00018833132023FYfalsehttp://fasb.org/us-gaap/2023#PropertyPlantAndEquipmentAndFinanceLeaseRightOfUseAssetAfterAccumulatedDepreciationAndAmortizationhttp://fasb.org/us-gaap/2023#AccountsPayableAndAccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrent37139840700018833132023-01-012023-12-3000018833132023-07-01iso4217:USD00018833132024-02-26xbrli:shares00018833132023-12-3000018833132022-12-31iso4217:USDxbrli:shares00018833132022-01-022022-12-3100018833132021-01-032022-01-010001883313us-gaap:CommonStockMemberus-gaap:CommonClassAMember2021-01-020001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-01-020001883313us-gaap:CommonStockMember2021-01-020001883313us-gaap:AdditionalPaidInCapitalMember2021-01-020001883313us-gaap:RetainedEarningsMember2021-01-020001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-0200018833132021-01-020001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-01-032022-01-010001883313us-gaap:RetainedEarningsMember2021-01-032022-01-010001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-032022-01-010001883313us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-01-010001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-01-010001883313us-gaap:CommonStockMember2022-01-010001883313us-gaap:AdditionalPaidInCapitalMember2022-01-010001883313us-gaap:RetainedEarningsMember2022-01-010001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-0100018833132022-01-010001883313us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-01-022022-12-310001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-01-022022-12-310001883313us-gaap:CommonStockMember2022-01-022022-12-310001883313us-gaap:AdditionalPaidInCapitalMember2022-01-022022-12-310001883313us-gaap:RetainedEarningsMember2022-01-022022-12-310001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-01-022022-12-310001883313us-gaap:CommonStockMemberus-gaap:CommonClassAMember2022-12-310001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-12-310001883313us-gaap:CommonStockMember2022-12-310001883313us-gaap:AdditionalPaidInCapitalMember2022-12-310001883313us-gaap:RetainedEarningsMember2022-12-310001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001883313us-gaap:CommonStockMember2023-01-012023-12-300001883313us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-300001883313us-gaap:RetainedEarningsMember2023-01-012023-12-300001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-01-012023-12-300001883313us-gaap:CommonStockMemberus-gaap:CommonClassAMember2023-12-300001883313us-gaap:CommonClassBMemberus-gaap:CommonStockMember2023-12-300001883313us-gaap:CommonStockMember2023-12-300001883313us-gaap:AdditionalPaidInCapitalMember2023-12-300001883313us-gaap:RetainedEarningsMember2023-12-300001883313us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-300001883313us-gaap:NonrelatedPartyMember2023-01-012023-12-300001883313us-gaap:NonrelatedPartyMember2022-01-022022-12-310001883313us-gaap:NonrelatedPartyMember2021-01-032022-01-010001883313us-gaap:RelatedPartyMember2023-01-012023-12-300001883313us-gaap:RelatedPartyMember2022-01-022022-12-310001883313us-gaap:RelatedPartyMember2021-01-032022-01-010001883313svv:CorporateConversionMember2022-01-0700018833132023-05-262023-05-26xbrli:pure0001883313us-gaap:IPOMember2023-07-032023-07-030001883313us-gaap:IPOMember2023-07-030001883313svv:SellingStockholdersMember2023-07-032023-07-030001883313us-gaap:OverAllotmentOptionMembersvv:SellingStockholdersMember2023-07-032023-07-0300018833132023-06-28svv:vote0001883313svv:GovernmentSubsidiesMembersvv:COVID19PandemicMember2021-01-032022-01-010001883313us-gaap:SalesChannelDirectlyToConsumerMember2023-01-012023-12-300001883313us-gaap:SalesChannelDirectlyToConsumerMember2022-01-022022-12-310001883313us-gaap:SalesChannelDirectlyToConsumerMember2021-01-032022-01-010001883313us-gaap:SalesChannelThroughIntermediaryMember2023-01-012023-12-300001883313us-gaap:SalesChannelThroughIntermediaryMember2022-01-022022-12-310001883313us-gaap:SalesChannelThroughIntermediaryMember2021-01-032022-01-01svv:financial_institution0001883313srt:MinimumMember2023-12-300001883313srt:MaximumMember2023-12-300001883313us-gaap:AccountsPayableAndAccruedLiabilitiesMember2023-12-300001883313us-gaap:AccountsPayableAndAccruedLiabilitiesMember2022-12-310001883313svv:AccruedPayrollAndRelatedTaxesMember2023-12-300001883313svv:AccruedPayrollAndRelatedTaxesMember2022-12-310001883313us-gaap:OtherLiabilitiesMember2023-12-300001883313us-gaap:OtherLiabilitiesMember2022-12-31svv:operating_segmentsvv:reportable_segment0001883313svv:A2ndAveAcquisitionMember2021-11-080001883313svv:A2ndAveAcquisitionMember2021-11-082021-11-080001883313us-gaap:LineOfCreditMembersvv:A2ndAveAcquisitionMemberus-gaap:SecuredDebtMember2021-11-082021-11-080001883313svv:A2ndAveAcquisitionMember2022-01-010001883313svv:A2ndAveAcquisitionMember2022-10-022022-12-310001883313svv:A2ndAveAcquisitionMemberus-gaap:SellingGeneralAndAdministrativeExpensesMember2022-01-010001883313svv:A2ndAveAcquisitionMember2021-01-032022-01-010001883313us-gaap:FurnitureAndFixturesMember2023-12-300001883313us-gaap:FurnitureAndFixturesMember2022-12-310001883313us-gaap:LeaseholdImprovementsMember2023-12-300001883313us-gaap:LeaseholdImprovementsMember2022-12-310001883313svv:USRetailMember2022-01-010001883313svv:CanadaRetailMember2022-01-010001883313svv:USRetailMember2022-01-022022-12-310001883313svv:CanadaRetailMember2022-01-022022-12-310001883313svv:USRetailMember2022-12-310001883313svv:CanadaRetailMember2022-12-310001883313svv:USRetailMember2023-01-012023-12-300001883313svv:CanadaRetailMember2023-01-012023-12-300001883313svv:USRetailMember2023-12-300001883313svv:CanadaRetailMember2023-12-300001883313us-gaap:TradeNamesMember2023-12-300001883313us-gaap:LicensingAgreementsMember2023-12-300001883313us-gaap:TradeNamesMember2022-12-310001883313us-gaap:LicensingAgreementsMember2022-12-310001883313us-gaap:SeniorNotesMembersvv:SeniorSecuredNotesMember2023-12-300001883313us-gaap:SeniorNotesMembersvv:SeniorSecuredNotesMember2022-12-310001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-12-300001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2022-12-310001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2023-12-300001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMember2022-12-310001883313us-gaap:SecuredDebtMembersvv:SeniorSecuredNotesMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313us-gaap:SeniorNotesMembersvv:SeniorSecuredNotesMember2023-01-012023-12-300001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:SecuredDebtMember2021-01-032022-01-010001883313us-gaap:SeniorNotesMembersvv:SeniorSecuredNotesMember2023-02-060001883313us-gaap:SeniorNotesMember2023-02-060001883313us-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodOneMembersvv:SeniorSecuredNotesMember2023-02-062023-02-060001883313us-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodTwoMembersvv:SeniorSecuredNotesMember2023-02-062023-02-060001883313us-gaap:DebtInstrumentRedemptionPeriodThreeMemberus-gaap:SeniorNotesMembersvv:SeniorSecuredNotesMember2023-02-062023-02-060001883313svv:February152025ThroughFebruary142026Member2023-01-012023-12-300001883313svv:February152026ThroughFebruary142027Member2023-01-012023-12-300001883313svv:OnOrAfterFebruary152027AndThereafterMember2023-01-012023-12-300001883313us-gaap:SeniorNotesMemberus-gaap:DebtInstrumentRedemptionPeriodFourMembersvv:SeniorSecuredNotesMember2023-02-062023-02-060001883313us-gaap:SeniorNotesMemberus-gaap:SubsequentEventMembersvv:SeniorSecuredNotesMember2024-03-040001883313us-gaap:SeniorNotesMemberus-gaap:SubsequentEventMembersvv:SeniorSecuredNotesMember2024-03-042024-03-040001883313svv:UncommittedIncrementalFacilityMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-12-300001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMembersrt:MinimumMemberus-gaap:SecuredDebtMember2023-12-300001883313svv:SeniorSecuredCreditFacilitiesMembersrt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-12-300001883313us-gaap:SubsequentEventMembersvv:SeniorSecuredCreditFacilitiesMembersrt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2024-01-300001883313us-gaap:SubsequentEventMembersvv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMembersrt:MinimumMemberus-gaap:SecuredDebtMember2024-01-300001883313us-gaap:SubsequentEventMembersvv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2024-01-302024-01-300001883313us-gaap:SubsequentEventMembersvv:UncommittedIncrementalFacilityMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2024-01-300001883313us-gaap:SubsequentEventMembersvv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2024-02-092024-02-090001883313svv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313us-gaap:BaseRateMembersvv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMembersrt:MinimumMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313us-gaap:BaseRateMembersvv:SeniorSecuredCreditFacilitiesMembersrt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313svv:SecuredOvernightFinancingRateSOFRMembersvv:SeniorSecuredCreditFacilitiesMemberus-gaap:LineOfCreditMembersrt:MinimumMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313svv:SecuredOvernightFinancingRateSOFRMembersvv:SeniorSecuredCreditFacilitiesMembersrt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:SecuredDebtMember2023-01-012023-12-300001883313us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2023-12-300001883313us-gaap:LetterOfCreditMemberus-gaap:LineOfCreditMembersvv:TheRevolvingCreditFacilityMember2023-12-300001883313us-gaap:RevolvingCreditFacilityMembersvv:SwinglineSublimitMembersvv:TheRevolvingCreditFacilityMember2023-12-300001883313us-gaap:BaseRateMemberus-gaap:LineOfCreditMembersrt:MinimumMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2023-01-012023-12-300001883313us-gaap:BaseRateMembersrt:MaximumMemberus-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2023-01-012023-12-300001883313us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2022-12-310001883313us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2022-01-022022-12-310001883313us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembersvv:TheRevolvingCreditFacilityMember2023-01-012023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:MoneyMarketFundsMember2023-12-300001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMemberus-gaap:FairValueInputsLevel2Member2023-12-300001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-300001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMember2023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:ForwardContractsMember2023-12-300001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2023-12-300001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2023-12-300001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMemberus-gaap:FairValueInputsLevel2Member2022-12-310001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CurrencySwapMember2022-12-310001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Memberus-gaap:ForwardContractsMember2022-12-310001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:ForwardContractsMember2022-12-310001883313us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001883313us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001883313us-gaap:FairValueMeasurementsRecurringMember2022-12-310001883313us-gaap:SeniorNotesMemberus-gaap:FairValueInputsLevel1Membersvv:SeniorSecuredNotesMember2023-12-300001883313us-gaap:CurrencySwapMember2023-12-300001883313us-gaap:CurrencySwapMember2022-12-310001883313us-gaap:ForeignExchangeForwardMember2023-12-300001883313us-gaap:ForeignExchangeForwardMember2022-12-310001883313us-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:InterestRateSwapMember2022-12-310001883313svv:DerivativeAssetCurrentMemberus-gaap:ForeignExchangeForwardMemberus-gaap:NondesignatedMember2023-12-300001883313svv:DerivativeAssetCurrentMemberus-gaap:ForeignExchangeForwardMemberus-gaap:NondesignatedMember2022-12-310001883313svv:DerivativeAssetCurrentMemberus-gaap:CurrencySwapMemberus-gaap:NondesignatedMember2023-12-300001883313svv:DerivativeAssetCurrentMemberus-gaap:CurrencySwapMemberus-gaap:NondesignatedMember2022-12-310001883313us-gaap:CurrencySwapMemberus-gaap:NondesignatedMembersvv:DerivativeAssetNoncurrentMember2023-12-300001883313us-gaap:CurrencySwapMemberus-gaap:NondesignatedMembersvv:DerivativeAssetNoncurrentMember2022-12-310001883313us-gaap:NondesignatedMember2023-12-300001883313us-gaap:NondesignatedMember2022-12-310001883313us-gaap:AccountsPayableAndAccruedLiabilitiesMemberus-gaap:ForeignExchangeForwardMemberus-gaap:NondesignatedMember2023-12-300001883313us-gaap:AccountsPayableAndAccruedLiabilitiesMemberus-gaap:ForeignExchangeForwardMemberus-gaap:NondesignatedMember2022-12-310001883313us-gaap:CurrencySwapMemberus-gaap:AccountsPayableAndAccruedLiabilitiesMemberus-gaap:NondesignatedMember2023-12-300001883313us-gaap:CurrencySwapMemberus-gaap:AccountsPayableAndAccruedLiabilitiesMemberus-gaap:NondesignatedMember2022-12-310001883313svv:DerivativeAssetCurrentMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2023-12-300001883313svv:DerivativeAssetCurrentMemberus-gaap:DesignatedAsHedgingInstrumentMemberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:DesignatedAsHedgingInstrumentMembersvv:DerivativeAssetNoncurrentMemberus-gaap:InterestRateSwapMember2023-12-300001883313us-gaap:DesignatedAsHedgingInstrumentMembersvv:DerivativeAssetNoncurrentMemberus-gaap:InterestRateSwapMember2022-12-310001883313us-gaap:DesignatedAsHedgingInstrumentMember2023-12-300001883313us-gaap:DesignatedAsHedgingInstrumentMember2022-12-310001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:ForeignExchangeForwardMember2023-01-012023-12-300001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:ForeignExchangeForwardMember2022-01-022022-12-310001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:ForeignExchangeForwardMember2021-01-032022-01-010001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:CurrencySwapMember2023-01-012023-12-300001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:CurrencySwapMember2022-01-022022-12-310001883313us-gaap:ForeignCurrencyGainLossMemberus-gaap:CurrencySwapMember2021-01-032022-01-010001883313us-gaap:InterestExpenseMemberus-gaap:InterestRateSwapMember2023-01-012023-12-300001883313us-gaap:InterestExpenseMemberus-gaap:InterestRateSwapMember2022-01-022022-12-310001883313us-gaap:InterestExpenseMemberus-gaap:InterestRateSwapMember2021-01-032022-01-010001883313us-gaap:OperatingSegmentsMembersvv:USRetailMember2023-01-012023-12-300001883313us-gaap:OperatingSegmentsMembersvv:USRetailMember2022-01-022022-12-310001883313us-gaap:OperatingSegmentsMembersvv:USRetailMember2021-01-032022-01-010001883313us-gaap:OperatingSegmentsMembersvv:CanadaRetailMember2023-01-012023-12-300001883313us-gaap:OperatingSegmentsMembersvv:CanadaRetailMember2022-01-022022-12-310001883313us-gaap:OperatingSegmentsMembersvv:CanadaRetailMember2021-01-032022-01-010001883313us-gaap:MaterialReconcilingItemsMember2023-01-012023-12-300001883313us-gaap:MaterialReconcilingItemsMember2022-01-022022-12-310001883313us-gaap:MaterialReconcilingItemsMember2021-01-032022-01-010001883313country:US2023-12-300001883313country:US2022-12-310001883313country:CA2023-12-300001883313country:CA2022-12-310001883313country:AU2023-12-300001883313country:AU2022-12-310001883313svv:A2019ManagementIncentivePlanMemberus-gaap:EmployeeStockOptionMember2019-03-282019-03-280001883313svv:A2019ManagementIncentivePlanMemberus-gaap:EmployeeStockOptionMember2023-12-300001883313svv:OmnibusIncentivePlanMember2023-01-012023-12-300001883313svv:TimeBasedOptionsMember2023-01-012023-12-300001883313svv:TimeBasedOptionsMember2022-01-022022-12-310001883313svv:TimeBasedOptionsMember2021-01-032022-01-010001883313svv:TimeBasedOptionsMember2022-12-310001883313svv:TimeBasedOptionsMember2023-12-300001883313us-gaap:PerformanceSharesMember2023-01-012023-12-300001883313us-gaap:ShareBasedCompensationAwardTrancheOneMemberus-gaap:PerformanceSharesMemberus-gaap:IPOMember2023-01-012023-12-300001883313us-gaap:ShareBasedCompensationAwardTrancheTwoMemberus-gaap:PerformanceSharesMember2023-01-012023-12-300001883313us-gaap:PerformanceSharesMember2022-10-012023-07-02svv:grantee0001883313us-gaap:PerformanceSharesMembersvv:IPOVestingMember2023-07-032023-07-030001883313svv:GradedVestingBasisMemberus-gaap:PerformanceSharesMember2023-07-032023-12-300001883313svv:BlackScholesMertonOptionPricingModelMemberus-gaap:PerformanceSharesMember2023-01-012023-12-300001883313svv:BlackScholesMertonOptionPricingModelMemberus-gaap:PerformanceSharesMember2022-01-022022-12-310001883313svv:MonteCarloSimulationMemberus-gaap:PerformanceSharesMember2023-01-012023-12-300001883313svv:MonteCarloSimulationMembersrt:MinimumMemberus-gaap:PerformanceSharesMember2023-01-012023-12-300001883313svv:MonteCarloSimulationMembersrt:MaximumMemberus-gaap:PerformanceSharesMember2023-01-012023-12-300001883313svv:MonteCarloSimulationMemberus-gaap:PerformanceSharesMember2023-07-012023-07-310001883313us-gaap:PerformanceSharesMember2022-12-310001883313us-gaap:PerformanceSharesMember2022-01-022022-12-310001883313us-gaap:PerformanceSharesMember2023-12-300001883313us-gaap:PerformanceSharesMember2021-01-032022-01-010001883313srt:MinimumMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-300001883313srt:MaximumMemberus-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-300001883313us-gaap:RestrictedStockUnitsRSUMember2022-12-310001883313us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-300001883313us-gaap:RestrictedStockUnitsRSUMember2023-12-300001883313country:US2023-01-012023-12-300001883313country:US2022-01-022022-12-310001883313country:US2021-01-032022-01-010001883313us-gaap:NonUsMember2023-01-012023-12-300001883313us-gaap:NonUsMember2022-01-022022-12-310001883313us-gaap:NonUsMember2021-01-032022-01-010001883313us-gaap:StateAndLocalJurisdictionMember2023-12-300001883313us-gaap:StateAndLocalJurisdictionMember2022-12-310001883313us-gaap:CanadaRevenueAgencyMembersvv:A20122019Member2022-01-01iso4217:CAD0001883313us-gaap:CanadaRevenueAgencyMembersvv:A20122019Member2021-01-032022-01-010001883313us-gaap:CanadaRevenueAgencyMembersvv:A20122019Member2022-01-022022-12-3100018833132023-10-012023-12-300001883313svv:MarkWalshMember2023-01-012023-12-300001883313svv:MarkWalshMember2023-10-012023-12-300001883313svv:MarkWalshMember2023-12-300001883313svv:MindyGeisserMember2023-01-012023-12-300001883313svv:MindyGeisserMember2023-10-012023-12-300001883313svv:MindyGeisserMember2023-12-300001883313svv:RichardMedwayMember2023-01-012023-12-300001883313svv:RichardMedwayMember2023-10-012023-12-300001883313svv:RichardMedwayMember2023-12-30

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________________________

FORM 10-K

________________________________________

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 30, 2023

OR

| | | | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from _________ to ________

Commission file number 001-04321

________________________________________

Savers Value Village, Inc.

________________________________________

(Exact name of registrant as specified in its charter)

| | | | | | | | |

Delaware | | 83-4165683 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

11400 S.E. 6th Street Suite 125, Bellevue, WA | | 98004 |

| (Address of Principal Executive Offices) | | (Zip Code) |

425-462-1515

Registrant's telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, par value $0.000001 per share | SVV | The New York Stock Exchange |

Securities registered pursuant to section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ¨ | Accelerated filer | ¨ |

| Non-accelerated filer | x | Smaller reporting company | ¨ |

| | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ¨

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

As of July 1, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, there was no established public trading market for the registrant’s equity securities. The registrant’s common stock began trading on the New York Stock Exchange on June 29, 2023 and completed its initial public offering on July 3, 2023.

The registrant had outstanding 161,363,892 shares of common stock as of February 26, 2024.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s Proxy Statement for the Annual Meeting of Shareholders to be held on June 5, 2024, are incorporated by reference into Part III of this Form 10-K.

Table of Contents

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K (the “Annual Report”) contains forward-looking statements within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and are made in reliance on the safe harbor protections provided thereunder. Forward looking statements can be identified by words such as “could,” “may,” “might,” “will,” “likely,” “anticipates,” “intends,” “plans,” “seeks,” “believes,” “estimates,” “expects,” “continues,” “projects” or the negative of these terms or other comparable terminology. In particular, statements about the markets in which we operate, including competition, growth and trends in our markets and industry; our strategies, outcomes and prospects; our expectations, beliefs, plans, objectives, assumptions; and future events or performance made in the sections titled “Risk Factors”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations”, “Business” and “Notes to Consolidated Financial Statements” are forward-looking statements.

Forward-looking statements are based on our current expectations and assumptions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks and changes in circumstances that are difficult to predict. As a result, the Company’s actual results may differ materially from those contemplated by the forward-looking statements. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include:

•the impact on both the supply and demand for our products caused by general economic conditions and changes in consumer confidence and spending;

•our ability to anticipate consumer demand and to source and process a sufficient quantity of quality secondhand items at attractive prices on a recurring basis;

•risks related to attracting new, and retaining existing customers, including by increasing acceptance of secondhand items among new and growing customer demographics;

•risks associated with our status as a “brick and mortar” only retailer and our lack of operations in the growing online retail marketplace;

•our failure to open new profitable stores or successfully enter new markets on a timely basis or at all;

•risks associated with doing business with international manufacturers and suppliers including, but not limited to, transportation and shipping challenges, regulatory risks in foreign jurisdictions (particularly in Canada, where we maintain extensive operations) and exchange rate risks, which we may not be able to fully hedge;

•the loss of, or disruption or interruption in the operations of, our centralized distribution centers;

•risks associated with litigation, the expense of defense, and the potential for adverse outcomes;

•our failure to properly hire and to retain key personnel and other qualified personnel;

•risks associated with the timely and effective deployment, protection, and defense of our computer networks and other electronic systems, including e-mail;

•changes in government regulations, procedures and requirements;

•our ability to maintain an effective system of internal controls and produce timely and accurate financial statements or comply with applicable regulations;

•risks associated with heightened geopolitical instability due to the conflicts in the Middle East and Eastern Europe;

•the outbreak of viruses or widespread illness, including the continued impact of COVID-19 and continuing or renewed regulatory responses thereto; and

•other factors set forth under the heading “Risk Factors” in this Annual Report.

These risks are not exhaustive. Other sections of this Annual Report include additional factors that could adversely affect our business and financial performance.

Any forward-looking statement made by us in this Annual Report speaks only as of the date on which it is made, and while we believe that information forms a reasonable basis for such statements, that information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. Moreover, factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We are not under any obligation (and we specifically disclaim any such obligation) to update or alter these forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

Part I

Item 1. Business

Company Overview

Our mission

To champion reuse and inspire a future where secondhand is second nature.

From the thrill of the hunt to the joy of decluttering, we help communities harness the power of pre-loved stuff to keep reusable items around for years to come.

Who we are

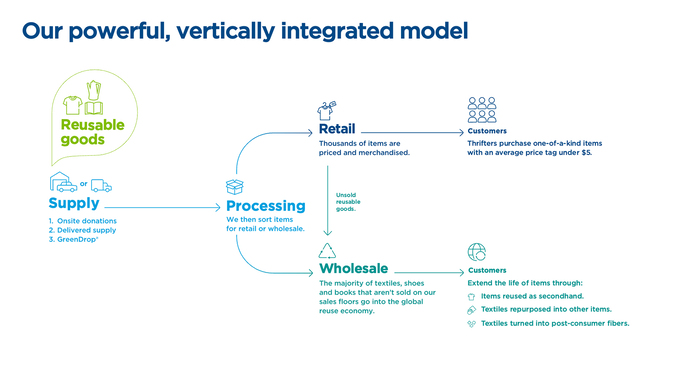

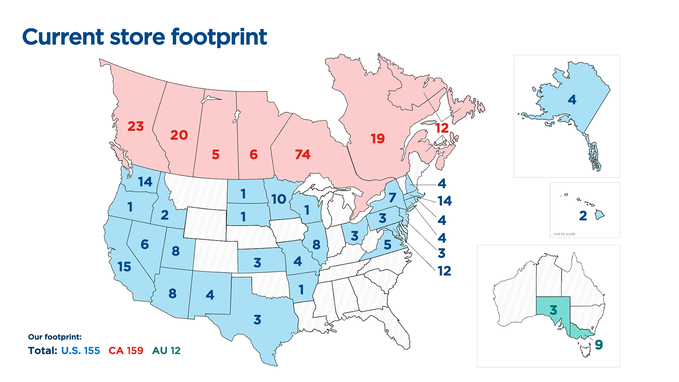

We are the largest for-profit thrift operator in the United States and Canada based on number of stores. With more than 22,000 team members, we operate a total of 326 stores under the Savers®, Value Village®, Value Village Boutique™, Village des Valeurs™, Unique® and 2nd Ave.® banners. We are committed to redefining secondhand shopping by providing one-of-a-kind, low-priced merchandise ranging from quality clothing to home goods in an exciting treasure-hunt shopping environment. We purchase secondhand textiles (e.g., clothing, bedding and bath items), shoes, accessories, housewares, books and other goods from our non-profit partners (“NPPs”), either directly from them or via on-site donations (“OSDs”) at Community Donation Centers at our stores as well as through GreenDrop locations. We then process, select, price, merchandise and sell these items in our stores. Items that are not sold to our retail customers are marketed to wholesale customers who reuse or repurpose the items they purchase from us. We believe our hyper-local and socially responsible procurement model, industry-leading and innovative operations, differentiated value proposition and deep relationships with our customers distinguish us from other secondhand and value-based retailers.

We offer a dynamic, ever-changing selection of items, with an average unit retail price (“AUR”) of approximately $5. We have a highly engaged customer base, with over 5.3 million active loyalty program members in the United States and Canada who shopped with us as of December 30, 2023, driving 70.3% of point-of-sale transaction value during fiscal year 2023. Our business model is rooted in ESG principles, with a mission to positively impact our stakeholders—thrifters, NPPs and their donors, our team members and our stockholders. As a leader and pioneer of the for-profit thrift category, we seek to positively impact the environment by reducing waste and extending the life of reusable goods. The vast majority of the clothing and textiles we source is sold to our retail or wholesale customers. During fiscal year 2023, we processed 984 million pounds of secondhand goods, compared to 985 million pounds during fiscal year 2022 and 860 million pounds during fiscal year 2021.

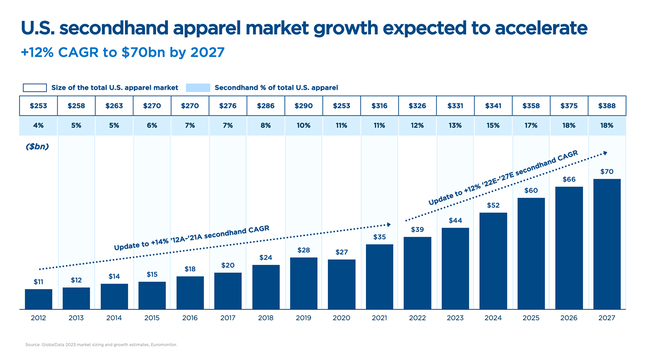

The U.S. secondhand market, which is a subset of the broader retail market, reached approximately $39 billion in 2022 and is expected to grow to more than $70 billion by 2027. Thrift accounted for approximately 56% of the total secondhand market in 2022, and we believe we benefit from the powerful secular trends driving growth in the sector. We also believe consumers are increasingly concerned about the environmental impact of the clothes they wear. There is a growing awareness that the textile and clothing industry is one of the most environmentally damaging sectors of the economy.

Meanwhile, discarded clothing remains the largest source of textile waste in the world, with the average U.S. citizen throwing away 81 pounds of clothing each year, 95% of which could have been re-worn or repurposed; yet 85% of this material ends up in landfills. To put this another way, the Ellen MacArthur Foundation reports that one garbage truck of textiles is landfilled or incinerated every second. Thrift as a business model provides one of the most effective solutions in mitigating the environmental cost of clothing and extending its life.

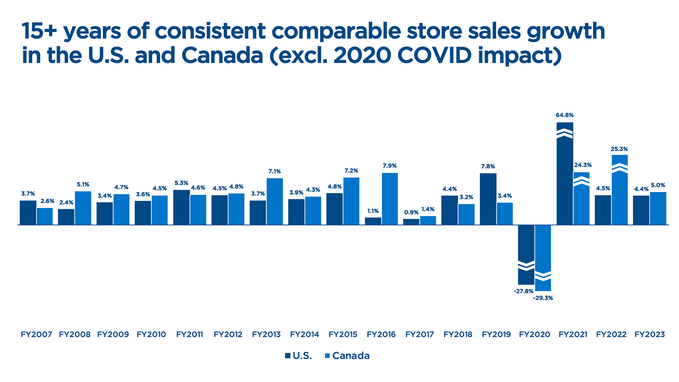

Track record of consistent growth and recent performance

We have a proven track record of consistently delivering comparable store sales growth across the United States and Canada. Prior to the start of the COVID-19 pandemic in March 2020, we achieved over ten years of positive comparable store sales growth across the United States and Canada and our business has recovered strongly from COVID-19-related disruptions.

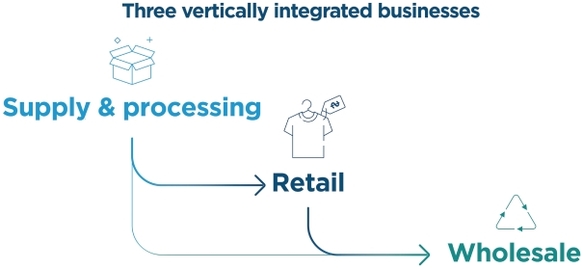

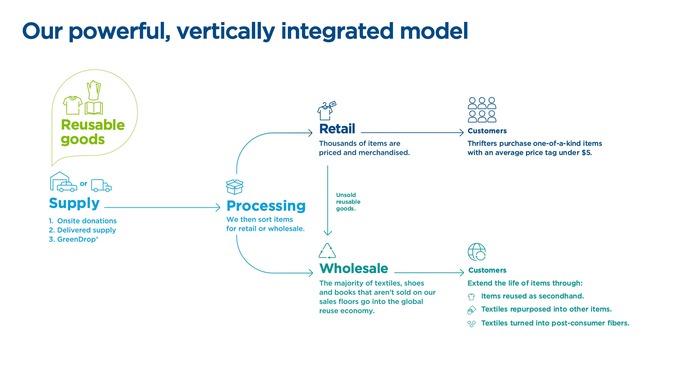

Powerful, Vertically Integrated Business Model

We have innovated and invested in the development of significant operational expertise in order to integrate the three highly-complex parts of thrift operations—supply and processing, retail, and sales to wholesale markets. Our business model enables us to provide value to our NPPs and our customers, while driving attractive profitability and cash flow.

Three vertically integrated businesses Supply & processing Retail Wholesale

Supply and processing

We source our merchandise locally by purchasing secondhand items donated to our NPPs primarily through three distinct and strategic procurement models:

•delivered supply, which includes items donated to and collected by NPPs through a variety of methods, such as neighborhood collections and donation drives, and delivered to our stores or Centralized Processing Centers, or “CPCs”;

•OSDs, which are donations of items by individuals to our NPPs made at Community Donation Centers located at our stores; and

•GreenDrop locations, which are mobile donation stations (and in some cases, brick and mortar facilities) placed in convenient, attractive and high-traffic locations that offer a fast and friendly experience to donors in the communities surrounding our stores.

Our business model is predicated on sourcing and selling quality secondhand items to our customers in local communities. We are able to meet our customer demand given our deep relationships with an extensive network of NPPs that is unmatched in the thrift industry. Our local sourcing strategy also reduces transportation costs and emissions typically associated with the production and distribution of new merchandise.

The quantity and quality of our supply of secondhand items have continued to evolve and improve, particularly as OSDs have grown as a percentage of the pounds of goods we process. While it is strategically important for us to maintain a diverse supply mix, items sourced through OSDs have a cost per pound that is on average less than one-third that of delivered supply from our NPPs. Because OSD volume is primarily driven by convenience, the more we are able to expand our footprint and geographic reach, the more we expect to attract and procure additional OSD supply, which benefits our supply cost and yields. On a comparable store basis, the average store’s OSDs have grown at a 3.5% compound annual growth rate (“CAGR”) from fiscal year 2019 through fiscal year 2023, which has expanded OSDs as a percentage of total pounds processed from 53.0% to 65.2% during the same period. Additionally, our acquisition of 2nd Ave. in November 2021 included GreenDrop, which allows donors to drop off their items at attended donation stations that are movable and can be placed in attractive locations that optimize for high-quality donations, is strengthening our supply base. During fiscal year 2023, 8.4% of total pounds processed stemmed from GreenDrop. We are currently expanding the use of GreenDrop to locations in certain other markets.

In addition, data analytics have played a critical role in elevating the quality of our delivered supply by enabling us to concentrate on supply sources with quality goods, which has been a significant driver of our gross product margin.

The vast majority of our retail stores have space dedicated to handle the processing of secondhand goods that provide the inventory to be sold on our retail sales floors. We are currently implementing our offsite processing strategy which allows us to process goods at larger-scale facilities and distribute goods to multiple stores in a local market. The processing of donations under this strategy can occur at warehouses, stores with surplus processing capacity or at CPCs. We opened our first CPC in the third quarter of fiscal year 2021, a second CPC in the second quarter of fiscal year 2022 and three additional CPCs during fiscal year 2023. The CPC system is an offsite, semi-automated processing facility that mechanizes the flow of clothing, accessories and shoes through an integrated series of conveyor belts, robotics, sensors, and other technology. We have prioritized processing capacity at CPCs toward new store growth that would not be possible without a CPC.

Retail

Our continued investment in our stores has both elevated and modernized the thrift shopping experience, transforming our stores into destinations for all generations with increasing traffic from younger generations.

Our store experience directly reflects our mission to make secondhand second nature. We deliver a well merchandised environment that maximizes customer engagement and supports a core tenet for any thrifter—the treasure hunt. Our stores offer a wide selection of quality items across clothing, home goods, books and other items at convenient locations. During fiscal year 2023, more than 35,000 items were merchandised per store every week. Our sales floor inventory is also regularly rotated and refreshed, with inventory turns of roughly 17 times a year, providing our customers with an extensive, ever-changing selection at tremendous value.

We have enhanced our visual presentation with the roll out of our updated “Thrift Proud” sign package that has a great new look, while communicating who we are and what we do. In addition, we have enhanced the customer experience by completing the roll out of self-checkout kiosks in all of our stores in the U.S. and Canada that significantly shorten and, at most times of the day, eliminate payment lines.

We have a continuous feedback loop on the customer experience. Our REactions surveys take the pulse of our customers on a weekly basis regarding the shopping experience and environment. This information is proactively shared with our leadership team and cascaded to store managers, who are measured on their ability to improve operations.

As donations continue to grow and awareness of secondhand shopping increases, we believe more consumers are likely to become thrift shoppers.

Wholesale reuse and repurpose

We display approximately 50% of all textile items we receive on our retail sales floors, approximately 50% of which are sold to thrifters. In support of our efforts to extend the life of reusable goods and recover a portion of the cost of acquiring our supply of secondhand items, we sell the majority of textile items unsold at retail to our wholesale customers, predominately comprised of textile graders and small business owners, who supply local communities across the globe with gently-used, affordable items like clothing, housewares, toys and shoes. Textiles not suitable for reuse as secondhand clothing can be repurposed into other textile items (e.g., wiping rags) and post-consumer fibers (e.g., insulation and carpet padding), further reducing waste.

ESG impact

Environmental: Our business model is designed to maximize the life of reusable goods, and we found a reuse for over 3.2 billion pounds of secondhand items from 2019 to 2023. During fiscal year 2023, our thrifters purchased 274 million various items.

The environmental impacts of textile manufacturing are well documented. The textile industry largely relies on non-renewable resources such as oil for synthetic fibers, fertilizer to grow cotton, and chemicals associated with the production, dyeing, and finishing of fibers and textiles. Between 2002 and 2017, the Ellen MacArthur Foundation (“EMF”) found that clothing production approximately doubled, while utilization decreased by 36%. In addition, textile production is both energy-intensive and water-intensive. EMF estimates that the production of textiles resulted in 1.2 billion tons of carbon dioxide equivalent in 2015, which outpaced the year’s carbon dioxide emissions from all international flights and marine shipping, with additional impacts on local environments. With respect to water usage, which includes cotton farming, EMF also found that the textile industry used approximately 93 billion cubic meters of water each year, while contributing to water scarcity in many parts of the world. Since less than 1% of the material used to produce new clothing (including factory offcuts) is recycled to make new clothing, the reuse of clothing, rather than the purchase of new clothing, is key to mitigating the environmental impacts of the textile industry. In order to achieve the 2030 Paris climate objectives, 20% of garments worldwide must be traded through circular business models.

During 2021 and 2022, we purchased enough Renewable Energy Certificates to match our electricity usage with renewable energy at our two corporate offices and our largest U.S. and Canadian Wholesale Distribution and Reuse Centers through July 2023. In February 2024 we purchased sufficient Renewable Energy Certificates to cover our usage from August to December 2023 and our estimated usage for these facilities through July 2024. Over the last several years, we have completed a LED lighting retrofit for more than 90% of our U.S. and Canadian stores and warehouses.

We have engaged third-party consultants to perform assessments of the Company’s economic and environmental impacts in various communities where we have operations. For example, the Canadian accounting firm MNP studied our impact across Canada in 2022. Including direct, indirect and induced impacts, MNP concluded that our Canadian operations were estimated to generate approximately $1.2 billion of total output, $864.2 million of total GDP, $162.4 million in total revenue for all three levels of government, and 12,650 total jobs. When studying our 2022 Canadian environmental impact, MNP found that we diverted approximately 146,500 metric tonnes of material from Canada’s waste stream, with approximately half of that being clothing materials. The decrease in production of an amount of textiles equivalent to what Value Village diverted was estimated to reduce the emission of greenhouse gasses by 605,352 tonnes of carbon dioxide equivalent, comparable to the annual emissions of 131,598 passenger vehicles and reduce water used in textile production by 80.8 billion liters, comparable to the annual volume of water used by more than 1,000,000 Canadians (2.7 percent of Canada’s population).

Social: Our business model is predicated on sourcing our supply from non-profit organizations in the communities where we do business. The contracts we enter into with our NPPs are typically 1-3 years in duration. Our relationships with our top 10 NPPs average more than 27 years. Over the last five years, we have paid our NPPs more than $530 million for secondhand goods, providing them with unrestricted revenue to support their community-focused missions. From 2019 to 2023, over 90% of our supply was locally sourced, delivering a broad and diverse selection to our customers and fostering a sense of community.

Our leading “people” metric across our organization is team member engagement, which is scored across various areas, including overall job satisfaction, whether the team member would recommend us as a place to work, personal commitment, being energized at work and intent to remain employed. Our team member engagement is considered best-in-class, as measured by an external consultant, comparing our results to other companies in the retail sector. Team member engagement is crucial to customer satisfaction and the satisfaction of our NPPs and their donors.

We also invest in the training, development and advancement of our team members. During fiscal year 2023, 72% of open salaried management positions in the United States and Canada were filled by internal promotions. As of December 30, 2023, 58% of the management roles in our stores and corporate operations were held by team members identifying as female, and 57% of our U.S. workforce was represented by diverse backgrounds and ethnicities.

Governance: We are committed to ethical practices in every aspect of our business and have adopted a Savers Code of Conduct that outlines our expectations for internal interactions and helps us maintain compliance with local laws and regulations. Our five core values guide our strategic direction and how our team members interact with one another, our communities and our customers: (1) make service count; (2) celebrate uniqueness; (3) do the right thing; (4) find a better way; and (5) make an impact.

We continuously evolve our corporate governance policies, procedures and teams to ensure not only our compliance with applicable legal requirements, but that we also live up to our high ethical standards for good governance. We are proud of our highly skilled and diverse Board of Directors, which includes three key standing committees: the Audit Committee, the Compensation Committee and the Nominating, Governance, and Sustainability Committee.

Board-level oversight of ESG strategy and disclosure is a crucial component of our corporate governance. Our Company’s Nominating, Governance, and Sustainability Committee takes the lead in ESG-related matters, while our Audit Committee focuses on internal controls, cyber security and data privacy. Details of our cybersecurity risk management, strategy and governance are provided in Item 1C of this Annual Report. We also established an executive-led ESG Committee with cross-functional representation. The Committee helps to set strategic direction, plays an important role in data validation and reporting, and informs key stakeholders about new initiatives and impacts.

Giving Back to our Communities

We strive to positively impact our team members, customers and the communities in which we live and do business. We encourage team member involvement to support local causes and our stores are empowered to support local relief efforts and community nonprofits. For example, our stores have worked with local charitable organizations to provide items or discounts to individuals impacted by natural disasters such as fires and floods, teachers for their classrooms, victims of house fires, and other community requests. In partnership with Veterans Emergency Transition Service (VETS) Canada, our stores provide move-in kits to help homeless veterans settle into new homes. Kits typically include kitchenware, bed and bath accessories, and other essential items.

We have sponsored and engaged our corporate workforce in local charitable events such as nonprofit lunch and dinner galas and other community events. In 2021, we increased our commitment to corporate charitable giving by establishing a $1.5 million Donor Advised Fund in the United States and a CAD 1.5 million Donor Advised Account in Canada. Our Charitable Giving Committee establishes our corporate giving philosophy, policies, and grant making from our Donor Advised Funds. In 2023, following receipt of an award for attorneys’ fees and costs following the successful resolution of our litigation with the Washington Attorney General, we donated over $1.0 million from such award to our Donor Advised Funds.

Our Market

We operate within the large, fragmented and fast-growing secondhand market, which is a subset of the broader retail market. In addition to being recession-resilient, growth in the secondhand market is accelerating due to a number of powerful secular trends.

The emergence of conscious consumerism

Consumers are increasingly taking into consideration the ESG impacts of their shopping decisions and the brands with which they choose to interact.

Growing importance of value retail and treasure hunt experience

The relevance of value shopping and treasure hunting has grown stronger in recent years. We believe that our thrift model provides a highly compelling, differentiated customer proposition and experience that gives us a competitive advantage over traditional retail and other existing secondhand options. Today’s consumers, and thrifters specifically, are seeking experiential shopping opportunities and compelling value propositions, combined with the multifaceted possibilities of brands and styles. They are drawn to the excitement of finding great value through a treasure hunt experience. We believe that experience, combined with our low AUR, makes us more attractive to customers than traditional retail.

Furthermore, our in-store experience and broad, ever-changing inventory cannot be replicated online. The in-store thrift shopping experience is overwhelmingly preferred by consumers over online resale. We believe that we operate leading brands within the thrift industry offering consumers this unique experience.

Fast-growing secondhand market across both demand and supply

Secondhand demand-side total addressable market: The secondhand market is rapidly growing and continues to gain share in the total retail market from a wide range of traditional retailers, including department stores, fast fashion brands and off-price retailers. The secondhand market consists of both resale (e.g., consignment) and thrift goods, with thrift accounting for approximately 56% of the total market during 2022. In the United States alone, the secondhand market reached approximately $39 billion in 2022 and is expected to grow to $70 billion by 2027, representing a CAGR of 12% between 2022 to 2027.

Our total market opportunity continues to grow due to a general rise in demand for secondhand goods in part as consumers continue to expand the occasions for shopping for secondhand goods. As of the most recent date for which their Annual Reports are available, Salvation Army and Goodwill, the two leading non-profit thrift operators in the United States, operated approximately 6,900 locations and 3,300 locations, respectively, further indicating that there is a robust market for secondhand goods.

Secondhand supply-side total addressable market: There is an abundant and growing source of supply that facilitates the availability of secondhand and thrift goods. As this market continues to develop and expand with the opening of new points of collection, there is significant opportunity to unlock and drive further donations to our NPPs from OSDs and GreenDrop locations, both of which are typically driven by a combination of location, convenience, ease of drop and a fast and friendly experience, all of which will ultimately benefit our NPPs.

As donations continue to grow and awareness of secondhand shopping increases, we believe more consumers are likely to become thrift shoppers.

Competitive Strengths

We have been able to delight millions of customers each year and grow our business consistently through the following competitive strengths:

A leader in the industry with a powerful business model

We are the largest for-profit thrift operator in the United States and Canada. With 326 retail stores under the Savers, Value Village, Value Village Boutique, Village des Valeurs, Unique and 2nd Ave. banners, we are ten times larger than the next largest for-profit thrift operator. We believe our significant scale advantage allows us to deliver extreme value and a superior shopping experience to customers, while generating strong cash flow that can be reinvested in our business.

We have innovated and integrated the three highly-complex parts of thrift operations—supply and processing, retail and sales to wholesale markets—through significant operational expertise and investments. This has created a compelling business model which is differentiated against online competition and traditional retail, based on our treasure-hunt experience and low AUR. Further, our business has demonstrated resilience through economic cycles. Such advantages of our business model provide compelling value to customers, drive attractive profitability for the business, and underpin positive comparable store sales growth. Prior to the start of the COVID-19 pandemic in March 2020, we achieved over ten years of positive comparable store sales growth across the United States and Canada, and our business has recovered strongly from COVID-19-related disruptions. As interest in the secondhand market continues to grow, we will have the opportunity to elevate and define the thrift experience for decades to come.

Unmatched value proposition driving exceptional customer engagement

We offer quality items at one of the deepest values across all of our product categories and an exciting, engaging treasure hunt experience in a contemporary in-store atmosphere, which underpins strong customer loyalty. Our most engaged customers are members of our Super Savers Club® loyalty program. As of December 30, 2023, we had 5.3 million active members enrolled in our U.S. and Canadian loyalty programs who have made a purchase within the last 12 months, compared to 4.8 million active members as of December 31, 2022. Our members earn points or store credit, which further enhances the value shopping experience. Members in both the United States and Canada receive exclusive coupons and offers via email, as well as a special birthday coupon.

During fiscal year 2023, U.S. loyalty members spent approximately 29% more per shopping trip than non-members. During the same period, U.S. loyalty members shopped at our stores an average of 6.8 times annually. During fiscal year 2023, the top three loyalty segments, which represented approximately 48% of active members in the United States during that period, shopped with us more than 12 times per year. For the same period, the attrition rate was less than 5% among the top two loyalty segments. We have email addresses for 78% of our U.S. and Canadian active loyalty members as of December 30, 2023. In addition, as of December 30, 2023, 38% of our U.S. loyalty members had annual household incomes of over $75,000 and 68% identified as female.

We have a particularly active presence on social media platforms, including Facebook, Instagram and Pinterest, to connect with our customers, and we also partner with a number of social media “influencers” who generate further awareness of our brands through sponsored content. At the core of our “Thrift Proud” movement, our customers and followers on social media serve as influential peer-to-peer brand ambassadors and are tagging our brand and banners in thousands of photos and videos weekly. We enjoy highly engaged communities on social media who are inspired by thrift hauls, shopping cart photos, do-it-yourself and upcycling, and creating “new from used”. As of December 30, 2023, Savers, Value Village, Village des Valeurs and Thrift Proud branded hashtags had more than 418 million organic views on TikTok alone, 165,000 followers on Instagram and 364,000 likes on Facebook.

Supply model with proven capacity to drive growth

Quality and volume of supply play a critical role in driving traffic, customer frequency and engagement. We have developed a proven strategy to continuously improve our supply model. In order to maximize supply quality, we periodically assess sales yield, which we define as retail sales generated per pound processed on a currency neutral and comparable store basis, from each supply source to make informed decisions on supplier selection. This approach ultimately improves both our revenue and profitability. We have been strategically focused on increasing our OSDs, particularly in increasing convenience and proximity to potential donors. OSDs not only drive profitability but also enhance the consistency and reliability of supply to each of our stores. We expect our focus on increasing OSDs will contribute to further improvement and growth in our supply.

Culture of innovation and operational excellence

Our culture of innovation underpins our key decisions and the way we run our business. We continue to be an industry leader with innovation to improve the customer experience, while enhancing operational efficiency. We have continuously improved our thrift operations across sourcing, processing, and retailing. We have recently launched major initiatives that will further reinforce our competitive advantage and have a measurable impact on our financial profile:

•Self-checkout: In fiscal year 2023 we completed the roll out self-checkout kiosks in all of our stores in order to enhance the customer experience, with shorter lines and more access points.

•Automated Book Processing (ABP): The ABP system is an integrated set of technologies that efficiently identify, price, and sort books based on their critical attributes (e.g., genre, author, market price). The system design consists of high-speed conveyors, optic recognition, robot tagging and an automated book distribution system working in concert to increase throughput over traditional, manual processes.

•Centralized Processing Centers (CPCs): The CPC system is an offsite, semi-automated processing facility that mechanizes the flow of clothing, accessories, and shoes through an integrated series of conveyor belts, robotics, sensors, and other technology. CPCs play an integral role in our offsite processing strategy.

Attractive financial profile with proven track record of consistent growth

We achieved positive comparable store sales growth from 2007 through 2019, even throughout recessionary periods. We have also delivered steady and consistent gross product margin expansion over the last several years, from 46.4% for fiscal year 2015 to 58.7% for fiscal year 2023. We define gross product margin as net sales minus cost of merchandise sold, exclusive of depreciation and amortization, divided by net sales. We have utilized multiple levers that are unique to our business model to drive margin improvements, especially the growth of OSDs as part of our supply mix and sales yield improvement. As a result of our attractive financial profile, we have significant flexibility with respect to capital allocation, giving us the ability to drive long-term shareholder and stakeholder value through various operating and financial strategies.

Highly experienced and strategic leadership

Our strategic vision and culture are directed by a leadership team that combines deep industry expertise and advanced operational capabilities to continuously innovate our business. Given the unique needs of the business, our leadership team has diverse backgrounds across not only retail but also technology, manufacturing, and supply chain. We are committed to ethical practices in every aspect of our business and are guided by people who fundamentally do the right thing.

How We Plan to Grow

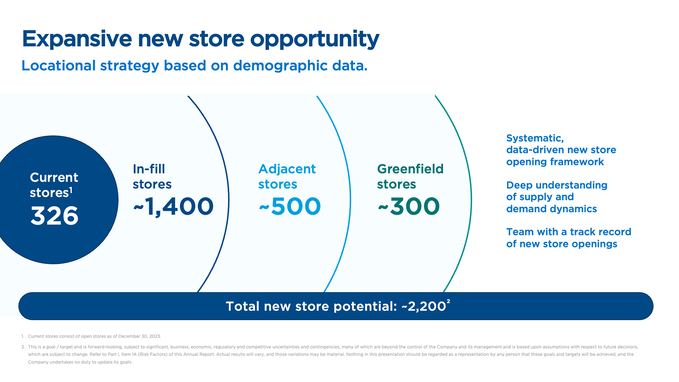

Strategically grow our store base

Our goal is to expand our position as the leading for-profit thrift operator by expanding our store footprint. We have identified approximately 2,200 potential new locations across the United States and Canada. We opened 12 new stores during fiscal year 2023, and target opening approximately 22 new stores in 2024. We target opening approximately 25 or more new stores annually from 2025 through 2027.

•In-fill opportunities: We will continue to identify attractive locations in our existing markets by leveraging our brand awareness and operational capabilities, and where we have the advantage of both attractive supply and demand. These in-fill opportunities will include both traditional and alternative format stores.

•Adjacent store opportunities: We also will pursue opportunities to expand our regional footprint in adjacent areas where we can leverage our operational capabilities and regional market knowledge.

•Greenfield store opportunities: We are currently underpenetrated in multiple important regional markets, including the South and West regions of the United States and in Central Canada.

Driven by our disciplined real estate selection approach, we expect to deliver attractive return on investment and store-level profitability. Our new stores generally take on average four years to reach mature processing efficiency, donation volume and retail demand. Our alternative store format is designed to capitalize on high real estate availability in in-fill markets through smaller formats.

Drive consistent comparable store sales growth

Our goal is to drive consistent growth in comparable store sales by maintaining a superior value proposition to our customers and continuing to offer a compelling selection of quality secondhand items. Benefiting from secular tailwinds, we expect to further drive comparable store sales growth with the following strategies:

•Quality product offerings: We will continue to procure ample supply of quality items to delight our customers. Our compelling selection of offerings enables us to drive both frequency with existing customers and the acquisition of new customers.

•Improving shopping experience: We will continue to invest in the in-store shopping experience to facilitate the treasure hunt dynamics for our customers. We have invested in renovations to modernize our stores; new technologies to optimize store operations; and alternative store formats supported by our offsite processing strategy.

•Expanding engagement with our loyalty program members: We are investing in email and text messaging as a cost-effective means of reaching our existing customers. We extended our text messaging program into Canada in August 2022 and continue to focus on collecting valid emails for our loyalty program members. Our personalized email communication and targeted offers are designed to increase engagement and drive purchase frequency of our growing loyalty program member base.

•Conducting brand marketing: We will continue to utilize our brand marketing spend to improve our brand awareness, bolstered by the broader adoption of thrift shopping overall to drive new customer acquisition.

Continue to implement strategic initiatives to drive efficiency and expand margin, and to unlock new store potential

Compared to our traditional retail competitors, we have multiple levers within our control that have been critical in driving our profitability and Free Cash Flow. For instance, our data analysis has improved our sales yield, which we define as retail sales generated per pound processed on a currency neutral and comparable store basis, which has been a primary driver of comparable store profitability. Our deliberate strategy of increasing the penetration of OSDs as a percentage of total supply has had a significant impact on the quality of our supply, further increasing sales yield and ultimately our gross product margin. In addition, the company-wide self-checkout initiative was completed in the second quarter of 2023 achieving an annual average contribution of $91,000 per store in 2023. Also, a total of eight ABP systems were deployed during 2023 bringing to eleven the total number of ABP systems in operation at December 30, 2023. Consistent with initial projections, each ABP system is projected to deliver $250,000 per year in incremental contribution.

We continue to expand offsite processing capacity and have re-allocated and prioritized CPC and warehouse processing capacity to support new store growth; the majority of new stores planned for 2024 will be serviced by an offsite processing facility and would not have been possible without offsite processing. These stores can have a more flexible layout and size; in more densely populated areas specifically, offsite processing enables in-fill opportunities in alternative store formats without the need for a full-scale processing facility in the back-of-store. Our culture of innovation and data orientation has been critical to driving operational efficiencies, and we will continue to lead in terms of innovating the thrift business model.

Selectively pursue other growth opportunities

In addition to our organic growth initiatives, we will also take an opportunistic yet disciplined approach toward potential inorganic growth opportunities. Given the fragmented nature of the thrift category, we believe there are significant opportunities for growth. This can be conducted through the acquisition of well-operated regional players where we believe we can build upon our infrastructure and scale to accelerate the growth of a potential target and generate synergies. Our acquisition criteria include a significant regional presence; access to a robust flow of quality supply; strong brand awareness; and a complementary cultural fit for our company.

For example, in November 2021, we completed the acquisition of 2nd Ave., which added 12 stores in the Northeastern and Mid-Atlantic regions of the United States, representing a complementary store footprint for our existing store network and offering new store expansion opportunities. The 2nd Ave. Acquisition also included the GreenDrop system used to provide supply to 2nd Ave. stores, which allows donors to drop off their items at attended donation stations that are movable and can be placed in attractive, high traffic areas that are convenient to donors. We are currently expanding GreenDrop to locations in certain other markets.

Supply

Supply sources overview. Our supplier base for a majority of our stores is predominantly local, with over 90% of our supply locally-sourced. As a result, each store draws its supply predominantly from local NPPs and their donors, delivering a broad and diverse selection for our customers and fostering a sense of community. Our local sourcing strategy reduces transportation costs and emissions typically associated with the production and distribution of new merchandise.

We are a for-profit company that champions reuse. While purchases made by our customers in our stores do not directly benefit any NPP, we pay our NPPs a contracted rate for all OSDs and delivered product. Our subsidiaries are registered professional fundraisers where such registration is required.

We source our merchandise primarily through three distinct and strategic methods: (i) on-site donations, (ii) delivered supply and (iii) GreenDrop locations, all of which we purchase directly from our NPPs. We pay a market-competitive contractual rate to purchase items received as OSDs or as part of delivered supply. OSDs are the largest part of our supply mix, accounting for 65.2% of our total pounds processed for fiscal year 2023.

On-Site Donations: OSDs are donations of items made by individuals to our NPPs at our stores’ Community Donation Centers. We operate as a registered professional fundraiser, where required, on behalf of NPPs in accepting donations from their respective donors. Each store is specifically designated as an OSD location for a particular NPP, such that all donations received at the Community Donation Center are credited to that NPP.

Delivered supply: Delivered supply is comprised of two types of supply: firstly, items collected by our NPPs through a variety of methods such as neighborhood collections and donation drives that they deliver to our stores and CPCs; and secondly, items we may solicit, collect and deliver to our stores and CPCs on behalf of our NPPs.

GreenDrop collections: Donations of items made by individuals to our NPPs at convenient and well-signed brick and mortar and trailer locations in neighborhoods surrounding a store location. On behalf of our NPPs, we solicit, collect, and deliver items to our stores and CPCs.

Donation drives: Donation drives operate within our FUNDrive® program and include smaller, local non-profits such as schools, sports teams, community groups and other charitable organizations. These drives are one-time and event-based, with contractual agreements based on each distinct donation drive itself.

Third-party credential: Third-party credential goods are purchased in small amounts on an as-needed basis from regional for-profit collectors, generally consisting of bin operators and other for-profit resellers.

We leverage an analytical platform to measure the sales yield and product margin of an individual stream of supply in our stores. In general, this tool is either used to periodically confirm the performance of an existing stream of supply or to evaluate the performance of a new source of supply.

Non-Profit Partners. We have deep relationships with an extensive roster of NPPs that is unmatched in the thrift industry. Our relationships with our top 10 NPPs average more than 27 years. Over the last five years we have paid our NPPs more than $530 million for goods donated to them. We support both large and small partners alike and offer a reliable, unrestricted source of revenue. Delivered product enables our NPPs to not only generate additional revenue, but also promote awareness of their missions even further throughout the community via collection truck signage, collection bin messaging and home pickup flyers.

On-Site Donations. The quantity and quality of our supply of secondhand items has continued to evolve and improve, particularly as OSDs have grown as a percentage of pounds of goods we process. While it is strategically important for us to maintain a diverse supply mix, items sourced through OSDs have a cost per pound that is on average less than one-third that of delivered supply from our NPPs. Our store footprint has played a critical role in strengthening our OSD intake by accepting OSDs on behalf of our NPPs. Additionally, because OSD volume is primarily driven by convenience, the more we are able to expand our footprint and geographic reach, the more we will be able to attract and procure additional OSD supply, which benefits our growth and margin profiles.

On a comparable store basis, the average store’s OSDs have grown at a 3.5% CAGR from fiscal year 2019 to fiscal year 2023, which has expanded OSDs as a percentage of total pounds processed from 53.0% to 65.2% during the same period. In addition, data analytics have played a critical role in elevating the quality of our delivered supply by enabling us to concentrate on supply sources with quality goods, which has been a significant driver of our gross product margin.

Processing

Overview. The vast majority of all of our retail stores have a dedicated space that handles the processing of soft and hard goods that provide the inventory to be sold on our retail sales floors. In fiscal year 2023, we processed 984 million pounds of secondhand goods. We are currently implementing our offsite processing strategy, which allows us to process goods at a larger-scale facility, such as a CPC, and distribute the goods to multiple stores in a local market. We opened our first CPC in the third quarter of fiscal year 2021, a second CPC in the second quarter of fiscal year 2022, and opened three additional CPCs during fiscal year 2023.

We display approximately 50% of all textile items we receive on our retail sales floors, approximately 50% of which are sold to thrifters. In support of our efforts to extend the life of reusable goods and recover a portion of the cost of acquiring our supply of secondhand items, we sell the majority of textile items unsold at retail to our wholesale customers, predominately comprised of textile graders and small business owners, who supply local communities across the globe with gently-used, affordable items like clothing, housewares, toys and shoes. Textiles not suitable for reuse as secondhand clothing can be repurposed into other textile items (e.g., wiping rags) and post-consumer fibers (e.g., insulation, carpet padding), further reducing waste.

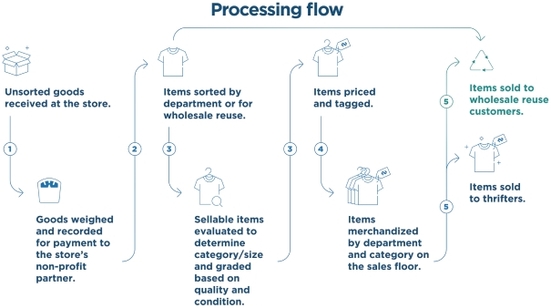

Our process has five sequential and interdependent steps: (1) Receiving; (2) Sorting; (3) Grading and Pricing; (4) Merchandising; and (5) Wholesale. Given the high volumes processed in our stores, effective process management is critical to ensuring each step is done properly and in coordination with the other steps. The typical processing room has approximately 30 team members, each of whom is trained in a specific area with many who are cross trained to support adjacent roles as needed.

Receiving

Upon receipt, most of our supply is separated into either soft goods, hard goods or books and then weighed in aggregate. The weight is then recorded into our inventory management system which initiates the payment process to our NPPs, as defined by their contracted rate. The one exception is the receipt of furniture and other large items which are received and purchased by the piece. The aggregated goods are then staged in designated areas of the processing room.

Sorting

The sorting process consists of emptying the contents of each donated bag or box, separating them by department, and then transferring them to that specific area for further inspection. Each item is inspected and determined to be either salable, unsalable or backstock storage. The salability of an item is based primarily on its quality and condition. Every effort is made by our stores to maximize the extraction of salable items, including the use of well-established analytics which are routinely used by store management. Items deemed unsalable are removed from the processing stream and incorporated into the wholesale process. Salable items that are seasonal are backstocked and stored for future sale during the appropriate season (e.g., winter coats received in the summer). On average, each of our stores evaluate approximately 15,000 items every day.

Grading and pricing

The price for a garment is determined through a grading process that ends with a centrally controlled pricing algorithm. Grading involves a team member assessing a garment for quality and condition relative to other garments within the same category. This enables a more scalable, consistent and comparative approach in determining the value of items for which there are many of the same kind. The grader enters in their assessment and the system generates a price based on an underlying pricing algorithm based on quality and condition for garments in that category. The algorithms are centrally controlled and we conduct routine analyses to monitor price and sales performance.

Merchandising

Priced goods are merchandised in our stores to maximize both customer selection and sales yield using a data-driven approach. Our stores do this by balancing and optimizing three primary levers: (i) allocation of retail floor space, (ii) processing output targets by category, and (iii) sales floor rotation. Our point-of-sale system is integrated with our grading and pricing system which provides visibility into the exact performance for over 200 categories across 10 departments. Our stores routinely modulate each of the three levers in accordance with real-time data analytics available to them.

Additionally, our stores utilize colored price tags which reflect the processing date and enable us to manage the sales floor rotation and retail lifecycle of each item. The system makes it easy for team members to determine the age of each item and distinguish between which should be removed to be sold through wholesale and which should remain on the floor.

Wholesale