Table of Contents

As filed with the Securities and Exchange Commission on August 19, 2022

Registration No. 333-264220

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 4

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Crescent Energy Company

(Exact name of registrant as specified in its charter)

| Delaware | 1311 | 87-1133610 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification Number) |

600 Travis Street, Suite 7200

Houston, Texas 77002 (713) 337-4600

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bo Shi General Counsel

600 Travis Street, Suite 7200

Houston, Texas 77002

(713) 337-4600

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Douglas E. McWilliams 845 Texas Avenue, Suite 4700 Houston, Texas 77002 |

David Azarkh Brian E. Rosenzweig 425 Lexington Avenue New

York, New York 10017 |

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☒ | |||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

| Emerging growth company | ☐ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. The securities described herein may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities, in any state or jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED AUGUST 19, 2022

5,000,000 Shares

Crescent Energy Company

Class A Common Stock

We are offering shares of our Class A common stock, par value $0.0001 per share (“Class A Common Stock”), and the selling stockholder identified in this prospectus is offering shares of our Class A Common Stock. We will not receive any of the proceeds from the sale of the shares by the selling stockholder.

Our Class A Common Stock is listed on The New York Stock Exchange (“NYSE”) under the symbol “CRGY.” The last reported sales price of our Class A Common Stock on the NYSE on , 2022 was $ per share.

Investing in our Class A Common Stock involves risks. See “Risk Factors” on page 26.

| Per Share | Total | |||||||

| Price to Public |

$ | $ | ||||||

| Underwriting Discounts and Commissions(1) |

$ | $ | ||||||

| Proceeds to Crescent Energy Company, Before Expenses |

$ | $ | ||||||

| Proceeds to the Selling Stockholder, Before Expenses |

$ | $ | ||||||

| (1) | See “Underwriting (Conflicts of Interest)” for additional information regarding underwriting compensation. |

We have granted the underwriters the option to purchase up to additional shares of Class A Common Stock, and the selling stockholder has granted the underwriters the option to purchase up to additional shares of Class A Common Stock, in each case on the same terms and conditions set forth above within 30 days from the date of this prospectus.

Delivery of the shares of Class A Common Stock will be made on or about , 2022.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse |

KKR | Wells Fargo Securities |

The date of this prospectus is , 2022.

Table of Contents

| Crescent Energy Company | ||

| Proved Reserves at SEC Pricing(1) |

598 MMBoe | |

| Proved Reserves % Liquids / % Developed at SEC Pricing(1) |

55% / 83% | |

| Proved PV-10 at SEC Pricing(1) |

$6.2 Bn | |

| Proved PV-10 at 6/30/2022 NYMEX Pricing |

$8.6 Bn | |

| First Year PDP Decline (%)(1) |

22% | |

| 2022E Capital Budget ($MM)(2) |

$600 – $700 | |

| % Operated of Capital Budget (%)(2) |

80 – 85% | |

| Total Gross Inventory(3) |

1,679 | |

| Total Net Inventory(3) |

810 | |

Note: As of December 31, 2021, after giving effect to the Uinta Acquisition, which closed on March 30, 2022.

| (1) | SEC reserves based on reports prepared or audited by our independent reserve engineers. |

| (2) | For more information, see “Summary—Development program and capital budget.” |

| (3) | For more information, see “Summary—Attractive development opportunities.” |

Table of Contents

| 1 | ||||

| 26 | ||||

| 30 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 37 | ||||

| 43 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSIDERATIONS FOR NON-U.S. HOLDERS |

46 | |||

| 51 | ||||

| 56 | ||||

| 56 | ||||

| 56 | ||||

| 57 | ||||

| A-1 |

You should rely only on the information included or incorporated by reference in this prospectus and any free writing prospectus prepared by us or on behalf of us or the information to which we have referred you. Neither we, the underwriters, the selling stockholder nor any of our or their representatives have authorized anyone to provide you with information different from that included or incorporated by reference in this prospectus and any free writing prospectus. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We, the selling stockholder and the underwriters are offering to sell shares of Class A Common Stock and seeking offers to buy shares of Class A Common Stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the Class A Common Stock. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

Industry and Market Data

The market data and certain other statistical information included or incorporated by reference in this prospectus are based on our own internal company surveys, the good faith estimates of management, independent industry publications, government publications and other independently published sources. Although we believe our internal surveys, estimates of management and these third-party sources are reliable as of their respective dates, neither we nor the underwriters have independently verified the accuracy or completeness of this information. The industry in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section entitled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these publications.

Trademarks and Trade Names

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not, imply a relationship with us or

Table of Contents

an endorsement or sponsorship by or of us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable licensor to these trademarks, service marks and trade names.

Merger Transactions

On December 7, 2021, we completed the Merger Transactions (as defined below), pursuant to which the business of Contango Oil & Gas Company, a Texas corporation (“Contango”), and the business of Independence Energy LLC (“Independence”), a Delaware limited liability company and our predecessor for financial reporting purposes, combined indirectly under a new publicly traded holding company named “Crescent Energy Company.” Our Class A Common Stock is listed on the NYSE under the symbol “CRGY.” The combined company is structured as an “Up-C,” with all of our assets and operations (including those of Contango) indirectly held by our operating subsidiary, Crescent Energy OpCo LLC, a Delaware limited liability company (“OpCo”). Our sole material asset consists of economic, non-voting limited liability company interests in OpCo (“OpCo Units” and, the holders of such OpCo Units, “OpCo Unitholders”). We are the sole managing member of OpCo. Former Contango stockholders own shares of our Class A Common Stock, which have both voting and economic rights. The former owners of Independence (“Former Independence Owners”) own OpCo Units and shares of our Class B Common Stock (as defined below), which have voting (but no economic) rights. OpCo Units (together with shares of Class B Common Stock) may be redeemed or exchanged for Class A Common Stock or, at our election, cash on the terms and conditions set forth in Amended and Restated Limited Liability Company Agreement of OpCo.

Basis of Presentation

Holding Company Structure

Crescent Energy Company is a holding company that conducts substantially all of its business through its consolidated subsidiaries. See “Summary—Our Corporate Structure.” The predecessor of Crescent Energy Company is Independence, which merged with and into OpCo, a subsidiary of Crescent Energy Company, on December 7, 2021, pursuant to the Merger Transactions. Crescent Energy Company is the sole managing member of OpCo and is responsible for all operational, management and administrative decisions relating to OpCo’s business and consolidates the financials results of OpCo and its subsidiaries. In the sections of this prospectus that describe our business, except as otherwise indicated or required by the context, references to the “Company,” “we,” “us,” “our” and like terms refer (i) prior to the consummation of the Merger Transactions, to Independence and its subsidiaries, and (ii) subsequent to the consummation of the Merger Transactions, to Crescent Energy Company and its subsidiaries, including OpCo and its subsidiaries.

Pro Forma Presentation

This prospectus also includes or incorporates by reference certain pro forma financial and operating data. As used herein, except as otherwise indicated, the term “pro forma” when used with respect to any financial or operating data, refers to the historical data of Crescent Energy Company (including, as applicable, its predecessor, Independence), as adjusted after giving effect to the Merger Transactions. In addition, the pro forma financial data includes adjustments relating to (i) the redemption by certain of Independence’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by a certain third-party investor in exchange for its proportionate share of the underlying oil and natural gas interests held directly or indirectly by such subsidiaries (the “Carve-Out”) and the redemption by certain of Independence’s consolidated subsidiaries of the noncontrolling equity interests held in such subsidiaries by certain third-party investors in exchange for membership interests in Independence in April 2021 (the “April 2021 Exchange,” and together with the Carve-Out, the “Carve-Out/Exchange”), (ii) the entry into the Revolving Credit Facility (as defined below) and the offering of the Original Notes (as defined below) (the “Independence Refinancing”), (iii) the acquisition of a portfolio of oil and natural gas mineral assets located in the DJ Basin from an unrelated third-party operator (the “DJ Basin Acquisition”), (iv) the acquisition of certain operated producing oil and natural gas properties

Table of Contents

predominantly located in the Central Basin Platform in Texas and New Mexico (the “Central Basin Platform Acquisition”), (v) the February 2022 issuance of the New Notes (as defined below) and the use of proceeds therefrom to repay amounts outstanding under the Revolving Credit Facility (the “Crescent Refinancing” and together with the Carve-Out/Exchange, the Independence Refinancing, the DJ Basin Acquisition and the Central Basin Platform Acquisition, the “Crescent Transactions”) and (vi) the Uinta Acquisition (as defined under “Summary—Recent Developments”) consummated on March 30, 2022. Further, Contango completed the acquisition of Mid-Con Energy Partners, LP (the “Mid-Con Acquisition”), the acquisition of Grizzly Operating, LLC (the “Grizzly Acquisition”), and the acquisition of certain assets located in the Wind River Basin of Wyoming (the “Wind River Basin Acquisition” and, together with the Mid-Con Acquisition and the Grizzly Acquisition, the “Contango Transactions”) during the period presented.

The unaudited pro forma condensed combined statement of operations (the “pro forma statement of operations”) for the year ended December 31, 2021 gives effect to each of the Merger Transactions, the Crescent Transactions, the Uinta Acquisition and the Contango Transactions (together, the “Transactions”) as if they had been consummated on January 1, 2021. The unaudited pro forma condensed combined statements of operations for the six months ended June 30, 2022 give effect to the Uinta Acquisition as if it had occurred on January 1, 2021. Pro forma financial data contains certain reclassification adjustments to conform the historical Contango financial statement presentation to our financial statement presentation. In each case, the pro forma data is presented for illustrative purposes only and should not be relied upon as an indication of the financial condition or the operating results that would have been achieved if the Transactions had taken place on the specified dates. In addition, future results may vary significantly from the results reflected in such pro forma financial and operating data and should not be relied on as an indication of future results. For additional information regarding the pro forma data included or incorporated by reference herein, see our pro forma statements of operations, together with the related notes thereto, as filed on our Current Report on Form 8-K on April 8, 2022, our Current Report on Form 8-K/A on May 19, 2022, and our Current Report on Form 8-K on August 19, 2022, in each case as incorporated by reference herein.

Rounding; Percentages

Further, the financial information and certain other information presented in this prospectus have been rounded to the nearest whole number or the nearest decimal. Therefore, the sum of the numbers in a column may not conform exactly to the total figure given for that column in certain tables in this prospectus. In addition, certain percentages presented in this prospectus reflect calculations based upon the underlying information prior to rounding and, accordingly, may not conform exactly to the percentages that would be derived if the relevant calculations were based upon the rounded numbers or may not sum due to rounding.

Table of Contents

This summary highlights information included elsewhere in, or incorporated by reference into, this prospectus. This summary does not contain all of the information that you should consider before investing in our Class A Common Stock. You should carefully read the entire prospectus, together with the additional information described under “Information Incorporated by Reference,” before investing in our Class A Common Stock. The information presented in this prospectus assumes, unless otherwise indicated, that the underwriters’ option to purchase additional shares of Class A Common Stock is not exercised. References in this prospectus to the “selling stockholder” refer to the selling stockholder that is offering shares of Class A Common Stock as set forth in the section entitled “Selling Stockholder.” This prospectus includes certain terms commonly used in the oil and natural gas industry, which are defined elsewhere in this prospectus in the “Glossary of Terms” contained in Annex A. Unless otherwise indicated, the estimates of our proved, probable and possible reserves as of December 31, 2021 have been prepared or audited, as applicable, by Netherland, Sewell & Associates, Inc. (“NSAI”), Haas Petroleum Engineering Services, Inc., Cawley, Gillespie & Associates, Inc. (“CG&A”) and William M. Cobb & Associates, Inc., our independent reserve engineers (collectively, “Independent Reserve Engineers”).

Our Company

Overview

We are a well-capitalized U.S. independent energy company with a portfolio of low-decline assets in proven regions across the lower 48 states that generate substantial cash flow and deliver significant stockholder returns. Our core leadership team is a group of experienced investment, financial and industry professionals who continue to execute on the strategy we have employed since 2011. Our mission is to invest in energy assets and deliver better returns through strong operations and stewardship. We seek to deliver attractive risk-adjusted investment returns and predictable cash flows across cycles by employing our differentiated approach to investing in the oil and gas industry. Our approach employs a unique business model that combines an investor mindset and deep operational expertise to pursue a cash flow-based investment mandate focused on operated working interests with an active risk management strategy. Our Class A Common Stock trades on the NYSE under the symbol “CRGY.”

We pursue our strategy through the production, development and acquisition of oil, natural gas and natural gas liquid (“NGL”) reserves. Our free cash flow-focused portfolio includes a balanced set of oil and natural gas assets in proven onshore U.S. basins with substantial existing production, a low decline rate and an acreage position that is 96% held by production, inclusive of the assets acquired in the Uinta Acquisition. Based on forecasts used in our reserve reports, our PDP reserves as of December 31, 2021 have estimated average five-year and ten-year annual decline rates of approximately 13% and 11%, respectively, and an estimated 2022 PDP decline rate of 22%. The relatively higher decline rate in 2022 is due primarily to the high initial production profiles of certain more recently drilled PDP wells acquired in the Uinta Acquisition, which we expect to decrease over time as wellbore pressure gradually declines and stabilizes. As a result of this overall low decline profile, we require relatively minimal capital expenditures to maintain our production and cash flows while supporting our dividend policy. We have a robust inventory of attractive operated undeveloped locations, providing for optimal flexibility to maintain or grow our production base. Our portfolio is enhanced and complemented by our additional interests in mineral acreage and midstream infrastructure, which provide operational benefits and enhance our cash flow margins.

We have built a substantial portfolio of reserves, production, cash flows and reinvestment opportunities. On a pro forma basis after giving effect to the Transactions, our portfolio of assets:

| • | at December 31, 2021, consisted of 597.8 net MMBoe of proved reserves, of which approximately 55% were liquids, reflecting: |

| • | $6.0 billion in net proved standardized measure and $6.2 billion in net proved present value discounted at PV-10 at SEC pricing; and |

1

Table of Contents

| • | $8.6 billion in net proved present value discounted at PV-10 at NYMEX pricing as of June 30, 2022; |

| • | during the year ended December 31, 2021, produced 148 net MBoe/d and during the six months ended June 30, 2022, produced 145 net MBoe/d; |

| • | during the year ended December 31, 2021, generated a $245.2 million net loss, $963.5 million of Adjusted EBITDAX and $665.4 million of Levered Free Cash Flow, and during the six months ended June 30, 2022, generated $25.7 million of net loss, $698.7 million of Adjusted EBITDAX and $357.1 million of Levered Free Cash Flow; and |

| • | at December 31, 2021 had 1,679 gross (810 net) undrilled locations, including 718 gross (575 net) operated drilling locations. Of our total 810 net locations, 211 net locations are identified as PUD drilling locations. In total, our drilling locations represent an aggregate of over $4.7 billion of reinvestment potential, of which $1.3 billion is attributable to PUD drilling locations in total. |

For definitions of Adjusted EBITDAX and Levered Free Cash Flow, including reconciliations to the nearest U.S. generally accepted accounting principles (“GAAP”) measure, see “—Summary Historical Financial Data—Non-GAAP Financial Measures.”

Free cash flow-focused portfolio promotes return of capital to investors

We have constructed a liquids-weighted portfolio of long-lived reserves and low decline production that generates substantial cash flow with a robust inventory of attractive undeveloped locations. We believe that the stable nature of our producing assets combined with our hedging strategy and low leverage profile provides us the ability to generate strong free cash flow in a variety of commodity price environments, which positions us to maintain financial strength and consistently return capital to stockholders. Our estimated 2022 PDP decline rate of 22%, based on forecasts used in our reserve reports, is substantially lower than the industry average. The low decline nature of our asset base requires minimal reinvestment to maintain our production, and provides us with significant flexibility to pursue both reinvestment opportunities within our current portfolio, strategic acquisitions and/or return capital to investors. While many of our peers have historically outspent their cash flows, we have averaged a reinvestment rate, which we define as our historical capital expenditures (excluding acquisitions) over a specified period as a percentage of our historical Adjusted EBITDAX for such period, of 40% of Adjusted EBITDAX since 2018. This highlights management’s capital discipline and commitment to returning capital to stockholders. Adjusted EBITDAX is a non-GAAP financial measure, as discussed further under “—Summary Historical Financial Data—Non-GAAP Financial Measures.”

Our fixed within a framework dividend policy is generally set annually and targets distributing 10% of Adjusted EBITDAX. Our dividend is designed to deliver a reliable return of capital to our stockholders and we believe it is more stable than that of our peers as it is not impacted by capital expenditures with Crescent’s dividends taking priority to reinvestment decisions and is supported by an active hedging program. Our management team has a long history of paying dividends to stockholders and Independence, our predecessor, paid dividends for nine consecutive years as a private company, through volatile commodity and market conditions and while maintaining a low leverage profile.

Low-decline production base underpins free cash flow generation and dividend

Based on forecasts used in our reserve reports, our PDP reserves as of December 31, 2021 have estimated average five-year and ten-year annual decline rates of approximately 13% and 11%, respectively, and an estimated 2022 PDP decline rate of 22%. The relatively higher decline rate in 2022 is due primarily to the high initial production profiles of certain more recently drilled PDP wells acquired in the Uinta Acquisition, which we expect to decrease over time as wellbore pressure gradually declines and stabilizes. As a result of this overall low decline profile, we require relatively minimal capital expenditures to maintain our production

2

Table of Contents

and cash flows while supporting our dividend policy. Our properties located in the Eagle Ford, Rockies and Barnett represent approximately 80% of our proved reserves as of December 31, 2021, and provide us with diversification from both a regional location and commodity price perspective, which provides us certain downside protection as it relates to commodity-specific pressures, isolated infrastructure constraints or severe weather events. Our net proved standardized measure totaled $6.0 billion as of December 31, 2021. The table below illustrates the aggregate leasehold acreage positions, reserve volumes and weighted average decline profiles associated with our proved assets as of December 31, 2021.

| Net Acreage |

Net Proved Reserves (1) |

% Oil & Liquids (1) |

Net PD Reserves (1) |

Weighted Average Annual PDP Decline (2) |

Net Proved PV-10 (1)(3) |

Net PD PV-10 (1)(3) |

Net Proved PV-10 (1)(3) |

Net PD PV-10 (1)(3) |

||||||||||||||||||||||||||||||||

| Operating Area |

Five Year |

Ten Year |

SEC (1) | NYMEX (6) | ||||||||||||||||||||||||||||||||||||

| (M) | (MMBoe) | (MMBoe) | (MM) | (MM) | (MM) | (MM) | ||||||||||||||||||||||||||||||||||

| Eagle Ford |

143 | 136 | 79 | % | 84 | 13 | % | 11 | % | $ | 1,954 | $ | 1,307 | $ | 2,593 | $ | 1,697 | |||||||||||||||||||||||

| Rockies (4) |

243 | 147 | 52 | % | 143 | 10 | % | 10 | % | 1,319 | 1,250 | 1,877 | 1,794 | |||||||||||||||||||||||||||

| Barnett |

133 | 130 | 16 | % | 129 | 6 | % | 6 | % | 605 | 605 | 930 | 930 | |||||||||||||||||||||||||||

| Permian |

107 | 54 | 69 | % | 37 | 15 | % | 12 | % | 594 | 458 | 779 | 611 | |||||||||||||||||||||||||||

| Other (5) |

402 | 65 | 68 | % | 66 | 13 | % | 10 | % | 687 | 685 | 912 | 907 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total excluding Uinta Acquisition |

1,028 | 532 | 54 | % | 459 | 11 | % | 10 | % | $ | 5,159 | $ | 4,305 | $ | 7,091 | $ | 5,939 | |||||||||||||||||||||||

| Uinta Acquisition |

145 | 66 | 65 | % | 40 | 28 | % | 21 | % | 1,054 | 733 | 1,551 | 1,091 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Total including Uinta Acquisition |

1,174 | 598 | 55 | % | 499 | 13 | % | 11 | % | $ | 6,213 | $ | 5,038 | $ | 8,642 | 7,030 | ||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| (1) | Our reserves and present value (discounted at ten percent, or PV-10) were determined using average first-day-of-the-month prices for the prior 12 months in accordance with guidance from the Securities and Exchange Commission (“SEC”). For oil and NGL volumes, the average WTI posted price of $66.56 per barrel as of December 31, 2021, was adjusted for items such as gravity, quality, local conditions, gathering, transportation fees and distance from market. For natural gas volumes, the average Henry Hub Index spot price of $3.598 per MMBtu as of December 31, 2021, was similarly adjusted for items such as quality, local conditions, gathering, transportation fees and distance from market. All prices are held constant throughout the lives of the properties. The average adjusted product prices over the remaining lives of the properties are $64.84 per barrel of oil, $3.46 per Mcf of natural gas and $27.21 per barrel of NGLs. |

| (2) | Reflects the estimated annualized decline rates of our PDP reserves as of December 31, 2021 from the monthly period ending January 31, 2022 and the monthly period ending January 31, 2027 for the five-year decline and from the monthly period ending January 31, 2022 and the monthly period ending January 31, 2032 for the ten-year decline, in each case based on the forecasts used in estimating our proved reserves. |

| (3) | Reflects the net Proved and PD present values reflected in our proved reserve estimates as of December 31, 2021. PV-10 is not a financial measure prepared in accordance with GAAP. See “—Summary Reserve and Operating Data” for additional discussion. |

| (4) | We have a contractual right to participate in 29 thousand net acres in the DJ Basin through an agreement with a large operator and will be entitled to receive our proportionate share of acreage in the future based on our participation in proposed wells. |

| (5) | Includes working interest properties located in Mid-Con, California as well as diversified mineral and royalty interests. |

| (6) | The NYMEX reserves, PV-0 and PV-10 of Crescent Energy Company and the Uinta Acquisition were determined using index prices for oil and natural gas, respectively, without giving effect to derivative transactions and were calculated based on settlement prices to better reflect the market expectations as of that date, as adjusted for our estimates of quality, transportation fees, and market differentials. The NYMEX reserves calculations are based on NYMEX futures pricing at closing on June 30, 2022 for oil and natural gas. The average adjusted product prices over the remaining lives of the properties are $70.17 per barrel of oil, $4.45 per Mcf of natural gas and $29.40 per barrel of NGLs as of December 31, 2021. We believe that the use of forward prices provides investors with additional useful information about our reserves, as the forward prices are based on the market’s forward-looking expectations of oil and natural gas prices as of a certain date, although we caution investors that this information should be viewed as a helpful alternative, not a substitute, for the data presented based on SEC Pricing. See “—Summary Reserve and Operating Data—Summary Reserve Data based on NYMEX Pricing.” |

3

Table of Contents

Attractive development opportunities

Our development inventory is low-risk and located in proven basins with substantial well control. As of December 31, 2021, we have identified 1,679 gross (810 net) undrilled locations, including 718 gross (575 net) operated drilling locations. Of our total 810 net locations, 211 net locations are identified as PUD drilling locations as of December 31, 2021. The majority of these locations are on acreage that is held by production, providing valuable optionality. This allows us to react quickly to commodity price fluctuations and focus on opportunities that provide high return on invested capital.

Eagle Ford. We have operated and non-operated Eagle Ford development opportunities with attractive return profiles in Dimmit, Frio, Atascosa, Zavala and Webb Counties, Texas. As of December 31, 2021, we have identified 890 gross (393 net) undrilled locations in the Eagle Ford basin, including 270 gross (259 net) operated drilling locations. Of our total 393 net locations, 123 net locations are reflected as PUDs.

Permian. We have operated and non-operated Permian development opportunities with attractive return profiles in Reeves, Ector and Pecos Counties, Texas targeting the Wolfcamp, Bone Spring and Spraberry formations. As of December 31, 2021, we have identified 326 gross (123 net) undrilled locations in the Permian basin, including 153 gross (88 net) operated drilling locations. Of our total 123 net locations, 18 net locations are reflected as PUDs.

Uinta. As a result of the Uinta Acquisition, we have operated Uinta development opportunities with attractive return profiles in Duchesne and Uintah Counties, Utah targeting the Uteland Butte and Wasatch formations. As of December 31, 2021, on a pro forma basis after giving effect to the Uinta Acquisition, we have identified 151 gross (125 net) undrilled locations in the Uinta basin, all of which are operated. Of our total 125 net locations, 52 net locations are reflected as PUDs.

Total identified drilling locations. The following table describes our net identified drilling locations and total reinvestment opportunity calculated based on the estimated net drilling and completion (“D&C”) expenditures by area, in each case, as of December 31, 2021.

| Total Net Identified Drilling Locations (1) |

Operated Net Identified Drilling Locations (1) |

Total Estimated Net D&C Expenditures |

||||||||||

| (in millions) | ||||||||||||

| Eagle Ford |

393 | 259 | $ | 2,166 | ||||||||

| Permian |

123 | 88 | 842 | |||||||||

| Other (2) |

169 | 103 | 587 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total excluding Uinta Acquisition |

685 | 450 | $ | 3,595 | ||||||||

| Uinta Acquisition |

125 | 125 | 1,100 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total including Uinta Acquisition |

810 | 575 | $ | 4,745 | ||||||||

|

|

|

|

|

|

|

|||||||

| (1) | Includes 123, 18, 19 and 52 net PUD locations in the Eagle Ford, Permian, other operating areas and Uinta, respectively, with associated estimated net D&C expenditures of $766 million, $136 million, $21 million and $391 million, respectively. Does not include minerals. For information regarding the assumptions underlying our identified reinvestment opportunities, see “Items 1 and 2. Business and Properties” in our Annual Report on Form 10-K for the year ended December 31, 2021, incorporated herein by reference. |

| (2) | Includes drilling locations in the Rockies, Barnett and other areas. |

4

Table of Contents

In addition to our identified drilling locations listed in the table above and the Uinta Acquisition assets, we have additional undeveloped locations under our mineral and royalty interests that, when developed by the oil and natural gas companies designated as the operators on such acreage, will provide cash flows unburdened by capital costs.

Business Strategies

Our primary business objective is to deliver free cash flow and attractive risk-adjusted returns for our investors through the execution of the following strategies:

| • | Build and operate a diversified portfolio of proven, low-risk, cash-flowing assets. We have constructed a liquids-weighted portfolio of long-lived reserves and low decline production that generates substantial cash flow with a robust inventory of attractive undeveloped locations. We believe that the stable nature of our producing assets combined with our hedging strategy and low leverage profile provides us the opportunity to generate strong free cash flow in a variety of commodity price environments, which positions us to consistently return capital to stockholders. For example, while many of our peers have historically outspent their cash flows in pursuit of production growth and left themselves particularly vulnerable to declines in commodity prices, we have averaged a reinvestment rate of 40% of Adjusted EBITDAX since 2018. For a definition of Adjusted EBITDAX, including a reconciliation to the nearest GAAP measure, see “—Summary Historical Financial Data—Non-GAAP Financial Measures.” We expect to continue to utilize the free cash flow generated from our producing assets to pay dividends to stockholders, maintain conservative leverage levels, reinvest in existing development opportunities and strategically pursue complementary, accretive acquisitions. |

| • | Maximize returns to stockholders through disciplined reinvestment. We believe we have an extensive inventory of low-risk, high-return development opportunities that are capable of generating attractive cash on cash returns. However, we seek to find the right balance between returning additional capital to investors in the short-term and investing for longer-term value creation, such as through drilling and accretive acquisitions. As of December 31, 2021, we identified 1,679 gross (810 net) undrilled locations, including 718 gross (575 net) operated drilling locations representing over $4.7 billion of reinvestment potential. Of our total 810 net locations, 211 net locations were identified as PUD drilling locations and reflect $1.3 billion of anticipated capital spend. After accounting for the Uinta Acquisition, our 2022 expected capital program, which totals between $600 million and $700 million, is approximately 95% allocated to D&C (80 to 85% to our operated assets primarily in the Eagle Ford and Uinta basins and 10 to 15% to non-operated activity) and approximately 5% to other capital expenditures. Our high degree of operational control and the fact that our asset base is largely held by production provides flexibility over the execution of our development program, including the timing, amount and allocation of our capital expenditures. Including the Uinta Acquisition assets, approximately 96% of our net acreage as of December 31, 2021 was held by production. |

| • | Focus on financial strength and flexibility. We intend to maintain a conservative and flexible capital structure to actively manage risk across the business. As of June 30, 2022, we had $508 million in liquidity, including $55 million in cash and cash equivalents and $453 million of available borrowings under the credit agreement (the “Revolving Credit Facility”), and total outstanding principal indebtedness of $1.5 billion. We intend to maintain conservative leverage in the future with a long-term corporate leverage target at or below 1.0x net debt to Adjusted EBITDAX. See “—Summary Historical Financial Data—Non-GAAP Financial Measures” for our |

5

Table of Contents

| definition of Adjusted EBITDAX and reconciliations of Adjusted EBITDAX to net income (loss), the nearest comparable GAAP measure. In addition, we employ an active hedging strategy that allows us to protect the balance sheet and corporate returns while maintaining adequate exposure to commodity prices and upside therefrom. |

| • | Develop industry-leading environmental, social and governance (“ESG”) practices that benefit our stakeholders and the communities in which we operate. We view exceptional performance in managing ESG issues as an opportunity to differentiate ourselves from our peers, mitigate risks and strengthen operational performance, as well as benefit our stakeholders and the communities in which we operate. Our ESG program is overseen by senior management, executed together with experienced industry professionals throughout our organization and supported by the resources of the KKR Group, along with the assistance of expert third-party advisors for insights on best practices. In December 2021, we released our inaugural ESG report, which included key performance metrics according to Value Reporting Foundation’s Sustainability Accounting Standards Board (“SASB”) Standard for Oil & Gas – Exploration & Production and also established our key ESG priorities. We are committed to engaging across our organization to assess and manage key ESG issues. In connection with that commitment, we have also established an ESG Advisory Council to advise management and our board of directors on ESG-related issues. We are also working to reduce greenhouse gas (“GHG”) emissions by implementing aggressive methane reduction targets and eliminating routine flaring where feasible, among other initiatives. In February 2022, we joined the Oil & Gas Methane Partnership (“OGMP”) 2.0 Initiative to enhance reporting of methane emissions reduction programs. Our inaugural OGMP 2.0 submission was rated the highest-level, “Gold Standard.” We plan to include short- and long-term ESG targets focused on EHS and emissions in our 2021 ESG report. |

| • | Evaluate and pursue opportunistic and value-oriented acquisitions focused on cash-on-cash returns. Our business has been built over time through a series of strategic mergers and acquisitions. We are experienced acquirers and have been executing a strategy of opportunistically acquiring well understood cash flow oriented assets since the founding of the business. We employ a differentiated business model that combines an investor mindset with deep operational expertise to deliver sustainable stockholder value creation. Since 2020, we have completed ten acquisitions, including the Uinta Acquisition (as defined below), as discussed further under “—Recent Developments.” We believe today’s market dynamic creates an attractive market for consolidation, driven by historically low equity capital formation and an increasing supply of assets and businesses for sale. We anticipate a large and increasing universe of attractive target opportunities from the divestiture programs of majors and large-cap independents, subscale public and private companies, private and unnatural owners seeking liquidity and bolt-on opportunities near existing assets. We will continue to evaluate acquisitions consistent with our cash flow-based strategy to further improve our asset portfolio and enhance investor returns. Our recent Uinta Acquisition highlights our acquisition strategy to buy low-risk cash flow oriented assets that are accretive and enhance our portfolio while maintaining low leverage. |

Competitive Strengths

We believe that the following competitive strengths differentiate us from our peers and uniquely position us to achieve our primary business objective.

| • | Diversified free cash flow-generating production base supports the dividend and drives enhanced stockholder returns. Our fixed within a framework dividend policy is generally set annually and targets distributing 10% of Adjusted EBITDAX. Our dividend is designed to deliver a reliable return of capital to our stockholders and we believe it is more stable than that of our peers as it is not impacted by capital expenditures with Crescent’s dividends taking priority to reinvestment decisions and is supported by an active hedging program. Our management team |

6

Table of Contents

| has a long history of paying dividends to stockholders and Independence, our predecessor, paid dividends for nine consecutive years as a private company, through volatile commodity and market conditions and while maintaining a low leverage profile. Our dividend is supported by our large, balanced portfolio of producing properties that generate substantial free cash flow and our significant developmental upside that enhances our production, free cash flow and stockholder returns. Our reserves are generally long-lived and characterized by relatively low production decline rates. Our estimated 2022 PDP decline rate of 22% is substantially lower than the industry average. The low decline nature of our asset base requires minimal capital reinvestment to maintain our production, and provides us with significant flexibility to pursue both reinvestment opportunities within our current portfolio, strategic acquisitions and/or return capital to investors. Our producing properties have been substantially de-risked from years of development and have sufficient existing infrastructure to transport our production to market. Our geographic diversity also leaves us less susceptible to geographically isolated infrastructure constraints, severe weather events and other risks. We believe the combination of our low decline and liquids-weighted asset profile combined with our active hedging strategy and low leverage profile positions us to generate free cash flow throughout the commodity cycles that may be returned to stockholders through dividends. |

| • | Disciplined investment in development and complementary opportunities. We have a proven history of utilizing cash flows generated from our producing assets to reinvest in the development of our oil and natural gas assets. As of December 31, 2021, we identified 1,679 gross (810 net) undrilled locations, of which 211 net drilling locations are identified as PUD drilling locations, representing over $4.7 billion of reinvestment potential, of which $1.3 billion is attributable to PUD drilling locations. We believe that our reinvestment in development opportunities has generated attractive risk-adjusted returns through strong operations, commercial creativity, capital discipline and strong risk management. Additionally, we will continue to strategically evaluate accretive acquisitions of oil and natural gas assets in targeted areas that are complementary to our underlying asset base and are supported by strong cash flow. |

| • | Aligned management team with a proven track record and ESG focus. Our executive leadership team is a group of experienced investment, financial and industry professionals who have a demonstrated track record of employing our strategy since 2011, with experience in asset management, capital allocation, ESG stewardship, risk management, investing, finance and accounting. Our differentiated approach, which was created through combining superior financial and risk management capabilities with premier operational capabilities, provides us with a competitive advantage in navigating a variety of commodity price and market environments. Our talented and highly motivated operational leadership are experts in their respective geographies and utilize their expertise to drive the day-to-day operations of our assets. Furthermore, the performance-based incentive structure of our Management Agreement (as defined below) and the significant equity ownership of stockholders associated with our Manager provide for alignment of interests for long-term value creation. Additionally, our relationship with the KKR Group also provides us access to a constellation of global resources, including a deep bench of experienced investment professionals and resources specifically dedicated to monitoring and understanding issues and trends, recommending strategies, providing assistance and otherwise helping companies navigate changing market dynamics with respect to ESG-related issues, including the KKR Group’s Global Institute and Public Affairs team. |

| • | Well-capitalized balance sheet and strong liquidity profile supported by active risk management approach. As of June 30, 2022, we had total principal indebtedness of $1.5 billion and $508 million in liquidity, including $55 million in cash and cash equivalents and $453 million of available borrowings under the Revolving Credit Facility. Since our inception, our |

7

Table of Contents

| strategy has been to maintain a conservative balance sheet, low leverage and an active risk management program. For example, our net leverage ratio on a net debt to trailing twelve month Adjusted EBITDAX basis has averaged 1.2x since 2011. While maintaining these conservative leverage levels, we generated a net loss of $432.2 million and Levered Free Cash Flow of $276.7 million for the year ended December 31, 2021, and during the six months ended June 30, 2022, we generated a net loss of $124.1 million and Levered Free Cash Flow of $226.7 million. See “—Summary Historical Financial Data—Non-GAAP Financial Measures” for definitions of Adjusted EBITDAX and Levered Free Cash Flow and reconciliations to the nearest comparable GAAP metrics. |

Development Program and Capital Budget

Our development program is designed to prioritize the generation of attractive risk-adjusted returns and meaningful free cash flow and is inherently flexible, with the ability to modify our capital program as necessary to react to the current market environment. On a pro forma basis for the Transactions, our capital expenditures, excluding acquisitions, incurred during the year ended December 31, 2021 and the six months ended June 30, 2022 totaled approximately $231.6 million and $278.9 million, respectively.

After accounting for the Uinta Acquisition, our 2022 expected capital program, which totals between $600 million and $700 million, is approximately 95% allocated to D&C drilling and completion (80 to 85% to our operated assets primarily in the Eagle Ford and Uinta basins and 10 to 15% to non-operated activity) and approximately 5% to other capital expenditures. Due to the flexible nature of our capital program and the fact that our acreage is 96% held by production, inclusive of the Uinta Acquisition, we could choose to defer a portion or all of these planned capital expenditures depending on a variety of factors, including, but not limited to, the success of our drilling activities, prevailing and anticipated prices for oil, gas and NGLs and resulting well economics, the availability of necessary equipment, infrastructure and capital, the receipt and timing of required regulatory permits and approvals, seasonal conditions, drilling and acquisition costs and the level of participation by other interest owners.

Our Relationship with the KKR Group

On December 7, 2021, in connection with the closing of the Merger Transactions, we entered into the management agreement (the “Management Agreement”), dated as of December 7, 2021, by and between the Company and KKR Energy Assets Manager LLC, a Delaware limited liability company (the “Manager”), that engages the Manager to provide certain management and investment advisory services to us and our subsidiaries. Our management team provides services to us pursuant to the Management Agreement.

The Manager is an indirect subsidiary of KKR & Co. Inc. (together with its subsidiaries, the “KKR Group”). The KKR Group is a leading global investment firm that offers alternative asset management as well as capital markets and insurance solutions.

Pursuant to the Management Agreement, the Manager has agreed to provide us with management services, including senior members of our full executive and corporate management teams, and other assistance, including with respect to strategic planning, risk management, identifying and screening potential acquisitions, identifying and analyzing ESG issues and providing such other assistance as we may require. Furthermore, entities affiliated with the KKR Group invested in the predecessor of Crescent, helped found the strategy we have employed since 2011 and continue to hold a significant investment in our company.

Through our integration with the KKR Group’s global platform, we believe that we benefit from: the power of the “KKR” brand; KKR Global Macro and Asset Allocation, which assists with assessing the impact of macroeconomic factors on potential investments and helps identify market opportunities; KKR Capital

8

Table of Contents

Markets, which assists with optimizing the capital structure of investments and underwrites and arranges debt, equity and other forms of financing for both KKR portfolio companies and independent clients; KKR Public Affairs, which, together with the KKR Global Institute, provides insight into public policy, government and regulatory affairs, including experience working with key stakeholders, such as labor unions, industry and trade associations and non-governmental organizations, and ESG issues and opportunities; and KKR Capstone, which creates value by assisting with due diligence and identifying and delivering sustainable operational performance improvements within the KKR Group’s portfolio companies.

For additional information regarding our Management Agreement and our relationship with the KKR Group, see “Risks related to our business and the oil and natural gas industry” in “Item 1A. Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2021, incorporated herein by reference, “Underwriting (Conflicts of Interest)” and “Selling Stockholder” herein.

Merger Transactions and Our Corporate Structure

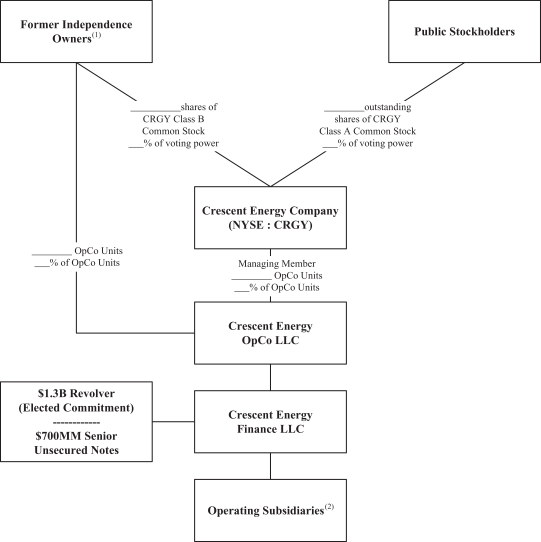

On December 7, 2021, we completed the transactions contemplated by the Transaction Agreement, which included the merger of Independence with and into OpCo, the merger of IE Merger Sub Inc., a Delaware corporation, with and into Contango, with Contango surviving the merger as a direct wholly owned corporate subsidiary of the Company (the “Contango Merger”), the subsequent merger of Contango with and into IE L Merger Sub LLC, a Delaware limited liability company, with IE L Merger Sub LLC surviving the merger as a wholly owned subsidiary of us, which we describe as the “Merger”, and the subsequent contribution of such surviving subsidiary by us to OpCo (such transactions, the “Merger Transactions”), pursuant to which Contango’s business combined with Independence’s business indirectly under a new publicly traded holding company named “Crescent Energy Company.” From and after December 8, 2021, our Class A Common Stock has been listed on the NYSE and trades under the symbol “CRGY.” Our company is structured as an “Up-C.” Former Contango stockholders own shares of our Class A Common Stock, which have both voting and economic rights. Former Independence Owners own OpCo Units and corresponding shares of Class B common stock, par value $0.0001 per share, of the Company (“Class B Common Stock” and, together with Class A Common Stock, “Common Stock”), which shares of Class B Common Stock have voting (but no economic) rights. We are a holding company, and our sole material asset consists of OpCo Units. We are the sole managing member of OpCo. We are therefore responsible for all operational, management and administrative decisions relating to OpCo’s business and consolidate the financial results of OpCo and its subsidiaries.

The shares of our Class A Common Stock being sold in this offering by the selling stockholder represent shares of Class A Common Stock to be issued upon redemption by such selling stockholder of an equivalent number of OpCo Units and a corresponding number of shares of our Class B Common Stock.

9

Table of Contents

The following diagram displays our simplified ownership structure, as of June 30, 2022 and after giving effect to this offering, assuming that the underwriters do not exercise their option to purchase additional shares:

| (1) | The shares of Class A Common Stock to be sold by the selling stockholder, a Former Independence Owner, represent the shares of Class A Common Stock to be issued upon redemption of an equivalent number of OpCo Units and a corresponding number of shares of Class B Common Stock immediately prior to the closing of this offering. See “Selling Stockholder.” |

| (2) | Guarantors under the Revolving Credit Facility and Senior Notes. |

Recent Developments

Uinta Basin Acquisition

On March 30, 2022, one of our operating subsidiaries (the “Purchaser”), and OpCo consummated the purchase from Verdun Oil Company II LLC, a Delaware limited liability company (the “Seller”), all of the

10

Table of Contents

issued and outstanding membership interests (the “Purchased Interests”) of Uinta AssetCo, LLC, a Texas limited liability company and wholly owned subsidiary of the Seller (“UtahCo” and, such transactions, the “Uinta Acquisition”), pursuant to a Membership Interest Purchase Agreement (the “Purchase Agreement”) with Seller, with an effective date of January 1, 2022. As a result, UtahCo—and indirectly the Company—now holds all previously held development and production assets of, and certain obligations of, EP Energy E&P Company, L.P. (“EP Energy”) located in the state of Utah. Such assets include an aggregate approximately 145,000 net acres, primarily located in Duchesne and Uintah Counties, Utah, with approximately 400 currently producing wells. Through this acquisition, we acquired low-risk assets with a strong production base and what we believe to be a multiyear inventory of high-quality oil-weighted undeveloped locations. The proved reserves we acquired in the Uinta Acquisition assets had, as of December 31, 2021, an associated $1.0 billion in net proved standardized measure and $1.1 billion and $1.6 billion in net proved present value (discounted at ten percent, or PV-10) at SEC Pricing as of December 31, 2021 and NYMEX Pricing as of June 30, 2022, respectively. For additional information regarding the reserves acquired in the Uinta Acquisition, see “—Summary Reserve and Operating Data.”

Total consideration was approximately $690 million at closing, inclusive of purchase price adjustments, expenses and costs incurred in connection with modifying certain hedges that we assumed from EP Energy at closing. The Uinta Acquisition was funded with cash on hand and borrowings under the Revolving Credit Facility. In connection with the closing of the transaction, we entered into an amendment to the Revolving Credit Facility (the “Revolving Credit Facility Amendment”) to, among other things, increase the borrowing base to $1.8 billion and the elected commitment amount to $1.3 billion.

Commodity Hedging Program

A key tenet of our focused risk management effort is an active economic hedging strategy to mitigate near-term price volatility while maintaining long-term exposure to underlying commodity prices. Our hedging program limits our near-term exposure to product price volatility and allows us to protect the balance sheet and corporate returns through commodity cycles and return capital to investors. Future transactions may include price swaps whereby we will receive a fixed price for our production and pay a variable market price to the contract counterparty. Additionally, we may enter into collars, whereby we receive the excess, if any, of the fixed floor over the floating rate or pay the excess, if any of the floating rate over the fixed ceiling.

11

Table of Contents

As of June 30, 2022, our derivative portfolio had an aggregate notional value of approximately $2.0 billion. We determine the fair value of our oil and natural gas commodity derivatives using valuation techniques that utilize market quotes and pricing analysis. Inputs include publicly available prices and forward price curves generated from a compilation of data gathered from third parties. The following table details our net volume positions by commodity as of June 30, 2022.

| Production Period |

Volumes | Weighted Average Fixed Price |

Fair Value |

|||||||||

| (in thousands) | (in thousands) | |||||||||||

| Crude oil swaps (Bbls): |

||||||||||||

| WTI |

||||||||||||

| 2022 |

6,881 | $ | 64.35 | $ | (234,085 | ) | ||||||

| 2023 |

9,710 | $ | 60.00 | (248,904 | ) | |||||||

| 2024 |

5,721 | $ | 63.82 | (80,403 | ) | |||||||

| Brent |

||||||||||||

| 2022 |

252 | $ | 56.36 | (11,398 | ) | |||||||

| 2023 |

527 | $ | 52.52 | (19,454 | ) | |||||||

| 2024 |

276 | $ | 68.65 | (4,029 | ) | |||||||

| Crude oil collars – WTI (Bbls): |

||||||||||||

| 2023 |

1,155 | $ | 48.68 - $57.87 | (32,709 | ) | |||||||

| Natural gas swaps (MMBtu): |

||||||||||||

| 2022 |

40,814 | $ | 2.77 | (116,709 | ) | |||||||

| 2023 |

62,248 | $ | 2.73 | (119,329 | ) | |||||||

| 2024 |

9,604 | $ | 4.14 | (2,288 | ) | |||||||

| NGL swaps (Bbls): |

||||||||||||

| 2022 |

1,505 | $ | 32.64 | (15,023 | ) | |||||||

| 2023 |

1,379 | $ | 40.80 | 3,351 | ||||||||

| Crude oil basis swaps (Bbls): |

||||||||||||

| 2022 |

2,857 | $ | (0.13 | ) | (5,154 | ) | ||||||

| Natural gas basis swaps (MMBtu): |

||||||||||||

| 2022 |

12,654 | $ | (0.17 | ) | (2,610 | ) | ||||||

| Calendar Month Average (“CMA”) roll swaps (Bbls): |

||||||||||||

| 2022 |

740 | $ | 1.08 | (1,557 | ) | |||||||

| Natural gas collars (MMBtu): |

||||||||||||

| 2023 |

550 | $ | 2.63 - $3.01 | (1,145 | ) | |||||||

| 2024 |

18,300 | $ | 3.38 - $4.56 | (7,603 | ) | |||||||

|

|

|

|||||||||||

| Total |

$ | (899,049 | ) | |||||||||

|

|

|

|||||||||||

12

Table of Contents

The Offering

Class A Common Stock offered

| by us |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

Class A Common Stock offered by

| the selling stockholder |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). All of such shares represent shares of Class A Common Stock to be issued to the selling stockholder upon redemption of an equivalent number of OpCo Units and a corresponding number of shares of Class B Common Stock immediately prior to the closing of this offering. See “Selling Stockholder.” |

Class A Common Stock outstanding

| immediately after this offering |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

Class B Common Stock outstanding

| immediately after this offering |

shares (or shares if the underwriters exercise their option to purchase additional shares in full). |

Shares held by the selling stockholder

| immediately after this offering |

shares of Class B Common Stock (or shares of Class B Common Stock if the underwriters exercise their option to purchase additional shares in full). See “Selling Stockholder.” |

Voting power of Class A Common Stock

| after giving effect to this offering |

% (or 100% if all outstanding OpCo Units held by the OpCo Unitholders were redeemed (along with a corresponding number of shares of our Class B Common Stock) for newly issued shares of Class A Common Stock on a one-for-one basis). |

Voting power of Class B Common Stock

| after giving effect to this offering |

% (or 0% if all outstanding OpCo Units held by the OpCo Unitholders were redeemed (along with a corresponding number of shares of our Class B Common Stock) for newly issued shares of Class A Common Stock on a one-for-one basis). |

| Voting rights |

Prior to the Trigger Date (as defined in the section herein titled “Description of Capital Stock”), holders of our Common Stock will not be entitled to elect directors to our Board of Directors. On and after the Trigger Date, the holders of our Common Stock will be entitled to elect directors but will not have cumulative voting rights in the election of directors. Holders of our Common Stock will otherwise be entitled to one vote per share held of |

13

Table of Contents

| record on all matters to be voted upon by the stockholders. Holders of our Class A Common Stock and Class B Common Stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law or by our amended and restated certificate of incorporation. See the section titled “Description of Capital Stock.” |

| Use of proceeds |

We estimate that, after deducting underwriting discounts and commissions and estimated offering expenses payable by us, we will receive approximately $ million of net proceeds from this offering (or $ million if the option to purchase additional shares is exercised in full). |

| We anticipate that we will contribute all of the net proceeds we receive from this offering to OpCo in exchange for a number of OpCo Units equal to the number of shares of our Class A Common Stock issued in this offering by us. We intend to use the net proceeds we receive from this offering to repay a portion of the amounts outstanding under the Revolving Credit Facility that were incurred in connection with the closing of the Uinta Acquisition. Affiliates of certain of the underwriters are lenders under the Revolving Credit Facility and, as a result, will receive a portion of the net proceeds from this offering. See the section titled “Use of Proceeds.” |

| We will not receive any of the proceeds from the sale of shares of our Class A Common Stock by the selling stockholder in this offering (including any sales pursuant to the underwriters’ option to purchase additional shares from the selling stockholder). |

| Dividend policy |

On August 9, 2022, our Board of Directors approved a quarterly cash dividend of $0.17 per share, or $0.68 per share on an annualized basis, to be paid to our shareholders. The quarterly dividend is payable on September 6, 2022 to shareholders of record as of the close of business on August 23, 2022. Future dividend payments will depend on our level of earnings, financial requirements and other factors and will be subject to approval by our board of directors, applicable law and the terms of our existing debt documents. Please see the section titled “Dividend Policy.” |

| Listing and trading symbol |

Shares of our Class A Common Stock trade on the NYSE under the symbol “CRGY.” |

| Risk factors |

You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our Class A Common Stock. |

14

Table of Contents

| Conflicts of interest |

Affiliates of KKR Capital Markets LLC own in excess of 10% of our issued and outstanding common stock. In addition, affiliates of Credit Suisse Securities (USA) LLC and Wells Fargo Securities, LLC are lenders under the Revolving Credit Facility and will each receive at least 5% of the net offering proceeds as a result of repayment of borrowings under the Revolving Credit Facility. See “Use of Proceeds.” Accordingly, this offering will be conducted in accordance with Rule 5121 of the Financial Industry Regulatory Authority (“FINRA”). Pursuant to that rule, the appointment of a “qualified independent underwriter” is not required in connection with this offering as a “bona fide public market,” as defined in paragraph (f)(3) of Rule 5121, exists for our Class A Common Stock. KKR Capital Markets LLC, Credit Suisse Securities (USA) LLC and Wells Fargo Securities, LLC will not confirm sales to any account over which they exercise discretionary authority without the specific written approval of the account holder. |

The number of shares of our Class A Common Stock to be outstanding after this offering is based on the number of shares of our Class A Common Stock outstanding as of June 30, 2022 and excludes 861,349 shares of Class A Common Stock reserved for issuance under our 2021 Equity Incentive Plan as of December 31, 2021, any shares of Class A Common Stock issuable under the 2021 Manager Incentive Plan, and any shares of Class A Common Stock issuable pursuant to the Management Agreement. See “Item 12. Security Ownership of Certain Beneficial Owner and Management and Related Stockholder Matters—Equity Compensation Plan Information” and “Items 1 and 2. Business and Properties—Management Agreement” in our Annual Report on Form 10-K for the year ended December 31, 2021 incorporated herein by reference for more information.

15

Table of Contents

Summary Historical Financial Data

The following table shows our summary historical financial data for each of the periods indicated. The summary historical financial data as of December 31, 2021 and 2020 and for the years ended December 31, 2021, 2020 and 2019 were derived from our audited combined and consolidated financial statements incorporated by reference herein. The summary historical financial data as of June 30, 2022 and for the six months ended June 30, 2022 and 2021, were derived from our unaudited condensed consolidated financial statements incorporated by reference herein. The summary pro forma financial data for the year ended December 31, 2021 and for the six months ended June 30, 2022 were derived from our unaudited pro forma condensed combined and consolidated financial statements incorporated by reference herein, which have been prepared from the respective historical consolidated financial statements of the Company for the six months ended June 30, 2022 and for the year ended December 31, 2021 and the statements of revenues and direct operating expenses of certain exploration and production assets acquired from the Uinta Acquisition for the period from January 1, 2022 through June 30, 2022 and for the year ended December 31, 2021. Pro forma financial data gives effect to the Transactions as if they had been consummated on January 1, 2021. See our Current Report on Form 8-K filed on April 8, 2022, our Current Report on Form 8-K/A filed on May 19, 2022, and our Current Report on Form 8-K filed on August 19, 2022, each incorporated by reference herein.

Neither our historical nor pro forma results are necessarily indicative of future operating results. The summary financial data presented below are qualified in their entirety by reference to, and should be read in conjunction with, “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included or incorporated by reference elsewhere in this prospectus, and the historical and pro forma financial statements and related notes incorporated by reference in this prospectus.

| Historical | Pro Forma | Historical | ||||||||||||||||||||||||||

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2021 | 2022 | 2022 | 2021 | ||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||

| Statement of operations data: |

||||||||||||||||||||||||||||

| Revenues and other operating income |

||||||||||||||||||||||||||||

| Oil |

$ | 883,087 | $ | 491,780 | $ | 785,750 | $ | 1,404,058 | $ | 1,107,236 | $ | 975,076 | $ | 405,743 | ||||||||||||||

| Natural gas |

354,298 | 149,317 | 173,386 | 588,716 | 366,152 | 350,488 | 143,492 | |||||||||||||||||||||

| Natural gas liquids |

185,530 | 69,902 | 86,473 | 235,600 | 155,043 | 155,043 | 74,291 | |||||||||||||||||||||

| Midstream and other |

54,062 | 43,222 | 41,631 |

|

69,421 |

|

26,737 | 26,737 | 24,464 | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total revenues |

1,476,977 | 754,221 | 1,087,240 | 2,297,795 | 1,655,168 | 1,507,344 | 647,990 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Expenses |

||||||||||||||||||||||||||||

| Lease operating expense |

243,501 | 202,180 | 255,106 | — | — | 201,198 | 117,628 | |||||||||||||||||||||

| Workover expense |

10,842 | 6,385 | 9,789 | — | — | 34,976 | 4,891 | |||||||||||||||||||||

| Asset operating expense |

45,940 | 39,023 | 40,364 | — | — | 33,862 | 13,496 | |||||||||||||||||||||

| Gathering, transportation and marketing |

187,059 | 173,122 | 142,214 | — | — | 86,514 | 91,422 | |||||||||||||||||||||

| Production and other taxes |

108,992 | 61,124 | 88,696 | — | — | 111,980 | 52,186 | |||||||||||||||||||||

| Operating expense |

— | — | — | 843,922 | 485,937 | — | — | |||||||||||||||||||||

| Depreciation, depletion, and amortization |

312,787 | 372,300 | 311,185 | 495,773 | 256,129 | 230,592 | 160,097 | |||||||||||||||||||||

| Impairment of oil and natural gas properties |

— | 247,215 | — | 761 | — | — | — | |||||||||||||||||||||

| Exploration expense |

1,180 | 486 | 469 | 1,661 | 1,939 | 1,939 | 79 | |||||||||||||||||||||

| Midstream operating expense |

13,389 | 9,472 | 9,968 | 15,355 | 6,422 | 6,422 | 6,330 | |||||||||||||||||||||

| General and administrative expense |

78,342 | 16,542 | 2,357 | 171,327 | 42,178 | 42,178 | 22,751 | |||||||||||||||||||||

| Gain on sale of assets |

(8,794 | ) | — | (22 | ) | (9,232 | ) | (4,987 | ) | (4,987 | ) | (9,417 | ) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total expenses |

993,238 | 1,127,849 | 860,126 | 1,519,567 | 787,618 | 744,674 | 459,463 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

16

Table of Contents

| Historical | Pro Forma | Historical | ||||||||||||||||||||||||||

| Year Ended December 31, | Six Months Ended June 30, | |||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2021 | 2022 | 2022 | 2021 | ||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||

| Income (loss) from |

483,739 | (373,628 | ) | 227,114 | 778,228 | 867,550 | 762,670 | 188,527 | ||||||||||||||||||||

| Other income (expense) |

||||||||||||||||||||||||||||

| Interest expense |

(50,740 | ) | (38,107 | ) | (53,577 | ) | (73,698 | ) | (41,461 | ) | (41,461 | ) | |

(24,826 |

) | |||||||||||||

| Gain (loss) on derivatives(1) |

(866,020 | ) | 195,284 | (127,202 | ) | (970,659 | ) | (850,695 | ) | (850,695 | ) | (602,810 | ) | |||||||||||||||

| Income (loss) from equity affiliates |

368 | — | — | (1,529 | ) | 3,252 | 3,252 | — | ||||||||||||||||||||

| Gain on extinguishment of debt |

— | — | — | 3,369 | — | — | — | |||||||||||||||||||||

| Other income (expense) |

120 | 341 | 402 | 5,926 | (1,802 | ) | (1,802 | ) | |

(6 |

) | |||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total other income (expense) |

(916,272 | ) | 157,518 | (180,377 | ) | (1,036,591 | ) | (890,706 | ) | (890,706 | ) | |

(627,642 |

) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income (loss) before income taxes |

(432,533 | ) | (216,110 | ) | 46,737 | (258,363 | ) | (23,156 | ) | (128,036 | ) | |

(439,115 |

) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Income tax benefit (expense) |

306 | (14 | ) | (28 | ) | 13,153 | (2,519 | ) | 3,927 | |

(14 |

) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income (loss) |

(432,227 | ) | (216,124 | ) | 46,709 | (245,210 | ) | (25,675 | ) | (124,109 | ) | |

(439,129 |

) | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Less: net (income) loss attributable to Predecessor |

339,168 | 118,649 | (45,839 | ) | — | — | — | 425,237 | ||||||||||||||||||||

| Less: net (income) loss attributable to noncontrolling interests(2) |

14,922 | 97,475 | (870 | ) | 3,570 | (1,183 | ) | (1,183 | ) | 13,892 | ||||||||||||||||||

| Less: net loss attributable to redeemable noncontrolling interests |

58,761 | — | — | 181,682 | 15,896 | 94,815 | — | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Net income (loss) attributable to Crescent Energy |

$ | (19,376 | ) | $ | — | $ | — | $ |

(59,958 |

) |

$ | (10,962 | ) | $ | (30,477 | ) | $ | — | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Balance sheet data (at period end): |

|

|||||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 128,578 | $ | 36,861 | $ | 19,894 | $ | 54,580 | ||||||||||||||||||||

| Property, plant and equipment, net |

4,555,113 | 3,642,147 | 3,773,539 | 5,462,964 | ||||||||||||||||||||||||

| Total assets |

5,157,462 | 3,907,369 | 3,997,520 | 6,273,672 | ||||||||||||||||||||||||

| Total debt |