Registration No. 333-279828

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

to

Form

REGISTRATION STATEMENT

Under

The Securities Act of 1933

(Exact name of Registrant as specified in its charter)

| 511210 | ||||

| (State or other jurisdiction of | (Primary Standard Industrial | (IRS Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

THUMZUP MEDIA CORPORATION

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Chief Executive Officer

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Please send copies of all communications to:

with copies to:

Gregory Sichenzia, Esq. Jesse

L. Blue, Esq. 1185 Avenue of the Americas New York, NY 10036 (212) 930-9700 |

Ralph

V. De Martino, Esq. Marc E. Rivera, Esq. ArentFox Schiff LLP 1717 K Street NW Washington, D.C. 20006 (202) 724-6848 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging growth company |

If

an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Commission acting pursuant to said Section 8(a) may determine.

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | JUNE 20, 2024 |

Thumzup Media Corporation

Up to [______] Shares of Common Stock

This is the initial public offering of [_______] shares of common stock, $0.001 par value per share of Thumzup Media Corporation, a Nevada corporation (the “Company”).

We are offering [_____] shares of common stock. Prior to this offering, our shares have been quoted on OTC Markets OTCQB since February 2022, with very limited trading. We currently estimate that the public offering price per share of common stock will be $[ ] per share. We intend to list our shares of common stock for trading on the Nasdaq Capital Market (the “Nasdaq”), under the symbol “TZUP”. Completion of this offering is contingent on the approval of our listing application for trading of our common stock on the Nasdaq.

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended, and, as such, may elect to comply with certain reduced public company reporting requirements for future filings. This prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

Investing in our securities is highly speculative and involves a high degree of risk. See “Risk Factors” beginning on page 11 of this prospectus for a discussion of information that should be considered in connection with an investment in our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share of Common Stock | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discounts and commissions (8%)(1) | $ | $ | ||||||

| Proceeds to us, before expenses | $ | $ | ||||||

| (1) | Does not include additional compensation payable to the underwriter. We have agreed to reimburse the underwriter for certain expenses in connection with this offering. In addition, we have agreed to issue to the underwriter, or its designees, warrants to purchase a number of shares of common stock equal to 5% of the number of shares of common stock sold in this offering, including any shares sold in the over-allotment option, if any (the “Underwriter Warrants”). We refer you to the section entitled “Underwriting” for additional information regarding underwriting compensation. |

We have granted the underwriter a 45-day option to purchase up to [______] additional shares of common stock sold in the offering, solely to cover over-allotments, if any. The purchase price to be paid per additional share will be equal to the public offering price per share of common stock, less the underwriting discount.

We will issue to the underwriter or its designees warrants to purchase up to a total of 5% of the shares of common stock sold in this offering, including the exercise of the over-allotment option, if any.

The underwriter expects to deliver the shares of common stock to purchasers in the offering on or about [_______], 2024.

Sole Book-Running Manager

DAWSON JAMES SECURITIES, INC.

The date of this prospectus is [_______], 2024

TABLE OF CONTENTS

Through and including [_______], 2024 all dealers effecting transactions in our securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter with respect to an unsold allotment or subscription.

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Market data and certain industry data and forecasts used throughout this prospectus were obtained from internal company surveys, market research, consultant surveys, publicly available information, reports of governmental agencies and industry publications and surveys. Industry surveys, publications, consultant surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. We have not independently verified any of the data from third party sources, nor have we ascertained the underlying economic assumptions relied upon therein. Similarly, internal surveys, industry forecasts and market research, which we believe to be reliable based on our management’s knowledge of the industry, have not been independently verified. Forecasts are particularly likely to be inaccurate, especially over long periods of time. In addition, we do not necessarily know what assumptions regarding general economic growth were used in preparing the forecasts we cite. Statements as to our market position are based on the most currently available data. While we are not aware of any misstatements regarding the industry data presented in this prospectus, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” in this prospectus.

| i |

GENERAL MATTERS

Unless otherwise indicated, all references to “dollars,” “US$,” or “$” in this prospectus are to United States dollars.

This prospectus contains various company names, product names, trade names, trademarks and service marks, all of which are the properties of their respective owners.

Unless otherwise indicated or the context otherwise requires, all information in this prospectus assumes no exercise of the over-allotment option.

Unless otherwise indicated, all references to “GAAP” in this prospectus are to United States generally accepted accounting principles.

Information contained on our websites, including ThumzupMedia.com, shall not be deemed to be part of this prospectus or incorporated herein by reference and should not be relied upon by prospective investors for the purposes of determining whether to purchase the securities offered hereunder.

For investors outside the United States, neither we nor any of our agents have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourself about and to observe any restrictions relating to this offering and the distribution of this prospectus.

USE OF MARKET AND INDUSTRY DATA

This prospectus includes market and industry data that has been obtained from third party sources, including industry publications, as well as industry data prepared by our management on the basis of its knowledge of and experience in the industries in which we operate (including our management’s estimates and assumptions relating to those industries based on that knowledge). Management’s knowledge of such industries has been developed through its experience and participation in those industries. Although our management believes such information to be reliable, neither we nor our management have independently verified any of the data from third party sources referred to in this prospectus or ascertained the underlying economic assumptions relied upon by such sources. In addition, the underwriters have not independently verified any of the industry data prepared by management or ascertained the underlying estimates and assumptions relied upon by management. Furthermore, references in this prospectus to any publications, reports, surveys or articles prepared by third parties should not be construed as depicting the complete findings of the entire publication, report, survey or article. The information in any such publication, report survey or article is not incorporated by reference in this prospectus.

| ii |

| (1) | https://meetanshi.com/blog/display-advertising-statistics/ | |

| (2) | https://www.nielsen.com/news-center/2015/still-recommended-by-friends-and-relatives-the-most-authentic-advertising-according-to-consumers-the-most-trusted-on-brand-websites/ | |

| (3) | https://emplifi.io/resources/blog/the-user-generated-content-stats-you-need-to-know?utm_source=pixlee.com | |

| (4) | https://morningconsult.com/wp-content/uploads/2019/11/The-Influencer-Report-Engaging-Gen-Z-and-Millennials.pdf | |

| (5) | https://www.cnn.com/business/newsfeeds/globenewswire/7812666.html | |

| (6) | https://www.bankrate.com/personal-finance/social-media-survey/ | |

| (7) | https://www.retaildive.com/news/generation-z-social-media-influence-shopping-behavior-purchases-tiktok-instagram/652576/ | |

| (8) | https://www.emarketer.com/content/us-time-spent-with-media-2021-update | |

| (9) | https://hbr.org/2022/11/does-influencer-marketing-really-pay-off | |

| (10) | https://www.prnewswire.com/news-releases/influencer-marketing-market-to-reach-199-6-billion-globally-by-2032-at-28-6-cagr-allied-market-research-301987451.html |

TRADEMARKS

We own or have rights to various trademarks, service marks and/or trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks and trade names or products in this prospectus is not intended to, and does not imply a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, TM or SM symbols, but the omission of such references is not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the right of the applicable owner of these trademarks, service marks and trade names.

| iii |

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus and may not contain all of the information that you should consider before investing in the shares. You are urged carefully to read this prospectus in its entirety, including the information under “Risk Factors” and our financial statements and related notes included elsewhere in this Prospectus before investing in our common stock.

Overview

General

As used herein, “we,” “us,” “our,” the “Company,” “Thumzup®,” means Thumzup® Media Corporation unless otherwise indicated. Thumzup® operates in a single business segment which is social media marketing. Thumzup® has a mobile iPhone and Android application called “Thumzup®” that connects brands and people who use and love these brands. For the advertiser, Thumzup® incentivizes ordinary people to become paid content creators and post authentic valuable posts on social media about the advertiser and its products.

The Company was incorporated on October 27, 2020, under the laws of the State of Nevada. Its headquarters are located in Los Angeles, CA. The Company has never been the subject of any bankruptcy or receivership. The Company has never engaged in any material reclassification, merger, or consolidation of the Company. The Company has not acquired or disposed of any material amount of assets except in the normal course of business.

In February 2022, the Company was admitted to the Over-The-Counter Venture Market quotation system (OTCQB) under the symbol TZUP. We intend to list our common stock on the Nasdaq under the symbol “TZUP”. This offering will not be consummated until we have received Nasdaq approval of our application. There is currently very limited trading of our Common Stock, and an active trading market may never develop.

Thumzup® Products and Services

The Company operates in a single business segment which is social media marketing and advertising. The Thumzup® App works on both iPhone and Android mobile operating systems and connects brands and people who use and love these brands. For the Advertiser, Thumzup® incentivizes ordinary people to become paid content Creators and post authentic valuable posts on social media about the Advertiser and its products.

The Company seeks to capitalize on nationwide-wide gig economy and business democratization trends. Immense value and opportunity have been created through the democratization of ride sharing, hospitality, finance and other industries. The Thumzup® tools are designed to facilitate this democratization trend for the consumer and the Advertiser within the online marketing and advertising space.

The Company has built the technology to support an influencer and “gig” economy community around its Thumzup® App. This technology and community are designed to generate scalable authentic product posts and recommendations for advertisers on social media. It is designed to connect advertisers with individuals who are willing to tell their friends about the advertisers’ products online and offline.

Social Media Marketing Software Technology

The Thumzup® mobile App enables Creators, to select from brands advertising on the App and get paid to post about the advertiser on social media. Once the Thumzup® Creator selects the brand and takes a photo using the Thumzup® App, the Thumzup® App posts the photo and a caption to the Creator’s social media accounts. The advertiser then reviews and approves the post for payment and the Creator can cash out whenever they choose through popular digital payment systems. For the advertiser, the Thumzup® system enables brands to get real people to promote their products to their friends. In 2023, $148 billion was spent on digital display ads in the United States and while 43% of marketers consider display ads to be the least effective channel, 84% of marketers were still investing in them(1). We feel this demonstrates a significant need among advertisers for new methods of messaging to potential customers. We believe Thumzup’s ability to scale brand messages from the general population on social media could be part of addressing this substantial need in the market.

A recent Nielsen report found 81% of consumers believe friends and family are the most reliable sources of information about products(2). According to a Emplifi article, 64% of millennials recommend a product at least once a month(3), and according to a 2019 Morning Consult survey, 86% of Gen Z and millennials would post content for monetary compensation(4). Further, according to a 2020 IZEA Insights Study, 67% of social media consumers aspire to be paid social media influencers(5). According to a 2023 Bankrate, 48% of social media users have impulsively purchased a product seen on social media(6). Lastly, 85% of Gen Z says social media impacts purchase decisions according to a 2023 Retail Dive Survey(7).

| 1 |

The average American adult spent 7 hours and 58 minutes per day using digital media in 2020 according to a 2020 eMarketer Report(8). The amount of daily usage has increased significantly since 2019, again according to an eMarketer Report(8), and the Company believes such usage will continue to accelerate. The Company empowers businesses that want to interact with these Creators and provides tools and data so they can increase consumer awareness and expand their customer bases.

In the past decade, social media platforms like Instagram, Facebook, Twitter, Pinterest, and TikTok have achieved mass worldwide consumer acceptance and created hundreds of billions of dollars in shareholder value. This worldwide viral growth demonstrates that compelling new social media platforms which present the right combination of experience and value, will attract Creators who will invest significant amounts of time on the platforms.

The Company is an early-stage entity building a new real-time platform which enables Advertisers to pay their customers and fans cash for their positive social media posts about their products and services, which in turn supports those individuals who earn money from various gig economy opportunities. The Company believes that acceptance of its App and subsequent revenue growth can be driven by empowering everyday people to make money by posting about brands and services that they already find enjoyable and attractive on social media. The Company believes that the Thumzup® App is a conduit for Advertisers to connect directly with consumers. The Company will need to secure enough advertisers to make the App an attractive platform for adoption and scalability, and to ensure that the platform is interesting enough for the Creators to return to on a regular basis. No assurance can be given that the Company will be able to achieve these results.

| (1) | https://meetanshi.com/blog/display-advertising-statistics/) | |

| (2) | https://www.nielsen.com/news-center/2015/still-recommended-by-friends-and-relatives-the-most-authentic-advertising-according-to-consumers-the-most-trusted-on-brand-websites/ | |

| (3) | https://emplifi.io/resources/blog/the-user-generated-content-stats-you-need-to-know?utm_source=pixlee.com | |

| (4) | https://morningconsult.com/wp-content/uploads/2019/11/The-Influencer-Report-Engaging-Gen-Z-and-Millennials.pdf | |

| (5) | https://www.cnn.com/business/newsfeeds/globenewswire/7812666.html | |

| (6) | https://www.bankrate.com/personal-finance/social-media-survey/ | |

| (7) | https://www.retaildive.com/news/generation-z-social-media-influence-shopping-behavior-purchases-tiktok-instagram/652576/ | |

| (8) | https://www.emarketer.com/content/us-time-spent-with-media-2021-update |

Intellectual Property

The Company owns the copyrights to the source code for the Thumzup® App on the iPhone iOS and Android operating mobile operating systems as used on the majority of mobile phone and tablet devices. The Company also owns the source code for the “backend” system that administrates the Thumzup® App, tracks payments and advertising campaigns.

The

Thumzup® thumb logo  is a registered trademark owned by Thumzup® Media Corporation, Reg.

No. 6,842,424, registered Sep. 13, 2022. On April 13, 2021, the Company filed a trademark application ser. No. 90642789 with the

U.S. Patent and Trademark Office (“USPTO”) for the word mark THUMZUP, which was granted registration on June 21, 2022,

resulting in reg. no. 6764158. Also on April 13, 2021, the Company filed a trademark application ser. No. 90642848 for the

Thumzup® logo, featuring a stylized hand with an upwardly extended thumb. Meta Platforms, Inc. (which owns and operates Facebook

and Instagram) initially filed opposition to the logo on June 30, 2022. Thumzup® agreed to not use the logo as a reaction to a

post and Meta Platforms, Inc. subsequently withdrew their opposition on August 5, 2022 and it was dismissed without

prejudice.

is a registered trademark owned by Thumzup® Media Corporation, Reg.

No. 6,842,424, registered Sep. 13, 2022. On April 13, 2021, the Company filed a trademark application ser. No. 90642789 with the

U.S. Patent and Trademark Office (“USPTO”) for the word mark THUMZUP, which was granted registration on June 21, 2022,

resulting in reg. no. 6764158. Also on April 13, 2021, the Company filed a trademark application ser. No. 90642848 for the

Thumzup® logo, featuring a stylized hand with an upwardly extended thumb. Meta Platforms, Inc. (which owns and operates Facebook

and Instagram) initially filed opposition to the logo on June 30, 2022. Thumzup® agreed to not use the logo as a reaction to a

post and Meta Platforms, Inc. subsequently withdrew their opposition on August 5, 2022 and it was dismissed without

prejudice.

| 2 |

Business Model

Advertisers purchase an ad campaign on the Thumzup® advertiser dashboard website. Once the Advertiser approves a post for payment, the platform facilitates the payment to Creators’ a monetary amount per screened post which may range from $1.00 to $1,000.00. The Thumzup® platform enables the Advertiser to screen posts so that the Advertiser only pays for posts that are commercially valuable and rewards Creators for posts that have images and text that represent the Advertiser in a positive manner.

Per Post Fee. Thumzup® Advertisers are charged a “Per Post Fee.” By way of illustration, an Advertiser that buys 100,000 posts from Thumzup®, to pay out $10 per post to Thumzup® Creators, would purchase the posts for $13.00 each or $1,300,000. The Creators in this illustration would receive a total of $1,000,000 and Thumzup® would retain $300,000 for its services. The Thumzup® platform would facilitate 100,000 posts for the Advertiser from Thumzup® Creators sharing with their friends about their endorsed products on social media.

Value Proposition

The Thumzup® App is designed to generate scalable social media authentic social media content for Advertisers. It is designed to connect Advertisers with individuals who are willing to authentically promote their products online. The Company envisions that many gig economy workers will be ideal candidates to become Creators posting on Thumzup®. Imagine a gig economy driver waiting for their next fare who takes a moment to post about the good experience they had at their lunch spot where they are waiting. Imagine a gig economy worker on a laptop at a coffee shop doing a graphic design project from a gig economy site who takes a moment to post about the coffee shop where they are working on Thumzup®. The Company believes that Thumzup® can readily provide extra income for this existing pool of gig economy workers. The Company believes these gig economy workers will be able to provide quality Thumzup® posts on social media for which Advertisers will be willing to pay.

The Thumzup® App can also facilitate digital word of mouth recommendations of products and services from people who do not need to make extra money doing gigs, who are in fact quite affluent. The Company believes that many people who are well off may also use the App to recommend products and services to their network of friends on social media, many of whom may also be affluent.

Key Metrics as of May 10, 2024

Thumzup has had paid out on 19,182 approved posts to 1,127 Thumzup users regarding 223 advertisers since inception.

Thumzup advertisers have grown by a 148% CAGR since May 10, 2023.

Since May 10, 2023, the reach of the last 15,605 posts was 25,784,957 followers. Many of these campaigns were promotional campaigns but at list price this would have been $0.006 per reach, which is below many citations for other leading social media advertising costs.

The average number of followers for an individual Thumzup user since May 10, 2023 has been about 1,600. Many users with tens of thousands of followers posted about our advertisers, including one with more than 600,000 followers. We find that even though we are targeting the general public, in aggregate a Thumzup campaign can reach an average of more than 1,600 followers per post. So, a Thumzup campaign combines the high trust factor of the general public with less followers and also draws in some professional influencers who post because they like the product at a lower cost per post than if they were hired as an influencer.

Regulatory Compliance

The Federal Trade Commission regulates and requires certain disclosures by social media influencers, specifying when disclosure is required, and how the disclosure should be presented. These rules are codified in the Code of Federal Regulations, 16 CFR Part 255. Specifically, the FTC requires that influencers disclose any financial, employment, personal, or family relationship with a brand. Influencers must disclose financial relationships and consideration paid including any money, discounted products or other benefits paid to the influencer. Creators on the Thumzup® platform are being paid to post about Thumzup® advertisers. Thumzup® puts #ad in each post made on its platform to disclose that the creator has been paid to make the post.

| 3 |

The Company does not believe its compliance with existing FTC regulations will have a material effect on capital expenditures, earnings and competitive position of the Company and its subsidiaries, for the current fiscal year and any other material future period.

Thumzup® App Workflow

|

For direct-to-consumer (“DTC”) brands, a customer might get a postcard in the box upon receiving a purchase in the mail. A postcard would inform the customer about the opportunity to get cashback by sharing a picture of the purchase with friends on social media. If the Creator takes a picture of the postcard, a link to download the Thumzup® App will appear on the customer’s phone. The illustration to the left and those below are intended as examples only and will not necessarily correlate to a final version or an amount. Actual wording and amounts will depend on agreements with Advertisers, products or brands seeking recommendations and other market factors as may be assessed by management. |

|

For physical stores and restaurants, the Company offers signage to make patrons aware that they can be paid to tell their friends about their positive experience in the store or restaurant.

|

| 4 |

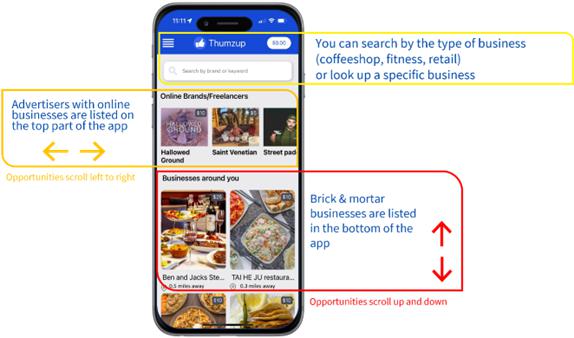

The main screen appears after a Creator enters the unique code the Company sent. The main screen enables each Creator to easily select brands, nearby restaurants, and stores that will pay the Thumzup Creator to post to friends and other followers about products and places recommended by the Creator on social media.

The main screen has seven main areas where the Creator can take action. There is a “hamburger” menu in the upper left to access administrative functions and there is a balance due to the Creator displayed on the upper right. Next, going down the screen there is a search bar, a map tool, a left to the right slider to select brands that will pay for posts, and an up and down slider to select locations nearby that will pay to post. The “hamburger” menu in the upper left gives the Creator access to change bank or payment information, to link to social media, and to invite friends. The balance due to the Creator number in the upper right has the total of monies pending and monies due but not yet transferred to the Creator.

| 5 |

|

When Creators select a brand or location tile from the main menu, the App enables them to take pictures of them enjoying the product or experience. The App then enables them to customize the caption that will be posted to social media. Once Creators submit the pictures and captions, they get uploaded and displayed on the social media account of those Creators. | |

|

Thumzup® inserts the tag required to disclose that the post is a paid promotion. If the Advertiser, has chosen to offer a discount code to the Thumzup Creator’s friends on social media, that discount code gets embedded in the post along with the offer.

When the Creator makes a new post, the post is reviewed by Thumzup on behalf of the Advertiser to assure that it meets community standards, does not include sexually explicit images or text, and that the post reflects the Advertiser in a commercially favorable light. For instance, if images are poorly lit or irrelevant to the brand, Creators may be sent text messages to the Creators giving them this feedback and explaining that the post is not due for payment.

When Creators want to receive the money they have earned they tap on the “PayMe!” selection on the App menu. The App then pays the Creator via online payment systems, such as Venmo or PayPal, the amount due from all screened posts made by that Creator.

The App enables the Creator to search for brands they like that will pay them to post. This is useful so that Thumzup® Creators can easily discover brands they like to post about. The App pays Creators to post about brands. |

| 6 |

|

In the Company’s opinion, paid posts from happy customers about how much they like an Advertiser’s goods or services offer attractive, compelling values to both Advertisers and Creators compared to traditional online advertising because those posts should yield higher response rates. |

The Thumzup® system provides Advertisers with quality control by enabling the Advertiser to review posts to make sure that the posts meet community standards and are commercially useful to the Advertiser. This helps reduce the number of people who may try to game the system to otherwise not use it properly. Thumzup® Creators can opt-in to receive text message from brands. This opt-in opportunity is valuable to Advertiser brands because text messages have higher visibility to potential customers than emails.

The Thumzup® system enables “campaign spend” to be limited by a total dollar amount as determined by the Advertiser. Once the posts that the Advertiser has paid for have been posted and approved for payment, the campaign expires and the Advertiser incurs no additional cost until it chooses to increase the amount. It also enables the Advertiser to limit the number of posts made by an individual Creator by day, week, and month. The Company believes that this feature enables more efficient budgetary control while reducing unintended cost overruns. This feature may eliminate abuse or saturation by Creators who post more than what may be commercially valuable to Advertisers.

| 7 |

Available Information:

Thumzup® is located at 11845 W. Olympic Blvd, Ste 1100W #13, Los Angeles, CA 90064. Our telephone number is (800) 403-6150 and our Internet website address is www.ThumzupMedia.com.

We file or furnish electronically with the U.S. Securities and Exchange Commission (“SEC”) annual reports on Form 10-K, quarterly reports on Form 10- Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act. We make copies of these reports available free of charge through our investor relations website as soon as reasonably practicable after we file or furnish them with the SEC. These reports are also accessible through the SEC website at www.sec.gov. Information contained on or accessible through our website www.ThumzupMedia.com is not incorporated into, and does not form a part of, this Annual Report or any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

Our Corporate Information

Thumzup Media Corporation is located at 11845 W. Olympic Blvd, Ste 1100W #13, Los Angeles, CA 90064. Our telephone number is (800) 403-6150 and our Internet website address is www.ThumzupMedia.com. We expect the website to enable the unattended onboarding of new customers in the second quarter of 2021.The information contained on, or that can be accessed through, our website is not a part of this prospectus. We have applied for a trademark for “Thumzup.” We own the source code for the Thumzup applications on the iPhone iOS and the Android. We also own the source code for the “backend” system that administrates the Thumzup app, tracks payments and advertising campaigns.

| 8 |

THE OFFERING

| Common shares offered by us: | [_______] shares of common stock. | |

| Assumed public offering price | $[_______] per share of common stock. | |

| Over-allotment option(1) | We have granted the underwriters a 45-day option to purchase up to [______] additional shares of common stock, representing 15% of the shares sold in the offering. The purchase price to be paid per additional share will be equal to the public offering price per share of common stock. | |

| Common stock outstanding before the offering(2) | 7,741,731 shares of common stock. | |

| Common stock to be outstanding after the offering(3) | [______] shares of common stock. If the underwriter’s over-allotment option is exercised in full, the total number of shares of common stock outstanding immediately after this offering would be [______]. | |

| Use of proceeds | We intend to use the net proceeds of this offering for general corporate purposes. See “Use of Proceeds.” | |

| Risk factors | Investing in our securities is highly speculative and involves a high degree of risk. You should carefully consider the information set forth in the “Risk Factors” section beginning on page 11 before deciding to invest in our securities. | |

| Proposed Nasdaq trading symbol | We intend to list our common stock on the Nasdaq under the symbol “TZUP”. This offering will not be consummated until we have received Nasdaq approval of our application. | |

| Lock-ups | Our directors and executive officers and holders of 5% or more of our outstanding common stock, will agree with the underwriter not to offer for sale, issue, sell, contract to sell, pledge or otherwise dispose of any of our common stock or securities convertible into common stock for a period of 180 days after the date of this prospectus. The Company will agree not to issue any shares of common stock or securities convertible into common stock, subject to certain exceptions, for a period of 6 months after the date of this prospectus without the consent of the underwriter. See “Underwriting.” | |

| Underwriter’s Warrants | The Company has agreed to issue to Dawson James or its designees warrants to purchase up to a total of 5.0% of the shares of common stock sold in this offering, including the exercise of the over-allotment option, if any. Such warrants and underlying shares of common stock are included in this prospectus. The warrants are exercisable at $[_____] per share (125% of the public offering price per share of Common Stock) commencing on a date which is six (6) months from the effective date of the offering under this prospectus supplement and expiring on a date which is no more than five (5) years from the commencement of sales of the offering in compliance with FINRA Rule 5110. |

| (1) | Unless otherwise indicated, all information in this prospectus assumes no exercise by the underwriter of its option to purchase up to [______] additional shares of common stock to cover over-allotments, if any. |

| (2) | Based on shares of common stock outstanding on June 17, 2024, and excludes 120,000 shares (or [_____] shares if the Underwriter exercise its over-allotment in full) underlying the warrants we will issue to the Underwriter under this offering. |

| (3) | Based on assumed public offering price of $[____] per share of common stock (the price listed on the cover page of this prospectus). |

| 9 |

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

In the tables below, we provide you with our summary consolidated financial data for the periods indicated. We have derived the following summary of our condensed financial statements for the three months ended March 31, 2024 and 2023, and the balance sheet data as of March 31, 2024 and December 31, 2023, from our financial statements appearing elsewhere in this prospectus. The historical financial data presented below is not necessarily indicative of our financial results in future periods. You should read the summary consolidated financial data in conjunction with those financial statements and the accompanying notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. Our consolidated financial statements are prepared and presented in accordance with accounting principles generally accepted in the United States, or U.S. GAAP.

| Three Months Ended March 31, 2024 | Three Months Ended March 31, 2023 | |||||||

| Selected Income Statement Data: | ||||||||

| Operating Expenses | $ | 2,521,078 | $ | 1,213,035 | ||||

| Loss from Operation | $ | (2,519,030 | ) | $ | (1,210,614 | ) | ||

| Net Loss | $ | (3,324,180 | ) | $ | (1,504,681 | ) | ||

| Net Loss per Common Share: | ||||||||

| Basic | $ | (0.47 | ) | $ | (0.24 | ) | ||

| Fully Diluted | $ | (0.47 | ) | $ | (0.24 | ) | ||

| Cash Dividend per Common Share | ||||||||

| December 31, 2023 | December 31, 2022 | |||||||

| Selected Balance Sheet Data: | ||||||||

| Cash and cash equivalents | $ | 259,212 | $ | 1,155,343 | ||||

| Capitalized software costs | $ | 142,614 | $ | - | ||||

| Total Assets | $ | 415,187 | $ | 1,160,799 | ||||

| Accounts payable and accrued expenses | $ | 65,680 | $ | 374,275 | ||||

| Shareholders’ Equity (Deficit) | $ | 349,327 | $ | 786,524 | ||||

| 10 |

RISK FACTORS

An investment in our in our common stock involves a high degree of risk. The risks described below include all material risks to our company or to investors in this offering that are known to our company. You should carefully consider such risks before participating in this offering. If any of the following risks actually occur, our business, financial condition and results of operations could be materially harmed. As a result, should a trading market develop, as to which no assurance can be given, the trading price of our common stock could decline, and you might lose all or part of your investment. When determining whether to buy our common stock, you should also refer to the other information in this prospectus, including our financial statements and the related notes included elsewhere in this prospectus.

Risks Relating to Our Business

In addition to the other information in this Annual Report, you should carefully consider the following factors in evaluating us and our business. This Annual Report on Form 10-K contains, in addition to historical information, forward-looking statements that involve risks and uncertainties, some of which are beyond our control. Should one or more of these risks and uncertainties materialize or should underlying assumptions prove incorrect, our actual results could differ materially. Factors that could cause or contribute to such differences include, but are not limited to, those discussed below, as well as those discussed elsewhere in this Form 10-K, including the documents incorporated by reference.

There are risks associated with investing in companies such as ours who are primarily engaged in research and development. In addition to risks which could apply to any company or business, you should also consider the business we are in and the following:

The Company is a recently formed company with an unproven business plan, has not yet established profitable operations and has generated minimal revenue.

The Company has principally funded its operations through the sale of equity and equity instruments, including sales of common stock of $1,573,891 and $587,863, net offering costs of $17,601 and $149,137, along with sales of preferred stock of $0 and $1,259,995, during the years ended December 31, 2023 and 2022, respectively. As the Company moves forward in developing its technology and commercializing the Thumzup® mobile application (the “Thumzup® App” or “App”), or as it responds to potential opportunities and/or adverse events, the Company’s working capital needs may change. Pending its ability to generate adequate cash flow, as to which no assurance can be given, the Company likely will continue to incur significant losses in the foreseeable future for various reasons, including unforeseen expenses, difficulties, complications, and delays, and other unknown events. As a result, the Company will require additional funding to sustain its ongoing operations and to continue its research and development activities. The Company cannot assure that its available funds will be sufficient to meet its anticipated needs for working capital and capital expenditures through any period of twelve months.

The Company’s ability to generate positive cash flow will be dependent upon its ability to recruit and retain Advertisers and Creators. The Company can give no assurances it will generate sufficient cash flows in the future to satisfy its liquidity requirements or sustain continuing operations, or that additional funding, if required, will be available when needed or, if available, on favorable terms.

The Company was formed in October 2020 and has not yet established profitable operations and has generated nominal revenue.

For the year ended December 31, 2023, we incurred a net loss available to shareholders of $3,324,180 primarily due to software research and development expenses of $513,088, marketing expenses of $855,270, professional and consulting expenses of $727,554, and general and administrative expenses of $395,624. For the year ended December 31, 2022, the Company incurred a net loss available to shareholders of $1,504,681, primarily due to software research and development expenses of $567,408, marketing expenses of $224,088, and general and administrative expenses of $418,940.

The Company expects to continue to incur losses from operations and negative cash flows, which raise substantial doubt about its ability to continue as a “going concern.”

The Company anticipates incurring additional losses until such time, if ever, it can obtain adequate Advertiser support and acceptance by Creators. Substantial additional financing will be needed to fund the Company’s development, marketing and sales activities and generally to commercialize its technology and develop brand support and Creator acceptance. These factors raise substantial doubt about the Company’s ability to continue as a going concern.

The Company will seek to obtain additional capital through the issuance of debt or equity financings or other arrangements to fund operations; however, there can be no assurance it will be able to raise needed capital under acceptable terms, if at all. The sale of additional equity may dilute existing shareholders and newly issued shares may contain senior rights and preferences compared to currently outstanding shares of Common Stock. Should the Company choose to issue debt in the future, such debt securities may contain covenants and limit the Company’s ability to pay dividends or make other distributions to shareholders. If the Company is unable to obtain such additional financing, future operations would need to be scaled back or discontinued. Due to the uncertainty in the Company’s ability to raise capital, the Company believes that there is substantial doubt as to its ability to continue as a going concern.

| 11 |

The Company’s independent registered public accounting firm’s reports have raised substantial doubt as to its ability to continue as a “going concern.”

The Company’s independent registered public accounting firm indicated in its reports on the audited financial statements for the years ended December 31, 2023 and 2022, that there is substantial doubt about the Company’s ability to continue as a going concern. A “going concern” opinion indicates that the financial statements have been prepared assuming the business will continue as a going concern and do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets, or the amounts and classification of liabilities that may result if the Company does not continue as a going concern. Therefore, prospective Investors should not rely on the Company balance sheet as an indication of the amount of proceeds that would be available to satisfy claims of creditors, and potentially be available for distribution to shareholders, in the event of liquidation. The presence of the going concern note to the Company’s financial statements may have an adverse impact on the relationships the Company is developing and plan to develop with third parties as it continues the commercialization of its products and could make it challenging and difficult for the Company to raise additional financing, all of which could have a material adverse impact on the business and prospects and result in a significant or complete loss of an investment.

There is no assurance that the Company will ever be profitable or that debt or equity financing will be available to it in the amounts, on terms, and at times deemed acceptable to the Company, if at all. The issuance of additional equity securities by the Company would result in a significant dilution in the equity interests of its Shareholders. Obtaining commercial loans, assuming those loans would be available, would increase the Company’s liabilities and future cash commitments. If the Company is unable to obtain financing in the amounts and on terms deemed acceptable to it, the Company may be unable to continue the business, as planned, and as a result may be required to scale back or cease operations, the results of which would be that shareholders would lose some or all of their investment. The financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result should the Company be unable to continue as a going concern.

The Company may not generate sufficient cash flows to cover its operating expenses.

As noted previously, the Company has incurred operating losses since inception and expects to continue to incur losses as a result of expenses related to research and continued development of its technology, marketing expense, and corporate general and administrative expenses. The Company has principally funded its operations through the sale of equity and equity instruments, including sales of common stock of $1,573,891 and $587,863, net offering costs of $17,601 and $149,137, along with sales of preferred stock of $0 and $1,259,995, during the years ended December 31, 2023 and 2022, respectively.

As of December 31, 2023, the Company had total Shareholders’ equity of $349,327, an accumulated deficit of $5,691,803, and cash and cash equivalents of approximately $259,212. Although the Company had cash on hand of $259,212 as of December 31, 2023, there is no assurance that these funds will prove adequate beyond twelve months.

In the event that the Company is unable to generate sufficient cash from its operating activities or raise additional funds, it may be required to delay, reduce or severely curtail its operations or otherwise impede the Company’s on-going business efforts, which could have a material adverse effect on its business, operating results, financial condition and long-term prospects.

Security breaches and other disruptions could compromise the Company’s information and expose it to liability, which would cause its business and reputation to suffer.

In the ordinary course of the Company’s business, it may collect and store sensitive data, including intellectual property, proprietary business information, proprietary business information of its customers, including, credit card and payment information, and personally identifiable information of customers and employees. The secure processing, maintenance, and transmission of this information is critical to the Company’s operations and business strategy. As such, the Company is subject to federal, state, provincial and foreign laws regarding privacy and protection of data. Some jurisdictions have enacted laws requiring companies to notify individuals of data security breaches involving certain types of personal data and the Company’s agreements with certain customers require it to notify them in the event of a security incident. Evolving regulations regarding personal data and personal information, in the European Union and elsewhere, including, but not limited to, the General Data Protection Regulation (GDPR), and the California Consumer Privacy Act of 2018, especially relating to classification of IP addresses, machine identification, location data and other information, may limit or inhibit the Company’s ability to operate or expand its business. Such laws and regulations require or may require the Company or its customers to implement privacy and security policies, permit consumers to access, correct or delete personal information stored or maintained by the Company or its customers, inform individuals of security incidents that affect their personal information, and, in some cases, obtain consent to use personal information for specified purposes.

| 12 |

The Company intends to take reasonable steps to protect the security, integrity and confidentiality of the information it collects, uses, stores, and discloses, and it takes steps to strengthen its security protocols and infrastructure, however, the Company’s information technology and infrastructure may be vulnerable to attacks by hackers or breached due to employee error, malfeasance, or other disruptions. The Company also could be negatively impacted by software bugs or other technical malfunctions, as well as employee error or malfeasance. Advanced cyber-attacks can be multi-staged, unfold over time, and utilize a range of attack vectors with military-grade cyber weapons and proven techniques, such as spear phishing and social engineering, leaving organizations and users at high risk of being compromised. Any such access, disclosure, or other loss of information could result in legal claims or proceedings, liability under laws that protect the privacy of personal information, regulatory penalties, a disruption of the Company’s operations, damage to its reputation, a loss of confidence in the Company’s business, early termination of its contracts and other business losses, indemnification of its customers, liability for stolen assets or information, increased cybersecurity protection and insurance costs, financial penalties, litigation, regulatory investigations and other significant liabilities, any of which could materially harm and adversely affect the Company’s business, revenues, and competitive position.

The Company is dependent on third parties to, among other things, maintain its servers, provide the bandwidth necessary to transmit content, and utilize the content derived therefrom for the potential generation of revenues.

The Company depends on third-party service providers, suppliers, and licensors to supply some of the services, hardware, software, and operational support necessary to provide some of its products and services. Some of these third parties do not have a long operating history or may not be able to continue to supply the equipment and services the Company desires in the future. If demand exceeds these vendors’ capacity, or if these vendors experience operating or financial difficulties or are otherwise unable to provide the equipment or services the Company needs in a timely manner, at its specifications and at reasonable prices, the Company’s ability to provide some products and services might be materially adversely affected, or the need to procure or develop alternative sources of the affected materials or services might delay its ability to serve its users. These events could materially and adversely affect the Company’s ability to retain and attract users, and have a material negative impact on its operations, business, financial results, and financial condition.

Because the Company does not intend to pay any cash dividends on its shares of common stock in the near future, shareholders will not be able to receive a return on their shares unless and until they sell them.

The Company intends to retain a significant portion of any future earnings to finance the development, operation and expansion of its business. The Company does not anticipate paying any cash dividends on its Common Stock in the near future. The declaration, payment, and amount of any future dividends will be made at the discretion of the Company Board of Directors, and will depend upon, among other things, the results of operations, cash flows, and financial condition, operating and capital requirements, and other factors as its Board of Directors considers relevant. There is no assurance that future dividends will be paid, and, if dividends are paid, there is no assurance with respect to the amount of any such dividend. Unless the Board of Directors determines to pay dividends, Shareholders will be required to look to appreciation of the Company’s Common Stock to realize a gain on their investment. There can be no assurance that this appreciation will occur.

The Company is dependent on key personnel.

The Company’s continued success will depend, to a significant extent, on the services of its Directors, executive management team, and key personnel. If one or more of these individuals were to leave, there is no guarantee the Company could replace them with qualified individuals in a timely or economically satisfactory manner or at all. The loss or unavailability of any or all of these individuals could harm the Company’s ability to execute its business plan, maintain important business relationships and complete certain product development initiatives, which would have a material adverse effect on its business, results of operations and financial conditions.

| 13 |

The Company may not be able to successfully execute the business plan.

The Company is raising significant amounts of capital in order to scale its operations. This will allow the Company to expand its operations and continue to build out its business model. There is no guarantee that the Company will be able to achieve or sustain the foregoing within the anticipated timeframe, or at all - even though the Company’s Directors and Officers are industry professionals. The Company may exceed the budget, encounter obstacles in development activities, or be hindered or delayed in implementing the Company’s plans, any of which could imperil the Company’s ability to execute its business plan.

The Company is a new company with a brief operating history, no revenue and an untested business plan which may not be accepted in the markets in which it intends to operate.

The Company was formed in Nevada in October 2020 and will encounter difficulties, including unforeseen difficulties as an early-stage, pre-revenue company in establishing the credibility of its brand and service.

The Company will incur net losses in the foreseeable future if it is unable to anticipate market trends and match its service offerings to market patterns. The Company’s business strategy is unproven, and it may not be successful in addressing early-stage challenges, such as establishing the Company’s position in the market and developing effective marketing of its Thumzup® App. To implement its business plan, the Company will be required to obtain additional financing but cannot guaranty that such additional financing will be available.

The Company’s prospects must be considered highly speculative, considering the risks, expenses, and difficulties frequently encountered in the establishment of a new business with an unproven business plan, specifically the risks inherent in developmental stage companies seeking to have mobile app users with limited number social media followers endorse products or services at a level that Advertisers will seek to fund and support. The Company expects to continue to incur significant operating and capital expenditures and, as a result, it expects significant net losses in the future. The Company cannot assure that it will be able to achieve positive cash flow operations or, if achieved, that positive cash can be maintained for any significant period, or at all.

Although the Company believes that its business strategy addresses an underserved but significant niche of market segment utilizing important Creators or consumers whom it defines as “micro-influencers,” the Company may not be successful in the implementation of its business strategy or its business strategy may not be successful, either of which will impede the Company’s development and growth. The Company’s business strategy involves attracting a large number of Creators who are active in social media and who are willing to make recommendations over the Thumzup® App with Advertisers who find the Company’s service cost effective in generating sales and market support. The Company’s ability to implement this business strategy is dependent on its ability to:

| ● | predict concerns of Advertisers; | |

| ● | identify and engage Advertisers; | |

| ● | convince a large number of end users to adopt the Thumzup® App; | |

| ● | establish brand recognition and customer loyalty; and | |

| ● | manage growth in administrative overhead costs during the initiation of the Company’s business efforts. |

The Company does not know whether it will be able to successfully implement its business strategy or whether the Company’s business strategy will ultimately be successful. In assessing the Company’s ability to meet these challenges, a potential Investor should consider the Company’s lack of operating history and brand recognition, its focus on nano-influencer Creators, management’s relative inexperience, the competitive conditions existing in its industry and general economic conditions and consumer discretionary spending habits. The Company’s growth is largely dependent on its ability to successfully implement its business strategy. The Company’s revenue may be adversely affected if it fails to implement its business strategy or if the Company diverts resources to a business strategy that ultimately proves unsuccessful.

| 14 |

The Company has not yet established brand identity and customer loyalty.

The Company believes that establishing and maintaining brand identity and brand loyalty is critical to attracting and retaining active users to the Thumzup® App program. In order to attract Thumzup® App Creators to the Company’s program quarter over quarter, the Company may need to spend substantial funds to create and maintain brand recognition among Thumzup® App users. If the Company’s branding efforts are not successful, its ability to earn revenues and sustain its operations will be materially impaired.

Promotion and enhancement of the Thumzup® App will also depend on the Company’s success in consistently providing high-quality, ease-of-use, fun-to-share products or recommended services to the Company’s App users. Since the Company relies on technology partners to provide portions of the service to its customers, if the Company’s suppliers do not send accurate and timely data, or if its customers do not perceive the products it offers as attractive or superior, the value of the Thumzup® brand could be harmed. Any brand impairment or dilution could decrease the attractiveness of Thumzup® to one or more of these groups, which could harm the Company’s business, results of operations and financial condition.

The Company cannot assure investors that the Thumzup® App will be accepted.

Anticipation of demand and market acceptance of service offerings are subject to a high level of uncertainty and challenges to implementation. The success of the Company’s service offerings primarily depends on the interest of Creators joining its service, as to which it cannot assure to prospective Investors. In general, achieving market acceptance for the Company’s services will require substantial marketing efforts and the expenditure of significant funds, the availability of which the Company cannot be assured, to create awareness and demand among customers. The Company has limited financial, personnel and other resources to undertake extensive marketing activities. Accordingly, no assurance can be given as to the acceptance of the Thumzup® App services or the Company’s ability to generate the revenues necessary to remain in business.

A better financed competitor may enter the marketplace, cause the Company’s market share or acceptance rates to plummet and adversely affect its ability to sustain viable operations.

While platforms are in operation for professional or large-scale influencers, to the Company’s knowledge no other company is currently offering Advertisers a scalable platform to activate everyday end-user micro-influencers who do not possess a large legion of followers. The success of the Company’s service offerings primarily depends on the interest of Creators and Advertisers joining its service, as opposed to a similar service offered by a competitor catering to celebrities or other large-scale influencers. If a direct competitor having greater human and cash resources enters the market targeting micro-influencers, the Company’s achieving market acceptance for the Thumzup® App may require additional marketing efforts and the expenditure of significant funds to create awareness and demand among customers. The Company has limited financial, personnel and other resources to undertake additional marketing activities. Accordingly, the Company may be unable to compete, its operations may suffer, and it may suffer greater losses.

Although the Company may own various intellectual property rights, these rights may not provide it with any competitive advantage.

The Company uses “Thumzup®” as a brand name, however it cannot assure prospective Investors that the services it sells, or that its brand name will not infringe on the intellectual property rights of others, or that the Company’s assertions of intellectual property rights will be enforceable or provide protection against competitive products or otherwise be commercially valuable. Moreover, enforcement of intellectual property rights typically requires time-consuming and costly litigation, and the Company cannot assure that others will not independently develop substantially similar products.

| 15 |

The Company’s future financial results are uncertain and its operating results may fluctuate, due to, among other things, consumer trends, App user activity, competition, and changing social media behaviors.

As a result of the Company’s lack of operating history, it is unable to forecast market penetration or anticipated revenue and it has little historical financial data upon which to base planned operating expenses. The Company bases its current and future expense levels on its operating plans and estimates of future expenses. The Company’s expenses are dependent in large part upon expenses associated with its proposed marketing expenditures and related overhead expenses, and the costs of hiring and maintaining qualified personnel to carry out its respective services. Sales and operating results are difficult to forecast because they will depend on the growth of the Company’s customer base, changes in customer demands based on consumer trends, the degree of utilization of its advertising services as well as the mix of products and services sold by its Advertisers.

As a result, the Company may be unable to make accurate financial forecasts and adjust its spending in a timely manner to compensate for any unexpected revenue shortfall. This inability could cause the Company’s net losses in a given quarter to be greater than expected and could further cause continuing greater losses quarter over quarter.

The Company’s ability to succeed will depend on the ability of its management to control costs.

The Company has used reasonable commercial efforts to assess and predict costs and expenses based on the and restricted cash experience of its management. However, the Company has a limited operating history upon which to base predictions. Implementing its business plan may require more employees, equipment, supplies or other expenditure items than the Company has predicted. Similarly, the cost of compensating additional management, employees and consultants or other operating costs may be more than its estimates, which could result in sustained losses.

Key personnel of the Company do not devote full time to the affairs of the Company and could allocate their time and attention to other business ventures which may not benefit the Company.

The Company’s Officers and Directors may engage in other activities. Although there are none known to the Company, the potential for conflicts of interest exists among the Officers, Directors, and affiliated persons for future business opportunities that may not be presented to the Company. The Company’s Officers and Directors may have conflicts of interests in allocating time, services, and functions between the other business ventures in which those persons may be or become involved. The Company’s Officers and Directors however believe that the business will have sufficient staff, consultants, employees, agents, contractors, and managers to adequately conduct its business.

The Company’s Officers, Directors, and employees are entitled to receive compensation, payments and reimbursements, regardless of whether it operates at a profit or a loss.

Any compensation received by the Officers, management personnel, and Directors, and for the Company’s founders will be determined from time to time by the Board of Directors. The Company’s Officers, Directors and management personnel will be reimbursed for any out-of-pocket expenses incurred on their behalf.

Combination or “layering” of multiple risk factors may significantly increase the risk of loss on share of the Company’s common stock.

Although the various risks discussed in this prospectus are generally described separately, investors should consider the potential effects of the interplay of multiple risk factors. Where more than one significant risk factor is present, the risk of loss to an investor may be significantly increased. In considering the potential effects of layered risks, an Investor should carefully review the descriptions of the shares.

Our business is sensitive to consumer spending, inflation and economic conditions.

Consumer purchases of discretionary retail items and restaurants may be adversely affected by national and regional economic, market and other conditions such as employment levels, salary and wage levels, the availability of consumer credit, inflation, high interest rates, high tax rates, high fuel prices, the threat of a pandemic or other health crisis (such as COVID-19) and consumer confidence with respect to current and future economic, market and other conditions. Consumer purchases may decline during recessionary periods or at other times when unemployment is higher or disposable income is lower. These risks may be exacerbated for retailers such as our Advertisers. Consumer willingness to make discretionary purchases may decline, may stall or may be slow to increase due to national and regional economic conditions. Our financial performance is particularly susceptible to economic and other conditions in regions or states where we have a significant presence. There remains considerable uncertainty and volatility in the national and global economy. Further or future slowdowns or disruptions in the economy, market and other conditions could adversely affect mall traffic and new mall and shopping center development and could materially and adversely affect us and our business strategy. We may not be able to sustain or increase our current net sales if there is a decline in consumer spending.

| 16 |

A deterioration of economic conditions and future recessionary periods may exacerbate the other risks faced by our business, including those risks we encounter as we attempt to execute our business plans. Such risks could be exacerbated individually or collectively.

Russia’s Invasion of Ukraine may negatively impact our business.

On February 24, 2022, Russia launched an invasion of Ukraine which has resulted in increased volatility in various financial markets and across various sectors. The United States and other countries, along with certain international organizations, have imposed economic sanctions on Russia and certain Russian individuals, banking entities and corporations as a response to the invasion. The extent and duration of the military action, resulting sanctions and future market disruptions in the region are impossible to predict. Moreover, the ongoing effects of the hostilities and sanctions may not be limited to Russia and Russian companies and may spill over to and negatively impact other regional and global economic markets of the world, including Europe and the United States. The ongoing military action along with the potential for a wider or nuclear conflict could further increase financial market volatility and cause negative effects on regional and global economic markets, industries, and companies. It is not currently possible to determine the severity of any potential adverse impact of this event on the financial condition of any of the Company’s securities, or more broadly, upon the global economy.

Several of our outsourced developers are based in Pakistan and our product development could be impacted by conflict in the Middle East.

Pakistan’s economy is heavily dependent on exports and subject to high interest rates, economic volatility, inflation, currency devaluations, high unemployment rates and high level of debt and public spending. There is also the possibility of nationalization, expropriation or confiscatory taxation, security market restrictions, political changes, government regulation, a conflict with India, or diplomatic developments (including war or terrorist attacks), which could affect adversely the economy of Pakistan or the ability of the Company to continue developing its platform. As an emerging country, Pakistan’s economy is susceptible to economic, political and social instability; unanticipated economic, political or social developments could impact economic growth. Pakistan is also subject to natural disaster risk. In addition, recent political instability and protests in the Middle East have caused significant disruptions to many industries. Pakistan has recently seen elevated levels of ethnic and religious conflict, in some cases resulting in violence or acts of terrorism. Continued political and social unrest in these areas may negatively affect the Company.

Changes in Instagram, PayPal, Apple App Store, or Google Play Store policies could disrupt our business operations. In addition, our third-party service providers may decline to provide services due to their policies, or cease to provide services previously provided to us due to a change of policy.

We rely on the Apple App Store and the Google Play Store to distribute our mobile applications, PayPal and Venmo to pay our Creators, while Instagram is currently the sole channel through which Creators can make posts utilizing our platform. Should these third parties change policy or modify interpretations of existing policies, it may cause disruptions to our business and have a material adverse effect on our business and financial condition.

We rely on third-party internal and outsourced software to run our critical development and information systems. As a result, any sudden loss, disruption or unexpected costs to maintain these systems could significantly increase our operational expense and disrupt the management of our business operations.

We rely on third-party software to run our critical development and information systems. We also depend on our software vendors to provide long-term software maintenance support for our information systems. Software vendors may decide to discontinue further development, integration or long-term software maintenance support for our information systems, in which case we may need to abandon one or more of our current information systems and migrate some or all of our development and information systems, thus increasing our operational expense as well as disrupting the management of our business operations.

Cyber security breaches of our systems and information technology could adversely impact our ability to operate.

We need to protect our own internal trade secrets, work product for our clients, and other business confidential information from disclosure. We face the threat to our computer systems of unauthorized access, computer hackers, computer viruses, malicious code, organized cyber-attacks and other security problems and system disruptions, including possible unauthorized access to our and our clients’ proprietary or classified information.

| 17 |

We rely on industry-accepted security measures and technology to maintain securely all confidential and proprietary information on our information systems. We have devoted and will continue to devote significant resources to the security of our computer systems, but they are still vulnerable to these threats. A user who circumvents security measures can misappropriate confidential or proprietary information, including information regarding us, our personnel and/or our clients, or cause interruptions or malfunctions in operations. Our industry has not been immune from organized cyber-attacks from persons seeking a ransom as a condition of releasing access to the firm’s computer systems. As a result, we can be required to expend significant resources to protect against the threat of these system disruptions and security breaches or to alleviate problems caused by these disruptions and breaches. Any of these events can damage our reputation and have a material adverse effect on our business, financial condition, results of operations and cash flows.

Risks Related to the Common Stock

There can be no assurance that our Common Stock will ever be approved for listing on a national securities exchange. Failure to develop or maintain an active trading market could negatively affect the value of our Common Stock and make it difficult or impossible for investors to sell their shares in a timely manner.

There is currently very limited trading of our Common Stock, and an active trading market may never develop. Our Common Stock is quoted on the OTCQB tier of the OTC Markets. The OTCQB tier of the OTC Markets is a thinly traded market and lacks the liquidity of certain other public markets with which some investors may have more experience. While we remain determined to work towards getting our securities listed on a national exchange, there can be no assurance that this will occur. As a result, we may never develop an active trading market for our securities which may limit our investors’ ability to liquidate their investments.

The Company is controlled by its Chairman/Board of Directors, Chief Executive Officer, President, and additional Officers of the Company.