UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________

FORM 20-F

___________________________

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended | |||||

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Date of event requiring this shell company report. . . . . . . . . . . . . . . . . . .

Commission file number: 001-41327

___________________________

(Exact Name of Registrant as Specified in Its Charter)

___________________________

N/A

(Translation of Registrant’s Name Into English)

___________________________

(Jurisdiction of Incorporation or Organization)

___________________________

(Address of Principal Executive Offices)

Telephone: +886 -3-273 0900

Email: ir@gogoro.com

(Name, Telephone, Email and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class | Trading Symbol(s) | Name of Each Exchange On Which Registered | ||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

1

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

As of December 31, 2022, there were 244,211,643 Ordinary shares outstanding, par value US$0.0001 per share,

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

o Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. o Yes x No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | ||||||||

x | Emerging growth company | ||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. § 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| o | U.S. GAAP | x | o | Other | |||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. o Item 17 o Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o Yes x No

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. o Yes o No

2

Table of Contents

E. Critical Accounting Estimates | |||||

3

4

INTRODUCTION

Unless otherwise indicated or the context otherwise requires, all references in this annual report on Form 20-F to the terms “Gogoro,” the “Company,” “we,” “us” and “our” refer to Gogoro Inc., a Cayman Islands exempted holding company, together as a group with its subsidiaries, including its Operating Subsidiaries.

Our consolidated financial statements are presented in U.S. dollars. All references in this annual report to “$,” “U.S. $,” “U.S. dollars” and “dollars” mean U.S. dollars, unless otherwise noted.

Gogoro completed a merger with Poema Global Holdings. Corp on April 4, 2022 and Gogoro’s ordinary shares began trading on the Nasdaq Stock Exchange on April 5, 2022. Poema Global Holdings Corp., an exempted company incorporated with limited liability under the laws of Cayman Islands (“Poema”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Gogoro and the other two entities established for the purpose of effecting the mergers under the Merger Agreement (the “Mergers”).

In this annual report on Form 20-F, or this annual report, except where the context otherwise requires and for purposes of this annual report only:

▪“Business Combination” refers to the transactions contemplated under the Merger Agreement;

▪“Cayman Companies Act” refers to the Companies Act (As Revised) of the Cayman Islands;

▪“Exchange Act” refer to the Securities Exchange Act of 1934, as amended;

▪“Gogoro” refers to Gogoro Inc., a Cayman Islands exempted holding company, together as a group with its subsidiaries, including its Operating Subsidiaries;

▪“Gogoro Ordinary Shares” refers to the ordinary shares of Gogoro, par value $0.0001 per share, which trade on the Nasdaq under the ticker symbol “GGR”;

▪“GoStation®” refers to Gogoro Battery Swapping Stations;

▪“IASB” refer to International Accounting Standards Board;

▪“ICE” refers to internal combustion engine;

▪“IFRS” refers to the International Financial Reporting Standards;

▪“Merger Agreement” refers to the Agreement and Plan of Merger, dated as of September 16, 2021 and amended as of March 21, 2022, by and among Poema Global, Gogoro, Starship Merger Sub I Limited, a wholly-owned subsidiary of Gogoro, and Starship Merger Sub II Limited, a wholly-owned subsidiary of Gogoro;

▪“Nasdaq” refers to the Nasdaq Global Select Market;

▪“NTD” refers to New Taiwan dollar;

▪“OEM” refers to original equipment manufacturer;

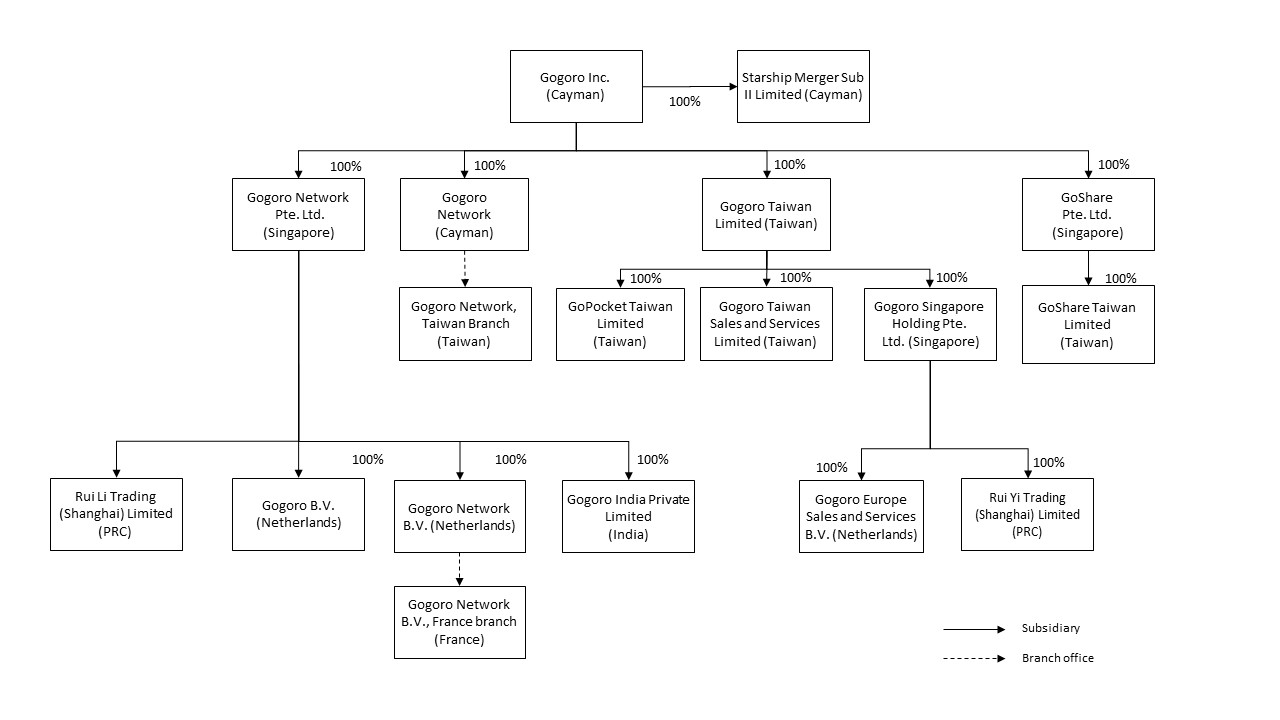

▪“Operating Subsidiaries” refers to collectively, the operating subsidiaries of Gogoro, which include Gogoro Taiwan Limited, Gogoro Taiwan Sales and Services Limited, Gogoro Network, Taiwan Branch, Gogoro Network Pte. Ltd., and GoShare Taiwan Limited;

▪“PBGN” refers to Powered by Gogoro Network™;

▪“PCAOB” refers to the Public Company Accounting Oversight Board;

▪“PIPE Investments” refers to the issuance of an aggregate of 29,482,000 Gogoro Ordinary Shares pursuant to the Subscription Agreements at a price per share of $10.00;

▪“Poema Global” refers to Poema Global Holdings Corp., a blank check Cayman Islands exempted company formed for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination;

▪“PTW/ePTW” refers to powered two-wheeler/electric-powered two-wheeler;

▪“PRC” refers to the People’s Republic of China;

▪“Public Warrants” refers to the redeemable warrants to purchase Gogoro Ordinary Shares for an exercise price of $11.50 per share, subject to adjustment, which trade on the Nasdaq under the ticker symbol “GGROW”;

▪“SEC” refers to the U.S. Securities and Exchange Commission;

▪“Securities Act” refers to the Securities Act of 1933, as amended;

▪“Subscription Agreements” refers to such subscription agreements entered into between Gogoro and certain investors on September 16, 2021, January 18, 2022 and March 21, 2022, relating to the PIPE Investments; and

▪“Warrants” refers to (i) Public Warrants and (ii) private placement warrants each entitles the holder thereof to purchase one Gogoro Ordinary Share for an exercise price of $11.50 per share, subject to adjustment.

1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This annual report contains forward-looking statements that reflect our current expectations and views of future events. These forward-looking statements are made under the “safe-harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. Known and unknown risks, uncertainties and other factors, including those listed under “Item 3. Key Information—D. Risk Factors,” may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from those expressed or implied by the forward-looking statements.

This annual report contains forward-looking statements that involve substantial risks and uncertainties. All statements other than statements of historical facts contained in this annual report, including statements regarding our future financial position, business strategy and plans and objectives of management for future operations, are forward-looking statements. In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar expressions. Forward-looking statements include, without limitation, our expectations concerning the outlook for our business, productivity, plans and goals for future operational improvements and capital investments, operational performance, future market conditions or economic performance and developments in the capital and credit markets and expected future financial performance.

Forward-looking statements involve a number of risks, uncertainties and assumptions, and actual results or events may differ materially from those projected or implied in those statements. Important factors that could cause such differences include, but are not limited to:

▪Our future financial and operating results, including forecasts, trends, expectations and market opportunity;

▪Growth of our business and operations and our ability to effectively manage our growth;

▪Our ability to launch and ramp up the production of our products and features, and our ability to control our manufacturing costs;

▪Our ability to expand our sales and marketing capabilities in order to increase our customer base and achieve broader market acceptance of our solutions;

▪Our dependence on a limited number of vendors, suppliers and manufacturers;

▪Our ability to expand effectively into new markets, including India, Indonesia and PRC, including the timing and estimates on the number of cities we will expand to;

▪Successful acquisitions of new businesses, products or technologies, or entering into strategic collaborations alliances or joint ventures in Taiwan and internationally,

▪Our ability to develop and maintain relationships with our partners, including our OEM partners;

▪Significant risks associated with construction, cost overruns and delays, and other contingencies that may arise in the course of completing installations, and such risks may increase in the future as we expand the scope of such services with other parties;

▪Increases in costs, disruption of supply or shortage of materials, in particular for lithium-ion cells and metals, including as a result of inflation;

▪Our ability to offer high-quality support to the battery swapping stations and station suppliers, or failure to maintain strong user experience;

▪The impacts of service disruptions, outages, errors and performance problems in any of our products;

▪The impact of health pandemics, including the COVID-19 pandemic;

▪The ability of our products and services to successfully compete with a growing list of established and new competitors;

▪Changes to fuel economy standards or the success of alternative fuels;

▪Our ability to continue to develop new products and product innovations to adapt to the rapid technological change that characterizes the ePTW market;

▪Our ability to continue to grow the number of incremental battery swapping subscribers and cumulative battery swapping subscribers;

▪Our ability to successfully implement the pilot programs intended to extend the life of our battery packs beyond use in ePTWs and to create additional revenue streams in the future;

▪Our ability to protect our technology and intellectual property from unauthorized use by third parties;

▪Our expectations about entering into definitive agreements with our partners;

▪Our exposure to fluctuations in currency exchange rates.

▪The legal, regulatory and financial challenges that we may face with conducting business through subsidiaries in Taiwan and international markets; and

▪The other matters described in the section titled “Item 3. Key Information—D. Risk Factors” in this annual report.

2

We caution you against placing undue reliance on forward-looking statements, which reflect current beliefs and are based on information currently available as of the date a forward-looking statement is made. Forward-looking statements set forth herein speak only as of the date of this annual report. We undertake no obligation to revise forward-looking statements to reflect future events, changes in circumstances, or changes in beliefs. In the event that any forward-looking statement is updated, no inference should be made that we will make additional updates with respect to that statement, related matters, or any other forward-looking statements. Any corrections or revisions and other important assumptions and factors that could cause actual results to differ materially from forward-looking statements, including discussions of significant risk factors, may appear in our public filings with the SEC, which are or will be (as appropriate) accessible at www.sec.gov, and which you are advised to consult.

Market, ranking and industry data used throughout this annual report, including statements regarding market size, is based on the good faith estimates of our management, which in turn are based upon our management’s review of internal surveys, independent industry surveys and publications, and other third-party research and publicly available information. These data involve a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. While we are not aware of any misstatements regarding the industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Item 3. Key Information—D. Risk Factors” and “Item 5. Operating and Financial Review and Prospects” in this annual report.

3

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Summary Risk Factors

The below summary risks provide an overview of the material risks we are exposed to in the normal course of our business activities. The below summary risks do not contain all of the information that may be important to you, and you should read the summary risks below together with the more detailed discussion of risks set forth following this section under the heading “Risk Factors,” as well as elsewhere in this annual report. The summary risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not currently known to us or that we currently deem less significant may also affect our business operations or financial results. Consistent with the foregoing, we are exposed to a variety of risks, including those associated with the following:

▪We have incurred operating losses historically and expect to incur significant expenses and continuing losses at least for the near and medium term.

▪Our expectations for future operating and financial results are subject to significant uncertainty and are based on assumptions, analyses and internal estimates developed by management, any or all of which may not prove to be correct or accurate. If these assumptions, analyses or estimates prove to be incorrect or inaccurate, our actual operating results may differ materially and adversely from our anticipated results.

▪Our future success depends on our success in expanding our sales in both Taiwan and into other geographic markets. We may attempt to enter into strategic collaborations or alliances, including forming partnerships or joint ventures, and if we are unsuccessful in such strategic collaborations or alliances, we may fail to realize expected benefits from such transactions or such transactions could harm our existing business.

▪If we fail to execute our growth strategy or manage growth effectively, our business, financial condition and results of operations would be adversely affected.

▪If we fail to expand effectively into new product or technology markets, our revenues and business may be negatively affected.

▪Our financial results may vary significantly from period to period due to fluctuations in our operating costs or expenses and other foreseeable or unforeseeable factors.

▪Our business is subject to risk associated with product design and manufacturing quality for our existing products including vehicles, battery packs, battery swapping stations, ride-share vehicles, and other products and may also be negatively impacted by product quality in the future.

▪Our business is subject to risks associated with construction, cost overruns and delays, and other contingencies that may arise in the course of completing installations, and such risks may increase in the future as we expand the scope of such services with other parties.

▪Due to the complexity of our manufacturing operations, we are not always able to timely respond to fluctuations in demand and we may incur significant charges and costs.

▪We rely on a limited number of vendors, suppliers and manufacturers. A loss of any of these partners could negatively affect our business, or they may fail to deliver components according to schedules, prices, quality and volumes that are acceptable to us, or we may be unable to manage these components effectively.

▪We may experience delays in launching and ramping the production of our products and features, or we may be unable to control our manufacturing costs.

▪Failure to effectively expand our sales and marketing capabilities could harm our ability to increase our customer base and achieve broader market acceptance of our solutions.

4

▪Our success depends on the ability to develop and maintain relationships with our partners, including our OEM partners, manufacturing partners and demand generation partners.

▪We may be unable to retain our key personnel and attract additional qualified personnel to operate and expand our business.

▪We may need to raise additional funds and these funds may not be available when needed or may be available only on unfavorable terms.

▪We are exposed to fluctuations in currency exchange rates.

▪We face strong competition for our products and services from a growing list of established and new competitors.

▪Failure to successfully develop and manage a B2B business model and markets may negatively impact our results of operations.

▪Changes to fuel economy standards or the success of alternative fuels may negatively impact the ePTW market and thus the demand for our products and services.

▪Our growth and success are highly correlated with and thus dependent upon the continuing rapid adoption of and demand for ePTWs and battery swapping services.

▪The ePTW markets are characterized by rapid technological change, which requires us to continue to develop new products and product innovations. Any delays in such development could adversely affect market adoption of our products and our financial results.

▪Our business may be adversely affected if we are unable to protect our technology and intellectual property from unauthorized use by third parties.

▪Our business may be adversely affected by the changes of governmental policy and subsidy program in Taiwan or international electric scooters markets.

▪Our Taiwan subsidiaries bear product liabilities for damages caused by our products under Taiwan regulations on consumer protection. In other markets we may also be exposed to product liability risks.

▪A downturn in global economy, and economic and political policies of the relevant markets could materially and adversely affect our business operations such markets.

▪Uncertainties in the interpretation and enforcement of the applicable laws and regulations in the relevant markets could limit the legal protections available to us and our security holders.

▪Our business, financial condition and results of operations, and/or the value of our securities or our ability to offer or continue to offer securities to investors may be materially and adversely affected to the extent the government of the relevant markets intervenes in or influences our operations.

In addition to the other information contained in this annual report, we have identified the following risks and uncertainties that may have a material adverse effect on our business, financial condition, or results of operation. Investors should carefully consider the risks described below together with all of the other information in this annual report, including our consolidated financial statements and related notes thereto included elsewhere in this annual report and in our other filings with the SEC, before making an investment decision. The trading price of our securities could decline due to any of these risks, and investors may lose all or part of their investment. In this section, unless the context otherwise requires, “Gogoro,” “we,” “us” and “our” refer to Gogoro Inc., a Cayman Islands exempted holding company, together as a group with its subsidiaries including the Operating Subsidiaries.

Risks Related to Our Business

We have incurred operating losses historically and expect to incur significant expenses and continuing losses at least for the near and medium term.

We have a history of operating losses and negative operating cash flows. We incurred a net loss of $98.9 million, $67.4 million and $49.3 million for the year ended December 31, 2022, 2021 and 2020, respectively, and, as of December 31, 2022, our accumulated deficits was approximately $349.9 million. We believe we will continue to incur operating and net losses each quarter in the foreseeable future. Even if we achieve profitability, there can be no assurance that we will be able to maintain profitability in the future. Our potential profitability is particularly dependent upon the continued adoption of electric vehicles (“EVs”) and ePTWs by consumers and other electric transportation modalities, continued support from regulatory programs and in each case, the use of our battery swapping technology, any of which may not occur at the levels we currently anticipate or at all. We may need to raise additional financing through loans, securities offerings, or additional investments in order to fund our ongoing operations. There is no assurance that we will be able to obtain such additional financing or that we will be able to obtain such additional financing on favorable terms. Our forecasts and projections are based upon assumptions, analyses and internal estimates developed by management. If these assumptions, analyses, or estimates prove to be incorrect or inaccurate, our actual operating results may differ materially and adversely from those forecasted or projected.

Our expectations for future operating and financial results are subject to significant uncertainty and are based on assumptions, analyses and internal estimates developed by management, any or all of which may not prove to be correct or accurate. If these assumptions, analyses or estimates prove to be incorrect or inaccurate, our actual operating results may differ materially and adversely from our anticipated results.

5

Our expectations for our future operating and financial results depend on the successful implementation of our proposed business plan, and policies and procedures consistent with the assumptions. Future results will also be affected by events and circumstances beyond our control, for example, the competitive environment, rapid technological change, economic and other conditions in the markets in which we operate or seek to enter, governmental regulation and, uncertainties inherent in product development and testing, our future financing needs and our ability to grow and to manage growth effectively, our executive team, and other factors described under the section entitled “Cautionary Statement Regarding Forward-Looking Information” in this annual report. In particular, our forecasts and projections include forecasts and estimates relating to the expected size and growth of the markets in which we operate or seek to enter. Our forecasts and projections also assume that we are able to perform our obligations under our commercial contracts. For the reasons described above, it is likely that our actual results of operations will be different from our expectations and we may be required to make adjustments in our business operations that may have a material adverse effect on our financial condition and results of operations. For example, we were unable to achieve the projected financial results set at the beginning of the year in 2022. We cannot assure you that we will be able to achieve our expectations in the future.

Our future success depends on our success in expanding into other geographic markets. We may attempt to enter into strategic collaborations or alliances, including forming partnerships or joint ventures, and if we are unsuccessful in such strategic collaborations or alliances, we may fail to realize expected benefits from such transactions or such transactions could harm our existing business.

Our success will depend, in part, on our ability to expand our product offerings and grow our business by ourselves or through local partners in response to changing technologies, customer demands and competitive pressures. For example, in addition to the collaboration we started in 2021 with Yadea Technology Group Co. Ltd. (“Yadea”) and Dachangjiang Group Co., Ltd. (“DCJ”) to expand in the PRC, Hero MotoCorp (“Hero”) in India, GoTo in Indonesia, and Foxconn as a global manufacturing partner, we also entered into a strategic partnership with Zypp, India's leading EV-as-a-Service platform in November 2022 and signed Memorandum of Understanding for a strategic energy partnership with the Indian State of Maharashtra and Belrise Industries in January 2023 to further expand our presence in the Indian market. Furthermore, we partnered with Jardine Cycle & Carriage (SGX: C07), a diversified group with market-leading businesses across Southeast Asia to kick-off our sandbox pilot to deploy and validate battery swapping as awarded by Singapore's Land Transport Authority. We also partnered with Metro Motor and Paz Group to launch of our industry leading battery swapping system and Smartscooters in the Tel Aviv metropolitan area. Our success is highly reliant on local partners’ successful performance and such local partners may not perform as they expect due to various reasons or factors including the product price or business model and any failure of performance may impact significantly on our success. In some circumstances, we may determine to do so through collaborating with complementary businesses, including forming joint ventures, rather than through internal development. The identification of suitable alliance and joint venture partner candidates can be difficult, time consuming, and costly, and we may not be able to successfully complete identified alliances or joint ventures. Other companies may compete with us for these strategic opportunities. In addition, even if we successfully complete an alliance or joint venture, we may not be able to timely and effectively commence operations of any joint venture or other alliance because the process of integration could be expensive, time consuming and may strain our resources. Furthermore, we may be required to contribute significant amounts of capital or incur losses in the initial stages of an alliance or joint venture, particularly as selling and marketing activities increase ahead of expected long-term revenue. For example, capital contributions to a joint venture may be necessary in the future if we expands our operations in the geographic market that we wish to expand into in order to achieve our long-term strategy in such locations. In addition, the process for customers of the alliance or joint venture to comply with local or foreign regulatory requirements that may be required to purchase our products may cause delays in the alliance partner or joint venture’s ability to conduct business. Furthermore, the products and technologies that we jointly develop, or with respect to which we collaborate, may not be successful or may require significantly greater resources and investments than we originally anticipated. For example, as of the date of this annual report, we had not been able to generate satisfactory results from our collaborations with partners in mainland China, such as Yadea and DCJ. Implementing new lines of business or offering new products and services within existing lines of business can affect the sales and profitability of existing lines of business or products and services, including as a result of sales channel conflicts. In addition, we may not be in a position to exercise sole decision-making authority regarding any strategic collaboration, alliance or joint venture, which could result in impasses on decisions or decisions made by our partners, and our partners in such collaborations, alliances or joint ventures may have economic or business interests that are, or may become, inconsistent with our interests. Furthermore, we may adjust our business strategies in different geographic markets from time to time based on the latest development in such market, which may also require significant amounts of capital or incur losses and may strain our resources.

Collaborations, alliances and joint ventures can be difficult to manage and may involve significant expense and divert the focus and attention of our management and other key personnel away from our existing businesses. With respect to joint ventures, we may not be able to attract qualified employees, acquire customers or develop reliable supply, distribution or other partnerships. As a result of certain collaborations, alliances and joint ventures we could face potential damage to existing customer relationships or lack of customer acceptance or inability to attract new customers. These risks could be magnified to the extent that any new collaboration, alliance or joint venture would result in a significant increase in operations in developing markets. Future alliances could also result in potentially dilutive issuances of equity securities or the incurrence of debt, contingent liabilities, or expenses or other charges such as in-process research and development, any of which could harm our business and affect our financial results or cause a reduction in the price of Gogoro Ordinary Shares. Further, alliance partners and joint ventures may also operate in foreign jurisdictions with laws and regulations with which we have limited familiarity, which could adversely impact our ability to comply with such laws and regulations and may lead to increased litigation risk. Such laws may also offer us inadequate or less intellectual property protection relative to U.S. laws, which may impact our ability, as well as the ability of the alliance partner and joint venture, to safeguard our respective intellectual property from infringement and misappropriation. As a result of these and other factors, we may not realize the expected benefits of any

6

collaboration, joint venture or strategic alliance or such benefits may not be realized at expected levels or within the expected time period. The failure to successfully consummate such strategic transactions and effectively integrate and execute following such consummation may have an adverse impact on our growth, profitability, financial position and results of operations.

If we fail to execute growth strategy or manage growth effectively, our business, financial condition and results of operations would be adversely affected.

The expected continued growth and expansion of our business and execution of our growth strategy may place a significant strain on management, business operations, financial condition and infrastructure and corporate culture. With continued growth, our information technology systems and our internal control over financial reporting and procedures may not be adequate to support our operations and may allow data security incidents that may interrupt business operations and allow third parties to obtain unauthorized access to business information or misappropriate funds. We may also face risks to the extent such third parties infiltrate the information technology infrastructure of our contractors.

To manage growth in operations and personnel and execute our growth strategy, we will need to continue to improve our operational, financial and management controls and reporting systems and procedures. In addition, we may face difficulties as we expand our operations into new markets in which we have limited or no prior experience. See “—Our future success depends on our success in expanding into other geographic markets. We may attempt to enter into strategic collaborations or alliances, including forming joint ventures, and if we are unsuccessful in such strategic collaborations or alliances, we may fail to realize expected benefits from such transactions or such transactions could harm our existing business.” Failure to manage growth effectively could result in difficulty or delays in attracting new customers, declines in quality or customer satisfaction, increases in costs, difficulties in introducing new products and services or enhancing existing products and services, loss of customers, information security vulnerabilities or other operational difficulties, any of which could adversely affect our business performance and operating results. Our strategy is based on a combination of growth and maintenance of strong performance on our existing asset base, and any inability to scale, maintain customer experience or manage operations at our battery swapping stations may impact our growth trajectory.

If we fail to expand effectively into new product or technology markets, our revenues and business may be negatively affected.

The ePTW charging market and energy storage technology market are characterized by rapid technological change, which requires us to continue to develop new products and product innovations or shift our strategy, which is focused on the battery swapping and energy optimization on our customers’ sites and pursue new product and service offerings. We are, and intend in the future to continue, investing significant resources in developing new product and service offerings to address the changing needs in these markets. Our ability to continue to maintain our competitive position and grow our market share will depend on the successful development of our position in these markets. New partnerships and initiatives are inherently risky, as each involves unproven business strategies and new product offerings with which we have limited or no prior development or operating experience. Our success in new markets depends on a variety of factors, including but not limited to the success of our partnerships, our ability to develop new products, new product features and services that address the customer requirements for the relevant markets, to attract a customer base in markets in which we have less experience, to compete with new and existing competitors in these adjacent markets, and to gain market acceptance of our new products. Developing our products is expensive, and the investment in product development may involve a long or unmaterialized payback cycle. Difficulties in any of our new product development efforts or our efforts to enter adjacent markets could adversely affect our business, financial condition and results of operations.

In addition, as a result of our new product offerings, we could experience increased warranty claims, reputational damage or other adverse effects, which could be material. We also cannot provide assurance that we will be able to develop, obtain regulatory approval for, commercially market and/or achieve acceptance of our new product offerings.

Our research and development expenses were approximately $46.0 million, $30.6 million, and $28.7 million for the years ended December 31, 2022, 2021, and 2020, respectively, and are likely to grow in the future. However, our investment of resources to develop new product offerings may either be insufficient or may result in expenses that are excessive as compared to revenue produced from these new product offerings. Even if we are able to keep pace with changes in technology and develop new products and services, our research and development expenses could increase, our gross margins could be adversely affected and our prior products could become obsolete more quickly than expected.

Failure to accurately predict demand or growth with respect to our new product offerings could materially and adversely affect our business, financial condition, results of operations, and prospects, and there is always risk that these new product offerings will be unprofitable, will increase our costs or will decrease operating margins or take longer than anticipated to achieve target margins. We cannot guarantee that any new products will be released in a timely manner, or at all, or achieve market acceptance. Delays in delivering new products that meet customer requirements could damage our relationships with customers and lead them to seek alternative providers. Delays in introducing products and innovations or the failure to offer innovative products or services at competitive prices may cause existing and potential customers to purchase our competitors’ products or services.

If we are unable to devote adequate resources to develop products or cannot otherwise successfully develop products or services that meet customer requirements on a timely basis or that remain competitive with technological alternatives, our products and services could lose market share, our revenue could decline, we may experience higher operating losses, and our business and prospects could be adversely affected. Further, our development efforts with respect to these initiatives could distract management from current operations

7

and could divert capital and other resources from our existing business. If we do not realize the expected benefits of our investments, our business, financial condition, results of operations, and prospects, could be materially and adversely affected.

Our financial results may vary significantly from period to period due to fluctuations in our operating costs or expenses and other foreseeable or unforeseeable factors.

We expect our period-to-period financial results to vary based on our operating costs, which we anticipate will fluctuate as a result of inflation and since the pace at which we design, develop and manufacture products and expand our manufacturing facilities may not be consistent or linear between periods. Additionally, our revenues from period to period may fluctuate due to macroeconomic volatility and other internal and external factors. However, we cannot assure you that we will not experience fluctuations in our operating results in the future due to factors we may or may not be able to foresee in the future.

Our business is subject to risk associated with product design and manufacturing quality for our existing products including vehicles, battery packs, battery swapping stations, ride-share vehicles, and other products and may also be negatively impacted by product quality in the future.

If our products contain design or manufacturing defects that cause them not to perform as expected or that require repair, are legally restricted or become subject to onerous regulation, our ability to develop, market and sell our products and services may be harmed, and we may experience delivery delays, product recalls, product liability, breach of warranty and consumer protection claims and significant warranty and other expenses.

Our products are also highly dependent on software, which is inherently complex and may contain latent defects or errors or be subject to external attacks. Although we attempt to remedy any issues we observe in our products as effectively and rapidly as possible, such efforts may not be timely, may hamper production or may not completely satisfy our customers. While we have performed, and continue to perform, extensive internal testing on our products and features, we currently have a limited frame of reference by which to evaluate their long-term quality, reliability, durability and performance characteristics. There can be no assurance that we will be able to detect and fix any defects in our products prior to their sale to or installation for customers.

Our business is subject to risks associated with construction, cost overruns and delays, and other contingencies that may arise in the course of completing installations, and such risks may increase in the future as we expand the scope of such services with other parties.

We do not typically install battery swapping stations at customer sites. These installations are typically performed by our partners or electrical contractors with an existing relationship with the customer and/ or knowledge of the site. The installation of battery swapping stations at a particular site is generally subject to oversight and regulation in accordance with state and local laws and ordinances relating to building codes, safety, environmental protection and related matters, and typically requires various local and other governmental approvals and permits that may vary by jurisdiction. In addition, building codes, accessibility requirements or regulations may hinder battery swapping site installation because they end up costing the developer or installer more in order to meet the code requirements. Meaningful delays or cost overruns may impact our recognition of revenue in certain cases and/or impact customer relationships, either of which could impact our business and profitability.

Furthermore, we may in the future elect to install battery swapping stations at customer sites or manage contractors, likely as part of offering customers a turnkey solution. Working with contractors may require us to obtain licenses or require us or our customers to comply with additional rules, working conditions and other union requirements, which can add costs and complexity to an installation project. In addition, if these contractors are unable to provide timely, thorough and quality installation-related services, customers could fall behind their construction schedules leading to liability to us or cause customers to become dissatisfied with the solutions we offer.

Due to the complexity of our manufacturing operations, we are not always able to timely respond to fluctuations in demand and we may incur significant charges and costs.

Because we own and operate scooter and battery manufacturing facilities, our operations have high costs that are fixed or difficult to reduce in the short term, including our costs related to utilization of existing facilities and equipment, facility construction and equipment, R&D, and the employment and training of a skilled workforce. To the extent product demand decreases or we fail to forecast demand accurately, our gross margin and operating income can be disproportionately affected due to our high fixed cost structure, which is difficult to reduce in response to lower revenues. We could also be required to write off inventory or record excess manufacturing capacity charges, which would also lower our gross margin and operating income. To the extent the demand decrease is prolonged, our manufacturing capacity could be underutilized, and we may be required to write down our long-lived assets, which would increase our expenses. We may also be required to shorten the useful lives of under-used facilities and equipment and accelerate depreciation. As we continue to make substantial investments in increasing our manufacturing capacity as part of our international growth strategy, these underutilization risks may be heightened. Conversely, at times, demand increases or we fail to forecast accurately or produce the mix of products demanded. To the extent we are unable to add capacity or increase production fast enough, we are at times required to make production decisions and/or are unable to fully meet market demand, which can result in a loss of revenue opportunities or market share, legal claims, and/or damage to customer relationships.

Our international investments in capacity and our product roadmap require capital expenditures above our historical levels, and if demand for our business grows rapidly, we anticipate that we would need to accelerate our planned investments to meet that demand. To

8

the extent we do not generate expected cash flows, we may be required to increase our use of external funding sources to fund our investments and operations, which may not be available on favorable terms or at all. To the extent such funding is below our expectations, our anticipated cash requirements would increase. Efforts to expand capacity require available sources of labor, materials, and equipment. Increasing demand for such sources, including from other manufacturers; supply constraints, labor shortages, and other adverse market conditions; issues with permits or approvals; on-site incidents; and other issues arise from time to time and can result in significant delays and increased costs for our projects, as well as legal and reputational harm.

We rely on a limited number of vendors, suppliers and manufacturers. A loss of any of these partners could negatively affect our business, or they may fail to deliver components according to schedules, prices, quality and volumes that are acceptable to us, or we may be unable to manage these components effectively.

We rely on a limited number of vendors and suppliers for design, testing and manufacturing of vehicles, battery packs, and battery swapping stations. At this stage of the industry these may be unique to each supplier and thus singularly sourced with respect to components as well as aftermarket maintenance and warranty services. This reliance on a limited number of manufacturers increases our risks, since it does not currently have proven reliable alternatives or replacement vendors or manufacturers beyond these key parties. In the event of production interruptions or supply chain disruptions including but not limited to availability of certain key components such as semiconductors, we may not be able to take advantage of increased production from other sources or develop alternate or secondary vendors without incurring material additional costs and substantial delays. Thus, our business could be adversely affected if one or more of our vendors or suppliers is impacted by any interruption at a particular location.

As the demand for battery swapping technology increases, the relevant equipment vendors may not be able to dedicate sufficient supply chain, production, or sales channel capacity to keep up with the required pace of battery swapping infrastructure expansion. In addition, as the ePTW market grows, the industry may be exposed to deteriorating design requirements, undetected faults or the erosion of testing standards by the relevant equipment and component suppliers, which may adversely impact the performance, reliability and lifecycle cost of the components in our battery swapping stations.

If we or our suppliers experience a significant increase in demand, or if we need to replace an existing supplier, we may not be able to supplement service or replace them on acceptable terms, which may undermine our ability to deliver products to customers in a timely manner. For example, it may take a significant amount of time to identify a vendor or manufacturer that has the capability and resources to supply battery swapping equipment in sufficient volume. Identifying and approving suitable vendors, suppliers and manufacturers could be an extensive process that requires us to become satisfied with their quality control, technical capabilities, responsiveness and service, financial stability, regulatory compliance, and labor and other ethical practices. Accordingly, a loss of any significant vendor, supplier or manufacturer would have an adverse effect on our business, financial condition and results of operations. In addition, our suppliers may face supply chain risks and constraints of their own, which may impact the availability and pricing of our products as well as our gross margins. For example, we have experienced and continue to experience shortages as well as increased costs for semiconductors.

We may experience delays in launching and ramping the production of our products and features, or we may be unable to control our manufacturing costs.

We have previously experienced and may in the future experience launch and production ramp delays for new products and features. In addition, we may introduce in the future new or unique manufacturing processes and design features for our products. There is no guarantee that we will be able to successfully and timely introduce and scale such processes or features.

In particular, our future business depends in large part on increasing the production of mass-market ePTWs. We have relatively limited experience to date in manufacturing ePTWs at high volumes and even less experience building and ramping production lines across multiple factories in different geographies. In order to be successful, we will need to implement, maintain and ramp efficient and cost-effective manufacturing capabilities, processes and supply chains and achieve necessary design tolerances, quality and output rates. We have planned to expand our production capacity in overseas markets through collaborations with local business partners. Bottlenecks and other unexpected challenges such as those we experienced in the past may arise during our production ramps, and we must address them promptly while continuing to improve manufacturing processes and reducing costs. If we are not successful in achieving these goals, we could face delays in establishing and/or sustaining our ePTW ramps or be unable to meet our related cost and profitability targets.

Any delay or other complication in ramping the production of our current products or the development, manufacture, launch and production ramp of our future products, features and services, or in doing so cost-effectively and with high quality, may harm our brand, business, prospects, financial condition and results of operations.

Failure to effectively expand our sales and marketing capabilities could harm our ability to increase our customer base and achieve broader market acceptance of our solutions.

Our ability to grow our customer base, achieve broader market acceptance, grow revenue, and achieve and sustain profitability will depend, to a significant extent, on our ability to effectively expand our sales and marketing operations and activities. We rely on our business development, sales and marketing teams to obtain new original equipment manufacturer (“OEM”) and grow our retail business, and on the technology, site development, and project management personnel to build out and serve new battery swapping stations. We

9

plan to continue to expand in these functional areas but we may not be able to recruit and hire a sufficient number of competent personnel with requisite skills, technical expertise and experience, which may adversely affect our ability to expand our sales capabilities. The hiring process can be costly and time-consuming, and new employees may require significant training and time before they achieve full productivity. Recent hires and planned hires may not become as productive as quickly as anticipated, and we may be unable to hire or retain sufficient numbers of qualified individuals. Our ability to achieve significant revenue growth in the future will depend, in large part, on our success in recruiting, training, incentivizing and retaining a sufficient number of qualified personnel attaining desired productivity levels within a reasonable time. Our business will be harmed if investment in personnel related to business development and related company activities does not generate a significant increase in revenue.

Our success depends on the ability to develop and maintain relationships with our partners, including our OEM partners, manufacturing partners and demand generation partners.

The success of our business depends on our ability to develop and maintain relationships with our partners, including our OEM partners, such as Aeon Motor and Yamaha Motor in Taiwan, Yadea and DCJ in the PRC, and Hero in India, manufacturing partners, such as Foxconn, and demand generation partners, such as GoTo in Indonesia and Zypp in India. These relationships help us access new customers and build brand awareness through co-marketing. In some cases, our partners have agreed to fund capital expenditures related to the build out of our battery swapping station network. If we fail to maintain or develop relationships with our partners, or if our partners opt to partner with competitors rather than us, our revenues may decline and our business may suffer.

There can be no certainty that we will be able to identify and contract with suitable additional partners. To the extent we do identify such partners, we will need to negotiate the terms of a commercial agreement with such partners. There can be no assurance that we will be able to negotiate commercially-attractive terms with additional partners, if at all. We may also be limited in negotiating future commercial agreements by the provisions of our existing contracts such as “most-favored nations” clauses.

Increases in costs, disruption of supply or shortage of materials, in particular for lithium-ion cells and metals, could harm our business.

We and our suppliers may experience increases in the cost of or a sustained interruption in the supply or shortage of materials. Any such increase, supply interruption or shortage could materially and negatively impact our business, prospects, financial condition and results of operations. We and our suppliers use various materials in our respective businesses and products, including for example lithium-ion battery cells and steel, and the prices for these materials fluctuate and may, together with other key components, increase significantly as a result of an increased electrification and demand for materials required to manufacture and assemble battery cells and ePTWs. The available supply of these materials may be unstable, depending on market conditions and global demand, including as a result of increased production of ePTWs by our competitors, and could adversely affect our business, financial condition and results of operations. For instance, we are exposed to multiple risks relating to lithium-ion battery cells. These risks include:

▪an increase in the cost, or decrease in the available supply, of materials used in the battery cells;

▪disruption in the supply of battery cells due to quality issues or recalls by battery cell manufacturers; and

▪fluctuations in the value of any foreign currencies in which battery cell and related raw material purchases are or may be denominated against the New Taiwan Dollar.

Our business is dependent on the continued supply of battery cells for the battery packs used in our ePTWs. Any disruption in the supply of battery cells from our suppliers could disrupt maintenance of our battery swapping stations and production of ePTWs. Furthermore, fluctuations or shortages in petroleum and other economic conditions, including increasing inflation have caused us to experience significant increases in freight charges and material costs. We have experienced a shortage in semiconductors and a shortage of semiconductors or other key components could cause a significant disruption to our production schedule. If we are unable to pre-purchase supply for semiconductors or other key components that may experience shortages, or if we cannot find other methods to mitigate the impact of any such shortage, then any such short shortage could have a substantial adverse effect on our financial condition or results of operations generally in the same manner, it could cause the same for other vehicle and ePTW manufacturers. Substantial increases in the prices for our materials or prices charged to us, such as those charged by suppliers of battery cells, semiconductors or other key components, have increased our operating costs, and could reduce our margins if the increased costs cannot be recouped through increased ePTW sales. Given the competitive nature of the markets in which we operate in, it is unlikely that increases in expenses can be passed on to customers. Any attempts to increase ePTW prices in response to increased material costs could result in cancellations of orders and reservations and therefore materially and adversely affect our brand, image, business, prospects, financial condition and results of operations. Thus, substantial increases in the prices for our materials or components would materially and adversely affect our business, increase our operating costs and negatively impact our prospects.

If we fail to offer high-quality support to the battery swapping stations and station suppliers, or experience system or hardware failure, or fail to maintain strong user experience, our business and reputation will suffer.

Once a customer has subscribed to our services, they will rely on us to provide support services to resolve any issues that might arise in the future. Rapid and high-quality customer support is important so drivers can receive reliable battery swapping services for their ePTWs. The importance of high-quality customer support will increase as we seek to expand our business and pursue new customers and geographies. Any failure to quickly resolve issues and provide effective support, or a market perception that we do not

10

maintain effective and responsive support, could adversely affect our brand and reputation, our ability to retain customers or sell additional products and services to existing customers, and our business, financial condition, and results of operations.

We may be unable to retain our key personnel and attract additional qualified personnel to operate and expand our business. If we are unable to attract and retain key personnel and hire qualified management, technical, engineering and sales personnel, our ability to compete and successfully grow our business would be harmed.

Our success depends largely on the skills, experience and performance of the members of our senior management and other key personnel. In particular, Mr. Horace Luke, our Chief Executive Officer and Chairman of the Board and Director, is critical to the management of our business and operations and the development of our strategic direction. The loss of the services of any of our key employees or any significant portion of our workforce could disrupt our operations or delay the development, introduction and ramp of our products and services. None of our key employees is bound by an employment agreement for any specific term and we may not be able to successfully attract and retain senior leadership necessary to grow our business. Our future success also depends upon our ability to attract, hire and retain a large number of engineering, manufacturing, marketing, sales and delivery, service, installation, technology and support personnel, especially to support our planned high-volume product sales, market and geographical expansion and technological innovations. Recruiting efforts, particularly for senior employees, may be time-consuming, which may delay the execution of our plans. If we are not successful in managing these risks, our business, financial condition and results of operations may be harmed.

Employees may leave us or choose other employers, including competitors,over us due to various factors, such as a very competitive labor market for talented individuals with automotive or technology experience, or any negative publicity related to us. In regions where we have or will have operations, particularly significant engineering and manufacturing centers, there is strong competition for individuals with skill sets needed for our business, including specialized knowledge of ePTWs, software engineering, manufacturing engineering and electrical and building construction expertise. We also compete with both mature and prosperous companies that have large financial resources and start-ups and emerging companies that promise short-term growth opportunities.

We expect to incur research and development costs and devote significant resources to developing new products, which could significantly reduce our profitability and may never result in revenue to us.

Our future growth depends on penetrating new markets, adapting existing products to new applications and customer requirements, and introducing new products that achieve market acceptance. For example, we have deployed a number of pilot programs in Taiwan which are intended to extend the life of our battery packs beyond use in ePTWs. We have begun the deployment of smart parking meters in New Taipei City, enabling New Taipei to embrace smart city technologies for their paid parking locations that are off the power grid and wirelessly connected. If we are unable to anticipate technological changes in the industry by introducing new or enhanced products and services in a timely and cost-effective manner, if we fail to introduce products and services that meet market demand, or we do not successfully expand into adjacent markets, we may lose our competitive position, our products may become obsolete, and our business, financial condition or results of operations could be adversely affected.

Our success in these new markets depends on a variety of factors, including but not limited to our ability to develop new products, new product features and services that address the customer requirements for these markets, attract a customer base in markets in which we have less experience, compete with new and existing competitors in these adjacent markets, and gain market acceptance of our new products.

Developing our products is expensive, and the investment in product development may involve a long payback cycle. Our results of operations will be impacted by the timing and size of these investments. These investments may take several years to generate positive returns, if ever.

Additionally, future market share gains may take longer than planned and cause us to incur significant costs. Difficulties in any of our new product development efforts or our efforts to enter adjacent markets could adversely affect our operating results and financial condition.

We may not be able to accurately plan our production based on our sales contracts, which may result in carrying excess raw material inventory.

Our sales contracts typically provide for a forecast of 12 months on the quantity of products that our customers may purchase from us. We typically have a 12-week lead time to manufacture products to meet our customers’ requirements once our customers place orders with us. To meet this delivery deadline, we generally make decisions on our production level and timing, procurement, facility requirements, personnel needs and other resources requirements based on estimates made in light of this forecast, our past dealings with such customers, market conditions and other relevant factors. Our customers’ final purchase orders may not be consistent with our estimates. If the final purchase orders substantially differ from our estimates, we may have excess raw material inventory or material shortages. Excess inventory could result in unprofitable sales or write-offs as our products are susceptible to obsolescence and price declines. Expediting additional material to make up for any shortages within a short time frame could result in unprofitable sales or cause us to adjust delivery dates. In either case, our results of operation would fluctuate from period-to-period. These factors could have an adverse effect on our result of operations as a result of impairments. Further, such excess material and inventory could also lead to a decision of exiting certain products and models.

We may experience issues with vehicle and battery components, which may harm the production and profitability of our products.

11

Our plan to grow the volume and profitability of our ePTWs and battery swapping services depends on significant production of the relevant components. We produce several vehicle components, vehicles, and battery packs. In the past, some of the manufacturing lines for certain product components took longer than anticipated to ramp to their full capacity, and additional bottlenecks may arise in the future as we continue to increase the production rate and introduce new lines. If we are unable to or otherwise do not maintain and grow our respective operations, or if we are unable to do so cost-effectively or hire and retain highly-skilled personnel there, our ability to manufacture our products profitably would be limited, which may harm our business, financial condition and results of operations.

Finally, lithium-ion cells can rapidly release the energy they contain by venting smoke and flames in a manner that can ignite nearby materials as well as other lithium-ion cells. Negative public perceptions regarding the suitability of lithium-ion cells or any future incident involving lithium-ion cells, such as a vehicle or other fire, even if such incident does not involve our battery cells, could seriously harm our business and reputation. Any incident involving our battery cells could result in lawsuits, recalls or redesign efforts, all of which would be time consuming and expensive and could harm our brand image. The high volumes of battery cells and battery modules and packs manufactured at our facilities are stored and recycled at our various facilities. Any mishandling of battery cells may cause disruption to the operation of such facilities. While we have implemented safety procedures related to the handling of the cells, there can be no assurance that a safety issue or fire related to the cells would not disrupt our operations. Any such disruptions or issues may harm our brand and business.

We may be subject to declining average selling prices, which may harm our revenue and gross profits.

ePTWs and battery swapping services are subject to declines in average selling prices due to rapidly evolving technologies, industry standards and consumer preferences. As a result, our customers may expect us, as a supplier, to cut our costs and lower the price of our products in order to mitigate the negative impact on their own margins.

We continue to refine and optimize our manufacturing process to provide our top-notch products at competitive prices. Our revenue and profitability will suffer if we are unable to offset any declines in our average selling prices by developing new or enhanced products with higher selling prices or gross profit margins, increasing our sales volumes or reducing the material costs of our products on a timely basis.

Our products and services may be impacted by service disruptions, outages, errors, performance, and quality problems. These disruptions, outages, quality, and other performance problems may result in material and adverse impacts to our business and operations.

We have previously experienced, and may in the future experience, service disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, third-party service providers, human or software errors and capacity constraints. If our products or services are unavailable or otherwise fail to function appropriately when customers attempt to access them or they do not operate or perform in a responsive and effective manner, customers may seek other products and services.

We expect to continue to make significant investments to maintain and improve our software and other aspects of our product and service offerings. To the extent that we do not effectively address capacity constraints, upgrade our systems as needed and continually develop our technology and network architecture to accommodate actual and anticipated changes in technology, our business, financial condition and results of operations may be harmed.

If our software is unavailable for a significant period of time as a result of such a transition, especially during peak periods, we could suffer damage to our reputation or brand, or loss of revenues any of which could adversely affect our business, financial condition and results of operations.

Our technology could have undetected defects, errors or bugs in hardware, firmware or software, which could reduce market adoption, increase cost of maintenance, repair, or replacement, damage our reputation with current or prospective customers, and/or expose us to product liability and other claims that could materially and adversely affect our business.

We may be subject to claims that batteries from our battery swapping stations have malfunctioned and persons were injured or purported to be injured due to latent defects. Any insurance that we carry may not be sufficient or may not apply to all situations. Similarly, to the extent that such malfunctions are related to components obtained from third-party vendors, such vendors may not assume responsibility for such malfunctions. Any of these events could adversely affect our brand, reputation, financial condition or results of operations.

Our software platform is complex and includes a number of licensed third-party commercial and open-source software libraries. Our software may contain latent defects or errors that may be difficult to detect and remediate. We are continuing to evolve the features and functionality of our platform through updates and enhancements, and as we do, we may introduce additional defects or errors that may not be detected until after deployment to customers.

In addition, if our products and services, including any updates or patches, are not implemented or used correctly or as intended, inadequate performance and disruptions in service may result. Any defects or errors in product or services offerings, or the perception of such defects or errors, or other performance problems could result in any of the following, each of which could adversely affect our business and results of operations:

12

▪expenditure of significant financial and product development resources, including recalls, in efforts to analyze, correct, eliminate or work around errors or defects;

▪loss of existing or potential customers or partners;

▪interruptions or delays in sales;

▪equipment replacements;

▪delayed or lost revenue;

▪delay or failure to attain market acceptance;

▪delay in the development or release of new functionality or improvements;

▪negative publicity and reputational harm;

▪sales credits or refunds;

▪exposure of confidential or proprietary information;

▪diversion of development and customer service resources;

▪breach of warranty claims;

▪legal claims under applicable laws, rules and regulations; and

▪the expense and risk of litigation.

We also face the risk that any contractual protections we seek to include in our agreements with customers are rejected, not implemented uniformly or may not fully or effectively protect from claims by customers, reseller, business partners or other third parties. In addition, any insurance coverage or indemnification obligations of suppliers for our benefit may not adequately cover all such claims, or cover only a portion of such claims. A successful product liability, warranty, or other similar claim could have an adverse effect on our business, financial condition and results of operations. In addition, even claims that ultimately are unsuccessful could result in expenditure of funds in litigation, divert management’s time and other resources and cause reputational harm.

Our insurance coverage strategy may not be adequate to protect us from all business risks.

We may be subject, in the ordinary course of business, to losses resulting from products liability, accidents, acts of God and other claims against us, for which we may have no insurance coverage. As a general matter, we do not maintain as much insurance coverage as many other companies do, and in some cases, we do not maintain any at all. Additionally, the policies that we do have may include significant deductibles or self-insured retentions, policy limitations and exclusions, and we cannot be certain that our insurance coverage will be sufficient to cover all future losses or claims against us. A loss that is uninsured or which exceeds policy limits may require us to pay substantial amounts, which may harm our financial condition and results of operations.

We may choose to or be compelled to undertake product recalls or take other similar actions.

As a company that manufactures our own vehicles, battery packs, and battery swapping stations, we must manage the risk of product recalls with respect to our products. In addition to recalls that might be initiated by us for various causes, testing of or investigations into our products by government regulators or industry groups may compel us to initiate product recalls or may result in negative public perceptions about the safety of our products, even if we disagree with the defect determination or have data that shows the actual safety risk to be non-existent. We have initiated product recalls three times since our first vehicle launch in 2015, which occurred in 2017, 2018, and 2020, respectively, in Taiwan. In the future, we may voluntarily or involuntarily initiate recalls if any of our products are determined by us or a regulator to contain a safety defect or be noncompliant with applicable laws and regulations. Such recalls, whether voluntary or involuntary or caused by systems or components engineered or manufactured by us or our suppliers, has previously resulted in and could in the future result in significant expense, supply chain complications and service burdens, premature replacement of assets, and may harm our brand, business, prospects, financial condition and results of operations.

Any legal proceedings or claims against us could be costly and time-consuming to defend and could harm reputation regardless of the outcome.