Filed by Carbon Revolution Public Limited Company

Pursuant to Rule 425 under the Securities Act of 1933

and deemed filed pursuant to Rule 14a-12

under the Securities Exchange Act of 1934

Subject Company: Twin Ridge Capital Acquisition Corp.

|

Carbon Revolution Limited

Geelong Technology Precinct

75 Pigdons Road

Waurn Ponds, 3216

Australia

ABN: 96 128 274 653

|

|

Carbon Revolution (ASX code: CBR)

PRELIMINARY FY23 FINANCIAL RESULTS (UNAUDITED)

Geelong, Australia, 31 August 2023: Geelong-based advanced manufacturer Carbon Revolution Limited (the “Company” or “Carbon Revolution”) (ASX:CBR), whose lightweight carbon fiber wheels are used on some of

the world’s best cars, today released its preliminary (unaudited) financial results for the financial year ended 30 June 2023 (“FY23”).

Commenting on the FY23 results the Company’s CEO and MD, Jake Dingle said: “The year has been one of significant operational achievement for Carbon Revolution. We are experiencing strong growth in demand for our

carbon fiber wheels. With four new programs awarded during the year and combined with changes to existing awarded programs, our projected revenue backlog1 has more than doubled since October 2022 to over US$680 (AU$970) million. This

strong demand for our wheels and the nearing completion of the transformational proposed merger provides Carbon Revolution with a clear pathway to profitable long-term growth”.

FY23 Highlights

| • |

4 programs awarded for the financial year – along with two further awards in FY24 to date – takes all-time total awarded programs to 18 with six global OEMs.

|

| • |

Backlog2 has more than doubled to US$680 (AU$970) million since October 2022, due primarily to new program awards. Almost 50% of backlog is for Electric Vehicles.

|

| • |

Jaguar Land Rover revealed the 2024 Range Rover Sport SV, the first vehicle in the SUV segment featuring Carbon Revolution’s carbon fiber wheels. Ford also revealed the Mustang Dark Horse, marking Carbon

Revolution’s first core vehicle program with Ford3,

|

| • |

Exited the year with strong production cost improvement following Mega-line commissioning and increased volumes.

|

| • |

Merger announced with Twin Ridge Capital Acquisition Corp. (“TRCA”) and a US$60 (AU$85.8) million debt program completed.

|

1 Backlog as of 29th May 2023. Backlog (remaining lifetime gross program projected revenue) is based on awarded programs and excludes programs that are contracted for engineering. See Projection Methodologies from 6th June 2023 ASX

announcement titled “Revised Financial Projections for CY23 and Accompanying Presentation”.

2 As above.

3 As compared to a Ford Special Vehicle Team. Supplying a core vehicle program at Ford is an important step in allowing a wider adoption of the Company’s lightweight wheel technology within the Ford portfolio.

Merger Transaction Update

In November 2022, Carbon Revolution announced a proposed merger, referred to as the “Transaction”, with TRCA. The Transaction, and subsequent access to U.S. capital markets, are anticipated to unlock critical

investment capital to fund operations, capital expenditure and strategic growth opportunities, support commercialization and accelerate the path to expected profitability. The Transaction is expected to complete in October or November 2023. At

completion of the Transaction, Carbon Revolution will be acquired by Carbon Revolution plc, an Irish company whose shares are expected to be traded on NYSE American, and the Company’s shares shall cease to be quoted on the ASX.

Program Update

The Company is experiencing strong growth in demand for its carbon fiber wheels. Four programs awarded across FY23, combined with changes to existing awarded programs, have doubled our backlog since October 2022 to

over US$680 (AU$970) million4. Approximately 50% of the backlog is associated with Electric Vehicle programs. A further two programs were awarded in August, subsequent to FY23.

One newly awarded program is with a new customer, a premium brand of a major European OEM. This has added to our impressive track record, with a cumulative count of 18 awarded wheel programs (as of 31 August 2023)

with six global OEMs, 5 in aftersales, 6 in production and 7 programs in development.

Other program highlights through FY23 included:

| • |

Ford launched the new Mustang ‘Dark Horse’ with Carbon Revolution’s carbon fiber wheels. This marks Carbon Revolution's first core vehicle program with Ford, demonstrating broader adoption of our lightweight wheel technology.

|

| • |

General Motors’ Chevrolet Corvette E-Ray, the second Corvette model will also feature Carbon Revolution wheels as announced early in the second half of the financial year. The E-Ray will be the first Corvette to utilize electric power in

addition to its V8 engine, and the first all-wheel drive Corvette.

|

| • |

Jaguar Land Rover revealed the 2024 Range Rover Sport SV with Carbon Revolution carbon fiber wheels. This is Carbon Revolution’s debut in the SUV carbon fiber wheel sector, highlighting an important expansion of our advanced lightweight

wheel technology into the SUV segment.

|

New Debt Program

Improved access to international capital markets is being progressed. In addition to progressing the Transaction in May 2023, a new US$60 (AU$42) million debt program (secured by the Company’s assets, including its

intellectual property) was completed, providing funding for Mega-line automation and capacity expansion, general corporate and other working capital purposes. It was also used to refinance existing debt and to pay creditors who had assisted the

Company with its liquidity initiatives.

4 See footnote 1 above.

2

Operational progress

Installation and commissioning of phase 1 of the Mega-line is progressing well with production wheels now being produced on the Mega-line. Through the final months of FY23 the Company saw production rates rise

steadily, with improved reliability and tool loop cycle times and improved labor productivity. This resulted in significantly improved production costs at year end.

Financials (Unaudited)

FY23 revenue of US$26.8 (AU$38.3) million was 5% down on the financial year ended 30 June 2022 (FY22) and below the Company’s original expectations primarily due to timing of the Corvette program. Corvette wheel

sales were pushed back by approximately 6 months from early to mid FY23 after General Motors delayed wheel orders due to their broader supply chain challenges on the vehicle. Shipments resumed progressively for this program from January 2023. The

average price of wheels sold in FY23 was US$1,993 (AU$2,847), a 6% increase on FY22 due primarily to product mix changes.

Initial revenue from the newly launched Range Rover Sport SV program was included in FY23 following production commencing in the third quarter of FY23. We exited the financial year with strong sales momentum.

In July 2023 the Company passed 70,000 cumulative wheels sold.

We exited the year with strong production cost improvement following Mega-line commissioning and increased volumes. Contribution margin increased by 33% to US$1,75 (AU$2.5) million in FY23 driven by improved Q4

operating performance.

Operating, selling and administrative expenses changed little from FY22 to FY23 as inflationary pressures on these expenses were offset by a focus on cost control.

Finance costs of US$3.85 (AU$5.5) million and capital raising costs of US$17.3 (AU$24.7) million were incurred in FY23 to support the New Debt Program and the Transaction. These higher finance and capital raising

costs substantially contributed to the increased loss after tax of US$55.4 (AU$79.2) million, compared with a loss of US$33.4 (AU$47.8) million in FY22.

While the Company continued to support Mega-line milestones and invested in program development, management of cash expenditure and collections was a priority focus throughout the year given balance sheet constraints, especially before the

completion of the New Debt Program in May 2023.

Net cash provided by financing activities significantly increased by US$44.2 (AU$63.2) million, arising primarily from the net proceeds of the New Debt Program.

The Group is managing its liquidity to enable it to complete the Transaction which is expected to occur in October or November 2023. Liquidity initiatives include support from customers and suppliers. While these

initiatives are expected to enable the Company to complete the Transaction, there can be no assurance that the Transaction will complete at the expected time or that Company will have sufficient liquidity to complete the Transaction. If the

Transaction is not realized or is delayed, the Group will have to seek other options including delaying or reducing operating and capital expenditure, considering the possibility of an alternative transaction or fundraising, and in the event that

none of these are available, the Board may be forced to place the Company into liquidation or voluntary administration.

3

The Directors are of the opinion that it is appropriate for the Company to prepare the unaudited financial statement on the basis that the Group is a going concern. The financial statements do not include any

adjustments relating to the recoverability and classification of recorded asset amounts or to the amounts and classification of liabilities that might be necessary should the Company not continue as a going concern. Notwithstanding this assessment,

there exists a material uncertainty that casts doubt on the Company’s ability to continue as a going concern for at least the next 12 months. Therefore, the Company may be unable to realize its assets and discharge its liabilities in the normal

course of business. The independent auditor’s audit report is expected to highlight this matter by noting the existence of a material uncertainty in relation to the Company’s ability to continue as a going concern and referring to the Company’s

disclosures in the attached financial statements. Refer to Note 1 of the Company’s financial statements for further detail regarding the basis of preparation of the financial statements.

- ENDS -

Approved for release by the Board of Directors of Carbon Revolution Limited.

For further information, please contact:

Investors

Investors@carbonrev.com

Investors@carbonrev.com

Media

Media@carbonrev.com

Media@carbonrev.com

ABOUT CARBON REVOLUTION

Carbon Revolution is an Australian technology company, which has successfully innovated, commercialized and industrialized the advanced manufacture of carbon fiber wheels for the global automotive industry. The Company has progressed from

single prototypes to designing and manufacturing lightweight wheels for cars and SUVs in the high performance, premium and luxury segments, for the world’s most prestigious automotive brands. Carbon Revolution is creating a significant and

sustainable advanced technology business that supplies its lightweight wheel technology to automotive manufacturers around the world.

For more information, visit carbonrev.com

Information about Proposed Business Combination for shareholders of Twin Ridge Capital Acquisition Corp

As previously announced, Carbon Revolution Limited (“CBR”, “Carbon Revolution” or the “Company”) (ASX: CBR) and Twin Ridge Capital Acquisition Corp. (“Twin Ridge” or “TRCA”) (NYSE: TRCA) have entered into a definitive business combination

agreement and accompanying scheme implementation deed (“SID”) that is expected to result in the Carbon Revolution business becoming publicly listed in the U.S. via a series of transactions, including a scheme of arrangement. Upon closing of the

transactions, the ordinary shares and warrants of the merged company, Carbon Revolution plc. (formerly known as Poppetell Limited), a public company incorporated in Ireland with registered number 607450 (“MergeCo”), that will become the parent

company of the Company and Twin Ridge, are expected to trade on the NYSE American in the United States, and Carbon Revolution’s shares shall be delisted from the ASX.

4

Additional Information about the Proposed Business Combination and Where to Find It

This communication relates to the proposed business combination involving CBR, TRCA, MergeCo, and Poppettell Merger Sub, a Cayman Islands exempted company and wholly owned subsidiary of MergeCo (“Merger Sub”). In connection with the proposed

business combination, MergeCo has filed with the U.S. Securities and Exchange Commission (the “SEC”) a Registration Statement on Form F-4 (the “Registration Statement”) and several amendments thereto, including a preliminary proxy statement of

TRCA and a preliminary prospectus of MergeCo relating to the MergeCo Shares to be issued in connection with the proposed business combination. The Registration Statement, as amended, is subject to SEC review and further revision and is not yet

effective. This communication is not a substitute for the Registration Statement, the definitive proxy statement/final prospectus, when available, or any other document that MergeCo or TRCA has filed or will file with the SEC or send to its

shareholders in connection with the proposed business combination. This communication does not contain all the information that should be considered concerning the proposed business combination and other matters and is not intended to form the

basis for any investment decision or any other decision in respect of such matters.

BEFORE MAKING ANY VOTING OR INVESTMENT DECISION, TRCA’S SHAREHOLDERS AND OTHER INTERESTED PARTIES ARE URGED TO READ THE PRELIMINARY PROXY STATEMENT/PROSPECTUS AND THE DEFINITIVE PROXY

STATEMENT/ PROSPECTUS, WHEN IT BECOMES AVAILABLE, AND ANY AMENDMENTS THERETO AND ANY OTHER DOCUMENTS FILED BY TRCA OR MERGECO WITH THE SEC IN CONNECTION WITH THE PROPOSED BUSINESS COMBINATION OR INCORPORATED BY REFERENCE THEREIN IN THEIR

ENTIRETY BEFORE MAKING ANY VOTING OR INVESTMENT DECISION WITH RESPECT TO THE PROPOSED BUSINESS COMBINATION BECAUSE THEY CONTAIN IMPORTANT INFORMATION ABOUT THE PROPOSED BUSINESS COMBINATION AND THE PARTIES TO THE PROPOSED BUSINESS COMBINATION.

After the Registration Statement, as amended, is declared effective, the definitive proxy statement will be mailed to shareholders of TRCA as of a record date to be established for voting on the proposed business combination. Additionally,

TRCA and MergeCo will file other relevant materials with the SEC in connection with the proposed business combination. Copies of the Registration Statement, as amended, the definitive proxy statement/ prospectus and all other relevant materials

for the proposed business combination filed or that will be filed with the SEC may be obtained, when available, free of charge at the SEC’s website at www.sec.gov. In addition, the documents filed by TRCA or MergeCo may be obtained, when

available, free of charge from TRCA at www.twinridgecapitalac.com. TRCA’s shareholders may also obtain copies of the definitive proxy statement/prospectus, when available, without charge, by directing a request to Twin Ridge Capital Acquisition

Corp., 999 Vanderbilt Beach Road, Suite 200, Naples, Florida 60654.

No Offer or Solicitation

This communication is for information purposes only and is not intended to and does not constitute, or form part of, an offer, invitation or the solicitation of an offer or invitation to purchase, otherwise acquire, subscribe for, sell or

otherwise dispose of any securities, or the solicitation of any vote or approval in any jurisdiction, pursuant to the proposed business combination or otherwise, nor shall there be any sale, issuance or transfer of securities in any jurisdiction

in contravention of applicable law. The proposed business combination will be implemented solely pursuant to the Business Combination Agreement and Scheme Implementation Deed, in each case, filed as exhibits to the Current Report on Form 8-K

filed by TRCA with the SEC on November 30, 2022, which contains the full terms and conditions of the proposed business combination. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities

Act.

5

Participants in the Solicitation of Proxies

This communication may be deemed solicitation material in respect of the proposed business combination. TRCA, CBR, MergeCo, Merger Sub and their respective directors and executive officers, under SEC rules, may be deemed to be participants in

the solicitation of proxies from TRCA’s shareholders in connection with the proposed business combination. Investors and security holders may obtain more detailed information regarding the names and interests in the proposed business combination

of TRCA’s directors and officers in the Registration Statement, TRCA’s filings with the SEC, including TRCA’s initial public offering prospectus, which was filed with the SEC on March 5, 2021, TRCA’s subsequent annual reports on Form 10-K and

quarterly reports on Form 10-Q. To the extent that holdings of TRCA’s securities by insiders have changed from the amounts reported therein, any such changes have been or will be reflected on Statements of Change in Ownership on Form 4 filed with

the SEC. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies to TRCA’s shareholders in connection with the business combination will be included in the definitive proxy

statement/prospectus relating to the proposed business combination, when it becomes available. You may obtain free copies of these documents, when available, as described in the preceding paragraphs.

Forward-Looking Statements

All statements other than statements of historical facts contained in this communication are forward-looking statements. Forward-looking statements may generally be identified by the use of words such as “believe,” “may,” “will,” “estimate,”

“continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “project,” “forecast,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” “target” or other similar expressions (or the negative versions of such words or

expressions) that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding the financial position, business strategy and

the plans and objectives of management for future operations including as they relate to the proposed business combination and related transactions, pricing and market opportunity, the satisfaction of closing conditions to the proposed business

combination and related transactions, the level of redemptions by TRCA’s public shareholders and the timing of the completion of the proposed business combination, including the anticipated closing date of the proposed business combination and

the use of the cash proceeds therefrom. These statements are based on various assumptions, whether or not identified in this communication, and on the current expectations of CBR’s and TRCA’s management and are not predictions of actual

performance. These forward-looking statements are provided for illustrative purposes only and are not intended to serve as and must not be relied on by any investor as a guarantee, an assurance, a prediction or a definitive statement of fact or

probability. Actual events and circumstances are difficult or impossible to predict and may differ from such assumptions, and such differences may be material. Many actual events and circumstances are beyond the control of CBR and TRCA.

6

These forward-looking statements are subject to a number of risks and uncertainties, including (i) changes in domestic and foreign business, market, financial, political and legal conditions; (ii) the inability of the parties to successfully

or timely consummate the proposed business combination, including the risks that we will not secure sufficient funding to proceed through to completion of the Transaction, any required regulatory approvals are not obtained, are delayed or are

subject to unanticipated conditions that could adversely affect the combined company or the expected benefits of the proposed business combination, or that the approval of the shareholders of TRCA or CBR is not obtained; (iii) the ability to

maintain the listing of MergeCo’s securities on the stock exchange; (iv) the inability to complete any private placement financing, the amount of any private placement financing or the completion of any private placement financing on favorable

terms; (v) the risk that the proposed business combination disrupts current plans and operations CBR or TRCA as a result of the announcement and consummation of the proposed business combination and related transactions; (vi) the risk that any of

the conditions to closing of the business combination are not satisfied in the anticipated manner or on the anticipated timeline or are waived by any of the parties thereto; (vii) the failure to realize the anticipated benefits of the proposed

business combination and related transactions; (viii) risks relating to the uncertainty of the costs related to the proposed business combination; (ix) risks related to the rollout of CBR’s business strategy and the timing of expected business

milestones; (x) the effects of competition on CBR’s future business and the ability of the combined company to grow and manage growth, establish and maintain relationships with customers and healthcare professionals and retain its management and

key employees; (xi) risks related to domestic and international political and macroeconomic uncertainty, including the Russia-Ukraine conflict; (xii) the outcome of any legal proceedings that may be instituted against TRCA, CBR or any of their

respective directors or officers; (xiii) the amount of redemption requests made by TRCA’s public shareholders; (xiv) the ability of TRCA to issue equity, if any, in connection with the proposed business combination or to otherwise obtain

financing in the future; (xv) the impact of the global COVID-19 pandemic and governmental responses on any of the foregoing risks; (xvi) risks related to CBR’s industry; (xvii) changes in laws and regulations; and (xviii) those factors discussed

in TRCA’s Annual Report on Form 10-K for the year ended December 31, 2022 under the heading “Risk Factors,” and other documents of TRCA or MergeCo to be filed with the SEC, including the proxy statement / prospectus. If any of these risks

materialize or TRCA’s or CBR’s assumptions prove incorrect, actual results could differ materially from the results implied by these forward-looking statements. There may be additional risks that neither TRCA nor CBR presently know or that TRCA

and CBR currently believe are immaterial that could also cause actual results to differ from those contained in the forward-looking statements. In addition, forward-looking statements reflect TRCA’s and CBR’s expectations, plans or forecasts of

future events and views as of the date of this communication. TRCA and CBR anticipate that subsequent events and developments will cause TRCA’s and CBR’s assessments to change. However, while TRCA and CBR may elect to update these forward-looking

statements at some point in the future, each of TRCA, CBR, MergeCo and Merger Sub specifically disclaim any obligation to do so, unless required by applicable law. These forward-looking statements should not be relied upon as representing TRCA’s

and CBR’s assessments as of any date subsequent to the date of this communication. Accordingly, undue reliance should not be placed upon the forward-looking statements.

FY23 financial information included in this announcement is unaudited and may differ from the information in final, audited financial statements.

7

|

Carbon Revolution Limited (ASX:CBR)

|

|

Appendix 4E Preliminary Final Report

|

Appendix 4E - Preliminary Final Report

Entity details

This Preliminary Final Report prepared in accordance with ASX listing rule 4.3A covers Carbon Revolution Limited (Company) ABN 96 128 274 653 and its controlled entities.

| 1. |

Reporting period.

|

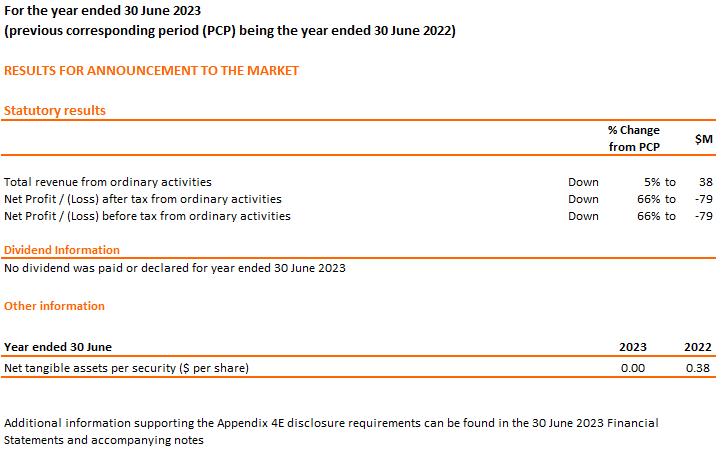

Except where stated otherwise, all figures relate to the current reporting period being the year ended 30 June 2023 and the previous corresponding period being the year ended 30 June 2022.

| 2. |

Results for announcement to the market.

|

| 3. |

Statement of comprehensive income.

|

A consolidated statement of comprehensive income is attached.

| 4. |

Statement of financial position.

|

A consolidated statement of financial position is attached.

| 5. |

Statement of cash flows.

|

A consolidated statement of cash flows is attached.

| 6. |

Statement of changes in equity.

|

A consolidated statement of changes in equity is attached.

| 7. |

Dividends.

|

See above table in Item 2.

|

|

Carbon Revolution Limited (ASX:CBR)

|

|

Appendix 4E Preliminary Final Report

|

| 8. |

Dividend or distribution reinvestment plans.

|

No dividend or distribution reinvestment plans were in place.

| 9. |

Net tangible assets per security.

|

See above table in Item 2.

| 10. |

Details of entities over which control has been gained or lost during the period.

|

Not applicable.

| 11. |

Details of associates and joint venture entities.

|

Not applicable.

| 12. |

Any other significant information needed by an investor to make an informed assessment of the entity’s financial performance and financial position.

|

Refer to attached financial statements.

| 13. |

For foreign entities, which set of accounting standards is used in compiling the report (e.g. International Financial reporting Standards).

|

Not applicable.

| 14. |

Commentary on the results for the period.

|

Carbon Revolution has positioned itself as the clear global leader in the production and distribution of lightweight carbon fibre wheels for the automotive industry. Financial Year 2023 (FY23) was a year of very significant operational

achievement for Carbon Revolution.

In November 2022, Carbon Revolution announced a proposed merger, referred to as the "Transaction", with Twin Ridge Capital Acquisition Corp. The Transaction, and subsequent access to U.S. capital markets, are anticipated to unlock critical

investment capital to fund operations, capital expenditure and strategic growth opportunities, support commercialisation and accelerate the path to expected profitability. The Transaction is expected to complete in October or November 2023.

At completion of the Transaction, Carbon Revolution will be acquired by Carbon Revolution plc, an Irish company whose shares are expected to trade on NYSE American and the Company’s shares shall cease to be quoted on the ASX.

The Company is experiencing strong growth in demand for its carbon fibre wheels. Four programs awarded across FY23, combined with changes to existing awarded programs, have doubled the Company’s projected revenue backlog1 since October 2022 to over $970 million. Approximately 50% of the backlog is associated with Electric Vehicle programs.

One newly awarded program is with a new customer, a premium brand of a major European OEM. This has added to our impressive track record, with a cumulative count of 18 awarded wheel programs with six global OEMs, 5 in aftersales, 6 in

production and 7 programs in development.

1 Backlog as of 29th May 2023. Backlog (remaining lifetime gross program projected revenue) is based on awarded programs and excludes programs that are

contracted for engineering. See Projection Methodologies from 6th June 2023 ASX announcement titled “Revised Financial Projections for CY23 and Accompanying Presentation”.

|

|

Carbon Revolution Limited (ASX:CBR)

|

|

Appendix 4E Preliminary Final Report

|

Other program highlights through FY23 included:

| • |

Ford launched the new Mustang ‘Dark Horse’ with Carbon Revolution’s carbon fibre wheels. This marks Carbon Revolution's first core vehicle program with Ford, demonstrating broader adoption of our

lightweight wheel technology.

|

| • |

General Motors’ Chevrolet Corvette E-Ray, the second Corvette model will also feature Carbon Revolution wheels as announced early in the second half of the financial year. The E-Ray will be the first

Corvette to utilise electric power in addition to its V8 engine, and the first all-wheel drive Corvette.

|

| • |

Jaguar Land Rover revealed the 2024 Range Rover Sport SV with Carbon Revolution carbon fibre wheels. This is Carbon Revolution’s debut in the SUV carbon fibre wheel sector, highlighting an important

expansion of our advanced lightweight wheel technology into the SUV segment.

|

Improved access to international capital markets is being progressed. In addition to progressing the Transaction, in May 2023 a new US$60 million debt program (New Debt Program) was secured providing funding for Mega-line automation and

capacity expansion, general corporate and other working capital purposes. It was also used to refinance existing debt providers and to pay creditors who had assisted the Company with its liquidity initiatives.

Installation and commissioning of Phase 1 of the Mega-line is progressing well with production wheels now being produced on the Mega-line. Through the final months of FY23 the Company saw production rates rise steadily, with improved

reliability and tool loop cycle times.

FY23 revenue of $38.3m was 5% down on the financial year ended 30 June 2022 (FY22) and below the Company’s original expectations primarily due to timing of the Corvette program. Corvette wheel sales were pushed back by approximately 6

months from early to mid FY23 after General Motors delayed wheel orders due to their broader supply chain challenges on the vehicle. Shipments resumed progressively for this program from January 2023. The average price of wheels sold in

FY23 was $2,847, a 6% increase on FY22 due to product mix changes.

Initial revenue from the newly launched Range Rover Sport SV program was included in FY23 following production commencing in the third quarter of FY23. We exited the financial year with strong sales momentum.

The Company subsequently passed 70,000 cumulative wheels sold in July 2023.

We exited the year with strong production cost improvement following Mega-line commissioning and increased volumes. Contribution margin increased by 33% to $2.5m in FY23 driven by improved Q4 operating performance.

Operating, selling and administrative expenses changed little from FY22 to FY23 as inflationary pressures on these expenses were offset by a focus on cost control.

Finance costs of $5.5 million and capital raising costs of $24.7 million were incurred in FY23 to support the New Debt Program and the Transaction. These higher finance and capital raising costs substantially contributed to the

increased loss after tax of $79.2 million, compared with a loss of $47.8 million in FY22.

Net cash used in operating activities increased to $52.5m from $46.0m with increases in receipts from customers of $12.1m and government grants of $11.7m respectively which included a level of early payments arising from liquidity

initiatives. These were offset by increases in borrowing costs of $20.7m related to initial cost of the new debt program and $9.0m of transaction costs. Net cash used in investing activities decreased by 16.9% to $18.0m. While the Company

continued to support Mega-line milestones and invested in program development, management of cash expenditure and collections was a priority focus throughout the year given balance sheet constraints, especially before the completion of the

New Debt Program in May 2023.

|

|

Carbon Revolution Limited (ASX:CBR)

|

|

Appendix 4E Preliminary Final Report

|

Net cash provided by financing activities significantly increased by $63.2m, arising primarily from the net proceeds of the New Debt Program.

The Group is managing its liquidity to enable it to complete the Transaction which is expected to occur in October or November 2023. Liquidity initiatives include support from customers and suppliers. While these initiatives are expected

to enable the Company to complete the Transaction, there can be no assurance that the Transaction will complete at the expected time or that Company will have sufficient liquidity to complete the Transaction. If the Transaction is not

realised or is delayed, the Group will have to seek other options including delaying or reducing operating and capital expenditure, considering the possibility of an alternative transaction or fundraising, and in the event that none of

these are available, the Board may be forced to place the Company into liquidation or voluntary administration.

The Directors are of the opinion that it is appropriate for the Company to prepare the unaudited financial statement on the basis that the Group is a going concern. The financial statements do not include any adjustments relating to the

recoverability and classification of recorded asset amounts or to the amounts and classification of liabilities that might be necessary should the Company not continue as a going concern. Notwithstanding this assessment, there exists a

material uncertainty that casts doubt on the Company’s ability to continue as a going concern for at least the next 12 months. Therefore, the Company may be unable to realise its assets and discharge its liabilities in the normal course of

business.

Refer to Note 1 to the financial statements for further detail regarding the basis of preparation of the financial statements.

| 15. |

Audit Status.

|

This preliminary report is based on financial statements which are in the process of being audited by Deloitte Touche Tohmatsu and are expected to be made available during September 2023.

| 16. |

Description of likely emphasis of matter.

|

The audit report is anticipated to include an emphasis of matter referring to the reasons why the Company has concluded it is appropriate to prepare the financial statements on a going concern basis which are described in note 1.3 to the

attached financial statements.

|

CARBON REVOLUTION LIMITED

ABN 96 128 274 653

|

|

|

FINANCIAL STATEMENTS

FOR THE YEAR ENDED 30 JUNE 2023

Preliminary and Unaudited

|

|

TABLE OF CONTENTS

Financial Report

|

Consolidated statement of profit or loss and other comprehensive income

|

3 | |

|

Consolidated statement of financial position

|

4 | |

|

Consolidated statement of changes in equity

|

5 | |

|

Consolidated statement of cash flows

|

6 | |

|

Notes to the financial statements

|

8 |

|

Consolidated statement of profit or loss and other comprehensive income

For the Year Ended 30 June 2023

|

|

|

Note

|

2023

$’000

|

2022

$’000

|

||||||||

|

Sale of wheels

|

37,477

|

38,276

|

|||||||||

|

Engineering services

|

530

|

464

|

|||||||||

|

Sale of tooling

|

253

|

1,596

|

|||||||||

|

Revenue

|

2.1

|

38,260

|

40,336

|

||||||||

|

Cost of goods sold

|

3.2.1

|

(55,094

|

)

|

(57,445

|

)

|

||||||

|

Gross loss

|

(16,834

|

)

|

(17,109

|

)

|

|||||||

|

Other income

|

2.2

|

3,096

|

4,320

|

||||||||

|

Operational expenses

|

(2,997

|

)

|

(2,013

|

)

|

|||||||

|

Research and development expenses

|

2.4

|

(16,180

|

)

|

(16,933

|

)

|

||||||

|

Administrative expenses

|

(14,566

|

)

|

(13,146

|

)

|

|||||||

|

Marketing expenses

|

(1,494

|

)

|

(1,550

|

)

|

|||||||

|

Capital raising transaction costs

|

4.7

|

(24,746

|

)

|

-

|

|||||||

|

Finance costs

|

2.4

|

(5,502

|

)

|

(1,390

|

)

|

||||||

|

Loss before income tax expense

|

(79,223

|

)

|

(47,821

|

)

|

|||||||

|

Income tax expense

|

5

|

-

|

-

|

||||||||

|

Loss for the year after income tax

|

(79,223

|

)

|

(47,821

|

)

|

|||||||

|

Other comprehensive loss

|

|||||||||||

|

Items that may be reclassified subsequently to profit or loss:

|

|||||||||||

|

Foreign currency translation differences – foreign operations

|

(62

|

)

|

(147

|

)

|

|||||||

|

Other comprehensive loss

|

(62

|

)

|

(147

|

)

|

|||||||

|

Total comprehensive loss for the year, net of tax

|

(79,285

|

)

|

(47,968

|

)

|

|||||||

|

Earnings per share

|

|||||||||||

|

Basic

|

2.5

|

$

|

(0.38

|

)

|

$

|

(0.23

|

)

|

||||

|

Diluted

|

2.5

|

$

|

(0.38

|

)

|

$

|

(0.23

|

)

|

||||

The accompanying notes form an integral part of these financial statement.

|

Consolidated statement of financial position

As at 30 June 2023

|

|

|

Note

|

30 June 2023

$’000

|

30 June 2022

$’000

|

||||||||

|

Current assets

|

|||||||||||

|

Cash and cash equivalents

|

4.1

|

19,582

|

22,693

|

||||||||

|

Restricted trust fund

|

4.1

|

14,677

|

-

|

||||||||

|

Receivables

|

3.1

|

6,430

|

14,483

|

||||||||

|

Contract assets

|

2.1

|

8,239

|

5,909

|

||||||||

|

Inventories

|

3.2

|

22,173

|

20,164

|

||||||||

|

Other current assets

|

378

|

1,587

|

|||||||||

|

Total current assets

|

71,479

|

64,836

|

|||||||||

|

Non-current assets

|

|||||||||||

|

Property, plant and equipment

|

3.3

|

62,638

|

57,616

|

||||||||

|

Right-of-use assets

|

3.4

|

7,446

|

7,564

|

||||||||

|

Intangible assets

|

3.5

|

16,774

|

14,364

|

||||||||

|

Total non-current assets

|

86,858

|

79,544

|

|||||||||

|

Total assets

|

158,337

|

144,380

|

|||||||||

|

|

|||||||||||

|

Current liabilities

|

|||||||||||

|

Payables

|

3.6

|

15,474

|

9,502

|

||||||||

|

Borrowings

|

4.2

|

13,829

|

18,686

|

||||||||

|

Lease liability

|

3.4

|

645

|

579

|

||||||||

|

Contract liability

|

2.1

|

748

|

458

|

||||||||

|

Deferred income

|

3.7

|

1,919

|

1,028

|

||||||||

|

Provisions

|

3.8

|

12,957

|

4,161

|

||||||||

|

Total current liabilities

|

45,572

|

34,414

|

|||||||||

|

Non-current liabilities

|

|||||||||||

|

Borrowings

|

4.2

|

70,833

|

4,333

|

||||||||

|

Lease liability

|

3.4

|

7,368

|

7,461

|

||||||||

|

Contract liability

|

2.1

|

1,755

|

323

|

||||||||

|

Deferred income

|

3.7

|

15,235

|

5,211

|

||||||||

|

Provisions

|

3.8

|

1,843

|

713

|

||||||||

|

Total non-current liabilities

|

97,034

|

18,041

|

|||||||||

|

Total liabilities

|

142,606

|

52,455

|

|||||||||

|

Net assets

|

15,731

|

91,925

|

|||||||||

|

|

|||||||||||

|

Equity

|

|||||||||||

|

Contributed equity

|

4.4

|

386,432

|

383,822

|

||||||||

|

Reserves

|

4.6

|

7,166

|

6,747

|

||||||||

|

Accumulated losses

|

(377,867

|

)

|

(298,644

|

)

|

|||||||

|

Total equity

|

15,731

|

91,925

|

|||||||||

The accompanying notes form an integral part of these financial statements.

|

Consolidated statement of changes in equity

As at 30 June 2023

|

|

|

Note

|

Contributed

equity

|

Share

buyback

reserve

|

Share

based

payment

reserve

|

Accumulated

losses

|

Foreign

currency

translation

reserve

|

Total

equity

|

|||||||||||||||||||||

|

|

|

$’000

|

|

$’000

|

|

$’000

|

|

$’000

|

|

$’000

|

|

$’000

|

||||||||||||||||

|

Balance as at 30 June 2021

|

381,890

|

(311

|

)

|

5,979

|

(250,823

|

)

|

(9

|

)

|

136,726

|

|||||||||||||||||||

|

Net loss after tax for the full year

|

-

|

-

|

-

|

(47,821

|

)

|

-

|

(47,821

|

)

|

||||||||||||||||||||

|

Other comprehensive loss for the full year

|

-

|

-

|

-

|

-

|

(147

|

)

|

(147

|

)

|

||||||||||||||||||||

|

Total comprehensive loss for the full year

|

-

|

-

|

-

|

(47,821

|

)

|

(147

|

)

|

(47,968

|

)

|

|||||||||||||||||||

|

Transactions with owners in their capacity as owners

|

||||||||||||||||||||||||||||

|

Share-based payments

|

4.4

|

1,932

|

-

|

1,235

|

-

|

-

|

3,167

|

|||||||||||||||||||||

|

Total transactions with owners in their capacity as owners

|

1,932

|

-

|

1,235

|

-

|

-

|

3,167

|

||||||||||||||||||||||

|

Balance as at 30 June 2022

|

383,822

|

(311

|

)

|

7,214

|

(298,644

|

)

|

(156

|

)

|

91,925

|

|||||||||||||||||||

|

|

||||||||||||||||||||||||||||

|

Balance as at 30 June 2022

|

383,822

|

(311

|

)

|

7,214

|

(298,644

|

)

|

(156

|

)

|

91,925

|

|||||||||||||||||||

|

|

||||||||||||||||||||||||||||

|

Net loss after tax for the full year

|

-

|

-

|

-

|

(79,223

|

)

|

-

|

(79,223

|

)

|

||||||||||||||||||||

|

Other comprehensive loss for the full year

|

-

|

-

|

-

|

-

|

(62

|

)

|

(62

|

)

|

||||||||||||||||||||

|

Total comprehensive loss for the full year

|

-

|

-

|

-

|

(79,223

|

)

|

(62

|

)

|

(79,285

|

)

|

|||||||||||||||||||

|

Transactions with owners in their capacity as owners

|

||||||||||||||||||||||||||||

|

Share-based payments

|

4.4

|

2,610

|

-

|

481

|

-

|

-

|

3,091

|

|||||||||||||||||||||

|

Total transactions with owners in their capacity as owners

|

2,610

|

-

|

481

|

-

|

-

|

3,091

|

||||||||||||||||||||||

|

Balance as at 30 June 2023

|

386,432

|

(311

|

)

|

7,695

|

(377,867

|

)

|

(218

|

)

|

15,731

|

|||||||||||||||||||

The accompanying notes form an integral part of these financial statements.

|

Consolidated statement of cash flows

As at 30 June 2023

|

|

Note

|

2023

$’000

|

2022

$’000

|

|||||||||

|

Cash flow from operating activities

|

|||||||||||

|

Receipts from customers

|

45,742

|

33,643

|

|||||||||

|

Receipt of grants and research and development incentives

|

3.7

|

15,446

|

3,767

|

||||||||

|

Payments to suppliers and employees

|

(80,215

|

)

|

(81,005

|

)

|

|||||||

|

Interest received

|

61

|

94

|

|||||||||

|

Capital raising transaction costs

|

4.7

|

(9,030

|

)

|

-

|

|||||||

|

Borrowing costs

|

4.2

|

(20,676

|

)

|

-

|

|||||||

|

Finance costs

|

(3,810

|

)

|

(2,475

|

)

|

|||||||

|

Net cash used in operating activities

|

4.1.2

|

(52,482

|

)

|

(45,976

|

)

|

||||||

|

Cash flow from investing activities

|

|||||||||||

|

Payments for property, plant and equipment

|

3.3

|

(13,082

|

)

|

(15,634

|

)

|

||||||

|

Payments for intangible assets

|

3.5

|

(4,874

|

)

|

(6,007

|

)

|

||||||

|

Sale proceeds from sale of property, plant and equipment

|

3.3

|

3

|

-

|

||||||||

|

Net cash used in investing activities

|

(17,953

|

)

|

(21,641

|

)

|

|||||||

|

Cash flow from financing activities

|

|||||||||||

|

Proceeds from third party borrowings

|

4.2

|

124,963

|

33,657

|

||||||||

|

Repayment of third-party borrowings

|

4.2

|

(43,212

|

)

|

(29,370

|

)

|

||||||

|

Reclass to restricted trust fund

|

4.2

|

(14,677

|

)

|

-

|

|||||||

|

Capital raising transaction costs

|

-

|

(422

|

)

|

||||||||

|

Repayment of lease liability

|

(604

|

)

|

(596

|

)

|

|||||||

|

Net cash provided by financing activities

|

66,470

|

3,269

|

|||||||||

|

Net decrease in cash held

|

(3,965

|

)

|

(64,348

|

)

|

|||||||

|

Cash at beginning of financial year

|

22,693

|

87,257

|

|||||||||

|

Effects of exchange rate changes on cash and cash equivalents

|

854

|

(216

|

)

|

||||||||

|

Cash at end of financial year

|

19,582

|

22,693

|

|||||||||

The accompanying notes form an integral part of these financial statements.

|

Notes to the financial statements

|

Contents

|

1

|

BASIS OF PREPARATION

|

8 | |

|

1.1

|

Corporate information

|

8 | |

|

1.2

|

Basis of preparation

|

8 | |

|

1.3

|

Going concern

|

8 | |

|

1.4

|

Basis of consolidation

|

11 | |

|

1.5

|

Significant accounting judgements, estimates and assumptions

|

12 | |

|

1.6

|

Goods and Services Tax (“GST”)

|

12 | |

|

2

|

OPERATING PERFORMANCE

|

13 | |

|

2.1

|

Revenue from contracts with customers

|

13 | |

|

2.2

|

Other income

|

14 | |

|

2.3

|

Segments

|

15 | |

|

2.4

|

Expenses

|

16

|

|

|

2.5

|

Earnings per share

|

17

|

|

|

3

|

OPERATING ASSETS AND LIABILITIES

|

19 | |

|

3.1

|

Receivables

|

19 | |

|

3.2

|

Inventories

|

20 | |

|

3.3

|

Property, plant and equipment

|

21 | |

|

3.4

|

Leases

|

22

|

|

|

3.5

|

Intangible assets

|

23 | |

|

3.6

|

Payables

|

24 | |

|

3.7

|

Deferred income

|

25 | |

|

3.8

|

Provisions

|

26 | |

|

4

|

CAPITAL STRUCTURE AND FINANCING

|

28 | |

|

4.1

|

Cash and cash equivalents, restricted cash

|

28 | |

|

4.2

|

Borrowings and other financial liabilities

|

29 | |

|

4.3

|

Financial risk management

|

31 | |

|

4.4

|

Contributed equity

|

34 | |

|

4.5

|

Share-based payment plan arrangements

|

35 | |

|

4.6

|

Reserves

|

37 | |

|

4.7

|

Transaction costs

|

38 | |

|

5

|

TAXES

|

39 | |

|

5.1

|

Income tax expense

|

39 | |

|

5.2

|

Deferred taxes

|

39 | |

|

5.3

|

Recognised deferred tax assets and liabilities in statement of financial position

|

40 | |

|

5.4

|

Carry forward unrecognised tax losses and R&D tax credits

|

40 | |

|

6

|

OTHER NOTES

|

41 | |

|

6.3

|

Information about subsidiaries

|

41 | |

|

6.4

|

Deed of cross guarantee

|

41 | |

|

6.5

|

Directors and Key management personnel

|

43 | |

|

6.6

|

Transactions with related parties

|

43 | |

|

6.7

|

Parent entity disclosures

|

43 | |

|

6.8

|

Auditor’s remuneration

|

44 | |

|

6.9

|

Unrecognised items

|

44 | |

|

6.10

|

Changes in accounting policies

|

44 | |

|

6.11

|

Adoption of new and revised Australian Accounting Standards

|

44 | |

|

6.12

|

Subsequent events

|

45 | |

|

Notes to the financial statements

|

| 1 |

Basis of preparation

|

| 1.1 |

Corporate information

|

This note sets out the accounting policies adopted by Carbon Revolution Limited (the “Company” or “parent”) and its consolidated entities, collectively known as the “consolidated entity” or

the “Group” in the preparation and presentation of the financial statements. Where an accounting policy is specific to one note, the policy is described within the note to which it relates.

The financial statements were authorised for issue by the directors as of 31 August 2023.

Carbon Revolution Limited is a listed public company limited by shares, incorporated and domiciled in Australia. Its principal activity is the manufacture and sale of carbon fibre wheels,

as well as research and development projects relating to carbon fibre wheel technology.

The address of the Company’s registered office and its principal place of business is:

Building NR

75 Pigdons Road

Waurn Ponds VIC 3216, Australia

On November 29, 2022, the Company, Twin Ridge Capital Acquisition Corp. ("Twin Ridge"), Carbon Revolution Public Limited Company (formerly known as Poppetell Limited), a public limited

company incorporated in Ireland ("MergeCo") and Poppetell Merger Sub, a Cayman Islands exempted company and wholly-owned subsidiary of MergeCo ("Merger Sub"), entered into a Business Combination Agreement, and the Company, Twin Ridge and

MergeCo entered into a Scheme Implementation Deed. Consummation of the Business Combination (the ‘‘Transaction’’), which is expected to result in MergeCo becoming publicly listed in the U.S., is subject to approval by the Company’s

shareholders, Twin Ridge’s shareholders and applicable regulatory institutions.

Under the Scheme Implementation Deed, the Group has agreed to propose a scheme of arrangement under Part 5.1 of the Corporations Act (‘‘Scheme’’) and capital reduction under Part 2J.1 of

the Corporations Act (‘‘Capital Reduction’’) which, if implemented, will result in all shares of Carbon Revolution being cancelled in return for the issuance of MergeCo Ordinary Shares, with MergeCo then being issued one share in Carbon

Revolution (resulting in the Group becoming a wholly-owned subsidiary of MergeCo), subject to Carbon Revolution shareholder approval, Australian court approval and the satisfaction of various conditions.

| 1.2 |

Basis of preparation

|

The Group financial statements are general purpose financial statements which:

| • |

Have been prepared in accordance with the Corporations Act 2001, Australian Accounting Standards, and other authoritative pronouncements of the Australian

Accounting Standards Board (“AASB”);

|

| • |

Have adopted all accounting policies in accordance with Australian accounting standards, and where a standard permits a choice in accounting policy, the policy adopted by the Group has been disclosed in

these financial statements;

|

| • |

Do not early adopt any accounting standards or interpretations that have been issued or amended but are not yet effective;

|

| • |

Comply with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”);

|

| • |

Have been prepared for a for profit entity under the historical cost convention;

|

| • |

Are presented in Australian dollars, which is the Group’s functional and presentation currency;

|

| • |

Have been rounded to the nearest thousand dollars, unless otherwise stated, in accordance with ASIC Corporations (Rounding in Financial/Director’s Reports) Instrument 2016/191;

|

| • |

The Group has elected to present the statement of profit or loss and other comprehensive income using the function of expense method.

|

In accordance with the announcements to the Australian Securities Exchange on 31 January 2023 and 27 February 2023 the Company re-issued its financial report for the year ended 30 June 2022

on 27 February 2023. The comparative financial information contained within this financial report is that contained within/from the reissued financial report dated 27 February 2023.

| 1.3 |

Going concern

|

The financial statements of the Group have been prepared on the going concern basis including the financial statements of the parent entity which contemplates the continuity of normal

business activities and the realisation of assets and the discharge of liabilities in the normal course of business.

Carbon Revolution is an advanced technology manufacturing business which is in the process of industrialising and scaling up its production processes. At this pre-profitability stage of

Carbon Revolution’s business lifecycle, it is essential that it has sufficient funding to meet its working capital requirements, as well as to fund the Group’s ongoing research and development of its products, material and process

technologies, and investment in the expansion of its production facility (Mega-Line) required to achieve profitability and positive cash generation.

|

Notes to the financial statements

|

For the year ended 30 June 2023, the Group incurred an operating loss after tax of $79.2 million (2022: $47.8 million) and had negative cash flows from operating activities of $52.3 million

(2022: $46.0 million), with a net current asset position of $25.9 million (2022: $30.4 million) and a cash and cash equivalent balance of $19.6 million as of 30 June 2023 (2022: $22.7 million).

Carbon Revolution has prepared a detailed cash flow projection for the 12-month period from September 1, 2023 (the “Cash Flow Projection”) in connection with its assessment of its current

and estimated liquidity, including its financing needs and ability to continue as a going concern.. The information and assumptions available to Carbon Revolution in connection with the preparation of the Cash Flow Projections was as of a

later date than the Financial Projections contained in Shareholder Proposal 1 - The Business Combination and, accordingly, such information and assumptions, as well as the amounts presented, may differ materially.

In the 12-month cash flow projection, Carbon Revolution projects:

| • |

transaction costs related to the Business Combination of approximately A$35.7 million (of which A$4.4 million is expected to be payable prior to closing of the Business Combination, A$23.4 million on

completion and A$7.9 million after completion); and

|

| • |

net cash outflows in the 12-month period unrelated to the Business Combination of approximately A$78.4 million, being cash inflows from customers (and grants), less operating costs, research and

development costs, working capital needs and capital expenditure.

|

The Group’s Cash Flow Projection includes the injection of US$70 million coming from a combination of any remaining funds in the Trust Account following redemptions and the raise of

additional capital through the 12 month forecast period, with US$55 million required through the period from closing of the Business Combination to December 31, 2023, to pay transaction costs, to maintain sufficient cash on hand to comply

with the liquidity covenants under the New Debt Program, to cover the above net cash outflows and to allow the Group to continue as a going concern.

The Cash Flow Projection assumes that the closing of the Business Combination will occur in October 2023 and that the Group will be funded to the closing of the Business Combination and

comply with the liquidity covenant under the New Debt Program, including with the support from customers in the form of earlier payments for shipped wheels than under normal business terms, or other customer liquidity support, and careful

management of capital expenditures.

In relation to the expected A$23.4 million transaction costs otherwise payable on completion of the Business Combination, the Cash Flow Projection assumes that if MergeCo is unable to raise

sufficient additional equity funding prior to or at the closing of the Business Combination these costs will be deferred by agreement between Carbon Revolution and Twin Ridge and various transaction advisers for the amount and time period

necessary to ensure sufficient liquidity is available and no covenants under the New Debt Program are breached (“Transaction Cost Deferrals”). The Group must work with the relevant advisors to obtain these deferrals. While no agreements have

been reached, the majority (approximately 90% in amount) of the relevant advisors have indicated in writing that they are willing to work with Carbon Revolution and Twin Ridge to agree terms on which payments can be deferred if sufficient

funding is not obtained before such payments become due.

The latest Cash Flow Projection assumes that US$70 million will be sourced from any remaining funds in the Trust Account following redemptions and the raise of additional capital following

completion of the Business Combination. As of the date of issuance of this proxy statement/prospectus:

| • |

Craig-Hallum has been engaged by Twin Ridge to act as placement agent and capital markets advisor to support the Group in raising new capital. Craig-Hallum has in particular been engaged to identify and

contact potential investors, formulate a strategy, coordinate due diligence and assist in preparing any offering documents;

|

| • |

Separately, Carbon Revolution is seeking to obtain a Structured Rquity Facility (“SEF”), which would involve the issue of SEF Preference Shares and SEF Warrants by MergeCo in exchange for up to US$100

million which is likely to be conditional and available in tranches; and

|

| • |

In addition, the Committed Equity Financing is in place under which Yorkville Advisors has agreed to purchase up to US$60 million in MergeCo Ordinary shares, subject to the terms of the Equity Purchase

Agreement, including the CEF Ownership Restriction. Given this ownership restriction in particular, MergeCo is planning to use the CEF in combination with other funding sources.

|

|

Notes to the financial statements

|

Notwithstanding the fact that management is seeking to undertake a Qualified Capital Raise of US$60 million by December 31, 2023, the Cash Flow Projection assumes that the PIUS Additional

Monthly Fee will be payable from January 2024.

The Cash Flow Projection projects that subject to the risks set out below and the successful raising of up to an additional US$70 million of capital, which is also subject to the risks

including those set out below, the Group will have sufficient funds to meet its commitments and continue to comply with the financial covenants under the New Debt Program over the twelve months commencing September 1, 2023. The board of

directors of Carbon Revolution considers it has reasonable grounds to believe that Carbon Revolution will be successful in obtaining sufficient liquidity through the above funding initiatives. For these reasons, the Carbon Revolution board of

directors believe that the Group is a going concern.

There are risks associated with the Cash Flow Projection including but not limited to:

| • |

the Group may not receive the customer support it may require, or management of capital expenditure may not be possible without impacting supply obligations to customers and its ability to meet the

financial projections;

|

| • |

the Business Combination may not be completed, or may be materially delayed;

|

| • |

there may be no cash remaining in the Trust Account upon completion of the Business Combination if redemptions of Twin Ridge Class A Ordinary Shares are 100%;

|

| • |

there may be a delay in the availability of the Committed Equity Financing (the Committed Equity Financing will not be available until after the closing of the Business Combination and the filing by

MergeCo with the SEC of a registration statement for the resale of the MergeCo Ordinary Shares, and such registration statement being declared effective by the SEC);

|

| • |

as the terms of the Committed Equity Financing will not require the Yorkville Advisors to purchase additional shares under the Committed Equity Financing beyond the CEF Ownership Restriction, the Group

may have access to materially less than the US$60 million (A$90.3 million) Committed Equity Financing capital;

|

| • |

the Group may not be able to raise further equity funds from sources other than the Committed Equity Financing, in the amounts and within the timeframes necessary for the Group to remain solvent and to

comply with its liquidity covenants, on satisfactory terms, or at all;

|

| • |

the relevant advisers may not agree to the Transaction Cost Deferrals; and

|

| • |

the 12 Month Cash Flow Projection is subject to achievement of the financial projections of Carbon Revolution for CY23 and CY24 (as relevant) detailed in the accompanying assumptions and risks

applicable to these financial projections.

|

Should there be a material delay in the timing of the closing of the Business Combination or should the closing of the Business Combination not occur at all (including if Carbon Revolution

ceases to be funded before the closing of the Business Combination or breaches its liquidity covenant and the servicer exercises its rights under the New Debt Program), this would have adverse implications for the Group, Carbon Revolution

shareholders and its creditors. As the Group is not yet profitable and does not yet derive positive net operating cash flows (and does not expect to be profitable or be able to derive positive net operating cash flows through the 12-month

forecast period of the Cash Flow Projection), if the closing of the Business Combination is materially delayed beyond October 2023 or it is not completed, in order to remain viable, the Group will need to seek other funding and liquidity

options which may not be available

Further, in the context of the New Debt Program, if the Business Combination is delayed and if the Group does not raise additional funds through other sources, the Group is likely to breach

the liquidity covenants in the New Debt Program documentation and therefore be reliant on the Servicer waiving such default in order to avoid the consequences of a default. Furthermore, subject to the length of the delay, Carbon Revolution

could fail to cure, within the provided 60-day time period, the breach of the covenant in the New Debt Program documents to complete the Business Combination by August 31, 2023.

Should the Business Combination be completed but sufficient liquidity not be secured through the above funding initiatives, or should there be a delay in the timing of securing funds

through these funding initiatives, this would have adverse implications for the Group, MergeCo shareholders and its creditors. In these scenarios, the Group will need to seek other options, including seeking further liquidity support from

customers and suppliers, delaying or reducing operating and capital expenditure, seeking waivers in respect of potential covenant breaches, the possibility of an alternative transaction or fundraising, and in the event that any of these are

not available, liquidation or examinership (the Irish equivalent of voluntary administration).

Based on the factors above, a material uncertainty exists which may cast significant doubt as to whether Carbon Revolution will continue as a going concern and therefore whether it will

realise its assets and discharge its liabilities in the normal course of business and at the amounts stated in the financial statements. The financial statements do not include any adjustments relating to the recoverability and classification

of recorded asset amounts or to the amounts and classification of liabilities that might be necessary should the Group not continue as a going concern.

|

Notes to the financial statements

|

| 1.4 |

Basis of consolidation

|

The consolidated financial statements are presented in Australian dollars which is also the functional currency of the parent entity and its Australian subsidiaries.

Controlled entities

The consolidated financial statements comprise the financial statements of the parent and of its subsidiaries as at reporting date. The Group controls an entity when it is exposed, or has

rights, to variable returns from its involvement with the entity and has the ability to affect those returns through its power over the entity.

The financial statements of subsidiaries are prepared for the same reporting period as the parent entity, using consistent accounting policies. Adjustments are made to bring into line any

dissimilar accounting policies which may exist. Subsidiaries are consolidated from the date on which control is established and are de-recognised from the date that control ceases.

All intra-group assets and liabilities, equity, income, expenses and cash flows relating to transactions between members of the Group are eliminated in full on consolidation.

Any changes in the Group’s ownership interests in subsidiaries that do not result in the Group losing control over the subsidiaries are accounted for as equity transactions.

Foreign currency translation

The Group has one overseas subsidiary in the United States of America (“US”) and one in the United Kingdom (”UK”). The UK subsidiary was dormant during the financial year.

The results and financial position of all of the Group entities that have a functional currency different from the presentation currency are translated into the presentation currency as

follows:

| • |

assets and liabilities are translated at the closing rate at the reporting date;

|

| • |

income and expenses are translated at average exchange rates throughout the course of the year (unless this is not a reasonable approximation of the cumulative effect of the rates prevailing on the

transaction dates, in which case income and expenses are translated at the rates on the dates of the transactions); and

|

| • |

all resulting exchange differences are recognised in other comprehensive income and accumulated in the foreign currency translation reserve, a separate component of equity.

|

|

Notes to the financial statements

|

| 1.5 |

Significant accounting judgements, estimates and assumptions

|

In preparing these consolidated financial statements, management has made judgements, estimates and assumptions that affect the application of the Group’s accounting policies and the

reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to estimates are recognised prospectively. The

significant judgements made by management in applying the Group’s accounting policies and the key sources of estimation uncertainty are outlined in detail within the specific note to which they relate.

Information about critical judgements in applying accounting policies that have the most significant effect on the amounts recognised in the consolidation financial statements are included

in the following notes.

|

Note 3.2 Inventories

|

Note 3.5 Intangible assets

|

|

Note 3.3 Property, plant and equipment

|

Note 5.5 Income tax

|

|

Note 3.7 Deferred income

|

Note 4.7 Transaction costs

|

|

Note 4.2 Borrowings and other financial liabilities

|

| 1.6 |

Goods and Services Tax (“GST”)

|

Goods and Services Tax (“GST”) is recognised in these financial statements as follows:

| 1. |

Revenues, expenses and assets are recognised net of the amount of associated GST, unless the GST incurred is not recoverable from the taxation authority;

|

| 2. |

Receivables and payables are stated inclusive of the amount of GST receivable or payable;

|

| 3. |

The net amount of GST recoverable from, or payable to, the taxation authority is included with other receivables or payables in the consolidated balance sheet;

|

| 4. |

Cash flows are presented on a gross basis. The GST components of cash flows arising from investing and financing activities are presented as operating cash flows; and

|

| 5. |

Commitments are disclosed net of GST.

|

|

Notes to the financial statements

|

| 2 |

Operating performance

|

Revenue is recognised either at a point in time or over time, when (or as) the Group satisfies performance obligations by transferring the promised goods or services to its customers,

regardless of when the payment is received. Revenue is measured at the fair value of consideration received or receivable, taking into account contractually defined terms of payment and excluding taxes or duty. The Group has concluded that

it is the principal in all of its revenue arrangements since it is the primary obligor in all the revenue arrangements, has pricing discretion, and is also exposed to inventory and credit risks.

| 2.1 |

Revenue from contracts with customers

|

In addition to the comments in Note 2.2.1 the disclosure requirements arising from AASB 15, Revenue from Contracts with Customers, are grouped together in this note.

Disaggregation of revenue

|

2023

$’000

|

2022

$’000

|

|||||||

|

External revenue by product line

|

||||||||

|

Sale of wheels

|

37,477

|

38,276

|

||||||

|

Engineering services

|

530

|

464

|

||||||

|

Sale of tooling

|

253

|

1,596

|

||||||

|

Total revenue

|

38,260

|

40,336

|

||||||

|

2023

$’000

|

2022

$’000

|

|||||||

|

External revenue by timing of revenue

|

||||||||

|

Goods transferred at a point in time

|

19,307

|

15,730

|

||||||

|

Goods transferred over time

|

18,170

|

22,546

|

||||||

|

Services transferred at a point in time

|

253

|

1,277

|

||||||

|

Services transferred over time

|

530

|

783

|

||||||

|

Total revenue

|

38,260

|

40,336

|

||||||

|

2023