non-controlling interest | | | 14,376 | | | | | (8) | | | | | |||

| | | | | | | | | | | ||||||

Non-controlling interest – ENE Onshore | | | (130,282) | | | | | | | | | ||||

Total equity | | | 1,003,926 | | | | | | | | | ||||

Total liabilities and equity | | | $2,500,736 | | | | | | | | | ||||

| | | | | Transaction Adjustments | | | |||||||||

| | | EELP Historical Consolidated | | | Vessel Acquisition Adjustments | | | Reorganization Adjustments | | | Offering Adjustments | | | Excelerate Condensed Consolidated | |

| | | (in thousands) | |||||||||||||

Revenues | | | | | | | | | | | |||||

FSRU and terminal services | | | $468,030 | | | | | | | | | ||||

Gas Sales | | | 420,525 | | | | | | | | | ||||

Total revenues | | | 888,555 | | | | | | | | | ||||

Operating expenses | | | | | | | | | | | |||||

Cost of revenue and vessel operating expense | | | 192,723 | | | (1) | | | | | | | |||

Direct cost of gas sales | | | 390,518 | | | | | | | | | ||||

Depreciation and amortization | | | 104,908 | | | (2) | | | | | | | |||

Selling, general, and administrative expenses | | | 47,088 | | | | | | | | | ||||

Restructuring, transition and transaction expenses | | | 13,974 | | | | | | | | | ||||

Total operating expenses | | | 749,211 | | | | | | | | | ||||

Operating income | | | 139,344 | | | | | | | | | ||||

Other income (expense) | | | | | | | | | | | |||||

Interest expense, net | | | (31,892) | | | | | | | | | ||||

Interest expense – related party | | | (48,922) | | | (3) | | | | | | | |||

Earnings from equity-method investment | | | 3,263 | | | | | | | | | ||||

Other income, net | | | 564 | | | | | | | | | ||||

Income before income taxes | | | 62,357 | | | | | | | | | ||||

Provision for income taxes | | | (21,168) | | | (4) | | | (4) | | | | | ||

Net income | | | 41,189 | | | | | | | | | ||||

Less net income attributable to non-controlling interest | | | 3,035 | | | (5) | | | (5) | | | | | ||

Less net income attributable to non-controlling interest – ENE Onshore | | | (2,964) | | | | | | | | | ||||

Net income attributable to partners | | | $41,118 | | | | | | | | | ||||

Pro forma earnings per share (basic and diluted) | | | | | | | | | (7) | | | $ | |||

Pro forma weighted-average shares outstanding (basic and diluted) | | | | | | | | | (7) | | | ||||

(1) | This reflects the netting down of deferred revenue with lease prepayments along with the removal of prepaid drydocking costs between the Foundation and EELP as it relates to the Foundation Vessels. Upon acquisition of these vessels, any remaining deferred revenue will be net against lease prepayments and prepaid drydocking costs (net of tax) will be removed and included in the loss on acquisition on the Foundation Vessels since these prepaid drydocking costs were considered in the purchase price paid to the Foundation. On a pro forma basis as of December 31, 2021, this loss is expected to be $ and be recognized on our income statement upon the completion of this offering. |

(2) | Reflects the net impact to property and equipment, net for the acquisition of the Excelsior vessel. This includes the removal of the historical right-of-use asset and related accumulated amortization and recognizes the new basis of $ million as an owned vessel. The new basis for the owned asset represents historical basis of the asset plus the difference between the preliminary fair value of all consideration transferred for acquisition less the lease liability relieved. The pro forma adjustments included in this unaudited pro forma condensed consolidated financial information are subject to modification as additional information becomes available and as additional analyses are performed depending on changes in the final fair value determination of the assets acquired and liabilities assumed as part of the Vessel Acquisition. The final allocation of the total consideration transferred will be determined as of the Vessel Acquisition date. The total consideration includes approximately $ million of cash, $ of Class A Common Stock (based on an assumed initial public offering price of $ per share, the midpoint of the price range set forth on the cover page of this prospectus), and $ million of contingent consideration related to the Tax Receivable Agreement. |

(3) | As described in greater detail under “Organizational Structure” and “Certain Relationships and Related Person Transactions—Proposed Transactions with Excelerate—Tax Receivable Agreement,” in connection with the |

(4) | In relation to the acquisition of the Foundation Vessels, which are expected to be completed in connection with this offering, these adjustments reflect the removal of the related current and non-current finance lease liabilities as reported in the historical consolidated financial statements of EELP. |

(5) | Reflects the issuance of $ million of Class A Common Stock, which serves as consideration for the acquisition of the Foundation Vessels. This consideration represents $ million for the acquisition of Excellence, and $ million for the acquisition of Excelsior. |

(6) | The computation of pro forma additional paid-in capital is set forth below: |

($ in thousands) | | | Vessel Acquisition Adjustments | | | Reorganization Adjustments | | | Offering Adjustments |

Proceeds from offering net of underwriting discounts and offering expenses | | | | | | | |||

Transaction costs incurred prior to this offering deferred as prepaid expenses and other current assets | | | | | | | |||

Purchase of Foundation Vessels | | | | | | | |||

Deferred tax impact of becoming a taxable Corporation | | | | | | | |||

Tax Receivable Agreement | | | | | | | |||

Additional paid-in capital | | | | | | |

(7) | The Tax Receivable Agreement will provide for the payment by Excelerate to EE Holdings of 85% of the amount of the net cash tax savings, if any, that Excelerate realizes, or under certain circumstances is deemed to realize, resulting from (i) certain increases in the tax basis of assets of EELP and its subsidiaries resulting from exchanges of EELP partnership interests in the future, (ii) certain tax attributes of EELP and subsidiaries of EELP that exist as of the time of this offering or may exist at the time when Class B interests of EELP are exchanged for shares of Class A common stock and (iii) certain other tax benefits related to Excelerate entering into the Tax Receivable Agreement, including tax benefits attributable to payments that Excelerate makes under the Tax Receivable Agreement. |

(8) | Upon completion of the Transactions, we will become (or wholly own) the general partner of EELP. Although initially we will have a minority economic interest in EELP, we will have the majority voting interest in, and control of the management of, EELP. As a result, we will consolidate the financial results of EELP and will report non-controlling interests related to the interests in EELP held by the other partners of EELP on our consolidated balance sheet. Immediately following the Transactions, the economic interests held by the non-controlling interests will be approximately %. If the underwriters were to exercise their option to purchase additional shares of our Class A common stock in full, the economic interests held by the non-controlling interests would be approximately %. Through its ownership of shares of Class B common stock, EE Holdings will control a majority of the voting power of the common stock of Excelerate, the general partner of EELP (or the sole owner of the general partner of EELP), and will therefore have indirect control over EELP. |

(9) | Reflects the net effect on cash of the receipt of offering proceeds to us of $ , based on the sale of shares of Class A common stock at an assumed initial public offering price of $ per share of Class A common stock (the midpoint of the price range set forth on the cover of this prospectus), after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

(10) | Due to the uncertainty in the amount and timing of future exchanges of EELP Class B interests into shares of our Class A common stock by the other partners of EELP, and the uncertainty of when those exchanges will |

(11) | Reflects deferred costs associated with this offering, including certain legal, accounting and other related costs, which have been recorded in prepaid expenses and other current assets on the consolidated balance sheet. Upon completion of this offering, these deferred costs will be charged against the proceeds from this offering with a corresponding reduction to additional paid-in capital. |

(1) | This amount reflects the incremental operating costs associated with owning the Foundation Vessels during the year ended December 31, 2021, as if the vessels had been acquired on January 1, 2021. These incremental operating costs reflect the historical difference between actual expenses incurred by the Foundation in operating the Foundation Vessels and the fixed fee that EELP paid to the Foundation for this period for operating the Foundation Vessels. |

(2) | Reflects the net impact to depreciation expense as it relates to the acquisition of Excelsior. The unaudited pro forma condensed consolidated statement of income gives effect to the acquisition of Excelsior as if it had occurred as of January 1, 2021. The amortization expense previously recorded for Excelsior for the year ended December 31, 2021 was approximately $ million based on the historical carrying value of the right of use asset. As an owned asset, the new depreciation amount of $ for the year ended December 31, 2021 is based on the purchase price of Excelsior. |

(3) | Reflects the removal of the interest expense incurred during the year ended December 31, 2021 related to the Foundation Vessels which were historically accounted for as finance leases. The unaudited pro forma condensed consolidated statement of income gives effect to the acquisition of Excelsior as if it had occurred as of January 1, 2021 and therefore no interest expense would have been incurred during this period in relation to these assets. |