Exhibit 99.2

LICHEN CHINA LIMITED

TABLE OF CONTENTS

INDEX TO INTERIM UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

F-1

LICHEN CHINA LIMITED

CONDENSED CONSOLIDATED BALANCE SHEETS

AS OF JUNE 30, 2023 AND DECEMBER 31, 2022

(UNAUDITED)

(All amounts in thousands of USD, except for share and per share data, unless otherwise noted)

June 30, 2023 | December 31, 2022 | |||||||

| Assets | ||||||||

| Current assets: | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable and unbilled receivable | ||||||||

| Inventories | ||||||||

| Prepayments, deposits, and other current assets | ||||||||

| Total current assets | ||||||||

| Property and equipment, net | ||||||||

| Intangible assets, net | ||||||||

| Operating lease – right-of-use asset, net | ||||||||

| Deferred IPO costs | ||||||||

| Prepayments and other non-current assets | ||||||||

| Total assets | $ | $ | ||||||

| Liabilities And Shareholders’ Equity | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | $ | ||||||

| Accrued expenses and other current liabilities | ||||||||

| Unearned revenues | ||||||||

| Taxes payable | ||||||||

| Due to the related parties | ||||||||

| Current maturities of operating lease liability | ||||||||

| Total current liabilities | ||||||||

| Long-term portion of operating lease liability | ||||||||

| Total Liabilities | ||||||||

| Commitments and contingencies | ||||||||

| Shareholders’ equity: | ||||||||

| Class A Ordinary Share, $ | ||||||||

| Class B Ordinary Share, $ | ||||||||

| Additional paid-in capital | ||||||||

| Statutory surplus reserves | ||||||||

| Retained earnings | ||||||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| Total shareholders’ equity | ||||||||

| Total liabilities and shareholders’ equity | $ | $ | ||||||

The accompanying notes are an integral part of these interim unaudited condensed consolidated financial statements.

F-2

LICHEN CHINA LIMITED

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

FOR THE SIX MONTHS ENDED JUNE 30, 2023 AND 2022

(UNAUDITED)

(All amounts in thousands of USD, except for share and per share data, unless otherwise noted)

| June 30, 2023 | June 30, 2022 | |||||||

| Revenues | ||||||||

| Financial and taxation solution services | $ | $ | ||||||

| Education support services | ||||||||

| Software and maintenance services | ||||||||

| Total revenues | ||||||||

| Cost of revenues | ( | ) | ( | ) | ||||

| Gross profit | ||||||||

| Operating expenses: | ||||||||

| Selling and marketing | ( | ) | ( | ) | ||||

| General and administrative | ( | ) | ( | ) | ||||

| Total operating expenses | ( | ) | ( | ) | ||||

| Income from operations | ||||||||

| Other income (expense) | ||||||||

| Other income (expense), net | ( | ) | ||||||

| Interest income | ||||||||

| Income before income tax | ||||||||

| Provision for income tax | ( | ) | ( | ) | ||||

| Net income | $ | $ | ||||||

| Comprehensive income: | ||||||||

| Net income | $ | $ | ||||||

| Foreign currency translation adjustments | ( | ) | ( | ) | ||||

| Comprehensive income | $ | ( | ) | $ | ||||

The accompanying notes are an integral part of these interim unaudited condensed consolidated financial statements.

F-3

LICHEN CHINA LIMITED

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

(UNAUDITED)

(All amounts in thousands of USD, except for share and per share data, unless otherwise noted)

FOR THE SIX MONTHS ENDED JUNE 30, 2023

| Class

A Ordinary Shares (US$ 0.00004 par value) | Class

B Ordinary Shares (US$ 0.00004 par value) | Additional paid-in | Statutory surplus | Retained | Accumulated

other comprehensive | Total

shareholders’ | ||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | capital | reserves | earnings | Income (loss) | equity | ||||||||||||||||||||||||||||

| Balance as of December 31, 2021 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||

| Net income | - | - | ||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | ( | ) | ( | ) | ||||||||||||||||||||||||||||||

| Balance

as of June 30, 2022 | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||||||||||

FOR THE SIX MONTHS ENDED JUNE 30, 2023

| Class A Ordinary Shares (US$ 0.00004 par value) |

Class B Ordinary Shares (US$ 0.00004 par value) |

Additional paid-in |

Statutory surplus |

Retained | Accumulated other comprehensive |

Total shareholders’ |

||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | capital | reserves | earnings | income | equity | ||||||||||||||||||||||||||||

| Balance as of December 31, 2022 | $ | $ | $ | $ | $ | ( |

) | $ | ||||||||||||||||||||||||||||

| Net income | - | - | ||||||||||||||||||||||||||||||||||

| Net Proceeds from the initial public offering | ||||||||||||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | - | ( |

) | ( |

) | ||||||||||||||||||||||||||||||

| Balance as of June 30, 2023 |

$ | $ | $ | $ | $ | ( |

) | $ | ||||||||||||||||||||||||||||

| * |

The accompanying notes are an integral part of these interim unaudited condensed consolidated financial statements.

F-4

LICHEN CHINA LIMITED

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE SIX MONTHS ENDED JUNE 30, 2023 AND 2022

(UNAUDITED)

(All amounts in thousands of USD, except for share and per share data, unless otherwise noted)

| June 30, 2023 |

June 30, 2022 |

|||||||

| Cash flows from operating activities: | ||||||||

| Net income | $ | $ | ||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Depreciation of property and equipment | ||||||||

| Amortization of other assets | ||||||||

| Amortization of right-of-use assets | ||||||||

| Amortization of intangible assets | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | ( |

) | ||||||

| Prepayments and other current assets | ( |

) | ||||||

| Other receivables – related party | ( |

) | ||||||

| Right-of-use-asset costs | ( |

) | ||||||

| Deferred IPO costs | ||||||||

| Accounts payable | ( |

) | ||||||

| Unearned revenues | ( |

) | ( |

) | ||||

| Accrued expenses and other current liabilities | ( |

) | ( |

) | ||||

| Due to related parties | ( |

) | ||||||

| Tax payables | ( |

) | ||||||

| Inventories | ( |

) | ( |

) | ||||

| Net cash (used in ) provided by operating activities | ( |

) | ||||||

| Cash flows from investing activities: | ||||||||

| Purchase of intangible assets | ( |

) | ||||||

| Purchase of property and equipment | ( |

) | ( |

) | ||||

| The deposits for Haicang property | ( |

) | ||||||

| The deposits for ChatGPT Software | ( |

) | ||||||

| The deposits for potential acquisition | ( |

) | ||||||

| Net cash used in investing activities | ( |

) | ( |

) | ||||

| Cash flows from financing activities: | ||||||||

| Repayments on short-term loan | ( |

) | ||||||

| Proceeds from IPO | ||||||||

| Net cash provided by (used in) financing activities | ( |

) | ||||||

| Effects of foreign currency exchange rate changes on cash | ( |

) | ( |

) | ||||

| Net (decrease) increase in cash | ( |

) | ||||||

| Cash, beginning of period | ||||||||

| Cash, end of period | $ | $ | ||||||

| Supplemental disclosure of cash flows information: | ||||||||

| Cash paid for income taxes | $ | $ | ||||||

| Cash paid for interest | $ | $ | ||||||

The accompanying notes are an integral part of these interim unaudited condensed consolidated financial statements.

F-5

Lichen China Limited

NOTES TO INTERIM UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 1. | ORGANIZATION AND NATURE OF OPERATIONS |

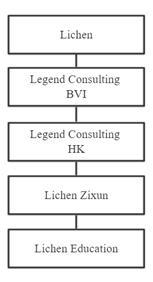

Legend China Limited was incorporated in the Cayman Islands on April 13, 2016 with limited liability. Pursuant to a special resolution dated November 8, 2016, Legend China Limited changed its name to Legend China Ltd. Pursuant to a special resolution dated April 6, 2017, Legend China Ltd. changed its name to Lichen China Limited (“Lichen”).

Lichen is an investment holding company. Through its wholly owned subsidiaries, Lichen is principally engaged in the provision of: (i) financial and taxation solution services; (ii) education support services to partnered institutions; and (iii) software and maintenance services.

| Name of subsidiaries | Place of incorporation |

Date of incorporation |

Percentage of direct or indirect interests |

Principal activities | ||||

| Legend Consulting Investments Limited (“Legend Consulting BVI”) | ||||||||

| Legend Consulting Limited (“Legend Consulting HK”) | ||||||||

| Fujian Province Lichen Management and Consulting Company Limited (“Lichen Zixun”) | ||||||||

| Xiamen City Legend Education Services Company Limited (“Lichen Education”) |

F-6

As shown above, Legend Consulting BVI is an investment holding company wholly owned by Lichen.

Legend Consulting HK is an investment holding company wholly owned by Legend Consulting BVI.

Lichen Zixun, which is wholly owned by Legend Consulting HK, is engaged in providing financial and taxation solution services, education support services, and software and maintenance services.

Lichen Education, which is wholly owned by Lichen Zixun, is engaged in providing financial and taxation solution services and education support services.

Reorganization and Share Issuance

On April 28, 2021, Lichen passed a resolution

to increase the share capital. Pursuant to such resolution, the authorized share capital of Lichen was increased from HK$

On December 15, 2021, Lichen China Limited executed

a special resolution to change the par value of the ordinary shares from $

On February 8, 2023, the Company closed its initial

public offering of

| 2. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

Basis of presentation

These unaudited condensed consolidated financial statements have been prepared in accordance with rules and regulations of the Securities and Exchange Commission (“SEC”) and generally accepted accounting principles in the United States of America (“GAAP”) for interim financial information and with the instructions to Regulation S-X. Accordingly, the unaudited consolidated financial statements do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of management, the Company has included all adjustments considered necessary for a fair presentation and such adjustments are of a normal recurring nature. These unaudited consolidated financial statements should be read in conjunction with the consolidated financial statements for the year ended December 31, 2022 and notes thereto. The results of operations for the six months ended June 30, 2023, are not necessarily indicative of the results to be expected for the full fiscal year ended December 31, 2023

F-7

Principles of consolidation

The condensed consolidated financial statements include the condensed financial statements of Lichen and its wholly owned subsidiaries (collectively, the “Company”). All significant inter-company transactions and balances have been eliminated upon consolidation.

Use of estimate and assumptions

The preparation of the Company’s condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the dates of the condensed consolidated financial statements and the reported amounts of revenues and expenses during the reporting periods presented. Estimates are adjusted to reflect actual experience when necessary. Significant accounting estimates reflected in the Company’s condensed consolidated financial statements include revenue recognition, allowance for doubtful accounts, useful lives of long-lived assets, impairment of long-lived assets, allowance for deferred tax assets, and uncertain tax position. Actual results could differ from these estimates.

Functional currency and foreign currency translation

The reporting currency of the Company is the United States dollar (“US$”). The Company’s operations are principally conducted through its subsidiaries in PRC in the local currency, Renminbi (RMB), as its functional currency. The functional currency of the Company’s entities incorporated in Hong Kong is the Hong Kong dollars (“HK$”). The determination of the respective functional currency is based on the criteria of Accounting Standard Codification (“ASC”) 830, Foreign Currency Matters. Assets and liabilities are translated at the unified exchange rate as quoted by the People’s Bank of China at the balance sheet date. The statement of income accounts are translated at the average exchange rates for the periods and the equity accounts are translated at historical rates. Translation adjustments resulting from this process are included in accumulated other comprehensive income (loss). Transaction gains and losses that arise from exchange rate fluctuations on transactions denominated in a currency other than the functional currency are included in the results of operations as incurred.

Translation adjustments included in accumulated

other comprehensive income (loss) amounted to $

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| Period-end RMB: US$1 exchange rate | ||||||||

| Period-end HK$: US$1 exchange rate | ||||||||

| For the six months ended June 30, | ||||||||

| 2023 | 2022 | |||||||

| Period-average RMB: US$1 exchange rate | ||||||||

| Period-average HK$: US$1 exchange rate | ||||||||

Related parties

Parties, which can be a corporation or individual, are considered to be related if the Company has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Companies are also considered to be related if they are subject to common control or common significant influence, such as a family member or relative, shareholder, or a related corporation.

F-8

Fair value of financial instruments

ASC 825-10 requires certain disclosures regarding the fair value of financial instruments. Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. A three-level fair value hierarchy prioritizes the inputs used to measure fair value. The hierarchy requires entities to maximize the use of observable inputs and minimize the use of unobservable inputs. The three levels of inputs used to measure fair value are as follows:

| ● | Level 1 — inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| ● | Level 2 — inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, quoted market prices for identical or similar assets in markets that are not active, inputs other than quoted prices that are observable and inputs derived from or corroborated by observable market data. |

| ● | Level 3 — inputs to the valuation methodology are unobservable. |

The fair value of the Company’s financial instruments, including cash, accounts receivable, other receivables – related party, accounts payable, due to related parties, and short-term bank loans, approximate their recorded values due to their short-term maturities as of June 30, 2023 and December 31, 2022.

Cash

Cash represents demand deposits placed with banks, which are unrestricted as to withdrawal or use. The Company maintains most of its bank accounts in the PRC.

Accounts receivable and allowance for doubtful accounts

Accounts receivable represents the Company’s right to consideration in exchange for goods and services that the Company has transferred to the customers before payment is due. Accounts receivable is stated at the historical carrying amount, net of an estimated allowance for uncollectible accounts. The Company reviews on a periodic basis for doubtful accounts for the outstanding trade receivable balances based on historical collection trends, aging of receivables and other information available. Additionally, the Company evaluates individual customer’s financial condition, credit history, and the current economic conditions to make specific bad debt provisions when it is considered necessary, based on (i) the Company’s specific assessment of the collectability of all significant accounts; and (ii) any specific knowledge we have acquired that might indicate that an account is uncollectible. The facts and circumstances of each account may require the Company to use substantial judgment in assessing its collectability. The allowance is based on management’s best estimates of specific losses on individual exposures, as well as a provision on historical trends of collections. Account balances are charged off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. The Company’s management continues to evaluate the reasonableness of the valuation allowance policy and update it if necessary. There was no allowance for accounts receivable set up by the Company as of June 30, 2023 and December 31, 2022, respectively.

F-9

Inventories

Inventories are stated at the lower of cost and net realizable value. Cost elements of inventories comprise the purchase price of products, shipping charges to receive products from the suppliers when they are embedded in the purchase price. Cost is determined using the weighted average method. Provisions are made for excessive, slow moving, expired and obsolete inventories as well as for inventories with carrying values in excess of market. Certain factors could impact the realizable value of inventory, so the Company continually evaluates the recoverability based on assumptions about customer demand and market conditions. The evaluation may take into consideration historical usage, inventory aging, expiration date, expected demand, anticipated sales price, product obsolescence and other factors. The reserve or write-down is equal to the difference between the cost of inventory and the estimated net realizable value based upon assumptions about future demand and market conditions. If actual market conditions are less favorable than those projected by management, additional inventory reserves or write-downs may be required that could negatively impact the Company’s gross margin and operating results. If actual market conditions are more favorable, the Company may have higher gross margin when products that have been previously reserved or written down are eventually sold. As of June 30, 2023 and December 31, 2022, management compared the cost of inventories with their net realizable value and determined no inventory write-down was necessary.

Prepayments, deposits and other current assets

Represents cash prepaid to suppliers and cash deposited for acquisition of potential company. The deposits are refundable and bear no interest pursuant to terms of contract. Other current assets represent the monthly withholding social benefits for the staff.

Property and equipment

| Useful Life | Estimated Residual Value | |||||

| Building | | % | ||||

| Motor vehicles | % | |||||

| Furniture and equipment | % | |||||

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the condensed consolidated statements of income and comprehensive income. Expenditures for maintenance and repairs are charged to earnings as incurred, while additions, renewals and betterments, which are expected to extend the useful life of assets, are capitalized. The Company also re-evaluates the periods of depreciation to determine whether subsequent events and circumstances warrant revised estimates of useful lives.

Intangible assets

Intangible assets consist primarily of licensed

software acquired, which are stated at cost less accumulated amortization and impairment, if any. Intangible assets are amortized using

the straight-line method over the estimated useful lives, which are generally

F-10

Impairment of long-lived assets

The Company evaluates its long-lived assets, including property and equipment and intangibles with finite lives, for impairment whenever events or changes in circumstances, such as a significant adverse change to market conditions that will impact the future use of the assets, indicate that the carrying amount of an asset may not be fully recoverable. When these events occur, the Company evaluates the recoverability of long-lived assets by comparing the carrying amount of the assets to the future undiscounted cash flows expected to result from the use of the assets and their eventual disposition. If the sum of the expected undiscounted cash flows is less than the carrying amount of the assets, the Company recognizes an impairment loss based on the excess of the carrying amount of the assets over their fair value. Fair value is generally determined by discounting the cash flows expected to be generated by the assets, when the market prices are not readily available. The adjusted carrying amount of the assets become new cost basis and are depreciated over the assets’ remaining useful lives. Long-lived assets are grouped with other assets and liabilities at the lowest level for which identifiable cash flows are largely independent of the cash flows of other assets and liabilities. Given no events or changes in circumstances indicating the carrying amount of long-lived assets may not be recovered through the related future net cash flows, the Company did not recognize any impairment loss on long-lived assets for the six months ended June 30, 2023 and 2022. There can be no assurance that future events will not have impact on company’s revenue or financial position which could result in impairment in the future.

Contingencies

From time to time, the Company is a party to various legal actions arising in the ordinary course of business. The Company accrues costs associated with these matters when they become probable and the amount can be reasonably estimated. Legal costs incurred in connection with loss contingencies are expensed as incurred. The Company’s management does not expect any liability from the disposition of such claims and litigation individually or in the aggregate would have a material adverse impact on the Company’s consolidated financial position, results of operations and cash flows.

Revenue recognition

The Company adopted ASC Topic 606, Revenue from Contracts with Customers, effective as of January 1, 2019. Accordingly, the condensed consolidated financial statements for the six months ended June 30, 2023 and 2022 are presented under ASC 606. The core principle of the guidance is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Revenue is the transaction price the Company expects to be entitled to in exchange for the promised goods or services in a contract in the ordinary course of the Company’s activities and is recorded net of value-added tax (“VAT”). To achieve that core principle, the Company applies the following steps:

Step 1: Identify the contract (s) with a customer

Step 2: Identify the performance obligations in the contract

Step 3: Determine the transaction price

Step 4: Allocate the transaction price to the performance obligations in the contract

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation

No practical expedients were used when the Company adopted the ASC 606. Revenue recognition policies for each type of revenue stream are as follow:

Financial and taxation solution services

Revenues from financial and taxation solution services for which control of services is transferred over time is recognized progressively based on the contract costs incurred to date (primarily comprising staff costs and industry expert cost by reference to the time as recorded in the monthly working record incurred to date) as compared to the total costs to be incurred under the transaction (by reference to the total budgeted time of the respective project) to depict the Company’s performance in transferring control of services promised to a customer. The Company recognizes revenues over time only if it can reasonably measure its progress toward complete satisfaction of the performance obligation. The Company normally requires the customers to pay a deposit upon entering into the service contracts. Progress payments are normally billed with the final payment received upon completion of the contract.

F-11

Education support services - sales of teaching and learning materials

Revenues from the sales of educational materials for which control of assets is transferred at a point in time is recognized when the goods are delivered to customers. The Company does not provide any sales-related warranties. There is no right of return by customers under the Company’s standard contract terms.

Education support services - Provision of marketing, operation and technical support services

Revenues from provision of marketing, operation and technical support services from the partnered institutions is recognized on a straight-line basis over the term of the partnership agreement. The transaction price inclusive of value added tax as received from customers in advance is recognized as a unearned revenue at the time of the initial transaction and is released on a straight-line basis over the period of service (usually one year).

Software and maintenance services

Standard software is a right to use license because the software has standalone functionality and the customer can use the software as it is available at a point in time. The Company recognizes revenues for such licenses at a point in time when the customer has received licenses and thus has control over the software. In case there is an update of the standard software, end customers or distributors are required to pay additional consideration to buy upgraded version. Revenues from maintenance services is recognized over time within the service period.

Unearned revenues

Unearned revenue is recorded when a payment is received from a customer before the Company transfers the related services. Unearned revenue is recognized as revenue when the Company performs the services under the contract.

| For the six months ended June 30 | ||||||||

| 2023 | 2022 | |||||||

| In thousands of USD | ||||||||

| Revenues: | ||||||||

| Financial and taxation solution services | $ | $ | ||||||

| Education support services | ||||||||

| Software and maintenance services | ||||||||

| Total | $ | $ | ||||||

F-12

Segment reporting

The Company’s Chief Executive Officer, Mr. Ya Li, has been identified as the Company’s chief operating decision-maker (“CODM”), who is responsible for overall performance of all the service lines and reviews of the consolidated results when making decisions about allocating resources and assessing the performance of the Company as a whole. We set up departments by functionality, but not by service lines. All services lines are supervised by one vice president, who directly reports to CEO; and selling and operation functions are supervised by other vice presidents. As our clients from all the three services could be the same, and we treat the services as a whole consulting package to our clients. For example, while providing our financial solution services, we also try to sell our software to the clients to assist them with office software upgrades. Additionally, we do not separate or allocate our research and development activities to selling functions or other supporting functions into these services. The Company prepares the forecast annually by departments instead of services. We set up certain revenue targets by service lines; however, we do not prepare other forecasts by service lines for costs or expenses. Our CEO, the CODM, reviews the forecasts annually and reviews finance performance monthly. He reviews the condensed consolidated balance sheets, statements of operations, and cash flows thoroughly and raises his review comments at the group level. The Board of Directors reviews the finance performance annually at the group level as well. Furthermore, there is no compensation based on the performance of a single service line, as the Company compensation is based on the performance results of the total target set at the beginning of the year, which is based on the whole performance of the three service lines. Hence, the Company has only one single operating segment. The Company does not distinguish between markets or segments for the purpose of internal reporting. The Company’s long-lived assets are all located in the PRC and substantially all of the Company’s revenues are derived from the PRC. Therefore, no geographical segments are presented in these condensed financial statements.

Value added tax (“VAT”)

Revenue represents the invoiced value of goods

and service, net of VAT. The VAT is based on gross sales price and VAT rates range up to

Income taxes

The Company follows the liability method of accounting for income taxes in accordance with ASC 740, Income Taxes. The Company accounts for current income taxes in accordance with the laws of the relevant tax authorities. Deferred income taxes are recognized when temporary differences exist between the tax bases of assets and liabilities and their reported amounts in the condensed consolidated financial statements. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period including the enactment date. Valuation allowances are established, when necessary, to reduce deferred tax assets to the amount expected to be realized.

The Company is not subject to tax on income or capital gain under the current tax laws of U.S. The Company is subject to tax on income or capital gain under the tax laws of PRC.

An uncertain tax position is recognized as a benefit

only if it is “more likely than not” that the tax position would be sustained in a tax examination. The amount recognized

is the largest amount of tax benefit that is greater than

F-13

Statutory surplus reserves

The Company’s PRC subsidiaries are required

to allocate at least

Advertising expenses

Advertising expenditures are expensed as incurred

and such expenses were included as part of selling and marketing expenses. For the six months ended June 30, 2023 and 2022, the advertising

expenses amounted to approximately

Comprehensive income (loss)

Comprehensive income (loss) consists of two components, net income and other comprehensive income (loss). Other comprehensive income (loss) refers to revenue, expenses, gains and losses that under GAAP are recorded as an element of equity but are excluded from net income. Other comprehensive income (loss) consists of a foreign currency translation adjustment resulting from the Company’s subsidiaries not using the U.S. dollar as its functional currencies.

Earnings per ordinary share

The Company computes earnings per ordinary share (“EPS”) in accordance with ASC 260, Earnings per Share. ASC 260 requires companies to present basic and diluted EPS. Basic EPS is measured as net income divided by the weighted average ordinary share outstanding for the period. Diluted EPS presents the dilutive effect on a per-share basis of the potential ordinary shares (e.g., convertible securities, options and warrants) as if they had been converted at the beginning of the periods presented, or issuance date, if later. Potential ordinary shares that have an anti-dilutive effect (i.e., those that increase income per share or decrease loss per share) are excluded from the calculation of diluted EPS.

Recent accounting pronouncements

The Company considers the applicability and impact of all accounting standards updates. Management periodically reviews new accounting standards that are issued

In June 2016, the FASB issued ASU No. 2016-13, “Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments”. This amends guidelines on reporting credit losses for assets held at amortized cost basis and available-for-sale debt securities. For assets held at amortized cost basis, Topic 326 eliminates the probable initial recognition threshold in current U.S. GAAP and, instead, requires an entity to reflect its current estimate of all expected credit losses. The allowance for credit losses is a valuation account that is deducted from the amortized cost basis of the financial assets to present the net amount expected to be collected. For available-for-sale debt securities, credit losses should be measured in a manner similar to current U.S. GAAP, however Topic 326 will require that credit losses be presented as an allowance rather than as a write-down. ASU 2016-13 affects entities holding financial assets and net investment in leases that are not accounted for at fair value through net income. The amendments affect loans, debt securities, trade receivables, net investments in leases, off balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. The amendments in this ASU will be effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years. In November 2019, the FASB issued ASU No. 2019-10, Financial Instruments—Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates, which amended the effective date of ASU 2016-13. The amendments in these ASUs are effective for the Company’s fiscal years, and interim periods within those fiscal years beginning April 1, 2022. The Company has adopted this guidance for the Company’s consolidated financial statements. The adoption of this policy has no material impact.

F-14

Except for the above-mentioned pronouncement, there are no new recent issued accounting standards that will have a material impact on the consolidated financial position, statements of operations and cash flows.

| 3. | Cash |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| RMB | $ | $ | ||||||

| HKD | ||||||||

| Total | $ | $ | ||||||

| 4. | Prepayments, deposits and other current assets |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Deposits to software developer | $ | $ | ||||||

| Prepayments to suppliers | ||||||||

| Prepayments to potential companies | ||||||||

| Prepaid service fee | ||||||||

| Other current assets | ||||||||

| Total | $ | $ | ||||||

On February 27, 2023, the Company (the “Buyer”) entered

into a purchase agreement (the “SPA”) with Mrs. Jianxia Zhuang, a PRC citizen (the “Seller”), and Fujian Hongxing

Management Consulting Co., Limited, registered in Fujian Province (the “Target”), pursuant to which the Company agreed to

purchase

On

February 27, 2023, the Company (the “Buyer”) entered into another purchase agreement (the “SPA”) with Mr. Ya Li,

a PRC citizen (the “Seller”), and two schools named: Quanzhou City Lichen Accounting Vocational Training School (Quanzhou

School) and Jinjiang Xingminqi Accounting Vocational Training School (Jinjiang School), registered in Fujian Province (the “Target”),

pursuant to which the Company agreed to purchase

On March 9, 2023, the Company (the “Buyer”)

entered into a purchase agreement (the “SPA”) with Zhou Zisu, a PRC citizen (the “Seller”), and Bounly Enterprise

Limited, a proprietary company registered in HongKong (the “Target”), pursuant to which the Company agreed to purchase

On February 10, 2023, the Company prepaid $

F-15

| 5. | Property and equipment, net |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Buildings | $ | $ | ||||||

| Furniture and equipment | ||||||||

| Motor vehicles | ||||||||

| Office improvements | ||||||||

| Subtotal | ||||||||

| Less: accumulated depreciation | ( | ) | ( | ) | ||||

| Property and equipment, net | $ | $ | ||||||

Depreciation expenses

for the six months ended June 30, 2023 and 2022 amounted to approximately $

The Company has no pledged property and equipment as of June 30, 2023 and December 31, 2022 to secure general banking facilities.

The Company did not recognize any impairment loss on property and equipment for the six months ended June 30, 2023 and year ended December 31, 2022.

| 6. | Intangible assets |

The Company’s intangible

assets with definite useful lives primarily consisted of licensed software, which are for support the Company’s business and operation.

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Software | $ | $ | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Intangible assets, net | $ | $ | ||||||

Amortization expense

recognized in cost of revenues for the six months ended June 30, 2023 and 2022 amounted to approximately $

The Company has no pledged intangible assets as of June 30, 2023 and December 31, 2022 to secure general banking facilities.

The Company did not recognize any impairment loss on intangible assets for the six months ended June 30, 2023 and year ended December 31, 2022.

F-16

| Twelve months ending June 30, | Amortization expenses | |||

| In thousands of USD | ||||

| 2024 | $ | |||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 | ||||

| Total | $ | |||

| 7. | Leases |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Beijing Office | $ | $ | ||||||

| Exchange gain and loss | ( | ) | ||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Right-of-use assets, net | $ | $ | ||||||

The Company recognized

lease expense amounted to approximately $

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Beijing office | $ | $ | ||||||

| Total operating lease liability | $ | $ | ||||||

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Current maturities of operating lease liability | $ | $ | ||||||

| Long-term portion of operating lease liability | ||||||||

| Total | $ | $ | ||||||

F-17

| Operating lease payment | BJ office | |||

| Discount rate at commencement | % | |||

| One year | $ | |||

| Two years | ||||

| Total undiscounted cash flows | $ | |||

| Total financing lease liabilities | ||||

| Difference between undiscounted cash flows and discounted cash flows | ||||

The incremental borrowing

rate for the Company is

The lease agreement of

Office was entered into on March 29, 2022, bears interest at about

| 8. | Prepayments and other non-current assets |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Prepayments to software developer | $ | $ | ||||||

| Prepayments to Haicang property | ||||||||

| Other current assets | ||||||||

| Total | $ | $ | ||||||

On May 5, 2023, the Company made a deposit of

On May 18, 2023, the Company (the “Buyer”)

entered into a pre-sale agreement with Xiamen Haicang District People’s Government (the “Seller”), pursuant to which

the Company agreed to purchase the Service industrial park building, located in Haicang District of Xiamen City. The buyer immediately

pays $

F-18

| 9. | Related party transactions and balances |

| Name of related parties | Relationship with the Company | |

| Jinjiang Xingminqi Accounting Vocational Training School (“Jinjiang School”) |

||

| Quanzhou City Lichen Accounting Vocational Training School (“Quanzhou School”) |

| i) |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2022 | |||||||

| In thousands of USD | ||||||||

| Provision of marketing, operation and technical support services to Jinjiang School | $ | $ | ||||||

| Provision of marketing, operation and technical support services to Quanzhou School | ||||||||

| Processing of academic education applications to Jinjiang School | ||||||||

| Processing of academic education applications to Quanzhou School | ||||||||

| Sales of teaching and learning materials to Jinjiang School | ||||||||

| Sales of teaching and learning materials to Quanzhou School | ||||||||

| Online training to Jinjiang School | ||||||||

| Online training to Quanzhou School | ||||||||

| Total revenues – related parties | $ | $ | ||||||

| ii) |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Due to related parties | ||||||||

| Quanzhou School | $ | $ | ||||||

| Jinjiang School | $ | $ | ||||||

| Ya Li | $ | $ | ||||||

| Total Due to related parties | $ | $ | ||||||

Balances due to Quanzhou school, Jinjiang school and Ya Li are the result of the normal business transactions stated above. The balances were all unsecured, non-interest bearing and payable on demand.

F-19

| 10. | Accrued expenses and other current liabilities |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Accrued payroll | $ | $ | ||||||

| Other | ||||||||

| Total | $ | $ | ||||||

| 11. | Unearned revenue |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Unearned revenue | $ | $ | ||||||

| Total | $ | $ | ||||||

| 12. | Taxes |

| (a) | Taxes payable |

| As of June 30, 2023 | As of December 31, 2022 | |||||||

| In thousands of USD | ||||||||

| Income tax payable | $ | $ | ||||||

| VAT payable | ||||||||

| Other tax payable | ||||||||

| Total | $ | $ | ||||||

| (b) | Corporate Income Taxes (“CIT”) |

Cayman Islands

Under the current tax laws of Cayman Islands, the Company is not subject to tax on income or capital gain. Additionally, the Cayman Islands does not impose a withholding tax on payments of dividends to shareholders.

BVI

Under the current tax laws of BVI, the Company is not subject to tax on income or capital gain. Additionally, the BVI does not impose a withholding tax on payments of dividends to shareholders.

Hong Kong

Under the current Hong

Kong Inland Revenue Ordinance, the Company’s subsidiaries incorporated in Hong Kong are subject to

F-20

PRC

The Company’s PRC

subsidiaries are governed by the income tax laws of the PRC and the income tax provision in respect to operations in the PRC is calculated

at the applicable tax rates on the taxable income for the periods based on existing legislation, interpretations and practices in respect

thereof. Under the Enterprise Income Tax Laws of the PRC (the “EIT Laws”), domestic enterprises and Foreign Investment Enterprises

(the “FIE”) are usually subject to a unified

| i) |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2022 | |||||||

| In thousands of USD | ||||||||

| Provisions for current income tax | $ | $ | ||||||

| Provisions for deferred income tax | ||||||||

| Total | $ | $ | ||||||

There are no deferred tax assets recognized or impaired for the six months ended June 30, 2023 and 2022.

| ii) | The following table reconciles PRC statutory rates to the Company’s effective tax rate: |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2022 | |||||||

| PRC statutory income tax rate | % | % | ||||||

| Effect of different tax jurisdiction | % | % | ||||||

| Non-deductible expenses (1) | % | % | ||||||

| Change in valuation allowance | % | % | ||||||

| Effective income tax rate | % | % | ||||||

| (1) |

F-21

| iii) |

| For the six months ended June 30, 2023 | For the six months ended June 30, 2022 | |||||||

| Deferred tax assets: | In thousands of USD | |||||||

| Net accumulated loss-carry forward | $ | $ | ||||||

| Less: valuation allowance | ( | ) | ( | ) | ||||

| Net deferred tax assets | $ | $ | ||||||

| For the six months ended June 30, 2023 | For the six months ended June 30, 2022 | |||||||

| In thousands of USD | ||||||||

| Beginning balance | $ | $ | ||||||

| Write-off | ( | ) | ( | ) | ||||

| Change of valuation allowance | ||||||||

| Ending balance | $ | $ | ||||||

Certain subsidiaries had tax loss of approximately

$

Uncertain tax positions

The Company evaluates each uncertain tax position (including the potential application of interest and penalties) based on the technical merits, and measure the unrecognized benefits associated with the tax positions. As of June 30, 2023 and December 31, 2022, the Company did not have any significant unrecognized uncertain tax positions. The Company did not incur interest and penalties during the six months ended June 30, 2023 and 2022.

| 13. | Ordinary share |

The Company was established as a holding company

under the laws of Cayman Islands. The Company’s authorized share capital of US$

On February 6, 2023,

the Company announced the closing of its initial public offering of

F-22

| 14. | Statutory surplus reserves |

The Company is required

to make appropriations to certain reserve funds, comprising the statutory surplus reserve and the discretionary surplus reserve, based

on after-tax net income determined in accordance with generally accepted accounting principles of the PRC (“PRC GAAP”). Appropriations

to the statutory surplus reserve are required to be at least

| 15. | Restricted assets |

The Company’s ability to pay dividends is primarily dependent on the Company receiving distributions of funds from its subsidiary. Relevant PRC statutory laws and regulations permit payments of dividends by the PRC subsidiaries only out of its retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. The results of operations reflected in the accompanying condensed consolidated financial statements prepared in accordance with U.S. GAAP differ from those reflected in the statutory condensed financial statements of the PRC entities.

The PRC entities are

required to set aside at least

As a result of the foregoing restrictions, the

PRC entities are restricted in their ability to transfer their assets to the Company. Foreign exchange and other regulation in the PRC

may further restrict the PRC entities from transferring funds to the Company in the form of dividends, loans and advances. As of June

30, 2023 and December 31, 2022, amounts restricted are the paid-in-capital and statutory reserve of the PRC entities, which amounted to

$

Although there are undistributed earnings of the Company’s subsidiaries in the PRC that are available for distribution to the Company, the undistributed earnings of the Company’s subsidiaries located in the PRC are considered to be indefinitely reinvested, because the Company does not have any present plan to pay any cash dividends on its ordinary shares in the foreseeable future and intends to retain most of its available funds and any future earnings for use in the operation and expansion of its business. Accordingly, no deferred tax liability has been accrued for the PRC dividend withholding taxes that would be payable upon the distribution of those amounts to the Company as of June 30, 2023 and December 31, 2022.

| 16. | Risks and Concentration |

| a) | Interest rate risk |

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market interest rates. The Company’s interest rate risk arises primarily from short-term borrowings. Borrowings issued at variable rates and fixed rates expose the Company to cash flow interest rate risk and fair value interest rate risk respectively.

F-23

| b) | Concentration of credit risk |

Financial instruments

that potentially subject the Company to significant concentrations of credit risk consist primarily of cash. As of June 30, 2023 and December

31, 2022, approximately $

The Company is also exposed to risk from its accounts receivable and other receivables. These assets are subjected to credit evaluations. An allowance has been made for estimated unrecoverable amounts which have been determined by reference to past default experience and the current economic environment.

A majority of the Company’s expense transactions are denominated in RMB and a significant portion of the Company and its subsidiaries’ assets and liabilities are denominated in RMB. RMB is not freely convertible into foreign currencies. In the PRC, certain foreign exchange transactions are required by law to be transacted only by authorized financial institutions at exchange rates set by the People’s Bank of China (“PBOC”). Remittances in currencies other than RMB by the Company in China must be processed through the PBOC or other China foreign exchange regulatory bodies which require certain supporting documentation in order to affect the remittance.

The Company’s functional

currency is RMB, and its condensed consolidated financial statements are presented in U.S. dollars. The RMB depreciated by

To the extent that the Company needs to convert U.S. dollars into RMB for capital expenditures and working capital and other business purposes, appreciation of RMB against U.S. dollar would have an adverse effect on the RMB amount the Company would receive from the conversion. Conversely, if the Company decides to convert RMB into U.S. dollar for the purpose of making payments for dividends, strategic acquisition or investments or other business purposes, appreciation of U.S. dollar against RMB would have a negative effect on the U.S. dollar amount available to the Company.

| c) | Concentration of customers and suppliers |

All revenue was derived

from customers located in PRC. There are no customers from whom revenues individually represent greater than

For the six months ended

June 30, 2023, Beijing Duoying Times Culture Media Co., Ltd, Jimei University and Guangzhou Xingjinhui Trade Co., Ltd contributed approximately

F-24

| 17. | Commitments and contingencies |

| (a) | Commitments |

The Company did not have any significant commitments, long-term obligations, or guarantees as of June 30, 2023.

| (b) | Contingencies |

The Company is subject to legal proceedings and regulatory actions in the ordinary course of business. The results of such proceedings cannot be predicted with certainty, but the Company does not anticipate that the final outcome arising out of any such matter will have a material adverse effect on our consolidated financial position, cash flows or results of operations on an individual basis or in the aggregate. As of June 30, 2023, the Company is not a party to any material legal or administrative proceedings.

| 18. | Subsequent events |

On August 28, 2023, the Company terminated the purchase agreement (the

“SPA”) with Mrs. Jianxia Zhuang, a PRC citizen (the “Seller”), and Fujian Hongxing Management Consulting Co.,

Limited potential acquisition after due diligence with unsatisfactory performance and withdraw the full payment of $

On September 12, 2023, the Company terminated

another purchase agreement (the “SPA”) with Mr. Ya Li, a PRC citizen (the “Seller”), and two schools named: Quanzhou

City Lichen Accounting Vocational Training School (Quanzhou School) and Jinjiang Xingminqi Accounting Vocational Training School (Jinjiang

School)potential acquisition after comprehensive consideration on the unsatisfactory performance of the Targets from the due diligence.

Mr. Ya Li has returned back the deposits of $

In preparing these condensed consolidated financial statements, the Company has evaluated events and transactions for potential recognition or disclosure through October 11, 2023, the date the condensed consolidated financial statements were available to be issued. No events require adjustment to or disclosure in the condensed consolidated financial statements.

F-25