Table of Contents

As filed with the Securities and Exchange Commission on October 8, 2021.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

DELIMOBIL HOLDING S.A.

(Exact name of Registrant as specified in its charter)

| Grand Duchy of Luxembourg | 7389 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

10, rue C.M. Spoo

L-2546, Luxembourg

Grand Duchy of Luxembourg

+352 26 97 63 04

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

C T Corporation System

28 Liberty Street

New York,

New York 10005

(212) 894-8940

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| David I. Gottlieb, Esq. Cleary Gottlieb Steen & 2 London Wall Place London EC2Y 5AU United Kingdom +44 20 7614 2200 |

Yulia A. Solomakhina Cleary Gottlieb Steen & Paveletskaya Square 2/3 +7 495 660 8500 |

Claire-Marie Darnand Stibbe Avocats 6, rue Jean Monnet 2180 Luxembourg Luxembourg +352 26 61 81 00 |

Pranav L. Trivedi, Esq. Skadden, Arps, Slate, 40 Bank Street, Canary London E14 5DS United Kingdom +44 20 7519 7000 |

Ryan J. Dzierniejko Skadden, Arps, Slate, One Manhattan West New York, NY 10001 United States +1 (212) 735-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

| † | The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered(1) | Proposed Maximum |

Amount of | ||

| Ordinary shares, par value of €0.01 |

$100,000,000 | $9,270 | ||

|

| ||||

|

| ||||

| (1) | American depositary shares, or ADSs, issuable upon deposit of the ordinary shares registered hereby will be registered under a separate registration statement on Form F-6 (Registration No. 333- ). Each ADS represents ordinary shares. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | Includes the aggregate offering price of additional ordinary shares represented by ADSs that may be acquired by the underwriters if the underwriters’ option to purchase additional ADSs is exercised. |

| (4) | Calculated pursuant to Rule 457(o) under the Securities Act of 1933, as amended, based on an estimate of the proposed maximum aggregate offering price. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the U.S. Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2021

PRELIMINARY PROSPECTUS

DELIMOBIL HOLDING S.A.

American Depositary Shares

Representing Ordinary Shares

$ per ADS

This is the initial public offering of American Depositary Shares, or ADSs, representing ordinary shares of Delimobil Holding S.A., a public limited liability company (société anonyme) incorporated under the laws of Luxembourg. Each ADS will represent ordinary shares. We are offering ADSs.

Prior to this offering, there has been no public market for the ADSs. The estimated initial public offering price per ADS will be between $ and $ . We intend to apply to have the ADSs listed on the New York Stock Exchange (“NYSE”) in the United States under the symbol “DMOB.”

We are and will continue to be a “controlled company” within the meaning of the NYSE corporate governance rules due to the fact upon completion of this offering that our controlling shareholder, Mikro Kapital Group SARL, as well as (i) all its direct and indirect subsidiaries, (ii) special purpose vehicles managed by such direct and indirect subsidiaries and (iii) equity investments of such special purpose vehicles (together “Mikro Kapital Group”), will control approximately % of the voting power of our ordinary shares. As a “controlled company”, we are permitted to elect to rely on certain exemptions from corporate governance rules. See “Management—Controlled Company Exemption.”

We are both an “emerging growth company” and a “foreign private issuer” as defined under the U.S. federal securities laws and, as such, may elect to comply with certain reduced public company reporting requirements. See “Prospectus Summary—Implications of Being an Emerging Growth Company and a Foreign Private Issuer.”

Investing in the ADSs involves risks. See “Risk Factors” beginning on page 24.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per ADS |

Total |

|||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discounts and commissions(1) |

$ | $ | ||||||

| Proceeds to us (before expenses) |

$ | $ | ||||||

| (1) | We have agreed to reimburse the underwriters for certain expenses in connection with this offering. See “Underwriting.” |

The underwriters have a 30-day option to purchase up to an aggregate of additional ADSs from us at the initial public offering price, less the underwriting discounts and commissions.

The underwriters expect to deliver the ADSs to purchasers on or about , 2021.

| BofA Securities | Citigroup | VTB Capital |

| Banco Santander | RenCap |

SberCIB | ||

Prospectus dated , 2021

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| iv | ||||

| vii | ||||

| viii | ||||

| 1 | ||||

| 17 | ||||

| 19 | ||||

| 24 | ||||

| 77 | ||||

| 79 | ||||

| 80 | ||||

| 81 | ||||

| 82 | ||||

| SELECTED COMBINED AND CONSOLIDATED FINANCIAL AND OPERATING DATA |

84 | |||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

89 | |||

| 126 | ||||

| 143 | ||||

| 174 | ||||

| 181 | ||||

| 192 | ||||

| 194 | ||||

| 198 | ||||

| 215 | ||||

| SHARES AND AMERICAN DEPOSITARY SHARES ELIGIBLE FOR FUTURE SALE |

224 | |||

| 226 | ||||

| 245 | ||||

| 254 | ||||

| 255 | ||||

| 256 | ||||

| 257 | ||||

| 260 |

Neither we nor the underwriters have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared, and neither we nor the underwriters take responsibility for, or can provide any assurance as to the reliability of, any other information others may give you. We and the underwriters are not making an offer to sell, or seeking offers to buy, these securities in any jurisdiction where the offer or sale is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than its date, regardless of the time of delivery of this prospectus or of any sale of the ADSs.

For investors outside the United States: Neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction, other than the United States, where action for that purpose is required. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the ADSs and the distribution of this prospectus outside the United States.

We are incorporated in Luxembourg, and a majority of our outstanding securities are owned by non-U.S. residents. Under the rules of the United States Securities and Exchange Commission, or the SEC, we

i

Table of Contents

are currently eligible for treatment as a “foreign private issuer.” As a foreign private issuer, we will not be required to file periodic reports and financial statements with the SEC as frequently or as promptly as domestic registrants whose securities are registered under the Securities Exchange Act of 1934, as amended.

ii

Table of Contents

ABOUT THIS PROSPECTUS

Except where the context otherwise requires or where otherwise indicated, all references in this prospectus to “Delimobil Holding” or the “issuer” are to Delimobil Holding S.A., a Luxembourg public limited liability company (société anonyme) registered with the Luxembourg Register of Commerce and Companies under number B 250892; and to “Delimobil,” the “Company,” “we,” “us,” “our” or similar terms refer to Delimobil Holding together with its consolidated subsidiaries as a consolidated entity.

All references in this prospectus to the “Companies” are to Carsharing Russia LLC, Anytime LLC and

Smart Mobility Management LLC (“SMM LLC”), our consolidated subsidiaries, all of which are Russian limited liability companies

; and to the “Group” are to Delimobil Holding and the Companies on a combined and consolidated basis.

; and to the “Group” are to Delimobil Holding and the Companies on a combined and consolidated basis.

All references in this prospectus to “Russia” are to the Russian Federation; to “Luxembourg” are to the Grand Duchy of Luxembourg; and to the “EU” are to the European Union.

All references in this prospectus to

“RUB,” “rubles” or “P” are to Russian rubles, the official currency of Russia; to “USD,” “dollar” or “$” are to U.S. dollars; and

to “EUR,” “euro” or “€” are to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the treaty establishing the European Community, as

amended.

All references in this prospectus to the “Commission” or to the “SEC” are to the United States Securities and Exchange Commission; to the “Exchange Act” are to the U.S. Securities Exchange Act of 1934, as amended; and to the “Securities Act” are to the U.S. Securities Act of 1933, as amended.

iii

Table of Contents

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Information

Our audited combined and consolidated financial statements for the years ended December 31, 2020 and 2019 are included in this prospectus, and reflect the combined and consolidated financial information of the Companies, our Russian subsidiaries through which our business is operated. Our audited combined and consolidated financial statements were prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”), and audited in accordance with the standards established by Public Company Accounting Oversight Board (“PCAOB”). Our unaudited interim condensed combined and consolidated financial statements for the six months ended June 30, 2021 and 2020 have been prepared in accordance with IAS 34, “Interim Financial Reporting,” as issued by the IASB. None of our financial statements were prepared in accordance with generally accepted accounting principles of the United States (“U.S. GAAP”). References in this prospectus to “our financial statements” are to our audited combined and consolidated financial statements for the years ended December 31, 2020 and 2019, and the related notes thereto, and to our unaudited interim condensed combined and consolidated financial statements for the six months ended June 30, 2021 and 2020, and the related notes thereto, included elsewhere in this prospectus.

Delimobil Holding, the company offering the ADSs in this prospectus, was incorporated on January 18, 2021, as a public limited liability company (société anonyme) under the laws of Luxembourg. Its subsidiary, Carsharing Russia LLC, through which the principal business of Delimobil Holding is conducted, has operated since 2015. Until the contribution of the equity interests in the Companies, Delimobil Holding had not commenced operations. Following this offering, Delimobil Holding will begin reporting consolidated financial information to shareholders. Our fiscal year ends on December 31 of each year. References to 2020 are to the fiscal year ended December 31, 2020, and references to 2019 are to the fiscal year ended December 31, 2019.

The financial information presented in this prospectus should be read in conjunction with our financial statements, including the related notes, and the section of this prospectus titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Use of Non-IFRS Financial Measures

Certain parts of this prospectus contain non-IFRS financial measures, specifically Adjusted Gross Profit/(Loss), Adjusted Gross Profit/(Loss) Margin, Adjusted EBITDA and Adjusted EBITDA Margin. The most directly comparable IFRS measure for Adjusted Gross Profit/(Loss) and Adjusted Gross Profit/(Loss) Margin is gross profit/(loss). The most directly comparable IFRS measure for Adjusted EBITDA and Adjusted EBITDA Margin is loss for the period. We define:

| • | Adjusted Gross Profit/(Loss) as gross profit/(loss) adjusted for: (i) compulsory civil liability insurance proceeds, (ii) expected credit losses of trade receivables and (iii) following the adoption of our phantom share plan (the “Phantom Share Plan”), share-based remuneration; |

| • | Adjusted Gross Profit/(Loss) Margin as Adjusted Gross Profit/(Loss) divided by revenue expressed as a percentage; |

| • | Adjusted EBITDA as loss for the period adjusted for: (i) income tax benefit, (ii) finance costs, (iii) finance income, (iv) impairment of a right-of-use asset, (v) VAT write-off, (vi) loss on lease terminations, (vii) impairment of property, plant and equipment, (viii) (gain)/loss on disposal of property, plant and equipment, net, (ix) reversal of an impairment loss on a right-of-use asset, (x) subsidies received, (xi) insurance compensation received for damage of vehicles, (xii) reversal of impairment loss on property, plant and equipment, (xiii) depreciation of property, plant and equipment, (xiv) amortization of intangible assets, (xv) depreciation of right-of-use assets and (xvi) following the adoption of our Phantom Share Plan, share-based remuneration; and |

| • | Adjusted EBITDA Margin as Adjusted EBITDA divided by revenue expressed as a percentage. |

iv

Table of Contents

The non-IFRS financial measures included in this prospectus are unaudited supplementary measures that are not required by or presented in accordance with IFRS or any other generally accepted accounting principles. See “Selected Combined and Consolidated Financial and Operating Data” for a reconciliation of these non-IFRS measures to the most directly comparable IFRS measures as set forth in the combined and consolidated financial statements.

Prospective investors should not consider them as: (a) an alternative to gross profit/(loss), operating profit or net profit as determined in accordance with IFRS or other generally accepted accounting principles, or as measures of operating performance; or (b) an alternative to any other measures of performance under IFRS or other generally accepted accounting principles.

These measures are used by our management to monitor the underlying performance of the business and our operations. However, not all companies calculate these measures in an identical manner and, therefore, our presentation may not be comparable with similar measures used by other companies. As a result, prospective investors should not place undue reliance on this data.

Rounding

Certain figures and some percentages included in this prospectus have been subject to rounding adjustments. Accordingly, the totals included in certain tables contained in this prospectus may not correspond to the arithmetic aggregation of the figures or percentages that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

Key Operating and Financial Metrics

Throughout this prospectus, we provide a number of key operating and financial metrics used by our management and often used by competitors in our industry. We use different key operating and financial metrics for our two different operating segments, Delimobil and Anytime Prime. These and other key performance indicators are discussed in more detail in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Financial and Operating Metrics.” We define certain terms used in this prospectus as follows:

Delimobil Segment

| • | EoP Fleet means the total number of vehicles in our car sharing fleet at the end of a given period. |

| • | Weighted Average Fleet represents the average number of vehicles that constituted our car sharing fleet in a given period, calculated as the sum of the number of days each vehicle was part of our fleet divided by the number of calendar days in the given period. |

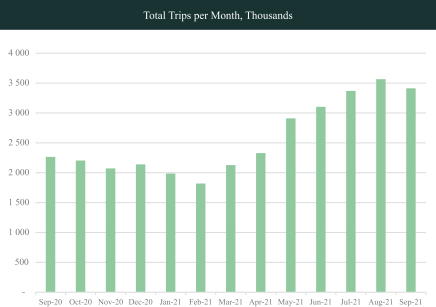

| • | Total Trips is the total number of trips completed by customers using our car sharing fleet in a given period. A trip lasts from the moment a customer books a vehicle until the moment the customer signals the completion of their journey on the Delimobil app. |

| • | Monthly Active Users (MAU) is the total number of unique customers who completed at least one trip per month using our car sharing fleet calculated as an average over the reporting period. |

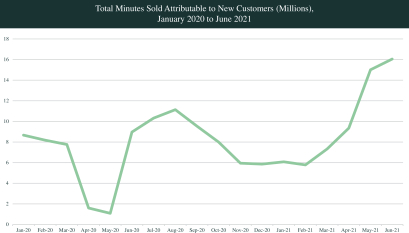

| • | Total Minutes Sold is the total number of minutes that customers were charged for using our car sharing service in a given period. |

| • | Revenue for Car Sharing is the total amount of revenue generated from our car sharing service in a given period, in line with Note 32 to our audited combined and consolidated financial statements and with Note 30 to our unaudited interim condensed combined and consolidated financial statements. |

v

Table of Contents

| • | Revenue per Weighted Average Fleet is revenue generated from our car sharing service divided by Weighted Average Fleet in a given period. |

| • | Revenue per Minute is revenue generated from our car sharing service divided by Total Minutes Sold in a given period. |

Anytime Prime Segment

| • | EoP Fleet means the total number of vehicles in our long-term rental fleet at the end of a given period. |

| • | Weighted Average Fleet represents the average number of vehicles that constituted our long-term rental fleet in a given period, calculated as the sum of the number of days each vehicle was part of our fleet divided by the number of calendar days in the given period. |

| • | Total Rental Days is the total number of rental days completed by customers for use of a vehicle in our long-term rental fleet in a given period. A rental day lasts from the moment a customer books the vehicle until the moment the customer signals the completion of their journey on the Anytime Prime app. As we only began to collect data on rental days from April 2019 as part of our strategic decision to focus on long-term rentals in the Anytime Prime segment, for the year ended December 31, 2019, Total Rental Days relates only to the period from April to December 2019. |

| • | Revenue for Long-Term Rentals is the total amount of revenue generated from our long-term rental service in a given period, in line with Note 32 to our audited combined and consolidated financial statements and with Note 30 to our unaudited interim condensed combined and consolidated financial statements. Revenue for Long-Term Rentals does not include any car sharing revenue recorded in the Anytime Prime segment for the year ended December 31, 2019. |

| • | Revenue per Rental Day is revenue generated from our long-term rental service divided by Total Rental Days in a given period. |

vi

Table of Contents

The industry, market and competitive position data included in this prospectus is derived from our own internal estimates and research, our management’s understanding of our business and the market in which we operate, as well as from publicly available information, including information of the Russian Federal State Statistics Service (“Rosstat”), the Moscow Department of Transport, the International Monetary Fund (“IMF”), industry and general publications and research, surveys and studies conducted by third parties, such as Frost & Sullivan Ltd. (“Frost & Sullivan”).

There are a number of studies that address either specific market segments, or regional markets, within our industry. However, given the rapid changes in our industry and the markets in which we operate, no industry research that is generally available covers some of the car sharing market trends we view as key to understanding our industry and our place in it worldwide and, in particular, in Russia. We believe that it is important that we maintain as broad a view on industry developments as possible. To assist us in formulating our business plan and in anticipation of this offering, we commissioned Frost & Sullivan in 2021 to provide an independent view of the car sharing landscape in Russia including an overview of macroeconomic indicators of Russia, the evolution of Russia’s public and private transportation markets size, shared mobility and car sharing markets size and an analysis of its underlying trends over time, relevant demographics, peer countries benchmarks, COVID-19 impact and potential growth factors, as well as an assessment of key competitors and evaluation of their and our market position. Frost & Sullivan produced a research report titled “Industry Report on the Russian Car Sharing Market” dated July 15, 2021. In connection with the preparation of Frost & Sullivan’s report, we furnished to Frost & Sullivan certain of our historical information and market competitive data. In preparation of the report, Frost & Sullivan conducted research including a customer survey, a study of a broad range of secondary sources including other market reports, association and trade press publications, other databases and other sources. We use the data contained in Frost & Sullivan’s report to assist us in describing the nature of our industry and our position in it. Such information is included in this prospectus in reliance on Frost & Sullivan’s authority as an expert in such matters. See “Experts.”

Due to the evolving nature of our industry and competitors, we believe that it is difficult for any market participant, including us, to provide precise data on the market or our industry. Industry publications and forecasts generally state that the information they contain has been obtained from sources believed to be reliable. We have not independently verified the accuracy or completeness of the data contained in these industry publications and reports. Although we are not aware of any misstatements regarding the industry data that we present in this prospectus, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

Some market data and statistical information contained in this prospectus are also based on management’s estimates and calculations, which are derived from our review and interpretation of the independent sources, our internal market and brand research and our knowledge of our industry. Information that is based on estimates, forecasts, projections or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information. The forward-looking information obtained from these sources is subject to the same qualifications and uncertainties as other forward looking statements in this prospectus.

vii

Table of Contents

We have proprietary rights to certain trademarks used in this prospectus that are important to our business, many of which are registered under applicable intellectual property laws.

Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the “®” or “™” symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent possible under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names. Except where expressly indicated, we do not intend our use or display of other companies’ trademarks, trade names or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. Each trademark, trade name or service mark of any other company appearing in this prospectus is the property of its respective owner.

viii

Table of Contents

This summary highlights selected information contained elsewhere in this prospectus. This summary does not contain all the information that you should consider before deciding to invest in the ADSs. You should read the entire prospectus carefully, including the “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections as well as our financial statements and the related notes thereto before making an investment decision.

Our Mission

To foster human connection by placing fast, easy and affordable mobility at the heart of it. Let’s share the future together.

Overview

We are a leading shared mobility provider in Russia, offering convenient, affordable and sustainable transportation alternatives supported by an advanced technology framework. Founded in 2015, we were a pioneer in the Russian car sharing industry and created the standard for car sharing services on the Russian market. We have developed through both organic growth and strategic acquisitions to become a leading car sharing operator in Russia, in terms of geographic presence, fleet size, number of trips in Moscow and revenue growth, as well as a first-mover in car subscription services. Our MAU increased from 270 thousand for the year ended December 31, 2019 to 461 thousand for the nine months ended September 30, 2021, which we believe was the combined result of our fleet growth, competitive customer proposition (including a user rating system with gamification and loyalty triggers, operations across 11 cities and smart churn prevention activities) and strong brand awareness.

We operate in the Russian shared mobility market under two principal business lines: free-floating car sharing under our brand “Delimobil” and car subscription for long-term rentals under our brand “Anytime Prime.” Delimobil was ranked first in top-of-mind and brand awareness among Russian car sharing providers in December 2020, according to brand health tracking research done by Tiburon Brand Health Research. Each brand has its own separate fleet of vehicles that caters to the needs of our customers. As of September 30, 2021, Delimobil’s car sharing fleet comprised almost 18,000 vehicles across 11 cities in Russia and Anytime Prime’s long-term car rental fleet consisted of almost 600 vehicles. Delimobil’s car sharing fleet is composed mostly of economy class vehicles, including VW Polo, Fiat, Hyundai Solaris, Renault Kaptur and Kia Rio. Anytime Prime’s long-term rental fleet is composed of premium class and luxury vehicles, including top-of-the-line models from Mercedes-Benz, BMW and Porsche, enabling customers to enjoy a high-quality driving experience. Delimobil’s and Anytime Prime’s fleets are available to individual (“B2C”) and corporate (“B2B”) customers.

Our mobility offerings are supported by our advanced technology framework. We have two mobile apps for customers, our Delimobil and Anytime Prime apps, through which customers can sign up, view, select and book a vehicle as well as pay for their trip or rental. The number of registered users on our Delimobil and Anytime Prime apps has increased by 78%, from 4 million registered users as of December 31, 2019 to 7.1 million registered users as of September 30, 2021. We also rely on our proprietary data analytics technology to assess traffic, car demand and driving behavior, which we use to feed our pricing models and to continually improve the user experience of our customers.

A key differentiator of our business is our robust offline capabilities, which we offer through Smart Mobility Management (“SMM”), our fleet management infrastructure. We engage approximately 600 personnel, including full- and part-time employees as well as contractors, who provide repair and maintenance and tire, washing and refueling services for our vehicles to help ensure that our fleet is consistently in excellent condition

1

Table of Contents

and operating at maximum capacity. We have also developed Guido, a separate fleet management platform with a web application and mobile app for our operational personnel to use, that enables us to process and allocate servicing-related tasks for optimum efficiency.

In response to the COVID-19 pandemic, we promptly undertook a number of measures aimed at optimizing costs and increasing financial stability. These measures included the launch of our delivery service to capture increased delivery needs during the pandemic-related lockdown in 2020 when our core business operations were almost completely suspended from April 13 to June 10, 2020. After the lockdown, we continued with our delivery service and now regard this service not only as an additional source of revenue but also as a way to optimize fleet usage when our vehicles are not employed for car sharing.

We grew our total revenue from RUB 2,245 million for the six months ended June 30, 2020 to RUB 4,930 million for the six months ended June 30, 2021, representing a period-over-period growth of 120%. We grew our total revenue from RUB 5,012 million for the year ended December 31, 2019 to RUB 6,449 million for the year ended December 31, 2020, representing a year-over-year growth of 29%. For the six months ended June 30, 2021, we had a gross profit/(loss) of RUB 1,021 million and an Adjusted Gross Profit/(Loss) of RUB 1,115 million, compared to a gross profit/(loss) of RUB (521) million and an Adjusted Gross Profit/(Loss) of RUB (502) million for the six months ended June 30, 2020. For the year ended December 31, 2020, we had a gross profit/(loss) of RUB 72 million and Adjusted Gross Profit/(Loss) of RUB 163 million, compared to a gross profit/(loss) of RUB (476) million and an Adjusted Gross Profit/(Loss) of RUB (441) million for the year ended December 31, 2019. For the six months ended June 30, 2021, we generated a loss for the period of RUB 1,070 million and an Adjusted EBITDA gain of RUB 785 million, compared to a loss for the period of RUB 2,296 million and an Adjusted EBITDA loss of RUB 605 million for the six months ended June 30, 2020. For the year ended December 31, 2020, we generated a loss for the period of RUB 3,056 million and Adjusted EBITDA loss of RUB 286 million, compared to a loss for the period of RUB 3,573 million and Adjusted EBITDA loss of RUB 1,055 million, for the year ended December 31, 2019. See “Selected Combined and Consolidated Financial and Operating Data—Non-IFRS Measures” for more information and for reconciliations of Adjusted Gross Profit/(Loss) to gross profit/(loss) and Adjusted EBITDA to loss for the period, the most directly comparable financial measures calculated and presented in accordance with IFRS.

Our results of operations for the six months ended June 30, 2020 were materially affected by the COVID-19 pandemic, as we suspended our car sharing and long-term rental services from April 13 to June 10, 2020 in compliance with mobility restrictions put in place by the Russian government. Despite these restrictions, our business proved resilient during this uncertain period, and partially as a result of the measures we undertook at the time, we experienced revenue growth of 29% for the year ended December 31, 2020, when compared to the year ended December 31, 2019. For further discussion on the impact of the COVID-19 pandemic, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Key Factors Affecting Our Performance—Impact of the COVID-19 Pandemic.”

Our Industry

Russia Macroeconomic Overview

Russia is the world’s ninth most populous country, with 146.2 million inhabitants as of December 31, 2020. According to Rosstat, the country had an urbanization rate, or the percentage of people living in cities compared to people living in rural areas, of nearly 75% as of January 1, 2021. In 2020, Russia’s economy was the sixth largest globally and the second largest in Europe in terms of total nominal gross domestic product (“GDP”) based on purchasing power parity (“PPP”), according to the IMF. GDP per capita PPP was $26,450 in Russia in 2020.

With an estimated 123 million users, the Russian internet user base is Europe’s largest and the world’s sixth largest, according to Frost & Sullivan estimates. As of December 31, 2020, the country had an internet

2

Table of Contents

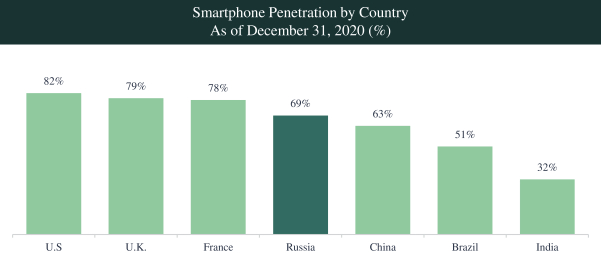

penetration rate, or the share of active internet users (people who use the internet at least once per month) as a percentage of the total population, of 84% and a smartphone penetration rate, or the share of active smartphone users (usage frequency of at least once a month) as a percentage of the total population, of 69%, according to Rosstat. Ongoing telecommunication infrastructure expansion is expected to push internet penetration to over 90% and smartphone penetration to approximately 80% by 2025, according to Frost & Sullivan estimates.

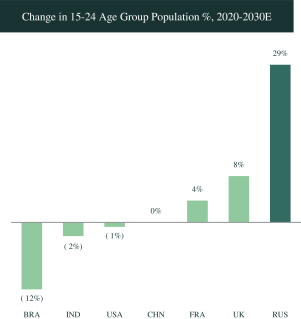

Together, these factors—large population, high urbanization, robust economy and digital readiness—are expected to drive disruption in on-demand, online-based shared mobility services, including car sharing and ride hailing. For example, most public transportation users, especially younger users, reveal a growing preference for digital platforms that offer on-demand services rather than physical cards or ticket-based services. Additionally, according to the United Nations Department of Economic and Social Affairs, the number of people aged 15 to 24 years in Russia is expected to increase 29% by 2030, compared to 8% in the United Kingdom, 4% in France and 0.01% in China. This has positive implications for shared mobility whose market value increased by approximately 4% in 2020, despite pandemic-related mobility restrictions, according to Frost & Sullivan.

Technology disruption in transportation has led to the emergence of new, online-based shared mobility services, such as ride hailing and car sharing, on top of existing methods of transportation. We define our market opportunity by reference to the Russian total addressable market (“TAM”) that we believe we can address over the long term. Our TAM consists of the aggregate value of the personal car market (limited to cars in cities with populations of over 100,000 people), the public city transportation market (limited to public transportation trips (excluding airlines) undertaken by passengers with driving licenses in cities with populations of over 100,000 people), the shared mobility market (ride-hailing, car sharing and long-term car rental markets) and the corporate car market (both leased and non-leased). Therefore, our TAM includes personal and corporate cars, shared mobility services (i.e., taxis and car sharing) and all modes of public transportation. According to Frost & Sullivan, our TAM totaled RUB 7.8 trillion (approximately $110 billion) in 2020 and is projected to increase at a compound annual growth rate (“CAGR”) of 7.8%, reaching RUB 11.4 trillion in 2025.

This increase is expected to be driven by growing demand, rising consumer incomes, shifting passenger preference for different modes of mobility, government mandates for sustainability and institutional support, according to Frost & Sullivan. Between 2017 and 2019, the Russian transportation market value grew consistently at a CAGR of 7.6%. In 2020, the market increased by more than 5%, despite the negative impact of the COVID-19 pandemic. Frost & Sullivan estimates that the total transportation market accounted for approximately 9% of Russia’s real GDP in 2020. The market is expected to further accelerate in 2021, growing to RUB 8.6 trillion.

Russian Car Sharing Market

Car sharing services in Russia are characterized by vehicles undertaking one-way, free-floating trips offered predominantly on a per-minute rental basis and usually in a pre-defined service coverage area. As of September 2020, the average travel time for a car sharing trip in Moscow was about 33 minutes, with an average trip distance of 12 km, according to the Moscow Department of Transport.

Russia had more than 20 car sharing operators with a total fleet of almost 45,300 vehicles and presence in 26 cities as of December 31, 2020. Car sharing services are now available in all Russian federal districts with the exception of the North Caucasus and Far Eastern federal districts, according to Russian Automotive Market Research.

The launch of Anytime (which was later rebranded by us as Anytime Prime) in 2012 in Moscow marked the start of Russia’s car sharing market. After a period of slow growth, the market picked up momentum with the introduction of the Moscow Car Sharing Project in 2015. Since 2017, the Moscow government has been providing certain subsidies to car sharing operators. For example, in 2020, annual parking permit costs were around RUB

3

Table of Contents

26,700 for car sharing operators in Moscow, which represented more than a 90% discount relative to those for personal car owners. Additionally, the Moscow government provided taxi and car sharing operators with subsidies of approximately RUB 300 million and RUB 280 million in 2020 and 2021 year-to-date, respectively.

Moscow accounted for over 80% of Russia’s car sharing fleet in 2018, according to Frost & Sullivan. In 2019, its share fell to 66% due to strong adoption of car sharing services in other cities with over one million inhabitants, including St. Petersburg, Novosibirsk, Yekaterinburg, Kazan, Nizhny Novgorod, Samara and Rostov-on-Don.

With over 25,000 vehicles, Moscow has the world’s largest car sharing fleet, while St. Petersburg ranks fifth with 9,560 vehicles. According to Frost & Sullivan, the car sharing fleet size in Moscow is expected to grow from 25,000 vehicles in 2020 to more than 49,000 vehicles by 2025. The car sharing fleet size in St. Petersburg is also expected to grow during the same period, from approximately 9,600 vehicles to more than 16,000 vehicles, on the back of growing popularity of car sharing, rising fuel prices and the costs associated with car ownership.

Furthermore, according to Frost & Sullivan, in 2020, car sharing penetration among Russian drivers between the ages of 18 and 60 with a valid driver’s license was only 5.3% in cities with more than 500,000 inhabitants and 22% in Moscow. Frost & Sullivan forecasts that by 2025, 21% of eligible drivers1 in such cities and almost 50% of people eligible to drive in Moscow and St. Petersburg will become car sharing users, indicating significant growth potential for the Russian car sharing market.

Our Strengths

Large and Rapidly Growing Car Sharing Market in Russia

Russia is one of the world’s leading car sharing markets, according to Frost & Sullivan. Additionally, among cities worldwide, Moscow is the global leader in car sharing in terms of fleet size, with an estimated 25,000 vehicles as of the end of 2020, which is 20% larger than the fleet size of Tokyo, the next largest market.

Despite the strong and established presence of car sharing in Russia, there is still significant room for growth, with the overall mobility market, which also includes public transportation, taxis and ride hailing and personal and corporate car use, remaining much larger. In 2020, car sharing represented 0.3% of the total transportation gross merchandise value (“GMV”) in Russia, while over 70% of the estimated RUB 7.8 trillion market GMV remained allocated to personal cars. According to a report by Frost & Sullivan, the overall shared mobility market is estimated to reach approximately RUB 1,250 billion by 2025.

There are a number of key factors which support the recent and future growth of the car sharing market.

| • | Attractive Cost and Value Proposition |

| • | When compared to other shared mobility options, car sharing comes closest to an ownership experience but without additional costs related to depreciation, fuel, insurance and maintenance. Russia’s cost of capital, combined with relatively high car prices, makes it challenging for certain segments of the population to own a personal car. Our mobility services allow customers to focus on the things that matter, providing cars on demand without the related hassle and many of the costs of car ownership. |

| • | Untapped Regional Opportunity |

| • | Car sharing is expected to gain significance in cities with over 500,000 inhabitants, relatively low income levels and ineffective public transportation networks. Cost considerations will play |

| 1 | Population over 18 years with driving licenses. |

4

Table of Contents

| a major role in the expected shift from personal car use to car sharing in these cities. We expect that a younger car sharing fleet, compared to the older age of personal cars in use, will further attract users by offering a better driving experience in terms of performance, comfort and safety. |

| • | The growth of car sharing in these cities is expected to result in improved unit economics, which we believe is reflected by the growth of our car sharing operations in, for example, Novosibirsk and Yekaterinburg. In both cities, the increase in the size of our car sharing fleet corresponded with the following unit economics improvements: |

| • | In Novosibirsk, the increase in our car sharing fleet from approximately 90 to 460 vehicles between August 2019 and August 2021 corresponded with a 34% increase in revenue per car per day;2 and |

| • | In Yekaterinburg, the increase in our car sharing fleet from approximately 240 to 570 vehicles over the same period corresponded with a 45% increase in revenue per car per day.2 |

| • | Infrastructure Readiness |

| • | Organic growth of car sharing in cities will be heavily influenced by smartphone and internet penetration. Rising internet penetration and smartphone adoption rates are poised to drive a greater uptake of app-based mobility services such as car sharing. |

| • | Institutional Support |

| • | Government subsidies for the car sharing industry have catalyzed growth in several cities. Government support, particularly during the initial stages of operations, will be instrumental to the expansion of car sharing services in other regions. Car sharing provides an opportunity for governments to deal with issues such as parking, space management and congestion. |

| • | Urbanization |

| • | Russia has 38 cities with populations of over 500,000 people, which is, for example, more than in the United States, and 133 cities with populations between 100,000 and 500,000 people, providing a strong basis for future growth. Migration and urbanization impact such cities in multiple ways, including (i) leading to congestion, inadequate parking space and an overstrained public transportation infrastructure and (ii) expanding the geographical limits of a city as housing requirements increase. Consequently, there is a growing need for more efficient and economic transportation options. Car sharing is well-positioned to offer such a sustainable transportation alternative. |

| • | Congestion |

| • | Consistent increases in the total number of cars on the road is one of the key factors behind high congestion levels. Car sharing can effectively minimize congestion levels by reducing the number of vehicles on the road. The Moscow Department of Transport estimated that as of March 2021, car sharing resulted in 250,000 fewer cars on roads per day in Moscow. |

| • | New Business Models and User Base |

| • | New business models such as long-term car rentals and vehicle subscription are expected to drive the car sharing market in three ways: (i) by improving vehicle utilization; (ii) by |

| 2 | Revenue per car per day has been derived from Revenue for Car Sharing for the respective city. |

5

Table of Contents

| expanding the existing user base; and (iii) by diversifying revenue streams for car sharing operators. Long-term car rentals are typically full-day rentals which can be used for both intra- and inter-city trips. Under a vehicle subscription model, vehicles from a wide range of brands and models can be rented for up to 18 months continuously with no requirement of credible financial history. Rental fees under this subscription model typically account for insurance, repairs and tire services. |

Market Leader Advantage in a Market with Significant Barriers to Entry

For any new player entering the car sharing market in Russia, there are a number of meaningful hurdles. We have determined five key barriers to entry that any potential new market player would need to address in order to compete with us, as Delimobil has all critical components in place—which we believe are difficult to replicate:

| • | Large Fleet and Customer Base Requirement |

| • | While the car sharing market offers significant growth potential, opportunities for new entrants and smaller incumbents are limited, since market success is largely determined by the ability to achieve high car density to provide customers with quicker access to vehicles. Furthermore, established operators have a wide customer base that is essential for optimal fleet utilization. New entrants would be required to acquire a large customer base, establish a brand name and gain customer loyalty, which would take significant time and investment. |

| • | Capital Intensive Market |

| • | The car sharing market requires significant investments into fleet, operations, maintenance and technology. Access to finance and low-cost capital is crucial to scale up an operator’s business. New entrants would be dependent on their ability to obtain such financing and low-cost capital in order to effectively compete with established players. |

| • | Advanced Technology Solutions |

| • | The need for advanced technological capabilities represents an increasingly significant barrier to entry. Car sharing operators require technology to achieve competitive differentiation and to mitigate risks such as reckless driving and vehicle damage. New technological platforms are improving efficiency, safety and security of car sharing systems. The need to make simultaneous investments into both technology and fleet expansion would put significant pressure on the ability of new operators to enter the market, gain scale and/or reach profitability. |

| • | Need for Offline Service Infrastructure |

| • | Enhancing efficiency and reducing downtime through fleet management, maintenance and repair have become vital for car sharing operators. In order to reduce downtime, operators are investing in fleet rebalancing capabilities and aftermarket services such as maintenance, repairs, cleaning and insurance. The development of a similar ecosystem that results in profitability would require investment of significant operational, financial and time resources for new entrants. |

| • | Strategic Partnerships with OEMs and Leasing Companies |

| • | Partnerships are a prerequisite to ensure cost-effective access to a wide range of high quality vehicles. For car sharing operators, this is critical for achieving financial stability. Established |

6

Table of Contents

| operators have been able to develop long-standing relationships with Original Equipment Manufacturers (“OEMs”) and leasing companies that we believe may be difficult for new market entrants to replicate in light of their limited history of operations. |

Leading Car Sharing Service in Russia with Widest Presence in Regions

Delimobil’s presence across a wide range of Russian regions is one of our key differentiators when compared to our competitors. Since our launch in Moscow in 2015, we have expanded to an additional 10 cities, including most recently to Kazan and Rostov-on-Don. Currently, our total operational reach covers more than 25% of the Russian urban population (based on Rosstat data). Our rivals, BelkaCar, Yandex.Drive and CityDrive, operate in five, four and three cities, respectively. With almost 18,000 cars in our fleet as of September 30, 2021, we capture approximately one-third of the Russian car sharing market, according to Frost & Sullivan. In Moscow, we have become the leader in the market by number of trips, achieving a market share of approximately 44% as of August 2021, according to the Moscow Transportation Department.

Given our wide geographic presence, we also have the flexibility to relocate cars between cities and benefit from a wide range of options of where to relocate cars, which increases our business efficiency and resilience to the possible shortfalls of limiting our vehicles to specific locations. This proved critical to our performance during the lockdown in Moscow in response to the COVID-19 pandemic, as we were able to mitigate the sharp decline in customer demand in Moscow by relocating a portion of our fleet to cities with less strict mobility restrictions in place. Under this relocation campaign, we moved 2,435 cars from Moscow to the regions during the period of March to May 2020. Moreover, we have a wide range of options of where to transfer our cars after three years of operating in Moscow, where the local regulator gives special parking permits for car sharing vehicles only during the first three years of their use and for cars not older than one year when first used. We continually monitor the situation in the cities in which we operate and can quickly relocate cars from lower-demand to higher-demand areas.

Delimobil’s wide regional presence is also in high demand among our clients, especially given international travel restrictions and the growing interest in domestic tourism, which differentiates us from our competitors. We believe that our experience and track record of successful regional expansion will support our further growth in the Russian regions and already positions us strongly to capture additional market opportunities.

Shared Mobility Platform for Seamless User Experience, Driven by the Mobile App

Delimobil’s full customer proposition is delivered through its mobile app, facilitating a simple and seamless user experience by taking customers through each step of the process. The simplicity and speed by which customers can book and then drive our cars, a process which consists of locating the car, booking the car, checking its condition, renting and driving, is a core element of our customer experience. There are a number of elements that make up Delimobil’s differentiated customer proposition:

| • | High availability and convenience driven by a large optimized fleet |

| • | Delimobil has a large fleet with almost 18,000 cars, allowing for high availability and accessibility for customers looking to travel via car sharing. Across Moscow, the average travel time on foot for customers to reach the car they booked is approximately 5 minutes. |

| • | Superior Car Quality |

| • | Delimobil’s cars offer a consistently strong, high quality service—supported by the in-house operations of SMM, which carry out repair and maintenance, car washing and refueling services. |

7

Table of Contents

| • | Superior Value Proposition |

| • | Unlike most public transportation and car rental services, Delimobil offers 24/7 availability with the same level of safety and around-the-clock service. Customers are able to access Delimobil’s cars at any time, unconstrained by schedules, timetables and car rental offices. After an easy and fast online onboarding process, customers are also able to use our vehicles for whatever duration they require – from minutes to multiple days. Customers are able to benefit from the comfort of having exclusive use of a car, choosing from a wide selection of makes and models, with the flexibility to leave it at any available parking space. |

| • | User Rating-based Transparent Smart Pricing |

| • | Delimobil offers smart-pricing, which dynamically reflects a number of factors including a customer’s driving profile as well as the supply and demand of vehicles at a particular location and time of day. For example, disciplined drivers can receive up to a 40% discount on the price of their trip. Delimobil’s pricing approach is both transparent and cost effective, and it captures essentially all of the customer’s costs in one easy-to-comprehend figure. |

| • | Broadest coverage area |

| • | With the largest coverage area of any Russian competitor of approximately 1 million square kilometers, according to the Company’s estimates, Delimobil provides the greatest access to its customers to travel across the country. This also supports customers’ ability to take trips of any length, from across the city to across the country. |

| • | Strong Independent Brand |

| • | Delimobil ranked first in top-of-mind and brand awareness among Russian car sharing providers in December 2020, according to brand health tracking research done by Tiburon Brand Health Research. Our strong brand allows us to build a deep connection between our brand and our customers, helping us to drive further growth of MAU and to improve customer loyalty and engagement. |

| • | Large Fleet with a Wide Variety of High Quality Cars |

| • | Car density is a key driver of the success of our business model. We have consistently adhered to our strategy, even during the peak of the COVID-19 outbreak in 2020. Due to our strong relationship with OEMs, we were able to maintain supply of new vehicles to support our fleet growth. As a result, our EoP Fleet grew almost three times more than the market average. We provide access to a large fleet, with a wide range of high quality cars—ranging from VW Polos to Mini Coopers and BMWs. The quality of our cars, supported by our strong offline service infrastructure, helps ensure a strong customer experience for every trip taken. Although our fleet is composed of four classes of vehicles—economy, comfort, premium and vans—our business strategy is focused on economy class models, targeting the largest audience in Russia. As of September 30, 2021 economy class models accounted for 84% of our fleet, with comfort class models, premium class models and vans accounting for 11%, 4% and 1% of our fleet, respectively. |

8

Table of Contents

Comprehensive Technology Stack Driving Operations and Efficiency

Delimobil’s operations are supported by a powerful, data driven technology platform. This platform not only supports a seamless customer experience through our mobile app, but it also bolsters our fleet management, pricing and innovation. The cloud-based platform is highly scalable, and it is maintained and optimized by a dedicated team of approximately 80 highly qualified engineers. Our comprehensive platform supports and powers all elements of our operations, with three core aspects of the technology.

| • | In-vehicle technology. Our entire car sharing fleet is equipped with Internet of Things (“IoT”) devices, which have been optimized for each car model, to collect real-time data on driving behavior and car telemetry which feeds into our pricing and customer rating models as well as Guido, our fleet management software, so we can ensure that our fleet is consistently in excellent condition and operating at maximum capacity. |

| • | Data analytics technology. We developed our platform to analyze the big data we collect from various sources, such as IoT devices installed in our cars, customer feedback (via call center or in-app functionality) and our fleet maintenance software (Guido and enterprise resource planning (“ERP”)). Its algorithms and other business intelligence tools are the backbone of our operations. |

| • | Fleet management technology. To support SMM, our fleet management infrastructure, we have developed Guido, our fleet management technology platform which our operational personnel access through our operational personnel-only mobile app. As of August 31, 2021, the Guido app had over 500 daily active users, or the total number of unique users who completed at least one work order for a car in our fleet per day calculated as an average over the reporting period, and, as of September 30, 2021, processed approximately 11,000 work orders per day covering over 30 different types of vehicle services, including repair and maintenance and tire, washing and refueling services. |

To provide support for our technology platform, we have data systems capable of supporting 5TB of telemetry data per year, and we use third-party cloud computing services and maintain a data center in partnership with large IT companies such as Dataline and Rostelecom in order to scale up our technology-based services to meet spikes in usage. In September 2021, we processed an average of 398,000 requests per minute from users of our platform.

Strong In-House Fleet Management and Operations Infrastructure

Our own in-house fleet management infrastructure, SMM, is one of the main differentiators of our business model versus other car sharing companies in Russia. We have our own capabilities to repair and maintain, wash and refuel our cars. Out of the three main capabilities of SMM, only refueling is performed on a proprietary basis by some of our competitors, while repair and maintenance, including tire services, and car washing are outsourced by our competitors to multiple third-party providers, according to market sources.

SMM enables us to reduce car idle time, thereby maintaining car uptime (i.e., availability for booking by customers) at up to a 90% level. In addition, our fleet management infrastructure helps us ensure a consistent quality of car maintenance across our fleet, simplifies the roll-out of vehicles in new cities and allows us to provide timely support to our customers in case of road accidents.

Based on our internal estimates, SMM is the largest proprietary car fleet management operator in Russia and we believe that there are no independent car service providers that could provide the full range of SMM’s services at the scale needed to support our fleet. SMM has operations in Moscow, St. Petersburg and

9

Table of Contents

Yekaterinburg, engages third-party providers in other regions and services almost 18,000 cars. SMM’s operations engage over 600 personnel, including full- and part-time employees as well as contractors as of September 30, 2021, and its facilities have a total area of approximately 25.7 thousand square meters.

To support SMM, we have developed Guido, a separate fleet management technology platform with a web application and mobile app for our operational personnel to use. It collects, stores and instantly analyzes the data on each car’s servicing history, including technical inspections, repairs, spare parts and costs. Guido enables us to provide customers with high-quality cars while keeping the maintenance costs at an optimal level.

Rapid Growth and Progress towards Profitability

We have grown rapidly since inception, with a 29% growth in revenue for the year ended December 31, 2020, outpacing the growth of the total car sharing market in Russia by 11%, according to Frost & Sullivan. We believe our growth in 2020 also demonstrates the resilience of our business model despite the COVID-19 headwinds. We believe that our business model provides a substantial degree of protection from economic volatility as car sharing has proven to be a more favorable mobility option than ride hailing and private car ownership from a usage costs perspective. This is the main idea behind Delimobil’s focus on the mass-market mobility segment: our car fleet composition is skewed towards economy and comfort class models. We believe that our growth is underpinned by a predictable and loyal customer base, as well as our ability to increase monetization per user through price revisions. For our car sharing service, we increased Revenue per Minute by 28% over the years ended December 31, 2019 and 2020 and by 24% between the year ended December 31, 2020 and the six months ended June 30, 2021. See “Management’s Discussion and Analysis of Financial Condition And Results–Key Operating and Financial Metrics” for more information on Revenue per Minute.

Our business has also experienced increasing customer engagement, which we attribute to the high-quality user experience and diverse offering of vehicles and pricing methods we offer to customers through our platform. For our car sharing service, we measure customer engagement by monitoring customer cohorts, which we define as a group of customers who took their first trip in a given period, in two ways: (i) by assessing the retention of a specific customer cohort from one period to another and (ii) by calculating the frequency of usage of our service by a specific customer cohort during a given period. See “Management’s Discussion and Analysis of Financial Condition and Results—Key Factors Affecting Our Performance—Growth” for more information on how we measure retention rate. In addition, the customers we retain tend to use our car sharing services with increasing frequency and the number of days between each trip booked tends to decrease. As the graph below shows, in 2020, 80% of customers who booked a first trip went on to book a second and 88% of customers who booked a fourth trip went on to book a fifth. For the same period, there was a decrease in the number of days between each trip booked from 1.7 days between the first and second trip to 1.3 days between the fourth and fifth trip. We believe this decrease in number of days between each trip booked is a strong indicator of customer engagement. This in turn links strongly to increased spending: for example, our 2019 customer cohort spent on average 73% more in their second month of usage and 59% more in 2020. Eventually, these factors create a powerful network effect: the more our customers use our services, the more they enjoy it, stay with us and spend

10

Table of Contents

with us. This also creates a powerful brand impact as engaged users act as a free and very natural source of “word of mouth” marketing.

(1) All data for car sharing services only. Days between trips based on the median customer. Data for 2020.

Source: Company data

Our disruptive business model and strong execution has helped us improve performance. For example, we generated a gross profit/(loss) of RUB 1,021 million and an Adjusted Gross Profit/(Loss) of RUB 1,115 million for the six months ended June 30, 2021, compared to a gross profit/(loss) of RUB (521) million and an Adjusted Gross Profit/(Loss) of RUB (502) million for the six months ended June 30, 2020. We also demonstrated a 20 percentage point improvement in Adjusted Gross Profit/(Loss) Margin between the year ended December 31, 2020 and the six months ended June 30, 2021. We reached a break-even point in 2020 due to cost of revenue optimization efforts and the ability to generate revenue at a higher rate than costs. As we scaled our operations, we were able to decrease sales and marketing expenses as well as general and administrative expenses as a percentage of revenue and improved Adjusted EBITDA Margin by 17 percentage points between the years ended December 31, 2019 and 2020 and by 20 percentage points between the year ended December 31, 2020 and the six months ended June 30, 2021 despite restrictions and limitations caused by the COVID-19 pandemic. The most directly comparable IFRS measure for Adjusted EBITDA Margin, which is derived from Adjusted EBITDA, is loss for the period. See “Selected Combined and Consolidated Financial and Operating Data” for a reconciliation of Adjusted EBITDA and Adjusted EBITDA Margin to loss for the period. We believe that we have further significant upside in performance as we continue to grow our market share and revenue base, considering the high operating leverage embedded in our business model.

As we continue to scale up our business, we believe that these factors, among others, will continue to positively impact our operations and drive improvement in results and unit economics.

Experienced Management Team and Dedicated Founders are Key to our Success

Delimobil benefits from a highly experienced and motivated management team, with a strong track record of success. Our management team has relevant industry experience in some of Russia’s and Europe’s

11

Table of Contents

largest and most established companies. This covers companies across a range of relevant sectors, including tech-driven internet platforms like Ozon, consumer-facing names like Procter & Gamble and transport and mobility companies like Scania. Through the leadership and management of the team, Delimobil was able to achieve a revenue increase of 29% for the year ended December 31, 2020, despite the COVID-19 pandemic and the resulting lockdowns. Moreover, through efficient planning and expert guidance we were able to concurrently increase our Adjusted EBITDA Margin by 17 percentage points between December 31, 2019 and 2020. For the six months ended June 30, 2021, we achieved a revenue increase of 120% compared to the same period of 2020, and an increase in Adjusted EBITDA Margin by 43 percentage points over the same period. The most directly comparable IFRS measure for Adjusted EBITDA Margin, which is derived from Adjusted EBITDA, is loss for the period. See “Selected Combined and Consolidated Financial and Operating Data” for a reconciliation of Adjusted EBITDA and Adjusted EBITDA Margin to loss for the period.

Our management team has a wide range of complementary skill sets and has gained meaningful experience serving in and leading some of the well established companies. The combination of their international expertise and knowledge of the local mobility market has allowed us to build and grow a leading platform that delivers for our customers.

Our Growth Strategy

Our growth strategy is based on the following four pillars: regional expansion in Russia, further growth in major cities, offering of SMM services to third parties and further development of subscription services.

To facilitate implementation of our growth strategy, we aim to continue expanding our car sharing and long-term car rental fleets and to increase their uptime by improving our operating efficiency with smart fleet management. In addition, we plan to pursue additional marketing efforts to maintain high awareness of and further strengthen our brand. We also expect to further enhance our customer experience by introducing new features, meeting the needs of new target audiences and updating our mobile applications. Moreover, as we upgrade our dynamic pricing algorithms, we expect that higher average revenue per user (“ARPU”) will also drive growth across our geographical presence. See “Management’s Discussion and Analysis of Financial Condition and Results—Key Factors Affecting our Performance—Growth—Customers Base” for more information on ARPU.

Regional Expansion

We aim to have an operating car fleet in all Russian cities with populations exceeding 500,000 people in the long term. According to Rosstat, there are 38 such cities in Russia, which would provide for a total population coverage of approximately 48 million people. Delimobil is well-positioned to achieve this target considering its significant track record of regional expansion. Delimobil has operational presence in 11 Russian cities as of September 30, 2021, ahead of competitors BelkaCar, Yandex.Drive and CityDrive, which are present in only five, four and three cities, respectively, according to Frost & Sullivan. We believe that we can leverage our scalable in-house fleet management infrastructure, large fleet size and flexibility to promptly relocate cars in order to roll out operations in new cities.

We also plan to further grow our business in all regional cities in which we currently operate, as Russian regional markets remain significantly under-penetrated. According to Frost & Sullivan, the level of car sharing penetration in cities with populations exceeding 500,000 (excluding Moscow and St. Petersburg) and among Russian drivers between the ages of 18 and 60 years with a valid driver’s license was only 5.3% in 2020, a figure which is expected to rise to 21.4% by 2025. In addition, we are also promoting inter-city travel via car sharing to capitalize on expanding domestic tourism in Russia, and we already have a roadmap of IT developments to tailor our services for such purpose.

12

Table of Contents

Further Growth in Major Cities

We believe that Delimobil has substantial room for continued growth in Moscow and St. Petersburg. Frost & Sullivan forecasts that 50% of people eligible to drive in Moscow and St. Petersburg will become car sharing users by 2025, compared to 22.3% and 12.9% in 2020 in Moscow and St. Petersburg, respectively.

We expect to continue leveraging our well-recognized brand, our deep knowledge and expertise of operating in these cities and our established approach to car location and utilization to pursue further growth in these cities. In particular, we expect to focus on targeting new audiences such as the younger population of 18 to 24 years and the middle-aged population of 50 years and older.

Further Development of Subscription Services

While continuing to develop and expand our car sharing service, which is our primary offering, we also expect to scale up our vehicle subscription model for our long-term rental service in Anytime Prime and to introduce a similar subscription model to our car sharing business in Delimobil. We also plan to further develop our B2B car sharing offerings. Anytime Prime provides a revenue stream based on longer-term relationships as customers can book cars for a period ranging from one day to one year. The car fleet available to Anytime Prime users consists of almost 600 cars as of September 30, 2021. Our long-term rental service also provides further up-selling opportunities, shifting the focus of our revenue model from fleet size to the size of our customer base. Furthermore, Anytime Prime targets a different customer audience, with a focus on the premium segment, and has only a minor overlap with Delimobil, which is more focused on the mass market. At the same time, we are testing subscription services on car sharing for Delimobil’s mass market audience. Our corporate B2B car sharing service, launched in May 2019, allows us to capture enterprise clients.

SMM Services to Third Parties

We are also currently evaluating opportunities for new product launches. For example, we are exploring the opportunity to offer our SMM capabilities to third parties, including consumers and enterprises, since our fleet maintenance operations feature a streamlined process and significant economies of scale which are not available to smaller companies.

International Expansion

In addition to the four strategy pillars described above, we consider the potential to enter into foreign markets as an additional long-term growth opportunity rather than a short-term goal. We are contemplating the opportunity to develop a franchising model in order to extend our international presence.

Moreover, in August 2021, we entered into call option agreements with one of our shareholders under common control of our ultimate controlling party that will provide us with the option to purchase all or substantially all of the shares of D-Mobility Czech Republic s.r.o., Carsharing Club LLC and D-Mobility Kazakhstan LLC, which operate car sharing businesses in the Czech Republic, Belarus and Kazakhstan, respectively, under a similar business model as ours. The exercise of the call options is subject to approval by our board of directors and would be exercisable from January 1, 2023 until July 1, 2023. For further information on these transactions, see “Certain Relationships and Related Party Transactions—Option Agreements.”

Risk Factors

Investing in the ADSs involves risks. You should carefully consider the risks described in “Risk Factors” before making a decision to invest in the ADSs. If any of these risks actually occurs, our business,

13

Table of Contents

financial condition or results of operations could be materially and adversely affected. In such case, the trading price of the ADSs would likely decline, and you may lose all or part of your investment. The following is a summary of some of the principal risks we face:

| • | the continuing impact of the COVID-19 pandemic on demand for our service and the effects of regulations of car sharing enacted to mitigate the pandemic; |

| • | significant competition in our markets; |

| • | any ability to effectively manage our growth; |

| • | our lack of historical profitability and risks in achieving profitability in the future; |

| • | our ability to effectively manage our technology platform; |

| • | our ability to maintain and enhance our brand; |

| • | our ability to successfully manage the size, effectiveness and resale of our fleet; |

| • | our ability to maintain favorable terms of insurance for our fleet; |

| • | our ability to attract and retain key personnel and IT specialists; |

| • | our ability to successfully manage and continually advance technology used in our business; |

| • | global political and economic stability; |

| • | ongoing development of the Russian legal system and developing legal framework governing car sharing in Russia; |

| • | our ability to successfully remediate the significant deficiencies in our internal control over financial reporting and our ability to establish and maintain an effective system of internal control over financial reporting; |

| • | the ability of our controlling shareholder to exert significant control over us, and its interests conflicting with those of the holders of the ADSs; and |

| • | as a foreign private issuer and a “controlled company”, we are exempt from a number of rules under the U.S. securities laws and the NYSE corporate governance rules and are permitted to file less information with the SEC than U.S. companies, which may limit the information available to holders of the ADSs. |

Corporate Information

Delimobil Holding S.A. is a public limited liability company (société anonyme) organized and incorporated under the laws of Luxembourg on January 18, 2021. Our registered office is located at 10, rue C.M. Spoo, L-2546 Luxembourg, Grand Duchy of Luxembourg, and we are registered with the Luxembourg Register of Commerce and Companies under number B250892. Our telephone number at this address is +352 26 97 63 04. Our main office outside of Luxembourg is located at 27 Elektrozavodskaya St., Moscow, Russia. Our website is https://delimobil.com/. We have included our website address in this prospectus solely for informational purposes. None of the information available on our website is incorporated in this prospectus, and it should not be relied upon in making a decision to invest in the ADSs.

14

Table of Contents

Implications of Being an Emerging Growth Company and a Foreign Private Issuer