As filed with the Securities and Exchange Commission on April

11

, 2022 Registration

No. 333-260390

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST EFFECTIVE AMENDMENT No. 1 TO

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact Name of Registrant as Specified in Its Charter)

State of Israel |

3674 |

Not applicable | ||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) | ||

Valens Semiconductor Ltd. 8 Hanagar St. POB 7152 Hod Hasharon 4501309 Israel +972 (9) 762-6900 |

||||

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | ||||

Cogency Global Inc. 122 East 42nd Street, 18th Floor New York, NY 10168 (800) 221-0102 |

(Name, address, including zip code, and telephone number, including area code, of agent for service) |

Copies of all correspondence to:

Michael Kaplan Brian Wolfe Davis Polk & Wardwell LLP 450 Lexington Avenue New York, New York 10017 Tel: (212) 450-4000 |

Dror Heldenberg Keren Shmueli Sidi Valens Semiconductor Ltd. 8 Hanagar St. POB 7152 Hod Hasharon 4501309 Israel Tel: +972 (9) 762-6900 |

Shachar Hadar Assaf Naveh Ran Camchy Elad Ziv Meitar | Law Offices 16 Abba Hillel Silver Rd. Ramat Gan 52506, Israel Tel: (+972) (3) 610-3100 |

Approximate date of commencement of proposed sale to the public

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. Emerging growth company. ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

This Post-Effective Amendment No. 1 to the Registration Statement on Form

F-1

(File No. 333-260390)

(as amended, the “Registration Statement”) of Valens Semiconductor Ltd. (the “Registrant”), as originally declared effective by the Securities and Exchange Commission (the “SEC”) on October 27, 2021, is being filed pursuant to the undertakings in Item 9 of the Registration Statement to update the information in the Registration Statement to reflect the Company’s results for the year ended December 31, 2021. The information included in this filing amends the Registration Statement and the prospectus contained therein. No additional securities are being registered under this Post-Effective Amendment No. 1. All applicable registration fees were paid at the time of the original filing of the Registration Statement.

The information in this preliminary prospectus is not complete and may be changed. The selling stockholders may not

sell these securities until the U.S. Securities and Exchange Commission declares the registration statement effective.

This preliminary prospectus is not an offer to sell these securities and we and the selling stockholders are not soliciting

offers to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 11, 2022

PRELIMINARY PROSPECTUS

VALENS SEMICONDUCTOR LTD.

21,580,000 Ordinary Shares

The selling shareholders named in this prospectus (the “Selling Shareholders”) may offer and sell from time to time up to 12,500,000 of our ordinary shares, no par value per share purchased in a private placement in connection with our business combination (the “Business Combination”) with PTK Acquisition Corporation (“PTK”) and up to 3,330,000 ordinary shares underlying the private placement warrants (the “private placement warrants”) issued in a private placement to PTK Holdings LLC (the “Sponsor”).

The Selling Shareholders may offer, sell or distribute all or a portion of the securities hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from such sales of the ordinary shares or warrants, except with respect to amounts received by us upon the exercise of the warrants. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The Selling Shareholders will bear all commissions and discounts, if any, attributable to their sale of ordinary shares or warrants. See “Plan of Distribution.”

In addition, this prospectus relates to the issuance by us of up to 5,750,000 ordinary shares that are issuable by us upon the exercise of the public warrants assumed by us, which were previously registered in connection with the Business Combination (the “public warrants”).

Our ordinary shares and public warrants are listed on The New York Stock Exchange under the symbols “VLN” and “VLNW”, respectively. On April 8, 2022, the last reported sales price of our ordinary shares was $5.10 per share and the last reported sales price of our warrants was $0.52 per warrant.

Investing in our securities involves a high degree of risk. You should review carefully the risks and uncertainties described under the heading “Risk Factors” beginning on page 8 of this prospectus, and under similar headings in any amendment or supplements to this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2022.

TABLE OF CONTENTS

Page |

||||

1 |

||||

3 |

||||

5 |

||||

7 |

||||

8 |

||||

40 |

||||

41 |

||||

42 |

||||

63 |

||||

73 |

||||

98 |

||||

107 |

||||

110 |

||||

111 |

||||

113 |

||||

115 |

||||

124 |

||||

130 |

||||

132 |

||||

132 |

||||

132 |

||||

F-1 |

||||

No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

For investors outside the United States: We have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

i

SELECTED DEFINITIONS

“Ancillary Documents” means the Sponsor Letter Agreement (as defined herein), the Subscription Agreements (as defined herein), the Support Agreements (as defined herein), the Investors’ Rights Agreement (as defined herein), the Valens Warrant Agreement (as defined herein), and each other agreement, document, instrument and/or certificate contemplated by the Business Combination Agreement executed or to be executed in connection with the transactions contemplated thereby.

“Cash” means (i) the cash on hand (including petty cash), cash in current accounts (including checking and savings accounts and money market accounts), cash in short-term deposit or similar accounts (including interest accrued with respect thereto), money orders, certified checks, checks and drafts received from third parties and not yet deposited and cleared, and cash equivalents (including negotiable or other readily marketable securities and short term investments or any short-term Indebtedness issued or guaranteed by the government of the United States or the State of Israel), but excluding any restricted cash, plus (ii) Valens transaction expenses paid by Valens prior to the Closing, plus (iii) any PTK transaction expenses paid by Valens prior to Closing, if any.

“Company Equity Award” means, as of any determination time, each Valens option and each other award to any current or former director, manager, officer, employee, individual independent contractor or other service provider of Valens or its subsidiaries of rights of any kind to receive any equity security of Valens or its subsidiaries under any Company Equity Plan or otherwise that is outstanding.

“Company Equity Plan” means, collectively, Valens’ 2007 Option Plan, the Company’s 2012 Option Plan and the U.S.

Sub-Plan

of the Company’s 2012 Option Plan, and each other plan that provides for the award to any current or former director, manager, officer, employee, individual independent contractor or other service provider of Valens or its subsidiaries of rights of any kind to receive Equity Securities of Valens or its subsidiaries or benefits measured in whole or in part by reference to equity securities of Valens or its subsidiaries. “DGCL” means the Delaware General Corporation Law, as amended.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“Founder Shares” means the 2,875,000 shares of PTK common stock, par value $0.0001 per share, of PTK held by the Sponsor, which were acquired for an aggregate purchase price of $25,000 prior to the PTK IPO.

“GAAP” means accounting principles generally accepted in the United States of America.

“Indebtedness” means, as of any time, without duplication, with respect to any Person, the outstanding principal amount of, accrued and unpaid interest on, fees, expenses and other payment obligations (including any prepayment penalties, premiums, costs, breakage, termination fees or other amounts payable upon the discharge thereof) arising under or in respect of (a) indebtedness for borrowed money or indebtedness issued or incurred in substitution or exchange for indebtedness for borrowed money, (b) other obligations evidenced by any note, bond, debenture or other debt security, (c) obligations for the deferred and unpaid purchase price of property, assets or services, including “earn-outs” and “seller notes” (but excluding any amounts payable under purchase orders made in the ordinary course of business, including any trade payables), (d) reimbursement and other obligations with respect to letters of credit, bank guarantees, bankers’ acceptances or other similar instruments, in each case, solely to the extent drawn, (e) leases (other than operating leases) required to be capitalized under GAAP, (f) derivative, hedging, swap, cap, collar, foreign exchange or similar arrangements, including all obligations or unrealized losses of Valens and its subsidiaries pursuant to hedging or foreign exchange arrangements, or (g) any of the obligations of any other person of the type referred to in clauses (a) through (f) above guaranteed by such person or secured by any assets of such Person, whether or not such Indebtedness has been assumed by such Person.

“PCAOB” means the Public Company Accounting Oversight Board.

“private placement warrants” means the warrants PTK sold to Sponsor via private placement in connection with the PTK IPO.

1

“Securities Act” means the Securities Act of 1933, as amended.

“Sponsor” means PTK Holdings LLC, a Delaware limited liability company.

“PTK IPO” means the initial public offering of PTK, which was consummated on July 15, 2020.

“Transactions” means the transactions contemplated by the Business Combination Agreement and the Ancillary Documents.

“units” means the 10,000,000 units sold as part of the PTK IPO and the 1,500,000 units sold to the underwriter following the exercise of its overallotment option, each consisting of one share of PTK common stock and

one-half

of one redeemable PTK warrant. “Valens preferred shares” means, collectively, the redeemable convertible preferred shares composed of Series A, Series B1, Series B2, Series C, Series D and Series E preferred shares of Valens, in each case NIS 0.01 par value per share.

“Valens warrants” means the warrants received by warrant holders of PTK in exchange for PTK warrants pursuant to the Business Combination Agreement.

2

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. Valens’ forward-looking statements include, but are not limited to, statements regarding Valens or its management team’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “appear,” “approximate,” “believe,” “continue,” “could,” “estimate,” “expect,” “foresee,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “seek,” “should,” “would” and similar expressions (or the negative version of such words or expressions) may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

Forward-looking statements involve a number of risks, uncertainties and assumptions, and actual results or events may differ materially from those projected or implied in those statements. Important factors that could cause such differences include, but are not limited to:

| • | The cyclicality of the semiconductor industry; |

| • | The effects of health epidemics, such as the recent global COVID-19 pandemic; |

| • | The impact of the global pandemic caused by COVID-19 on our customers’ budgets and on economic conditions generally, as well as the length, severity of and pace of recovery following the pandemic; |

| • | Competition in the semiconductor industry, and the failure to introduce new technologies and products in a timely manner to compete successfully against competitors; |

| • | If Valens fails to adjust its supply chain volume due to changing market conditions or fails to estimate its customers’ demand; |

| • | Disruptions in relationships with any one of Valens’ key customers; |

| • | Any difficulty selling Valens’ products if customers do not design its products into their product offerings; |

| • | Valens’ dependence on winning selection processes; |

| • | Even if Valens succeeds in winning selection processes for its products, Valens may not generate timely or sufficient net sales or margins from those wins; |

| • | Sustained yield problems or other delays in the manufacturing process of products; |

| • | Our ability to effectively manage, invest in, grow, and retain our sales force, research and development capabilities, marketing team and other key personnel; |

| • | Our ability to timely adjust product prices to customers following price increase by the supply chain; |

| • | Our ability to adjust our inventory level due to sudden reduction in demand due to inventory buffers accrued by customers; |

| • | Our expectations regarding the outcome of any future litigation in which we are named as a party; |

| • | Our ability to adequately protect and defend our intellectual property and other proprietary rights; |

| • | The market price and trading volume of the Valens ordinary shares may be volatile and could decline significantly; |

| • | Political, economic, governmental and tax consequences associated with our incorporation and location in Israel; |

3

| • | Political, economic and governmental consequences associated with the Russia-Ukraine conflict; and |

| • | The other matters described in the section titled “Risk Factors”. |

4

SUMMARY OF THE PROSPECTUS

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you in making an investment decision. This summary is qualified in its entirety by the more detailed information included in this prospectus. Before making your investment decision with respect to our securities, you should carefully read this entire prospectus, including the information under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the financial statements included elsewhere in this prospectus.

Unless otherwise indicated or the context otherwise requires, references in this prospectus to “Company”, “we,” “our,” “us” and other similar terms refer to Valens Semiconductor Ltd. and our consolidated subsidiaries.

General

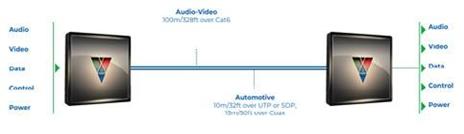

Valens is a leading provider of semiconductor products, pushing the boundaries of connectivity by enabling long-reach, high-speed video and data transmission for the professional audio-video and automotive industries. Valens’ Emmy to ship engineering samples of its VA7000 chipset, compliant with the MIPI

®

award-winning HDBaseT technology is the leading standard in the professional audio-video market, with tens of millions of Valens chipsets integrated into thousands of HDBaseT-enabled products and implemented in millions of audio-video products globally. Valens technology for Automotive is a key enabler of the evolution of autonomous driving, providing chipsets that support Advanced Driver-Assistance Systems (“ADAS

”), Automated Driving Systems (“ADS

”), infotainment, telecommunications and basic connectivity. Valens’ underlying technology has been selected in 2020 by the MIPI Alliance as the basis for the new standard for high-speed automotive video connectivity. In 2021, the IEEE standards association adopted A-PHY

in full as one of its own standards and Valens was the first-in-industry

A-PHY

Standard, to leading Automotive OEMs and Tier 1s. On July 15, 2020, PTK consummated its initial public offering of 11,500,000 units, which included the full exercise by the underwriters of the over-allotment option. The units sold in the PTK IPO were sold at an offering price of $10.00 per unit, generating total gross proceeds of $115,000,000. On September 29, 2021, we consummated our previously announced Business Combination with PTK.

The mailing address of Valens’ principal executive office is 8 Hanagar St. POB 7152, Hod Hasharon 4501309, Israel and its telephone number is +(972)

9-762-6900.

Risks Related to Our Business

Investing in our securities involves risks. You should carefully consider the risks described in “Risk Factors” before making a decision to invest in our ordinary shares. If any of these risks actually occurs, our business, financial condition and results of operations would likely be materially adversely affected. In such case, the trading price of our securities would likely decline, and you may lose all or part of your investment. Set forth below is a summary of some of the principal risks we face:

| • | The cyclicality of the semiconductor industry; |

| • | The effects of health epidemics, such as the recent global COVID-19 pandemic; |

| • | Competition in the semiconductor industry, and the failure to introduce new technologies and products in a timely manner to compete successfully against competitors; |

| • | If Valens fails to adjust its supply chain volume due to changing market conditions or fails to estimate its customers’ demand; |

| • | Disruptions in relationships with any one of Valens’ key customers; |

| • | Any difficulty selling Valens’ products if customers do not design its products into their product offerings; |

| • | Valens’ dependence on winning selection processes; |

5

| • | Even if Valens succeeds in winning selection processes for its products, Valens may not generate timely or sufficient net sales or margins from those wins; |

| • | Sustained yield problems or other delays in the manufacturing process of products; and |

| • | The other matters described in the section titled “ Risk Factors |

6

THE OFFERING

| Securities offered by the Selling Shareholders | We are registering the resale by the Selling Shareholders named in this prospectus, or their permitted transferees, of an aggregate of 12,500,000 ordinary shares and up to 3,330,000 ordinary shares underlying private placement warrants issued in a private placement to the Sponsor. In addition, we are registering up to 5,750,000 ordinary shares issuable upon exercise of the public warrants that were previously registered. | |

| Terms of the Offering | The Selling Shareholders will determine when and how they will dispose of the ordinary shares registered under this prospectus for resale. | |

| Shares outstanding prior to the offering | As of April 1, 2022, we had 98,197,717 ordinary shares issued and outstanding. | |

| Shares outstanding after the offering | 107,277,717 ordinary shares (assuming the exercise for cash of warrants to purchase 9,080,000 ordinary shares). | |

| Use of proceeds | We will not receive any of the proceeds from the sale of the warrants or ordinary shares by the Selling Shareholders except with respect to amounts received by us due to the exercise of the warrants. We expect to use the proceeds received from the exercise of the warrants, if any, for working capital and general corporate purposes. | |

| New York Stock Exchange ticker symbol | Our ordinary shares and warrants are listed on the New York Stock Exchange under the symbols “VLN” and “VLNW.” | |

7

RISK FACTORS

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not known to us or that we consider immaterial as of the date of this prospectus. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

Risks Related to Our Business and Industry

The semiconductor industry is highly cyclical.

The semiconductor industry is highly cyclical and is characterized by short product life cycles and wide fluctuations in product supply and demand. The industry has, from time to time, experienced significant downturns, often connected with, or in anticipation of, excess manufacturing capacity worldwide, maturing product cycles of both semiconductor companies’ and their customers’ products and declines in general economic conditions. Cyclical downturns can result from a variety of market forces including constant and rapid technological change, rapid product obsolescence, price erosion, evolving standards, short product life cycles and wide fluctuations in product supply and demand.

The industry has experienced downturns in the past and may experience such downturns in the future. For example, the industry experienced a significant downtown in connection with the most recent global recession in 2008, and further experienced a downturn from 2019 to 2021, which may be prolonged as a result of the economic impact of the

COVID-19

pandemic as well as the trade dispute among China and the United States and implications of the Russia- Ukraine conflict. These downturns have been characterized by diminished product demand, production overcapacity, high inventory levels and accelerated erosion of average selling prices. Recent downturns in the semiconductor industry have been attributed to a variety of factors, including the

COVID-19

pandemic, trade disputes among the United States and China, weakness in demand in certain markets, supply chain capacity challenges and pricing for semiconductors across applications and excess inventory. Recent downturns have directly impacted our business, as has been the case with many other companies, suppliers, distributors and customers in the semiconductor industry and other industries around the world, and any prolonged or significant future downturns in the semiconductor industry could have a material adverse effect on our business, financial condition and results of operations. Conversely, significant upturns can cause us to be unable to satisfy demand in a timely and cost-efficient manner and could result in increased competition for access to third-party foundry and assembly capacity. In the event of such an upturn, we may not be able to procure adequate capacity within our semiconductor supply chains, resources and raw materials, some of which are single-sourced or locate suitable third-party suppliers or other third-party subcontractors to respond effectively to changes in demand for our existing products. As the shortage in the semiconductor industry increases, we continue to face the impact of extended lead times from our suppliers as well as cost increases for certain raw materials that are in short supply, which may impact our revenues, gross margins and our ability to obtain future design wins, while potentially increasing order cancellations. If the availability of those materials and supplies continues to be interrupted, we may not be able to find suitable replacements and, as a result, our business, financial condition and results of operations could be materially and adversely affected.

Downturns or volatility in general economic conditions could have a material adverse effect on our business, financial condition, results of operations and liquidity.

Our net sales, gross margin, and profitability depend significantly on general economic conditions and the demand for products in the markets in which our customers compete. Weaknesses in the global economy and financial markets, including the current weaknesses resulting from the ongoing

COVID-19

pandemic, and any adverse changes in general domestic and global economic conditions that may occur in the future, including any recession, economic slowdown or disruption of credit markets, may also lead to, lower demand for products that incorporate our solutions, particularly in the automotive and audio-video markets. A decline in end-user

demand can affect our customers’ demand for our products, the ability of our customers to obtain credit and otherwise meet their payment obligations. Our net sales, financial condition and results of operations could be negatively affected by such actions. Volatile and/or uncertain economic conditions can adversely impact sales, gross margin and profitability and make it difficult for us to accurately forecast and plan our future business activities. To the extent we incorrectly plan for favorable economic conditions that do not materialize or take longer to materialize than expected, we may face oversupply of our products relative to customer demand. 8

Conversely, if we overestimate customer demand, we may manufacture products that we may not be able to sell. As a result, we would have excess inventory, which could result in losses. To the extent that our sales, profitability and strategies are negatively affected by downturns or volatility in general economic conditions, our business, financial condition and results of operations may be materially and adversely affected. In addition, any disruption in the credit markets, including as a result of the current

COVID-19

pandemic, could impede our access to capital, which could be further adversely affected if we are unable to obtain or maintain favorable credit ratings. If we have limited access to additional financing sources, we may be required to defer capital expenditures or seek other sources of liquidity, which may not be available to us on acceptable terms or at all. Similarly, if our suppliers face challenges in obtaining credit or other financial difficulties, they may be unable to provide the materials we need to manufacture our products. All of these factors related to global economic conditions, which are beyond our control, could adversely impact our business, financial condition, results of operations and liquidity.

The effects of health epidemics, such as the recent global

COVID-19

pandemic, have had and could in the future have an adverse impact on our revenue, our employees and results of operations. Our business and operations have been and could in the future be adversely affected by health epidemics, such as the global

COVID-19

pandemic. The COVID-19

pandemic and efforts to control its spread have curtailed the movement of people, goods and services worldwide, including in the regions in which we and our customers and partners operate, and are significantly impacting economic activity and financial markets. During 2020 and early 2021, we noticed a negative impact from COVID-19

on some of our customers’ demand, particularly with respect to end users’ audio-video and multimedia products that are used in public areas and for public events. In addition, many automotive companies decreased or paused their manufacturing in 2020 and early 2021 as a result of COVID-19,

which negatively impacted our revenue and results of operations. In addition, our customers’ businesses or cash flows have been and may continue to be negatively impacted by COVID-19,

which may continue to lead them to seek adjustments to payment terms or delay making payments or default on their payables, any of which may impact the timely receipt and/or collectability of our receivables. Our operations are subject to a range of external factors related to the

COVID-19

pandemic that are not within our control. We have taken precautionary measures intended to minimize the risk of the spread of the virus to our employees, customers, and the communities in which we operate. A wide range of governmental restrictions has also been imposed on our employees’ and customers’ physical movement to limit the spread of COVID-19. There can be no assurance that precautionary measures, whether adopted by us or imposed by others, will be effective, and such measures could negatively affect our sales, marketing, business development activities and customer service efforts, delay and lengthen our sales cycles, decrease our employees’ and customers’ productivity, or create operational or other challenges especially with respect to extended supply lead times, any of which could harm our business and results of operations. Although there are effective vaccines for

COVID-19

that have been approved for use, not all of our employees are vaccinated. In addition, new strains of the virus have appeared (primarily, and most recently the Omicron variant), which may complicate treatment and vaccination programs. Accordingly, concerns remain regarding additional surges of COVID-19

as seen for example, towards the end of 2021, and the economic impact thereof, all of which may impact our future results of operations and financial condition. The economic uncertainty caused by the

COVID-19

pandemic may continue to make it difficult for us to forecast revenue and operating results and to make decisions regarding operational cost structures and investments. We have committed, and we plan to continue to commit, resources to grow our business, including to expand our international presence, employee base, and technology development, and such investments may not yield anticipated returns, particularly if worldwide business activity continues to be impacted by COVID-19.

The duration and extent of the impact from the COVID-19

pandemic depend on future developments that cannot be accurately predicted at this time, and if we are not able to respond to and manage the impact of such events effectively, our business may be harmed. 9

Events beyond our control could have an adverse effect on our business, financial condition, results of operations and cash flows.

Our ability to make, transport and sell products in coordination with our suppliers, customers, distributors and third-party manufacturers or other subcontractors is critical to our success. Damage or disruption to our supply, manufacturing, supply chain or distribution capabilities resulting from weather, freight carrier availability, any potential effects of climate change, natural disaster, disease, fire, explosion, cyber-attacks, terrorism, pandemics, epidemics or other outbreaks of infectious disease, strikes, civil unrest, repairs or enhancements at facilities manufacturing or distribution of our products or other reasons could impair our ability to manufacture, sell our products, and to deliver products to our customers on a timely basis or at all.

Similarly, over demand on existing supply chain manufacturing lines as well as disruptions in the operations of our key suppliers or in the services provided by contract manufacturers, including disruptions due to natural disasters, materials shortages or other disruptions, or by the transition by us to other suppliers or third-party manufacturers could lead also to supply chain problems and otherwise impair or delay our ability to deliver products to our customers on a timely basis or at all. Additionally, we do not have long-term agreements for the materials and supplies used in our business, which could make it more difficult to obtain such materials and supplies.

Other companies in our industry may be affected differently by natural disasters or other disruptions depending on the location of their suppliers, operations and customers. In addition, many of our competitors are larger companies with more substantial financial and other resources and, as a result, may be better able to plan for, withstand or otherwise mitigate the effects of any such disruption. While we may take steps to plan for or address the occurrence of any such event, we cannot guarantee that we will be successful. If we fail to take adequate steps to reduce the likelihood or mitigate the potential impact of such events, or to effectively manage such events if they occur, it could adversely affect our business, financial condition, results of operations and cash flows and/or require additional resources to restore our supply chain.

Any downturn in the automotive or audio-video markets could significantly harm our financial results.

Approximately 11% and 89% of our total net sales in fiscal year 2021 and 4% and 96% of our total net sales in fiscal year 2020 were generated by our automotive products and audio-video products, respectively. This concentration of sales as well as current government-imposed restrictions on businesses, operations and travel due to the

COVID-19

pandemic and the related economic uncertainty have impacted demand in many global markets exposing us to the risks associated with such markets as follows: | • | Audio-Video market COVID-19 pandemic on some of our Audio-Video customers’ demand, particularly with respect to end users’ audio-video and multimedia products that are used in public areas and for public events. However, at the same time, we did receive an increase in demand for high-speed connectivity products driven by a need for products and infrastructure to support trends that emerged from the impact of the COVID-19 pandemic such as working from home, hybrid work models, hybrid educational models and remote healthcare. |

| • | Automotive market COVID-19 to be highly dependent on its duration and severity. The foregoing impacts and other adverse effects on the automotive industry could have a material adverse effect on our business, financial condition, and results of operations, as well as our ability to execute our growth strategy. |

The semiconductor industry is highly competitive. If we fail to introduce new technologies and products in a timely manner, this could adversely affect our business.

The semiconductor industry is highly competitive and characterized by constant and rapid technological change, short product life cycles (in certain cases), significant price erosion and evolving standards. Our ability to compete in this industry depends on many factors, including our ability to identify emerging markets and technology trends in an accurate and timely manner, introduce new and innovative technologies and products, implement advanced manufacturing technologies at a sustainable pace, maintain the performance and quality of our products, and manufacture our products in a cost-effective manner, as well as our competitors’ performance and general economic and industry market conditions.

10

The success of our business depends to a significant extent on our ability to develop new technologies and products that are ultimately successful in the market. The costs related to the research and development necessary to develop new technologies and products are significant and any reduction of our research and development budget could harm our competitiveness. Meeting evolving industry requirements and introducing new products to the market in a timely manner and at prices that are acceptable to our customers are significant factors in determining our competitiveness and success. Given the long development cycle of semiconductor products, commitments to develop new products must be made well in advance of any resulting sales, and technologies and standards may change during development, potentially rendering our products outdated or uncompetitive before their introduction. If we are unable to successfully develop new products, our revenues may decline substantially.

Moreover, some of our competitors are well-established entities, are larger than us and have greater resources than we do. If these competitors increase the resources they devote to developing and marketing their products, we may not be able to compete effectively. Any consolidation among our competitors could enhance their product offerings and financial resources, further strengthening their competitive position. In addition, some of our competitors operate in narrow business areas relative to us, allowing them to concentrate their research and development efforts directly on products and services for those areas, which may give them a competitive advantage. As a result of these competitive pressures, we may face declining sales volumes or lower prevailing prices for our products, and we may not be able to reduce our total product costs in line with these declining revenues. If any of these risks materialize, they could have a material adverse effect on our business, financial condition and results of operations.

The semiconductor industry is characterized by significant price erosion, especially after a product has been on the market for a significant period of time.

The products we develop and sell are subject to rapid declines in average selling prices over the life of the products. Product life cycles can be relatively short, and as a result, products tend to be replaced by more technologically advanced substitutes on a regular basis. In turn, demand for older technology falls, causing the price at which such products can be sold to drop, in some cases precipitously. Additionally, competitors may be able to quickly introduce new products to compete with our products, and sometimes competitors will anticipate our entry into a market and start to lower the prices on their products before our entry. To the extent we are unable to reduce the prices of our products and remain competitive, our net sales will likely decline, resulting in further pressure on our gross margins, which could have a material adverse effect on our business, financial condition and results of operations and our ability to grow our business.

Additionally, because we do not operate our own manufacturing, assembly or testing facilities, we may not be able to reduce our costs as rapidly as companies that operate their own facilities and consequently our costs may increase, which could also impact our gross margins. Our gross margin could also be impacted by increased cost (including those caused by tariffs), loss of cost savings or dilution of savings due to changes in charges incurred due to inventory holding periods if parts ordering does not correctly anticipate product demand or if the financial health of either contract manufacturers or suppliers deteriorates as well as excess inventory and inventory storage and obsolescence charges. In addition, we are subject to risks from fluctuating market prices of certain components, which are incorporated into our products or used by our suppliers to manufacture our products. Supplies of these components may, from time to time, become restricted, or general market factors and conditions may affect pricing of such commodities. For example, recent supply shortages in the semiconductor industry of multi-layer complex substrates, IC packaging capacity and fab constraints have resulted in increased lead times, inability to meet demand, and overall increased costs. Any increase in the price of components used in our products may adversely affect our gross margins.

In order to continue profitably supplying our products, we must reduce our production costs in line with the lower revenues we can expect to receive per unit. Usually, this must be accomplished through improvements in process technology and production efficiencies. If we cannot advance our process technologies or improve our efficiencies to a degree sufficient to maintain required margins, we will no longer be able to make a profit from the

11

sale of these products. Additionally, we may not be able to cease production of such products, either due to contractual obligations or for customer relationship reasons, and as a result may be required to bear a loss on such products. We cannot guarantee that competition in our core product markets will not lead to price erosion, lower revenue growth rates and lower margins in the future. Should reductions in our manufacturing costs fail to keep pace with reductions in market prices for the products we sell, this could have a material adverse effect on our business, financial condition and results of operations. Similarly, if our suppliers increase their production prices, and we are not able to roll over such increases to our customers in a timely manner, it could adversely impact our business, decrease our gross margins and operating income.

To attract new customers or retain existing customers, from time to time we offer certain price concessions to our customers, which could cause our average selling prices and gross margins to decline. In the past, we have reduced the average selling prices of our products in anticipation of future competitive pricing pressures, new product introductions by us or by our competitors and other factors. We expect that we will continue to have to reduce prices of existing products in the future. Moreover, because of the wide price differences across the markets we serve, the mix and types of performance capabilities of our products sold may affect the average selling prices of our products and have a substantial impact on our revenue and gross margin. We may enter new markets in which a significant amount of competition exists, and this may require us to sell our products with lower gross margins than we earn in our established businesses. If we are successful in growing revenue in these markets, our overall gross margin may decline. Fluctuations in the mix and types of our products may also affect the extent to which we are able to recover the fixed costs and investments associated with a particular product, and as a result may harm our financial results.

Failure to adjust our supply chain volume due to changing market conditions or failure to estimate our customers’ demand could adversely affect our net sales and could result in additional charges for obsolete or excess inventories or

non-cancelable

purchase commitments. Conversely, we may have insufficient inventory or be unable to obtain the supplies or contract manufacturing capacity to meet that demand which would result in lost revenue opportunities and potential loss of market share as well as damaged customer relationships. We typically sell products pursuant to purchase orders rather than long-term purchase commitments. Some of our customers may cancel or defer purchase orders on short notice without incurring a significant penalty. Due to their inability to predict demand or other reasons, some of our customers may accumulate excess inventories and, as a consequence, defer purchase of our products.

We make significant decisions, including determining the levels of business that we will seek and accept, production schedules, levels of reliance on outsourced contract manufacturing, personnel needs, and other resource requirements, based on our estimates of customer requirements. The short- term nature of the commitments by many of our customers and the possibility of rapid changes in demand for their products reduces our ability to accurately estimate future requirements of our customers. Anticipating future demand is difficult because our customers face unpredictable demand for their own products and are increasingly focused more on cash preservation and tighter inventory management. In addition, as an increasing number of our chips are being incorporated into consumer products, we anticipate greater fluctuations in demand for our products, which makes it more difficult to forecast customer demand. Occasionally, our customers may require rapid increases in production, which can challenge our resources. We may not have sufficient capacity at any given time to meet our customers’ demands. Conversely, downturns in the semiconductor industry have in the past caused, and may in the future, cause our customers to significantly reduce the solutions or the number of products ordered from us. Because many of our sales, research and development, and manufacturing expenses are relatively fixed, a reduction in customer demand may decrease our gross margins and operating income.

In addition, we base many of our operating decisions, and enter long term purchase commitments, on the basis of anticipated net sales trends which are highly unpredictable. Some of our purchase commitments are not cancelable, and in some cases we are required to recognize a charge representing the amount of material purchased or ordered which exceeds our actual requirements. These

non-cancelable

purchase commitments could reduce our ability to adjust our inventory to address declining market demands. If demand for our products is less than we expect, we may experience additional excess and obsolete inventories and be forced to incur additional charges, which would reduce our gross margin and adversely affect our financial results. If net sales in future periods fall substantially below our expectations, or if we fail to accurately forecast changes in demand mix, we could again be required to record substantial charges for obsolete or excess inventories or non-cancelable

purchase commitments. 12

Conversely, if we underestimate customer demand or otherwise lack the required manufacturing capacity, we may miss revenue opportunities and potentially lose market share. In addition, any future significant cancellations or deferrals of product orders or the return of previously sold products could materially and adversely affect our profit margins, increase product obsolescence and restrict our ability to fund our operations.

Moreover, during a market upturn, we may not be able to purchase sufficient supplies or components to meet increasing product demand, which could prevent us from taking advantage of opportunities and reduce our net sales. In addition, a supplier could discontinue a component necessary for our design, extend lead times, limit supply, or increase prices due to capacity constraints or other factors. Our failure to adjust our supply chain volume or estimate our customers’ demands could have a material adverse effect on our net sales, business, financial condition and results of operations.

Disruptions in our relationships with any one of our key customers could adversely affect our business.

Approximately 30% of our revenues 2021 and 39% of our 2020 revenues were generated by our top three customers in each of those periods that purchase products from us based on short term purchase orders that reflect the demand they have from their end customers. We cannot guarantee that we will be able to generate similar levels of revenues from our largest customers in the future. Should one or more of these customers substantially reduce their purchases from us, this could have a material adverse effect on our business, financial condition and results of operations.

Our customers continued success will depend in large part on growth within the markets for our automotive and audio-video solutions and products and their success within such markets. Demand in these markets fluctuates significantly, driven by consumer spending, consumer preferences, the development of new technologies and prevailing economic conditions. Factors affecting these markets could seriously harm our customers and, as a result, harm us, including:

| • | the effects of catastrophic and other disruptive events at our customers’ offices or facilities including, but not limited to, natural disasters, telecommunications failures, cyber-attacks, terrorist attacks, pandemics, epidemics or other outbreaks of infectious disease, including the current COVID-19 pandemic, breaches of security or loss of critical data; |

| • | increased costs associated with potential disruptions to our customers’ supply chain and other manufacturing and production operations; |

| • | the deterioration of our customers’ financial condition; |

| • | delays and project cancellations as a result of design flaws in the products developed by our customers; the inability of customers to dedicate the resources necessary to promote and commercialize their products; |

| • | the inability of our customers to adapt to changing technological demands resulting in their products becoming obsolete; and |

| • | the failure of our customers’ products to achieve market success and gain broad market acceptance. |

Any slowdown in the growth of these end markets could adversely affect our financial results.

We will have difficulty selling our products if customers do not design our products into their product offerings.

Our products are not sold directly to the

end-users,

but are components of other products. Our products are generally incorporated into our customers’ products at the design stage. As a result, we rely on our customers to select our products from among alternative offerings to be designed into the products they sell. If they do not include our products in their designs, we will have difficulty selling our products. Even after a customer designs our products into the products it sells, the customer is not obligated to purchase our products, nor can we guarantee that the customer is not using competitive products. In addition, the customer can choose at any time to reduce or discontinue their use of our products, for example, if its own products are not commercially successful, or for any other reason. In addition, we often incur significant expenditures on the development of a new product without any 13

assurance that our product will be designed into our customers’ products. Once a customer designs a competitor’s product into its product offering, it becomes significantly more difficult for us to sell our products to that customer because changing suppliers involves significant cost, time, effort and risk for the customer. Our customers may not continue to design our products into their products or we might not be able to convert any such design into actual sales, either of which could materially and adversely affect our results of operations.

If we are unable to manage our growth effectively, our business and financial results may be adversely affected.

To continue to grow, we must continue to expand our operational, engineering, accounting and financial systems, procedures, controls and other internal management systems. This may require substantial managerial and financial resources, and our efforts in this regard may not be successful. Our current systems, procedures and controls may not be adequate to support our future operations. Unless our growth results in an increase in our revenues that is proportionate to the increase in our costs associated with this growth, our operating margins and profitability will be adversely affected. If we fail to adequately manage our growth effectively, improve our operational, financial and management information systems, or effectively train, motivate and manage our new and future employees, it could adversely affect our business, financial condition and results of operations.

The estimates of market opportunity and growth forecasts included in this disclosure may prove to be inaccurate.

Market opportunity estimates and growth forecasts are inherently uncertain. Our estimates regarding the expected growth in our served available markets are based on our experience, as well as internal research and industry forecasts, which are subject to a number of estimates and assumptions. While we believe our assumptions and the data underlying our estimates to be reasonable, these assumptions and estimates may not be correct and the conditions supporting our assumptions or estimates may change at any time, thereby reducing the predictive accuracy of these underlying factors. As a result, our estimates regarding the size and expected growth rates of our served available markets may prove to be incorrect. If our served available markets are smaller than we have estimated, our sales growth and/or market share may fail to reach the levels implied by these estimates.

Our quarterly net sales and operating results are difficult to predict accurately and may fluctuate significantly from period to period. As a result, we may fail to meet the expectations of investors, which could cause our share price to decline.

We operate in a highly dynamic industry and our future operating results could be subject to significant fluctuations, particularly on a quarterly basis. Our quarterly net sales and operating results have fluctuated significantly in the past and may continue to vary from quarter to quarter due to a number of factors, many of which are not within our control. Although some of our customers provide us with rolling forecasts of their future requirements for our products, a significant percentage of our net sales in each fiscal quarter is dependent on sales that are booked and shipped during that fiscal quarter and are typically attributable to a large number of orders from diverse customers and markets. As a result, accurately forecasting our operating results in any fiscal quarter is difficult. If our operating results do not meet the expectations of securities analysts and investors, our share price may decline.

Additional factors that can contribute to fluctuations in our operating results include:

| • | the rescheduling, increase, reduction or cancellation of significant customer orders; |

| • | the timing of customer qualification of our products and commencement of volume sales by our customers of systems that include our products; |

| • | the timing and amount of research and development and sales and marketing expenditures; |

| • | the rate at which our present and future customers and end users adopt our technologies in our target end markets; |

| • | the timing and success of the introduction of new products and technologies by us and our competitors, and the acceptance of our new products by our customers; |

14

| • | our ability to anticipate changing customer product requirements; |

| • | our gain or loss of one or more key customers; |

| • | the availability, cost and quality of materials and components that we purchase from third-party vendors and any problems or delays in the manufacturing, testing or delivery of our products; |

| • | the availability of production capacity at our third-party facilities or other third-party subcontractors and other interruptions in the supply chain, including as a result of materials shortages, bankruptcies or other causes; |

| • | supply constraints for and changes in the cost of the other components incorporated into our customers’ products; |

| • | our ability to reduce the manufacturing costs of our products; |

| • | fluctuations in manufacturing yields; |

| • | the changes in our product mix or customer mix; |

| • | the timing of expenses related to the acquisition of technologies or businesses; |

| • | product rates of return or price concessions in excess of those expected or forecasted; |

| • | the emergence of new industry standards; |

| • | product obsolescence; |

| • | unexpected inventory write-downs or write-offs; |

| • | costs associated with litigation over intellectual property rights and other litigation; |

| • | the length and unpredictability of the purchasing and budgeting cycles of our customers; |

| • | loss of key personnel or the inability to attract qualified engineers; |

| • | the quality of our products and any remediation costs; |

| • | adverse changes in economic conditions in various geographic areas where we or our customers do business; |

| • | the general industry conditions and seasonal patterns in our target end markets, particularly the automotive market and the audio-video market; |

| • | other conditions affecting the timing of customer orders or our ability to fill orders of customers subject to export control or economic sanctions; and |

| • | geopolitical events, such as war, threat of war or terrorist actions, or the occurrence of pandemics, epidemics or other outbreaks of disease, including the current COVID-19 pandemic, or natural disasters, and the impact of these events on the factors set forth above. |

The February 2022 invasion of Ukraine by the Russian military has significantly amplified existing geopolitical tensions among Russia and Ukraine. We cannot predict how the war in Ukraine will evolve, but any escalation or expansion of the conflict into other countries, particularly in Europe, would exacerbate geopolitical tensions and could lead to additional political and/or economic response from the U.S., the E.U. and other countries, which may adversely impact economic conditions. In particular, Russia’s military incursion and the resulting sanctions have and could continue to adversely affect global energy and financial markets and thus could adversely impact our operations and the price of our ordinary shares. The extent and duration of the military action, the response thereto, including resulting sanctions, and resulting future market disruptions, are impossible to predict, but could be significant.

15

We may experience a delay in generating or recognizing revenues for a number of reasons. For example, open backlogs at the beginning of each quarter are typically lower than expected net sales for that quarter and are generally cancelable or reschedulable with minimal notice. Accordingly, we depend on obtaining orders during each quarter for shipment in that quarter to achieve our net sales objectives and failure to fulfill such orders by the end of a quarter may adversely affect our operating results. Furthermore, our customer agreements typically provide that the customer may delay scheduled delivery dates and cancel orders within specified timeframes without a significant penalty. In addition, we maintain an infrastructure of facilities and human resources in several locations around the world and have a limited ability to reduce the expenses required to maintain such infrastructure. Because we base our operating expenses on anticipated revenue trends and a high percentage of our expenses are fixed in the short term, any delay in generating or recognizing forecasted net sales or changes in levels of our customers’ forecasted demand could materially and adversely impact our business, financial condition, and results of operations. Due to our limited ability to reduce expenses, in the event our revenues decline or our forecasted net sales do not meet our expectations, it is likely that in some future quarters our operating results will decrease from the previous quarter or fall below the expectations of securities analysts and investors. As a result of these factors, our operating results may vary significantly from quarter to quarter.

Accordingly, we believe that comparisons of our results of operations should not solely be relied upon as indications of future performance. Any shortfall in net sales or net income from a previous quarter or from levels expected by the investment community could cause a decline in the trading price of our share.

period-to-period

We depend on winning selection processes, and failure to be selected could adversely affect our business in those market segments.

One of our business strategies is to participate in and win competitive bid selection processes to develop products for use in our customers’ equipment and products. These selection processes are typically lengthy and require us to incur significant design and development expenditures, with no guarantee of winning a contract or generating revenues. Incurrence of such significant expenditures, failure to win new design projects and delays in developing new products with anticipated technological advances or in commencing volume shipments of these products may have an adverse effect on our business. This risk is particularly pronounced in markets where there are only a few potential customers and in the automotive market, where, due to the longer design cycles involved, failure to win a

design-in

could prevent access to a customer for several years. Our failure to win a sufficient number of these bids could result in reduced revenues and hurt our competitive position in future selection processes because we may not be perceived as being a technology or industry leader, each of which could have a material adverse effect on our business, financial condition and results of operations. Even if we succeed in winning selection processes for our products, we may not generate timely or sufficient net sales or margins from those wins and our financial results could suffer.

After incurring significant design and development expenditures, a substantial period of time generally elapses before we generate meaningful net sales relating to such product, if at all, particularly with respect to the automotive industry. The reasons for this delay include, among other things, the following:

| • | changing customer requirements, resulting in an extended development cycle for the product; |

| • | delay in the ramp-up of volume production of the customer’s products into which our solutions are designed; |

| • | delay or cancellation of the customer’s product development plans; |

| • | competitive pressures to reduce our selling price for the product; |

| • | the discovery of design flaws, defects, errors or bugs in the products; |

| • | lower than expected customer acceptance of the solutions designed for the customer’s products; |

16

| • | lower than expected acceptance of our customers’ products; and |

| • | higher manufacturing costs than anticipated. |

If we do not continue to win selection processes for our products in the short term, then we may not be able to achieve expected net sales levels associated with these winnings. If we experience delays in achieving such sales levels, our operating results could be adversely affected. Moreover, even if a customer selects our product, we cannot guarantee that this will result in any sales of our products, as the customer may ultimately change or cancel its product plans, or our customer’s efforts to market and sell its product may not be successful.

If we fail in a timely and cost-effective manner to develop new product features or new products that address customer preferences and achieve market acceptance, our operating results could be adversely affected.

Our customers are constantly seeking new products with more features and functionality at a lower cost, and our success relies heavily on our ability to continue to develop and market to our customers new and innovative products and improvements of existing products. In order to respond to new and evolving customer demands, achieve strong market share and keep pace with new technological, processing and other developments, we must constantly introduce new and innovative products into the market. Although we strive to respond to customer preferences and industry expectations in the development of our products, we may not be successful in developing, introducing or commercializing any new or enhanced products on a timely basis or at all. Further, if initial sales volumes for new or enhanced products do not reach anticipated levels within the time periods we expect, we may be required to engage in additional marketing efforts to promote such products and the costs of developing and commercializing such products may be higher than we predict. Moreover, new and enhanced products may not perform as expected. We may also encounter lower manufacturing yields and longer delivery schedules in commencing volume production of new products that we introduce, which could increase our costs and disrupt our supply of such products.

A fundamental shift in technologies, the regulatory climate or demand patterns and preferences in our existing product markets or the product markets of our customers or

end-users

could make our current products obsolete, prevent or delay the introduction of new products or enhancements to our existing products or render our products irrelevant to our customers’ needs. If our new product development efforts fail to align with the needs of our customers, including due to circumstances outside of our control like a fundamental shift in the product markets of our customers and end users or regulatory changes, our business, financial condition and results of operations could be materially and adversely affected. The development of our products is highly complex. New and enhanced products require substantial financial and other resources to research and development. Occasionally, we have experienced delays in completing the development and introduction of new products and product enhancements, and we could experience delays in the future. Unanticipated problems in developing products could also divert substantial research and development and engineering resources, which may impair our ability to develop new products and enhancements and could substantially increase our costs. Even if we introduce new and enhanced products to the market, we may not be able to achieve market acceptance of these products in a timely manner or at all.

Our competitive position could be adversely affected if we are unable to meet customers’ quality requirements.

Suppliers in the semiconductor industry must meet increasingly stringent quality standards of certain original equipment manufacturers and customers, particularly for automotive and audio-video applications. While our quality performance to date has generally met these requirements, we may experience problems in achieving acceptable quality results in the manufacture of our products, particularly in connection with the production of new products or adoption of a new manufacturing process. Our failure to achieve acceptable quality levels could adversely affect our business results.

Changes in industry standards could limit our ability to sell our products and force us to write down our inventory.

The markets for semiconductors are characterized by rapidly evolving industry standards. We must continuously develop new products or upgrade our existing products to keep pace with these evolving standards. Changes in industry standards, or the development of new industry standards, may make our products less

17

competitive or obsolete. Our products comprise only a component of an automotive vehicle or a part of an electronic device. All components of these end products must uniformly comply with industry standards (if any) in order to operate efficiently together. We depend on companies that provide other components of the end products to support prevailing industry standards. Many of these companies are significantly larger and more influential in driving industry standards than we are. Some industry standards may not be widely adopted or implemented uniformly, and competing standards may emerge that may be preferred by our customers or end users. If larger companies do not support the same industry standards that we do, or if competing standards emerge, market acceptance of our products could be adversely affected, which would harm our business.

Because it is not practicable to develop products that comply with all current standards and new standards that may be adopted in the future, our ability to compete effectively will depend on our ability to select industry standards that will be widely adopted by the market and to design our products to support those relevant industry standards. We may be required to invest significant effort and to incur significant expense to redesign our products to address relevant standards, and we may lose market share if we do not redesign our products quickly enough. If our products do not meet relevant industry standards that are widely adopted for a significant period of time, our results of operations, business, and prospects would be adversely affected.

If we encounter sustained yield problems or other delays in the manufacturing process of our products, we may lose sales and damage our customer relationships.

The manufacture of our products, including the fabrication of semiconductor microchip, and the assembly and testing of our products, involve highly complex processes. For example, difficulties in the microchip fabrication process or other factors can cause a substantial portion of the components on a microchip to be nonfunctional. These problems may be difficult to detect at an early stage of the manufacturing process and are often time-consuming and expensive to correct. From time to time, we have experienced problems achieving acceptable yields at our third-party facilities, resulting in delays in the availability of components. Moreover, an increase in the rejection rate of products during the quality control process before, during or after manufacture and/or shipping of such products, results in lower yields and margins. In addition, changes in manufacturing processes required as a result of changes in product specifications, changing customer needs and the introduction of new product lines have historically significantly reduced our manufacturing yields, resulting in low or negative margins on those products. Poor manufacturing yields over a prolonged period of time could adversely affect our ability to deliver our products on a timely basis and harm our relationships with customers, which could materially and adversely affect our business, financial condition and results of operations.

Our ability to raise capital in the future may be limited and could prevent us from executing our growth strategy.

Our ability to operate and expand our business depends on the availability of adequate capital, which in turn depends on cash flow generated by our business and the availability of debt, equity, or other applicable financing arrangements. We cannot assure you that our existing resources will be sufficient to meet our future liquidity needs. We may require additional capital to respond to business opportunities, challenges, acquisitions or other strategic transactions and/or unforeseen circumstances. The timing and amount of our working capital and capital expenditure requirements may vary significantly depending on numerous factors, including: market acceptance of our products; the need to adapt to changing technologies and technical requirements; the existence of opportunities for expansion; and access to and availability of sufficient management, technical, marketing and financial personnel.

If our capital resources are insufficient to satisfy our liquidity requirements, we may seek to sell additional equity securities or debt securities or obtain debt financing. The sale of additional equity securities or convertible debt securities would result in additional dilution to our shareholders. Additional debt would result in increased expenses and could result in covenants that would restrict our operations and our ability to incur additional debt or engage in other capital-raising activities. We have not made arrangements to obtain additional financing and there is no assurance that financing, if required, will be available in amounts or on terms acceptable to us, if at all. If we are unable to obtain adequate financing or financing on terms satisfactory to us, when we require it, our ability to continue to grow and support our business and respond to business opportunities and challenges could be significantly limited.

18

We are exposed to a variety of financial risks, including currency risk, interest rate risk, liquidity risk, commodity price risk, credit risk and other

non-insured

risks, which may have an adverse effect on our financial results. We are a global company and, as a direct consequence, movements in the financial markets may impact our financial results. We are exposed to a variety of financial risks, including currency fluctuations primarily due to the fact that while our functional currency is the U.S. dollar, our Israeli employees’ payroll which is a significant expense in our income statement is paid in NIS, interest rate risk, liquidity risk, commodity price risk and credit risk and other

non-insured

risks. If we create debt, the rating thereof by major rating agencies may further improve or deteriorate. As a result, our additional borrowing capacity and financing costs may be impacted. Credit risk represents the loss that would be recognized at the reporting date if counterparties failed to perform upon their agreed payment obligations. Credit risk is present within our trade receivables. Such exposure is reduced through ongoing credit evaluations of the financial conditions of our customers and by adjusting payment terms and credit limits when appropriate. We invest available cash and cash equivalents with various financial institutions and are in that respect exposed to credit risk with these counterparties. Cash is invested and financial transactions are concluded where possible with financial institutions with a strong credit rating. If we are unable to successfully manage these risks, they could have a material adverse effect on our business, financial condition and results of operations. We may pursue acquisitions and investments in new businesses, products or technologies, joint ventures and other strategic transactions, which may not be successful and could disrupt our business and divert financial and management resources from more productive uses.