As filed with the United States Securities and Exchange Commission on September 8, 2023.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

Delaware |

| 6770 |

| 86-2556699 |

(State or other Jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

400 Skokie Blvd, Suite 820

Northbrook, Illinois 60062

Telephone: (847) 757-3812

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jerry Hyman | Keith Jaffee |

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Christian O. Nagler, P.C. | Mark D. Wood, Esq. |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective and all other conditions to the business combination described in the enclosed joint proxy statement/consent solicitation statement/prospectus have been satisfied or waived.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

☒ | Smaller reporting company | |||

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

The information in this preliminary joint proxy statement/consent solicitation statement/prospectus is not complete and may be changed. Banyan Acquisition Corporation may not issue the securities offered by this preliminary proxy statement/ prospectus until the registration statement filed with the Securities and Exchange Commission, of which this preliminary joint proxy statement/consent solicitation statement/prospectus is a part, is declared effective. This preliminary joint proxy statement/consent solicitation statement/prospectus does not constitute an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale of these securities is not permitted.

PRELIMINARY — SUBJECT TO COMPLETION, DATED SEPTEMBER 8, 2023

PROXY STATEMENT FOR

SPECIAL MEETING OF BANYAN ACQUISITION CORPORATION

CONSENT SOLICITATION STATEMENT FOR STOCKHOLDERS OF PINSTRIPES, INC.

PROSPECTUS FOR UP TO 48,185,117 SHARES OF COMMON STOCK OF BANYAN ACQUISITION CORPORATION

(WHICH WILL BE RENAMED PINSTRIPES HOLDINGS, INC. IN CONNECTION WITH THE BUSINESS COMBINATION)

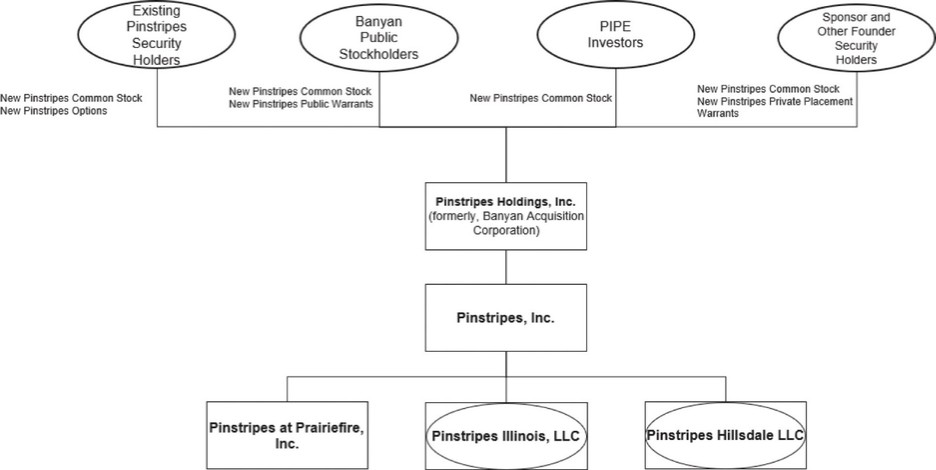

The board of directors of Banyan Acquisition Corporation, a Delaware corporation (“Banyan”), has approved the transactions (collectively, the “Business Combination”) contemplated by that certain Business Combination Agreement, dated as of June 22, 2023 (as amended, supplemented or otherwise modified from time to time, the “Business Combination Agreement”), by and among Banyan, Panther Merger Sub Inc., a Delaware corporation and a wholly owned subsidiary of Banyan (“Merger Sub”), and Pinstripes, Inc., a Delaware corporation (“Pinstripes”), a copy of which is attached to this joint proxy statement/consent solicitation statement/prospectus as Annex A. As described in this joint proxy statement/consent solicitation statement/prospectus, Banyan’s stockholders are being asked to consider and vote upon the Business Combination, among other items. As used in this joint proxy statement/consent solicitation statement/prospectus, “New Pinstripes” refers to Banyan after giving effect to the consummation of the Business Combination.

In connection with the Business Combination, among other things, (i) the governing documents of Banyan will be replaced by governing documents for New Pinstripes, (ii) Banyan will change its name to “Pinstripes Holdings, Inc.,” (iii) each of the then-issued and outstanding shares of Class A common stock, par value $0.0001 per share, of Banyan (the “Banyan Class A Common Stock”) will be converted, on a one-for-one basis, into a share of common stock of New Pinstripes, par value $0.0001 per share (“New Pinstripes Common Stock”), (iv) each of the then-issued and outstanding shares of Class B common stock, par value $0.0001 per share, of Banyan will be converted, on a one-for-one basis, into a share of New Pinstripes Common Stock, and (v) each then-issued and outstanding whole warrant exercisable for one share of Banyan Class A Common Stock will become exercisable for one share of New Pinstripes Common Stock at an exercise price of $11.50 per share on the terms and conditions set forth in the Warrant Agreement, dated as of January 19, 2022, by and between Banyan and Continental Stock Transfer & Trust Company, as warrant agent (as amended or amended and restated from time to time). In connection with clauses (iii) and (v) of this paragraph, each issued and outstanding unit of Banyan that has not been previously separated into the underlying Banyan Class A Common Stock and the underlying Banyan warrants will be canceled and will entitle the holder thereof to one share of New Pinstripes Common Stock and one-half of one New Pinstripes warrant.

On the date of closing of the Business Combination (the “Closing”), Merger Sub will merge with and into Pinstripes (the “Merger”), with Pinstripes being the surviving corporation of the Merger (the date and time that the Merger becomes effective being referred to as the “Effective Time”), and, as a result of which, the surviving company will become a wholly owned subsidiary of Banyan.

In accordance with the terms and subject to the conditions of the Business Combination Agreement, immediately prior to the Effective Time, each outstanding share of Pinstripes preferred stock will be converted into shares of Pinstripes common stock, par value $0.01 per share (“Pinstripes Common Stock”), in accordance with the governing documents of Pinstripes, and each warrant and convertible note of Pinstripes will be automatically exercised for, or convert into, shares of Pinstripes Common Stock in accordance with their respective terms. At the Effective Time, each share of Pinstripes Common Stock (including as a result of the conversions specified above, but excluding any dissenting shares and cancelled treasury stock and shares of Pinstripes Common Stock issued in connection with the conversion of the Series I Convertible Preferred Stock of Pinstripes) will be automatically cancelled and extinguished and converted into the right to receive shares of New Pinstripes Common Stock, determined in accordance with the Business Combination Agreement, at an exchange ratio of approximately 2.33 shares of New Pinstripes Common Stock for each share of Pinstripes Common Stock. In addition, each outstanding share of Pinstripes Common Stock received upon conversion of Series I Convertible Preferred Stock of Pinstripes will be automatically cancelled and extinguished and converted into the right to receive shares of New Pinstripes Common Stock determined in accordance with the Business Combination Agreement, based on an exchange ratio of 2.5 shares of New Pinstripes Common Stock for each share of Pinstripes Common Stock.

At or prior to the Closing of the Business Combination, Banyan may enter into one or more equity financings with aggregate gross proceeds of up to $53,733,800. The proceeds of such financings will be used to satisfy the minimum cash condition of $75,000,000 contained in the Business Combination Agreement.

The Banyan Class A Common Stock is currently listed on the New York Stock Exchange (the “NYSE”) under the symbol “BYN.” Banyan will apply for listing, to be effective at the time of the Closing, of New Pinstripes Common Stock and the public and private warrants of New Pinstripes on the NYSE under the proposed symbols “PNST” and “PNST WS,” respectively. It is a condition of the consummation of the Business Combination that Banyan’s initial listing application with the NYSE (or the Nasdaq Stock Market LLC (“Nasdaq”)) in connection with the Business Combination shall have been conditionally approved, and immediately following the Effective Time, Banyan will satisfy any applicable initial and continued listing requirements of the NYSE (or Nasdaq), and the New Pinstripes Common Stock issued in connection with the Business Combination shall have been approved for listing on the NYSE (or Nasdaq). However, there can be no assurance such listing condition will be met or that Banyan will obtain such approval from the NYSE (or Nasdaq). If such listing condition is not met or if such approval is not obtained, the Business Combination will not be consummated unless the stock exchange approval condition set forth in the Business Combination Agreement is waived by the applicable parties.

Banyan reserves the right to postpone or adjourn the stockholder meeting on one or more occasions in accordance with the terms and conditions of the Business Combination Agreement.

This joint proxy statement/consent solicitation statement/prospectus provides stockholders of Banyan with detailed information about the Business Combination and other matters to be considered at the special meeting of Banyan. It also includes information about Banyan and Pinstripes. We encourage you to read this entire joint proxy statement/consent solicitation statement/prospectus, including the Annexes and other documents referred to therein, carefully and in their entirety. You should also carefully consider the risk factors described in the section titled “Risk Factors” beginning on page 49 of this joint proxy statement/consent solicitation statement/prospectus.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THIS JOINT PROXY STATEMENT/CONSENT SOLICITATION STATEMENT/PROSPECTUS, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS JOINT PROXY STATEMENT/CONSENT SOLICITATION STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

This joint proxy statement/consent solicitation statement/prospectus is dated , 2023, and is first being mailed to Banyan’s stockholders on or about , 2023.

BANYAN ACQUISITION CORPORATION

400 Skokie Blvd, Suite 820

Northbrook, Illinois 60062

To the Stockholders of Banyan Acquisition Corporation:

You are cordially invited to attend a special meeting of stockholders (the “Special Meeting”) of Banyan Acquisition Corporation, a Delaware corporation (“Banyan”), which will be held virtually at https://www.cstproxy.com/ [a.m./p.m.], Eastern Time, on , 2023, or at such other date and at such other place to which the meeting may be postponed or adjourned. We are planning for the Special Meeting to be held virtually over the internet.

You or your proxyholder will be able to attend and vote at the Special Meeting by visiting https://www.cstproxy.com/ and using a control number assigned by Continental Stock Transfer & Trust Company. To register and receive access to the virtual meeting, registered stockholders and beneficial holders of Banyan stock (i.e., those holding shares through a stock brokerage account or by a bank or other holder of record) will need to follow the instructions applicable to them provided in the accompanying joint proxy statement/consent solicitation statement/prospectus.

On June 22, 2023, Banyan entered into a Business Combination Agreement (the “Business Combination Agreement”) with Panther Merger Sub Inc., a Delaware corporation (“Merger Sub”), and Pinstripes, Inc., a Delaware corporation (“Pinstripes”). The transactions contemplated by the Business Combination Agreement are referred to herein as the “Business Combination.” You are being asked to consider and vote upon a proposal, which is referred to herein as the “Business Combination Proposal,” to approve and adopt (i) the Business Combination Agreement, a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex A, and (ii) the Business Combination.

As further described in the accompanying joint proxy statement/consent solicitation statement/prospectus, subject to the terms and conditions of the Business Combination Agreement, the following transactions will occur on the date of closing: (i) Merger Sub will merge with and into Pinstripes (the “Merger”) with Pinstripes being the surviving corporation of the merger and, as a result of which, Banyan will become the parent company of Pinstripes (the time at which the Merger becomes effective is being referred to herein as the “Effective Time”), (ii) the governing documents of Banyan will be replaced by governing documents for New Pinstripes (as defined below), (iii) upon the effectiveness of the Business Combination (the “Closing”), Banyan will change its name to “Pinstripes Holdings, Inc.” (“New Pinstripes”), (iv) each of the then-issued and outstanding shares of Class A common stock, par value $0.0001 per share, of Banyan (the “Banyan Class A Common Stock”) will be converted, on a one-for-one basis, into a share of common stock of New Pinstripes (“New Pinstripes Common Stock”), (v) each of the then-issued and outstanding shares of Class B common stock, par value $0.0001 per share, of Banyan (the “Banyan Class B Common Stock,” and together with the Banyan Class A Common Stock, the “Banyan Common Stock”) will be converted, on a one-for-one basis, into a share of New Pinstripes Common Stock, and (vi) each then-issued and outstanding whole warrant exercisable for one share of Banyan Class A Common Stock will become exercisable for one share of New Pinstripes Common Stock at an exercise price of $11.50 per share on the terms and conditions set forth in the Warrant Agreement, dated as of January 19, 2022, by and between Banyan and Continental Stock Transfer & Trust Company, as warrant agent (as amended or amended and restated from time to time). In connection with clauses (iv) and (vi) of this paragraph, each issued and outstanding unit of Banyan that has not been previously separated into the underlying Banyan Class A Common Stock and the underlying Banyan warrants will be canceled and will entitle the holder thereof to one share of New Pinstripes Common Stock and one-half of one New Pinstripes warrant.

Furthermore, in accordance with the Business Combination Agreement, immediately prior to the Effective Time, all outstanding shares of Pinstripes preferred stock will convert into shares of Pinstripes common stock, par value $0.01 per share (“Pinstripes Common Stock”), in accordance with the governing documents of Pinstripes, and all warrants and convertible notes of Pinstripes will be automatically exercised for, or convert into, shares of Pinstripes Common Stock in accordance with their respective terms. At the Effective Time, (i) each outstanding share of Pinstripes Common Stock (including as a result of the conversions specified above, but excluding any dissenting shares and cancelled treasury stock and shares of Pinstripes Common Stock issued in connection with the conversion of the Series I Convertible Preferred Stock of Pinstripes) will be automatically cancelled and extinguished and converted into the right to receive shares of New Pinstripes Common Stock, determined in accordance with the Business Combination Agreement, based on an exchange ratio of approximately 2.33 shares of New Pinstripes Common Stock for each share of Pinstripes Common Stock, (ii) each outstanding share of Pinstripes Common Stock received upon conversion of Series I Convertible Preferred Stock of Pinstripes will be automatically cancelled and extinguished and converted into the right to receive shares of New Pinstripes Common Stock determined in accordance with the Business Combination Agreement, based on an exchange ratio of 2.5 shares of New Pinstripes Common Stock for each share of Pinstripes Common Stock and (iii) each outstanding option of Pinstripes (whether vested or unvested) will be assumed by New Pinstripes and substituted for an option to purchase shares of New Pinstripes Common

Stock. For additional information regarding the consideration payable under the Business Combination Agreement, see the section in the accompanying proxy statement entitled “Proposal No. 1 — The Business Combination Proposal — Consideration to be Received in the Business Combination.”

At or prior to the Closing of the Business Combination, Banyan may enter into one or more equity financings with aggregate gross proceeds of up to $53,733,800. The proceeds of such financings will be used to satisfy the minimum cash condition of $75,000,000 contained in the Business Combination Agreement.

In connection with the foregoing and concurrently with the execution of the Business Combination Agreement, Banyan Acquisition Sponsor LLC, a Delaware limited liability company (the “Sponsor”), George Courtot, Bruce Lubin, Otis Carter, Kimberley Annette Rimsza, Matt Jaffee and Brett Biggs (together with the Sponsor, the “Sponsor Holders”) entered into a Sponsor Letter Agreement (the “Sponsor Letter Agreement”), pursuant to which, among other things, the Sponsor Holders have agreed, (i) for no additional consideration to waive their respective redemption rights in connection with the consummation of the Business Combination with respect to any Banyan Class A Common Stock and Banyan Class B Common Stock they may hold, (ii) to subject two-thirds of the Banyan Class B Common Stock (or Banyan Class A Common Stock, if converted) held by the Sponsor Holders to certain vesting conditions and forfeiture and (iii) to vote any shares of Banyan Class A Common Stock or Banyan Class B Common Stock held by them in favor of the Business Combination Proposal and the other proposals to be considered at the Special Meeting. Currently, the Sponsor Holders hold 64.4% of issued and outstanding Banyan Common Stock. For additional information regarding the Sponsor Letter Agreement, see the section entitled “Proposal No. 1 — The Business Combination Proposal — Related Agreements — Sponsor Letter Agreement” in the accompanying joint proxy statement/consent solicitation statement/prospectus.

In addition to the Business Combination Proposal, Banyan stockholders are being asked to consider and vote upon (a) a proposal to approve the proposed certificate of incorporation of New Pinstripes (the “Proposed Charter”), a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex B (the “Charter Proposal”), (b) on a nonbinding advisory basis, proposals related to material differences between Banyan’s existing amended and restated certificate of incorporation and the Proposed Charter (the “Governance Proposals”), (c) a proposal to approve, for purpose of complying with Section 312.03 of the NYSE Listed Company Manual, the issuance of shares of New Pinstripes Common Stock in connection with the Business Combination (the “Listing Proposal”), (d) a proposal to approve and adopt the New Pinstripes Equity Incentive Plan, a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex D (the “Equity Incentive Plan Proposal”), (e) a proposal to approve and adopt the New Pinstripes Employee Stock Purchase Plan, a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex E (the “ESPP Proposal”), and (f) a proposal to adjourn the Special Meeting to a later date or dates to the extent necessary (the “Adjournment Proposal”).

Each of the Business Combination Proposal, the Charter Proposal, the Listing Proposal and the Equity Incentive Plan Proposal (collectively, the “Condition Precedent Proposals”) is conditioned on the approval and adoption of each of the other Condition Precedent Proposals, and the Business Combination will be consummated only if each of the Condition Precedent Proposals is approved by the requisite number of Banyan stockholders. If the Business Combination Proposal is not approved, the other proposals (except the Adjournment Proposal) will not be presented to the Banyan stockholders for a vote. The Adjournment Proposal is not conditioned on the approval of any other proposal. Each of these proposals is more fully described in the accompanying joint proxy statement/consent solicitation statement/prospectus, which each Banyan stockholder is encouraged to read carefully and in its entirety.

The board of directors of Banyan (the “Banyan Board”) has determined that each of the Condition Precedent Proposals is advisable and in the best interests of Banyan and its stockholders. The Banyan Board approved the Business Combination Agreement and the transactions contemplated thereby and recommends that Banyan’s stockholders vote “FOR” the Business Combination Proposal, “FOR” the Charter Amendment Proposal, “FOR” the Governance Proposals, “FOR” the Listing Proposal, “FOR” the Equity Incentive Plan Proposal, “FOR” the ESPP Proposal, and “FOR” the Adjournment Proposal (if necessary). Each such proposal is described in the accompanying joint proxy statement/consent solicitation statement/prospectus.

Banyan’s directors and officers may have financial interests in the Business Combination that are different from, or in addition to, their interests as stockholders of Banyan and the interests of stockholders of Banyan generally. The existence of financial and personal interests of Banyan’s directors and officers may result in conflicts of interest, including a conflict between what may be in the best interests of Banyan and its stockholders and what may be best for a director’s personal interests when determining to recommend that the Banyan stockholders vote for the aforementioned proposals. See the sections in the accompanying joint proxy statement/consent solicitation statement/prospectus entitled “Proposal No. 1 — The Business Combination Proposal — Interests of Certain Persons in the Business Combination” and “Beneficial Ownership of Securities.”

Subject to the terms and provisions of the Business Combination Agreement, Banyan reserves the right at any time to cancel the Special Meeting and not to submit to its stockholders any of the aforementioned proposals. In the event the Special Meeting is canceled, Banyan will liquidate and dissolve in accordance with its certificate of incorporation. In additional, subject to the terms and provisions of the Business Combination Agreement, Banyan reserves the right to postpone or adjourn the Special Meeting on one or more occasions to a later date.

Banyan’s units, the Banyan Class A Common Stock, and Banyan’s redeemable warrants are traded on the New York Stock Exchange (the “NYSE”) under the symbols “BYN.U,” “BYN” and “BYN WS,” respectively. At the closing of the Business Combination, the units will separate into their component shares of common stock and warrants so that the units will no longer trade. New Pinstripes will apply to list, to be effective at the time of the Closing, its common stock and warrants on the NYSE (or the Nasdaq Stock Market LLC) under the symbols “PNST” and “PNST WS,” respectively.

Only holders of record of shares of Banyan Class A Common Stock and shares of Banyan Class B Common Stock at the close of business on , 2023 (the “Record Date”) are entitled to notice of and to vote and have their respective votes counted at the Special Meeting and any adjournments or postponements of the Special Meeting. A complete list of Banyan’s stockholders of record entitled to vote at the Special Meeting will be available for 10 days before the Special Meeting at Banyan’s principal executive offices for inspection by its stockholders during ordinary business hours for any purpose related to the Special Meeting and electronically during the Special Meeting at https://www.cstproxy.com/ .

The accompanying joint proxy statement/consent solicitation statement/prospectus provides you with detailed information about the Business Combination and other matters to be considered at the Special Meeting. We urge you to read this document and the documents incorporated herein by reference carefully and in their entirety. See the section entitled “Risk Factors” in the accompanying joint proxy statement/consent solicitation statement/prospectus for a discussion of the risks you should consider in evaluating the proposed Business Combination and how it will affect you. Events occurring prior to the Special Meeting may require Banyan to supplement or amend the accompanying joint proxy statement/consent solicitation statement/prospectus, in which case, you are encouraged to read such supplement or amendment along with the accompanying joint proxy statement/consent solicitation statement/prospectus.

Your vote is very important. To ensure your representation at the Special Meeting, please complete and return the enclosed proxy card or submit your proxy by following the instructions contained in the accompanying joint proxy statement/consent solicitation statement/prospectus and on your proxy card. Please submit your proxy promptly whether or not you expect to participate in the Special Meeting. Submitting a proxy now will NOT prevent you from being able to virtually vote online during the Special Meeting. If you hold your shares in “street name,” you should instruct your broker, bank or other nominee how to vote in accordance with the voting instruction form you receive from your broker, bank or other nominee. If you have any questions regarding the accompanying joint proxy statement/consent solicitation statement/prospectus, you may contact Morrow Sodali LLC, Banyan’s proxy solicitor, by calling (800) 662-5200 (toll-free), or banks and brokers can call (203) 658-9400, or by emailing .info@investor.morrowsodali.com. If you return your proxy card signed and without an indication of how you wish to vote, your shares will be voted in favor of each of the aforementioned proposals.

Pursuant to Banyan’s certificate of incorporation, a holder of Banyan Class A Common Stock (such holder, a “Public Stockholder”) may request that Banyan redeem all or a portion of such Banyan Class A Common Stock for cash if the Business Combination is consummated. These redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Banyan’s transfer agent in order to validly redeem its shares. Public Stockholders may elect to redeem their respective shares of Banyan Class A Common Stock whether they vote “For” or “Against” the Business Combination Proposal or abstain from voting. If the Business Combination is not consummated, the shares of Banyan Class A Common Stock will be returned to the respective holder, broker or bank. If the Business Combination is consummated, and if a Public Stockholder properly exercises its right to redeem all or a portion of the Banyan Class A Common Stock that it holds and timely tenders or delivers its applicable shares to Banyan’s transfer agent, Banyan will redeem such Banyan Class A Common Stock for a per-share price, payable in cash, equal to the pro rata portion of the trust account established at the consummation of Banyan’s initial public offering, calculated as of two business days prior to the consummation of the Business Combination, including interest earned on the funds held in such trust account (net of taxes payable).

Notwithstanding the foregoing, a Public Stockholder, together with any such stockholder’s affiliates or any other person or entity with whom such stockholder is acting in concert or as a “group” (as defined in Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from seeking redemption rights with respect to more than an aggregate of 15% of the Banyan Class A Common Stock sold in Banyan’s initial public offering.

For illustrative purposes, as of , 2023, the most recent practicable date prior to the date of the accompanying joint proxy statement/consent solicitation statement/prospectus, the redemption price per share would have amounted to approximately $ , based on the aggregate amount on deposit in the aforementioned trust account of approximately $ as of , 2023 (including interest earned on the funds held in such trust account and not previously released to Banyan to pay its taxes), divided by the total number of then-outstanding Public Shares (as defined in the accompanying joint proxy statement/consent solicitation statement/prospectus). If a Public Stockholder exercises its redemption rights in full, then it will be electing to exchange its Banyan Class A Common Stock for cash and will no longer own Banyan Class A Common Stock. See “Special Meeting of Banyan Stockholders — Redemption Rights” in the accompanying joint proxy statement/consent solicitation statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your Banyan Class A Common Stock for cash. A Public Stockholder must complete the procedures for electing to redeem its Banyan Class A Common Stock in the manner described in the accompanying joint proxy statement/consent solicitation statement/prospectus prior to 5:00 p.m., Eastern Time, on , 2023 (two business days before the initially scheduled date of the Special Meeting) in order for its shares to be redeemed.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST ELECT TO HAVE BANYAN REDEEM YOUR SHARES FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE AFOREMENTIONED TRUST ACCOUNT AND TENDER YOUR SHARES TO BANYAN’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE INITIALLY SCHEDULED DATE OF THE SPECIAL MEETING. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR STOCK CERTIFICATES TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL NOT BE REDEEMED FOR CASH. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

On behalf of the Banyan Board, I would like to thank you for your support of Banyan and look forward to a successful completion of the Business Combination.

Very truly yours, | |

Jerry Hyman | |

Chairman of the Board of Directors of |

BANYAN ACQUISITION CORPORATION

400 Skokie Blvd, Suite 820

Northbrook, Illinois 60062

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2023

TO THE STOCKHOLDERS OF BANYAN ACQUISITION CORPORATION:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders (the “Special Meeting”) of Banyan Acquisition Corporation, a Delaware corporation (“Banyan”), will be held at [a.m./p.m.], Eastern Time, on , 2023. We are planning for the Special Meeting to be held virtually over the internet. You are cordially invited to attend the Special Meeting online by visiting https://www.cstproxy.com/ and using a control number assigned by Continental Stock Transfer & Trust Company. To register and receive access to the Special Meeting, registered stockholders and beneficial holders of Banyan stock (those holding shares through a stock brokerage account or by a bank or other holder of record) will need to follow the instructions applicable to them provided in the accompanying proxy statement.

At the Special Meeting, you will be asked to consider and vote on the following proposals:

| 1. | Proposal No. 1 — The Business Combination Proposal — To consider and vote upon a proposal to adopt and approve the Business Combination Agreement (the “Business Combination Agreement”), dated as of June 22, 2023, by and among Banyan, Panther Merger Sub Inc., a Delaware corporation (“Merger Sub”), and Pinstripes, Inc., a Delaware corporation (“Pinstripes”), pursuant to which, among other things, Merger Sub shall merge with and into Pinstripes (the “Merger”), with Pinstripes being the surviving corporation of the Merger, and, as a result of which, it will become a wholly owned subsidiary of Banyan (Banyan, after giving effect to the consummation of the Business Combination (as defined below), being referred to herein as “New Pinstripes”). A copy of the Business Combination Agreement is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex A. Proposal No. 1 is referred to as the “Business Combination Proposal.” |

| 2. | Proposal No. 2 — The Charter Amendment Proposal — To consider and vote upon a proposal to approve the proposed amended and restated certificate of incorporation of New Pinstripes (as defined below) in the form attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex B (the “Proposed Charter”). Proposal No. 2 is referred to as the “Charter Amendment Proposal.” |

| 3. | Proposal No. 3 — The Governance Proposals — To consider and vote upon, on a non-binding advisory basis, certain governance provisions in the Proposed Charter, presented separately in accordance with the U.S. Securities and Exchange Commission (“SEC”) requirements (Proposals No. 3.A through 3.D). Proposal No. 3 is referred to as the “Governance Proposals”: |

| ● | Proposal No. 3.A: An amendment to change the authorized capital stock of Banyan from (i) 240,000,000 shares of Class A common stock, par value $0.0001 per share (the “Banyan Class A Common Stock”), 60,000,000 shares of Class B common stock, par value $0.0001 per share (the “Banyan Class B Common Stock,” and together with the Banyan Class A Common Stock, the “Banyan Common Stock”) and 1,000,000 shares of Banyan preferred stock, each with par value $0.0001 per share, to (ii) shares of New Pinstripes common Stock and shares of New Pinstripes preferred stock, each with par value $0.0001 per share. |

| ● | Proposal No. 3.B: An amendment to require that the affirmative vote of holders of at least 662/3% of the voting power of all then-outstanding shares of New Pinstripes common stock entitled to vote generally in the election of directors, voting together as a single class, to adopt, amend or repeal the bylaws of New Pinstripes and the provisions in the Proposed Charter related to New Pinstripes common stock, the board of directors, the bylaws, stockholders, limitation on liability and indemnification of directors and officers, forum selection and amendments to the Proposed Charter. |

| ● | Proposal No. 3.C: An amendment to permit the removal of a director only for cause and only by the affirmative vote of the holders of at least 662/3% of the voting power of all then outstanding shares of capital stock entitled to vote generally in the election of directors, voting together as a single class. |

| ● | Proposal No. 3.D: An amendment to allow the holders of 331/3% of the voting power of all outstanding shares of capital stock of New Pinstripes entitled to vote at such meeting to constitute a quorum. |

| 4. | Proposal No. 4 — The Listing Proposal — To consider and vote upon a proposal to approve the issuance of shares of Pinstripes Holdings, Inc. common stock in connection with the business combination contemplated by the Business Combination Agreement (the “Business Combination”) for purposes of complying with the applicable provisions of Section 312.03 of the NYSE Listed Company Manual. Proposal No. 4 is referred to as the “Listing Proposal.” |

| 5. | Proposal No. 5 — The Equity Incentive Plan Proposal — To consider and vote upon a proposal to approve and adopt the Equity Incentive Plan, a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex D. Proposal No. 5 is referred to as the “Equity Incentive Plan Proposal” and, collectively with the Business Combination Proposal, the Charter Amendment Proposal and the Listing Proposal, the “Condition Precedent Proposals.” |

| 6. | Proposal No. 6 — The ESPP Proposal — To consider and vote upon a proposal to approve and adopt the Employee Stock Purchase Plan, a copy of which is attached to the accompanying joint proxy statement/consent solicitation statement/prospectus as Annex E. Proposal No. 6 is referred to as the “ESPP Proposal.” |

| 7. | Proposal No. 7 — The Adjournment Proposal — To adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and voting of proxies if, based upon the tabulated vote at the time of the Special Meeting, there are not sufficient votes received to pass the resolution to approve the aforementioned proposals at the Special Meeting. Proposal No. 7 is referred to as the “Adjournment Proposal.” |

Each of the Condition Precedent Proposals is conditioned on the approval and adoption of each of the other Condition Precedent Proposals, and the Business Combination will be consummated only if each of the Condition Precedent Proposals is approved by the requisite Banyan stockholders. If the Business Combination Proposal is not approved, the other proposals (except the Adjournment Proposal) will not be presented to the Banyan stockholders for a vote. The Adjournment Proposal is not conditioned on the approval of any other proposal. Each of these proposals is more fully described in the accompanying joint proxy statement/consent solicitation statement/prospectus, which each Banyan stockholder is encouraged to read carefully and in its entirety.

The above matters are more fully described in the accompanying joint proxy statement/consent solicitation statement/prospectus, which also includes, as Annex A, a copy of the Business Combination Agreement. We urge you to read carefully the accompanying joint proxy statement/consent solicitation statement/prospectus in its entirety, including the Annexes and accompanying financial statements.

The board of directors of Banyan (the “Banyan Board”) has determined that each of the Condition Precedent Proposals is advisable and in the best interests of Banyan and its stockholders. The Banyan Board approved the Business Combination Agreement and the transactions contemplated thereby and recommends that Banyan’s stockholders vote “FOR” the Business Combination Proposal, “FOR” the Charter Amendment Proposal, “FOR” the Governance Proposals, “FOR” the Listing Proposal, “FOR” the Equity Incentive Plan Proposal, “FOR” the ESPP Proposal, and “FOR” the Adjournment Proposal (if necessary). Each such proposal is described in the accompanying joint proxy statement/consent solicitation statement/prospectus.

Banyan’s directors and officers may have financial interests in the Business Combination that are different from, or in addition to, their interests as stockholders of Banyan and the interests of stockholders of Banyan generally. The existence of financial and personal interests of Banyan’s directors and officers may result in conflicts of interest, including a conflict between what may be in the best interests of Banyan and its stockholders and what may be best for a director’s personal interests when determining to recommend that Banyan’s stockholders vote for the aforementioned proposals. See the sections in the accompanying joint proxy statement/consent solicitation statement/prospectus entitled “Proposal No. 1 — The Business Combination Proposal — Interests of Certain Persons in the Business Combination” and “Beneficial Ownership of Securities.”

Subject to the terms and provisions of the Business Combination Agreement, Banyan reserves the right at any time to cancel the Special Meeting and not to submit to its stockholders any of the aforementioned proposals. In the event the Special Meeting is canceled, Banyan will liquidate and dissolve in accordance with its certificate of incorporation. In addition, subject to the terms and provisions of the Business Combination Agreement, Banyan reserves the right to postpone or adjourn the Special Meeting on one or more occasions to a later date.

The record date for the Special Meeting is , 2023 (the “Record Date”). Only holders of record of shares of Banyan Class A Common Stock and shares of Banyan Class B Common Stock at the close of business on the Record Date are entitled to notice of and to vote and have their respective votes counted at the Special Meeting and any adjournments or postponements of the Special Meeting. A complete list of Banyan’s stockholders of record entitled to vote at the Special Meeting will be available for 10 days before the Special Meeting at Banyan’s principal executive offices for inspection by Banyan’s stockholders during ordinary business hours for any purpose related to the Special Meeting and electronically during the Special Meeting at https://www.cstproxy.com/ .

Our Banyan Class A Common Stock and warrants are currently listed on the New York Stock Exchange (the “NYSE”) under the symbols “BYN” and “BYN WS,” respectively. Certain of our shares of Banyan Class A Common Stock and warrants currently trade as units consisting of one share of Banyan Class A Common Stock and one-half of one redeemable warrant, and are listed on the NYSE under the symbol “BYN.U.” These units will automatically separate into their component securities upon consummation of the Business Combination and, as a result, will no longer trade as an independent security. Upon the Closing, we intend to change our name from “Banyan Acquisition Corporation” to “Pinstripes Holdings, Inc.” New Pinstripes will apply to list, to be effective at the time of the closing of the Business Combination, its common stock and warrants on the NYSE (or Nasdaq Stock Market LLC) under the symbols “PNST” and “PNST WS,” respectively.

Pursuant to Banyan’s certificate of incorporation, a holder of Banyan Class A Common Stock (such holder, a “Public Stockholder”) may request that Banyan redeem all or a portion of such Banyan Class A Common Stock for cash if the Business Combination is consummated. These redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Banyan’s transfer agent in order to validly redeem its shares. Public Stockholders may elect to redeem their respective shares of Banyan Class A Common Stock whether they vote “For” or “Against” the Business Combination Proposal or abstain from voting. If the Business Combination is not consummated, the shares of Banyan Class A Common Stock will be returned to the respective holder, broker or bank. If the Business Combination is consummated, and if a Public Stockholder properly exercises its right to redeem all or a portion of the Banyan Class A Common Stock that it holds and timely tenders or delivers its shares to Banyan’s transfer agent, Banyan will redeem such Banyan Class A Common Stock for a per-share price, payable in cash, equal to the pro rata portion of the trust account established at the consummation of Banyan’s initial public offering, calculated as of two business days prior to the consummation of the Business Combination, including interest earned on the funds held in such trust account (net of taxes payable).

For illustrative purposes, as of , 2023, the most recent practicable date prior to the date of the accompanying joint proxy statement/consent solicitation statement/prospectus, the redemption price per share would have amounted to approximately $ , based on the aggregate amount on deposit in the aforementioned trust account of approximately $ as of , 2023 (including interest earned on the funds held in such trust account and not previously released to Banyan to pay its taxes), divided by the total number of then-outstanding Public Shares (as defined in the accompanying joint proxy statement/consent solicitation statement/prospectus). If a Public Stockholder exercises its redemption rights in full, then it will be electing to exchange its Banyan Class A Common Stock for cash and will no longer own Banyan Class A Common Stock. See “Special Meeting of Banyan Stockholders—Redemption Rights” in the accompanying joint proxy statement/consent solicitation statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your Banyan Class A Common Stock for cash. A Public Stockholder must complete the procedures for electing to redeem its Banyan Class A Common Stock in the manner described in the accompanying joint proxy statement/consent solicitation statement/prospectus prior to 5:00 p.m., Eastern Time, on , 2023 (two business days before the initially scheduled date of the Special Meeting) in order for its shares to be redeemed.

Notwithstanding the foregoing, a Public Stockholder, together with any such stockholder’s affiliates or any other person or entity with whom such stockholder is acting in concert or as a “group” (as defined in Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from seeking redemption rights with respect to more than an aggregate of 15% of the Banyan Class A Common Stock sold in Banyan’s initial public offering.

Approval of the Charter Amendment Proposal requires the affirmative vote of the holders of 65% of the then outstanding shares of Banyan Common Stock, voting together as a single class, at a meeting at which a quorum is present. Approval of the Business Combination Proposal, the Governance Proposals (each which is a non-binding, advisory vote), the Listing Proposal, the Equity Incentive Plan Proposal, the ESPP Proposal and the Adjournment Proposal require the affirmative vote of a majority of the votes cast by holders of shares of the issued and outstanding Banyan Common Stock, voting together as a single class, at a meeting at which a quorum is present.

Concurrently with the execution of the Business Combination Agreement, Banyan Acquisition Sponsor LLC, a Delaware limited liability company (the “Sponsor”), George Courtot, Bruce Lubin, Otis Carter, Kimberley Annette Rimsza, Matt Jaffee and Brett Biggs (together with the Sponsor, the “Sponsor Holders) entered into a Sponsor Letter Agreement (the “Sponsor Letter Agreement”), pursuant to which, among other things, the Sponsor Holders have agreed, (i) for no additional consideration, to waive their respective redemption rights in connection with the consummation of the Business Combination with respect to any shares of the Banyan Class A Common Stock and Banyan Class B Common Stock they may hold, (ii) to subject two-thirds of the Banyan Class B Common Stock (or Banyan Class A Common Stock, if converted) held by the Sponsor Holders to certain vesting conditions and forfeiture and (iii) to vote any shares of Banyan Common Stock held by them in favor of the Business Combination Proposal and the other proposals to be considered at the Special Meeting. Currently, the Sponsor Holders hold 64.4% of the issued and outstanding shares of Banyan Common Stock. For additional information regarding the Sponsor Letter Agreement, see the section entitled “Proposal No. 1 — The Business Combination Proposal — Related Agreements — Sponsor Letter Agreement” in the accompanying joint proxy statement/consent solicitation statement/prospectus.

The Business Combination Agreement is subject to the satisfaction or waiver of certain other closing conditions as described in the accompanying joint proxy statement/consent solicitation statement/prospectus. There can be no assurance that the parties to the Business Combination Agreement would waive any such provision of the Business Combination Agreement.

If Banyan does not consummate the Business Combination and fails to complete an initial business combination by December 24, 2023 (as such date may be extended by approval of the Banyan stockholders), Banyan will be required to dissolve and liquidate its trust account by returning the then-remaining funds in such account to the Public Stockholders. The joint proxy statement/consent solicitation statement/prospectus accompanying this notice describes the Business Combination Agreement and the transactions contemplated thereby, as well as the proposals to be considered at the Special Meeting. Please review the accompanying joint proxy statement/consent solicitation statement/prospectus carefully.

YOUR VOTE IS VERY IMPORTANT, REGARDLESS OF THE NUMBER OF SHARES OF BANYAN COMMON STOCK YOU OWN. Whether or not you plan to attend the Special Meeting, please complete, sign, date and mail the enclosed proxy card in the postage-paid envelope provided at your earliest convenience. You may also submit a proxy via the internet by following the instructions printed on your proxy card. If you hold your shares through a broker, bank or other nominee, you should direct the vote of your shares in accordance with the voting instruction form received from your broker, bank or other nominee.

If you have any questions or need assistance with voting, please contact Banyan’s proxy solicitor, Morrow Sodali LLC, by calling (800) 662-5200 (toll-free), or banks and brokers can call (203) 658-9400, or by emailing .info@investor.morrowsodali.com.

If you plan to attend the Special Meeting and are a beneficial holder of Banyan Common Stock who owns your shares of Banyan Common Stock through a bank or broker, you will need to contact Continental Stock Transfer & Trust Company to receive a control number. Please read carefully the sections in the accompanying joint proxy statement/consent solicitation statement/prospectus regarding attending and voting at the Special Meeting to ensure that you comply with these requirements.

Very truly yours, | |

Jerry Hyman | |

Chairman of the Board of Directors of | |

Banyan Acquisition Corporation |

NOTICE OF SOLICITATION OF WRITTEN CONSENT

To the Stockholders of Pinstripes, Inc.:

On June 22, 2023, Banyan Acquisition Corporation, a Delaware Corporation (“Banyan”), and Panther Merger Sub Inc., a Delaware corporation and wholly-owned subsidiary of Banyan (“Merger Sub”), entered into a Business Combination Agreement (as it may be amended, supplemented or otherwise modified from time to time in accordance with its terms, the “Business Combination Agreement”) with Pinstripes, Inc., a Delaware corporation (“Pinstripes”). If the transactions contemplated by the Business Combination Agreement are completed, Merger Sub will merge with and into Pinstripes, with Pinstripes surviving such merger as a wholly-owned subsidiary of Banyan (the “Business Combination”). Upon consummation of the Business Combination and the other transactions contemplated by the Business Combination Agreement, the holders of Pinstripes common stock, preferred stock, options, warrants and other convertible securities (collectively, the “Pinstripes equityholders”) will become equityholders of Banyan, which will change its name to “Pinstripes Holdings, Inc.” in connection with the Business Combination. We refer to Banyan after the consummation of the Business Combination as “New Pinstripes.”

The accompanying joint proxy statement/consent solicitation statement/prospectus is being delivered to you on behalf of Pinstripes’ board of directors (the “Pinstripes Board”) to request that Pinstripes’ stockholders as of the record date of , 2023 execute and return written consents to adopt the Business Combination Agreement and approve the Business Combination. Under the Business Combination Agreement, Pinstripes must provide to Banyan a written consent of Pinstripes’ stockholders evidencing the affirmative vote of the holders of a majority of the outstanding Pinstripes common stock and Pinstripes preferred stock, voting together as a single class on an as-converted basis, to adopt the Business Combination Agreement and approve the Business Combination within three (3) business days of the registration statement containing the accompanying joint proxy statement/consent solicitation statement/prospectus being declared effective under the Securities Act of 1933, as amended.

The accompanying joint proxy statement/consent solicitation statement/prospectus describes the proposed Business Combination and the actions to be taken in connection with the Business Combination, provides additional information about the parties involved, and describes the risks, in the section entitled “Risk Factors,” related to the parties, the proposed Business Combination and other matters. Please give all of this information your careful attention. A copy of the Business Combination Agreement is attached as Annex A to the accompanying joint proxy statement/consent solicitation statement/prospectus.

A summary of the appraisal rights that may be available to you is described in the accompanying joint proxy statement/consent solicitation statement/prospectus in the section entitled “Solicitation of Consents from Pinstripes Stockholders—Appraisal Rights of Pinstripes Stockholders.” To exercise such rights, you must take all other steps necessary to perfect your appraisal rights, as described in the aforementioned section of the accompanying joint proxy statement/consent solicitation statement/prospectus. Please note that if you wish to exercise appraisal rights, you must not sign and return a written consent adopting the Business Combination Agreement. However, so long as you do not return a consent form at all, it is not necessary to affirmatively vote against or disapprove the Business Combination to preserve your ability to exercise appraisal rights. The closing of the Business Combination Agreement is subject to, among other things, holders of not more than ten percent (10%) of the collective outstanding Pinstripes common stock and Pinstripes preferred stock exercising their appraisal rights.

The Pinstripes Board has considered the Business Combination and the terms of the Business Combination Agreement and has determined unanimously that the Business Combination and the Business Combination Agreement are advisable, fair to and in the best interests of Pinstripes and Pinstripes’ stockholders and recommends that Pinstripes’ stockholders adopt the Business Combination Agreement and approve the Business Combination by submitting a written consent. As described in the section entitled “Proposal No. 1—The Business Combination Proposal—Related Agreements—Security Holder Support Agreement” of the accompanying joint proxy statement/consent solicitation statement/prospectus, certain stockholders of Pinstripes, whose ownership interests collectively represent over 50% of the outstanding shares of Pinstripes common stock and Pinstripes preferred stock, and as such are sufficient to approve the Business Combination on behalf of Pinstripes, are parties to a Security Holder Support Agreement with Banyan, whereby such stockholders agreed to vote all of their shares of Pinstripes common stock and Pinstripes preferred stock in favor of approving the Business Combination and the other proposed transactions contemplated by the Business Combination Agreement and have waived their appraisal rights with respect to such matters. Accordingly, if you are party to the Security Holder Support Agreement, you are obligated to execute and return the written consent furnished with the accompanying joint proxy statement/consent solicitation statement/prospectus within three (3) business days of , and the approval by the Pinstripes stockholders is effectively assured.

Please complete, date and sign the written consent furnished with the accompanying joint proxy statement/consent solicitation statement/prospectus and return it promptly to Pinstripes by one of the means described in the section entitled “Solicitation of Consents from Pinstripes Stockholders.”

If you have any questions concerning the Business Combination Agreement, the Business Combination, the consent solicitation or the accompanying joint proxy statement/consent solicitation statement/prospectus, or if you have any questions about how to deliver your written consent, please email or contact Pinstripes, Inc. at 1150 Willow Road, Northbrook, IL 60062, Attention: Chief Executive Officer.

Dale Schwartz | |

Chief Executive Officer |

TABLE OF CONTENTS

i

267 | |

268 | |

F-1 | |

A-1 | |

B-1 | |

ANNEX C - FORM OF AMENDED AND RESTATED BYLAWS OF PINSTRIPES HOLDINGS, INC. | C-1 |

ANNEX D - FORM OF EQUITY INCENTIVE PLAN | D-1 |

ANNEX E - FORM OF ESPP PLAN | E-1 |

ANNEX F - FORM OF REGISTRATION RIGHTS AGREEMENT | F-1 |

G-1 | |

ANNEX H - SECTION 262 OF THE DELAWARE GENERAL CORPORATION LAW | H-1 |

ii

ABOUT THIS JOINT PROXY STATEMENT/CONSENT SOLICITATION STATEMENT/PROSPECTUS

This document, which forms part of a registration statement (the “Registration Statement”) on Form S-4 filed with the U.S. Securities and Exchange Commission (the “SEC”) by Banyan (File No. 333- ), constitutes a prospectus of Banyan under Section 5 of the U.S. Securities Act of 1933, as amended, with respect to certain securities of Banyan to be issued in connection with the Business Combination described below. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the Securities Exchange Act of 1934, as amended, for the Special Meeting to be held in connection with the Business Combination and at which Banyan stockholders will be asked to consider and vote upon a proposal to adopt the Business Combination Agreement and approve the Business Combination, among other matters. This document also constitutes a consent solicitation statement that Pinstripes is providing to the holders of Pinstripes Common Stock and Pinstripes Preferred Stock to solicit, among other things, the required written consent to adopt and approve in all respects the Business Combination Agreement and the transactions contemplated thereby. All share and per share information in this joint proxy statement/consent solicitation statement/prospectus, including the number of Public Shares required to approve the proposals to be voted on, give effect to the Extension Amendment Redemptions (as defined below). See “Summary of the Joint proxy statement/consent solicitation statement/prospectus—The Special Meeting—Quorum and Vote of Banyan Stockholders” and “Information About Banyan—Extension of Time to Complete a Business Combination.”

ADDITIONAL INFORMATION

You may request copies of this joint proxy statement/consent solicitation statement/prospectus and any other publicly available information concerning Banyan, without charge, by written request to Banyan Acquisition Corporation, 400 Skokie Blvd., Suite 820, Northbrook, Illinois 60062, or by telephone request at (847) 757-3812; or Morrow Sodali LLC, our proxy solicitor, by calling (800) 662-5200 (toll free), or banks and brokers can call (203) 658-9400, or by emailing .info@investor.morrowsodali.com, or from the SEC through the SEC website at http://www.sec.gov.

In order for a Banyan stockholder to receive timely delivery of the applicable documents in advance of the Special Meeting to be held on , 2023, such stockholder must request the information no later than five business days prior to the date of the Special Meeting, by , 2023.

iii

CERTAIN DEFINED TERMS

Unless otherwise stated or unless the context otherwise requires, the terms “we,” “us,” “our,” and “Banyan” refer to Banyan Acquisition Corporation. The terms “New Pinstripes,” “combined company” and

“post-Business Combination company” refer to New Pinstripes and its subsidiaries following the consummation of the Business Combination. The term “Pinstripes” refers to Pinstripes, Inc., together with its subsidiaries, prior to the Business Combination.

“2023 EIP Plan” means the Equity Incentive Plan, dated , 2023, a copy of which is attached to this joint proxy statement/consent solicitation statement/prospectus as Annex D. For additional information, see “Proposal No. 5—The Equity Incentive Plan Proposal” section of this joint proxy statement/consent solicitation statement/prospectus.

“A&R Registration Rights Agreement” means the Amended and Restated Registration Rights Agreement to be entered into by and among New Pinstripes, the Sponsor Holder, and certain New Pinstripes equityholders at Closing.

“Adjournment Proposal” means the proposal to be considered at the Special Meeting to adjourn the Special Meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if it is determined by Banyan that more time is necessary or appropriate to approve one or more proposals at the Special Meeting.

“AMR Report” means the U.S. Corporate Event Market by Event Type (Conference/Seminar, Trade Shows/Exhibitions, Incentive Programs, Company Meetings, and Others), and Industry (Banking and Financial Sector, Information Technology, Real Estate and Infrastructure, Automotive, Insurance, and Others): Global Opportunity Analysis and Industry Forecast 2021-2030 report prepared by Allied Market Research.

“Banyan” means Banyan Acquisition Corporation, a Delaware corporation, prior to the consummation of the Business Combination.

“Banyan Board” means Banyan’s board of directors.

“Banyan Class A Common Stock” means the Class A common stock, par value $0.0001 per share, of Banyan.

“Banyan Class B Common Stock” means the Class B common stock, par value $0.0001 per share, of Banyan.

“Banyan Common Stock” means, collectively, the Banyan Class A Common Stock and the Banyan Class B Common Stock.

“Banyan Parties” means Banyan and Merger Sub.

“Banyan Private Placement Warrants” means the warrants issued to the Sponsor and the IPO Underwriters in a private placement simultaneously with the closing of the IPO.

“Banyan Public Warrants” means the warrants sold as part of the units in the IPO (whether they were purchased in the IPO or thereafter in the open market).

“Banyan Stockholder Matters” means (a) the adoption and approval of the Business Combination Proposal, (b) the adoption and approval of the Charter Amendment Proposal, (c) the adoption and approval of the Governance Proposals, (d) the adoption and approval of the Listing Proposal, (e) the adoption and approval of the Equity Incentive Plan Proposal, (f) the adoption and approval of the ESPP Proposal, and (g) the adoption and approval of the Adjournment Proposal.

“Brookfield” means Norwalk Land Development, LLC and its affiliates.

“Business Combination” means the transactions contemplated by the Business Combination Agreement, including the Merger.

iv

“Business Combination Agreement” means the Business Combination Agreement, dated as of June 22, 2023, by and among Banyan, Merger Sub and Pinstripes, as it may be amended and supplemented from time to time in accordance with its terms. A copy of the Business Combination Agreement is attached to this joint proxy statement/consent solicitation statement/prospectus as Annex A.

“Business Combination Proposal” means the proposal to be considered at the Special Meeting to approve the Business Combination.

“Cash-on-Cash Returns” means, in connection with any new Pinstripes location, such location’s Venue-Level Contribution divided by its Net Buildout Costs.

“Charter Amendment Proposal” means the proposal to approve and adopt the Proposed Charter, in the form attached to this joint proxy statement/consent solicitation statement/prospectus as Annex B, which will amend and restate the Existing Charter in its entirety and be effective when duly filed with the Secretary of State of the State of Delaware in connection with the Closing.

“Closing” means the closing of the Business Combination.

“Closing Date” means the date on which the Closing occurs.

“Code” means the Internal Revenue Code of 1986, as amended.

“Cohen Warrant” means that certain Warrant to Purchase Shares of Common Stock (No. 12), exercisable into up to 50,000 shares of Pinstripes Common Stock, issued to Cindy Cohen in December 2017, as amended.

“Condition Precedent Proposals” collectively refers to the Business Combination Proposal, the Charter Amendment Proposal, the Equity Incentive Plan Proposal and the Listing Proposal.

“Continental” mean Continental Stock Transfer & Trust Company.

“Converted Banyan Class A Common Stock” means the 2,000,000 shares of Banyan Class A Common Stock that were converted from Banyan Class B Common Stock.

“DGCL” means the Delaware General Corporation Law, as amended.

“Director Designation Agreement” means the director designation agreement that will be entered into upon Closing, by and between New Pinstripes and Dale Schwartz.

“DLLCA” means the Delaware Limited Liability Company Act, as amended.

“DTC” means The Depository Trust Company.

“DWAC” means The Depository Trust Company’s deposit/withdrawal at custodian system.

“Effective Time” means the effective time of the Merger.

“Equity Incentive Plan Proposal” means the proposal to consider and vote upon the 2023 EIP Plan, a copy of which is attached to the joint proxy statement/consent solicitation statement/prospectus as Annex D.

“ESPP” means the 2023 Employee Stock Purchase Plan, a copy of which is attached to the joint proxy statement/consent solicitation statement/prospectus as Annex E.

“ESPP Proposal” means the proposal to consider and vote upon the ESPP, a copy of which is attached to the joint proxy statement/consent solicitation statement/prospectus as Annex E.

v

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“Existing Charter” means Banyan’s amended and restated certificate of incorporation, as amended, in effect prior to the Closing.

“Extension Amendment” means the amendment to the amended and restated certificate of incorporation of Banyan as proposed in the Extension Amendment Proposal that was approved at the Extension Meeting.

“Extension Amendment Proposal” means the proposal presented at the Extension Meeting to amend the amended and restated certificate of incorporation of Banyan to (i) allow Banyan the option to extend the date by which it must complete its initial business combination from April 24, 2023 to December 24, 2023 and (ii) allow each holder of shares of Banyan Class B Common Stock to elect to convert such shares into shares of Banyan Class A Common Stock prior to the Closing.

“Extension Amendment Redemptions” means the redemption by Banyan stockholders of 20,151,313 shares of Banyan Class A Common Stock in connection with the approval and implementation of the Extension Amendment Proposal.

“Extension Meeting” means the special meeting of Banyan stockholders held on April 21, 2023 to consider, among other things, the Extension Amendment Proposal.

“Founder Shares” means Converted Banyan Class A Common Stock and the Banyan Class B Common Stock.

“Full-Service Restaurants: Global Strategic Business Report” means the Global Full-Service Restaurants market trends (2022-2030) report prepared by Global Industry Analysts Inc.

“GAAP” means U.S. generally accepted accounting principles.

“Governance Proposals” means the proposals to approve, on a non-binding advisory basis, certain governance provisions in the Proposed Charter, presented separately in accordance with SEC requirements.

“Governmental Authority” means any federal, state, provincial, municipal, local or foreign government, governmental authority, regulatory or administrative agency, governmental commission, department, board, bureau, agency or instrumentality, court, arbitral body (public or private) or tribunal.

“Granite Creek Warrant” means that certain Warrant No. 27, exercisable into up to 111,619 shares of Pinstripes Common Stock, issued to Granite Creek FlexCap III, L.P. on April 19, 2023.

“Gross Buildout Cost” means, in connection with any new Pinstripes location, the design and construction costs, plus the cost of furniture, fixtures and equipment, associated with the opening of such location.

“HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, and the rules and regulations promulgated thereunder.

“HBC US Holdings” means Hudson’s Bay Company and its affiliates.

“IAAPA Report” means the 2019 to 2023 Global Theme and Amusement Park Outlook Report prepared by the International Association of Amusement Parks Attractions.

“IBISWorld Weddings Report” means the Wedding Services in the US industry trends (2018 - 2023) report prepared by IBISWorld.

“Insiders” means the directors and officers of Banyan.

“IPO” means Banyan’s initial public offering of its units, common stock and warrants pursuant to registration statements on Form S-1 declared effective by the SEC on January 19, 2022 (SEC File Nos. 333-258599 and 333-262248).

vi

“IPO Underwriters” means BTIG, LLC and I-Bankers Securities, Inc.

“Leon Warrant” means that certain Warrant to Purchase Shares of Common Stock (No. 13), exercisable into up to 10,000 shares of Pinstripes Common Stock, issued to Larry Leon in December 2018, as amended.

“Letter Agreement” means the letter agreement, dated January 19, 2022, by and among Banyan, the Sponsor and other parties thereto.

“Listing Proposal” means the proposal to be considered at the Special Meeting to approve the listing of the New Pinstripes Common Stock on the NYSE (or Nasdaq).

“Lockup Agreement” means the lockup agreement, dated June 22, 2023, and entered into concurrently with the execution and delivery of the Business Combination Agreement, by and among Banyan, Pinstripes and certain security holders of Pinstripes.

“Macerich” means Macerich HHF Broadway Plaza LLC and its affiliates.

“Merger” means the merger of Merger Sub with and into Pinstripes, with Pinstripes being the surviving entity and continuing as a direct, wholly owned subsidiary of New Pinstripes.

“Merger Sub” means Panther Merger Sub Inc., a Delaware corporation and direct, wholly-owned subsidiary of Banyan.

“Middleton Partners” means, collectively, Middleton Pinstripes Investor LLC, a Delaware limited liability company, and Middleton Pinstripes Investor SBS LLC, a Delaware limited liability company.

“Minimum Cash Amount” means $75,000,000.

“Nasdaq” means the Nasdaq Stock Market LLC.

“Net Buildout Cost” means, in connection with the opening of any new Pinstripes location, the Gross Buildout Costs for such location, less any tenant improvement allowances and equipment financing that offset such Gross Buildout Costs.

“New Pinstripes” refers to the combined company immediately following the Closing that shall be renamed upon the Closing.

“New Pinstripes Board” means the board of directors of the combined company subsequent to the completion of the Business Combination.

“New Pinstripes Common Stock” means New Pinstripes’ common stock, par value $0.0001 per share.

“New Pinstripes Private Placement Warrants” means warrants representing the right to purchase shares of New Pinstripes Common Stock following the Closing on the same contractual terms and conditions as the Banyan Private Placement Warrants.

“New Pinstripes Public Warrants” means the warrants representing the right to purchase shares of New Pinstripes Common Stock following the Closing on the same contractual terms and conditions as the Banyan Public Warrants.

“New Pinstripes Warrants” means the New Pinstripes Private Placement Warrants and the New Pinstripes Public Warrants.

“Non-Redemption Agreements” means the non-redemption agreements entered into by the Sponsor in connection with the Extension Meeting, pursuant to which the Sponsor will transfer 1,018,750 shares of Banyan Class B Common Stock to certain investors in Banyan in exchange for such investors agreeing not to redeem their respective shares of Banyan Class A Common Stock in connection with the Extension Meeting.

“NYSE” means the New York Stock Exchange.

“O’Connor/LaSalle” means LaSalle Investment Management and its affiliates.

vii

“Payback Period” means, as to any new Pinstripes location, the number of years that it takes the Venue-Level Contribution of such location to equal or exceed the Net Buildout Costs for such location.

“Person” means any individual, firm, corporation, partnership, limited liability company, incorporated or unincorporated association, joint venture, joint stock company, Governmental Authority or other entity of any kind.

“Pinstripes” means Pinstripes, Inc., a Delaware corporation.

“Pinstripes Board” means Pinstripes’ board of directors.

“Pinstripes Charter” means Pinstripes’ Third Amended and Restated Certificate of Incorporation, as amended by that certain Certificate of Amendment to the Third Amended and Restated Certificate of Incorporation of Pinstripes, together with (a) that certain Certificate of Designations of the Series F Convertible Preferred Stock of Pinstripes, filed with the Secretary of State of the State of Delaware as of September 13, 2018, (i) as amended by that certain Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of September 23, 2019, (ii) as further amended by that certain Second Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of January 28, 2020, and (iii) as further amended by that certain Third Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of June 21, 2023; (b) that certain Certificate of Designations of the Series G Convertible Preferred Stock of Pinstripes, filed with the Secretary of State of the State of Delaware as of April 23, 2021, (i) as amended by that certain Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of August 18, 2021, and (ii) as further amended by that certain Second Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of June 21, 2023; (c) that certain Certificate of Designations of the Series H Convertible Preferred Stock of Pinstripes, filed with the Secretary of State of the State of Delaware as of August 18, 2021, as amended by that certain Certificate of Amendment, filed with the Secretary of State of the State of Delaware as of June 21, 2023; and (d) that certain Certificate of Designations of the Series I Convertible Preferred Stock of Pinstripes, filed with the Secretary of State of the State of Delaware as of June 21, 2023, in each case, as the same may be amended and/or restated from time to time, and Pinstripes’ Amended and Restated Bylaws, as amended and in effect on the date hereof.

“Pinstripes Common Stock” means the Common Stock, par value $0.01 per share, of Pinstripes.

“Pinstripes Convertible Notes” means (a) the Convertible Note, dated June 4, 2021, by and between Pinstripes and Fashion Square Eco LP (as amended), and (b) the Convertible Note, dated June 4, 2021, by and between Pinstripes and URW US Services, Inc. (as amended).

“Pinstripes Group” means each of Pinstripes and its direct and indirect Subsidiaries.

“Pinstripes Option” means each option to purchase Pinstripes Common Stock.

“Pinstripes Party” means any member of the Pinstripes Group.

“Pinstripes Preferred Stock” means, collectively, shares of preferred stock, par value $0.01 per share, of Pinstripes designated as “Series A Preferred Stock,” “Series B Preferred Stock,” “Series C Preferred Stock,” “Series D-1 Preferred Stock,” “Series D-2 Preferred Stock,” “Series E Preferred Stock,” “Series F Convertible Preferred Stock,” “Series G Convertible Preferred Stock,” “Series H Convertible Preferred Stock” and “Series I Convertible Preferred Stock” authorized pursuant to the Pinstripes Charter.

“Pinstripes Stock” means, collectively, the Pinstripes Common Stock and Pinstripes Preferred Stock.

“Pinstripes Warrants” means any warrants to acquire equity securities of Pinstripes, including (a) the Silverview Warrants, (b) the Granite Creek Warrant, (c) the Cohen Warrant and (d) the Leon Warrant.

“PIPE Investors” means the investors in the PIPE Financing.

“PIPE Financing” means the proposed equity financing for up to $53,733,800 of gross proceeds to be consummated by Banyan at the Closing.

viii

“Proposed Bylaws” mean the proposed amended and restated bylaws of New Pinstripes to be in effect following the Business Combination, a form of which is attached hereto as Annex C.

“Proposed Charter” means the proposed amended and restated certificate of incorporation of New Pinstripes in the form attached hereto as Annex B.

“Proxy Solicitor” means Morrow Sodali LLC.

“Public Shares” means Banyan Class A Common Stock sold in the IPO (whether they were purchased in the IPO or thereafter in the open market).

“Public Stockholders” means the holders of shares of Banyan Class A Common Stock that were sold in the IPO (whether they were purchased in the IPO or thereafter in the open market).