As filed with the Securities and Exchange Commission on April 23, 2024

Registration Statement No. 333-276849

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________

AMENDMENT NO. 1

TO

FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_____________________

(Exact name of registrant as specified in its charter)

_____________________

| | 2860 | 85-3115899 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

10 E. 53rd Street, 13th Floor

New York, NY 10022

Telephone: (212) 430-2214

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

_____________________

Timothy Babich

Chief Executive Officer and Chief Financial Officer

Golden Arrow Merger Corp.

10 E. 53rd Street, 13th Floor

New York, NY 10022

Telephone: (212) 430-2214

(Name, address, including zip code, and telephone number, including area code, of agent for service)

_____________________

Copies to:

|

Alan I. Annex, Esq. |

Jim Morrone, Esq. |

_____________________

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| | ☒ | Smaller reporting company | | |||

| Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ☐

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the SEC, acting pursuant to Section 8(a), may determine.

____________

* Upon the closing of the business combination referred to in the proxy statement/prospectus within this registration statement, the name of the registrant is expected to change to Bolt Projects Holdings, Inc.

The information in this preliminary proxy statement/prospectus is not complete and may be changed. The securities described herein may not be sold until the registration statement filed with the U.S. Securities and Exchange Commission is declared effective. This preliminary proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROXY STATEMENT/PROSPECTUS

SUBJECT TO COMPLETION, DATED APRIL 23, 2024

PROXY STATEMENT FOR THE SPECIAL MEETING OF

GOLDEN ARROW MERGER CORP.

PROSPECTUS FOR

UP TO 25,863,982 SHARES OF COMMON STOCK

OF

GOLDEN ARROW MERGER CORP.

(WHICH WILL BE RENAMED BOLT PROJECTS HOLDINGS, INC.)

Dear Golden Arrow Merger Corp. Stockholders:

On October 4, 2023, Golden Arrow Merger Corp., a Delaware corporation (“GAMC”) entered into a Business Combination Agreement (as it may be amended and/or restated from time to time, the “Business Combination Agreement”) with Beam Merger Sub, Inc., a Delaware corporation and a direct, wholly owned subsidiary of GAMC (“Merger Sub”) and Bolt Threads, Inc., a Delaware corporation (“Bolt Threads”). If the Business Combination Agreement and the transactions contemplated thereby are adopted and approved by Bolt Threads’ stockholders and GAMC’s stockholders and upon satisfaction or waiver of certain other customary conditions, the parties will consummate a business combination transaction pursuant to which Merger Sub will merge with and into Bolt Threads, with Bolt Threads surviving the merger as a wholly-owned subsidiary of GAMC (the “Merger” and, together with the other transactions contemplated by the Business Combination Agreement, the “Business Combination” and the closing of the Business Combination, the “Closing”). In connection with the Closing, GAMC will be renamed “Bolt Projects Holdings, Inc.” (GAMC immediately upon the consummation of the Business Combination and the other transactions contemplated by the Business Combination Agreement is referred to herein as the “Post-Combination Company.”)

The aggregate equity consideration to be paid to Bolt Threads’ security holders in the Business Combination will be equal to the quotient of (i) $250,000,000 (the “Equity Value”) divided by (ii) $10.00. Immediately prior to the Closing, (i) all of the outstanding principal and accrued interest under the Company Convertible Notes (as defined in the Business Combination Agreement) will be converted into shares of Bolt Threads common stock and (ii) all of the shares of Bolt Threads preferred stock will be converted into shares of Bolt Threads common stock. At the Closing, each share of Bolt Threads common stock that is issued and outstanding immediately prior to the Effective Time of the Merger and following the conversion of the Company Convertible Notes and Bolt Threads preferred stock (other than Dissenting Shares, Treasury Shares and shares of Bolt Threads capital stock subject to Company Share Awards, each as defined in the Business Combination Agreement) will be cancelled and converted into the right to receive a number of shares of the Post-Combination Company’s common stock equal to an exchange ratio determined by dividing the number of shares of common stock of the Post-Combination Company, par value $0.0001 per share (the “Post-Combination Company Common Stock”), constituting the Aggregate Transaction Consideration, by the Aggregate Fully Diluted Company Common Stock (as defined in the Business Combination Agreement) (the “Exchange Ratio”).

As of March 1, 2024, Bolt Threads had (i) $22,240,122 in principal and accrued interest under the Company Convertible Notes, (ii) 27,293,219 shares of preferred stock outstanding, (iii) 11,312,318 shares of common stock outstanding, (iv) 3,774,977 outstanding restricted stock units, (v) 1,824,405 outstanding options to purchase shares of Bolt Threads common stock, (vi) outstanding warrants to purchase 294,609 shares of preferred stock, and (vii) outstanding warrants to purchase 4,534,468 shares of common stock.

At the Closing, each option to purchase Bolt Threads common stock, whether or not exercisable and whether or not vested, will automatically be converted into an option to purchase a number of shares of the Post-Combination Company Common Stock in the manner set forth in the Business Combination Agreement.

At the Closing, each award of restricted stock units relating to a share of Bolt Threads Common Stock granted under Bolt Threads’ existing equity plans will automatically be converted into an award of restricted stock units covering the number of shares of the Post-Combination Company Common Stock in the manner set forth in the Business Combination Agreement.

At the Closing, unless otherwise exercised into Bolt Threads capital stock prior to the Effective Time of the Merger, each warrant to purchase Bolt Threads preferred stock issued and outstanding immediately prior to the Closing will, by virtue of the Merger and upon the terms and subject to the conditions set forth in the Business Combination Agreement, be assumed by GAMC, and will automatically be converted into a warrant to purchase shares of Post-Combination Company Common Stock in the manner set forth in the Business Combination Agreement.

Based on shares of Bolt Threads capital stock outstanding as of March 1, 2024, and an assumed exchange ratio of 0.4661 (the “Exchange Ratio”) based on Bolt Threads’ capital stock outstanding as of March 1, 2024, at Closing there would be an estimated (i) 23,107,445 shares of Post-Combination Company Common Stock issued to Bolt Threads securityholders (including 472,687 shares to be issued in respect of warrants to purchase Bolt Threads Common Stock that were issued to the Sponsor and other investors as part of a bridge financing concurrently with the signing of the Business Combination Agreement (the “Bridge Warrants”), which will be automatically exercised immediately prior to Closing); (ii) 1,768,981 shares of Post-Combination Company Common Stock issued or issuable upon the vesting of restricted stock units currently held by Bolt Threads securityholders; (iii) 850,259 shares of Post-Combination Company Common Stock issued or issuable upon the exercise of options currently held by Bolt Threads securityholders; and (iv) 137,297 shares of Post-Combination Company issuable upon the exercise of warrants currently held by Bolt Threads securityholders that will not be automatically exercised in connection with the Closing. The actual numbers will vary depending on the number of shares of Bolt Threads capital stock outstanding immediately prior to Closing. Based on the assumed Exchange Ratio of 0.4661 as of March 1, 2024, the Per Share Transaction Consideration is estimated to be $4.661.

At the Closing, each share of Class B common stock of GAMC, par value $0.0001 per share (“GAMC Class B Common Stock”), that is issued and outstanding immediately prior to the Effective Time of the Merger will automatically be converted into and exchanged for a number of validly issued, fully paid and nonassessable shares of Class A common stock of GAMC, par value $0.0001 per share (“GAMC Class A Common Stock”), equal to the Class B Conversion Ratio (as defined in the Business Combination Agreement), and each share of GAMC Class A Common Stock will be reclassified into a share of Post-Combination Company Common Stock. As of March 1, 2024, there were 140,000 shares of GAMC Class B Common Stock issued and outstanding, which would convert into an equal number of shares of Post-Combination Company Common Stock at the Closing.

GAMC has also entered into subscription agreements, pursuant to which certain investors have agreed to purchase at Closing an aggregate of up to 2,296,975 shares of GAMC Class A Common Stock (the “PIPE Shares”), for a price of $10.00 per share (the “PIPE Transaction”). The Sponsor has agreed to purchase up to 656,499 of the PIPE Shares for an and current securityholders of Bolt Threads have agreed to purchase 1,640,476 of the PIPE Shares (“Bolt Threads PIPE Subscribers”). However, the number of PIPE Shares to be purchased by the Sponsor will be reduced by the number of shares of GAMC Class A Common Stock that have not been elected for redemption as of the expiration of the redemption period related to the Closing and that are held by certain individuals mutually agreed upon by GAMC and Bolt Threads at any time up to immediately prior to the expiration of such redemption period.

It is anticipated that, following the Business Combination and as described further in this proxy statement/prospectus, Bolt Threads’ existing securityholders (with respect to their outstanding securities of Bolt Threads), Bolt Threads PIPE Subscribers (with respect to the PIPE Shares to be purchased by them), GAMC’s public stockholders (“Public Stockholders”), the Sponsor and holders of shares of GAMC Class B Common Stock (and any shares of GAMC Class A Common Stock issued upon the conversion thereof), issued prior to GAMC’s initial public offering (the “Initial Stockholders”), will own approximately 69.5%, 5.0%, 0% and 23.5%, respectively, of the issued and outstanding Post-Combination Company Common Stock if all outstanding public shares of GAMC are redeemed in connection with the Business Combination and assuming the Sponsor purchases 656,499 PIPE Shares and receives 472,687 shares to be issued in respect of the Sponsor’s Bridge Warrants, which will be automatically exercised into Bolt Threads Common Stock immediately prior to Closing, and 68.2%, 5.0%, 1.7% and 23.1%, respectively, of the issued and outstanding Post-Combination Company Common Stock if none of the outstanding public shares of GAMC are redeemed in connection with the Business Combination and assuming the Sponsor purchases 656,499 PIPE Shares and receives 472,687 shares to be issued in respect of the Sponsor’s Bridge Warrants, which will be automatically exercised into Bolt Threads Common Stock immediately prior to Closing and exchanged for the Post-Combination Company Common Stock. An aggregate of 28,172,063 public shares of GAMC, representing approximately 98% of the shares issued in GAMC’s initial public offering, were previously

redeemed in March 2023 and December 2023, respectively, in connection with votes by GAMC’s stockholders to extend the deadline by which GAMC must consummate an initial business combination to up to September 19, 2024. As of the date of this proxy statement/prospectus, the current deadline to consummate an initial business combination is [•], 2024.

GAMC is holding a special meeting in order to obtain the stockholder approvals necessary to complete the Business Combination. At the GAMC special meeting of stockholders, which will be held in a virtual format on [•], 2024, at [•], Eastern time, unless postponed or adjourned to a later date, GAMC will ask its stockholders to adopt the Business Combination Agreement, thereby approving the Business Combination and approve the other proposals described in this proxy statement/prospectus.

As described in this proxy statement/prospectus, certain stockholders of Bolt Threads are parties to a stockholder support agreement with GAMC whereby such stockholders agreed to vote to adopt and approve, upon the registration statement on Form S-4 being declared effective, the Business Combination Agreement and all other documents and transactions contemplated thereby and to subject their shares to certain transfer restrictions.

While we will not be considered a “controlled company” under the relevant listing rules of Nasdaq, we estimate that our directors, executive officers and expected holders of greater than 10% of the Post-Combination Company Common Stock will beneficially own approximately [•]% of the Post-Combination Company Common Stock following the Closing (assuming no redemptions), and will be able to exert significant influence over matters requiring stockholder approval, though they have no agreement to do so.

After careful consideration, the GAMC board of directors has unanimously approved the Business Combination Agreement, the Business Combination and the other proposals described in this proxy statement/prospectus, and has determined that it is advisable to consummate the Business Combination. The board of directors of GAMC recommends that its stockholders vote “FOR” the proposals described in this proxy statement/prospectus.

More information about GAMC, Bolt Threads and the Business Combination is contained in this proxy statement/prospectus. GAMC and Bolt Threads urge you to read the accompanying proxy statement/prospectus, including the financial statements and annexes and other documents referred to herein, carefully and in their entirety. IN PARTICULAR, YOU SHOULD CAREFULLY CONSIDER THE MATTERS DISCUSSED UNDER “RISK FACTORS” BEGINNING ON PAGE 37 OF THIS PROXY STATEMENT/PROSPECTUS.

On behalf of our board of directors, I thank you for your support and look forward to the successful completion of the Business Combination.

|

Sincerely, |

||

|

|

||

|

__________, 2024 |

Jacob Doft |

This proxy statement/prospectus is dated __________, 2024 and is first being mailed to the stockholders of GAMC on or about that date.

NEITHER THE U.S. SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THIS PROXY STATEMENT/PROSPECTUS OR ANY OF THE SECURITIES TO BE ISSUED IN THE BUSINESS COMBINATION, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

GOLDEN ARROW MERGER CORP.

10 E. 53rd Street, 13th Floor

New York, NY 10022

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON __________, 2024

To the Stockholders of Golden Arrow Merger Corp.:

NOTICE IS HEREBY GIVEN that a special meeting of stockholders (the “special meeting”) of Golden Arrow Merger Corp., a Delaware corporation (“GAMC,” “we,” “our” or “us”), which will be held in virtual format on __________, 2024, at __________, Eastern time. The special meeting can be accessed by visiting [https:// ], where you will be able to listen to the meeting live and vote during the meeting. Additionally, you have the option to listen to the special meeting by dialing [•] (toll-free within the U.S. and Canada) or [•] (outside of the U.S. and Canada, standard rates apply). The passcode for telephone access is [•], but please note that you cannot vote or ask questions if you choose to participate telephonically. Please note that you will only be able to access the special meeting by means of remote communication.

You are cordially invited to attend the special meeting, which will be held for the following purposes:

(1) Proposal No. 1 — The “Business Combination Proposal” — to consider and vote on a proposal to approve and adopt the Business Combination Agreement, dated as of October 4, 2023 (as it may be amended and/or restated from time to time, the “Business Combination Agreement”), by and among GAMC, Bolt Threads, Inc. (“Bolt Threads”) and Beam Merger Sub, Inc. (“Merger Sub”), and the transactions contemplated thereby, pursuant to which Merger Sub will merge with and into Bolt Threads, with Bolt Threads surviving the merger and becoming a wholly-owned direct subsidiary of GAMC (collectively with the other transactions contemplated by the Business Combination Agreement, the “Business Combination”);

(2) Proposal No. 2 — The “Charter Amendment Proposal” — to consider and vote on a proposal to adopt the proposed second amended and restated certificate of incorporation of GAMC attached as Annex B to the proxy statement/prospectus (the “Charter Amendment Proposal”);

(3) Proposal Nos. 3A-3G — The “Governance Proposals” — to consider and vote on, on a non-binding advisory basis, seven separate governance proposals relating to the following material differences between GAMC’s current amended and restated certificate of incorporation and the proposed second amended and restated certificate of incorporation (collectively, the “Governance Proposals”):

(a) change the name of GAMC to “Bolt Projects Holdings, Inc.” from the current name of “Golden Arrow Merger Corp.” (Proposal No. 3A);

(b) increase the number of shares of (i) common stock GAMC is authorized to issue from 220,000,000 shares to 500,000,000 shares and (ii) preferred stock GAMC is authorized to issue from 1,000,000 shares to 50,000,000 shares (Proposal No. 3B);

(c) increase the required voting thresholds to approve amendments to the bylaws and to certain provisions of the proposed amended and restated certificate of incorporation of (Proposal No. 3C);

(d) require a supermajority vote for the removal of directors for cause (Proposal No. 3D);

(e) remove the provision renouncing the corporate opportunity doctrine (Proposal No. 3E);

(f) eliminate the rights and privileges of GAMC Class B common stock and to redesignate GAMC Class A common stock and GAMC Class B common stock as common stock (after giving effect to the conversion of each outstanding share of GAMC Class B common stock immediately prior to the Closing into one share of GAMC Class A common stock) (Proposal No. 3F); and

(g) eliminate certain provisions related to related to GAMC’s status as a special purpose acquisition company that will no longer be relevant following the closing of the Business Combination (the “Closing”) (Proposal No. 3G).

(4) Proposal No. 4 — The “Election of Directors Proposal” — to consider and vote on a proposal to elect, effective at Closing, seven directors to serve staggered terms on the board of directors until the first, second and third annual meetings of stockholders after the Closing of the Business Combination, respectively, and until their respective successors are duly elected and qualified;

(5) Proposal No. 5 — The “Incentive Plan Proposal” — to consider and vote on a proposal to approve and adopt the incentive plan established to be effective after the Closing of the Business Combination;

(6) Proposal No. 6 — The “ESPP Proposal” — to consider and vote on a proposal to approve and adopt the employee stock purchase plan established to be effective after the Closing of the Business Combination;

(7) Proposal No. 7 — The “Nasdaq Proposal” — to consider and vote on a proposal to issue GAMC Class A common stock to the Bolt Threads stockholders in the Business Combination and to the PIPE Subscribers and as described herein; and

(8) Proposal No. 8 — The “Adjournment Proposal” — to consider and vote on a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve one or more proposals presented to stockholders for vote.

Your attention is directed to the proxy statement/prospectus accompanying this notice (including the financial statements and annexes attached thereto) for a more complete description of the proposed Business Combination and related transactions and each of our proposals. We encourage you to read this proxy statement/prospectus carefully. If you have any questions or need assistance voting your shares, please call our proxy solicitor, Morrow Sodali LLC at (800) 662-5200; banks and brokers can call collect at (203) 658-9400.

All GAMC stockholders are cordially invited to attend the special meeting in virtual format. GAMC stockholders may attend, vote and examine the list of GAMC stockholders entitled to vote at the special meeting by visiting [https:// ] and entering the control number found on their proxy card, voting instruction form or notice included in their proxy materials. The special meeting will be held in virtual meeting format only. You will not be able to attend the special meeting physically. To ensure your representation at the special meeting, you are urged to complete, sign, date and return the enclosed proxy card as soon as possible. If your shares are held in an account at a brokerage firm or bank, you must instruct your broker or bank on how to vote your shares.

Your vote is important regardless of the number of shares you own. Whether you plan to attend the special meeting or not, please sign, date and return the enclosed proxy card as soon as possible in the envelope provided. If your shares are held in “street name” or are in a margin or similar account, you should contact your broker to ensure that votes related to the shares you beneficially own are properly counted.

Thank you for your participation. We look forward to your continued support.

|

By Order of the Board of Directors, |

||

|

|

||

|

__________, 2024 |

Jacob Doft |

If you return your signed proxy without an indication of how you wish to vote, your shares will be voted in favor of each of the proposals.

All holders (the “Public Stockholders”) of shares of GAMC Class A common stock issued in GAMC’s initial public offering (the “Public Shares”) have the right to have their Public Shares redeemed for cash in connection with the proposed Business Combination. Public Stockholders are not required to affirmatively vote for or against the Business Combination Proposal, to vote on the Business Combination Proposal at all, or to be holders of record on the record date in order to have their shares redeemed for cash. This means that any Public Stockholder holding Public Shares may exercise redemption rights regardless of whether they are even entitled to vote on the Business Combination Proposal.

To exercise redemption rights, holders must tender their stock to Continental Stock Transfer & Trust Company, GAMC’s transfer agent, no later than two (2) business days prior to the originally scheduled date of the special meeting. You may tender your stock by either delivering your stock certificate to the transfer agent or by delivering your shares electronically using the Depository Trust Company’s Deposit Withdrawal at Custodian System. If the Business Combination is not completed, then these shares will not be redeemed for cash, though such shares may still be redeemed in the event of an alternative business combination or GAMC’s liquidation. If you hold the shares in street name, you will need to instruct your bank or broker to withdraw the shares from your account in order to exercise your redemption rights. See “Special Meeting of GAMC Stockholders — Redemption Rights” for more specific instructions.

TABLE OF CONTENTS

i

ABOUT THIS PROXY STATEMENT/PROSPECTUS

This document, which forms part of a registration statement on Form S-4 filed with the SEC, by GAMC (File No. 333-276849) (the “Registration Statement”), constitutes a prospectus of GAMC under Section 5 of the Securities Act, with respect to the securities to be issued if the Business Combination described below is consummated. This document also constitutes a notice of meeting and a proxy statement under Section 14(a) of the Exchange Act with respect to the special meeting in lieu of the 2024 annual meeting of GAMC stockholders at which GAMC stockholders will be asked to consider and vote on a proposal to approve the Business Combination by the approval and adoption of the Business Combination Agreement, among other matters.

1

MARKET, INDUSTRY AND OTHER DATA

This proxy statement/prospectus includes estimates regarding market and industry data and forecasts, which are based on publicly available information, industry publications and surveys, reports from government agencies, reports by market research firms or other independent sources and our own estimates based on our management’s knowledge of and experience in the market sectors in which we compete.

Certain monetary amounts, percentages and other figures included in this proxy statement/prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables or charts may not be the arithmetic aggregation of the figures that precede them, and figures expressed as percentages in the text may not total 100% or, as applicable, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

TRADEMARKS

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this proxy statement/prospectus may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. GAMC does not intend its use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of it by, any other companies.

2

FREQUENTLY USED TERMS

In this document:

“2024 Incentive Plan” means the Bolt Projects Holdings, Inc. 2024 Incentive Award Plan, attached to this proxy statement prospectus as Annex H and described in “Proposal No. 5 — The Incentive Plan Proposal.”

“Aggregate Transaction Consideration” means the aggregate transaction consideration to be paid to Bolt Threads’ stockholders, option holders, holders of Bolt Threads RSUs and warrant holders in the Business Combination.

“ASC” means Accounting Standards Codification.

“ASU” means Accounting Standards Update.

“Bolt Threads” means Bolt Threads, Inc., a Delaware corporation.

“Bolt Threads Board of Directors” means the board of directors of Bolt Threads.

“Bolt Threads Capital Stock” means Bolt Threads’ Common Stock and Bolt Threads’ Preferred Stock.

“Bolt Threads Common Stock” means Bolt Threads’ common stock, par value $0.0001 per share.

“Bolt Threads Founders” means, collectively, Daniel Widmaier and David Breslauer.

“Bolt Threads Options” means all outstanding options to purchase shares of Bolt Threads Common Stock, whether or not exercisable and whether or not vested, immediately prior to the Closing under the Bolt Threads stock incentive plans or otherwise.

“Bolt Threads Preferred Stock” means the outstanding shares of Bolt Threads’ preferred stock, consisting of Bolt Threads Series A Preferred Stock, Bolt Threads Series B Preferred Stock, Bolt Threads Series C Preferred Stock, Bolt Threads Series D Preferred Stock and Bolt Threads Series E Preferred Stock.

“Bolt Threads RSUs” means all outstanding restricted stock units relating to shares of Bolt Threads Common Stock immediately prior to the Closing under the Bolt Threads stock incentive plans or otherwise.

“Bolt Threads Series A Preferred Stock” means preferred stock of Bolt Threads, par value $0.0001 per share, designated as Series A convertible preferred stock.

“Bolt Threads Series B Preferred Stock” means preferred stock of Bolt Threads, par value $0.0001 per share, designated as Series B convertible preferred stock.

“Bolt Threads Series C Preferred Stock” means preferred stock of Bolt Threads, par value $0.0001 per share, designated as Series C convertible preferred stock.

“Bolt Threads Series D Preferred Stock” means preferred stock of Bolt Threads, par value $0.0001 per share, designated as Series D convertible preferred stock.

“Bolt Threads Series E Preferred Stock” means preferred stock of Bolt Threads, par value $0.0001 per share, designated as Series E convertible preferred stock.

“Bolt Threads Stockholders” means the holders of Bolt Threads Capital Stock.

“broker non-vote” means the failure of an GAMC stockholder, who holds his, her or its shares in “street name” through a broker or other nominee, to give voting instructions to such broker or other nominee.

“BTIG” means BTIG, LLC.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement, dated as of October 4, 2023, as it may be amended and/or restated from time to time, by and among GAMC, Bolt Threads and Merger Sub.

“Closing” means the closing of the Business Combination.

3

“Closing Date” means the date on which the Closing occurs.

“Code” means the Internal Revenue Code of 1986, as amended.

“Convertible Notes” means, collectively, the convertible promissory notes issued by Bolt Threads to certain holders for cash in October 2023 and February 2024, and to Ginkgo pursuant to the Ginkgo Note Purchase Agreement Amendment No. 1.

“DGCL” means the Delaware General Corporation Law.

“DTC” means The Depository Trust Company.

“DWAC System” means The Depository Trust Company’s Deposit/Withdrawal at Custodian System.

“Effective Time” means the date the Merger becomes effective.

“ESPP” means the Bolt Projects Holdings, Inc. 2024 Employee Stock Purchase Plan, attached to this proxy statement/prospectus as Annex J and described in “Proposal No. 6 — The ESPP Proposal.”

“Equity Value” means the equity value of Bolt Threads at the time of Closing, which has been designated as $250,000,000.

“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

“Exchange Ratio” means the ratio used to determine the number of shares of the Post-Combination Company’s Common Stock that the designated Bolt Threads Common Stock and Bolt Threads Preferred Stock will be converted into, as contemplated by the Business Combination Agreement, and will be calculated pursuant to the terms of the Business Combination Agreement as the quotient obtained by dividing the number of shares of common stock of the Post-Combination Company constituting the Aggregate Transaction Consideration by the number of shares of Aggregate Fully Diluted Company Common Stock (as defined in the Business Combination Agreement).

“Existing Certificate of Incorporation” means GAMC’s current amended and restated certificate of incorporation.

“Extended Date” means the date that is up to nine months after the Second Termination Date.

“Extension Notes” means the First Extension Note and the Second Extension Note.

“Extension Payment” means payments by the Sponsor (or its affiliates or permitted designees) into the Trust Account for each one-month extension of the initial business combination date.

“FDA” means the U.S. Food and Drug Administration.

“FDCA” means the U.S. Federal Food, Drug and Cosmetic Act, as amended.

“FIRRMA” means the Foreign Investment Risk Review Modernization Act of 2018, as amended.

“First Extension” means the election by GAMC to extend the date to consummate an initial business combination.

“First Extension Note” means the unsecured promissory note issued by GAMC to the Sponsor on March 17, 2023.

“First Termination Date” means March 19, 2023.

“Founder Shares” means the shares of GAMC Class B Common Stock initially purchased by the Sponsor in a private placement in January 2021, 7,047,500 of which the Sponsor voluntarily converted to shares of GAMC Class A Common Stock in March 2023 but which, unlike the Public Shares, are not subject to redemption.

“FTC” means the U.S. Federal Trade Commission.

“GAAP” means accounting principles generally accepted in the United States.

“GAMC” means Golden Arrow Merger Corp., a Delaware corporation.

4

“GAMC Board” means the board of directors of GAMC.

“GAMC Class A Common Stock” means GAMC’s Class A common stock, par value $0.0001 per share.

“GAMC Class B Common Stock” means GAMC’s Class B common stock, par value $0.0001 per share.

“GAMC Common Stock” means GAMC Class A Common Stock and GAMC Class B Common Stock.

“GAMC Proposals” means the Business Combination Proposal, the Nasdaq Proposal, the Incentive Plan Proposal, the ESPP Proposal, the Charter Amendment Proposal, the Election of Directors Proposal or any other any proposals the parties to the Business Combination Agreement deem necessary to effectuate the Business Combination.

“GAMC Unit” means one share of GAMC Class A Common Stock and one-third GAMC Warrant.

“GAMC Warrant Agreement” means the warrant agreement, dated as of March 16, 2021, by and between GAMC and Continental Stock Transfer & Trust Company, governing GAMC’s outstanding warrants.

“GAMC Warrants” means warrants to purchase shares of GAMC Class A Common Stock as contemplated under the GAMC Warrant Agreement, with each whole warrant exercisable for one share of GAMC Class A Common Stock at an exercise price of $11.50 per whole share.

“Ginkgo” means Ginkgo Bioworks, Inc.

“Ginkgo Note Purchase Agreement” means the agreement between Bolt Threads and Ginkgo, dated October 14, 2022.

“Ginkgo Note Purchase Agreement Amendment No. 1” means the amendment, dated December 29, 2023, to the Ginkgo Note Purchase Agreement.

“Ginkgo Note Purchase Agreement Amendment No. 2” means the amendment, dated April 3, 2024, to the Ginkgo Note Purchase Agreement.

“GMP” means voluntary good manufacturing practices that the FDA has historically recommended.

“Greenberg Traurig” means Greenberg Traurig, LLP.

“Guides” means the FTC Guides Concerning the Use of Endorsements and Testimonials in Advertising.

“Holders” means the Sponsor, certain stockholders of GAMC, and certain securityholders of Bolt Threads, who will enter into the Registration Rights and Lock-Up Agreement.

“HSR Act” means the Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended.

“Initial Stockholders” means GAMC’s Sponsor and holders of shares of GAMC Class B Common Stock (and any shares of GAMC Class A Common Stock issued upon the conversion thereof), issued prior to GAMC’s initial public offering.

“Investment Company Act” means the Investment Company Act of 1940, as amended.

“IPO” means GAMC’s initial public offering of units, consummated on March 19, 2021.

“IR Act” means the Inflation Reduction Act, as amended.

“IRS” means the U.S. Internal Revenue Service.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012, as amended.

“Key Bolt Threads Stockholders” means certain of the Bolt Threads’ stockholders whose names appear on the signature pages of the Stockholder Support Agreement dated October 4, 2023.

“Laurus Bio” means Laurus Bio Private Limited.

“LOI” means the letter of intent executed by GAMC and Bolt Threads, dated August 13, 2023.

5

“Merger” means the merging of Merger Sub with and into Bolt Threads, with Bolt Threads surviving the Merger as a wholly-owned subsidiary of GAMC.

“Merger Sub” means Beam Merger Sub, Inc., a Delaware corporation and wholly-owned subsidiary of GAMC.

“Merger Sub Common Stock” means Merger Sub’s common stock, par value $0.01 per share.

“MoCRA” means the Modernization of Cosmetics Regulation Act of 2022, as amended.

“Nasdaq” means the Nasdaq Stock Market LLC.

“Nasdaq Deadline” means March 19, 2024.

“NOLs” means net operating losses.

“Payment Spreadsheet” means the payment spreadsheet setting forth (i) the calculation of Aggregate Transaction Consideration, (ii) the allocation of the Aggregate Transaction Consideration among the holders of Bolt Threads Common Stock, (iii) the portion of Aggregate Transaction Consideration payable to each holder of Bolt Threads Common Stock and (iv) the number of shares of Post-Combination Company Common Stock that will be subject to each Rollover Option, Rollover RSU and Converted Warrants (each as defined in the Business Combination Agreement), in each case, prepared in good faith by Bolt Threads.

“PCAOB” means the Public Company Accounting Oversight Board.

“Per Share Transaction Consideration” means the Exchange Ratio multiplied by $10.00.

“PIPE Shares” means an aggregate of up to 2,296,975 shares of GAMC Class A Common Stock to be issued to the PIPE Subscribers in the PIPE Transaction.

“PIPE Subscribers” means the purchasers of the PIPE Shares.

“PIPE Transaction” means the sale of the PIPE Shares to the PIPE Subscribers, for a purchase price of $10.00 per share, in a private placement.

“Post-Combination Board” means the board of directors of the Post-Combination Company.

“Post-Combination Company” means GAMC immediately upon the consummation of the Business Combination and the other transactions contemplated by the Business Combination Agreement.

“Post-Combination Company Bylaws” means the GAMC amended and restated bylaws that are attached to this proxy statement/prospectus as Annex C.

“Post-Combination Company Common Stock” means shares of common stock, par value $0.0001 per share, of the Post-Combination Company.

“Private Placement Warrants” means the warrants to purchase shares of GAMC Class A Common Stock issued to the Sponsor in a private placement simultaneously with the closing of the IPO.

“Proposed Certificate of Incorporation” means the GAMC amended and restated certificate of incorporation that is attached to this proxy statement/prospectus as Annex B.

“Public Shares” means shares of GAMC Class A Common Stock issued as part of the units sold in the IPO.

“Public Stockholders” means the holders of shares of GAMC Class A Common Stock.

“Public Warrants” means the warrants included in the units sold in the IPO, each of which is exercisable for one share of GAMC Class A Common Stock, in accordance with its terms.

“Registration Rights and Lock-Up Agreement” means the Amended and Restated Registration Rights Agreement of GAMC to be entered into in connection with the Closing by the Post-Combination Company, certain stockholders of Bolt Threads, independent directors of GAMC, and Sponsor.

“Registration Statement” means the Registration Statement on Form S-4, initially filed with the SEC by GAMC (File No. 333-276849), of which this proxy statement/prospectus forms a part.

6

“ROU” means right-of-use.

“RSUs” means restricted stock units.

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002.

“SEC” means the U.S. Securities and Exchange Commission.

“Second Extension” means the election by GAMC to extend the date to consummate an initial business combination.

“Second Extension Note” means the unsecured promissory note issued by GAMC to the Sponsor on December 12, 2023.

“Second Termination Date” means December 19, 2023.

“Securities Act” means the U.S. Securities Act of 1933, as amended.

“Senior Secured Notes” means senior secured notes issued by Bolt Threads and sold to Ginkgo on October 14, 2022, pursuant to the terms of the Ginkgo Note Purchase Agreement.

“Severance Policy” means the severance policy maintained by Bolt Threads.

“special meeting” means the special meeting of the stockholders of GAMC that is the subject of this proxy statement/prospectus.

“Sponsor” means Golden Arrow Sponsor, LLC, a Delaware limited liability company.

“Sponsor Earn-Out Shares” means the 1,437,500 Sponsor Shares that Sponsor agreed will be unvested and subject to forfeiture as of the Closing and will only vest if, during the five-year period following the Closing, (i) the price of the Post-Combination Company Common Stock equals or exceeds $12.50 (as adjusted for stock splits, stock dividends, reorganizations, recapitalizations and the like) for any 20 trading days within a period of 30 consecutive trading days or (ii) there is a change of control of the Post-Combination Company during such five-year period. Any Sponsor Shares that remain unvested after the fifth anniversary of the Closing will be forfeited and canceled. The Sponsor Support Agreement will terminate upon the earliest of (i) the Effective Time, (ii) the termination of the Business Combination Agreement in accordance with its terms and (iii) the effective date of a written agreement of the parties terminating the Sponsor Support Agreement.

“Sponsor Support Agreement” means the sponsor support agreement by and between the Sponsor, GAMC, and Bolt Threads, dated October 4, 2023.

“Stockholder Support Agreement” means the Stockholder Support Agreement, dated as of October 4, 2023, by and among GAMC and the Key Bolt Threads Stockholders.

“Subscription Agreements” means the PIPE subscription agreements, as amended.

“Surviving Corporation” means the entity surviving the Merger as a wholly-owned subsidiary of GAMC.

“SRLY” means separate-return-limitation-year.

“Treasury” means the U.S. Department of the Treasury.

“Trust Account” means the trust account that holds a portion of the proceeds of the IPO and the concurrent sale of the Private Placement Warrants.

“Trust Agreement” means the Investment Management Trust Agreement, by and between GAMC and Continental Stock Transfer & Trust Company, dated as of March 16, 2021.

“warrants” means the Public Warrants together with the Private Placement Warrants.

“Warrant Agreement” means the Warrant Agreement, dated March 16, 2021, by and between GAMC and Continental Stock Transfer & Trust Company, as warrant agent.

7

QUESTIONS AND ANSWERS ABOUT THE BUSINESS COMBINATION

The following questions and answers briefly address some commonly asked questions about the proposals to be presented at the special meeting of GAMC stockholders, including with respect to the proposed Business Combination. The following questions and answers may not include all the information that is important to GAMC stockholders. Stockholders are urged to read carefully this entire proxy statement/prospectus, including the financial statements and annexes attached hereto and the other documents referred to herein.

Questions and Answers About the Special Meeting of GAMC’s Stockholders and the Related Proposals

Q. Why am I receiving this proxy statement/prospectus?

A. GAMC has entered into the Business Combination Agreement with Merger Sub and Bolt Threads, pursuant to which Merger Sub will be merged with and into Bolt Threads, with Bolt Threads surviving the Merger as a wholly-owned subsidiary of GAMC. A copy of the Business Combination Agreement is attached to this proxy statement/prospectus as Annex A. GAMC stockholders are being asked to consider and vote on the Business Combination Proposal to approve the adoption of the Business Combination Agreement and approve the Business Combination, among other proposals.

There currently are 7,765,437 shares of GAMC Common Stock issued and outstanding, consisting of 577,937 Public Shares and 7,187,500 Founder Shares. In addition, there currently are 14,583,333 GAMC Warrants issued and outstanding, consisting of 9,583,333 Public Warrants and 5,000,000 Private Placement Warrants. Each whole GAMC Warrant entitles the holder thereof to purchase one share of GAMC Class A Common Stock at a price of $11.50 per share. The GAMC Warrants will become exercisable 30 days after the completion of a business combination, and expire at 5:00 p.m., New York City time, five years after the completion of a business combination or earlier upon redemption or liquidation. The Private Placement Warrants, however, are non-redeemable so long as they are held by the Sponsor or its permitted transferees. Under its current amended and restated certificate of incorporation, GAMC must provide all Public Stockholders with the opportunity to have their Public Shares redeemed for cash upon the consummation of GAMC’s initial business combination in conjunction with a stockholder vote.

This proxy statement/prospectus and its annexes contain important information about the proposed Business Combination and the proposals to be acted upon at the special meeting. You should read this proxy statement/prospectus and its annexes carefully and in their entirety. This document also constitutes a prospectus with respect to the Post-Combination Company Common Stock issuable in connection with the Business Combination.

Q. What matters will stockholders consider at the special meeting?

A. At the special meeting, GAMC will ask its stockholders to vote in favor of the following proposals:

• The Business Combination Proposal — a proposal to approve and adopt the Business Combination Agreement and the Business Combination.

• The Charter Amendment Proposal — a proposal to adopt the proposed second amended and restated certificate of incorporation of GAMC attached as Annex B to this proxy statement/prospectus.

• The Governance Proposals — to approve, on a non-binding advisory basis, separate governance proposals relating to certain material differences between GAMC’s current amended and restated certificate of incorporation and the proposed second amended and restated certificate of incorporation.

• The Election of Directors Proposal — a proposal to elect, effective at Closing, seven directors to serve staggered terms on the board of directors until the first, second and third annual meetings of stockholders after the Closing of the Business Combination, as applicable, and until their respective successors are elected and qualified.

• The Incentive Plan Proposal — a proposal to approve and adopt the incentive plan established to be effective after the Closing of the Business Combination.

8

• The ESPP Proposal — a proposal to approve and adopt the employee stock purchase plan established to be effective after the Closing of the Business Combination.

• The Nasdaq Proposal — a proposal to issue GAMC Class A Common Stock to the Bolt Threads stockholders in the Merger pursuant to the Business Combination Agreement and to the investors in the PIPE.

• The Adjournment Proposal — a proposal to adjourn the special meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies if, based upon the tabulated vote at the time of the special meeting, there are not sufficient votes to approve one or more proposals presented to stockholders for vote.

Q. Are any of the proposals conditioned on one another?

A. The Charter Amendment Proposal, Incentive Plan Proposal, ESPP Proposal and Nasdaq Proposal are all conditioned on the approval of the Business Combination Proposal. The Election of Directors Proposal, Governance Proposals and the Adjournment Proposal are not conditioned on, and therefore do not require the approval of, the Business Combination Proposal and Business Combination to be effective. It is important for you to note that in the event that any of the Business Combination Proposal, Charter Amendment Proposal, Election of Directors Proposal, Incentive Plan Proposal, ESPP Proposal or Nasdaq Proposal is not approved, then GAMC will not consummate the Business Combination. If GAMC does not consummate the Business Combination and fails to complete an initial business combination by the Extended Date, then GAMC will be required to dissolve and liquidate. See “Information About GAMC — The Second Extension.”

Q. What will happen upon the consummation of the Business Combination?

A. On the Closing Date, Merger Sub will merge into Bolt Threads, whereupon Merger Sub will cease to exist and Bolt Threads will continue as the Surviving Corporation and become a wholly-owned subsidiary of GAMC. The Merger will have the effects specified under Delaware law. The aggregate equity consideration to be paid to Bolt Threads’ stockholders, option holders, holders of Bolt Threads RSUs and warrant holders in the Business Combination will be a number of shares of Post-Combination Company Common Stock equal to the quotient of (i) $250,000,000 (the “Equity Value”) divided by (ii) $10.00.

Q. Why is GAMC proposing the Business Combination Proposal?

A. GAMC was organized for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization or similar business combination with one or more businesses. GAMC is not limited to any particular industry or sector.

GAMC received $287,500,000 from its IPO (including net proceeds from the exercise by the underwriters of their over-allotment option) and sale of the Private Placement Warrants, which was placed into the Trust Account immediately following the IPO.

On March 15, 2023, GAMC’s stockholders approved an amendment to GAMC’s amended and restated certificate of incorporation and an amendment to the trust agreement. The amendments enabled GAMC to extend the period of time it had to consummate an initial business combination from March 19, 2023 (the “First Termination Date”) to December 19, 2023, by electing to extend the date to consummate an initial business combination on a monthly basis for up to nine times by an additional one month each time after the First Termination Date, until December 19, 2023 or a total of up to nine months after the First Termination Date, or such earlier date as determined by the GAMC Board (the “First Extension”), unless the closing of GAMC’s initial business combination shall have occurred, provided that the Sponsor (or its affiliates or permitted designees) had deposited into the Trust Account an amount determined by multiplying $0.03 by the number of Public Shares then outstanding, up to a maximum of $105,000 for each such one-month extension unless the closing of GAMC’s initial business combination shall have occurred, in exchange for a non-interest bearing, unsecured promissory note payable upon consummation of a business combination. In connection with the votes to approve the First Extension, the holders of 26,649,519 shares of GAMC Class A Common Stock properly exercised their right to redeem their shares for cash at a redemption price of approximately $10.16 per share, for an aggregate redemption amount of approximately $270.8 million, leaving approximately $21.3 million in the Trust Account immediately following redemptions.

9

On December 12, 2023, GAMC’s stockholders approved an additional amendment to GAMC’s amended and restated certificate of incorporation to extend the period of time it had to consummate an initial business combination from December 19, 2023 (the “Second Termination Date”) to September 19, 2024, by electing to extend the date to consummate an initial business combination on a monthly basis for up to nine times by an additional one month each time after the Second Termination Date, until September 19, 2024 or a total of up to nine months after the Second Termination Date, or such earlier date as determined by the GAMC Board (the “Second Extension” and such later date, the “Extended Date”), unless the closing of GAMC’s initial business combination shall have occurred, provided that the Sponsor (or its affiliates or permitted designees) will deposit into the Trust Account an amount determined by multiplying $0.02 by the number of Public Shares then outstanding, up to a maximum of $20,000 for each such one-month extension, in exchange for a non-interest bearing, unsecured promissory note payable upon consummation of a business combination (each, an “Extension Payment”). In connection with the votes to approve the Second Extension, the holders of 1,522,544 shares of GAMC Class A Common Stock properly exercised their right to redeem their shares for cash at a redemption price of approximately $10.71 per share, for an aggregate redemption amount of approximately $16.3 million, leaving approximately $6.2 million in the Trust Account immediately following redemptions.

As of December 31, 2023, GAMC had approximately $6.2 million in the Trust Account (including an aggregate of $578,694 of Extension Payments deposited into the Trust Account).

There currently are 7,765,437 shares of GAMC Common Stock issued and outstanding, consisting of 577,937 Public Shares and 7,187,500 Founder Shares. In addition, there currently are 14,583,333 GAMC Warrants issued and outstanding, consisting of 9,583,333 Public Warrants and 5,000,000 Private Placement Warrants. Each whole GAMC Warrant entitles the holder thereof to purchase one share of GAMC Class A Common Stock at a price of $11.50 per share. The GAMC Warrants will become exercisable 30 days after the completion of a business combination, and expire at 5:00 p.m., New York City time, five years after the completion of a business combination or earlier upon redemption or liquidation. The Private Placement Warrants, however, are non-redeemable so long as they are held by their initial purchasers or their permitted transferees.

Under GAMC’s amended and restated certificate of incorporation, GAMC must provide all Public Stockholders with the opportunity to have their Public Shares redeemed for cash upon the consummation of GAMC’s initial business combination in conjunction with a stockholder vote.

In accordance with GAMC’s amended and restated certificate of incorporation, the funds held in the Trust Account will be released upon the consummation of the Business Combination. See the question entitled “What happens to the funds held in the Trust Account upon consummation of the Business Combination?”

Q. Who is Bolt Threads?

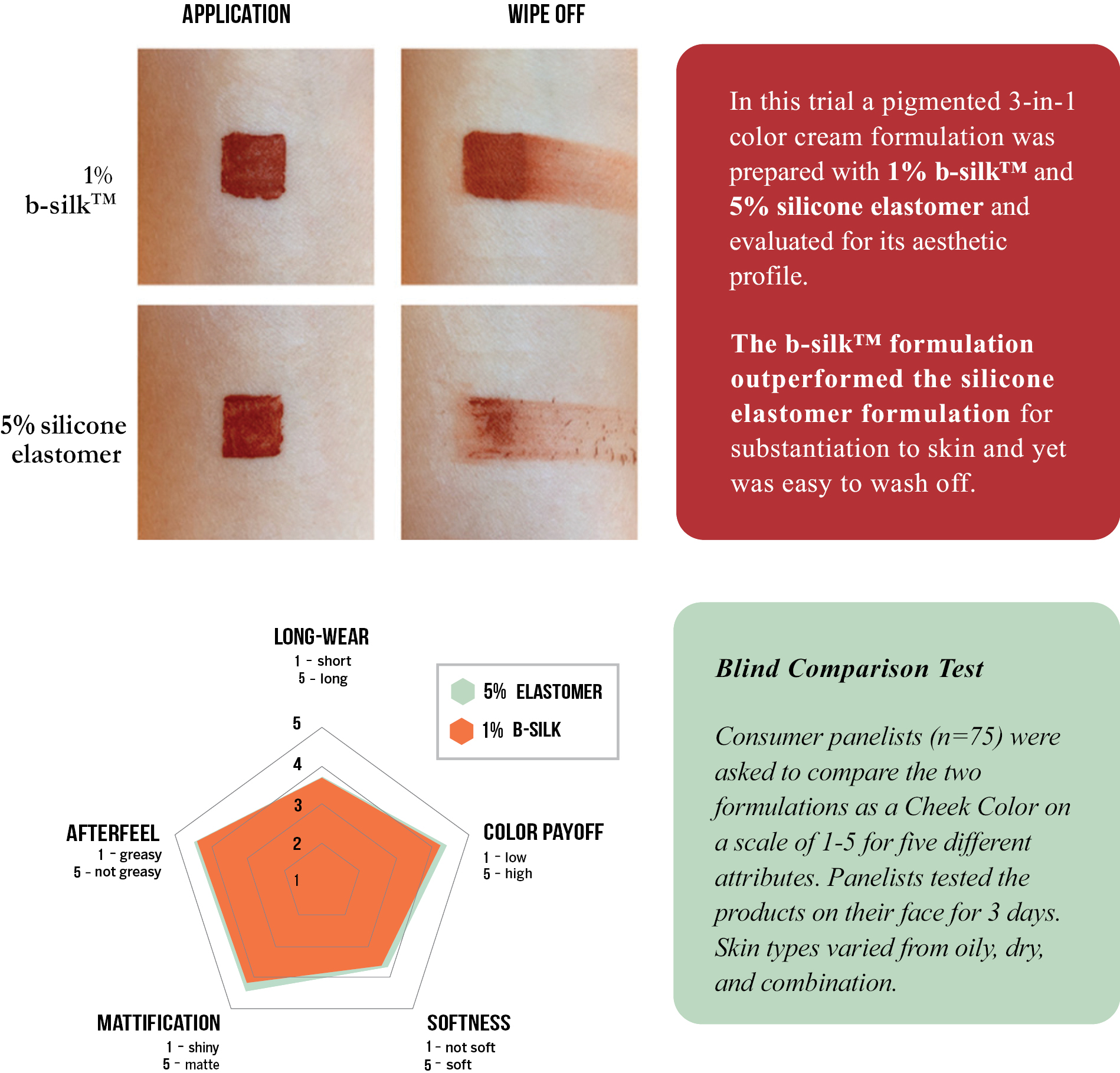

Bolt Threads is built on a biomaterials platform that aims to disrupt and transform high-volume consumer goods industries. Bolt Threads is a pioneer in the consumer biomaterials space. Its key product, b-silk, is a fully biodegradable, non-toxic, and versatile ingredient for the beauty industry that has been on the market since 2019. Its intellectual property portfolio is anchored by 52 granted patents and 176 pending patent applications.

In the years ended December 31, 2023 and 2022, Bolt Threads incurred net losses of $57.7 million and $51.7 million, respectively. As of December 31, 2023, Bolt Threads’ accumulated deficit was $396.4 million. Prior to the Business Combination, Bolt Threads’ history of losses and negative cash flows from operations and need for substantial capital raise substantial doubt about its ability to continue as a going concern. See “Information About Bolt Threads,” “Risk Factors,” “Bolt Threads Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Bolt Threads’ financial statements included elsewhere in this proxy statement/prospectus.

10

Q. How much dilution may non-redeeming GAMC stockholders experience in connection with the Business Combination and what equity stake will current GAMC stockholders and Bolt Threads Stockholders have in the Post-Combination Company after the Closing?

A. GAMC’s Public Stockholders are not required to vote “FOR” the Business Combination in order to exercise their redemption rights. Accordingly, the Business Combination may be consummated even though the funds available from the Trust Account and the number of Public Stockholders are reduced as a result of redemptions by Public Stockholders. The Business Combination Agreement does not include any closing condition relating to a minimum amount of cash proceeds available to the Post-Combination Company following redemptions. The PIPE Subscribers’ obligations under the Subscription Agreements are subject to the aggregate gross proceeds (x) under the Note Purchase Agreement (inclusive of proceeds received by the Company as consideration for promissory notes issued in October 2023 and March 2024), (y) under the Subscription Agreements and (z) remaining in the Trust Account at the Closing following redemptions being no less than $32.0 million (less any amounts that GAMC is entitled to withdraw from the Trust Account to pay tax obligations owed by GAMC as of the Closing Date in excess of $140,000 in the aggregate). The gross proceeds actually raised under the Note Purchase Agreement and the gross proceeds committed under the Subscription Agreements are $34.9 million, such that GAMC and Bolt Threads expect this condition to be satisfied even if all of GAMC’s outstanding Public Shares are redeemed in connection with the Business Combination.

If a Public Stockholder exercises its redemption rights, such exercise will not result in the loss of any Public Warrants that it may hold. GAMC cannot predict the ultimate value of the GAMC Warrants following the consummation of the Business Combination, but based on the price per Public Warrant of $[•] on [•], 2024, the most recent practicable date prior to the date of this proxy statement/prospectus, the 9,583,333 retained outstanding Public Warrants would have an aggregate value of $[•]. In addition, on [•], 2024, the most recent practicable date prior to the date of this proxy statement/prospectus, the price per share of GAMC Class A Common Stock closed at $[•]. If the shares of GAMC Class A Common Stock are trading above the exercise price of $11.50 per warrant, the warrants are considered to be “in the money” and are therefore more likely to be exercised by the holders thereof (when they become exercisable). This in turn increases the risk to the non-redeeming Public Stockholders that the warrants will be exercised, which would result in immediate dilution to the non-redeeming Public Stockholders.

The following table illustrates varying ownership levels in the Post-Combination Company following the Closing, assuming no redemptions of any of GAMC’s Public Shares in connection with the special meeting to approve the Business Combination, redemption of 50% of GAMC’s Public Shares in connection with the special meeting to approve the Busines Combination and the redemption of all of GAMC’s outstanding Public Shares in connection with the special meeting to approve the Business Combination:

|

Assuming No |

Assuming 50% Redemption |

Assuming Max Redemption |

||||||||||||||||

|

Stockholder |

Shares |

Percentage |

Shares |

Percentage |

Shares |

Percentage |

||||||||||||

|

Public Stockholder |

|

577,937 |

1.7 |

% |

|

288,969 |

0.9 |

% |

|

— |

— |

|

||||||

|

Sponsor and GAMC Independent Directors(1) |

|

7,660,187 |

23.1 |

% |

|

7,660,187 |

23.3 |

% |

|

7,660,187 |

23.5 |

% |

||||||

|

Former Bolt Threads Securityholders under Business Combination Agreement(2) |

|

22,634,758 |

68.2 |

% |

|

22,634,758 |

68.8 |

% |

|

22,634,758 |

69.5 |

% |

||||||

|

PIPE Shares – Sponsor(3) |

|

656,499 |

2.0 |

% |

|

656,499 |

2.0 |

% |

|

656,499 |

2.0 |

% |

||||||

|

PIPE Shares – Former Bolt Threads Securityholders |

|

1,640,476 |

5.0 |

% |

|

1,640,476 |

5.0 |

% |

|

1,640,476 |

5.0 |

% |

||||||

|

Total Shares Outstanding |

|

33,169,857 |

100.0 |

% |

|

32,880,889 |

100.00 |

% |

|

32,591,920 |

100.00 |

% |

||||||

|

Implied Per Share Value(4) |

$ |

7.72 |

|

$ |

7.70 |

|

$ |

7.67 |

|

|||||||||

____________

(1) Amount includes (i) 140,000 Founder Shares held by GAMC’s independent directors, (ii) 1,437,500 Sponsor Earn-Out Shares subject to vesting and forfeiture but that will confer the right to vote prior to vesting and (iii) 472,687 shares to be issued in connection with the Sponsor’s Bridge Warrants, which will be automatically exercised into Bolt Threads Common Stock immediately prior to Closing and exchanged for Post-Combination Company Common Stock.

(2) Estimated number of shares of Post-Combination Company Common Stock that would be issued to Bolt Threads securityholders pursuant to the Business Combination Agreement at Closing, based on shares of Bolt Threads capital stock outstanding as of March 1, 2024, and an assumed exchange ratio of 0.4661. The actual number of outstanding shares of Post-Combination Company Common Stock held by former Bolt Threads securityholders at Closing will vary depending on the number of shares of Bolt Threads capital stock outstanding immediately prior to Closing.

11

(3) Assumes the purchase by the Sponsor of the maximum number of PIPE Shares Sponsor may be obligated to purchase pursuant to its Subscription Agreement. However, the number of PIPE Shares to be purchased by the Sponsor will be reduced by the number of shares of GAMC Class A Common Stock that have not been elected for redemption as of the expiration of the redemption period related to the Closing and that are held by certain individuals mutually agreed upon by GAMC and Bolt Threads at any time up to immediately prior to the expiration of such redemption period. The no additional redemption scenario assumes that none of the outstanding public shares are redeemed in connection with the Business Combination, and that there is no corresponding reduction to the number of PIPE Shares Sponsor is required to buy. However, the actual reduction in number of PIPE Shares Sponsor is required to buy will only be to the extent unredeemed public shares are held by individuals mutually agreed upon by GAMC and Bolt Threads prior to the expiration of the redemption period.

(4) Calculation of implied per share value assumes (i) an enterprise value of $250 million of Bolt Threads upon consummation of the Business Combination, (ii) approximately (A) $6.2 million of proceeds from GAMC Class A Common Stock assuming no redemptions; (B) $3.1 million of proceeds from GAMC Class A Common Stock assuming 50% redemptions; and (C) no proceeds assuming maximum redemptions of GAMC Class A Common Stock and (iii) approximately $34.9 million of gross proceeds actually raised under the Note Purchase Agreement and the gross proceeds committed under the Subscription Agreements.

Stockholders will experience additional dilution to the extent the Post-Combination Company issues additional shares after the Closing. The tables above do not include (i) shares expected to be issued to various advisors and former creditors of the parties following the Closing, (ii) shares issuable upon exercise or settlement of equity awards or warrants of Bolt Threads that are expected to remain outstanding after the Closing, (iii) up to 9,583,333 shares of Post-Combination Company Common Stock that will be issuable upon exercise of the Public Warrants, which have an initial exercise price of $11.50 per share (subject to adjustment in accordance with the Warrant Agreement), (iv) up to 5,000,000 shares of Post-Combination Company Common Stock that will be issuable upon exercise of the Private Placement Warrants, which have an initial exercise price of $11.50 per share (subject to adjustment in accordance with the Warrant Agreement), (v) shares of Post-Combination Company Common Stock that will be available for issuance under the 2024 Incentive Plan, which will initially be equal to 15% of the fully-diluted shares as of the Closing or (vi) shares of Post-Combination Company Common Stock that will be available for issuance under the ESPP, which will initially be equal to 2% of the fully-diluted shares as of the Closing.

The following table illustrates the impact on relative ownership levels assuming the issuance of all such shares.

|

Assuming No |

Assuming 50% Redemption |

Assuming Max |

||||||||||||||||

|

Stockholder |

Shares |

Percentage |

Shares |

Percentage |

Shares |

Percentage |

||||||||||||

|

Public Stockholders |

|

577,937 |

1.0 |

% |

|

288,969 |

0.5 |

% |

|

— |

— |

|

||||||

|

Sponsor and GAMC Independent Directors(1) |

|

7,660,187 |

13.5 |

% |

|

7,660,187 |

13.6 |

% |

|

7,660,187 |

13.6 |

% |

||||||

|

Former Bolt Threads Securityholders(2) |

|

22,634,758 |

39.8 |

% |

|

22,634,758 |

40.1 |

% |

|

22,634,758 |

40.3 |

% |

||||||

|

Advisors and Former |

|

1,250,000 |

2.2 |

% |

|

1,250,000 |

2.2 |

% |

|

1,250,000 |

2.2 |

% |

||||||

|

Bolt Threads Equity Awards and Warrants(4) |

|

2,756,537 |

4.9 |

% |

|

2,756,537 |

4.9 |

% |

|

2,756,537 |

4.9 |

% |

||||||

|

Shares underlying Public Warrants |

|

9,583,333 |

16.9 |

% |

|

9,583,333 |

17.0 |

% |

|

9,583,333 |

17.1 |

% |

||||||

|

Shares underlying Private Placement Warrants |

|

5,000,000 |

8.8 |

% |

|

5,000,000 |

8.9 |

% |

|

5,000,000 |

8.9 |

% |

||||||

|

Shares initially reserved for issuance under the 2024 Incentive Plan(5) |

|

6,492,721 |

11.4 |

% |

|

6,449,376 |

11.4 |

% |

|

6,406,030 |

11.4 |

% |

||||||

|

Shares initially reserved for issuance under the ESPP(5) |

|

865,696 |

1.5 |

% |

|

859,917 |

1.5 |

% |

|

854,137 |

1.5 |

% |

||||||

|

Total Shares Outstanding |

|

56,821,169 |

100.0 |

% |

|

56,483,077 |

100.0 |

% |

|

56,144,982 |

100.0 |

% |

||||||

|

Implied Per Share Value(6) |

$ |

4.51 |

|

$ |

4.48 |

|

$ |

4.45 |

|

|||||||||

____________

(1) Amount includes (i) 140,000 Founder Shares held by GAMC’s independent directors, (ii) 1,437,500 Sponsor Earn-Out Shares, and (iii) an assumed purchase by the Sponsor of 656,499 PIPE Shares. However, the number of PIPE Shares to be purchased by the Sponsor will be reduced by the number of shares of GAMC Class A Common Stock that have not been

12

elected for redemption as of the expiration of the redemption period related to the Closing and that are held by certain individuals mutually agreed upon by GAMC and Bolt Threads at any time up to immediately prior to the expiration of such redemption period.

(2) Amount includes (i) the purchase of 1,640,476 PIPE Shares by current securityholders of Bolt Threads and (ii) the estimated number of shares of Post-Combination Company Common Stock that would be issued to Bolt Threads securityholders pursuant to the Business Combination Agreement at Closing, based on shares of Bolt Threads capital stock outstanding as of March 1, 2024, and an assumed exchange ratio of 0.4661. The actual number of outstanding shares of Post-Combination Company Common Stock held by former Bolt Threads securityholders at Closing will vary depending on the number of shares of Bolt Threads capital stock outstanding immediately prior to Closing.

(3) Consists of (i) 600,000 shares of the Post-Combination Company to be issued to the landlord of Bolt Threads’ Berkeley lease, pursuant to a lease termination agreement upon Closing or shortly thereafter; (ii) 150,000 shares of the Post-Combination Company to be issued to Bolt Threads’ vendor, pursuant to a vendor termination agreement upon Closing or shortly thereafter; and (iii) 500,000 shares of shares of Post-Combination Company Common Stock to be issued to BTIG as partial compensation in lieu of the deferred cash underwriting commission otherwise due to BTIG at the Closing in connection with GAMC’s IPO. The number of shares issuable to BTIG will be equivalent to the greater of (i) 500,000 shares of Post-Combination Company Common Stock, or (ii) the number of shares calculated by dividing (x) $5,000,000 by (y) the volume-weighted average price of the Post-Combination Company Common Stock over the three trading days immediately preceding the initial filing of the registration statement relating to the resale of such shares, provided that clause (y) shall not be less than $8.00 per share. In no event will the number of shares issuable to BTIG be greater than 625,000.

(4) Consists of (i) 1,768,981 shares of Post-Combination Company Common Stock issued or issuable upon the vesting of restricted stock units currently held by Bolt Threads securityholders; (ii) 850,259 shares of Post-Combination Company Common Stock issued or issuable upon the exercise of options currently held by Bolt Threads securityholders; and (iii) 137,297 shares of Post-Combination Company issuable upon the exercise of warrants currently held by Bolt Threads securityholders that will not be automatically exercised in connection with the Closing.

(5) The number of shares of Post-Combination Company Common Stock available for issuance under the 2024 Incentive Plan and the ESPP will be annually increased on January 1 of each calendar year beginning in 2025 and ending in 2034 by amounts described in the sections entitled “Proposal No. 5 — The Incentive Plan Proposal” and “Proposal No. 6 — The ESPP Proposal” elsewhere in this proxy statement/prospectus.

(6) Calculation of implied per share value assumes (i) an enterprise value of $250 million of Bolt Threads upon consummation of the Business Combination, (ii) approximately (A) $6.2 million of proceeds from GAMC Class A Common Stock prior to any redemptions; (B) $3.1 million of proceeds from GAMC Class A Common Stock assuming 50% redemptions; and (C) no proceeds assuming maximum redemptions of GAMC Class A Common Stock, (iii) approximately $34.9 million of gross proceeds actually raised under the Note Purchase Agreement and the gross proceeds committed under the Subscription Agreements and (iv) none of the GAMC Warrants or Bolt Threads options or warrants are exercised for cash.

Additionally, subject to the rules of Nasdaq and the Post-Combination Company’s organizational documents, the board of directors of the Post-Combination Company will retain broad authority after the Closing to issue additional capital stock without obtaining stockholder approval.

GAMC paid BTIG, the representative in GAMC’s IPO, an underwriting discount of $0.20 per GAMC Unit sold in the IPO, and agreed to pay a deferred underwriting fee of $0.35 per GAMC Unit sold in the IPO (or $8,750,000) upon the consummation of GAMC’s initial business combination. On February 2, 2024, BTIG, Bolt Threads and GAMC entered into an amendment to the underwriting agreement between BTIG and GAMC, pursuant to which, in lieu of the initial deferred underwriting fee of $8,750,000, $500,000 will be deposited and held in the Trust Account and payable in cash directly from the Trust Account, without accrued interest, to BTIG for its own account upon consummation of GAMC’s initial Business Combination. Additionally, upon consummation of GAMC’s initial Business Combination, BTIG will receive shares of Post-Combination Company Common Stock as described in footnote 3 above.

No portion of the payment to BTIG is subject to adjustment to account for redemptions of GAMC Class A Common Stock by Public Stockholders.

Q. Who will be the officers and directors of GAMC if the Business Combination is consummated?

A. The Business Combination Agreement provides that, immediately following the consummation of the Business Combination, the board of directors of the Post-Combination Company (the “Post-Combination Board”) will be comprised of seven individuals designated as provided in the Business Combination Agreement, who are currently expected to include Daniel Widmaier, David Breslauer, and [•]. The directors of the Post-Combination Board shall be designated as follows: (A) two directors shall be designated by Bolt Threads, who shall be the founders of Bolt Threads, (B) one director shall be designated by the Sponsor, who shall be reasonably acceptable to Bolt Threads, and (C) four directors shall be designated by the Chief

13

Executive Officer of Bolt Threads in good faith consultation with GAMC and who shall each qualify as an “independent director” as such term is defined in Nasdaq Listing Rule 5605(a)(2). Immediately following the consummation of the Business Combination, we expect that the following will be the officers of the Post-Combination Company: Daniel Widmaier, David Breslauer, Randy Befumo, Cintia Nardi and Paul Slattery. See “Management of the Post-Combination Company Following the Business Combination.”

Q. What conditions must be satisfied to complete the Business Combination?

A. There are a number of closing conditions in the Business Combination Agreement, including that GAMC’s stockholders have approved and adopted the Business Combination Agreement. For a summary of the conditions that must be satisfied or waived prior to completion of the Business Combination, see the section entitled “The Business Combination Agreement — Conditions to Closing.”

Q. What happens if I sell my shares of GAMC Class A Common Stock before the special meeting of stockholders?

A. The record date for the special meeting of stockholders will be earlier than the date that the Business Combination is expected to be completed. If you transfer your shares of GAMC Class A Common Stock after the record date, but before the special meeting of stockholders, unless the transferee obtains from you a proxy to vote those shares, you will retain your right to vote at the special meeting of stockholders.

Q. What vote is required to approve the proposals presented at the special meeting of stockholders?

A. The approval of the Business Combination Proposal, Governance Proposals (on an advisory basis), Incentive Plan Proposal, ESPP Proposal, Nasdaq Proposal and Adjournment Proposal requires the affirmative vote in person (which would include presence at a virtual meeting) or by proxy of the holders of a majority of the then outstanding shares of GAMC Common Stock present and entitled to vote at the special meeting. Accordingly, an GAMC stockholder’s failure to vote by proxy or to vote in person at the special meeting of stockholders or a broker non-vote will have no effect on these proposals. An abstention will have the same effect as a vote against these proposals.