As filed with the Securities and Exchange Commission on January 23, 2024

Registration No. 333-268184

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

TO

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

Delaware |

| 6770 |

| 86-2970927 |

|

(State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | |||

incorporation or organization) | Classification Code Number) | Identification No.) |

Digital Health Acquisition Corp.

980 N Federal Hwy #304

Boca Raton, FL 33432

Tel: (561) 672-7068

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Scott Wolf

Chief Executive Officer

Digital Health Acquisition Corp.

980 N Federal Hwy #304

Boca Raton, FL 33432

Tel: (561) 672-7068

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

Thomas Poletti, Esq. |

| Ali Panjwani, Esq. |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective and all other conditions to the transactions contemplated by the Business Combination Agreement described in the included proxy statement/prospectus/consent solicitation have been satisfied or waived.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934 (“Exchange Act”).

Large accelerated filer | ☐ | Accelerated filer | ☐ |

☒ | Smaller reporting company | ||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary proxy statement/prospectus/consent solicitation is not complete and may be changed. These securities may not be issued until the registration statement filed with the U.S. Securities and Exchange Commission is effective. The preliminary proxy statement/prospectus/consent solicitation is not an offer to sell these securities and does not constitute the solicitation of offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROXY STATEMENT/PROSPECTUS/CONSENT SOLICITATION SUBJECT TO COMPLETION, DATED JANUARY 23, 2024

PROPOSED MERGER

YOUR VOTE IS VERY IMPORTANT

Dear Stockholders:

You are cordially invited to attend the special meeting of the stockholders (the “Meeting”) of Digital Health Acquisition Corp. (“DHAC”), which will be held at 9:30 a.m., Eastern time, on [•], 2024. The Board of Directors has determined to convene and conduct the Meeting in a virtual meeting format at www.virtualshareholdermeeting.com/DHAC2024SM. Stockholders will NOT be able to attend the Meeting in-person. This proxy statement/prospectus/consent solicitation includes instructions on how to access the virtual Meeting and how to listen, vote, and submit questions from home or any remote location with Internet connectivity.

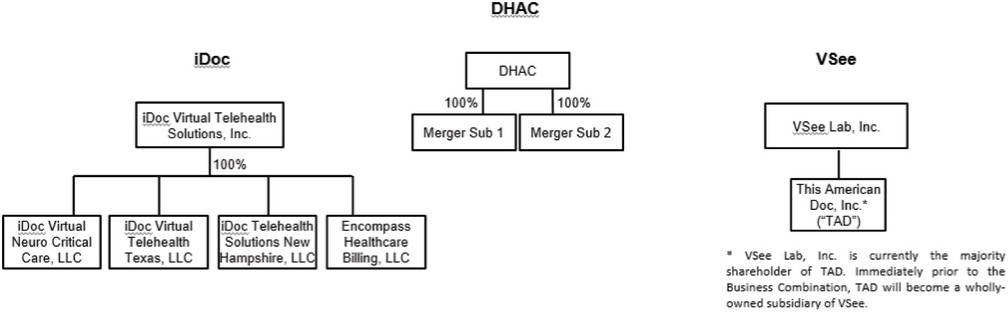

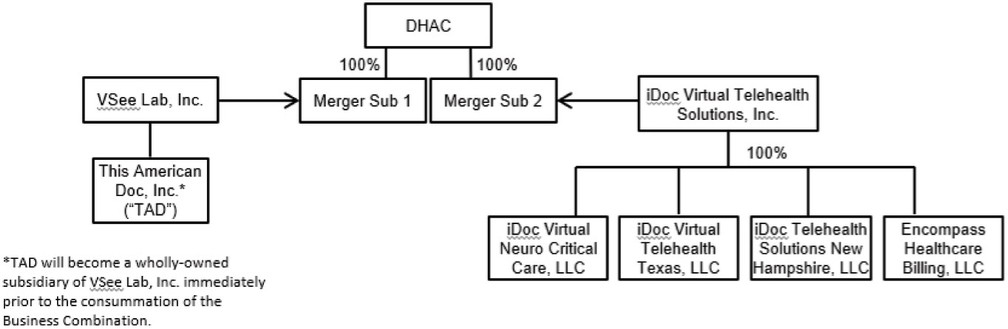

DHAC is a Delaware blank check company established for the purpose of entering into a merger, share exchange, asset acquisition, stock purchase, recapitalization, reorganization or other similar business transaction with one or more businesses or entities, which we refer to as a “target business.” Holders of DHAC common stock will be asked to approve, among other things, the Third Amended and Restated Business Combination Agreement, dated as of November 21, 2023 (the “Business Combination Agreement”), by and among DHAC, DHAC Merger Sub I, Inc., a Delaware corporation and wholly owned subsidiary of DHAC (“Merger Sub I”), DHAC Merger Sub II, Inc., a Texas corporation and wholly owned subsidiary of DHAC (“Merger Sub II”), VSee Lab, Inc., a Delaware corporation (“VSee”), and iDoc Virtual Telehealth Solutions, Inc., a Texas corporation (“iDoc”), and the other related proposals.

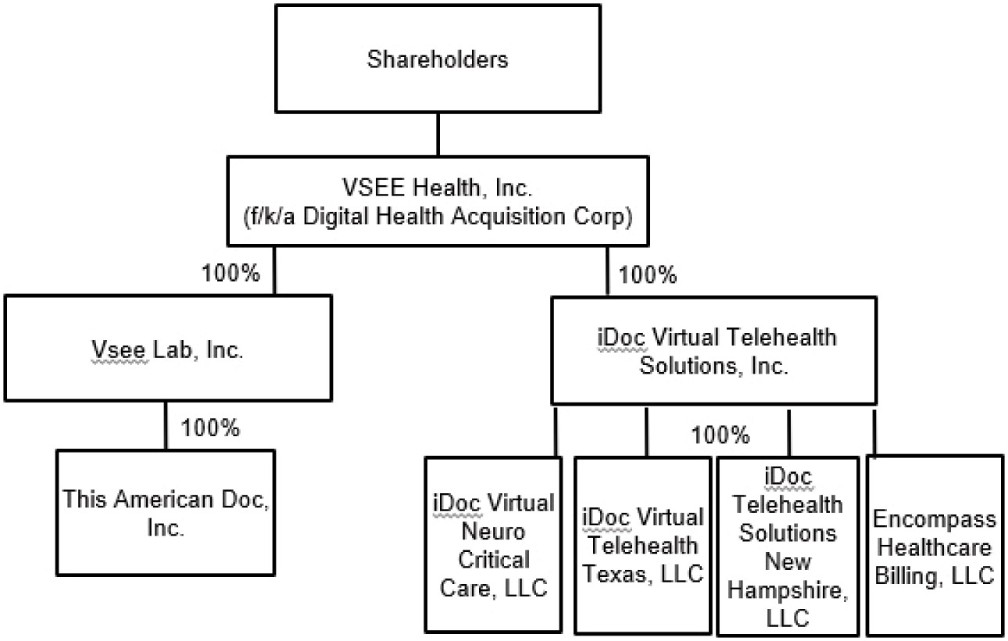

Upon the closing (the “Closing”) of the transactions contemplated in the Business Combination Agreement, Merger Sub I will merge with and into VSee (the “VSee Merger”), with VSee surviving the VSee merger as a wholly owned subsidiary of DHAC, and Merger Sub II will merge with and into iDoc (the “iDoc Merger” and, together with the VSee Merger, the “Mergers”), with iDoc surviving the iDoc Merger as a wholly owned subsidiary of DHAC. In addition, in connection with the consummation of the Business Combination, DHAC will be renamed “VSee Health, Inc.” The transactions contemplated under the Business Combination Agreement relating to the Business Combination are referred to in this proxy statement/prospectus/consent solicitation as the “Business Combination” and the combined company after the Business Combination is referred to in this proxy statement/prospectus/consent solicitation as the “Company” or the “Combined Company.” The closing and closing date of the Business Combination are referred to as the “Closing” and the “Closing Date,” respectively.

As a result of and upon the Closing, pursuant to the terms of the Business Combination Agreement, all of the outstanding capital stock of each of VSee and iDoc (excluding shares of the holders of which perfect rights of appraisal under Delaware and Texas law, as applicable) will be cancelled in exchange for the right to receive shares of DHAC common stock. The shares of DHAC common stock to be received by VSee and iDoc shareholders will be allocated pro rata, with each VSee and iDoc stockholder receiving a number of shares of DHAC common stock determined in accordance with the terms of the Business Combination Agreement and as described herein. All VSee options that are outstanding prior to the effective time of the merger will be terminated. At the Effective Time, DHAC will issue options exercisable for shares of DHAC common stock to certain VSee employees. The aggregate merger consideration that VSee stockholders (excluding certain lenders who will become stockholders of VSee immediately prior to the Effective Time as described herein) will receive is an amount equal to $60,500,000, less the value of the options granted to VSee employees at the Effective Time and VSee transaction expenses. The aggregate merger consideration that iDoc stockholders (excluding certain lenders who will become stockholders of iDoc immediately prior to the Effective Time as described herein) will receive is an amount equal to $49,500,000 less iDoc transaction expenses. The estimated net cash per share of DHAC common stock that is being contributed by DHAC to the Combined Company is less than the $10.00 per share ascribed to such shares in the Business Combination Agreement or the amount per share that holders of DHAC common stock would be entitled to receive upon exercise of their redemption rights, as described in the accompanying proxy statement/prospectus.

Concurrently with or prior to the execution of the Business Combination Agreement, DHAC, VSee and iDoc collectively or respectively entered into the following transactions as described further below.

Bridge Financing and Exchange

On October 5, 2022, DHAC, VSee and iDoc entered into a securities purchase agreement (the “Original Bridge SPA”) with Dominion Capital LLC (the “Bridge Investor”), who is also an investor in our Sponsor, pursuant to which DHAC, VSee and iDoc each issued and sold to such investor 10% original issue discount senior secured promissory notes due October 5, 2023 (collectively the “Bridge Notes” and individually, the “DHAC Bridge Notes,” “VSee Bridge Notes” and “iDoc Bridge Notes” when referring to Bridge Notes issued to DHAC, VSee, and iDoc, respectively) in the respective principal amount of $888,888.80, $666,666.60 and $666,666.60 for an aggregate principal amount of $2,222,222. The Bridge Notes bear guaranteed interest at a rate of 10.00% per annum and are convertible into shares of DHAC common stock under certain conditions described below. In connection with the purchase of the Bridge Notes, DHAC issued the investor (i) 173,913 warrants, each representing the right to purchase one share of DHAC common stock at an initial exercise price of $11.50, subject to certain adjustments (the “Bridge Warrants”) and (ii) 30,000 shares of DHAC common stock. In connection with the Original Bridge SPA, DHAC entered into a Registration Rights Agreement with the Bridge Investor, dated October 5, 2022, and as amended further on January 22, 2024 (the “Bridge RRA”), which provides that DHAC will file a registration statement to register the shares of Common Stock underlying the Bridge Notes, the Additional Bridge Notes (as defined below), and the Bridge Warrants and the 30,000 commitment shares. None of the shares underlying the Bridge Notes and the Additional Bridge Notes, the shares underlying the Bridge Warrants or the aforementioned 30,000 commitment shares are being registered pursuant to this Registration Statement.

On November 21, 2023, DHAC, VSee and iDoc entered into a letter agreement (the “Bridge Amendment” and together with the Original Bridge SPA, the “Bridge SPA”) amending the Original Bridge SPA, pursuant to which the Bridge Investor agreed to purchase additional 10% original issue discount senior secured convertible promissory notes in the aggregate principal amount of $166,667 (with an aggregate subscription amount of $150,000) from DHAC with (1) a $111,111.33 note purchased at signing of the Bridge Amendment, which will mature on May 21, 2025 and (2) a $55,555.67 note purchased at a later date mutually agreed upon by DHAC and the Bridge Investor, which is currently expected to be upon the filing of an amendment to DHAC’s Registration Statement on Form S-4 in connection with the Business Combination (the “Additional Bridge Notes”). The Additional Bridge Notes bear guaranteed interest at a rate of 8.00% per annum and are convertible into shares of DHAC common stock, par value $0.0001 at a fixed conversion price of $10 per share. The conversion price of the Additional Bridge Notes is subject to reset if DHAC’s common stock trades below $10.00 on the 10th business day after the conversion shares are registered or may otherwise be freely resold, and every 90th day thereafter, to a price equal to the greater of (x) 95% of the average lowest VWAP of the DHAC common stock in the 10 trading dates prior to the measurement date and (y) $2.00. In addition, optional prepayment of the Additional Bridge Notes requires the payment of 110% of the outstanding obligations, including the guaranteed minimum interest. If an event of default occurs, the Additional Bridge Notes would bear interest at a rate of 24.00% per annum and require the payment of 125% of the outstanding obligations, including the guaranteed minimum interest.

On November 21, 2023, DHAC, VSee and iDoc entered into an exchange agreement (the “Exchange Agreement”) with the Bridge Investor, pursuant to which the amounts currently due and owning under (i) the DHAC Bridge Note, (ii) the VSee Bridge Note other than $600,000 of the principal amount thereof, and (iii) the iDoc Bridge Note other than $600,000 of the principal amount thereof, will be exchanged at the Closing for a senior secured convertible promissory note issued by DHAC with an aggregate principle value of $2,523,744.29 (the “Exchange Note”), which will be guaranteed by each of DHAC, VSee and iDoc. The Exchange Note will bear interest at a rate of 8.00% per annum and will be convertible into shares of common stock of the Combined Company at a fixed conversion price of $10 per share. The conversion price of the Exchange Note is subject to reset if DHAC’s common stock trades below $10.00 on the 10th business day after the conversion shares are registered or may otherwise be freely resold, and every 90th day thereafter, to a price equal to the greater of (x) 95% of the average lowest VWAP of DHAC’s common stock in the 10th trading dates prior to the measurement date and (y) $2.00. In addition, optional prepayment of the Exchange Note requires the payment of 110% of the outstanding obligations. If an event of default occurs, the Exchange Note would bear interest at a rate of 24.00% per annum and require the payment of 125% of the outstanding obligations. The transactions contemplated by the Bridge SPA and the Exchange Agreement are referred to as the “Bridge Financing.”

Pursuant to the Exchange Agreement, DHAC will enter into a registration rights agreement at the Closing, pursuant to which it will agree to register (i) the shares of DHAC common stock underlying the Exchange Note; (ii) the shares of DHAC common stock issuable as interest or principal on the Exchange Note; (iii) the shares of DHAC common stock issuable pursuant to any anti-dilution or any remedies provisions of the Exchange Note; and (iv) any securities issued or then issuable upon any stock split, dividend or other distribution, recapitalization or similar event.

In connection with Exchange Agreement, the sponsor of DHAC and certain directors and officers of DHAC will enter into a lock-up agreement in a form under the Exchange Agreement at the Closing, pursuant to which each will agree, from the date of the lock-up agreement until the 180 days after the Closing, subject to certain customary exceptions, to not offer, sell, contract to sell, hypothecate, pledge or otherwise dispose of, or establish or increase a put equivalent position or liquidate or decrease a call equivalent position within the meaning of Section 16 of the Securities Exchange Act of 1934, as amended with respect to any shares of DHAC common stock or securities convertible, exchangeable or exercisable into, shares of DHAC common stock beneficially owned, held or hereafter acquired by the person signing the lock-up agreement.

Quantum Financing

On November 21, 2023, DHAC entered into a convertible note purchase agreement (the “Quantum Purchase Agreement”), pursuant to which an institutional and accredited investor (the “Quantum Investor”) subscribed for and will purchase, and DHAC will issue and sell to the Quantum Investor, at the Closing, a 7% original issue discount convertible promissory note (the “Quantum Note”) in the aggregate principal amount of $3,000,000 (the “Quantum Financing”). The Quantum Note will bear interest at rate of 12% per annum and are convertible into shares of Common Stock of DHAC at (1) a fixed conversion price of $10 per share; or (2) 85% of the lowest daily VWAP (as defined in the Quantum Note) during the seven (7) consecutive trading days immediately preceding the date of conversion or other date of determination. The conversion price of the Quantum Note is subject to reset if the average of the daily VWAPs for the three (3) trading days prior to the 30th-day anniversary of the Quantum Note issuance date (the “Average Price”) is less than $10, to a price equal to the Average Price but in no event less than $2. In addition, the Company at its option can redeem early a portion or all amounts outstanding under the Quantum Note if the Company provides the Quantum Note holder a notice at least ten (10) trading days prior to such redemption and on the notice day the VWAP of the Company’s Common Stock is less than $10. If an event of default occurs, the Quantum Note would bear interest at a rate of 18.00% per annum. Concurrently with the consummation of the transactions contemplated by the Quantum Purchase Agreement, the Company will enter into a registration rights agreement pursuant to which it will agree to register the shares of DHAC common stock underlying the Quantum Note.

The Quantum Investor is a Delaware LLC that is owned 33% by SCS Capital Partners, an entity owned by Lawrence Sands who is a beneficial owner of founder shares and the manager of our Sponsor, 33% by the Bridge Investor and 33% by M2B Funding Corp. This financial interest of SCS Capital Partners may mean that the Sponsor may be incentivized to complete the Business Combination with a less favorable target company or on terms less favorable to stockholders than they would otherwise recommend or approve, as the case may be, rather than allow DHAC to wind up having failed to consummate a business combination and lose the Sponsor’s entire investment.

A.G.P. Financing

DHAC executed a Securities Purchase Agreement with A.G.P./Alliance Global Partners (“A.G.P.”) on November 3, 2022 and as amended on November 21, 2023 (the “A.G.P. Securities Purchase Agreement”)whereby A.G.P. subscribed for and will purchase, and DHAC will issue and sell, at the closing of the Business Combination, 4,370 shares (“A.G.P. Series A Shares”) of Series A Preferred Stock, par value $0.0001 per share, of the Combined Company (the “Series A Preferred Stock”) at a per share price of $1,000 (the “A.G.P. Financing”). A.G.P. will not receive deferred underwriting commissions of $4,370,000 which it has agreed to take as the A.G.P. Series A Shares. The Series A Preferred Stock is convertible at any time on or after the earlier of (i) 12 months from the date of issuance of the shares of Series A Preferred Stock and (ii) the date on which no shares of Series A Preferred Stock remain outstanding. The initial conversion price of the Series A Preferred Stock of $10 is subject to reset to an “Alternate Conversion Price,” which means the lowest of (i) the applicable conversion price as in effect on the applicable conversion date, and (ii) the greater of (x) $10.00 (or (i) $5.00, after the later of (x) 90 days after issuance of the shares of Series A Preferred Stock or (y) the earlier of the date the shares underlying the shares of Series A Preferred Stock are eligible to be resold pursuant to Rule 144 or the date a resale registration statement is declared effective, or (ii) $2.00, after the earlier of (x) the date the VWAP of the Combined Company common stock trades at less than $5.00 for 10 consecutive trading days and (y) the first anniversary of issuance) and (y) 90% of the price computed as the quotient of (I) the sum of the VWAP of the Common Stock for each of the three (3) trading days with the lowest VWAP of the Common Stock during the ten (10) consecutive trading day period ending and including the trading day immediately preceding the delivery or deemed delivery of the applicable conversion notice, divided by three (3), as appropriately adjusted for any stock dividend, stock split, stock combination, reclassification or similar transaction. Therefore, the A.G.P. Series A Shares would convert into an aggregate of (i) 437,000 shares of Combined Company common stock assuming a $10.00 conversion price and a common stock equivalent per share price of $10.00, (ii) 874,000 shares of Combined Company common stock assuming a $5.00 conversion price and a common stock equivalent per share price of $5.00 and (iii) 2,185,000 shares of Combined Company common stock assuming a $2.00 conversion price and a common stock equivalent per share price of $2.00.

Loan Conversions

On November 21, 2023, DHAC, VSee, and/or iDoc, as applicable, entered into various securities purchase agreements (the “Conversion SPAs”) with various lenders of each of DHAC, VSee and iDoc, which include the Bridge Investor, pursuant to which (1) certain indebtedness owed by DHAC will be converted into Series A Preferred Stock at the Closing; (2) certain indebtedness owed by VSee will be converted into Series A Preferred Stock of the Combined Company at the Closing; (3) certain indebtedness owed by iDoc will be converted into Series A Preferred Stock of the Combined Company at the Closing (the shares of Series A Preferred Stock to be issued in consideration of the loan conversions described in the foregoing clauses (1) – (3) are referred to as the “Loan Conversion Series A Shares” and together with the A.G.P. Series A Shares, the “Series A Shares”); (4) the $600,000 balance of the VSee Bridge Note not included in the Exchange Note will be converted into class B common stock of VSee immediately prior to the Closing, which will then be exchanged for Combined Company common stock at the Closing; and (5) the $600,000 balance of the iDoc Bridge Note not included in the Exchange Note and certain indebtedness owned by iDoc will be converted into class B common stock of iDoc immediately prior to the Closing, which will then be exchanged for Combined Company common stock at the Closing (the shares of Combined Company common stock to be issued in consideration of the loan conversions described in the foregoing clauses (4) – (5) are referred to as the “Loan Conversion Common Shares” and all of the foregoing transactions, the “Loan Conversions”).

The Loan Conversion Series A Shares would convert into an aggregate of (i) 178,800 shares of Combined Company common stock assuming a $10.00 conversion price and a common stock equivalent per share price of $10.00, (ii) 357,600 shares of Combined Company common stock assuming a $5.00 conversion price and a common stock equivalent per share price of $5.00 and (iii) 894,000 shares of Combined Company common stock assuming a $2.00 conversion price and a common stock equivalent per share price of $2.00. The Loan Conversion Common Shares would convert into an aggregate of 600,000 shares of Combined Company common stock.

Equity Financing

On November 21, 2023, DHAC entered into an equity purchase agreement (the “Equity Purchase Agreement”) with the Bridge Investor pursuant to which DHAC may sell and issue to the Bridge Investor, and the Bridge Investor is obligated to purchase from DHAC, up to $50,000,000 of its newly issued shares of the Combined Company’s common stock, from time to time over a 36-month period (the “Equity Purchase Commitment Period”) beginning from the sixth (6th) trading day following the Closing (the “Equity Purchase Effective Day”), provided that certain conditions are met. DHAC also agreed to file a resale registration statement to register shares of common stock to be purchased under the Equity Purchase Agreement with the SEC within 45 days following the Equity Purchase Effective Day, and shall use commercially reasonable efforts to have such registration statement declared effective by the SEC within 30 days of such filing. On the Equity Purchase Effective Day, the Combined Company will issue to the Bridge Investor, as a commitment fee, a senior unsecured convertible note in a principal amount of $500,000 that is convertible into shares of the Combined Company’s common stock at a fixed conversion price of $10 per share (the “Equity Purchase Note” and together with the Additional Bridge Notes and the Exchange Note, the “Bridge Investor Notes”). The Bridge Investor Notes and the Quantum Note are referred to herein as the “Convertible Notes.”

On October 20, 2022, stockholders of DHAC approved a proposal to amend DHAC’s amended and restated certificate of incorporation to, among other things, extend the date by which DHAC has to consummate a business combination through November 8, 2023 in accordance with the terms described by DHAC’s amendment to amended and restated certificate of incorporation dated October 26, 2022. In connection with the related stockholder vote, an aggregate of 10,805,877 shares of DHAC’s common stock were redeemed. On September 8, 2023, stockholders of DHAC approved an additional amendment to DHAC’s amended and restated certificate of incorporation to expand the methods that the Company may employ to not become subject to the “penny stock” rules of the SEC. On November 6, 2023, at DHAC’s annual stockholder meeting, the stockholders of DHAC approved another proposal to amend DHAC’s amended and restated certificate of incorporation to (a) extend the date by which DHAC must consummate a Business Combination up to four (4) times, each by an additional three (3) months, for an aggregate of twelve (12) additional months (i.e., from November 8, 2023 up to November 8, 2024) or such earlier date as determined by the DHAC board of directors; and (b) permit stockholders to act by written consent in compliance with Section 228 of the Delaware General Corporation Law in lieu of a meeting. In connection with such stockholder vote, an aggregate of 579,157 shares of DHAC’s common stock were redeemed. The current term of DHAC has been extended to February 8, 2024.

The below charts set forth the Combined Company’s ownership and voting power percentages following the Closing, assuming that (i) no indemnity claims or expenses are deducted from VSee’s or iDoc’s merger consideration at or after closing, (ii) all Series A Shares and Convertible Notes are converted at the described conversion prices, (iii) no warrants or options of the Combined Company

are exercised and (iv) no shares are issued pursuant to the Equity Purchase Agreement (other than pursuant to assumed conversion of the Equity Purchase Note). If the actual facts are different from these assumptions (which they are likely to be), the percentage ownership retained by the below stockholder groups will be different.

Assuming no further redemptions by the DHAC Public Stockholders and a $10.00 conversion price of each of the Series A Shares and the Convertible Notes:

Sponsor (1)(3) |

| 2,665,250 |

| 16.8 | % |

Sponsor Affiliates (1)(2) | 936,300 | 5.9 | % | ||

Current Management, Board and Advisors | 301,750 | 1.9 | % | ||

Public Stockholders whose shares are subject to redemption | 114,966 | 0.7 | % | ||

VSee | 5,191,142 | 32.7 | % | ||

iDoc | 4,950,000 | 31.2 | % | ||

AGP | 437,000 | 2.8 | % | ||

Bridge Investor (3) | 950,375 | 6.0 | % | ||

Quantum Investor (2)(3) | 300,000 | 1.9 | % | ||

Other Stockholders | 27,000 | 0.2 | % |

(1) | Marc Munro, through his ownership of Tidewater and Whacky, beneficially owns 66.35% of the Sponsor and will beneficially own 344,500 shares of Common Stock held by Sponsor Affiliates, consisting of 292,500 shares of Common Stock and 520 shares of Series A Preferred Stock to be received upon conversion of notes held by such entities controlled by him. |

(2) | Lawrence Sands, through his ownership of SCS and SCS Capital Partners beneficially owns 500,000 founder shares and 33% of the Quantum Investor, and will beneficially own 591,800 shares of Common Stock held by Sponsor Affiliates, consisting of 500,000 founder shares and 918 shares of Series A Preferred Stock to be received upon conversion of notes held by such entities controlled by him. |

(3) | The Bridge Investor owns 4.91% of the Sponsor and 33% of the Quantum Investor. |

Assuming no further redemptions by the DHAC Public Stockholders and a $2.00 conversion price of each of the Series A Shares and the Convertible Notes:

Sponsor (1)(3) |

| 2,805,250 |

| 13.5 | % |

Sponsor Affiliates (1)(2) | 1,511,500 | 7.3 | % | ||

Current Management, Board and Advisors | 301,750 | 1.4 | % | ||

Public Stockholders whose shares are subject to redemption | 114,966 | 0.6 | % | ||

VSee | 5,191,142 | 24.9 | % | ||

iDoc | 4,950,000 | 23.8 | % | ||

AGP | 2,185,000 | 10.5 | % | ||

Bridge Investor (3) | 2,231,872 | 10.7 | % | ||

Quantum Investor (2)(3) | 1,500,000 | 7.2 | % | ||

Other Stockholders | 27,000 | 0.1 | % |

(1) | Marc Munro, through his ownership of Tidewater and Whacky, beneficially owns 66.35% of the Sponsor and will beneficially own 344,500 shares of Common Stock held by Sponsor Affiliates, consisting of 292,500 shares of Common Stock and 520 shares of Series A Preferred Stock to be received upon conversion of notes held by such entities controlled by him. |

(2) | Lawrence Sands, through his ownership of SCS and SCS Capital Partners beneficially owns 500,000 founder shares and 33% of the Quantum Investor, and will beneficially own 591,800 shares of Common Stock held by Sponsor Affiliates, consisting of 500,000 founder shares and 918 shares of Series A Preferred Stock to be received upon conversion of notes held by such entities controlled by him. |

(3) | The Bridge Investor owns 4.91% of the Sponsor and 33% of the Quantum Investor. |

As of January 19, 2024, there was approximately $1.37 million in DHAC’s trust account (the “Trust Account”). On [●], 2024, the record date for the Meeting of stockholders, the last sale price of DHAC’s Common Stock was $[●] per share.

Each stockholder’s vote is very important. Whether or not you plan to participate in the virtual Meeting, please submit your proxy card without delay. Stockholders may revoke proxies at any time before they are voted at the meeting. Voting by proxy will not prevent a stockholder from voting virtually at the Meeting if such stockholder subsequently chooses to participate in the Meeting.

DHAC’s units, Common Stock, and Warrants are currently listed on the Nasdaq Stock Market, under the symbols “DHACU,” “DHAC,” and “DHACW,” respectively. DHAC has applied for listing, to be effective upon consummation of the Business Combination, of VSee Health, Inc.’s Common Stock and Public Warrants to purchase VSee Health, Inc.’s Common Stock on Nasdaq under the proposed symbols “ VSEE” and “VSEEW,” respectively. The Nasdaq listing requirement is a condition to the closing of the Business Combination and neither DHAC, VSee or iDoc will proceed forward with the closing of the Business Combination unless Nasdaq approves the listing.

We encourage you to read this proxy statement/prospectus/consent solicitation carefully. In particular, you should review the matters discussed under the caption “Risk Factors” beginning on page 74.

DHAC’s board of directors recommends that DHAC stockholders vote “FOR” approval of each of the Proposals.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the Business Combination or otherwise, or passed upon the adequacy or accuracy of this proxy statement. Any representation to the contrary is a criminal offense.

This proxy statement/prospectus/consent solicitation is dated [•], 2024, and is first being mailed to stockholders of DHAC on or about [•], 2024.

/s/ Scott Wolf |

|

Scott Wolf |

|

Chief Executive Officer |

|

Digital Health Acquisition Corp. |

|

[·], 2024 |

|

DIGITAL HEALTH ACQUISITION CORP.

980 N Federal Hwy #304

Boca Raton, FL

Telephone: (561) 672-7068

NOTICE OF SPECIAL MEETING OF

DIGITAL HEALTH ACQUISITION CORP. STOCKHOLDERS

To Be Held on [·], 2024

To Digital Health Acquisition Corp. Stockholders:

NOTICE IS HEREBY GIVEN, that you are cordially invited to attend a meeting of the stockholders of Digital Health Acquisition Corp. (“DHAC,” “we”, “our”, or “us”), which will be held at 9:30 a.m., Eastern time, on [·], 2024, at (the “Meeting”). We will hold the Meeting online by remote communication, in virtual only format. You can participate in the virtual Meeting as described in “The Meeting.”

During the Meeting, DHAC’s stockholders will be asked to consider and vote upon the following proposals, which we refer to herein as the “Proposals”:

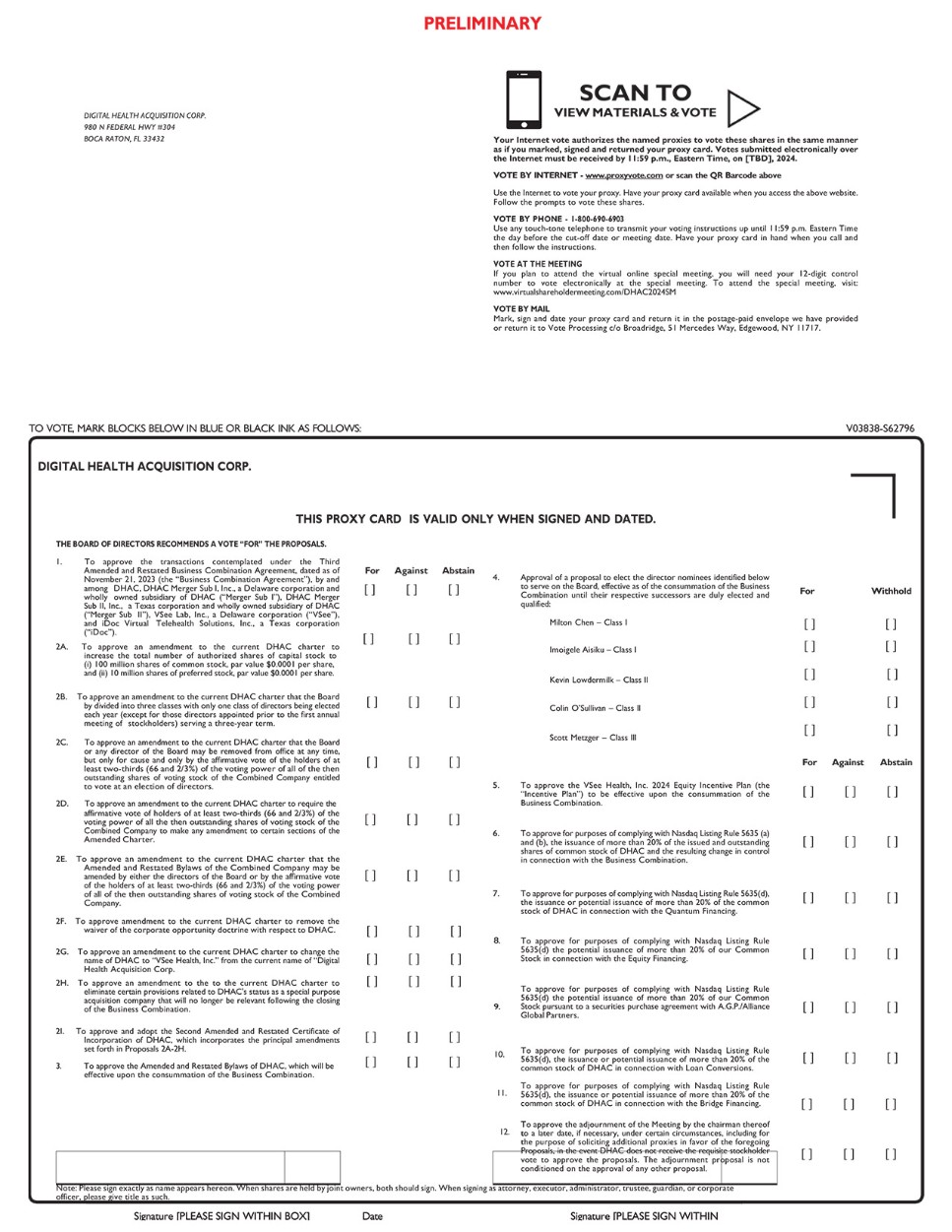

1. | Proposal No. 1 — The Business Combination Proposal — to consider and vote upon a proposal to approve the transactions (the “Business Combination”) contemplated under the Third Amended and Restated Business Combination Agreement, dated as of November 21, 2023 (the “Business Combination Agreement”), by and among DHAC, DHAC Merger Sub I, Inc., a Delaware corporation and wholly owned subsidiary of DHAC (“Merger Sub I”), DHAC Merger Sub II, Inc., a Texas corporation and wholly owned subsidiary of DHAC (“Merger Sub II”), VSee Lab, Inc., a Delaware corporation (“VSee”), and iDoc Virtual Telehealth Solutions, Inc., a Texas corporation (“iDoc”), a copy of which is attached to this proxy statement/prospectus/consent solicitation as Annex A. This Proposal is referred to as the “Business Combination Proposal” or “Proposal 1.” |

2. | Proposals No. 2A-2I — The Charter Amendment Proposals |

| ● | Proposal 2A — To consider and vote on an amendment to the Current Charter to increase the total number of authorized shares of capital stock to (i) 100 million shares of common stock, par value $0.0001 per share, and (ii) 10 million shares of preferred stock, par value $0.0001 per share. |

| ● | Proposal 2B — To consider and vote on an amendment to the Current Charter that the Board by divided into three classes with only one class of directors being elected each year (except for those directors appointed prior to the first annual meeting of stockholders) serving a three- year term. |

| ● | Proposal 2C — To consider and vote on an amendment to the Current Charter that the Board or any director of the Board may be removed from office at any time, but only for cause and only by the affirmative vote of the holders of at least two-thirds (66 and 2/3%) of the voting power of all of the then outstanding shares of voting stock of the Combined Company entitled to vote at an election of directors. |

| ● | Proposal 2D — To consider and vote on an amendment to the Current Charter to require the affirmative vote of holders of at least two-thirds (66 and 2/3%) of the voting power of all the then outstanding shares of voting stock of the Combined Company to make any amendment to certain sections of the Amended Charter. |

| ● | Proposal 2E — To consider and vote on an amendment to the Current Charter that the Amended and Restated Bylaws of the Combined Company may be amended by either the directors of the Board or by the affirmative vote of the holders of at least two-thirds (66 and 2/3%) of the voting power of all of the then outstanding shares of voting stock of the Combined Company. |

| ● | Proposal 2F — To consider and vote on an amendment to the Current Charter to remove the waiver of the corporate opportunity doctrine with respect to DHAC. |

| ● | Proposal 2G — To consider and vote on an amendment to the Current Charter to change the name of DHAC to “VSee Health, Inc.” from the current name of “Digital Health Acquisition Corp.” |

| ● | Proposal 2H — To consider and vote on an amendment to the Current Charter to eliminate certain provisions related to DHAC’s status as a special purpose acquisition company that will no longer be relevant following the closing of the Business Combination. |

| ● | Proposal 2I — To consider and vote upon the approval and adoption of the Second Amended and Restated Certificate of Incorporation of DHAC, a copy of which is attached to this proxy statement/prospectus/consent solicitation as Annex B-1 (the “Amended Charter”), which incorporates the principal amendments set forth in Proposals 2A-2H. Proposals 2A-2I are collectively referred to as the “Charter Amendment Proposals.” |

3. | Proposal No. 3 — The Bylaws Proposal — to consider and vote upon a proposal to approve the Amended and Restated Bylaws of DHAC, a copy of which is attached to this proxy statement/prospectus/consent solicitation as Annex C (the “Amended Bylaws”), which will be effective upon the consummation of the Business Combination. This Proposal is referred to as the “Bylaws Proposal” or “Proposal 3.” |

4. | Proposal No. 4 — The Directors Proposal — to consider and vote upon a proposal to elect, effective as of the consummation of the Business Combination, Milton Chen, Imoigele Aisiku, Kevin Lowdermilk, Colin O’Sullivan and Scott Metzger, to serve on the Board until their respective successors are duly elected and qualified. This Proposal is referred to as the “Directors Proposal” or “Proposal 4.” |

5. | Proposal No. 5 — The Stock Plan Proposal - to consider and vote upon a proposal to approve the VSee Health, Inc. 2024 Equity Incentive Plan (the “Incentive Plan”), a copy of which is to be attached to this proxy statement/prospectus/consent solicitation as Annex D, to be effective upon the consummation of the Business Combination. This Proposal is referred to as the “Stock Plan Proposal” or “Proposal 5.” |

6. | Proposal No. 6 — The Nasdaq Merger Proposal — to consider and vote upon a proposal to approve: for purposes of complying with Nasdaq Listing Rule 5635 (a) and (b), the issuance of more than 20% of the issued and outstanding shares of common stock of DHAC and the resulting change in control in connection with the Business Combination. This Proposal is referred to as the “Nasdaq Merger Proposal” or “Proposal 6.” |

7. | Proposal No. 7 — The Nasdaq Quantum Financing Proposal — to consider and vote upon a proposal to approve for purposes of complying with Nasdaq Listing Rule 5635(d), the issuance or potential issuance of more than 20% of the issued and outstanding shares of common stock of DHAC in connection with the Quantum Financing. This Proposal is referred to as the “Nasdaq Quantum Financing Proposal” or “Proposal 7.” |

8. | Proposal No. 8 — The Nasdaq Equity Financing Proposal — to consider and vote upon a proposal to approve for purposes of complying with Nasdaq Listing Rule 5635(d) the potential issuance of more than 20% of the issued and outstanding shares of common stock of DHAC in connection with the Equity Financing. This Proposal is referred to as the “Nasdaq Equity Financing Proposal” or “Proposal 8.” |

9. | Proposal No. 9 — The Nasdaq A.G.P. Financing Proposal — to consider and vote upon a proposal to approve for purposes of complying with Nasdaq Listing Rule 5635(d) the potential issuance of more than 20% of our Common Stock pursuant to a securities purchase agreement with A.G.P./Alliance Global Partners. This Proposal is referred to as the “Nasdaq A.G.P. Financing Proposal” or “Proposal 9.” |

10. | Proposal No. 10 — The Nasdaq Loan Conversion Proposal — to consider and vote upon a proposal to approve for purposes of complying with Nasdaq Listing Rule 5635(d), the issuance or potential issuance of more than 20% of the common stock of DHAC in connection with Loan Conversions. This Proposal is referred to as the “Nasdaq Loan Conversion Proposal” or “Proposal 10”. |

11. | Proposal No. 11 — The Nasdaq Bridge Financing Proposal — to consider and vote upon a proposal to approve for purposes of complying with Nasdaq Listing Rule 5635(d), the issuance or potential issuance of more than 20% of the |

common stock of DHAC in connection with the Bridge Financing. This Proposal is referred to as the “Nasdaq Bridge Financing Proposal” or “Proposal 11”.

12. | Proposal No. 12 — The Adjournment Proposal — to consider and vote upon a proposal to approve the adjournment of the Meeting by the chairman thereof to a later date, if necessary, under certain circumstances, including for the purpose of soliciting additional proxies in favor of the foregoing Proposals, in the event DHAC does not receive the requisite stockholder vote to approve the Proposals. This Proposal is called the “Adjournment Proposal” or “Proposal 12.” |

The Business Combination Proposal is conditioned upon the approval of Proposals 2A-2I, 3, 5, 6, 7, 8, 9, 10 and 11. Proposals 2A-2I, 3, 4, 5, 6, 7, 8, 9, 10 and 11 are dependent upon approval of the Business Combination Proposal. It is important for you to note that in the event that the Business Combination Proposal is not approved, DHAC will not consummate the Business Combination. If DHAC does not consummate the Business Combination and fails to complete an initial business combination by February 8, 2024 (or a later time upon the election by DHAC to extend the time period to complete an initial business combination subject to satisfaction of certain conditions under our Current Charter), DHAC will be required to dissolve and liquidate, unless we seek stockholder approval to amend our Current Charter to extend the date by which the Business Combination may be consummated.

Approval of the Business Combination Proposal, the Charter Amendment Proposals, the Bylaws Proposal, the Directors Proposal, the Stock Plan Proposal, the Nasdaq Merger Proposal, the Nasdaq Quantum Financing Proposal, the Nasdaq Equity Financing Proposal, the Nasdaq A.G.P. Financing Proposal, the Nasdaq Loan Conversion Proposal, the Nasdaq Bridge Financing Proposal and the Adjournment Proposal will each require the affirmative vote of the holders of a majority of the issued and outstanding shares of common stock of DHAC present in person by virtual attendance or represented by proxy and entitled to vote at the Meeting or any adjournment thereof.

On November 6, 2023, at DHAC’s annual stockholder meeting, the stockholders of DHAC approved a proposal to amend DHAC’s amended and restated certificate of incorporation to (a) extend the date by which DHAC must consummate a Business Combination up to four (4) times, each by an additional three (3) months, for an aggregate of twelve (12) additional months (i.e., from November 8, 2023 up to November 8, 2024) or such earlier date as determined by the DHAC board of directors; and (b) permit stockholders to act by written consent in compliance with Section 228 of the Delaware General Corporation Law in lieu of a meeting. In connection with such stockholder vote, an aggregate of 579,157 shares of DHAC’s common stock were redeemed leaving 3,603,966 shares issued and outstanding and entitled to vote as November 7, 2023. As of January 19, 2024, there are 3,603,966 shares of DHAC common stock issued and outstanding and entitled to vote. The current term of DHAC has been extended to February 8, 2024.

DHAC is requiring stockholders who wish to redeem their Shares to either tender their certificates to Continental or to deliver their Shares to Continental electronically using the DTC’s DWAC (Deposit/ Withdrawal At Custodian) System at least two business days before the DHAC Special Meeting. In order to obtain a physical certificate, a stockholder’s broker and/or clearing broker, DTC and Continental will need to act to facilitate this request. It is DHAC’s understanding that stockholders should generally allot at least two weeks to obtain physical certificates from Continental. However, because DHAC does not have any control over this process or over the brokers or DTC, it may take significantly longer than two weeks to obtain a physical certificate. While DHAC has been advised that it takes a short time to deliver Shares through the DWAC System, DHAC cannot assure you of this fact. Accordingly, if it takes longer than DHAC anticipates for stockholders to deliver their Shares, stockholders who wish to redeem may be unable to meet the deadline for exercising their redemption rights and thus may be unable to redeem their Shares; this requirement may limit stockholders being afforded meaningful redemption rights.

The redemption rights include the requirement that a stockholder must identify itself in writing as a beneficial holder and provide its legal name, phone number, and address in order to validly redeem its public shares.

Only DHAC stockholders who hold common stock of record as of the close of business on [●], 2024 are entitled to vote at the Meeting or any adjournment of the Meeting. This proxy statement/prospectus/consent solicitation is first being mailed to DHAC stockholders on or about [●], 2024.

Investing in DHAC’s securities involves a high degree of risk. See “Risk Factors” beginning on page 74 for a discussion of information that should be considered in connection with an investment in DHAC’s securities.

YOUR VOTE IS VERY IMPORTANT. PLEASE VOTE YOUR SHARES PROMPTLY.

Whether or not you plan to participate in the virtual Meeting, please complete, date, sign and return the enclosed proxy card without delay, or submit your proxy through the internet or by telephone as promptly as possible in order to ensure your representation at the Meeting no later than the time appointed for the Meeting or adjourned meeting. Voting by proxy will not prevent you from voting your shares of common stock online if you subsequently choose to participate in the virtual Meeting. Please note, however, that if your shares are held of record by a broker, bank or other agent and you wish to vote at the Meeting, you must obtain a proxy issued in your name from that record. Only stockholders of record at the close of business on the record date may vote at the Meeting or any adjournment or postponement thereof. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not participate in the virtual Meeting, your shares will not be counted for purposes of determining whether a quorum is present at, and the number of votes voted at, the Meeting.

You may revoke a proxy at any time before it is voted at the Meeting by executing and returning a proxy card dated later than the previous one, by participating in the virtual Meeting and casting your vote by hand or by ballot (as applicable) or by submitting a written revocation to Broadridge Financial Solutions (“Broadridge”), that is received by the tabulator before we take the vote at the Meeting. If you hold your shares through a bank or brokerage firm, you should follow the instructions of your bank or brokerage firm regarding revocation of proxies.

DHAC’s board of directors recommends that DHAC stockholders vote “FOR” approval of each of the Proposals. When you consider DHAC’s Board of Director’s recommendation of these Proposals, you should keep in mind that DHAC’s directors and officers have interests in the Business Combination that may conflict or differ from your interests as a stockholder. See the section titled “Proposal 1: The Business Combination — Interests of Certain Persons in the Business Combination.”

On behalf of the DHAC Board of Directors, I thank you for your support and we look forward to the successful consummation of the Business Combination.

By Order of the Board of Directors, | |

/s/ Scott Wolf | |

Scott Wolf | |

Chief Executive Officer | |

Digital Health Acquisition Corp. | |

[●], 2024 |

IF YOU RETURN YOUR PROXY CARD WITHOUT AN INDICATION OF HOW YOU WISH TO VOTE, YOUR SHARES WILL BE VOTED IN FAVOR OF EACH OF THE PROPOSALS.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST (I) IF YOU: (A) HOLD PUBLIC SHARES, OR (B) HOLD PUBLIC SHARES THROUGH PUBLIC UNITS AND YOU ELECT TO SEPARATE YOUR PUBLIC UNITS INTO THE UNDERLYING PUBLIC SHARES PRIOR TO EXERCISING YOUR REDEMPTION RIGHTS WITH RESPECT TO THE PUBLIC SHARES; AND (II) PRIOR TO [·] A.M./P.M., EASTERN TIME, ON [·], 2024, (A) SUBMIT A WRITTEN REQUEST TO CONTINENTAL STOCK TRANSFER & TRUST COMPANY THAT DHAC REDEEM YOUR PUBLIC SHARES FOR CASH AND (B) DELIVER YOUR PUBLIC SHARES TO CONTINENTAL STOCK TRANSFER & TRUST COMPANY, PHYSICALLY OR ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM, IN EACH CASE, IN ACCORDANCE WITH THE PROCEDURES DESCRIBED IN THE PROXY STATEMENT/PROSPECTUS/CONSENT SOLICITATION. IF THE BUSINESS COMBINATION IS NOT CONSUMMATED, THEN THE PUBLIC SHARES WILL NOT BE REDEEMED FOR CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS. THE REDEMPTION RIGHTS INCLUDE THE REQUIREMENT THAT A STOCKHOLDER MUST IDENTIFY ITSELF IN WRITING AS A BENEFICIAL HOLDER AND PROVIDE ITS LEGAL NAME, PHONE NUMBER, AND ADDRESS IN ORDER TO VALIDLY REDEEM ITS PUBLIC SHARES. SEE “THE MEETING - REDEMPTION RIGHTS” IN THIS PROXY STATEMENT/PROSPECTUS/CONSENT SOLICITATION FOR MORE SPECIFIC INSTRUCTIONS.

HOW TO OBTAIN ADDITIONAL INFORMATION

This proxy statement/prospectus/consent solicitation incorporates important business and financial information about DHAC that is not included or delivered herewith. If you would like to receive additional information or if you want additional copies of this document, agreements contained in the appendices or any other documents filed by DHAC with the Securities and Exchange Commission, such information is available without charge upon written or oral request. Please contact our proxy solicitor:

D.F. King & Co.

48 Wall Street, 22nd Floor

New York, NY 10005

Brokers and Banks Call Collect: (212) 269-5550

All Others Call Toll-Free: (800) 290-6429

Email: DHAC@dfking.com

If you would like to request documents, please do so no later than [·], 2024 to receive them before the Meeting. Please be sure to include your complete name and address in your request. Please see “Where You Can Find Additional Information” to find out where you can find more information about DHAC, VSee and iDoc.

NOTICE OF SOLICITATION OF WRITTEN CONSENT

VSee Lab Inc.

3188 Kimlee Drive

San Jose, CA 95132

To Stockholders of VSee Lab, Inc.:

We are pleased to enclose the proxy statement/prospectus/consent solicitation relating to the proposed merger further to that Third Amended and Restated Business Combination Agreement, dated as of November 21, 2023 (the “Business Combination Agreement”), by and among Digital Health Acquisition Corp, a Delaware corporation (“DHAC”), DHAC Merger Sub I, Inc., a Delaware corporation and wholly owned subsidiary of DHAC (“Merger Sub I”), DHAC Merger Sub II, Inc., a Texas corporation and wholly owned subsidiary of DHAC (“Merger Sub II”), VSee Lab, Inc., a Delaware corporation (“VSee”), and iDoc Virtual Telehealth Solutions, Inc., a Texas corporation (“iDoc”). If (i) the Business Combination Agreement is adopted and the merger and the other transactions contemplated thereby (collectively, the “Business Combination”) are approved by each of DHAC’s, VSee’s and iDoc’s stockholders, and (ii) the Business Combination is subsequently completed, Merger Sub I will merge with and into VSee (the “VSee Merger”), with VSee surviving the VSee merger as a wholly owned subsidiary of DHAC, and Merger Sub II will merge with and into iDoc (the “iDoc Merger” and, together with the VSee Merger, the “Mergers”), with iDoc surviving the iDoc Merger as a wholly owned subsidiary of DHAC. All shares of VSee and iDoc capital stock issued and outstanding immediately prior to the effective time of the Business Combination (the “Effective Time”) (other than those properly exercising any applicable dissenters rights under Delaware or Texas law, as applicable) will be converted into the right to receive the applicable merger consideration. Upon the consummation of the Business Combination, DHAC will change its name to “VSee Health, Inc.”

The proxy statement/prospectus/consent solicitation attached to this notice is being delivered to you on behalf of VSee’s board of directors to request that holders of the outstanding shares of VSee’s class A common stock, VSee’s Series A preferred stock and VSee’s Series A-1 preferred stock, as of the record date of [·], 2024 execute and return written consents to adopt and approve the Business Combination Agreement, the Business Combination and the other transactions contemplated by the Business Combination Agreement, in all respects.

The attached proxy statement/prospectus/consent solicitation describes the proposed Business Combination and the actions to be taken in connection with the Business Combination and provides additional information about the parties involved. A copy of the Business Combination Agreement is attached as Annex A to this proxy statement/prospectus/consent solicitation.

A summary of the appraisal rights that may be available to you under Section 262 of the General Corporation Law of the State of Delaware (“DGCL”) with respect to the Business Combination is described in “Appraisal Rights — VSee Stockholder Appraisal Rights”. A copy of Section 262 of the DGCL is attached as Annex E to this proxy statement/prospectus/consent solicitation.

The VSee board of directors has considered the Business Combination and the terms of the Business Combination Agreement and has unanimously determined that the Business Combination and the Business Combination Agreement are advisable, fair to and in the best interests of VSee and its stockholders, and recommends that VSee stockholders approve the Business Combination Agreement, the Business Combination and the other transactions contemplated by the Business Combination Agreement, by submitting a written consent.

Please complete, date and sign the written consent enclosed with this proxy statement/prospectus/consent solicitation and return it promptly to VSee by one of the means described in “VSee’s Solicitation of Written Consents.”

By Order of the Board of Directors, |

|

/s/ Milton Chen |

|

Milton Chen | |

Executive Vice Chairman | |

VSee Lab Inc. | |

[·], 2024 |

|

NOTICE OF SOLICITATION OF WRITTEN CONSENT

iDoc Virtual Telehealth Solutions, Inc.

2311 West Main Street

Houston, Texas 77098

To Stockholders of iDoc Virtual Telehealth Solutions, Inc.:

We are pleased to enclose the proxy statement/prospectus/consent solicitation relating to the proposed merger further to that Third Amended and Restated Business Combination Agreement, dated as of November 21, 2023 (the “Business Combination Agreement”), by and among Digital Health Acquisition Corp, a Delaware corporation (“DHAC”), DHAC Merger Sub I, Inc., a Delaware corporation and wholly owned subsidiary of DHAC (“Merger Sub I”), DHAC Merger Sub II, Inc., a Texas corporation and wholly owned subsidiary of DHAC (“Merger Sub II”), VSee Lab, Inc., a Delaware corporation (“VSee”), and iDoc Virtual Telehealth Solutions, Inc., a Texas corporation (“iDoc”). If (i) the Business Combination Agreement is adopted and the merger and the other transactions contemplated thereby (collectively, the “Business Combination”) are approved by each of DHAC’s, VSee’s and iDoc’s stockholders, and (ii) the Business Combination is subsequently completed, Merger Sub I will merge with and into VSee (the “VSee Merger”), with VSee surviving the VSee merger as a wholly owned subsidiary of DHAC, and Merger Sub II will merge with and into iDoc (the “iDoc Merger” and, together with the VSee Merger, the “Mergers”), with iDoc surviving the iDoc Merger as a wholly owned subsidiary of DHAC. All shares of VSee and iDoc stock issued and outstanding immediately prior to the effective time of the Business Combination (the “Effective Time”) (other than those properly exercising any applicable dissenters rights under Delaware or Texas law, as applicable) will be converted into the right to receive shares of DHAC common stock. Upon the consummation of the Business Combination, DHAC will change its name to “VSee Health, Inc.”

The proxy statement/prospectus/consent solicitation attached to this notice is being delivered to you on behalf of iDoc’s board of directors to request that holders of the outstanding shares of iDoc’s class A common stock as of the record date of [·], 2024 execute and return written consents to adopt and approve the Business Combination Agreement, the Business Combination and the other transactions contemplated by the Business Combination Agreement, in all respects.

The attached proxy statement/prospectus/consent solicitation describes the proposed Business Combination and the actions to be taken in connection with the Business Combination and provides additional information about the parties involved. A copy of the Business Combination Agreement is attached as Annex A to this proxy statement/prospectus/consent solicitation.

A summary of the appraisal rights that may be available to you under Subchapter H, Chapter 10, Title 1 of the Texas Business Organizations Code (“TBOC”) with respect to the Business Combination is described in “Appraisal Rights — iDoc Stockholder Appraisal Rights”. A copy of Subchapter H, Title 1, Chapter 10 of the TBOC is attached as Annex F to this proxy statement/prospectus/consent solicitation.

The iDoc board of directors has considered the Business Combination and the terms of the Business Combination Agreement and has unanimously determined that the Business Combination and the Business Combination Agreement are advisable, fair to and in the best interests of iDoc and its stockholders, and recommends that iDoc stockholders approve the Business Combination Agreement and the Business Combination, by submitting a written consent.

Please complete, date and sign the written consent enclosed with this proxy statement/prospectus/consent solicitation and return it promptly to iDoc by one of the means described in “iDoc’s Solicitation of Written Consents.”

By Order of the Board of Directors, |

|

/s/ Imoigele Aisiku |

|

Imoigele Aisiku, Executive Chairman | |

iDoc Virtual Telehealth Solutions, Inc. | |

[·], 2024 |

ABOUT THIS PROXY STATEMENT/PROSPECTUS/CONSENT SOLICITATION

This document, which forms part of a registration statement on Form S-4 filed with the SEC by DHAC, constitutes a prospectus of DHAC under the Securities Act of 1933, as amended (the “Securities Act”), with respect to the shares of common stock of DHAC to be issued to VSee’s and iDoc’s stockholders under the Business Combination Agreement. This document also constitutes a proxy statement of DHAC under Section 14(a) of the Exchange Act.

You should rely only on the information contained in this proxy statement/prospectus/consent solicitation in deciding how to vote on the Business Combination. None of DHAC, VSee or iDoc has authorized anyone to give any information or to make any representations other than those contained in this proxy statement/prospectus/consent solicitation. Do not rely upon any information or representations made outside of this proxy statement/prospectus/consent solicitation. The information contained in this proxy statement/prospectus/consent solicitation may change after the date of this proxy statement/prospectus/consent solicitation. Do not assume after the date of this proxy statement/prospectus/consent solicitation that the information contained in this proxy statement/prospectus/consent solicitation is still correct.

Information contained in this proxy statement/prospectus/consent solicitation regarding DHAC and its business, operations, management and other matters has been provided by DHAC and information contained in this proxy statement/prospectus/consent solicitation regarding each of VSee and iDoc and each of their respective businesses, operations, management and other matters has been provided by VSee and iDoc, respectively.

This proxy statement/prospectus/consent solicitation does not constitute an offer to sell or a solicitation of an offer to buy any securities, or the solicitation of a proxy or consent, in any jurisdiction to or from any person to whom it is unlawful to make any such offer or solicitation in such jurisdiction.

TRADEMARKS

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this proxy statement/prospectus/consent solicitation may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

1

Table of Contents

Page | |

1 | |

1 | |

4 | |

13 | |

15 | |

17 | |

44 | |

52 | |

SUMMARY OF THE PROXY STATEMENT/PROSPECTUS/CONSENT SOLICITATION | 19 |

SUMMARY UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | 36 |

73 | |

74 | |

119 | |

123 | |

164 | |

168 | |

170 | |

172 | |

177 |

182 | |

186 | |

190 | |

194 | |

198 | |

204 |

2

A-1 | |

B-1-1 |

ANNEX B-2 FORM OF CERTIFICATE OF DESIGNATION OF SERIES A CONVERTIBLE PREFERRED STOCK | B-2-1 |

C-1 |

D-1 |

E-1 | |

ANNEX F TEXAS BUSINESS ORGANIZATIONAL CODE SUBCHAPTER H, CHAPTER 10, TITLE 1 APPRAISAL RIGHTS | F-1 |

G-1 | |

H-1 | |

II-1 |

3

SELECTED DEFINITIONS

When used in this proxy statement/prospectus/consent solicitation, unless the context otherwise requires:

“Acquisition Proposal” refers to (a) any transaction or series of related transactions under which any person(s), directly or indirectly, (i) acquires or otherwise purchases VSee, iDoc or any of their controlled affiliates or (ii) all or a material portion of assets or businesses of VSee, iDoc or any of their controlled affiliates (in the case of each of clause (i) and (ii), whether by merger, consolidation, recapitalization, purchase or issuance of equity securities, tender offer or otherwise), or (b) any equity or similar investment in VSee, iDoc or any of their controlled affiliates (other than the issuance of the applicable class of shares of capital stock of a VSee upon the exercise or conversion of any VSee Options outstanding as of November 21, 2023 in accordance with the terms of VSee Equity Plan and the underlying grant, award or similar agreement).

“Additional Bridge Notes” refers to the 10% original issue discount senior secured promissory notes in the principal amount of $111,111.33 purchased at signing of the Bridge Letter Agreement on November 21, 2023, which will mature on May 21, 2025 and (2) $55,555.67 purchased at a later date mutually agreed upon by DHAC and the Bridge Investor, which is currently expected to be upon the filing of an amendment to the Company’s Registration Statement on Form S-4 in connection with the Business Combination, bearing guaranteed interest at a rate of 8.00% per annum and are convertible into shares of DHAC common stock, par value $0.0001 at an initial fixed conversion price of $10 per share.

“A.G.P.” refers to A.G.P./Alliance Global Partners, the representative of the underwriters in the IPO.

“A.G.P. Securities Purchase Agreement” refers to the Securities Purchase Agreement, dated as of November 3, 2022 and as amended on November 21, 2023, by and between DHAC and A.G.P. pursuant to which DHAC has agreed to issue the A.G.P. Series A Shares to A.G.P., as the same may be amended, modified, supplemented or waived from time to time in accordance with its terms.

“A.G.P. Series A Shares” means the shares of Series A Preferred Stock to be issued to A.G.P. pursuant to the terms of the A.G.P. Securities Purchase Agreement.

“Amended Charter” refers to the Second Amended & Restated Certificate of Incorporation of DHAC to take effect upon DHAC’s stockholders approving the Second Amended & Restated Certificate of Incorporation, in the form included as Annex B-1 to this proxy statement/prospectus/consent solicitation, which shall be further amended by the filing of the Series A Preferred Certificate of Designation on the Closing Date, as further described in the “Charter Amendment Proposals” section of this proxy statement/prospectus/consent solicitation.

“Amended Bylaws” refers to the Amended & Restated Bylaws of DHAC, in the form included as Annex C to this proxy statement/prospectus/consent solicitation, as further described in the “Charter Amendment Proposals” section of this proxy statement/prospectus/consent solicitation.

“Bridge Amendment” refers to the letter agreement, dated November 21, 2023, among DHAC, VSee, iDoc and the Bridge Investor amending the Original Bridge SPA.

“Bridge Financing” refers to the sale of the Bridge Notes, the Additional Bridge Notes, Bridge Warrants, Bridge Shares and the Exchange Note and the other transactions contemplated by the Bridge SPA.

“Bridge Investor” refers to the investor who executed the Bridge SPA, the Exchange Agreement and the Equity Purchase Agreement.

“Bridge Investor Notes” refers to the Additional Bridge Notes, the Exchange Note and the Equity Purchase Note.

“Bridge Notes” refers to the 10% original issue discount senior secured promissory notes issued by DHAC, VSee and iDoc pursuant to the Original Bridge SPA.

“Bridge RRA” refers to the Registration Rights Agreement, dated October 5, 2022, between DHAC and the Bridge Investor and as amended further on January 22, 2024.

“Bridge SPA” refers to the Original Bridge SPA, as amended by the Bridge Amendment.

4

“Bridge Shares” refers to the 30,000 shares of DHAC Common Stock issued to the Bridge Investor on October 5, 2022 in connection with the Bridge Financing.

“Bridge Warrants” refers to 173,913 five-year warrants, each representing the right to purchase one share of DHAC Common Stock at an initial exercise price of $11.50, subject to certain adjustments, issued by DHAC to the Bridge Investor.

“Broadridge” refers to Broadridge Financial Solutions.

“Business Combination” refers to the VSee Merger, the iDoc Merger and the other transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” refers to the Third Amended and Restated Business Combination Agreement, dated as of November 21, 2023, by and among DHAC, Merger Sub I, Merger Sub II, VSee and iDoc, as the same may be amended, modified, supplemented or waived from time to time in accordance with its terms (attached to this proxy statement/prospectus/consent solicitation as Annex A).

“Cassel Salpeter” refers to Cassel Salpeter & Co., LLC.

“Closing” refers to the consummation of the Business Combination.

“Closing Date” refers to the date on which the Closing occurs.

“Code” refers to the Internal Revenue Code of 1986, as amended.

“Combined Company” refers to DHAC (to be renamed as VSee Health, Inc.) and its subsidiaries, following consummation of the Business Combination.

“Combined Company Board” refers to the board of directors of the Combined Company.

“Combined Company Equity Incentive Plan” refers to the VSee Health, Inc. 2024 Equity Incentive Plan (substantially in the form attached hereto as Annex D).

“Company,” “our,” “we” or “us” refers, prior to the Business Combination, to DHAC, as the context suggests, and, following the Business Combination, to the Combined Company.

“Common Stock” or “Combined Company Common Stock” refers to the common stock, par value $0.0001 per share, of the Combined Company.

“Continental” refers to Continental Stock Transfer & Trust Company.

“Conversion SPAs” refers to respective securities purchase agreements entered on November 21, 2023, as may be amended from time to time, with various lenders of each of DHAC, VSee and iDoc, which include the Bridge Investor, pursuant to which (1) certain indebtedness owed by DHAC will be converted into Series A Preferred Stock at the Closing; (2) certain indebtedness owed by VSee will be converted into Series A Preferred Stock of the Combined Company at the Closing; (3) certain indebtedness owed by iDoc will be converted into Series A Preferred Stock of the Combined Company at the Closing (the shares of Series A Preferred Stock to be issued in consideration of the loan conversions described in the foregoing clauses (1) – (3) are referred to as the “Loan Conversion Series A Shares” and together with the A.G.P. Series A Shares, the “Series A Shares”); (4) the $600,000 balance of the VSee Bridge Note not included in the Exchange Note will be converted into class B common stock of VSee immediately prior to the Closing, which will then be exchanged for Combined Company common stock at the Closing; and (5) the $600,000 balance of the iDoc Bridge Note not included in the Exchange Note and certain indebtedness owned by iDoc will be converted into class B common stock of iDoc immediately prior to the Closing, which will then be exchanged for Combined Company common stock at the Closing (the shares of Combined Company common stock to be issued in consideration of the loan conversions described in the foregoing clauses (4) – (5) are referred to as the “Loan Conversion Common Shares” and all of the foregoing transactions, the “Loan Conversions”).

5

“Current Charter” refers to DHAC’s Amended and Restated Certificate of Incorporation, effective as of November 3, 2021, as amended by the Amendment to the Amended and Restated Certificate of Incorporation effective as of October 26, 2022, September 8, 2023 and November 6, 2023, as may hereafter be amended.

“DGCL” refers to the General Corporation Law of the State of Delaware, as amended.

“DHAC” refers to Digital Health Acquisition Corp., a blank check company incorporated in Delaware.

“DHAC Board” refers to the board of directors of DHAC.

“Effective Time” refers to the effective time of the Business Combination.

“Effective Time Option Grants” refers to the stock options with an exercise price of $10 per share pursuant to the Incentive Plan to the individuals, in the amounts, and on the terms set forth on Exhibit E to the Business Combination Agreement.

“Equity Financing” refers to the transactions contemplated by the Equity Purchase Agreement.

“Equity Purchase Agreement” refers to the equity purchase agreement dated November 21, 2023 with the Bridge Investor pursuant to which the Combined Company may sell and issue to the Bridge Investor, and the Bridge Investor is obligated to purchase from the Combined Company, up to $50,000,000 of its newly issued shares of the Combined Company’s common stock, from time to time over a 36-month period beginning from the sixth (6th) trading day following the Closing and the Combined Company will issue to the Bridge Investor the Equity Purchase Note.

“Equity Purchase Note” refers to the senior unsecured convertible note in a principal amount of $500,000 that is convertible into shares of the Combined Company’s common stock at a fixed conversion price of $10 per share.

“Escrow Agent” refers to Continental.

“Exchange Act” refers to the Securities Exchange Act of 1934, as amended.

“Exchange Agreement” refers to the exchange agreement, dated November 21, 2023, among DHAC, VSee, iDoc, and the Bridge Investor pursuant to which the amounts currently due and owing under (i) the DHAC Bridge Note, (ii) the VSee Bridge Note other than $600,000 of the principal amount thereof, and (iii) the iDoc Bridge Note other than $600,000 of the principal amount thereof, will be exchanged at the Closing for the Exchange Note.

“Exchange Note” refers to the senior secured convertible promissory note issued by the Combined Company to the Bridge Investor with an aggregate principle value of $2,523,744.29, which will be guaranteed by each of DHAC, VSee and iDoc, bearing guaranteed interest at a rate of 8.00% per annum and will be convertible into shares of Combined Company common stock at an initial fixed conversion price of $10 per share.

“Exchange RRA” refers to the registration rights agreement to be entered into between the Bridge Investor and the Combined Company at the Closing pursuant to the terms of the Exchange Agreement.

“Extension Financing” refers to the issuance of the Extension Note and related Extension Warrants and Extension Shares pursuant to the Extension Securities Purchase Agreement.

“Extension Note” refers to the promissory note, dated as of May 5, 2023, by DHAC in favor of the unaffiliated institutional investor party to the Extension Securities Purchase Agreement.

“Extension RRA” refers to the registration rights agreement dated May 5, 2023 between the Extension Financing Investor and DHAC in connection with the Extension Financing.

“Extension Securities Purchase Agreement” refers to the Securities Purchase Agreement, dated as of May 5, 2023, by and between DHAC and the unaffiliated institutional investor party thereto.

“Extension Shares” refers to the 7,000 shares of Common Stock issued to the investor in the Extension Financing.

6

“Extension Warrants” refers to 26,086 five year warrants, each representing the right to purchase one share of DHAC Common Stock at an initial exercise price of $11.50, subject to certain adjustments, issued by DHAC to the purchaser of the Extension Note.

“First Amended and Restated Business Combination Agreement” refers to the Amended and Restated Business Combination Agreement, dated as of August 9, 2022, by and among DHAC, Merger Sub I, Merger Sub II, VSee and iDoc,

“First Amendment to Second Amended and Restated Business Combination” refers to the First Amendment to Second Amended and Restated Business Combination Agreement, dated as of November 3, 2022, by and among DHAC, Merger Sub I, Merger Sub II, VSee and iDoc.

“Founder Shares” refers to an aggregate of 2,875,000 shares of Common Stock held by our Sponsor and our directors, officers and advisors, which reflects 4,312,500 shares of Common Stock originally purchased on June 7, 2021 and 1,437,500 shares of Common Stock that were forfeited on October 2021, resulting in 2,875,000 founder shares outstanding.

“GAAP” refers to United States generally accepted accounting principles, consistently applied.

“Group Companies” refers to, collectively, (a) VSee and its Subsidiaries and (b) iDoc and its Subsidiaries.

“HSR Act” refers to the Hart-Scott Rodino Antitrust Improvements Act of 1976.

“iDoc” refers to iDoc Virtual Telehealth Solutions, Inc., a Texas corporation.

“iDoc Class A Common Stock” refers to the shares of iDoc Class A Common Stock, par value $1.00 per share.

“iDoc Class A Consideration” means an amount equal to (1) $49,500,000, minus (2) the aggregate amount of iDoc’s transaction expenses.

“iDoc Class A Outstanding Shares” means the total number of shares of iDoc Class A Common Stock outstanding immediately prior to the Effective Time, expressed on a fully-diluted and as-converted to iDoc Class A Common Stock basis.

“iDoc Class B Common Stock” refers to the shares of iDoc Class B Common Stock, par value $1.00 per share.

“iDoc Class B Consideration” means 592,500 shares of Common Stock.

“iDoc Class B Outstanding Shares” means the total number of shares of iDoc Class B Common Stock outstanding immediately prior to the Effective Time, expressed on a fully-diluted and as-converted to iDoc Class B Common Stock basis.

“iDoc Closing Consideration” refers to the iDoc Class A Consideration and the iDoc Class B Consideration.

“iDoc Common Stock” refers to the iDoc Class A Common Stock and the iDoc Class B Common Stock.

“iDoc Indemnity Escrow Account” refers to the indemnity escrow account established pursuant to an escrow agreement among DHAC, iDoc and the Escrow Agent with respect to the iDoc Indemnity Escrow Amount.

“iDoc Indemnity Escrow Amount” refers to 2% of the iDoc Class A Consideration.

“iDoc Merger” refers to that certain merger of Merger Sub II with and into iDoc, with iDoc surviving as a wholly owned subsidiary of DHAC.

“iDoc Stockholders” refers to the stockholders of iDoc holding iDoc Class A Common Stock.

“iDoc Outstanding Shares” refers to the total number of shares of iDoc Common Stock outstanding immediately prior to the Effective Time, expressed on a fully-diluted and as-converted to iDoc Common Stock basis.

“iDoc Per Share Consideration” means the iDoc Per Share Class A Consideration and the iDoc Per Share Class B Consideration.

7

“iDoc Per Share Class A Consideration” means a number of shares of Parent Common Stock equal to (a) (1) the iDoc Class A Consideration, divided by (2) the total number of iDoc Class A Outstanding Shares, divided by (b) $10.

“iDoc Per Share Class B Consideration” means a number of shares of Parent Common Stock equal to (1) the iDoc Class B Consideration, divided by (2) the total number of iDoc Class B Outstanding Shares. “Initial Public Offering” or “IPO” refers to DHAC’s initial public offering of its Public Shares pursuant to the IPO registration statement became effective on November 3, 2021 and closed on November 8, 2021.

“Initial Stockholders” refer to the Sponsor and DHAC’s advisors, officers and directors who own all of DHAC’s founder shares.

“Investment Company Act” refers to the Investment Company Act of 1940, as amended, and the rules and regulations promulgated thereunder.

“Letter Agreement” refers to that certain letter agreement, dated as of November 3, 2021, among DHAC, the Representative and the Initial Stockholders of DHAC at the time of its initial public offering, pursuant to which the Initial Stockholders agreed, among other things, to vote their founder shares, as well as any Public Shares held by them, in favor of DHAC’s initial business combination (including any proposals recommended by DHAC’s board of directors in connection with such business combination).

“Loan Conversion Common Shares” has the meaning ascribed to such term in the definition of “Conversion SPA.”

“Loan Conversion Series A Shares” has the meaning ascribed to such term in the definition of “Conversion SPA.”

“Loan Conversions” refers to the transactions contemplated by the Conversion SPAs.

“M2B” refers to M2B Funding Corp.

“Merger Sub I” refers to DHAC Merger Sub I, Inc., a Delaware corporation and wholly owned subsidiary of DHAC.