UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

_________________________

FORM 20-F

_________________________

(Mark One)

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(B) OR 12(G) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

OR

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

Commission File Number: 001-41329

_________________________

(Exact Name of Registrant as Specified in Its Charter)

_________________________

| Not applicable | The | ||||

| (Translation of Registrant’s Name Into English) | (Jurisdiction of Incorporation or Organization) | ||||

Allego N.V.

(Address of Principal Executive Offices)

+31 (0) 88 033 3033

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

_________________________

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: As of December 31, 2023, Allego N.V. had 271,010,790 ordinary shares outstanding.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | x | Non-accelerated filer | o | |||||||||||||

| Emerging growth company | |||||||||||||||||

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. o

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting over Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| US GAAP | o | by the International Accounting Standards Board | x | Other | o | ||||||||||||

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 o Item 18 o

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

TABLE OF CONTENTS

Financial Statement Presentation | |||||

Industry and Market Data | |||||

F-1 | |||||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F (this “Annual Report”) contains forward-looking statements as defined in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995, that involve significant risks and uncertainties. All statements other than statements of historical facts are forward-looking statements. These forward-looking statements include information about our possible or assumed future results of operations or our performance.

Words such as, “anticipate,” “appear,” “approximate,” “believe,” “continue,” “could,” “estimate,” “expect,” “foresee,” “intends,” “indicates,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “would” and variations of such words and similar expressions (or the negative version of such words or expressions) may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. The risk factors and cautionary language referring to or incorporated by reference in this Annual Report provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described in our forward-looking statements, including among other things, the items identified in the section entities “Item 3. Key Information—D. Risk Factors” of this Annual Report. Forward-looking statements in this Annual Report may include, for example, statements about:

•the ability of Allego to cure the minimum share price deficiency and regain compliance with NYSE listing standards and for Allego’s ordinary shares to remain listed on the NYSE;

•changes adversely affecting Allego’s business;

•the price and availability of electricity and other energy sources;

•the risks associated with vulnerability to industry downturns and regional or national downturns;

•fluctuations in Allego’s revenue and operating results;

•unfavorable conditions or further disruptions in the capital and credit markets;

•Allego’s ability to generate cash, service indebtedness and incur additional indebtedness;

•competition from existing and new competitors;

•the agreement of various landowners to deployment of Allego charging stations;

•the growth of the electric vehicle market;

•Allego’s ability to integrate any businesses it may acquire;

•Allego’s ability to recruit and retain experienced personnel;

•risks related to legal proceedings or claims, including liability claims;

•Allego’s dependence on third-party contractors to provide various services;

•data security breaches or other network outages;

•Allego’s ability to obtain additional capital on commercially reasonable terms;

•Allego’s ability to remediate its material weaknesses in internal control over financial reporting;

•the impact of a pandemic or other health crises, including related supply chain disruptions and expense increases;

•general economic or political conditions, including the Russia/Ukraine and Israel/Hamas conflicts or increased trade restrictions between the United States, Russia, China and other countries; and

•other factors detailed under the section entitled “Item 3. Key Information—D. Risk Factors” in this Annual Report and in Allego’s other filings with the SEC.

Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this Annual Report. Although we believe that the expectations reflected in such forward-looking statements are reasonable, there can be no assurance that such expectations will prove to be correct. These statements involve known and unknown risks and are based upon a number of assumptions and estimates, which are inherently subject to significant uncertainties and contingencies, many of which are beyond our control. Actual results may differ materially from those expressed or implied by such forward-looking statements. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

FINANCIAL STATEMENT PRESENTATION

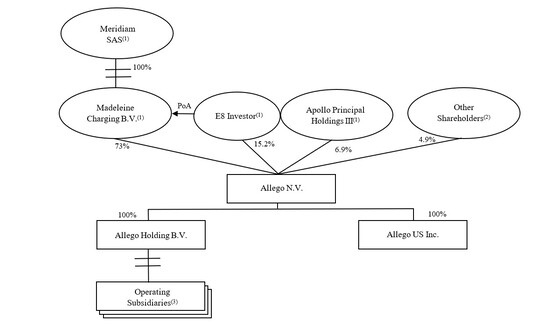

Athena Pubco B.V. was incorporated by Madeleine Charging B.V. on June 3, 2021 for the purpose of effectuating the Business Combination. Prior to the Business Combination, Athena Pubco B.V., which was redesignated as Allego N.V. in connection with the Closing, had no material assets and did not operate any businesses. The Business Combination resulted in Allego acquiring Allego Holding and combining with Spartan, with an exchange of the shares and warrants issued by

ii

Spartan for those of Allego. The Business Combination was accounted for as a capital reorganization followed by the combination with Spartan, which was treated as a recapitalization. Following the Business Combination, both Allego Holding and Spartan are wholly owned subsidiaries of Allego.

INDUSTRY AND MARKET DATA

In this Annual Report, we present industry data, forecasts, information and statistics regarding the markets in which Allego competes as well as Allego management’s analysis of statistics, data and other information that it has derived from third-parties, including independent consultant reports, publicly available information, various industry publications and other published industry sources, including: (i) traffic data from governmental agencies, such as Germany’s BAST (Bundesanstalt für Straßenwesen), the Netherlands’ Rijkswaterstaat, and the United Kingdom’s Department of Transport, (ii) population data from EUROSTAT, (iii) registered cars data from governmental statistics agencies, such as Germany’s Kraftfahrt Bundesamt, the Netherlands’ CBS (Centraal Bureau voor de Statistiek) and the United Kingdom’s Department of Transport, (iv) electric vehicle sales forecasts from consultancy firms, such as ING, UBS, BCG and Navigant, (v) electric vehicle sales data from the European Automobile Manufacturers’ Association, and (vi) industry growth forecasts from BloombergNEF. Independent consultant reports, industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be reliable. Such information is supplemented where necessary with our own internal estimates and information obtained from discussions with our customers, taking into account publicly available information about other industry participants and our management’s judgment where information is not publicly available. This information appears in “Item 4. Information on the Company—B. Business Overview,” “Item 5. Operating and Financial Review and Prospects” and other sections of this Annual Report.

Although we believe that these third-party sources are reliable, we cannot guarantee the accuracy or completeness of this information, and we have not independently verified this information. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this Annual Report. These forecasts and forward-looking information are subject to uncertainty and risk due to a variety of factors, including those described under “Item 3. Key Information—D. Risk Factors.” These and other factors could cause results to differ materially from those expressed in any forecasts or estimates. Some market data and statistical information are also based on our good faith estimates, which are derived from management’s knowledge of our industry and such independent sources referred to above. Certain market, ranking and industry data included elsewhere in this Annual Report, including the size of certain markets and our size or position and the positions of our competitors within these markets, including its services relative to its competitors, are based on estimates by us. These estimates have been derived from Allego management’s knowledge and experience in the markets in which Allego operates, as well as information obtained from surveys, reports by market research firms, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which Allego operates and have not been verified by independent sources. Unless otherwise noted, all of Allego’s market share and market position information presented in this Annual Report is an approximation. Allego’s market share and market position, unless otherwise noted, is based on Allego’s volume relative to the estimated volume in the markets served by Allego’s business segments. References herein to Allego being a leader in a market or product category refer to Allego management’s belief that Allego has a leading market share position in each specified market, unless the context otherwise requires. As there are no publicly available sources supporting this belief, it is based solely on Allego management’s internal analysis of Allego volume as compared to the estimated volume of its competitors.

Internal data and estimates are based upon information obtained from trade and business organizations and other contacts in the markets in which Allego operates and Allego management’s understanding of industry conditions. Although we believe that such information is reliable, this information has not been verified by any independent sources.

DEFINED TERMS

“Allego”, the “Company”, “we”, “us” and “our” means (i) prior to the consummation of the Business Combination, Allego Holding B.V. and (ii) following the consummation of the Business Combination, Allego N.V. Simultaneously with Closing, Athena Pubco B.V. was redesignated as Allego N.V., such that the go-forward public company is Allego N.V.

“Allego Articles” or “Articles” means the articles of association of Allego N.V. contained in the notarial deed of conversion and amendment of the articles of association of Allego N.V. dated March 16, 2022.

“Allego Board” or “Board” means the board of directors of Allego.

iii

“Allego Holding” means Allego Holding B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid).

“Allego Ordinary Shares” or “Ordinary Shares” means the ordinary shares of Allego N.V. immediately following the Business Combination, with a nominal value of €0.12 per share.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement and Plan of Reorganization, dated as of July 28, 2021, by and among Allego, Allego Holding, Merger Sub, Spartan, Madeleine, and, solely with respect to the sections specified therein, E8 Investor.

“Closing” means the consummation of the Business Combination.

“Closing Date” means the date on which the Closing took place.

“E8 Investor” means E8 Partenaires, a French société par actions simplifée.

“First Special Fees Agreement” means the first agreement pursuant to which E8 Investor provided services to the Group relating to the strategic and operational advice for one or more contemplated share transactions. The agreement was terminated in connection with the Business Combination in 2022.

“General Meeting” means the general meeting of Allego.

“Group” means Allego Holding B.V. and its subsidiaries prior to the completion of the Business Combination and Allego N.V. and its subsidiaries after the completion of the Business Combination, unless indicated requires otherwise.

“IFRS” means International Financial Reporting Standards as issued by the International Accounting Standards Board.

“LTIP” means the Allego Long-Term Incentive Plan.

“Madeleine” means Madeleine Charging B.V., a Dutch private limited liability company (besloten vennootschap met beperkte aansprakelijkheid).

“Mega-E” means Mega-E Charging B.V. and “Mega-E Group” means Mega-E and its subsidiaries.

“MOMA” means Modélisation, Mesures et Applications S.A., an unlisted software company.

“Merger Sub” means Athena Merger Sub, Inc., a Delaware corporation.

“NYSE” means the New York Stock Exchange.

”PIPE” means the commitments obtained from certain investors for a private placement of an aggregate of 15,000,000 Allego Ordinary Shares, for a purchase price of $10.00 per share and an aggregate purchase price of $150,000,000.

“Private Placement Warrants” means the warrants issued to the Sponsor in a private placement simultaneously with the closing of Spartan’s IPO.

“Public Warrants” means the warrants sold as part of the Spartan Units.

“SEC” means the United States Securities and Exchange Commission.

“Second Special Fees Agreement” has meaning provided in “Item 7. Major Shareholders and Related Party Transactions—B. Related Party Transactions” in this Annual Report.

“Spartan” means Spartan Acquisition Corp. III, a Delaware corporation, prior to the Business Combination and Allego US Inc., a Delaware corporation, following completion of the Business Combination, unless indicated otherwise.

iv

“Spartan Class A Common Stock” means Spartan’s Class A common stock, par value $0.0001 per share.

“Spartan Founders Stock” means Spartan’s Class B common stock, par value $0.0001 per share.

“Spartan Units” means the units sold in connection with Spartan’s IPO.

“Spartan Warrants” means the Private Placement Warrants and the Public Warrants, collectively.

“Special Fees Agreements” mean the First Special Fees Agreement and the Second Special Fees Agreement.

“Sponsor” means Spartan Acquisition Sponsor III LLC, a Delaware limited liability company.

“Warrant Agreement” means the Warrant Agreement dated February 8, 2021 by and between Spartan and Continental Stock Transfer & Trust Company.

“Warrants” or “Assumed Warrants” means the Spartan Warrants that were automatically converted in connection with the Business Combination into warrants to acquire one Allego Ordinary Share, and remain subject to the same terms and conditions (including exercisability) as were applicable to the corresponding Spartan Warrant immediately prior to the Business Combination.

v

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A.[RESERVED]

B.Capitalization and Indebtedness

Not applicable.

C.Reasons For the Offer and Use of Proceeds

Not applicable.

D.Risk Factors

Summary Risk Factors

The following summarizes some, but not all, of the risks provided below. Please carefully consider all of the information discussed in this “Item 3. Risk Factors—D. Risk Factors.” in this Annual Report for a detailed description of these risks.

•Allego is an early stage company with a history of operating losses, and expects to incur significant expenses and continuing losses for the near term and medium term.

•Allego has experienced growth and expects to invest substantially in growth for the foreseeable future. If it fails to manage growth effectively, its business, operating results and financial condition could be adversely affected.

•Allego’s forecasts and projections are based upon assumptions, analyses and internal estimates developed by Allego’s management. If these assumptions, analyses or estimates prove to be incorrect or inaccurate, Allego’s actual operating results may differ adversely and materially from those forecasted or projected.

•Allego’s estimates of market opportunity and forecasts of market growth may prove to be inaccurate.

•Allego’s business is subject to risks associated with the price of electricity, which may hamper its profitability and growth.

•Allego is dependent on the availability of electricity at its current and future charging sites. Delays and/or other restrictions on the availability of electricity (for example, grid connections delays) would adversely affect Allego’s business and results of operations.

•Allego currently faces competition from a number of companies and expects to face significant competition in the future as the market for EV charging develops.

•Allego’s future revenue growth will depend in significant part on its ability to increase the number and size of its charging sites, traffic, and the sales of services to Business to Business customers.

•Allego may need to raise additional funds or debt and these funds may not be available when needed.

•If Allego fails to offer high-quality support to its customers and fails to maintain the availability of its charging points, its business and reputation may suffer.

1

•Allego relies on a limited number of suppliers and manufacturers for its hardware and equipment and charging stations. A loss of any of these partners or issues in their manufacturing and supply processes could negatively affect its business.

•Allego’s EV driver base will depend upon the effective operation of Allego’s EVCloudTM platform and its applications with mobile service providers, firmware from hardware manufacturers, mobile operating systems, payment systems, networks and standards that Allego does not control.

•If Allego is unable to attract and retain key employees and hire qualified management, technical, engineering and sales personnel, its ability to compete and successfully grow its business would be harmed.

•Allego is expanding operations in many countries in Europe, which will expose it to additional tax, compliance, market, local rules and other risks.

•New alternative fuel technologies may negatively impact the growth of the EV market and thus the demand for Allego’s charging stations and services.

•The European EV market currently benefits from the availability of rebates, scrappage schemes, tax credits and other financial incentive schemes from governments to offset and incentivize the purchase of EVs. The reduction, modification, or elimination of such benefits could cause reduced demand for EVs and EV charging, which would adversely affect Allego’s financial results.

•Allego’s business may be adversely affected if it is unable to maintain, protect or enforce its rights in its technology and intellectual property.

•Computer malware, viruses, ransomware, hacking, phishing attacks and similar disruptions could result in security and privacy breaches and interruption in service, which could harm Allego’s business.

•Allego’s technology could have undetected defects, errors or bugs in hardware or software which could reduce market adoption, damage its reputation with current or prospective customers, and/or expose it to product liability and other claims that could materially and adversely affect its business.

•Allego has identified, and has previously identified, material weaknesses in its internal control over financial reporting. If Allego is unable to remediate these material weaknesses, or if Allego identifies additional material weaknesses in the future or otherwise fails to maintain an effective system of internal control over financial reporting, this may result in material misstatements contained within Allego’s consolidated financial statements or cause Allego to fail to meet its periodic reporting obligations.

•Members of Allego’s management have limited experience in operating a public company.

•Future sales, or the perception of future sales, of our Ordinary Shares by us or selling security holders, including Madeleine, could cause the market price for our Ordinary Shares to decline significantly.

•Madeleine owns a significant amount of Allego’s voting shares and its interests may conflict with those of other shareholders.

Shareholders should carefully consider the following factors in addition to the other information set forth in this Annual Report. If any of the following risks actually occur, our business, financial condition and results of operations and the value of Allego Ordinary Shares would likely suffer.

Risks Related to Allego’s Business, Industry and Regulatory Environment

Allego is an early stage company with a history of operating losses, and expects to incur significant expenses and continuing losses for the near term and medium term.

Allego incurred a net loss of €110.3 million and €305.3 million for the years ended December 31, 2023 and December 31, 2022, respectively, and as of December 31, 2023, Allego had total equity of approximately €79.3 million. Allego believes it will continue to incur net losses for the near term. Even if it achieves profitability, there can be no assurance that it will be able maintain profitability in the future. Allego’s potential profitability is particularly dependent upon the continued adoption of electric vehicles (“EVs”) by consumers in Europe, which may occur at a slower pace than anticipated or may

2

not occur at all. This continued adoption may depend upon continued support from regulatory programs and in each case, the use of Allego chargers and Allego services may be at much lower levels than Allego currently anticipates.

Allego has experienced growth and expects to invest substantially in growth for the foreseeable future. If it fails to manage growth effectively, its business, operating results and financial condition could be adversely affected.

Allego has experienced growth in recent periods that has placed and continues to place a significant strain on employee retention, management, operations, financial infrastructure and corporate culture and has required several strategic adjustments. Allego’s revenue has increased from €133.9 million in 2022 to €145.5 million in 2023. In addition, in the event of further growth, Allego’s information technology systems and Allego’s internal control over financial reporting and procedures may not be adequate to support its operations and may increase the risk of data security incidents that may interrupt business operations and permit bad actors to obtain unauthorized access to business information or misappropriate company funds. Allego may also face risks to the extent such bad actors infiltrate the information technology infrastructure of its contractors. Allego may also face the risk that EVCloudTM, its core platform, is not able to support Allego’s growth due to increased traffic on Allego charging points, which would interrupt business operations. Allego could then also face contractual penalties with its customers if this results in a failure to meet its contractual obligations.

To manage growth in operations and personnel management, Allego will need to continue to improve its operational, financial and management controls and reporting systems and procedures. Failure to manage growth effectively could result in difficulty or delays in developing new EV charging sites, in attracting new customers, declines in quality or customer satisfaction, increases in costs, difficulties in introducing new solutions and services or enhancing existing solutions and services, loss of EV sites and customers, information security vulnerabilities or other operational difficulties, any of which could adversely affect its business performance and operating results.

Allego’s forecasts and projections are based upon assumptions, analyses and internal estimates developed by Allego’s management. If these assumptions, analyses or estimates prove to be incorrect or inaccurate, Allego’s actual operating results may differ adversely and materially from those forecasted or projected.

Allego’s business forecasts and projections are subject to different parameters with significant uncertainty and are based on assumptions, analyses and internal estimates developed by Allego’s management and teams, any or all of which may not prove to be correct or accurate. If these assumptions, analyses or estimates prove to be incorrect or inaccurate, Allego’s actual operating results may differ materially and adversely from those forecasted or projected. Realization of the operating results forecasted will depend on the successful implementation of Allego’s proposed business plan, and the development of policies and procedures consistent with Allego’s assumptions. Future results will also be affected by events and circumstances beyond Allego’s control, for example, the competitive environment, Allego’s executive team, technological change, economic and other conditions in the markets in which Allego operates or proposes to operate, national and regional regulations, uncertainties inherent in product and software development and testing, Allego’s future financing needs, and Allego’s ability to grow and to manage growth effectively. In particular, Allego’s forecasts and projections include forecasts and estimates relating to the expected size and growth of the markets in which Allego operates in Europe or seeks to enter and demand for its current and future charging points. For the reasons described above, it is likely that the actual results of its operations will be different from the results forecasted and those differences may be material and adverse.

Allego’s estimates of market opportunity and forecasts of market growth may prove to be inaccurate.

Market opportunity estimates and growth forecasts, whether obtained from third-party sources or developed internally, are subject to significant uncertainty and are based on assumptions and estimates that may prove to be inaccurate. Estimates and forecasts relating to the size and expected growth of the target market, market demand, EV adoption across each individual national market in Europe and use cases, capacity of automotive and battery original equipment manufacturers (“OEMs”) and ability of charging infrastructure to address this demand and related pricing may also prove to be inaccurate. In particular, estimates regarding the current and projected market opportunity for public fast and ultra-fast charging or Allego market share capture are difficult to predict. The estimated addressable market may not materialize in the timeframe of the projections, if ever, and even if the markets meet the size estimates and growth estimates, Allego’s business could fail to grow at similar rates.

Allego’s business is subject to risks associated with the price of electricity, which may hamper its profitability and growth.

Allego obtains electricity for its own charging stations through contracts with power suppliers or through direct sourcing on the market from producers. In most of the countries in which Allego operates, there are many suppliers that can offer medium or long-term contracts that can allow Allego to hedge the price of electricity. However, market conditions may

3

change, triggering fluctuations and global increases in the price of electricity. For example, the price of electricity is generally higher in the winter due to higher electricity demands, and Europe experience record high electricity price increases in 2022 caused in large part by the Russia/Ukraine conflict. While these costs could be passed on to EV customers, increases in the price of electricity could result in near-term cash flow strains to Allego. In addition, global increases in electricity pricing will increase the price of charging, which could impact demand and hamper the use of public charging by EV customers, thus decreasing the number of charging sessions on Allego’s charging stations and adversely impacting its profitability and growth. Furthermore, competitors may be able to source electricity on better terms than Allego, which may allow those competitors to offer lower prices for charging, which may also decrease the number of charging sessions on Allego’s charging stations and adversely impact its profitability and growth.

Allego is dependent on the availability of electricity at its current and future charging sites. Delays and/or other restrictions on the availability of electricity (for example, grid connections delays) would adversely affect Allego’s business and results of operations.

The operation and development of Allego’s charging points is dependent upon the availability of electricity, which is beyond its control. Allego’s charging points are affected by problems accessing electricity sources, such as planned or unplanned power outages or limited grid capacity. In the event of a power outage, Allego will be dependent on the grid operator, and in some cases the site host, to restore power for its B2B solutions or to unlock grid capacity. Any prolonged power outage or limited grid capacity could adversely affect customer experience and Allego’s business and results of operations.

Allego’s public charging points may be exposed to vandalism or misuse by customers and other individuals, increasing wear and tear of the charging equipment. Such increased wear and tear could shorten the usable lifespan of the chargers and require Allego to increase its spending on replacement and maintenance costs.

Allego currently faces competition from a number of companies and expects to face significant competition in the future as the market for EV charging develops.

The EV charging market is relatively new, and competition is still developing. Apart from China, Europe is currently the biggest EV market in the world and is currently more mature than the United States. Allego competes in its charging network and services businesses with many competitors in different countries. With respect to the development of its own ultra-fast public EV charging network, Allego primarily competes with incumbent utilities and oil and gas companies alongside pure EV charging players and companies linked to car manufacturers. With respect to its services business, Allego competes with a variety of companies, including hardware manufacturers, software platform vendors, installation companies and maintenance contractors. Despite Allego’s longstanding European presence, it must continuously strive to remain competitive in its markets. Competition may hamper global EV adoption as an influx of providers may lead to poor service and trust in any one provider of EV charging solutions.

In addition, there are means for charging EVs other than publicly accessible charging, which could affect the level of demand for onsite charging capabilities at public or commercial areas, which are Allego’s primary focus. For example, Tesla Inc. ("Tesla") continues to build out its supercharger network across Europe for its vehicles, which could reduce overall demand for EV charging at other sites. Tesla is also opening its supercharger network to support charging of non-Tesla EVs, which could further reduce demand for charging at Allego’s sites. Additionally, third-party contractors can provide basic electric charging capabilities to potential customers of Allego, including commercial on premise charging and home charging solutions. Many EV hardware manufacturers are now offering home charging equipment, which could reduce demand for public charging if EV owners find charging at home to be more convenient. Regulations imposing home or workplace charging capabilities for all new buildings could also adversely affect the development of public charging versus home charging.

Furthermore, Allego’s current or potential competitors may be acquired by third parties with greater available resources. As a result, competitors may be able to respond more quickly and effectively than Allego to new or changing opportunities, technologies, standards or customer requirements and may have the ability to initiate or withstand substantial price competition. In addition, competitors may in the future establish cooperative relationships with vendors of complementary products, technologies or services to increase the availability of their solutions in the marketplace. This competition may also materialize in the form of costly intellectual property disputes or litigation.

New competitors or alliances may emerge in the future that have greater market share, more widely adopted proprietary technologies, greater marketing expertise and greater financial resources, which could put Allego at a competitive disadvantage. Future competitors could also be better positioned to serve certain segments of Allego’s current or future target markets, which could increase costs and create downward pricing pressure on charging sessions. In light of these factors, even if Allego’s public charging network is larger and provides faster charging, and if its services offerings are

4

more effective, higher quality and address more complex demands than those of its competitors, current or potential customers may accept other competitive solutions. If Allego fails to adapt to changing market conditions or continue to compete successfully with current charging providers or new competitors, its growth will be limited, which would adversely affect its business and results of operations.

Allego’s future revenue growth will depend in significant part on its ability to increase the number and size of its charging sites, traffic, and the sales of services to Business to Business (“B2B”) customers.

Allego’s future revenue growth will depend in significant part on its ability to increase the number and size of its charging sites, traffic, and its sales of services to B2B customers. The sites Allego may wish to lease or acquire may first be leased or acquired by competitors or they may no longer be economically attractive due to certain adverse conditions such as increased rent which would hamper the growth and profitability of Allego’s business.

Furthermore, Allego’s B2B customer base may not increase as quickly as expected because the adoption of EVs may be delayed or transformed by new technologies. In addition to the factors affecting the growth of the EV market generally, transitioning to an EV fleet for some customers or providing EV equipment to facilities for other customers can be costly and capital intensive, which could result in slower than anticipated adoption. The sales cycle for certain B2B customers could also be longer than expected.

Allego has entered into a credit facility that imposes certain restrictions on its business and operations that may affect its ability to operate its business and make payments on its indebtedness.

We entered into the renewed credit facility on December 19, 2022, which requires us to comply with various affirmative and negative restrictions and covenants. See “Item 5. Operating and Financial Review and Prospects – B. Liquidity and Capital Resources – Sources of Liquidity – Borrowings” and “Note 34 (Capital management) – Loan covenants” of the consolidated financial statements included elsewhere in this Annual Report. The restrictions and covenants under the renewed credit facility may prevent us from engaging in certain transactions which might otherwise be considered beneficial to us and could have other important consequences to shareholders. For example, they could increase our vulnerability to general adverse economic and industry conditions, to fund future working capital, capital expenditures and other requirements; to engage in future acquisitions, construction or development activities; to access capital markets (debt and equity); or to otherwise fully realize the value of our assets and opportunities because of the need to dedicate a substantial portion of our cash flows from operations to payments on our indebtedness or to comply with any restrictive terms of our indebtedness; limit our flexibility in planning for, or reacting to, changes in our businesses and the industries in which we operate; and place us at a competitive disadvantage as compared to our competitors that have less debt.

Further, even though the Group has complied with the covenants of the old facility and renewed facility throughout all reporting periods presented, the Group also forecasts the potential breach of the interest cover ratio and leverage ratio covenants at December 31, 2024 and the Group is dependent on obtaining additional financing to execute on its business plan. The covenant ratios are increasing every testing date until June 30, 2027 in line with this business plan. Failure to comply with the terms and conditions of any existing or future indebtedness would constitute an event of default. If an event of default occurs, the lenders or note holders will have the right to accelerate the maturity of such indebtedness and foreclose upon the collateral, if any, securing that indebtedness.

Allego may need to raise additional funds or debt and these funds may not be available when needed.

Allego may need to raise additional capital or debt in the future to further scale its business and expand to additional markets. Allego may raise additional funds through the issuance of equity, equity-related or debt securities, or through obtaining credit from financial institutions. Allego cannot be certain that additional funds will be available on favorable terms when required, or at all. If Allego cannot raise additional funds when needed, its financial condition, results of operations, business and prospects could be materially and adversely affected. If Allego raises funds through the issuance of debt securities or through loan arrangements, the terms of such arrangements could require significant interest payments, contain covenants that restrict Allego’s business, or other unfavorable terms. In addition, to the extent Allego raises funds through the sale of additional equity securities, Allego shareholders would experience additional dilution.

If Allego fails to offer high-quality support to its customers and fails to maintain the availability of its charging points, its business and reputation may suffer.

Once Allego charging points are operational, customers rely on Allego to provide maintenance services to resolve any issues that might arise in the future. Rapid and high-quality customer and equipment support is important so that drivers can reliably charge their EVs. The importance of high-quality customer and equipment support will increase as Allego seeks to expand its public charging network and retain customers, while pursuing new EV drivers and geographies. If

5

Allego does not quickly resolve issues and provide effective support, its ability to retain EV drivers or sell additional services to B2B customers could suffer and its brand and reputation could be harmed.

A potential pandemic or other health crises could have a material adverse effect on Allego’s business and results of operations.

The impact of a pandemic or other health crises, including changes in consumer and business behavior, pandemic fears and market downturns, and restrictions on business and individual activities, can create significant volatility in the global economy or lead to reduced economic activity. The recent COVID-19 pandemic created supply chain disruptions for vehicle manufacturers, suppliers and hardware manufacturers, as well as impacted the capacities of installers. Any sustained new disruption could impact demand for EVs and would harm Allego’s business despite its historical growth.

If a pandemic or other health crises occurs, it could require a modification of our business (for example, grid connections delays), triggering mitigating actions (as may be required by government authorities or otherwise) in the best interests of our employees, customers, suppliers, vendors and business partners. If significant portions of our workforce in the future is unable to work effectively, including due to illness, quarantines, social distancing, government actions or other restrictions, our operations will be negatively impacted. Furthermore, if significant portions of our customers’ or potential customers’ workforce are subject to stay-at-home orders or otherwise have substantial numbers of their employees working remotely for sustained periods of time, user demand for EV charging sessions and services may decline.

As of December 31, 2023, the impact of COVID-19 to Allego’s business has been limited, but prospects and results of operations will depend on any future developments. Ongoing effects from a pandemic or other health crises could limit the ability of customers, suppliers, vendors and business partners to perform, including third-party suppliers’ ability to provide components and materials used for Allego’s charging stations or in providing transport, installation or maintenance services.

Any economic recession that has occurred or may occur in the future will impact the growth of EVs and the growth of EV charging demand.

Difficult macroeconomic conditions, such as decreases in per capita income and level of disposable income, increased and prolonged unemployment or a decline in consumer confidence, as well as reduced spending by businesses, could each have a material adverse effect on the demand for Allego’s charging points network and services.

Allego relies on a limited number of suppliers and manufacturers for its hardware and equipment and charging stations. A loss of any of these partners or issues in their manufacturing and supply processes could negatively affect its business.

Allego has extended its hardware and equipment supplier base, but it still relies on a limited number of suppliers, although it is not dependent on any one supplier. This reliance on a limited number of hardware manufacturers increases Allego’s risks, since it does not currently have proven alternatives or replacement manufacturers beyond these key parties. In the event of interruption or insufficient capacity, it may not be able to increase capacity from other sources or develop alternate or secondary sources without incurring material additional costs and substantial delays. In particular, disruptions or shortages at such suppliers, including as a result of delays or issues with their supply chain, in respect of electronic chips, processors, semiconductors and other electronic components or materials, can negatively impact deliveries by such suppliers to Allego. Thus, Allego’s business could be adversely affected if one or more of its suppliers is impacted by any interruption at a particular location or decides to reduce its deliveries to Allego for any reason including its acquisition by a third party or is unable to provide Allego with the quantities Allego requires for its growth.

If Allego experiences an increase in demand greater than expected for the development of its charging stations or from its services customers or if it needs to replace an existing supplier, it may not be possible to supplement or replace them on acceptable terms, which may undermine Allego’s ability to capture higher growth or deliver solutions to customers in a timely manner. For example, it may take a significant amount of time to identify a new hardware manufacturer that has the capability and resources to build hardware and equipment in sufficient volume that meets Allego’s specifications. Identifying suitable suppliers and manufacturers could be an extensive process that would require Allego to become satisfied with such suppliers’ and manufacturers’ quality control, technical capabilities, responsiveness and service, financial stability, regulatory compliance, and labor and other ethical practices. Accordingly, a loss of any significant suppliers or manufacturers could have an adverse effect on Allego’s business, financial condition and operating results.

Allego’s hardware and equipment may also experience technical issues, including safety issues, which could, on a large scale, negatively impact Allego’s business and potentially in the most extreme cases lead Allego to an early replacement program of such hardware, resulting in Allego incurring substantial additional costs and delays.

6

In addition, the military conflict between Russia and Ukraine, and more recently the conflict between Israel and Hamas, could lead to additional disruption, instability and volatility in global markets and industries that could negatively impact Allego’s supply chain. The European Union, the United States and other governments have already imposed severe sanctions and export controls against Russia and Russian interests and may impose additional sanctions and controls. The impact of these measures, as well as potential responses to them by Russia, is currently unknown and could adversely affect Allego’s supply chain, which, in turn, could affect Allego’s business and operating results.

Further, the United States imposed extraordinary tariffs and extensive export controls targeted primarily at the semiconductor industry in China. If China retaliates to such measures or there is a conflict between China and Taiwan, which is a leading producer of semiconductors, there could be further disruption to the semiconductor industry and global supply chains. Allego or the suppliers it procures components from may be unable to manufacture products at prices our customers would accept, or at all. Any inability to pass on future increased costs to customers would put downward pressure on Allego’s gross margins and adversely affect Allego’s business, results of operations and financial condition.

Allego’s business is subject to risks associated with construction, cost overruns and delays, and other contingencies that may arise in the course of completing installations, and such risks may increase in the future as Allego expands its charging networks and increases its service to third parties.

Allego does not typically install charging points directly on leased sites or at customer sites. These installations are typically performed by Allego’s electrical contractors at its own sites or with contractors with an existing relationship with the customer and/or knowledge of the site. The installation of charging stations at a particular site is generally subject to oversight and regulation in accordance with national and local laws and regulations relating to building codes, safety, environmental protection and related matters, and typically requires various local approvals and permits, such as grid connection permits that may vary by jurisdiction. In addition, building codes, accessibility requirements or regulations may hinder EV charger installation due to potential increased costs to the developer or installer in order to meet such requirements. Meaningful delays or cost overruns may impact Allego’s recognition of revenue in certain cases and/or impact customer relationships, either of which could impact Allego’s business and profitability.

Contractors may require that Allego or Allego’s customers obtain licenses in order to perform their services. Furthermore, additional rules on working conditions and other labor requirements may result in more complex projects with higher project management costs. If these contractors are unable to provide timely, thorough and quality installation-related services, Allego could fall behind its construction schedules which may cause EV drivers and Allego’s customers to become dissatisfied with Allego’s network and charging solutions. As the demand for public fast and ultra-fast charging increases and qualifications for contractors become more stringent, Allego may encounter shortages in the number of qualified contractors available to complete all of Allego’s desired new charging stations and their maintenance.

Allego’s business model is predicated on the presence of qualified and capable electrical and civil contractors and subcontractors in the new markets it intends to enter. There is no guarantee that there will be an adequate supply of such partners. A shortage in the number of qualified contractors may impact the viability of Allego’s business plan, increase risks around the quality of work performed and increase costs if outside contractors are brought into a new market.

Allego’s business is subject to risks associated with increased cost of land and competition from third parties that can create cost overruns and delays and can decrease the value of some of Allego’s charging stations.

Allego typically enters into long-term leases for its charging stations. With the growing adoption of EVs, increased competition may develop in securing suitable sites for charging stations, especially in high traffic areas. This competition may trigger increases in the cost of land leases, tenders organized by landowners, delays in securing sites and a quicker depletion of available sites for Allego’s charging stations. The term of leases may also be impacted by increased competition. This could negatively impact the potential economic return of building such charging stations in certain zones or on certain sites and therefore negatively impact Allego’s business and profitability.

Allego’s EV driver base depends upon the effective operation of Allego’s EVCloudTM platform and its applications with mobile service providers, firmware from hardware manufacturers, mobile operating systems, payment systems, networks and standards that Allego does not control.

Allego is dependent on the interoperability of mobile service providers for the payment of charging sessions that must use open protocols. Its own mobile payment application is dependent upon popular mobile operating systems that Allego does not control, such as Google’s Android and Apple’s iOS software systems, and any changes in such systems that degrade or hamper the functionality of Allego’s products or give preferential treatment to competitive products could adversely affect the usage of Allego’s applications on mobile devices. Changes in standards, such as Open Charge Point Protocol, may require Allego to incur development expenses and delay its operations and the potential launch of new services. Continued

7

support and operability of Allego’s charging stations depends upon hardware manufacturers’ firmware of which Allego has no control over. Additionally, in order to deliver high quality services to its customers, it is important that Allego’s products work well with a range of technologies, including various firmware, software, payment systems, networks and standards that Allego does not control. Allego may not be successful in maintaining and updating its EVCloudTM platform and may not have sufficient knowledge to effectively keep up with new technologies, systems, networks or standards.

Should Allego pursue acquisitions in the future, it would be subject to risks associated with acquisitions.

Allego may acquire additional assets such as public charging networks, products, technologies or businesses that are complementary to its existing business or that reinforce its core or adjacent competencies. The process of identifying and consummating acquisitions and the subsequent integration of new assets and businesses into Allego’s own business would require attention from management and could result in a diversion of resources from its existing business, which in turn could have an adverse effect on its operations. Acquired assets or businesses may not generate the expected financial results or the expected technological gains. Key employees of acquired companies may also decide to leave. Acquisitions could also result in the use of cash, potentially dilutive issuances of equity securities, the occurrence of goodwill impairment charges, amortization expenses for other intangible assets and exposure to potential unknown liabilities of the acquired business.

If Allego is unable to attract and retain key employees and hire qualified management, technical, engineering and sales personnel, its ability to compete and successfully grow its business would be harmed.

Allego’s success depends, in part, on its continuing ability to identify, hire, attract, train, develop and retain highly qualified and skilled personnel, including software engineers and other employees with the technical skills in design and engineering that will enable us to deliver quality EV charging products and energy management solutions. The inability to do so effectively would adversely affect its business.

Competition for employees can be intense in the various parts of Europe where Allego operates, as there is a high demand of qualified personnel, and we expect certain of our key competitors, who generally are larger than us and have access to more substantial resources, to pursue top talent even more aggressively. The ability to attract, hire and retain personnel depends on Allego’s ability to provide competitive compensation. Allego may not be able to attract, assimilate, develop or retain qualified personnel in the future, and failure to do so could adversely affect its business, including the execution of its strategy.

Allego is expanding operations in many countries in Europe, which will expose it to additional tax, compliance, market, local rules and other risks.

Allego’s operations are within the European Union and in the United Kingdom, and it maintains contractual relationships with parts and manufacturing suppliers in Asia, directly or indirectly through its suppliers. Allego also intends to expand into other EEA countries. Managing this global presence and expansion in Europe requires additional resources and controls, and could subject Allego to certain risks, associated with international operations, including:

•conformity with applicable business customs, including translation into foreign languages and associated expenses;

•ability to find and secure sites in new jurisdictions;

•availability of reliable and high quality contractors for the development of its sites and more globally installation challenges;

•challenges in arranging, and availability of, financing for customers;

•difficulties in staffing and managing foreign operations in an environment of diverse culture, laws, and customers, and the increased travel, infrastructure, and legal and compliance costs associated with European operations;

•differing driving habits and transportation modalities in other markets;

•different levels of demand among commercial customers;

•quality of wireless communication that can hinder the use of its software platform with charging stations in the field;

•compliance with multiple, potentially conflicting and changing governmental laws, regulations, certifications, and permitting processes including environmental, banking, employment, tax, information security, privacy,

8

and data protection laws and regulations such as the European Union General Data Protection Regulation (“GDPR”), national legislation implementing the same;

•compliance with the United Kingdom Anti-Bribery Act;

•safety requirements as well as charging and other electric infrastructures;

•difficulty in establishing, staffing and managing foreign operations;

•difficulties in collecting payments in foreign currencies and associated foreign currency exposure;

•restrictions on operations as a result of the dependence on subsidies to fulfill capitalization requirements;

•restrictions on repatriation of earnings;

•compliance with potentially conflicting and changing laws of taxing jurisdictions, the complexity and adverse consequences of such tax laws, and potentially adverse tax consequences due to changes in such tax laws; and

•regional economic and political conditions.

As a result of these risks, Allego’s current expansion efforts and any potential future international expansion efforts may not be successful.

Inflation could adversely affect Allego’s business and financial results.

Inflation, which increased significantly during 2022 and 2023, could adversely affect Allego by increasing the costs of materials and labor needed to operate Allego’s business and could continue to adversely affect the Company in future periods. If this current inflationary environment continues, there can be no assurance that Allego would be able to recover related cost increases through price increases, which could result in downward pressure on Allego’s operating margins. As a result, Allego’s financial condition, results of operations, and cash flows, could be adversely affected over time.

Certain of Allego’s strategic and development arrangements could be terminated or may not materialize into long-term contract partnership arrangements and may restrict or limit Allego from developing arrangements with other strategic partners.

Allego has arrangements with strategic development partners and collaborators. Some of these arrangements are evidenced by memorandums of understanding, non-binding letters of intent, and early stage agreements that are used for design and development purposes but will require renegotiation at later stages of development, each of which could be terminated or may not materialize into next-stage contracts or long-term contract partnership arrangements. In addition, Allego does not currently have formal agreements with all partners and collaborators that are contemplated in the execution of its business plan. Moreover, existing or future arrangements may contain limitations on Allego’s ability to enter into strategic and development arrangements with other partners. If Allego is unable to maintain such arrangements and agreements, or if such agreements or arrangements contain other restrictions from or limitations on developing arrangements with other strategic partners, its business, prospects, financial condition and operating results may be materially and adversely affected.

Risks Related to the EV Market

New alternative fuel technologies may negatively impact the growth of the EV market and thus the demand for Allego’s charging stations and services.

As a number of European Union regulations have sought to achieve a sharp decrease in CO2 emissions in Europe, consumer acceptance of EVs and other alternative vehicles has been increasing. If new technologies such as hydrogen for light trucks or load transportation develop and are widely adopted, the demand for electric charging could diminish. In addition, the EV fueling model is different than gas or other fuel models, requiring behavioral change and education of influencers, consumers and others such as regulatory bodies. Developments in alternative technologies, such as fuel cells, compressed natural gas or hydrogen may materially and adversely affect demand for EVs and EV charging stations, which in turn would materially and adversely affect Allego’s business, operating results, financial condition and prospects.

Allego’s future growth and success is highly correlated with and thus dependent upon the continuing rapid adoption of EVs.

Allego’s future growth is highly dependent upon the adoption of EVs by consumers. The market for EVs is still rapidly evolving, characterized by rapidly changing technologies, competitive pricing and competitive factors, evolving government regulation and industry standards and changing consumer demands and behaviors and the environment

9

generally. Although demand for EVs has grown in recent years, bolstered in part by pro-EV regulations in Europe, there is no guarantee that such demand will continue to grow. If the market for EVs develops more slowly than expected, Allego’s business, prospects, financial condition and operating results would be harmed. The market for EVs could be affected by numerous factors, such as:

•perceptions about EV features, quality, safety, performance and cost;

•perceptions about the limited range over which EVs may be driven on a single battery charge;

•competition, including from other types of alternative fuel vehicles as hydrogen or fuel cells;

•concerns regarding the stability of the electrical grid;

•the decline of an EV battery’s ability to hold a charge over time;

•availability of service for EVs;

•consumers’ perception about the convenience and cost of charging EVs;

•government regulations and economic incentives, including adverse changes in, or expiration of, favorable tax incentives related to EVs, EV charging stations or decarbonization generally; and

•concerns about the future viability of EV manufacturers.

In addition, sales of vehicles in the automotive industry can be cyclical, which may affect growth in acceptance of EVs. It is uncertain how macroeconomic factors will impact demand for EVs, particularly since they can be more expensive than traditional fuel-powered vehicles, when the automotive industry globally has been experiencing a recent decline in sales.

Demand for EVs may also be affected by factors directly impacting automobile prices or the cost of purchasing and operating automobiles, such as sales and financing incentives, prices of raw materials and parts and components and governmental regulations, including tariffs, import regulation and other taxes. Volatility in demand may lead to lower vehicle unit sales, which may result in reduced demand for EV charging solutions and therefore adversely affect Allego’s business, financial condition and operating results.

The European EV market currently benefits from the availability of rebates, scrappage schemes, tax credits and other financial incentive schemes from governments to offset and incentivize the purchase of EVs. The reduction, modification, or elimination of such benefits could cause reduced demand for EVs and EV charging, which would adversely affect Allego’s financial results.

Most European countries provide incentives to end users and purchasers of EVs and EV charging stations in the form of rebates, scrappage schemes for internal combustion engines (“ICEs”), tax credits and other financial incentives. The EV market relies on these governmental rebates, scrappage schemes for ICEs, tax credits and other financial incentives to significantly lower the effective price of EVs and EV charging stations to customers and to support widespread installation of EV charging infrastructure. However, these incentives may expire on a particular date, may end when allocated funding is exhausted, or may be reduced or terminated as a matter of regulatory or legislative policy. For example, in Germany, incentives are expected to continue until 2030, and in the Netherlands, these incentives are expected to continue until 2025. Any reduction in rebates, scrappage schemes for ICEs, tax credits or other financial incentives could reduce the demand for EVs and EV charging stations and as a result, may adversely impact Allego’s business and expansion potential.

The EV charging market is characterized by rapid technological change, which requires Allego to continue developing new innovations of its software platform and to keep up with new hardware technologies. Any delays in such development could adversely affect market adoption of its solutions and Allego’s financial results.

Continuing technological changes in battery and other EV technologies or payment technologies could adversely affect adoption of current EV charging technology and/or Allego’s charging network or services. Allego’s future success will depend upon its ability to develop new sites and introduce a variety of new capabilities and innovations to enhance EV drivers experience using its network and its existing services offerings.

As EV technologies change, Allego may need to upgrade or adapt its charging stations technology and introduce new hardware in order to serve vehicles that have the latest technology, in particular battery cell technology, which could involve substantial costs. This could lead Allego to replace some charging hardware before its expected lifespan involving financial costs and reduced return. Even if Allego is able to keep pace with changes in technology and develop new features and services, its research and development expenses could increase and its gross margins could be adversely affected.

10

Allego cannot guarantee that any new services or features of its software platform will be released in a timely manner or at all, or that if such services or features are released, that they will achieve market acceptance. Delays in delivering new services that meet customer requirements could damage Allego’s relationships with customers and lead them to seek alternative providers. For some customers, delays in delivering new services and features could induce the application of contractual penalties. Delays in introducing innovations or the failure to offer innovative services at competitive prices may cause existing and potential customers to purchase Allego’s competitors’ products or services.

If Allego is unable to devote adequate resources to develop new features and services or cannot otherwise successfully develop features or services that meet customer requirements on a timely basis or that remain competitive with technological alternatives, its charging network or services could lose market share, its revenue will decline, it may experience operating losses and its business and prospects will be adversely affected.

Risks Related to Allego’s Technology, Intellectual Property and Infrastructure

Allego may need to defend against intellectual property infringement or misappropriation claims, which may be time consuming and expensive.

From time to time, the holders of intellectual property rights may assert their rights and urge Allego to obtain licenses, and/or may bring suits alleging infringement or misappropriation of such rights. There can be no assurance that Allego will be able to mitigate the risk of potential suits or other legal demands by competitors or other third parties. Accordingly, Allego may consider entering into licensing agreements with respect to such rights, although no assurance can be given that such licenses can be obtained on acceptable terms or at all or that litigation will not occur, and such licenses and/or associated litigation could significantly increase Allego’s operating expenses. In addition, if Allego is determined to have or believes there is a high likelihood that it has infringed upon or misappropriated a third party’s intellectual property rights, it may be required to cease making, selling or incorporating certain key components or intellectual property into the products and services it offers, to pay substantial damages and/or royalties, to redesign its products and services, and/or to establish and maintain alternative branding. In addition, to the extent that Allego’s customers and business partners become the subject of any allegation or claim regarding the infringement or misappropriation of intellectual property rights related to Allego’s products and services, Allego may be required to indemnify such customers and business partners. If Allego were required to take one or more such actions, its business, prospects, operating results and financial condition could be materially and adversely affected. In addition, any litigation or claims, whether or not valid, could result in substantial costs, negative publicity and diversion of resources and management attention.

Allego’s business may be adversely affected if it is unable to maintain, protect or enforce its rights in its technology and intellectual property.

Allego’s success depends, in part, on Allego’s ability to establish, maintain and protect its rights in its core technology and intellectual property. To accomplish this, Allego relies on, and plans to continue relying on, trade secrets, copyright, trademark and other intellectual property laws, employee and third-party nondisclosure agreements, intellectual property licenses and other contractual rights. Failure to adequately maintain, protect or enforce its rights in its technology and intellectual property could result in competitors offering similar products, potentially resulting in the loss of some of

Allego’s competitive advantage and a decrease in revenue which would adversely affect its business, prospects, financial condition and operating results.

Allego cannot guarantee that competitors will not infringe its intellectual property. Despite Allego’s efforts to protect its intellectual property, third parties may attempt to copy or otherwise obtain and use Allego’s intellectual property or seek court declarations that Allego’s intellectual property is invalid or unenforceable or that they do not infringe upon Allego’s intellectual property. Monitoring unauthorized use of Allego’s intellectual property is difficult and costly and the steps Allego has taken or may take in the future in an effort to prevent infringement or misappropriation may not be successful. From time to time, Allego may have to resort to litigation to enforce its intellectual property, which could result in substantial costs and diversion of our resources, and ultimately may not be successful.

In addition, it is possible that:

•current and future competitors may independently develop similar trade secrets or works of authorship, such as software;

•know-how and other proprietary information Allego purports to hold as a trade secret may not qualify as a trade secret under applicable laws; and

•proprietary designs, software design and technology embodied in Allego’s offers may be discoverable by third parties through means that do not constitute violations of applicable laws.

11

Patent, trademark and trade secret laws vary significantly throughout the world. Some foreign countries do not protect intellectual property rights to the same extent as do the laws of the European Union, United Kingdom, or EEA countries. Further, policing the unauthorized use of its intellectual property in foreign jurisdictions may be difficult or impossible. Therefore, Allego’s intellectual property rights may not be as strong or as easily enforced outside of the European Union, United Kingdom, and EEA.

Computer malware, viruses, ransomware, hacking, phishing attacks and similar disruptions could result in security and privacy breaches and interruption in service, which could harm Allego’s business.

Computer malware, viruses, physical or electronic break-ins and similar disruptions could lead to interruption and delays in Allego’s operations and loss, misuse or theft of data. Computer malware, viruses, ransomware, hacking and phishing attacks against online networks have become more prevalent and may continue to occur on Allego’s systems in the future and on hardware manufacturers that supply Allego. Any attempts by cyber attackers to disrupt Allego’s operations, services or systems, if successful, could harm its business, introduce liability to data subjects, result in the misappropriation of company funds, be expensive to remedy and damage Allego’s reputation or brand. Insurance may not be sufficient to cover significant expenses and losses related to cyber-attacks. Efforts to prevent cyber attackers from entering computer systems are expensive to implement, and Allego may not be able to cause the implementation or enforcement of such prevention. Though it is difficult to determine what, if any, harm may directly result from any specific interruption or attack, any failure to maintain performance, reliability, security and availability of systems and technical infrastructure may, in addition to other losses, harm Allego’s reputation, brand and ability to operate reliably and to retain customers.

Allego has previously experienced, and may in the future experience, service disruptions, outages and other performance problems due to a variety of factors, including infrastructure changes, third-party service providers, scalability issues with its software tools, human or software errors and capacity constraints. Allego relies on telecom networks to support reliable operation, management and maintenance of its charger network, charging session management, and driver authentication, and payment processing by customers depends on reliable connections with wireless communications networks. As a result, Allego’s operations depend on a handful of public carriers and are exposed to disruptions related to network outages and other communications issues on the carrier networks. Disruptions experienced in the payment chain from authorization to settlement also might cause financial harm, directly or indirectly to Allego. If Allego’s services or charging points are unavailable when users attempt to access them, they may seek other services or networks, which could reduce demand for Allego’s charging stations and services.