UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

OR

For the fiscal year ended

OR

For the transition period from _______________ to _______________

OR

Commission file number:

(Exact name of Registrant as specified in its charter) |

ONTARIO,

(Jurisdiction of incorporation or organization)

(Address of principal executive offices

TELEPHONE: (

EMAIL:

ADDRESS:

(Name, Telephone, E-Mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12 (b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

Common Shares (no par value) |

|

| OTCQB CSE Frankfurt |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

The number of outstanding common shares of GameSquare’s only class of capital or common stock as at May 2, 2022 was

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None.

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report: 244,381,900.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See the definition of “accelerated filer” and “large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☐ | Emerging growth company |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP | ☒ | ☐ | Other | ☐ |

If “Other” has been checked in response to previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes

TABLE OF CONTENTS

|

|

| 4 |

| |

|

| 4 |

| ||

|

| 4 |

| ||

|

| 4 |

| ||

|

| 17 |

| ||

|

| 27 |

| ||

|

| 35 |

| ||

|

| 39 |

| ||

|

| 40 |

| ||

|

| 41 |

| ||

|

| 41 |

| ||

| 50 |

| |||

|

| 50 |

| ||

|

|

| 51 |

| |

|

| 51 |

| ||

| ITEM 14. | MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

| 51 |

| |

| 51 |

| |||

| 51 |

| |||

|

| 53 | |||

| F-1 - F-39 |

| |||

|

| 53 |

| ||

| 2 |

| Table of Contents |

In this Form 20-F, the terms “we”, “our”, “us” and “GameSquare” refer, unless the context requires otherwise, to GameSquare Esports Inc.

CURRENCY

All amounts are expressed in Canadian dollars (“C$”) unless otherwise stated. See the information under the heading “Item 3.A. Selected Financial Data - Exchange Rates” for relevant information about the rates of exchange between Canadian dollars and the other functional currencies used by certain subsidiaries of GameSquare.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements contained in this registration statement on Form 20-F (this “Form 20-F”) constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward- looking information” within the meaning of Canadian provincial securities laws (such forward-looking statements and forward-looking information are referred to herein as “forward-looking statements”). These statements reflect our management’s expectations with respect to future events, the Company’s financial performance and business prospects. All statements other than statements of historical fact are forward-looking statements. The words “plans”, “expects”, “estimated”, “anticipates”, “intend”, “focus”, “outlook”, “potential”, “seek”, “strategy”, “vision”, “goal”, “targets” or “believes”, or variations of such words and phrases or statements that certain future conditions, actions, events or results “will”, “may”, “could”, “would”, “should”, “might” or “can”, or negative versions thereof, “be taken”, “occur”, “continue” or “be achieved”, and other similar expressions, frequently identify forward-looking statements. These statements involve known and unknown risks, uncertainties, and other factors that may cause actual results or events to differ materially from those anticipated or implied in such forward-looking statement. No assurance can be given that these expectations will prove to be correct and such forward-looking statement included in this Form 20-F should not be unduly relied upon. Unless otherwise indicated, these statements speak only as of the date of this Form 20-F.

In particular, this Form 20-F contains forward-looking statements pertaining to, among other things, opportunities within esports, industry trends, the Company’s growth strategy, ability to pursue and execute on opportunistic and accretive acquisitions; synergies available to the Company following acquisitions; the Company’s business objectives; the Company’s ability to monetize its core asset portfolio; and the Company’s ability to execute on its business plan and the factors discussed under “Item 3. Key Information - D. Risk Factors.”

In addition to any factors and assumptions set forth in this Form 20-F, the material factors and assumptions used to develop the forward-looking information include, but are not limited to: the Company being able to grow its business and execute on its business plan, the Company being able to successfully identify and integrate strategic acquisition opportunities; the Company being able to recognize and capitalize on opportunities earlier than its competitors; the culture and business structure of the Company supporting its growth; the Company continuing to attract qualified personnel to support its development requirements; and that the risk factors noted below, collectively, do not have a material impact on the Company.

Known and unknown risk factors, many of which are beyond the control of the Company, could cause actual results to differ materially from the forward-looking information in this Form 20-F. Such factors include, without limitation, the following: industry competition, the Company’s ability to achieve its objectives, the Company’s size and position in the industry and its growth strategy, the ability of the Company to obtain future financings or complete offerings on acceptable terms, the ability of the Company to leverage its portfolio across entertainment and media platforms, dependence on the Company’s key personnel, ability to execute on future acquisitions, mergers or dispositions, currency exchange rates, laws and government regulations, electronic data compromises and general business, economic, competitive, political and social uncertainties including the impact of the COVID-19 pandemic and its variants. This list is not exhaustive of the factors that may affect any of our forward-looking statements. Some of the important risks and uncertainties that could affect forward-looking statements are described further under the heading “Item 3. Key Information - D. Risk Factors.”. If one or more of these risks or uncertainties materializes, or if underlying assumptions prove incorrect, our actual results may vary materially from those expected, estimated or projected. Forward-looking statements in this document are not a prediction of future events or circumstances, and those future events or circumstances may not occur. Given these uncertainties, users of the information included in this Form 20-F, including investors and prospective investors are cautioned not to place undue reliance on such forward-looking statements.

The forward-looking statements in this Form 20-F speak only as to the date hereof and are based on our beliefs, opinions and expectations at the time they are made. Except as required by applicable law, including the securities laws of the United States and Canada, the Company does not intend to update any of the forward-looking statements to conform these statements to actual results.

Any forward-looking statements included in this Form 20-F are expressly qualified by this cautionary statement, and except as otherwise indicated, are made as of the date of this Form 20-F. The Company does not assume or undertake any obligation to update or revise any forward-looking statements or departures from them, except as required by applicable law. New factors emerge from time to time, and it is not possible for our management to predict all such factors and to assess in advance the impact of each such factor on the business of the Company or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statement.

| 3 |

| Table of Contents |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

Selected Financial Data

The following tables present selected historical financial data for GameSquare and its subsidiaries (collectively, the “Group”). The balance sheet financial data as at December 31, 2021 and the income statement financial data for the year ended December 31, 2021, in each case as set forth below, has been derived from the Group’s audited consolidated financial statements incorporated by reference in this Form 20-F. The Company changed its fiscal year-end from November 30 to December 31 during the 2021 fiscal year which resulted in a transition year of thirteen months.

| 4 |

| Table of Contents |

Balance Sheet

($ Canadian) |

| December 31, 2021 |

|

| November 30, 2020 |

| ||

|

|

|

|

|

|

| ||

ASSETS |

|

|

|

|

|

| ||

|

|

|

|

|

|

| ||

Current |

|

|

|

|

|

| ||

Cash |

| $ | 7,642,593 |

|

| $ | 660,686 |

|

Amounts receivable |

|

| 3,911,638 |

|

|

| 381,749 |

|

Prepaid expenses and deposits |

|

| 385,639 |

|

|

| 109,142 |

|

Other investments |

|

| - |

|

|

| 62,635 |

|

Other current assets |

|

| 388,478 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

Total current assets |

|

| 12,328,348 |

|

|

| 1,214,212 |

|

|

|

|

|

|

|

|

|

|

Long-term |

|

|

|

|

|

|

|

|

Equipment |

|

| 4,600,404 |

|

|

| 1,419 |

|

Intangibles |

|

| 9,339,175 |

|

|

| 2,361,567 |

|

Goodwill |

|

| - |

|

|

| 2,258,109 |

|

Right-of-use asset |

|

| 3,501,614 |

|

|

| - |

|

Reclamation deposits |

|

| 340,443 |

|

|

| 338,606 |

|

Non-current assets held for sale |

|

| 99,535 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

Total assets |

| $ | 30,209,519 |

|

| $ | 6,173,913 |

|

|

|

|

|

|

|

|

|

|

LIABILITIES |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Current |

|

|

|

|

|

|

|

|

Accounts payable and accrued liabilities |

| $ | 2,796,756 |

|

| $ | 845,273 |

|

Deferred revenue |

|

| 414,628 |

|

|

| 104,630 |

|

Current portion of lease liability |

|

| 382,057 |

|

|

| - |

|

Loan payable |

|

| 152,305 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

Total current liabilities |

|

| 3,745,746 |

|

|

| 949,903 |

|

|

|

|

|

|

|

|

|

|

Deferred consideration on acquisition of Code Red |

|

| - |

|

|

| 335,000 |

|

Long term loan |

|

| - |

|

|

| 40,000 |

|

Lease liability, net of current portion |

|

| 3,421,383 |

|

|

| - |

|

Reclamation provision |

|

| 323,933 |

|

|

| 323,933 |

|

Deferred tax liability |

|

| 347,958 |

|

|

| 464,000 |

|

|

|

|

|

|

|

|

|

|

Total liabilities |

|

| 7,839,020 |

|

|

| 2,112,836 |

|

|

|

|

|

|

|

|

|

|

SHAREHOLDERS' EQUITY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Common shares |

|

| 45,690,856 |

|

|

| 6,340,328 |

|

Share based payments reserve |

|

| 3,923,193 |

|

|

| 718,951 |

|

Contingently issuable shares |

|

| 66,238 |

|

|

| - |

|

Warrants |

|

| 2,923,808 |

|

|

| 827,461 |

|

Accumulated other comprehensive income |

|

| 221,183 |

|

|

| 884 |

|

Accumulated deficit |

|

| (30,341,957 | ) |

|

| (3,826,547 | ) |

|

|

|

|

|

|

|

|

|

Equity attributable to owners of the parent |

|

| 22,483,321 |

|

|

| 4,061,077 |

|

Non-controlling interest |

|

| (112,822 | ) |

|

| - |

|

|

|

|

|

|

|

|

|

|

Total Shareholders' Equity |

|

| 22,370,499 |

|

|

| 4,061,077 |

|

|

|

|

|

|

|

|

|

|

Total liabilities and shareholders' equity |

| $ | 30,209,519 |

|

| $ | 6,173,913 |

|

| 5 |

| Table of Contents |

Income Statement

The following tables present the Group’s statement of loss and comprehensive loss for the year ended December 31, 2021.

During the period ended December 31, 2021, the Company changed its fiscal year end from November 30 to December 31. As a result of this change, the results of the quarter ended December 31, 2021 are for the four months ended December 31, 2021 with the comparative period consisting of the three months ended November 31, 2020

($ Canadian) |

| December 31, 2021 |

|

| November 30, 2020 |

| ||

|

|

|

|

|

|

| ||

Revenue |

| $ | 13,687,889 |

|

|

| 488,774 |

|

|

|

|

|

|

|

|

|

|

Cost of sales |

|

| 9,250,631 |

|

|

| 331,228 |

|

|

|

|

|

|

|

|

|

|

Gross profit |

|

| 4,437,258 |

|

|

| 157,546 |

|

|

|

|

|

|

|

|

|

|

Other income |

|

|

|

|

|

|

|

|

Interest and other income |

|

| 9,645 |

|

|

| 1,947 |

|

|

|

|

|

|

|

|

|

|

Total other income |

|

| 9,645 |

|

|

| 1,947 |

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

Salaries, consulting and management fees |

|

| 7,617,319 |

|

|

| 760,648 |

|

Player compensation |

|

| 724,777 |

|

|

| - |

|

Professional fees |

|

| 1,436,522 |

|

|

| 8,323 |

|

General office expenses |

|

| 1,340,366 |

|

|

| 202,569 |

|

Selling and marketing expenses |

|

| 1,426,503 |

|

|

| - |

|

Travel expenses |

|

| 676,221 |

|

|

| 4,107 |

|

Shareholder communications and filing fees |

|

| 209,830 |

|

|

| 52,229 |

|

Interest expense |

|

| 181,527 |

|

|

| 11,497 |

|

Bad debt expense |

|

| 56,318 |

|

|

| 74,581 |

|

Foreign exchange loss |

|

| 2,972 |

|

|

| 5,110 |

|

Change in provision for reclamation deposit |

|

| (97,323 | ) |

|

| 6,308 |

|

Share-based compensation |

|

| 3,644,287 |

|

|

| 709,953 |

|

Transaction costs |

|

| 9,744,815 |

|

|

| 1,817,540 |

|

Amortization |

|

| 1,879,825 |

|

|

| 81,433 |

|

Impairment on goodwill |

|

| 2,258,109 |

|

|

| - |

|

|

|

|

|

|

|

|

|

|

Total expenses |

|

| 31,102,068 |

|

|

| 3,734,298 |

|

|

|

|

|

|

|

|

|

|

Loss for the period before income taxes |

|

| (26,655,165 | ) |

|

| (3,574,805 | ) |

Income tax (recovery) |

|

| (98,854 | ) |

|

| (1,697 | ) |

Loss for the period |

|

| (26,556,311 | ) |

|

| (3,573,108 | ) |

|

|

|

|

|

|

|

|

|

Other comprehensive loss |

|

|

|

|

|

|

|

|

Items that will subsequently be reclassified to operations: |

|

|

|

|

|

|

|

|

Foreign currency translation |

|

| 220,299 |

|

|

| 884 |

|

|

|

|

|

|

|

|

|

|

Total comprehensive loss for the period |

| $ | (26,336,012 | ) |

| $ | (3,572,224 | ) |

|

|

|

|

|

|

|

|

|

(Loss) for the period attributable to: |

|

|

|

|

|

|

|

|

Owners of the parent |

|

| (26,515,410 | ) |

|

| (3,573,108 | ) |

Non-controlling interest |

|

| (40,901 | ) |

|

| - |

|

|

| $ | (26,556,311 | ) |

| $ | (3,573,108 | ) |

Basic and diluted net loss per share |

| $ | (0.17 | ) |

| $ | (0.14 | ) |

|

|

|

|

|

|

|

|

|

Weighted average number of common shares outstanding - basic and diluted |

|

| 156,258,509 |

|

|

| 24,995,371 |

|

| 6 |

| Table of Contents |

Exchange Rates

Our consolidated financial information is presented in Canadian dollars. However, the functional currency of Code Red Ltd. (“Code Red”) is the U.K. pound sterling (“GBP”) and GameSquare Esports (USA) Inc. and its subsidiaries is the U.S. dollar (“USD”). Transactions in foreign currencies, including GBP and USD, are translated into the transacting entities’ functional currency at the exchange rates at the dates of the transactions. Monetary assets and liabilities denominated in foreign currencies are retranslated at the rate of exchange ruling at the statement of financial position dates. Non-monetary items in a foreign currency are measured in terms of historical cost and are translated using the exchange rates on the dates of the initial transactions. All differences are taken to the statements of income in the periods in which they arise.

The assets and liabilities of foreign operations are translated at the exchange rates at the reporting date to the presentation currency. The income and expenses of foreign operations are translated at the exchange rates at the dates of the transactions. Foreign currency differences are recognized in other comprehensive income (loss) and accumulated in the translation reserve.

A. (Reserved)

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

An investment in our securities involves a high degree of risk and the securities must be considered highly speculative. You should consider carefully all of the risks described below, together with the other information contained in this Form 20-F, before making a decision to invest in our securities. If any of the following events occur, our business, financial condition and operating results may be materially adversely affected. In that event, the trading price of our securities could decline, and you could lose all or part of your investment.

The risk factors outlined below are not a definitive list of all risk factors associated with an investment in the securities described hereunder. Additional risks and uncertainties not presently known to us, or which we currently deem not to be material, may also have a material adverse effect. Prospective investors and shareholders should consider carefully all of the information set out in this Form 20-F and the risks attaching to an investment in us before making any investment decision and consult with their own professional advisors where necessary.

Risks Related to Our Business

GameSquare has limited operating history and operates in an evolving sector.

GameSquare Inc. was acquired by oil and gas exploration company Magnolia Colombia Ltd. (“Magnolia”) pursuant to a reverse-takeover transaction (“RTO”), which was completed on October 2, 2020. On September 30, 2020, Magnolia changed its name to GameSquare Esports Inc.

GameSquare had no experience in the esports industry prior to the RTO. GameSquare acquired its first revenue-generating asset, Code Red, on October 2, 2020. Prior to the acquisition of Code Red, GameSquare’s operations were limited to identifying and acquiring target companies in the esports industry.

| 7 |

| Table of Contents |

Consequently, we are subject to all the risks and uncertainties inherent in a new business and in connection with the development and sale of new services. In addition, the esports and gaming industry is a relatively new and an evolving sector. Accordingly, investors should consider our prospects in light of the costs, uncertainties, delays, and difficulties frequently encountered by companies in this early stage of development and operating in a changing and evolving sector. Investors should carefully consider the risks and uncertainties that a company, such as GameSquare, with a limited operating history will face. In particular, investors should consider that we cannot provide assurance that we will be able to:

a. successfully implement or execute our current business plan;

b. maintain our management team;

c. raise sufficient funds in the capital markets to effectuate our business plan;

d. attract, enter into or maintain contracts with, and retain clients; and/or

e. compete effectively in the extremely competitive environment in which we operate.

If we cannot successfully accomplish any of the foregoing objectives, our business may not succeed.

GameSquare generates a significant portion of revenue from representing esports players, influencers, gaming personalities and other on-screen talent through our agency operating segment. Failure to attract new clients or to successfully represent our existing clients, may adversely affect revenue.

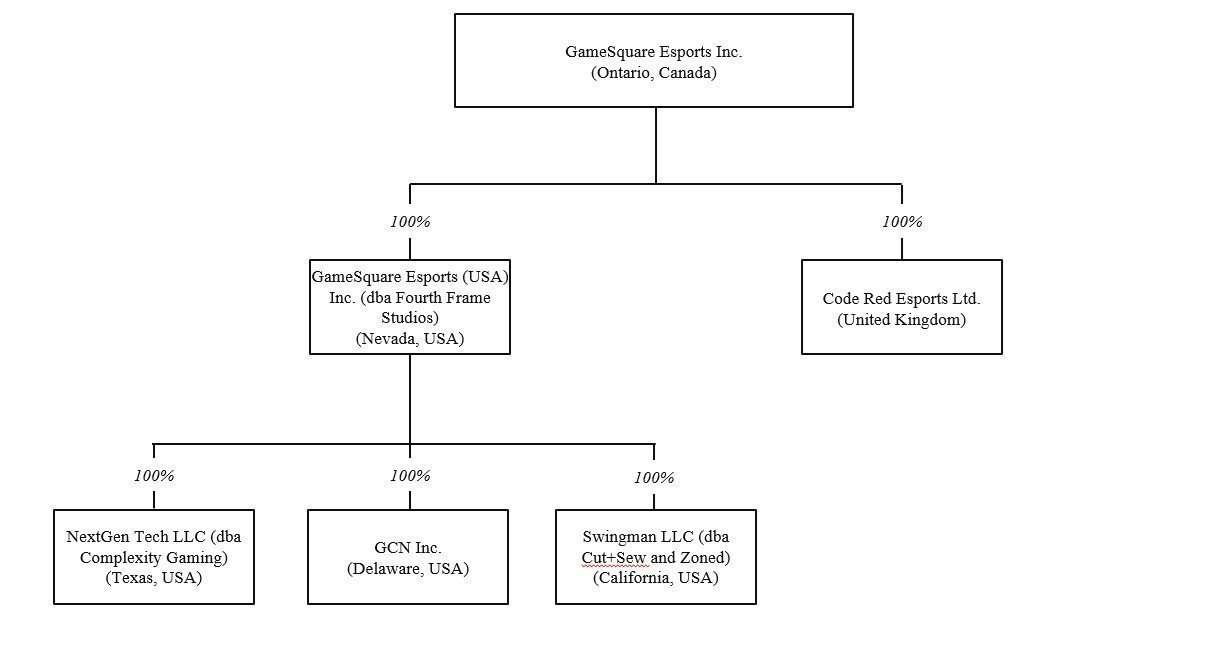

Our Agency Services segment represents esports agencies which include Code Red, the Gaming Community Network (“GCN”) and Swingman LLC (dba Cut+Sew and Zoned) (“Cut+Sew/Zoned”). Our agencies generate revenue through representing players, influencers and on-screen talent, consulting and managing and brokering brand activations for influencers. Our agency services sector generates the majority of our revenue.

The agency segment of the esports industry is highly competitive and there is no guarantee that we will succeed in attracting new clients to represent or that we will retain our existing clients. Factors that influence our success in attracting and retaining clients include our ability to:

f. successfully negotiate contracts on behalf of our clients;

g. secure sponsorships for our clients; and

h. secure event and tournament participation for our clients.

Failure to attract or retain clients would have a material, adverse effect on our business, financial condition and results of operations.

GameSquare’s agency services business model may not remain effective and it cannot guarantee that its future monetization strategies will be successfully implemented or generate sustainable revenues and profit.

Our agencies business generates a portion of its revenue from securing talent for live esports events. Although we anticipate that the audience for such live esports will continue to grow, creating more opportunities for us to provide services, such growth is not guaranteed and demand for GameSquare’s services may change, decrease substantially or dissipate, or we may fail to anticipate and serve client demands effectively. For example, COVID-19 and related variants have reduced demand for in-person esports events while increasing demand for online and broadcasted events. Although we also provide a variety of services relating to online and broadcasted events, any decision to reduce or eliminate its service offering for live esports events in order to prioritize online and broadcasted events may be unsuccessful and would involve additional risks and costs that could materially and adversely affect our business, financial condition and results of operations.

If GameSquare fails to maintain and enhance its brands, its business, financial condition and results of operations may be materially and adversely affected.

We believe that maintaining and enhancing our brands, including GameSquare, NextGen Tech LLC (dba Complexity Gaming) (“Complexity”), Swingman LLC (dba Cut+Sew and Zoned) and Code Red, as well as any other brands that we may acquire in the future, is important for our business to succeed by increasing our visibility and reputation in the esports industry and enabling GameSquare to attract new clients and retain existing clients for our businesses. Since GameSquare operates in a highly competitive industry, brand maintenance and enhancement directly affect our ability to maintain and enhance our market position. As GameSquare expands, we may conduct various marketing and brand promotion activities using various methods to continue promoting our brands, but we cannot assure investors that these activities will be successful. In addition, negative publicity, regardless of its veracity, could harm our brands and reputation, which may materially and adversely affect our business, financial condition and results of operations.

| 8 |

| Table of Contents |

GameSquare’s teams business is substantially dependent on the continued popularity and success of our teams and players.

The financial results of our teams segment are largely depended on our esports teams remaining popular with our fan bases. The popularity of our teams will, in part, depend on their performance in the leagues and tournaments in which they participate. We cannot ensure that our teams will be successful in the leagues and tournaments in which they play and therefore our ability to attract or retain talented players and coaching staff, supporters, sponsors and other commercial partners, as well as potentially result in lower prize money. Moreover, the popularity of the individual players can impact online viewership and television ratings, which could affect the long-term value of the media rights and sponsorship opportunities. There can be no assurance that our players will develop or maintain continued popularity. Furthermore, the popularity of the teams, and, in turn, their financial results, further depend, in part, upon the popularity of the esports played and their ability to attract audiences and generate online viewership. There can be no guarantee that games currently popular, will develop or maintain continued popularity in esports.

Defection of GameSquare’s players to other teams could hinder our success.

GameSquare competes with other esports teams to sign and retain world class esports players, some of which have greater resources or brand recognition and popularity than GameSquare. GameSquare’s players under contract may choose to move to other esports organizations for various reasons, including higher pay or that they have chosen to pursue new or other opportunities. The loss of any of our players could have negative consequences on our business and results of operations.

Adverse publicity concerning GameSquare, one of our businesses or key personnel or talent could negatively affect our business.

GameSquare’s reputation is essential to our continued success, and any decrease in the quality of our reputation could impair our ability to, among other things, recruit and retain key personnel, retain or attract clients and maintain relationships with our partners. GameSquare’s reputation can be negatively impacted by a number of factors, including negative publicity concerning GameSquare, members of our management or other key personnel including our talent and players. In addition, GameSquare is dependent for a portion of our revenues on our key talent and our ability to monetize through various channels. Such publicity could have a negative impact on GameSquare and adversely affect our business, financial condition and results of operations.

If GameSquare fails to anticipate, adopt and build expertise in new esports technologies, our business may suffer.

Rapid technology changes in the esports gaming market requires us to anticipate which technologies we should adopt and build expertise in to remain competitive in the esports industry. GameSquare has invested, and in the future may invest, in new business strategies, technologies or services to engage a growing number of esports players, influencers and other on-screen talent, sponsors and others. For example, Code Red assists game publishers and developers such as Ubisoft and Massive Entertainment in designing broadcast-ready games by honing in-game spectator modes for improved viewing and commentating. Such advice typically relates to overlay placement, broadcasting options for streamers and commentators and scoreboard, replay and timer displays, as well as a number of other design elements. If we fail to anticipate, adopt or build expertise in new technologies which impact in-game spectator modes, GameSquare may fail to attract new or retain existing game publishers, developers, influencers and brands as clients.

Adopting new technologies involves significant risks and uncertainties, and no assurance can be given that GameSquare will successfully identify which technologies will complement our business. If we do not successfully implement new technologies, our reputation may be materially adversely affected and our business, financial condition and operating results may be impacted.

The success of GameSquare’s business depends on our marketing efforts.

Achieving market success will require substantial marketing efforts and investments to inform potential clients of the distinctive benefits and characteristics of our products and services. GameSquare’s long-term success will depend on our ability to expand current marketing capabilities. We will, among other things, need to attract and retain experienced marketing and sales personnel. No assurance can be given that we will be able to attract and retain such personnel or that any efforts undertaken by such personnel will be successful.

| 9 |

| Table of Contents |

Acquisitions may never materialize, may be subject to unexpected delays or may entail unexpected costs or prove unsuccessful.

As a growing company, we are engaged in identifying, acquiring and developing esports and gaming assets that we believe are a strategic fit for our business. However, we cannot predict what form future acquisitions might take or when such acquisitions will be consummated, if at all. GameSquare is likely to face significant competition in seeking appropriate acquisitions and these acquisitions can be complicated and time consuming to negotiate and document. We may not be able to negotiate acquisitions on acceptable terms, or at all, and we are unable to predict when, if ever, we will consummate such acquisitions due to the numerous risks and uncertainties associated with them.

Since GameSquare may not be able to accurately predict these difficulties and expenditures, these costs may outweigh the value we realize from a future acquisition. Future acquisitions could result in issuances of securities that would dilute shareholders’ ownership interest, the incurrence of debt, contingent liabilities, amortization of expenses related to other intangible assets, and the incurrence of large, immediate write-offs.

Any of the forgoing could materially and adversely affect our business, financial condition and results of operations.

Difficulties integrating acquisitions.

GameSquare has acquired a number of businesses since the RTO and acquisitions continue to be part of our growth strategy. The benefits of an acquisition may take considerable time to develop, and we cannot be certain that any particular acquisition will produce the intended benefits. These risks and difficulties associated with acquisitions, if they materialize, could disrupt our ongoing business, distract management, result in the loss of key personnel, increase expenses and otherwise have a material adverse effect on our business, results of operations and financial performance.

GameSquare may be unable to achieve or sustain profitability or continue as a going concern.

There is no assurance that GameSquare will earn profits in the future, or that profitability will be sustained in the near future or at all. Beyond this, we may incur significant losses in the future for a number of reasons including other risks described in this document, and we may encounter unforeseen expenses, difficulties, complications, delays and other unknown events. There is also no assurance that future revenues will be sufficient to generate the funds required to continue our business development and our activities. If we do not have sufficient capital to fund our operations, we may be required to reduce our sales and marketing efforts or forego certain business opportunities and strategies.

Our consolidated financial statements have been prepared on the assumption that we will continue as a going concern. Our continuation as a going concern is dependent upon our ability to raise equity capital or borrowings sufficient to meet current and future obligations and ultimately achieve profitable operations. There is no assurance that we will be able to obtain such financings or obtain them on favourable terms. These matters represent material uncertainties that cast significant doubt on our ability to continue as a going concern.

GameSquare will require additional financing and cannot be certain that such additional financing will be available on reasonable terms when required, or at all.

To date, we have relied primarily on equity financing to carry on our business. We have limited financial resources and operating cash flow and can make no assurance that sufficient funding will be available to us to fund our operating expenses and to further develop our business. As of December 31, 2021, GameSquare had cash of $7,642,593. Additionally, on April 5, 2022, GameSquare announced a fully subscribed US$3 million non-brokered private placement. As at that date of this Form 20-F, the private placement had not closed. We also entered into US$5 million credit facility which will provide the Company with access to capital, if required, to execute on its strategic priorities. The credit agreement will become available for draw down after satisfaction of certain conditions precedent.

GameSquare does not have any contracts or commitments for additional financing other than a US$5 million revolving credit facility. $Nil has been drawn on that facility as of the date of this Form 20-F. Any additional equity financing may involve substantial dilution to then existing shareholders. There can be no assurance that such additional capital will be available, on a timely basis or on acceptable terms. Failure to obtain such additional financing could result in delay or indefinite postponement of operations or the further development of our business with the possible loss of such properties or assets. If adequate funds are not available or are not available on acceptable terms, we may not be able to fund our business or the expansion thereof, take advantage of strategic acquisitions or investment opportunities or respond to competitive pressures. Such inability to obtain additional financing when needed could have a material adverse effect on our business, financial condition and results of operations.

| 10 |

| Table of Contents |

Future cash flow fluctuations may affect GameSquare’s ability to fund our working capital requirements or achieve our business objectives in a timely manner.

The working capital requirements and cash flows are expected to be subject to quarterly and yearly fluctuations, depending on such factors as timing and size of capital expenditures, acquisitions, levels of sales and collection of receivables and client payment terms and conditions. If our revenues and cash flows are materially lower than we currently expect, we may be required to reduce our capital expenditures and investments or take other measures in order to meet our cash requirements. GameSquare may also seek additional funds from liquidity-generating transactions and other conventional sources of external financing (which may include a variety of debt, convertible debt and/or equity financings). We cannot provide any assurance that the net cash requirements will be as we currently expect. Our inability to manage cash flow fluctuations resulting from the above factors could have a material adverse effect on our ability to fund the working capital requirements from operating cash flows and other sources of liquidity or to achieve our business objectives in a timely manner.

International operations and expansion exposes GameSquare to risks associated with international markets.

GameSquare currently operates and has businesses predominantly in U.K., EU and U.S. markets and may further expand internationally and operate in select foreign markets. Managing a global organization is more time consuming and expensive than managing a company operating in one jurisdiction. Conducting international operations subjects GameSquare to risks related to foreign regulatory requirements and complying with a wide variety of laws and legal standards, managing and staffing international operations, fluctuations in foreign exchange rates, managing tax consequences, accounting and reporting complexities and political, social and economic instability in various jurisdictions. The investment and additional resources required to establish and manage operations in various countries and jurisdictions may result in lower levels of revenue or profitability.

The requirements related to being a public company.

As a reporting issuer, GameSquare is subject to and must comply with applicable securities legislation, the listing requirements and rules of the exchange and other applicable securities rules and regulations. Compliance with these rules and regulations may increase our legal and financial compliance costs, make some activities more difficult, time consuming or costly and increase demand on our systems and resources. Applicable securities laws require GameSquare to, among other things, file certain annual and quarterly reports with respect to our business and results of operations. In addition, applicable securities laws require GameSquare to, among other things, maintain effective disclosure controls and procedures and internal control over financial reporting. In order to maintain and, if required, improve our disclosure controls and procedures and internal control over financial reporting to meet this standard, significant resources and management oversight may be required including due to complexity of transactions and our expanding international business. As a result, management’s attention may be diverted from other business concerns in order to comply with these requirements. To comply with these requirements, GameSquare may need to hire more employees in the future or engage outside consultants, which will increase our costs and expenses.

In addition, changing laws, regulations and standards relating to corporate governance and public disclosure are creating increasing legal and financial compliance costs and making some activities more time consuming. We intend to continue to invest resources to comply with evolving laws, regulations and standards, and this investment may result in increased general and administrative expenses and a diversion of management’s time and attention from revenue generating activities to compliance activities.

GameSquare is subject to privacy laws in each jurisdiction in which we operate and we may face risks related to breaches of the applicable privacy laws.

GameSquare collects and stores personal information about our users, clients and partners and is responsible for protecting that information from privacy breaches. A privacy breach may occur through procedural or process failure, information technology malfunction or deliberate unauthorized intrusions. Theft of data for competitive purposes, particularly user and partner lists, is an ongoing risk whether perpetrated via employee collusion or negligence or through deliberate cyber-attack. Any such theft or privacy breach could have a material adverse effect on our business, financial condition or results of operations.

In addition, there are a number of Canadian federal and provincial laws as well as local rules which are applicable to GameSquare and our subsidiaries which protect the confidentiality of personal information and restrict the use and disclosure of that protected information. The Canadian privacy rules under the Personal Information Protection and Electronics Documents Act (Canada) (“PIPEDA”) protect personal information by limiting its use and disclosure of personal information. If we are found to be in violation of the privacy or security rules under PIPEDA or other laws protecting the confidentiality of personal information, we could be subject to sanctions and civil or criminal penalties, which could increase our liability, harm our reputation and have a material adverse effect on our business, financial condition or results of operations.

| 11 |

| Table of Contents |

GameSquare is exposed to cyber security incidents resulting from deliberate attacks or unintentional events.

Cyber security incidents can result from deliberate attacks or unintentional events, and may arise from internal sources (e.g., employees, contractors, service providers, suppliers and operational risks) or external sources (e.g., nation states, terrorists, hacktivists, competitors and acts of nature). Cyber incidents include, but are not limited to, unauthorized access to information systems and data (e.g., through hacking or malicious software) for purposes of misappropriating or corrupting data or causing operational disruption. Cyber incidents also may be caused in a manner that does not require unauthorized access, such as causing denial-of-service attacks on websites (e.g., efforts to make network services unavailable to intended users).

A cyber incident that affects our business or our service providers might cause disruptions and adversely affect their respective business operations and might also result in violations of applicable law (e.g., personal information protection laws), each of which might result in potentially significant financial losses and liabilities, regulatory fines and penalties, reputational harm and reimbursement and other compensation costs. In addition, substantial costs might be incurred to investigate, remediate and prevent cyber incidents.

GameSquare uses third-party services and partnerships in connection with our business, and any disruption to these services or partnerships could result in a disruption to our business, negative publicity and a slowdown in the growth of our clients, materially and adversely affecting our business, financial condition and results of operations.

GameSquare depends upon third-party software and services to conduct our business. The inability to access these services could result in a disruption while sourcing replacement service vendors. Additionally, we rely on contracted third-party partnerships to conduct our business. While we have minimized our reliance on any single vendor or partner, any disruption of service from our partners could have a material adverse effect on our business, financial condition or results of operations.

Failure to attract, retain and motivate key employees may adversely affect GameSquare’s ability to compete and the loss of the services of key personnel could have a material adverse effect on our business.

GameSquare depends on the services of a few key executive officers. The loss of any of these key persons could have a material adverse effect on our business, financial condition and results of operations. Our success is also highly dependent on our continuing ability to identify, hire, train, motivate and retain highly qualified technical, marketing and management personnel. Competition for such personnel can be intense, and we cannot provide assurance that we will be able to attract or retain highly qualified technical, marketing and management personnel in the future. Stock options and other share-based compensation plans may comprise a significant component of key employee compensation, and if the price of the Common Shares declines, it may be difficult to retain such individuals. Similarly, changes in the share price may hinder our ability to recruit key employees, as they may elect to seek employment with other companies that they believe have better long-term prospects. Our inability to attract and retain the necessary technical, marketing and management personnel may adversely affect our future growth and profitability. Our retention and recruiting may require significant increases in compensation expense, which would adversely affect our results of operation.

Our executive officers and other members of senior management have substantial experience and expertise in the business and have made significant contributions to our growth and success. The unexpected loss of services of one or more of these individuals could also adversely affect the business, financial condition and results of operations. GameSquare is not protected by key man or similar life insurance covering members of senior management.

Litigation costs and the outcome of litigation could have a material adverse effect on our business.

From time to time, GameSquare may be subject to litigation claims through the ordinary course of our business operations regarding, but not limited to, employment matters, security of client and employee personal information, contractual relations with clients, including gamers, influencers and other on-screen talent, production crew and sponsors, among others and marketing and infringement of trademarks. Litigation to defend against claims by third parties, or to enforce any rights that we may have against third parties, may be necessary, which could result in substantial costs and diversion of our resources, causing a material adverse effect on our business, financial condition and results of operations.

We are not aware of any current material legal proceedings outstanding, threatened or pending as of the date hereof by or against GameSquare. However, given the nature of our business, we are, and may from time to time in the future be, party to various, and at times numerous, legal investigations, proceedings and claims that arise in the ordinary course of business. Because the outcome of litigation is inherently uncertain, if one or more of such legal matters were to be resolved against us for amounts in excess of our expectations, our business, financial condition and results of operations could be materially adversely affected.

| 12 |

| Table of Contents |

GameSquare is exposed to foreign currency risk and we have not hedged against risk associated with foreign exchange rate exposure.

Although GameSquare’s functional currency is the Canadian dollar, it generates revenue and incurs costs in foreign currencies. In particular, we expect to generate revenue and incur costs in GBP, the functional currency of Code Red, and euro, as well as, U.S. dollars, the functional currency of our other subsidiaries. Accordingly, GameSquare is subject to risk from fluctuations in the rates of currency exchange between such foreign currency and the Canadian dollar, and such fluctuations may materially adversely affect our business, financial condition and results of operations. GameSquare does not currently hedge against such currency fluctuations.

Public health crises may adversely affect our growth.

GameSquare may be negatively impacted by volatility in the equity markets as a result of certain events that are beyond our control, including infectious diseases, pandemics or similar health threats, such as the COVID-19 outbreak and its variants. Many governments, including in the United States, the United Kingdom and Canada, imposed stringent restrictions to seek to mitigate, or slow, the spread of COVID-19 and its variants, including restrictions on international and local travel, public gatherings and participation in business meetings, as well as closures of workplaces, schools, and other public sites, and are continuing to encourage “social distancing.” While many of these measures are being eased, the duration of such measures is highly uncertain, but could be prolonged, and stricter measures may still be put in place or reintroduced in areas where such measures have very recently started to be gradually eased.

As a result of the COVID-19 related restrictions, in-person esports tournaments and other events have been cancelled or required to enforce social distancing and other policies designed to reduce the spread of the virus. The resulting loss of revenue from ticket sales has not been fully offset by a corresponding increase in paid online or televised esports events. There can be no guarantee that demand for in-person esports events will resume in the near future. Any continuation of COVID-19 related or other restrictions could have a material adverse effect on our business, financial condition and operating results may be impacted.

Risks Related to the Industry

GameSquare’s business and success is dependent on the continuing popularity and growth of the esports industry.

Our business is substantially dependent on the continuing popularity of the esports industry which is in the early stages of its development. Although the esports industry has experienced rapid growth and we anticipate the industry to continue to grow, consumer preferences may shift and there is no assurance that this growth will continue in the future. We have taken steps to diversify our business and continues to seek out new opportunities in the esports industry but there is no guarantee that it will be successful in doing so. Given the dynamic evolution of this industry, it can be difficult to plan strategically, and it is possible that competitors will be more successful than we are at adapting to change and pursuing business opportunities.

The esports and gaming industry is intensely competitive. GameSquare faces competition from a growing number of companies and, if we are unable to compete effectively, our business could be negatively impacted.

The esports and gaming industry is in competition with other sporting and entertainment events, both live and delivered over television networks, radio, the Internet, mobile applications and other sources. As a result of the large number of options available and the global nature of the esports industry, we face strong competition for esports fans. There is also intense competition amongst businesses operating in the segments of the esports industry where we currently operate or may operate in the future, including esports agencies, influencer technology platforms, analytics technologies, content creation and media content assets.

As some of GameSquare’s competitors have greater financial resources, they may spend more money and time on developing their products or services, undertake more extensive marketing campaigns, adopt more aggressive pricing policies or otherwise develop more commercially successful products or services, which could impact our ability to secure new clients or retain existing clients. Competition may also lead to reduced margins as companies compete for clients by adopting aggressive pricing policies or our costs of doing business may increase in a competitive environment. Furthermore, new competitors may enter the segments of the esports industry where we currently operate or may operate in the future. If GameSquare is unable to obtain significant market presence or if we lose market share to our competitors, our business, financial condition and results of operations could be materially adversely affected. Finally, there are many companies with established relationships with third parties, including sponsors, event and tournament organizers, influencers and esports organizations. Consequently, some competitors may be able to develop and expand their esports organization more quickly. Our success depends on our ability to develop and maintain relationships with such third parties.

| 13 |

| Table of Contents |

As a result, GameSquare may not be able to continue to effectively compete against current and future competitors which could materially and adversely affect our business, financial condition and results of operations.

Esports is a new and evolving industry, which presents significant uncertainty and business risks.

The esports industry is relatively new and continues to evolve. GameSquare has taken steps to diversify our business and continues to seek out new opportunities in the esports industry, including in the teams segment through the acquisition of Complexity, but most of our revenue continues to be generated from our agency business. However, whether this industry grows and whether our business will ultimately succeed will be affected by, among other things, the success of efforts to monetize the esports industry through tournament fees, live event ticket sales, advertising and sponsorships, spectator demand for in-person, online and televised esports events and tournaments, the success of industry marketing efforts, including on social media platforms, the development of new games and technologies to attract and retain gamers and spectators, data privacy laws and regulation and other factors that we are unable to predict and which are beyond our control. Given the dynamic evolution of this industry, it can be difficult to plan strategically, and it is possible that competitors will be more successful than GameSquare at adapting to change and pursuing business opportunities.

Reliance on advertisers for revenue.

The esports industry relies on advertisers as part of its revenue. Our inability to secure contracts for advertising revenues may have a material adverse effect on our business, financial condition and results of operations. Additionally, this is a relatively new and rapidly evolving industry and as such, it is difficult to predict the prospects of growth. There is no assurance that advertisers will continue to increase their purchases of online advertising or that the supply of advertising inventory on digital media properties will not exceed the demand. If the industry grows slower than anticipated or we fail to maintain and grow our market position, we may not be able to achieve our revenue projections.

Our business is vulnerable to changing economic conditions and to other factors that adversely affect the industries in which we operate.

The demand for entertainment and leisure activities, including esports and gaming, tends to be highly sensitive to changes in consumers’ free time and disposable income, and thus can be affected by changes in the economy and consumer tastes, both of which are difficult to predict and beyond our control. Unfavorable changes in general economic conditions, including recessions, economic slowdown, inflation, sustained high levels of unemployment, and increasing fuel or transportation costs, may reduce customers’ disposable income or result in fewer individuals attending ticketed in-person or online esports events or tournaments, paying for subscriptions to esports media channels or otherwise engaging in entertainment and leisure activities. As a result, we cannot ensure that demand for our services will remain constant. Continued or renewed adverse developments affecting economies throughout the world, including a general tightening of availability of credit, inflation, increasing interest rates, increasing energy costs, acts of war or armed conflicts (including the conflict in Ukraine), terrorism, transportation disruptions, natural disasters, pandemics, declining consumer confidence, sustained high levels of unemployment or significant declines in stock markets, could lead to a further reduction in discretionary spending on leisure activities, such as esports. Any significant or prolonged decrease in consumer spending on entertainment or leisure activities could reduce demand for our services, which would have a material adverse effect on our business, financial condition and results of operations.

Risk Factors Related to the Common Shares

Future sales or the issuances of our securities may cause the market price of the Common Shares to decline.

The market price of the Common Shares could decline as a result of issuances of securities (including additional Common Shares) by the Company, exercises of outstanding options or warrants for additional Common Shares or sales by existing shareholders of Common Shares in the market, or the perception that these issuances or sales could occur. Sales of Common Shares by shareholders may make it more difficult for GameSquare to sell equity securities at a time and price that we deem appropriate. Sales or issuances of substantial numbers of Common Shares, including in the context of future acquisitions, or the perception that such sales or issuances could occur, may adversely affect prevailing market prices of the Common Shares. With any such sale or issuance of Common Shares, investors may suffer dilution and GameSquare may experience dilution in our earnings per share.

| 14 |

| Table of Contents |

GameSquare expects that the price of the Common Shares may fluctuate significantly.

The market price of securities of many companies, particularly development and early commercial stage esports companies, experiences wide fluctuations in price that are not necessarily related to the operating performance, underlying asset values or prospects of such companies.

The market price of the Common Shares could be subject to wide fluctuations in response to many risk factors set out herein, and others beyond our control. These and other market and industry factors may cause the market price and demand for the Common Shares to fluctuate substantially, regardless of the actual operating performance of GameSquare, which may limit or prevent investors from readily selling their Common Shares and may otherwise negatively affect the liquidity of the Common Shares. In addition, stock markets in general, and the share prices of esports and early-growth companies in particular, have experienced price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of such companies.

Significant ownership by principal shareholders.

As of the date of this Form 20-F, two shareholders hold approximately 40% of the Common Shares. As a result, these shareholders have significant influence over all corporate actions and securities matters requiring shareholder approval, including election of our directors and significant corporate transactions. The concentrated voting control of the Common Shares will limit the ability of other shareholders to influence corporate matters and actions may be approved that certain shareholders may not view as beneficial. Additionally, the principal shareholders’ interest in GameSquare may discourage transactions involving a change of control, including transactions in which shareholders might otherwise receive a premium for their shares over the then current market price.

If equity research analysts do not publish research or reports about GameSquare and our business or if they issue unfavorable commentary or downgrade the Common Shares, the price of the Common Shares could decline.

The trading market for the Common Shares will rely in part on the research and reports that equity research analysts publish about GameSquare and our business. The price of the Common Shares could decline if one or more equity analysts downgrade the Common Shares or if analysts issue other unfavorable commentary or cease publishing reports about GameSquare or our business.

GameSquare may be subject to securities litigation, which is expensive and could divert management attention.

The market price of the Common Shares may be volatile, and in the past companies that have experienced volatility in the market price of their shares have been subject to securities class action litigation. GameSquare may be the target of this type of litigation in the future. Litigation of this type could result in substantial costs and diversion of management’s attention and resources, which could adversely impact its business. Any adverse determination in litigation could also subject GameSquare to significant liabilities.

| 15 |

| Table of Contents |

Variable revenues and earnings.

The revenues and earnings of GameSquare may fluctuate from quarter to quarter, which could affect the market price of the Common Shares. Revenues and earnings may vary quarter to quarter as a result of a number of factors, including acquisition of new customers and clients, cyclical fluctuations related to the evolution of the industry and impairment of goodwill or intangible assets which may result in a significant change to earnings in the period in which impairment is determined. Any of the risk factors listed in this Form 20-F could also cause significant variations to our revenues, gross margins and earnings in any given quarter.

GameSquare has never paid dividends on the Common Shares and it does not anticipate paying any dividends in the foreseeable future. Consequently, any gains from an investment in the Common Shares will likely depend on whether the price of the Common Shares increases.

GameSquare has not paid dividends on the Common Shares to date and we currently intend to retain our future earnings, if any, to fund the development and growth of our business. As a result, capital appreciation, if any, of the Common Shares will be investors sole source of gain for the foreseeable future. Consequently, in the foreseeable future, investors will likely only experience a gain from their investment in the Common Shares if the price of the Common Shares increases.

GameSquare may lose foreign private issuer status in the future, which could result in significant additional costs and expenses.

GameSquare may in the future lose foreign private issuer status if a majority of the Common Shares are held in the United States and GameSquare fails to meet the additional requirements necessary to avoid loss of foreign private issuer status, such as if: (i) a majority of our directors or executive officers are U.S. citizens or residents; (ii) a majority of our assets are located in the United States; or (iii) our business is administered principally in the United States. The regulatory and compliance costs to the Company under U.S. securities laws as a U.S. domestic issuer will be significantly more than the costs incurred as an SEC foreign private issuer. If GameSquare is not a foreign private issuer, we would be required to file periodic and current reports and registration statements on U.S. domestic issuer forms with the SEC, which are generally more detailed and extensive than the forms available to a foreign private issuer. In addition, GameSquare may lose the ability to rely upon exemptions from corporate governance requirements that are available to foreign private issuers.

| 16 |

| Table of Contents |

ITEM 4. INFORMATION ON THE COMPANY

A. History and Development of the Company History of GameSquare Inc.

GameSquare Inc. was incorporated under the laws of the province of Ontario, Canada on December 13, 2018 for the purposes of identifying, acquiring and developing esports-focused companies in the areas of agency, influencer technology platforms, analytics technologies, content creation and media content assets. On May 27, 2019, GameSquare Inc. changed its name to Octane Play Inc. On September 18, 2019, GameSquare Inc. changed its name back to GameSquare Inc.

On November 7, 2019, GameSquare Inc. and Code Red entered into a share purchase agreement pursuant to which GameSquare Inc. would acquire all outstanding common shares of Code Red (as amended on January 24, 2020 and February 18, 2020, the “Share Purchase Agreement”).

On February 10, 2020, Magnolia signed a letter of intent pursuant to which Magnolia would acquire all of the issued and outstanding shares in the capital of GameSquare Inc. by way of a reverse-takeover transaction. The RTO was structured as a three-cornered amalgamation, pursuant to which 2631443 Ontario Inc. (“Magnolia Subco”), a wholly-owned subsidiary of Magnolia, and GameSquare Inc. amalgamated (the “Amalgamation”) to form a new company, GameSquare (Ontario) Inc. (“Amalco”). Prior to the completion of the Amalgamation, the existing common shares in the capital of Magnolia were consolidated and GameSquare Inc.’s shareholders received one common share of Magnolia for each common share of GameSquare Inc. As a result, Amalco became a wholly-owned subsidiary of Magnolia.

Magnolia was previously involved in oil and gas exploration activities in Canada, the U.S. and Colombia. Magnolia ceased all direct oil and gas exploration activities in 2014.

Magnolia completed the RTO on October 2, 2020. Effective September 30, 2020, Magnolia delisted its common shares from the TSX Venture Exchange and, effective October 8, 2020, listed them on the Canadian Securities Exchange. On September 30, 2020 Magnolia changed its name to GameSquare Esports Inc..On December 1, 2020, Amalco and GameSquare amalgamated to become GameSquare Esports Inc.

Pursuant to the Share Purchase Agreement, Amalco acquired all outstanding common shares of Code Red on October 2, 2020.

On December 31, 2020, GameSquare and Reciprocity, a gaming and esports company, entered into an arrangement agreement pursuant to which GameSquare would acquire all outstanding common shares in Reciprocity (the “Reciprocity Acquisition”). The Reciprocity Acquisition closed on March 16, 2021. The Reciprocity Acquisition constituted a ‘significant acquisition’ for the Company and the Company filed a business acquisition report with respect to the acquisition in accordance with Form 51-102F4.

On January 22, 2021, the Company announced the appointment of Justin Kenna as its Chief Executive Officer.

On June 30, 2021, the Company completed the acquisition of all of the issued and outstanding membership interests (the “Interests”) in the capital of Nextgen Tech LLC (dba Complexity Gaming) pursuant to a purchase agreement (the “Purchase Agreement”) among the Company, Blue & Silver Ventures Ltd., Goff NextGen Holdings LLC and Jason Lake.

Complexity is a leading esports organization, which fields world-class esports teams in CS:GO, Fortnite, Valorant, APEX Legends, Hearthstone, Madden Football and FIFA Soccer and has participated and hosted numerous major esports events with combined annual viewer minutes of 3.2 billion. Complexity has also attracted blue-chip sponsors, including Miller Lite, Dairy MAX, ARterra Labs and Herman Miller and is one of only four esports organizations to have an exclusive partnership with Twitch.

As consideration for the acquisition of the Interests, the Company issued 83,328,750 Common Shares pursuant to the terms of the Purchase Agreement. The Common Shares issued in consideration for the Interests were subject to a standard statutory four-month hold period, which expired on October 31, 2021. In addition, the parties entered into a voluntary lock-up agreement with the Company pursuant to which, among other things, the Common Shares received by the vendors as consideration are subject to restrictions on sale for a period of 180 days following the date of the acquisition.

| 17 |

| Table of Contents |

On July 27, 2021, the Company closed its acquisition of 100% of the issued and outstanding membership units of Swingman LLC (dba Cut+Sew and Zoned), a privately held marketing agency based in Los Angeles, California operating in the sports and esports industries (the “Cut+Sew/Zoned Transaction”). The Company issued two (2) million Common Shares and paid $3 million in cash on closing of the Cut+Sew/Zoned Transaction. Additionally, certain former members of Cut+Sew/Zoned are entitled to receive: (i) up to $1,250,000 in Common Shares (such shares to be issued at a deemed issue price of $0.50 per Common Share), up to $975,000 in Common Shares (such shares to be issued at the closing price of the Common Shares on July 27, 2022) and up to $150,000 in cash if Cut+Sew/Zoned generates up to US$1 million in EBITDA in the 12 months following closing of the Cut+Sew/Zoned Transaction; and (ii) up to $650,000 in Common Shares (such shares to be issued at a deemed issue price of $0.50 per Common Share), up to $1,560,000 in Common Shares (such shares to be issued at the closing price of the Common Shares on July 27, 2022) and up to $240,000 in cash if Cut+Sew/Zoned generates up to US$1.5 million in EBITDA in the period from 12 to 24 months following the closing. The Common Shares issued pursuant to the Cut+Sew/Zoned Transaction are subject to a 6-month lock up period.

On July 30, 2021, GameSquare changed its fiscal year-end from November 30 to December 31.

On September 21, 2021, the Company announced the election of the Board including Tom Walker, Travis Goff, Craig Armitage, Paul LeBreux, Justin Kenna, and Kevin Wright. Neil Said resigned as a director of the Company at this time.

Effective November 1, 2021, as part of an internal reorganization, GameSquare Esports Inc. amalgamated with its wholly-owned subsidiary, Reciprocity Corp. The amalgamated company retained the name GameSquare Esports Inc.

On December 20, 2021, the Common Shares began trading on the OTCQB Venture Market in the United States under the symbol “GMSQF”.

Recent Developments

On January 6, 2022, the Company, announced that Justin Kenna, CEO of GameSquare, and Christina Grushkin, Head of Sales at Complexity Gaming, were named by Business Insider as top executives defining the future of advertising in video games and esports. The list includes executives from leading companies such as Anheuser-Busch, McDonald’s, Verizon, State Farm, Nike, and Honda as well as top agencies and esports organizations like Dentsu, Omnicom Media Group, and Evil Geniuses. The article, published by Business Insider, highlights the acquisitions that GameSquare has completed under Justin’s tenure as CEO and the positive impact that the business can have on satisfying advertisers’ needs around marketing, talent management, and organizing events. Business Insider also noted that Complexity provides sponsorship opportunities for brands and that its head of sales, Christina Grushkin, is key to these efforts.

On January 27, 2022, the Company announced that it had entered into a sponsorship agreement with ARterra Labs Co. (“ARterra”), an NFT (Non-Fungible Token) platform hyper-focused on the esports and gaming market. ARterra has been named the Official NFT Marketplace of Complexity Gaming and the Exclusive NFT Platform of Complexity Gaming. The sponsorship is meaningful to Complexity with additional opportunities to expand and grow the sponsorship as ARterra seeks to accelerate engagement within the esports and gaming community. Complexity and ARterra will collaborate on the official launch of the platform and together intend to build engagement strategies to ensure authenticity for the gaming and esports community through education and enhanced understanding of digital collectibles. ARterra has created a carbon neutral platform and marketplace and strives to create genuine utility for its fans and creators.

On February 23, 2022, the Company released a Letter to Shareholders, available on the Company’s website, which highlights the importance of identifying and launching new businesses that scale rapidly and the importance of building diversity to improve the Company’s ability to make great decisions and become a world class organization. Management believes that the launch of Fourth Frame Studios, with Mr. Okusanya at the helm, supports these initiatives.

On March 1, 2022, Oluwafemi “Femi” Okusanya joined the Company to lead the newly launched Fourth Frame Studios. Mr. Okusanya is a leading creative director with extensive experience growing content studios. He is the recipient of numerous Streamy Awards, including best branded content in 2021. His extensive resume of working with top tier companies includes global brands and household names within the automotive, sports apparel, footwear, luxury brands, and professional sports teams and leagues. Fourth Frame Studios is a first-of-its-kind content production and creative execution studio at the intersection of gaming and culture. The LA based studio will develop creative content solutions for brands to reach the next generation of consumers.

Additionally, on April 5, 2022, GameSquare announced a fully subscribed US$3 million non-brokered private placement. As of the date of this Form 20-F, the private placement had not closed.

| 18 |

| Table of Contents |

We also entered into US$5 million credit facility which will provide the Company with access to capital, if required, to execute on its strategic priorities. The credit agreement will become available for draw down after satisfaction of certain conditions precedent.

History of Magnolia Colombia Ltd.

Camflo Resources Ltd. (“Camflo”), a predecessor to Magnolia, was incorporated on March 21, 1997 under the Business Corporations Act (Alberta) (“ABCA”).

By articles of continuance dated May 24, 2001, Camflo was continued into Yukon Territory, and its name was changed to Camflo International Inc. by articles of amendment dated November 22, 2001. Camflo was continued back into Alberta by articles of continuance dated August 20, 2004 pursuant to the ABCA.

696406 Alberta Inc. (“Spearhead”), another predecessor to Magnolia, was incorporated on May 24, 1996 under the ABCA. By articles of amendment dated July 22, 1996, Spearhead changed its name to Spearhead Resources Inc.

Camflo amalgamated with Spearhead to become Arctos Petroleum Corp. (“Arctos”) on September 30, 2004 by way of articles of amalgamation under the ABCA. Thereafter, Arctos amalgamated with Stetson Oil & Gas Ltd. and changed its name to Stetson Oil & Gas Ltd. (“Stetson”) by way of articles of amalgamation dated November 9, 2007.

By articles of amalgamation pursuant to the ABCA dated June 1, 2009, Stetson amalgamated with 1470975 Alberta Ltd. to become Stetson. Stetson was then continued into Ontario pursuant to the provisions of the OBCA by articles of continuance dated August 21, 2014, and its name was changed to Magnolia Colombia Ltd. by articles of amendment dated June 14, 2017.