UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________

FORM 10-Q

________________

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Quarterly Period Ended March 31, 2024

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the Transition Period From to

______________________________

Commission File Number 001-40718

________________

(Exact Name of Registrant as Specified in its Charter)

________________

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||

(Registrant’s Telephone Number, Including Area Code)

N/A

(Former name, former address and and former fiscal year if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (paragraph 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13 (a) of the Exchange

Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The number of shares outstanding of the registrant’s common stock, par value $1.00 per share, as of May 3, 2024 was 41,127,768 .

INDEX

| PAGE NO. | ||||||||

| Item 2. | ||||||||

ITEM 1. FINANCIAL STATEMENTS

SYLVAMO CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited)

(In millions, except per share amounts)

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| NET SALES | $ | $ | ||||||||||||

| COSTS AND EXPENSES | ||||||||||||||

| Cost of products sold (exclusive of depreciation, amortization and cost of timber harvested shown separately below) | ||||||||||||||

| Selling and administrative expenses | ||||||||||||||

| Depreciation, amortization and cost of timber harvested | ||||||||||||||

| Taxes other than payroll and income taxes | ||||||||||||||

| Interest (income) expense, net | ||||||||||||||

| INCOME BEFORE INCOME TAXES | ||||||||||||||

| Income tax provision | ||||||||||||||

| NET INCOME | $ | $ | ||||||||||||

| EARNINGS PER SHARE | ||||||||||||||

| Basic | $ | $ | ||||||||||||

| Diluted | $ | $ | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

1

SYLVAMO CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS)

(Unaudited)

(In millions)

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

NET INCOME | $ | $ | ||||||||||||

OTHER COMPREHENSIVE INCOME (LOSS), NET OF TAXES | ||||||||||||||

| Defined Benefit Pension and Postretirement Adjustments: | ||||||||||||||

Amortization of pension and postretirement loss (less taxes of $ | ||||||||||||||

Change in cumulative foreign currency translation adjustment | ( | |||||||||||||

Net gains/losses on cash flow hedging derivatives: | ||||||||||||||

Net gains (losses) arising during the period (less taxes of $ | ( | |||||||||||||

Reclassification adjustment for (gains) losses included in net earnings (less taxes of $ | ( | ( | ||||||||||||

TOTAL OTHER COMPREHENSIVE INCOME (LOSS), NET OF TAXES | ( | |||||||||||||

COMPREHENSIVE INCOME (LOSS) | $ | $ | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

2

SYLVAMO CORPORATION

CONDENSED CONSOLIDATED BALANCE SHEETS

(In millions)

| March 31, 2024 | December 31, 2023 | ||||||||||

| (unaudited) | |||||||||||

| ASSETS | |||||||||||

| Current Assets | |||||||||||

| Cash and temporary investments | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Accounts and notes receivable, net | |||||||||||

| Contract assets | |||||||||||

| Inventories | |||||||||||

| Other current assets | |||||||||||

| Total Current Assets | |||||||||||

| Plants, Properties and Equipment, net | |||||||||||

| Forestlands | |||||||||||

| Goodwill | |||||||||||

| Right of Use Assets | |||||||||||

| Deferred Charges and Other Assets | |||||||||||

| TOTAL ASSETS | $ | $ | |||||||||

| LIABILITIES AND EQUITY | |||||||||||

| Current Liabilities | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Notes payable and current maturities of long-term debt | |||||||||||

| Accrued payroll and benefits | |||||||||||

| Other current liabilities | |||||||||||

| Total Current Liabilities | |||||||||||

| Long-Term Debt | |||||||||||

| Deferred Income Taxes | |||||||||||

| Other Liabilities | |||||||||||

| Commitments and Contingent Liabilities (Note 12) | |||||||||||

| Equity | |||||||||||

Common stock $ | |||||||||||

| Paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Less: Common stock held in treasury, at cost, | ( | ( | |||||||||

| Total Equity | |||||||||||

| TOTAL LIABILITIES AND EQUITY | $ | $ | |||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

3

SYLVAMO CORPORATION

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(In millions)

| Three Months Ended March 31, | ||||||||||||||

| 2024 | 2023 | |||||||||||||

| OPERATING ACTIVITIES | ||||||||||||||

| Net income | $ | $ | ||||||||||||

| Adjustments to reconcile net income to cash provided by operating activities: | ||||||||||||||

| Depreciation, amortization, and cost of timber harvested | ||||||||||||||

| Deferred income tax provision (benefit), net | ||||||||||||||

| Stock-based compensation | ||||||||||||||

| Changes in operating assets and liabilities and other: | ||||||||||||||

| Accounts and notes receivable | ||||||||||||||

| Inventories | ( | ( | ||||||||||||

| Accounts payable and accrued liabilities | ( | ( | ||||||||||||

| Other | ( | |||||||||||||

| CASH PROVIDED BY OPERATING ACTIVITIES | ||||||||||||||

| INVESTMENT ACTIVITIES | ||||||||||||||

| Invested in capital projects | ( | ( | ||||||||||||

| Acquisition of business, net of cash acquired | ( | |||||||||||||

| CASH PROVIDED BY (USED FOR) INVESTMENT ACTIVITIES | ( | ( | ||||||||||||

| FINANCING ACTIVITIES | ||||||||||||||

| Dividends paid | ( | ( | ||||||||||||

| Issuance of debt | ||||||||||||||

| Reduction of debt | ( | ( | ||||||||||||

| Repurchases of common stock | ( | ( | ||||||||||||

| Other | ( | ( | ||||||||||||

| CASH PROVIDED BY (USED FOR) FINANCING ACTIVITIES | ( | ( | ||||||||||||

| Effect of Exchange Rate Changes on Cash | ( | |||||||||||||

| Change in Cash, Temporary Investments and Restricted Cash | ( | ( | ||||||||||||

| Cash, Temporary Investments and Restricted Cash | ||||||||||||||

| Beginning of the period | ||||||||||||||

| End of the period | $ | $ | ||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

4

SYLVAMO CORPORATION

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States and in accordance with the instructions to Form 10-Q and, in the opinion of management, include all adjustments that are necessary for the fair presentation of Sylvamo Corporation’s ("Sylvamo's", "the Company’s" or "our") financial position, results of operations, and cash flows for the interim periods presented. Except as disclosed herein, such adjustments are of a normal, recurring nature. Results for the first three months of the year may not necessarily be indicative of full year results due to factors such as the Company’s planned maintenance outage schedule at its mills. All intercompany transactions have been eliminated. Intra-Europe paper revenue and related cost of products sold reflect the correction of an immaterial error which reduced both net sales and cost of products sold by $18 million for three-month period ended March 31, 2023. You should read these condensed consolidated financial statements in conjunction with the audited financial statements and the notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023 (the "Annual Report"), which have previously been filed with the Securities and Exchange Commission. These consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States that require the use of management’s estimates. Actual results could differ from management’s estimates.

Acquisition of Nymölla

NOTE 2 SIGNIFICANT ACCOUNTING POLICIES

Our significant accounting policies are described in Note 2 Significant Accounting Policies to the audited consolidated financial statements included in our 2023 Form 10-K. There have been no material changes to the significant accounting policies for the three months ended March 31, 2024.

Recently Issued Accounting Pronouncements Not Yet Adopted

Income Taxes

In December 2023, the FASB issued ASU 2023-09, “Income Taxes (Topic 740): Improvements to Income Tax Disclosures.” This guidance requires a public entity to disclose in their rate reconciliation table additional categories of information about federal, state and foreign income taxes and to provide more details about the reconciling items in some categories if the items meet a quantitative threshold. The guidance also requires all entities to disclose annually income taxes paid (net of refunds received) disaggregated by federal (national), state and foreign taxes and to disaggregate the information by jurisdiction based on a quantitative threshold. This guidance is effective for annual periods beginning after December 15, 2024. Early adoption is permitted and this guidance should be applied prospectively but there is the option to apply it retrospectively. The Company plans to adopt the provisions of this guidance in conjunction with our Form 10-K for the annual period ending December 31, 2025.

Segment Reporting

In November 2023, the FASB issued ASU 2023-07, “Segment Reporting (Topic 280): Improvements to Reportable Segment Disclosures.” This guidance requires a public entity to disclose for each reportable segment, on an interim and annual basis, the significant expense categories and amounts that are regularly provided to the chief operating decision-maker (“CODM”) and included in each reported measure of a segment’s profit or loss. Additionally, it requires a public entity to disclose the title and position of the individual or the name of the group or committee identified as the CODM. This guidance is effective for fiscal years beginning after December 31, 2023, and interim periods within fiscal years beginning after December 15, 2024. Early adoption is permitted and the guidance should be applied retrospectively to all periods presented in the financial statements,

5

unless it is impracticable. The Company plans to adopt the provisions of this guidance in conjunction with our Form 10-K for the period ending December 31, 2024.

NOTE 3 REVENUE RECOGNITION

External Net Sales by Product

External net sales by major products were as follows by business segment:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Europe | ||||||||||||||

Uncoated Papers | $ | $ | ||||||||||||

Market Pulp | ||||||||||||||

Europe | ||||||||||||||

Latin America | ||||||||||||||

Uncoated Papers | ||||||||||||||

| Market Pulp | ||||||||||||||

Latin America | ||||||||||||||

North America | ||||||||||||||

Uncoated Papers | ||||||||||||||

Market Pulp | ||||||||||||||

North America | ||||||||||||||

Total | $ | $ | ||||||||||||

Revenue Contract Balances

A contract asset is created when the Company recognizes revenue on its customized products for which we have an enforceable right to payment.

A contract liability is created when customers prepay for goods prior to the Company transferring those goods to the customer. The contract liability is reduced when control of the goods is transferred to the customer, satisfying our performance obligation. Contract liabilities of $8 million and $8 million are included in “Other current liabilities” as of March 31, 2024 and December 31, 2023, respectively.

The difference between the opening and closing balances of the Company’s contract assets and contract liabilities primarily results from the difference between the price and quantity at comparable points in time for goods which we have an unconditional right to payment or receive pre-payment from the customer, respectively.

6

NOTE 4 EQUITY

A summary of changes in equity for the three months ended March 31, 2024 and 2023 is provided below:

| Three Months Ended March 31, 2024 | ||||||||||||||||||||||||||||||||||||||||||||

In millions | Shares | Common Stock | Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Common Stock Held In Treasury, At Cost | Total Equity | |||||||||||||||||||||||||||||||||||||

Balance, December 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

Stock-based employee compensation | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

| Share repurchases | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||

Dividends ($ | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||

Comprehensive income (loss) | — | — | — | ( | — | |||||||||||||||||||||||||||||||||||||||

Balance, March 31, 2024 | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

| Three Months Ended March 31, 2023 | ||||||||||||||||||||||||||||||||||||||||||||

In millions | Shares | Common Stock | Paid-In Capital | Retained Earnings | Accumulated Other Comprehensive Loss | Common Stock Held In Treasury, At Cost | Total Equity | |||||||||||||||||||||||||||||||||||||

Balance, December 31, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

Stock-based employee compensation | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||

| Share repurchases | — | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||

Dividends ($ | — | — | — | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||

Comprehensive income (loss) | — | — | — | |||||||||||||||||||||||||||||||||||||||||

Balance, March 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | ||||||||||||||||||||||||||||||||||||

NOTE 5 OTHER COMPREHENSIVE INCOME

The following table presents the changes in Accumulated Other Comprehensive Income (Loss) (“AOCI”), net of taxes, reported in the condensed consolidated financial statements:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Defined Benefit Pension and Postretirement Adjustments | ||||||||||||||

Balance at beginning of period | $ | ( | $ | ( | ||||||||||

Amounts reclassified from accumulated other comprehensive income | ||||||||||||||

Balance at end of period | ( | ( | ||||||||||||

Change in Cumulative Foreign Currency Translation Adjustments | ||||||||||||||

Balance at beginning of period | ( | ( | ||||||||||||

Other comprehensive income (loss) before reclassifications | ( | |||||||||||||

Balance at end of period | ( | ( | ||||||||||||

Net Gains and Losses on Cash Flow Hedging Derivatives | ||||||||||||||

Balance at beginning of period | ||||||||||||||

Other comprehensive income (loss) before reclassifications | ( | |||||||||||||

| Amounts reclassified from accumulated other comprehensive income | ( | ( | ||||||||||||

Balance at end of period | ||||||||||||||

Total Accumulated Other Comprehensive Income (Loss) at End of Period | $ | ( | $ | ( | ||||||||||

NOTE 6 EARNINGS PER SHARE

Basic earnings per share is computed by dividing net income by the weighted average number of shares of common stock outstanding during the period. Diluted earnings per share is computed by dividing net income by the weighted-average number of shares of common stock outstanding during the period, increased to include the number of shares of common stock that

7

would have been outstanding had potentially dilutive shares of common stock been issued. The dilutive effect of restricted stock units is reflected in diluted earnings per share by applying the treasury stock method.

There are no adjustments required to be made to net income for purposes of computing basic and diluted earnings per share.

Basic and diluted earnings per share are calculated as follows:

| Three Months Ended March 31, | ||||||||||||||

In millions, except per share amounts | 2024 | 2023 | ||||||||||||

Net income | $ | $ | ||||||||||||

Weighted average common shares outstanding | ||||||||||||||

| Effect of dilutive securities | ||||||||||||||

Weighted average common shares outstanding - assuming dilution | ||||||||||||||

Earnings per share - basic | $ | $ | ||||||||||||

Earnings per share - diluted | $ | $ | ||||||||||||

Anti-dilutive shares (a) | ||||||||||||||

NOTE 7 ACQUISITIONS

In January 2023, the Company completed the acquisition of Stora Enso’s uncoated freesheet paper mill in Nymölla, Sweden, for €157 million (approximately $167 million) after post-close working capital adjustments. The integrated mill has the capacity to produce approximately 500,000 short tons of uncoated freesheet on two paper machines.

Sylvamo accounted for the acquisition under ASC 805, “Business Combinations” and the Nymölla mill’s results of operations are included in Sylvamo’s consolidated financial statements from the date of acquisition.

The following table summarizes the final allocation of the purchase price to the fair value assigned to assets and liabilities acquired as of January 2, 2023:

| In millions | |||||

| Accounts receivable | $ | ||||

| Inventory | |||||

| Plants, properties and equipment | |||||

| Other assets | |||||

| Total assets acquired | |||||

| Accounts payable | |||||

| Other liabilities | |||||

| Total liabilities assumed | |||||

| Net assets acquired | $ | ||||

In connection with the allocation of fair value, inventories were written up by $9 million to their estimated fair value. During the first quarter of 2023, $9 million before taxes ($7 million after taxes) was expensed related to the impact of the step-up of acquired Nymölla inventory sold during the quarter.

8

NOTE 8 SUPPLEMENTARY FINANCIAL STATEMENT INFORMATION

Temporary Investments

Temporary investments with an original maturity of three months or less and money market funds with greater than three-month maturities but with the right to redeem without notice are treated as cash equivalents and are stated at cost. Temporary investments totaled $69 million and $109 million at March 31, 2024 and December 31, 2023, respectively.

Restricted Cash

Restricted cash of $60 million as of March 31, 2024 and December 31, 2023 represents funds held in escrow related to the Brazil Tax Dispute. See Note 13 Long-Term Debt for further details.

The following table provides a reconciliation of cash, temporary investments and restricted cash in the condensed consolidated balance sheets to total cash, temporary investments and restricted cash in the condensed consolidated statements of cash flows:

In millions | March 31, 2024 | December 31, 2023 | ||||||||||||

Cash and temporary investments | $ | $ | ||||||||||||

Restricted cash | ||||||||||||||

Total cash, temporary investments and restricted cash in the statements of cash flows | $ | $ | ||||||||||||

Accounts and Notes Receivable

Accounts and notes receivable, net, by classification were:

In millions | March 31, 2024 | December 31, 2023 | ||||||||||||

Accounts and notes receivable: | ||||||||||||||

Trade | $ | $ | ||||||||||||

Notes and other | ||||||||||||||

Total | $ | $ | ||||||||||||

The allowance for expected credit losses was $25 million and $25 million at March 31, 2024 and December 31, 2023, respectively. Based on the Company’s accounting estimates and the facts and circumstances available as of the reporting date, we believe our allowance for expected credit losses is adequate.

Inventories

In millions | March 31, 2024 | December 31, 2023 | |||||||||

Raw materials | $ | $ | |||||||||

Finished paper and pulp products | |||||||||||

Operating supplies | |||||||||||

Other | |||||||||||

| Total | $ | $ | |||||||||

Plants, Properties and Equipment, Net

Accumulated depreciation was $3.7 billion and $3.8 billion at March 31, 2024 and December 31, 2023, respectively. Depreciation expense was $33 million and $30 million for the three months ended March 31, 2024 and 2023, respectively.

Non-cash additions to plants, property and equipment included within accounts payable were $17 17 million each at March 31, 2024 and December 31, 2023.

9

Forestlands

Non-cash additions to Forestlands included within accounts payable were $10 million at March 31, 2024. There were no non-cash additions to Forestlands included within accounts payable as of December 31, 2023.

Other Liabilities and Costs

During the three months ended September 30, 2023, the Company recorded approximately $13 million before taxes ($10 million after taxes) of severance costs related to a planned reduction in our salaried workforce. These severance amounts are reflected in Other current liabilities in our condensed consolidated balance sheet. As of March 31, 2024, the reserve totaled approximately $8 million which will be paid in cash over the remainder of 2024.

Interest

Interest payments of $17 million and $24 million were made during the three months ended March 31, 2024 and March 31, 2023, respectively.

Amounts related to interest were as follows:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Interest expense (a) | $ | $ | ||||||||||||

Interest income (b) | ( | ( | ||||||||||||

| Capitalized interest cost | ( | ( | ||||||||||||

| Total | $ | $ | ||||||||||||

(a) Interest expense for the three months ended March 31, 2023 includes $5 million of debt extinguishment cost related to the tender offer for our 7.00 % 2029 Senior Notes.

ASSET RETIREMENT OBLIGATIONS

As of March 31, 2024 and December 31, 2023, we have recorded liabilities of $28 million and $27 million related to asset retirement obligations. These amounts are included in “Other liabilities.”

NOTE 9 LEASES

The Company leases various real estate, including certain operating facilities, warehouses, office space and land. The Company also leases material handling equipment, vehicles and certain other equipment. The Company’s leases have a remaining lease term of up to 15 years. Total lease cost was $14 million and $17 million for the three months ended March 31, 2024 and 2023, respectively.

10

Supplemental Balance Sheet Information Related to Leases

In millions | Classification | March 31, 2024 | December 31, 2023 | ||||||||||||||

Assets | |||||||||||||||||

Operating lease assets | Right of use assets | $ | $ | ||||||||||||||

Finance lease assets | |||||||||||||||||

Total leased assets | $ | $ | |||||||||||||||

Liabilities | |||||||||||||||||

Current | |||||||||||||||||

Operating | $ | $ | |||||||||||||||

Finance | |||||||||||||||||

Noncurrent | |||||||||||||||||

Operating | |||||||||||||||||

Finance | |||||||||||||||||

Total lease liabilities | $ | $ | |||||||||||||||

(a)Finance leases are recorded net of accumulated amortization of $16 million and $16 million as of March 31, 2024 and December 31, 2023, respectively.

NOTE 10 GOODWILL

The following table presents changes in the goodwill balance as allocated to each business segment for the three months ended March 31, 2024:

In millions | Europe | Latin America | North America | Total | ||||||||||||||||||||||

Balance as of December 31, 2023 | ||||||||||||||||||||||||||

Goodwill | $ | $ | $ | $ | ||||||||||||||||||||||

Accumulated impairment losses | ( | ( | ||||||||||||||||||||||||

| $ | $ | $ | $ | |||||||||||||||||||||||

Currency translation and other | ( | ( | ||||||||||||||||||||||||

Balance as of March 31, 2024 | ||||||||||||||||||||||||||

Goodwill | ||||||||||||||||||||||||||

Accumulated impairment losses | ( | ( | ||||||||||||||||||||||||

Total | $ | $ | $ | $ | ||||||||||||||||||||||

NOTE 11 INCOME TAXES

An income tax provision of $17 million and $44 million was recorded for the three months ended March 31, 2024 and March 31, 2023, and the reported effective income tax rate was 28 % and 31 %, respectively.

The Brazilian Federal Revenue Service has challenged the deductibility of goodwill amortization generated in a 2007 acquisition by International Paper do Brasil Ltda., now named Sylvamo do Brasil Ltda. (“Sylvamo Brasil”), a wholly-owned subsidiary of the Company (the “Brazil Tax Dispute”). Sylvamo Brasil received assessments for the tax years 2007-2015 totaling approximately $119 million in tax, and $278 million in interest, penalties and fees as of March 31, 2024 (adjusted for variation in currency exchange rates and recent law change pursuant to which the Brazil tax authority agreed to cancel a portion of the interest, penalties, and fees). International Paper challenged and is managing the litigation of this matter pursuant to the Tax Matters Agreement between us and International Paper. After a previous favorable ruling challenging the basis for these assessments, there were subsequent unfavorable decisions from the Brazilian Administrative Council of Tax Appeals. On behalf of Sylvamo Brasil, International Paper has appealed and at present, has advised us that it intends to further appeal these and any future unfavorable administrative judgments to the Brazilian federal courts; however, this tax litigation matter may take

11

many years to resolve. The Company believes that the transaction underlying these assessments was appropriately evaluated, and that the Company’s tax position would be sustained, based on Brazilian tax law.

Pursuant to the terms of the Tax Matters Agreement, International Paper will pay 60 %, and Sylvamo will pay 40 % on up to $300 million of any assessment related to this matter, and International Paper will pay all amounts of the assessment over $300 million. Also in connection with this agreement, all decisions concerning the conduct of the litigation related to this matter, including settlement strategy, pursuit and abandonment, will continue to be made by International Paper, which is vigorously defending Sylvamo Brasil’s historic tax position against the current assessments and any similar assessments that may be issued for tax years subsequent to 2015.

NOTE 12 COMMITMENTS AND CONTINGENT LIABILITIES

Environmental and Legal Proceedings

The Company is subject to environmental and legal proceedings in the countries in which we operate. Accruals for contingent liabilities, such as environmental remediation costs, are recorded in the consolidated financial statements when it is probable that a liability has been incurred or an asset impaired and the amount of the loss can be reasonably estimated. The Company has estimated some probable liability associated with environmental remediation matters that is immaterial in the aggregate as of March 31, 2024.

At the Company’s Mogi Guaçu mill, there are legacy basin areas that were formerly lagoons used for treatment of mill wastewater from pulp and paper manufacturing. In coordination with and in response to a request by the Environmental Company of the State of São Paulo (“CETESB”), which is the state environmental regulatory authority, there has been continuous regulatory monitoring and sampling of the former basins, which began prior to their closure in 2006, both to assess for contamination and evaluate whether additional remediation is needed beyond the basins’ ongoing natural vegetation growth. This monitoring and sampling detected metal contamination, with the main constituent of potential environmental impact being mercury. The Company has presented CETESB with proposals for studies and other actions to further assess the scope and type of contamination and the possible need for an additional remediation approach.

Additionally, in October 2022, CETESB requested that the Company expand its efforts to include providing CETESB with a proposed pilot intervention (remediation) plan for a portion of the former basins. The purpose of the pilot intervention plan is to facilitate determination of the appropriate actions to take for the basins generally, guided by the results of the pilot intervention plan in the subset portion of the basins. The Company submitted a proposed pilot intervention plan to CETESB and, in the fourth quarter of 2023 CETESB approved the pre-intervention stages of the pilot intervention plan and requested that some additional measures be added to the plan. In the first quarter of 2024, the Company submitted additional measures that were approved by CETESB.

As of March 31, 2024, the Company has recorded an immaterial liability for the ongoing and additional environmental studies and sampling of the basins. While this matter could in the future have a material impact on our results of operations or cash flows, the Company is unable to estimate its potential additional liability because the further studies to be conducted and the remediation that may be required will depend on the results of the pilot intervention plan, the Company’s environmental studies assessing the existence of ecological risk due to the contamination and what intervention may be required beyond vegetation of the basins, the extent to which there is eventual risk of harm from the contamination, and CETESB’s approval of any ultimate intervention plan for the basins.

Taxes Other Than Payroll Taxes

During the first quarter of 2024, the State of Sao Paulo issued a tax assessment to our Brazilian subsidiary for approximately $52 million regarding unpaid VAT arising from intercompany transactions. This assessment includes $21 million in tax and $31 million in interest and penalties. As of March 31, 2024, no reserve has been recorded by the Company because the risk of loss is not probable.

12

The Company reached an amnesty agreement with the Brazilian government related to certain VAT amounts assessed in prior years, which are unrelated to the 2024 tax assessment noted above. This agreement resulted in the recognition of $9 million of interest income during the first quarter of 2023.

We have other open tax matters awaiting resolution in Brazil, which are at various stages of review in various administrative and judicial proceedings. We routinely assess these tax matters for materiality and probability of loss or gain, and appropriate amounts have been recorded in our financial statements for any open items where the risk of loss is deemed probable. We currently do not consider any of these other tax matters to be material individually. However, it is reasonably possible that settlement of any of these matters concurrently could result in a material loss or that over time a matter could become material, for example, if interest were accruing on the amount at issue for a significant period of time. Also, future exchange rate fluctuations could be unfavorable to the U.S. dollar and significant enough to cause an open matter to become material. The expected timing for resolution of these open matters ranges from one year to ten years .

General

The Company is involved in various other inquiries, administrative proceedings and litigation relating to environmental and safety matters, taxes (including VAT), personal injury, product liability, labor and employment, contracts, sales of property and other matters, some of which allege substantial monetary damages. Assessments of lawsuits and claims can involve a series of complex judgments about future events, can rely heavily on estimates and assumptions, and are otherwise subject to significant uncertainties. As a result, there can be no certainty that the Company will not ultimately incur charges in excess of presently recorded liabilities. The Company believes that loss contingencies arising from pending matters, including the matters described herein, will not have a material effect on the consolidated financial position or liquidity of the Company. However, in light of the inherent uncertainties involved in pending or threatened legal matters, some of which are beyond the Company's control, and the large or indeterminate damages sought in some of these matters, a future adverse ruling, settlement, unfavorable development, or increase in accruals with respect to these matters, could result in future charges that could be material to the Company's results of operations or cash flows in any particular reporting period.

NOTE 13 LONG-TERM DEBT

Long-term debt is summarized in the following table:

In millions | March 31, 2024 | December 31, 2023 | ||||||||||||

Term Loan F - due 2027 (a) | $ | $ | ||||||||||||

Term Loan A - due 2028 (b) | ||||||||||||||

| Securitization Program | ||||||||||||||

| Other | ||||||||||||||

| Less: current portion | ( | ( | ||||||||||||

| Total | $ | $ | ||||||||||||

(a) As of March 31, 2024 and December 31, 2023, presented net of $3 million and $3 million in unamortized debt issuance costs, respectively.

(b) As of March 31, 2024 and December 31, 2023, presented net of $2 million and $2 million in unamortized debt issuance costs, respectively.

In addition to the debt noted above, the Company has the ability to access a cash flow-based revolving credit facility with a total borrowing capacity of $450 million (“Revolving Credit Facility”), which matures in 2026. As of March 31, 2024, the Company had no outstanding borrowings on the Revolving Credit Facility and $21 million of letters of credit related to the Revolving Credit Facility, resulting in an available borrowing capacity of $429 million. As of December 31, 2023, the Company had no outstanding borrowings on the Revolving Credit Facility and $21 million of letters of credit related to the Revolving Credit Facility, resulting in an available borrowing capacity of $429 million. Any outstanding balance on the Revolving Credit Facility is recorded within “Notes payable and current maturities of long-term debt” in the condensed consolidated balance sheet.

13

Sylvamo North America LLC, a wholly owned subsidiary of the Company, maintains a $120 million accounts receivable finance facility (the “Securitization Program”), maturing in 2025. The Company sells substantially all of its North American accounts receivable balances to Sylvamo Receivables, LLC, a special purpose entity, which pledges the receivables as collateral for the Securitization Program. The borrowing availability under this facility is limited by the balance of eligible receivables within the program. The average interest rate for the quarter ended March 31, 2024 was 6.29 %, and the average interest rate for the year ended December 31, 2023 was 5.92 %.

In the first quarter of 2023, in connection with the tender offer and the consent solicitation related to the 2029 Senior Notes, the Company entered into a new senior secured term loan facility amendment which provided an aggregate principal amount of $300 million (“Term Loan A”) maturing in 2028. Term Loan A, together with $60 million borrowings under the Revolving Credit Facility, were used to pay the total consideration for all notes tendered in the tender offer, plus accrued interest and all fees and expenses incurred in connection with the tender offer and consent solicitation. Upon close in the first quarter of 2023, $360 million aggregate principal of the notes were tendered, resulting in a debt extinguishment cost of $5 million, related to the write-off of debt issuance costs. This cost was recorded within “Interest expense (income), net.”

The 2029 Senior Notes are unsecured bonds with a 7.00 % fixed interest rate, payable semi-annually. The interest rates applicable to the Term Loan F, Term Loan A and Revolving Credit Facility are based on a fluctuating rate of interest measured by reference to SOFR plus a fixed percentage of 1.85 %, 1.85 % and 1.60 %, respectively, payable monthly, with a SOFR floor of 0.00

We are receiving interest patronage credits under the Term Loan F. Patronage distributions, which are made primarily in cash but also in equity in the lenders, are generally received in the first quarter of the year following that in which they were earned. Expected patronage credits are accrued in accounts and notes receivable as a reduction to interest expense in the period earned. After giving effect to expected patronage distributions of 90 basis points, of which 75 basis points is expected as a cash rebate, the effective net interest rate on the Term Loan F was approximately 6.28 % and 6.31 % as of March 31, 2024 and December 31, 2023, respectively.

In connection with the Term Loan F, the Company was party to interest rate swaps with various counterparties with a notional amount of $200 million maturing in 2024 and $200 million maturing in 2026. In the first quarter of 2023, the Company received cash proceeds of $12 million from the unwind of four interest rate swaps maturing in 2024 with a total notional amount of $200 million. The related gain from all swap proceeds has been deferred within “Accumulated other comprehensive loss” in the condensed consolidated balance sheet and will be amortized into interest expense over the original contract term of the swaps, of which less than year is remaining for the swaps originally maturing in 2024. In addition, the Company liquidated the swaps maturing in 2026 with a notional amount of $200 million in the third quarter of 2023.

In the first quarter of 2023, the Company entered into four new interest rate swaps with various counterparties with a notional amount of $200 million, maturing in 2025. The interest rate swaps are designated as cash flow hedges, and are utilized to manage interest rate risk. The interest rate swaps allow for the Company to exchange the difference in the variable rates on Term Loan F determined in reference to SOFR and the fixed interest rate per notional amount ranging from 3.72 % to 3.75 %.

As of March 31, 2024 and December 31, 2023, the fair value of the interest rate swaps related to Term Loan F resulted in an asset of $3 million and $1 million, respectively. Assets resulting from interest rate swaps are reflected in “Deferred charges and other assets.”

In relation to Term Loan A, the Company is party to interest rate swaps with a current aggregate notional amount of $265 million that amortize each quarter and mature in 2028. These interest rate swaps allow for the Company to exchange the difference in the variable rates on Term Loan A determined in reference to SOFR and the fixed interest rate per notional amount ranging from 4.13 % to 4.16 %. As of March 31, 2024 and December 31, 2023, the fair value of these interest rate swaps resulted in a liability of $1 million and $5 million, respectively, recorded within “Other liabilities.”

The Company is subject to certain covenants limiting, among other things, the ability of most of its subsidiaries to: (a) incur additional indebtedness or issue certain preferred shares; (b) pay dividends on or make distributions in respect of the Company’s or its subsidiaries’ capital stock or make investments or other restricted payments; (c) create restrictions on the ability of the Company’s restricted subsidiaries to pay dividends to the Company or make certain other intercompany transfers; (d) sell certain assets; (e) create liens; (f) consolidate, merge, sell or otherwise dispose of all or substantially all of the

14

Company’s assets; and (g) enter into certain transactions with its affiliates. The Company is currently subject to a maximum consolidated total leverage ratio of 3.75 to 1.00.

The limit on restricted payments that we may make prior to the resolution of the Brazil Tax Dispute is $60 million if our pro-forma consolidated leverage ratio is less than 2.50 to 1.00 and greater than or equal to 2.00 to 1.00, or $90 million if the pro-forma consolidated leverage ratio is less than 2.00 to 1.00. However, limitations imposed on restricted payments are eliminated prior to the final settlement of the Brazil Tax Dispute if (i) we deposit $120 million in an account subject to the control of the administrative agent under our credit agreement, or (ii) we deposit $60 million in such an account and maintain $225 million of available liquidity at the time we make restricted payments. The funds deposited in the account would be used to pay the Company’s share of the settlement of the Brazil Tax Dispute, with any excess funds returned to us if our portion of any final settlement amount is less than the amount on deposit. In 2023, the Company deposited $60 million in an account subject to the control of the administrative agent. Therefore, our ability to make restricted payments under the credit agreement is governed by the provisions in the credit agreement in effect as if the Brazil Tax Dispute is settled, if at the time of any restricted payments we maintain $225 million of available liquidity.

As of March 31, 2024, we were in compliance with our debt covenants.

NOTE 14 PENSION AND POSTRETIREMENT BENEFIT PLANS

Defined Benefit Plans

The Company sponsors and maintains pension plans for the benefit of certain of the Company’s employees. The service and non-service cost components of net periodic pension expense for these employees is recorded within cost of products sold and selling and administrative expenses. The assets and liabilities related to plans sponsored by the Company are reflected in deferred charges and other assets and other liabilities, respectively.

Net periodic pension expense (benefit) for all pension plans sponsored by the Company for the three months ended March 31, 2024 and March 31, 2023 was immaterial.

The Company’s funding policy for the pension plans is to contribute amounts sufficient to meet legal funding requirements, plus any additional amounts that the Company may determine to be appropriate considering the funded status of the plans, tax deductibility, cash flow generated by the Company, and other factors. The Company continually reassesses the amount and timing of any discretionary contributions. Generally, the non-U.S. pension plans are funded using the projected benefit as a target, except in certain countries where funding of benefit plans is not required.

NOTE 15 INCENTIVE PLANS

The Company has adopted the Sylvamo 2021 Incentive Compensation Plan, which includes shares under its long-term incentive plan (“LTIP”) that grants certain employees, consultants, or non-employee directors of the Company different forms of awards, including time-based and performance-based restricted stock units. As of March 31, 2024, 2,551,633 shares remain available for future grants.

Total stock-based compensation cost recognized by the Company was as follows:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Total stock-based compensation expense (included in selling and administrative expense) | $ | $ | ||||||||||||

As of March 31, 2024, $30 million of compensation cost, net of estimated forfeitures, related to all stock-based compensation arrangements for Company employees had not yet been recognized. This amount will be recognized in expense over a weighted-average period of 1.6 years.

15

NOTE 16 FINANCIAL INFORMATION BY BUSINESS SEGMENT AND GEOGRAPHIC AREA

The Company’s business segments, Europe, Latin America and North America, are consistent with the internal structure used to manage these businesses. All segments are differentiated on a common product, common customer basis, consistent with the business segmentation generally used in the Forest Products industry.

Business segment operating profit is used by the Company’s management to measure the earnings performance of its businesses. Management believes that this measure provides investors and analysts useful insights into our operating performance. Business segment operating profit is defined as income before income taxes, excluding interest (income) expense, net, and net special items.

External sales are defined as those that are made to parties outside the Company’s combined group, whereas sales by segment in the Net Sales table are determined using a management approach and include intersegment sales.

Information By Business Segment

Net Sales

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

| Europe | $ | $ | ||||||||||||

| Latin America | ||||||||||||||

| North America | ||||||||||||||

| Intersegment Sales | ( | ( | ||||||||||||

| Net Sales | $ | $ | ||||||||||||

Business Segment Operating Profit

| Three Months Ended March 31, | ||||||||||||||

| In millions | 2024 | 2023 | ||||||||||||

| Europe | $ | ( | $ | |||||||||||

| Latin America | ||||||||||||||

| North America | ||||||||||||||

| Business Segment Operating Profit | $ | $ | ||||||||||||

| Income before income taxes | $ | $ | ||||||||||||

| Interest (income) expense, net | ||||||||||||||

| Net special items expense (income) (a) | ||||||||||||||

| Business Segment Operating Profit | $ | $ | ||||||||||||

(a) Special items represent income or expenses that are incurred periodically, rather than on a regular basis. Net special items in the periods presented primarily include integration costs related to the Nymölla acquisition, professional and legal fees related to negotiations resulting in a shareholder cooperation agreement, the impact of the step-up of acquired Nymölla inventory sold during the first quarter of 2023 and other charges.

16

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our condensed consolidated financial statements and related notes included in “Financial Information” of this Quarterly Report on Form 10-Q (this “Form 10-Q”) and the Company’s Form 10-K for the three years ended December 31, 2023, 2022 and 2021. In addition to historical consolidated financial information, the following discussion contains forward-looking statements that reflect our plans, estimates, and beliefs that involve significant risks and uncertainties. Our actual results could differ materially from those stated and implied in any forward-looking statements. Factors that could cause or contribute to those differences include those discussed below and elsewhere in this Form 10-Q and in our 2023 Form 10-K, particularly under the headings “Risk Factors” and “Forward-Looking Statements.”

EXECUTIVE SUMMARY

First quarter 2024 net income was $43 million ($1.02 per diluted share) compared with $97 million ($2.25 per diluted share) for the first quarter of 2023. Net sales were $905 million in the current quarter compared with $941 million in the prior year. Cash from operations was $27 million compared to $63 million in the first quarter of last year. Adjusted EBITDA was $118 million and our adjusted EBITDA margin was 13% compared to $208 million and an adjusted EBITDA margin of 22% in the first quarter of 2023. Free cash flow was $(33) million compared to $2 million in the first quarter of 2023.

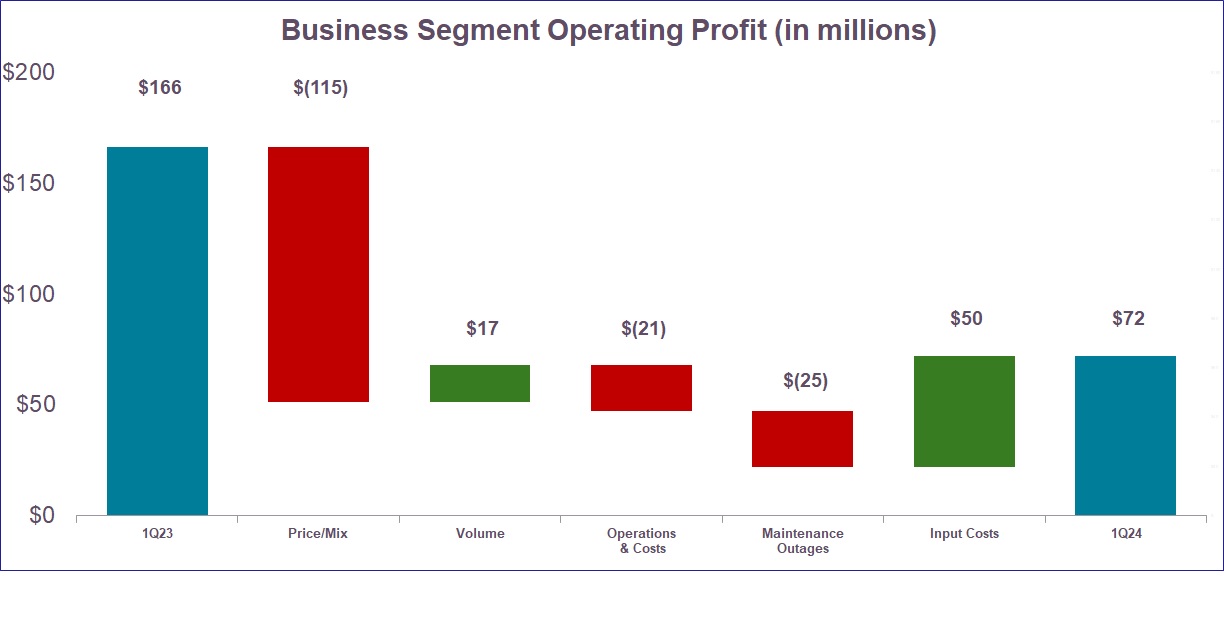

Comparing our performance in the first quarter of 2024 to the prior year, price and mix decreased, partially offset by higher volume in all three regions. We benefited from lower input and transportation costs in the current quarter which was partially offset by higher planned maintenance outage costs due to the timing of outages in Latin America and North America as compared to the prior year.

Uncoated freesheet conditions continue to improve. Our order books in Europe and North America have strengthened versus 2023 levels and we have implemented previously communicated price increases in both paper and pulp across all regions. In addition, we are experiencing stabilization of input costs.

Looking ahead to the second quarter of 2024, we expect price and mix to be favorable reflecting the realization of prior price increases in all regions and favorable mix in Latin America. Volume is expected to improve, reflecting seasonally stronger demand in Latin America plus continued momentum in Europe and North America. Operations and costs are expected to improve due to lower costs in Europe and North America as well as lower economic downtime in North America. Additionally, we expect input and transportation costs to be flat as better transportation and energy costs in North America will be largely offset by unfavorable fiber costs in Latin America. Lastly, we expect planned maintenance outage costs to increase slightly from the first quarter as we will spend about three quarters of our total annual planned maintenance costs in the first half of the year.

Acquisition of Nymölla

On January 2, 2023, the Company completed the acquisition of Stora Enso’s uncoated freesheet paper mill in Nymölla, Sweden. Sylvamo accounted for the acquisition under ASC 805, “Business Combinations” and the Nymölla mill’s results of operations are included in Sylvamo’s condensed consolidated financial statements from the date of acquisition. See Note 7 Acquisitions for further details.

Pillar Two Directive

The Organization for Economic Co-Operation and Development (“OECD”) has been working on a project to act to prevent what it refers to as base erosion and profit shifting (“BEPS”). Most recently, the OECD, through an association of almost 140 countries known as the “inclusive framework,” has announced a consensus to address, among other things, perceived challenges presented by global digital commerce (“Pillar 1”) and the perceived need for a minimum global effective tax rate of 15% (“Pillar 2”). On December 15, 2022, the European Union formally adopted the Pillar Two Directive, and a majority of EU member states have enacted the directive into domestic law as of December 31, 2023. Other countries are taking similar actions. The Pillar Two Directive has not had a material impact on our condensed consolidated financial statements.

17

BUSINESS SEGMENT RESULTS

Overview

Management provides business segment operating profit, a non-GAAP financial measure, to supplement our GAAP financial information, and it should be considered in addition to, but not instead of, the financial statements prepared in accordance with GAAP. Management believes that business segment operating profit provides investors and analysts useful insights into our operating performance. Business segment operating profit is reconciled to Income before income taxes, the most directly comparable GAAP measure. Business segment operating profit may be determined or calculated differently by other companies and therefore may not be comparable among companies.

The following table presents a comparison of Income before taxes to business segment operating profit:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Income Before Income Taxes | $ | 60 | $ | 141 | ||||||||||

Interest (income) expense, net | 9 | 7 | ||||||||||||

Net special items expense (income) (b) | 3 | 18 | ||||||||||||

Business Segment Operating Profit (a) | $ | 72 | $ | 166 | ||||||||||

Europe | $ | (4) | $ | 23 | ||||||||||

Latin America | 14 | 46 | ||||||||||||

North America | 62 | 97 | ||||||||||||

Business Segment Operating Profit (a) | $ | 72 | $ | 166 | ||||||||||

(a) We define business segment operating profit as our income before income taxes calculated in accordance with GAAP, excluding net interest expense (income) and net special items. We believe that business segment operating profit is an important indicator of operating performance as it is a measure reported to our management for purposes of making decisions about allocating resources to our business segments and assessing the performance of our business segments.

(b) Net special items represent income or expenses that are incurred periodically, rather than on a regular basis. Net special items in the periods presented primarily include integration costs related to the Nymölla acquisition, professional and legal fees related to negotiations resulting in a shareholder cooperation agreement, the impact of the step-up of acquired Nymölla inventory sold during the first quarter of 2023 and other charges.

Three Months Ended March 31, 2024 Compared to the Three Months Ended March 31, 2023

18

The following tables present net sales and operating profit, which is the Company’s measure of business segment profitability, for each of the Company’s segments. See Note 16 Financial Information by Business Segment and Geographic Area for more information on the Company’s segments.

Europe

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Net Sales | $ | 207 | $ | 230 | ||||||||||

Operating Profit | $ | (4) | $ | 23 | ||||||||||

Our Europe business segment net sales decreased $23 million, compared to the same period in 2023, primarily due to lower sales price and mix ($46 million) which more than offset higher volumes ($26 million).

Europe operating profit was $27 million lower than the same period in 2023, driven primarily by lower sales prices and less favorable product mix ($46 million) and higher operating costs ($1 million) which more than offset the impacts of lower input costs, primarily for chemicals ($8 million), higher volumes ($7 million) and lower unabsorbed costs due to economic downtime ($5 million).

Latin America

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Net Sales | $ | 216 | $ | 222 | ||||||||||

Operating Profit | $ | 14 | $ | 46 | ||||||||||

Our Latin America business segment net sales decreased $6 million, compared to the same period in 2023, primarily driven by a decrease in sales price and mix ($34 million) which more than offset higher volumes ($25 million).

19

Operating profit for Latin America was $32 million lower than the same period in 2023, as lower sales prices and less favorable product mix ($34 million), along with higher operating costs ($14 million) and higher outage costs ($11 million) more than offset higher volumes ($5 million) and lower input costs ($22 million), primarily for purchased pulp, chemicals and energy.

North America

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Net Sales | $ | 490 | $ | 505 | ||||||||||

Operating Profit | $ | 62 | $ | 97 | ||||||||||

Our North America business segment net sales decreased $15 million, compared to the same period in 2023, as decreased sales prices and less favorable product mix ($35 million) more than offset higher volumes ($16 million).

Operating profit for North America was $35 million lower than the same period in 2023, primarily due to decreased sales prices and less favorable product mix ($35 million), higher outage costs ($14 million) and operating costs ($17 million) which more than offset higher volumes ($5 million), lower unabsorbed costs due to economic downtime ($6 million) and lower input costs ($20 million) primarily for wood, energy and chemicals, as well as lower distribution costs.

Non-GAAP Financial Measures

Management provides Adjusted EBITDA, a non-GAAP financial measure, to supplement our GAAP financial information, and it should be considered in addition to, but not instead of, the financial statements prepared in accordance with GAAP. Management uses this measure in managing the operating performance of our business and believes that Adjusted EBITDA provide investors and analysts meaningful insights into our operating performance and is a relevant metric for the third-party debt. Adjusted EBITDA is reconciled to Net income, the most directly comparable GAAP measure. Adjusted EBITDA may be determined or calculated differently by other companies and therefore may not be comparable among companies.

| Three Months Ended March 31, | |||||||||||

| In millions | 2024 | 2023 | |||||||||

| Net Income | $ | 43 | $ | 97 | |||||||

| Income tax provision | 17 | 44 | |||||||||

| Interest (income) expense, net | 9 | 7 | |||||||||

| Depreciation, amortization and cost of timber harvested | 39 | 35 | |||||||||

| Stock-based compensation | 7 | 7 | |||||||||

Net special items expense (income) (a) | 3 | 18 | |||||||||

Adjusted EBITDA (b) | $ | 118 | $ | 208 | |||||||

| Net Sales | $ | 905 | $ | 941 | |||||||

| Adjusted EBITDA Margin | 13.0 | % | 22.1 | % | |||||||

(a) Net special items represent income or expenses that are incurred periodically, rather than on a regular basis. Net special items in the periods presented primarily include integration costs related to the Nymölla acquisition, professional and legal fees related to negotiations resulting in a shareholder cooperation agreement, the impact of the step-up of acquired Nymölla inventory sold during the first quarter of 2023 and other charges.

(b) We define Adjusted EBITDA (non-GAAP) as net income (GAAP), net of taxes plus the sum of income taxes, net interest expense (income), depreciation, amortization and cost of timber harvested, stock-based compensation, and, when applicable for the periods reported, special items.

Free cash flow is a non-GAAP measure and the most directly comparable GAAP measure is cash provided by operating activities. Management believes that free cash flow is useful to investors as a liquidity measure because it measures the amount of cash generated that is available, after reinvesting in the business, to maintain a strong balance sheet and service debt, and return cash to shareowners. It should not be inferred that the entire free cash flow amount is available for discretionary

20

expenditures. By adjusting for certain items that are not indicative of the Company’s ongoing performance, free cash flow also enables investors to perform meaningful comparisons between past and present periods.

The following is a reconciliation of Cash provided by operations to Free Cash Flow:

| Three Months Ended March 31, | ||||||||||||||

| In millions | 2024 | 2023 | ||||||||||||

| Cash provided by operating activities | $ | 27 | $ | 63 | ||||||||||

| Adjustments: | ||||||||||||||

| Cash invested in capital projects | (60) | (61) | ||||||||||||

| Free Cash Flow | $ | (33) | $ | 2 | ||||||||||

The non-GAAP financial measures presented in this Form 10-Q as referenced above have limitations as analytical tools and should not be considered in isolation or as a substitute for an analysis of our results calculated in accordance with GAAP. In addition, because not all companies utilize identical calculations, the Company’s presentation of non-GAAP measures in this Form 10-Q may not be comparable to similarly titled measures disclosed by other companies, including companies in the same industry as the Company.

LIQUIDITY AND CAPITAL RESOURCES

Overview

Our ability to fund the Company’s cash needs depends on our ongoing ability to generate cash from operations and obtain financing on acceptable terms. Based upon our history of generating strong operating cash flow, we believe we will be able to meet our short-term liquidity needs. We believe we will meet known or reasonably likely future cash requirements through the combination of cash flows from operating activities, available cash balances and available borrowings through the issuance of third-party debt, as needed.

A major factor in our liquidity and capital resource planning is our generation of operating cash flow, which is highly sensitive to changes in the pricing and demand for our products. While changes in key operating cash costs, such as raw materials, energy, mill outages and distribution expenses do have an effect on operating cash generation, we believe that our focus on commercial and operational excellence, as well as our ability to manage costs and working capital, will provide sufficient cash flow generation to meet our operational and capital spending needs.

The terms of the agreements governing our debt contain customary limitations for the financing as well as other provisions. These provisions may also restrict our business and, in the event we cannot meet the terms of those provisions, may adversely impact our financial condition, results of operations or cash flows.

Operating Activities

Cash provided by operating activities totaled $27 million for the three months ended March 31, 2024, compared with cash provided by operating activities of $63 million for the three months ended March 31, 2023. The decrease in cash provided by operating activities in 2024 relates primarily to lower net income offset by changes in working capital.

Cash used for working capital components (accounts and notes receivable, inventories, accounts payable and accrued liabilities, and other) was $64 million for the three months ended March 31, 2024, compared with cash used for working capital components of $81 million for the three months ended March 31, 2023. The three months ended March 31, 2024 working capital components primarily reflect $8 million of cash provided by our accounts and notes receivable balance, offset by $5 million, $45 million and $22 million of cash used for our inventories, accounts payable and accrued liabilities balances, and other operating activities, respectively. The three months ended March 31, 2023 working capital components primarily reflect $82 million and $18 million of cash provided by our accounts and notes receivable and other operating activities, respectively, offset by $81 million and $100 million of cash used for our inventories and accounts payable and accrued liabilities balances, respectively.

21

Investment Activities

The total cash used for investing activities for the three months ended March 31, 2024 decreased from the three months ended March 31, 2023, primarily due to the purchase of the Nymölla mill which occurred in the prior year.

The following table shows capital spending by business segment:

| Three Months Ended March 31, | ||||||||||||||

In millions | 2024 | 2023 | ||||||||||||

Europe | $ | 2 | $ | 11 | ||||||||||

| Latin America | 49 | 32 | ||||||||||||

North America | 8 | 14 | ||||||||||||

| Corporate | 1 | 4 | ||||||||||||

Total | $ | 60 | $ | 60 | $ | 61 | ||||||||

Capital spending primarily consists of purchases of machinery and equipment related to our global mill operations and reforestation and timber purchase costs in Latin America.

Financing Activities

Cash used for financing activities for the three months ended March 31, 2024 primarily reflects the payments of $6 million, $7 million, and $4 million on our outstanding principal debt balances for the AR Securitization, Term Loan F, and Term Loan A, respectively. These amounts are primarily offset by a draw on our AR Securitization of $6 million. During the three months ended March 31, 2024 the Company also paid $12 million in dividends and repurchased $5 million of our shares pursuant to our share repurchase program. Cash used for financing activities for the three months ended March 31, 2023 primarily reflects the payments of $30 million, $10 million, and $7 million on our outstanding principal debt balances for the AR Securitization, Revolving Credit Facility, and Term Loan F, respectively. Additionally, $360 million was paid to bond holders as part of our tender offer. These amounts are primarily offset by the issuance of Term Loan A, draws on our Revolving Credit Facility, and AR Securitization of $300 million, $70 million, and $60 million, respectively. During the three months ended March 31, 2023 the Company also paid $10 million in dividends and repurchased $10 million of our shares pursuant to our share repurchase program.

Contractual Obligations

Our 2023 Form 10-K included disclosures of our contractual obligations and commitments as of December 31, 2023. We continue to make the contractually required payments, and, therefore, the 2023 obligations and commitments described in our 2023 Form 10-K have been reduced by the required payments.

Capital Expenditures

For the three months ended March 31, 2024, we have invested approximately $60 million, or 6.6% of net sales, in total capital expenditures. Over that period, we spent approximately $56 million, or 6.2% of net sales, in maintenance, regulatory and reforestation capital expenditures, and approximately $4 million, or 0.4% of net sales, in high-return capital projects. Our annual maintenance, regulatory and reforestation capital expenditures are expected to be in the range of approximately $175 to $190 million per year (before inflation) for the next several years, which we believe will be sufficient to maintain our operations and productivity. In addition, we expect to spend approximately $30 million to $35 million on high-return projects in 2024.

CRITICAL ACCOUNTING POLICIES AND SIGNIFICANT ACCOUNTING ESTIMATES

The preparation of financial statements in conformity with U.S. GAAP requires the Company to establish accounting policies and to make estimates that affect both the amounts and timing of the recording of assets, liabilities, revenues and expenses. Some of these estimates require subjective judgments about matters that are inherently uncertain.

22

Accounting policies whose application may have a significant effect on the reported results of operations and financial position of the Company, and that can require judgments by management that affect their application, include the accounting for impairment or disposal of long-lived assets and goodwill, business combinations and income taxes.

The Company has included in the Form 10-K a discussion of these critical accounting policies, which are important to the portrayal of the Company’s financial condition and results of operations and require management’s judgments. The Company has not made any changes in these critical accounting policies during the first three months of 2024.

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains information that includes or is based upon forward-looking statements. Forward-looking statements forecast or state expectations concerning future events. These statements often can be identified by the fact that they do not relate strictly to historical or current facts. They typically use words such as “anticipate,” “assume,” “could,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “should,” “will” and other words and terms of similar meaning, or they are tied to future periods in connection with discussions of the Company’s performance. Some examples of forward-looking statements include those relating to our business and operating outlook, future obligations and anticipated expenditures.

Forward-looking statements are not guarantees of future performance. Any or all forward-looking statements may turn out to be incorrect, and actual results could differ materially from those expressed or implied in forward-looking statements. Forward-looking statements are based on current expectations and the current economic environment. They can be affected by inaccurate assumptions or by known or unknown risks, uncertainties and other factors that are difficult to predict.

Although it is not possible to identify all of these risks, uncertainties and other factors, the impact of the following factors, among others, on us or on our suppliers or customers, could cause our actual results to differ from those in the forward-looking statements: deterioration of global and regional economic and political conditions, including the impact of wars and other conflicts in Ukraine and the Middle East; physical, financial and reputational risks associated with climate change; public health crises that could have impacts similar to those experienced as a result of the COVID-19 pandemic; increased costs or reduced availability of the raw materials, energy, transportation (truck, rail and ocean) and labor needed to manufacture and deliver our products; reduced demand for our products due to industry-wide declines in demand for paper, the cyclical nature of the paper industry or competition from other businesses; a material disruption at any of our manufacturing facilities; information technology risks including potential cybersecurity breaches; extensive environmental laws and regulations, as well as tax and other laws, in the United States, Brazil and other jurisdictions to which we are subject, including our compliance costs and risk of violations and liability; our reliance on a small number of customers; a failure by us to attract and retain senior management and other key and skilled employees; loss of our commercial agreements with International Paper; our indebtedness having a material adverse effect on our financial condition, or our inability to generate sufficient cash to service our indebtedness; and the factors disclosed in Item 1A. Risk Factors, as such disclosures may be amended, supplemented or superseded from time to time by other reports we file with the U.S. Securities and Exchange Commission (the “SEC”), including subsequent annual reports on Form 10-K and quarterly reports on Form 10-Q.

We assume no obligation to update any forward-looking statements made in this quarterly report to reflect subsequent events or circumstances or actual outcomes.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

Information relating to quantitative and qualitative disclosures about market risk is shown on page 44 of the Company’s Form 10-K, which information is incorporated herein by reference. There have been no material changes in the Company’s exposure to market risk since December 31, 2023.

ITEM 4. CONTROLS AND PROCEDURES

Disclosure Controls and Procedures:

Management carried out an evaluation, under the supervision and with the participation of our Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of our disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) as of March 31, 2024. Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of such date and designed to ensure that information required to be disclosed by us in reports we file or submit under the Exchange Act is: recorded,

23

processed, summarized and reported within the time periods specified in SEC rules and forms; and accumulated and communicated to our management, including our Chief Executive Officer and Chief Financial Officer, to allow timely decisions regarding required disclosure.

Changes in Internal Control over Financial Reporting:

In January 2023, the Company completed its acquisition of Stora Enso’s uncoated freesheet paper mill in Nymölla, Sweden. As of January 1, 2024, the Company had completed its integration of the Nymölla mill into the Company’s internal control over financial reporting. In the first quarter of 2024, there were no changes in the Company’s internal control over financial reporting that have materially affected, or are reasonably likely to materially affect, its internal control over financial reporting.

24

PART II. OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS

Sylvamo may be involved in legal proceedings arising from time to time in the ordinary course of business. Sylvamo is not involved in any legal proceedings that we believe will result, individually or in the aggregate, in a material adverse effect upon our financial condition or results of operations. Note 11 Income Taxes and Note 12 Commitments and Contingent Liabilities of the Notes to the Condensed Consolidated Financial Statements in this Form 10-Q are incorporated into this Item 1 by reference.

Item 103 of Regulation S-K requires disclosure of certain environmental matters when a governmental authority is a party to the proceedings and the proceedings involve potential monetary sanctions, unless we reasonably believe the monetary sanctions will not equal or exceed a threshold of $1 million (which is the threshold we elected to use as permitted by this regulation). The matters set forth in Note 12 Commitments and Contingent Liabilities and incorporated herein are disclosed in accordance with such requirement.

ITEM 1A. RISK FACTORS

The risk factors that affect our business and financial results are set forth under Part I, Item 1A, “Risk Factors,” in our 2023 Form 10-K. There have been no material changes to the risk factors described in the 2023 Form 10-K. The risk factors in “Item 1A. Risk Factors,” in the 2023 Form 10-K and the risks described in this Form 10-Q or our other SEC filings could cause our actual results to differ materially from those stated in any forward-looking statements.

ITEM 2. PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS

| Period | Total Number of Shares Purchased (a) | Average Price Paid Per Share | Total Number of Shares (or Units) Purchased as Part of the Publicly Announced Program | Maximum Number (or Approximate Dollar Value) of Shares that May Yet Be Purchased Under the Program (in millions) | ||||||||||

| January 1, 2024 - January 31, 2024 | 1,613 | $ | 49.11 | — | $ | 150 | ||||||||

| February 1, 2024 - February 29, 2024 | 1,948 | $ | 46.43 | — | $ | 150 | ||||||||

| March 1, 2024 - March 31, 2024 | 202,074 | $ | 60.12 | 91,264 | $ | 145 | ||||||||

| Total | 205,635 | 91,264 | ||||||||||||

(a) 114,371 shares were acquired from employees from share withholdings under the Company’s long term incentive compensation program.

On May 18, 2022, the Board approved a share repurchase program under which the Company may purchase up to an aggregate amount of $150 million of shares of its common stock (the “Repurchase Program”). In the third quarter of 2023, the Board authorized an additional $150 million for the Repurchase Program, bringing the total program capacity to $300 million, of which $145 million remains available for repurchases. Pursuant to the Repurchase Program, the Company may repurchase in amounts, at prices and at such times as it deems appropriate, subject to market conditions and other considerations, including all applicable legal requirements. Repurchases may include purchases on the open market or privately negotiated transfers, under Rule 10b5-1 trading plans, under accelerated share repurchase programs, in tender offers and otherwise. The Repurchase Program does not obligate the Company to acquire any particular amount of shares of its common stock and may be modified or suspended at any time at the Company’s discretion. The Company repurchased $5 million of shares during the three months ended March 31, 2024.

25

ITEM 6. EXHIBITS

| 3.1 | ||||||||

| 3.2 | ||||||||

| 10.2 | † | |||||||

| 10.3 | † | |||||||

| 31.1* | ||||||||

| 31.2* | ||||||||

| 32** | ||||||||

| 101.INS | XBRL Instance Document – the instance document does not appear in the Interactive Data File because its XBRL tags are embedded within the inline XBRL document. | |||||||

| 101.SCH XBRL | Taxonomy Extension Schema. | |||||||

| 101.CAL XBRL | Taxonomy Extension Calculation Linkbase. | |||||||

| 101.DEF XBRL | Taxonomy Extension Definition Linkbase. | |||||||

| 101.LAB XBRL | Taxonomy Extension Label Linkbase. | |||||||

| 101.PRE XBRL | Extension Presentation Linkbase. | |||||||

| 104. | Cover Page Interactive Data File (formatted as Inline XBRL, and contained in Exhibit 101). | |||||||